RawCuts_01Library "RawCuts_01"

A collection of functions by:

mutantdog

The majority of these are used within published projects, some useful variants have been included here aswell.

This is volume one consisting mainly of smaller functions, predominantly the filters and standard deviations from Weight Gain 4000.

Also included at the bottom are various snippets of related code for demonstration. These can be copied and adjusted according to your needs.

A full up-to-date table of contents is located at the top of the main script.

WEIGHT GAIN FILTERS

A collection of moving average type filters with adjustable volume weighting.

Based upon the two most common methods of volume weighting.

'Simple' uses the standard method in which a basic VWMA is analogous to SMA.

'Elastic' uses exponential method found in EVWMA which is analogous to RMA.

Volume weighting is applied according to an exponent multiplier of input volume.

0 >> volume^0 (unweighted), 1 >> volume^1 (fully weighted), use float values for intermediate weighting.

Additional volume filter switch for smoothing of outlier events.

DIVA MODULAR DEVIATIONS

A small collection of standard and absolute deviations.

Includes the weightgain functionality as above.

Basic modular functionality for more creative uses.

Optional input (ct) for external central tendency (aka: estimator).

Can be assigned to alternative filter or any float value. Will default to internal filter when no ct input is received.

Some other useful or related functions included at the bottom along with basic demonstration use.

weightgain_sma(src, len, xVol, fVol)

Simple Moving Average (SMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Standard Simple Moving Average with Simple Weight Gain applied.

weightgain_hsma(src, len, xVol, fVol)

Harmonic Simple Moving Average (hSMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Harmonic Simple Moving Average with Simple Weight Gain applied.

weightgain_gsma(src, len, xVol, fVol)

Geometric Simple Moving Average (gSMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Geometric Simple Moving Average with Simple Weight Gain applied.

weightgain_wma(src, len, xVol, fVol)

Linear Weighted Moving Average (WMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Basic Linear Weighted Moving Average with Simple Weight Gain applied.

weightgain_hma(src, len, xVol, fVol)

Hull Moving Average (HMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Basic Hull Moving Average with Simple Weight Gain applied.

diva_sd_sma(src, len, xVol, fVol, ct)

Standard Deviation (SD SMA): Diva / Weight Gain (Simple Volume)

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_sma().

Returns:

diva_sd_wma(src, len, xVol, fVol, ct)

Standard Deviation (SD WMA): Diva / Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_wma().

Returns:

diva_aad_sma(src, len, xVol, fVol, ct)

Average Absolute Deviation (AAD SMA): Diva / Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_sma().

Returns:

diva_aad_wma(src, len, xVol, fVol, ct)

Average Absolute Deviation (AAD WMA): Diva / Weight Gain (Simple Volume) .

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_wma().

Returns:

weightgain_ema(src, len, xVol, fVol)

Exponential Moving Average (EMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Exponential Moving Average with Elastic Weight Gain applied.

weightgain_dema(src, len, xVol, fVol)

Double Exponential Moving Average (DEMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Double Exponential Moving Average with Elastic Weight Gain applied.

weightgain_tema(src, len, xVol, fVol)

Triple Exponential Moving Average (TEMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Triple Exponential Moving Average with Elastic Weight Gain applied.

weightgain_rma(src, len, xVol, fVol)

Rolling Moving Average (RMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Rolling Moving Average with Elastic Weight Gain applied.

weightgain_drma(src, len, xVol, fVol)

Double Rolling Moving Average (DRMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Double Rolling Moving Average with Elastic Weight Gain applied.

weightgain_trma(src, len, xVol, fVol)

Triple Rolling Moving Average (TRMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Triple Rolling Moving Average with Elastic Weight Gain applied.

diva_sd_ema(src, len, xVol, fVol, ct)

Standard Deviation (SD EMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_ema().

Returns:

diva_sd_rma(src, len, xVol, fVol, ct)

Standard Deviation (SD RMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_rma().

Returns:

weightgain_vidya_rma(src, len, xVol, fVol)

VIDYA v1 RMA base (VIDYA-RMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: VIDYA v1, RMA base with Elastic Weight Gain applied.

weightgain_vidya_ema(src, len, xVol, fVol)

VIDYA v1 EMA base (VIDYA-EMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: VIDYA v1, EMA base with Elastic Weight Gain applied.

diva_sd_vidya_rma(src, len, xVol, fVol, ct)

Standard Deviation (SD VIDYA-RMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_vidya_rma().

Returns:

diva_sd_vidya_ema(src, len, xVol, fVol, ct)

Standard Deviation (SD VIDYA-EMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_vidya_ema().

Returns:

weightgain_sema(src, len, xVol, fVol)

Parameters:

src (float)

len (simple int)

xVol (float)

fVol (bool)

diva_sd_sema(src, len, xVol, fVol)

Parameters:

src (float)

len (simple int)

xVol (float)

fVol (bool)

diva_mad_mm(src, len, ct)

Median Absolute Deviation (MAD MM): Diva (no volume weighting).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

ct (float) : Central tendency (optional, na = bypass). Internal: ta.median()

Returns:

source_switch(slct, aux1, aux2, aux3, aux4)

Custom Source Selector/Switch function. Features standard & custom 'weighted' sources with additional aux inputs.

Parameters:

slct (string) : Choose from custom set of string values.

aux1 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

aux2 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

aux3 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

aux4 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

Returns: Float value, to be used as src input for other functions.

colour_gradient_ma_div(ma1, ma2, div, bull, bear, mid, mult)

Colour Gradient for plot fill between two moving averages etc, with seperate bull/bear and divergence strength.

Parameters:

ma1 (float) : Input for fast moving average (eg: bullish when above ma2).

ma2 (float) : Input for slow moving average (eg: bullish when below ma1).

div (float) : Input deviation/divergence value used to calculate strength of colour.

bull (color) : Colour when ma1 above ma2.

bear (color) : Colour when ma1 below ma2.

mid (color) : Neutral colour when ma1 = ma2.

mult (int) : Opacity multiplier. 100 = maximum, 0 = transparent.

Returns: Colour with transparency (according to specified inputs)

Search in scripts for "harmonic"

EphemerisLibrary "Ephemeris"

TODO: add library description here

mercuryElements()

mercuryRates()

venusElements()

venusRates()

earthElements()

earthRates()

marsElements()

marsRates()

jupiterElements()

jupiterRates()

saturnElements()

saturnRates()

uranusElements()

uranusRates()

neptuneElements()

neptuneRates()

rev360(x)

Normalize degrees to within [0, 360)

Parameters:

x (float) : degrees to be normalized

Returns: Normalized degrees

scaleAngle(longitude, magnitude, harmonic)

Scale angle in degrees

Parameters:

longitude (float)

magnitude (float)

harmonic (int)

Returns: Scaled angle in degrees

julianCenturyInJulianDays()

Constant Julian days per century

Returns: 36525

julianEpochJ2000()

Julian date on J2000 epoch start (2000-01-01)

Returns: 2451545.0

meanObliquityForJ2000()

Mean obliquity of the ecliptic on J2000 epoch start (2000-01-01)

Returns: 23.43928

getJulianDate(Year, Month, Day, Hour, Minute)

Convert calendar date to Julian date

Parameters:

Year (int) : calendar year as integer (e.g. 2018)

Month (int) : calendar month (January = 1, December = 12)

Day (int) : calendar day of month (e.g. January valid days are 1-31)

Hour (int) : valid values 0-23

Minute (int) : valid values 0-60

julianCenturies(date, epoch_start)

Centuries since Julian Epoch 2000-01-01

Parameters:

date (float) : Julian date to conver to Julian centuries

epoch_start (float) : Julian date of epoch start (e.g. J2000 epoch = 2451545)

Returns: Julian date converted to Julian centuries

julianCenturiesSinceEpochJ2000(julianDate)

Calculate Julian centuries since epoch J2000 (2000-01-01)

Parameters:

julianDate (float) : Julian Date in days

Returns: Julian centuries since epoch J2000 (2000-01-01)

atan2(y, x)

Specialized arctan function

Parameters:

y (float) : radians

x (float) : radians

Returns: special arctan of y/x

eccAnom(ec, m_param, dp)

Compute eccentricity of the anomaly

Parameters:

ec (float) : Eccentricity of Orbit

m_param (float) : Mean Anomaly ?

dp (int) : Decimal places to round to

Returns: Eccentricity of the Anomaly

planetEphemerisCalc(TGen, planetElementId, planetRatesId)

Compute planetary ephemeris (longtude relative to Earth or Sun) on a Julian date

Parameters:

TGen (float) : Julian Date

planetElementId (float ) : All planet orbital elements in an array. This index references a specific planet's elements.

planetRatesId (float ) : All planet orbital rates in an array. This index references a specific planet's rates.

Returns: X,Y,Z ecliptic rectangular coordinates and R radius from reference body.

calculateRightAscensionAndDeclination(earthX, earthY, earthZ, planetX, planetY, planetZ)

Calculate right ascension and declination for a planet relative to Earth

Parameters:

earthX (float) : Earth X ecliptic rectangular coordinate relative to Sun

earthY (float) : Earth Y ecliptic rectangular coordinate relative to Sun

earthZ (float) : Earth Z ecliptic rectangular coordinate relative to Sun

planetX (float) : Planet X ecliptic rectangular coordinate relative to Sun

planetY (float) : Planet Y ecliptic rectangular coordinate relative to Sun

planetZ (float) : Planet Z ecliptic rectangular coordinate relative to Sun

Returns: Planet geocentric orbital radius, geocentric right ascension, and geocentric declination

mercuryHelio(T)

Compute Mercury heliocentric longitude on date

Parameters:

T (float)

Returns: Mercury heliocentric longitude on date

venusHelio(T)

Compute Venus heliocentric longitude on date

Parameters:

T (float)

Returns: Venus heliocentric longitude on date

earthHelio(T)

Compute Earth heliocentric longitude on date

Parameters:

T (float)

Returns: Earth heliocentric longitude on date

marsHelio(T)

Compute Mars heliocentric longitude on date

Parameters:

T (float)

Returns: Mars heliocentric longitude on date

jupiterHelio(T)

Compute Jupiter heliocentric longitude on date

Parameters:

T (float)

Returns: Jupiter heliocentric longitude on date

saturnHelio(T)

Compute Saturn heliocentric longitude on date

Parameters:

T (float)

Returns: Saturn heliocentric longitude on date

neptuneHelio(T)

Compute Neptune heliocentric longitude on date

Parameters:

T (float)

Returns: Neptune heliocentric longitude on date

uranusHelio(T)

Compute Uranus heliocentric longitude on date

Parameters:

T (float)

Returns: Uranus heliocentric longitude on date

sunGeo(T)

Parameters:

T (float)

mercuryGeo(T)

Parameters:

T (float)

venusGeo(T)

Parameters:

T (float)

marsGeo(T)

Parameters:

T (float)

jupiterGeo(T)

Parameters:

T (float)

saturnGeo(T)

Parameters:

T (float)

neptuneGeo(T)

Parameters:

T (float)

uranusGeo(T)

Parameters:

T (float)

moonGeo(T_JD)

Parameters:

T_JD (float)

mercuryOrbitalPeriod()

Mercury orbital period in Earth days

Returns: 87.9691

venusOrbitalPeriod()

Venus orbital period in Earth days

Returns: 224.701

earthOrbitalPeriod()

Earth orbital period in Earth days

Returns: 365.256363004

marsOrbitalPeriod()

Mars orbital period in Earth days

Returns: 686.980

jupiterOrbitalPeriod()

Jupiter orbital period in Earth days

Returns: 4332.59

saturnOrbitalPeriod()

Saturn orbital period in Earth days

Returns: 10759.22

uranusOrbitalPeriod()

Uranus orbital period in Earth days

Returns: 30688.5

neptuneOrbitalPeriod()

Neptune orbital period in Earth days

Returns: 60195.0

jupiterSaturnCompositePeriod()

jupiterNeptuneCompositePeriod()

jupiterUranusCompositePeriod()

saturnNeptuneCompositePeriod()

saturnUranusCompositePeriod()

planetSineWave(julianDateInCenturies, planetOrbitalPeriod, planetHelio)

Convert heliocentric longitude of planet into a sine wave

Parameters:

julianDateInCenturies (float)

planetOrbitalPeriod (float) : Orbital period of planet in Earth days

planetHelio (float) : Heliocentric longitude of planet in degrees

Returns: Sine of heliocentric longitude on a Julian date

Regression Channel Alternative MTF V2█ OVERVIEW

This indicator is a predecessor to Regression Channel Alternative MTF , which is coded based on latest update of type, object and method.

█ IMPORTANT NOTES

This indicator is NOT true Multi Timeframe (MTF) but considered as Alternative MTF which calculate 100 bars for Primary MTF, can be refer from provided line helper.

The timeframe scenarios are defined based on Position, Swing and Intraday Trader.

Suppported Timeframe : W, D, 60, 15, 5 and 1.

Channel drawn based on regression calculation.

Angle channel is NOT supported.

█ INSPIRATIONS

These timeframe scenarios are defined based on Harmonic Trading : Volume Three written by Scott M Carney.

By applying channel on each timeframe, MW or ABCD patterns can be easily identified manually.

This can also be applied on other chart patterns.

█ CREDITS

Scott M Carney, Harmonic Trading : Volume Three (Reaction vs. Reversal)

█ TIMEFRAME EXPLAINED

Higher / Distal : The (next) longer or larger comparative timeframe after primary pattern has been identified.

Primary / Clear : Timeframe that possess the clearest pattern structure.

Lower / Proximate : The (next) shorter timeframe after primary pattern has been identified.

Lowest : Check primary timeframe as main reference.

█ FEATURES

Color is determined by trend or timeframe.

Some color is depends on chart contrast color.

Color is determined by trend or timeframe.

█ EXAMPLE OF USAGE / EXPLAINATION

Lyapunov Hodrick-Prescott Oscillator w/ DSL [Loxx]Lyapunov Hodrick-Prescott Oscillator w/ DSL is a Hodrick-Prescott Channel Filter that is modified using the Lyapunov stability algorithm to turn the filter into an oscillator. Signals are created using Discontinued Signal Lines.

What is the Lyapunov Stability?

As soon as scientists realized that the evolution of physical systems can be described in terms of mathematical equations, the stability of the various dynamical regimes was recognized as a matter of primary importance. The interest for this question was not only motivated by general curiosity, but also by the need to know, in the XIX century, to what extent the behavior of suitable mechanical devices remains unchanged, once their configuration has been perturbed. As a result, illustrious scientists such as Lagrange, Poisson, Maxwell and others deeply thought about ways of quantifying the stability both in general and specific contexts. The first exact definition of stability was given by the Russian mathematician Aleksandr Lyapunov who addressed the problem in his PhD Thesis in 1892, where he introduced two methods, the first of which is based on the linearization of the equations of motion and has originated what has later been termed Lyapunov exponents (LE). (Lyapunov 1992)

The interest in it suddenly skyrocketed during the Cold War period when the so-called "Second Method of Lyapunov" (see below) was found to be applicable to the stability of aerospace guidance systems which typically contain strong nonlinearities not treatable by other methods. A large number of publications appeared then and since in the control and systems literature. More recently the concept of the Lyapunov exponent (related to Lyapunov's First Method of discussing stability) has received wide interest in connection with chaos theory . Lyapunov stability methods have also been applied to finding equilibrium solutions in traffic assignment problems.

In practice, Lyapunov exponents can be computed by exploiting the natural tendency of an n-dimensional volume to align along the n most expanding subspace. From the expansion rate of an n-dimensional volume, one obtains the sum of the n largest Lyapunov exponents. Altogether, the procedure requires evolving n linearly independent perturbations and one is faced with the problem that all vectors tend to align along the same direction. However, as shown in the late '70s, this numerical instability can be counterbalanced by orthonormalizing the vectors with the help of the Gram-Schmidt procedure (Benettin et al. 1980, Shimada and Nagashima 1979) (or, equivalently with a QR decomposition). As a result, the LE λi, naturally ordered from the largest to the most negative one, can be computed: they are altogether referred to as the Lyapunov spectrum.

The Lyapunov exponent "λ" , is useful for distinguishing among the various types of orbits. It works for discrete as well as continuous systems.

λ < 0

The orbit attracts to a stable fixed point or stable periodic orbit. Negative Lyapunov exponents are characteristic of dissipative or non-conservative systems (the damped harmonic oscillator for instance). Such systems exhibit asymptotic stability; the more negative the exponent, the greater the stability. Superstable fixed points and superstable periodic points have a Lyapunov exponent of λ = −∞. This is something akin to a critically damped oscillator in that the system heads towards its equilibrium point as quickly as possible.

λ = 0

The orbit is a neutral fixed point (or an eventually fixed point). A Lyapunov exponent of zero indicates that the system is in some sort of steady state mode. A physical system with this exponent is conservative. Such systems exhibit Lyapunov stability. Take the case of two identical simple harmonic oscillators with different amplitudes. Because the frequency is independent of the amplitude, a phase portrait of the two oscillators would be a pair of concentric circles. The orbits in this situation would maintain a constant separation, like two flecks of dust fixed in place on a rotating record.

λ > 0

The orbit is unstable and chaotic. Nearby points, no matter how close, will diverge to any arbitrary separation. All neighborhoods in the phase space will eventually be visited. These points are said to be unstable. For a discrete system, the orbits will look like snow on a television set. This does not preclude any organization as a pattern may emerge. Thus the snow may be a bit lumpy. For a continuous system, the phase space would be a tangled sea of wavy lines like a pot of spaghetti. A physical example can be found in Brownian motion. Although the system is deterministic, there is no order to the orbit that ensues.

For our purposes here, we transform the HP by applying Lyapunov Stability as follows:

output = math.log(math.abs(HP / HP ))

You can read more about Lyapunov Stability here: Measuring Chaos

What is. the Hodrick-Prescott Filter?

The Hodrick-Prescott (HP) filter refers to a data-smoothing technique. The HP filter is commonly applied during analysis to remove short-term fluctuations associated with the business cycle. Removal of these short-term fluctuations reveals long-term trends.

The Hodrick-Prescott (HP) filter is a tool commonly used in macroeconomics. It is named after economists Robert Hodrick and Edward Prescott who first popularized this filter in economics in the 1990s. Hodrick was an economist who specialized in international finance. Prescott won the Nobel Memorial Prize, sharing it with another economist for their research in macroeconomics.

This filter determines the long-term trend of a time series by discounting the importance of short-term price fluctuations. In practice, the filter is used to smooth and detrend the Conference Board's Help Wanted Index (HWI) so it can be benchmarked against the Bureau of Labor Statistic's (BLS) JOLTS, an economic data series that may more accurately measure job vacancies in the U.S.

The HP filter is one of the most widely used tools in macroeconomic analysis. It tends to have favorable results if the noise is distributed normally, and when the analysis being conducted is historical.

What are DSL Discontinued Signal Line?

A lot of indicators are using signal lines in order to determine the trend (or some desired state of the indicator) easier. The idea of the signal line is easy : comparing the value to it's smoothed (slightly lagging) state, the idea of current momentum/state is made.

Discontinued signal line is inheriting that simple signal line idea and it is extending it : instead of having one signal line, more lines depending on the current value of the indicator.

"Signal" line is calculated the following way :

When a certain level is crossed into the desired direction, the EMA of that value is calculated for the desired signal line

When that level is crossed into the opposite direction, the previous "signal" line value is simply "inherited" and it becomes a kind of a level

This way it becomes a combination of signal lines and levels that are trying to combine both the good from both methods.

In simple terms, DSL uses the concept of a signal line and betters it by inheriting the previous signal line's value & makes it a level.

Included:

Bar coloring

Alerts

Signals

Loxx's Expanded Source Types

Weight Gain 4000 - (Adjustable Volume Weighted MA) - [mutantdog]Short Version:

This is a fairly self-contained system based upon a moving average crossover with several unique features. The most significant of these is the adjustable volume weighting system, allowing for transformations between standard and weighted versions of each included MA. With this feature it is possible to apply partial weighting which can help to improve responsiveness without dramatically altering shape. Included types are SMA, EMA, WMA, RMA, hSMA, DEMA and TEMA. Potentially more will be added in future (check updates below).

In addition there are a selection of alternative 'weighted' inputs, a pair of Bollinger-style deviation bands, a separate price tracker and a bunch of alert presets.

This can be used out-of-the-box or tweaked in multiple ways for unusual results. Default settings are a basic 8/21 EMA cross with partial volume weighting. Dev bands apply to MA2 and are based upon the type and the volume weighting. For standard Bollinger bands use SMA with length 20 and try adding a small amount of volume weighting.

A more detailed breakdown of the functionality follows.

Long Version:

ADJUSTABLE VOLUME WEIGHTING

In principle any moving average should have a volume weighted analogue, the standard VWMA is just an SMA with volume weighting for example. Actually, we can consider the SMA to be a special case where volume is a constant 1 per bar (the value is somewhat arbitrary, the important part is that it's constant). Similar principles apply to the 'elastic' EVWMA which is the volume weighted analogue of an RMA. In any case though, where we have standard and weighted variants it is possible to transform one into the other by gradually increasing or decreasing the weighting, which forms the basis of this system. This is not just a simple multiplier however, that would not work due to the relative proportions being the same when set at any non zero value. In order to create a meaningful transformation we need to use an exponent instead, eg: volume^x , where x is a variable determined in this case by the 'volume' parameter. When x=1, the full volume weighting applies and when x=0, the volume will be reduced to a constant 1. Values in between will result in the respective partial weighting, for example 0.5 will give the square root of the volume.

The obvious question here though is why would you want to do this? To answer that really it is best to actually try it. The advantages that volume weighting can bring to a moving average can sometimes come at the cost of unwanted or erratic behaviour. While it can tend towards much closer price tracking which may be desirable, sometimes it needs moderating especially in markets with lower liquidity. Here the adjustability can be useful, in many cases i have found that adding a small amount of volume weighting to a chosen MA can help to improve its responsiveness without overpowering it. Another possible use case would be to have two instances of the same MA with the same length but different weightings, the extent to which these diverge from each other can be a useful indicator of trend strength. Other uses will become apparent with experimentation and can vary from one market to another.

THE INCLUDED MODES

At the time of publication, there are 7 included moving average types with plans to add more in future. For now here is a brief explainer of what's on offer (continuing to use x as shorthand for the volume parameter), starting with the two most common types.

SMA: As mentioned above this is essentially a standard VWMA, calculated here as sma(source*volume^x,length)/sma(volume^x,length). In this case when x=0 then volume=1 and it reduces to a standard SMA.

RMA: Again mentioned above, this is an EVWMA (where E stands for elastic) with constant weighting. Without going into detail, this method takes the 1/length factor of an RMA and replaces it with volume^x/sum(volume^x,length). In this case again we can see that when x=0 then volume=1 and the original 1/length factor is restored.

EMA: This follows the same principle as the RMA where the standard 2/(length+1) factor is replaced with (2*volume^x)/(sum(volume^x,length)+volume^x). As with an RMA, when x=0 then volume=1 and this reduces back to the standard 2/(length+1).

DEMA: Just a standard Double EMA using the above.

TEMA: Likewise, a standard Triple EMA using the above.

hSMA: This is the same as the SMA except it uses harmonic mean calculations instead of arithmetic. In most cases the differences are negligible however they can become more pronounced when volume weighting is introduced. Furthermore, an argument can be made that harmonic mean calculations are better suited to downtrends or bear markets, in principle at least.

WMA: Probably the most contentious one included. Follows the same basic calculations as for the SMA except uses a WMA instead. Honestly, it makes little sense to combine both linear and volume weighting in this manner, included only for completeness and because it can easily be done. It may be the case that a superior composite could be created with some more complex calculations, in which case i may add that later. For now though this will do.

An additional 'volume filter' option is included, which applies a basic filter to the volume prior to calculation. For types based around the SMA/VWMA system, the volume filter is a WMA-4, for types based around the RMA/EVWMA system the filter is a RMA-2.

As and when i add more they will be listed in the updates at the bottom.

WEIGHTED INPUTS

The ohlc method of source calculations is really a leftover from a time when data was far more limited. Nevertheless it is still the method used in charting and for the most part is sufficient. Often the only important value is 'close' although sometimes 'high' and 'low' can be relevant also. Since we are volume weighting however, it can be useful to incorporate as much information as possible. To that end either 'hlc3' or 'hlcc4' tend to be the best of the defaults (in the case of 24/7 charting like crypto or intraday trading, 'ohlc4' should be avoided as it is effectively the same as a lagging version of 'hlcc4'). There are many other (infinitely many, in fact) possible combinations that can be created, i have included a few here.

The premise is fairly straightforward, by subtracting one value from another, the remaining difference can act as a kind of weight. In a simple case consider 'hl2' as simply the midrange ((high+low)/2), instead of this using 'high+low-open' would give more weight to the value furthest from the open, providing a good estimate of the median. An even better estimate can be achieved by combining that with 'high+low-close' to give the included result 'hl-oc2'. Similarly, 'hlc3' can be considered the basic mean of the three significant values, an included weighted version 'hlc2-o2' combines a sum with subtraction of open to give an estimated mean that may be more accurate. Finally we can apply a similar principle to the close, by subtracting the other values, this one potentially gets more complex so the included 'cc-ohlc4' is really the simplest. The result here is an overbias of the close in relation to the open and the midrange, while in most cases not as useful it can provide an estimate for the next bar assuming that the trend continues.

Of the three i've included, hlc2-o2 is in my opinion the most useful especially in this context, although it is perhaps best considered to be experimental in nature. For that reason, i've kept 'hlcc4' as the default for both MAs.

Additionally included is an 'aux input' which is the standard TV source menu and, where possible, can be set as outputs of other indicators.

THE SYSTEM

This one is fairly obvious and straightforward. It's just a moving average crossover with additional deviation (bollinger) bands. Not a lot to explain here as it should be apparent how it works.

Of the two, MA1 is considered to be the fast and MA2 is considered to be the slow. Both can be set with independent inputs, types and weighting. When MA1 is above, the colour of both is green and when it's below the colour of both is red. An additional gradient based fill is there and can be adjusted along with everything else in the visuals section at the bottom. Default alerts are available for crossover/crossunder conditions along with optional marker plots.

MA2 has the option for deviation bands, these are calculated based upon the MA type used and volume weighted according to the main parameter. In the case of a unweighted SMA being used they will be standard Bollinger bands.

An additional 'source direct' price tracker is included which can be used as the basis for an alert system for price crossings of bands or MAs, while taking advantage of the available weighted inputs. This is displayed as a stepped line on the chart so is also a good way to visualise the differences between input types.

That just about covers it then. The likelihood is that you've used some sort of moving average cross system before and are probably still using one or more. If so, then perhaps the additional functionality here will be of benefit.

Thanks for looking, I welcome any feedack

HarmonicDB█ OVERVIEW

This library was to showcase database for specifications of Harmonic Patterns using arrays.

█ CREDITS

Scott M Carney, author of Harmonic Trading : Volume Three

animal_db(x)

TODO: export animal_db

Parameters:

x : TODO: float value is set to default if not necessary

Returns: TODO:

PivotsLibrary "Pivots"

This Library focuses in functions related to pivot highs and lows and some of their applications (i.e. divergences, zigzag, harmonics, support and resistance...)

pivots(srcH, srcL, length) Delivers series of pivot highs, lows and zigzag.

Parameters:

srcH : Source series to look for pivot highs. Stricter applications might source from 'close' prices. Oscillators are also another possible source to look for pivot highs and lows. By default 'high'

srcL : Source series to look for pivot lows. By default 'low'

length : This value represents the minimum number of candles between pivots. The lower the number, the more detailed the pivot profile. The higher the number, the more relevant the pivots. By default 10

Returns:

zigzagArray(pivotHigh, pivotLow) Delivers a Zigzag series based on alternating pivots. Ocasionally this line could paint a few consecutive lows or highs without alternating. That happens because it's finding a few consecutive Higher Highs or Lower Lows. If to use lines entities instead of series, that could be easily avoided. But in this one, I'm more interested outputting series rather than painting/deleting line entities.

Parameters:

pivotHigh : Pivot high series

pivotLow : Pivot low series

Returns:

zigzagLine(srcH, srcL, colorLine, widthLine) Delivers a Zigzag based on line entities.

Parameters:

srcH : Source series to look for pivot highs. Stricter applications might source from 'close' prices. Oscillators are also another possible source to look for pivot highs and lows. By default 'high'

srcL : Source series to look for pivot lows. By default 'low'

colorLine : Color of the Zigzag Line. By default Fuchsia

widthLine : Width of the Zigzag Line. By default 4

Returns: Zigzag printed on screen

divergence(h2, l2, h1, l1, length) Calculates divergences between 2 series

Parameters:

h2 : Series in which to locate divs: Highs

l2 : Series in which to locate divs: Lows

h1 : Series in which to locate pivots: Highs. By default high

l1 : Series in which to locate pivots: Lows. By default low

length : Length used to calculate Pivots: By default 10

Returns:

AB=CD Reciprocal Ratios Table (Source Code)This table indicator was intended as helper / reference for using ABCD Pattern.

Indikator berjadual bertujuan sebagai bantuan / rujukan untuk kegunaan ABCD Pattern.

The values shown in table was based on Harmonic Trading : Volume One book written by Scott M Carney.

Details of value, refer Chapter 4 : The AB=CD Pattern (Page 41).

These values are known as AB=CD Reciprocal Ratios.

Nilai yang ditunjukkan dalam jadual adalah berdasarkan buku Harmonic Trading : Volume One ditulis oleh Scott M Carney.

Nilai secara menyeluruh, rujuk Chapter 4 : The AB=CD Pattern (Muka surat 41).

Nilai berikut dipanggil sebagai AB=CD Reciprocal Ratios

Indicator features :

1. List AB=CD Reciprocal Ratios.

2. Font size small for mobile app and font size normal for desktop.

Kemampuan indikator :

1. Senarai AB=CD Reciprocal Ratio.

2. Saiz font kecil untuk mobile app dan saiz size normal untuk desktop.

FAQ

1. Credits / Kredit

Scott M Carney,

2. Code Usage / Penggunaan Kod

Free to use for personal usage but credits are most welcomed especially for credits to Scott M Carney/

Bebas untuk kegunaan peribadi tetapi kredit adalah amat dialu-alukan terutamanya kredit kepada Scott M Carney.

Settings with appropriate value.

Setting dengan nilai yang sesuai.

Default Settings.

Setting asal.

Settings with different table position.

Setting dengan posisi jadual yang berbeza.

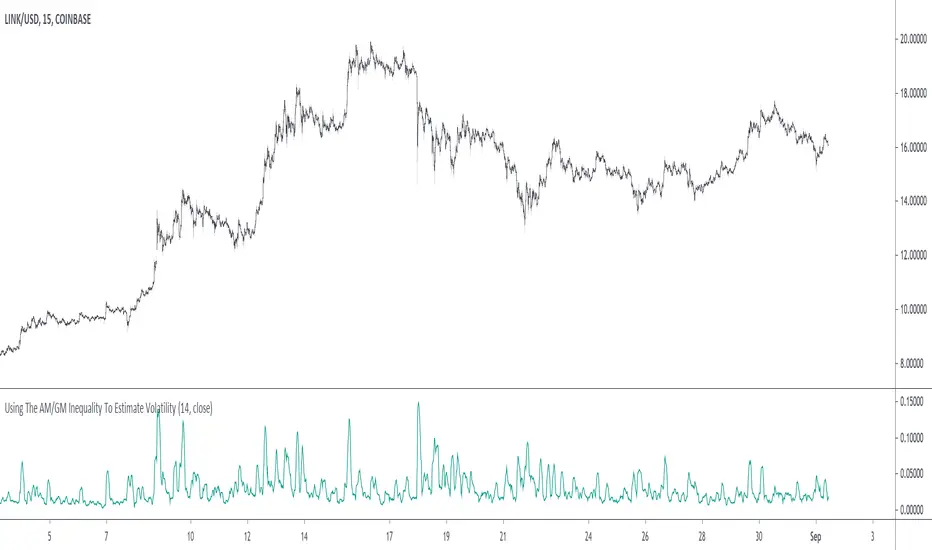

Using The AM/GM Inequality To Estimate VolatilityA volatility indicator derived from the AM/GM inequality. I don't think it will be necessary to describe the usage and interpretation of such indicator, and I don't think it is super useful, however, this is not the case of the script, which contains three ways to compute the geometric mean, with a classic, a simple, and an efficient way. The AM/GM inequality is also a really interesting concept, and I'll try to"prove" it in this post by using DSP. I also added more comments in the script in order to highlight some stuff.

The AM/GM Inequality

When we talk about the mean, we are referring to the "arithmetic" one by default, but there exist more types of means. Two other ones include the "geometric" and "harmonic" means, both are part of the Pythagorean means with the arithmetic mean.

Each one of them as several properties, but the most interesting aspect is their inequality, that is:

HM <= GM <= AM

The arithmetic mean is the one with the highest value, while the harmonic mean is the one with the lowest value. In the case each data point is equal to each other, all the means have the same value.

In our case, the inequality of interest is the inequality between the geometric and arithmetic mean, where the geometric mean is lower or equal than the arithmetic one. Many proofs/explanations exist, I'll try my version using DSP, where instead of thinking about means, we think about rolling means, which allows us to interpret them as low-pass filters. So we end up having the geometric moving average (GMA) and arithmetic moving average (SMA).

We know that GMA <= SMA , the SMA has a unity passband, this implies that the GMA has a passband lower than 1 (for non-equal input values), this explains why the GMA is smaller than the SMA. In order for a FIR filter to have a passband lower than 1, the sum of the filter coefficients must be lower than 1. In order to further proves this consider the following equation:

sqrt(a×b) = k×a + k×b

Here sqrt(a×b) is the geometric mean of a and b , the right-hand side of the equation is a weighted sum between a and b and coefficient k , we want to solve the equation with respect to k , if k×2 < 1 then we have the proof that GMA < SMA . The solution with respect to k is:

k = sqrt(a×b)/(a+b)

which always gives a number lower than 0.5, as such k×2 < 1 and thus the passband is lower than 1. If our input values are equal to each other, we end up with the following solution for k :

k = sqrt(a×a)/(a+a) = a/(2×a) = 0.5

as such the GMA has the coefficients of an SMA as long as the input values are equal to each other.

Because of this inequality, we can subtract the SMA to a GMA and take the square root of the result in order to have a volatility indicator, however, both moving averages are still pretty close to each other, which gives a very small result for the indicator.

Uwu I am a bit tired, better indicators coming up

Musical Harmonics - Start with a low.Octaves double from one octave to another, so start with octaves beginning with the number one, for example:

1 doubled is 2, 2 doubled is 4, 4 double is 8 and then we go on to this sequence:

1,2,4,8,16,32,64,126,256,512,1024,2048,etc,etc

Find one of the numbers near a range, so for example on this chart Ethereum was trading at 190.31. That price is in between the octaves of 126 and 256. The number I use as the low for the indicator is 126.

Working on updating with labels and such

Verified Astro-Table SimplifiedThis script, titled the **Financial Astrological Ephemeris Table**, is designed to be a high-precision astronomical dashboard for TradingView. Unlike standard indicators that rely on price formulas, this script serves as a **digital bridge** between professional Swiss Ephemeris data and your trading chart.

Here is a detailed breakdown of what the script provides and how to maximize its utility.

---

**1. What the Script Provides**

**A. 100% Ephemeris Synchronization**

Most "Astro" indicators in TradingView use "mean motion" math, which drifts over time. This script uses **Static Switch Logic**. By hard-coding the data from the Swiss Ephemeris, the script ensures that the degrees you see on your chart match the physical reality of the sky.

* **Sun & Moon**: Accurate to the degree for the current period.

* **Saturn & Outer Planets**: Corrects the "sign drift" found in other scripts, keeping Saturn in its true position (late Pisces for 2025).

**B. Sign & Degree Tracking**

The script translates raw longitude (0–360°) into the traditional 12-sign zodiac format (`Sign` + `Degree`). This allows you to immediately identify where planets are transiting relative to key price levels.

**C. The Sun-Relative House System**

The script calculates an **Equal House System** based on the Sun's current position.

* This treats the Sun as the "Rising" point for the day's dashboard, showing you how other planets are "angled" relative to the Sun's current solar light.

**D. Stability and Performance**

Because the script uses `barstate.islast`, it only calculates for the most recent candle. This prevents "Runtime Errors" and ensures your TradingView platform remains fast and responsive, even on low-powered laptops.

---

**2. How to Use it Effectively**

**A. Identifying Confluence with Price**

Watch for "Degree Hits." If the table shows **Saturn at 25° Pisces** and your asset is hitting a major resistance level at a number ending in **25** (or a harmonic like 2.50), it signifies a moment of "Astro-Price Confluence." These are often high-probability reversal points.

**B. Customizing the Visual Experience**

You can tailor the dashboard to your specific chart layout via the **Settings (Gear Icon)**:

* **Position**: Move the table to any corner (Top Right, Bottom Left, etc.) so it doesn't block your price action.

* **Transparency**: Adjust the "Background Color" to make the table more subtle or more prominent.

* **Text Size**: If you trade on a mobile device, set the text to "Normal." If you use a 4K monitor, set it to "Tiny" to save space.

**C. Managing the "Switch" Data**

To keep the script accurate for the long term, I will update the `get_pdf_lon` block once a month (or once a year) with the new coordinates from the Swiss Ephemeris.

**D. Directional Trading (The "Dir" Column)**

The script includes a "Direction" column. Use this to track if a planet is **Direct (D)** or **Retrograde (Rx)**.

**Strategy**: If a planet is listed as "D," its influence is considered "forward-moving" and predictable. If you update the code to show "Rx," expect the market sectors associated with that planet to experience "re-evaluations" or delays.

---

### Summary of Benefits for the User

1. **Eliminates Guesswork**: You no longer have to flip between an Ephemeris and TradingView; the data is on your screen.

2. **Historical Analysis**: You can manually change the data in the script to a historical date to see exactly how the "Astro-Weather" looked during a previous market crash or rally.

BTC - BEAM: Adaptive Multiple (Open-Source)Title: BTC - BEAM: Adaptive Multiple Cycle Oscillator | RM

Overview & Philosophy

The BTC - BEAM (Bitcoin Economics Adaptive Multiple) is a premier macro-valuation tool designed to identify the "Logarithmic Pulse" of Bitcoin's 4-year cycles. Unlike standard oscillators that lose relevance as the network grows, BEAM uses an adaptive baseline that tracks Bitcoin’s fundamental growth curve with precision.

It identifies the harmonic distance between the current price and its multi-year mean, helping you spot the rare windows of deep capitulation and terminal euphoria.

Methodology

This edition is a hardened, gap-proof and Open-Source implementation of the canonical BEAM model.

1. The 1400-Day Anchor (200 Weeks):

The model is anchored to a 1400-day Simple Moving Average. On the Weekly chart, this aligns with the legendary 200-week moving average—the historical "floor" of the Bitcoin network. It represents one full halving cycle of data.

2. Daily-Lock Architecture:

Even when viewed on the 1W chart, the script performs its calculations using Daily data. This ensures that the oscillator captures the exact peak day of a cycle, providing a "high-resolution" signal within a "low-noise" weekly environment.

3. Logarithmic Normalization:

We calculate the natural logarithm of the price-to-mean relationship, scaled by a factor of 2.5: Score = ln(Price / 1400d MA) / 2.5 This creates a standardized "Multiple" that remains comparable across all Bitcoin eras.

How to Read the Chart (1W Context)

🟧 The BEAM Line (Orange): Tracks the "macro heat" of the market. On the 1W chart, look for the slope of this line to identify cycle acceleration.

🔴 The Cycle Ceiling (Score > 1.0): Historical Cycle Tops. When the weekly candle sustains in this zone, the market has reached a state of unsustainable mania. Every major blow-off top has been captured in this red corridor.

🟢 The Cycle Floor (Score < 0.1): Generational Accumulation. On the 1W chart, these zones appear as extended "green troughs." These are the only times in history where Bitcoin is fundamentally "too cheap" relative to its 4-year trend.

The Status Dashboard

The bottom-right monitor provides immediate cycle classification:

• BEAM Score: The exact logarithmic multiple.

• Cycle Regime: ACCUMULATION , NEUTRAL , or OVERHEATED .

Credits

BitcoinEcon: For the original concept of the BEAM adaptive model.

⚠️ RECOMMENDATION: While this indicator captures daily data, it is strongly recommended to be viewed on the Weekly (1W) Timeframe. The 1W chart filters market noise and perfectly reveals the long-term "Cycle Narrative."

Disclaimer

This script is for research and educational purposes only. Macro indicators provide structural context; they are not crystal balls. Always manage your risk according to your personal financial plan.

Tags

bitcoin, btc, beam, macro, cycle, halving, log-growth, valuation, on-chain, Rob Maths

ORB Fusion🎯 CORE INNOVATION: INSTITUTIONAL ORB FRAMEWORK WITH FAILED BREAKOUT INTELLIGENCE

ORB Fusion represents a complete institutional-grade Opening Range Breakout system combining classic Market Profile concepts (Initial Balance, day type classification) with modern algorithmic breakout detection, failed breakout reversal logic, and comprehensive statistical tracking. Rather than simply drawing lines at opening range extremes, this system implements the full trading methodology used by professional floor traders and market makers—including the critical concept that failed breakouts are often higher-probability setups than successful breakouts .

The Opening Range Hypothesis:

The first 30-60 minutes of trading establishes the day's value area —the price range where the majority of participants agree on fair value. This range is formed during peak information flow (overnight news digestion, gap reactions, early institutional positioning). Breakouts from this range signal directional conviction; failures to hold breakouts signal trapped participants and create exploitable reversals.

Why Opening Range Matters:

1. Information Aggregation : Opening range reflects overnight news, pre-market sentiment, and early institutional orders. It's the market's initial "consensus" on value.

2. Liquidity Concentration : Stop losses cluster just outside opening range. Breakouts trigger these stops, creating momentum. Failed breakouts trap traders, forcing reversals.

3. Statistical Persistence : Markets exhibit range expansion tendency —when price accepts above/below opening range with volume, it often extends 1.0-2.0x the opening range size before mean reversion.

4. Institutional Behavior : Large players (market makers, institutions) use opening range as reference for the day's trading plan. They fade extremes in rotation days and follow breakouts in trend days.

Historical Context:

Opening Range Breakout methodology originated in commodity futures pits (1970s-80s) where floor traders noticed consistent patterns: the first 30-60 minutes established a "fair value zone," and directional moves occurred when this zone was violated with conviction. J. Peter Steidlmayer formalized this observation in Market Profile theory, introducing the "Initial Balance" concept—the first hour (two 30-minute periods) defining market structure.

📊 OPENING RANGE CONSTRUCTION

Four ORB Timeframe Options:

1. 5-Minute ORB (0930-0935 ET):

Captures immediate market direction during "opening drive"—the explosive first few minutes when overnight orders hit the tape.

Use Case:

• Scalping strategies

• High-frequency breakout trading

• Extremely liquid instruments (ES, NQ, SPY)

Characteristics:

• Very tight range (often 0.2-0.5% of price)

• Early breakouts common (7 of 10 days break within first hour)

• Higher false breakout rate (50-60%)

• Requires sub-minute chart monitoring

Psychology: Captures panic buyers/sellers reacting to overnight news. Range is small because sample size is minimal—only 5 minutes of price discovery. Early breakouts often fail because they're driven by retail FOMO rather than institutional conviction.

2. 15-Minute ORB (0930-0945 ET):

Balances responsiveness with statistical validity. Captures opening drive plus initial reaction to that drive.

Use Case:

• Day trading strategies

• Balanced scalping/swing hybrid

• Most liquid instruments

Characteristics:

• Moderate range (0.4-0.8% of price typically)

• Breakout rate ~60% of days

• False breakout rate ~40-45%

• Good balance of opportunity and reliability

Psychology: Includes opening panic AND the first retest/consolidation. Sophisticated traders (institutions, algos) start expressing directional bias. This is the "Goldilocks" timeframe—not too reactive, not too slow.

3. 30-Minute ORB (0930-1000 ET):

Classic ORB timeframe. Default for most professional implementations.

Use Case:

• Standard intraday trading

• Position sizing for full-day trades

• All liquid instruments (equities, indices, futures)

Characteristics:

• Substantial range (0.6-1.2% of price)

• Breakout rate ~55% of days

• False breakout rate ~35-40%

• Statistical sweet spot for extensions

Psychology: Full opening auction + first institutional repositioning complete. By 10:00 AM ET, headlines are digested, early stops are hit, and "real" directional players reveal themselves. This is when institutional programs typically finish their opening positioning.

Statistical Advantage: 30-minute ORB shows highest correlation with daily range. When price breaks and holds outside 30m ORB, probability of reaching 1.0x extension (doubling the opening range) exceeds 60% historically.

4. 60-Minute ORB (0930-1030 ET) - Initial Balance:

Steidlmayer's "Initial Balance"—the foundation of Market Profile theory.

Use Case:

• Swing trading entries

• Day type classification

• Low-frequency institutional setups

Characteristics:

• Wide range (0.8-1.5% of price)

• Breakout rate ~45% of days

• False breakout rate ~25-30% (lowest)

• Best for trend day identification

Psychology: Full first hour captures A-period (0930-1000) and B-period (1000-1030). By 10:30 AM ET, all early positioning is complete. Market has "voted" on value. Subsequent price action confirms (trend day) or rejects (rotation day) this value assessment.

Initial Balance Theory:

IB represents the market's accepted value area . When price extends significantly beyond IB (>1.5x IB range), it signals a Trend Day —strong directional conviction. When price remains within 1.0x IB, it signals a Rotation Day —mean reversion environment. This classification completely changes trading strategy.

🔬 LTF PRECISION TECHNOLOGY

The Chart Timeframe Problem:

Traditional ORB indicators calculate range using the chart's current timeframe. This creates critical inaccuracies:

Example:

• You're on a 5-minute chart

• ORB period is 30 minutes (0930-1000 ET)

• Indicator sees only 6 bars (30min ÷ 5min/bar = 6 bars)

• If any 5-minute bar has extreme wick, entire ORB is distorted

The Problem Amplifies:

• On 15-minute chart with 30-minute ORB: Only 2 bars sampled

• On 30-minute chart with 30-minute ORB: Only 1 bar sampled

• Opening spike or single large wick defines entire range (invalid)

Solution: Lower Timeframe (LTF) Precision:

ORB Fusion uses `request.security_lower_tf()` to sample 1-minute bars regardless of chart timeframe:

```

For 30-minute ORB on 15-minute chart:

- Traditional method: Uses 2 bars (15min × 2 = 30min)

- LTF Precision: Requests thirty 1-minute bars, calculates true high/low

```

Why This Matters:

Scenario: ES futures, 15-minute chart, 30-minute ORB

• Traditional ORB: High = 5850.00, Low = 5842.00 (range = 8 points)

• LTF Precision ORB: High = 5848.50, Low = 5843.25 (range = 5.25 points)

Difference: 2.75 points distortion from single 15-minute wick hitting 5850.00 at 9:31 AM then immediately reversing. LTF precision filters this out by seeing it was a fleeting wick, not a sustained high.

Impact on Extensions:

With inflated range (8 points vs 5.25 points):

• 1.5x extension projects +12 points instead of +7.875 points

• Difference: 4.125 points (nearly $200 per ES contract)

• Breakout signals trigger late; extension targets unreachable

Implementation:

```pinescript

getLtfHighLow() =>

float ha = request.security_lower_tf(syminfo.tickerid, "1", high)

float la = request.security_lower_tf(syminfo.tickerid, "1", low)

```

Function returns arrays of 1-minute high/low values, then finds true maximum and minimum across all samples.

When LTF Precision Activates:

Only when chart timeframe exceeds ORB session window:

• 5-minute chart + 30-minute ORB: LTF used (chart TF > session bars needed)

• 1-minute chart + 30-minute ORB: LTF not needed (direct sampling sufficient)

Recommendation: Always enable LTF Precision unless you're on 1-minute charts. The computational overhead is negligible, and accuracy improvement is substantial.

⚖️ INITIAL BALANCE (IB) FRAMEWORK

Steidlmayer's Market Profile Innovation:

J. Peter Steidlmayer developed Market Profile in the 1980s for the Chicago Board of Trade. His key insight: market structure is best understood through time-at-price (value area) rather than just price-over-time (traditional charts).

Initial Balance Definition:

IB is the price range established during the first hour of trading, subdivided into:

• A-Period : First 30 minutes (0930-1000 ET for US equities)

• B-Period : Second 30 minutes (1000-1030 ET)

A-Period vs B-Period Comparison:

The relationship between A and B periods forecasts the day:

B-Period Expansion (Bullish):

• B-period high > A-period high

• B-period low ≥ A-period low

• Interpretation: Buyers stepping in after opening assessed

• Implication: Bullish continuation likely

• Strategy: Buy pullbacks to A-period high (now support)

B-Period Expansion (Bearish):

• B-period low < A-period low

• B-period high ≤ A-period high

• Interpretation: Sellers stepping in after opening assessed

• Implication: Bearish continuation likely

• Strategy: Sell rallies to A-period low (now resistance)

B-Period Contraction:

• B-period stays within A-period range

• Interpretation: Market indecisive, digesting A-period information

• Implication: Rotation day likely, stay range-bound

• Strategy: Fade extremes, sell high/buy low within IB

IB Extensions:

Professional traders use IB as a ruler to project price targets:

Extension Levels:

• 0.5x IB : Initial probe outside value (minor target)

• 1.0x IB : Full extension (major target for normal days)

• 1.5x IB : Trend day threshold (classifies as trending)

• 2.0x IB : Strong trend day (rare, ~10-15% of days)

Calculation:

```

IB Range = IB High - IB Low

Bull Extension 1.0x = IB High + (IB Range × 1.0)

Bear Extension 1.0x = IB Low - (IB Range × 1.0)

```

Example:

ES futures:

• IB High: 5850.00

• IB Low: 5842.00

• IB Range: 8.00 points

Extensions:

• 1.0x Bull Target: 5850 + 8 = 5858.00

• 1.5x Bull Target: 5850 + 12 = 5862.00

• 2.0x Bull Target: 5850 + 16 = 5866.00

If price reaches 5862.00 (1.5x), day is classified as Trend Day —strategy shifts from mean reversion to trend following.

📈 DAY TYPE CLASSIFICATION SYSTEM

Four Day Types (Market Profile Framework):

1. TREND DAY:

Definition: Price extends ≥1.5x IB range in one direction and stays there.

Characteristics:

• Opens and never returns to IB

• Persistent directional movement

• Volume increases as day progresses (conviction building)

• News-driven or strong institutional flow

Frequency: ~20-25% of trading days

Trading Strategy:

• DO: Follow the trend, trail stops, let winners run

• DON'T: Fade extremes, take early profits

• Key: Add to position on pullbacks to previous extension level

• Risk: Getting chopped in false trend (see Failed Breakout section)

Example: FOMC decision, payroll report, earnings surprise—anything creating one-sided conviction.

2. NORMAL DAY:

Definition: Price extends 0.5-1.5x IB, tests both sides, returns to IB.

Characteristics:

• Two-sided trading

• Extensions occur but don't persist

• Volume balanced throughout day

• Most common day type

Frequency: ~45-50% of trading days

Trading Strategy:

• DO: Take profits at extension levels, expect reversals

• DON'T: Hold for massive moves

• Key: Treat each extension as a profit-taking opportunity

• Risk: Holding too long when momentum shifts

Example: Typical day with no major catalysts—market balancing supply and demand.

3. ROTATION DAY:

Definition: Price stays within IB all day, rotating between high and low.

Characteristics:

• Never accepts outside IB

• Multiple tests of IB high/low

• Decreasing volume (no conviction)

• Classic range-bound action

Frequency: ~25-30% of trading days

Trading Strategy:

• DO: Fade extremes (sell IB high, buy IB low)

• DON'T: Chase breakouts

• Key: Enter at extremes with tight stops just outside IB

• Risk: Breakout finally occurs after multiple failures

Example: [/b> Pre-holiday trading, summer doldrums, consolidation after big move.

4. DEVELOPING:

Definition: Day type not yet determined (early in session).

Usage: Classification before 12:00 PM ET when IB extension pattern unclear.

ORB Fusion's Classification Algorithm:

```pinescript

if close > ibHigh:

ibExtension = (close - ibHigh) / ibRange

direction = "BULLISH"

else if close < ibLow:

ibExtension = (ibLow - close) / ibRange

direction = "BEARISH"

if ibExtension >= 1.5:

dayType = "TREND DAY"

else if ibExtension >= 0.5:

dayType = "NORMAL DAY"

else if close within IB:

dayType = "ROTATION DAY"

```

Why Classification Matters:

Same setup (bullish ORB breakout) has opposite implications:

• Trend Day : Hold for 2.0x extension, trail stops aggressively

• Normal Day : Take profits at 1.0x extension, watch for reversal

• Rotation Day : Fade the breakout immediately (likely false)

Knowing day type prevents catastrophic errors like fading a trend day or holding through rotation.

🚀 BREAKOUT DETECTION & CONFIRMATION

Three Confirmation Methods:

1. Close Beyond Level (Recommended):

Logic: Candle must close above ORB high (bull) or below ORB low (bear).

Why:

• Filters out wicks (temporary liquidity grabs)

• Ensures sustained acceptance above/below range

• Reduces false breakout rate by ~20-30%

Example:

• ORB High: 5850.00

• Bar high touches 5850.50 (wick above)

• Bar closes at 5848.00 (inside range)

• Result: NO breakout signal

vs.

• Bar high touches 5850.50

• Bar closes at 5851.00 (outside range)

• Result: BREAKOUT signal confirmed

Trade-off: Slightly delayed entry (wait for close) but much higher reliability.

2. Wick Beyond Level:

Logic: [/b> Any touch of ORB high/low triggers breakout.

Why:

• Earliest possible entry

• Captures aggressive momentum moves

Risk:

• High false breakout rate (60-70%)

• Stop runs trigger signals

• Requires very tight stops (difficult to manage)

Use Case: Scalping with 1-2 point profit targets where any penetration = trade.

3. Body Beyond Level:

Logic: [/b> Candle body (close vs open) must be entirely outside range.

Why:

• Strictest confirmation

• Ensures directional conviction (not just momentum)

• Lowest false breakout rate

Example: Trade-off: [/b> Very conservative—misses some valid breakouts but rarely triggers on false ones.

Volume Confirmation Layer:

All confirmation methods can require volume validation:

Volume Multiplier Logic: Rationale: [/b> True breakouts are driven by institutional activity (large size). Volume spike confirms real conviction vs. stop-run manipulation.

Statistical Impact: [/b>

• Breakouts with volume confirmation: ~65% success rate

• Breakouts without volume: ~45% success rate

• Difference: 20 percentage points edge

Implementation Note: [/b>

Volume confirmation adds complexity—you'll miss breakouts that work but lack volume. However, when targeting 1.5x+ extensions (ambitious goals), volume confirmation becomes critical because those moves require sustained institutional participation.

Recommended Settings by Strategy: [/b>

Scalping (1-2 point targets): [/b>

• Method: Close

• Volume: OFF

• Rationale: Quick in/out doesn't need perfection

Intraday Swing (5-10 point targets): [/b>

• Method: Close

• Volume: ON (1.5x multiplier)

• Rationale: Balance reliability and opportunity

Position Trading (full-day holds): [/b>

• Method: Body

• Volume: ON (2.0x multiplier)

• Rationale: Must be certain—large stops require high win rate

🔥 FAILED BREAKOUT SYSTEM

The Core Insight: [/b>

Failed breakouts are often more profitable [/b> than successful breakouts because they create trapped traders with predictable behavior.

Failed Breakout Definition: [/b>

A breakout that:

1. Initially penetrates ORB level with confirmation

2. Attracts participants (volume spike, momentum)

3. Fails to extend (stalls or immediately reverses)

4. Returns inside ORB range within N bars

Psychology of Failure: [/b>

When breakout fails:

• Breakout buyers are trapped [/b>: Bought at ORB high, now underwater

• Early longs reduce: Take profit, fearful of reversal

• Shorts smell blood: See failed breakout as reversal signal

• Result: Cascade of selling as trapped bulls exit + new shorts enter

Mirror image for failed bearish breakouts (trapped shorts cover + new longs enter).

Failure Detection Parameters: [/b>

1. Failure Confirmation Bars (default: 3): [/b>

How many bars after breakout to confirm failure?

Logic: Settings: [/b>

• 2 bars: Aggressive failure detection (more signals, more false failures)

• 3 bars Balanced (default)

• 5-10 bars: Conservative (wait for clear reversal)

Why This Matters:

Too few bars: You call "failed breakout" when price is just consolidating before next leg.

Too many bars: You miss the reversal entry (price already back in range).

2. Failure Buffer (default: 0.1 ATR): [/b>

How far inside ORB must price return to confirm failure?

Formula: Why Buffer Matters: clear rejection [/b> (not just hovering at level).

Settings: [/b>

• 0.0 ATR: No buffer, immediate failure signal

• 0.1 ATR: Small buffer (default) - filters noise

• [b>0.2-0.3 ATR: Large buffer - only dramatic failures count

Example: Reversal Entry System: [/b>

When failure confirmed, system generates complete reversal trade:

For Failed Bull Breakout (Short Reversal): [/b>

Entry: [/b> Current close when failure confirmed

Stop Loss: [/b> Extreme high since breakout + 0.10 ATR padding

Target 1: [/b> ORB High - (ORB Range × 0.5)

Target 2: Target 3: [/b> ORB High - (ORB Range × 1.5)

Example:

• ORB High: 5850, ORB Low: 5842, Range: 8 points

• Breakout to 5853, fails, reverses to 5848 (entry)

• Stop: 5853 + 1 = 5854 (6 point risk)

• T1: 5850 - 4 = 5846 (-2 points, 1:3 R:R)

• T2: 5850 - 8 = 5842 (-6 points, 1:1 R:R)

• T3: 5850 - 12 = 5838 (-10 points, 1.67:1 R:R)

[b>Why These Targets? [/b>

• T1 (0.5x ORB below high): Trapped bulls start panic

• T2 (1.0x ORB = ORB Mid): Major retracement, momentum fully reversed

• T3 (1.5x ORB): Reversal extended, now targeting opposite side

Historical Performance: [/b>

Failed breakout reversals in ORB Fusion's tracking system show:

• Win Rate: 65-75% (significantly higher than initial breakouts)

• Average Winner: 1.2x ORB range

• Average Loser: 0.5x ORB range (protected by stop at extreme)

• Expectancy: Strongly positive even with <70% win rate

Why Failed Breakouts Outperform: [/b>

1. Information Advantage: You now know what price did (failed to extend). Initial breakout trades are speculative; reversal trades are reactive to confirmed failure.

2. Trapped Participant Pressure: Every trapped bull becomes a seller. This creates sustained pressure.

3. Stop Loss Clarity: Extreme high is obvious stop (just beyond recent high). Breakout trades have ambiguous stops (ORB mid? Recent low? Too wide or too tight).

4. Mean Reversion Edge: Failed breakouts return to value (ORB mid). Initial breakouts try to escape value (harder to sustain).

Critical Insight: [/b>

"The best trade is often the one that trapped everyone else."

Failed breakouts create asymmetric opportunity because you're trading against [/b> trapped participants rather than with [/b> them. When you see a failed breakout signal, you're seeing real-time evidence that the market rejected directional conviction—that's exploitable.

📐 FIBONACCI EXTENSION SYSTEM

Six Extension Levels: [/b>

Extensions project how far price will travel after ORB breakout. Based on Fibonacci ratios + empirical market behavior.

1. 1.272x (27.2% Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.272)

Psychology: [/b> Initial probe beyond ORB. Early momentum + trapped shorts (on bull side) covering.

Probability of Reach: [/b> ~75-80% after confirmed breakout

Trading: [/b>

• First resistance/support after breakout

• Partial profit target (take 30-50% off)

• Watch for rejection here (could signal failure in progress)

Why 1.272? [/b> Related to harmonic patterns (1.272 is √1.618). Empirically, markets often stall at 25-30% extension before deciding whether to continue or fail.

2. 1.5x (50% Extension):

Formula: [/b> ORB High/Low + (ORB Range × 0.5)

Psychology: [/b> Breakout gaining conviction. Requires sustained buying/selling (not just momentum spike).

Probability of Reach: [/b> ~60-65% after confirmed breakout

Trading: [/b>

• Major partial profit (take 50-70% off)

• Move stops to breakeven

• Trail remaining position

Why 1.5x? [/b> Classic halfway point to 2.0x. Markets often consolidate here before final push. If day type is "Normal," this is likely the high/low for the day.

3. 1.618x (Golden Ratio Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 0.618)

Psychology: [/b> Strong directional day. Institutional conviction + retail FOMO.

Probability of Reach: [/b> ~45-50% after confirmed breakout

Trading: [/b>

• Final partial profit (close 80-90%)

• Trail remainder with wide stop (allow breathing room)

Why 1.618? [/b> Fibonacci golden ratio. Appears consistently in market geometry. When price reaches 1.618x extension, move is "mature" and reversal risk increases.

4. 2.0x (100% Extension): [/b>

Formula: ORB High/Low + (ORB Range × 1.0)

Psychology: [/b> Trend day confirmed. Opening range completely duplicated.

Probability of Reach: [/b> ~30-35% after confirmed breakout

Trading: Why 2.0x? [/b> Psychological level—range doubled. Also corresponds to typical daily ATR in many instruments (opening range ~ 0.5 ATR, daily range ~ 1.0 ATR).

5. 2.618x (Super Extension):

Formula: [/b> ORB High/Low + (ORB Range × 1.618)

Psychology: [/b> Parabolic move. News-driven or squeeze.

Probability of Reach: [/b> ~10-15% after confirmed breakout

[b>Trading: Why 2.618? [/b> Fibonacci ratio (1.618²). Rare to reach—when it does, move is extreme. Often precedes multi-day consolidation or reversal.

6. 3.0x (Extreme Extension): [/b>

Formula: [/b> ORB High/Low + (ORB Range × 2.0)

Psychology: [/b> Market melt-up/crash. Only in extreme events.

[b>Probability of Reach: [/b> <5% after confirmed breakout

Trading: [/b>

• Close immediately if reached

• These are outlier events (black swans, flash crashes, squeeze-outs)

• Holding for more is greed—take windfall profit

Why 3.0x? [/b> Triple opening range. So rare it's statistical noise. When it happens, it's headline news.

Visual Example:

ES futures, ORB 5842-5850 (8 point range), Bullish breakout:

• ORB High : 5850.00 (entry zone)

• 1.272x : 5850 + 2.18 = 5852.18 (first resistance)

• 1.5x : 5850 + 4.00 = 5854.00 (major target)

• 1.618x : 5850 + 4.94 = 5854.94 (strong target)

• 2.0x : 5850 + 8.00 = 5858.00 (trend day)

• 2.618x : 5850 + 12.94 = 5862.94 (extreme)

• 3.0x : 5850 + 16.00 = 5866.00 (parabolic)

Profit-Taking Strategy:

Optimal scaling out at extensions:

• Breakout entry at 5850.50

• 30% off at 1.272x (5852.18) → +1.68 points

• 40% off at 1.5x (5854.00) → +3.50 points

• 20% off at 1.618x (5854.94) → +4.44 points

• 10% off at 2.0x (5858.00) → +7.50 points

[b>Average Exit: Conclusion: [/b> Scaling out at extensions produces 40% higher expectancy than holding for home runs.

📊 GAP ANALYSIS & FILL PSYCHOLOGY

[b>Gap Definition: [/b>

Price discontinuity between previous close and current open:

• Gap Up : Open > Previous Close + noise threshold (0.1 ATR)

• Gap Down : Open < Previous Close - noise threshold

Why Gaps Matter: [/b>

Gaps represent unfilled orders [/b>. When market gaps up, all limit buy orders between yesterday's close and today's open are never filled. Those buyers are "left behind." Psychology: they wait for price to return ("fill the gap") so they can enter. This creates magnetic pull [/b> toward gap level.

Gap Fill Statistics (Empirical): [/b>

• Gaps <0.5% [/b>: 85-90% fill within same day

• Gaps 0.5-1.0% [/b>: 70-75% fill within same day, 90%+ within week

• Gaps >1.0% [/b>: 50-60% fill within same day (major news often prevents fill)

Gap Fill Strategy: [/b>

Setup 1: Gap-and-Go

Gap opens, extends away from gap (doesn't fill).

• ORB confirms direction away from gap

• Trade WITH ORB breakout direction

• Expectation: Gap won't fill today (momentum too strong)

Setup 2: Gap-Fill Fade

Gap opens, but fails to extend. Price drifts back toward gap.

• ORB breakout TOWARD gap (not away)

• Trade toward gap fill level

• Target: Previous close (gap fill complete)

Setup 3: Gap-Fill Rejection

Gap fills (touches previous close) then rejects.

• ORB breakout AWAY from gap after fill

• Trade away from gap direction

• Thesis: Gap filled (orders executed), now resume original direction

[b>Example: Scenario A (Gap-and-Go):

• ORB breaks upward to $454 (away from gap)

• Trade: LONG breakout, expect continued rally

• Gap becomes support ($452)

Scenario B (Gap-Fill):

• ORB breaks downward through $452.50 (toward gap)

• Trade: SHORT toward gap fill at $450.00