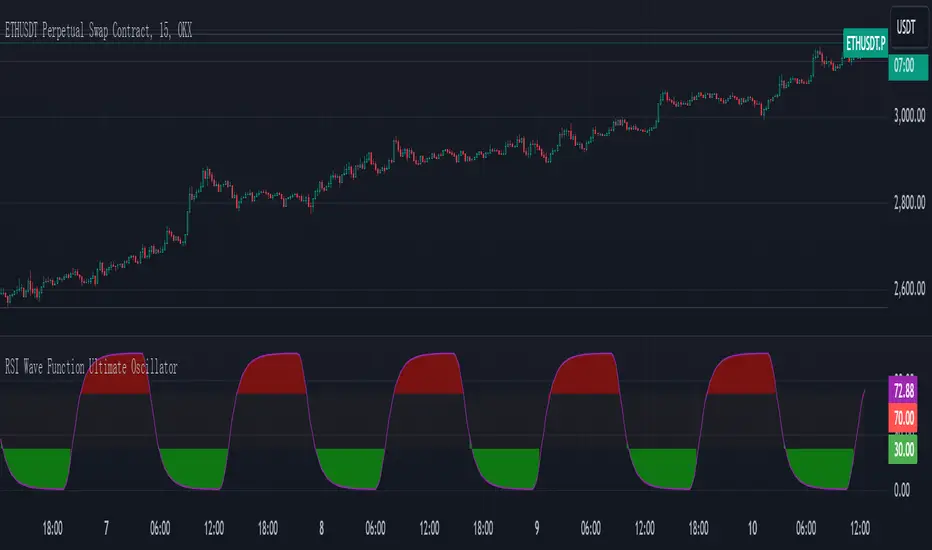

RSI Wave Function Ultimate OscillatorEnglish Explanation of the "RSI Wave Function Ultimate Oscillator" Pine Script Code

Understanding the Code

Purpose:

This Pine Script code creates a custom indicator that combines the Relative Strength Index (RSI) with a wave function to potentially provide more nuanced insights into market dynamics.

Key Components:

* Wave Function: This is a custom calculation that introduces a sinusoidal wave component to the price data. The frequency parameter controls the speed of the oscillation, and the decay factor determines how quickly the influence of past prices diminishes.

* Smoothed Signal: The wave function is applied to the closing price to create a smoothed signal, which is essentially a price series modulated by a sine wave.

* RSI: The traditional RSI is then calculated on this smoothed signal, providing a measure of the speed and change of price movements relative to recent price changes.

Calculation Steps:

* Wave Function Calculation:

* A sinusoidal wave is generated based on the bar index and the frequency parameter.

* The wave is combined with the closing price using a weighted average, where the decay factor determines the weight given to previous values.

* RSI Calculation:

* The RSI is calculated on the smoothed signal using a standard RSI formula.

* Plotting:

* The RSI values are plotted on a chart, along with horizontal lines at 70 and 30 to indicate overbought and oversold conditions.

* The area between the RSI line and the overbought/oversold lines is filled with color to visually represent the market condition.

Interpretation and Usage

* Wave Function: The wave function introduces cyclical patterns into the price data, which can help identify potential turning points or momentum shifts.

* RSI: The RSI provides a measure of the speed and change of price movements relative to recent price changes. When applied to the smoothed signal, it can help identify overbought and oversold conditions, as well as potential divergences between price and momentum.

* Combined Indicator: The combination of the wave function and RSI aims to provide a more sensitive and potentially earlier indication of market reversals.

* Signals:

* Crossovers: Crossovers of the RSI line above or below the overbought/oversold lines can be used to generate buy or sell signals.

* Divergences: Divergences between the price and the RSI can indicate a weakening trend.

* Oscillations: The amplitude and frequency of the oscillations in the RSI can provide insights into the strength and duration of market trends.

How it Reflects Market Volatility

* Amplified Volatility: The wave function can amplify the volatility of the price data, making it easier to identify potential turning points.

* Smoothing: The decay factor helps to smooth out short-term fluctuations, allowing the indicator to focus on longer-term trends.

* Sensitivity: The combination of the wave function and RSI can make the indicator more sensitive to changes in market momentum.

In essence, this custom indicator attempts to enhance traditional RSI analysis by incorporating a cyclical component that can potentially provide earlier signals of market reversals.

Note: The effectiveness of this indicator will depend on various factors, including the specific market, time frame, and the chosen values for the frequency and decay parameters. It is recommended to conduct thorough backtesting and optimize the parameters to suit your specific trading strategy.

Search in scripts for "change"

CMF and Scaled EFI OverlayCMF and Scaled EFI Overlay Indicator

Overview

The CMF and Scaled EFI Overlay indicator combines the Chaikin Money Flow (CMF) and a scaled version of the Elder Force Index (EFI) into a single chart. This allows traders to analyze both indicators simultaneously, facilitating better insights into market momentum and volume dynamics , specifically focusing on buying/selling pressure and momentum , without compromising the integrity of either indicator.

Purpose

Chaikin Money Flow (CMF): Measures buying and selling pressure by evaluating price and volume over a specified period. It indicates accumulation (buying pressure) when values are positive and distribution (selling pressure) when values are negative.

Elder Force Index (EFI): Combines price changes and volume to assess the momentum behind market moves. Positive values indicate upward momentum (prices rising with strong volume), while negative values indicate downward momentum (prices falling with strong volume).

By scaling the EFI to match the amplitude of the CMF, this indicator enables a direct comparison between pressure and momentum , preserving their shapes and zero crossings. Traders can observe the relationship between price movements, volume, and momentum more effectively, aiding in decision-making.

Understanding Pressure vs. Momentum

Chaikin Money Flow (CMF):

- Indicates the level of demand (buying pressure) or supply (selling pressure) in the market based on volume and price movements.

- Accumulation: When institutional or large investors are buying significant amounts of an asset, leading to an increase in buying pressure.

- Distribution: When these investors are selling off their holdings, increasing selling pressure.

Elder Force Index (EFI):

- Measures the strength and speed of price movements, indicating how forceful the current trend is.

- Positive Momentum: Prices are rising quickly, indicating a strong uptrend.

- Negative Momentum: Prices are falling rapidly, indicating a strong downtrend.

Understanding the difference between pressure and momentum is crucial. For example, a market may exhibit strong buying pressure (positive CMF) but weak momentum (low EFI), suggesting accumulation without significant price movement yet.

Features

Overlay of CMF and Scaled EFI: Both indicators are plotted on the same chart for easy comparison of pressure and momentum dynamics.

Customizable Parameters: Adjust lengths for CMF and EFI calculations and fine-tune the scaling factor for optimal alignment.

Preserved Indicator Integrity: The scaling method preserves the shape and zero crossings of the EFI, ensuring accurate analysis.

How It Works

CMF Calculation:

- Calculates the Money Flow Multiplier (MFM) and Money Flow Volume (MFV) to assess buying and selling pressure.

- CMF is computed by summing the MFV over the specified length and dividing by the sum of volume over the same period:

CMF = (Sum of MFV over n periods) / (Sum of Volume over n periods)

EFI Calculation:

- Calculates the EFI using the Exponential Moving Average (EMA) of the price change multiplied by volume:

EFI = EMA(n, Change in Close * Volume)

Scaling the EFI:

- The EFI is scaled by multiplying it with a user-defined scaling factor to match the CMF's amplitude.

Plotting:

- Both the CMF and the scaled EFI are plotted on the same chart.

- A zero line is included for reference, aiding in identifying crossovers and divergences.

Indicator Settings

Inputs

CMF Length (`cmf_length`):

- Default: 20

- Description: The number of periods over which the CMF is calculated. A higher value smooths the indicator but may delay signals.

EFI Length (`efi_length`):

- Default: 13

- Description: The EMA length for the EFI calculation. Adjusting this value affects the sensitivity of the EFI to price changes.

EFI Scaling Factor (`efi_scaling_factor`):

- Default: 0.000001

- Description: A constant used to scale the EFI to match the CMF's amplitude. Fine-tuning this value ensures the indicators align visually.

How to Adjust the EFI Scaling Factor

Start with the Default Value:

- Begin with the default scaling factor of `0.000001`.

