TradingView Alerts (Expo)█ Overview

The TradingView inbuilt alert feature inspires this alert tool.

TradingView Alerts (Expo) enables traders to set alerts on any indicator on TradingView, both public, protected, and invite-only scripts (if you are granted access). In this way, traders can set the alerts they want for any indicator they have access to. This feature is highly needed since many indicators on TradingView do not have the particular alert the trader looks for, this alert tool solves that problem and lets everyone create the alert they need. Many predefined conditions are included, such as "crossings," "turning up/down," "entering a channel," and much more.

█ TradingView alerts

TradingView alerts are a popular and convenient way of getting an immediate notification when the asset meets your set alert criteria. It helps traders to stay updated on the assets and timeframe they follow.

█ Alert table

Keep track of the average amount of alerts that have been triggered per day, per month, and per week. It helps traders to understand how frequently they can expect an alert to trigger.

█ Predefined alerts types

Crossing

The Crossing alert is triggered when the source input crosses (up or down) from the selected price or value.

Crossing Down / Crossing Up

The Crossing Down alert is triggered when the source input crosses down from the selected price or value.

The Crossing Up alert is triggered when the source input crosses up from the selected price or value.

Greater Than / Less Than

The Greater Than alert is triggered when the source input reaches the selected value or price.

The Less Than alert is triggered when the source input reaches the selected value or price.

Entering Channel / Exiting Channel

The Entering Channel alert is triggered when the source input enters the selected channel value.

The Exiting Channel alert is triggered when the source input exits the selected channel value.

Notice that this alert only works if you have selected "Channels."

Inside Channel / Outside Channel

The Inside Channel alert is triggered when the source input is within the selected Upper and Lower Channel boundaries.

The Outside Channel alert is triggered when the source input is outside the selected Upper and Lower Channel boundaries.

Notice that this alert only works if you have selected "Channels."

Moving Up / Moving Down

This alert is the same as "crossing up/down" within x-bars.

The Moving Up alert is triggered when the source input increases by a certain value within x-bars.

The Moving Down alert is triggered when the source input decreases by a certain value within x-bars.

Notice that you have to set the Number of Bars parameter!

The calculation starts from the last formed candlestick.

Moving Up % / Moving Down %

The Moving Up % alert is triggered when the source input increases by a certain percentage value within x-bars.

The Moving Down % alert is triggered when the source input decreases by a certain percentage value within x-bars.

Notice that you have to set the Number of Bars parameter!

The calculation starts from the last formed candlestick.

Turning Up / Turning Down

The Turning Up alert is triggered when the source input turns up.

The Turning Down alert is triggered when the source input turns down.

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Search in scripts for "algo"

CFB-Adaptive Velocity Histogram [Loxx]CFB-Adaptive Velocity Histogram is a velocity indicator with One-More-Moving-Average Adaptive Smoothing of input source value and Jurik's Composite-Fractal-Behavior-Adaptive Price-Trend-Period input with Dynamic Zones. All Juirk smoothing allows for both single and double Jurik smoothing passes. Velocity is adjusted to pips but there is no input value for the user. This indicator is tuned for Forex but can be used on any time series data.

What is Composite Fractal Behavior ( CFB )?

All around you mechanisms adjust themselves to their environment. From simple thermostats that react to air temperature to computer chips in modern cars that respond to changes in engine temperature, r.p.m.'s, torque, and throttle position. It was only a matter of time before fast desktop computers applied the mathematics of self-adjustment to systems that trade the financial markets.

Unlike basic systems with fixed formulas, an adaptive system adjusts its own equations. For example, start with a basic channel breakout system that uses the highest closing price of the last N bars as a threshold for detecting breakouts on the up side. An adaptive and improved version of this system would adjust N according to market conditions, such as momentum, price volatility or acceleration.

Since many systems are based directly or indirectly on cycles, another useful measure of market condition is the periodic length of a price chart's dominant cycle, (DC), that cycle with the greatest influence on price action.

The utility of this new DC measure was noted by author Murray Ruggiero in the January '96 issue of Futures Magazine. In it. Mr. Ruggiero used it to adaptive adjust the value of N in a channel breakout system. He then simulated trading 15 years of D-Mark futures in order to compare its performance to a similar system that had a fixed optimal value of N. The adaptive version produced 20% more profit!

This DC index utilized the popular MESA algorithm (a formulation by John Ehlers adapted from Burg's maximum entropy algorithm, MEM). Unfortunately, the DC approach is problematic when the market has no real dominant cycle momentum, because the mathematics will produce a value whether or not one actually exists! Therefore, we developed a proprietary indicator that does not presuppose the presence of market cycles. It's called CFB (Composite Fractal Behavior) and it works well whether or not the market is cyclic.

CFB examines price action for a particular fractal pattern, categorizes them by size, and then outputs a composite fractal size index. This index is smooth, timely and accurate

Essentially, CFB reveals the length of the market's trending action time frame. Long trending activity produces a large CFB index and short choppy action produces a small index value. Investors have found many applications for CFB which involve scaling other existing technical indicators adaptively, on a bar-to-bar basis.

What is Jurik Volty used in the Juirk Filter?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

What are Dynamic Zones?

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

Included:

Bar coloring

3 signal variations w/ alerts

Divergences w/ alerts

Loxx's Expanded Source Types

CFB-Adaptive, Williams %R w/ Dynamic Zones [Loxx]CFB-Adaptive, Williams %R w/ Dynamic Zones is a Jurik-Composite-Fractal-Behavior-Adaptive Williams % Range indicator with Dynamic Zones. These additions to the WPR calculation reduce noise and return a signal that is more viable than WPR alone.

What is Williams %R?

Williams %R , also known as the Williams Percent Range, is a type of momentum indicator that moves between 0 and -100 and measures overbought and oversold levels. The Williams %R may be used to find entry and exit points in the market. The indicator is very similar to the Stochastic oscillator and is used in the same way. It was developed by Larry Williams and it compares a stock’s closing price to the high-low range over a specific period, typically 14 days or periods.

What is Composite Fractal Behavior ( CFB )?

All around you mechanisms adjust themselves to their environment. From simple thermostats that react to air temperature to computer chips in modern cars that respond to changes in engine temperature, r.p.m.'s, torque, and throttle position. It was only a matter of time before fast desktop computers applied the mathematics of self-adjustment to systems that trade the financial markets.

Unlike basic systems with fixed formulas, an adaptive system adjusts its own equations. For example, start with a basic channel breakout system that uses the highest closing price of the last N bars as a threshold for detecting breakouts on the up side. An adaptive and improved version of this system would adjust N according to market conditions, such as momentum, price volatility or acceleration.

Since many systems are based directly or indirectly on cycles, another useful measure of market condition is the periodic length of a price chart's dominant cycle, (DC), that cycle with the greatest influence on price action.

The utility of this new DC measure was noted by author Murray Ruggiero in the January '96 issue of Futures Magazine. In it. Mr. Ruggiero used it to adaptive adjust the value of N in a channel breakout system. He then simulated trading 15 years of D-Mark futures in order to compare its performance to a similar system that had a fixed optimal value of N. The adaptive version produced 20% more profit!

This DC index utilized the popular MESA algorithm (a formulation by John Ehlers adapted from Burg's maximum entropy algorithm, MEM). Unfortunately, the DC approach is problematic when the market has no real dominant cycle momentum, because the mathematics will produce a value whether or not one actually exists! Therefore, we developed a proprietary indicator that does not presuppose the presence of market cycles. It's called CFB (Composite Fractal Behavior) and it works well whether or not the market is cyclic.

CFB examines price action for a particular fractal pattern, categorizes them by size, and then outputs a composite fractal size index. This index is smooth, timely and accurate

Essentially, CFB reveals the length of the market's trending action time frame. Long trending activity produces a large CFB index and short choppy action produces a small index value. Investors have found many applications for CFB which involve scaling other existing technical indicators adaptively, on a bar-to-bar basis.

What is Jurik Volty used in the Juirk Filter?

