Monthly DI+ & RSI StrategyOverview This strategy is designed to capture significant trend reversals and continuations on the Monthly timeframe. It combines the trend-following capability of the Directional Movement Index (DMI) with the fast momentum detection of RSI (Period 6).

Core Logic The strategy triggers a long position based on a dual-confirmation system. It looks for a specific "handshake" between Trend (DI) and Momentum (RSI).

Entry Conditions (OR Logic) A Buy signal is generated if EITHER of the following occurs:

Trend Trigger: DI+ crosses over DI- (while RSI is already bullish, trading above its SMA).

Momentum Trigger: RSI(6) crosses over RSI SMA(14) (while the trend is already bullish, with DI+ > DI-).

Exit Condition (Stop Loss)

Trend Reversal: The position is closed immediately if DI- crosses over DI+, indicating the bullish trend has been invalidated.

Default Settings

Timeframe: Optimized for 1M (Monthly) charts.

RSI: Length 6

RSI SMA: Length 14

DMI: Length 14 / Smoothing 14

Risk Warning This script is for educational purposes only. Past performance does not guarantee future results. Always backtest on your specific asset classes before trading.

Relative Strength Index (RSI)

Strategy with VWRSI and SAVE orders Long or Short or BothVWRSI is very powerful indicator coded by Algo Alpha and I Make Strategy of it

But there is no stop loss instate the Strategy is using Save orders to minimize the market manipulation

The best to used is side way market with long and short enable

The Strategy trigger long or short market order -

long - ta.crossover(rsi, 20)

short - ta.crossunder(rsi, 80)

And if is not take profit from the first trade start with the save trades until will do

the sum of the first order - base order and the save order can be adjust from the user

as well the deviation from the first order

IF some user have questions let me know

StrategyScript77 Is a rule-based strategy built on top of an Ichimoku based engine.

Ichimoku concepts are used as the backbone for trend and momentum filtering, so the strategy tends to stay on the side of the dominant move instead of fighting it.

The name “Super77” comes from the behavior I consistently observed in testing because the win rate tends to hover around the 70–80% range, often clustering around ~77% when used as intended.

It’s not a promise or guarantee, but it reflects the core design philosophy: frequent, relatively small but steady wins, with controlled and manageable losses.

Trading Style – Built for Conservative Traders

Super77 is intentionally designed for traders who prefer a conservative and calm approach:

Entries only at bar close

The strategy waits for bar close confirmation before entering a position. No intrabar guessing, no chasing half-formed signals. If the signal is still valid at close, only then will it enter.

Exits automated on bar close

Exits are also managed on bar close, which makes the logic transparent, easy to review on the chart, and more robust in backtesting compared to tick-based or intrabar hacks.

Semi-auto friendly

If you like to keep some discretion, you can treat it as semi-automatic:

Let the strategy generate entry signals

Manually cancel or skip certain trades if market context changes (news, extreme volatility, etc.)

This combination makes Super77 suitable for traders who don’t want to stare at the screen all day but still want structure and automation.

How to Use

Works best with bar-close execution (avoid trying to simulate intrabar fills if you want consistent behavior).

Designed for conservative, trend-aligned trading, not for hyper-scalping or news gambling.

Can be used as:

Fully automated (let all entries/exits trigger on bar close), or

Semi-automated (use alerts/signals but manually cancel some entries).

Step-by-Step: Automation with Cornix (Webhook Setup)

You can automate Super77 using Cornix by connecting TradingView alerts to your Cornix group via webhook.

Note: Exact button names may differ slightly depending on Cornix / TradingView updates, but the flow is always the same:

Cornix group → get webhook URL & mapping → TradingView alerts → signals sent to Cornix.

(Optional) Map specific pairs / directions

If you use UUID / signal mapping per symbol and per side (long/short), set them up in Cornix according to your own template.

Super77 can be used either:

On a single pair (simple setup), or

On multiple pairs if your alert / webhook structure supports that. So you can pick many pairs with 1 script.

Final Notes & Disclaimer

Super77 is an educational and experimental trading tool, not financial advice.

Past performance in back tests does not guarantee future results.

Always:

Test on demo or paper first

Adjust risk to match your own profile

Accept that losses and drawdowns are a natural part of any strategy

If you’re looking for a strategy that reflects a conservative, confirmation-based trading style with a focus on steady win rate and smoother equity behavior, Super77 was built exactly with that mindset in mind.

Profitable Pair Correlation Divergence Scanner v6This strategy identifies divergence opportunities between two correlated assets using a combination of Z-Score spread analysis, trend confirmation, RSI & MACD momentum checks, correlation filters, and ATR-based stop-loss/take-profit management. It’s optimized for positive P&L and realistic trade execution.

Key Features:

Pair Divergence Detection:

Measures deviation between returns of two assets and identifies overbought/oversold spread conditions using Z-Score.

Trend Alignment:

Trades only in the direction of the primary asset’s trend using a fast EMA vs slow EMA filter.

Momentum Confirmation:

Confirms trades with RSI and MACD to reduce false signals.

Correlation Filter:

Ensures the pair is strongly correlated before taking trades, avoiding noisy signals.

Risk Management:

Dynamic ATR-based stop-loss and take-profit ensures proper reward-to-risk ratio.

Exit Conditions:

Automatically closes positions when Z-Score normalizes, or ATR-based exits are hit.

How It Works:

Calculate Returns:

Computes returns for both assets over the selected timeframe.

Z-Score Spread:

Calculates the spread between returns and normalizes it using moving average and standard deviation.

Trend Filter:

Only takes long trades if the fast EMA is above the slow EMA, and short trades if the fast EMA is below the slow EMA.

Momentum Confirmation:

Confirms trade direction with RSI (>50 for longs, <50 for shorts) and MACD alignment.

Correlation Check:

Ensures the pair’s recent correlation is strong enough to validate divergence signals.

Trade Execution:

Opens positions when Z-Score crosses thresholds and all conditions align. Positions close when Z-Score normalizes or ATR-based SL/TP is hit.

Plot Explanation:

Z-Score: Blue line shows divergence magnitude.

Entry Levels: Red/Green lines mark long/short thresholds.

Exit Zone: Gray lines show normalization zone.

EMA Trend Lines: Purple (fast), Orange (slow) for trend alignment.

Correlation: Teal overlay shows current correlation strength.

Usage Tips:

Use highly correlated pairs for best results (e.g., EURUSD/GBPUSD).

Run on higher timeframe charts (1h or 4h) to reduce noise.

Adjust ATR multiplier based on volatility to avoid premature stops.

Combine with alerts for automated notifications or webhook execution.

Conclusion:

The Profitable Pair Correlation Divergence Scanner v6 is designed for traders who want systematic, low-risk, positive P&L trading opportunities with minimal manual monitoring. By combining trend alignment, momentum confirmation, correlation filters, and dynamic exits, it reduces false signals and improves execution reliability.

Run it on TradingView and watch how it captures divergence opportunities while maintaining positive P&L across trades.

Bollinger Bands Mean Reversion using RSI [Krishna Peri]How it Works

Long entries trigger when:

- RSI reaches oversold levels, and

- At least one bullish candle closes inside the lower Bollinger Band

Short entries trigger when:

- RSI reaches overbought levels, and

- At least one bearish candle closes inside the upper Bollinger Band

This approach aims to capture exhaustion moves where price pushes into extreme deviation from its mean and then snaps back toward the middle band.

Important Disclaimer

This is a mean-reversion strategy, which means it performs best in sideways, ranging, or slowly oscillating market conditions. When markets shift into strong trends, Bollinger Bands expand and volatility increases, which may cause some signals to become inaccurate or fail altogether.

For best results, combine this script with:

- Price action

- Market structure

- Higher-timeframe trend context

- Previous day/week/month highs & lows

- Untested liquidity levels or imbalance zones

- Session timing (Asia, London, NY)

Using these confluences helps filter out low-probability trades and significantly improves consistency and precision.

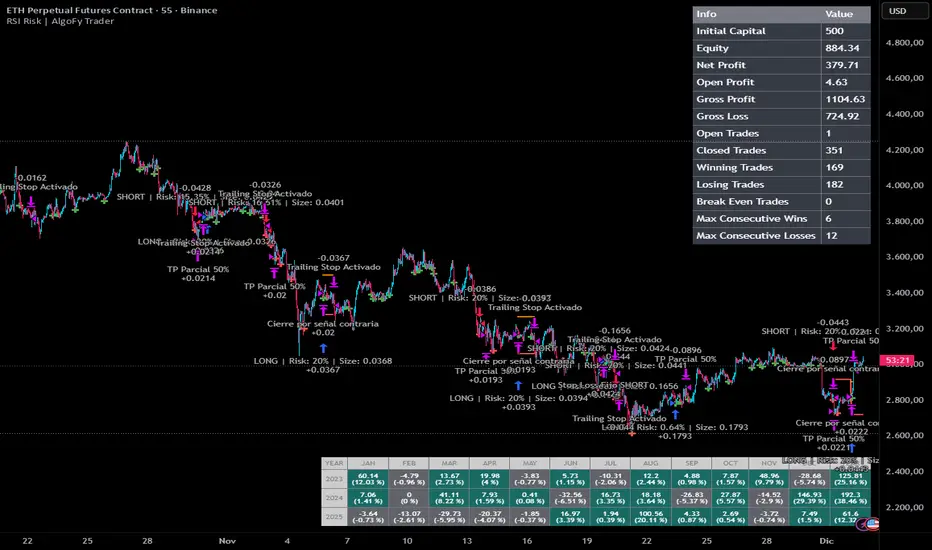

RSI Risk | AlgoFy TraderRSI Risk | AlgoFy Trader

Overview

The RSI Risk | AlgoFy Trader is a trading system that combines RSI-based entry signals with automated capital management. This strategy identifies potential momentum shifts while controlling risk through calculated position sizing.

Key Features

Dynamic Risk Management:

Fixed Risk Per Trade: Users set maximum risk percentage per trade.

Automatic Position Sizing: Calculates position size based on stop-loss distance.

Capital Protection: Limits each trade's risk to user-defined percentage.

RSI Entry System:

Momentum Detection: Uses RSI crossovers above/below defined thresholds.

Clear Signals: Provides long/short entries on momentum transitions.

Multiple Exit Layers:

Dynamic Stop Loss: Stop based on recent price structure.

Fixed Safety Stop: Optional percentage-based stop loss.

Partial Take Profit: Optional early profit-taking.

Trailing Stop: Optional dynamic profit protection.

Performance Tracking:

Trade Statistics: Tracks win/loss streaks and performance metrics.

Monthly Dashboard: Shows monthly/yearly P&L with equity views.

Trade Details: Displays risk percentage and position size.

How It Works

Signal Detection: Monitors RSI for crossover events.

Risk Calculation: Determines stop-loss based on recent volatility.

Position Sizing: Calculates exact position to match risk percentage.

Example:

Account: $10,000 | Risk: 2% ($200 max)

Stop loss at 4% distance

Position size: $5,000

Result: 4% loss on $5,000 = $200 (2% of account)

Recommended Settings

Risk: 1-2% per trade

Enable fixed stop at 3-4%

Consider trailing stop activation

This script provides disciplined RSI trading with automated risk control, adjusting exposure while maintaining strict risk limits.

Oleg_Aryukov_StrategyTrader Oleg Aryukov's strategy, based on a variety of oscillators, allows him to try to catch reversals in cryptocurrencies.

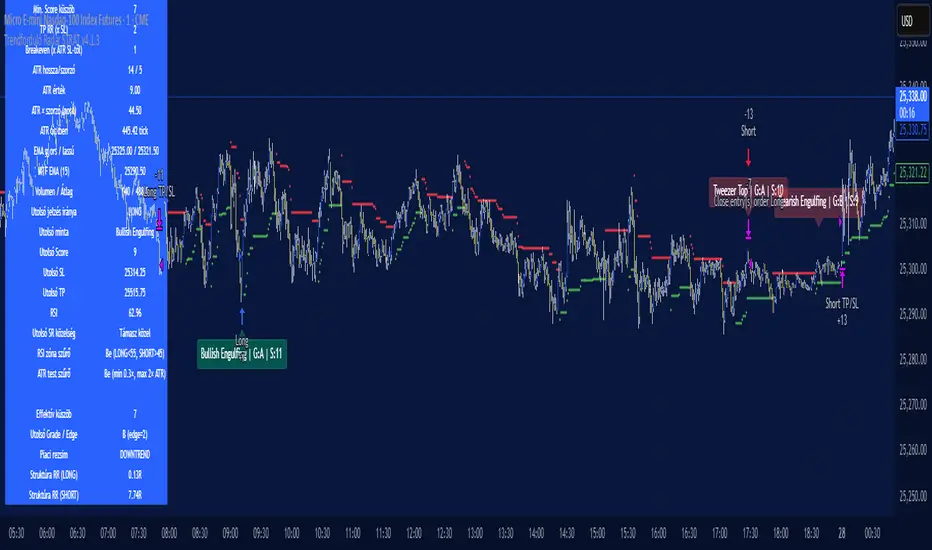

Trendforduló Radar STRAT v4.1.3Trend Reversal Radar is a proprietary indicator that examines potential turning points in market trends. It combines data from multiple time frames, support and resistance levels, and volume movements to provide visual signals to traders. Its purpose is not to provide trading advice, but to complement technical analysis and provide more confident decision support.- A Trendforduló Radar egy saját fejlesztésű indikátor, amely a piaci trendek lehetséges fordulópontjait vizsgálja. Több idősík adatait, támasz–ellenállás szinteket és volumenmozgásokat kombinálva ad vizuális jelzést a kereskedőnek. A célja nem a kereskedési tanácsadás, hanem hogy kiegészítse a technikai elemzést és magabiztosabb döntéstámogatást adjon.

Retracement Strategy [OmegaTools]Retracement Strategy is a systematic trend–retracement framework designed to identify directional opportunities after a confirmed momentum shift, and to manage exits using either trend reversals or overextension conditions. It is built around a smoothed RSI regime filter and a simple, price-based retracement trigger, making it applicable across a wide range of markets and timeframes while remaining transparent and easy to interpret.

The strategy begins by defining the underlying trend through a two-stage RSI signal. A standard RSI is computed over the user-defined Length input, then smoothed with a short moving average to reduce noise. Two symmetric thresholds are derived from the Threshold parameter: an upper band at 100 minus the threshold and a lower band at the threshold itself. When the smoothed RSI crosses above the upper band, the environment is classified as bullish and the internal trend state is set to uptrend. When the smoothed RSI crosses below the lower band, the environment is classified as bearish and the trend state becomes downtrend. When RSI moves back into the central zone between the two bands, the trend is considered neutral. In addition to the current trend, the strategy tracks the last non-neutral trend direction, which is used to detect genuine trend changes rather than transient oscillations.

Once a trend is established, the strategy looks for retracement entries in the direction of that trend. For long setups in an uptrend, it computes the lowest low over the previous Length minus one bars, excluding the current bar. A long signal is generated when price dips below this recent low while the trend state remains bullish. Symmetrically, for short setups in a downtrend, it computes the highest high over the previous Length minus one bars and enters short when price spikes above this recent high while the trend state remains bearish. This logic is designed to capture pullbacks against the prevailing RSI-defined trend, entering when the market tests or slightly violates recent extremes, rather than chasing breakouts. The candles are visually coloured to reflect the detected trend, highlighting bullish and bearish environments while keeping neutral phases distinguishable on the chart. An ATR-based measure is used solely to position the “UP” and “DN” labels on the chart for clearer visualisation of entry points; it does not directly influence position sizing or stop calculation in this implementation.

Take profit and stop loss behaviour are fully parameterized through the “Take Profit” and “Stop Loss” inputs, each offering three modes: None, Trend Change and Extension. When “Trend Change” is selected for the take profit, the strategy will only exit profitable positions when a confirmed trend reversal occurs. For a long position, this means that the strategy will close the trade when the trend state flips from uptrend to downtrend, and the last recorded trend direction validates that this is a genuine reversal rather than a neutral fluctuation; the same logic applies symmetrically for short positions. When “Extension” is selected as the take profit mode, the strategy closes profitable long trades when the smoothed RSI reaches or exceeds the upper threshold, interpreted as an overbought extension within the bullish regime, and closes profitable short trades when the smoothed RSI falls to or below the lower threshold, interpreted as an oversold extension within the bearish regime. When “None” is chosen, the strategy does not apply any explicit take profit logic, leaving trades to be managed by the stop loss settings or by user discretion in backtesting.

The stop loss parameter works in a parallel way. With “Trend Change” selected as stop loss, any open long position is closed when the trend flips from uptrend to downtrend, regardless of whether the trade is currently in profit or loss, and any open short is closed when the trend flips from downtrend to uptrend. This turns the RSI trend regime into a hard invalidation rule: once the underlying momentum structure reverses, the position is exited. With “Extension” selected for stop loss, long positions are closed when RSI falls back below the upper band and moves towards the opposite side of the range, while short positions are closed when RSI rises above the lower band and moves towards the upper side. In practice, this acts as a dynamic exit based on the oscillator moving out of a favourable context for the existing trade. Selecting “None” for stop loss disables these automatic exits, leaving only the take profit logic, if any, to manage the position. Because take profit and stop loss configuration are independent, the user can construct different profiles, such as pure trend-change exits on both sides, pure overextension exits, or a mix (for example, take profit on overextension and stop loss on trend reversal).

This strategy is designed as an analytical and backtesting framework rather than a finished plug-and-play trading system. It does not include position sizing, risk-per-trade controls, multi-timeframe confirmation, volatility filters or instrument-specific fine-tuning. Its primary purpose is to provide a clear, rule-based structure for testing retracement logic within RSI-defined trends, and to allow users to explore how different exit regimes (trend-change based versus extension based) affect performance on their instruments and timeframes of interest.

Nothing in this script or its description should be interpreted as financial advice, investment recommendation or solicitation to buy or sell any financial instrument. Past performance on backtests does not guarantee future results. The behaviour of this strategy can vary significantly across symbols, timeframes and market conditions, and correlations, volatility and liquidity can change without warning. Before considering any live application, users should thoroughly backtest and forward test the strategy on their own data, adjust parameters to their risk profile and instrument characteristics, and integrate proper money management and trade management rules. Use of this script is entirely at the user’s own risk.

RSI Strategy [PrimeAutomation]⯁ OVERVIEW

The RSI Strategy is a momentum-driven trading system built around the behavior of the Relative Strength Index (RSI).

Instead of using traditional overbought/oversold zones, this strategy focuses on RSI breakouts with volatility-based trailing stops, adaptive profit-targets, and optional early-exit logic.

It is designed to capture strong continuation moves after momentum shifts while protecting trades using ATR-based dynamic risk management.

⯁ CONCEPTS

RSI Breakout Momentum: Entries happen when RSI breaks above/below custom thresholds, signaling a shift in momentum rather than mean reversion.

Volatility-Adjusted Risk: ATR defines both stop-loss and profit-target distances, scaling positions based on market volatility.

Dynamic Trailing Stop: The strategy maintains an adaptive trailing level that tightens as price moves in the trade’s favor.

Single-Position System: Only one trade at a time (no pyramiding), maximizing clarity and simplifying execution.

⯁ KEY FEATURES

RSI Signal Engine

• Long when RSI crosses above Upper threshold

• Short when RSI crosses below Lower threshold

These levels are configurable and optimized for trend-momentum detection.

ATR-Based Stop-Loss

A custom ATR multiplier defines the initial stop.

• Long stop = price – ATR × multiplier

• Short stop = price + ATR × multiplier

Stops adjust continuously using a trailing model.

ATR-Based Take Profit (Optional)

Profit targets scale with volatility.

• Long TP = entry + ATR × TP-multiplier

• Short TP = entry – ATR × TP-multiplier

Users can disable TP and rely solely on trailing stops.

Real-Time Trailing Logic

The stop updates bar-by-bar:

• In a long trade → stop moves upward only

• In a short trade → stop moves downward only

This keeps the stop tight as trends develop.

Early Exit Module (Optional)

After X bars in a trade, opposite RSI signals trigger exit.

This reduces holding time during weak follow-through phases.

Full Visual Layer

• RSI plotted with threshold fills

• Entry/TP/Stop visual lines

• Color-coded zones for clarity

⯁ HOW TO USE

Look for RSI Breakouts:

Focus on RSI crossing above the upper boundary (long) or below the lower boundary (short). These moments identify fresh momentum surges.

Use ATR Levels to Manage Risk:

Because stops and targets scale with volatility, the strategy adapts well to both quiet and explosive market phases.

Monitor Trailing Stops for Trend Continuation:

The trailing stop is the primary driver of exits—often outperforming fixed targets by catching larger runs.

Use on Liquid Markets & Mid-Higher Timeframes:

The system performs best where RSI and ATR signals are clean—crypto majors, FX, and indices.

⯁ CONCLUSION

The RSI Strategy is a modern RSI breakout system enhanced with volatility-adaptive risk management and flexible exit logic. It is designed for traders who prefer momentum confirmation over mean reversion, offering a disciplined framework with robust protections and dynamic trend-following capability.

Its blend of ATR-based stops, optional profit targets, and RSI-driven entries makes it a reliable strategy across a wide range of market conditions.

BTC 30 m Long singal Asset: Bitcoin only

Timeframe: 30 minutes

Entry Conditions (Long):

MACD histogram turns from red to green (negative to positive)

Stochastic K line crosses above D line AND this crossover happens below the lower band (20)

RSI is above the middle band (50)

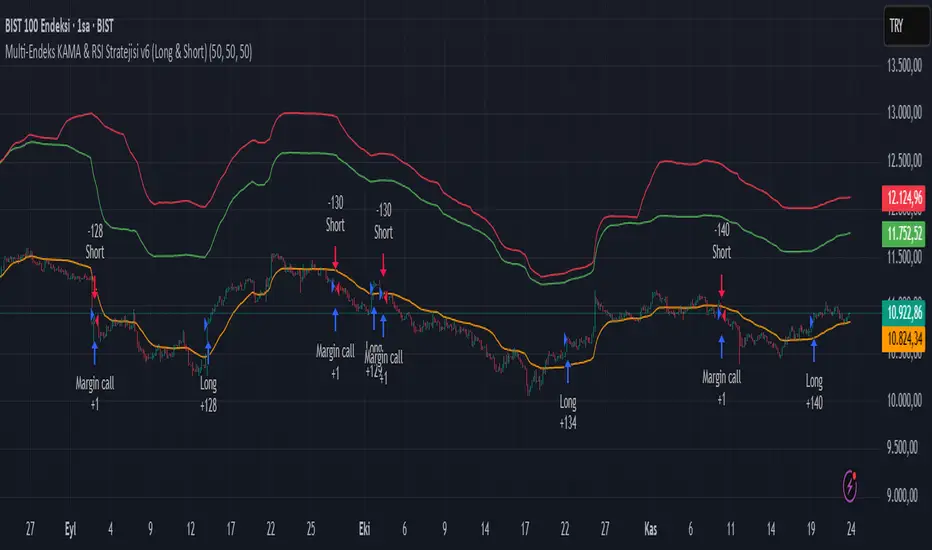

Multi-Endeks KAMA & RSI Stratejisi v6 (Long & Short)Multi-Index KAMA & RSI Strategy v6 (Long & Short)

This is a hybrid trading strategy that combines two powerful technical analysis tools—the Kaufman's Adaptive Moving Average (KAMA) for trend following and the Relative Strength Index (RSI) for measuring momentum and identifying overbought/oversold conditions.

The term "Multi-Index" suggests that the decision-making process might incorporate data or conditions from several different market indices or timeframes, rather than just the single asset being traded.

🧭 Core Components

1. KAMA (Kaufman's Adaptive Moving Average)

KAMA is an adaptive moving average developed by quantitative financial theorist Perry J. Kaufman.

Adaptivity: Unlike standard moving averages, KAMA automatically adjusts its smoothing factor (speed) based on market volatility.

Mechanism:

Trending Markets (Low Noise): When prices move clearly in one direction (low volatility), KAMA speeds up, hugging the price closely and providing fast signals.

Sideways Markets (High Noise): When prices are choppy (high volatility/noise), KAMA slows down, smoothing out price fluctuations to reduce the risk of whipsaws (false signals).

Role in Strategy: To define the main trend direction. The position of the price relative to the KAMA line determines the base directional bias (Long or Short).

2. RSI (Relative Strength Index)

RSI is a momentum oscillator developed by J. Welles Wilder Jr. that measures the speed and change of price movements.

Overbought/Oversold: It oscillates between 0 and 100. Conventionally, a reading above 70 suggests overbought conditions (potential sell signal), and a reading below 30 suggests oversold conditions (potential buy signal).

Role in Strategy: Timing and Confirmation. Once the trend is confirmed by KAMA, the RSI acts as a timing filter, often confirming an entry as it moves away from extreme overbought (for Short) or oversold (for Long) levels.

📉 Potential Trading Logic (V6)

This "v6" strategy likely aims to capture more reliable entries by requiring both trend (KAMA) and momentum (RSI) alignment:

1. LONG (Buy) Entry Conditions

Trend Confirmation (KAMA): The asset's price (Closing Price) must be above the KAMA line (confirming an uptrend).

Momentum Confirmation (RSI):

Option A (Reversal): The RSI must cross above the 30 level (exiting oversold) or decisively move above the 50 level.

Option B (Trend-Continuation): In a strong uptrend, the RSI might bounce off the 40-50 zone and turn upwards, confirming trend continuation.

2. SHORT (Sell) Entry Conditions

Trend Confirmation (KAMA): The asset's price (Closing Price) must be below the KAMA line (confirming a downtrend).

Momentum Confirmation (RSI):

Option A (Reversal): The RSI must cross below the 70 level (exiting overbought) or decisively move below the 50 level.

Option B (Trend-Continuation): In a strong downtrend, the RSI might be rejected from the 50-60 zone and turn downwards, confirming continuation.

3. Exit Management

The strategy likely utilizes dynamic risk controls:

Stop-Loss: A dynamic stop placed on the opposite side of the KAMA, or an ATR-based distance to adjust to volatility.

Take-Profit: Conditions such as the RSI reaching extreme levels or the KAMA line being crossed in the reverse direction.

🌟 Implication of the "V6" Version

The "v6" designation implies that the strategy has been refined and iterated upon over time to address weaknesses in prior versions (v1, v2, etc.). These improvements might include:

Filters: Adding stricter RSI or KAMA cross filters to reduce false signals.

Multi-Index Logic: Using the RSI or KAMA of a secondary instrument (e.g., a major index or volatility measure) as a macro filter for the main trade execution.

Optimization: Optimizing the default lookback periods for KAMA and RSI for different asset classes.

RSI + 55 EMA + Volume (SL Marked, No Engulfing)This is to help entering in trades by considering 50 EMA and RSI indicators, Volume is used for confirmations

ATR Trend + RSI Pullback Strategy [Profit-Focused]This strategy is designed to catch high-probability pullbacks during strong trends using a combination of ATR-based volatility filters, RSI exhaustion levels, and a trend-following entry model.

Strategy Logic

Rather than relying on lagging crossovers, this model waits for RSI to dip into oversold zones (below 40) while price remains above a long-term EMA (default: 200). This setup captures pullbacks in strong uptrends, allowing traders to enter early in a move while controlling risk dynamically.

To avoid entries during low-volatility conditions or sideways price action, it applies a minimum ATR filter. The ATR also defines both the stop-loss and take-profit levels, allowing the model to adapt to changing market conditions.

Exit logic includes:

A take-profit at 3× the ATR distance

A stop-loss at 1.5× the ATR distance

An optional early exit if RSI crosses above 70, signaling overbought conditions

Technical Details

Trend Filter: 200 EMA – must be rising and price must be above it

Entry Signal: RSI dips below 40 during an uptrend

Volatility Filter: ATR must be above a user-defined minimum threshold

Stop-Loss: 1.5× ATR below entry price

Take-Profit: 3.0× ATR above entry price

Exit on Overbought: RSI > 70 (optional early exit)

Backtest Settings

Initial Capital: $10,000

Position Sizing: 5% of equity per trade

Slippage: 1 tick

Commission: 0.075% per trade

Trade Direction: Long only

Timeframes Tested: 15m, 1H, and 30m on trending assets like BTCUSD, NAS100, ETHUSD

This model is tuned for positive P&L across trending environments and volatile markets.

Educational Use Only

This strategy is for educational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Always validate performance on multiple markets and timeframes before using it in live trading.

Bank nifty with RSI + SMA (Bli-Rik)best to trade for 100 points on 15 mins time frame, very rarly fails

KDH v2.0 (English) Trading Strategy Indicator# KDH Diamond Strategy v3.3 - TradingView Description

---

## 🇬🇧 ENGLISH VERSION

### 📊 KDH Diamond Strategy v3.3

**Professional High-Leverage Futures Trading System**

---

#### 🎯 Overview

KDH Diamond is an advanced algorithmic trading strategy specifically optimized for **1-hour timeframe futures trading** with high-leverage environments. Built on proven institutional concepts including Fair Value Gaps (FVG), Volume Profile analysis, and multi-layered confirmation filters, this strategy delivers consistent results without repainting.

---

#### ✨ Key Features

**🔥 Optimized for 1H Timeframe**

- Extensively backtested across multiple markets

- Highest profit rate achieved on 1-hour charts

- Perfect for swing traders and active position management

**🎨 No Repainting - 100% Reliable Signals**

- All signals are confirmed and locked on bar close

- What you see in backtest is what you get in real-time

- Complete transparency with `calc_on_order_fills=true`

**💎 Automated Risk Management**

- Automatic Stop Loss and Take Profit calculation

- Intelligent SL/TP placement based on market structure

- Built-in position sizing controls (adjustable % per trade)

**🚀 High-Leverage Futures Optimized**

- Designed specifically for leveraged futures trading

- Risk-reward ratios calibrated for 10-20x leverage environments

- Precision entry timing to maximize profit potential

**🔄 Advanced Position Management**

- Automatic reversal entries at TP levels

- Multiple re-entry opportunities per signal

- Dynamic trade management based on market conditions

**🎛️ Multi-Layer Confirmation System**

- **SMA50 Filter (1H)**: Trend alignment confirmation

- **Momentum Filter**: KAMA-based directional strength

- **RSI Divergence Filter**: Reversal detection at extremes

- **Volume Profile Filter**: Order flow and liquidity analysis

---

#### 📈 How It Works

**Signal Generation**

The strategy identifies **Inverted Fair Value Gaps (IFVG)** - institutional order blocks that signal high-probability reversal or continuation zones. Each signal is validated through multiple confirmation filters before execution.

**Entry Logic**

- Limit orders placed at optimal price levels within FVG zones

- Price must touch the midline and close in favorable direction

- All filters must align for signal activation

**Exit Strategy**

- Stop Loss: Placed at the next opposing FVG level

- Take Profit: Calculated using nearest FVG in profit direction

- Automatic reversal entry option at TP levels

**Visual System**

- Color-coded boxes show FVG zones (green/red)

- Real-time position tracking with entry, SL, and TP lines

- Comprehensive dashboard displaying filter status and P&L

---

#### 🎯 Who Is This For?

✅ **Perfect For:**

- Futures traders using 10-20x leverage

- Traders seeking systematic, rule-based strategies

- Those who want automated SL/TP management

- 1-hour chart swing traders

- Traders familiar with institutional concepts (FVG, order flow)

❌ **Not Ideal For:**

- Scalpers (designed for 1H timeframe)

- Spot-only traders (optimized for leveraged futures)

- Beginners unfamiliar with leverage risks

- Set-and-forget automated trading (requires monitoring)

---

#### 📊 What You Get

**Strategy Features:**

- Complete FVG detection and inversion system

- 4 professional-grade confirmation filters

- Automated SL/TP calculation and placement

- TP reversal entry system

- Volume Profile sentiment analysis

- Real-time position tracking dashboard

- Webhook alert support for automation

- Clean, organized code with detailed comments

**Visual Components:**

- FVG boxes with inversion coloring

- Volume Profile sentiment boxes (optional)

- Entry, SL, and TP lines for each position

- Position status table with live P&L

- Filter status dashboard

---

#### ⚙️ Customization Options

**Adjustable Filters (User Control):**

- SMA50 Filter (1H) - Trend alignment ON/OFF

- Momentum Filter - Directional strength ON/OFF

- RSI Divergence Filter - Reversal detection ON/OFF

- Volume Profile Filter - Order flow analysis ON/OFF

**Fixed Parameters (Optimized):**

- All core parameters are pre-optimized for 1H timeframe

- Ensures consistent performance without overwhelming options

- Prevents parameter over-fitting by users

---

#### ⚠️ Important Disclaimers

**Risk Warning:**

This strategy is designed for leveraged futures trading, which carries substantial risk. High leverage (10-20x) can result in rapid losses. Only trade with capital you can afford to lose.

**Performance:**

Past performance does not guarantee future results. Always backtest on your specific market and timeframe before live trading.

**Usage:**

This is a trading tool, not financial advice. Users are responsible for their own trading decisions and risk management.

**Requirements:**

- Understanding of futures trading and leverage

- Familiarity with Fair Value Gaps and institutional concepts

- Ability to monitor positions (not fully automated)

- Proper risk management discipline

---

#### 🔧 Technical Specifications

- **Platform:** TradingView Pine Script v5

- **Type:** Strategy (with backtesting capabilities)

- **Timeframe:** Optimized for 1H (works on other timeframes)

- **Markets:** Any futures market (crypto, stocks, indices, forex)

- **Repainting:** NO - All signals are final on bar close

- **Alerts:** Full webhook support for automation

- **Default Settings:** 10% position size, pyramiding enabled (max 10 positions)

---

#### 📞 Support

Questions about setup or usage? Contact the author through TradingView messages.

**Note:** This indicator is for educational and trading tool purposes only. The author is not responsible for trading losses. Trade responsibly and within your risk tolerance.

EMA Cross + RSI + ADX - Autotrade Strategy V2Overview

A versatile trend-following strategy combining EMA 9/21 crossovers with RSI momentum filtering and optional ADX trend strength confirmation. Designed for both cryptocurrency and traditional futures/options markets with built-in stop loss management and automated position reversals.

Key Features

Multi-Market Compatibility: Works on both crypto futures (Bitcoin, Ethereum) and traditional markets (NIFTY, Bank NIFTY, S&P 500 futures, equity options)

Triple Confirmation System: EMA crossover + RSI filter + ADX strength (optional)

Automated Risk Management: 2% stop loss with wick-touch detection

Position Auto-Reversal: Opposite signals automatically close and reverse positions

Webhook Ready: Six distinct alert messages for automation (Entry Buy/Sell, Close Long/Short, SL Hit Long/Short)

Performance Metrics

NIFTY Futures (15min): 50%+ win rate with ADX filter OFF

Crypto Markets: Requires extensive backtesting before live deployment

Optimal Timeframes: 15-minute to 1-hour charts (patience required for higher timeframes)

Strategy Logic

Entry Signals:

LONG: EMA 9 crosses above EMA 21 + RSI > 55 + ADX > 20 (if enabled)

SHORT: EMA 9 crosses below EMA 21 + RSI < 45 + ADX > 20 (if enabled)

Exit Signals:

Opposite EMA crossover (auto-closes current position)

Stop loss hit at 2% from entry price (tracks candle wicks)

Technical Indicators:

Fast EMA: 9-period (short-term trend)

Slow EMA: 21-period (primary trend)

RSI: 14-period with 55/45 thresholds (momentum confirmation)

ADX: 14-period with 20 threshold (trend strength filter - optional)

Market-Specific Settings

Traditional Markets (NIFTY, Bank NIFTY, S&P Futures, Options)

Recommended Settings:

ADX Filter: Turn OFF (less choppy, cleaner trends)

Timeframe: 15-minute chart

Win Rate: 50%+ on NIFTY Futures

Why No ADX: Traditional markets have more institutional participation and smoother price action, making ADX unnecessary

Cryptocurrency Markets (BTC, ETH, Altcoins)

Recommended Settings:

ADX Filter: Turn ON (ADX > 20)

Timeframe: 15-minute to 1-hour

Extensive backtesting required before live trading

Why ADX: Crypto markets are highly volatile and prone to false breakouts; ADX filters low-quality chop

Best Practices

✅ Backtest thoroughly on your specific instrument and timeframe

✅ Use larger timeframes (1H, 4H) for higher quality signals and better risk/reward

✅ Adjust RSI thresholds based on market volatility (try 52/48 for more signals, 60/40 for fewer but stronger)

✅ Monitor ADX effectiveness - disable for traditional markets, enable for crypto

✅ Proper position sizing - adjust default_qty_value based on your capital and instrument price

✅ Paper trade first - test for 2-4 weeks before risking real capital

Risk Management

Fixed 2% stop loss per trade (adjustable)

Stop loss tracks candle wicks for accurate execution

Positions auto-reverse on opposite signals (no manual intervention needed)

0.075% commission built into backtest (adjust for your broker)

Customization Options

All parameters are adjustable via inputs:

EMA periods (default: 9/21)

RSI length and thresholds (default: 14-period, 55/45 levels)

ADX length and threshold (default: 14-period, 20 threshold)

Stop loss percentage (default: 2%)

Webhook Automation

This strategy includes six distinct alert messages for automated trading:

"Entry Buy" - Long position opened

"Entry Sell" - Short position opened

"Close Long" - Long position closed on opposite crossover

"Close Short" - Short position closed on opposite crossover

"SL Hit Long" - Long stop loss triggered

"SL Hit Short" - Short stop loss triggered

Compatible with Delta Exchange, Binance Futures, 3Commas, Alertatron, and other webhook platforms.

Important Notes

⚠️ Crypto markets require extensive backtesting - volatility patterns differ significantly from traditional markets

⚠️ Higher timeframes = better results - 15min works but 1H/4H provide cleaner signals

⚠️ ADX toggle is critical - OFF for traditional markets, ON for crypto

⚠️ Not financial advice - always conduct your own research and use proper risk management

⚠️ Past performance ≠ future results - backtest results may not reflect live trading conditions

Disclaimer

This strategy is for educational and informational purposes only. Trading futures and options involves substantial risk of loss. Always backtest thoroughly, start with paper trading, and never risk more than you can afford to lose. The author assumes no responsibility for any trading losses incurred using this strategy.

3-Minute RSI and EMA Crossover Strategy 3-Minute RSI and EMA Crossover Sell Strategy with Exit Conditions and Re-entry

RSI + MACD Multi-Timeframe StrategyThis strategy combines the Relative Strength Index (RSI) from the daily timeframe with the Moving Average Convergence Divergence (MACD) from the 4-hour timeframe to generate precise long entry and exit signals.

The system uses a multi-timeframe approach to align longer-term trend conditions with shorter-term momentum shifts — allowing traders to catch dips with confirmation and exit before reversals.

🧠 Strategy Logic

✅ Long Entry Condition:

- RSI on the daily (1D) timeframe is oversold (below your defined threshold)

- MACD on the 4H timeframe crosses above the signal line

→ A long trade is opened when these two align

✅ Long Exit Condition:

- RSI on the daily timeframe is overbought

- MACD on the 4H timeframe crosses below the signal line

→ The long trade is closed when these two conditions are met

💡 This strategy currently supports long entries only. Short logic can be added if needed.

📊 Indicator Components

🔹 RSI (Relative Strength Index):

- A momentum oscillator that measures the speed and magnitude of price changes.

- Helps identify overbought (potential sell) and oversold (potential buy) conditions.

- Applied on the 1D timeframe (by default) to reflect broader market trend or exhaustion levels.

🔹 MACD (Moving Average Convergence Divergence):

- A trend-following momentum indicator based on moving averages.

- The MACD Line (fast EMA - slow EMA) crossing above the Signal Line indicates bullish momentum.

- Used here on the 4-hour timeframe (by default) for shorter-term momentum confirmation.

🔹 Multi-Timeframe (MTF) Logic:

- Uses request.security() to pull higher timeframe data (1D for RSI, 4H for MACD).

- Ensures no repainting, as it only uses closed candles from the higher timeframe.

- Aligns longer-term signals with shorter-term entries, reducing false signals.

📈 Plotting Options

The script includes a plot selector input allowing you to toggle between:

- RSI Plot (with overbought/oversold lines)

- MACD Plot (MACD line and signal line)

- This helps visualize signal conditions clearly on your chart.

🛠 Customization

- RSI & MACD settings are fully configurable

- RSI and MACD timeframes can be adjusted independently

⚠️ Disclaimer

This strategy is provided for educational and informational purposes only.

It is not financial advice or a recommendation to buy or sell any asset.

Past performance does not guarantee future results. Always test strategies in a simulated environment before live use, and consult with a licensed financial advisor for investment decisions.

Sniper StrategyThe Sniper Strategy is a clean and data-driven RSI-based system designed for precision entries and exits.

It combines multi-timeframe RSI analysis, automated labeling, and dynamic P/L tracking — perfect for traders who want clarity, visual feedback, and strict risk control in one tool.

🧩 Core Features

Dual RSI Framework:

Calculates both the current timeframe RSI and a higher timeframe RSI to confirm trend strength and avoid false signals.

Smart Entry Logic:

Long signals when RSI drops below oversold level.

Short signals when RSI exceeds overbought level.

Automatic Exit Management:

Configurable Stop Loss and Take Profit percentages.

Optional RSI-based exit for flexible trade closures.

All exits are visually labeled for transparency.

Real-Time Profit Tracking:

Displays a floating label above each bar showing current P/L (%), updated live while the position is open — giving you instant insight into trade performance.

Clean Visual Design:

Uses arrows and colored labels for entry/exit clarity.

Optional RSI line and higher timeframe RSI plot included.

Alerts Ready:

Built-in alert conditions for both Long and Short signals — ideal for automation or notifications.

⚙️ Inputs & Customization

Adjustable RSI lengths for both timeframes.

Selectable RSI source (Close, HL2, etc.).

Configurable stop loss and take profit levels.

Customizable leverage and precision for P/L display.

Optional wick-based calculation for sensitivity tuning.

💡 How to Use

Apply the strategy on your preferred symbol and timeframe.

Adjust RSI and risk settings to match your trading style.

Optionally enable higher timeframe RSI confirmation.

Set alerts for “Long Entry Signal” and “Short Entry Signal.”

Backtest and fine-tune before going live.

⚠️ Disclaimer

This script is for educational and research purposes only.

It is not financial advice. Always backtest thoroughly and manage your risk before using it in live trading.

Quantura - Quantified Price Action StrategyIntroduction

“Quantura – Quantified Price Action Strategy” is an invite-only Pine Script strategy designed to combine multiple price action concepts into a single trading framework. It integrates supply and demand zones, liquidity sweeps and runs, fair value gaps (FVGs), RSI filters, and EMA trend confirmation. The strategy also provides a visual overlay with dynamic trend-colored candles for easier chart interpretation. It is intended for multi-market use across cryptocurrencies, Forex, equities, and indices.

Originality & Value

The strategy is original in how it unifies several institutional-style price action elements and validates trades only when they align. This reduces noise compared to using single indicators in isolation. Its unique value lies in the combination of:

Supply & Demand detection: Dynamic boxes identified through pivots, ATR, and volume sensitivity.

Liquidity sweeps and runs: Detects when swing highs/lows are broken and retested, distinguishing between liquidity grabs (sweeps) and directional runs.

RSI filter: Can be set to normal or aggressive, confirming momentum before trades.

Fair Value Gaps (FVGs): Optional detection and filtering of price inefficiencies.

EMA filter: Aligns trades with the broader market trend.

Trend candle visualization: Candles dynamically colored bullish, bearish, or neutral, based on strategy positions.

This layered confluence approach ensures that entries are not taken on a single condition but require agreement across several dimensions of market structure, momentum, and order flow.

Functionality & Indicators

Supply & Demand Zones: Zones are created when pivots, ATR sensitivity, and volume thresholds overlap.

Liquidity: Swing highs and lows are tracked, with options for sweep (fakeout/reversal) or run (continuation) detection.

RSI: Confirms long signals when oversold and shorts when overbought, with configurable aggressiveness.

FVG filter: Adds validation by requiring price interaction with inefficiency zones.

EMA filter: Ensures longs are above EMA and shorts below EMA.

Signals & Visualization: Trade entries are marked on the chart, while candles change color to reflect trade direction and status.

Parameters & Customization

Supply & Demand: Sensitivity (swing range, volume multiplier, ATR multiplier) and display options.

Liquidity filter: Mode (Run or Sweep), display, and swing length.

RSI: Enable/disable, length, and style (normal or aggressive).

Fair Value Gaps: Sensitivity via ATR factor, optional volume filter, and display toggles.

EMA: Length, enable/disable, and visualization.

Risk management: Up to three configurable take-profit levels, stop-loss, break-even logic, and capital-based position sizing.

Visualization: Custom candle coloring and optional overlay for better clarity.

Default Properties (Strategy Settings)

Initial Capital: 10,000 USD

Position Size: 100% of equity per trade (backtest default)

Commission: 0.1%

Slippage: 1

Pyramiding: 0 (only one position at a time)

Note: The default of 100% equity per trade is used for testing purposes only and would not be sustainable in real trading. A typical allocation in practice would be between 1–5% of account equity per trade, sometimes up to 10%.

Backtesting & Performance

Backtests on XPTUSD over 2.5 years with the default settings produced:

164 trades

67.68% win rate

Profit factor: 1.7

Maximum drawdown: 27.81%

These results show how the confluence of supply/demand, liquidity, and RSI filters can produce robust setups. However, past performance does not guarantee future results. While the trade count (164) is sufficient for statistical analysis, results may vary across markets and timeframes.

Risk Management

Three configurable take-profit levels with percentage allocation.

Initial stop-loss based on user-defined percentage.

Dynamic stop-loss that adjusts with market movement.

Break-even logic that shifts stops to entry after predefined gains.

Position sizing based on risk percentage of equity.

This framework allows both conservative and aggressive configurations, depending on user preference.

Limitations & Market Conditions

Works best in volatile and liquid markets such as crypto, metals, indices, and FX.

May produce false signals in low-volume or sideways environments.

Unexpected news or macro events can override technical conditions.

Default position sizing of 100% equity is highly aggressive and should be reduced before any practical use.

Usage Guide

Add “Quantura – Quantified Price Action Strategy” to your chart.

Select Supply & Demand, Liquidity, RSI, EMA, and FVG settings according to your market and timeframe.

Configure risk management: take-profits, stop-loss, and risk-per-trade percentage.

Use the Strategy Tester to analyze statistics, equity curve, and performance under different conditions.

Optimize parameters before applying the strategy to different markets.

Author & Access

Developed 100% by Quantura. Published as an Invite-Only script.

Important

This description complies with TradingView’s publishing rules. It clarifies originality, explains the underlying logic, discloses default properties, and presents backtest results with realistic disclaimers.

Quantura - Quantitative AlgorythmIntroduction

“Quantura – Quantitative Algorithm” is an invite-only Pine Script strategy designed for multi-timeframe analysis, combining technical filters with user-adjustable fundamental sentiment. It was primarily developed for cryptocurrency markets but can also be applied across other assets such as Forex, stocks, and indices. The goal is to generate structured trade signals through a confluence of techniques rather than relying on a single indicator.

Originality & Value

Quantura is not a simple mashup of indicators. Its originality comes from how multiple layers of analysis are integrated into a single decision framework . Instead of showing indicators separately, the strategy only issues trades when several conditions align simultaneously:

RSI entry triggers confirm overbought/oversold reversals.

Market structure on a higher timeframe confirms trend direction.

Order block detection highlights zones of concentrated supply and demand.

Premium/Discount zones identify potential over- and undervaluation.

HTF EMA provides trend confirmation.

Optional candlestick patterns strengthen reversal or continuation signals.

An optional correlation filter compares the main asset to a reference instrument.

This design forces agreement between different methodologies (momentum, structure, value, volume, sentiment), which reduces noise compared to using them in isolation.

Functionality & Indicators

Entry trigger: RSI exits from extreme zones.

Filters: Only valid when all selected filters (HTF structure, EMA, order blocks, premium/discount, candlesticks, correlation, volume) confirm the direction.

Fundamental bias: User-defined sentiment and analysis settings (bullish, bearish, neutral) influence whether long or short trades are permitted.

Exits: ATR-based take profit and stop loss, with optional breakeven, opposite-signal exit, and session-end exit.

Visualization: Buy/Sell markers, trend-colored candles, and an optional dashboard summarizing indicator status.

Parameters & Customization

Timeframes: Independent HTF and LTF selection.

Trading direction: Long / Short / Both.

Session and weekday filters.

RSI length and thresholds.

Filters: HTF structure, order blocks, premium/discount, EMA, candlestick, ATR volatility, volume zones, correlation.

Exit rules: ATR multipliers for TP/SL, breakeven logic, session-end exit, opposite-signal exit.

Visuals: Toggle signals, candles, dashboard, custom colors.

Default Properties (Strategy Settings)

Initial Capital: 100,000 USD

Position Size: 15% of equity per trade

Commission: 0.25%

Slippage: enabled

Pyramiding: 0 (one position at a time)

Note: The position sizing of 15% equity per trade is intentionally set for backtesting demonstration. In real trading, risking this much is considered aggressive. Most traders prefer to risk 1-5% of equity, and rarely above 10%.

Backtesting & Performance

Backtests on BTCUSD (2 years) with the above defaults showed:

112 trades

Win rate: 40%

Profit factor: 1.4

Maximum drawdown: 34%

These results illustrate how the confluence model behaves, but they are not predictive of future performance . The trade sample size (72 trades) is below the 100+ usually recommended for statistical robustness. Users should re-test with their own preferred symbols, settings, and timeframes.

Risk Management

ATR-based stops and targets scale with volatility.

Commission and slippage are included by default for realistic modeling.

Opposite-signal exit helps capture trend reversals.

Session-end exit can close intraday positions before illiquid hours.

Breakeven option protects profits when available.

Although the default allocation uses 15% per trade for demonstration, this is not a recommendation. Users are encouraged to adjust risk sizing downwards to sustainable levels (commonly 1-5%).

Limitations & Market Conditions

Performs best in volatile, liquid markets (e.g., crypto).

May struggle in prolonged sideways markets with low volatility.

News events and fundamentals outside user inputs can override signals.

Backtests below 100 trades should be considered exploratory, not statistically conclusive.

Usage Guide

Add “Quantura – Quantitative Algorithm” to your chart in strategy mode.

Select HTF and LTF timeframes, trading direction, and session filters.

Configure confluence filters (structure, EMA, order blocks, premium/discount, candlestick, correlation, volume).

Set sentiment and analysis bias in fundamental settings.

Adjust ATR multipliers and exits.

Review buy/sell signals and analyze performance in the Strategy Tester.

Author & Access

Developed 100% by Quantura . Distributed as an Invite-Only script . Details are provided in the Author’s Instructions field.

Important: This description complies with TradingView’s Script Publishing Rules and House Rules. It does not guarantee profitability, avoids unrealistic claims, and explains how the strategy integrates multiple methods into a coherent decision framework.

Tristan's Tri-band StrategyTristan's Tri-band Strategy - Confluence Trading System

Strategy Overview:

This strategy combines three powerful technical indicators - RSI, Williams %R, and Bollinger Bands - into a single visual trading system. Instead of cluttering your chart with separate indicator panels, all signals are displayed directly on the price chart using color-coded gradient overlays, making it easy to spot high-probability trade setups at a glance.

How It Works:

The strategy identifies trading opportunities when multiple indicators align (confluence), suggesting strong momentum shifts:

📈 Long Entry Signals:

RSI drops to 30 or below (oversold)

Williams %R reaches -80 to -100 range (oversold)

Price touches or breaks below the lower Bollinger Band

All three conditions must align during your selected trading session

📉 Short Entry Signals:

RSI rises to 70 or above (overbought)

Williams %R reaches 0 to -20 range (overbought)

Price touches or breaks above the upper Bollinger Band

All three conditions must align during your selected trading session

Visual Indicators:

(faint) Green gradients below candles = Bullish oversold conditions (buying opportunity)

(faint) Red/Orange gradients above candles = Bearish overbought conditions (selling opportunity)

Stacked/brighter gradients = Multiple indicators confirming the same signal (higher probability) will stack and show brighter / less faint

Blue Bollinger Bands = Volatility boundaries and mean reversion zones

Exit Strategy:

Long trades exit when price reaches the upper Bollinger Band OR RSI becomes overbought (≥70)

Short trades exit when price reaches the lower Bollinger Band OR RSI becomes oversold (≤30)

Key Features:

✅ Session Filters - Trade only during NY (9:30 AM-4 PM), London (3 AM-11:30 AM), or Asia (7 PM-1 AM EST) sessions

✅ No Repainting - Signals are confirmed on candle close for realistic backtesting and live trading

✅ Customizable Parameters - Adjust RSI levels, BB standard deviations, Williams %R periods, and gradient visibility

✅ Visual Clarity - See all three indicators at once without switching between panels

✅ Built-in Alerts - Get notified when entry and exit conditions are met

How to Use Effectively:

Choose Your Trading Session - For day trading US stocks, enable only the NY session. For forex or 24-hour markets, select the sessions that match your schedule.

Look for Gradient Stacking - The brightest, most visible gradients occur when both RSI and Williams %R signal together. These are your highest-probability setups.

Confirm with Price Action - Wait for the candle to close before entering. The strategy enters on the next bar's open to prevent repainting.

Respect the Bollinger Bands - Entries occur at the outer bands (price extremes), and exits occur at the opposite band or when momentum reverses.

Backtest First - Test the strategy on your preferred instruments and timeframes. Works best on liquid assets with clear trends and mean reversion patterns (stocks, major forex pairs, indices).

Adjust Gradient Visibility - Use the "Gradient Strength" slider (lower = more visible) to make signals stand out on your chart style.

Best Timeframes: 5-minute to 1-hour charts for intraday trading; 4-hour to daily for swing trading (I have also found the 3 hour timeframe to work really well for some stocks / ETFs.)

Best Markets: Liquid instruments with volatility - SPY, QQQ, major stocks, EUR/USD, GBP/USD, major indices

Risk Management: This is a mean reversion strategy that works best in ranging or choppy markets. In strong trends, signals may appear less frequently. Always use proper position sizing and stop losses based on your risk tolerance.

----------------------------------------------

Note: Past performance does not guarantee future results. This strategy is provided for educational purposes. Always backtest thoroughly and practice proper risk management before live trading.RetryClaude can make mistakes. Please double-check responses. Sonnet 4.5