Visual Inspection:

- Observe the plotted indicators. If the EFI appears too large or small compared to the CMF, proceed to adjust the scaling factor.

Fine-Tune the Scaling Factor:

- Increase or decrease the scaling factor incrementally (e.g., `0.000005`, `0.00001`, `0.00005`) until the amplitudes of the CMF and EFI visually align.

- The optimal scaling factor may vary depending on the asset and timeframe.

Verify Alignment:

- Ensure that the scaled EFI preserves the shape and zero crossings of the original EFI.

- Overlay the original EFI (if desired) to confirm alignment.

How to Use the Indicator

Analyze Buying/Selling Pressure and Momentum:

- Positive CMF (>0): Indicates accumulation (buying pressure).

- Negative CMF (<0): Indicates distribution (selling pressure).

- Positive EFI: Indicates positive momentum (prices rising with strong volume).

- Negative EFI: Indicates negative momentum (prices falling with strong volume).

Look for Indicator Alignment:

- Both CMF and EFI Positive:

- Suggests strong bullish conditions with both buying pressure and upward momentum.

- Both CMF and EFI Negative:

- Indicates strong bearish conditions with selling pressure and downward momentum.

Identify Divergences:

- CMF Positive, EFI Negative:

- Buying pressure exists, but momentum is negative; potential for a bullish reversal if momentum shifts.

- CMF Negative, EFI Positive:

- Selling pressure exists despite rising prices; caution advised as it may indicate a potential bearish reversal.

Confirm Signals with Other Analysis:

- Use this indicator in conjunction with other technical analysis tools (e.g., trend lines, support/resistance levels) to confirm trading decisions.

Example Usage

Scenario 1: Bullish Alignment

- CMF Positive: Indicates accumulation (buying pressure).

- EFI Positive and Increasing: Shows strengthening upward momentum.

- Interpretation:

- Strong bullish signal suggesting that buyers are active, and the price is likely to continue rising.

- Action:

- Consider entering a long position or adding to existing ones.

Scenario 2: Bearish Divergence

- CMF Negative: Indicates distribution (selling pressure).

- EFI Positive but Decreasing: Momentum is positive but weakening.

- Interpretation:

- Potential bearish reversal; price may be rising but underlying selling pressure suggests caution.

- Action:

- Be cautious with long positions; consider tightening stop-losses or preparing for a possible trend reversal.

Tips

Adjust for Different Assets:

- The optimal scaling factor may differ across assets due to varying price and volume characteristics.

- Always adjust the scaling factor when analyzing a new asset.

Monitor Indicator Crossovers:

- Crossings above or below the zero line can signal potential trend changes.

Watch for Divergences:

- Divergences between the CMF and EFI can provide early warning signs of trend reversals.

Combine with Other Indicators:

- Enhance your analysis by combining this overlay with other indicators like moving averages, RSI, or Ichimoku Cloud.

Limitations

Scaling Factor Sensitivity:

- An incorrect scaling factor may misalign the indicators, leading to inaccurate interpretations.

- Regular adjustments may be necessary when switching between different assets or timeframes.

Not a Standalone Indicator:

- Should be used as part of a comprehensive trading strategy.

- Always consider other market factors and indicators before making trading decisions.

Disclaimer

No Guarantee of Performance:

- Past performance is not indicative of future results.

- Trading involves risk, and losses can exceed deposits.

Use at Your Own Risk:

- This indicator is provided for educational purposes.

- The author is not responsible for any financial losses incurred while using this indicator.

Code Summary

//@version=5

indicator(title="CMF and Scaled EFI Overlay", shorttitle="CMF & Scaled EFI", overlay=false)

cmf_length = input.int(20, minval=1, title="CMF Length")

efi_length = input.int(13, minval=1, title="EFI Length")

efi_scaling_factor = input.float(0.000001, title="EFI Scaling Factor", minval=0.0, step=0.000001)

// --- CMF Calculation ---

ad = high != low ? ((2 * close - low - high) / (high - low)) * volume : 0

mf = math.sum(ad, cmf_length) / math.sum(volume, cmf_length)

// --- EFI Calculation ---

efi_raw = ta.ema(ta.change(close) * volume, efi_length)

// --- Scale EFI ---

efi_scaled = efi_raw * efi_scaling_factor

// --- Plotting ---

plot(mf, color=color.green, title="CMF", linewidth=2)

plot(efi_scaled, color=color.red, title="EFI (Scaled)", linewidth=2)

hline(0, color=color.gray, title="Zero Line", linestyle=hline.style_dashed)

- Lines 4-6: Define input parameters for CMF length, EFI length, and EFI scaling factor.

- Lines 9-11: Calculate the CMF.

- Lines 14-16: Calculate the EFI.

- Line 19: Scale the EFI by the scaling factor.

- Lines 22-24: Plot the CMF, scaled EFI, and zero line.

Feedback and Support

Suggestions: If you have ideas for improvements or additional features, please share your feedback.

Support: For assistance or questions regarding this indicator, feel free to contact the author through TradingView.

---

By combining the CMF and scaled EFI into a single overlay, this indicator provides a powerful tool for traders to analyze market dynamics more comprehensively. Adjust the parameters to suit your trading style, and always practice sound risk management.

Pulse Oscillator [UAlgo]The "Pulse Oscillator " is a trading tool designed to capture market momentum and trend changes by combining the strengths of multiple well-known technical indicators. By integrating the RSI (Relative Strength Index), CCI (Commodity Channel Index), and Stochastic Oscillator, this indicator provides traders with a comprehensive view of market conditions, offering both trend filtering and precise buy/sell signals. The oscillator is customizable, allowing users to fine-tune its parameters to match different trading strategies and timeframes. With its built-in smoothing techniques and level adjustments, the Pulse Oscillator aims to be a reliable tool for both trend-following and counter-trend trading strategies.

🔶 Key Features

Multi-Indicator Integration: Combines RSI, CCI, and Stochastic Oscillator to create a weighted momentum oscillator.

Why Use Multi-Indicator Integration?

Script uses Multi-Indicator Integration to combine the strengths of different technical indicators—such as RSI, CCI, and Stochastic Oscillator—into a single tool. This approach helps to reduce the weaknesses of individual indicators, providing a more comprehensive and reliable analysis of market conditions. By integrating multiple indicators, we can generate more accurate signals, filter out noise, and enhance our trading decisions.

Customizable Parameters: Allows users to adjust weights, periods, and smoothing techniques, providing flexibility to adapt the indicator to various market conditions.

Trend Filtering Option: An optional trend filter is available to enhance the accuracy of buy and sell signals, reducing the risk of false signals in choppy markets.

Dynamic Levels: The indicator dynamically calculates multiple levels of support and resistance, adjusting to market conditions with customizable decay factors and offsets.

Visual Clarity: The indicator visually represents different levels and trends with color-coded plots and fills, making it easier for traders to interpret market conditions at a glance.

Alerts: Configurable alerts for buy and sell signals, as well as trend changes, enabling traders to stay informed of key market movements without constant monitoring.

🔶 Interpreting the Indicator

Buy Signal: A buy signal is generated when the Slow Line crosses under the Fast Line during an uptrend or when the trend filter is disabled. This indicates a potential bullish reversal or continuation of an upward trend.

Sell Signal: A sell signal occurs when the Slow Line crosses above the Fast Line during a downtrend or when the trend filter is disabled, signaling a potential bearish reversal or continuation of a downward trend.

Trend Change: The indicator detects trend changes when the Fast Line shifts from increasing to decreasing or vice versa, providing early warning of possible market reversals.

Dynamic Levels: The indicator calculates upper and lower levels based on the Fast Line's values. These levels can be used to identify overbought or oversold conditions and potential areas of support or resistance.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Saral Relative StrengthRelative Strength Indicator

### Overview

The Relative Strength (RS) Indicator is a robust tool designed to measure the performance of a security relative to a benchmark or another security. Unlike traditional indicators, this RS Indicator calculates the outperformance or underperformance in percentage terms, providing a clear and concise comparison.

The equation for calculation can be found in the code itself. This equation compares how much a security's price has changed over a given period (len) relative to the change in price of a benchmark over the same period. The result is expressed as a percentage, showing whether the security has outperformed or underperformed the benchmark. A positive RS value indicates outperformance, while a negative value signals underperformance.