One of the lesser known qualities of Juirk smoothing is that the Jurik smoothing process is adaptive. "Jurik Volty" (a sort of market volatility ) is what makes Jurik smoothing adaptive. The Jurik Volty calculation can be used as both a standalone indicator and to smooth other indicators that you wish to make adaptive.

What is the Jurik Moving Average?

Have you noticed how moving averages add some lag (delay) to your signals? ... especially when price gaps up or down in a big move, and you are waiting for your moving average to catch up? Wait no more! JMA eliminates this problem forever and gives you the best of both worlds: low lag and smooth lines.

Ideally, you would like a filtered signal to be both smooth and lag-free. Lag causes delays in your trades, and increasing lag in your indicators typically result in lower profits. In other words, late comers get what's left on the table after the feast has already begun.

What are Dynamic Zones?

As explained in "Stocks & Commodities V15:7 (306-310): Dynamic Zones by Leo Zamansky, Ph .D., and David Stendahl"

Most indicators use a fixed zone for buy and sell signals. Here’ s a concept based on zones that are responsive to past levels of the indicator.

One approach to active investing employs the use of oscillators to exploit tradable market trends. This investing style follows a very simple form of logic: Enter the market only when an oscillator has moved far above or below traditional trading lev- els. However, these oscillator- driven systems lack the ability to evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market. And therein lies the problem.

Once traders begin introducing their market opinions into trading equations, by changing the zones, they negate the system’s mechanical nature. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market — bull or bear. Dynamic zones offer a solution to the problem of fixed buy and sell zones for any oscillator-driven system.

An indicator’s extreme levels can be quantified using statistical methods. These extreme levels are calculated for a certain period and serve as the buy and sell zones for a trading system. The repetition of this statistical process for every value of the indicator creates values that become the dynamic zones. The zones are calculated in such a way that the probability of the indicator value rising above, or falling below, the dynamic zones is equal to a given probability input set by the trader.

To better understand dynamic zones, let's first describe them mathematically and then explain their use. The dynamic zones definition:

Find V such that:

For dynamic zone buy: P{X <= V}=P1

For dynamic zone sell: P{X >= V}=P2

where P1 and P2 are the probabilities set by the trader, X is the value of the indicator for the selected period and V represents the value of the dynamic zone.

The probability input P1 and P2 can be adjusted by the trader to encompass as much or as little data as the trader would like. The smaller the probability, the fewer data values above and below the dynamic zones. This translates into a wider range between the buy and sell zones. If a 10% probability is used for P1 and P2, only those data values that make up the top 10% and bottom 10% for an indicator are used in the construction of the zones. Of the values, 80% will fall between the two extreme levels. Because dynamic zone levels are penetrated so infrequently, when this happens, traders know that the market has truly moved into overbought or oversold territory.

Calculating the Dynamic Zones

The algorithm for the dynamic zones is a series of steps. First, decide the value of the lookback period t. Next, decide the value of the probability Pbuy for buy zone and value of the probability Psell for the sell zone.

For i=1, to the last lookback period, build the distribution f(x) of the price during the lookback period i. Then find the value Vi1 such that the probability of the price less than or equal to Vi1 during the lookback period i is equal to Pbuy. Find the value Vi2 such that the probability of the price greater or equal to Vi2 during the lookback period i is equal to Psell. The sequence of Vi1 for all periods gives the buy zone. The sequence of Vi2 for all periods gives the sell zone.

In the algorithm description, we have: Build the distribution f(x) of the price during the lookback period i. The distribution here is empirical namely, how many times a given value of x appeared during the lookback period. The problem is to find such x that the probability of a price being greater or equal to x will be equal to a probability selected by the user. Probability is the area under the distribution curve. The task is to find such value of x that the area under the distribution curve to the right of x will be equal to the probability selected by the user. That x is the dynamic zone.

Included:

Bar coloring

3 signal variations w/ alerts

Divergences w/ alerts

Loxx's Expanded Source Types

Intermediate Williams %R w/ Discontinued Signal Lines [Loxx]Intermediate Williams %R w/ Discontinued Signal Lines is a Williams %R indicator with advanced options:

-Williams %R smoothing, 30+ smoothing algos found here:

-Williams %R signal, 30+ smoothing algos found here:

-DSL lines with smoothing or fixed overbought/oversold boundaries, smoothing algos are EMA and FEMA

-33 Expanded Source Type inputs including Heiken-Ashi and Heiken-Ashi Better, found here:

What is Williams %R?

Williams %R, also known as the Williams Percent Range, is a type of momentum indicator that moves between 0 and -100 and measures overbought and oversold levels. The Williams %R may be used to find entry and exit points in the market. The indicator is very similar to the Stochastic oscillator and is used in the same way. It was developed by Larry Williams and it compares a stock’s closing price to the high-low range over a specific period, typically 14 days or periods.

Included:

-Toggle on/off bar coloring

-Toggle on/off signal line

OrdinaryLeastSquaresLibrary "OrdinaryLeastSquares"

One of the most common ways to estimate the coefficients for a linear regression is to use the Ordinary Least Squares (OLS) method.

This library implements OLS in pine. This implementation can be used to fit a linear regression of multiple independent variables onto one dependent variable,

as long as the assumptions behind OLS hold.

solve_xtx_inv(x, y) Solve a linear system of equations using the Ordinary Least Squares method.

This function returns both the estimated OLS solution and a matrix that essentially measures the model stability (linear dependence between the columns of 'x').

NOTE: The latter is an intermediate step when estimating the OLS solution but is useful when calculating the covariance matrix and is returned here to save computation time

so that this step doesn't have to be calculated again when things like standard errors should be calculated.

Parameters:

x : The matrix containing the independent variables. Each column is regarded by the algorithm as one independent variable. The row count of 'x' and 'y' must match.

y : The matrix containing the dependent variable. This matrix can only contain one dependent variable and can therefore only contain one column. The row count of 'x' and 'y' must match.

Returns: Returns both the estimated OLS solution and a matrix that essentially measures the model stability (xtx_inv is equal to (X'X)^-1).

solve(x, y) Solve a linear system of equations using the Ordinary Least Squares method.

Parameters:

x : The matrix containing the independent variables. Each column is regarded by the algorithm as one independent variable. The row count of 'x' and 'y' must match.

y : The matrix containing the dependent variable. This matrix can only contain one dependent variable and can therefore only contain one column. The row count of 'x' and 'y' must match.

Returns: Returns the estimated OLS solution.

standard_errors(x, y, beta_hat, xtx_inv) Calculate the standard errors.

Parameters:

x : The matrix containing the independent variables. Each column is regarded by the algorithm as one independent variable. The row count of 'x' and 'y' must match.

y : The matrix containing the dependent variable. This matrix can only contain one dependent variable and can therefore only contain one column. The row count of 'x' and 'y' must match.

beta_hat : The Ordinary Least Squares (OLS) solution provided by solve_xtx_inv() or solve().

xtx_inv : This is (X'X)^-1, which means we take the transpose of the X matrix, multiply that the X matrix and then take the inverse of the result.

This essentially measures the linear dependence between the columns of the X matrix.

Returns: The standard errors.

estimate(x, beta_hat) Estimate the next step of a linear model.

Parameters:

x : The matrix containing the independent variables. Each column is regarded by the algorithm as one independent variable. The row count of 'x' and 'y' must match.

beta_hat : The Ordinary Least Squares (OLS) solution provided by solve_xtx_inv() or solve().

Returns: Returns the new estimate of Y based on the linear model.

