Fed Net Liquidity [Premium] [by Golman Armi]This indicator visualizes the USD Net Liquidity injected into the financial system by the Federal Reserve.

It is a fundamental macro-economic tool essential for understanding the underlying "fuel" driving risk assets such as the S&P 500 (SPX), Nasdaq (NDX), and Bitcoin (BTC).

Unlike many other liquidity scripts that incorrectly use Commercial Bank Assets (USCBBS), this script uses the Federal Reserve Total Assets (WALCL) to provide a mathematically accurate representation of Central Bank liquidity.

How It Works (The Formula)

Net Liquidity represents the actual cash available to the banking system for investment after government liabilities are subtracted. The formula used is:

NetLiquidity=WALCL−TGA−RRP

Where:

WALCL (Fed Balance Sheet): The total assets held by the Federal Reserve (The source of money printing).

TGA (Treasury General Account - WTREGEN): The checking account of the US Government. When the TGA goes up, money is removed from the economy; when it goes down, money is spent into the economy.

RRP (Reverse Repo - RRPONTTLD): Cash parked by banks and money market funds at the Fed overnight. A rise in RRP removes liquidity from the markets.

Features

Accurate Data Sourcing: Pulls daily data directly from FRED (Federal Reserve Economic Data).

Unit Correction: Automatically adjusts conflicting units (Millions vs Billions) from TradingView data feeds to output a correct value in Trillions of Dollars.

Trend Cloud: Features a smoothing EMA (Exponential Moving Average) with a color-coded cloud to easily identify the macro trend (Green for expansion, Red for contraction).

How to Use

Trend Correlation:

Rising Line (Green): Liquidity is expanding. Historically, this supports bullish trends in stocks and crypto.

Falling Line (Red): Liquidity is being drained (QT or TGA refill). This often leads to volatility or bearish trends in risk assets.

Divergences (The most powerful signal):

If the S&P 500 or Bitcoin makes a New High, but Net Liquidity makes a Lower High, it indicates a "hollow rally" lacking fundamental support, often preceding a correction.

Disclaimer

This tool is for educational purposes and macro-economic analysis only. It is not financial advice.

Macro

BTC Price Prediction Model [Global PMI]V2🇺🇸 English Guide

1. Introduction

This indicator was created by GW Capital using Gemini Vibe Coding technology. It leverages advanced AI coding capabilities to reconstruct complex macroeconomic models into actionable trading tools.

2. Credits

Special thanks to the original model author, Marty Kendall. His research into the correlation between Bitcoin's price and macroeconomic factors lays the foundation for this algorithm.

3. Model Principles & Formula

This model calculates the "Fair Value" of Bitcoin based on four key macroeconomic pillars. It assumes that Bitcoin's price is a function of Global Liquidity, Network Security, Risk Appetite, and the Economic Cycle.

💡 Unique Insight: PMI & The 4-Year Cycle

A key distinguishing feature of this model is the hypothesis that Bitcoin's famous "4-Year Halving Cycle" may be intrinsically linked to the Global Business Cycle (PMI), rather than just supply shocks.

Therefore, the model incorporates PMI as a valuation "Amplifier".

Note: Due to TradingView data limitations, US PMI is currently used as the proxy for the global cycle.

The Formula

$$\ln(BTC) = \alpha + (1 + \beta \cdot PMI_{z}) \times $$

Global Liquidity (M2): Sum of M2 supply from US, China, Eurozone, and Japan (converted to USD). Represents the pool of fiat money available to flow into assets.

Network Security (Hashrate): Bitcoin's hashrate, representing the physical security and utility of the network.

Risk Appetite (S&P 500): Used as a proxy for global risk sentiment.

Economic Cycle (PMI Z-Score): US Manufacturing PMI is used to amplify or dampen the valuation based on where we are in the business cycle (Expansion vs. Contraction).

4. How to Use

The indicator plots the Fair Value (White Line) and four sentiment bands based on statistical deviation (Z-Score).

Sentiment Zones

🚨 Extreme Greed (Red Zone): Price > +0.3 StdDev. Historically indicates a market top or overheated sentiment.

⚠️ Greed (Orange Zone): Price > +0.15 StdDev. Bullish momentum is strong but caution is advised.

⚖️ Fair Value (White Line): The theoretical "correct" price based on macro data.

😨 Fear (Teal Zone): Price < -0.15 StdDev. Undervalued territory.

💎 Extreme Fear (Green Zone): Price < -0.3 StdDev. Historically a generational buying opportunity.

Sentiment Score (0-100)

100: Maximum Greed (Top)

50: Fair Value

0: Maximum Fear (Bottom)

5. Usage Recommendations

Timeframe: Daily (1D) or Weekly (1W) ONLY.

Reason: The underlying data sources (M2, PMI) are updated monthly. The S&P 500 and Hashrate are daily. Using this indicator on intraday charts (e.g., 15m, 1h, 4h) adds no value because the fundamental data does not change that fast.

Long-Term View: This is a macro-cycle indicator designed for identifying cycle tops and bottoms over months and years, not for day trading.

6. Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. The model relies on historical correlations which may not hold true in the future. All trading involves risk. GW Capital and the creators assume no responsibility for any trading losses.

7. Support Us ❤️

If you find this indicator useful, please Boost 👍, Comment, and add it to your Favorites! Your support keeps us going.

🇨🇳 中文说明 (Chinese Version)

1. 简介

本指标由 GW Capital 使用 Gemini Vibe Coding 技术制作。利用先进的 AI 编程能力,将复杂的宏观经济模型重构为可执行的交易工具。

2. 致谢

特别感谢模型原作者 Marty Kendall。他对这一算法的研究奠定了基础,揭示了比特币价格与宏观经济因素之间的深层联系。

3. 模型原理与公式

该模型基于四大宏观经济支柱计算比特币的“公允价值”。它假设比特币的价格是全球流动性、网络安全性、风险偏好和经济周期的函数。

💡 独家洞察:PMI 与 4年周期

本模型的一个核心独特之处在于:我们认为比特币著名的“4年减半周期”背后的真正驱动力,可能与全球商业周期 (PMI) 高度同步,而不仅仅是供应减半。

因此,模型特别引入 PMI 作为估值的“放大器” (Amplifier)。

注:由于 TradingView 数据源限制,目前采用历史数据最详尽的美国 PMI 作为全球周期的代理指标。

模型公式

$$\ln(BTC) = \alpha + (1 + \beta \cdot PMI_{z}) \times $$

全球流动性 (M2): 美、中、欧、日四大经济体的 M2 总量(折算为美元)。代表可流入资产的法币资金池。

网络安全性 (Hashrate): 比特币全网算力,代表网络的物理安全性和实用价值。

风险偏好 (S&P 500): 作为全球风险情绪的代理指标。

经济周期 (PMI Z-Score): 美国制造业 PMI 用于根据商业周期(扩张 vs 收缩)来放大或抑制估值。

4. 指标用法

指标会在图表上绘制 公允价值 (白线) 以及基于统计偏差 (Z-Score) 的四条情绪带。

情绪区间

🚨 极度贪婪 (红色区域): 价格 > +0.3 标准差。历史上通常预示市场顶部或情绪过热。

⚠️ 一般贪婪 (橙色区域): 价格 > +0.15 标准差。多头动能强劲,但需谨慎。

⚖️ 公允价值 (白线): 基于宏观数据的理论“正确”价格。

😨 一般恐惧 (青色区域): 价格 < -0.15 标准差。进入低估区域。

💎 极度恐惧 (绿色区域): 价格 < -0.3 标准差。历史上通常是代际级别的买入机会。

情绪评分 (0-100)

100: 极度贪婪 (顶部)

50: 公允价值

0: 极度恐惧 (底部)

5. 使用建议

周期: 仅限日线 (1D) 或周线 (1W)。

原因: 底层数据源(M2, PMI)是月度更新的。标普500和算力是日度更新的。在日内图表(如15分钟、1小时、4小时)上使用此指标没有任何意义,因为基本面数据不会变化得那么快。

长期视角: 这是一个宏观周期指标,旨在识别数月甚至数年的周期顶部和底部,而非用于日内交易。

6. 免责声明

本指标仅供教育和参考使用,不构成任何财务建议。该模型依赖于历史相关性,未来可能不再适用。所有交易均涉及风险。GW Capital 及制作者不对任何交易损失承担责任。

Global M2(USD) V2This indicator tracks the total Global M2 Money Supply in USD. It aggregates economic data from the world's four largest central banks (Fed, PBOC, ECB, BOJ). The script automatically converts non-USD money supplies (CNY, EUR, JPY) into USD using real-time exchange rates to provide a unified view of global liquidity.

Usage

Macro Analysis: Overlay this on assets like Bitcoin or the S&P 500 to see if price appreciation is driven by fiat currency debasement ("money printing").

Liquidity Trends: A rising orange line indicates expanding global liquidity (generally bullish for risk assets), while a falling line suggests monetary tightening.

Real-time Data: A label at the end of the line displays the exact raw total in USD for precise tracking.