Basically, this indicator is an enhanced version of 'Relative Strength' indicator of 'BharatTrader' Sir with added features like automatic divergence plotting, color-coded filled area and sector names for NSE F&O securities. Default values for some of the parameters are based on discussion by Subhadip Nandy Sir in Trader's Talk with Mr. Rohit Katwal.

### Input Parameters:

Source: The price of a security used in the calculation, with the default being the 'close' price.

Comparative Symbol: Ticker ID of the comparative security, with the default set to NIFTY 50.

Period-RS: The period for calculating the RS line, with a default of 22. The RS line measures the relative performance of the security against the benchmark, helping to identify outperformance or underperformance over time.

Period-MA: The period for calculating the Simple Moving Average (SMA) overlay on the RS line, with a default of 11. The SMA provides a smoothed view of the RS line, helping to identify trends more clearly.

Lookback - Zero Line Trend: Zero Line Trend look-back period, used to determine the angle of the RS line, with a default of 5. This parameter influences the color of the Zero Line based on whether the RS line’s angle is positive or negative.

Lookback - Divergence: Divergence look-back period, with a default of 2, used to detect divergence between the price and the RS line.

Display MA Line: Controls the display of the SMA line. When enabled, the SMA line is plotted over the RS line to indicate trend strength.

Toggle RS Color on MA Crossovers: Controls the color of the RS line. If disabled, the RS line is purple. If enabled, the RS line changes color based on its position relative to the SMA: green for RS > MA, red for RS < MA.

Display Zero Line Trend: Controls the display of the Zero Line. If disabled, the Zero Line is black. If enabled, the Zero Line’s color changes to green or maroon based on the RS line’s angle over time.

Display Divergence: Controls the display of divergence dots on the RS line, indicating potential reversal points.

Display Filled Area: Controls whether the area between the Zero Line and the RS line is filled with color. The fill color changes based on the relationship of the RS line with the SMA & Zero Line as given below.

- Dark Green: RS > 0 and RS > MA, indicating strong outperformance.

- Light Green: RS > 0 and RS < MA, indicating weakening outperformance.

- Dark Red: RS < 0 and RS < MA, indicating strong underperformance.

- Light Red: RS < 0 and RS > MA, indicating weakening underperformance.

Display Sector Name: Controls the display of sector names for NSE F&O securities, helping to plot RS with sectoral indices.

### Key Features:

RS Line:

The RS line represents the relative performance of a security against a benchmark over a specified period (default 22). It helps traders identify whether the security is outperforming or underperforming the benchmark.

SMA Overlay:

A Simple Moving Average (SMA) line is plotted over the RS line, with a default period of 11. The SMA provides a smoothed trend of the RS, making it easier to identify consistent performance trends.

Trend-Sensitive Zero Line:

The Zero Line’s color adapts based on the RS line’s trend:

- Green: Positive angle of the RS line, indicating upward momentum.

- Maroon: Negative angle, indicating downward momentum.

The color can be toggled, with an option to display the Zero Line in black.

Divergence Detection:

Automatically detects and highlights divergences.

- Positive Divergence: RS line rises while the price falls, marked by blue dots.

- Negative Divergence: RS line falls while the price rises, marked by black dots.

Color-Coded Fill Area:

The area between the RS line and the Zero Line is filled with color to visually distinguish different market conditions, with Dark and Light colors providing insight into the strength of the performance:

- Dark Green: Indicates strong outperformance (RS > 0 and RS > MA), suggesting the security is showing significant strength compared to the benchmark.

- Light Green: Indicates weakening outperformance (RS > 0 and RS < MA), signaling that while the security is still outperforming, its strength is diminishing.

- Dark Red: Indicates strong underperformance (RS < 0 and RS < MA), showing the security is significantly weaker than the benchmark.

- Light Red: Indicates weakening underperformance (RS < 0 and RS > MA), suggesting the security is still underperforming but may be regaining some strength.

Sectoral Strength:

Displays sector names for NSE F&O securities, helping users to compare the RS of individual securities with their respective sectoral indices. Comparative Security can be changed easily based on this sector name. Users need not to remember sector names for individual securities.

If any security is not categorized in a specific sector, CNX500 has been considered as a default sector for NSE F&O securities. For other securities, NIFTY50 has been considered as a default sector.

S&P 2024: Magnificent 7 vs. the rest of S&PThis chart is designed to calculate and display the percentage change of the Magnificent 7 (M7) stocks and the S&P 500 excluding the M7 (Ex-M7) from the beginning of 2024 to the most recent data point. The Magnificent 7 consists of seven major technology stocks: Apple (AAPL), Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta (META), Nvidia (NVDA), and Tesla (TSLA). These stocks are a significant part of the S&P 500 and can have a substantial impact on its overall performance.

Key Components and Functionality:

1. Start of 2024 Baseline:

- The script identifies the closing prices of the S&P 500 and each of the Magnificent 7 stocks on the first trading day of 2024. These values serve as the baseline for calculating percentage changes.

2. Current Value Calculation:

- It then fetches the most recent closing prices of these stocks and the S&P 500 index to calculate their current values.

3. Percentage Change Calculation:

- The script calculates the percentage change for the M7 by comparing the sum of the current prices of the M7 stocks to their combined value at the start of 2024.

- Similarly, it calculates the percentage change for the Ex-M7 by comparing the current value of the S&P 500 excluding the M7 to its value at the start of 2024.

4. Plotting:

- The calculated percentage changes are plotted on the chart, with the M7’s percentage change shown in red and the Ex-M7’s percentage change shown in blue.

Use Case:

This indicator is particularly useful for investors and analysts who want to understand how much the performance of the S&P 500 in 2024 is driven by the Magnificent 7 stocks compared to the rest of the index. By showing the percentage change from the start of the year, it provides clear insights into the relative growth or decline of these two segments of the market over the course of the year.

Visualization:

- Red Line (M7 % Change): Displays the percentage change of the combined value of the Magnificent 7 stocks since the start of 2024.

- Blue Line (Ex-M7 % Change): Displays the percentage change of the S&P 500 excluding the Magnificent 7 since the start of 2024.

This script enables a straightforward comparison of the performance of the M7 and Ex-M7, highlighting which segment is contributing more to the overall movement of the S&P 500 in 2024.

Follow the Volumes / Path of Least ResistanceThis indicator tracks price movements following significant volume increases. It identifies volume spikes by comparing recent average volume to a longer-term average. After a spike, it monitors price changes over a specified number of bars.

In plain English, the point of this is to “let the market show it’s hand”, vs. other common and preemptive methods of execution.

You can think of it as a better version of a volume up/down indicator which only uses opening and closing prices to identify "bullish" or "bearish" behavior.

To optimize this, I used a very small range chart, hence the small values. You will need to experiment with other values, ESPECIALLY the % change. If you do not do this, the indicator will generate a lot of noise.

The indicator has three main conditions:

1. Significant price increase, bullish: A green triangle appears below the bar.

2. Significant price decrease, bearish: A red triangle appears above the bar.

3. Price change within thresholds: A fuschia triangle appears, pointing up or down based on the overall (short-term) trend. This is common behavior during trends. A spike in volume will appear, and price simply does not budge. Volume/price is essentially declaring a new found value, in which case prices tend to follow the impulse movement (see market profile theory).

The color scheme is intuitive: green for positive moves, red for negative, and fuschia for subtle changes following the existing trend. Blue circles mark volume spikes for reference, which I recommend using only for reference, and disabling to remove unneeded noise.

Because this indicator "lags" in the sense of waiting for the market to show its hand, best opportunities are typically found on retests of the volume spikes themselves. On drives, however, the market will unlikely pullback, which (in my view) is one of its best use cases.

Bottom line, you will need to adjust the parameters to the instrument. This is not a plug and play solution, but far more accurate than those which are.

Settings, and what they mean:

Volume spike average bars: length for identification of high volumes. On smaller timeframes, such as my optimization period, you’ll want several bars. But on something such as a 5 minute or higher, only 1.

Lookback period: for identification of high volumes.

Volume Increase Threshold (%): % which constitutes a jump in volume

Bars After Spike: How long to wait for ensuing price movement. Also sensitive to the timeframe you are using. 1-2 recommended for 5m+, more for smaller range-based.

Negative Price Change Threshold (%): For red arrows (Volume + Price Movement)

Positive Price Change Threshold (%): Inverse of above

WMA Period for Stability Function: When price spikes on high volumes but does not move (price is “trapped” between negative and positive price change thresholds) the indicator marks direction (in fuchsia) in the direction of the underlying trend. This short-term MA identifies that trend.

Finally, because this indicator is volume-based, I recommend using primary instruments only and discourage its use on CFDs or other firm-generated instruments. Just use the primary. I would ignore signals off the open, which is subject to erroneous behavior. Other methods are far more effective for that.

This script is purposely uncomplicated. Feel free to play with settings and change code to suit your needs.

Sharpe and Sortino Ratios█ OVERVIEW

This indicator calculates the Sharpe and Sortino ratios using a chart symbol's periodic price returns, offering insights into the symbol's risk-adjusted performance. It features the option to calculate these ratios by comparing the periodic returns to a fixed annual rate of return or the returns from another selected symbol's context.

█ CONCEPTS

Returns, risk, and volatility

The return on an investment is the relative gain or loss over a period, often expressed as a percentage. Investment returns can originate from several sources, including capital gains, dividends, and interest income. Many investors seek the highest returns possible in the quest for profit. However, prudent investing and trading entails evaluating such returns against the associated risks (i.e., the uncertainty of returns and the potential for financial losses) for a clearer perspective on overall performance and sustainability.

The profitability of an investment typically comes at the cost of enduring market swings, noise, and general uncertainty. To navigate these turbulent waters, investors and portfolio managers often utilize volatility , a measure of the statistical dispersion of historical returns, as a foundational element in their risk assessments because it provides a tangible way to gauge the uncertainty in returns. High volatility suggests increased uncertainty and, consequently, higher risk, whereas low volatility suggests more stable returns with minimal fluctuations, implying lower risk. These concepts are integral components in several risk-adjusted performance metrics, including the Sharpe and Sortino ratios calculated by this indicator.

Risk-free rate

The risk-free rate represents the rate of return on a hypothetical investment carrying no risk of financial loss. This theoretical rate provides a benchmark for comparing the returns on a risky investment and evaluating whether its excess returns justify the risks. If an investment's returns are at or below the theoretical risk-free rate or the risk premium is below a desired amount, it may suggest that the returns do not compensate for the extra risk, which might be a call to reassess the investment.

Since the risk-free rate is a theoretical concept, investors often utilize proxies for the rate in practice, such as Treasury bills and other government bonds. Conventionally, analysts consider such instruments "risk-free" for a domestic holder, as they are a form of government obligation with a low perceived likelihood of default.

The average yield on short-term Treasury bills, influenced by economic conditions, monetary policies, and inflation expectations, has historically hovered around 2-3% over the long term. This range also aligns with central banks' inflation targets. As such, one may interpret a value within this range as a minimum proxy for the risk-free rate, as it may correspond to the minimum rate required to maintain purchasing power over time. This indicator uses a default value of 2% as the risk-free rate in its Sharpe and Sortino ratio calculations. Users can adjust this value from the "Risk-free rate of return" input in the "Settings/Inputs" tab.

Sharpe and Sortino ratios

The Sharpe and Sortino ratios are two of the most widely used metrics that offer insight into an investment's risk-adjusted performance . They provide a standardized framework to compare the effectiveness of investments relative to their perceived risks. These metrics can help investors determine whether the returns justify the risks taken to achieve them, promoting more informed investment decisions.

Both metrics measure risk-adjusted performance similarly. However, they have some differences in their formulas and their interpretation:

1. Sharpe ratio

The Sharpe ratio , developed by Nobel laureate William F. Sharpe, measures the performance of an investment compared to a theoretically risk-free asset, adjusted for the investment risk. The ratio uses the following formula:

Sharpe Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑎

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑎 = Standard deviation of the investment's returns (volatility)

A higher Sharpe ratio indicates a more favorable risk-adjusted return, as it signifies that the investment produced higher excess returns per unit of increase in total perceived risk.

2. Sortino ratio

The Sortino ratio is a modified form of the Sharpe ratio that only considers downside volatility , i.e., the volatility of returns below the theoretical risk-free benchmark. Although it shares close similarities with the Sharpe ratio, it can produce very different values, especially when the returns do not have a symmetrical distribution, since it does not penalize upside and downside volatility equally. The ratio uses the following formula:

Sortino Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑑

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑑 = Downside deviation (standard deviation of negative excess returns, or downside volatility)

The Sortino ratio offers an alternative perspective on an investment's return-generating efficiency since it does not consider upside volatility in its calculation. A higher Sortino ratio signifies that the investment produced higher excess returns per unit of increase in perceived downside risk.

The risk-free rate (𝑅𝑓) in the numerator of both ratio formulas acts as a baseline for comparing an investment's performance to a theoretical risk-free alternative. By subtracting the risk-free rate from the expected return (𝑅𝑎−𝑅𝑓), the numerator essentially represents the risk premium of the investment.

Comparison with another symbol

In addition to the conventional Sharpe and Sortino ratios, which compare an instrument's returns to a risk-free rate, this indicator can also compare returns to a user-specified benchmark symbol , allowing the calculation of Information ratios .

An Information ratio is a generalized form of the Sharpe ratio that compares an investment's returns to a risky benchmark , such as SPY, rather than a risk-free rate. It measures the investment's active return (the difference between its returns and the benchmark returns) relative to its tracking error (i.e., the volatility of the active return) using the following formula:

𝐼𝑅 = (𝑅𝑝 − 𝑅𝑏) / 𝑇𝐸

Where:

• 𝑅𝑝 = Average return on the portfolio or investment

• 𝑅𝑏 = Average return from the benchmark instrument

• 𝑇𝐸 = Tracking error (volatility of 𝑅𝑝 − 𝑅𝑏)

Comparing returns to a benchmark instrument rather than a theoretical risk-free rate offers unique insights into risk-adjusted performance. Higher Information ratios signify that the investment produced higher active returns per unit of increase in risk relative to the benchmark. Conventional choices for non-risk-free benchmarks include major composite indices like the S&P 500 and DJIA, as the resulting ratios can provide insight into the effectiveness of an investment relative to the broader market.

Users can enable this generalized calculation for both the Sharpe and Sortino ratios by selecting the "Benchmark symbol returns" option from the "Benchmark type" dropdown in the "Settings/Inputs" tab.

It's crucial to note that this indicator compares the charts symbol's rate of change (return) to the rate of change in the benchmark symbol. Consequently, not all symbols available on TradingView are suitable for use with these ratios due to the nature of what their values represent. For instance, using a bond as a benchmark will produce distorted results since each bar's values represent yields rather than prices, meaning it compares the rate of change in the yield. To maintain consistency and relevance in the calculated ratios, ensure the values from the compared symbols strictly represent price information.

█ FEATURES

This indicator provides traders with two widely used metrics for assessing risk-adjusted performance, generalized to allow users to compare the chart symbol's price returns to a fixed risk-free rate or the returns from another risky symbol. Below are the key features of this indicator:

Timeframe selection

The "Returns timeframe" input determines the timeframe of the calculated price returns. Users can select any value greater than or equal to the chart's timeframe. The default timeframe is "1M".

Periodic returns tracking

This indicator compounds and collects requested price returns from the selected timeframe over monthly or daily periods, similar to how the Broker Emulator works when calculating strategy performance metrics on trade data. It employs the following logic:

• Track returns over monthly periods if the chart's data spans at least two months.

• Track returns over daily periods if the chart's data spans at least two days but not two months.

• Do not track or collect returns if the data spans less than two days, as the amount of data is insufficient for meaningful ratio calculations.

The indicator uses the returns collected from up to a specified number of periods to calculate the Sharpe and Sortino ratios, depending on the available historical data. It also uses these periodic returns to calculate the average returns it displays in the Data Window.

Users can control the maximum number of periods the indicator analyzes with the "Max no. of periods used" input in the "Settings/Inputs" tab. The default value is 60 periods.

Benchmark specification

The "Benchmark return type" input specifies the benchmark type the indicator compares to the chart symbol's returns in the ratio calculations. It features the following two options:

• "Risk-free rate of return (%)": Compares the price returns to a user-specified annual rate of return representing a theoretical risk-free rate (e.g., 2%).