NormalizedOscillatorsLibrary "NormalizedOscillators"

Collection of some common Oscillators. All are zero-mean and normalized to fit in the -1..1 range. Some are modified, so that the internal smoothing function could be configurable (for example, to enable Hann Windowing, that John F. Ehlers uses frequently). Some are modified for other reasons (see comments in the code), but never without a reason. This collection is neither encyclopaedic, nor reference, however I try to find the most correct implementation. Suggestions are welcome.

rsi2(upper, lower) RSI - second step

Parameters:

upper : Upwards momentum

lower : Downwards momentum

Returns: Oscillator value

Modified by Ehlers from Wilder's implementation to have a zero mean (oscillator from -1 to +1)

Originally: 100.0 - (100.0 / (1.0 + upper / lower))

Ignoring the 100 scale factor, we get: upper / (upper + lower)

Multiplying by two and subtracting 1, we get: (2 * upper) / (upper + lower) - 1 = (upper - lower) / (upper + lower)

rms(src, len) Root mean square (RMS)

Parameters:

src : Source series

len : Lookback period

Based on by John F. Ehlers implementation

ift(src) Inverse Fisher Transform

Parameters:

src : Source series

Returns: Normalized series

Based on by John F. Ehlers implementation

The input values have been multiplied by 2 (was "2*src", now "4*src") to force expansion - not compression

The inputs may be further modified, if needed

stoch(src, len) Stochastic

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

ssstoch(src, len) Super Smooth Stochastic (part of MESA Stochastic) by John F. Ehlers

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

Introduced in the January 2014 issue of Stocks and Commodities

This is not an implementation of MESA Stochastic, as it is based on Highpass filter not present in the function (but you can construct it)

This implementation is scaled by 0.95, so that Super Smoother does not exceed 1/-1

I do not know, if this the right way to fix this issue, but it works for now

netKendall(src, len) Noise Elimination Technology by John F. Ehlers

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

Introduced in the December 2020 issue of Stocks and Commodities

Uses simplified Kendall correlation algorithm

Implementation by @QuantTherapy:

rsi(src, len, smooth) RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

vrsi(src, len, smooth) Volume-scaled RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

This is my own version of RSI. It scales price movements by the proportion of RMS of volume

mrsi(src, len, smooth) Momentum RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Inspired by RocketRSI by John F. Ehlers (Stocks and Commodities, May 2018)

rrsi(src, len, smooth) Rocket RSI

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Inspired by RocketRSI by John F. Ehlers (Stocks and Commodities, May 2018)

Does not include Fisher Transform of the original implementation, as the output must be normalized

Does not include momentum smoothing length configuration, so always assumes half the lookback length

mfi(src, len, smooth) Money Flow Index

Parameters:

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

lrsi(src, in_gamma, len) Laguerre RSI by John F. Ehlers

Parameters:

src : Source series

in_gamma : Damping factor (default is -1 to generate from len)

len : Lookback period (alternatively, if gamma is not set)

Returns: Oscillator series

The original implementation is with gamma. As it is impossible to collect gamma in my system, where the only user input is length,

an alternative calculation is included, where gamma is set by dividing len by 30. Maybe different calculation would be better?

fe(len) Choppiness Index or Fractal Energy

Parameters:

len : Lookback period

Returns: Oscillator series

The Choppiness Index (CHOP) was created by E. W. Dreiss

This indicator is sometimes called Fractal Energy

er(src, len) Efficiency ratio

Parameters:

src : Source series

len : Lookback period

Returns: Oscillator series

Based on Kaufman Adaptive Moving Average calculation

This is the correct Efficiency ratio calculation, and most other implementations are wrong:

the number of bar differences is 1 less than the length, otherwise we are adding the change outside of the measured range!

For reference, see Stocks and Commodities June 1995

dmi(len, smooth) Directional Movement Index

Parameters:

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Based on the original Tradingview algorithm

Modified with inspiration from John F. Ehlers DMH (but not implementing the DMH algorithm!)

Only ADX is returned

Rescaled to fit -1 to +1

Unlike most oscillators, there is no src parameter as DMI works directly with high and low values

fdmi(len, smooth) Fast Directional Movement Index

Parameters:

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Same as DMI, but without secondary smoothing. Can be smoothed later. Instead, +DM and -DM smoothing can be configured

doOsc(type, src, len, smooth) Execute a particular Oscillator from the list

Parameters:

type : Oscillator type to use

src : Source series

len : Lookback period

smooth : Internal smoothing algorithm

Returns: Oscillator series

Chande Momentum Oscillator (CMO) is RSI without smoothing. No idea, why some authors use different calculations

LRSI with Fractal Energy is a combo oscillator that uses Fractal Energy to tune LRSI gamma, as seen here: www.prorealcode.com

doPostfilter(type, src, len) Execute a particular Oscillator Postfilter from the list

Parameters:

type : Oscillator type to use

src : Source series

len : Lookback period

Returns: Oscillator series

Average Down [Zeiierman]AVERAGING DOWN

Averaging down is an investment strategy that involves buying additional contracts of an asset when the price drops. This way, the investor increases the size of their position at discounted prices. The averaging down strategy is highly debated among traders and investors because it can either lead to huge losses or great returns. Nevertheless, averaging down is often used and favored by long-term investors and contrarian traders. With careful/proper risk management, averaging down can cover losses and magnify the returns when the asset rebounds. However, the main concern for a trader is that it can be hard to identify the difference between a pullback or the start of a new trend.

HOW DOES IT WORK

Averaging down is a method to lower the average price at which the investor buys an asset. A lower average price can help investors come back to break even quicker and, if the price continues to rise, get an even bigger upside and thus increase the total profit from the trade. For example, We buy 100 shares at $60 per share, a total investment of $6000, and then the asset drops to $40 per share; in order to come back to break even, the price has to go up 50%. (($60/$40) - 1)*100 = 50%.

The power of Averaging down comes into play if the investor buys additional shares at a lower price, like another 100 shares at $40 per share; the total investment is ($6000+$4000 = $10000). The average price for the investment is now $50. (($60 x 100) + ($40 x 100))/200; in order to get back to break even, the price has to rise 25% ($50/$40)-1)*100 = 25%, and if the price continues up to $60 per share, the investor can secure a profit at 16%. So by averaging down, investors and traders can cover the losses easier and potentially have more profit to secure at the end.

THE AVERAGE DOWN TRADINGVIEW TOOL

This script/indicator/trading tool helps traders and investors to get the average price of their position. The tool works for Long and Short and displays the entry price, average price, and the PnL in points.

HOW TO USE

Use the tool to calculate the average price of your long or short position in any market and timeframe.

Get the current PnL for the investment and keep track of your entry prices.

APPLY TO CHART

When you apply the tool on the chart, you have to select five entry points, and within the setting panel, you can choose how many of these five entry points are active and how many contracts each entry has. Then, the tool will display your average price based on the entries and the number of contracts used at each price level.

LONG

Set your entries and the number of contracts at each price level. The indicator will then display all your long entries and at what price you will break even. The entry line changes color based on if the entry is in profit or loss.

SHORT

Set your entries and the number of contracts at each price level. The indicator will then display all your short entries and at what price you will break even. The entry line changes color based on if the entry is in profit or loss.

-----------------

Disclaimer

Copyright by Zeiierman.

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual’s trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

Example: Monte Carlo SimulationExperimental:

Example execution of Monte Carlo Simulation applied to the markets(this is my interpretation of the algo so inconsistencys may appear).

note:

the algorithm is very demanding so performance is limited.

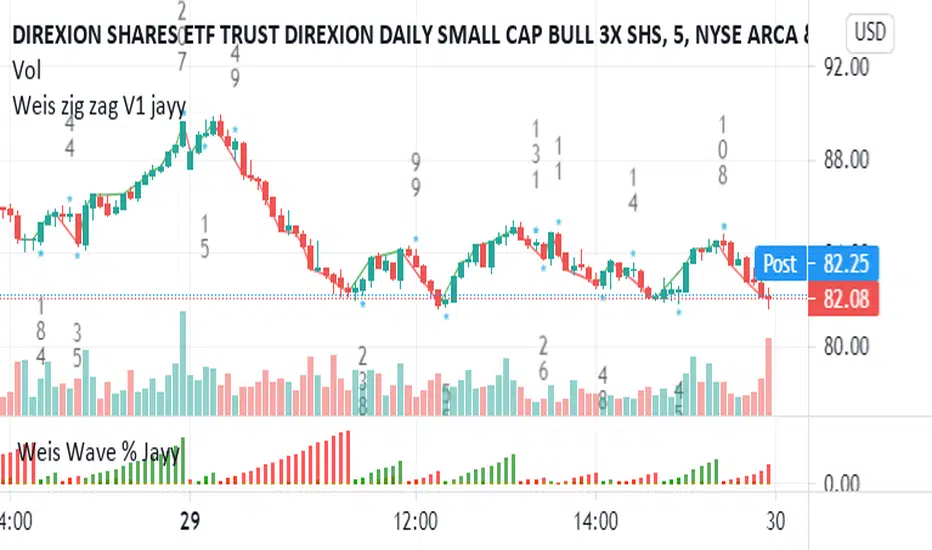

Weis pip zigzag jayyWhat you see here is the Weis pip zigzag wave plotted directly on the price chart. This script is the companion to the Weis pip wave ( ) which is plotted in the lower panel of the displayed chart and can be used as an alternate way of plotting the same results. The Weis pip zigzag wave shows how far in terms of price a Weis wave has traveled through the duration of a Weis wave. The Weis pip zigzag wave is used in combination with the Weis cumulative volume wave. The two waves must be set to the same "wave size".

