Cast ForwardThis indicator will not forecast price action. It will not predict price movement nor will it in any way predict the outcome of any trade you may take. This is not a signal for buying or selling. You must do your own back testing and analysis for trading.

Time and price are the two most important components of market data. Where was price at what time? To help visualize this question I created this indicator. It allows for the previous session data to be overlayed onto the chart offset forward 24 hours. What this means is that you have the high, (high/low)/2, and low of each candle plotted on top of your chart for the time frame of the current chart, but offset so that the data from the current candle has the data from the corresponding candle 24 hours prior lined up on the x-axis.

SMA Logic: I used the SMA (Simple Moving Average) function with a length of 1 to plot the data points without any smoothing to give the true values of the data.

For Intraday Charting

For Electronic Trading Hours:

In order to line up the data correctly, for intraday charts, I used the current chart timeframe and divided it into 1380 (number of minutes in the 23 hour futures market trading day) to set the data offset. Using the same math logic, this indicator also gives the correct correlated data on the 30 second time frame. If the chart time frame that is currently being used does not allow for correct data correlation (not a factor of 1380) it will not plot the data.

For Regular Trading Hours:

In order to line up the data correctly, for intraday charts, I used the current chart timeframe and divided it into 405 (number of minutes in the 6 hour 45 minutes New York regular session trading day, including the 15 minute settlement time) to set the data offset. This indicator also gives the correct correlated data on the 30 second time frame. If the chart time frame that is currently being used does not allow for correct data correlation (not a factor of 405) it will not plot the data.

For the Daily Chart:

This indicator plots a visualization of the 20-40-60 day IPDA data range; (The IPDA data range helps traders identify liquidity, price gaps, and equilibrium points in the market, providing insights for optimal trade entries and market structure shifts). It does this using the same SMA logic as the intraday plot. What this means is it offsets the historical data of the daily chart 20, 40, or 60 bars forward. You can plot any combination of the three on the chart at one time, but these will not show on the intraday chart. This allows for visualization of where the market will possibly seek liquidity, seek to rebalance, or seek equilibrium in the future.

Search in scripts for "TAKE"

Lot Size Calculator (CZ) This is upgraded version of existing Lot size Calculator from melodicfish.

I added CZK as a new base currency and translated the whole user interface into Czech language, so this version is made mainly for people from Czech Republic.

Here is the original code description from the original creator:

This is a public release of my Lot Size Calculator. I received a request for the code from a user so I am republishing the script so I can make it public (TV doesn't seem to give me the option to simply make it public once published ).

This is a very simple script to use. Simply choose your entry level and stop level on the chart and the indicator will calculate the lots. You can change your account risk and base currency units in the settings along with changing the scaling of the calculation to adjust the results with the lot sizing units of your broker. This allows the calculator to be used with CFDs, forex, Gold, etc.. Hope it helps in your trading it has been the single most useful tool in my trading as it has helped me always keep my risk locked up and on point that is why I released it.

One final quick note: Remember you can save your settings for your own account size and risk so you do not always have to modify the defaults when loading the script. Just a ease of use tip. I only add the script to my chart when I am about to take a trade so it is helpful to have everything set up in advance.

As i said, the whole user interface is in Czech language, but you can find exactly the same indicator in english language under the name Lot Size Calculator by melodicfish. So i hope i don´t need to provide english translation here.

I hope this time it won´t get taken down :( :D

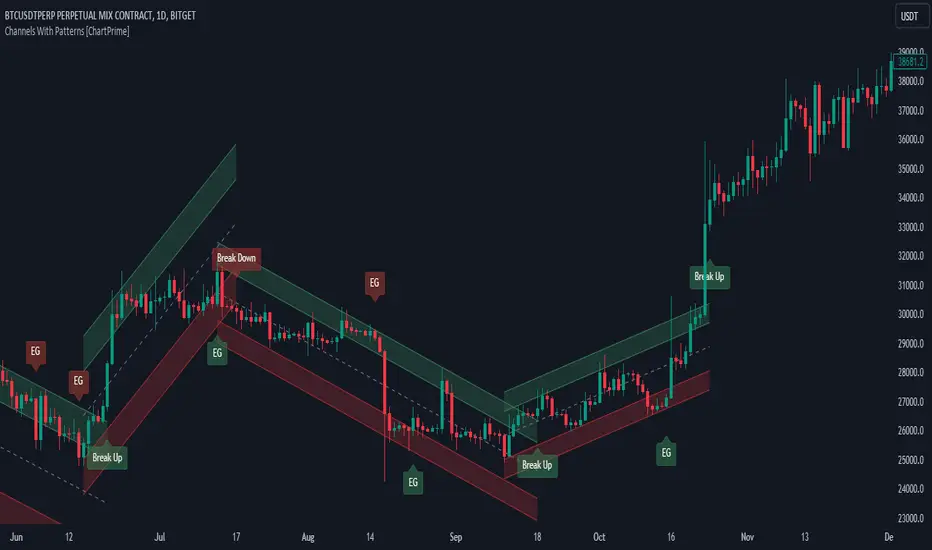

Channels With Patterns [ChartPrime]The Channels With Patterns indicator is an attempt at minimizing the delay in forming a trend channel. This indicator uses a single pivot in conjunction with a smooth version of the price to estimate the direction of an emerging trend. Using ATR, this indicator estimates the volatility of the new trend by adjusting the channel size by a multiple of the current ATR.

One of the biggest complains for any trend indicator is that it takes too long to create a channel or trend line. This indicator estimates the trend channel by checking if the price is moving in the correct direction and then it projects the channel from a single pivot. To allow for some margin of error, this script uses an offset to help center the channel.

This offset is generated from the ATR at the time of formation. In conjunction with forming estimated trend channels, this indicator features select candle stick patterns. These candle stick patterns are filtered by location in the formed trend channel. If the price is within an extremity of the trend channel it will appear. Filtering classical vanilla candle stick patterns using this methodology can result in some interesting results and possible confluence points for traders. For example; a bearish hammer appearing when filtered in an upper zone might add an extra level of realtime unique confluence traders.

Traders can use this script as a general trend line indicator that is a bit more forward looking than others, or it can be used it as its full blown trend channel estimator. Due to the fact that this is an estimate using the minimum possible information to make the channel, its accuracy will not always be perfect and can suffer compared to alternative methods.

When configuring the indicator it is important to understand the role of each input. Here is a description of all of the settings provided:

Presets (`preset`): This input allows users to quickly configure the indicator based on the market they are trading in. Selecting "Stocks," "Forex," or "Crypto" automatically adjusts various parameters to settings deemed optimal for these markets. The "User" option lets traders manually configure settings for a more personalized approach.

Style (`style`): This setting determines how pivot points are calculated. "Wick" uses the high and low of candlesticks (including wicks), which can be more sensitive to market extremes. "Body" uses only the open and close prices (the body of the candlesticks), potentially offering a more stable pivot point calculation.

Break Style (`break_style`): This option defines what price is used to determine if a channel has been broken. "Close" uses the closing price of a candlestick, while "High/Low" uses the highest and lowest prices. This affects how channel breaks are identified and can influence trading signals.

Instant Mode (`instant`): When enabled, this feature allows the indicator to form channels more quickly by initiating them as soon as potential formations are detected. This can provide earlier signals but may increase the risk of false positives.

ATR Length (`atr_length`): This input sets the period for the Average True Range (ATR), a common volatility indicator. A longer ATR period may smooth out the channel but could delay responsiveness to market changes. A shorter period might make the channel more responsive but potentially more erratic.

Offset Center (`offset`): Adjusts the vertical positioning of the channel. This can help in aligning the channel more accurately with the price action, depending on market conditions and personal trading strategies.

Size (`atr_multiplier`): Alters the channel's size relative to the ATR. A higher multiplier makes a wider channel, which might be useful in more volatile markets. A lower multiplier tightens the channel, which could be better for less volatile conditions.

Padding % (`padding`): This setting adjusts the padding within the top and bottom quarters of the channel. It essentially fine-tunes the channel's sensitivity to price movements near its boundaries.

Pivot Length (`pivot_length`): Determines the number of bars used to calculate pivot points. A longer length may provide more significant pivot points but can reduce the number of channels formed.

Pivot Look Forward (`look_forward`): Sets the number of bars to look forward in the pivot calculation, affecting how quickly the channel adapts to new pivots.

Average H/L Length (`avg_length`): Controls the smoothing of the high and low prices used in the channel calculation. A longer average length can lead to smoother, more gradual channel slopes.

Enable Hammer (`enable_hammer`): When enabled, the indicator will highlight Hammer candlestick patterns, which are often considered bullish reversal indicators.

Enable Inverted Hammer (`enable_ihammer`): This toggles the display of Inverted Hammer patterns, typically viewed as potential bullish reversal signals.

Enable Bullish Engulfing (`enable_bullish_engulfing`): Enables the identification of Bullish Engulfing patterns, another type of bullish reversal indicator.

Enable Bearish Engulfing (`enable_bearish_engulfing`): When activated, this highlights Bearish Engulfing patterns, which are often interpreted as bearish reversal signals.

Extend Channel (`extend`): This option, when enabled, extends the drawn channels forward until they are either broken or a new channel is formed.

Show Break Label (`show_break_label`): Toggles the display of labels indicating where the channel has been broken, providing visual cues for potential trade entries or exits.

Channel History Length (`history_length`): Determines how many historical channels are displayed on the chart. This can be useful for analyzing past performance and patterns.

Channel Colors (`top_color`, `bottom_color`, `center_color`): These settings allow customization of the channel's appearance by setting the colors of the top, bottom, and center lines.

Line Transparency (`line_trans`): Adjusts the transparency of the channel lines, helping to balance visibility with chart readability.

Center Line Transparency (`center_trans`): Specifically sets the transparency level of the center line of the channel.

Channel Fill Transparency (`fill_trans`): Modifies the transparency of the filled areas between the channel lines, which can enhance chart clarity and focus on the price action.

Break Colors (`break_up_color`, `break_down_color`): Sets the colors for labels that appear when the channel is broken, either upwards or downwards.

Break Label Text Color (`text_color`): Determines the color of the text in the break labels, enhancing readability based on the chart's background and color scheme.

Candle Pattern Colors (`h_color`, `ih_color`, `bullish_engulfing_color`, `bearish_engulfing_color`): These inputs allow for the customization of the colors used to highlight various candle patterns on the chart.

Candle Pattern Text Color (`candle_text_color`): Sets the color of the text for labels associated with candle pattern indicators.

Alerts (`new_channel_alert`, `break_alert`, `hammer_alert`, `ihammer_alert`, `bullish_engulfing_alert`, `bearish_engulfing_alert`): These toggles enable or disable alerts for different events, such as the formation of new channels, channel breaks, or the appearance of specific candle patterns. This feature is crucial for traders who rely on timely notifications for potential trading opportunities.

We have provided a few presets to allow you to get a feeling for how the indicator works with different settings easily. Here is a description of the settings used in each preset:

Stocks Preset:

Style: "Wick"

Break Style: False (High/Low)

Instant Mode: True

ATR Length: 10

Size (ATR Multiplier): 4

Pivot Length: 10

Pivot Look Forward: 15

Average H/L Length: 18

Forex Preset:

Style: "Wick"

Break Style: False (High/Low)

Instant Mode: True

ATR Length: 100

Size (ATR Multiplier): 5

Pivot Length: 10

Pivot Look Forward: 15

Average H/L Length: 18

Crypto Preset:

Style: "Wick"

Break Style: False (High/Low)

Instant Mode: True

ATR Length: 10

Size (ATR Multiplier): 4

Pivot Length: 10

Pivot Look Forward: 15

Average H/L Length: 18

This script first starts by defining and collecting the relevant data for the main body of the code with data(). This generates the pivot data, the levels, the ranges, the averages, the deltas, and finally the candle sticks. Once there is a higher low, or lower high detected via the pivots and the current price it triggers the formation of the new channel. It takes the delta between the last pivot and the current average price and projects the trend channel using this delta. If the price exceeds the extremities of the channel it will classify this as a break from the estimated structure and begin looking for a new channel. The idea is that when trending, the price will oscillate between extremities as defined by a range and direction. If the price is inside of one of these extremities the script will look for candle stick patterns. This is how the script operates.

On a more technical level, this script is meant to showcase Pine Script's custom types and methods. We have made use of a properties pattern allows functions to use a minimal number of arguments. This allows you to add new inputs without modifying a string of functions. The use of methods and data structures allows the main body of the code to be easy to understand and for the script as a whole to be easily modified. We have made sure that the script is modular so that users can incorporate this into their own custom scripts. It should be easy to expand on this script as the main logic is fairly compact and open for easy modification. All features are packed into their own function for easy use elsewhere. This is particularly evident in the candle stick section. I have simplified the process of creating candle stick patterns by creating a type. All users have to do is make methods for this type.

candle()=>

polarity = open < close

body_top = math.max(open, close)

body_bottom = math.min(open, close)

body_range = body_top - body_bottom

top_wick = high - body_top

bottom_wick = body_bottom - low

average_body = ta.ema(body_range, 14)

average_top_wick = ta.ema(top_wick, 14)

average_bottom_wick = ta.ema(bottom_wick, 14)

has_body = body_range != 0

has_top_wick = top_wick != 0

has_bottom_wick = bottom_wick != 0

above_average_body = body_range > average_body

above_average_top_wick = top_wick > average_top_wick

above_average_bottom_wick = bottom_wick > average_bottom_wick

candle_data.new(

polarity

, body_top

, body_bottom

, body_range

, top_wick

, bottom_wick

, average_body

, average_top_wick

, average_bottom_wick

, has_body

, has_top_wick

, has_bottom_wick

, above_average_body

, above_average_top_wick

, above_average_bottom_wick

)

In conclusion, this script offers a blend of rapid trend channel formation and candlestick pattern recognition, making it a unique tool for traders looking for a more proactive approach to trend analysis.

Fair Value Gap Finder with Integrated Gann BoxTitle: Fair Value Gap Finder with Integrated Gann Box Analysis

Description:

The "Fair Value Gap Finder with Integrated Gann Box Analysis" is a unique technical indicator designed for traders who wish to incorporate the concepts of Fair Value Gaps (FVG) and Gann Box methodologies into their trading strategy. This tool is beneficial for both trend-following and scalping techniques across various markets and timeframes.

Functionality:

The indicator identifies Fair Value Gaps, which are areas on the chart where price has skipped a range, creating a 'gap'. Recognizing these zones can be crucial for understanding potential price support and resistance areas. Alongside FVG detection, this script employs Gann Box principles to project potential levels of interest. Gann Boxes are drawn automatically when an FVG is identified, providing additional insights based on W.D. Gann's theories, which relate to time and price symmetry.

Usage:

Upon detecting an FVG, the indicator will highlight the gap on the chart and overlay a Gann Box between the high and low points of the gap. Traders can use these zones to make informed decisions about entry and exit points, stop loss, and take profit levels. The script offers customization options for the appearance and behavior of the FVG boxes and Gann Lines, allowing users to adapt the tool to their preferences.

Originality:

What sets this indicator apart is the integration of FVG with Gann Box levels within a single tool, streamlining the analysis process. It takes the classic approach of identifying gaps and enriches it with the geometric significance of Gann's work, all while allowing users to visualize and interact with these levels in a user-friendly manner.

Open-Source Nature:

This script is open-source, making it a transparent solution for those who wish to understand the underlying calculations. While not all traders are versed in Pine Script, the logic of identifying FVGs and applying Gann Box levels is explained through the script's annotations and the user interface itself.

Instructions for Use:

Apply the script to your chart, and it will automatically detect FVGs.

Adjust the settings in the indicator's input menu to match your trading style and preferences.

Use the FVG and Gann Box levels as potential areas of interest for trade setups.

This script does not guarantee profits and should be used as part of a comprehensive trading plan. It is best used in conjunction with other analysis methods to confirm signals and strategies.

BreakoutTrendFollowingINFO:

The "BreakoutTrendFollowing" indicator is a comprehensive trading system designed for trend-following in various market environments. It combines multiple technical indicators, including Moving Averages (MA), MACD, and RSI,

along with volume analysis and breakout detection from consolidation, to identify potential entry points in trending markets. This strategy is particularly effective for assets that exhibit strong trends and significant price movements.

Note that using the consolidation filter reduces the amount of entries the strategy detects significantly, and needs to be used if we want to have an increased confidence in the trend via breakout.

However, the strategy can be easily transformed to various only trend-following strategies, by applying different filters and configurations.

The indicator can be used to connect to the Signal input of the TTS (TempalteTradingStrategy) by jason5480 in order to backtest it, thus effectively turning it into a strategy (instructions below in TTS CONNECTIVITY section)

DETAILS:

The strategy's core is built upon several key components:

Moving Average (MA): Used to determine the general trend direction. The strategy checks if the price is above the selected MA type and length.

MACD Filter: Analyzes the relationship between two moving averages to confirm the trend's momentum.

Consolidation Detection: Identifies periods of price consolidation and triggers trades on breakouts from these ranges.

Volume Analysis: Assesses trading volume to confirm the strength and validity of the breakout.

RSI: Used to avoid overbought conditions, ensuring trades are entered in favorable market situations.

Wick filters: make sure there is not a long wick that indicates selling pressure from above

The strategy generates buy signals when several conditions are met concurrently (each one of them can be individually enabled/disabled)"

The price is above the selected MA.

A breakout occurs from a configurable consolidation range.

The MACD line is above the signal line, indicating bullish momentum.

The RSI is below the overbought threshold.

There's an increase in trading volume, confirming the breakout's strength.

Currently the strategy fires SL signals, as the approach is to check for loss of momentum - i.e. crossunder of the MACD line and signal line, but that is to everyone to determine the exit conditions.

The buy and SL signals are set on the chart using green or orange triangles on the below/above the price action.

SETTINGS:

Users can customize various parameters, including MA type and period, MACD settings, consolidation length, and volume increase percentage. The strategy is equipped with alert conditions for both entry (buy signals) and exit (set stop loss) points, facilitating both manual and automated trading.

Each one of the technical indicators, as well as the consilidation range and breakout/wick settings can be configured and enabled/disabled individually.

Please thoroughly review the available settings of the script, but here is an outline of the most important ones:

Use bar wicks (instead of open/close) - the ref_high/low will be taken based on the bar wicks, rather than the open/close when determining the breakout and MA

Enter position only on green candles - additional filters to make sure that we enter only on strong momentum

MA Filter: (enable, source, type, length) - general settings for MA filter to be checked against the stock price (close or upper wick)

MACD Filter: (enable, source, Osc MA type, Signal MA type, Fast MA length, Slow MA length, Low MACD Hist) - detailed settings for fine MACD tuning

Consolidation:

Consolidation Type: we have two different ways of detecting the consolidation, note the types below.

CONSOLIDATION_BASIC - consolidation areas by looking for the pivot point of a trend and counts the number of bars that have not broken the consolidation high/low levels.

CONSOLIDATIO_RANGE_PERCENT - identifies consolidation by comparing the range between the highest and lowest price points over a specified period.

So in summary the CONSOLIDATIO_RANGE_PERCENT uses a percentage-based range to define consolidation, while CONSOLIDATION_BASIC uses a count of bars within a high-low range to establish consolidation.

Thus the former is more focused on the tightness of the price range, whereas the latter emphasizes the duration of the consolidation phase.

The CONSOLIDATIO_RANGE_PERCENT might be more sensitive to recent price movements and suitable for shorter-term analysis, while CONSOLIDATION_BASIC could be better for identifying longer-term consolidation patterns.

Min consolidation length - applicable for CONSOLIDATION_BASIC case, the min number of bars for the price to be in the range to consider consolidation

Consolidation Loopback period - applicable for CONSOLIDATION_BASIC case, the loopback number of bars to look for consolidation

Consolidation Range percent - applicable for CONSOLIDATIO_RANGE_PERCENT, the percent between the high and low in the range to consider consolidation

Plot consolidation - enables plotting of the consolidation (only for debug purposes)

Breakout: (enable, low, high) - the definition of the breakout from the previous consolidation range, the price should be between to determine the breakout as successfull

Upper wick: (enable, percent) - defines the percent of the upper wick compared to the whole candle to allow breakout (if the wick is too big part of the candle we can consider entering the position riskier)

RSI: (enable, length, overbought) - general settings for RSI TA

Volume (enbale, percentage increase, average volume filter en, loopback bars) - percentage of increase of the volume to consider for a breakout. There are two modes - percentage increase compared to the previous bar, or percentage against the average volume for the last loopback bars.

Note that there are many different configuration that you can play with, and I believe this is the strength of the strategy, as it can provide a single solution for different cases and scenarios.

My advice is to try and play with the different options for different markets based on the approach you want to implement and try turning features on/off and tuning them further.

TTS SETTINGS (NEEDED IF USED TO BACKTEST WITH TTS):

The TempalteTradingStrategy is a strategy script developed in Pine by jason5480, which I recommend for quick turn-around of testing different ideas on a proven and tested framework

I cannot give enough credit to the developer for the efforts put in building of the infrastructure, so I advice everyone that wants to use it first to get familiar with the concept and by checking

by checking jason5480's profile www.tradingview.com

The TTS itself is extremely functional and have a lot of properties, so its functionality is beyond the scope of the current script -

Again, I strongly recommend to be thoroughly explored by everyone that plans on using it.

In the nutshell it is a script that can be feed with buy/sell signals from an external indicator script and based on many configuration options it can determine how to execute the trades.

The TTS has many settings that can be applied, so below I will cover only the ones that differ from the default ones, at least according to my testing - do your own research, you may find something even better :)

The current/latest version that I've been using as of writing and testing this script is TTSv48

Settings which differ from the default ones:

Deal Conditions Mode - External (take enter/exit conditions from an external script)

🔌Signal 🛈➡ - BreakoutTrendFollowing: 🔌Signal to TTS (this is the output from the indicator script, according to the TTS convention)

Order Type - STOP (perform stop order)

Distance Method - HHLL (HigherHighLowerLow - in order to set the SL according to the strategy definition from above)

The next are just personal preferences, you can feel free to experiment according to your trading style

Take Profit Targets - 0 (either 100% in or out, no incremental stepping in or out of positions)

Dist Mul|Len Long/Short- 10 (make sure that we don't close on profitable trades by any reason)

Quantity Method - EQUITY (personal backtesting preference is to consider each backtest as a separate portfolio, so determine the position size by 100% of the allocated equity size)

Equity % - 100 (note above)

FX Forecasting Model [TrendX_]FX Forecasting Model indicator is a forecasting tool that takes advantages of macroeconomic analysis and market surveillance to predict Exchange rate movement.

*** Customize the macro data for home country (base currency) and foreign country

USAGE

This consists of 4 editable options align with 4 Forecasting Models

TrendX Model)

TrendX Model is a type of multiple linear regression, which is a statistical method that estimates the relationship between the currency exchange rate and various macroeconomic indicators.

*** Remember the 1st thing to do is to customize the macro data for home country (base currency) and foreign country, before take any further steps.

Purchasing Power Parity (PPP Model)

The PPP model is a conceptual model of currency exchange. The model illustrates how the exchange rate between two countries’ currencies is influenced by the variations in the prices of goods and services in those countries, which depend on the inflation rate. The activity of buying and selling goods and services internationally will shift the exchange rate to balance the prices in both countries.

Interest Rate Parity (IRP Model)

Interest Rate Parity (IRP) model is a theoretical model that relates the interest rates and the exchange rates of two countries. According to IRP, the difference between the forward and spot exchange rates of two currencies should be equal to the difference between their interest rates. IRP helps traders to determine the fair value of a currency pair and compare it with the market value. If the market value deviates from the fair value, then there is a potential for arbitrage or hedging.

Combined Forecast Model (Mixed Model)

Since each model has its own advantages, many people are interested in the concept of using a mix of forecasts to get better results than any single forecast. Mix Model is a method that uses different proportions of the forecasts from three models: TrendX, PPP and IRP models. The default proportion is 0.2 for TrendX, and 0.4 for both PPP and IRP. You can change these proportions according to your liking.

CONCLUSION

FX Forecasting Model Indicator is very practical for FOREX traders who wants to make informed and rational decisions based on Macroeconomic Analysis. It can help find arbitrage opportunity in currency exchange market. Accordingly, it can also be helpful for traders to use alongside other forms of Technical Analysis.

DISCLAIMER

The results achieved in the past are not all reliable sources of what will happen in the future. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur.

Therefore, you should always exercise caution and judgment when making decisions based on past performance.

Backtesting ModuleDo you often find yourself creating new 'strategy()' scripts for each trading system? Are you unable to focus on generating new systems due to fatigue and time loss incurred in the process? Here's a potential solution: the 'Backtesting Module' :)

INTRODUCTION

Every trading system is based on four basic conditions: long entry, long exit, short entry and short exit (which are typically defined as boolean series in Pine Script).

If you can define the conditions generated by your trading system as a series of integers, it becomes possible to use these variables in different scripts in efficient ways. (Pine Script is a convenient language that allows you to use the integer output of one indicator as a source in another.)

The 'Backtesting Module' is a dynamic strategy script designed to adapt to your signals. It boasts two notable features:

⮞ It produces a backtest report using the entry and exit variables you define.

⮞ It not only serves for system testing but also to combine independent signals into a single system. (This functionality enables to create complex strategies and report on their success!)

The module tests Golden and Death cross signals by default, when you enter your own conditions the default signals will be neutralized. The methodology is described below.

PREPARATION

There are three simple steps to connect your own indicator to the Module.

STEP 1

Firstly, you must define entry and exit variables in your own script. Let's elucidate it with a straightforward example. Consider a system generating long and short signals based on the intersections of two moving averages. Consequently, our conditions would be as follows:

// Signals

long = ta.crossover(ta.sma(close, 14), ta.sma(close, 28))

short = ta.crossunder(ta.sma(close, 14), ta.sma(close, 28))

Now, the question is: How can we convert boolean variables into integer variables? The answer is conditional ternary block, defined as follows:

// Entry & Exit

long_entry = long ? 1 : 0

long_exit = short ? 1 : 0

short_entry = short ? 1 : 0

short_exit = long ? 1 : 0

The mechanics of the Entry & Exit variables are simple. The variable takes on a value of 1 when your trading system generates the signal and if your system does not produce any signal, variable returns 0. In this example, you see how exit signals can be generated in a trading system that only contains entry signals. If you have a system with original exit signals, you can also use them directly. (Please mind the NOTES section below).

STEP 2

To utilize the Entry & Exit variables as source in another script, they must be plotted on the chart. Therefore, the final detail to include in the script containing your trading system would be as follows:

// Plot The Output

plot(long_entry, "Long Entry", display=display.data_window, editable=false)

plot(long_exit, "Long Exit", display=display.data_window, editable=false)

plot(short_entry, "Short Entry", display=display.data_window, editable=false)

plot(short_exit, "Short Exit", display=display.data_window, editable=false)

STEP 3

Now, we are ready to test the system! Load the Backtesting Module indicator onto the chart along with your trading system/indicator. Then set the outputs of your system (Long Entry, Long Exit, Short Entry, Short Exit) as source in the module. That's it.

FEATURES & ORIGINALITY

⮞ Primarily, this script has been created to provide you with an easy and practical method when testing your trading system.

⮞ I thought it might be nice to visualize a few useful results. The Backtesting Module provides insights into the outcomes of both long and short trades by computing the number of trades and the success percentage.

⮞ Through the 'Trade' parameter, users can specify the market direction in which the indicator is permitted to initiate positions.

⮞ Users have the flexibility to define the date range for the test.

⮞ There are optional features allowing users to plot entry prices on the chart and customize bar colors.

⮞ The report and the test date range are presented in a table on the chart screen. The entry price can be monitored in the data window.

⮞ Note that results are based on realized returns, and the open trade is not included in the displayed results. (The only exception is the 'Unrealized PNL' result in the table.)

STRATEGY SETTINGS

The default parameters are as follows:

⮞ Initial Balance : 10000 (in units of currency)

⮞ Quantity : 10% of equity

⮞ Commission : 0.04%

⮞ Slippage : 0

⮞ Dataset : All bars in the chart

For a realistic backtest result, you should size trades to only risk sustainable amounts of equity. Do not risk more than 5-10% on a trade. And ALWAYS configure your commission and slippage parameters according to pessimistic scenarios!

NOTES

⮞ This script is intended solely for development purposes. And it'll will be available for all the indicators I publish.

⮞ In this version of the module, all order types are designed as market orders. The exit size is the sum of the entry size.

⮞ As your trading conditions grow more intricate, you might need to define the outputs of your system in alternative ways. The method outlined in this description is tailored for straightforward signal structures.

⮞ Additionally, depending on the structure of your trading system, the backtest module may require further development. This encompasses stop-loss, take-profit, specific exit orders, quantity, margin and risk management calculations. I am considering releasing improvements that consider these options in future versions.

⮞ An example of how complex trading signals can be generated is the OTT Collection. If you're interested in seeing how the signals are constructed, you can use the link below.

THANKS

Special thanks to PineCoders for their valuable moderation efforts.

I hope this will be a useful example for the TradingView community...

DISCLAIMER

This is just an indicator, nothing more. It is provided for informational and educational purposes exclusively. The utilization of this script does not constitute professional or financial advice. The user solely bears the responsibility for risks associated with script usage. Do not forget to manage your risk. And trade as safely as possible. Best of luck!

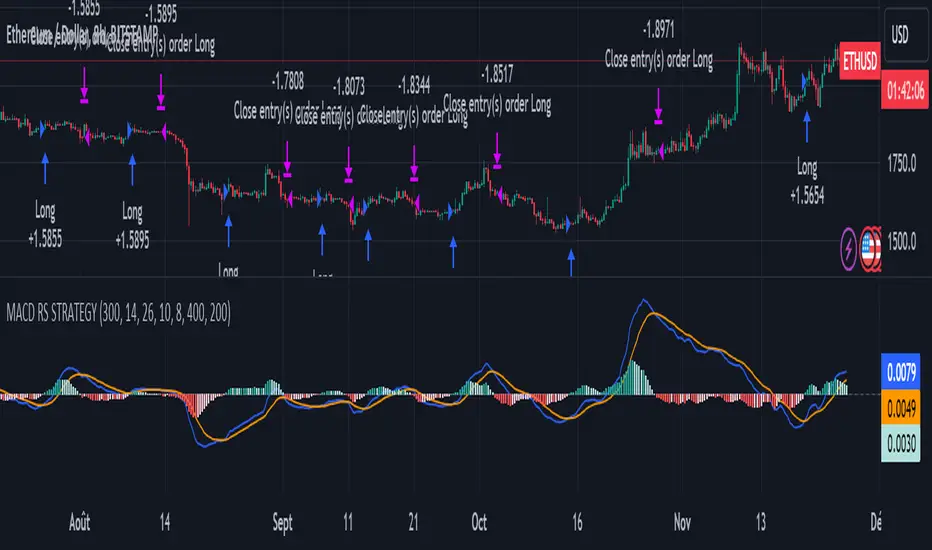

MACD of Relative Strenght StrategyMACD Relative Strenght Strategy :

INTRODUCTION :

This strategy is based on two well-known indicators: MACD and Relative Strenght (RS). By coupling them, we obtain powerful buy signals. In fact, the special feature of this strategy is that it creates an indicator from an indicator. Thus, we construct a MACD whose source is the value of the RS. The strategy only takes buy signals, ignoring SHORT signals as they are mostly losers. There's also a money management method enabling us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RELATIVE STRENGHT :

RS is an indicator that measures the anomaly between momentum and the assumption of market efficiency. It is used by professionals and is one of the most robust indicators. The idea is to own assets that do better than average, based on their past performance. We calculate RS using this formula :

RS = close/highest_high(RS_Length)

Where highest_high(RS_Length) = highest value of the high over a user-defined time period (which is the RS_Length).

We can thus situate the current price in relation to its highest price over this user-defined period.

MACD (Moving Average Convergence - Divergence) :

This is one of the best-known indicators, measuring the distance between two exponential moving averages : one fast and one slower. A wide distance indicates fast momentum and vice versa. We'll plot the value of this distance and call this line macdline. The MACD uses a third moving average with a lower period than the first two. This last moving average will give a signal when it crosses the macdline. It is therefore constructed using the values of the macdline as its source.

It's important to note that the first two MAs are constructed using RS values as their source. So we've just built an indicator of an indicator. This kind of method is very powerful because it is rarely used and brings value to the strategy.

PARAMETERS :

RS Length : Relative Strength length i.e. the number of candles back to find the highest high and compare the current price with this high. Default is 300.

MACD Fast Length : Relative Strength fast EMA length used to plot the MACD. Default is 14.

MACD Slow Length : Relative Strength slow EMA length used to plot the MACD. Default is 26.

MACD Signal Smoothing : Macdline SMA length used to plot the MACD. Default is 10.

Max risk per trade (in %) : The maximum loss a trade can incur (in percentage of the trade value). Default is 8%.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. Default is 400, meaning that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:ETHUSD in 8h timeframe with the parameters set by default.

ENTER RULES :

The entry rules are very simple : we open a long position when the MACD value turns positive. You are therefore LONG when the MACD is green.

EXIT RULES :

We exit a position (whether losing or winning) when the MACD becomes negative, i.e. turns red.

RISK MANAGEMENT :

This strategy can incur losses, so it's important to manage our risks well. If the position is losing and has incurred a loss of -8%, our stop loss is activated to limit losses.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

Enjoy the strategy and don't forget to take the trade :)

Immediate rebalanceGuided by the new ICT tutoring, I create this versatile Immediate Rebalance indicator

This indicator shows a different way on how to view the "Spikes or Shadows", based on the direction of the price this indicator divides the "Spike or Shadows" into levels 0.5 - 0.75 - 0.25 Fibonacci, giving the possibility to view the levels both in normal or in pre-Macro times

The user has the possibility to:

- Choose to have Spike levels shown in MultiTimeframe

- Choose to show Sike levels only Bullish or only Bearish

- Choose to show Sike levels only in pre-Macro/Macro times

- Choose to view the maximum amount of levels with Max Show

The indicator must be used as ICT shows in its concepts, the indicator takes into consideration the last 2 candles already closed so on the candle that is forming it is possible to expect reactions on the levels it marks, below is an example of how to use it in MultiTimeframe

Below I show an example on how to set the indicator to see Immediate Rebalance in Macro times

Below is an example of when not to take the indicator into consideration

Blockunity Stablecoin Liquidity (BSL)Monitor the liquidity of the crypto market by tracking the capitalizations of the major Stablecoins.

Stablecoin Liquidity (BSL) is an ideal tool for visualizing data on major Stablecoins. The number of Stablecoins in circulation is one of the best indices of liquidity within the crypto market. It’s an important metric to keep an eye on, as an increase in the number of Stablecoins in circulation offers a great opportunity to see cryptoasset prices rise. The tool’s multiple on-board display modes enable analysis of its data in the best possible conditions.

The Idea

The goal is to provide the community with the ideal tool to visualize the liquidity of the crypto market, via the state of the market capitalizations of the major Stablecoins.

How to Use

The tool is very easy to use and interpret. First of all, let's distinguish two main elements:

The chart as 3 distinct display modes to let you observe data in the best possible conditions.

There is a panel that summarizes the market capitalizations of the main Stablecoins.

Display Mode: Cumulative

In Cumulative mode (default), the different capitalizations are displayed one on top of the other with colored bands.

You can see that when the number of Stablecoins in circulation increases, crypto asset prices enter an uptrend. And if the liquidity of Stablecoins dries up, the trend will become bearish.

Display Mode: Aggregated

Aggregated mode displays a single line, which is the sum of the different capitalizations, varying between green and red depending on the state of this data according to its moving average declared in the 'Aggregated MA Lengh' field.

You can thus easily see trend changes and therefore opportunities to enter or exit the crypto market.

Display Mode: Independent

The Independent mode also displays the different capitalizations, but detached from each other with labels.

This display mode is particularly interesting for studying transfers from one Stablecoin to another, as can be seen below.

Other Settings

You can choose whether or not to include each of the Stablecoins data, and configure their display color. Note that in 'Cumulative' display mode, the data is taken into account even if the box is unchecked.

How it Works

The tool works in a simple way: We take the market capitalization data of the Stablecoins that interest us, then we process them according to the different display modes.

Let us know if you would like other ways of visualizing this data!

The Ultimate Buy and Sell IndicatorThis indicator should be used in conjunction with a solid risk management strategy that does not over-leverage positions and uses stop-losses. You can not rely 100% on the signals provided by this indicator (or any other for that matter).

With that said, this indicator can provide some excellent signals.

It has been designed with a large number of customization options intended for advanced traders, but you do not HAVE to be an advanced user to simply use the indicator. I have tried to make it easy to understand, and this section will provide you with a better understanding of how to use it.

NOTE:

While NOT REQUIRED, I would recommend also finding my indicator called, "Ultimate RSI", which is designed to work together with this indicator (visually). They both contain the same settings and allow you to visualize changes made in this indicator that can not be displayed on the main chart.

This indicator creates it's own candles(bars), so you have to go into your main settings and turn off the "body, border and wick" color settings. Using a dark background is also recommended.

How does it work?

The indicator mainly relies on the RSI indicator with Bollinger Bands for signals. (Though not entirely)

First, there are something that I call "Watch Signals", which are various Bollinger Band crossing events. This could be the price crossing Bollinger Bands or the RSI crossing Bollinger Bands.

There are separate watch signals for buys and sells. Buy watch signals are colored orange to match the BUY signal candle color and Fuchsia (kind of a bright purple) to match SELL signal candles.

In order for most buy or sell signals to be created, there must first be a watch signal. There is a lookback period (or length) for watch signals to be used, and after that many candles (bars) have passed, they will be ignored. You can set a length to look back as well as a time to wait before creating any.

What this means is that if there has previously been (for instance) a sell signal. You can tell it to wait 10 bars before creating any buy watch signals. You can then also tell it that it should look back 10 bars from the current one in order to find any buy watch signals. This means that if you had it set up that way 10 to wait and 10 to validate, it would start allowing buy watch signals 11 bars after a sell, and then once you hit 20 bars, it will start leaving a gap (invisible to you) as the 10 bar lookback period starts moving forward with each new bar. This is useful in order to keep signals more spaced apart as some bad signals come quickly after another one.

Example: You may get a sell signal where the Bollinger bands are tight, then the price easily drops down into the lower band creating a buy watch signal, then you get a "fake" or short pump up and it says buy, but then drops dramatically afterwards. The wait period can ensure that the sell stays in effect longer before a buy is considered by blocking any buy watch signals for a period of time.

After you get a watch signal, the system then looks for various other things to happen to create buy or sell signals. This could be the RSI crossing the (slow) RSI Basis line (from its Bollinger bands), it could be the price crossing its basis line, it could be MACD crosses, it could even be RSI crossing certain levels. All of these are options. If you like the MACD strategy and want it to give you buy and sell signals from just MACD crosses, simply select that option for signals.

It is also able to use the first of any of the options that takes place.

I included an option to force alternating buy and sell signals, rather than showing groups of, or subsequent buy, buy, buy signals, for instance.

Moving on....

You can change the moving average that is used to calculate the RSI. The standard moving average for RSI is the RMA (aka SWMA). Changes to this can dramatically change your signals. You also have the option to change the moving average type used in the Bollinger bands calculation. You can change the length of these as well. The same goes for the Bollinger bands over the Price chart. I added an ATR option for the RSI Bollinger bands to play with, as well. You are able to adjust the standard deviation (multiplier) of the bands as well, which will of course affect the signals.

The ways you can play with signals are nearly infinite, so have fun figuring it out.

The indicator allows for moving averages to be shown as well, with a variety of types to choose from. The standard numbers are 5, 10, 20, 50, 100 and 200, with the addition of a custom moving average of your choice. You can also change the color of this one. You can choose to show them all or any of them you want to show, in any combination, although the TYPE of moving average (SMA, EMA, WMA, etc.) will apply to all of them.

You may also notice the Bollinger Bands over the Price are colored, and become more or less transparent.

The color is derived from the trend of the RSI or the RSI basis (your choice). It looks back at the value however many bars you want and compares the values and that's how it determines if it is trending up or down. Since RSI is a directional momentum indicator, this can be quite useful. If you see the bands are getting darker, this will explain why.

The indicator has a lookback period for determining the widest the bands (which measure volatility) have been over that period of time. This is the baseline. It then will make the bands disappear (by making them more transparent) if the volatility is low. This indicates that a change in volatility is coming and that price isn't really changing much compared to the past (default 500) bars. If they become bright, this is because price has started trending in a direction and volatility is increasing.

I should also note that the candles are colored based on RSI levels.

If you use the Ultimate Companion indicator, you will be able to see the RSI levels (zones) that the colors are based on. As RSI moves into a new range, the candle color will change.

I have created a yellow zone where the candles turn yellow. This is when RSI is between (default) 45 and 55, indicating there is basically no momentum and price is going sideways. This is a good place to get trapped in bad trades, and there is a Yellow RSI Filter to block signals in this area to keep you from entering bad trades.

Green candles indicate values over 55 (getting brighter as RSI rises) and red candles are RSI values under 45 (getting brighter as RSI values get lower). If you see white, this means RSI is either over 80 or under 20. A sharp reversal is almost always imminent at this stage.

When we talk about Buy and Sell Signals, they draw a green or red triangle and it literally says BUY or SELL. There is an option to color the background for added visibility. These signals do not "repaint", what this means is that they can be late. To account for this, I have included a background color that will flash as a warning that a buy or sell could be imminent, although it may fail to break through and set a buy or sell signal. This is simply an advanced warning. The reason is that sometimes a candle may be very large and you won't be told to buy or sell during the candle until the move is completely over and now you're getting in on the next one. That's not a great feeling, so I made it repaint the background color and not repaint the completed signal. You get the best of both worlds.

This indicator also uses complex logic to handle things.

When there is a buy signal, it enters into a state of having been bought, or a "bought state". The same for sells. If Force alternating signals is off, you could have more than one buy in a bought state, or more than one sell in a sell state. There is an option to color the background green during the full duration of a bought state, or red during the full duration of a sold state.

I have added divergence.

This shows that the lows or highs of RSI and PRICE are different. If RSI is making higher highs but the price is not, then the price is likely to follow this bullish divergence, if the opposite happens, it's bearish. It will draw a line on the chart connecting the highs and lows and call it bearish or bullish. You can adjust this as well.

I have an RSI High/Low filter. If the RSI basis (or average) is very high or low, you can block signal from this area since the price is likely to continue in that direction before actually reversing.

You can change the settings of the MACD if you choose to use it for signals, and if you want to see it, you'll have to run that indicator below the chart and match the settings to see what is going on, just like the RSI.

Going back to Watch Signals. You can also choose to require more than one watch signal if you choose. You can skip watch signals, so it will ignore the first or second one, whatever you want to do. You can color the background to show you where watch signals have been skipped.

Regarding the wait period for creating watch signals after a sell or after a buy, you can also color the background to see where these were blocked by the wait period.

Lastly you can choose which type of watch signals to use, or keep them from being shown on the chart. This allows you to study the history of how the asset you are trading behaves and customize the behavior of signals based on your study of it.

Everything in the settings area has tooltips, which will explain what that thing does to help you along this journey.

I hope this indicator (and perhaps Ultimate RSI alongside this) will help you take your trading to the next level.

Multi-TF AI SuperTrend with ADX - Strategy [PresentTrading]

## █ Introduction and How it is Different

The trading strategy in question is an enhanced version of the SuperTrend indicator, combined with AI elements and an ADX filter. It's a multi-timeframe strategy that incorporates two SuperTrends from different timeframes and utilizes a k-nearest neighbors (KNN) algorithm for trend prediction. It's different from traditional SuperTrend indicators because of its AI-based predictive capabilities and the addition of the ADX filter for trend strength.

BTC 8hr Performance

ETH 8hr Performance

## █ Strategy, How it Works: Detailed Explanation (Revised)

### Multi-Timeframe Approach

The strategy leverages the power of multiple timeframes by incorporating two SuperTrend indicators, each calculated on a different timeframe. This multi-timeframe approach provides a holistic view of the market's trend. For example, a 8-hour timeframe might capture the medium-term trend, while a daily timeframe could capture the longer-term trend. When both SuperTrends align, the strategy confirms a more robust trend.

### K-Nearest Neighbors (KNN)

The KNN algorithm is used to classify the direction of the trend based on historical SuperTrend values. It uses weighted voting of the 'k' nearest data points. For each point, it looks at its 'k' closest neighbors and takes a weighted average of their labels to predict the current label. The KNN algorithm is applied separately to each timeframe's SuperTrend data.

### SuperTrend Indicators

Two SuperTrend indicators are used, each from a different timeframe. They are calculated using different moving averages and ATR lengths as per user settings. The SuperTrend values are then smoothed to make them suitable for KNN-based prediction.

### ADX and DMI Filters

The ADX filter is used to eliminate weak trends. Only when the ADX is above 20 and the directional movement index (DMI) confirms the trend direction, does the strategy signal a buy or sell.

### Combining Elements

A trade signal is generated only when both SuperTrends and the ADX filter confirm the trend direction. This multi-timeframe, multi-indicator approach reduces false positives and increases the robustness of the strategy.

By considering multiple timeframes and using machine learning for trend classification, the strategy aims to provide more accurate and reliable trade signals.

BTC 8hr Performance (Zoom-in)

## █ Trade Direction

The strategy allows users to specify the trade direction as 'Long', 'Short', or 'Both'. This is useful for traders who have a specific market bias. For instance, in a bullish market, one might choose to only take 'Long' trades.

## █ Usage

Parameters: Adjust the number of neighbors, data points, and moving averages according to the asset and market conditions.

Trade Direction: Choose your preferred trading direction based on your market outlook.

ADX Filter: Optionally, enable the ADX filter to avoid trading in a sideways market.

Risk Management: Use the trailing stop-loss feature to manage risks.

## █ Default Settings

Neighbors (K): 3

Data points for KNN: 12

SuperTrend Length: 10 and 5 for the two different SuperTrends

ATR Multiplier: 3.0 for both

ADX Length: 21

ADX Time Frame: 240

Default trading direction: Both

By customizing these settings, traders can tailor the strategy to fit various trading styles and assets.

UtilsLibrary "Utils"

A collection of convenience and helper functions for indicator and library authors on TradingView

formatNumber(num)

My version of format number that doesn't have so many decimal places...

Parameters:

num (float) : (float) the number to be formatted

Returns: (string) The formatted number

getDateString(timestamp)

Convenience function returns timestamp in yyyy/MM/dd format.

Parameters:

timestamp (int) : (int) The timestamp to stringify

Returns: (int) The date string

getDateTimeString(timestamp)

Convenience function returns timestamp in yyyy/MM/dd hh:mm format.

Parameters:

timestamp (int) : (int) The timestamp to stringify

Returns: (int) The date string

getInsideBarCount()

Gets the number of inside bars for the current chart. Can also be passed to request.security to get the same for different timeframes.

Returns: (int) The # of inside bars on the chart right now.

getLabelStyleFromString(styleString, acceptGivenIfNoMatch)

Tradingview doesn't give you a nice way to put the label styles into a dropdown for configuration settings. So, I specify them in the following format: . This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

styleString (string)

acceptGivenIfNoMatch (bool) : (bool) If no match for styleString is found and this is true, the function will return styleString, otherwise it will return tradingview's preferred default

Returns: (string) The string expected by tradingview functions

getTime(hourNumber, minuteNumber)

Given an hour number and minute number, adds them together and returns the sum. To be used by getLevelBetweenTimes when fetching specific price levels during a time window on the day.

Parameters:

hourNumber (int) : (int) The hour number

minuteNumber (int) : (int) The minute number

Returns: (int) The sum of all the minutes

getHighAndLowBetweenTimes(start, end)

Given a start and end time, returns the high or low price during that time window.

Parameters:

start (int) : The timestamp to start with (# of seconds)

end (int) : The timestamp to end with (# of seconds)

Returns: (float) The high or low value

getPremarketHighsAndLows()

Returns an expression that can be used by request.security to fetch the premarket high & low levels in a tuple.

Returns: (tuple)

getAfterHoursHighsAndLows()

Returns an expression that can be used by request.security to fetch the after hours high & low levels in a tuple.

Returns: (tuple)

getOvernightHighsAndLows()

Returns an expression that can be used by request.security to fetch the overnight high & low levels in a tuple.

Returns: (tuple)

getNonRthHighsAndLows()

Returns an expression that can be used by request.security to fetch the high & low levels for premarket, after hours and overnight in a tuple.

Returns: (tuple)

getLineStyleFromString(styleString, acceptGivenIfNoMatch)

Tradingview doesn't give you a nice way to put the line styles into a dropdown for configuration settings. So, I specify them in the following format: . This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

styleString (string) : (string) Plain english (or TV Standard) version of the style string

acceptGivenIfNoMatch (bool) : (bool) If no match for styleString is found and this is true, the function will return styleString, otherwise it will return tradingview's preferred default

Returns: (string) The string expected by tradingview functions

getPercentFromPrice(price)

Get the % the current price is away from the given price.

Parameters:

price (float)

Returns: (float) The % the current price is away from the given price.

getPositionFromString(position)

Tradingview doesn't give you a nice way to put the positions into a dropdown for configuration settings. So, I specify them in the following format: . This function takes care of converting those custom strings back to the ones expected by tradingview scripts.

Parameters:

position (string) : (string) Plain english position string

Returns: (string) The string expected by tradingview functions

getTimeframeOfChart()

Get the timeframe of the current chart for display

Returns: (string) The string of the current chart timeframe

getTimeNowPlusOffset(candleOffset)

Helper function for drawings that use xloc.bar_time to help you know the time offset if you want to place the end of the drawing out into the future. This determines the time-size of one candle and then returns a time n candleOffsets into the future.

Parameters:

candleOffset (int) : (int) The number of items to find singular/plural for.

Returns: (int) The future time

getVolumeBetweenTimes(start, end)

Given a start and end time, returns the sum of all volume across bars during that time window.

Parameters:

start (int) : The timestamp to start with (# of seconds)

end (int) : The timestamp to end with (# of seconds)

Returns: (float) The volume

isToday()

Returns true if the current bar occurs on today's date.

Returns: (bool) True if current bar is today

padLabelString(labelText, labelStyle)

Pads a label string so that it appears properly in or not in a label. When label.style_none is used, this will make sure it is left-aligned instead of center-aligned. When any other type is used, it adds a single space to the right so there is padding against the right end of the label.

Parameters:

labelText (string) : (string) The string to be padded

labelStyle (string) : (string) The style of the label being padded for.

Returns: (string) The padded string

plural(num, singular, plural)

Helps format a string for plural/singular. By default, if you only provide num, it will just return "s" for plural and nothing for singular (eg. plural(numberOfCats)). But you can optionally specify the full singular/plural words for more complicated nomenclature (eg. plural(numberOfBenches, 'bench', 'benches'))

Parameters:

num (int) : (int) The number of items to find singular/plural for.

singular (string) : (string) The string to return if num is singular. Defaults to an empty string.

plural (string) : (string) The string to return if num is plural. Defaults to 's' so you can just add 's' to the end of a word.

Returns: (string) The singular or plural provided strings depending on the num provided.

timeframeInSeconds(timeframe)

Get the # of seconds in a given timeframe. Tradingview's timeframe.in_seconds() expects a simple string, and we often need to use series string, so this is an alternative to get you the value you need.

Parameters:

timeframe (string)

Returns: (int) The number of secondsof that timeframe

timeframeToString(tf)

Convert a timeframe string to a consistent standard.

Parameters:

tf (string) : (string) The timeframe string to convert

Returns: (string) The standard format for the string, or the unchanged value if it is unknown.

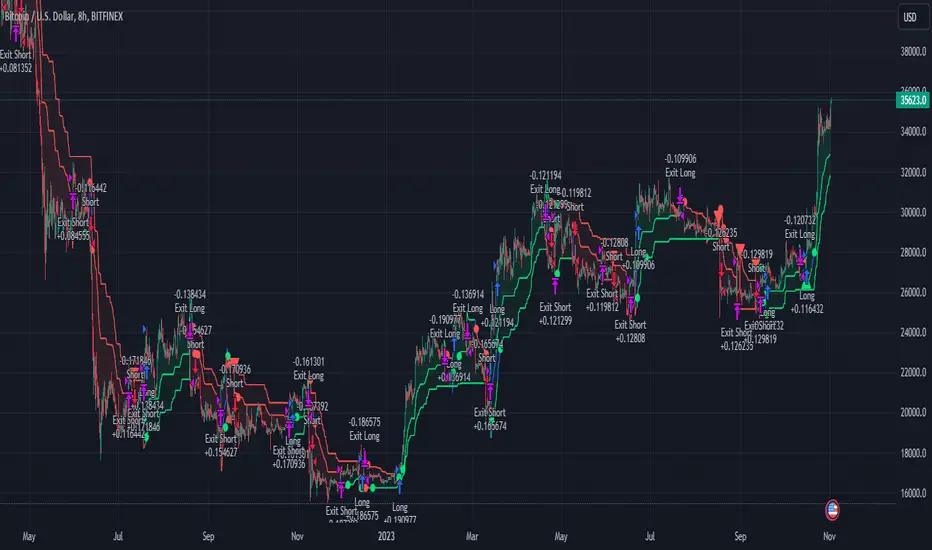

Renko StrategyRENKO STRATEGY

CAUTION : This strategy must be applied to a candlestick chart (not a Renko chart).

INTRODUCTION :

The Traditional Renko chart has been reproduced and is plotted according to the evolution of the price. It will enable us to receive buy or sell signals and follow major trends. This is a medium/long term strategy and depends a lot on the box size chosen in the parameters. There's also a money management method allowing us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RENKO CHART :

Renko chart construction methodology :

The user must first choose the box size. The minimum is 0.00001 and there is no maximum. The default is 10. The user must then choose the source that will define the data on which the calculations will be based (high, low, open, close). By default, close is selected. The first candle on the chart is used to draw the first box with its high and low.

Each time the price changes by the amount of the box size relative to the high or low of the last box, a new box is added above or below the previous one. If price variations are less than the box size, the same box is added next to the previous one. If price variations are N (integer number) times greater than box size, N boxes are added above or below the previous one. Each box added above the previous one is a green box, while each box added below the previous one is a red box.

Conditions for drawing a green box above the previous one :

(source - high_of_the_last_box) / box_size > 1

Condition for drawing a red box below the previous one :

(low_of_the_last_box - source) / box_size > 1

If neither condition is triggered, the same box is drawn next to the previous one.

Example :

The last candle has drawn a box with low 12 and high 14. The box size is therefore 2. The strategy will look at the value of the close each time a candle ends. The current candle closes with a close equal to 15.5. As the variation from the previous high is only 1.5 (which is less than the box size), the same box is added next to the previous one. The next candle closes at 16.2. The price variation is therefore 2.2 compared with the previous high. We can now add a new green box just above the previous one, with a low of 14 and a high of 16. The same process applies if the candle's close is at least one box size below the low of the last box. In this case, a new red box is placed below the previous one.

PARAMETERS :

Source : Allows you to specify which data will be taken into account by the strategy when performing calculations. The default is close.

Box size : Size of Renko graph boxes. This is a very important parameter to choose carefully, as it has a strong impact on the strategy's performance. Defaults to 10.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. The default is 400, meaning that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test all possible box sizes to find out which one generates the highest return on BITSTAMP:LTCUSD while limiting the drawdown. This strategy is the most optimal with a box size equal to 5.08 in 8h timeframe.

BUY AND SHORT SIGNALS :

As the aim of this strategy is to follow major trends based on price movements, we need to be on the right side of price fluctuation. We trade every box reversal, i.e. we are LONG when the boxes are green indicating an uptrend and SHORT when they are red indicating a downtrend.

RISK MANAGEMENT :

This strategy can incur losses. The size of the box is decisive, as it is used to plot the RENKO chart and thus trigger buy or sell signals. It's also what allows us to manage risk. For every trade, we risk a maximum amount equal to 2 times the size of the box, i.e. :(5.08*2*nb_contract)/trade_value.

MONEY MANAGEMENT :

The fixed ratio method has been used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy not only increases our performance, but also our drawdown.

Enjoy the strategy and don't forget to take the trade :)

Gap Statistics (Zeiierman)█ Overview

The Gap Statistics (Zeiierman) indicator is crafted to monitor, analyze, and visually present price gaps on a trading chart. Price gaps are areas on a chart where the price jumps up or down from the previous close to the next open, creating a "gap" in the normal price pattern. This script delivers an extensive range of statistics related to these gaps, encompassing their size, direction (whether bullish or bearish), frequency of getting filled, as well as the average number of bars it takes for a gap to be filled. The indicator also visually represents the gaps, making it easier for traders to spot and analyze them.

█ How It Works

Gap Identification: The script identifies gaps by comparing the open price of a bar to the close price of the previous bar. If there is a discrepancy between the two, it is recognized as a gap.

Gap Classification: Once a gap is identified, it is classified based on its size (as a percentage of the previous close price) and direction (bullish or bearish). The gap is then added to a specific category based on its size.

Gap Tracking: The script keeps track of all identified gaps using arrays and user-defined types, storing details like their size, direction, and whether they have been filled.

Gap Filling: The script continuously monitors the price to check if any previously identified gaps get filled. A gap is considered filled if the price moves back into the gap area.

Statistics and Alerts: The script calculates various statistics like the total number of gaps, the number of filled gaps, the average number of bars it takes for a gap to fill, and the percentage of gaps that get filled. It also generates alerts when a new gap is identified or an existing gap gets filled.

█ How to Use

Gaps are often classified into four main types:

Common Gaps: These are not associated with any major news and are likely to get filled quickly.

Breakaway Gaps: These occur at the end of a price pattern and signal the beginning of a new trend.

Runaway Gaps: Also known as continuation gaps, these occur in the middle of a trend and signal a surge in interest in the stock.

Exhaustion Gaps: These occur near the end of a price pattern and signal a final attempt to hit new highs or lows.

The Gap Statistics (Zeiierman) indicator enhances a trader's ability to use gaps in their trading strategy in several ways:

Statistical Analysis: Traders get comprehensive statistics on gaps, such as their size, direction, and how often they get filled.

Performance Tracking: The indicator tracks how many bars it typically takes for a gap to fill, providing traders with an average timeframe for gap closure.

█ Settings

Display Gaps: Choose to display "All Gaps," "Active Gaps," or "None."

Show Gap Size: Toggle on/off the display of the gap size.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Volume Profile with a few polylinesThe base of "Volume Profile with a few polylines" is another script of mine, Volume Profile (Maps) .

The structure of maps is used to gather the data. However, the drawings is done with polylines.

This enables coders to draw an entire volume profile with just a few polylines, while the range is broader.

This results in the benefit to draw more "lines" than with line.new() / box.new() alone.

🔶 CONCEPTS

🔹 Polylines

polyline.new creates a new polyline instance and displays it on the chart, sequentially connecting all of the points in the `points` array with line segments.

The segments in the drawing can be straight or curved depending on the `curved` parameter.

In this script, points are connected, starting from the bottom. The created line moves up until there is a price level where a volume value needs to be displayed,

at which the line goes to the left to the concerning volume value, coming back at the same price level until the line returns to its initial x-axis,

after which the line will continue to rise until all values are displayed.

A polyline can contain maximum 10000 points (10K).

Since the line has to go back and forth, each price/volume line takes 3 points.

In the case that 20K bars all have a different price, we would need 60K points, or just 6 polylines. A maximum of 100 polylines can be displayed.

The 3 highest volume values are displayed with line.new(), each with their own colour.

🔹 Maps

A map object is a collection that consists of key - value pairs

Each key is unique and can only appear once. When adding a new value with a key that the map already contains, that value replaces the old value associated with the key .

You can change the value of a particular key though, for example adding volume (value) at the same price (key), the latter technique is used in this script.

Volume is added to the map, associated with a particular price (default close, can be set at high, low, open,...)

When the map already contains the same price (key), the value (volume) is added to the existing volume at the associated price.

A map can contain maximum 50K values, which is more than enough to hold 20K bars (Basic 5K - Premium plan 20K), so the whole history can be put into a map.

🔹 Rounding function

This publication contains 2 round functions, which can be used to widen the Volume Profile

Round

• "Round" set at zero -> nothing changes to the source number

• "Round" set below zero -> x digit(s) after the decimal point, starting from the right side, and rounded.

• "Round" set above zero -> x digit(s) before the decimal point, starting from the right side, and rounded.

Example: 123456.789

0->123456.789

1->123456.79

2->123456.8

3->123457

-1->123460

-2->123500

Step

Another option is custom steps.

After setting "Round" to "Step", choose the desired steps in price,

Examples

• 2 -> 1234.00, 1236.00, 1238.00, 1240.00

• 5 -> 1230.00, 1235.00, 1240.00, 1245.00

• 100 -> 1200.00, 1300.00, 1400.00, 1500.00

• 0.05 -> 1234.00, 1234.05, 1234.10, 1234.15

•••

🔶 FEATURES

🔹 Volume * currency

Let's take as example BTCUSD, relative to USD, 10 volume at a price of 100 BTCUSD will be very different than 10 volume at a price of 30000 (1K vs. 300K)

If you want volume to be associated with USD, enable Volume * currency . Volume will then be multiplied by the price:

• 10 volume, 1 BTC = 100 -> 1000

• 10 volume, 1 BTC = 30K -> 300K

Polylines has the attributes curved & closed.

When "curved" is enabled the drawing will connect all points from the `points` array using curved line segments.

When "closed" is enabled the drawing will also connect the first point to the last point from the `points` array, resulting in a closed polyline.

They are default disabled, but can be enabled:

🔶 DETAILS

🔹 Put

When the map doesn't contain a price, it will be added, using map.put(id, key, value)

In our code:

map.put(originalMap, price, volume)

or

originalMap.put(price, volume)

A key (price) is now associated with a value (volume) -> key : value

Since all keys are unique, we don't have to know its position to extract the value, we just need to know the key -> map.get(id, key)

We use map.get() when a certain key already exists in the map, and we want to add volume with that value.

if originalMap.contains(price)

originalMap.put(price, originalMap.get(price) + volume)

-> At the last bar, all prices (source) are now associated with volume.

🔶 SETTINGS