• "Benchmark symbol return": Compares the price returns to a selected benchmark symbol (e.g., "AMEX:SPY) to calculate Information ratios.

When comparing a chart symbol's returns to a specified benchmark symbol, this indicator aligns the times of data points from the benchmark with the times of data points from the chart's symbol to facilitate a fair comparison between symbols with different active sessions.

Visualization and display

• The indicator displays the periodic returns requested from the specified "Returns timeframe" in a separate pane. The plot includes dynamic colors to signify positive and negative returns.

• When the "Returns timeframe" value represents a higher timeframe, the indicator displays background highlights on the main chart pane to signify when a new value is available and whether the return is positive or negative.

• When the specified benchmark return type is a benchmark symbol, the indicator displays the requested symbol's returns in the separate pane as a gray line for visual comparison.

• Within the separate pane, the indicator displays a single-cell table that shows the base period it uses for periodic returns, the number of periods it uses in the calculation, the timeframe of the requested data, and the calculated Sharpe and Sortino ratios.

• The Data Window displays the chart symbol and benchmark returns, their periodic averages, and the Sharpe and Sortino ratios.

█ FOR Pine Script™ CODERS

• This script utilizes the functions from our RiskMetrics library to determine the size of the periods, calculate and collect periodic returns, and compute the Sharpe and Sortino ratios.

• The `getAlignedPrices()` function in this script requests price data for the chart's symbol and a benchmark symbol with consistent time alignment by utilizing spread symbols , which helps facilitate a fair comparison between different symbol types. Retrieving prices from spreads avoids potential information loss and data misalignment that can otherwise occur when using separate requests from each symbol's context when those symbols have different sessions or data times.

• For consistency, the `getAlignedPrices()` function includes extended hours and dividend adjustment modifiers in its data requests. Additionally, it includes other settings inherited from the chart's context, such as "settlement-as-close" preferences for fair comparison between futures instruments.

• This script uses the `changePercent()` function from our ta library to calculate the percentage changes of the requested data.

• The newly released `force_overlay` parameter in display-related functions allows indicators to display visuals on the main chart and a separate pane simultaneously. We use the parameter in this script's bgcolor() call to display background highlights on the main chart.

Look first. Then leap.

Consolidation Channels (AstroHub)Consolidation Channels (AstroHub) Indicator

Overview:

The Consolidation Channels (AstroHub) indicator is a powerful tool designed for traders seeking to identify consolidation periods within financial markets. Unlike traditional indicators that merely follow trends or focus on specific trading strategies, this script utilizes a unique approach based on fractal dimension calculations and multidimensional momentum analysis to detect consolidation zones in price action.

Key Concepts:

Fractal Dimension (Di):

The script employs the concept of fractal dimension to define the consolidation period (N). The user can customize this parameter to adjust the sensitivity of the indicator to consolidation patterns.

Multidimensional Momentum (M):

Multidimensional momentum is calculated by assessing the interaction between the closing prices (Pi) and opening prices (Pj) over a specified period (T). This dynamic calculation provides a comprehensive view of momentum changes in the market.

Consolidation Start:

The indicator marks the beginning of consolidation by identifying the lowest point in the multidimensional momentum. The consolidation start line is displayed on the chart, providing a clear reference for traders.

High and Low Lines:

High and low lines are drawn from the highest and lowest price levels over the consolidation period. These lines help visualize the upper and lower bounds of the consolidation channel.

Bar Color Change:

The color of each bar changes based on whether the closing price is above or below the consolidation start line. This visual cue assists traders in quickly identifying shifts in market dynamics.

Dashed Lines into the Future:

Dashed lines extending into the future from the high and low points of consolidation provide a forward-looking perspective, aiding traders in anticipating potential price movements.

How to Use:

Customization:

Adjust the input parameters (N, r, T, Z, Color1, Color2, Color3) to suit your trading preferences and market conditions.

Interpretation:

Look for periods where the bar color changes, indicating shifts in market sentiment during consolidation. Pay attention to the start of consolidation, high, and low lines for potential reversal or breakout signals.

Alerts:

Set up alerts for key events such as reaching the lowest point, closing above the high line, or closing below the low line to stay informed about potential trading opportunities.

Conclusion:

The Consolidation Channels (AstroHub) indicator goes beyond conventional trend-following techniques, offering traders a unique perspective on market consolidation. By combining fractal dimension analysis and multidimensional momentum calculations, this script equips traders with a valuable tool for identifying potential reversal zones and making informed trading decisions.

Dope DPOThe "Dope DPO" (DDPO) indicator is a technical analysis tool designed for traders to identify trends and potential trend changes in the market. It's based on the concept of the Detrended Price Oscillator (DPO), but with several enhancements for greater versatility and user customization.

Key Features of the Dope DPO Indicator:

Averaging Multiple Periods: The indicator averages the DPO calculations over ten different time periods. This averaging helps in smoothing out the volatility and providing a more comprehensive view of the market trend.

Customizable Smoothing: Users can choose the length of the smoothing as well as the type of moving average (SMA, EMA, WMA, or RMA) for smoothing. This allows for flexibility in how the indicator responds to price changes.

Trend Change Detection: The indicator includes a feature to detect changes in the market trend. It does this by comparing the current value of the smoothed DPO to its value a specified number of bars back. This helps in identifying potential reversals or shifts in momentum.

Dynamic Color Coding: The indicator uses color coding (green and red) to visually represent the trend direction. If the smoothed DPO is trending upwards compared to a previous value, the color will be green, indicating bullish momentum. Conversely, a red color signifies bearish momentum.

Horizontal Reference Lines: It includes horizontal lines at specific levels (overbought, zero, and oversold) to provide reference points for interpreting the indicator's values.

Usage:

Traders can use the Dope DPO to gauge the overall market trend and to look for potential entry and exit points based on trend changes.

The color-coded histogram makes it easy to spot when the trend might be reversing, which can be particularly useful in conjunction with other technical analysis tools.

The flexibility in choosing the smoothing method and length allows traders to tailor the indicator to different trading styles and timeframes.

[MAD] Harmonic Wave Fourier AnalysisThis script uses Fourier Analysis with additional postcalculations to draw a plot which displays the Amplitude-Change of the Fouriers

Parameter Settings:

You can set the number of data points to analyze

the period to check for extremes.

Fourier Transform: The script breaks down the time series data into its frequency components using cosine and sine calculations.

Harmonic Analysis: It calculates the strength and phase of each frequency component, producing harmonic waves.

Amplitude Change: It determines the change in amplitude between peaks and troughs for each harmonic.

Latest Value Extraction: The script selects the middle amplitude change as the latest data point.

High/Low Points: Finds the maximum and minimum amplitude changes over a specified period.

Visualization: It plots the latest amplitude change with a color that indicates its value relative to the identified extremes.

splitted by 3 Blue plots (1/3 1/2 2/3 from min to max)

How to trade?

May go for retests to the blue lines after big moves.

See this script as braindump of an idea, so its just a concept :-)

Trend_Trader_WMA (Momentum)<---> Caution! This is first test version of indicator. I am ready to get more ideas+feedback to develop it more. <--->

The "Momentum_Trader_WMA" indicator is a versatile technical analysis tool designed to help traders identify potential trend changes and momentum shifts in the market. It combines multiple indicators and moving averages to provide a comprehensive view of price action and momentum.

Key Features:

Weighted Moving Averages (WMAs): The indicator calculates two different WMAs with user-defined lengths, providing a smoothed representation of price data.

Average True Range (ATR) Bands: ATR is used to calculate dynamic bands around the WMA Average. These bands can help traders gauge market volatility and potential breakout points. The color of the ATR bands can be seen as an early signal of trends or the continuation of current trends.

Commodity Channel Index (CCI): CCI is a momentum oscillator that measures the relative strength of price changes. The indicator calculates CCI values based on a user-defined period.

Exponential Moving Average (EMA) of CCI: An EMA of CCI is plotted to help identify trends and momentum shifts.

Color-Coded Bands: The ATR bands change colors based on CCI conditions, providing visual cues for potential trading opportunities. When ATR bands transition from narrow (indicating low volatility) to wide (indicating increased volatility), it can be seen as an early signal of a potential trend change or the continuation of the current trend.