To use this script you must set the wave size. Using the traditional Weis method simply enter the desired wave size in the box "Select Weis Wave Size" In this example, it is set to 5. Each wave for each security and each timeframe requires its own wave size. Although not the traditional method a more automatic way to set wave size would be to use ATR. This is not the true Weis method but it does give you similar waves and, importantly, without the hassle described above. Once the Weis wave size is set then the pip wave will be shown.

I have put a pip zigzag of a 5 point Weis wave on the bar chart - that is a different script. I have added it to allow your eye to see what a Weis wave looks like. You will notice that the wave is not in straight lines connecting wave tops to bottoms this is a function of the limitations of Pinescript version 1. This script would need to be in version 4 to allow straight lines. There are too many calculations within this script to allow conversion to Pinescript version 4 or even Version 3. I am in the process of rewriting this script to reduce the number of calculations and streamline the algorithm.

The numbers plotted on the chart are calculated to be relative numbers. The script is limited to showing only three numbers vertically. Only the highest three values of a number are shown. For example, if the highest recent pip value is 12,345 only the first 3 numerals would be displayed ie 123. But suppose there is a recent value of 691. It would not be helpful to display 691 if the other wave size is shown as 123. To give the appropriate relative value the script will show a value of 7 instead of 691. This informs you of the relative magnitude of the values. This is done automatically within the script. There is likely no need to manually override the automatically calculated value. I will create a video that demonstrates the manual override method.

What is a Weis wave? David Weis has been recognized as a Wyckoff method analyst he has written two books one of which, Trades About to Happen, describes the evolution of the now popular Weis wave. The method employed by Weis is to identify waves of price action and to compare the strength of the waves on characteristics of wave strength. Chief among the characteristics of strength is the cumulative volume of the wave. There are other markers that Weis uses as well for example how the actual price difference between the start of the Weis wave from start to finish. Weis also uses time, particularly when using a Renko chart. Weis specifically uses candle or bar closes to define all wave action ie a line chart.

David Weis did a futures io video which is a popular source of information about his method.

This is the identical script with the identical settings but without the offending links. If you want to see the pip Weis method in practice then search Weis pip wave. If you want to see Weis chart in pdf then message me and I will give a link or the Weis pdf. Why would you want to see the Weis chart for May 27, 2020? Merely to confirm the veracity of my algorithm. You could compare my Weis chart here () from the same period to the David Weis chart from May 27. Both waves are for the ES!1 4 hour chart and both for a wave size of 5.

Price Action and 3 EMAs Momentum plus Sessions FilterThis indicator plots on the chart the parameters and signals of the Price Action and 3 EMAs Momentum plus Sessions Filter Algorithmic Strategy. The strategy trades based on time-series (absolute) and relative momentum of price close, highs, lows and 3 EMAs.

I am still learning PS and therefore I have only been able to write the indicator up to the Signal generation. I plan to expand the indicator to Entry Signals as well as the full Strategy.

The strategy works best on EURUSD in the 15 minutes TF during London and New York sessions with 1 to 1 TP and SL of 30 pips with lots resulting in 3% risk of the account per trade. I have already written the full strategy in another language and platform and back tested it for ten years and it was profitable for 7 of the 10 years with average profit of 15% p.a which can be easily increased by increasing risk per trade. I have been trading it live in that platform for over two years and it is profitable.

Contributions from experienced PS coders in completing the Indicator as well as writing the Strategy and back testing it on Trading View will be appreciated.

STRATEGY AND INDICATOR PARAMETERS

Three periods of 12, 48 and 96 in the 15 min TF which are equivalent to 3, 12 and 24 hours i.e (15 min * period / 60 min) are the foundational inputs for all the parameters of the PA & 3 EMAs Momentum + SF Algo Strategy and its Indicator.

3 EMAs momentum parameters and conditions

• FastEMA = ema of 12 periods

• MedEMA = ema of 48 periods

• SlowEMA = ema of 96 periods

• All the EMAs analyse price close for up to 96 (15 min periods) equivalent to 24 hours

• There’s Upward EMA momentum if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA

• There’s Downward EMA momentum if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA

PA momentum parameters and conditions

• HH = Highest High of 48 periods from 1st closed bar before current bar

• LL = Lowest Low of 48 periods from 1st closed bar from current bar

• Previous HH = Highest High of 84 periods from 12th closed bar before current bar

• Previous LL = Lowest Low of 84 periods from 12th closed bar before current bar

• All the HH & LL and prevHH & prevLL are within the 96 periods from the 1st closed bar before current bar and therefore indicative of momentum during the past 24 hours

• There’s Upward PA momentum if price close > HH and HH > prevHH and LL > prevLL

• There’s Downward PA momentum if price close < LL and LL < prevLL and HH < prevHH

Signal conditions and Status (BuySignal, SellSignal or Neutral)

• The strategy generates Buy or Sell Signals if both 3 EMAs and PA momentum conditions are met for each direction and these occur during the London and New York sessions

• BuySignal if price close > FastEMA and FastEMA > MedEMA and MedEMA > SlowEMA and price close > HH and HH > prevHH and LL > prevLL and timeinrange (LDN&NY) else Neutral

• SellSignal if price close < FastEMA and FastEMA < MedEMA and MedEMA < SlowEMA and price close < LL and LL < prevLL and HH < prevHH and timeinrange (LDN&NY) else Neutral

Entry conditions and Status (EnterBuy, EnterSell or Neutral)(NOT CODED YET)

• ENTRY IS NOT AT THE SIGNAL BAR but at the current bar tick price retracement to FastEMA after the signal

• EnterBuy if current bar tick price <= FastEMA and current bar tick price > prevHH at the time of the Buy Signal

• EnterSell if current bar tick price >= FastEMA and current bar tick price > prevLL at the time of the Sell Signal

NAND PerceptronExperimental NAND Perceptron based upon Python template that aims to predict NAND Gate Outputs. A Perceptron is one of the foundational building blocks of nearly all advanced Neural Network layers and models for Algo trading and Machine Learning.

The goal behind this script was threefold:

To prove and demonstrate that an ACTUAL working neural net can be implemented in Pine, even if incomplete.

To pave the way for other traders and coders to iterate on this script and push the boundaries of Tradingview strategies and indicators.

To see if a self-contained neural network component for parameter optimization within Pinescript was hypothetically possible.

NOTE: This is a highly experimental proof of concept - this is NOT a ready-made template to include or integrate into existing strategies and indicators, yet (emphasis YET - neural networks have a lot of potential utility and potential when utilized and implemented properly).

Hardcoded NAND Gate outputs with Bias column (X0):

// NAND Gate + X0 Bias and Y-true

// X0 // X1 // X2 // Y

// 1 // 0 // 0 // 1

// 1 // 0 // 1 // 1

// 1 // 1 // 0 // 1

// 1 // 1 // 1 // 0

Column X0 is bias feature/input

Column X1 and X2 are the NAND Gate

Column Y is the y-true values for the NAND gate

yhat is the prediction at that timestep

F0,F1,F2,F3 are the Dot products of the Weights (W0,W1,W2) and the input features (X0,X1,X2)

Learning rate and activation function threshold are enabled by default as input parameters

Uncomment sections for more training iterations/epochs:

Loop optimizations would be amazing to have for a selectable length for training iterations/epochs but I'm not sure if it's possible in Pine with how this script is structured.

Error metrics and loss have not been implemented due to difficulty with script length and iterations vs epochs - I haven't been able to configure the input parameters to successfully predict the right values for all four y-true values for the NAND gate (only been able to get 3/4; If you're able to get all four predictions to be correct, let me know, please).

// //---- REFERENCE for final output

// A3 := 1, y0 true

// B3 := 1, y1 true

// C3 := 1, y2 true

// D3 := 0, y3 true

PLEASE READ: Source article/template and main code reference:

towardsdatascience.com

towardsdatascience.com

towardsdatascience.com

Baseline-C [ID: AC-P]The "AC-P" version of jiehonglim's NNFX Baseline script is my personal customized version of the NNFX Baseline concept as part of the NNFX Algorithm stack/structure for 1D Trend Trading for Forex. Everget's JMA implementation is used for the baseline smoothing method, with optional ATR bands at 1.0x and 1.5x from the baseline.

NNFX = No Nonsense Forex

Baseline = Component of the NNFX Algorithm that consists of a single moving average

Baseline ---> Meant to be used in conjunction with ATR/C1/C2/Vol Indicator/Exit Indicator as per NNFX Algorithm setup/structure. C1 is 1st Confirmation Indicator, C2 is 2nd Confirmation Indicator.

JMA (Jurik Moving Average) is used for the baseline and slow baseline.

A slow baseline option is included, but disabled by default.

The faint orange/purple lines are 1.0x/1.5x ATR from the Baseline, and are what I use as potential TP/SL targets or to evaluate when to stay out of a trade (chop/missed entry/exit/other/ATR breach), depending on the trade setup (in conjunction with C1/C2/Vol Indicator/Exit Indicator)

This script is heavily based upon jiehonglim's NNFX Baseline script for signaling, barcoloring, and ATR.

SSL Channel option included but disabled by default (Erwinbeckers SSL component)

POC (Point of Control) from Volume Profile is included/enabled by default for both the current timeframe and 12HR timeframe

03.freeman's InfoPanel Divergence Indicator was used a reference to replace the current/previous ATR information infopanel/info draw from jiehonglim's script. I'm not sure whether I like the previous way ATR info was displayed vs how I have it currently, but it's something that is completely optional:

Specifically: I am tuning this baseline/indicator for 1D trading as part of the NNFX system, for Forex.

DO NOT USE THIS INDICATOR WITHOUT PROPER TUNING/ADJUSTMENT for your timeframe and asset class.

Note about lack of alerts:

Alerts for baseline crosses (and other crosses) have been purposefully omitted for this version upon initial publication. While getting alerts for baseline crosses under certain conditions/filtered conditions that eliminate low-importance signals and crossover whipsaw would be great, it's something I'm still looking into.

SPECIFICALLY: There are entry, exit, take profit, and continuation signal components in relation to the Baseline to the rest of the NNFX Algorithm stack (ATR/C1/C2/Vol Indicator/Exit Indicator), including but limited to the "1 candle rule" and the "7 candle rule" as per NNFX.

Implementing alerts that are significant that also factor in these rules while reducing alert spam/false signals would be ideal, but it's also the HTF/Daily chart - visually, entry/exit/continuation signal alignment is easy to spot when trading 1D - alerts may be redundant/a pursuit in diminishing returns (for now).

//-------------------------------------------------------------------

// Acknowledgements/Reference:

// jiehonglim, NNFX Baseline Script - Moving Averages

//

// Fractured, Many Moving Averages

//

// everget, Jurik Moving Average/JMA

//

// 03.freeman, InfoPanel Divergence Indicator

//

// Ggqmna Volume stops

//

// Libertus RSI Divs

//

// ChrisMoody, CM_Price-Action-Bars-Price Patterns That Work

//

// Erwinbeckers SSL Channel

//

WickPressureLibWickPressureLib: The Regime Dynamics Engine

DESCRIPTION:

WickPressureLib/b] is not a standard candlestick pattern library. It is an advanced analytical engine designed to deconstruct the internal dynamics of price action. It provides a definitive toolkit for analyzing candle microstructure and quantifying order flow pressure through statistical modeling.

█ CHAPTER 1: THE PHILOSOPHY — BEYOND PATTERNS, INTO DYNAMICS

A candlestick wick represents a specific market event: a rejection of price. Traditional analysis often labels these simply as "bullish" or "bearish." This library aims to go deeper by treating each candle as a dataset of opposing forces.

The WickPressureLib translates static price action into dynamic metrics. It deconstructs the candle into core components and subjects them to multi-layered analysis. It calculates Kinetic Force , estimates institutional Delta , tracks the Siege Decay of key levels, and uses Thompson Sampling (a Bayesian probability algorithm) to assess the statistical weight of each formation.

This library does not just identify patterns; it quantifies the forces that create them. It is designed for developers who need quantitative, data-driven metrics rather than subjective interpretation.

█ CHAPTER 2: THE ANALYTICAL PIPELINE — SIX LAYERS OF LOGIC

The engine's capabilities come from a six-stage processing pipeline. Each layer builds upon the last to create a comprehensive data object.

LAYER 1 — DELTA ESTIMATION: Uses a proprietary model to approximate order flow (Delta) within a single candle based on the relationship between wicks, body, and total range.

LAYER 2 — SIEGE ANALYSIS: A concept for measuring structural integrity. Every time a price level is tested by a wick, its "Siege Decay" score is updated. Repeated tests without a breakout result in a decayed score, indicating weakening support/resistance.

LAYER 3 — MAGNETISM ENGINE: Calculates the probability of a wick being "filled" (mean reversion) based on trend strength and volume profile. Distinguishes between rejection wicks and exhaustion wicks.

LAYER 4 — REGIME DETECTION: Context-aware analysis using statistical tools— Shannon Entropy (disorder), DFA (trend vs. mean-reversion), and Hurst Exponent (persistence)—to classify the market state (e.g., "Bull Trend," "Bear Range," "Choppy").

LAYER 5 — ADAPTIVE LEARNING (THOMPSON SAMPLING): Uses a Bayesian Multi-Armed Bandit algorithm to track performance. It maintains a set of "Agents," each tracking a different wick pattern type. Based on historical outcomes, the system updates the probability score for each pattern in real-time.

LAYER 6 — CONTEXTUAL ROUTING: The final layer of logic. The engine analyzes the wick, determines its pattern type, and routes it to the appropriate Agent for probability assessment, weighted by the current market regime.

█ CHAPTER 3: CORE FUNCTIONS

analyze_wick() — The Master Analyzer

The primary function. Accepts a bar index and returns a WickAnalysis object containing over 15 distinct metrics:

• Anomaly Score: Z-Score indicating how statistically rare the wick's size is.

• Kinetic Force: Metric combining range and relative volume to quantify impact.

• Estimated Delta: Approximation of net buying/selling pressure.

• Siege Decay: Structural integrity of the tested level.

• Magnet Score: Probability of the wick being filled.

• Win Probability: Adaptive success rate based on the Thompson Sampling engine.

scan_clusters() — Liquidity Zone Detection

Scans recent price history to identify "Pressure Clusters"—zones where multiple high-pressure wicks have overlapped. Useful for finding high-probability supply and demand zones.

detect_regime() — Context Engine

Uses statistical methods to determine the market's current personality (Trending, Ranging, or Volatile). This output allows the analysis to adapt dynamically to changing conditions.

█ CHAPTER 4: DEVELOPER INTEGRATION GUIDE

This library is a low-level engine for building sophisticated indicators.

1. Import the Library:

import DskyzInvestments/DafeWickLib/1 as wpk

2. Initialize the Agents:

var agents = wpk.create_learning_agents()

3. Analyze the Market:

regime = wpk.detect_regime(100)

wick_data = wpk.analyze_wick(0, regime, agents)

prob = wpk.get_probability(wick_data, regime)

4. Update Learning (Feedback Loop):

agent_id = wpk.get_agent_by_pattern(wick_data)

agents := wpk.update_learning_agent(agents, agent_id, 1.0) // +1 win, -1 loss

█ CHAPTER 5: THE DEVELOPER'S FRAMEWORK — INTEGRATION GUIDE

This library serves as a professional integration framework. This guide provides instructions and templates required to connect the DAFE components into a unified custom Pine Script indicator.

