Low-High Waves for NeowaveOpen your chart at daily and hide the symbol graphic. Now you can see the waves. It’s including limited data sorry for this but I’m not a programmer and TradingView have limitations.

Educational

Fair Value Gap [Tradeuminati]Fair Value Gap

Fair Value Gap is a clean and rule-based Fair Value Gap indicator for TradingView, designed to display only valid and confirmed Fair Value Gaps (FVGs) and Inverted Fair Value Gaps (iFVGs).

The indicator is built on a strict 3-candle FVG definition and operates exclusively on candle close, ensuring no repainting and no premature signals.

🔹 Key Features

Valid Fair Value Gaps (FVG)

- Detects bullish and bearish Fair Value Gaps using a precise 3-candle structure

- FVGs are only plotted after the confirming candle has closed

- A Fair Value Gap remains visible only as long as it is valid

- Once price closes beyond the FVG, it is removed or converted

Inverted Fair Value Gaps (iFVG)

- When a valid FVG is invalidated by a candle close, it can be converted into an iFVG

- iFVGs retain the original price range and structure

- Only valid iFVGs are displayed

- As soon as price closes through an iFVG, it is automatically removed

Clean & Controlled Visualization

- Only the last N active FVGs are displayed (bullish + bearish combined)

- Only the last N valid iFVGs are shown

- Boxes automatically extend to the current price + configurable bars

- Labels are dynamically positioned at the right edge of each zone

🔹 Technical Notes

- No repainting

- No intrabar signals

- Close-based validation only

- Works on all markets and timeframes

- Lightweight and performance-friendly

⚠️ Disclaimer

This indicator is for technical analysis purposes only and does not constitute trading or investment advice.

Trinity Swing Trading Buy and SellThis is a simple little Heiken Ashi MA + ADX & MACD trend-following trading system designed to capture medium- to longer-term moves while filtering out noise and weak trends. It combines modified Heiken Ashi candles (for smoother trend detection) with a moving average alignment, plus optional confirmation from ADX (trend strength) and MACD (momentum).

In practice, the indicator works well on higher timeframes (e.g., 1H, 4H, daily) where trends are more sustained. It performs best in trending markets and naturally avoids choppy/range-bound conditions thanks to the ADX filter (requiring ADX > 20 by default). All key components are fully customizable, so you can disable filters or adjust parameters to suit different instruments (stocks, forex, crypto, futures).

Default settings are:

16 HMA

8,17,9 MACD

15,20 ADX

Recommend to add an additional longer term EMA like 200 for long term trend confirmation.

Adjust inputs in the settings panel as needed:

Toggle MA, ADX, or MACD filters on/off.

Change MA type/length, MACD parameters, ADX threshold

- Use the visual blue diamonds (below bars) for long entries and purple diamonds (above bars) for short entries as confirmation of signals.

- Set alerts on the "Buy Alert" and "Sell Alert" conditions if you want real-time notifications.

This setup gives you a complete, rule-based system that avoids emotional trading and repetitive entries, making it suitable for both backtesting and live trading with proper risk management.

Kijun Sen Standard Deviation | QuantLapse SystemsOverview

The Kijun Sen Standard Deviation indicator by QuantLapse Systems is a volatility-aware trend-following framework that combines the structural equilibrium of the Kijun Sen (基準線) with statistically adaptive standard deviation bands.

By anchoring trend detection to market structure and confirming direction through volatility expansion, the indicator delivers a cleaner, more reliable regime classification across varying market conditions.

Rather than reacting to short-term noise, the system focuses on identifying statistically justified trend phases , making it well-suited for disciplined, rule-based trading.

Technical Composition, Calculation, Key Components & Features

📌 Kijun Sen (基準線) – Structural Trend Baseline

Calculated as the midpoint between the highest high and lowest low over a user-defined period.

Represents market equilibrium and structural balance rather than short-term momentum.

Naturally adapts to expanding and contracting price ranges.

Provides a stable baseline for regime detection and volatility validation.

Acts as the anchor for deviation bands and persistent trend-state logic.

Unlike fast or reactive moving averages, the Kijun Sen emphasizes price structure and equilibrium , making it especially effective for higher-quality trend confirmation.

📌 Volatility Adjustment – Standard Deviation Bands

Standard deviation is calculated over a configurable lookback to measure current price dispersion.

Upper and lower envelopes are formed by applying a deviation multiplier to the Kijun Sen.

Band width expands during volatility surges and contracts during consolidation.

Creates proportional, volatility-aware thresholds instead of static offsets.

Visually represents market energy through expanding and compressing channels.

These adaptive bands ensure that trend signals only occur when volatility supports directional movement.

📌 Trend Signal & Regime Calculation

Bullish Trend is confirmed when price closes above the upper deviation band.

Bearish Trend is confirmed when price closes below the lower deviation band.

Once established, the trend state persists until an opposing volatility break occurs.

This persistence reduces whipsaws and improves regime stability.

Trend state is reinforced with color-coded lines, envelopes, and background shading.

This volatility-confirmed persistence model is visible in the chart, where trends remain intact through minor pullbacks and only flip on decisive expansion.

How It Works in Trading

✅ Volatility-Confirmed Trend Detection – Requires expansion beyond deviation bands.

✅ Noise Suppression – Filters low-energy price movement within volatility envelopes.

✅ Regime Persistence – Maintains trend state until statistical invalidation.

✅ Immediate Visual Context – Direction, strength, and transitions are clear at a glance.

Visual Representation

Trend signals are displayed directly on price using both line and background context:

🟢 Green / Teal Kijun & Envelope → Confirmed bullish regime.

🔴 Red / Pink Kijun & Envelope → Confirmed bearish regime.

Semi-transparent band fill visualizes volatility expansion and compression.

Buy and Sell labels appear only on confirmed regime transitions.

The lower panel includes:

Strategy equity curve based on trend exposure.

Buy & Hold equity for performance comparison.

Background regime shading synchronized with trend state.

Features and User Inputs

The Kijun Sen Standard Deviation framework offers a focused yet powerful set of configurable inputs:

Kijun Sen Length – Controls structural trend sensitivity.

Standard Deviation Controls – Adjust lookback length and multiplier for regime strictness.

Backtesting & Date Filters – Define evaluation periods and starting conditions.

Display Options – Toggle labels, equity curves, and background shading.

Color Customization – Fully configurable buy/sell colors for trends and equity curves.

These controls allow users to balance responsiveness, stability, and clarity without overfitting.

Practical Applications

The Kijun Sen Standard Deviation indicator is designed for traders who prioritize structure, volatility confirmation, and regime awareness.

Primary Trend Filtering – Identify and stay aligned with dominant market direction.

Volatility-Aware Trend Following – Participate only when price expansion confirms intent.

Risk-Managed Exposure – Avoid chop during compression and transitional phases.

Systematic Strategy Development – Use as a regime engine or higher-timeframe filter.

Performance Evaluation – Compare trend-following equity against buy-and-hold benchmarks.

This framework bridges classical Ichimoku structure with modern statistical validation.

Conclusion

The Kijun Sen Standard Deviation indicator by QuantLapse Systems represents a refined evolution of Ichimoku-based trend analysis.

By integrating the structural equilibrium of the Kijun Sen with adaptive standard deviation confirmation, the system delivers clearer regime classification, reduced noise, and more reliable trend participation.

Rather than attempting to predict price, it focuses on confirming when trends are statistically justified .

Who should use Kijun Sen Standard Deviation:

📊 Trend-Following Traders – Stay aligned with dominant market structure.

⚡ Momentum & Swing Traders – Enter only on volatility-backed expansions.

🤖 Systematic & Algorithmic Traders – Ideal as a regime filter or trend-state engine.

Past performance is not indicative of future results.

Disclaimer: All trading involves risk, and no indicator can guarantee profitability.

Strategic Advice: Always backtest thoroughly, optimize parameters responsibly, and align settings with your timeframe, asset class, and risk tolerance before live deployment.

Futures Tick DashboardThis is a simple dashboard that shows the novice future trade the necessary info about the info about the Micro on mini futures contract they are thinking about trading

Udta Teer MKCIts normal vwap which is already available in TradingView. Now we have modified it with help of AI for bands

Resumo de Velas (120) ROMANOCounting the last 120 candles with volume data

Count of positive candles + count of negative candles

Ratio between negative and positive candles

If the ratio is greater than 1.20, enter a sell position

If the ratio is less than 0.80, enter a buy position

Use on a high timeframe chart

------------------------

Contagem das ultimas 120 velas com volumes

Contagem velas positivas + contagem velas negativas

Razão entre negativas e positivas

Se a razão é maior que 1.20 entra em venda

Se a razão é menor que 0.80 entra em compra

Uso no grafico de alto timeframe

BTC Gann Harmonics Weighted + Phase + EMA OptimizedBTC Gann Harmonics Weighted + Phase + EMA Optimized

Ram Key Levels (Daily Horizontals) + Day SeparatorsRam Key Levels (Daily Horizontals) + Day Separators

Stationary Notes (Paragraph Box)This indicator helps you journal and notate any analysis’s you’ve made and display them while remaining stationary.

PCR Sentiment & Max Pain by Rakesh Sharma🎯 PCR + SENTIMENT + MAX PAIN INDICATOR

Track options market sentiment to catch reversals before they happen! See where smart money is positioning through Put-Call Ratio analysis.

✨ KEY FEATURES:

- PCR (Put-Call Ratio) with visual zones

- Market Sentiment Analysis (Bullish/Bearish/Neutral)

- Max Pain Level calculation (expiry day advantage)

- Automatic Buy/Sell signals at extreme levels

- Real-time dashboard with actionable insights

- Fear & Greed gauge

- Trading action recommendations

🎯 PERFECT FOR:

Nifty, Bank Nifty, Index Options - Intraday & Swing Trading

⚡ TRADING SIGNALS:

- PCR > 1.5 = Market oversold (Fear) → BUY signal

- PCR < 0.7 = Market overbought (Greed) → SELL signal

- Extreme levels trigger STRONG signals

- Contrarian indicator - Trade against the crowd!

💡 UNIQUE ADVANTAGE:

Combines options sentiment with price action for high-probability reversals. Know when institutions are bullish or bearish!

Created by: Rakesh Sharma

UIA TrendCompass V1.0UIA TrendCompass v1.0 is a market structure interpretation tool designed to visualize trend states in real time.

The script identifies four structural states based on price behavior and trend continuity:

• T — Trend Start

• E — Trend Extension

• H — Structural High / Low

• X — Trend Exit / Reversal

This indicator is intended for market structure analysis and educational purposes only.

It does NOT provide trading signals, buy/sell recommendations, or investment advice.

All labels are generated based on historical price data and do not predict future market movements.

Users should combine this tool with their own analysis and risk management framework.

This script is provided "as is" with no guarantee of accuracy or performance.

ORB M15 Fibo din ORB EMA200 MTFTesting a new idea based on ORB m15. Still on testing, not worth it to translate it into English

SFI Follow Trend Level 1 ( SFI Academy )“SFI Trading Level 1 Indicator is a proprietary indicator used by SFI Academy for its students, in combination with SFI Academy’s exclusive capital management toolset.”

Fundamental Dashboard [Standalone]Overview

The Fundamental Strength Dashboard is a streamlined utility designed to evaluate the fundamental health of a stock directly on your chart. Instead of relying solely on price action, this indicator fetches real-time financial data to assess profitability, valuation, and financial stability.

It aggregates five core financial metrics into a single "Fundamental Score" (0-5) and displays a clear rating (Strong Buy, Buy, Neutral, or Weak/Sell) in a customizable dashboard table.

How It Works

The script analyzes the following 5 Key Fundamental Metrics. For a stock to receive a "point" for a specific metric, it must meet the criteria defined in your settings:

Net Income (Profitability): Checks if the company is actually profitable (Net Income > 0).

EPS (Earnings Per Share): Ensures the company has positive Earnings Per Share (TTM).

P/E Ratio (Valuation): Checks if the stock is valued reasonably compared to your maximum threshold (default: < 45).

Debt-to-Equity (Leverage): Analyzes financial risk. Lower is better (default: < 0.5).

ROE (Efficiency): Measures how effectively management uses equity to generate profit (default: > 15%).

The Scoring System

The indicator calculates a cumulative score based on how many of the above criteria are met:

Score 5/5 → STRONG BUY: The stock meets all profitability, valuation, and stability criteria.

Score 4/5 → BUY: The stock misses only one criterion but is otherwise fundamentally sound.

Score 0-3 → WEAK / SELL: The stock fails multiple fundamental checks (e.g., negative earnings, high debt, or overvaluation).

Features & Customization

Every trader has different risk appetites and sector preferences. You can fully customize the thresholds in the Settings menu:

Max P/E Threshold: Adjust this based on the sector (e.g., Tech stocks typically have higher P/Es than Utilities).

Min ROE %: Set your requirement for management efficiency.

Max Debt/Equity: Tighten or loosen leverage requirements.

Visuals: Change the table position (Top Right, Bottom Right, etc.) and color scheme to match your chart theme.

How to Use

Add the indicator to your chart.

Open the Settings (Gear icon).

Adjust the Dynamic Thresholds to fit the sector you are trading.

Look at the dashboard on the chart to see a snapshot of the stock's fundamental health.

Disclaimer

This script is for educational and informational purposes only. It relies on third-party financial data provided by TradingView, which may occasionally be missing or delayed. Always do your own research (DYOR) before making investment decisions.

Udta Teer Its normal vwap which is already available in tradingview. But it has added bands with help of AI

Druckenmiller Alpha-Physics [Dual-Core]Stop trading in a vacuum. Start trading like a Macro Fund Manager.

The Druckenmiller Alpha-Physics engine is a professional-grade dashboard designed to solve the single biggest problem in trading: Context. Most traders buy a "dip" only to realize it was a crash, or sell a "rip" only to watch it fly higher.

This tool solves this by synthesizing Market Physics (Velocity & Acceleration) across two distinct timeframes (Weekly Macro & Daily Tactical) and filtering every signal through a Global Liquidity Shield.

It is engineered based on the trading philosophy of Stanley Druckenmiller: “I don’t care about the news. I care about the liquidity and the acceleration of the trend.”

How It Works (The Dual-Core Logic)

The engine runs 27 distinct sector assets through a dual-loop physics processor:

The Macro Core (Weekly): Analyzes the 18-month trend. Is the "Tide" coming in or going out?

The Tactical Core (Daily): Analyzes the 3-day price action. Is the "Wave" crashing or rising?

It then synthesizes these two data streams into a single Action Signal.

The Signals (How to Read)

The dashboard tells you exactly what to do based on the conflict between Macro and Micro:

🟢 BUY PULLBACK (The "Alpha" Trade):

Logic: Macro is RIPPING (Bullish) + Tactical is TOP/CRASH (Bearish).

Meaning: You are buying a long-term leader on a short-term discount.

🔵 STINK BID (The "Bottom" Trade):

Logic: Macro is TURNING UP + Tactical is CRASHING.

Meaning: The physics have shifted positive, but price is still dumping. Place limit orders -5% lower to catch the panic bottom.

🔴 SELL RIP (The "Trap" Trade):

Logic: Macro is TOPPING (Bearish) + Tactical is RIPPING (Bullish).

Meaning: The long-term trend is dead. Sell into this short-term rally immediately.

⚪ HOLD: All systems go. Sit on your hands and ride the trend.

The "Invisible" Liquidity Shield

The most dangerous time to buy is when the Fed is draining liquidity. This script monitors the 10-Year Treasury Yield (TNX) and VIX in real-time.

If Liquidity is OK (Navy Header): Signals are valid. Green means Go.

If Liquidity is TIGHT (Maroon Header): The entire dashboard enters "Defense Mode." Buy signals are tinted Maroon to warn you that you are fighting the Fed.

Included Universe (The "Ultimate" List)

Includes 27 institutional-grade tickers covering every corner of the market:

Growth: XLK, SMH, IGV, GRID, QTUM

Cyclical: JETS, XHB, KRE, XLI, XLF

Commodities: GDX, URA, XLE, XLB, TAN

Risk/Safety: IBIT, TLT, XLV, XLP

Note: This script uses dynamic request handling optimized for Pine Script v6. It is designed for Premium/Ultimate plans due to the high volume of data processing (54+ simultaneous streams).

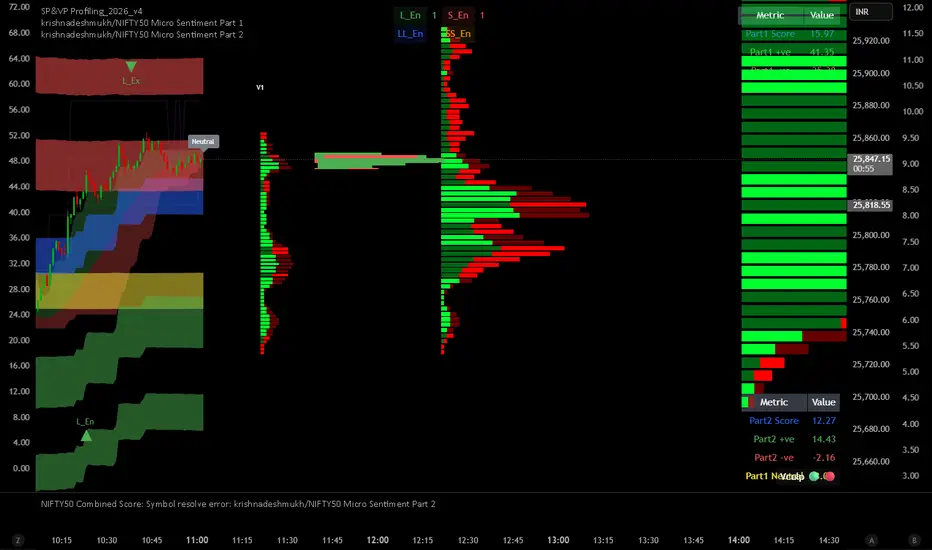

krishnadeshmukh/NIFTY50 Micro Sentiment Part 1📘 Script Description: NIFTY50 Micro Sentiment — Part 1

This indicator tracks real-time micro sentiment across the top 25 weighted stocks of the NIFTY50 index using a volume-based distribution model.

🔍 How it works:

Scans last N bars (configurable) for each stock.

Divides each stock’s price range into equal bins.

Measures bullish vs bearish volume in each bin based on:

Candle Color (Close > Open) or

Close Near High (Close > Midpoint).

Assigns a sentiment value:

+1 → Bullish dominance

-1 → Bearish dominance

0 → Neutral

📊 Each stock's sentiment is weighted by its contribution to the index.

🧮 Displays:

Weighted Sentiment Score

Bullish / Bearish / Neutral Components

Updated every 5 bars with an easy-to-read table.

Use this to gauge underlying micro shifts in sentiment before broader market moves.

krishnadeshmukh/NIFTY50 Micro Sentiment Part 1📘 Script Description: NIFTY50 Micro Sentiment — Part 1

This indicator tracks real-time micro sentiment across the top 25 weighted stocks of the NIFTY50 index using a volume-based distribution model.

🔍 How it works:

Scans last N bars (configurable) for each stock.

Divides each stock’s price range into equal bins.

Measures bullish vs bearish volume in each bin based on:

Candle Color (Close > Open) or

Close Near High (Close > Midpoint).

Assigns a sentiment value:

+1 → Bullish dominance

-1 → Bearish dominance

0 → Neutral

📊 Each stock's sentiment is weighted by its contribution to the index.

🧮 Displays:

Weighted Sentiment Score

Bullish / Bearish / Neutral Components

Updated every 5 bars with an easy-to-read table.

Use this to gauge underlying micro shifts in sentiment before broader market moves.

krishnadeshmukh/NIFTY50 Micro Sentiment Part 2📘 Script Description: NIFTY50 Micro Sentiment — Part 2

This indicator continues the NIFTY50 Micro Sentiment model by analyzing the remaining 25 stocks (Rank 26–50 by index weight) of the NIFTY50.

🔍 Key Features:

Applies the same volume-bin methodology used in Part 1.

Sentiment detection based on:

Candle Color (default) or

*Close vs Midpoint of the candle range.

Stocks are weighted by their index influence.

Output is a clean sentiment table:

+ve / -ve / Neutral Volume Score

Weighted Sentiment Output

Use this in conjunction with Part 1 to analyze the entire NIFTY50 sentiment landscape.

📘 Script Description: NIFTY50 Combined Score

This script aggregates live sentiment data from both:

🧩 NIFTY50 Micro Sentiment — Part 1

🧩 NIFTY50 Micro Sentiment — Part 2

🚀 What it does:

Imports Score, +ve, -ve, and Neutral components from both scripts.

Combines them to produce:

✅ Total Weighted Sentiment

🟢 Bullish Weight

🔴 Bearish Weight

🟡 Neutral Component

📊 Outputs are shown via a middle-right sentiment table, updated every 5 bars.

Perfect for traders seeking a unified view of micro sentiment across the entire NIFTY50 ecosystem — in one glance.

Triple Supertrend + EMA CrossoverCustomized 3 supertrend and EMA crossover which is helpful for identification of the trend.

Adaptive Trend-Based Fib Extension + TrendlinesThis advanced analysis tool is designed to take the guesswork out of Fibonacci trading. By combining Adaptive Fibonacci Extensions with multi-method Pivot Detection, Dynamic Trendlines, and Horizontal Support/Resistance, this indicator provides a comprehensive roadmap for any market trend.

Learn volume trading - @pricevolumetraders

Key Features

Adaptive Fibonacci Engine: Unlike static tools, this indicator uses an ATR-based adaptive factor to adjust extension levels according to current market volatility.

Smart Trend Detection: Automatically identifies trend direction using EMA cross-overs or Higher High/Higher Low sequences to determine whether to plot Bullish or Bearish extensions.

Multi-Method Pivots: Choose from six different pivot detection methods, including Volume-Based, Fractal, ATR-Based, and Long Wick detection, to suit your specific trading style.

Automated Trendlines & S/R: High-probability diagonal trendlines and horizontal S/R levels are drawn only when they meet a minimum "touch" requirement and volume confirmation.

Institutional Zones: Highlights the "Golden Zone" between the 127.2% and 161.8% extension levels, where trends often reach exhaustion or find major targets.

How to Use

Trend Alignment: Use the built-in Dashboard to quickly identify the current trend (Bull/Bear) and RSI momentum.

The 3-Point Setup: The indicator automatically finds Point 1 (Trend Start), Point 2 (Impulse End), and Point 3 (Retracement/Last Touch) to project future price targets.

Entry Confirmation: Look for price action near the 61.8% or 78.6% Retracement levels for high-probability entries in the direction of the trend.

Targeting: Use the extension levels (100%, 127.2%, 161.8%) as your primary Take Profit zones.

Confluence: The strongest setups occur when a Fibonacci level aligns perfectly with a Horizontal S/R line or a Diagonal Trendline.

Technical Settings

Pivot Settings: Adjust 'Left' and 'Right' bars to change the sensitivity of swing high/low detection.

Fib Timeframe: You can anchor Fibonacci levels to a higher timeframe (e.g., 1-hour levels) while trading on a lower timeframe (e.g., 5-minute).

Volume Multiplier: Filter for horizontal levels that were formed with significant institutional volume.

Disclaimer: Trading involves significant risk. This tool is for educational and analytical purposes only and should be used in conjunction with a complete trading plan.

First Presented FVGSummary: First Presented FVG Indicator

This is a Pine Script v6 TradingView indicator that identifies and visualizes the first Fair Value Gap (FVG) that forms within configurable time windows during a trading session.

What it Does

1. Detects FVGs : Uses the classic 3-candle FVG definition:

- Bullish FVG: When low > high (gap up)

- Bearish FVG: When high < low (gap down)

2. "First Presented" Logic : For each configured time slot, it captures only the first qualifying FVG that forms—subsequent FVGs in that window are ignored.

3. Visual Display :

- Draws a colored box spanning from detection time to session end

- Optional text label showing detection time (e.g., "9:38 Tue FP FVG")

- Optional grade lines at 25%, 50%, and 75% levels within the FVG

Key Configuration

Setting Description

Timeframe Only works on 5-minute charts or lower

Timezone IANA timezone for session times (default: America/New_York)

Session Futures trading hours (default: 1800-1715)

Min FVG Size Minimum gap size in ticks to qualify

4 Time Slots Each with enable toggle, time window, and color

Default Time Slots

Slot 1 (enabled): 09:30-10:30 — lime green

Slot 2 (enabled): 13:30-14:30 — blue

Slot 3 (disabled): 13:00-13:30 — teal

Slot 4 (disabled): 14:15-14:45 — fuchsia

Technical Features

Handles cross-midnight sessions correctly

Resets all drawings at each new session

Skips the first bar of each window to ensure valid 3-candle lookback

Clamps slot windows to session boundaries