Buy and Sell Signals: The indicator generates buy and sell signals based on crossovers of WMAs and CCI thresholds, making it easier for traders to identify entry and exit points.

Customizable Moving Averages: Traders can enable or disable different moving averages (e.g., SMA, EMA, WMA, RMA, VWMA, HMA) with various periods and colors to adapt the indicator to their trading preferences.

CCI Dot Alerts: Dots are displayed at the bottom of the chart based on CCI values, helping traders spot extreme CCI conditions.

How to Use:

Trend Identification: The WMAs and ATR bands can help identify the current trend direction and its strength. When the WMAs are in an uptrend (green) and the ATR bands widen, it may indicate a strong bullish trend. Conversely, when the WMAs are in a downtrend (red) and the ATR bands narrow, it may suggest a weakening bearish trend.

Momentum Confirmation: The CCI and its EMA provide insights into market momentum. Look for CCI crossovers above 100 for potential bullish momentum and below -100 for potential bearish momentum.

Buy and Sell Signals: Pay attention to the buy and sell signals generated by the indicator. Buy when the WMAs cross over and CCI crosses above 100. Sell when the WMAs cross under and CCI crosses below -100.

ATR Bands as Early Signals: The color changes in the ATR bands can be seen as early signals of trends or the continuation of current trends. Wide ATR bands may indicate increased volatility and potential trend changes, while narrow ATR bands suggest reduced volatility and potential trend continuation.

Moving Averages: Customize the indicator by enabling or disabling specific moving averages according to your preferred trading strategy.

CCI Dots: Use the CCI dots to identify extreme CCI conditions, which may indicate overbought or oversold market conditions.

PS:

Recommended to use Indicator with price action conecpts(eg. support and resistance) as they play important role in any market.

Buy and sell signals are not really accurate. I would personally look for trend shift in WMA middle line and confirmation from CCI dots at bottom. For example. If middle line turns green and within recent 3-4 candles (or next 3-4 candles) dots tunrns green also, that means momentum has been rised in the direction of bulls.

pls, take s/r concepts first when working. I am thinking to add more precise buy sell signal method to make it easier to trade.

Good luck with your trades :)

Advanced Volatility-Adjusted Momentum IndexAdvanced Volatility-Adjusted Momentum Index (AVAMI)

The AVAMI is a powerful and versatile trading index which enhances the traditional momentum readings by introducing a volatility adjustment. This results in a more nuanced interpretation of market momentum, considering not only the rate of price changes but also the inherent volatility of the asset.

Settings and Parameters:

Momentum Length: This parameter sets the number of periods used to calculate the momentum, which is essentially the rate of change of the asset's price. A shorter length value means the momentum calculation will be more sensitive to recent price changes. Conversely, a longer length will yield a smoother and more stabilized momentum value, thereby reducing the impact of short-term price fluctuations.

Volatility Length: This parameter is responsible for determining the number of periods to be considered in the calculation of standard deviation of returns, which acts as the volatility measure. A shorter length will result in a more reactive volatility measure, while a longer length will produce a more stable, but less sensitive measure of volatility.

Smoothing Length: This parameter sets the number of periods used to apply a moving average smoothing to the AVAMI and its signal line. The purpose of this is to minimize the impact of volatile periods and to make the indicator's lines smoother and easier to interpret.

Lookback Period for Scaling: This is the number of periods used when rescaling the AVAMI values. The rescaling process is necessary to ensure that the AVAMI values remain within a consistent and interpretable range over time.

Overbought and Oversold Levels: These levels are thresholds at which the asset is considered overbought (potentially overvalued) or oversold (potentially undervalued), respectively. For instance, if the AVAMI exceeds the overbought level, traders may consider it as a possible selling opportunity, anticipating a price correction. Conversely, if the AVAMI falls below the oversold level, it could be seen as a buying opportunity, with the expectation of a price bounce.

Mid Level: This level represents the middle ground between the overbought and oversold levels. Crossing the mid-level line from below can be perceived as an increasing bullish momentum, and vice versa.

Show Divergences and Hidden Divergences: These checkboxes give traders the option to display regular and hidden divergences between the AVAMI and the asset's price. Divergences are crucial market structures that often signal potential price reversals.

Index Logic:

The AVAMI index begins with the calculation of a simple rate of change momentum indicator. This raw momentum is then adjusted by the standard deviation of log returns, which acts as a measure of market volatility. This adjustment process ensures that the resulting momentum index encapsulates not only the speed of price changes but also the market's volatility context.

The raw AVAMI is then smoothed using a moving average, and a signal line is generated as an exponential moving average (EMA) of this smoothed AVAMI. This signal line serves as a trigger for potential trading signals when crossed by the AVAMI.

The script also includes an algorithm to identify 'fractals', which are distinct price patterns that often act as potential market reversal points. These fractals are utilized to spot both regular and hidden divergences between the asset's price and the AVAMI.

Application and Strategy Concepts:

The AVAMI is a versatile tool that can be integrated into various trading strategies. Traders can utilize the overbought and oversold levels to identify potential reversal points. The AVAMI crossing the mid-level line can signify a change in market momentum. Additionally, the identification of regular and hidden divergences can serve as potential trading signals:

Regular Divergence: This happens when the asset's price records a new high/low, but the AVAMI fails to follow suit, suggesting a possible trend reversal. For instance, if the asset's price forms a higher high but the AVAMI forms a lower high, it's a regular bearish divergence, indicating potential price downturn.

Hidden Divergence: This is observed when the price forms a lower high/higher low, but the AVAMI forms a higher high/lower low, suggesting the continuation of the prevailing trend. For example, if the price forms a lower low during a downtrend, but the AVAMI forms a higher low, it's a hidden bullish divergence, signaling the potential continuation of the downtrend.

As with any trading tool, the AVAMI should not be used in isolation but in conjunction with other technical analysis tools and within the context of a well-defined trading plan.

120x ticker screener (composite tickers)In specific circumstances, it is possible to extract data, far above the 40 `request.*()` call limit for 1 single script .

The following technique uses composite tickers . Changing tickers needs to be done in the code itself as will be explained further.

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

🔶 PRINCIPLE

Standard example:

c1 = request.security('MTLUSDT' , 'D', close)

This will give the close value from 1 ticker (MTLUSDT); c1 for example is 1.153

Now let's add 2 tickers to MTLUSDT; XMRUSDT and ORNUSDT with, for example, values of 1.153 (I), 143.4 (II) and 0.8242 (III) respectively.

Just adding them up 'MTLUSDT+XMRUSDT+ORNUSDT' would give 145.3772 as a result, which is not something we can use...

Let's multiply ORNUSDT by 100 -> 14340

and multiply MTLUSDT by 1000000000 -> 1153000000 (from now, 10e8 will be used instead of 1000000000)

Then we make the sum.

When we put this in a security call (just the close value) we get:

c1 = request.security('MTLUSDT*10e8+XMRUSDT*100+ORNUSDT', 'D', close)

'MTLUSDT*10e8+XMRUSDT*100+ORNUSDT' -> 1153000000 + 14340 + 0.8242 = 1153014340.8242 (a)

This (a) will be split later on, for example:

1153014330.8242 / 10e8 = 1.1530143408242 -> round -> in this case to 1.153 (I), multiply again by 10e8 -> 1153000000.00 (b)

We subtract this from the initial number:

1153014340.8242 (a)

- 1153000000.0000 (b)

–––––––––––––––––

14340.8242 (c)

Then -> 14340.8242 / 100 = 143.408242 -> round -> 143.4 (II) -> multiply -> 14340.0000 (d)

-> subtract

14340.8242 (c)

- 14340.0000 (d)

––––––––––––

0.8242 (III)

Now we have split the number again into 3 tickers: 1.153 (I), 143.4 (II) and 0.8242 (III)

⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯⎯

In this publication the function compose_3_() will make a composite ticker of 3 tickers, and the split_3_() function will split these 3 tickers again after passing 1 request.security() call.

In this example:

t46 = 'BINANCE:MTLUSDT', n46 = 10e8 , r46 = 3, t47 = 'BINANCE:XMRUSDT', n47 = 10e1, r47 = 1, t48 = 'BINANCE:ORNUSDT', r48 = 4 // T16

•••

T16= compose_3_(t48, t47, n47, t46, n46)

•••

= request.security(T16, res, )

•••

= split_3_(c16, n46, r46, n47, r47, r48)

🔶 CHANGING TICKERS

If you need to change tickers, you only have to change the first part of the script, USER DEFINED TICKERS

Back to our example, at line 26 in the code, you'll find:

t46 = 'BINANCE:MTLUSDT', n46 = 10e8 , r46 = 3, t47 = 'BINANCE:XMRUSDT', n47 = 10e1, r47 = 1, t48 = 'BINANCE:ORNUSDT', r48 = 4 // T16

( t46 , T16 ,... will be explained later)

You need to figure out how much you need to multiply each ticker, and the number for rounding, to get a good result.

In this case:

'BINANCE:MTLUSDT', multiply number = 10e8, round number is 3 (example value 1.153)

'BINANCE:XMRUSDT', multiply number = 10e1, round number is 1 (example value 143.4)

'BINANCE:ORNUSDT', NO multiply number, round number is 4 (example value 0.8242)

The value with most digits after the decimal point by preference is placed to the right side (ORNUSDT)

If you want to change these 3, how would you do so?

First pick your tickers and look for the round values, for example:

'MATICUSDT', example value = 0.5876 -> round -> 4

'LTCUSDT' , example value = 77.47 -> round -> 2

'ARBUSDT' , example value = 1.0231 -> round -> 4

Value with most digits after the decimal point -> MATIC or ARB, let's pick ARB to go on the right side, LTC at the left of ARB, and MATIC at the most left side.

-> 'MATICUSDT', LTCUSDT', ARBUSDT'

Then check with how much 'LTCUSDT' and 'MATICUSDT' needs to be multiplied to get this: 5876 0 7747 0 1.0231

'MATICUSDT' -> 10e10

'LTCUSDT' -> 10e3

Replace:

t46 = 'BINANCE:MTLUSDT', n46 = 10e8 , r46 = 3, t47 = 'BINANCE:XMRUSDT', n47 = 10e1, r47 = 1, t48 = 'BINANCE:ORNUSDT', r48 = 4 // T16

->

t46 = 'BINANCE:MATICUSDT', n46 = 10e10 , r46 = 4, t47 = 'BINANCE:LTCUSDT', n47 = 10e3, r47 = 2, t48 = 'BINANCE:ARBUSDT', r48 = 4 // T16

DO NOT change anything at t46, n46,... if you don't know what you're doing!

Only

• tickers ('BINANCE:MTLUSDT', 'BINANCE:XMRUSDT', 'BINANCE:ORNUSDT', ...),

• multiply numbers (10e8, 10e1, ...) and

• round numbers (3, 1, 4, ...)

should be changed.

There you go!

🔶 LIMITATIONS

🔹 The composite ticker fails when 1 of the 3 isn't in market in the weekend, while the other 2 are.

That is the reason all tickers are crypto. I think it is possible to combine stock,... tickers, but they have to share the same market hours.

🔹 The number cannot be as large as you want, the limit lays around 15-16 digits.

This means when you have for example 123, 45.67 and 0.000000000089, you'll get issues when composing to this:

-> 123045670.000000000089 (21 digits)

Make sure the numbers are close to each other as possible, with 1 zero (or 2) in between:

-> 1.230045670089 (13 digits by doing -> (123 * 10e-3) + (45.67 * 10e-7) + 0.000000000089)

🔹 This script contains examples of calculated values, % change, SMA, RMA and RSI.

These values need to be calculated from HTF close data at current TF (timeframe).

This gives challenges. For example the SMA / %change is not a problem (same values at 1h TF from Daily data).

RMA , RSI is not so easy though...

Daily values are rather similar on a 2-3h TF, but 1h TF and lower is quite different.

At the moment I haven't figured out why, if someone has an idea, don't hesitate to share.

The main goal of this publication is 'composite tickers ~ request.security()' though.

🔹 When a ticker value changes substantially (x10, x100), the multiply number needs to be adjusted accordingly.

🔶 SETTINGS

SHOW SETS

SET

• Length : length of SMA, RMA and RSI

• HTF : Higher TimeFrame (default Daily)

TABLE

• Size table : \ _ Self-explanatory

• Include exchange name : /

• Sort : If exchange names are shown, the exchanges will be sorted first

COLOURS

• CH%

• RSI

• SMA (RMA)

DEBUG

Remember t46 , T16 ,... ?

This can be used for debugging/checking

ALWAYS DISABLE " sort " when doing so.

Example:

Set string -> T1 (tickers FIL, CAKE, SOL)

(Numbers are slightly different due to time passing by between screen captures)

Placing your tickers at the side panel makes it easy to compare with the printed label below the table (right side, 332201415014.45 ),

together with the line T1 in the script:

t1 = 'BINANCE:FILUSDT' , n1 = 10e10, r1 = 4, t2 = 'BINANCE:CAKEUSDT' , n2 = 10e5 , r2 = 3, t3 = 'BINANCE:SOLUSDT' , r3 = 2 // T1

FIL : 3.322

CAKE: 1.415

SOL : 14.56

Now it is easy to check whether the tickers are placed close enough to each other, with 1-2 zero's in between.

If you want to check a specific ticker, use " Show Ticker" , see out initial example:

Set string -> T16

Show ticker -> 46 (in the code -> t46 = 'BINANCE:MTLUSDT')

(Set at 0 to disable " check string " and NONE to disable " Set string ")

-> Debug/check/set away! 😀

🔶 OTHER TECHNIQUES

• REGEX ( Regular expression ) and str.match() is used to delete the exchange name from the ticker, in other words, everything before ":" is deleted by following regex:

exch(t) => incl_exch ? t : str.match(t, "(?<=:) +")

• To sort, array.sort_indices() is used (line 675 in the code), just as in my first "sort" publication Sort array alphabetically - educational

aSort = arrT.copy()

sort_Indices = array.sort_indices(id= aSort, order= order.ascending)

• Numbers and text colour will adjust automatically when switching between light/dark mode by using chart.fg_color / chart.bg_color

🔹 DISCLAIMER

Please don't ask me for custom screeners, thank you.

3 Fib EMAs To Scalp Them AllThe "3 Fib EMAs To Scalp Them All" was made in order to clear up when we should look for shorts, longs, or walk away. Also it can alert you when a trend starts, or when there is a possible reversal. I use it for scalping/day trading in 5m-1h timeframes.

1. EMAs: By default, the indicator uses Fibonacci numbers (21, 55, 233), but you can change them.

2. Color Changes: The color of the Micro EMA line changes depending on its relation to the Mid and Macro EMAs.

When Micro EMA < Mid < Macro EMA, it turns red, indicating a potential bearish trend - that's when you should look for shorts

When Micro EMA > Mid > Macro EMA, it turns green, indicating a potential bullish trend - that's when you should look for longs

A white Micro EMA is when you need to take some rest, enjoy your coffee, and avoid overtrading.

3. Signals: The indicator provides visual signals in the form of diamonds and crosses and corresponding alert signals.

A red diamond above the bar signals a potential beginning of a downtrend

A red cross above the bar signals the end of the downtrend and can be used as a signal for a possible reversal up/breakout.

A green diamond below the bar signals a potential beginning of a downtrend,

A green cross below the bar signals the end of the uptrend and can be used as a signal for a possible reversal down/breakout.

4. Alerts: For algo traders and people who prefer to stay away from the monitor... there are alerts for every signal.

Friendly note: Don't blindly follow the signals for your long and short entries. The signals only pop up when the EMA cross value gets a confirmation. A smart move would be to wait for a retracement to the EMA line and use momentum indicators like market cipher B to pinpoint those ideal entry points.

Quinn-Fernandes Fourier Transform of Filtered Price [Loxx]Down the Rabbit Hole We Go: A Deep Dive into the Mysteries of Quinn-Fernandes Fast Fourier Transform and Hodrick-Prescott Filtering

In the ever-evolving landscape of financial markets, the ability to accurately identify and exploit underlying market patterns is of paramount importance. As market participants continuously search for innovative tools to gain an edge in their trading and investment strategies, advanced mathematical techniques, such as the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter, have emerged as powerful analytical tools. This comprehensive analysis aims to delve into the rich history and theoretical foundations of these techniques, exploring their applications in financial time series analysis, particularly in the context of a sophisticated trading indicator. Furthermore, we will critically assess the limitations and challenges associated with these transformative tools, while offering practical insights and recommendations for overcoming these hurdles to maximize their potential in the financial domain.