PART I: THE INPUTS TEMPLATE (CONTROL PANEL)

To provide users full control over the system, include the input templates from all connected libraries. This section details the bridge-specific controls.

// ╔═════════════════════════════════════════════════════════╗

// ║ BRIDGE INPUTS TEMPLATE (COPY INTO YOUR SCRIPT) ║

// ╚═════════════════════════════════════════════════════════╝

// INPUT GROUPS

string G_BRIDGE_MAIN = "════════════ 🌉 BRIDGE CONFIG ════════════"

string G_BRIDGE_EXT = "════════════ 🌐 EXTERNAL DATA ════════════"

// BRIDGE MAIN CONFIG

float i_bridge_min_conf = input.float(0.55, "Min Confidence to Trade",

minval=0.4, maxval=0.8, step=0.01, group=G_BRIDGE_MAIN,

tooltip="Minimum blended confidence required for a trade signal.")

int i_bridge_warmup = input.int(100, "System Warmup Bars",

minval=50, maxval=500, group=G_BRIDGE_MAIN,

tooltip="Bars required for data gathering before signals begin.")

// EXTERNAL DATA SOCKETS

bool i_ext_enable = input.bool(true, "🌐 Enable External Data Sockets",

group=G_BRIDGE_EXT,

tooltip="Enables analysis of external market data (e.g., VIX, DXY).")

// Example for one external socket

string i_ext1_name = input.string("VIX", "Socket 1: Name", group=G_BRIDGE_EXT, inline="ext1")

string i_ext1_sym = input.symbol("TVC:VIX", "Symbol", group=G_BRIDGE_EXT, inline="ext1")

string i_ext1_type = input.string("volatility", "Data Type",

options= ,

group=G_BRIDGE_EXT, inline="ext1")

float i_ext1_weight = input.float(1.0, "Weight", minval=0.1, maxval=2.0, step=0.1, group=G_BRIDGE_EXT, inline="ext1")

PART II: IMPLEMENTATION LOGIC (THE CORE LOOP)

This boilerplate code demonstrates the complete, unified pipeline structure.

// ╔════════════════════════════════════════════════════════╗

// ║ USAGE EXAMPLE (ADAPT TO YOUR SCRIPT) ║

// ╚════════════════════════════════════════════════════════╝

// 1. INITIALIZE ENGINES (First bar only)

var rl.RLAgent agent = rl.init(...)

var spa.SPAEngine spa_engine = spa.init(...)

var bridge.BridgeState bridge_state = bridge.init_bridge(i_spa_num_arms, i_rl_num_actions, i_bridge_min_conf, i_bridge_warmup)

// 2. CONNECT SOCKETS (First bar only)

if barstate.isfirst

// Connect internal sockets

agent := rl.connect_socket(agent, "rsi", ...)

// Register external sockets

if i_ext_enable

ext_socket_1 = bridge.create_ext_socket(i_ext1_name, i_ext1_sym, i_ext1_type, i_ext1_weight)

bridge_state := bridge.register_ext_socket(bridge_state, ext_socket_1)

// 3. MAIN LOOP (Every bar)

// --- A. UPDATE EXTERNAL DATA ---

if i_ext_enable

= request.security(i_ext1_sym, timeframe.period, )

bridge_state := bridge.update_ext_by_name(bridge_state, i_ext1_name, ext1_c, ext1_h, ext1_l)

bridge_state := bridge.aggregate_ext_sockets(bridge_state)

// --- B. RL/ML PROPOSES ---

rl.RLState ml_state = rl.build_state(agent)

= rl.select_action(agent, ml_state)

agent := updated_agent

// --- C. BRIDGE TRANSLATES ---

array arm_signals = bridge.generate_arm_signals(ml_action.action, ml_action.confidence, i_spa_num_arms, i_rl_num_actions, 0)

// --- D. SPA DISPOSES ---

spa_engine := spa.feed_signals(spa_engine, arm_signals, close)

= spa.select(spa_engine)

spa_engine := updated_spa

string arm_name = spa.get_name(spa_engine, selected_arm)

// --- E. RECONCILE REGIME & COMPUTE RISK ---

bridge_state := bridge.reconcile_regime(bridge_state, ml_regime_id, ml_regime_name, ml_conf, spa_regime_id, spa_conf, ...)

float risk = bridge.compute_risk(bridge_state, ml_action.confidence, spa_conf, ...)

// --- F. MAKE FINAL DECISION ---

bridge_state := bridge.make_decision(bridge_state, ml_action.action, ml_action.confidence, selected_arm, arm_name, final_spa_signal, spa_conf, risk, 0.25)

bridge.UnifiedDecision final_decision = bridge_state.decision

// --- G. EXECUTE ---

if final_decision.should_trade

// Plot signals, manage positions based on final_decision.direction

// --- H. LEARN (FEEDBACK LOOP) ---

if (trade_is_closed)

bridge_state := bridge.compute_reward(bridge_state, selected_arm, ...)

agent := rl.learn(agent, ..., bridge_state.reward.shaped_reward, ...)

// --- I. PERFORMANCE & DIAGNOSTICS ---

bridge_state := bridge.update_performance(bridge_state, actual_market_direction)

if barstate.islast

label.new(bar_index, high, bridge.bridge_diagnostics(bridge_state), textalign=text.align_left)

█ DEVELOPMENT PHILOSOPHY

DafeMLSPABridge represents a hierarchical design philosophy. We believe robust systems rely not on a single algorithm, but on the intelligent integration of specialized subsystems. A complete trading logic requires tactical precision (ML), strategic selection (SPA), and environmental awareness (External Sockets). This library provides the infrastructure for these components to communicate and coordinate.

█ DISCLAIMER & IMPORTANT NOTES

• LIBRARY FOR DEVELOPERS: This script is an integration tool and produces no output on its own. It requires implementation of DafeRLMLLib and DafeSPALib.

• COMPUTATION: Full bridged systems are computationally intensive.

• RISK: All automated decisions are based on statistical probabilities from historical data. They do not predict future market movements with certainty.

"The whole is greater than the sum of its parts." — Aristotle

Create with DAFE.

Acrobatic Loto Predictor [Taolue Remix]

市場のカオスを、幸運の数字へ。

このインジケーターは、現在のチャートの「価格変動」「時間」「ボラティリティ」を複雑な計算式(カオス力学)に通すことで、 Loto 6 (6/43) および Loto 7 (7/37) の予想数字を算出する実験的なツールです。

単なるランダム生成(乱数)ではありません。RSIやボリンジャーバンドといったテクニカル指標の数値を「乱数の種(シード)」として使用しているため、 「相場の息遣い」がそのまま数字として出力されます。

【主な機能】

1. モード: 設定画面から「Loto 6」と「Loto 7」を切り替え可能です。

2. カオス&テクニカル・ロジック:

- カオス力学: ローレンツ・アトラクタに着想を得た非線形計算。

- テクニカル: RSI(相対力指数)とボリンジャーバンドの位置関係を係数化。

- 概念定数: 黄金比(φ)や特定の数学的定数を隠し味に配合。

3. ストップ(固定)機能: チャートが動くたびに数字は変動しますが、「ここだ!」と思った瞬間にチェックボックスで数字を 完全固定(ロック) できます。

4. リロール(再抽選)機能: 固定した数字が気に入らない場合、リロール値を変更することで、その瞬間のパラレルワールド(別の計算結果)を呼び出せます。

5. ディスコモード: 数字が変動している間は背景色がリズミカルに変化し、固定すると色が落ち着く視覚効果付き。

【使い方】

1. チャートに追加します(ビットコインや為替など、動きのある銘柄推奨)。

2. 設定画面で Loto 6 か Loto 7 を選びます。

3. チャートを眺め、相場の「波」を感じます。

4. 直感的に良いタイミングで設定画面の 「ストップ(数値を固定)」 にチェックを入れます。

5. 表示された数字をメモします。(気に入らなければ「結果のリロール」数値を変更してください)

※免責事項:

このツールはエンターテインメント目的で作成されています。当選を保証するものではありません。宝くじの購入は自己責任で楽しみましょう。

---

Transform Market Chaos into Lucky Numbers.

This indicator is an experimental tool that generates predictions for Loto 6 and Loto 7 by feeding current chart data—price action, time, and volatility—into complex chaotic algorithms.

This is not a simple random number generator. It uses technical indicators like RSI and Bollinger Bands as "seeds" for generation. Essentially, the heartbeat of the market decides your numbers.

1. Mode: Switch between "Loto 6" (pick 6 from 43) and "Loto 7" (pick 7 from 37) in the settings.

2. Chaos & Technical Logic:

- Chaos Dynamics: Non-linear calculations inspired by the Lorentz Attractor.

- Technical Analysis: Weighing factors based on RSI and Bollinger Band positioning.

- Conceptual Constants: Incorporates the Golden Ratio (φ) and other mathematical constants.

3. Freeze/Lock Function: Numbers fluctuate with every tick. Use the "Stop" checkbox to lock the numbers at the exact moment you feel the market energy align.

4. Reroll System: If you lock the numbers but don't like the result, change the "Reroll" value to access a parallel timeline (alternate calculation result) for the same candle.

5. Disco Visuals: Background colors dance rhythmically while spinning and settle down when locked.

1. Add to chart (highly volatile assets like BTC or FX recommended).

2. Select Loto 6 or Loto 7 in the settings.

3. Watch the chart and feel the "wave" of the market.

4. Check the "Stop (Lock Numbers)" box in settings when your intuition strikes.

5. Note down the numbers. (Use the "Reroll" input if you want to reshape your destiny).

This tool is for entertainment purposes only. It does not guarantee any lottery winnings. Please play responsibly.

Acrobatic Loto Predictor [Taolue Remix]市場のカオスを、幸運の数字へ。

このインジケーターは、現在のチャートの「価格変動」「時間」「ボラティリティ」を複雑な計算式(カオス力学)に通すことで、 Loto 6 (6/43) および Loto 7 (7/37) の予想数字を算出する実験的なツールです。

単なるランダム生成(乱数)ではありません。RSIやボリンジャーバンドといったテクニカル指標の数値を「乱数の種(シード)」として使用しているため、 「相場の息遣い」がそのまま数字として出力されます。

【主な機能】

1. モード: 設定画面から「Loto 6」と「Loto 7」を切り替え可能です。

2. カオス&テクニカル・ロジック:

- カオス力学: ローレンツ・アトラクタに着想を得た非線形計算。

- テクニカル: RSI(相対力指数)とボリンジャーバンドの位置関係を係数化。

- 概念定数: 黄金比(φ)や特定の数学的定数を隠し味に配合。

3. ストップ(固定)機能: チャートが動くたびに数字は変動しますが、「ここだ!」と思った瞬間にチェックボックスで数字を 完全固定(ロック) できます。

4. リロール(再抽選)機能: 固定した数字が気に入らない場合、リロール値を変更することで、その瞬間のパラレルワールド(別の計算結果)を呼び出せます。

5. ディスコモード: 数字が変動している間は背景色がリズミカルに変化し、固定すると色が落ち着く視覚効果付き。

【使い方】

1. チャートに追加します(ビットコインや為替など、動きのある銘柄推奨)。

2. 設定画面で Loto 6 か Loto 7 を選びます。

3. チャートを眺め、相場の「波」を感じます。

4. 直感的に良いタイミングで設定画面の 「ストップ(数値を固定)」 にチェックを入れます。

5. 表示された数字をメモします。(気に入らなければ「結果のリロール」数値を変更してください)

※免責事項:

このツールはエンターテインメント目的で作成されています。当選を保証するものではありません。宝くじの購入は自己責任で楽しみましょう。

---

Transform Market Chaos into Lucky Numbers.

This indicator is an experimental tool that generates predictions for Loto 6 and Loto 7 by feeding current chart data—price action, time, and volatility—into complex chaotic algorithms.

This is not a simple random number generator. It uses technical indicators like RSI and Bollinger Bands as "seeds" for generation. Essentially, the heartbeat of the market decides your numbers.

1. Mode: Switch between "Loto 6" (pick 6 from 43) and "Loto 7" (pick 7 from 37) in the settings.

2. Chaos & Technical Logic:

- Chaos Dynamics: Non-linear calculations inspired by the Lorentz Attractor.

- Technical Analysis: Weighing factors based on RSI and Bollinger Band positioning.

- Conceptual Constants: Incorporates the Golden Ratio (φ) and other mathematical constants.

3. Freeze/Lock Function: Numbers fluctuate with every tick. Use the "Stop" checkbox to lock the numbers at the exact moment you feel the market energy align.

4. Reroll System: If you lock the numbers but don't like the result, change the "Reroll" value to access a parallel timeline (alternate calculation result) for the same candle.

5. Disco Visuals: Background colors dance rhythmically while spinning and settle down when locked.

1. Add to chart (highly volatile assets like BTC or FX recommended).

2. Select Loto 6 or Loto 7 in the settings.

3. Watch the chart and feel the "wave" of the market.

4. Check the "Stop (Lock Numbers)" box in settings when your intuition strikes.

5. Note down the numbers. (Use the "Reroll" input if you want to reshape your destiny).

This tool is for entertainment purposes only. It does not guarantee any lottery winnings. Please play responsibly.

Mine Shaft + Drift + Ore Pocket Detector (Gap+Touch)Mine Shaft + Drift + Ore Pocket Detector (Gap+Touch) — Full Description (v1.6.1, Pine v6)

*Experimental - *Test Phase*

1) What this indicator is intended to do

This indicator attempts to algorithmically discover “mine shaft” price structure on a chart by:

Collecting structural anchor points (gaps and optionally pivots),

Generating candidate trend “rails” (centerline + parallel upper/lower borders) from pairs of anchors,

Fitting an optimal channel width around each candidate centerline,

Scoring candidates based on how well price action conforms to the channel (touches + containment),

Selecting and rendering:

the main shaft channel (primary),

additional drifts (secondary shafts per direction),

And then detecting Ore Pockets: time locations where multiple selected lines intersect (time confluence / intersection clustering).

The conceptual model is:

A shaft = a best-fit channel that price respects over time (the “main tunnel”).

Drifts = alternate channels close in quality to the main shaft (secondary tunnels).

Ore pockets = future/past time coordinates where multiple channels’ centerlines intersect densely (confluence in time, not necessarily in price).

2) What it is doing right now (current behavior)

In its current form, the script does a bounded, performance-limited scan:

It stores a limited number of anchor points in arrays.

It only considers a bounded number of recent anchors per direction.

It constructs candidate lines from anchor pairs and evaluates channel fitness using sampled bars.

On the last bar, it selects top candidates per direction and draws:

a “main” channel per mode (single best overall, or separate up/down),

plus optional drift channels,

plus ore pocket markers.

It is producing meaningful channels and drifts, but it is currently more likely to lock onto a strong “local” shaft than the one macro shaft spanning the entire market structure.

3) Core mechanics (how the script finds shafts)

3.1 Anchor generation (what points it uses)

Anchors are the “support points” used to build candidate shaft centerlines.

Two anchor families are supported:

A) Gap anchors (from your selected gap mode)

These attempt to capture “displacement events” and their boundaries/mids.

B) Pivot anchors (optional structural anchors)

These use pivots to inject macro structure points that are not strictly gap-based.

All anchors are stored as:

anchorX: bar_index of anchor

anchorY: price of anchor

anchorD: direction flag (+1 for up, -1 for down)

Anchors are capped by maxAnchors with FIFO trimming.

3.2 Candidate generation (how it produces centerlines)

For each direction (+1 and -1):

Collect “recent” anchors of that direction within lookbackBars (bounded to maxDirAnchors).

For each pair of anchors (x1,y1) and (x2,y2) that satisfy:

spacing within ,

slope sign consistent with direction,

Construct the line equation:

slope m and intercept b

Fit a channel width w around that line (via width mode).

Score it (touches + inside count minus width penalty).

Keep the top K rails (K = driftCount+1 typically).

