Account GuardianAccount Guardian: Dynamic Risk/Reward Overlay

Introduction

Account Guardian is an open-source indicator for TradingView designed to help traders evaluate trade setups before entering positions. It automatically calculates Risk-to-Reward ratios based on market structure, displays visual Stop Loss and Take Profit zones, and provides real-time position sizing recommendations.

The indicator addresses a fundamental question every trader should ask before entering a trade: "Does this setup make mathematical sense?" Account Guardian answers this question visually and numerically, helping traders avoid impulsive entries with poor risk profiles.

Core Functionality

Account Guardian performs four primary functions:

Detects swing highs and swing lows to identify logical stop loss placement levels

Calculates Risk-to-Reward ratios for both long and short setups in real-time

Displays visual SL/TP zones on the chart for immediate trade planning

Computes position sizing based on your account size and risk tolerance

The goal is to provide traders with instant feedback on whether a potential trade meets their minimum risk/reward criteria before committing capital.

How It Works

Swing Detection

The indicator uses pivot point detection to identify recent swing highs and swing lows on the chart. These swing points serve as logical areas for stop loss placement:

For Long Trades: The most recent swing low becomes the stop loss level. Price breaking below this level would invalidate the bullish thesis.

For Short Trades: The most recent swing high becomes the stop loss level. Price breaking above this level would invalidate the bearish thesis.

The swing detection lookback period is configurable, allowing you to adjust sensitivity based on your trading timeframe and style.

It automatically adjusts the tp and sl when it is applied to your chart so it is always moving up and down!

Risk/Reward Calculation

Once swing levels are identified, the indicator calculates:

Entry Price: Current close price (where you would enter)

Stop Loss: Recent swing low (for longs) or swing high (for shorts)

Risk: Distance from entry to stop loss

Take Profit: Entry plus (Risk × Target Multiplier)

R:R Ratio: Reward divided by Risk

The R:R ratio is then evaluated against your configured thresholds to determine if the setup is valid, marginal, or poor.

Visual Elements

SL/TP Zones

When enabled, the indicator draws colored boxes on the chart showing:

Red Zone: Stop Loss area - the region between your entry and stop loss

Green/Gold/Red Zone: Take Profit area - colored based on R:R quality

The color coding provides instant visual feedback:

Green: R:R meets or exceeds your "Good R:R" threshold (default 3:1)

Gold: R:R meets minimum threshold but below "Good" (between 2:1 and 3:1)

Red: R:R below minimum threshold - setup should be avoided

Swing Point Markers

Small circles mark detected swing points on the chart:

Green circles: Swing lows (potential support / long SL levels)

Red circles: Swing highs (potential resistance / short SL levels)

Dashboard Panel

The dashboard in the top-right corner displays comprehensive trade planning information:

R:R Row: Current Risk-to-Reward ratio for long and short setups

Status Row: VALID, OK, BAD, or N/A based on R:R thresholds

Stop Loss Row: Exact price level for stop loss placement

Take Profit Row: Exact price level for take profit placement

Pos Size Row: Recommended position size based on your risk parameters

Risk $ Row: Dollar amount at risk per trade

Position Sizing Logic

The indicator calculates position size using the formula:

Position Size = Risk Amount / Risk per Unit

Where:

Risk Amount = Account Size × (Risk Percentage / 100)

Risk per Unit = Entry Price - Stop Loss Price

For example, with a $10,000 account risking 1% per trade ($100), if your entry is at 100 and stop loss at 98 (risk of 2 per unit), your position size would be 50 units.

Input Parameters

Swing Detection:

Swing Lookback: Number of bars to look back for pivot detection (default: 10). Higher values find more significant swing points but may be slower to update.

Target Multiplier: Multiplier applied to risk to calculate take profit distance (default: 2). A value of 2 means TP is 2× the distance of SL from entry.

Risk/Reward Thresholds:

Minimum R:R: Minimum acceptable Risk-to-Reward ratio (default: 2.0). Setups below this show as "BAD" in red.

Good R:R: Threshold for excellent setups (default: 3.0). Setups at or above this show as "VALID" in green.

Account Settings:

Account Size ($): Your trading account size in dollars (default: 10,000). Used for position sizing calculations.

Risk Per Trade (%): Percentage of account to risk per trade (default: 1.0%). Professional traders typically risk 0.5-2% per trade.

Display:

Show SL/TP Zones: Toggle visibility of the colored zone boxes on chart (default: enabled)

Show Dashboard: Toggle visibility of the information panel (default: enabled)

Analyze Direction: Choose to analyze Long only, Short only, or Both directions (default: Both)

How to Use This Indicator

Basic Workflow:

Add the indicator to your chart

Configure your account size and risk percentage in the settings

Set your minimum and good R:R thresholds based on your trading rules

Look at the dashboard to see current R:R for potential long and short entries

Only consider trades where the status shows "VALID" or at minimum "OK"

Use the displayed SL and TP levels for your order placement

Use the position size recommendation to determine lot/contract size

Interpreting the Dashboard:

VALID (Green): Excellent setup - R:R meets your "Good" threshold. This is the ideal scenario for taking a trade.

OK (Gold): Acceptable setup - R:R meets minimum but isn't optimal. Consider taking if other confluence factors align.

BAD (Red): Poor setup - R:R below minimum threshold. Avoid this trade or wait for better entry.

N/A (Gray): Cannot calculate - usually means no valid swing point detected yet.

Best Practices:

Use this indicator as a filter, not a signal generator. It tells you IF a trade makes sense, not WHEN to enter.

Combine with your existing entry strategy - use Account Guardian to validate setups from other analysis.

Adjust the swing lookback based on your timeframe. Lower timeframes may need smaller lookback values.

Be honest with your account size input - accurate position sizing requires accurate inputs.

Consider the target multiplier carefully. Higher multipliers mean larger potential reward but lower probability of hitting TP.

Alerts

The indicator includes four alert conditions:

Good Long Setup: Triggers when long R:R reaches or exceeds your "Good R:R" threshold

Good Short Setup: Triggers when short R:R reaches or exceeds your "Good R:R" threshold

Bad Long Setup: Triggers when long R:R falls below your minimum threshold

Bad Short Setup: Triggers when short R:R falls below your minimum threshold

These alerts can help you monitor multiple charts and get notified when favorable setups appear.

Technical Implementation

The indicator is built using Pine Script v6 and includes:

Pivot-based swing detection using ta.pivothigh() and ta.pivotlow()

Dynamic box drawing for visual SL/TP zones

Table-based dashboard for clean information display

Color-coded visual feedback system

Persistent variable tracking for swing levels

Code Structure:

// Swing Detection

float swingHi = ta.pivothigh(high, swingLen, swingLen)

float swingLo = ta.pivotlow(low, swingLen, swingLen)

// R:R Calculation for Long

float longSL = recentSwingLo

float longRisk = entry - longSL

float longTP = entry + (longRisk * targetMult)

float longRR = (longTP - entry) / longRisk

// Position Sizing

float riskAmount = accountSize * (riskPct / 100)

float posSize = riskAmount / longRisk

Limitations

The indicator uses historical swing points which may not always represent optimal SL placement for your specific strategy

Position sizing assumes you can trade fractional units - adjust accordingly for instruments with minimum lot sizes

R:R calculations assume linear price movement and don't account for gaps or slippage

The indicator doesn't predict price direction - it only evaluates the mathematical viability of a setup

Swing detection has inherent lag due to the lookback period required for pivot confirmation

Recommended Settings by Trading Style

Scalping (1-5 minute charts):

Swing Lookback: 5-8

Target Multiplier: 1-2

Minimum R:R: 1.5

Good R:R: 2.0

Day Trading (15-60 minute charts):

Swing Lookback: 8-12

Target Multiplier: 2

Minimum R:R: 2.0

Good R:R: 3.0

Swing Trading (4H-Daily charts):

Swing Lookback: 10-20

Target Multiplier: 2-3

Minimum R:R: 2.5

Good R:R: 4.0

Why Risk/Reward Matters

Many traders focus solely on win rate, but profitability depends on the combination of win rate AND risk/reward ratio. Consider these scenarios:

50% win rate with 1:1 R:R = Breakeven (before costs)

50% win rate with 2:1 R:R = Profitable

40% win rate with 3:1 R:R = Profitable

60% win rate with 1:2 R:R = Losing money

Account Guardian helps ensure you only take trades where the math works in your favor, even if you're wrong more often than you're right.

Disclaimer

This indicator is provided for educational and informational purposes only. It is not intended as financial, investment, trading, or any other type of advice or recommendation.

Trading involves substantial risk of loss and is not suitable for all investors. The calculations provided by this indicator are based on historical price data and mathematical formulas that may not accurately predict future price movements.

Position sizing recommendations are estimates based on user inputs and should be verified before placing actual trades. Always consider factors such as leverage, margin requirements, and broker-specific rules when determining actual position sizes.

The Risk-to-Reward ratios displayed are theoretical calculations based on swing point detection. Actual trade outcomes will vary based on market conditions, execution quality, and other factors not captured by this indicator.

Past performance does not guarantee future results. Users should thoroughly test any trading approach in a demo environment before risking real capital. The authors and publishers of this indicator are not responsible for any losses or damages arising from its use.

Always consult with a qualified financial advisor before making investment decisions.

Portfolio

Volatility Targeting: Single Asset [BackQuant]Volatility Targeting: Single Asset

An educational example that demonstrates how volatility targeting can scale exposure up or down on one symbol, then applies a simple EMA cross for long or short direction and a higher timeframe style regime filter to gate risk. It builds a synthetic equity curve and compares it to buy and hold and a benchmark.

Important disclaimer

This script is a concept and education example only . It is not a complete trading system and it is not meant for live execution. It does not model many real world constraints, and its equity curve is only a simplified simulation. If you want to trade any idea like this, you need a proper strategy() implementation, realistic execution assumptions, and robust backtesting with out of sample validation.

Single asset vs the full portfolio concept

This indicator is the single asset, long short version of the broader volatility targeted momentum portfolio concept. The original multi asset concept and full portfolio implementation is here:

That portfolio script is about allocating across multiple assets with a portfolio view. This script is intentionally simpler and focuses on one symbol so you can clearly see how volatility targeting behaves, how the scaling interacts with trend direction, and what an equity curve comparison looks like.

What this indicator is trying to demonstrate

Volatility targeting is a risk scaling framework. The core idea is simple:

If realized volatility is low relative to a target, you can scale position size up so the strategy behaves like it has a stable risk budget.

If realized volatility is high relative to a target, you scale down to avoid getting blown around by the market.

Instead of always being 1x long or 1x short, exposure becomes dynamic. This is often used in risk parity style systems, trend following overlays, and volatility controlled products.

This script combines that risk scaling with a simple trend direction model:

Fast and slow EMA cross determines whether the strategy is long or short.

A second, longer EMA cross acts as a regime filter that decides whether the system is ACTIVE or effectively in CASH.

An equity curve is built from the scaled returns so you can visualize how the framework behaves across regimes.

How the logic works step by step

1) Returns and simple momentum

The script uses log returns for the base return stream:

ret = log(price / price )

It also computes a simple momentum value:

mom = price / price - 1

In this version, momentum is mainly informational since the directional signal is the EMA cross. The lookback input is shared with volatility estimation to keep the concept compact.

2) Realized volatility estimation

Realized volatility is estimated as the standard deviation of returns over the lookback window, then annualized:

vol = stdev(ret, lookback) * sqrt(tradingdays)

The Trading Days/Year input controls annualization:

252 is typical for traditional markets.

365 is typical for crypto since it trades daily.

3) Volatility targeting multiplier

Once realized vol is estimated, the script computes a scaling factor that tries to push realized volatility toward the target:

volMult = targetVol / vol

This is then clamped into a reasonable range:

Minimum 0.1 so exposure never goes to zero just because vol spikes.

Maximum 5.0 so exposure is not allowed to lever infinitely during ultra low volatility periods.

This clamp is one of the most important “sanity rails” in any volatility targeted system. Without it, very low volatility regimes can create unrealistic leverage.

4) Scaled return stream

The per bar return used for the equity curve is the raw return multiplied by the volatility multiplier:

sr = ret * volMult

Think of this as the return you would have earned if you scaled exposure to match the volatility budget.

5) Long short direction via EMA cross

Direction is determined by a fast and slow EMA cross on price:

If fast EMA is above slow EMA, direction is long.

If fast EMA is below slow EMA, direction is short.

This produces dir as either +1 or -1. The scaled return stream is then signed by direction:

avgRet = dir * sr

So the strategy return is volatility targeted and directionally flipped depending on trend.

6) Regime filter: ACTIVE vs CASH

A second EMA pair acts as a top level regime filter:

If fast regime EMA is above slow regime EMA, the system is ACTIVE.

If fast regime EMA is below slow regime EMA, the system is considered CASH, meaning it does not compound equity.

This is designed to reduce participation in long bear phases or low quality environments, depending on how you set the regime lengths. By default it is a classic 50 and 200 EMA cross structure.

Important detail, the script applies regime_filter when compounding equity, meaning it uses the prior bar regime state to avoid ambiguous same bar updates.

7) Equity curve construction

The script builds a synthetic equity curve starting from Initial Capital after Start Date . Each bar:

If regime was ACTIVE on the previous bar, equity compounds by (1 + netRet).

If regime was CASH, equity stays flat.

Fees are modeled very simply as a per bar penalty on returns:

netRet = avgRet - (fee_rate * avgRet)

This is not realistic execution modeling, it is just a simple turnover penalty knob to show how friction can reduce compounded performance. Real backtesting should model trade based costs, spreads, funding, and slippage.

Benchmark and buy and hold comparison

The script pulls a benchmark symbol via request.security and builds a buy and hold equity curve starting from the same date and initial capital. The buy and hold curve is based on benchmark price appreciation, not the strategy’s asset price, so you can compare:

Strategy equity on the chart symbol.

Buy and hold equity for the selected benchmark instrument.

By default the benchmark is TVC:SPX, but you can set it to anything, for crypto you might set it to BTC, or a sector index, or a dominance proxy depending on your study.

What it plots

If enabled, the indicator plots:

Strategy Equity as a line, colored by recent direction of equity change, using Positive Equity Color and Negative Equity Color .

Buy and Hold Equity for the chosen benchmark as a line.

Optional labels that tag each curve on the right side of the chart.

This makes it easy to visually see when volatility targeting and regime gating change the shape of the equity curve relative to a simple passive hold.

Metrics table explained

If Show Metrics Table is enabled, a table is built and populated with common performance statistics based on the simulated daily returns of the strategy equity curve after the start date. These include:

Net Profit (%) total return relative to initial capital.

Max DD (%) maximum drawdown computed from equity peaks, stored over time.

Win Rate percent of positive return bars.

Annual Mean Returns (% p/y) mean daily return annualized.

Annual Stdev Returns (% p/y) volatility of daily returns annualized.

Variance of annualized returns.

Sortino Ratio annualized return divided by downside deviation, using negative return stdev.

Sharpe Ratio risk adjusted return using the risk free rate input.

Omega Ratio positive return sum divided by negative return sum.

Gain to Pain total return sum divided by absolute loss sum.

CAGR (% p/y) compounded annual growth rate based on time since start date.

Portfolio Alpha (% p/y) alpha versus benchmark using beta and the benchmark mean.

Portfolio Beta covariance of strategy returns with benchmark returns divided by benchmark variance.

Skewness of Returns actually the script computes a conditional value based on the lower 5 percent tail of returns, so it behaves more like a simple CVaR style tail loss estimate than classic skewness.

Important note, these are calculated from the synthetic equity stream in an indicator context. They are useful for concept exploration, but they are not a substitute for professional backtesting where trade timing, fills, funding, and leverage constraints are accurately represented.

How to interpret the system conceptually

Vol targeting effect

When volatility rises, volMult falls, so the strategy de risks and the equity curve typically becomes smoother. When volatility compresses, volMult rises, so the system takes more exposure and tries to maintain a stable risk budget.

This is why volatility targeting is often used as a “risk equalizer”, it can reduce the “biggest drawdowns happen only because vol expanded” problem, at the cost of potentially under participating in explosive upside if volatility rises during a trend.

Long short directional effect

Because direction is an EMA cross:

In strong trends, the direction stays stable and the scaled return stream compounds in that trend direction.

In choppy ranges, the EMA cross can flip and create whipsaws, which is where fees and regime filtering matter most.

Regime filter effect

The 50 and 200 style filter tries to:

Keep the system active in sustained up regimes.

Reduce exposure during long down regimes or extended weakness.

It will always be late at turning points, by design. It is a slow filter meant to reduce deep participation, not to catch bottoms.

Common applications

This script is mainly for understanding and research, but conceptually, volatility targeting overlays are used for:

Risk budgeting normalize risk so your exposure is not accidentally huge in high vol regimes.

System comparison see how a simple trend model behaves with and without vol scaling.

Parameter exploration test how target volatility, lookback length, and regime lengths change the shape of equity and drawdowns.

Framework building as a reference blueprint before implementing a proper strategy() version with trade based execution logic.

Tuning guidance

Lookback lower values react faster to vol shifts but can create unstable scaling, higher values smooth scaling but react slower to regime changes.

Target volatility higher targets increase exposure and drawdown potential, lower targets reduce exposure and usually lower drawdowns, but can under perform in strong trends.

Signal EMAs tighter EMAs increase trade frequency, wider EMAs reduce churn but react slower.

Regime EMAs slower regime filters reduce false toggles but will miss early trend transitions.

Fees if you crank this up you will see how sensitive higher turnover parameter sets are to friction.

Final note

This is a compact educational demonstration of a volatility targeted, long short single asset framework with a regime gate and a synthetic equity curve. If you want a production ready implementation, the correct next step is to convert this concept into a strategy() script, add realistic execution and cost modeling, test across multiple timeframes and market regimes, and validate out of sample before making any decision based on the results.

DCA Ladder CalculatorThis script is a DCA (Dollar-Cost Averaging) Ladder Calculator with Risk & Leverage Management baked in.

It’s designed for both LONG and SHORT positions, and helps you:

🎯 Strategically scale into positions across multiple entry points

🔐 Control risk exposure via defined capital allocation

⚖️ Utilize leverage responsibly — for efficiency, not destruction

🧮 Visualize risk, stop loss level, and entry distribution

🔁 Adapt to trend reversals or key zones, especially when combined with reversal indicators or higher timeframe signals

🧠 How It Works

This tool takes a capital allocation approach to building a ladder of positions:

1. You define:

- Portfolio value

- Risk per trade (as %)

- Leverage

- Number of DCA levels

- Entry multiplier (e.g. 1x, 2x, 4x...)

2. The script then:

- Calculates total margin to risk = Portfolio × Risk %

- Calculates total leveraged position size = Margin × Leverage

- Distributes entries according to exponential weights (1x, 2x, 4x...), totaling 7 for 3 levels

- Calculates per-entry:

- Entry price (based on price zone spacing)

- Multiplier

- Exact margin per entry

- Leverage per entry (margin × leverage)

- Computes:

- Average entry price (margin-weighted)

- Approximate stop loss level based on recent ATR and price structure

- % drawdown to SL

- Total margin and position size

3. Displays all this in a clean on-chart table.

📈 How to Use It

1. Apply the indicator to a chart (default: 1D — ideal for clean zones).

2. Configure your:

- Portfolio Value (total trading capital)

- Risk per Trade (%) (your acceptable loss)

- Leverage (exchange or strategy-based)

- DCA Levels (e.g. 3 = anchor + 2 entries)

- Multiplier (typically 2.0 for doubling)

3. Choose LONG or SHORT mode depending on direction.

4. The table will show:

- Entry price ladder

- Margin used per entry

- Total position size

- Approx. stop loss (where your full risk is defined)

Use in conjunction with price action, S/R zones, trendline breaks, volume divergence, or reversal indicators.

✅ Best Practices for Using This Tool

- Leverage is a tool, not a weapon. Use it to scale smartly — not recklessly.

- Use fewer, higher-conviction entries. Don’t blindly ladder; combine with price structure and signals.

- Stick to your risk percent. Never risk more than you can afford to lose. Let this calculator enforce discipline.

- Combine with other confirmation tools, like RSI divergence, momentum shifts, OB zones, etc.

- Avoid martingale-style over-exposure. This is not a gambling tool — it’s for capital efficiency.

🛡️ What This Tool Does NOT Do

- This is not a trade signal indicator.

- It does not place trades or auto-manage positions.

- It does not replace personal responsibility or strategy — it's a tool to help apply structure.

⚠️ Disclaimer

This script is for educational and informational purposes only.

It does not constitute financial advice, nor is it a recommendation to buy or sell any financial instrument.

Always consult a licensed financial advisor before making investment decisions.

Use of leverage involves high risk and can lead to substantial losses.

The author and publisher assume no liability for any trading losses resulting from use of this script.

Stock Management (Zeiierman)█ Overview

Stock Management (Zeiierman) gives investors a complete, real-time view of their portfolio directly inside TradingView. It tracks performance, allocation, volatility, and dividends in one unified interface, making it easy to understand both how your portfolio is performing and how it behaves in terms of risk and exposure.

Rather than analyzing each chart in isolation, Stock Management (Zeiierman) turns TradingView into a lightweight portfolio cockpit. You can define up to 20 stock positions (ticker, shares, average cost), and the tool will:

Normalize all positions into a single user-selected currency

Calculate live position value, PnL, PnL%, and daily movement

Compute total portfolio value, performance, and volatility

Optionally generate a risk-parity style Recommended Allocation

Display upcoming dividend amounts, ex-dates, and pay-dates for your holdings

All of this appears as clean on-chart tables, including a main portfolio table, an optional dividend table, and an optional summary panel, allowing you to manage your portfolio while still watching price action. It is a visual portfolio layer built entirely around your own inputs, integrated seamlessly into the TradingView environment.

⚪ Why This One Is Unique

Most investors rely on basic broker dashboards that show position values but provide little insight into risk, exposure, or how each holding interacts with the rest of the portfolio. Stock Management (Zeiierman) goes far beyond that by building an intelligent, unified portfolio layer directly inside TradingView.

It automatically normalizes global holdings into a single reporting currency using live FX data, stabilizes allocation with a volatility-aware weighting engine, and structures your information through an adaptive column framework that highlights performance and risk in real time. A weighted summary blends portfolio movement, volatility, and long-horizon behavior into a clean snapshot, while dividend schedules and projected payouts are fully integrated into the same interface.

█ Main Features

⚪ 1. Portfolio Tracker

The core of Stock Management (Zeiierman) is a dynamic, real-time portfolio table that brings all key position data into one intelligent view. Each holding is displayed with:

Ticker

Sector

Price

Average Paid Price

Shares

Position Value

Position Weight

Profit & Loss

Profit & Loss %

Today % Change

Recommended Allocation

The table updates continuously with market prices, giving investors an immediate understanding of performance, exposure, and risk across all positions.

⚪ 2. Dividend Information

Dividend data for your holdings is automatically fetched, organized, and presented alongside your positions. This includes dividend amount, ex-date, and pay-date, along with projected payouts based on your share count. All dividend-related information is integrated directly into the portfolio view, so you can plan cash flow without switching tools.

⚪ 3. Portfolio Summary

A dedicated summary panel consolidates the entire portfolio into a single snapshot: total value, total PnL, YTD %, today’s change, and overall volatility. The volatility reading is particularly valuable, providing a quick gauge of your portfolio’s risk level and how sensitive it may be to market movement.

⚪ 4. Portfolio Weight Recommendation

An intelligent weighting engine reviews your current allocations and highlights where your portfolio is overexposed or underweighted. It offers recommended allocation levels designed to reduce concentration risk and improve balance, giving you a clearer path toward a more stable long-term positioning.

█ How to Use

⚪ Performance Tracking

Quickly assess your entire portfolio’s profit, loss, daily movement, and volatility from one centralized dashboard. The summary panel gives you an instant read on how your holdings are performing and how sensitive they are to market swings.

⚪ Dividend Management

Monitor upcoming dividend amounts, ex-dates, and pay-dates directly inside your portfolio table. This ensures you never miss a payout opportunity and can plan your expected cash flow with complete clarity.

⚪ Risk Management & Optimization

Use portfolio-wide volatility and the intelligent Recommended Allocation engine to identify imbalances in your holdings. These insights help you adjust position sizes, reduce concentration risk, and maintain a more stable long-term portfolio profile.

⚪ Currency Comparison

Switch between different base currencies to evaluate performance in local or international terms. All positions are automatically normalized using live FX data, making global portfolio management effortless.

█ How It Works

Stock Management (Zeiierman) continuously gathers price, currency, dividend, and volatility data for every ticker you track. All values are automatically converted into your selected reporting currency, so global holdings remain comparable in one unified view.

It builds a live portfolio snapshot of each bar, updating position values, PnL, daily returns, YTD performance, and overall volatility. This gives you an always-current understanding of how your portfolio is performing and how each holding contributes to risk and exposure.

An intelligent, volatility-aware allocation model generates recommended portfolio weights and position sizes, helping you identify where you may be overexposed or underweighted. Dividend information is integrated directly into the table, projecting future payouts and highlighting upcoming ex-dates and pay-dates.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Multi-Asset % Performance Table | v2.1 | TCP Multi-Asset % Performance Table | v2.1 | TCP

ESSENTIAL SUMMARY:

Multi-Asset % Performance Table eliminates the need to manually draw and manage individual "Price Range" tools for every asset. It automatically tracks up to 15 tickers independently in a single dashboard, calculating a TOTAL SCORE (Portfolio Average) for you. Unlike manual drawings, it supports a Global Range while allowing Custom Dates for specific assets, ensuring each ticker is calculated based on its own precise entry/exit. The Smart Visuals dynamically draw the correct date lines only for the ticker you are currently viewing, keeping your chart automatic, accurate, and clutter-free.

FUL DESCRIPTION:

📊 What is this tool?

The Multi-Asset % Performance Table is a powerful portfolio dashboard designed to track the percentage performance of up to 15 different assets simultaneously.

Instead of checking tickers one by one or manually drawing price ranges, this indicator aggregates everything into a single, clean table. It allows you to compare the ROI (Return on Investment) of a basket of coins or stocks over a specific time period and calculates an aggregate TOTAL SCORE (Average %) for your selection.

🚀 Key Features

15 Asset Slots: Monitor up to 15 different tickers (Crypto, Stocks, Forex, etc.) in one view.

Global vs. Custom Dates: Set a "Global" start/end date for the whole portfolio, but override specific assets with Custom Dates if they entered the portfolio at a different time.

Smart Visuals: Automatically draws vertical dashed lines on your chart representing the start and end dates of the ticker you are currently viewing.

Total Score Calculation: Calculates the average percentage change of your portfolio. You can dynamically include or exclude specific assets from this average using the settings.

Status Column: A quick visual reference (✔ or ✘) in the table showing which assets are currently included in the Total Score calculation.

⚙️ How it Works

Data Fetching: The script pulls "Close" prices from the Daily timeframe to ensure accuracy across long periods.

Smart Matching: The visual lines automatically detect which asset you are viewing. For example, if you are looking at BTCUSDT and have custom dates set for it, the vertical lines will jump to those specific dates. If you view a ticker not in your list, it defaults to the Global dates.

Visual Protection: The script uses advanced logic to ensure only one set of range lines appears on the chart at a time, keeping your workspace clean.

🛠️ Instructions & Settings

1. Setting up your Assets

Open the Settings (Cogwheel icon).

Under ASSET 1 through ASSET 15, enter the tickers you want to track (e.g., BINANCE:BTCUSDT).

Include in Avg?: Uncheck this if you want to see the asset in the table but exclude it from the "TOTAL SCORE" average.

2. Defining Time Ranges

Global Settings: Set the Global Start and Global End dates at the top. This applies to all assets by default.

Custom Dates: If a specific asset (e.g., Asset 4) was bought on a different day, check the "Custom Dates?" box for that asset and enter its specific Start/End time.

3. Reading the Table

The table appears on the chart (default: Bottom Right) with three columns:

Asset: The name of the ticker.

% Change: The percentage move from Start Date to End Date. (Green = Positive, Red = Negative).

Inc: Shows a ✔ if the asset is included in the Total Score average, or a ✘ if excluded.

4. The Visual Lines

Two vertical dashed lines will appear on your chart.

Note: These lines are visual references only. You cannot drag them to change the dates. To change the dates, you must use the Settings menu.

💡 Tips

Hover for Details: Hover your mouse over the % Change value in the table to see a tooltip showing the exact Start Price and End Price used for the calculation.

Resolution: The script defaults to 1 Day resolution for optimal accuracy on historical data.

v2.1 | TCP - Custom Built for Precision Performance Tracking

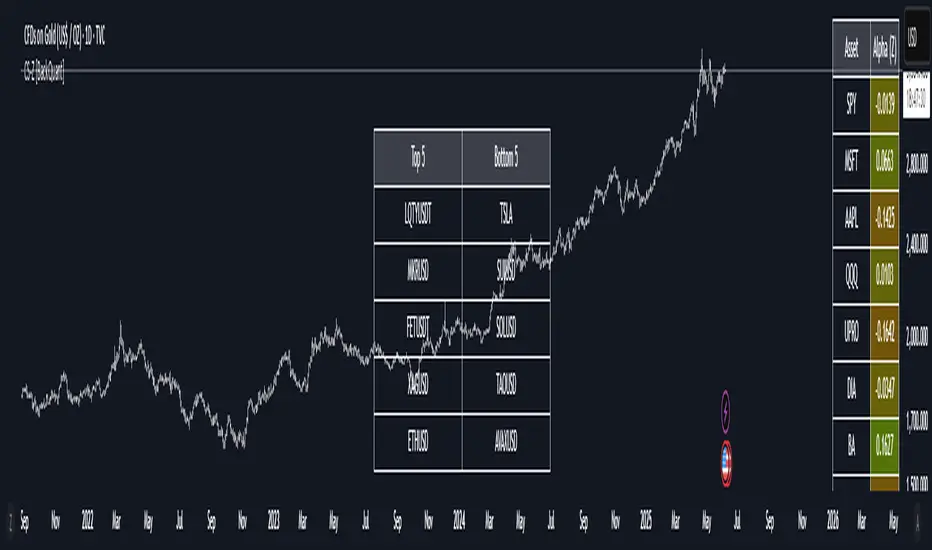

Volatility-Targeted Momentum Portfolio [BackQuant]Volatility-Targeted Momentum Portfolio

A complete momentum portfolio engine that ranks assets, targets a user-defined volatility, builds long, short, or delta-neutral books, and reports performance with metrics, attribution, Monte Carlo scenarios, allocation pie, and efficiency scatter plots. This description explains the theory and the mechanics so you can configure, validate, and deploy it with intent.

Table of contents

What the script does at a glance

Momentum, what it is, how to know if it is present

Volatility targeting, why and how it is done here

Portfolio construction modes: Long Only, Short Only, Delta Neutral

Regime filter and when the strategy goes to cash

Transaction cost modelling in this script

Backtest metrics and definitions

Performance attribution chart

Monte Carlo simulation

Scatter plot analysis modes

Asset allocation pie chart

Inputs, presets, and deployment checklist

Suggested workflow

1) What the script does at a glance

Pulls a list of up to 15 tickers, computes a simple momentum score on each over a configurable lookback, then volatility-scales their bar-to-bar return stream to a target annualized volatility.

Ranks assets by raw momentum, selects the top 3 and bottom 3, builds positions according to the chosen mode, and gates exposure with a fast regime filter.

Accumulates a portfolio equity curve with risk and performance metrics, optional benchmark buy-and-hold for comparison, and a full alert suite.

Adds visual diagnostics: performance attribution bars, Monte Carlo forward paths, an allocation pie, and scatter plots for risk-return and factor views.

2) Momentum: definition, detection, and validation

Momentum is the tendency of assets that have performed well to continue to perform well, and of underperformers to continue underperforming, over a specific horizon. You operationalize it by selecting a horizon, defining a signal, ranking assets, and trading the leaders versus laggards subject to risk constraints.

Signal choices . Common signals include cumulative return over a lookback window, regression slope on log-price, or normalized rate-of-change. This script uses cumulative return over lookback bars for ranking (variable cr = price/price - 1). It keeps the ranking simple and lets volatility targeting handle risk normalization.

How to know momentum is present .

Leaders and laggards persist across adjacent windows rather than flipping every bar.

Spread between average momentum of leaders and laggards is materially positive in sample.

Cross-sectional dispersion is non-trivial. If everything is flat or highly correlated with no separation, momentum selection will be weak.

Your validation should include a diagnostic that measures whether returns are explained by a momentum regression on the timeseries.

Recommended diagnostic tool . Before running any momentum portfolio, verify that a timeseries exhibits stable directional drift. Use this indicator as a pre-check: It fits a regression to price, exposes slope and goodness-of-fit style context, and helps confirm if there is usable momentum before you force a ranking into a flat regime.

3) Volatility targeting: purpose and implementation here

Purpose . Volatility targeting seeks a more stable risk footprint. High-vol assets get sized down, low-vol assets get sized up, so each contributes more evenly to total risk.

Computation in this script (per asset, rolling):

Return series ret = log(price/price ).

Annualized volatility estimate vol = stdev(ret, lookback) * sqrt(tradingdays).

Leverage multiplier volMult = clamp(targetVol / vol, 0.1, 5.0).

This caps sizing so extremely low-vol assets don’t explode weight and extremely high-vol assets don’t go to zero.

Scaled return stream sr = ret * volMult. This is the per-bar, risk-adjusted building block used in the portfolio combinations.

Interpretation . You are not levering your account on the exchange, you are rescaling the contribution each asset’s daily move has on the modeled equity. In live trading you would reflect this with position sizing or notional exposure.

4) Portfolio construction modes

Cross-sectional ranking . Assets are sorted by cr over the chosen lookback. Top and bottom indices are extracted without ties.

Long Only . Averages the volatility-scaled returns of the top 3 assets: avgRet = mean(sr_top1, sr_top2, sr_top3). Position table shows per-asset leverages and weights proportional to their current volMult.

Short Only . Averages the negative of the volatility-scaled returns of the bottom 3: avgRet = mean(-sr_bot1, -sr_bot2, -sr_bot3). Position table shows short legs.

Delta Neutral . Long the top 3 and short the bottom 3 in equal book sizes. Each side is sized to 50 percent notional internally, with weights within each side proportional to volMult. The return stream mixes the two sides: avgRet = mean(sr_top1,sr_top2,sr_top3, -sr_bot1,-sr_bot2,-sr_bot3).

Notes .

The selection metric is raw momentum, the execution stream is volatility-scaled returns. This separation is deliberate. It avoids letting volatility dominate ranking while still enforcing risk parity at the return contribution stage.

If everything rallies together and dispersion collapses, Long Only may behave like a single beta. Delta Neutral is designed to extract cross-sectional momentum with low net beta.

5) Regime filter

A fast EMA(12) vs EMA(21) filter gates exposure.

Long Only active when EMA12 > EMA21. Otherwise the book is set to cash.

Short Only active when EMA12 < EMA21. Otherwise cash.

Delta Neutral is always active.

This prevents taking long momentum entries during obvious local downtrends and vice versa for shorts. When the filter is false, equity is held flat for that bar.

6) Transaction cost modelling

There are two cost touchpoints in the script.

Per-bar drag . When the regime filter is active, the per-bar return is reduced by fee_rate * avgRet inside netRet = avgRet - (fee_rate * avgRet). This models proportional friction relative to traded impact on that bar.

Turnover-linked fee . The script tracks changes in membership of the top and bottom baskets (top1..top3, bot1..bot3). The intent is to charge fees when composition changes. The template counts changes and scales a fee by change count divided by 6 for the six slots.

Use case: increase fee_rate to reflect taker fees and slippage if you rebalance every bar or trade illiquid assets. Reduce it if you rebalance less often or use maker orders.

Practical advice .

If you rebalance daily, start with 5–20 bps round-trip per switch on liquid futures and adjust per venue.

For crypto perp microcaps, stress higher cost assumptions and add slippage buffers.

If you only rotate on lookback boundaries or at signals, use alert-driven rebalances and lower per-bar drag.

7) Backtest metrics and definitions

The script computes a standard set of portfolio statistics once the start date is reached.

Net Profit percent over the full test.

Max Drawdown percent, tracked from running peaks.

Annualized Mean and Stdev using the chosen trading day count.

Variance is the square of annualized stdev.

Sharpe uses daily mean adjusted by risk-free rate and annualized.

Sortino uses downside stdev only.

Omega ratio of sum of gains to sum of losses.

Gain-to-Pain total gains divided by total losses absolute.

CAGR compounded annual growth from start date to now.

Alpha, Beta versus a user-selected benchmark. Beta from covariance of daily returns, Alpha from CAPM.

Skewness of daily returns.

VaR 95 linear-interpolated 5th percentile of daily returns.

CVaR average of the worst 5 percent of daily returns.

Benchmark Buy-and-Hold equity path for comparison.

8) Performance attribution

Cumulative contribution per asset, adjusted for whether it was held long or short and for its volatility multiplier, aggregated across the backtest. You can filter to winners only or show both sides. The panel is sorted by contribution and includes percent labels.

9) Monte Carlo simulation

The panel draws forward equity paths from either a Normal model parameterized by recent mean and stdev, or non-parametric bootstrap of recent daily returns. You control the sample length, number of simulations, forecast horizon, visibility of individual paths, confidence bands, and a reproducible seed.

Normal uses Box-Muller with your seed. Good for quick, smooth envelopes.

Bootstrap resamples realized returns, preserving fat tails and volatility clustering better than a Gaussian assumption.

Bands show 10th, 25th, 75th, 90th percentiles and the path mean.

10) Scatter plot analysis

Four point-cloud modes, each plotting all assets and a star for the current portfolio position, with quadrant guides and labels.

Risk-Return Efficiency . X is risk proxy from leverage, Y is expected return from annualized momentum. The star shows the current book’s composite.

Momentum vs Volatility . Visualizes whether leaders are also high vol, a cue for turnover and cost expectations.

Beta vs Alpha . X is a beta proxy, Y is risk-adjusted excess return proxy. Useful to see if leaders are just beta.

Leverage vs Momentum . X is volMult, Y is momentum. Shows how volatility targeting is redistributing risk.

11) Asset allocation pie chart

Builds a wheel of current allocations.

Long Only, weights are proportional to each long asset’s current volMult and sum to 100 percent.

Short Only, weights show the short book as positive slices that sum to 100 percent.

Delta Neutral, 50 percent long and 50 percent short books, each side leverage-proportional.

Labels can show asset, percent, and current leverage.

12) Inputs and quick presets

Core

Portfolio Strategy . Long Only, Short Only, Delta Neutral.

Initial Capital . For equity scaling in the panel.

Trading Days/Year . 252 for stocks, 365 for crypto.

Target Volatility . Annualized, drives volMult.

Transaction Fees . Per-bar drag and composition change penalty, see the modelling notes above.

Momentum Lookback . Ranking horizon. Shorter is more reactive, longer is steadier.

Start Date . Ensure every symbol has data back to this date to avoid bias.

Benchmark . Used for alpha, beta, and B&H line.

Diagnostics

Metrics, Equity, B&H, Curve labels, Daily return line, Rolling drawdown fill.

Attribution panel. Toggle winners only to focus on what matters.

Monte Carlo mode with Normal or Bootstrap and confidence bands.

Scatter plot type and styling, labels, and portfolio star.

Pie chart and labels for current allocation.

Presets

Crypto Daily, Long Only . Lookback 25, Target Vol 50 percent, Fees 10 bps, Regime filter on, Metrics and Drawdown on. Monte Carlo Bootstrap with Recent 200 bars for bands.

Crypto Daily, Delta Neutral . Lookback 25, Target Vol 50 percent, Fees 15–25 bps, Regime filter always active for this mode. Use Scatter Risk-Return to monitor efficiency and keep the star near upper left quadrants without drifting rightward.

Equities Daily, Long Only . Lookback 60–120, Target Vol 15–20 percent, Fees 5–10 bps, Regime filter on. Use Benchmark SPX and watch Alpha and Beta to keep the book from becoming index beta.

13) Suggested workflow

Universe sanity check . Pick liquid tickers with stable data. Thin assets distort vol estimates and fees.

Check momentum existence . Run on your timeframe. If slope and fit are weak, widen lookback or avoid that asset or timeframe.

Set risk budget . Choose a target volatility that matches your drawdown tolerance. Higher target increases turnover and cost sensitivity.

Pick mode . Long Only for bull regimes, Short Only for sustained downtrends, Delta Neutral for cross-sectional harvesting when index direction is unclear.

Tune lookback . If leaders rotate too often, lengthen it. If entries lag, shorten it.

Validate cost assumptions . Increase fee_rate and stress Monte Carlo. If the edge vanishes with modest friction, refine selection or lengthen rebalance cadence.

Run attribution . Confirm the strategy’s winners align with intuition and not one unstable outlier.

Use alerts . Enable position change, drawdown, volatility breach, regime, momentum shift, and crash alerts to supervise live runs.

Important implementation details mapped to code

Momentum measure . cr = price / price - 1 per symbol for ranking. Simplicity helps avoid overfitting.

Volatility targeting . vol = stdev(log returns, lookback) * sqrt(tradingdays), volMult = clamp(targetVol / vol, 0.1, 5), sr = ret * volMult.

Selection . Extract indices for top1..top3 and bot1..bot3. The arrays rets, scRets, lev_vals, and ticks_arr track momentum, scaled returns, leverage multipliers, and display tickers respectively.

Regime filter . EMA12 vs EMA21 switch determines if the strategy takes risk for Long or Short modes. Delta Neutral ignores the gate.

Equity update . Equity multiplies by 1 + netRet only when the regime was active in the prior bar. Buy-and-hold benchmark is computed separately for comparison.

Tables . Position tables show current top or bottom assets with leverage and weights. Metric table prints all risk and performance figures.

Visualization panels . Attribution, Monte Carlo, scatter, and pie use the last bars to draw overlays that update as the backtest proceeds.

Final notes

Momentum is a portfolio effect. The edge comes from cross-sectional dispersion, adequate risk normalization, and disciplined turnover control, not from a single best asset call.

Volatility targeting stabilizes path but does not fix selection. Use the momentum regression link above to confirm structure exists before you size into it.

Always test higher lag costs and slippage, then recheck metrics, attribution, and Monte Carlo envelopes. If the edge persists under stress, you have something robust.

Crypto Index Price# Crypto Index Price - Indicator Description

## 📊 What is this indicator?

**Crypto Index Price** is an indicator for creating your own cryptocurrency index based on an equal-weighted portfolio. It allows you to track the overall dynamics of the cryptocurrency market through a composite index of selected assets.

## 🎯 Key Features

- **Up to 20 assets in the index** — create an index from any trading pairs

- **Equal-weighted methodology** — each asset has the same weight in the index

- **Moving average** — optional trend filter for the index

- **Flexible visualization settings** — customizable colors and line thickness

## 📈 How to Use

The indicator is displayed in a separate pane below the chart and shows:

1. **Blue line** — crypto index value

2. **Orange line** (optional) — moving average of the index

### Trading Applications:

- **Identify overall market trend** — if the index is rising, most coins are in an uptrend

- **Divergences** — divergence between your asset and the index may signal local opportunities

- **Signal confirmation** — use the index to confirm trading decisions on individual coins

- **Market condition filter** — trade longs when index is above MA, shorts when below

## ⚙️ Settings

### Assets (Symbols)

- **Asset 1-10** — main cryptocurrencies (default: BTC, ETH, BNB, SOL, XRP, ADA, AVAX, LINK, DOGE, TRX)

- **Asset 11-20** — additional slots for index expansion

### Visual Parameters

- **Index line color** — main line color (default: blue)

- **Line width** — from 1 to 5 pixels

- **Show moving average** — enable/disable MA

- **MA period** — moving average calculation period (default: 20)

- **MA color** — moving average line color (default: orange)

## 💡 Recommendations

- For a top coins index, use 5-10 largest cryptocurrencies by market cap

- For an altcoin index, add medium and small coins from your sector

- Use MA to filter false signals and identify the global trend

- Compare individual asset behavior with the index to find anomalies

## ⚠️ Important

The indicator uses equal-weighted methodology — each coin contributes equally regardless of price or market cap. This differs from cap-weighted indices and may provide a different market perspective.

---

*This indicator is intended for analysis and is not trading advice. Always conduct your own analysis before making trading decisions.*

---

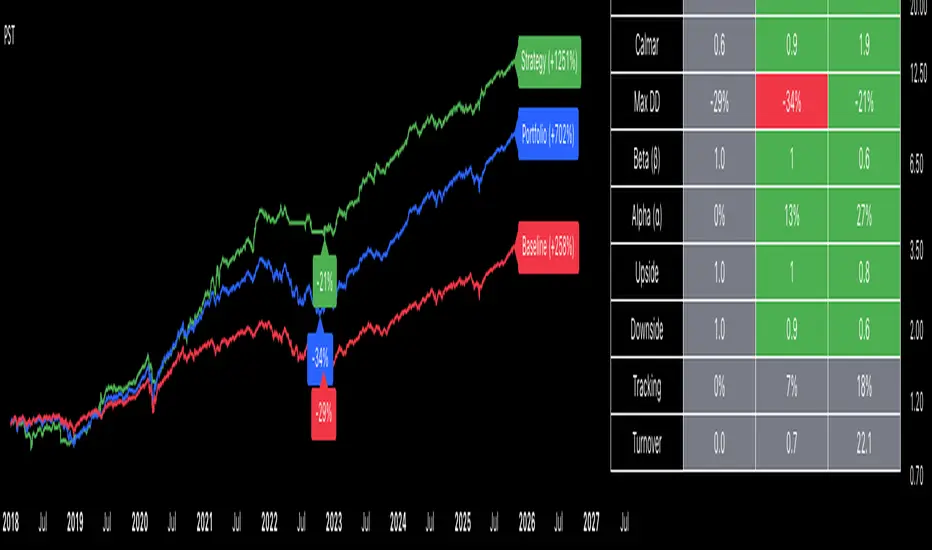

Portfolio Strategy TesterThe Portfolio Strategy Tester is an institutional-grade backtesting framework that evaluates the performance of trend-following strategies on multi-asset portfolios. It enables users to construct custom portfolios of up to 30 assets and apply moving average crossover strategies across individual holdings. The model features a clear, color-coded table that provides a side-by-side comparison between the buy-and-hold portfolio and the portfolio using the risk management strategy, offering a comprehensive assessment of both approaches relative to the benchmark.

Portfolios are constructed by entering each ticker symbol in the menu, assigning its respective weight, and reviewing the total sum of individual weights displayed at the top left of the table. For strategy selection, users can choose between Exponential Moving Average (EMA), Simple Moving Average (SMA), Wilder’s Moving Average (RMA), Weighted Moving Average (WMA), Moving Average Convergence Divergence (MACD), and Volume-Weighted Moving Average (VWMA). Moving average lengths are defined in the menu and apply only to strategy-enabled assets.

To accurately replicate real-world portfolio conditions, users can choose between daily, weekly, monthly, or quarterly rebalancing frequencies and decide whether cash is held or redistributed. Daily rebalancing maintains constant portfolio weights, while longer intervals allow natural drift. When cash positions are not allowed, capital from bearish assets is automatically redistributed proportionally among bullish assets, ensuring the portfolio remains fully invested at all times. The table displays a comprehensive set of widely used institutional-grade performance metrics:

CAGR = Compounded annual growth rate of returns.

Volatility = Annualized standard deviation of returns.

Sharpe = CAGR per unit of annualized standard deviation.

Sortino = CAGR per unit of annualized downside deviation.

Calmar = CAGR relative to maximum drawdown.

Max DD = Largest peak-to-trough decline in value.

Beta (β) = Sensitivity of returns relative to benchmark returns.

Alpha (α) = Excess annualized risk-adjusted returns relative to benchmark.

Upside = Ratio of average return to benchmark return on up days.

Downside = Ratio of average return to benchmark return on down days.

Tracking = Annualized standard deviation of returns versus benchmark.

Turnover = Average sum of absolute changes in weights per year.

Cumulative returns are displayed on each label as the total percentage gain from the selected start date, with green indicating positive returns and red indicating negative returns. In the table, baseline metrics serve as the benchmark reference and are always gray. For portfolio metrics, green indicates outperformance relative to the baseline, while red indicates underperformance relative to the baseline. For strategy metrics, green indicates outperformance relative to both the baseline and the portfolio, red indicates underperformance relative to both, and gray indicates underperformance relative to either the baseline or portfolio. Metrics such as Volatility, Tracking Error, and Turnover ratio are always displayed in gray as they serve as descriptive measures.

In summary, the Portfolio Strategy Tester is a comprehensive backtesting tool designed to help investors evaluate different trend-following strategies on custom portfolios. It enables real-world simulation of both active and passive investment approaches and provides a full set of standard institutional-grade performance metrics to support data-driven comparisons. While results are based on historical performance, the model serves as a powerful portfolio management and research framework for developing, validating, and refining systematic investment strategies.

Ultimate Risk Management Toolkit [ T W K ] :Smart Levels is Smart Trades!

All Trading View users and Stock market Enthusiast, get charged with the all new ( never seen before ) " Ultimate Risk Management Toolkit ⚙📏⚙ " .

Inputs and Features:

1: Drag the Bar-Time vertical line to the desired Entry candle ( manually ) for R:R management and controlling emotional trading.

2: Target, Entry, and SL line style, Width input.

3: Manual specific level Entry and Stop-Loss, input option.

4: Three types of Auto / Manual ' R:R ' risk reward ratio, targets with proper Entry, Stop-Loss points, and Stop-Loss level.

5: Three types of Entry options to fix Emotional trading habit.

6: Trailing Stop-Loss input option ( can be utilize as profit locking/booking ).

It will give more Power to manage your trades with proper R:R ( Auto / manual ) ratio, defined Entry and controlled Stop-Loss Levels.

Compatible with All Devices (Laptop / Mobile / Tablet / PC).

✅ HOW TO GET ACCESS :

Add to favorite and enjoy the true Trading View's sprit of community growth, without any limitations.

If you like any of my Invite-Only indicators, kindly DM and let me know!

⚠ RISK DISCLAIMER :

All content provided by "@TradeWithKeshhav" is for informational & educational purposes only.

It does not constitute any financial advice or a solicitation to buy or sell any securities of any type. All investments / trading involve risks. Past performance does not guarantee future results / returns.

Regards :

Team @TradeWithKeshhav

Happy trading and investing!

Portfolio Simulator & BacktesterMulti-asset portfolio simulator with different metrics and ratios, DCA modeling, and rebalancing strategies.

Core Features

Portfolio Construction

Up to 5 assets with customizable weights (must total 100%)

Support for any tradable symbol: stocks, ETFs, crypto, indices, commodities

Real-time validation of allocations

Dollar Cost Averaging

Monthly or Quarterly contributions

Applies to both portfolio and benchmark for fair comparison

Model real-world investing behavior

Rebalancing

Four strategies: None, Monthly, Quarterly, Yearly

Automatic rebalancing to target weights

Transaction cost modeling (customizable fee %)

Key Metrics Table

CAGR: Annualized compound return (S&P 500 avg: ~10%)

Alpha: Excess return vs. benchmark (positive = outperformance)

Sharpe Ratio: Return per unit of risk (>1.0 is good, >2.0 excellent)

Sortino Ratio: Like Sharpe but only penalizes downside (better metric)

Calmar Ratio: CAGR / Max Drawdown (>1.0 good, >2.0 excellent)

Max Drawdown: Largest peak-to-trough decline

Win Rate: % of positive days (doesn't indicate profitability)

Visualization

Dual-chart comparison - Portfolio vs. Benchmark

Dollar or percentage view toggle

Customizable colors and line width

Two tables: Statistics + Asset Allocation

Adjustable table position and text size

🚀 Quick Start Guide

Enter 1-5 ticker symbols (e.g., SPY, QQQ, TLT, GLD, BTCUSD)

Make sure percentage weights total 100%

Choose date range (ensure chart shows full period - zoom out!)

Configure DCA and rebalancing (optional)

Select benchmark (default: SPX)

Analyze results in statistics table

💡 Pro Tips

Chart data matters: Load SPY or your longest-history asset as main chart

If you select an asset that was not available for the selected period, the chart will not show up! E.g. BTCUSD data: Only available from ~2017 onwards.

Transaction fees: 0.1% default (adjust to match your broker)

⚠️ Important Notes

Requires visible chart data (zoom out to show full date range)

Limited by each asset's historical data availability

Transaction fees and costs are modeled, but taxes/slippage are not

Past performance ≠ future results

Use for research and education only, not financial advice

Let me know if you have any suggestions to improve this simulator.

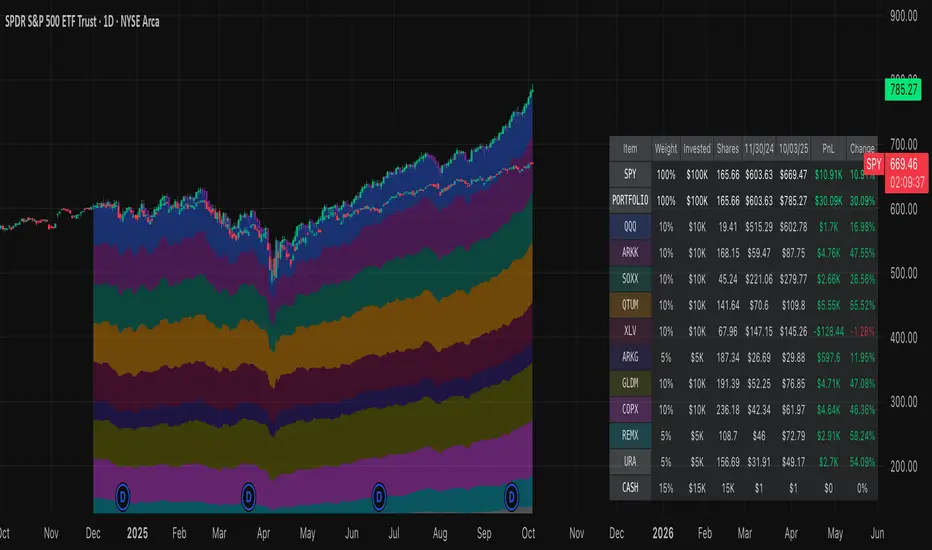

Normalized Portfolio TrackerThis script lets you create, visualize, and track a custom portfolio of up to 15 assets directly on TradingView.

It calculates a synthetic "portfolio index" by combining multiple tickers with user-defined weights, automatically normalizing them so the total allocation always equals 100%.

All assets are scaled to a common starting point, allowing you to compare your portfolio’s performance versus any benchmark like SPY, QQQ, or BTC.

🚀 Goal

This script helps traders and investors:

• Understand the combined performance of their portfolio.

• Normalize diverse assets into a single synthetic chart .

• Make portfolio-level insights without relying on external spreadsheets.

🎯 Use Cases

• Backtest your portfolio allocations directly on the chart.

• Compare your portfolio vs. benchmarks like SPY, QQQ, BTC.

• Track thematic baskets (commodities, EV supply chain, regional ETFs).

• Visualize how each component contributes to overall performance.

📊 Features

• Weighted Portfolio Performance : Combines selected assets into a synthetic value series.

• Base Price Alignment : Each asset is normalized to its starting price at the chosen date.

• Dynamic Portfolio Table : Displays symbols, normalized weights (%), equivalent shares (based on each asset’s start price, sums to 100 shares), and a total row that always sums to 100%.

• Multi-Asset Support : Works with stocks, ETFs, indices, crypto, or any TradingView-compatible symbol.

⚙️ Configuration

Flexible Portfolio Setup

• Add up to 15 assets with custom weight inputs.

• You can enter any arbitrary numbers (e.g. 30, 15, 55).

• The script automatically normalizes all weights so the total allocation always equals 100%.

Start Date Selection

• Choose any custom start date to normalize all assets.

• The portfolio value is then scaled relative to the main chart symbol, so you can directly compare portfolio performance against benchmarks like SPY or QQQ.

Chart Styles

• Candlestick chart

• Heikin Ashi chart

• Line chart

Custom Display

• Adjustable colors and line widths

• Optionally display asset list, normalized weights, and equivalent shares

⚙️ How It Works

• Fetch OHLC data for each asset.

• Normalizes weights internally so totals = 100%.

• Stores each asset’s base price at the selected start date.

• Calculates equivalent “shares” for each allocation.

• Builds a synthetic portfolio value series by summing weighted contributions.

• Renders as Candlestick, Heikin Ashi, or Line chart.

• Adds a portfolio info table for clarity.

⚠️ Notes

• This script is for visualization only . It does not place trades or auto-rebalance.

• Weight inputs are automatically normalized, so you don’t need to enter exact percentages.

TrendIsYourFriend Strategy (SPY,IWM,VYM,XLK,SPXL,BTC,GOLD,VT...)Personal disclaimer

Don’t trust this strategy. Don’t trust any other model either just because of its author or a backtest curve. Overfitting is an easy trap, and beginners often fall into it. This script isn’t meant to impress you. It’s meant to survive reality. If it does, maybe it will raise questions and you’ll remember it.

Legal disclaimer

Educational purposes only. Not financial advice. Past performance is not indicative of future results.

Strategy description

Long-only, trend-based logic with two entry types (trend continuation or excess-move reversion), dynamic stop-losses, and a VIX filter to avoid turbulent markets.

Minimal number of parameters with enough trades to support robustness.

For backtest, each trade is sized at $10,000 flat (no compounding, to focus on raw model quality and the regularity of its results over time).

Fees = $0 (neutral choice, as brokers differ).

Slippage = $0, deliberate choice: most entries occur on higher timeframes, and some assets start their history on charts at very low prices, which would otherwise distort results.

What makes this script original

Beyond a classical trend calculation, both excess-move entries and dynamic stop-loss exits also rely on trend logic. Except for the VIX filter, everything comes from trend functions, with very few parameters.

Pre-configurations are fixed in the code, allowing sincere performance tracking across a dozen cases over the medium to long term.

Allowed

SPY (ARCA) — 2-hour chart: S&P 500 ETF, most liquid equity benchmark

IWM (ARCA) — Daily chart: Russell 2000 ETF, US small caps

VYM (ARCA) — Daily chart: Vanguard High Dividend Yield ETF

XLK (ARCA) — Daily chart: Technology Select Sector SPDR

SPXL (ARCA) — Daily chart: 3× leveraged S&P 500 ETF

BTCUSD (COINBASE) — 4-hour chart: Bitcoin vs USD

GOLD (TVC) — Daily chart: Gold spot price

VT (ARCA) — Daily chart: Vanguard Total World Stock ETF

PG (NYSE) — Daily chart: Procter & Gamble Co.

CQQQ (ARCA) — Daily chart: Invesco China Technology ETF

EWC (ARCA) — Daily chart: iShares MSCI Canada ETF

EWJ (ARCA) — Daily chart: iShares MSCI Japan ETF

How to use and form an opinion on it

Works only on the pairs above.

Feel free to modify the input parameters (slippage, fees, order size, margins, …) to see how the model behaves under your own conditions

Compare it with a simple Buy & Hold (requires an order size of 100% equity).

You may also want to look at its time-in-market — the share of time your capital is actually at risk.

Finally, let me INSIST on this : let it run live for months before forming an opinion!

Share your thoughts in the comments 🚀 if you’d like to discuss its live performance.

Correlation Heatmap Matrix [TradingFinder] 20 Assets Variable🔵 Introduction

Correlation is one of the most important statistical and analytical metrics in financial markets, data mining, and data science. It measures the strength and direction of the relationship between two variables.

The correlation coefficient always ranges between +1 and -1 : a perfect positive correlation (+1) means that two assets or currency pairs move together in the same direction and at a constant ratio, a correlation of zero (0) indicates no clear linear relationship, and a perfect negative correlation (-1) means they move in exactly opposite directions.

While the Pearson Correlation Coefficient is the most common method for calculation, other statistical methods like Spearman and Kendall are also used depending on the context.

In financial market analysis, correlation is a key tool for Forex, the Stock Market, and the Cryptocurrency Market because it allows traders to assess the price relationship between currency pairs, stocks, or coins. For example, in Forex, EUR/USD and GBP/USD often have a high positive correlation; in stocks, companies from the same sector such as Apple and Microsoft tend to move similarly; and in crypto, most altcoins show a strong positive correlation with Bitcoin.

Using a Correlation Heatmap in these markets visually displays the strength and direction of these relationships, helping traders make more accurate decisions for risk management and strategy optimization.

🟣 Correlation in Financial Markets

In finance, correlation refers to measuring how closely two assets move together over time. These assets can be stocks, currency pairs, commodities, indices, or cryptocurrencies. The main goal of correlation analysis in trading is to understand these movement patterns and use them for risk management, trend forecasting, and developing trading strategies.

🟣 Correlation Heatmap

A correlation heatmap is a visual tool that presents the correlation between multiple assets in a color-coded table. Each cell shows the correlation coefficient between two assets, with colors indicating its strength and direction. Warm colors (such as red or orange) represent strong negative correlation, cool colors (such as blue or cyan) represent strong positive correlation, and mid-range tones (such as yellow or green) indicate correlations that are close to neutral.

🟣 Practical Applications in Markets

Forex : Identify currency pairs that move together or in opposite directions, avoid overexposure to similar trades, and spot unusual divergences.

Crypto : Examine the dependency of altcoins on Bitcoin and find independent movers for portfolio diversification.

Stocks : Detect relationships between stocks in the same industry or find outliers that move differently from their sector.

🟣 Key Uses of Correlation in Trading

Risk management and diversification: Select assets with low or negative correlation to reduce portfolio volatility.

Avoiding overexposure: Prevent opening multiple positions on highly correlated assets.

Pairs trading: Exploit temporary deviations between historically correlated assets for arbitrage opportunities.

Intermarket analysis: Study the relationships between different markets like stocks, currencies, commodities, and bonds.

Divergence detection: Spot when two typically correlated assets move apart as a possible trend change signal.

Market forecasting: Use correlated asset movements to anticipate others’ behavior.

Event reaction analysis: Evaluate how groups of assets respond to economic or political events.

❗ Important Note

It’s important to note that correlation does not imply causation — it only reflects co-movement between assets. Correlation is also dynamic and can change over time, which is why analyzing it across multiple timeframes provides a more accurate picture. Combining correlation heatmaps with other analytical tools can significantly improve the precision of trading decisions.

🔵 How to Use

The Correlation Heatmap Matrix indicator is designed to analyze and manage the relationships between multiple assets at once. After adding the tool to your chart, start by selecting the assets you want to compare (up to 20).

Then, choose the Correlation Period that fits your trading strategy. Shorter periods (e.g., 20 bars) are more sensitive to recent price movements, making them suitable for short-term trading, while longer periods (e.g., 100 or 200 bars) provide a broader view of correlation trends over time.

The indicator outputs a color-coded matrix where each cell represents the correlation between two assets. Warm colors like red and orange signal strong negative correlation, while cool colors like blue and cyan indicate strong positive correlation. Mid-range tones such as yellow or green suggest correlations that are close to neutral. This visual representation makes it easy to spot market patterns at a glance.

One of the most valuable uses of this tool is in portfolio risk management. Portfolios with highly correlated assets are more vulnerable to market swings. By using the heatmap, traders can find assets with low or negative correlation to reduce overall risk.

Another key benefit is preventing overexposure. For example, if EUR/USD and GBP/USD have a high positive correlation, opening trades on both is almost like doubling the position size on one asset, increasing risk unnecessarily. The heatmap makes such relationships clear, helping you avoid them.

The indicator is also useful for pairs trading, where a trader identifies assets that are usually correlated but have temporarily diverged — a potential arbitrage or mean-reversion opportunity.

Additionally, the tool supports intermarket analysis, allowing traders to see how movements in one market (e.g., crude oil) may impact others (e.g., the Canadian dollar). Divergence detection is another advantage: if two typically aligned assets suddenly move in opposite directions, it could signal a major trend shift or a news-driven move.

Overall, the Correlation Heatmap Matrix is not just an analytical indicator but also a fast, visual alert system for monitoring multiple markets at once. This is particularly valuable for traders in fast-moving environments like Forex and crypto.

🔵 Settings

🟣 Logic

Correlation Period : Number of bars used to calculate correlation between assets.

🟣 Display

Table on Chart : Enable/disable displaying the heatmap directly on the chart.

Table Size : Choose the table size (from very small to very large).

Table Position : Set the table location on the chart (top, middle, or bottom in various alignments).

🟣 Symbol Custom

Select Market : Choose the market type (Forex, Stocks, Crypto, or Custom).

Symbol 1 to Symbol 20: In custom mode, you can define up to 20 assets for correlation calculation.

🔵 Conclusion

The Correlation Heatmap Matrix is a powerful tool for analyzing correlations across multiple assets in Forex, crypto, and stock markets. By displaying a color-coded table, it visually conveys both the strength and direction of correlations — warm colors for strong negative correlation, cool colors for strong positive correlation, and mid-range tones such as yellow or green for near-zero or neutral correlation.

This helps traders select assets with low or negative correlation for diversification, avoid overexposure to similar trades, identify arbitrage and pairs trading opportunities, and detect unusual divergences between typically aligned assets. With support for custom mode and up to 20 symbols, it offers high flexibility for different trading strategies, making it a valuable complement to technical analysis and risk management.

Correlation HeatMap Matrix Data [TradingFinder]🔵 Introduction

Correlation is a statistical measure that shows the degree and direction of a linear relationship between two assets.

Its value ranges from -1 to +1 : +1 means perfect positive correlation, 0 means no linear relationship, and -1 means perfect negative correlation.

In financial markets, correlation is used for portfolio diversification, risk management, pairs trading, intermarket analysis, and identifying divergences.

Correlation HeatMap Matrix Data TradingFinder is a Pine Script v6 library that calculates and returns raw correlation matrix data between up to 20 symbols. It only provides the data – it does not draw or render the heatmap – making it ideal for use in other scripts that handle visualization or further analysis. The library uses ta.correlation for fast and accurate calculations.

It also includes two helper functions for visual styling :

CorrelationColor(corr) : takes the correlation value as input and generates a smooth gradient color, ranging from strong negative to strong positive correlation.

CorrelationTextColor(corr) : takes the correlation value as input and returns a text color that ensures optimal contrast over the background color.

Library

"Correlation_HeatMap_Matrix_Data_TradingFinder"

CorrelationColor(corr)

Parameters:

corr (float)

CorrelationTextColor(corr)

Parameters:

corr (float)

Data_Matrix(Corr_Period, Sym_1, Sym_2, Sym_3, Sym_4, Sym_5, Sym_6, Sym_7, Sym_8, Sym_9, Sym_10, Sym_11, Sym_12, Sym_13, Sym_14, Sym_15, Sym_16, Sym_17, Sym_18, Sym_19, Sym_20)

Parameters:

Corr_Period (int)

Sym_1 (string)

Sym_2 (string)

Sym_3 (string)

Sym_4 (string)

Sym_5 (string)

Sym_6 (string)

Sym_7 (string)

Sym_8 (string)

Sym_9 (string)

Sym_10 (string)

Sym_11 (string)

Sym_12 (string)

Sym_13 (string)

Sym_14 (string)

Sym_15 (string)

Sym_16 (string)

Sym_17 (string)

Sym_18 (string)

Sym_19 (string)

Sym_20 (string)

🔵 How to use

Import the library into your Pine Script using the import keyword and its full namespace.

Decide how many symbols you want to include in your correlation matrix (up to 20). Each symbol must be provided as a string, for example FX:EURUSD .

Choose the correlation period (Corr\_Period) in bars. This is the lookback window used for the calculation, such as 20, 50, or 100 bars.

Call Data_Matrix(Corr_Period, Sym_1, ..., Sym_20) with your selected parameters. The function will return an array containing the correlation values for every symbol pair (upper triangle of the matrix plus diagonal).

For example :

var string Sym_1 = '' , var string Sym_2 = '' , var string Sym_3 = '' , var string Sym_4 = '' , var string Sym_5 = '' , var string Sym_6 = '' , var string Sym_7 = '' , var string Sym_8 = '' , var string Sym_9 = '' , var string Sym_10 = ''

var string Sym_11 = '', var string Sym_12 = '', var string Sym_13 = '', var string Sym_14 = '', var string Sym_15 = '', var string Sym_16 = '', var string Sym_17 = '', var string Sym_18 = '', var string Sym_19 = '', var string Sym_20 = ''

switch Market

'Forex' => Sym_1 := 'EURUSD' , Sym_2 := 'GBPUSD' , Sym_3 := 'USDJPY' , Sym_4 := 'USDCHF' , Sym_5 := 'USDCAD' , Sym_6 := 'AUDUSD' , Sym_7 := 'NZDUSD' , Sym_8 := 'EURJPY' , Sym_9 := 'EURGBP' , Sym_10 := 'GBPJPY'

,Sym_11 := 'AUDJPY', Sym_12 := 'EURCHF', Sym_13 := 'EURCAD', Sym_14 := 'GBPCAD', Sym_15 := 'CADJPY', Sym_16 := 'CHFJPY', Sym_17 := 'NZDJPY', Sym_18 := 'AUDNZD', Sym_19 := 'USDSEK' , Sym_20 := 'USDNOK'