Our investigation will begin with a comprehensive examination of the origins and development of both the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter. We will trace their roots from classical Fourier analysis and time series smoothing to their modern-day adaptive iterations. We will elucidate the key concepts and mathematical underpinnings of these techniques and demonstrate how they are synergistically used in the context of the trading indicator under study.

As we progress, we will carefully consider the potential drawbacks and challenges associated with using the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter as integral components of a trading indicator. By providing a critical evaluation of their computational complexity, sensitivity to input parameters, assumptions about data stationarity, performance in noisy environments, and their nature as lagging indicators, we aim to offer a balanced and comprehensive understanding of these powerful analytical tools.

In conclusion, this in-depth analysis of the Quinn-Fernandes Fourier Transform and the Hodrick-Prescott Filter aims to provide a solid foundation for financial market participants seeking to harness the potential of these advanced techniques in their trading and investment strategies. By shedding light on their history, applications, and limitations, we hope to equip traders and investors with the knowledge and insights necessary to make informed decisions and, ultimately, achieve greater success in the highly competitive world of finance.

█ Fourier Transform and Hodrick-Prescott Filter in Financial Time Series Analysis

Financial time series analysis plays a crucial role in making informed decisions about investments and trading strategies. Among the various methods used in this domain, the Fourier Transform and the Hodrick-Prescott (HP) Filter have emerged as powerful techniques for processing and analyzing financial data. This section aims to provide a comprehensive understanding of these two methodologies, their significance in financial time series analysis, and their combined application to enhance trading strategies.

█ The Quinn-Fernandes Fourier Transform: History, Applications, and Use in Financial Time Series Analysis

The Quinn-Fernandes Fourier Transform is an advanced spectral estimation technique developed by John J. Quinn and Mauricio A. Fernandes in the early 1990s. It builds upon the classical Fourier Transform by introducing an adaptive approach that improves the identification of dominant frequencies in noisy signals. This section will explore the history of the Quinn-Fernandes Fourier Transform, its applications in various domains, and its specific use in financial time series analysis.

History of the Quinn-Fernandes Fourier Transform

The Quinn-Fernandes Fourier Transform was introduced in a 1993 paper titled "The Application of Adaptive Estimation to the Interpolation of Missing Values in Noisy Signals." In this paper, Quinn and Fernandes developed an adaptive spectral estimation algorithm to address the limitations of the classical Fourier Transform when analyzing noisy signals.

The classical Fourier Transform is a powerful mathematical tool that decomposes a function or a time series into a sum of sinusoids, making it easier to identify underlying patterns and trends. However, its performance can be negatively impacted by noise and missing data points, leading to inaccurate frequency identification.

Quinn and Fernandes sought to address these issues by developing an adaptive algorithm that could more accurately identify the dominant frequencies in a noisy signal, even when data points were missing. This adaptive algorithm, now known as the Quinn-Fernandes Fourier Transform, employs an iterative approach to refine the frequency estimates, ultimately resulting in improved spectral estimation.

Applications of the Quinn-Fernandes Fourier Transform

The Quinn-Fernandes Fourier Transform has found applications in various fields, including signal processing, telecommunications, geophysics, and biomedical engineering. Its ability to accurately identify dominant frequencies in noisy signals makes it a valuable tool for analyzing and interpreting data in these domains.

For example, in telecommunications, the Quinn-Fernandes Fourier Transform can be used to analyze the performance of communication systems and identify interference patterns. In geophysics, it can help detect and analyze seismic signals and vibrations, leading to improved understanding of geological processes. In biomedical engineering, the technique can be employed to analyze physiological signals, such as electrocardiograms, leading to more accurate diagnoses and better patient care.

Use of the Quinn-Fernandes Fourier Transform in Financial Time Series Analysis

In financial time series analysis, the Quinn-Fernandes Fourier Transform can be a powerful tool for isolating the dominant cycles and frequencies in asset price data. By more accurately identifying these critical cycles, traders can better understand the underlying dynamics of financial markets and develop more effective trading strategies.

The Quinn-Fernandes Fourier Transform is used in conjunction with the Hodrick-Prescott Filter, a technique that separates the underlying trend from the cyclical component in a time series. By first applying the Hodrick-Prescott Filter to the financial data, short-term fluctuations and noise are removed, resulting in a smoothed representation of the underlying trend. This smoothed data is then subjected to the Quinn-Fernandes Fourier Transform, allowing for more accurate identification of the dominant cycles and frequencies in the asset price data.

By employing the Quinn-Fernandes Fourier Transform in this manner, traders can gain a deeper understanding of the underlying dynamics of financial time series and develop more effective trading strategies. The enhanced knowledge of market cycles and frequencies can lead to improved risk management and ultimately, better investment performance.

The Quinn-Fernandes Fourier Transform is an advanced spectral estimation technique that has proven valuable in various domains, including financial time series analysis. Its adaptive approach to frequency identification addresses the limitations of the classical Fourier Transform when analyzing noisy signals, leading to more accurate and reliable analysis. By employing the Quinn-Fernandes Fourier Transform in financial time series analysis, traders can gain a deeper understanding of the underlying financial instrument.

Drawbacks to the Quinn-Fernandes algorithm

While the Quinn-Fernandes Fourier Transform is an effective tool for identifying dominant cycles and frequencies in financial time series, it is not without its drawbacks. Some of the limitations and challenges associated with this indicator include:

1. Computational complexity: The adaptive nature of the Quinn-Fernandes Fourier Transform requires iterative calculations, which can lead to increased computational complexity. This can be particularly challenging when analyzing large datasets or when the indicator is used in real-time trading environments.

2. Sensitivity to input parameters: The performance of the Quinn-Fernandes Fourier Transform is dependent on the choice of input parameters, such as the number of harmonic periods, frequency tolerance, and Hodrick-Prescott filter settings. Choosing inappropriate parameter values can lead to inaccurate frequency identification or reduced performance. Finding the optimal parameter settings can be challenging, and may require trial and error or a more sophisticated optimization process.

3. Assumption of stationary data: The Quinn-Fernandes Fourier Transform assumes that the underlying data is stationary, meaning that its statistical properties do not change over time. However, financial time series data is often non-stationary, with changing trends and volatility. This can limit the effectiveness of the indicator and may require additional preprocessing steps, such as detrending or differencing, to ensure the data meets the assumptions of the algorithm.

4. Limitations in noisy environments: Although the Quinn-Fernandes Fourier Transform is designed to handle noisy signals, its performance may still be negatively impacted by significant noise levels. In such cases, the identification of dominant frequencies may become less reliable, leading to suboptimal trading signals or strategies.

5. Lagging indicator: As with many technical analysis tools, the Quinn-Fernandes Fourier Transform is a lagging indicator, meaning that it is based on past data. While it can provide valuable insights into historical market dynamics, its ability to predict future price movements may be limited. This can result in false signals or late entries and exits, potentially reducing the effectiveness of trading strategies based on this indicator.

Despite these drawbacks, the Quinn-Fernandes Fourier Transform remains a valuable tool for financial time series analysis when used appropriately. By being aware of its limitations and adjusting input parameters or preprocessing steps as needed, traders can still benefit from its ability to identify dominant cycles and frequencies in financial data, and use this information to inform their trading strategies.

█ Deep-dive into the Hodrick-Prescott Fitler

The Hodrick-Prescott (HP) filter is a statistical tool used in economics and finance to separate a time series into two components: a trend component and a cyclical component. It is a powerful tool for identifying long-term trends in economic and financial data and is widely used by economists, central banks, and financial institutions around the world.

The HP filter was first introduced in the 1990s by economists Robert Hodrick and Edward Prescott. It is a simple, two-parameter filter that separates a time series into a trend component and a cyclical component. The trend component represents the long-term behavior of the data, while the cyclical component captures the shorter-term fluctuations around the trend.

The HP filter works by minimizing the following objective function: