Auto Position CalculatorA position sizing tool that automatically detects the instrument you're trading and calculates the correct position size based on your risk parameters.

What It Does

This indicator calculates how many contracts, lots, or shares to trade based on your account size, risk percentage, and stop loss distance. It auto-detects the instrument type and adjusts the point/pip value accordingly.

Supported Instruments

Futures: NQ, MNQ, ES, MES, YM, MYM, RTY, M2K, CL, MCL, GC, MGC

Forex: All major pairs (USD, EUR, GBP, JPY, etc.)

Index CFDs: NAS100, US500, US30, GER40, UK100

Metals: XAU, XAG

Crypto and Stocks: Automatic detection

How to Use

Set your account size and risk % in settings

Click the settings icon and place Entry, Stop Loss, and Take Profit on the chart

The position size and risk calculations appear automatically

Levels auto-reset at your chosen session (Asia, London, or New York open)

Limitations

CFD and forex pip values assume standard lot sizing - your broker may differ

Auto-detection relies on ticker naming conventions, which vary by broker/data feed

Session reset times are based on ET (Eastern Time)

Educational

piPH"Signals Refined. Opportunities Defined."

piPH is built for traders who value precision over noise. By demanding multiple confirmations, it avoids the trap of chasing every move and instead focuses on high-probability setups that align with trend, momentum, and divergence.

Josh FXJoshFX Multi-Timeframe Levels & Fair Value Gap Indicator

This powerful TradingView indicator provides a comprehensive view of key market levels and trends across multiple timeframes. Designed for traders who want precise entries and market context, it includes:

Previous Daily Levels: Automatically marks the previous day’s High, Low, and 50% midpoint.

Multi-Timeframe Trend: Displays the trend direction for 5-minute, 15-minute, 1-hour, and 4-hour charts directly on your current chart.

Daily Candle Display: Shows the current daily candle for quick visual reference.

Pivot Points: Accurately marks technical highs and lows (pivot points) to the exact unit on the chart.

Fair Value Gaps (FVGs): Highlights areas of imbalance for potential high-probability trade setups.

JoshFX Telegram Watermark: Includes branding for the JoshFX community.

This all-in-one tool is perfect for traders combining price action, liquidity concepts, and multi-timeframe analysis to find high-quality setups efficiently.

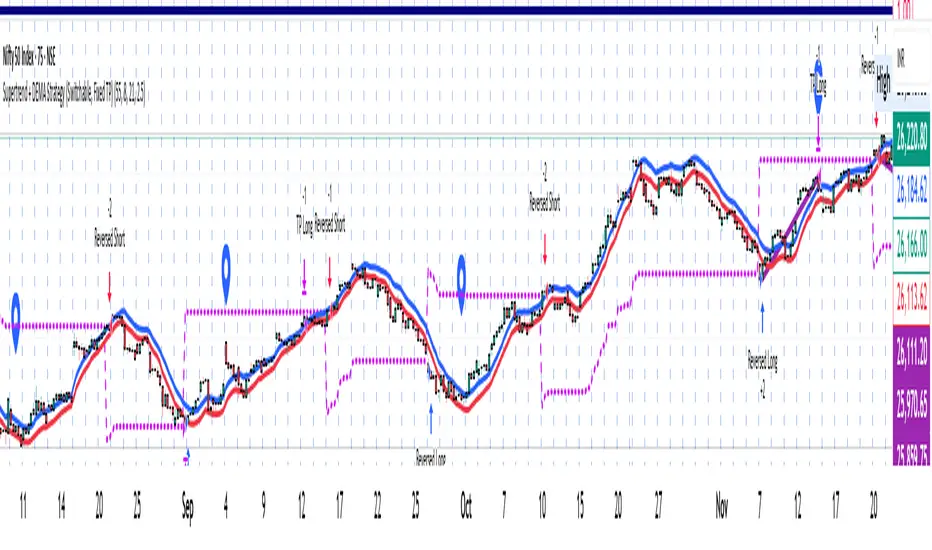

Supertrend + DEMA Strategy ( customised & Switchable, Fixed TP)Supertrend line – a moving line that follows the price and shows whether the market is trending up or down.

If the price goes above this line, it usually means the market is going up.

If the price goes below, it usually means the market is going down.

DEMA (Double Exponential Moving Average) – another line that smooths out price movements to spot trends more clearly.

It calculates an average of prices but reacts faster than a normal moving average.

TIK Options Trade Setup v2TIK Options Trade Setup v2 is a specialized options-based intraday framework designed for Expiryscalping Group Members, premium behavior analysis, and breakout confirmation using both Call (CE) and Put (PE) data.

Using this data, it calculates a set of high-accuracy option scalping levels.

Underlying index (e.g., NIFTY / BANKNIFTY / SENSEX)

💎 Why This Indicator Is Powerful

This system uses both CE and PE data together, making it superior to single-side indicators.

It helps expiry-day traders:

⭐ Identify premium equilibrium

⭐ Predict CE/PE combined reversal zones

⭐ Catch sharp scalps with predefined levels

⭐ Avoid fake breakouts

⭐ Trade with confidence using data-backed zones

EMA+维加斯通道+Boll「ED22x」Multi EMA & Boll Function

- 6 EMA Line.

- Boll Function.

多均线指标+布林带指标

- 6条EMA 均线可自调试

- 可设置维加斯通道

- 布林带指标

By ED22x

X : ED22_x

成交量分位高亮「ED22x」Vol Highlight

with 30% 85% and x3 highlight function.

成交量分位高亮指标

- 加入回朔周期

- 附带20均线

- 自动高亮分别为

< 30%

> 30% < 85%

> 85% <

> 大于平均交易量3倍

By ED22x

X : ED22_x

Top-Down 8 Levels + Wick Alerts + H4 Box (Stable)Top-Down Analysis Box

This Indicator Helps You Do

Perform top-down analysis quickly

Identify HTF liquidity levels instantly

Spot wick taps (liquidity grabs) in real-time

Trade key institutional levels with confidence

Use H4 zones for direction and bias

Set alerts for high-probability reaction levels

VWolf – Apex GateOverview

VWolf – Apex Gate is a trend-continuation system that blends a Pivot-weighted Supertrend (PVT ST) with an optional **Normal Supertrend** trigger, all **gated by a 200-EMA directional filter. The strategy’s risk controls are volatility-aware—**stops and targets scale by ATR**, and quantity is computed from a fixed **% risk per trade**. Clear **Backtest / Forwardtest** modes with date windows let you validate on segmented datasets before committing to live use.

Recommended Use

- **Markets:** High-liquidity instruments (indices, large-cap equities, liquid FX and major crypto pairs) where trends and pullbacks are clean.

- **Timeframes:** 15m–1h for active intraday; 4h–1D for swing. Lower timeframes may benefit from stricter EMA gating and slightly wider ATR stops.

- **Workflow:**

1. Start with **Backtest** to set baseline ATR/EMA parameters.

2. Move to **Forwardtest** to confirm generalization.

3. Consider walk-forward or multi-symbol rotation to assess robustness.

Strengths & Precautions

Strengths

- **Dual engine** (PVT ST + Normal ST) improves signal quality; the **EMA gate** screens counter-trend noise.

- **ATR-native** stops/targets standardize risk across regimes/instruments.

- **Capital-proportional sizing** preserves account geometry and smooths drawdowns.

- **Clear test segmentation** supports objective evaluation.

Precautions

- **Whipsaw risk** in tight ranges: widen ATR multipliers, enable the EMA gate, or require co-confirmation.

- **Supertrend-anchored stops** can expand in volatility spikes; ensure **% risk** remains within tolerance.

- **One-position policy** avoids stacking risk but forgoes scaling into strong trends; advanced users may prefer add-on frameworks outside this baseline.

Conclusion

VWolf – Apex Gate seeks to enter shortly after **regime flips**, demanding alignment between a **pivot-aware Supertrend** and (optionally) a **classic Supertrend**, while an **EMA gate** enforces directional discipline. With **ATR-driven** stops/targets and **fixed-fraction** sizing, the system adapts naturally to changing volatility. Use the **Backtest** window to dial ranges and the **Forwardtest** window to prove durability on unseen data. For best results, tailor ATR multipliers and the EMA gate to your instrument’s structure and your personal drawdown tolerance.

Pivot Alert Bot - Multi-TimeframeOverview

Pivot Alert Bot automatically detects and labels pivot highs and pivot lows as they confirm across multiple timeframes. Designed for active traders who want clean, actionable signals without chart clutter.

Two-Tier Pivot System

📍 Main Pivots (Length 20)

Confirmed swing points that have proven themselves with 20 bars of price action on each side. Marked with clean PH (Pivot High) and PL (Pivot Low) labels. These are your high-conviction levels.

⭐ Temporary Pivots (Length 3)

Early-stage pivots marked with ***** labels in blue. These signal potential reversals before full confirmation — ideal for aggressive entries with tighter stops.

How to Trade

The indicator is built around a simple pivot-to-pivot strategy:

🔴 Short Setup: Enter short at a Pivot High → Target the previous Pivot Low

🟢 Long Setup: Enter long at a Pivot Low → Target the previous Pivot High

This approach gives you logical, structure-based profit targets instead of arbitrary calculations.

Multi-Timeframe Support

Scan for setups across:

⚡ 5 minute — Scalping and quick intraday moves

📊 15 minute — Primary day trading timeframe

📊 30 minute — Confirmation and larger moves

⏱️ 1 hour — Context and swing trade setups

Built-In Alerts

Never miss a pivot. Alert conditions included for:

Main Pivot High confirmed

Main Pivot Low confirmed

Temporary Pivot High detected

Temporary Pivot Low detected

Set alerts once and get notified on any timeframe.

Best Used On

High-volume, liquid instruments: SPY, QQQ, NVDA, TSLA, AMD, META, AMZN, COIN, and similar names with clean price action.

Settings

Adjustable pivot lengths for both main and temporary pivots

Toggle temporary pivot visibility on/off

Customizable label colors and sizes

Global Liquidity - Impulse (ROC & Z-score) [GMI-style]What it is:

Liquidity is a faucet. When central banks add money, the faucet opens (risk-on). When they pull money out, it closes (risk-off). This indicator builds a global net-liquidity proxy and shows its impulse :

- ROC (green/red histogram): % change vs N weeks ago.

- Z-score (cyan line): how unusually strong the latest weekly move is.

Why it matters:

Liquidity impulse often leads risk assets (equities/crypto) by weeks to a few months.

- Green bars > 0 + positive Z → friendlier risk-on backdrop.

- Red bars < 0 + negative Z → tightening conditions; caution.

Data used (TV Economics / FRED):

USA (FRED, millions USD):

- FRED:WALCL (Fed assets)

- FRED:RRPONTSYD (Reverse Repo – subtract)

- FRED:WTREGEN (Treasury General Account – subtract)

Other CBs (Economics, units vary):

- ECONOMICS:EUCBBS (ECB)

- ECONOMICS:JPCBBS (BoJ)

- ECONOMICS:CNCBBS (PBoC)

Optional:

- ECONOMICS:GBCBBS (BoE, UK)

- ECONOMICS:CACBBS (BoC, Canada)

- ECONOMICS:CHCBBS (SNB, Switzerland)

- ECONOMICS:AUCBBS (RBA, Australia)

Proxy (scaled to billions):

(Fed − RRP − TGA) + ECB + BoJ + PBoC +

How to read:

- Green bars above 0 = faucet opening → money in → risk-on.

- Red bars below 0 = faucet closing → money out → risk-off.

- Taller bar = stronger push.

- Cyan Z > +1 = unusually strong positive impulse; Z < −1 = unusually strong negative impulse.

- Background : green when ROC>0 & Z>0 , red when ROC<0 & Z<0 .

Quick reading guide (TL;DR):

- Early risk-on: ROC crosses > 0 and Z > 0 (ideally Z ≥ +1 ).

- Early risk-off: ROC crosses < 0 and Z < 0 (ideally Z ≤ −1 ).

- Use weekly timeframe; price often reacts with a 0–12 week lag.

- Combine with PMIs/New Orders, real yields (down), and credit spreads (narrowing).

Notes:

Symbols may differ by provider; leave optional banks OFF if missing. Currencies/units differ across CBs; this is a pragmatic proxy, not a perfect macro model. Educational use only; not financial advice.

Nifty Participants - Top 10 📌 Nifty Participants – Top 10 (Indicator Description)

This indicator displays the top 10 weighted stocks from the NIFTY index and shows how each stock is contributing to the index movement in real time.

For each participant, the script calculates price change, percentage change, RSI, VWAP position, volume spike, previous day levels, and their estimated participation based on weightage.

A dynamic table is plotted on the chart with color-coded cells for bullish, bearish, and neutral conditions. Users can customize which columns to display (LTP, Change, Change %, Share, RSI, VWAP, Volume Spike, Previous Day High/Low) and select the timeframe for calculations. The index itself appears as the first row for quick comparison.

Volume spikes are highlighted when current volume exceeds a configurable multiple of the average volume. RSI and VWAP columns also use adaptive coloring to quickly show strength or weakness.

All weightages are user-editable, and the table automatically limits output to the selected number of rows. This makes it an ideal real-time market breadth and contribution tracker for intraday and positional traders.

Micro Pullback Entry SystemMicro Pullback Entry System - Quick Reference

The Pattern

▲ ENTRY (first green to break high)

│

┌──┴───┐

│ 1-3 │ ← PULLBACK (red candles)

│ red │ Stop = Low of this zone

└──────┘

│

┌──┴───┐

│ 3+ │ ← THE MOVE (green candles)

│green │ Strong momentum

└──────┘

Pattern Checklist

Requirement: Why It Matters

3+ green candlesConfirms momentum

1-3 red pullback Brief = momentum intact< 50% retracementShallow = buyers in controlVolume on entryConfirms breakout Above EMA Trend support

Status Flow

Scanning... → 📈 TRENDING → 👀 WATCHING → ⏳ FORMING → 🎯 ENTRY!

StatusMeaningActionScanningLooking for setupWait📈 TRENDINGGreen streak buildingMonitor👀 WATCHINGPullback startedPrepare⏳ FORMINGValid pullback readyGet ready!🎯 ENTRY!Signal triggeredExecute

Entry/Stop/Target

LevelLine ColorHow to SetEntryLime solidClose of signal candleStopRed dashedLow of pullbackTarget 1Aqua dottedEntry + (2 × Risk)Target 2Yellow dottedEntry + (3 × Risk)

Example

Entry: $5.00

Stop: $4.80

Risk: $0.20

Target 1 (2R): $5.00 + $0.40 = $5.40

Target 2 (3R): $5.00 + $0.60 = $5.60

Quality Grades

GradeScoreActionA+5/5 ✓Best setup - full sizeA4/5 ✓Good setup - standard sizeB3/5 ✓Average - reduced sizeC2/5 ✓Weak - skip or tiny size

Scoring Factors

✓ Green streak met minimum

✓ Pullback length valid (1-3)

✓ Retracement shallow (<50%)

✓ Volume confirmed

✓ Above EMA

Trade Execution

Entry

Wait for "⏳ FORMING" status

Watch for green candle forming

Entry triggers when green candle closes above pullback high

Enter at market or small limit above current price

Stop Loss

Set at pullback low (red dashed line)

Non-negotiable - this is your max risk

Trade Management

If no immediate follow-through → exit early

Take 50% off at Target 1 (aqua line)

Move stop to breakeven

Let remainder run to Target 2

Settings Guide

Default (Recommended)

Min Green Candles: 3

Min Pullback: 1

Max Pullback: 3

Max Retracement: 50%

Volume Multiplier: 1.2x

EMA Filter: ON (20)

Conservative (Fewer, Better)

Min Green Candles: 4

Min Pullback: 2

Max Pullback: 3

Max Retracement: 40%

Volume Multiplier: 1.5x

EMA Filter: ON (20)

Aggressive (More Signals)

Min Green Candles: 2

Min Pullback: 1

Max Pullback: 4

Max Retracement: 60%

Volume Multiplier: 1.0x

EMA Filter: OFF

Common Mistakes

❌ Entering before signal

Wait for green triangle

"FORMING" ≠ "ENTRY"

❌ Wide stop

Stop must be at pullback low

If too wide, skip the trade

❌ Ignoring volume

Low volume entries fail more often

Look for ✓ in volume row

❌ Fighting trend

Check EMA status

Should show "Above ✓"

❌ Chasing after entry

If you miss entry by 3+ candles, wait for next setup

Don't chase extended moves

Best Setups

A+ Quality Setup ✓

4-5 green candles (strong move)

2 candle pullback (brief)

25-35% retracement (shallow)

2x+ volume on entry

Well above EMA

Stock already up 5%+ on day

Avoid These ✗

Only 2 green candles

4+ candle pullback (losing momentum)

50%+ retracement (too deep)

Below average volume

Below or at EMA

Against market direction

Timeframe Guide

TFSignalsQualityBest For1mMostLowerScalping5mBalancedGoodDay trading15mFewestHigherSwing entries

Quick Decision Tree

1. Status showing "FORMING"?

NO → Wait

YES → Continue

2. Quality grade A or better?

NO → Skip or small size

YES → Continue

3. Volume confirmed (✓)?

NO → Caution, reduce size

YES → Continue

4. Above EMA (✓)?

NO → Skip

YES → Continue

5. Risk acceptable? (Stop not too wide)

NO → Skip

YES → TAKE THE TRADE

Alert Setup

Essential Alert

"Micro Pullback Entry" - Main signal

How to Set

Right-click chart → Add Alert

Condition: Micro Pullback Entry System

Select "Micro Pullback Entry"

Set notification preferences

Combining with Other Indicators

IndicatorHow to Use5 PillarsFind stocks meeting criteria firstGap & GoLook for micro pullbacks after gap breakoutsR2G TrackerConfirm stock is green before enteringFloat RotationHigh rotation + micro pullback = best setupsBull FlagMicro pullback is a "mini" bull flag

Example Trade

Stock: XYZ

Pre-market: Gapped up 15%

9:35 - 9:38: 4 green candles (move from $4.50 to $5.00)

9:39 - 9:40: 2 red candles (pullback to $4.85)

9:41: Green candle breaks $4.90 (pullback high)

ENTRY: $4.92

STOP: $4.82 (pullback low)

RISK: $0.10

TARGET 1: $5.12 (+$0.20 = 2R)

TARGET 2: $5.22 (+$0.30 = 3R)

Result: Hit Target 2 by 9:55 → +$0.30 per share

Key Takeaways

Micro = 1-3 candles - Brief pullback

Entry = First green to break high - Specific trigger

Stop = Pullback low - Tight risk

Quality matters - Focus on A/A+ setups

Breakout or bailout - Exit if no follow-through

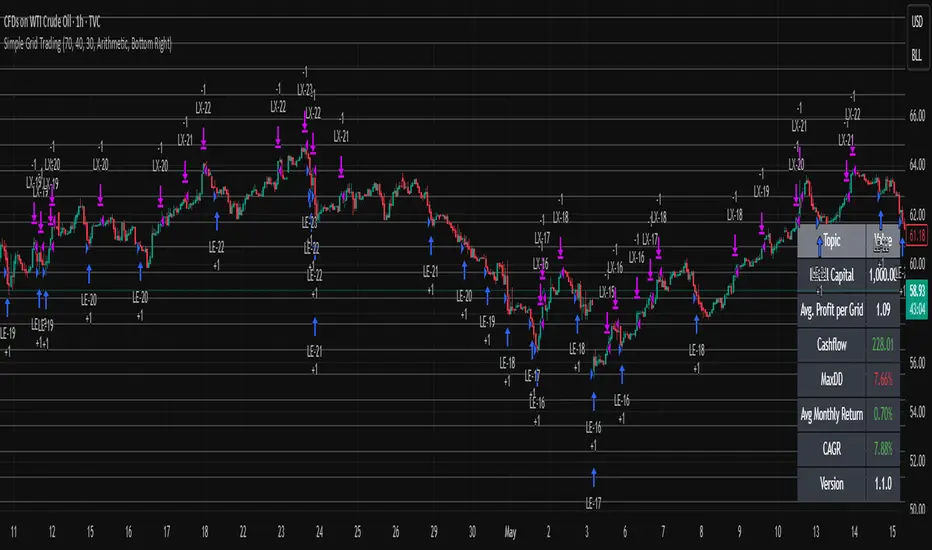

Simple Grid Trading v1.0 [PUCHON]Simple Grid Trading v1.0

Overview

This is a Long-Only Grid Trading Strategy developed in Pine Script v6 for TradingView. It is designed to profit from market volatility by placing a series of Buy Limit orders at predefined price levels. As the price drops, the strategy accumulates positions. As the price rises, it sells these positions at a profit.

Features

Grid Types : Supports both Arithmetic (equal price spacing) and Geometric (equal percentage spacing) grids.

Flexible Order Management : Uses strategy.order for precise control and prevents duplicate orders at the same level.

Performance Dashboard : A real-time table displaying key metrics like Capital, Cashflow, and Drawdown.

Advanced Metrics : Includes Max Drawdown (MaxDD) , Avg Monthly Return , and CAGR calculations.

Customizable : Fully adjustable price range, grid lines, and lot size.

Dashboard Metrics

The dashboard (default: Bottom Right) provides a quick snapshot of the strategy's performance:

Initial Capital : The starting capital defined in the strategy settings.

Lot Size : The fixed quantity of assets purchased per grid level.

Avg. Profit per Grid : The average realized profit for each closed trade.

Cashflow : The total realized net profit (closed trades only).

MaxDD : Maximum Drawdown . The largest percentage drop in equity (realized + unrealized) from a peak.

Avg Monthly Return : The average percentage return generated per month.

CAGR : Compound Annual Growth Rate . The mean annual growth rate of the investment over the specified time period.

Strategy Settings (Inputs)

Grid Settings

Upper Price : The highest price level for the grid.

Lower Price : The lowest price level for the grid.

Number of Grid Lines : The total number of levels (lines) in the grid.

Grid Type :

Arithmetic: Distance between lines is fixed in price terms (e.g., $10, $20, $30).

Geometric: Distance between lines is fixed in percentage terms (e.g., 1%, 2%, 3%).

Lot Size : The fixed amount of the asset to buy at each level.

Dashboard Settings

Show Dashboard : Toggle to hide/show the performance table.

Position : Choose where the dashboard appears on the chart (e.g., Bottom Right, Top Left).

How It Works

Initialization : On the first bar, the script calculates the price levels based on your Upper/Lower price and Grid Type.

Entry Logic :

The strategy places Buy Limit orders at every grid level below the current price.

It checks if a position already exists at a specific level to avoid "stacking" multiple orders on the same line.

Exit Logic :

For every Buy order, a corresponding Sell Limit (Take Profit) order is placed at the next higher grid level.

MaxDD Calculation :

The script continuously tracks the highest equity peak.

It calculates the drawdown on every bar (including intra-bar movements) to ensure accuracy.

Displayed as a percentage (e.g., 5.25%).

Disclaimer

This script is for educational and backtesting purposes only. Grid trading involves significant risk, especially in strong trending markets where the price may move outside your grid range. Always use proper risk management.

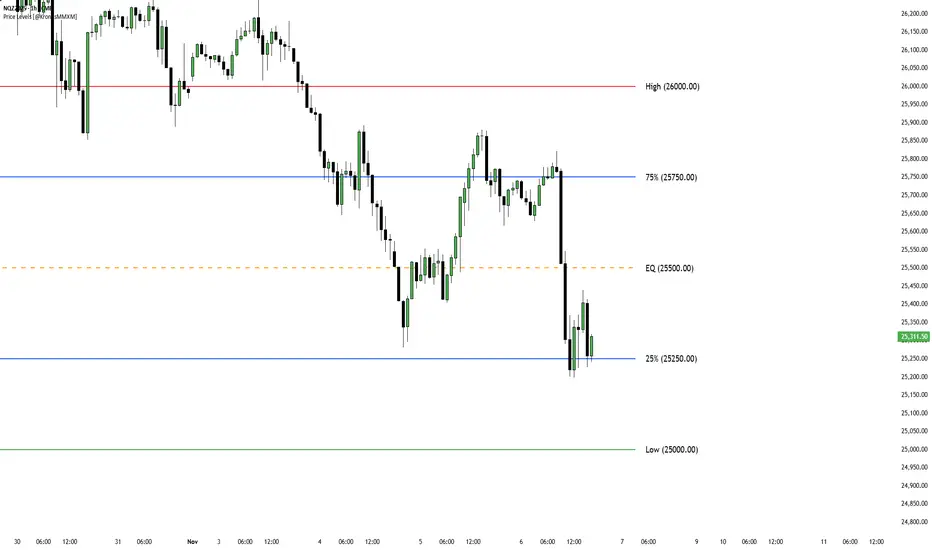

Fixed Price LevelsOverview

This indicator automatically calculates and plots fixed horizontal dealing ranges based on "Power of 10" mathematics. Unlike dynamic ranges that move with every tick or rely on lagging averages, these levels are fixed to specific mathematical grids (10s, 100s, 1000s, etc.). This provides a clean, objective structure for analyzing price action, psychological levels, and market equilibrium without the noise of repainting levels.

How it Works

The indicator uses a mathematical floor function to "snap" the current price to the nearest grid bottom based on your selected multiplier. This creates a static box around price.

The core formula concept is:

Dealing Range Low = math.floor(price / multiplier) * multiplier

Dealing Range High = Dealing Range Low + multiplier

Equilibrium (EQ) = Dealing Range Low + (multiplier / 2)

Key Features

Power of 10 Multipliers: Select between 1, 10, 100, 1000, or 10000 to suit your asset class (e.g., 100 for Indices, 0.01 logic for Forex).

Adjacent Ranges: Automatically plots ranges above and below the current price action to see future targets or support levels immediately.

Overlap Prevention: Includes logic to prevent label clutter. When multiple ranges are active, it ensures that a "Range High" and the next "Range Low" do not overlap visually.

Quarter Levels: Option to display the 25% and 75% levels within the range for granular precision.

Visual Customization: Full control over line extensions (Left, Right, Both, None) and label placement.

Settings Overview

Range Multiplier: Select the base grid size.

Number of Adjacent Ranges: Determines how many grid boxes to draw above and below the current price.

Visual Settings: Customize colors, styles (Solid, Dashed, Dotted), and widths for Low, High, EQ, and Quarters.

Pro Order Flow – NQ 5m/15mThis is a professional-grade order flow tool designed for scalpers and intraday futures traders (especially NQ 5m/15m, ES, SPY, BTC, and gold).

Right-click indicator → Move to new pane below (recommended, so price is clean)

It combines five high-probability institutional signals into one clean, fast indicator:

What This Indicator Shows

1. Candle Delta Histogram (Buyer vs Seller Pressure)

Each bar shows whether aggressive buyers (market orders lifting ask) or aggressive sellers (hitting bid) controlled that candle.

Green = buying pressure

Red = selling pressure

2.Session Cumulative Delta (True Direction)

Tracks buyer/seller domination for the entire session.

Rising cumDelta = buyers absorbing sellers

Falling cumDelta = sellers absorbing buyers

If price goes up but cumulative delta goes down → distribution (short signal)

If price goes down but cumulative delta goes up → accumulation (long signal)

This is one of the strongest institutional signals.

3 Big Delta Bars (Unusual Aggression)

Highlights candles where delta is 2.2× larger than average volume.

These mark:

Institutional absorption

Breakout pressure

Stop-run attacks

Failed breakout reversals

Green = big buying aggression

Red = big selling aggression

4 Smart-Money Wick Absorption (Absorb↑ / Absorb↓)

Tracks wick length vs body size + delta.

Used to detect:

Stop hunts

Liquidity grabs

Reversals off trapped traders

Absorb↓ (triangle up) = buyers absorbed sell-side liquidity (bullish)

Absorb↑ (triangle down) = sellers absorbed buy-side liquidity (bearish)

This is a high-confidence signal for NQ.

5 Real Delta Divergences (Δ Bull / Δ Bear)

Not RSI divergences — order flow divergences:

🔻 Bearish Delta Divergence (Δ Bear)

Price makes higher high

Cumulative delta makes lower high → buyers weakening

High-probability short

🔺 Bullish Delta Divergence (Δ Bull)

Price makes lower low

Cumulative delta makes higher low → sellers weakening

High-probability long

These are professional reversal points.

How to Use (Trading Strategy)

Recommended for:

NQ 5m entries + 15m bias, ES, SPY, BTC, gold.

🟩 Long Setup (Buy)

On 15m, session cumulative delta sloping UP

Price in an uptrend (higher highs/lows)

On 5m, look for ANY of these:

Δ Bull divergence

Absorb↓ tail after a stop-hunt wick

Big positive delta bar at support

Delta flips from red → green at VWAP

Entry: Enter on close of the signal candle

Stop: Below swing low or wick

Targets: Next liquidity high, or 2R–3R

🟥 Short Setup (Sell)

On 15m, session cumulative delta sloping DOWN

Price in a downtrend

On 5m, look for:

Δ Bear divergence

Absorb↑ tail above a high

Big negative delta bar

Delta flips from green → red at resistance

Entry: Enter on close

Stop: Above wick or structure

Targets: Prior low, or 2R–3R

Best Timeframes

15m = trend/bias

5m = signal + entry

Works on: NQ, ES, SPY, QQQ, BTC, Gold, Oil

Settings (Recommended)

Avg Volume Length = 100 (best for NQ volatility)

Big Delta Sensitivity = 2.2×

Pivots = 3 left / 3 right (good for intraday swings)

Included Alerts

Bullish Delta Divergence

Bearish Delta Divergence

Big Positive Delta (aggressive buying)

Big Negative Delta (aggressive selling)

Perfect for scalpers who want real-time signals.

Sessions Indicator(clean))🔰 True Day Open + Asian / London / NY Session Levels

Intraday Market Structure & Session Liquidity Indicator

This indicator automatically plots the True Day Opening Price, Asian Session High & Low, London Session High & Low, and New York Session Open — helping you understand daily directional bias, session liquidity zones, and potential reversal levels.

📌 What It Does

✔ Plots True Day Open (not broker-based — captures real market direction)

✔ Marks Asia Session High & Low – accumulation zone

✔ Marks London Session High & Low – expansion zone

✔ Shows New York Session Open – reversal / continuation zone

✔ Works on any chart: Forex, Indices, Crypto, Commodities

✔ Ideal for ICT / SMC / Day Trading / Scalping

✔ Fully customizable colors & display options

🧠 Why It’s Useful

The market often moves in this sequence:

➡ Asia → consolidation

➡ London → expansion / breakout

➡ New York → reversal OR continuation

This indicator helps you see this structure clearly, allowing traders to:

Avoid fake breakouts

Understand the daily bias earlier

Trade liquidity grabs & session-to-session transitions

Time entries with precision

📌 Best Timeframes

M5 / M15 / M30 → Scalping & intraday setups

H1 / H4 → Market structure view

Daily → Session zone backtesting

⚙ Inputs & Customization

Enable/Disable each session

Change session time manually

Color settings

Line styles: solid / dashed / background zones

🧠 Suggested Trading Concepts

Works great with:

Smart Money Concepts (SMC)

ICT Models

Liquidity Sweep Strategy

Session Breakout Trading

Mean Reversion Trading

📈 How to Use

Wait for Asian Range

Trade break of Asian High/Low during London

At NY Open, check for reversal or continuation

Use True Day Open for directional bias

Look for liquidity sweeps near session levels

📢 Coming Soon (Next Update)

🔔 Session Break Alerts

📊 Liquidity Sweep Labels

RSI Rate of Change (ROC of RSI)The RSI Rate of Change (ROC of RSI) indicator measures the speed and momentum of changes in the RSI, helping traders identify early trend shifts, strength of price moves, and potential reversals before they appear on the standard RSI.

While RSI shows overbought and oversold conditions, the ROC of RSI reveals how fast RSI itself is rising or falling, offering a deeper view of market momentum.

How the Indicator Works

1. RSI Calculation

The indicator first calculates the classic Relative Strength Index (RSI) using the selected length (default 14). This measures the strength of recent price movements.

2. Rate of Change (ROC) of RSI

Next, it computes the Rate of Change (ROC) of the RSI over a user-defined period.

This shows:

Positive ROC → RSI increasing quickly → strong bullish momentum

Negative ROC → RSI decreasing quickly → strong bearish momentum

ROC crossing above/below 0 → potential early trend shift

What You See on the Chart

Blue Line: RSI

Red Line: ROC of RSI

Grey dotted Zero Line: Momentum reference

Why Traders Use It

The RSI ROC helps you:

Detect momentum reversals early

Spot bullish and bearish accelerations not visible on RSI alone

Identify exhaustion points before RSI reaches extremes

Improve entry/exit precision in trend and swing trading

Validate price breakouts or breakdowns with momentum confirmation

Best For

Swing traders

Momentum traders

Reversal traders

Trend-following systems needing early confirmation signals

BETA ZONES v1.0BETA ZONES v1.0 Indicator

Overview

BETA ZONES v1.0 is a comprehensive technical analysis tool designed for TradingView, combining an EMA-based ribbon with dynamic glow zones, structural pivot detection, and real-time ATR visualization. This overlay indicator helps traders identify trends, support/resistance zones, and potential breakout points by blending moving averages, volatility-based shading, and pivot structures. It's particularly useful for trend-following strategies, swing trading, and confirming market reversals on any timeframe or asset, including those using Heikin Ashi candles (as it incorporates real close data to bypass transformations).

The indicator emphasizes visual clarity with color-coded elements: bullish trends in shades of green/lime and bearish in red/maroon. It includes customizable toggles for each component, allowing users to focus on specific features without cluttering the chart.

Key Features

• EMA Ribbon & Glow System:

o Displays a ribbon formed by three EMAs (5, 20, and 50 periods) with gradient fills between them, colored based on trend strength.

o A dynamic "glow" zone around the 50-period EMA, calculated using ATR (Average True Range), acts as a volatility-based support (bullish) or resistance (bearish) band. The glow expands/contracts with market volatility, providing a visual buffer for potential price reactions.

o Real Close Dot: A small circle plotted at the actual closing price of each bar (sourced from standard candles), aiding in precise data verification even on transformed charts like Heikin Ashi.

• Structural Pivots:

o Automatically detects and labels confirmed pivot highs and lows using customizable symbols (e.g., arrows, dots, or curves).

o Draws breakout lines connecting pivots to the bar where structure is broken (Break of Structure - BOS), highlighting bullish (green) or bearish (red) shifts.

o Pivots are trend-aware: In uptrends, it tracks higher highs/lows until a downside break; in downtrends, lower highs/lows until an upside break.

• Real ATR Display:

o A compact table at the bottom-center of the chart showing the current 14-period ATR value (calculated on real data), useful for gauging volatility and setting stop-losses or targets.

How It Works

• EMA Ribbon Logic: The fast EMA (5) is compared to the mid (20), and mid to slow (50), to determine sub-trends. Price relative to the slow EMA sets the overall bullish/bearish bias. Fills create a "ribbon" effect, with colors intensifying in strong trends.

• Glow Zone: Uses a user-defined ATR length and multiplier to create upper/lower bands around the slow EMA. The glow is one-sided: below for bullish (support) and above for bearish (resistance), with semi-transparent shading for easy price overlay.

• Pivot Detection: Tracks the current trend direction (up or down) and reference high/low from the last confirmed pivot. A breakout (close crossing the reference level) confirms a new pivot, labels it, and optionally draws a line to the breakout bar. Bar coloring (yellow) highlights breakout candles.

• Data Handling: All calculations use real close prices via request.security to ensure accuracy on non-standard chart types.

Settings and Customization

The indicator is divided into intuitive input groups for easy configuration:

1. EMA Ribbon & Glow:

o Show EMA Ribbon & Glow: Master toggle to enable/disable the entire ribbon and glow (default: true). Note: Real Close Dot is independent.

o ATR Length (Glow): Lookback for ATR calculation (default: 3; higher = smoother glow).

o ATR Multiplier (Glow Size): Scales the glow width (default: 0.15; higher = wider zone).

o Show Real Close Dot: Toggle for the orange dot at real closes (default: true).

o Real Close Dot Color: Customize the dot's color (default: orange).

2. Structural Pivots:

o Show Pivot Labels: Toggle visibility of high/low symbols (default: true).

o Pivot Symbol Style: Choose from pairs like "︽ ︾" (low/high) or "•" (dots) (default: "•").

o Label Size: Adjust symbol size (Tiny to Huge; default: Normal).

o Pivot High/Low Label Colors: Set colors for labels (default: white).

o Show Breakout Lines: Toggle lines from pivot to breakout (default: true).

o Line Width: Thickness of breakout lines (default: 2).

o Line Style: Solid, Dashed, or Dotted (default: Solid).

o Resistance Break Line (Bullish): Color for upside breaks (default: green).

o Support Break Line (Bearish): Color for downside breaks (default: red).

No additional inputs are required for the ATR table, as it's always displayed on the last bar for quick reference.

Usage Tips

• Trend Identification: Use the EMA ribbon colors to gauge momentum—full green for strong bulls, red for bears. The glow zone can act as a dynamic entry/exit area (e.g., buy near bullish glow support).

• Breakout Trading: Watch for pivot labels and BOS lines as signals for trend reversals. Combine with volume or other indicators for confirmation.

• Volatility Awareness: The displayed ATR(14) helps in position sizing; for example, set stops at 1-2x ATR from entry.

• Chart Compatibility: Works best on candlestick or Heikin Ashi charts. For lower timeframes, reduce ATR length for faster reactivity; increase for higher timeframes.

• Limitations: Pivots are reactive and may lag in ranging markets. Glow is based on historical ATR, so it doesn't predict future volatility.

This indicator is in beta (v1.0) and open to feedback for improvements. Add it to your chart via TradingView's indicator search and experiment with settings to fit your strategy!

Wyckoff Accumulation/Distribution - Enhanced by ChakraWyckoff Accumulation/Distribution - Enhanced Indicator

Overview

An advanced Pine Script v6 indicator that detects Wyckoff accumulation and distribution patterns using RSI-based trend analysis, pivot detection, and volume confirmation. This enhanced version improves upon traditional Wyckoff indicators with cleaner code, English variable names, and additional market structure signals.

Key Features

Wyckoff Phase Detection

Accumulation Phase:

SC (Selling Climax): Bottom pivot with extreme bearish RSI and high volume

AR (Automatic Rally): First bounce after selling climax

ST (Secondary Test): Retest of lows without extreme RSI

SOS (Sign of Strength): Strong bullish breakout with volume confirmation ⭐ NEW

Distribution Phase:

BC (Buying Climax): Top pivot with extreme bullish RSI and high volume

DAR (Automatic Reaction): First drop after buying climax

DST (Distribution Secondary Test): Retest of highs

SOW (Sign of Weakness): Strong bearish breakdown with volume confirmation ⭐ NEW

Market Structure Events

Spring: False breakdown (RSI crosses above lower band) with background highlight

UTAD (Upthrust After Distribution): False breakout (RSI crosses below upper band) with background highlight

Visual Features

Range Boxes: Automatically draws consolidation ranges (gray) that change color on breakout:

🟢 Green = Accumulation (bullish breakout)

🔴 Red = Distribution (bearish breakout)

Pivot Markers: Orange triangles show regular (non-Wyckoff) pivot points

Bar Coloring: Lime bars for bullish trends, purple bars for bearish trends

Color-Coded Labels: All Wyckoff events clearly marked with descriptive text

Customizable Settings

RSI Settings:

RSI Length (default: 14)

Trend Sensitivity (default: 20) - Higher values = more sideways detection

Pivot Settings:

Pivot Length (default: 5) - Controls pivot point detection sensitivity

Display Options:

Toggle range boxes on/off

Toggle regular pivot markers

Toggle bar coloring by trend

Customize label text color

Advanced Detection:

Volume Confirmation toggle - Require high volume for climax events

Volume Threshold (default: 1.5x) - Adjustable volume multiplier

Alerts

8 comprehensive alert conditions:

Selling Climax (SC)

Buying Climax (BC)

Spring detection

UTAD detection

Sign of Strength (SOS)

Sign of Weakness (SOW)

Range Breakout

Improvements Over Original

✅ Pine Script v6 (latest version)

✅ English variable names (was Turkish)

✅ Fixed DAR label bug (was showing "AR")

✅ Added SOS (Sign of Strength) detection

✅ Added SOW (Sign of Weakness) detection

✅ Optional volume confirmation toggle

✅ Organized input groups for better UX

✅ Enhanced visual options

✅ Comprehensive alert system

✅ Cleaner, more maintainable code structure

Best Use Cases

Timeframes: Works on all timeframes; best on 4H, Daily, or Weekly

Markets: Stocks, Forex, Crypto, Indices

Trading Style: Swing trading, position trading, market structure analysis

Combine With: Support/Resistance, Volume Profile, Order Flow analysis

How It Works

The indicator uses RSI to identify market states (sideways, bullish, bearish) and combines this with pivot point detection and volume analysis to identify key Wyckoff events. When price is ranging (RSI between upper/lower bands), it draws a box. On breakout, the box color changes to indicate accumulation or distribution, helping traders identify smart money positioning.

Tips for Use

Lower Trend Sensitivity (10-15) for more signals in trending markets

Higher Trend Sensitivity (25-30) for clearer signals in choppy markets

Enable Volume Confirmation in high-volume markets (stocks, major crypto)

Disable Volume Confirmation in low-volume or forex markets

Watch for Spring/UTAD events within boxes for potential reversals

Version: 1.0

Pine Script: v6

Author: Chakrapani Chittabathina

Pulse & Trend AnalysisPulse & Trend Analysis

The Pulse & Trend Analysis indicator is designed to help traders quickly identify potential trend shifts using the crossover and crossunder of EMA 20 and EMA 50.

When EMA 20 crosses above or below EMA 50, the indicator highlights it visually with colored arrows and “Pulse” signals, making trend changes easy to spot.

How the Script Works?

When EMA 20 crosses above EMA 50 and corresponding Candle close into Green color, the script generates a Pulse Positive signal,

shown with: Blue Arrow Up, Text: “PULSE POSITIVE”

When EMA 20 crosses below EMA 50 and corresponding Candle close into Red color, the script generates a Pulse Negative signal, shown with:

Red Arrow Down, Text: “PULSE NEGATIVE”

These signals help traders visually detect potential bullish or bearish momentum shifts.

How Users Can Benefit From This Indicator?

The Trend & Pulse Analysis indicator allows traders to quickly understand the prevailing market direction by analyzing the interaction between EMA 20 and EMA 50. When a Pulse Positive (bullish crossover) occurs, it signals increasing upward momentum, helping traders focus on long opportunities. Similarly, a Pulse Negative (bearish crossunder) highlights weakening trend strength and supports short-side setups.

This indicator becomes even more powerful when combined with Demand & Supply Zones.

By integrating trend direction, momentum pulses, and zone-based confluence, users can make more informed decisions.

What Makes This Indicator Unique?

The Trend & Pulse Analysis indicator stands out because it adds an important layer of price-action confirmation to traditional EMA crossover signals. Unlike standard crossover tools that trigger signals on every EMA interaction, this indicator filters out weak setups by checking candle strength and direction at the moment of crossover.

A Pulse Positive signal is triggered only when the crossover occurs on a bullish (green) candle.

A Pulse Negative signal is triggered only when the cross under occurs on a bearish (red) candle.

This built-in candle-confirmation mechanism makes the signals more reliable, reduces noise, and gives traders higher-confidence trend continuation.

Additionally, when combined with supply & demand concepts—

Pulse Positive with Demand Zone → strengthens bullish conviction

Pulse Negative with Supply Zone → strengthens bearish conviction

This fusion of EMA trend logic + candle confirmation + supply-demand confluence is what makes the indicator truly unique and powerful for smart traders.

How This Indicator Is Original?

The Trend & Pulse Analysis indicator is completely original because it is built on a custom-designed logic that goes beyond a simple EMA crossover system. While standard indicators only detect crossover/crossunder of moving averages, this tool introduces a dual-filter confirmation approach:

Directional Candle Validation

A Pulse Positive signal is triggered only when EMA20 crosses above EMA50 AND the same candle closes bullish (green).

A Pulse Negative signal is triggered only when EMA20 crosses below EMA50 AND the same candle closes bearish (red).

Custom Pulse System (Not a Standard EMA Indicator)

The “Pulse Positive / Pulse Negative” framework is a uniquely designed concept that combines trend direction, momentum shift, and candle strength.

Manual Programming & Original Condition Set

Every rule, filter, and plotting condition is hand-coded — not copied from open-source scripts.

The system uses:

Custom plotting rules

Custom conditional checks

Custom text + arrow logic

Combined trend + candle behavior analysis

This makes the indicator fully original and not a replica of any existing public script.

Disclaimer:

This indicator is created for educational and analytical purposes.

It does not provide buy or sell signals, financial advice, or guaranteed trading outcomes.

All trading decisions are solely your responsibility.

Market trading involves risk; always use proper risk management.

Micro/Mini P&L [LDT]Overview

Micro/Mini P&L is a risk and P&L visualization tool built primarily for futures traders.

It provides accurate dollar-based calculations for either micros or minis, regardless of which contract type you are currently charting.

The indicator automatically detects your instrument (NQ, MNQ, ES, MES, YM, RTY, CL, GC, etc.) and adjusts point-value data accordingly, allowing you to chart one contract while evaluating risk for another.

This removes the need for manual conversions and keeps your position data consistent at all times.

Although optimized for futures, the tool also works on any other asset for general trade-level visualization.

Features

• Automatic instrument detection for major futures markets including NQ/MNQ, ES/MES, YM/MYM, RTY/M2K, CL/MCL, GC/MGC and others.

Point-value logic adjusts instantly based on the detected symbol ensuring accurate calculations without manual configuration.

• Micro/Mini display toggle, allowing you to calculate dollar values for either contract type regardless of which contract is on your chart.

Useful for traders who prefer charting minis whilst trading micros or the opposite.

• Trade-level visualization, including Entry, Take Profit and Stop Loss levels with automatically drawn lines and optional TP/SL zone shading for clear and structured display on the chart.

• Dynamic P/L calculations, showing both point-based and dollar-based metrics in real time.

This includes TP/SL dollar values, points to target/stop, real-time P/L and an optional risk-reward ratio.

• Adaptive risk table, displaying contract counts from 1 up to your selected maximum, total dollar risk for each row and highlighting your chosen contract size.

This provides a straightforward method for evaluating risk, scaling and position sizing.

• Customizable display options, including color settings, label visibility, extension length, bar offsets and table positioning.

This allows the tool to remain clean, unobtrusive and easy to integrate into any chart layout.

Purpose

This tool is designed to give futures traders a clear, consistent and reliable way to view dollar-accurate risk per contract without performing manual conversions.

Whether you trade micros or minis, the displayed values always align with your selected contract type, even when charting the opposite market.