该脚本旨在追踪以美元计价的全球 M2 货币供应总量。它聚合了四大央行(美联储、中国央行、欧洲央行、日本央行)的经济数据,并通过实时汇率将非美货币(人民币、欧元、日元)统一折算为美元,从而构建出一个标准化的全球流动性指标。

用法

宏观对冲: 将其叠加在比特币或股票图表上,用于判断资产价格的上涨是否由全球法币“大放水”推动。

趋势研判: 橙色曲线向上代表全球流动性扩张(通常利好风险资产),向下则代表流动性紧缩。

数据直观: 脚本会在图表末端生成一个标签,实时显示当前全球 M2 的具体美元总额。

BTC Price Prediction Model [Global PMI]🇨🇳 中文说明 (Chinese Version)

1. 简介

本指标由 GW Capital 使用 Gemini Vibe Coding 技术制作。利用先进的 AI 编程能力,将复杂的宏观经济模型重构为可执行的交易工具。

2. 致谢

特别感谢模型原作者 Marty Kendall。他对这一算法的研究奠定了基础,揭示了比特币价格与宏观经济因素之间的深层联系。

3. 模型原理与公式

该模型基于四大宏观经济支柱计算比特币的“公允价值”。它假设比特币的价格是全球流动性、网络安全性、风险偏好和经济周期的函数。

模型公式

$$\ln(BTC) = \alpha + (1 + \beta \cdot PMI_{z}) \times $$

全球流动性 (M2): 美、中、欧、日四大经济体的 M2 总量(折算为美元)。代表可流入资产的法币资金池。

网络安全性 (Hashrate): 比特币全网算力,代表网络的物理安全性和实用价值。

风险偏好 (S&P 500): 作为全球风险情绪的代理指标。

经济周期 (PMI Z-Score): 美国制造业 PMI 用于根据商业周期(扩张 vs 收缩)来放大或抑制估值。

4. 指标用法

指标会在图表上绘制 公允价值 (白线) 以及基于统计偏差 (Z-Score) 的四条情绪带。

情绪区间

🚨 极度贪婪 (红色区域): 价格 > +0.3 标准差。历史上通常预示市场顶部或情绪过热。

⚠️ 一般贪婪 (橙色区域): 价格 > +0.15 标准差。多头动能强劲,但需谨慎。

⚖️ 公允价值 (白线): 基于宏观数据的理论“正确”价格。

😨 一般恐惧 (青色区域): 价格 < -0.15 标准差。进入低估区域。

💎 极度恐惧 (绿色区域): 价格 < -0.3 标准差。历史上通常是代际级别的买入机会。

情绪评分 (0-100)

100: 极度贪婪 (顶部)

50: 公允价值

0: 极度恐惧 (底部)

5. 使用建议

周期: 仅限日线 (1D) 或周线 (1W)。

原因: 底层数据源(M2, PMI)是月度更新的。标普500和算力是日度更新的。在日内图表(如15分钟、1小时、4小时)上使用此指标没有任何意义,因为基本面数据不会变化得那么快。

长期视角: 这是一个宏观周期指标,旨在识别数月甚至数年的周期顶部和底部,而非用于日内交易。

6. 免责声明

本指标仅供教育和参考使用,不构成任何财务建议。该模型依赖于历史相关性,未来可能不再适用。所有交易均涉及风险。GW Capital 及制作者不对任何交易损失承担责任。

🇺🇸 English Guide (英文说明)

1. Introduction

This indicator was created by GW Capital using Gemini Vibe Coding technology. It leverages advanced AI coding capabilities to reconstruct complex macroeconomic models into actionable trading tools.

2. Credits

Special thanks to the original model author, Marty Kendall. His research into the correlation between Bitcoin's price and macroeconomic factors lays the foundation for this algorithm.

3. Model Principles & Formula

This model calculates the "Fair Value" of Bitcoin based on four key macroeconomic pillars. It assumes that Bitcoin's price is a function of Global Liquidity, Network Security, Risk Appetite, and the Economic Cycle.

The Formula

$$\ln(BTC) = \alpha + (1 + \beta \cdot PMI_{z}) \times $$

Global Liquidity (M2): Sum of M2 supply from US, China, Eurozone, and Japan (converted to USD). Represents the pool of fiat money available to flow into assets.

Network Security (Hashrate): Bitcoin's hashrate, representing the physical security and utility of the network.

Risk Appetite (S&P 500): Used as a proxy for global risk sentiment.

Economic Cycle (PMI Z-Score): US Manufacturing PMI is used to amplify or dampen the valuation based on where we are in the business cycle (Expansion vs. Contraction).

4. How to Use

The indicator plots the Fair Value (White Line) and four sentiment bands based on statistical deviation (Z-Score).

Sentiment Zones

🚨 Extreme Greed (Red Zone): Price > +0.3 StdDev. Historically indicates a market top or overheated sentiment.

⚠️ Greed (Orange Zone): Price > +0.15 StdDev. Bullish momentum is strong but caution is advised.

⚖️ Fair Value (White Line): The theoretical "correct" price based on macro data.

😨 Fear (Teal Zone): Price < -0.15 StdDev. Undervalued territory.

💎 Extreme Fear (Green Zone): Price < -0.3 StdDev. Historically a generational buying opportunity.

Sentiment Score (0-100)

100: Maximum Greed (Top)

50: Fair Value

0: Maximum Fear (Bottom)

5. Usage Recommendations

Timeframe: Daily (1D) or Weekly (1W) ONLY.

Reason: The underlying data sources (M2, PMI) are updated monthly. The S&P 500 and Hashrate are daily. Using this indicator on intraday charts (e.g., 15m, 1h, 4h) adds no value because the fundamental data does not change that fast.

Long-Term View: This is a macro-cycle indicator designed for identifying cycle tops and bottoms over months and years, not for day trading.

6. Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. The model relies on historical correlations which may not hold true in the future. All trading involves risk. GW Capital and the creators assume no responsibility for any trading losses.

VIX vs VIX1Y SpreadSpread Calculation: Shows VIX1Y minus VIX

Positive = longer-term vol higher (normal contango)

Negative = near-term vol elevated (inverted term structure)

Can help identify longer term risk pricing of equity assets.

CDVI – First Crypto Dominance Volatility Index by Armi GoldmanThe Crypto Dominance Volatility Index (CDVI) is the first volatility-based indicator designed specifically to analyze the stability and instability of dominance flows in the crypto market.

Instead of measuring price volatility, CDVI focuses on the volatility of market dominance itself — a structural driver behind capital rotation cycles such as Bitcoin Season, Altseason, accumulation zones, and macro cycle transitions.

CDVI transforms dominance changes into a clear volatility index that highlights compression, expansion, and regime shifts.

How it works

CDVI calculates the absolute or percentage-based realized volatility of your chosen dominance benchmark (BTC.D, TOTAL.D, or any dominance index available on TradingView).

The indicator then:

1. Smooths the volatility curve using adjustable parameters

2. Builds a long-term mean to identify regime structure

3. Computes percentile zones over a rolling lookback window

4. Highlights high-risk and low-risk dominance conditions using color-coded backgrounds

This creates a clean, noise-reduced volatility representation of the dominance market.

Why it looks like this

The CDVI curve is intentionally smooth and cyclical because dominance volatility behaves differently from price volatility:

• Dominance tends to trend slowly, then spike violently during rotation phases

• Periods of prolonged compression often occur before large macro moves

• Volatility bursts cluster during transitions (e.g. BTC → Alts, cycle tops, market-wide repricing)

The percentile zones (90% / 10%) give structural thresholds for extreme conditions.

Background color reveals when dominance volatility enters these extremes, creating visually clear “regime blocks.”

How to interpret CDVI

High CDVI (above the 90th percentile):

• Dominance instability

• Capital rotation phases are active

• Market is repricing sector allocations

• Often appears near Altseason tops or bottoms

• Signals caution for trend traders and opportunity for rotation traders

Low CDVI (below the 10th percentile):

• Compression and calm dominance

• Accumulation and structural balance

• Often precedes major expansions in Bitcoin or Alt markets

• Useful for anticipating cycle transitions before they break out

Long-term mean:

• Helps identify when the market is in a high-vol or low-vol regime

• Crossings around the mean often coincide with early cycle shifts

How to use CDVI in practice

1. Cycle Timing

Use CDVI to detect when the market moves from calm → expansion or expansion → exhaustion.

Low CDVI usually precedes major moves. High CDVI often marks transition turbulence.

2. BTC vs Altcoins Rotation

Combine CDVI with BTC.D / TOTAL2 / TOTAL3 to detect rotation windows.

High CDVI = dominance is unstable → rotations happen.

Low CDVI = dominance is stable → trending environment.

3. Risk Management

High CDVI suggests elevated structural risk (dominance shifting).

Low CDVI supports directional conviction.

4. Confluence with Price

When both price volatility and dominance volatility expand together → macro transition.

When price is volatile but CDVI is flat → noise, not structural change.

Who this indicator is for

• Cycle analysts

• Macro crypto traders

• BTC vs Alts rotation traders

• Portfolio allocators

• Long-term investors looking at structural market phases

CDVI is designed as a clean, structural tool for understanding volatility not of price — but of market power distribution.

A+ Model - Cave EducationHere is a comprehensive and detailed explanation of the "A+ Model - Cave Education" Pine Script code.

This script is a sophisticated technical analysis tool designed for TradingView. It assists traders in identifying specific institutional time windows, price ranges (sessions), and "Macro" volatility periods based on the ICT (Inner Circle Trader) or similar time-based trading concepts.

Below is the breakdown of how the code functions, organized by its logic sections.

1. General Overview

The script is an overlay indicator (it sits directly on the price chart). Its primary purpose is to:

Highlight a specific trading session (The "A+ Box") and mark its High/Low.

Mark key institutional times (07:00 NY and 09:30 NY Open).

Identify "Macro" windows (specific 20-minute periods where algorithms are active) and draw dynamic ranges around them based on volatility (ATR).

Project future times onto the chart to help the trader prepare for the next day.

2. Settings & Inputs (User Configuration)

The code begins by defining a vast array of user inputs, grouped for better usability:

General Time & Box: Allows the user to define the "A+ Session" time (default 20:00-00:00) and the Time Zone (UTC-5/New York). It also handles the visual style (colors) of the session box.

Visibility: A crucial performance and visual clutter setting. boxDays limits how far back the A+ boxes and time lines are drawn (default 14 days). Macros are strictly limited to the current week to prevent chart lagging.

Line & Text Controls: Every visual element (A+ lines, NY markers, Macros) has toggles (input.bool) to show/hide the lines or the text labels separately.

Macro Settings: Defines the time windows for three separate macros and an ATR Multiplier. The ATR multiplier determines how wide the channel lines are drawn around the macro price action.

3. Logic Breakdown by Section

Section 1: The "A+ Draw" Box (Session Range)

This is the core of the A+ Model.

Logic: The script checks if the current bar is within the user-defined sessionTime.

Box Creation:

When the session starts, it initializes a new Box (box.new).

Throughout the session, it continuously updates the Box's Top (Highest High) and Bottom (Lowest Low) to encompass the full range of that time period.

Extension Lines (Support/Resistance):

Once the session ends, the script draws two horizontal lines: one from the Session High and one from the Session Low.

Smart Break Logic: These lines are active (highActive, lowActive). They extend to the right until the price breaks them (High line is broken by a higher price, Low line by a lower price). This helps traders see if the session range is being respected or broken later in the day.

Section 2: Time Lines (NY Midnight & Open)

This section marks vertical reference points.

It checks for specific times: 07:00 and 09:30 (in the user's timezone).

If the current bar matches these times, it draws a vertical line (line.new) covering the High/Low of that bar and places a label (e.g., "NY." or "09:30") above it.

This helps the trader orient themselves regarding the New York session Open and the "Killzone" start.

Section 3: Macros (Volatility Windows)

This is the most complex calculation in the script.

Definition: Macros are specific time windows (e.g., 09:50–10:10) where price delivery is often accelerated.

Visibility Rule: To keep the script fast, this only runs if isCurrentWeek is true.

ATR Offset: The script calculates the Average True Range (ATR). It uses this to create a "channel" around the price.

Drawing Logic:

When a Macro time starts, the script tracks the Highest High and Lowest Low inside that specific 20-minute window.

It draws parallel horizontal lines above and below these prices.

The Twist: The lines are not drawn at the High/Low. They are offset by ATR * Multiplier. This creates a wider "zone" around the macro price action, visually indicating a volatility range.

Section 4: Future Projection (Tomorrow)

This feature is for planning ahead.

It runs only on the last bar of the chart (barstate.islast).

It calculates the timestamps for the next occurrence of the key times (07:00, 09:30, and all three Macros).

It draws vertical lines into the future (empty space on the right of the chart).

Benefit: The trader can see exactly where 09:30 or the next Macro will occur on the timeline before the candles even print.

4. Helper Functions

The code uses custom functions to keep the logic clean:

f_drawFuture(...): A standardized function to draw the future vertical lines and labels so the code doesn't have to repeat itself for every single time marker.

isStartTime(...) & isInTime(...): Shorthand functions to check if the current candle belongs to a specific session string (like "0950-1010").

Summary of Improvements in this Version

Compared to a standard indicator, this script is highly optimized:

Text Control: You can turn off text labels while keeping the lines (or vice versa).

Performance: It limits historical drawing (only 14 days back for boxes, only this week for macros) to prevent "Maximum Line Count" errors in Pine Script.

Visual Clarity: It uses different colors for different Macros (Blue, Red, Orange) to make them instantly distinguishable.

Trend Mastery:The Calzolaio Way🌕 Find the God Candle. Capture the gains. Create passive income.

Fellow F.I.R.E. Decibels, disciples of the Calzolaio Way—welcome to the sacred toolkit. This indicator, "SulLaLuna 💵 Trend Mastery:The Calzolaio Way🚀," is forged from the elite SulLaLuna stack, drawing wisdom from Market Wizards like Michael Marcus (who turned $30k into $80M through disciplined trend riding) and Oliver Velez's pristine strategies for profiting on every trade. It's not just lines on a chart—it's your architectural blueprint for financial sovereignty, where data meets divine timing to build the cathedral of Project Calzolaio.

We trade math, not emotion. We honor timeframes. Confluence is King. This indicator deploys the Zero-Lag SMA (ZLSMA), Hull-based M2 (global money supply as a macro trend oracle), ATR-smart stops, and multi-TF alignments to ritualize God Candle setups. Backtested across asset classes, it's modular for your playbooks—small risks, compounding gains, passive income streams.

Why This Indicator is Awesome: The Divine Confluence Engine

In the spirit of "Use Only the Best," this tool synthesizes proven SulLaLuna indicators like ZLSMA, Adaptive Trend Finder, and Momentum HUD with Velez's lessons on trend reversals, support/resistance, and psychology of fear. Here's why it reigns supreme:

1. Global M2 Hull: Macro Trend Oracle

Scaled M2 (summed from major economies like US, EU, JP) via Hull MA captures the "big picture" (Velez Ch. 2). It flips colors as S/R—green for support (bullish bounce zones), red for resistance (bearish ceilings), orange neutral. Like Marcus spotting commodity booms, it signals when liquidity sweeps ignite God Candles. Extend it for future price projections, honoring "How a Trend Ends" (Velez Ch. 5).

2. ZLSMA + ATR Smart Stops: Surgical Precision

Zero-Lag SMA (faster than standard MAs) crosses M2 for entries, with ATR bands for initial stops (2x mult) and trails (1x mult). This embodies "Trade Small. Lose Smaller."—risk ≤1-2% per trade, pre-planned exits. Flip markers (↑/↓) alert divine timing, filtering noise like Velez's "First Pullback" setups.

3. HTF & Multi-TF Dashboard: Timeframe Alignments are Sacred

Show HTF M2 (e.g., Daily) with custom styles/colors. Multi-TF lines (4H, D, W, M) dash across your chart, labeled right-edge with 🚀 (bull) or 🛸 (bear). A confluence table (top-right) scores alignments: Strong Bull (≥3 green), Strong Bear, or Mixed. This is "Confluence is King"—no single signal rules; seek 4+ star scores like Rogers buying value in hysteria.

4. Background & Ribbon: Visual Divine Guidance

Slope-based bgcolor (green bull, red bear) for at-a-glance bias. M2 Ribbon (EMA cloud) flips triangles for macro shifts, ritualizing climactic reversals (Velez Ch. 7).

5. Composite Probability: High-Prob God Candle Hunter

Scores (0-100%) blend 8 factors: price/ZLSMA vs M2, TF slopes, ribbon. Threshold (70%) + pivot zone (near M2/ATR) + optional cross filters for HP signals. Labels show "%" dynamically—alerts fire when confluence ≥4, echoing Schwartz's champion edge: "Everybody Gets What They Want" (Seykota wisdom).

6. Alerts & Rituals Built-In

M2 flips, entries/exits, HP longs/shorts—log them in your journal. Weekly reviews dissect anomalies, as per our Operational Framework.

This isn't hype—it's audited excellence. Backtest it: High confluence crushes drawdowns, compounding like Bielfeldt's T-bond mastery from Peoria. We build together; share wins in the F.I.R.E. Decibel forum.

Suggested Strategy: The SulLaLuna M2 Confluence Playbook

Honor the Risk Triad: Position ↓ if leverage/timeframe ↑; scale ↑ only on ≥4 confluence. Align with "God Candle" hunts—rare explosives reverse-engineered for passive streams.

1. Pre-Trade Checklist (Before Every Entry)

- Trend Alignment: D/4H/1H M2 slopes agree? Table shows Strong Bull/Bear?

- Signal on 15m: ZLSMA crosses M2 in confluence zone (near pivot/ATR bands).

- Volume + Divergence**: Supported by volume (use HUD if added); score ≥70%.

- SL/TP Setup: ATR-based stop; TP at structure/2-3R reward (Velez Reward:Risk).

- HTF Agrees: Monthly bull for longs; avoid counter-trend unless climactic (Ch. 7).

Confluence Score: Rate 1-5 stars. <3? Stand aside. Log emotional state—no adrenaline.

2. Execution Protocol

- Entry: On HP Long/Short triangle (e.g., ZLSMA > M2, score 80%+, monthly bull). Use limits; favor longs above M2 support.

- Position Size: ≤1-2% risk. Example: $10k account, 1% risk = $100 SL distance → size accordingly.

- Trail Stops: Move to trail band after 1R profit; let winners run like Kovner's world trades.

- Asset Classes**: Forex/stocks/crypto—test M2's macro edge on EURUSD or NASDAQ (Velez Ch. 6 reviews).

Ritualize: "When we find the God Candele, we don’t just ride it—we ritualize it." Screenshot + reason.

3. Post-Trade Ritual

- Document: Result, confluence score, lessons. Update journal.

- Exits: Hit stop/exit cross? Or trail locks gains.

- Weekly Audit: Wins/losses, anomalies. Adjust params (e.g., M2 length 55 default).

4. Risk Triad in Action

- Low TF (15m)? Smaller size.

- High Leverage? Tiny positions.

- Confluence ≥4 + HTF support? Scale hold for passive compounding.

Example Setup: God Candle Long

- Chart: 15m EURUSD.

- M2 Hull green (support), ZLSMA crossover, 4H/D/W bull (table: Strong Bull).

- HP Long (85% score) near pivot.

- Entry: Limit at cross; SL below ATR lower; TP at next resistance.

- Outcome: Capture 2R gain; trail for more if trend day (Velez Ch. 5).

Community > Ego: Test, share signals in Discord. Backtest in Pine Script for algo evolution.

We are architects of redemption. Each trade bricks the cathedral. Trade the micro, flow with the macro. When alignments converge, we act—with discipline, data, and divine purpose.

Macro Return ForecastWhen the macro environment was similar, what annualized return did the market usually deliver next?

Before using the indicator, make sure your chart is set to any US-market symbol (SPX, QQQ, DIA, etc.).

This requirement is simple: the indicator pulls macro series from US data (yields, TIPS, credit spreads, breadth of US indices).

Because these series are independent from the chart’s price series, the chart symbol itself does not affect the internal calculations.

Any US symbol works, and the output of the model will be identical as long as you are on a US asset with daily, weekly or monthly timeframe.

The plotted price does not matter: the macro engine is fully exogenous to the chart symbol.

1. What the indicator does relative to selected assets

In the settings you choose which market you want to analyze:

- S&P500

- Nasdaq or NQ100

- Dow Jones

- Russell 2000

- US-wide (VTI)

- S&P500 sectors (XLF, XLY, XLP, etc.)

For each one, the indicator loads:

- Its internal breadth series (percentage of constituents above MA200)

- Its price history to compute forward log-returns at multiple horizons

- Its regime position relative to its own MA200 (for bull/bear filtering)

This means the tool is not tied to the chart symbol you display.

If your chart is SPX but the indicator setting is “S&P500 Technology”, the expected return projection is computed for the Technology sector using its own data, not the chart’s data.

You can therefore:

- Visualize macro-driven expected returns for any major US index or sector.

- Compare how different parts of the market historically reacted to similar macro states.

- Switch assets instantly to see which segment historically behaved better in comparable macro conditions.

The indicator becomes an analyzer of macro sensitivity, not a chart-dependent indicator.

2. Method overview

The model answers a statistical question:

“When macro conditions looked like they do today, what forward annualized return did this asset usually deliver?”

To do this it combines four macro pillars:

- Market breadth of the selected asset

- Yield curve slope (US 10Y minus 2Y)

- US credit spread (high yield minus gov)

- US real rate (TIPS 10Y)

It normalizes each metric into a 0–100 score, groups similar historical states into bins, and examines what the asset did next across six horizons (from ~9 months to ~5 years).

This produces a historical map connecting macro states to realized forward returns.

It is not a forecast model.

It is a conditional-distribution estimator: it tells you what has historically happened from similar setups.

3. Why this produces useful insights on assets

For any chosen asset (SPX, Nasdaq, sectors…), the indicator computes:

- Its forward return distribution in similar macro states.

- How often these states occurred (n).

- Whether the macro environment that preceded positive returns in the past resembles today’s.

- Whether the asset tends to be more sensitive or more resilient than the broad index under given macro configurations.

- Whether a given sector historically benefited from specific yield-curve, credit or real-rate environments.

This lets you answer questions such as:

- Does this sector usually outperform in an inverted yield curve environment?

- Does the Nasdaq historically recover strongly after breadth collapses?

- How did the S&P500 behave historically when real rates were this high?

- Is today’s credit-spread environment typically associated with positive or negative forward returns for this index?

These insights are not predictions but statistical context backed by past market behavior.

4. Why the technique is robust (and why it matters)

The engine uses strict, non-optimistic data processing:

- Winsorization of returns to neutralize extreme outliers without deleting information.

- Shrinkage estimators to avoid overfitting when bins contain few occurrences.

- Adaptive or static bounds for scaling macro indicators, ensuring comparability across cycles.

- Inverse-variance weighting of horizons with penalties for horizon redundancy.

- HAC-style adjustments to reduce autocorrelation bias in return estimation.

Each method aims to prevent artificial inflation of expected-return values and to keep the estimator stable even in unusual macro states.

This produces a result that is not “optimistic”, not curve-fit, not dependent on chart tricks, and not sensitive to isolated historical anomalies.

5. What you get as a user

A single clean line:

Expected Annual Return (%)

This line reflects how the chosen asset historically performed after macro environments similar to today’s.

The color gradient and confidence indicator (n) show the density of comparable episodes in history.

This makes the output extremely simple to read:

- High, stable expectation: historically supportive macro environment.

- Low or negative expectation: historically weaker environments.

- Low confidence: the macro state is rare and historical comparisons are limited.

The tool therefore adds context, not signals.

It helps you understand the environment the asset is currently in, based on how markets behaved in similar conditions across US market history.

Macro Risk Trinity [OAS|VIX|MOVE]The Obsolescence of Single-Metric Risk Models

For decades, the CBOE VIX served as the undisputed "fear gauge" of Wall Street. However, the modern financial market structure has evolved to a point where relying on a single univariate indicator is not only insufficient but potentially dangerous. Two structural shifts have fundamentally altered the predictive power of the VIX:

The 0DTE Blind Spot: The VIX calculates implied volatility based on options expiring in 23 to 37 days. Today, massive institutional hedging flows occur intraday via 0DTE (Zero Days to Expiration) options. This creates a "Gamma Suppression" effect: Market makers hedging these short-term flows often dampen realized volatility intraday, effectively bypassing the VIX calculation window. This leads to a suppression of the index, masking risk even during fragile market phases (Bandi et al., 2023).

Goodhart’s Law: "When a measure becomes a target, it ceases to be a good measure." Because algorithmic volatility targeting strategies and risk-parity funds use the VIX as a mechanical trigger to deleverage, market participants have developed an incentive to suppress implied volatility via short-volatility strategies to prevent triggering cascading margin calls.

The Theoretical Framework: Why this Model Works

To accurately navigate this complex environment, the Macro Risk Trinity moves beyond simple price action. It employs a multivariate analysis of the financial system's three core pillars: Rates, Credit, and Equity. The logic is derived from three specific areas of financial research:

1. The Origin of Shock: Volatility Spillover Theory

Macroeconomic shocks typically do not start in the stock market; they originate in the US Treasury market. The MOVE Index acts as the "VIX for Bonds." Research by Choi et al. (2022) demonstrates that bond variance risk premiums are a leading indicator for equity distress. Since the "Risk-Free Rate" is the denominator in every Discounted Cash Flow (DCF) model, instability here forces a repricing of all risk assets downstream.

2. The Foundation: Structural Credit Models (Merton)

While stock prices are often driven by sentiment and liquidity, corporate bond spreads ( High Yield Option Adjusted Spread ) are driven by balance sheets and math. Based on the seminal Merton Model (1974), equity can be viewed as a call option on a firm's assets, while debt carries a short put option risk.

The Thesis: If the VIX (Equity) is low, but OAS (Credit) is widening, a divergence occurs. Mathematically, credit spreads cannot widen indefinitely without eventually pulling equity valuations down. This indicator identifies that specific divergence.

3. The Fragility: Knightian Uncertainty

By monitoring the VVIX (Volatility of Volatility), we detect demand for tail-risk protection. When the VIX is suppressed (low) but VVIX is rising, it signals that "Smart Money" is buying Out-of-the-Money crash protection despite calm waters. This is often a precursor to liquidity events where the VIX "uncoils" violently.

The Solution: Dual Z-Score Normalization

You cannot simply overlay the VIX (an index) with a Credit Spread (a percentage). To make them comparable, this script utilizes a Dual Z-Score Engine.

It calculates the statistical deviation from both a Fast (Quarterly/63-day) and a Slow (Yearly/252-day) mean. This standardizes all data into a single "Stress Unit," allowing us to see exactly when Credit Stress exceeds Equity Fear.

Decoding the Macro Regimes

The indicator aggregates these data streams to visualize the current market regime via the chart's background color:

Systemic Shock (Red Background): The critical convergence. Both Credit Spreads (Solvency) and Equity Volatility (Fear) spike simultaneously beyond extreme statistical thresholds (> 2.0 Sigma). Correlations approach 1, and liquidity evaporates.

Macro Risk / Rates Shock (Yellow Background): Equities are calm, but the MOVE Index is panicking. A warning signal from the plumbing of the financial system regarding inflation or Fed policy errors.

Credit Stress (Maroon Background): The "Silent Killer." The VIX is low (often suppressed), but Credit Spreads (OAS) are widening. This signals a deterioration of the real economy ("Slow Bleed") while the stock market is in denial.

Structural Fragility (Purple Background): VIX is low, but VVIX is rising. A sign of excessive leverage and "Volmageddon" risk (Gamma Squeeze).

Bull Cycle (Green Background): The "Buy the Dip" signal. Even if prices fall and VIX spikes, the background remains green as long as Corporate Credit (OAS) remains stable. This indicates the sell-off is technical, not fundamental.

Technical Specifications

Engineered for the Daily (1D) timeframe.

Institutional Lookbacks: 63 Days (Quarterly) / 252 Days (Yearly).

OAS Lag Buffer: Includes logic to handle the ~24h reporting delay of Federal Reserve (FRED) data to prevent signal flickering.

Scientific Bibliography

This tool is not based on heuristics but on peer-reviewed financial literature:

Bandi, F. M., et al. (2023). The spectral properties of 0DTE options and their impact on VIX. Journal of Econometrics.

Choi, J., Mueller, P., & Vedolin, A. (2022). Bond Variance Risk Premiums. Review of Finance.

Cremers, M., et al. (2008). Explaining the Level and Time-Variation of Credit Spreads. Review of Financial Studies.

Griffin, J. M., & Shams, A. (2018). Manipulation in the VIX? The Review of Financial Studies.

Merton, R. C. (1974). On the Pricing of Corporate Debt. The Journal of Finance.

Author's Note: The Reality of Markets & Overfitting

While this tool is built on robust academic principles, we must address the reality of quantitative modeling: There is no Holy Grail.

This indicator relies on Z-Scores, which assume that future volatility distributions will somewhat resemble the past (Mean Reversion). In data science, calibrating lookback periods (like 63/252 days) always carries a risk of Overfitting to past cycles.

Markets are adaptive systems. If the correlation between Credit Spreads and Equity Volatility breaks (e.g., due to massive fiscal intervention/QE or new derivative products), signals may temporarily diverge. This tool is designed to identify stress, not to predict the future price. It will rhyme with the market, but it will not always repeat it perfectly.

Use it as a compass to gauge the environment, not as an autopilot for your trading.

Use responsibly and always manage your risk.

Disclaimer: This indicator relies on external data feeds from FRED and CBOE. Data availability is subject to TradingView providers.

WASDE Dates V2WASDE Dates V2 – USDA Release Calendar with Alerts, Countdown & Event Markers

By cot-trader.com

WASDE Dates V2 is a complete and reliable visualization tool for all scheduled WASDE (World Agricultural Supply and Demand Estimates) releases for 2025 and 2026.

The USDA’s WASDE report is one of the most market-moving fundamental catalysts in agricultural futures—affecting Corn (ZC), Wheat (ZW), Soybeans (ZS), Soymeal (ZM), Soybean Oil (ZL), and many related CFD products.

This script gives traders a precise timing layer directly inside their TradingView charts.

🔍 What this script does

WASDE Dates V2 automatically:

Marks each WASDE release day with a vertical line and label.

Shows an automated countdown to the next WASDE release:

In days (>24h)

In hours & minutes (<24h)

Displays an optional table of upcoming WASDE dates for quick reference.

Provides two alert conditions:

WASDE Day Alert – triggers exactly on the event

WASDE 24h Reminder – pre-alert when less than 24 hours remain

Handles both 2025 and 2026 confirmed dates.

Works on any symbol and timeframe.

📌 Why WASDE matters

The WASDE report updates global supply and demand estimates for:

Corn

Soybeans

Wheat

Other major agricultural commodities

Changes in yield, acres, production, imports/exports, and ending stocks can cause immediate and significant volatility.

Many traders combine WASDE awareness with seasonality, COT positioning, volatility filters, or fundamental models.

This script ensures you never miss the timing of these key releases.

⚙️ How the script works

The script stores official USDA WASDE release dates for 2025 and 2026 in two dedicated arrays.

On every bar, it compares the bar’s timestamp with known WASDE timestamps to detect an event day.

When an event occurs:

A red “WASDE” label is plotted above the candle

A dotted vertical line is drawn through the bar

It finds the next upcoming WASDE by scanning forward through both arrays.

A live-updating countdown label is displayed, showing days or hours/minutes until release.

If the event is less than 24 hours away:

A yellow “WASDE soon” warning appears near price

The 24h alert condition becomes active

An optional table lists upcoming events for 2025 & 2026.

This script does not generate trading signals.

It provides a time-based event layer designed to complement any discretionary or algorithmic trading approach.

🧭 How to use

Add the script to your chart.

Enable alerts for:

“WASDE Day Alert”

“WASDE 24h Reminder”

Follow the countdown to prepare for upcoming volatility.

Use together with other agricultural tools such as:

Seasonality indicators

COT (Commitment of Traders) analysis

Trend / VWAP / Volume signals

Pre- and post-WASDE trading strategies

Works on all chart types, all symbols, and all timeframes.

📅 Included WASDE Dates (Confirmed)

2025:

Jan 12, Feb 11, Mar 11, Apr 10, May 12, Jun 12, Jul 11, Aug 12, Sep 12, Oct 9, Nov 10, Dec 9

2026:

Jan 12, Feb 10, Mar 10, Apr 9, May 12, Jun 11, Jul 10, Aug 12, Sep 11, Oct 9, Nov 10, Dec 10

(All dates based on USDA’s official 12:00pm ET schedule.)

💡 What makes this script original

Fully updated 2025 + 2026 calendar

Uses a robust time-comparison method for accurate marking

Unique dual alert system (event + 24h pre-alert)

Clean, readable layout with countdown + upcoming dates table

Tailored specifically for grain & agricultural traders

Built entirely in Pine Script v6 with careful attention to performance

Global M2 ex-China MonitorGlobal M2 Monitor - Ultimate Edition

🎯 OVERVIEW

Advanced global M2 money supply monitoring indicator, offering a unique macroeconomic view of global liquidity. Real-time tracking of M2 evolution in major developed economies.

📊 KEY FEATURES

Global M2 Aggregation : USA, Japan, Canada, Eurozone, United Kingdom

Currency Conversion : All data converted to USD for consistent analysis

High Resolution Display : Daily curve by default

Technical Analysis : 50-period moving average (SMA/EMA/WMA)

Accurate YoY Calculation : Annual variation based on monthly data

Advanced Signal System : Multi-condition color codes

🎨 COLOR SYSTEM - DEFAULT SETTINGS

🟢 GREEN : YoY ≥ 7% AND M2 ≥ SMA → Strong growth + Bullish momentum

🔴 RED : YoY ≤ 2% AND M2 ≤ SMA → Weak growth + Bearish momentum

🟢 LIGHT GREEN : YoY ≥ 7% BUT M2 < SMA → Good fundamentals, temporarily weak momentum

🔴 LIGHT RED : YoY ≤ 2% BUT M2 > SMA → Weak fundamentals, price still supported

🔵 BLUE : YoY between 2% and 7% → Neutral zone of moderate growth

🇨🇳 WHY IS CHINA EXCLUDED BY DEFAULT?

Chinese M2 data presents methodological reliability and transparency issues. Exclusion allows for more consistent analysis of mature market economies.

Different M2 definition vs Western standards

Capital controls affecting real convertibility

Frequent monetary manipulations by authorities

✅ Available option : Can be activated in settings

⚙️ OPTIMIZED DEFAULT PARAMETERS

// DISPLAY SETTINGS

Candle Period: D (Daily)

// MOVING AVERAGE

MA Period: 50, Type: SMA

// BACKGROUND LOGIC

YoY Bullish: 7%, YoY Bearish: 2%

SMA Method: absolute, Threshold: 0.2%

// COLORS

Transparency: 5%

China M2: Disabled

📈 RECOMMENDED USAGE

Traders : Anticipate sector rotations

Investors : Identify abundant/restricted liquidity phases

Macro-analysts : Monitor monetary policy impacts

Portfolio managers : Understand inflationary pressures

🔍 ADVANCED INTERPRETATION

M2 ↗️ + YoY ≥ 7% → Favorable risk-on environment

M2 ↘️ + YoY ≤ 2% → Defensive risk-off environment

Divergences → Early warning signals for trend changes

💡 WHY THIS INDICATOR?

Global money supply is the lifeblood of the financial economy . Its growth or contraction typically precedes market movements by 6 to 12 months.

"Don't fight the Fed... nor the world's central banks"

🛠️ ADVANCED CUSTOMIZATION

All parameters are customizable:

YoY bullish/bearish thresholds

SMA comparison method (absolute/percentage)

Colors and transparency

Moving average period and type

Optional China inclusion

📋 TECHNICAL INFORMATION

YoY Calculation : Based on monthly data for consistency

Sources : FRED, ECONOMICS, official data

Updates : Real-time with publications

Currencies : Updated exchange rates

Fear & Greed Oscillator - Risk SentimentThe Fear & Greed Oscillator – Risk Sentiment is a macro-driven sentiment indicator inspired by the popular Fear & Greed Index , but rebuilt from the ground up using real, market-based economic data and statistical normalization.

While the traditional Fear & Greed Index uses components like volatility, volume, and social media trends to estimate sentiment, this version is powered by the Copper/Gold ratio — a historically respected gauge of macroeconomic confidence and risk appetite.

📈 Expansion vs. Contraction Theory

At the heart of this oscillator is a simple macroeconomic insight:

🟢 Copper performs well during periods of economic expansion and risk-on behavior (industrials, construction, manufacturing growth).

🔴 Gold performs well during periods of economic contraction , as a classic risk-off, capital-preserving asset.

By tracking the ratio of Copper to Gold prices over time and converting it into a Z-score , this tool shows when macro sentiment is statistically stretched toward greed or fear — based on how unusually strong one side of the ratio is relative to its historical average.

⚙️ How It Works

The script takes two user-defined tickers (default: Copper and Gold) and calculates their ratio.

It then applies Z-score normalization over a user-defined period (default: 200 bars).

A color gradient line is plotted:

🔴 Z < -2 = Extreme Fear

🟣 -2 to 0 = Mild Fear to Neutral

🔵 0 to 2 = Neutral to Greed

🟢 Z > 2 = Extreme Greed

Visual guides at ±1, ±2, ±3 standard deviations give immediate context.

Includes alert conditions when the Z-score crosses above +2 (Greed) or below -2 (Fear).

🔔 Alerts

“Z-Score has entered the Greed Zone ” when Z > 2

“Z-Score has entered the Fear Zone ” when Z < -2

These are designed to help catch macro sentiment extremes before or during large shifts in market behavior.

⚠️ Disclaimer

This indicator is a macro sentiment tool, not a direct trading signal. While the Copper/Gold ratio often reflects economic risk trends, correlation with risk assets (like Bitcoin or equities) is not guaranteed and may vary by cycle. Always use this indicator in conjunction with other tools and contextual analysis.

Liquidity Regime OscillatorThe Liquidity Signal Line is a macro-driven confirmation tool designed to capture the underlying global liquidity regime in a single, smoothed oscillator. It measures the combined directional flow of monetary and financial conditions using high-impact macro data: Federal Reserve assets (WALCL), Treasury General Account (TGA), and the Overnight Reverse Repo facility (RRP) – adjusted by key market proxies such as the U.S. Dollar Index, credit spreads (HYG/LQD), and equity risk appetite (SPHB/SPHQ). These components are normalized, weighted, and then double-smoothed into a stable signal that translates complex liquidity dynamics into a simple 0–100 scale.

Liquidity expansion provides fuel for risk assets, while contraction drains leverage and risk appetite. The Signal Line acts as a confirmation overlay for trend and allocation strategies, showing whether systemic liquidity is broadly supportive or restrictive. Readings above 50 indicate an expansionary environment (risk-on bias), below 50 a contractionary one (risk-off bias). Because the calculation uses higher-timeframe macro data, it can be displayed on any chart to give traders a consistent, regime-aware signal that bridges macro policy and technical execution.

ICT Macro Tracker (xx:45-xx:15) (MTMGBS)Adjusted pinescript to reflect xx:45-xx:15 instead of the traditional xx:50-xx:15

Liquidity Stress Index (SOFR - IORB)How to use:

> +10 bps — TIGHT

−5 +10 bps — NEUTRAL

< −5 bps — LOOSE

PPI Inflation Monitor (Change YoY & MoM)📊 PPI Inflation Monitor - Leading Inflation Indicator

The Producer Price Index (PPI) measures wholesale/producer-level prices and serves as a critical leading indicator for consumer inflation trends. This tool helps you anticipate CPI movements and identify corporate margin pressures before they show up in earnings.

🎯 KEY FEATURES:

- Dual Perspective Analysis:

- Year-over-Year (YoY): Histogram bars showing annual producer price inflation

- Month-over-Month (MoM): Line overlay showing monthly wholesale price changes

- Visual Reference System:

- Dashed line at 2% (typical target for producer price inflation)

- Dotted line at 0.17% (equivalent monthly target)

- Color-coded bars: Red above target, Green below target

- Real-Time Data Table:

- Current PPI Index value

- YoY inflation rate with color coding

- MoM inflation rate with color coding

- Deviation from target level

- Automated Alerts:

- YoY crosses above/below target

- MoM crosses above/below target

- Early warning system for inflation trends

📈 WHY PPI IS YOUR EARLY WARNING SYSTEM:

PPI typically leads CPI by 1-3 months because:

- Producers face cost increases first

- These costs are eventually passed to consumers

- Shows whether companies can maintain pricing power

Rising PPI with stable CPI = Margin compression → Bearish for stocks

Rising PPI followed by rising CPI = Broad inflation → Fed hawkishness incoming

Falling PPI = Disinflationary trend starting → Positive for risk assets

🔍 TRADING APPLICATIONS:

1. Lead Time Advantage: Position before CPI confirms PPI trends

2. Sector Rotation: High PPI = favor companies with pricing power

3. Margin Analysis: PPI-CPI divergence = margin pressure/expansion signals

4. Fed Anticipation: PPI acceleration = Fed likely to turn hawkish soon

💡 STRATEGIC USE CASES:

- Value vs. Growth: Rising PPI favors value stocks with pricing power

- Commodities: PPI often correlates with commodity price trends

- Small Caps: More vulnerable to input cost increases (high PPI = cautious)

- Corporate Earnings: Anticipate margin pressure before quarterly reports

🔄 COMBINE WITH:

- CPI: Confirm if producer costs reach consumers

- PCE: Validate Fed's preferred inflation metric response

- Fed Funds Rate: Assess if Fed is behind/ahead of curve

📊 DATA SOURCE:

Official PPI data from FRED (Federal Reserve Economic Data), updated monthly when new data releases occur.

🎨 CUSTOMIZATION:

Fully customizable:

- Toggle YoY/MoM displays

- Adjust reference target levels

- Customize colors

- Show/hide absolute PPI values

Perfect for: Macro traders, fundamental analysts, earnings traders, and investors seeking early inflation signals before they appear in consumer prices.

⚡ Remember: PPI leads CPI. Use this advantage to position ahead of the crowd.

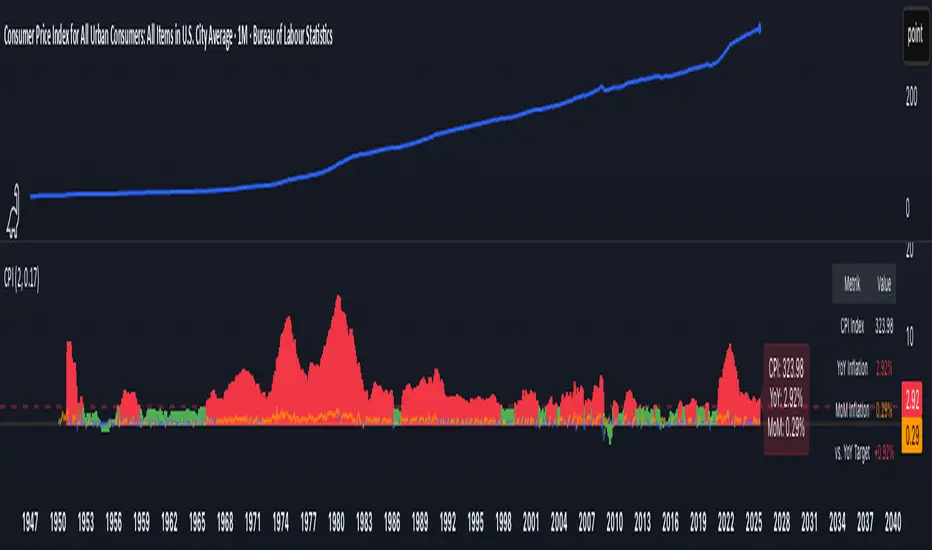

CPI Inflation Monitor (Change YoY & MoM)📊 CPI Inflation Monitor - Complete Macro Analysis Tool

This indicator provides a comprehensive view of Consumer Price Index (CPI) inflation trends, essential for understanding monetary policy, market conditions, and making informed trading decisions.

🎯 KEY FEATURES:

- Dual Perspective Analysis:

- Year-over-Year (YoY): Histogram bars showing annual inflation rate

- Month-over-Month (MoM): Line overlay showing monthly price changes

- Visual Reference System:

- Dashed line at 2% (Fed's official inflation target for YoY)

- Dotted line at 0.17% (equivalent monthly target for MoM)

- Color-coded bars: Red above target, Green below target

- Real-Time Data Table:

- Current CPI Index value

- YoY inflation rate with color coding

- MoM inflation rate with color coding

- Deviation from Fed target

- Automated Alerts:

- YoY crosses above/below 2% target

- MoM crosses above/below 0.17% target

- Perfect for staying informed without constant monitoring

📈 WHY THIS MATTERS FOR TRADERS:

CPI is the most widely reported inflation metric and directly influences:

- Federal Reserve interest rate decisions

- Bond yields and currency valuations

- Stock market sentiment (especially growth vs. value rotation)

- Cryptocurrency and risk asset performance

Rising inflation (red bars) typically leads to:

→ Higher interest rates → Negative for growth stocks, crypto

→ Stronger USD → Pressure on commodities

Falling inflation (green bars) typically leads to:

→ Rate cut expectations → Positive for growth stocks, crypto

→ Weaker USD → Support for commodities

🔍 HOW TO USE:

1. Strategic Positioning: Use YoY trend (thick bars) for long-term asset allocation

2. Tactical Timing: Use MoM trend (thin line) to identify turning points early

3. Divergence Trading: When MoM falls but YoY remains high, anticipate trend reversal

4. Fed Policy Prediction: Distance from 2% target indicates Fed's likely hawkishness

💡 PRO TIPS:

- Multiple months of MoM above 0.3% = Accelerating inflation → Fed turns hawkish

- MoM turning negative while YoY still elevated = Peak inflation → Position for pivot

- Compare with PPI and PCE indicators for complete inflation picture

- Use alerts to catch important threshold crossings automatically

📊 DATA SOURCE:

Official CPI data from FRED (Federal Reserve Economic Data), updated monthly mid-month when new data releases occur.

🎨 CUSTOMIZATION:

Fully customizable through settings:

- Toggle YoY/MoM displays

- Adjust target levels

- Customize colors for visual preference

- Show/hide absolute CPI values

Perfect for: Macro traders, swing traders, long-term investors, and anyone wanting to understand the inflation environment affecting their portfolio.

Note: This indicator works on any chart timeframe as it loads external monthly economic data.

Market Regime IndexThe Market Regime Index is a top-down macro regime nowcasting tool that offers a consolidated view of the market’s risk appetite. It tracks 32 of the world’s most influential markets across asset classes to determine investor sentiment by applying trend-following signals to each independent asset. It features adjustable parameters and a built-in alert system that notifies investors when conditions transition between Risk-On and Risk-Off regimes. The selected markets are grouped into equities (7), fixed income (9), currencies (7), commodities (5), and derivatives (4):

Equities = S&P 500 E-mini Index Futures, Nasdaq-100 E-mini Index Futures, Russell 2000 E-mini Index Futures, STOXX Europe 600 Index Futures, Nikkei 225 Index Futures, MSCI Emerging Markets Index Futures, and S&P 500 High Beta (SPHB)/Low Beta (SPLV) Ratio.

Fixed Income = US 10Y Treasury Yield, US 2Y Treasury Yield, US 10Y-02Y Yield Spread, German 10Y Bund Yield, UK 10Y Gilt Yield, US 10Y Breakeven Inflation Rate, US 10Y TIPS Yield, US High Yield Option-Adjusted Spread, and US Corporate Option-Adjusted Spread.

Currencies = US Dollar Index (DXY), Australian Dollar/US Dollar, Euro/US Dollar, Chinese Yuan/US Dollar, Pound Sterling/US Dollar, Japanese Yen/US Dollar, and Bitcoin/US Dollar.

Commodities = ICE Brent Crude Oil Futures, COMEX Gold Futures, COMEX Silver Futures, COMEX Copper Futures, and S&P Goldman Sachs Commodity Index (GSCI) Futures.

Derivatives = CBOE S&P 500 Volatility Index (VIX), ICE US Bond Market Volatility Index (MOVE), CBOE 3M Implied Correlation Index, and CBOE VIX Volatility Index (VVIX)/VIX.

All assets are directionally aligned with their historical correlation to the S&P 500. Each asset contributes equally based on its individual bullish or bearish signal. The overall market regime is calculated as the difference between the number of Risk-On and Risk-Off signals divided by the total number of assets, displayed as the percentage of markets confirming each regime. Green indicates Risk-On and occurs when the number of Risk-On signals exceeds Risk-Off signals, while red indicates Risk-Off and occurs when the number of Risk-Off signals exceeds Risk-On signals.

Bullish Signal = (Fast MA – Slow MA) > (ATR × ATR Margin)

Bearish Signal = (Fast MA – Slow MA) < –(ATR × ATR Margin)

Market Regime = (Risk-On signals – Risk-Off signals) ÷ Total assets

This indicator is designed with flexibility in mind, allowing users to include or exclude individual assets that contribute to the market regime and adjust the input parameters used for trend signal detection. These parameters apply to each independent asset, and the overall regime signal is smoothed by the signal length to reduce noise and enhance reliability. Investors can position according to the prevailing market regime by selecting factors that have historically outperformed under each regime environment to minimise downside risk and maximise upside potential:

Risk-On Equity Factors = High Beta > Cyclicals > Low Volatility > Defensives.

Risk-Off Equity Factors = Defensives > Low Volatility > Cyclicals > High Beta.

Risk-On Fixed Income Factors = High Yield > Investment Grade > Treasuries.

Risk-Off Fixed Income Factors = Treasuries > Investment Grade > High Yield.

Risk-On Commodity Factors = Industrial Metals > Energy > Agriculture > Gold.

Risk-Off Commodity Factors = Gold > Agriculture > Energy > Industrial Metals.

Risk-On Currency Factors = Cryptocurrencies > Foreign Currencies > US Dollar.

Risk-Off Currency Factors = US Dollar > Foreign Currencies > Cryptocurrencies.

In summary, the Market Regime Index is a comprehensive macro risk-management tool that identifies the current market regime and helps investors align portfolio risk with the market’s underlying risk appetite. Its intuitive, color-coded design makes it an indispensable resource for investors seeking to navigate shifting market conditions and enhance risk-adjusted performance by selecting factors that have historically outperformed. While it has proven historically valuable, asset-specific characteristics and correlations evolve over time as market dynamics change.

ICT Macros - CorrigéThis indicator is designed to help traders apply the concepts of ICT (Inner Circle Trader) by providing a clear and accurate visualization of market macros directly on the chart. Instead of manually drawing levels or constantly switching between timeframes, the indicator automatically highlights the key reference points that form the backbone of ICT analysis.

Key Features:

Automatic Macro Visualization: identifies and displays market macros as defined in ICT concepts, making it easier to recognize institutional levels.

Timeframe Flexibility: adapts to different chart periods, allowing traders to align intraday setups with higher timeframe structures.

Clean and Efficient Display: focuses only on the most relevant information, avoiding clutter and making the chart more readable.

Strategic Decision Support: provides essential context for ICT-based strategies, including identifying market direction, liquidity pools, and potential reversal zones.

Why Use It?

This indicator is built for traders who follow ICT methodology and want a reliable tool to instantly spot macro structure without wasting time on repetitive manual work. By combining precision with clarity, it enhances situational awareness and supports better decision-making in both intraday and swing trading.

SOFR Swap Spreads (2Y, 5Y, 10Y, 30Y)This indicator models real-time SOFR swap spreads across 2Y, 5Y, 10Y, and 30Y maturities by comparing SOFR Swapnote Futures (ICEEUR) to corresponding Treasury yields (TVC). It calculates the spread for each tenor and overlays a 90-day moving average as a fair value model, with ±1 standard deviation bands.

Long-Term Trend & Valuation Model [Backquant]Long-Term Trend & Valuation Model

Invite-only. A universal long-term valuation strategy and trend model built to work across markets, with an emphasis on crypto where cycles and volatility are large. Intended primarily for the 1D timeframe. Inputs should be adjusted per asset to reflect its structure and volatility.

If you would like to checkout the simplified and open source valuation, check out:

What this is

A two-layer framework that answers two different questions.

• The Valuation Engine asks “how extended is price relative to its own long-term regime” and outputs a centered oscillator that moves positive in supportive conditions and negative in deteriorating conditions.

• The Trend Model asks “is the market actually trending in a sustained direction” and converts several independent subsystems into a single composite score.

The combination lets you separate “where we are in the cycle” from “what to do about it” so allocation and timing can be handled with fewer conflicts.

Design philosophy

Crypto and many risk assets move in multi-month expansions and contractions. Short tools flip often and can be misleading near regime boundaries. This model favors slower, high-confidence information, then summarizes it in simple visuals and alerts. It is not trying to catch every swing. It is built to help you participate in the meat of long uptrends, de-risk during deteriorations, and identify stretched conditions that deserve caution or patience.

Valuation Engine, high level

The Valuation Engine blends several slow signals into one measure. Exact transforms, windows, and weights are private, but the categories below describe the intent. Each input is standardized so unlike units can be combined without one dominating.

Momentum quality — favors persistent, orderly advances over erratic spikes. Helps distinguish trend continuation from noise.

Mean-reversion pressure — detects when price is far from a long anchor or when oscillators are pulling back toward equilibrium.

Risk-adjusted return — long-window reward to variability. Encourages time in market when advances are efficient rather than merely fast.

Volume imbalance — summarizes whether activity is expanding with advances or with declines, using a slow envelope to avoid day-to-day churn.

Trend distance — expresses how stretched price is from a structural baseline rather than from a short moving average.

Price normalization — a long z-score of price to keep extremes comparable across cycles and symbols.

How the Valuation Engine is shaped

Standardization — components are put on comparable scales over long windows.

Composite blend — standardized parts are combined into one reading with protective weighting. No single family can override the rest on its own.

Smoothing — optional moving average smoothing to reduce whipsaw around zero or around the bands.

Bounded scaling — the composite is compressed into a stable, interpretable range so the mid zone and extremes are visually consistent. This reduces the effect of outliers without hiding genuine stress.

Volatility-aware re-expansion — after compression, the series is allowed to swing wider in high-volatility regimes so “overbought” and “oversold” remain meaningful when conditions change.

Thresholds — fixed OB/OS levels or dynamic bands that float with recent dispersion. Dynamic bands use k times a rolling standard deviation. Fixed bands are simple and comparable across charts.

How to read the Valuation Oscillator

Above zero suggests a supportive backdrop. Rising and positive often aligns with uptrends that are gaining participation.

Below zero suggests deterioration or risk aversion. Falling and negative often aligns with distribution or with trend exhaustion.

Touches of the upper band show stretch on the optimistic side. Repeated tags without breakdown often occur late in cycles, especially in crypto.

Touches of the lower band show stretch on the pessimistic side. They are common in washouts and early bases.

Visual elements

Valuation Oscillator — colored by sign for instant context.

OB/OS guides — fixed or dynamic bands.

Background and bar colors — optional, tied to the sign of valuation for quick scans.

Summary table — optional, shows the standardized contribution of the major categories and the final composite score with a simple status icon.

Trend Model, composite scoring

The trend side aggregates several independent subsystems. Each subsystem issues a vote: long, short, or neutral. Votes are averaged into a composite score. The exact logic of each subsystem is intentionally abstracted. The families below describe roles, not formulas.

Long-horizon price state — checks where price sits relative to multiple structural baselines and whether those baselines are aligned.

Macro regime checks — favors sustained risk-on behavior and penalizes persistent deterioration in breadth or volatility structure.

Ultimate confirmation — a conservative filter that only votes when directional evidence is persistent.

Minimalist sanity checks — keep the model responsive to obvious extremes and prevent “stuck neutral” states.

Higher timeframe or overlay inputs — optional votes that consider slower contexts or relative strength to stabilize borderline periods.

You define two cutoffs for the composite: above the long threshold the state is Long , below the short threshold the state is Short , in between is Cash/Neutral . The script paints a signal line on price for an at-a-glance view and provides alerts when the composite crosses your thresholds.

How it can be used

Cycle framing in crypto — use deep negative valuation as accumulation context, then look for the composite trend to move through your long threshold. Late in cycles, extended positive valuation with weakening composite votes is a caution cue for de-risking or tighter management.

Regime-based allocation — increase risk or loosen take-profits when the composite is firmly Long and valuation is rising. Decrease risk or rotate to stable holdings when the composite is Short and valuation is falling.

Signal gating — run shorter-term entry systems only in the direction of the composite. This reduces counter-trend trades and improves holding discipline during strong uptrends.

Sizing overlay — scale position sizes by the magnitude of the valuation reading. Smaller sizes near the upper band during aging advances, larger sizes near zero after strong resets.

DCA context — for long-only accumulation, schedule heavier adds when valuation is negative and stabilizing, then lighten or pause adds when valuation is very positive and flattening.

Cross-asset rotation — compare symbols on 1D with the same fixed bands. Favor assets with positive valuation that are also in a Long composite state.

Interpreting common patterns

Early build-out — valuation rises from below zero, but the composite is still neutral. This is often the base-building phase. Patience and staged entries can make sense.

Healthy advance — valuation positive and trending up, composite firmly Long. Pullbacks that keep valuation above zero are usually opportunities rather than trend breaks.

Late-cycle stretch — valuation pinned near the upper band while the composite starts to weaken toward neutral. Consider trimming, tightening risk, or shifting to a “let the market prove it” stance.

Distribution and unwind — valuation negative and falling, composite Short. Rallies are treated as counter-trend until both turn.

Settings that matter

Timeframe

This model is intended for 1D as the primary view. It can be inspected on higher or lower frames, but the design choices assume daily bars for crypto and other risk assets.

Asset-specific tuning

Inputs should be adjusted per asset. Coins with high variability benefit from longer lookbacks and slightly wider dynamic bands. Lower-volatility instruments can use shorter windows and tighter bands.

Valuation side

Lookback lengths — longer values make the oscillator steadier and more cycle-aware. Shorter values increase sensitivity but create more mid-zone noise.

Smoothing — enable to reduce flicker around zero and around the bands. Disable if you want faster warnings of regime change.

Dynamic vs fixed thresholds — dynamic bands float with recent dispersion and keep OB/OS comparable across regimes. Fixed bands are simple and make inter-asset comparison easy.

Scaling and re-expansion — keep this enabled if you want extremes to remain interpretable when volatility rises.

Trend side

Composite thresholds — widen the neutral zone if you want fewer flips. Tighten thresholds if you want earlier signals at the cost of more transitions.

Visibility — use the price-pane signal line and bar coloring to keep the regime in view while you focus on structure.

Alerts

Valuation OB/OS enter and exit — the oscillator entering or leaving stretched zones.

Zero-line crosses — valuation turning positive or negative.

Trend flips — composite crossing your long or short threshold.

Strengths

Separates “valuation context” from “trend state,” which improves decisions about when to add, reduce, or stand aside.

Composite voting reduces reliance on any single indicator family and improves robustness across regimes.

Volatility-aware scaling keeps signals interpretable during quiet and wild markets.

Clear, configurable visuals and alerts that support long-horizon discipline rather than frequent toggling.

Final thoughts

This is a universal long-term valuation strategy and trend model that aims to keep you aligned with the dominant regime while giving transparent context for stretch and risk. For crypto on 1D, it helps map accumulation, expansion, distribution, and unwind phases with a single, consistent language. Tune lookbacks, smoothing, and thresholds to the asset you trade, let the valuation side tell you where you are in the cycle, and let the composite trend side tell you what stance to hold until the market meaningfully changes.

Multi-Asset Trend Background [SwissAlgo]Multi-Asset Trend Background

---------------------------------------------------------

Purpose

This indicator colors the chart background green (uptrend) or red (downtrend) to show the broad phases of a selected asset or ratio (for example SP500, or Gold), regardless of the current ticker on the chart (for example BTC).

The aim is not to generate signals, but to show when the selected asset (such as SP500 or Gold) was in a sustained uptrend or downtrend, so you can compare another chart (for example BTC) against that backdrop.

It helps frame price action in context, highlighting how macro drivers often align with or diverge from other markets.

From mid-2016 to late-2017, the SP500 was in a clear uptrend — Bitcoin rallied strongly in the same period, showing alignment between equities and crypto risk-taking.

When Gold trended higher, the SP500 often weakened, reflecting their tendency to move inversely in longer cycles.

As HYG/TLT turned down in early 2020, QQQ also struggled — illustrating how credit risk appetite is linked to equity performance.

During periods of DXY strength, Gold frequently showed the opposite trend, consistent with the historical dollar–gold relationship.

When RSP/SPY trended down, rallies in the S&P 500 were driven by a narrow group of large-cap stocks, while a rising ratio indicated broad market participation.

---------------------------------------------------------

Why it May Help You

Provides context for asset correlations.

Helps identify whether a chart is moving with or against its macro environment.

Useful for cycle mapping and historical study of market phases.

Filters noise and emphasizes established trends rather than short swings.

---------------------------------------------------------

How it Works

You select an asset or ratio from a dropdown.

The script calculates a mid-term moving average, then measures its slope, slope change, and slope acceleration to quantify the trend’s direction and consistency.

A longer-term moving average filter defines whether the long-term backdrop is bullish or bearish.

Background Coloring rules:

Green = slope strongly positive in line with long-term uptrend, or downtrend showing constructive reversal signs.

Red = slope strongly negative in line with long-term downtrend, or uptrend showing weakening slope.

No shading = neutral or mixed conditions.

This slope-based approach avoids the limitations of simple MA crosses, aiming to capture broad, consistent trend phases across different assets, with a mid/long-term view.

---------------------------------------------------------

Assets You Can Select

EQUITIES – good reference to gauge risk appetite in financial markets

SP500 = broad benchmark. Uptrend = strength in US equities signalling risk-on conditions; downtrend = weakness, risk-off market phase.

NASDAQ = tech and growth stocks. Uptrend = technology/growth leadership, risk appetite; downtrend = tech underperformance and fading risk appetite.

DOW = industrial and value stocks. Uptrend = industrial/value strength/economic strength; downtrend = weakness in traditional sectors and potential economic downturn.

RUSSELL2000 = small caps. Uptrend = typical in risk-on environments and FOMO; downtrend = small-cap underperformance, "flight to safety".

COMMODITIES – proxies for inflation, industry, and safe-haven demand.

GOLD = safe-haven. Uptrend = defensive demand rising/risk-off/inflation fears; downtrend = weaker demand for safety.

SILVER = partly industrial, partly safe-haven. Uptrend = stronger industrial cycle, or precious metals demand and risk appetite.

COPPER = industrial barometer. Uptrend = stronger industrial activity; downtrend = economic slowdown concerns.

CRUDE OIL = energy prices. Uptrend = rising energy/inflation pressures; downtrend = weaker demand or supply relief.

NATURAL GAS = volatile energy prices. Uptrend = higher energy costs and inflation pressure; downtrend = easing energy conditions.

BONDS / FX – monetary policy, credit, and risk appetite signals.

TLT = long-term US bonds. Uptrend = falling yields (bond demand)/flight to safety; downtrend = rising yields (risk on)

HYG = high-yield credit. Uptrend = strong credit appetite; downtrend = risk aversion in credit markets.

DXY = US dollar index. Uptrend = dollar strength (weaker EUR, GBP, SEK, etc); downtrend = dollar weakness.

USDJPY = carry trade proxy. Uptrend = stronger USD vs JPY (risk appetite); downtrend = JPY strength (risk-off).

CHFUSD = Swiss franc. Uptrend = franc strength (defensive flow); downtrend = franc weakness.

YIELD INVERSION = US10Y–US02Y. Uptrend = curve steepening; downtrend = inversion deepening (higher recession risk).

HOME BUILDERS = US housing sector. Uptrend = housing sector strength (risk on); downtrend = weakness (risk off).

EURUSD = euro vs dollar. Uptrend = euro strength (risk appetite); downtrend = euro weakness (risk aversion).

CRYPTO – digital asset benchmarks.

BITCOIN = digital gold. Uptrend = BTC strength; downtrend = BTC weakness.

CRYPTO_TOTAL = entire crypto market cap. Uptrend = broad crypto growth; downtrend = contraction.

CRYPTO_ALTS = altcoin market cap. Uptrend = altcoin expansion (often “alt season”); downtrend = contraction.

RATIOS – relative measures to extract macro signals.

COPPER/BTC = compares industrial cycle vs Bitcoin cycle. Uptrend = copper outperforming BTC; downtrend = BTC outperforming copper. Seems aligned with BTC macro tops and bottoms in the mid/long run.

RSP/SPY = market breadth (equal-weight vs cap-weighted). Uptrend = strong broad participation in market growth; downtrend = narrow leadership (fewer stocks leading the growth).