3.3 Scoring model (what “best” means right now)

For a candidate centerline:

At sampled bars (stride sampling), compute:

channel top = y(x) + w

channel bot = y(x) - w

Evaluate:

Inside: candle range fits within the channel ± tolerance

Touches: high near top border, low near bottom border (within tolerance)

Score formula:

score = insideCount * insideWeight

+ touchCount * touchWeight

- (w / ATR) * widthPenalty

So:

Higher inside and touch counts increase score

Wider channels are penalized (in ATR units) to avoid “cheating” via enormous width

3.4 Width fitting (how the channel thickness is chosen)

Width is either:

Fit (scan widths): scans widths between a min width and a max deviation cap and selects the best scoring width.

Fixed ATR Envelope: uses a fixed width derived from ATR (currently hard-coded to a 2.0 ATR envelope in your present draft).

Fixed Max Deviation: width is max observed deviation from line in sampled window.

This matters because “macro shaft” detection is strongly influenced by whether the width-fitting is allowed to expand enough to contain large historical moves, without being penalized into losing to a smaller local shaft.

3.5 Rendering (what gets drawn)

For any selected rail, it draws:

Upper border line (top rail)

Lower border line (bottom rail)

Optional centerline (main only)

Optional fill between borders (main only)

Label at current bar with touches and inside count

Drifts render similarly but without main-only features (depending on flags).

3.6 Ore Pocket detection (time confluence)

Ore pockets are not “price zones” directly.

They are computed as follows:

Collect selected centerlines (m,b) for:

the main selected shaft(s),

and all drift centerlines (both directions if present)

For each pair of selected lines, compute intersection x-coordinate:

x* = (b2 - b1) / (m1 - m2)

Only keep intersections within:

Cluster intersections by time proximity (clusterBars)

Mark the strongest clusters (highest counts) as “Ore Pocket” vertical dotted lines with labels.

Interpretation:

A dense cluster indicates many selected rails converge around a similar time coordinate.

It is a “time confluence” hypothesis point.

4) Full settings reference (what each setting is for)

01) Gap Anchors

Gap Mode

FVG (3-candle)

Uses a classic 3-candle fair value gap pattern:

Up gap if low > high

Down gap if high < low

Anchors are derived from the gap boundaries.

Candle Gap (open-close)

Gap based on open vs close of the same bar with a tick threshold.

Candle Gap (open-prev close)

Gap based on open vs close with a tick threshold.

Gap Threshold (ticks)

Only used for the candle gap modes.

Controls the minimum gap size required to register an anchor.

Anchor Price

Boundary: anchors at one gap boundary (more “structural edge”)

Mid: anchors at midpoint of the gap (more “center of displacement”)

Include Pivot Anchors (structure)

When enabled, adds pivots as additional anchors to stabilize macro detection.

Pivot Length

Pivot sensitivity (how many bars left/right define a pivot).

Larger values = fewer, more structural pivots.

02) Channel Fit + Touch Scoring

Lookback Bars

The historical window used to:

filter which anchors are considered “recent enough”

evaluate channel fitness (sampled evaluation)

Larger lookback tends to favor macro shafts, but also increases computational risk (mitigated by evalBars and stride).

ATR Length

ATR period used for tolerance and width penalty scaling.

Tolerance (ATR mult)

Defines how close price must be to a rail to count as “touch” and how strict the “inside channel” containment is.

Higher tolerance = easier to score high on touch/inside.

Min Border Touches (keep rail)

Minimum number of border touches required before a candidate is even eligible.

Score: Inside Weight

Weight of inside count in score.

Score: Border Touch Weight

Weight of border touches in score.

This is a strong driver of “shaft-like” behavior.

Score: Width Penalty (in ATRs)

Penalizes wide channels relative to ATR.

Higher penalty biases toward narrow/local shafts.

03) Performance Controls

Max Stored Anchors (global)

Maximum anchor points kept in memory arrays.

Too low can cause loss of macro structure; too high increases candidate noise.

Max Anchors / Direction (scan)

Hard cap on how many anchors are used in candidate generation per direction.

Critical: this strongly influences whether macro shaft can be found, because if you only keep the most recent anchors, you lose the early-structure anchor points.

Eval Bars (max)

Maximum historical bars actually evaluated for scoring.

Even if lookbackBars is large, evaluation is capped here.

Eval Stride (sample every N bars)

Sampling step for evaluation.

Larger stride = faster but less accurate scoring.

04) Candidate Generation

Min Anchor Spacing (bars)

Minimum distance between the two anchors used to define a candidate line.

Prevents micro-noise lines from being evaluated.

Max Anchor Spacing (bars)

Maximum distance between the two anchors used to define a candidate line.

If this is too low, you cannot generate truly macro candidate lines.

05) Shaft + Drift Display

Main Shaft Mode

Best Overall (Single Shaft): chooses one best rail among Up/Down and draws it as main.

Up Only: show only the best upward rail.

Down Only: show only the best downward rail.

Up + Down: show both main up rail and main down rail simultaneously.

Show Ascending Shaft

Toggles rendering for the “up” main shaft (when mode allows it).

Show Descending Shaft

Toggles rendering for the “down” main shaft (when mode allows it).

Drifts per Direction

Number of additional top-ranked rails to draw per direction (after the best one).

Extend Lines

Right: extend lines to the right only.

Both: extend both left and right.

Fill Main Shaft Channel

Fill between upper and lower borders for main shaft.

Main Shaft Fill Transparency

Transparency level for main fill.

Show Main Shaft Centerline

Draw the dashed centerline for the main shaft.

06) Ore Pocket (Intersection-Time Confluence)

Show Ore Pockets (Time Confluence)

Enables ore pocket discovery and rendering.

Intersection Window Forward (bars)

How far into the future intersections are considered.

Intersection Window Backward (bars)

How far into the past intersections are considered.

Cluster Radius (bars)

How close in time intersections must be to merge into a cluster.

Min Intersections per Cluster

Minimum cluster count required before a pocket is shown.

Max Pocket Markers

Limit how many pocket clusters are drawn.

07) Visual Controls

Show Gap Anchors

Displays the gap anchor dots for debugging.

Show Pivot Anchors

Displays pivot anchor dots for debugging.

5) How to use it (practical workflow)

Step A — Confirm anchor behavior

Turn on Show Gap Anchors.

Choose your Gap Mode.

Verify you are seeing anchors where you expect (displacement boundaries).

If anchors are sparse:

Reduce gap threshold (ticks) for candle-gap modes

Enable pivots to inject structure

Increase lookbackBars and maxAnchors so early anchors are not dropped

Step B — Get stable main shaft candidate discovery

Enable Include Pivot Anchors with a medium pivotLen.

Use Fit (scan widths) initially.

Increase Max Anchors / Direction (scan) so you’re not only using recent anchors.

Increase Max Anchor Spacing so macro pairs are eligible.

If you keep getting only local shafts:

That is usually because the candidate pool does not include enough old anchors, or the maxSpacing prevents long-span lines.

Step C — Tune scoring so the “whole-structure” shaft wins

If the script picks a small local channel instead of the macro channel:

Increase insideWeight relative to touchWeight (macro channels tend to contain longer structure even with fewer perfect “touches”)

Reduce widthPenalty, because macro channels may need to be wider to accommodate historical volatility

Increase lookbackBars and evalBars to make “whole-structure fit” matter

Step D — Drifts as secondary shafts

Once main shaft is good:

Increase Drifts per Direction

Validate that drifts represent meaningful alternate sub-shafts rather than noisy duplicates.

If drifts look too similar:

This is expected if many candidates differ only slightly; future refinements should diversify drift selection (see “what still needs done”).

Step E — Ore pockets interpretation

Ore pockets indicate time confluence of multiple rails.

Use them as:

“Time windows to watch”

Not as deterministic price levels

Tune:

clusterBars (cluster tightness)

minClusterSize (signal strength)

6) What still needs done (explicit backlog)

The macro “main mining shaft channel” spanning the entire market structure, and

Smaller shafts/drifts nested inside the macro structure.

To accomplish that, the current algorithm needs additional architecture. Concretely: