VIX Dashboard [NariCapitalTrading]Overview

This VIX Dashboard is designed to provide traders with a quick visual reference into the current volatility and trend direction of the market as measured by CBOE VIX. It uses statistical measures and indicators including Rate of Change (ROC), Average True Range (ATR), and simple moving averages (SMA) to analyze the VIX.

Components

ATR Period : The ATR Period is used to calculate the Average True Range. The default period set is 24.

Trend Period : This period is used for the Simple Moving Average (SMA) to determine the trend direction. The default is set to 48.

Speed Up/Down Thresholds : These thresholds are used to determine significant increases or decreases in the VIX’s rate of change, signaling potential market volatility spikes or drops. These are customizable in the input section.

VIX Data : The script fetches the closing price of the VIX from a specified source (CBOE:VIX) with a 60-minute interval.

Rate of Change (ROC) : The ROC measures the percentage change in price from one period to the next. The script uses a default period of 20. The period can be customized in the input section.

VIX ATR : This is the Average True Range of the VIX, indicating the daily volatility level.

Trend Direction : Determined by comparing the VIX data with its SMA, indicating if the trend is up, down, or neutral. The trend direction can be customized in the input section.

Dashboard Display : The script creates a table on the chart that dynamically updates with the VIX ROC, ATR, trend direction, and speed.

Calculations

VIX ROC : Calculated as * 100

VIX ATR : ATR is calculated using the 'atrPeriod' and is a measure of volatility.

Trend Direction : Compared against the SMA over 'trendPeriod'.

Trader Interpretation

High ROC Value : Indicates increasing volatility, which could signal a market turn or increased uncertainty.

High ATR Value : Suggests high volatility, often seen in turbulent market conditions.

Trend Direction : Helps in understanding the overall market sentiment and trend.

Speed Indicators : “Mooning” suggests rapid increase in volatility, whereas “Cratering” indicates a rapid decrease.

The interpretation of these indicators should be combined with other market analysis tools for best results.

Search in scripts for "Volatility"

Average True Range Level█ Overview

The indicator uses color-coded columns to represent different levels of normalized ATR, helping traders identify periods of high or low volatility.

█ Calculations

The normalization process involves dividing the current True Range by the Average True Range. The formula for normalized ATR in the code is:

nAtr = nz(barRange/atr)

█ How To Use

Level < 1

During periods when the normalized ATR is less than 1, suggesting a lower level of volatility, traders may explore inside bar strategies. These strategies focus on trading within the range of the previous bar, aiming to capitalize on potential breakout opportunities.

Level between 1 and 3

In instances where the normalized ATR falls between 1 and 3, indicating moderate volatility, a pullback strategy may be considered. Traders look for temporary corrections against the prevailing trend, entering positions in anticipation of the trend's resumption

Level between 2 and 3

Within the range of normalized ATR between 2 and 3, signifying a balanced level of volatility, traders might explore breakout strategies. These strategies involve identifying potential breakout levels using support and resistance or other indicators and entering trades in the direction of the breakout.

Level > 3

When the normalized ATR exceeds 3, signaling high volatility, traders should approach with caution. While not ideal for typical mean reversion strategies, this condition may indicate that the price has become overextended. Traders might wait for subsequent candles, observing a normalized ATR between 2 and 3, to consider mean reversion opportunities after potential overpricing during the high volatility period.

* Note: These strategies are suggestions and may not be suitable for all trading scenarios. Traders should exercise discretion, conduct their own analysis, and adapt strategies based on individual preferences and risk tolerance.

Bull / Bear Market RegimeBull / Bear Market Regime

Instructions:

- A simple risk on or risk off indicator based on CBOE's Implied Correlation and VIX to highlight and indicate Bull / Bear Markets. To be used with the S&P500 index as that's the source from where the CBOE calculates and measures implied volatility & implied correlation. Can also be used with the other indices such as: Dow Jones, S&P 500, Nasdaq, & Nasdaq100, & Index ETF's such as DIA, SPY, QQQ, etc.

- Know the active regime, see the larger picture using the Daily or Weekly view, and visualize the current "Risk On (Bull) or Risk Off (Bear)" environment.

Description:

- Risk On and Risk Off simplified & visualized. Know if we are in a RISK ON or RISK OFF environment (Bull or Bear Market). (Absolute bottoms and tops will occur BEFORE a Risk On (Bull Market) or Risk Off (Bear Market) environment is confirmed!) This indicator is not meant to bottom tick or uptick market price action, but to show the active regime.

- Green: Bull Market, Risk On, low volatility, and low risk.

- Red: Bear Market, Risk Off, high volatility, and higher risk.

Buy & Sell Indicators (DAILY time frame)

- Nothing is 100% guaranteed! Can be used for short to medium term trades at the users discretion in BEAR MARKETS!!

- These signals are meant to be used during a RISK OFF / BEAR MARKET environment that tends to be accompanied with high volatility. A Risk on / Bull Market environment tends to have low volatility and endless rallies, so the signals will differ and in most instances not apply for Bull market / Risk on regime.

- The SELL signal will more often than not signal that a pullback is near in a BULL market and that a BMR-Bear Market Rally is almost over in a BEAR market.

- The BUY signal will have far more accuracy in a BEAR market-high volatility environment and can Identify short-term and major bottoms.

Always use proper sizing and risk management!

intraday_bondsStatistics for assisting with intraday bond trading, using five minute periods and one hour ranges. There are two tables, a volatility table and a correlation table. The correlation table shows the correlation of five minute returns (absolute) between the four different bond contracts that trade on the CME. The volatility table shows for each contract:

- The current realized volatility, based on the previous one hour of realized volatility. This figure is annualized for easy comparison with options contracts.

- The current realized volatility's z-score, based on all available data.

- The tick range of an "N" standard deviation move over one hour. Choose "N" using the stdevs input.

- The previous hour's true range (high - low).

The ranges are expressed in ticks.

Logarithmic Bollinger BandsLogarithmic Bollinger Bands

Published by Eric Thies on January 14, 2022

Summary

In this script I have taken the standard Bollinger band pinescript and made efforts to eliminate the behavior experienced in periods of high volatility in which we see the bands disappear completely off the chart by adding exponential plotting and logarithmic sourcing to the tool.

This tool will also show periods of Bearish and Bullish Expansion for users to see when volatility is running high in the market.

More On Bollinger Bands

Bollinger Bands consist of a center line representing the moving average of a security’s price over a certain period, and two additional parallel lines (called the upper and lower trading bands) one of which is just the moving average plus k-times the standard deviation over the selected time frame, and the other being the moving average minus k-times the standard deviation over that same timeframe. This technique has been developed in the 1980’s by John Bollinger, who lately registered the terms “Bollinger Bands” as a U.S. trademark in 2011. Technical analysts typically use 20 periods and k = 2 as default settings to build Bollinger Bands, while they can choose a simple or exponential moving average. Bollinger Bands provide a relative definition of high and low prices of a security. When the security is trading within the upper band, the price is considered high, while it is considered low when the security is trading within the lower band.

There is no general consensus on the use of Bollinger Bands among traders. Some traders see a buy signal when the price hits the lower Bollinger Band and close their position when the price hits the moving average. Some others buy when the price crosses over the upper band and sell when the price crosses below the lower band. We can see here two opposing interpretations based on different rationales, depending whether we are in a reversal or continuation pattern. Another interesting feature of the Bollinger Bands is that they give an indication of the volatility levels; a widening gap between the upper and lower bands indicates an increasing volatility, while a narrowing band indicates a decreasing volatility. Moreover, when the bands have an almost flat slope (parallel to the x-axis) the price will generally oscillate between the bands as if trading through a channel.

// © 2022 KINGTHIES THIS SOURCE CODE IS SUBJECT TO TERMS OF MOZILLA PUBLIC LICENSE 2.0 (MOZILLA.ORG/MPL/2.0)

//@version=5

//## !<---------------- © KINGTHIES --------------------->

indicator('Logarithmic Bollinger Bands (kingthies)',shorttitle='LogBands_KT',overlay=true)

// { BBANDS

src = math.log(input(close,title="Source"))

lenX = input(20,title='lenX')

highlights = input(false,title="Highlight Bear and Bull Expansions?")

mult = 2

bbandBasis = ta.sma(src,lenX)

dev = 2 * ta.stdev(src, 20)

upperBB = bbandBasis + dev

lowerBB = bbandBasis - dev

bbw = (upperBB-lowerBB)/bbandBasis

bbr = (src - lowerBB)/(upperBB - lowerBB)

// }

// { BBAND EXPANSIONS

bullExp= ta.rising(upperBB,1) and ta.falling(lowerBB,1) and ta.rising(bbandBasis,1) and ta.rising(bbw,1) and ta.rising(bbr,1)

bearExp= ta.rising(upperBB,1) and ta.falling(lowerBB,1) and ta.falling(bbandBasis,1) and ta.rising(bbw,1) and ta.falling(bbr,1)

// }

// { COLORS

greenBG = color.rgb(9,121,105,75), redBG = color.rgb(136,8,8,75)

bullCol = highlights and bullExp ? greenBG : na, bearCol = highlights and bearExp ? redBG : na

// }

// { INDICATOR PLOTTING

lowBB=plot(math.exp(lowerBB),title='Low Band',color=color.aqua),plot(math.exp(bbandBasis),title='BBand Basis',color=color.red),

highBB=plot(math.exp(upperBB),title='High Band',color=color.aqua),fill(lowBB,highBB,title='Band Fill Color',color=color.rgb(0,128,128,75))

bgcolor(bullCol,title='Bullish Expansion Highlights'),bgcolor(bearCol,title='Bearish Expansion Highlights')

// }

vol_premiaThis script shows the volatility risk premium for several instruments. The premium is simply "IV30 - RV20". Although Tradingview doesn't provide options prices, CBOE publishes 30-day implied volatilities for many instruments (most of which are VIX variations). CBOE calculates these in a standard way, weighting at- and out-of-the-money IVs for options that expire in 30 days, on average. For realized volatility, I used the standard deviation of log returns. Since there are twenty trading periods in 30 calendar days, IV30 can be compared to RV20. The "premium" is the difference, which reflects market participants' expectation for how much upcoming volatility will over- or under-shoot recent volatility.

The script loads pretty slow since there are lots of symbols, so feel free to delete the ones you don't care about. Hopefully the code is straightforward enough. I won't list the meaning of every symbols here, since I might change them later, but you can type them into tradingview for data, and read about their volatility index on CBOE's website. Some of the more well-known ones are:

ES: S&P futures, which I prefer to the SPX index). Its implied volatility is VIX.

USO: the oil ETF representing WTI future prices. Its IV is OVX.

GDX: the gold miner's ETF, which is usually more volatile than gold. Its IV is VXGDX.

FXI: a china ETF, whose volatility is VXFXI.

And so on. In addition to the premium, the "percentile" column shows where this premium ranks among the previous 252 trading days. 100 = the highest premium, 0 = the lowest premium.

strangle_pricerUsage:

1. Set the put and call strike inputs to values of your choosing.

2. Select "days to expiration".

3. Set the put and call standard deviations using the output table.

The indicator is meant help price a strangle using historical data and a volatility model. By default, the model is an ewma-method historical volatility. After selecting strikes and standard their corresponding standard deviation, theoretical values and probabilities will be shown in the table. The script is initialized with -1 for several inputs, and won't show any data until these are adjusted.

The theoretical values shown assume a strangle was bought or sold on every historical bar, and averaging their value at expiration.

For example, if you choose the $50 call and $40 put when the underlying is at $45 and there are 30 days until expiration, suppose the volatility is N and

these strikes correspond to M standard deviations. Input those and the resulting theoretial values shown will be based on opening a 30 dte call and put at M standard deviations with respect to the volatility at each bar.

- Past volatility forecasts are plotted in blue, and hidden by default.

- The current volatility forecast is drawn as a blue line.

- The put and call strikes are drawn as red lines.

This indicator is only meant for the daily chart!

Since I won't be able to edit this description later, also check the release notes and script comments for important changes.

3D Wave-PMThe Wave-PM (Whistler Active Volatility Energy - Price Mass) indicator is an oscillator described in Mark Whistler's book 'Volatility Illuminated'.

The Wave-PM was specifically designed to help read cycles of volatility. When visualizing volatility cycles as a heatmap we can get a clear overview of market volatility phases on multiple timeframes, and more importantly as traders give us insight into 'potential' volatility from to pent up energy signaled by the blue and green plumes which invariably give way to big moves signaled by the orange and red plumes.

This indicator can be quite GPU intensive, so simple and also line based visualization methods are included. Also, its free and open source so go ahead and hack it to your hearts content. Enjoy!

Pivots, Compressions and ExtensionsPivots, Compressions and Extensions

Best used with a monochromatic bar chart, ex. light gray bars that allow signals to stand out.///

Blue = volatility expansion warning, this means volatility has been compressed and is starting a new phase of volatility expansion.

(cont.) Think a ball at the top of a hill with very low positional volatility but high potential energy. Blue bars mark the point

(cont.) where potential energy starts to transition into kinetic energy. This often 'cycles' into a new regime of higher volatility.

Pink & purple bars signify extreme, exponential trend, often the climax of a particular bull or bear cycle. Can help identify tops.

Orange is meant to signal a pocket pivot as described by @RollyTrader among others. This pivot marks the end of consolidation.

Trend MagicTrend Magic is originally a MT platform (MetaTrader) indicator and it can be used with any forex trading systems / strategies for additional confirmation of trading entries or exits. Converted the MT platform code to TradingView Pine version 4. Also you can use Multiple Time Frame.

It also works well with Crypto and Stock Markets.

Trend Magic consists of two main calculation parts as momentum and volatility:

First part is ATR based (like ATR Trailing Stop) logic, second part is all about CCI which also determines the color of Trend Magic.

Blue: when CCI is positive

Red: when CCI is negative

Also added alert condition regarding price crosses :

when LOW CrossesAbove TM

and HIGH CrossesBelow TM

Enjoy

Kıvanç Özbilgiç

Indicator - EVZ Chart - DGHey Traders, this is the $EVZ chart plotted as an indicator. The $EVZ is the Euro Volatility Index, which can be used to measure volatility in markets.

The use of the $EVZ could be helpful for trend traders of FX. The concept developed by VP of no nonsense forex, we can use the value of the $EVZ to determine when we put on full risk if there is high volatility, half risk when there is medium volatility, or no risk if there is very low volatility.

This indicator has 2 adjustable horizontal lines, so you can put in the conditions or thresholds you need for your trading strategy.

Happy trading,

DG

LULD Bands & Trading Halt Detector [Volume Vigilante]📖 LULD Bands & Trading Halt Detector

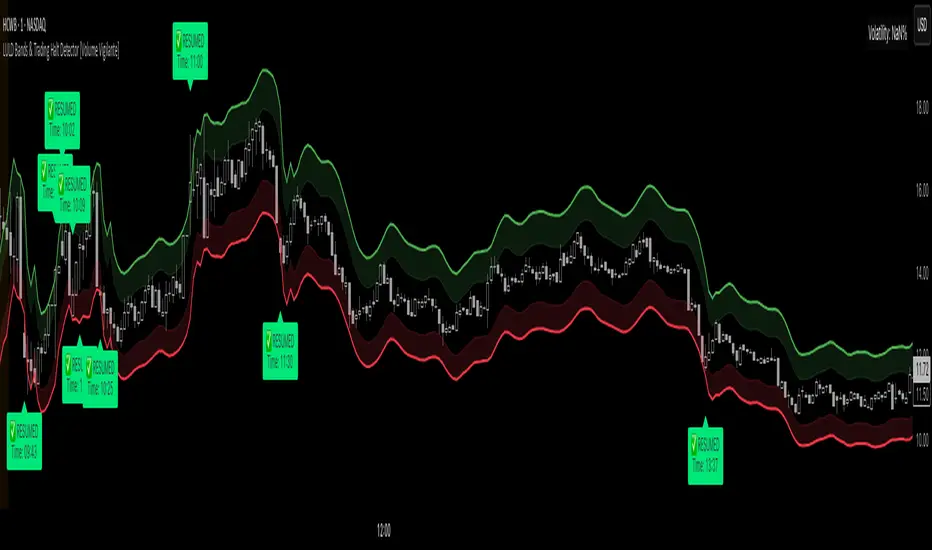

This advanced tool visualizes official Limit Up / Limit Down (LULD) price bands and detects regulatory trading halts and resumptions based on SEC and NASDAQ rules. It is engineered for high accuracy by anchoring all calculations to the 1-minute timeframe, ensuring reliable signals across any chart resolution.

📌 What Does This Script Do?

- Draws real-time LULD price band estimations and optional buffer (caution) zones directly on the chart.

- Detects trading halt resumptions by monitoring time gaps between candles and other regulatory criteria. (Note: Due to Pine Script limitations, halts cannot be detected in real-time, only resumptions after they occur.)

- Triggers real-time alerts for:

- Trading Resumptions (Limit Up & Limit Down)

- LULD Zone Entries (Caution Zone)

- Band Breaches (Limit Up and Limit Down)

- Plots historical halt resumption markers to analyse past events.

📐 How It Works:

- Implements official SEC/NASDAQ LULD rules for Tier 1 and Tier 2 securities.

- Applies special band adjustments for the final 25 minutes of trading (after 3:35 PM ET).

- Anchors all logic to the 1-minute timeframe for precise calculations, even on higher timeframe charts.

- Includes adjustable volume and volatility filters to eliminate false signals (ghost halts) on low-- liquidity assets, especially Tier 2 securities when TradingView fails to print candles.

⚙️ How to Use It:

1.) Apply the script to any asset or timeframe.

2.) Adjust Volume and Volatility Filters to reduce noise. (Recommended: 500,000+ volume, 10%+ volatility.)

3.) Enable or disable visual components like bands, buffer zones, and halt resumption labels.

4.) Configure alerts directly from the script settings panel.

5.) Apply alerts to individual assets via "Add Alert On..." or to entire watchlists using "Add Alert on the List."

🧩 What Makes This Script Unique?

- True 1-Minute Anchored Calculations: Ensures alerts and visuals match official trading halt criteria regardless of chart timeframe.

- Customisable Buffered Zones: Visualise proximity to regulatory price limits and avoid volatility traps.

- Combines halt resumption detection, limit up/down band visualisation, and real-time alerts into one clean, modular tool.

📚 Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Use at your own discretion and consult a licensed financial advisor before making trading decisions based on it.

Official Resources:

- NASDAQ LULD Regulations (FAQ):

www.nasdaqtrader.com

Current Nasdaq Trading Halts:

www.nasdaqtrader.com

Volatility Price FlowCapitalize on market volatility with our new volatility price flow indicator. We have designed this indicator to process historical price movements and indicate when price may have reached exhaustion in the context of current volatility.

This is achieved by taking the price deviation from a user defined moving average, and applying a weighting to the deviations from the candle body and candle wick on both buy side and sell side, over a user defined period. The period of the base moving average, type of moving average and the period of the historical price deviations can all be modified. This creates a typical 'band' style indicator, though with a unique characteristic that the buy and sell side vary independently as well as the band expansion being based on weighted variables tied to the actual price changes, rather than just a standard deviation the moves uniformly.

Additionally, these bands can be merged with an anchored vwap - we do this so that the deviations of price from the moving average can include a more volume based approach to identifying potential pivots.

The end result is an indicator that reflects the current market price movements, identifies and capitalizes on impulsive or beginning moves to indicate potential tops / bottoms / reversals.

The signals are simple - anytime price closes within a band, having been outside the band, a signal is displayed. As a basic guide to setting the indicator up for the first time, we suggest reducing all of the multipliers to a value less than 1. Then gradually increase each one, until the signals reduce in quantity and improve in quality, starting with the price deviation multiplier, then the volatility multiplier and finally the expansion multiplier.

Last of all, alerts can be created based on the current chart timeframe and indicator settings, simply by adding an alert that uses the built in buy or sell signal.

Note: We cannot guarantee the accuracy of the signals provided, since the user creates the signals by modifying the settings, and as such we can take no responsibility for any trading losses incurred using the indicator and highly encourage all users to manage their risk and only risk what you can afford to lose.

Trading Ranges + ZScoreOverview

The "Trading Ranges + ZScore" script is a versatile technical indicator developed for TradingView. This tool combines two powerful concepts—price ranges and Z-Score analysis—to help traders identify potential trend reversals, overbought/oversold conditions, and trend strength. The script dynamically calculates price ranges based on recent price action and utilizes Z-Score to detect deviations from a statistical norm, providing valuable insights for decision-making in both ranging and trending markets.

Features

Price Ranges: Calculates dynamic upper and lower price boundaries based on volatility and market structure.

Z-Score Oscillator: A statistical measure that highlights overbought/oversold conditions based on the deviation from a moving average.

Trend Detection: Identifies trend continuation or reversal points by comparing current price action against historical levels.

Customizable Alerts: Generates visual signals (diamonds and X crosses) for potential long/short entries and exits.

Visual Representation: Colors the bars based on Z-Score and trend direction, enhancing the chart’s readability and signal clarity.

Customizable Parameters: The script allows users to fine-tune perception length, analysis period, factor multiplier, and oscillator thresholds to fit different market conditions.

Key Input Parameters

Perception: The length used for calculating highest/lowest price points (default: 20).

Analysis: The length used for calculating the moving average and volatility (default: 100).

Factor: A multiplier to adjust the width of the price ranges (default: 2.0).

Oscillator Threshold: The overbought/oversold threshold for the Z-Score oscillator (default: 70).

Trend Filter: A boolean switch that filters signals based on trend direction.

Fill Zones: Option to color-fill between price levels when certain conditions are met.

Bullish/Bearish/Neutral Colors: Customizable colors for bullish, bearish, and neutral signals.

How It Works

Price Ranges Calculation:

The script calculates five levels: two upper boundaries, the average price level, and two lower boundaries. These levels are based on the highest/lowest prices over a user-defined period and adjusted by volatility (Average True Range).

When the price crosses either of these levels, it suggests a significant change in market direction, potentially indicating a trend reversal.

Z-Score Oscillator:

The Z-Score is a statistical measurement of a price's position relative to its moving average. The indicator calculates two variations:

Z-Score based on the absolute difference between the price and the moving average.

Z-Score based on standard deviation.

These oscillators help detect extreme conditions where the price is likely to revert (overbought/oversold zones).

Trend Detection and Signals:

The indicator generates potential buy/sell signals when the price crosses the predefined levels or based on the fast Z-Score crossing the overbought/oversold thresholds.

Weak long/short signals are shown when the faster Z-Score oscillator reaches extreme levels but trend filters are applied to avoid noise.

Bar Colors and Signal Shapes:

Bar colors change dynamically to reflect the trend direction and Z-Score conditions. Signals for potential trades are displayed using diamonds and X crosses, making it easy to spot opportunities visually.

Visuals and Plots

Bar Colors: Changes the bar color based on Z-Score and trend direction.

Z-Score Plot: Displays two Z-Score oscillators, the standard and a faster one for detecting quicker price deviations.

Overbought/Oversold Zones: Highlighted by upper and lower thresholds of the Z-Score.

Long/Short Signals: Uses diamond-shaped markers for strong long/short signals and X-shaped markers for weaker signals.

Dynamic Range Lines: Plots lines for key price levels (upper/lower boundaries, mid-range) based on the dynamic range calculations.

Usage Guide

Identify Overbought/Oversold Conditions: Look for the Z-Score reaching extreme positive or negative values. When combined with trend signals, these conditions often point to a potential reversal.

Follow the Trend: Use the trend filter option to focus only on trades in the direction of the prevailing trend, reducing false signals in ranging markets.

Watch for Range Breakouts: Pay attention to the upper and lower boundaries. Price crossing these levels often signals the start of a new trend or a major price movement.

Adjust Parameters: Tailor the perception length, analysis length, and multiplier to suit different asset classes or timeframes.

Customization

You can adjust the key parameters to adapt the indicator to different markets or personal trading preferences:

- Perception & Analysis Lengths: Control the sensitivity of the price range calculations.

- Factor Multiplier: Adjusts the width of the ranges, with higher values indicating larger zones.

- Oscillator Threshold: Modify the overbought/oversold levels to suit different market volatility.

- Trend Filter: Toggle on/off to focus on trend-following strategies or range-bound conditions.

- Visual Options: Customize colors for bullish, bearish, and neutral signals, as well as enable/disable the zone fills.

Hedge Coin M - Statistical Support and ResistanceHedge Coin M - Statistical Support and Resistance

Introduction

"Hedge Coin M - Statistical Support and Resistance" is a sophisticated, statistically-driven indicator designed specifically for traders in the COIN-M market on Binance. It offers a nuanced approach to identifying key market levels, focusing on the dynamics of support and resistance through advanced volatility analysis.

Foundation and Credits:

This script is an advanced adaptation of TradingView's standard code for the Bollinger Bands indicator. It extends the foundational concept of Bollinger Bands by integrating additional volatility metrics.

Calculation Method

This indicator employs Volume Weighted Moving Averages (VWMA) to create two distinct sets of Bollinger Bands, named BB-a and BB-b.

BB-a is derived from the VWMA of high prices, targeting potential resistance levels.

BB-b is based on the VWMA of low prices, aimed at identifying critical support levels.

Users can independently adjust the standard deviation (SD) multipliers for the upper and lower bands of both BB-a and BB-b, accommodating different market conditions.

Enhanced Volatility Analysis

The indicator calculates additional standard deviation lines for the upper band of BB-a and the lower band of BB-b. These lines provide deeper insights into market volatility.

Plotted Graphs

The primary plots include the upper and lower bands of BB-a and BB-b, marked in distinct colors for clarity.

Additional SD lines are plotted to indicate potential extended levels of support and resistance, offering traders a broader view of possible market movements.

Purpose and Usage

"Hedge Coin M - Statistical Support and Resistance" is designed to provide traders with a consistent, statistical method for identifying significant price levels.

It aids in scaling entry into positions, helping traders to navigate the COIN-M market with more informed decision-making.

This tool is especially useful for traders who combine long-term holding with swing trading strategies, offering a balanced approach to market engagement.

Integration and Adaptation

Easily integrate this indicator into your TradingView chart for the COIN-M market.

Use the insights provided to complement your overall trading strategy, particularly in identifying and reacting to significant market movements.

Disclaimer

Important Note: This indicator is provided for informational purposes only. It does not constitute financial advice, investment advice, trading advice, or any other sort of advice. Trading decisions should be made based on your own analysis, prudence, and judgment. Please be aware of the risks involved in trading and consult a financial advisor if necessary.

Pseudo-Entropy Oscillator with Standard Deviation (modified)Intuition: The Pseudo-Entropy Oscillator with Standard Deviation (PEO_SD) was created to provide traders with a way to analyze market momentum and potential reversals. It combines the concepts of entropy, standard deviation, and moving averages to offer insights into market behavior.The oscillator's core idea is to measure the pseudo-entropy of the market using standard deviation. Pseudo-entropy refers to the degree of disorder or randomness in the price data. By calculating the standard deviation of the closing prices over a specified period, the oscillator quantifies the market's volatility.To enhance the usefulness of the pseudo-entropy measurement, the oscillator incorporates moving averages. The entropy delta is calculated by applying momentum analysis to the pseudo-entropy values. This helps identify short-term changes in the entropy, indicating shifts in market sentiment or momentum.The oscillator further smoothes the pseudo-entropy values by calculating the simple moving average (SMA) over a specified length. This helps filter out noise and provides a clearer representation of the market's overall momentum.

------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

The "Pseudo-Entropy Oscillator with Standard Deviation" (PEO_SD) is a custom indicator designed to help traders analyze market momentum and potential reversal points. It can be applied to various markets like stocks, commodities, forex, or cryptocurrencies. By using this indicator, you can gain insights into the market's behavior and make more informed trading decisions.

The PEO_SD indicator plots three lines on your chart: the fast pseudo-entropy line, the medium pseudo-entropy line, and the slow pseudo-entropy line. Each line represents the combined pseudo-entropy values, which are calculated using standard deviation and moving averages.

The lines are color-coded for easy identification. The fast line is represented by blue, the medium line by yellow, and the slow line by red. Additionally, three horizontal reference lines are plotted: the mid line (at 50), the lower bound (at 20), and the upper bound (at 80).

To use this indicator effectively, you can observe the interactions of the lines with the reference lines. For example, when any of the lines cross above the mid line, it might indicate a bullish signal, suggesting an upward price movement. Conversely, a crossover below the mid line could be a bearish signal, indicating a potential downward price movement. If the lines reach the upper bound, it might suggest that the market is overbought, and a reversal could be imminent. Conversely, reaching the lower bound may indicate that the market is oversold, possibly leading to a price reversal.

By applying the PEO_SD indicator and studying the lines' movements, you can gain valuable insights into market momentum, identify potential reversal points, and make more informed trading decisions.

Fractal Dimension Index The Fractal Dimension Index is a technical indicator that gauges the amount of volatility currently present in the market.

The theory behind this indicator is that a value of 1.5 suggests the market is acting in a completely random fashion. As the market deviates from 1.5, the opportunity for earning profits is increased in proportion to the amount of deviation.

Keep in mind that the indicator does not show the direction of trends ! Although you can try to test it as a trend-following indicator that gives trend-following signals, that isn't the intended use of the indicator.

The Fractal Dimension Index is red when the market is in a trend. And it is blue when there is high volatility. When the Fractal Dimension Index changes its color from red to blue , it means that a trend is finishing. The market becomes erratic and high in volatility when the Fractal Dimension Index is blue . Usually, these "blue periods" do not go on for a long time, they come before a new trend.

So, look for trend-following signals while the Fractal Dimension Index is blue since this indicates high volatility before a potential trend, and avoid trend-following signals when the Fractal Dimension Index is red since this indicates a ranging/non-trending market or a trend that started long ago.

Volatility Funnel v2Using the contracting phase of what are basically bollinger bands and some fancy coloring, this indicator draws funnels to which show tightening ranges and doesn't take up too much screen space unless you want it to.

There is a smoothing option if you're into that.

Enjoy!!!

Hyper Frame Fibo MA RibbonsIntroduction

Moving averages are an integral part of the TA world. There are different types of moving averages and each person uses them depending on their strategy and market conditions.

Meanwhile, the main variable in calculating the averages is their LENGTH. This value is optional, but not every value is applicable.

After much experience in the world of financial markets, I came to the conclusion that although the most popular length values are 20, 50, 100, and 200, the Fibonacci number come with surprising results .

Description

The following script calculates seven averages with the length of Fibonacci numbers (34, 55, 89, 144, 233, 377 and 610) with the formula of your choice (SMA, EMA, WMA, HMA) and shows that we named it FiboMa .

You can also have Bollinger Bands with the desired frame at the same time.

This is not the whole story...

You can see the same values from smaller or larger frames at the same time!

We named this feature Hyper Frame Vision .

It is possible to display values for FiboMa up to three hyper frames (with the main frame a total of 4 levels) and in the Bollinger Bands one hyper frame (with the main frame a total of 2 levels).

By default, the display of FiboMa hyper frame values is limited to the last 10 bars, which you can change to an arbitrary value by changing the source code.

The display of hyper frame values is not limited for Bollinger Band.

What is its use? What is it good for?

Support and Resistance

Using dynamic support / resistance is much smarter than static! This protects you from the risk of many fake breaks, and your profit and loss limits will be more flexible and more efficient.

The intersection of FiboMa ribbons are potential points of support / resistance.

We use colors to easily identify supports / resistances.

Any average lower than the price is assumed as support and displayed in green, and any average above the price is assumed as resistance so displayed in red.

So the color of the averages is dynamic.

The color of FiboMa is a range from red to green. Whatever colors get saturated , the lenght is longer and the more power it has as support / resistance.

Volatility

With this script, you also have the ability to monitor the amount of market volatility ! The combination of Bollinger Bands and FiboMa provides a clear view of the market volatility.

The decrease and compression of the FiboMa width is a sign of a decrease in volatility and vice versa.

Trend

I don't see the need for additional explanation, only whenever the price is higher than the middle band , the BB cloud is green , and whenever it is lower , is red .

The wider FiboMa means the stronger trend.

How to use

In the script settings you have the ability to enable or disable anything except.

---------------------------------------------

Similar scripts have been published before and we were inspired by them and tried to improve idea and code uniqe one.

I hope it will be useful .. Support us with your likes and comments .. We have anothers great script .. Just started.

Average True Range % of PriceThis script easily shows in an indicator window the Average True Range % of Price, which helps people understand the volatility of an asset in % terms defined by custom MA periods for custom ATR periods.

The MA Period gives the average price.

The ATR Period gives the average range.

The Average Range / Average Price = Average Range % of Price.

Understanding the volatility of an asset can help people manage risk e.g. if an asset has a low entry cost, but very high volatility it may be more risky than another asset with a high entry cost, but much lower volatility.

IO_VRSIOriginal Idea by Invsto

In this indicator, I explore the core concepts of RSI and extend it with smoothening to determine volatility.

Usage:

LIME/GREEN : High Volatility and BULLISH trend

RED/FUCHSIA : High Volatility and BEARISH trend

GRAY: Low volatility/Potential Chop Zone

VIX-VXV-Ratio-Buschi

English:

This script shows the ratio between the VIX (implied volatility of SPX options over the next month) and the VXV (implied volatility of SPX options over the next three months). Since in normal "Contango" mode, the VXV should be higher than the VIX, the crossing under 1.0 or maybe 0.95 after a volatility spike could be a sign for a calming market or at least a calming volatility.

Deutsch:

Dieses Skript zeigt das Verhältnis zwischen dem VIX (implizite Volatilität der SPX-Optionen über den nächsten Monat) und dem VXV (implizite Volatilität der SPX-Optionen über die nächsten drei Monate). Da im normalen "Contango"-Modus der VXV höher als der VIX liegen sollte, kann das Abfallen unter 1,0 oder 0,95 nach einer Volatilitätsspitze ein Anzeichen für einen ruhiger werdenden Markt oder zumindest eine ruhiger werdende Volatilität sein.

Percent Change Histogram + MACandle Percent Move Columns with Optional Moving Average

Description:

This indicator calculates the percentage move of each candle over a specified number of bars and displays it as upward-facing columns, regardless of the candle direction. Each column is color-coded based on the candle’s direction—green for bullish, red for bearish. An optional moving average can be overlaid on the percentage values to help visualize trends and smooth out volatility.

Features:

Shows each candle’s percentage move as a column facing upward.

Columns are colored according to candle direction.

Adjustable input for the number of bars used in calculation.

Optional moving average overlay that can be added or removed.

Helps quickly assess volatility and trend strength in percentage terms.

Use Case:

Ideal for traders who want a clear visual representation of individual candle movements in percentage terms, making it easier to spot trends, pullbacks, and volatility patterns across different timeframes.