NUPL - Net Unrealized Profit-Loss BTC Tops/Bottoms [Logue]Net Unrealized Profit Loss (NUPL) - The NUPL measures the profit state of the bitcoin network to determine if past transfers of BTC are currently in an unrealized profit or loss state.

Values above zero indicate that the network is in overall profit, while values below zero indicate the network is in overall loss. Highly positive NUPL values indicate overvaluation of the BTC network and relatively negative NUPL values indicate an undervaluation of the BTC network.

For tops: The default setting for tops is based on decreasing "strength" of BTC tops. A decreasing linear function (trigger = slope * time + intercept) was fit to past cycle tops for this indicator and is used as the default to signal macro tops. The user can change the slope and intercept of the line by changing the slope and/or intercept factor. The user also has the option to indicate tops based on a horizontal line via a settings selection. This horizontal line default value is 73. This indicator is triggered for a top when the NUPL is above the trigger value.

For bottoms: Bottoms are displayed based on a horizontal line with a default setting of -13. The indicator is triggered for a bottom when the NUPL is below the bottom trigger value.

Search in scripts for "Cycle"

LMACD - Logarithmic MACD Weekly BTC Index [Logue]Logarithmic Moving Average Convergence Divergence (LMACD) Weekly Indicator - The LMACD is a momentum indicator that measures the strength of a trend using 12-period and 26-period moving averages. The weekly LMACD for this indicator is calculated by determining the difference between the log (base 10) of the 12-week and 26-week exponential moving averages. Larger positive numbers indicate a larger positive momentum.

For tops: The default setting for tops is based on decreasing "strength" of BTC tops. A decreasing linear function (trigger = slope * time + intercept) was fit to past cycle tops for this indicator and is used as the default to signal macro tops. The user can change the slope and intercept of the line by changing the slope and/or intercept factor. The user also has the option to indicate tops based on a horizontal line via a settings selection. This line default value is 0.125. This indicator is triggered for a top when the LMACD is above the trigger value.

For bottoms: Bottoms are displayed based on a horizontal line with a default setting of -0.07. The indicator is triggered for a bottom when the LMACD is below the bottom trigger value.

MCG - Meme Coin Gains [Logue]Meme Coin Gains. Investor preference for meme coin trading may signal irrational exuberance in the crypto market. If a large spike in meme coin gains is observed, a top may be near. Therefore, the gains of the most popular meme coins (DOGE, SHIB, SATS, ORDI, BONK, PEPE, and FLOKI) were averaged together in this indicator to help indicate potential mania phases, which may signal nearing of a top. Two simple moving averages of the meme coin gains are used to smooth the data and help visualize changes in trend. In back testing, I found a 10-day "fast" sma and a 20-day "slow" sma of the meme coin gains works well to signal tops and bottoms when extreme values of this indicator are reached.

Meme coins were not traded heavily prior to 2020. Therefore, there is only one cycle to test at the time of initial publication. Also, the meme coin space moves fast, so more meme coins may need to be added later. Also, once a meme coin has finished its mania phase where everyone and their mother has heard of it, it doesn't seem to run again (at least with the data up until time of publication). Therefore, the value of this indicator may not be great unless it is updated frequently.

The two moving averages are plotted. For the indicator, top and bottom "slow" sma trigger lines are plotted. The sma trigger line and the periods (daily) of the moving averages can be modified to your own preferences. The "slow" sma going above or below the trigger lines will print a different background color. Plot on a linear scale if you want to view this as similar to an RSI-type indicator. Plot on a log scale if you want to view as similar to a stochastic RSI.

Use this indicator at your own risk. I make no claims as to its accuracy in forecasting future trend changes of Bitcoin or the crypto market.

MCV - Meme Coin Volume [Logue]Meme Coin Volume. Investor preference for meme coin trading may signal irrational exuberance in the crypto market. If a large spike in meme coin volume is observed, a top may be near. Therefore, the volume of the most popular meme coins was added together in this indicator to help indicate potential mania phases, which may signal nearing of a top. A simple moving average of the meme coin volume also helps visualize the trend while reducing the noise. In back testing, I found a 10-day sma of the meme coin volume works well.

Meme coins were not traded heavily prior to 2020. Therefore, there is only one cycle to test at the time of initial publication. Also, the meme coin space moves fast, so more meme coins may need to be added later.

The total volume is plotted along with a moving average of the volume. For the indicator, you are able to change the raw volume trigger line, the sma trigger line, and the period (daily) of the sma to your own preferences. The raw volume or sma going above their respective trigger lines will print a different background color.

Use this indicator at your own risk. I make no claims as to its accuracy in forecasting future trend changes of Bitcoin or the crypto market.

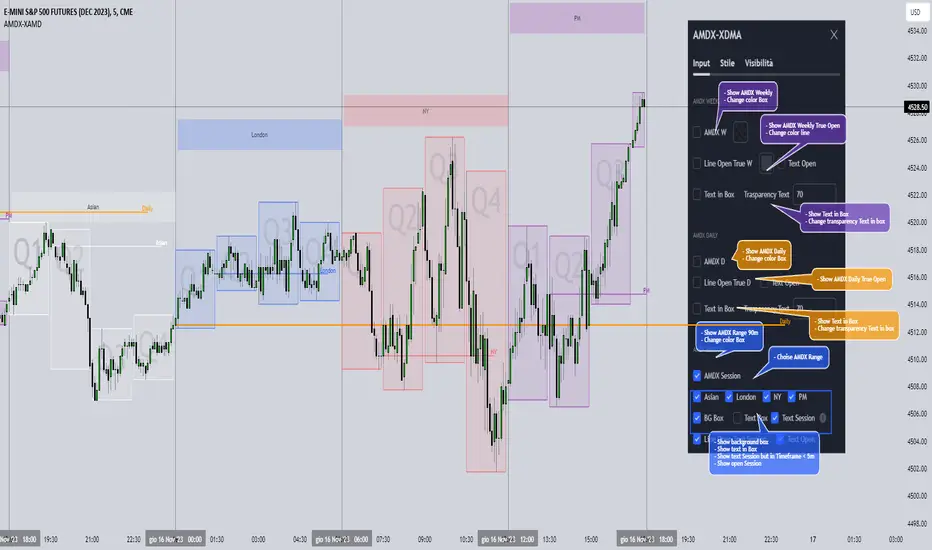

AMDX-XAMDGuided by ICT tutoring and also inspired by the teaching of

Daye', I create this versatile "AMDX" indicator.

A = Accumulation

M = Manipulation

D = Distribution

X = Continuation Or Reversal

This indicator shows a different way of viewing all the Timeframes by dividing them into Quarters, in this context the Trading sessions are divided into a 90m cycle, dividing each time range into Q1-Q2-Q3-Q4, in this way you have a clear vision of what the price is likely to do

True Open Times =

Opening Week - Monday at 6pm

Opening Day - 00:00

Asia -7.30pm

London -01.30

New York -07:30

PM -1.30pm

Session Times =

Q1 Asia 18:00-00:00

Q2 London 00:00-06:00

Q3 New York 06:00-12:00

Q4 PM 12:00-18:00

The user has the possibility to:

- Choose whether to display AMDX W

- Choose whether to display AMDX D

- Choose whether to display AMDX Session

- Choose to show the text in the Box

- Choose to show open levels

The indicator should be used as ICT and 'Daye' show in their concepts.

The indicator divides everything into Quarter ranges and classifies them into Q1-Q2-Q3-Q4 (as in the example above), and each Quarter has its own specific function, and can be used in this way:

If Q1 does an expansion it is likely that Q2 will do a consolidation, Q3 will do a Manipulation and Q4 will do a reversal returning to Q1

-If we are Bullish we buy under Open Session

-If we are Bearish we buy above open session

As in the example below:

If something is not clear, comment below and I will reply as soon as possible.

Recession Indicator (Unemployment Rate)Unemployment rate

percentage of unemployed individuals in an economy among individuals currently in the labour force. It is calcuated as Unemployed IndividualsTotal Labour Force × 100 where unemployed individuals are those who are currently not working but are actively seeking work.

The unemployment rate is one of the primary economic indicators used to measure the health of an economy. It tends to fluctuate with the business cycle, increasing during recessions and decreasing during expansions. It is among the indicators most commonly watched by policy makers, investors, and the general public.

Policy makers and central banks consider how much the unemployment rate has increased during a particular recession to gauge the recession’s impact on the economy and to decide how to tailor fiscal and monetary policies to mitigate its adverse effects. In addition, central banks carefully try to predict the future trend of the unemployment rate to devise long-term strategies to lower it.

This indicator is a representation of yearly rate of change of Unemployment rate. Historically (not always) when ROC(Yearly) of Unemployment rate crossover zero line was a signal of recession or economic contraction.

DR/IDR of Omega by TRSTNThis is an EXPERIMENTAL Script by @TRSTNGLRD derived from the coding of @IAmMas7er's "DR/IDR" Indicator that adds a total of 11 additional DR / IDR Ranges on both lower and higher timeframes.

This script is no-longer being worked on, so I have made it public.

Background:

This Script utilizes the Fibonacci-Doubling Sequence between the range of 18:30pm and 16:55pm NY-Time. Each Cycle is grouped into the following:

Omega/2, Omega/4, Omega/8, and Omega/16

The Mas7er's three original sessions are: Omega/4v1, Omega/4v2, and Omega/8v1

These three Sessions above take rule over all others. If you are looking to back-test this version of the script, please use the Experimental ranges as confirmation for the three above.

Important Notes:

- Please only select Sessions with their respected groups (All of Omega/4, All of Omega/16, etc...) rather than selecting all of them at once.

If you select all of them at once, the ranges will not be correct and cut each other off.

The only exceptions to this rule are the Mas7er's original ranges above.

- If you wish to have multiple groups of Ranges together, please add a second indicator to your chart.

- Omega/16v1 and Omega/16v6 are known to have a high-probability of a Judas Swing (takes out both sides of the range) - Be Cautious!

- Omega/2v1 is a very large DR / IDR range. I am working on shrinking it in size, but have more experimenting to do with different ranges.

- I do not use the experimental ranges with the IDR , only the DR . I have not been able to define probabilities fully yet, but the levels are respected nonetheless.

This script is not supposed to work EXACTLY like the Mas7er's, rather, generally instead.

Please comment and leave your opinion below about which ranges work the best and how you may utilize them.

Thank you!

VXD SupercycleVXD is a brand new indicator and still developing. to minimize stop losses and overcome sideways market conditions, Higher Timeframe are recommended

Trend lines

-using Rolling VWAP as trend line to determined if Volume related to a certain price.

-you can switch RVWAP to EMA in the setting

ATR

-trailing 12*ATR and 2.4 Mutiplier

Pivot point and Rejected Block

Pivot show last High and low of a price in past bars

Rejected Block show when that High or Low price are important level to determined if it's Hidden Divergence or Divergence

Symbols on chart show Premium and Discount Prices

X-Cross - show potential reversal trend with weak volume .

O-circle - show potential reversal trend with strong volume .

Setting

Momentum: RSI = 25 , RSI MA = 14

Trend: Rolling VWAP and ATR and Subhag

Trailing STOP: ATR 12 x 2.4

Highlight Bars color when volume is above SMA 6

SMA200 act as TP Line

Risk:Reward Calculation

if Buy your Stoploss will be previous Pivot low

if Sell your Stoploss will be previous Pivot high and will be calculated form there, then show TP in Orange color line

VXD เป็นระบบเทรดที่ผมทดลองเอาหลาย ๆ ไอเดีย ทั้งจาก Youtube facebook และกลุ่มคนต่าง ๆ มารวบรวมไว้ แล้วตกผลึกขึ้นมาเป็นระบบนี้ ใน Timeframe ใหญ่ ๆ สามารถลากได้ทั้ง Cycle กันเลย

Trend lines

-ใช้ Rolling VWAP ของแอพ Tradingview (สามารถตั้งแค่าเป็น EMA ได้)

ATR

-ใช้ค่า ATR 12 Mutiplier 2.4

Pivot point and Rejected Block

Pivot โชว์เส้น High low และมีผลกับออเดอร์ หากแท่งเทียนปิดทะลุเส้นนี้

Rejected Block วาดแนวรับ-ต้าน อัตโนมัติ ใช้ประกอบ RSI ว่ามี Divergence หรือไม่

สัญลักษณ์ต่าง ๆ

X-Cross - แท่งกลืนกิน วอลุ่มน้อย

O-circle - แท่งกลืนกิน มีวอลุ่ม

Setting

Momentum: RSI = 25 , RSI MA = 14

Trend: Rolling VWAP and ATR and Subhag

Trailing STOP: ATR 12 x 2.4

Highlight Bars color when volume is above SMA 6

SMA200 act as TP Line

Risk:Reward Calculation

หาก Buy จุด SL จะอยู่ที่ Pivot low

หาก Sell จุด SL จะอยู่ที่ Pivot high และระบบจะคำนวณจากตรงนั้น จากนั้นแสดงเป็นเส้น TP สีส้ม

This Strategy Combined the following indicators and conditioning by me

ATR , RSI , EMA , SMA

Rolling VWAP - /script/ZU2UUu9T-Rolling-VWAP/

Regression Lines - Subhag form Subhag Ghosh /script/LHHBVpQu-Subhag-Ghosh-Algo-Version-for-banknifty/

Rejection Block , Pivots , High Volume Bars and PPDD form Super OrderBlock / FVG / BoS Tools by makuchaku & eFe /script/aZACDmTC-Super-OrderBlock-FVG-BoS-Tools-by-makuchaku-eFe/

ขอให้รวยครับ.

ETH Gravity OscillatorThis indicator is a deviation of a Center of Gravity Oscillator corrected for the diminishing returns of Ethereum.

I've set up this indicator for it to be used on the weekly timeframe . The indicator oscillates between 0 and 10, where 0 indicates oversold conditions and 10 indicates overbought conditions. What is interesting is that it is not particularly ideal for identifying market cycle tops, but generally picks out the most euphoric region in the initial parabolic rally. Good to potentially keep in mind if there is a second bounce to the peak!

The indicator plots in any ETH charts. It paints in all time frames, but Weekly time frame is the correct one to interpret the 'official' read of it.

Made at the request of a kind commenter. If you would like to request different derivations of this script be sure to let me know!

TASC 2025.02 Autocorrelation Indicator█ OVERVIEW

This script implements the Autocorrelation Indicator introduced by John Ehlers in the "Drunkard's Walk: Theory And Measurement By Autocorrelation" article from the February 2025 edition of TASC's Traders' Tips . The indicator calculates the autocorrelation of a price series across several lags to construct a periodogram , which traders can use to identify market cycles, trends, and potential reversal patterns.

█ CONCEPTS

Drunkard's walk

A drunkard's walk , formally known as a random walk , is a type of stochastic process that models the evolution of a system or variable through successive random steps.

In his article, John Ehlers relates this model to market data. He discusses two first- and second-order partial differential equations, modified for discrete (non-continuous) data, that can represent solutions to the discrete random walk problem: the diffusion equation and the wave equation. According to Ehlers, market data takes on a mixture of two "modes" described by these equations. He theorizes that when "diffusion mode" is dominant, trading success is almost a matter of luck, and when "wave mode" is dominant, indicators may have improved performance.

Pink spectrum

John Ehlers explains that many recent academic studies affirm that market data has a pink spectrum , meaning the power spectral density of the data is proportional to the wavelengths it contains, like pink noise . A random walk with a pink spectrum suggests that the states of the random variable are correlated and not independent. In other words, the random variable exhibits long-range dependence with respect to previous states.

Autocorrelation function (ACF)

Autocorrelation measures the correlation of a time series with a delayed copy, or lag , of itself. The autocorrelation function (ACF) is a method that evaluates autocorrelation across a range of lags , which can help to identify patterns, trends, and cycles in stochastic market data. Analysts often use ACF to detect and characterize long-range dependence in a time series.

The Autocorrelation Indicator evaluates the ACF of market prices over a fixed range of lags, expressing the results as a color-coded heatmap representing a dynamic periodogram. Ehlers suggests the information from the periodogram can help traders identify different market behaviors, including:

Cycles : Distinguishable as repeated patterns in the periodogram.

Reversals : Indicated by sharp vertical changes in the periodogram when the indicator uses a short data length .

Trends : Indicated by increasing correlation across lags, starting with the shortest, over time.

█ USAGE

This script calculates the Autocorrelation Indicator on an input "Source" series, smoothed by Ehlers' UltimateSmoother filter, and plots several color-coded lines to represent the periodogram's information. Each line corresponds to an analyzed lag, with the shortest lag's line at the bottom of the pane. Green hues in the line indicate a positive correlation for the lag, red hues indicate a negative correlation (anticorrelation), and orange or yellow hues mean the correlation is near zero.

Because Pine has a limit on the number of plots for a single indicator, this script divides the periodogram display into three distinct ranges that cover different lags. To see the full periodogram, add three instances of this script to the chart and set the "Lag range" input for each to a different value, as demonstrated in the chart above.

With a modest autocorrelation length, such as 20 on a "1D" chart, traders can identify seasonal patterns in the price series, which can help to pinpoint cycles and moderate trends. For instance, on the daily ES1! chart above, the indicator shows repetitive, similar patterns through fall 2023 and winter 2023-2024. The green "triangular" shape rising from the zero lag baseline over different time ranges corresponds to seasonal trends in the data.

To identify turning points in the price series, Ehlers recommends using a short autocorrelation length, such as 2. With this length, users can observe sharp, sudden shifts along the vertical axis, which suggest potential turning points from upward to downward or vice versa.

Cycle & Flow Indicator - D_QuantCycle & Flow Architecture (CFA) | Multi-Factor Regime Analysis

Overview

The Cycle & Flow Architecture (CFA) is a trend-following visualization engine that utilizes a triple-confirmation "Voting Mechanism" to identify market regimes. Rather than relying on a single lagging indicator, the CFA aggregates Cyclical Momentum, Directional Bias, and Volume Flow from the Daily timeframe to provide a unified consensus signal on your current chart.

The goal of this script is to filter market noise by requiring a quantitative agreement between three non-correlated mathematical models before a "Regime Change" is visualized.

The Quantitative Logic

The core of the CFA is its Aggregation Engine, which calculates a normalized Quant Score ranging from -1.0 to +1.0. The engine polls three distinct components:

Schaff Trend Cycle (STC): This component identifies the cyclical nature of price. It applies a double-smoothed stochastic process to a MACD line. In this script, the STC contributes a bullish signal when the cycle is above 25 and a bearish signal when the cycle is below 75 and falling.

Parabolic SAR (PSAR): Used as a rigid directional filter. It calculates the "Stop and Reverse" points, if the price is above the PSAR, it contributes a +1 to the consensus, if below, a -1.

Ease of Movement (EOM): This is the volume-validation component. It analyzes the relationship between price change and volume. A positive EOM suggests price is moving up on light resistance (conviction), while negative EOM suggests easy downward movement.

How it Works: The Voting Mechanism

The script calculates these three values on the Daily (D) timeframe using request.security to ensure higher-timeframe confluence.

Bullish Regime: Triggered when the average score exceeds the Bullish Threshold (Default: 0.2).

Bearish Regime: Triggered when the average score falls below the Bearish Threshold (Default: -0.2).

Neutral Regime: When the components disagree or the scores hover near zero, the engine renders a "Grey" noise state, signaling a high-probability "sit on hands" environment.

How to Use

The Ghost Cloud: The central Hull Moving Average (HMA 20) acts as the baseline. The "cloud" fills between this baseline and the price, colored by the current Score.

Volatility Extensions: The script plots ATR-based bands (14-period) that only appear during confirmed regimes. In a Bullish regime, the upper band appears, in a Bearish regime, the lower.

Trade Execution: Traders typically look for the "Bullish/Bearish Start" alerts to signal the beginning of a new regime and use the "Grey" neutral zones to tighten stop-losses or exit positions.

Settings

Thresholds: Increase the Bullish/Bearish thresholds (e.g., to 0.5) to require more stringent agreement between the STC, PSAR, and EOM.

Timeframe Note: The calculations are hardcoded to the Daily timeframe to provide a "North Star" directional bias regardless of whether you are viewing the 15m or 4h chart.

Disclaimer: This tool is for educational and analytical purposes only. Quantitative models represent mathematical probabilities, not guarantees.

© D_QUANT

ALT Risk Metric StrategyHere's a professional write-up for your ALT Risk Strategy script:

ALT/BTC Risk Strategy - Multi-Crypto DCA with Bitcoin Correlation Analysis

Overview

This strategy uses Bitcoin correlation as a risk indicator to time entries and exits for altcoins. By analyzing how your chosen altcoin performs relative to Bitcoin, the strategy identifies optimal accumulation periods (when alt/BTC is oversold) and profit-taking opportunities (when alt/BTC is overbought). Perfect for traders who want to outperform Bitcoin by strategically timing altcoin positions.

Key Innovation: Why Alt/BTC Matters

Most traders focus solely on USD price, but Alt/BTC ratios reveal true altcoin strength:

When Alt/BTC is low → Altcoin is undervalued relative to Bitcoin (buy opportunity)

When Alt/BTC is high → Altcoin has outperformed Bitcoin (take profits)

This approach captures the rotation between BTC and alts that drives crypto cycles

Key Features

📊 Advanced Technical Analysis

RSI (60% weight): Primary momentum indicator on weekly timeframe

Long-term MA Deviation (35% weight): Measures distance from 150-period baseline

MACD (5% weight): Minor confirmation signal

EMA Smoothing: Filters noise while maintaining responsiveness

All calculations performed on Alt/BTC pairs for superior market timing

💰 3-Tier DCA System

Level 1 (Risk ≤ 70): Conservative entry, base allocation

Level 2 (Risk ≤ 50): Increased allocation, strong opportunity

Level 3 (Risk ≤ 30): Maximum allocation, extreme undervaluation

Continuous buying: Executes every bar while below threshold for true DCA behavior

Cumulative sizing: L3 triggers = L1 + L2 + L3 amounts combined

📈 Smart Profit Management

Sequential selling: Must complete L1 before L2, L2 before L3

Percentage-based exits: Sell portions of position, not fixed amounts

Auto-reset on re-entry: New buy signals reset sell progression

Prevents premature full exits during volatile conditions

🤖 3Commas Automation

Pre-configured JSON webhooks for Custom Signal Bots

Multi-exchange support: Binance, Coinbase, Kraken, Bitfinex, Bybit

Flexible quote currency: USD, USDT, or BUSD

Dynamic order sizing: Automatically adjusts to your tier thresholds

Full webhook documentation compliance

🎨 Multi-Asset Support

Pre-configured for popular altcoins:

ETH (Ethereum)

SOL (Solana)

ADA (Cardano)

LINK (Chainlink)

UNI (Uniswap)

XRP (Ripple)

DOGE

RENDER

Custom option for any other crypto

How It Works

Risk Metric Calculation (0-100 scale):

Fetches weekly Alt/BTC price data for stability

Calculates RSI, MACD, and deviation from 150-period MA

Normalizes MACD to 0-100 range using 500-bar lookback

Combines weighted components: (MACD × 0.05) + (RSI × 0.60) + (Deviation × 0.35)

Applies 5-period EMA smoothing for cleaner signals

Color-Coded Risk Zones:

Green (0-30): Extreme buying opportunity - Alt heavily oversold vs BTC

Lime/Yellow (30-70): Accumulation range - favorable risk/reward

Orange (70-85): Caution zone - consider taking initial profits

Red/Maroon (85-100+): Euphoria zone - aggressive profit-taking

Entry Logic:

Buys execute every candle when risk is below threshold

As risk decreases, position sizing automatically scales up

Example: If risk drops from 60→25, you'll be buying at L1 rate until it hits 50, then L2 rate, then L3 rate

Exit Logic:

Sells only trigger when in profit AND risk exceeds thresholds

Sequential execution ensures partial profit-taking

If new buy signal occurs before all sells complete, sell levels reset to L1

Configuration Guide

Choosing Your Altcoin:

Select crypto from dropdown (or use CUSTOM for unlisted coins)

Pick your exchange

Choose quote currency (USD, USDT, BUSD)

Risk Metric Tuning:

Long Term MA (default 150): Higher = more extreme signals, Lower = more frequent

RSI Length (default 10): Lower = more volatile, Higher = smoother

Smoothing (default 5): Increase for less noise, decrease for faster reaction

Buy Settings (Aggressive DCA Example):

L1 Threshold: 70 | Amount: $5

L2 Threshold: 50 | Amount: $6

L3 Threshold: 30 | Amount: $7

Total L3 buy = $18 per candle when deeply oversold

Sell Settings (Balanced Exit Example):

L1: 70 threshold, 25% position

L2: 85 threshold, 35% position

L3: 100 threshold, 40% position (final exit)

3Commas Setup

Bot Configuration:

Create Custom Signal Bot in 3Commas

Set trading pair to your altcoin/USD (e.g., ETH/USD, SOL/USDT)

Order size: Select "Send in webhook, quote" to use strategy's dollar amounts

Copy Bot UUID and Secret Token

Script Configuration:

Paste credentials into 3Commas section inputs

Check "Enable 3Commas Alerts"

Save and apply to chart

TradingView Alert:

Create Alert → Condition: "alert() function calls only"

Webhook URL: api.3commas.io

Enable "Webhook URL" checkbox

Expiration: Open-ended

Strategy Advantages

✅ Outperform Bitcoin: Designed specifically to beat BTC by timing alt rotations

✅ Capture Alt Seasons: Automatically accumulates when alts lag, sells when they pump

✅ Risk-Adjusted Sizing: Buys more when cheaper (better risk/reward)

✅ Emotional Discipline: Systematic approach removes fear and FOMO

✅ Multi-Asset: Run same strategy across multiple altcoins simultaneously

✅ Proven Indicators: Combines RSI, MACD, and MA deviation - battle-tested tools

Backtesting Insights

Optimal Timeframes:

Daily chart: Best for backtesting and signal generation

Weekly data is fetched internally regardless of display timeframe

Historical Performance Characteristics:

Accumulates heavily during bear markets and BTC dominance periods

Captures explosive altcoin rallies when BTC stagnates

Sequential selling preserves capital during extended downtrends

Works best on established altcoins with multi-year history

Risk Considerations:

Requires capital reserves for extended accumulation periods

Some altcoins may never recover if fundamentals deteriorate

Past correlation patterns may not predict future performance

Always size positions according to personal risk tolerance

Visual Interface

Indicator Panel Displays:

Dynamic color line: Green→Lime→Yellow→Orange→Red as risk increases

Horizontal threshold lines: Dashed lines mark your buy/sell levels

Entry/Exit labels: Green labels for buys, Orange/Red/Maroon for sells

Real-time risk value: Numerical display on price scale

Customization:

All threshold lines are adjustable via inputs

Color scheme clearly differentiates buy zones (green spectrum) from sell zones (red spectrum)

Line weights emphasize most extreme thresholds (L3 buy and L3 sell)

Strategy Philosophy

This strategy is built on the principle that altcoins move in cycles relative to Bitcoin. During Bitcoin rallies, alts often bleed against BTC (high sell, accumulate). When Bitcoin consolidates, alts pump (take profits). By measuring risk on the Alt/BTC chart instead of USD price, we time these rotations with precision.

The 3-tier system ensures you're always averaging in at better prices and scaling out at better prices, maximizing your Bitcoin-denominated returns.

Advanced Tips

Multi-Bot Strategy:

Run this on 5-10 different altcoins simultaneously to:

Diversify correlation risk

Capture whichever alt is pumping

Smooth equity curve through rotation

Pairing with BTC Strategy:

Use alongside the BTC DCA Risk Strategy for complete portfolio coverage:

BTC strategy for core holdings

ALT strategies for alpha generation

Rebalance between them based on BTC dominance

Threshold Calibration:

Check 2-3 years of historical data for your chosen alt

Note where risk metric sat during major bottoms (set buy thresholds)

Note where it peaked during euphoria (set sell thresholds)

Adjust for your risk tolerance and holding period

Credits

Strategy Development & 3Commas Integration: Claude AI (Anthropic)

Technical Analysis Framework: RSI, MACD, Moving Average theory

Implementation: pommesUNDwurst

Disclaimer

This strategy is for educational purposes only. Cryptocurrency trading involves substantial risk of loss. Altcoins are especially volatile and many fail completely. The strategy assumes liquid markets and reliable Alt/BTC price data. Always do your own research, understand the fundamentals of any asset you trade, and never risk more than you can afford to lose. Past performance does not guarantee future results. The authors are not financial advisors and assume no liability for trading decisions.

Additional Warning: Using leverage or trading illiquid altcoins amplifies risk significantly. This strategy is designed for spot trading of established cryptocurrencies with deep liquidity.

Tags: Altcoin, Alt/BTC, DCA, Risk Metric, Dollar Cost Averaging, 3Commas, ETH, SOL, Crypto Rotation, Bitcoin Correlation, Automated Trading, Alt Season

Feel free to modify any sections to better match your style or add specific backtesting results you've observed! 🚀Claude is AI and can make mistakes. Please double-check responses. Sonnet 4.5

CVDD Z-ScoreCumulative Value Days Destroyed (CVDD) - The CVDD was created by Willy Woo and is the ratio of the cumulative value of Coin Days Destroyed in USD and the market age (in days). While this indicator is used to detect bottoms normally, an extension is used to allow detection of BTC tops. When the BTC price goes above the CVDD extension, BTC is generally considered to be overvalued. Because the "strength" of the BTC tops has decreased over the cycles, a logarithmic function for the extension was created by fitting past cycles as log extension = slope * time + intercept. This indicator is triggered for a top when the BTC price is above the CVDD extension. For the bottoms, the CVDD is shifted upwards at a default value of 120%. The slope, intercept, and CVDD bottom shift can all be modified in the script.

Now with the automatic Z-Score calculation for ease of classification of Bitcoin's valuation according to this metric.

Created for TRW.

Goichi Hosoda TheoryGreetings to traders. I offer you an indicator for trading according to the Ichimoku Kinho Hyo trading system. This indicator determines possible time cycles of price reversal and expected asset price values based on the theory of waves and time cycles by Goichi Hosoda.

The indicator contains classic price levels N, V, E and NT, and is supplemented with intermediate levels V+E, V+N, N+NT and x2, x3, x4 for levels V and E, which are used in cases where the wave does not contain corrections and there is no possibility to update the impulse-corrective wave.

A function for counting bars from points A B and C has also been added.

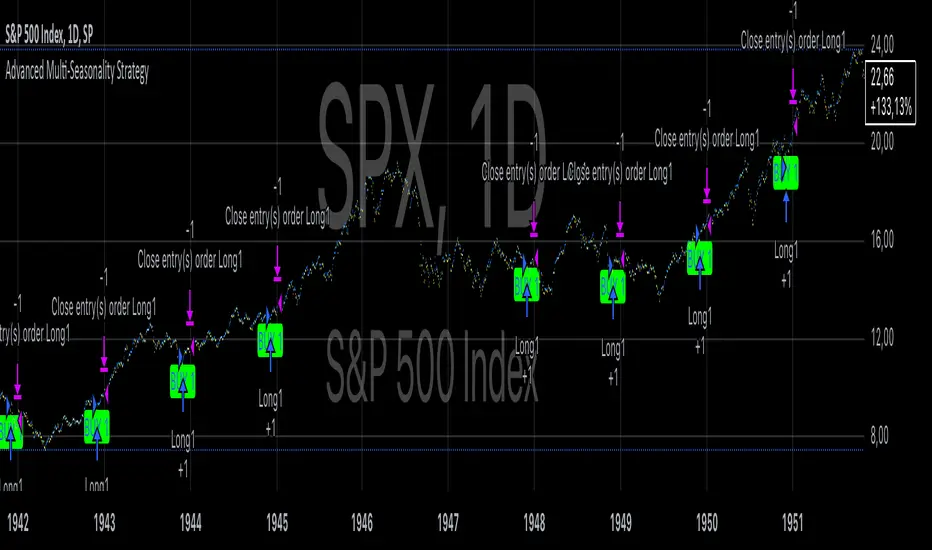

Advanced Multi-Seasonality StrategyThe Multi-Seasonality Strategy is a trading system based on seasonal market patterns. Seasonality refers to recurring market trends driven by predictable calendar-based events. These patterns emerge due to economic cycles, corporate activities (e.g., earnings reports), and investor behavior around specific times of the year. Studies have shown that such effects can influence asset prices over defined periods, leading to opportunities for traders who exploit these patterns (Hirshleifer, 2001; Bouman & Jacobsen, 2002).

How the Strategy Works:

The strategy allows the user to define four distinct periods within a calendar year. For each period, the trader selects:

Entry Date (Month and Day): The date to enter the trade.

Holding Period: The number of trading days to remain in the trade after the entry.

Trade Direction: Whether to take a long or short position during that period.

The system is designed with flexibility, enabling the user to activate or deactivate each of the four periods. The idea is to take advantage of seasonal patterns, such as buying during historically strong periods and selling during weaker ones. A well-known example is the "Sell in May and Go Away" phenomenon, which suggests that stock returns are higher from November to April and weaker from May to October (Bouman & Jacobsen, 2002).

Seasonality in Financial Markets:

Seasonal effects have been documented across different asset classes and markets:

Equities: Stock markets tend to exhibit higher returns during certain months, such as the "January effect," where prices rise after year-end tax-loss selling (Haugen & Lakonishok, 1987).

Commodities: Agricultural commodities often follow seasonal planting and harvesting cycles, which impact supply and demand patterns (Fama & French, 1987).

Forex: Currency pairs may show strength or weakness during specific quarters based on macroeconomic factors, such as fiscal year-end flows or central bank policy decisions.

Scientific Basis:

Research shows that market anomalies like seasonality are linked to behavioral biases and institutional practices. For example, investors may respond to tax incentives at the end of the year, and companies may engage in window dressing (Haugen & Lakonishok, 1987). Additionally, macroeconomic factors, such as monetary policy shifts and holiday trading volumes, can also contribute to predictable seasonal trends (Bouman & Jacobsen, 2002).

Risks of Seasonal Trading:

While the strategy seeks to exploit predictable patterns, there are inherent risks:

Market Changes: Seasonal effects observed in the past may weaken or disappear as market conditions evolve. Increased algorithmic trading, globalization, and policy changes can reduce the reliability of historical patterns (Lo, 2004).

Overfitting: One of the risks in seasonal trading is overfitting the strategy to historical data. A pattern that worked in the past may not necessarily work in the future, especially if it was based on random chance or external factors that no longer apply (Sullivan, Timmermann, & White, 1999).

Liquidity and Volatility: Trading during specific periods may expose the trader to low liquidity, especially around holidays or earnings seasons, leading to slippage and larger-than-expected price swings.

Economic and Geopolitical Shocks: External events such as pandemics, wars, or political instability can disrupt seasonal patterns, leading to unexpected market behavior.

Conclusion:

The Multi-Seasonality Strategy capitalizes on the predictable nature of certain calendar-based patterns in financial markets. By entering and exiting trades based on well-established seasonal effects, traders can potentially capture short-term profits. However, caution is necessary, as market dynamics can change, and seasonal patterns are not guaranteed to persist. Rigorous backtesting, combined with risk management practices, is essential to successfully implementing this strategy.

References:

Bouman, S., & Jacobsen, B. (2002). The Halloween Indicator, "Sell in May and Go Away": Another Puzzle. American Economic Review, 92(5), 1618-1635.

Fama, E. F., & French, K. R. (1987). Commodity Futures Prices: Some Evidence on Forecast Power, Premiums, and the Theory of Storage. Journal of Business, 60(1), 55-73.

Haugen, R. A., & Lakonishok, J. (1987). The Incredible January Effect: The Stock Market's Unsolved Mystery. Dow Jones-Irwin.

Hirshleifer, D. (2001). Investor Psychology and Asset Pricing. Journal of Finance, 56(4), 1533-1597.

Lo, A. W. (2004). The Adaptive Markets Hypothesis: Market Efficiency from an Evolutionary Perspective. Journal of Portfolio Management, 30(5), 15-29.

Sullivan, R., Timmermann, A., & White, H. (1999). Data-Snooping, Technical Trading Rule Performance, and the Bootstrap. Journal of Finance, 54(5), 1647-1691.

This strategy harnesses the power of seasonality but requires careful consideration of the risks and potential changes in market behavior over time.

US Presidential Elections (Names & Dates)US Presidential Elections (Names & Dates)

Description :

This indicator marks key dates in US presidential history, highlighting both election days and inauguration dates. It's designed to provide historical context to your charts, allowing you to see how major political events align with market movements.

Key Features:

• Displays US presidential elections from 1936 to 2052

• Shows inauguration dates for each president

• Customizable colors and styles for both election and inauguration markers

• Toggle visibility of election and inauguration labels separately

• Adapts to different timeframes (daily, weekly, monthly)

• Includes president names for historical context

The indicator uses yellow labels for election days and blue labels for inauguration dates. Election labels show the year and "Election", while inauguration labels display the name of the incoming president.

Customization options include:

• Colors for election and inauguration labels and text

• Line widths for both types of events

• Label placement styles

This tool is perfect for traders and analysts who want to correlate political events with market trends over long periods. It provides a unique perspective on how presidential cycles might influence financial markets.

Note: Future elections (2024 onwards) are marked with a placeholder (✅) as the presidents are not yet known.

Use this indicator to:

• Identify potential market patterns around election cycles

• Analyze historical market reactions to specific presidencies

• Add political context to your long-term chart analysis

Enhance your chart analysis with this comprehensive view of US presidential history!

CVDD - Coin Value Days Destroyed for Bitcoin (BTC) [Logue]Cumulative Value Days Destroyed (CVDD) - The CVDD was created by Willy Woo and is the ratio of the cumulative value of Coin Days Destroyed in USD and the market age (in days). While this indicator is used to detect bottoms normally, an extension is used to allow detection of BTC tops. When the BTC price goes above the CVDD extension, BTC is generally considered to be overvalued. Because the "strength" of the BTC tops has decreased over the cycles, a logarithmic function for the extension was created by fitting past cycles as log extension = slope * time + intercept. This indicator is triggered for a top when the BTC price is above the CVDD extension. For the bottoms, the CVDD is shifted upwards at a default value of 120%. The slope, intercept, and CVDD bottom shift can all be modified in the script.

Cycle Position TradingTitle: Cycle Position Trading Strategy v1.0

Description: Cycle Position Trading Strategy is a simple yet effective trading strategy based on a 200-day Simple Moving Average (SMA). Users can select between two modes, "Buy Uptrend" and "Buy Downtrend," to customize the strategy according to their trading preferences. The strategy allows users to set their own stop loss (SL) and take profit (TP) levels, providing more flexibility and control over their trades.

Features:

Choose between two trading modes: "Buy Uptrend" and "Buy Downtrend."

Customize your stop loss (SL) and take profit (TP) levels.

Clear visual representation of the 200-day Simple Moving Average (SMA) on the chart.

How to use:

Add the strategy to your chart by searching for "Cycle Position Trading Strategy" in the TradingView "Indicators & Strategies" section.

Configure the strategy settings according to your preferences:

Select the trading mode from the dropdown menu. "Buy Uptrend" will open long positions when the closing price is above the 200-day SMA. "Buy Downtrend" will open long positions when the closing price is below the 200-day SMA.

Set your desired stop loss (SL) and take profit (TP) levels. The default values are 0.9 (10% below the entry price) for the stop loss and 1.1 (10% above the entry price) for the take profit.

Monitor the chart for trade signals based on the chosen mode and settings. The strategy will enter and exit trades automatically based on the selected mode and the configured stop loss and take profit levels.

Analyze the performance of the strategy by checking the TradingView strategy performance summary or by viewing individual trades in the "Trades" list.

Disclaimer: This strategy is intended for educational and illustrative purposes only. Use it at your own risk. Past performance is not indicative of future results. Trading stocks, cryptocurrencies, or any other financial instrument involves significant risk and may result in the loss of capital.

Version: v1.0

Release date: 2023-03-25

Author: I11L

License: Mozilla Public License 2.0 (mozilla.org)

Cycle Channel Oscillator [LazyBear]Here's an oscillator derived from my previous script, Cycle Channel Clone ().

There are 2 oscillator plots - fast & slow. Fast plot shows the price location with in the medium term channel, while slow plot shows the location of short term midline of cycle channel with respect to medium term channel.

Usage of this is similar to %b oscillator. The slow plot can be considered as the signal line.

Bar colors can be enabled via options page. When short plot is above 1.0 or below 0, they are marked purple (both histo and the bar color) to highlight the extreme condition.

This makes use of the default 10/30 values of Cycle Channel, but may need tuning for your instrument.

More info:

List of my free indicators: bit.ly

List of my app-store indicators: blog.tradingview.com (More info: bit.ly)

ETH Dynamic Risk Strategy# ETH Dynamic Risk Strategy - Publication Description

## Overview

The ETH Dynamic Risk Strategy is a systematic approach to accumulating Ethereum during bear markets and distributing during bull markets. It combines multiple risk indicators into a single composite metric (0-1 scale) that identifies optimal buying and selling zones based on market conditions.

## Key Features

• **Multi-Component Risk Metric**: Combines 4 weighted indicators to assess market conditions

• **Tiered Buy/Sell System**: 3 levels of buy signals (L1, L2, L3) and 3 levels of sell signals based on risk thresholds

• **Configurable Filters**: Optional buy filters to reduce signal frequency by 30-50%

• **Visual Risk Zones**: Color-coded risk metric plot with clear threshold lines

• **Comprehensive Dashboard**: Real-time statistics including position size, P/L, and component scores

## How It Works

### Risk Components (Configurable Weights)

1. **Log Return from ATH** (Default: 35%)

- Tracks drawdown from all-time high over lookback period

- Deep drawdowns (-70% to -90%) = low risk / buying opportunity

- Near ATH (0% to -20%) = high risk / selling opportunity

2. **ETH/BTC Ratio** (Default: 25%)

- Measures ETH strength relative to Bitcoin

- Below historical average = ETH undervalued = low risk

- Above historical average = ETH overvalued = high risk

3. **Volatility Regime** (Default: 20%)

- Compares current volatility to long-term average

- Compressed volatility at lows = opportunity

- Expanded volatility at highs = danger

4. **Trend Strength** (Default: 20%)

- Uses multiple EMA alignment and slope analysis

- Strong downtrends = low risk scores

- Strong uptrends = high risk scores

### Trading Logic

**Buy Signals:**

- L1: Risk ≤ 0.30 → Buy $100 (default)

- L2: Risk ≤ 0.20 → Buy $250 total

- L3: Risk ≤ 0.10 → Buy $450 total

**Sell Signals (Sequential):**

- L1: Risk ≥ 0.75 → Sell 25% of position

- L2: Risk ≥ 0.85 → Sell 35% of remaining

- L3: Risk ≥ 0.95 → Sell 40% of remaining

**Buy Filters (Optional):**

- Minimum days between buys (prevents clustering)

- Minimum risk drop required (ensures falling risk)

- Toggle on/off to compare performance

## Settings Guide

### Risk Components

Toggle individual components on/off and adjust their weights. Total weight is automatically normalized. Experiment with different combinations to match your market view.

### Advanced Settings

- ATH Lookback: How far back to look for all-time highs (500-2000 recommended)

- Volatility Period: Window for volatility calculations (40-100 recommended)

- ETH/BTC MA Period: Moving average for ratio comparison (100-300 recommended)

- Trend Period: Base period for trend calculations (50-150 recommended)

### Trading Thresholds

Customize buy/sell trigger points and position sizes. Lower buy thresholds = more aggressive accumulation. Higher sell thresholds = holding longer into bull markets.

### Buy Filters

- Enable/disable filtering system

- Min Days Between Buys: Spacing between purchases (1-3 recommended)

- Min Risk Drop: How much risk must fall (-0.001 to -0.01 range)

## Best Practices

• **Timeframe**: Works best on daily (1D) and 3-day (3D) charts

• **Initial Capital**: Set based on your DCA budget (default $10,000)

• **Backtest First**: Test different parameter combinations on historical data

• **Position Sizing**: Adjust buy amounts to match your risk tolerance

• **Monitor Filters**: Check "Filtered Buys" stat to ensure filter isn't too strict

## Use Cases

- Long-term ETH accumulation strategy

- Systematic DCA with market-adaptive buying

- Risk-based portfolio rebalancing

- Educational tool for understanding crypto market cycles

## Disclaimer

This strategy is for educational purposes only. Past performance does not guarantee future results. Cryptocurrency trading involves substantial risk. The strategy uses historical price action and technical indicators which may not predict future movements. Always do your own research and never invest more than you can afford to lose.

## Credits

Strategy concept and development by nakphanan with assistance from Claude AI (Anthropic). Built using Pine Script v5....Mostly from Claude AI!!!

## Version History

v7.0 - Initial release with 4-component risk metric, tiered trading system, and optional buy filters

Gann Octave 8 Ver.2.0Gann Octave 8 Ver.2.0 - Complete Trading Guide

Overview

This indicator combines W.D. Gann's time-tested principles of market geometry with modern technical analysis. It identifies key market structures and projects precise support/resistance levels along with angular momentum lines to help traders identify high-probability trading opportunities.

________________________________________

Core Concepts

1. Gann's Octave Division (The Rule of 8)

W.D. Gann discovered that markets move in harmonic divisions based on the number 8. This indicator divides any swing movement into 8 equal parts (octaves):

• 0% - Swing extreme (High for bearish, Low for bullish)

• 12.5% - First octave

• 25% - Quarter level

• 37.5% - Three-eighths level

• 50% - Midpoint (most critical level)

• 62.5% - Five-eighths level

• 75% - Three-quarter level

• 87.5% - Seventh octave

• 100% - Swing extreme (opposite end)

Why 8? Gann believed natural market cycles follow mathematical harmonics. The octave division provides precise entry and exit points that frequently act as support/resistance zones.

2. Gann Angles (Price-Time Relationship)

Gann angles represent the relationship between price movement and time. Each angle shows different momentum levels:

• 1x1 (Black) - 45° angle, perfect balance between price and time. Most important Gann angle. Represents the natural trend line.

• 2x1 (Red) - Steeper angle, 2 units of price per 1 unit of time. Shows strong momentum.

• 1x2 (Red) - Flatter angle, 1 unit of price per 2 units of time. Shows weak momentum.

• 4x1 & 1x4 (Blue) - Even more extreme angles indicating very strong or very weak trends.

• 8x1 & 1x8 (Orange) - Most extreme angles, parabolic moves or complete consolidation.

Key Principle: When price is above the 1x1 angle = bullish. Below 1x1 = bearish. When price crosses from one angle to another, it signals a change in momentum.

________________________________________

How the Indicator Works

Structure Detection

The indicator automatically identifies market swings using pivot points:

1. Bullish Structure (Green): Detected when price makes a higher high

o Octave levels calculated from swing low (0%) to swing high (100%)

o Gann angles project upward from the swing low

2. Bearish Structure (Red): Detected when price makes a lower low

o Octave levels calculated from swing high (0%) to swing low (100%)

o Gann angles project downward from the swing high

Dynamic Updates

• Swing Tracker ON: Levels update continuously as the swing evolves

• Swing Tracker OFF: Levels lock at the initial swing detection (cleaner charts)

Historical Structures

The indicator maintains previous swing structures based on "Number of Swings to Show":

• Set to 1: Only current structure (cleanest)

• Set to 2-3: Current + recent history (recommended for context)

• Set to 4+: Multiple historical structures (may overlap but shows pattern)

________________________________________

Trading Strategy

Entry Signals

BUY SIGNALS (Green Triangle Up ▲)

Signal 1: Bounce from Support Levels

• Price drops to 0%, 50%, or 100% level and reverses

• Best when combined with bullish candlestick pattern (hammer, engulfing)

• Entry: On signal confirmation

• Stop Loss: Below the support level (0.5-1% below)

• Target: Next octave level up (12.5%, 25%, 50%)

Signal 2: Breakout Above Resistance

• Price breaks above 50% or 100% level with momentum

• Confirms trend continuation or reversal

• Entry: On close above the level

• Stop Loss: Below the breakout level

• Target: Previous swing high or next major level

Signal 3: Gann Angle Support

• Price bounces off 1x1 angle (black line)

• Indicates trend is intact

• Entry: When price respects the angle

• Stop Loss: Below the 1x1 angle

• Target: Next resistance level

SELL SIGNALS (Red Triangle Down ▼)

Signal 1: Rejection from Resistance Levels

• Price rallies to 0%, 50%, or 100% level and reverses

• Best when combined with bearish candlestick pattern (shooting star, bearish engulfing)

• Entry: On signal confirmation

• Stop Loss: Above the resistance level (0.5-1% above)

• Target: Next octave level down (87.5%, 75%, 50%)

Signal 2: Breakdown Below Support

• Price breaks below 50% or 0% level with momentum

• Confirms trend continuation or reversal

• Entry: On close below the level

• Stop Loss: Above the breakdown level

• Target: Previous swing low or next major level

Signal 3: Gann Angle Resistance

• Price fails at 1x1 angle (black line)

• Indicates trend weakness

• Entry: When price rejects the angle

• Stop Loss: Above the 1x1 angle

• Target: Next support level

________________________________________

Advanced Trading Techniques

1. The 50% Rule (Most Powerful)

The 50% octave level is the most critical in Gann theory:

• In Uptrend: Price should not break below 50% retracement. If it holds = trend intact, go long.

• In Downtrend: Price should not break above 50% retracement. If it holds = trend intact, go short.

• Reversal: Breaking and closing beyond 50% often signals trend reversal.

2. Gann Angle Confluence

When multiple Gann angles converge with octave levels = HIGH probability zone:

• Look for price to bounce or reverse at these zones

• Example: 1x2 angle meets 50% level = strong support/resistance

• These zones often become pivot points

3. Multiple Timeframe Analysis

• Use higher timeframe (daily) for major structure

• Use lower timeframe (5min, 15min) for precise entries

• Take trades when both timeframes align

4. Swing Failure Pattern

• Price breaks a key level (e.g., 50%) but quickly reverses back

• This "false breakout" often leads to strong move in opposite direction

• Wait for signal in the reversal direction

________________________________________

Settings Optimization

For Day Trading (Scalping)

• Structure Period: 0-2 (22 bars or less)

• Number of Swings: 1 (only current structure)

• Signal Sensitivity: High

• Swing Tracker: OFF (cleaner)

For Swing Trading

• Structure Period: 4-5 (44-88 bars)

• Number of Swings: 2-3

• Signal Sensitivity: Medium

• Swing Tracker: ON or OFF (preference)

For Position Trading

• Structure Period: 6-8 (176+ bars)

• Number of Swings: 3-5

• Signal Sensitivity: Low

• Swing Tracker: ON

________________________________________

Common Patterns to Watch

Bullish Reversal Setup

1. Price in bearish structure (red levels)

2. Price drops to 100% level (swing low)

3. Buy signal appears (green triangle)

4. Price breaks back above 50% level

5. Action: Go long with stop below 100%

Bearish Reversal Setup

1. Price in bullish structure (green levels)

2. Price rises to 100% level (swing high)

3. Sell signal appears (red triangle)

4. Price breaks back below 50% level

5. Action: Go short with stop above 100%

Trend Continuation

1. Price respects 1x1 Gann angle

2. Small pullback to 25% or 37.5% level

3. Buy/sell signal appears

4. Action: Enter in trend direction

________________________________________

________________________________________

Signal Sensitivity Guide

• Low: Conservative, only major breakouts (3-5 signals per day)

• Medium: Balanced, includes approaches (5-10 signals per day)

• High: Aggressive, includes bounces (10-20 signals per day)

Choose based on your trading style and risk tolerance

________________________________________

Final Words

This indicator is a powerful tool, but remember:

"The market is never wrong. Opinions are." - W.D. Gann

• No indicator is 100% accurate

• Always combine with price action and volume

• Backtest on your instrument and timeframe

• Keep learning and adapting your strategy

• Discipline and risk management are more important than the perfect setup

Happy Trading! 📈

Momentum Structural AnalysisMomentum Structural Analysis (MSA‑style Oscillator)

This indicator implements a simple, MSA‑style momentum oscillator that measures how far price has moved above or below its own long‑term trend on the active timeframe, expressed in percentage terms. Instead of looking at raw price, it "oscillates" price around a timeframe‑appropriate simple moving average (SMA) and plots the percentage distance from that SMA as an orange line around a zero baseline. Zero means price is exactly at its structural trend; positive values mean price is extended above trend; negative values mean it is trading below trend.

The script automatically selects the SMA length based on the chart timeframe:

On daily charts it uses the configurable Daily SMA Length (default 252 trading days, roughly 1 year).

On weekly charts it uses Weekly SMA Length (default 208 weeks).

On monthly charts it uses Monthly SMA Length (default 120 months).

This approach is inspired by the ideas behind Momentum Structural Analysis (MSA), which studies where a market trades relative to long‑term moving averages and then treats the momentum line (the oscillator) as the primary object of analysis. The goal is to highlight structural overbought/oversold conditions and regime changes that are often clearer on momentum than on the raw price chart.

--------------------------------------------------

What the script computes and how it works

For each bar, the indicator:

Chooses an SMA length based on the current timeframe (daily/weekly/monthly).

Calculates the SMA of the close.

Computes the percentage distance:

\text{Diff %} = \frac{\text{Close} - \text{SMA}}{\text{SMA}} \times 100

Plots this Diff % as an orange line, with a dashed horizontal zero line as the base.

This produces a momentum oscillator that oscillates around zero and reflects the "structural" position of price versus its own long‑term mean.

--------------------------------------------------

How to use it on index charts (e.g., NIFTY50)

On indices like NIFTY50, use the indicator to see how stretched the index is versus its structural trend.

Typical uses:

Identify extremes: a). Historically high positive readings can signal euphoric, late‑stage conditions where risk is elevated. b). Deep negative readings can highlight panic/capitulation zones where downside may be exhausted.

Draw structural levels: a). Mark horizontal bands on the oscillator where past turns have occurred (e.g., +15%, −10%, etc. specific to NIFTY50). b). Watch how price behaves when the oscillator revisits these zones: repeated rejections can validate them as structural bounds; clean breaks can indicate a change of regime.

This is not a buy/sell signal generator by itself; it is a framework to understand where the index sits within its long‑term momentum structure and to support risk‑management decisions.

--------------------------------------------------

How to use it on ratio charts

Apply the same indicator to ratio symbols such as NIFTY50/GOLD, BANKNIFTY/NIFTY50, sector vs index, or any spread you plot as a ratio.

On a ratio chart:

The oscillator now measures relative momentum: how far that ratio is above or below its own long‑term mean.

High positive readings = strong outperformance of the numerator vs the denominator (e.g., equities strongly outperforming gold).

Deep negative readings = strong underperformance (e.g., equities structurally lagging gold).

This is very much in the spirit of MSA’s work on spreads between asset classes: it helps visualize major rotations (equities → gold, financials → commodities, etc.) and whether a relative‑performance trend is stretched, reverting, or breaking into a new phase.

--------------------------------------------------

Using multiple timeframes for better decisions

You can stack information across timeframes to get a more robust view:

Monthly : a). Use monthly charts to see secular/structural phases. b). Long multi‑year stretches above or below zero, and large bases or trendline breaks on the monthly oscillator, can mark major bull or bear cycles and big rotations between asset classes.

Weekly : a). Use weekly charts for the primary trend. b). Weekly structures (multi‑month highs/lows, channels, or trendlines on the oscillator) are useful for medium‑term positioning and for confirming or rejecting signals seen on the monthly view.

Daily : a). Use daily charts mainly for timing entries/exits once the higher‑timeframe direction is clear. b). Short‑term extremes on the daily oscillator that align with the larger weekly/monthly structure can offer better‑timed opportunities, while signals that contradict higher‑timeframe momentum are more likely to be noise.

--------------------------------------------------

LJ Parsons Adjustable expanding MRT Fibpapers.ssrn.com

Market Resonance Theory (MRT) reinterprets financial markets as structured multiplicative, recursive systems rather than linear, dollar-based constructs. By mapping price growth as a logarithmic lattice of intervals, MRT identifies the deep structural cycles underlying long-term market behaviour. The model draws inspiration from the proportional relationships found in musical resonance, specifically the equal temperament system, revealing that markets expand through recurring octaves of compounded growth. This framework reframes volatility, not as noise, but as part of a larger self-organising structure.