loggerLibrary "logger"

◼ Overview

A dual logging library for developers. Tradingview lacks logging capability. This library provides logging while developing your scripts and is to be used by developers when developing and debugging their scripts.

Using this library would potentially slow down you scripts. Hence, use this for debugging only. Once your code is as you would like it to be, remove the logging code.

◼︎ Usage (Console):

Console = A sleek single cell logging with a limit of 4096 characters. When you dont need a large logging capability.

//@version=5

indicator("demo.Console", overlay=true)

plot(na)

import GETpacman/logger/1 as logger

var console = logger.log.new()

console.init() // init() should be called as first line after variable declaration

console.FrameColor:=color.green

console.log('\n')

console.log('\n')

console.log('Hello World')

console.log('\n')

console.log('\n')

console.ShowStatusBar:=true

console.StatusBarAtBottom:=true

console.FrameColor:=color.blue //settings can be changed anytime before show method is called. Even twice. The last call will set the final value

console.ShowHeader:=false //this wont throw error but is not used for console

console.show(position=position.bottom_right) //this should be the last line of your code, after all methods and settings have been dealt with.

◼︎ Usage (Logx):

Logx = Multiple columns logging with a limit of 4096 characters each message. When you need to log large number of messages.

//@version=5

indicator("demo.Logx", overlay=true)

plot(na)

import GETpacman/logger/1 as logger

var logx = logger.log.new()

logx.init() // init() should be called as first line after variable declaration

logx.FrameColor:=color.green

logx.log('\n')

logx.log('\n')

logx.log('Hello World')

logx.log('\n')

logx.log('\n')

logx.ShowStatusBar:=true

logx.StatusBarAtBottom:=true

logx.ShowQ3:=false

logx.ShowQ4:=false

logx.ShowQ5:=false

logx.ShowQ6:=false

logx.FrameColor:=color.olive //settings can be changed anytime before show method is called. Even twice. The last call will set the final value

logx.show(position=position.top_right) //this should be the last line of your code, after all methods and settings have been dealt with.

◼︎ Fields (with default settings)

▶︎ IsConsole = True Log will act as Console if true, otherwise it will act as Logx

▶︎ ShowHeader = True (Log only) Will show a header at top or bottom of logx.

▶︎ HeaderAtTop = True (Log only) Will show the header at the top, or bottom if false, if ShowHeader is true.

▶︎ ShowStatusBar = True Will show a status bar at the bottom

▶︎ StatusBarAtBottom = True Will show the status bar at the bottom, or top if false, if ShowHeader is true.

▶︎ ShowMetaStatus = True Will show the meta info within status bar (Current Bar, characters left in console, Paging On Every Bar, Console dumped data etc)

▶︎ ShowBarIndex = True Logx will show column for Bar Index when the message was logged. Console will add Bar index at the front of logged messages

▶︎ ShowDateTime = True Logx will show column for Date/Time passed with the logged message logged. Console will add Date/Time at the front of logged messages

▶︎ ShowLogLevels = True Logx will show column for Log levels corresponding to error codes. Console will log levels in the status bar

▶︎ ReplaceWithErrorCodes = True (Log only) Logx will show error codes instead of log levels, if ShowLogLevels is switched on

▶︎ RestrictLevelsToKey7 = True Log levels will be restricted to Ley 7 codes - TRACE, DEBUG, INFO, WARNING, ERROR, CRITICAL, FATAL

▶︎ ShowQ1 = True (Log only) Show the column for Q1

▶︎ ShowQ2 = True (Log only) Show the column for Q2

▶︎ ShowQ3 = True (Log only) Show the column for Q3

▶︎ ShowQ4 = True (Log only) Show the column for Q4

▶︎ ShowQ5 = True (Log only) Show the column for Q5

▶︎ ShowQ6 = True (Log only) Show the column for Q6

▶︎ ColorText = True Log/Console will color text as per error codes

▶︎ HighlightText = True Log/Console will highlight text (like denoting) as per error codes

▶︎ AutoMerge = True (Log only) Merge the queues towards the right if there is no data in those queues.

▶︎ PageOnEveryBar = True Clear data from previous bars on each new bar, in conjuction with PageHistory setting.

▶︎ MoveLogUp = True Move log in up direction. Setting to false will push logs down.

▶︎ MarkNewBar = True On each change of bar, add a marker to show the bar has changed

▶︎ PrefixLogLevel = True (Console only) Prefix all messages with the log level corresponding to error code.

▶︎ MinWidth = 40 Set the minimum width needed to be seen. Prevents logx/console shrinking below these number of characters.

▶︎ TabSizeQ1 = 0 If set to more than one, the messages on Q1 or Console messages will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ2 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ3 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ4 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ5 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ TabSizeQ6 = 0 If set to more than one, the messages on Q2 will indent by this size based on error code (Max 4 used)

▶︎ PageHistory = 0 Used with PageOnEveryBar. Determines how many historial pages to keep.

▶︎ HeaderQbarIndex = 'Bar#' (Logx only) The header to show for Bar Index

▶︎ HeaderQdateTime = 'Date' (Logx only) The header to show for Date/Time

▶︎ HeaderQerrorCode = 'eCode' (Logx only) The header to show for Error Codes

▶︎ HeaderQlogLevel = 'State' (Logx only) The header to show for Log Level

▶︎ HeaderQ1 = 'h.Q1' (Logx only) The header to show for Q1

▶︎ HeaderQ2 = 'h.Q2' (Logx only) The header to show for Q2

▶︎ HeaderQ3 = 'h.Q3' (Logx only) The header to show for Q3

▶︎ HeaderQ4 = 'h.Q4' (Logx only) The header to show for Q4

▶︎ HeaderQ5 = 'h.Q5' (Logx only) The header to show for Q5

▶︎ HeaderQ6 = 'h.Q6' (Logx only) The header to show for Q6

▶︎ Status = '' Set the status to this text.

▶︎ HeaderColor Set the color for the header

▶︎ HeaderColorBG Set the background color for the header

▶︎ StatusColor Set the color for the status bar

▶︎ StatusColorBG Set the background color for the status bar

▶︎ TextColor Set the color for the text used without error code or code 0.

▶︎ TextColorBG Set the background color for the text used without error code or code 0.

▶︎ FrameColor Set the color for the frame around Logx/Console

▶︎ FrameSize = 1 Set the size of the frame around Logx/Console

▶︎ CellBorderSize = 0 Set the size of the border around cells.

▶︎ CellBorderColor Set the color for the border around cells within Logx/Console

▶︎ SeparatorColor = gray Set the color of separate in between Console/Logx Attachment

◼︎ Methods (summary)

● init ▶︎ Initialise the log

● log ▶︎ Log the messages. Use method show to display the messages

● page ▶︎ Clear messages from previous bar while logging messages on this bar.

● show ▶︎ Shows a table displaying the logged messages

● clear ▶︎ Clears the log of all messages

● resize ▶︎ Resizes the log. If size is for reduction then oldest messages are lost first.

● turnPage ▶︎ When called, all messages marked with previous page, or from start are cleared

● dateTimeFormat ▶︎ Sets the date time format to be used when displaying date/time info.

● resetTextColor ▶︎ Reset Text Color to library default

● resetTextBGcolor ▶︎ Reset Text BG Color to library default

● resetHeaderColor ▶︎ Reset Header Color to library default

● resetHeaderBGcolor ▶︎ Reset Header BG Color to library default

● resetStatusColor ▶︎ Reset Status Color to library default

● resetStatusBGcolor ▶︎ Reset Status BG Color to library default

● setColors ▶︎ Sets the colors to be used for corresponding error codes

● setColorsBG ▶︎ Sets the background colors to be used for corresponding error codes. If not match of error code, then text color used.

● setColorsHC ▶︎ Sets the highlight colors to be used for corresponding error codes.If not match of error code, then text bg color used.

● resetColors ▶︎ Reset the colors to library default (Total 36, not including error code 0)

● resetColorsBG ▶︎ Reset the background colors to library default

● resetColorsHC ▶︎ Reset the highlight colors to library default

● setLevelNames ▶︎ Set the log level names to be used for corresponding error codes. If not match of error code, then empty string used.

● resetLevelNames ▶︎ Reset the log level names to library default. (Total 36) 1=TRACE, 2=DEBUG, 3=INFO, 4=WARNING, 5=ERROR, 6=CRITICAL, 7=FATAL

● attach ▶︎ Attaches a console to an existing Logx, allowing to have dual logging system independent of each other

● detach ▶︎ Detaches an already attached console from Logx

method clear(this)

Clears all the queue, including bar_index and time queues, of existing messages

Namespace types: log

Parameters:

this (log)

method resize(this, rows)

Resizes the message queues. If size is decreased then removes the oldest messages

Namespace types: log

Parameters:

this (log)

rows (int) : The new size needed for the queues. Default value is 40.

method dateTimeFormat(this, format)

Re/set the date time format used for displaying date and time. Default resets to dd.MMM.yy HH:mm

Namespace types: log

Parameters:

this (log)

format (string)

method resetTextColor(this)

Resets the text color of the log to library default.

Namespace types: log

Parameters:

this (log)

method resetTextColorBG(this)

Resets the background color of the log to library default.

Namespace types: log

Parameters:

this (log)

method resetHeaderColor(this)

Resets the color used for Headers, to library default.

Namespace types: log

Parameters:

this (log)

method resetHeaderColorBG(this)

Resets the background color used for Headers, to library default.

Namespace types: log

Parameters:

this (log)

method resetStatusColor(this)

Resets the text color of the status row, to library default.

Namespace types: log

Parameters:

this (log)

method resetStatusColorBG(this)

Resets the background color of the status row, to library default.

Namespace types: log

Parameters:

this (log)

method resetFrameColor(this)

Resets the color used for the frame around the log table, to library default.

Namespace types: log

Parameters:

this (log)

method resetColorsHC(this)

Resets the color used for the highlighting when Highlight Text option is used, to library default

Namespace types: log

Parameters:

this (log)

method resetColorsBG(this)

Resets the background color used for setting the background color, when the Color Text option is used, to library default

Namespace types: log

Parameters:

this (log)

method resetColors(this)

Resets the color used for respective error codes, when the Color Text option is used, to library default

Namespace types: log

Parameters:

this (log)

method setColors(this, c)

Sets the colors corresponding to error codes

Index 0 of input array c is color is reserved for future use.

Index 1 of input array c is color for debug code 1.

Index 2 of input array c is color for debug code 2.

There are 2 modes of coloring

1 . Using the Foreground color

2 . Using the Foreground color as background color and a white/black/gray color as foreground color

This is denoting or highlighting. Which effectively puts the foreground color as background color

Namespace types: log

Parameters:

this (log)

c (color ) : Array of colors to be used for corresponding error codes. If the corresponding code is not found, then text color is used

method setColorsHC(this, c)

Sets the highlight colors corresponding to error codes

Index 0 of input array c is color is reserved for future use.

Index 1 of input array c is color for debug code 1.

Index 2 of input array c is color for debug code 2.

There are 2 modes of coloring

1 . Using the Foreground color

2 . Using the Foreground color as background color and a white/black/gray color as foreground color

This is denoting or highlighting. Which effectively puts the foreground color as background color

Namespace types: log

Parameters:

this (log)

c (color ) : Array of highlight colors to be used for corresponding error codes. If the corresponding code is not found, then text color BG is used

method setColorsBG(this, c)

Sets the highlight colors corresponding to debug codes

Index 0 of input array c is color is reserved for future use.

Index 1 of input array c is color for debug code 1.

Index 2 of input array c is color for debug code 2.

There are 2 modes of coloring

1 . Using the Foreground color

2 . Using the Foreground color as background color and a white/black/gray color as foreground color

This is denoting or highlighting. Which effectively puts the foreground color as background color

Namespace types: log

Parameters:

this (log)

c (color ) : Array of background colors to be used for corresponding error codes. If the corresponding code is not found, then text color BG is used

method resetLevelNames(this, prefix, suffix)

Resets the log level names used for corresponding error codes

With prefix/suffix, the default Level name will be like => prefix + Code + suffix

Namespace types: log

Parameters:

this (log)

prefix (string) : Prefix to use when resetting level names

suffix (string) : Suffix to use when resetting level names

method setLevelNames(this, names)

Resets the log level names used for corresponding error codes

Index 0 of input array names is reserved for future use.

Index 1 of input array names is name used for error code 1.

Index 2 of input array names is name used for error code 2.

Namespace types: log

Parameters:

this (log)

names (string ) : Array of log level names be used for corresponding error codes. If the corresponding code is not found, then an empty string is used

method init(this, rows, isConsole)

Sets up data for logging. It consists of 6 separate message queues, and 3 additional queues for bar index, time and log level/error code. Do not directly alter the contents, as library could break.

Namespace types: log

Parameters:

this (log)

rows (int) : Log size, excluding the header/status. Default value is 50.

isConsole (bool) : Whether to init the log as console or logx. True= as console, False = as Logx. Default is true, hence init as console.

method log(this, ec, m1, m2, m3, m4, m5, m6, tv, log)

Logs messages to the queues , including, time/date, bar_index, and error code

Namespace types: log

Parameters:

this (log)

ec (int) : Error/Code to be assigned.

m1 (string) : Message needed to be logged to Q1, or for console.

m2 (string) : Message needed to be logged to Q2. Not used/ignored when in console mode

m3 (string) : Message needed to be logged to Q3. Not used/ignored when in console mode

m4 (string) : Message needed to be logged to Q4. Not used/ignored when in console mode

m5 (string) : Message needed to be logged to Q5. Not used/ignored when in console mode

m6 (string) : Message needed to be logged to Q6. Not used/ignored when in console mode

tv (int) : Time to be used. Default value is time, which logs the start time of bar.

log (bool) : Whether to log the message or not. Default is true.

method page(this, ec, m1, m2, m3, m4, m5, m6, tv, page)

Logs messages to the queues , including, time/date, bar_index, and error code. All messages from previous bars are cleared

Namespace types: log

Parameters:

this (log)

ec (int) : Error/Code to be assigned.

m1 (string) : Message needed to be logged to Q1, or for console.

m2 (string) : Message needed to be logged to Q2. Not used/ignored when in console mode

m3 (string) : Message needed to be logged to Q3. Not used/ignored when in console mode

m4 (string) : Message needed to be logged to Q4. Not used/ignored when in console mode

m5 (string) : Message needed to be logged to Q5. Not used/ignored when in console mode

m6 (string) : Message needed to be logged to Q6. Not used/ignored when in console mode

tv (int) : Time to be used. Default value is time, which logs the start time of bar.

page (bool) : Whether to log the message or not. Default is true.

method turnPage(this, turn)

Set the messages to be on a new page, clearing messages from previous page.

This is not dependent on PageHisotry option, as this method simply just clears all the messages, like turning old pages to a new page.

Namespace types: log

Parameters:

this (log)

turn (bool)

method show(this, position, hhalign, hvalign, hsize, thalign, tvalign, tsize, show, attach)

Display Message Q, Index Q, Time Q, and Log Levels

All options for postion/alignment accept TV values, such as position.bottom_right, text.align_left, size.auto etc.

Namespace types: log

Parameters:

this (log)

position (string) : Position of the table used for displaying the messages. Default is Bottom Right.

hhalign (string) : Horizontal alignment of Header columns

hvalign (string) : Vertical alignment of Header columns

hsize (string) : Size of Header text Options

thalign (string) : Horizontal alignment of all messages

tvalign (string) : Vertical alignment of all messages

tsize (string) : Size of text across the table

show (bool) : Whether to display the logs or not. Default is true.

attach (log) : Console that has been attached via attach method. If na then console will not be shown

method attach(this, attach, position)

Attaches a console to Logx, or moves already attached console around Logx

All options for position/alignment accept TV values, such as position.bottom_right, text.align_left, size.auto etc.

Namespace types: log

Parameters:

this (log)

attach (log) : Console object that has been previously attached.

position (string) : Position of Console in relation to Logx. Can be Top, Right, Bottom, Left. Default is Bottom. If unknown specified then defaults to bottom.

method detach(this, attach)

Detaches the attached console from Logx.

All options for position/alignment accept TV values, such as position.bottom_right, text.align_left, size.auto etc.

Namespace types: log

Parameters:

this (log)

attach (log) : Console object that has been previously attached.

Search in scripts for "ha溢价率"

Daily Gaps & Trapped PositionsThis script builds substantially upon the default Gaps script provided by Tradingview. Functionality was added to allow users to decide what price from the previous session is used to determine a daily gap, added support for showing gaps across all timeframes up to the daily time frame, and also allow gaps to be shown even with ETH enabled on the chart. This script provides support across normal securities, futures, and also crypto.

Users can decide between the following selections to determine if a daily gap has formed:

- Previous Session Close

- Previous Session High/Low

- Last RTH Candle High/Low

The other larger piece that was added is something called trapped positions or what some folks familiar with Market Profile would call "single prints". They could also be considered FVGs but they are a specific subset of FVGs as these must from above or below the current session's high/low.

Single prints form above or below a current session's high/low and can be considered an area where price has moved too fast in that area and price will most likely return to these areas at a later point in time. In some teachings, these are also looked at as "trapped shorts" (lighter blue box color) or "trapped supply" (yellow orange box color) which creates an area where there will be potential support (trapped shorts) or resistance (trapped supply) when this area is revisited in the future. Adding these to your chart will simply provide additional areas of interest where you may see buying or selling.

Both gaps and trapped positions have the following options:

- Show only active gaps/trapped positions. Selecting this will only show areas where price has not completely traded through the box.

- Close gaps/trapped positions partially. If this is selected, it will reduce the box size as price is traded through the area. If it is not selected, the box will only disappear once price has traded through the entire box completely.

There are some additional settings that allow you to tailor how many boxes show up on the chart. These settings are as follows:

- Max number of boxes. This setting will only plot up to this number of gaps/trapped positions.

- Minimum Deviation. This will prevent gaps/trapped positions from showing if they are too small relative to average across that last 14 periods.

- Limit Max Box Trail Length (bars). If checkbox is selected, the box will stop being extended after X number of bars given in this input.

Multi Time Frame Normalized PriceEnhance Your Trading Experience with the Multi Time Frame Normalized Price Indicator

Introduction

As a trader, having a clear and informative chart is crucial for making informed decisions. In this post, we will introduce the Multi Time Frame Normalized Price (MTFNP) Indicator, an innovative trading tool that offers an insightful perspective on price action. The script creates a symmetric chart, with the time axis going from top to bottom, making it easier to identify potential tops and bottoms in various ranges. Let's dive deeper into this powerful tool to understand how it works and how it can improve your trading experience.

The Multi Time Frame Normalized Price Indicator

The MTFNP Indicator is designed to provide a comprehensive view of price action across multiple time frames. By plotting the normalized price levels for each time frame, traders can easily identify areas of support and resistance, as well as potential tops and bottoms in various ranges.

One of the key features of this indicator is the symmetry of the chart. Instead of the traditional horizontal time axis, the MTFNP Indicator plots the time axis vertically from top to bottom. This innovative approach makes it easier for traders to visualize the price action across different time frames, enabling them to make more informed decisions.

Benefits of a Symmetric Chart

There are several advantages to using a symmetric chart with a vertical time axis, such as:

Easier to read: The unique layout of the chart makes it easier to analyze price action across multiple time frames. The clear separation between each time frame helps traders avoid confusion and identify important price levels more effectively.

Identifying tops and bottoms: The symmetric presentation of price action enables traders to quickly spot potential tops and bottoms in various ranges. This can be particularly useful for identifying potential reversal points or areas of support and resistance.

Improved decision-making: By offering a comprehensive view of price action, the MTFNP Indicator helps traders make better-informed decisions. This can lead to improved trading strategies and ultimately, better results.

The MTFNP Indicator Script

The MTFNP Indicator script leverages several custom functions, including the Chebyshev Type I Moving Average, to provide a smooth and responsive signal. Additionally, the indicator uses the Spider Plot function to create a symmetric chart with the time axis going from top to bottom.

To customize the MTFNP Indicator to your preferences, you can adjust the input parameters, such as the standard deviation length, multiplier, axes color, bottom color, and top color. You can also change the scale to fit your desired chart size.

Exploring the Relationship between Min, Max Values and Time Frames

In the Multi Time Frame Normalized Price (MTFNP) script, it is crucial to understand the relationship between the min and max values across different time frames. By analyzing how these values relate to each other, traders can make more informed decisions about market trends and potential reversals. In this section, we will dive deep into the relationship between the current time frame's min and max values and those of the further-out time frames.

Interpreting Min and Max Values Across Time Frames

When analyzing the min and max values of the current time frame in relation to the further-out time frames, it is essential to keep in mind the following points:

All min values: If the current time frame and all further-out time frames have min values, this is a strong indication that the current price level is not just a local minimum. Instead, it is likely a more significant support level. In such cases, there is a higher probability that the price will bounce back upwards, making it a potentially favorable entry point for a long position.

All max values: Conversely, if the current time frame and all further-out time frames have max values, this suggests that the current price level is not just a local maximum. Instead, it is likely a more significant resistance level. In these situations, there is a higher probability that the price will reverse downwards, making it a potentially favorable entry point for a short position.

Neutral values with high current time frame: If the current time frame has a high value while the further-out time frames are more neutral, it could indicate that the trend may continue. This is because the high value in the current time frame may signify momentum in the market, whereas the neutral values in the further-out time frames suggest that the trend has not yet reached an extreme level. In this case, traders might consider following the trend and entering a position in the direction of the current movement.

Neutral values with low current time frame: If the current time frame has a low value while the further-out time frames are more neutral, it could indicate that the trend may reverse. This is because the low value in the current time frame may suggest a potential reversal point, whereas the neutral values in the further-out time frames imply that the trend has not yet reached an extreme level. In this case, traders might consider entering a counter-trend position, anticipating a potential reversal.

Balancing Different Time Frames for Optimal Decision Making

It is essential to remember that relying solely on min and max values across different time frames can lead to potential pitfalls. The market is influenced by a wide array of factors, and no single indicator or data point can provide a complete picture. To make the most informed decisions, traders should consider incorporating additional technical analysis tools and evaluating the overall market context.

Moreover, it is crucial to maintain a balance between the current time frame and the further-out time frames. While the current time frame provides information about the most recent market movements, the further-out time frames offer a broader perspective on the market's historical behavior. By combining insights from both types of time frames, traders can make more comprehensive assessments of potential opportunities and risks.

Conclusion

In conclusion, the Multi Time Frame Normalized Price (MTFNP) script offers traders valuable insights by analyzing the relationship between the current time frame and further-out time frames. By identifying potential trend reversals and continuations, traders can make better-informed decisions about market entry and exit points.

Understanding the relationship between min and max values across different time frames is an essential component of using the MTFNP script effectively. By carefully analyzing these relationships and incorporating additional technical analysis tools, traders can improve their decision-making process and enhance their overall trading strategy.

However, it is important to remember that relying solely on the MTFNP script or any single indicator can lead to potential pitfalls. The market is influenced by a wide array of factors, and no single indicator or data point can provide a complete picture. To make the most informed decisions, traders should consider using a combination of technical analysis tools, evaluating the overall market context, and maintaining a balance between the current time frame and the further-out time frames for a comprehensive understanding of the market's behavior. By doing so, they can increase their chances of success in the ever-changing and complex world of trading.

Volume-based Support & Resistance Zones-V1 By Trade Mastership™ The all-new Support & Resistance Zones indicator, which has been upgraded to offer traders more powerful features and functionality. This innovative indicator identifies high-volume fractal lows or highs to create zones based on the size of the wick for that timeframe's candle. This makes it easy for traders to visualize which price levels are the most significant for either a trend continuation or a reversal when zones are broken and retested.

The original script for this indicator was created by Trade Mastership, with additional modifications by L N Behera. Credit goes to both of them for the majority of the logic behind this script. Since then, the script has been improved with several changes, including:

Changing the default S/R lines from plots to lines, and giving users the option to change between solid, dashed, or dotted lines for both S/R lines

Adding additional timeframes and more options for TF1, beyond the current TF. Now, users have four timeframes to plot S/R zones from

Giving users the option to easily change the line thickness for all S/R lines

Making it easier to change the colors of S/R lines and zones by consolidating the options under settings (rather than under style)

Adding extensions to active SR Zones to extend all the way right

Adding the option to extend or not extend the previous S/R zones up to the next S/R zone

Adding optional timeframe labels to active S/R zones, with left and right options, as well as the option to adjust how far to the right the label is set

Fixing an issue where the higher timeframe S/R zone was not properly starting from the high/low of fractal. Now, any higher timeframe S/R will begin exactly at the High/Low points. Note that this may not work perfectly on stocks, and if a fractal high/low is too many bars in the past, it will revert to a default max bars back to avoid script errors.

Adding a function to prevent S/R zones from lower timeframes displaying while on a higher timeframe. This helps clean up the chart quite a bit.

Creating arrays for each timeframe's boxes and lines so that the number of S/R zones can be controlled for each timeframe and limit memory consumption.

Adding new alert options and customized alert messages

Here's how this indicator works: it looks for fractal highs or fractal lows with volume that pierces above the volume's Moving Average. This moving average value can be modified in the settings for each timeframe. The fractal highs will be confirmed with three successive higher highs followed by two successive lower highs and vice versa for the fractal lows. The zone is created from the fractal high/low and the close of the candle for whatever timeframe you selected. The bigger the zone, the more significant that zone is.

Traders can disable any zone, change the zones to show lines only, and modify all the colors, transparencies, and thickness of lines for all the zones. To create alerts, traders can enable the types of alerts they want for each timeframe in the indicator's settings. After applying changes, right-click on one of the zones on the chart, and click "Add Alert on Vol S/R Zones." You do not need to add a title, as the correct alert messages are already built-in.

The latest update has migrated the script to Pine Script Version 5 and added a higher number of total boxes/lines to show on the chart. It has also increased the max bars count to the maximum Pine Script allows, enabling traders to utilize as many bars as possible when drawing the left side of SR zones that are very far back on the chart. Additionally, the update fixed issues where the indicator would not load on 1 minute and 3-minute charts unless higher timeframe SR zones

Bearish 5-0 Harmonic Patterns [theEccentricTrader]█ OVERVIEW

This indicator automatically draws bearish 5-0 harmonic patterns and price projections derived from the ranges that constitute the patterns.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Range

The range is simply the difference between the current peak and current trough prices, generally expressed in terms of points or pips.

Support and Resistance

• Support refers to a price level where the demand for an asset is strong enough to prevent the price from falling further.

• Resistance refers to a price level where the supply of an asset is strong enough to prevent the price from rising further.

Support and resistance levels are important because they can help traders identify where the price of an asset might pause or reverse its direction, offering potential entry and exit points. For example, a trader might look to buy an asset when it approaches a support level , with the expectation that the price will bounce back up. Alternatively, a trader might look to sell an asset when it approaches a resistance level , with the expectation that the price will drop back down.

It's important to note that support and resistance levels are not always relevant, and the price of an asset can also break through these levels and continue moving in the same direction.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

Muti-Part Upper and Lower Trends

• A multi-part return line uptrend begins with the formation of a new return line uptrend, or higher peak, and continues until a new downtrend, or lower peak, completes the trend.

• A multi-part downtrend begins with the formation of a new downtrend, or lower peak, and continues until a new return line uptrend, or higher peak, completes the trend.

• A multi-part uptrend begins with the formation of a new uptrend, or higher trough, and continues until a new return line downtrend, or lower trough, completes the trend.

• A multi-part return line downtrend begins with the formation of a new return line downtrend, or lower trough, and continues until a new uptrend, or higher trough, completes the trend.

Wave Cycles

A wave cycle is here defined as a complete two-part move between a swing high and a swing low, or a swing low and a swing high. The first swing high or swing low will set the course for the sequence of wave cycles that follow; for example a chart that begins with a swing low will form its first complete wave cycle upon the formation of the first complete swing high and vice versa.

Figure 1.

Fibonacci Retracement and Extension Ratios

The Fibonacci sequence is a series of numbers in which each number is the sum of the two preceding numbers, starting with 0 and 1. For example 0 + 1 = 1, 1 + 1 = 2, 1 + 2 = 3, and so on. Ultimately, we could go on forever but the first few numbers in the sequence are as follows: 0 , 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144.

The extension ratios are calculated by dividing each number in the sequence by the number preceding it. For example 0/1 = 0, 1/1 = 1, 2/1 = 2, 3/2 = 1.5, 5/3 = 1.6666..., 8/5 = 1.6, 13/8 = 1.625, 21/13 = 1.6153..., 34/21 = 1.6190..., 55/34 = 1.6176..., 89/55 = 1.6181..., 144/89 = 1.6179..., and so on. The retracement ratios are calculated by inverting this process and dividing each number in the sequence by the number proceeding it. For example 0/1 = 0, 1/1 = 1, 1/2 = 0.5, 2/3 = 0.666..., 3/5 = 0.6, 5/8 = 0.625, 8/13 = 0.6153..., 13/21 = 0.6190..., 21/34 = 0.6176..., 34/55 = 0.6181..., 55/89 = 0.6179..., 89/144 = 0.6180..., and so on.

1.618 is considered to be the 'golden ratio', found in many natural phenomena such as the growth of seashells and the branching of trees. Some now speculate the universe oscillates at a frequency of 0,618 Hz, which could help to explain such phenomena, but this theory has yet to be proven.

Traders and analysts use Fibonacci retracement and extension indicators, consisting of horizontal lines representing different Fibonacci ratios, for identifying potential levels of support and resistance. Fibonacci ranges are typically drawn from left to right, with retracement levels representing ratios inside of the current range and extension levels representing ratios extended outside of the current range. If the current wave cycle ends on a swing low, the Fibonacci range is drawn from peak to trough. If the current wave cycle ends on a swing high the Fibonacci range is drawn from trough to peak.

Harmonic Patterns

The concept of harmonic patterns in trading was first introduced by H.M. Gartley in his book "Profits in the Stock Market", published in 1935. Gartley observed that markets have a tendency to move in repetitive patterns, and he identified several specific patterns that he believed could be used to predict future price movements.

Since then, many other traders and analysts have built upon Gartley's work and developed their own variations of harmonic patterns. One such contributor is Larry Pesavento, who developed his own methods for measuring harmonic patterns using Fibonacci ratios. Pesavento has written several books on the subject of harmonic patterns and Fibonacci ratios in trading. Another notable contributor to harmonic patterns is Scott Carney, who developed his own approach to harmonic trading in the late 1990s and also popularised the use of Fibonacci ratios to measure harmonic patterns. Carney expanded on Gartley's work and also introduced several new harmonic patterns, such as the Shark pattern and the 5-0 pattern.

The bullish and bearish Gartley patterns are the oldest recognized harmonic patterns in trading and all the other harmonic patterns are ultimately modifications of the original Gartley patterns. Gartley patterns are fundamentally composed of 5 points, or 4 waves.

Bullish and Bearish 5-0 Patterns

• Bullish 5-0 patterns are fundamentally composed of three peaks and three troughs, with the second peak being lower than the first peak and the third peak being higher than the first peak. And similarly, the second trough being lower than the first trough and the third trough being higher than both the first and second troughs.

• Bearish 5-0 patterns are fundamentally composed of three troughs and three peaks, with the second trough being higher than the first trough and the third trough being lower than the first trough. And similarly, the second peak being higher than the first peak and the third peak being lower than both the first and second peaks.

The ratio measurements recommended by Scott Carney, who originated the pattern, are as follows:

• Wave 1 of the pattern, referred to as OX, has no specific ratio requirements.

• Wave 2 of the pattern, referred to as XA, has no specific ratio requirements.

• Wave 3 of the pattern, referred to as AB, should extend to at least 113%, but no further than 161.8% of the range set by wave 2.

• Wave 4 of the pattern, referred to as BC, should extend to at least 161.8%, but no further than 224% of the range set by wave 3.

• Wave 5 of the pattern, referred to as CD, should retrace to 50.0% of the range set by wave 4.

Measurement Tolerances

In general, tolerance in measurements refers to the allowable variation or deviation from a specific value or dimension. It is the range within which a particular measurement is considered to be acceptable or accurate. In this script I have applied this concept to the measurement of harmonic pattern ratios to increase to the frequency of pattern occurrences.

For example, the AB measurement of Gartley patterns is generally set at around 61.8%, but with such specificity in the measuring requirements the patterns are very rare. We can increase the frequency of pattern occurrences by setting a tolerance. A tolerance of 10% to both downside and upside, which is the default setting for all tolerances, means we would have a tolerable measurement range between 51.8-71.8%, thus increasing the frequency of occurrence.

█ FEATURES

Inputs

• AB Lower Tolerance

• AB Upper Tolerance

• BC Lower Tolerance

• BC Upper Tolerance

• CD Lower Tolerance

• CD Upper Tolerance

• Pattern Color

• Label Color

• Show Projections

• Extend Current Projection Lines

█ LIMITATIONS

All green and red candle calculations are based on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. This may cause some unexpected behaviour on some markets and timeframes. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with.

█ NOTES

Here is a link to Scott's harmonic patterns webpage for those who may be interested: harmonictrader.com

Bullish 5-0 Harmonic Patterns [theEccentricTrader]█ OVERVIEW

This indicator automatically draws bullish 5-0 harmonic patterns and price projections derived from the ranges that constitute the patterns.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Range

The range is simply the difference between the current peak and current trough prices, generally expressed in terms of points or pips.

Support and Resistance

• Support refers to a price level where the demand for an asset is strong enough to prevent the price from falling further.

• Resistance refers to a price level where the supply of an asset is strong enough to prevent the price from rising further.

Support and resistance levels are important because they can help traders identify where the price of an asset might pause or reverse its direction, offering potential entry and exit points. For example, a trader might look to buy an asset when it approaches a support level , with the expectation that the price will bounce back up. Alternatively, a trader might look to sell an asset when it approaches a resistance level , with the expectation that the price will drop back down.

It's important to note that support and resistance levels are not always relevant, and the price of an asset can also break through these levels and continue moving in the same direction.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

Muti-Part Upper and Lower Trends

• A multi-part return line uptrend begins with the formation of a new return line uptrend, or higher peak, and continues until a new downtrend, or lower peak, completes the trend.

• A multi-part downtrend begins with the formation of a new downtrend, or lower peak, and continues until a new return line uptrend, or higher peak, completes the trend.

• A multi-part uptrend begins with the formation of a new uptrend, or higher trough, and continues until a new return line downtrend, or lower trough, completes the trend.

• A multi-part return line downtrend begins with the formation of a new return line downtrend, or lower trough, and continues until a new uptrend, or higher trough, completes the trend.

Wave Cycles

A wave cycle is here defined as a complete two-part move between a swing high and a swing low, or a swing low and a swing high. The first swing high or swing low will set the course for the sequence of wave cycles that follow; for example a chart that begins with a swing low will form its first complete wave cycle upon the formation of the first complete swing high and vice versa.

Figure 1.

Fibonacci Retracement and Extension Ratios

The Fibonacci sequence is a series of numbers in which each number is the sum of the two preceding numbers, starting with 0 and 1. For example 0 + 1 = 1, 1 + 1 = 2, 1 + 2 = 3, and so on. Ultimately, we could go on forever but the first few numbers in the sequence are as follows: 0 , 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144.

The extension ratios are calculated by dividing each number in the sequence by the number preceding it. For example 0/1 = 0, 1/1 = 1, 2/1 = 2, 3/2 = 1.5, 5/3 = 1.6666..., 8/5 = 1.6, 13/8 = 1.625, 21/13 = 1.6153..., 34/21 = 1.6190..., 55/34 = 1.6176..., 89/55 = 1.6181..., 144/89 = 1.6179..., and so on. The retracement ratios are calculated by inverting this process and dividing each number in the sequence by the number proceeding it. For example 0/1 = 0, 1/1 = 1, 1/2 = 0.5, 2/3 = 0.666..., 3/5 = 0.6, 5/8 = 0.625, 8/13 = 0.6153..., 13/21 = 0.6190..., 21/34 = 0.6176..., 34/55 = 0.6181..., 55/89 = 0.6179..., 89/144 = 0.6180..., and so on.

1.618 is considered to be the 'golden ratio', found in many natural phenomena such as the growth of seashells and the branching of trees. Some now speculate the universe oscillates at a frequency of 0,618 Hz, which could help to explain such phenomena, but this theory has yet to be proven.

Traders and analysts use Fibonacci retracement and extension indicators, consisting of horizontal lines representing different Fibonacci ratios, for identifying potential levels of support and resistance. Fibonacci ranges are typically drawn from left to right, with retracement levels representing ratios inside of the current range and extension levels representing ratios extended outside of the current range. If the current wave cycle ends on a swing low, the Fibonacci range is drawn from peak to trough. If the current wave cycle ends on a swing high the Fibonacci range is drawn from trough to peak.

Harmonic Patterns

The concept of harmonic patterns in trading was first introduced by H.M. Gartley in his book "Profits in the Stock Market", published in 1935. Gartley observed that markets have a tendency to move in repetitive patterns, and he identified several specific patterns that he believed could be used to predict future price movements.

Since then, many other traders and analysts have built upon Gartley's work and developed their own variations of harmonic patterns. One such contributor is Larry Pesavento, who developed his own methods for measuring harmonic patterns using Fibonacci ratios. Pesavento has written several books on the subject of harmonic patterns and Fibonacci ratios in trading. Another notable contributor to harmonic patterns is Scott Carney, who developed his own approach to harmonic trading in the late 1990s and also popularised the use of Fibonacci ratios to measure harmonic patterns. Carney expanded on Gartley's work and also introduced several new harmonic patterns, such as the Shark pattern and the 5-0 pattern.

The bullish and bearish Gartley patterns are the oldest recognized harmonic patterns in trading and all the other harmonic patterns are ultimately modifications of the original Gartley patterns. Gartley patterns are fundamentally composed of 5 points, or 4 waves.

Bullish and Bearish 5-0 Patterns

• Bullish 5-0 patterns are fundamentally composed of three peaks and three troughs, with the second peak being lower than the first peak and the third peak being higher than the first peak. And similarly, the second trough being lower than the first trough and the third trough being higher than both the first and second troughs.

• Bearish 5-0 patterns are fundamentally composed of three troughs and three peaks, with the second trough being higher than the first trough and the third trough being lower than the first trough. And similarly, the second peak being higher than the first peak and the third peak being lower than both the first and second peaks.

The ratio measurements recommended by Scott Carney, who originated the pattern, are as follows:

• Wave 1 of the pattern, referred to as OX, has no specific ratio requirements.

• Wave 2 of the pattern, referred to as XA, has no specific ratio requirements.

• Wave 3 of the pattern, referred to as AB, should extend to at least 113%, but no further than 161.8% of the range set by wave 2.

• Wave 4 of the pattern, referred to as BC, should extend to at least 161.8%, but no further than 224% of the range set by wave 3.

• Wave 5 of the pattern, referred to as CD, should retrace to 50.0% of the range set by wave 4.

Measurement Tolerances

In general, tolerance in measurements refers to the allowable variation or deviation from a specific value or dimension. It is the range within which a particular measurement is considered to be acceptable or accurate. In this script I have applied this concept to the measurement of harmonic pattern ratios to increase to the frequency of pattern occurrences.

For example, the AB measurement of Gartley patterns is generally set at around 61.8%, but with such specificity in the measuring requirements the patterns are very rare. We can increase the frequency of pattern occurrences by setting a tolerance. A tolerance of 10% to both downside and upside, which is the default setting for all tolerances, means we would have a tolerable measurement range between 51.8-71.8%, thus increasing the frequency of occurrence.

█ FEATURES

Inputs

• AB Lower Tolerance

• AB Upper Tolerance

• BC Lower Tolerance

• BC Upper Tolerance

• CD Lower Tolerance

• CD Upper Tolerance

• Pattern Color

• Label Color

• Show Projections

• Extend Current Projection Lines

█ LIMITATIONS

All green and red candle calculations are based on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. This may cause some unexpected behaviour on some markets and timeframes. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with.

█ NOTES

Here is a link to Scott's harmonic patterns webpage for those who may be interested: harmonictrader.com

Bearish Shark Harmonic Patterns [theEccentricTrader]█ OVERVIEW

This indicator automatically draws bearish Shark harmonic patterns and price projections derived from the ranges that constitute the patterns.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Range

The range is simply the difference between the current peak and current trough prices, generally expressed in terms of points or pips.

Support and Resistance

• Support refers to a price level where the demand for an asset is strong enough to prevent the price from falling further.

• Resistance refers to a price level where the supply of an asset is strong enough to prevent the price from rising further.

Support and resistance levels are important because they can help traders identify where the price of an asset might pause or reverse its direction, offering potential entry and exit points. For example, a trader might look to buy an asset when it approaches a support level , with the expectation that the price will bounce back up. Alternatively, a trader might look to sell an asset when it approaches a resistance level , with the expectation that the price will drop back down.

It's important to note that support and resistance levels are not always relevant, and the price of an asset can also break through these levels and continue moving in the same direction.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

Muti-Part Upper and Lower Trends

• A multi-part return line uptrend begins with the formation of a new return line uptrend, or higher peak, and continues until a new downtrend, or lower peak, completes the trend.

• A multi-part downtrend begins with the formation of a new downtrend, or lower peak, and continues until a new return line uptrend, or higher peak, completes the trend.

• A multi-part uptrend begins with the formation of a new uptrend, or higher trough, and continues until a new return line downtrend, or lower trough, completes the trend.

• A multi-part return line downtrend begins with the formation of a new return line downtrend, or lower trough, and continues until a new uptrend, or higher trough, completes the trend.

Wave Cycles

A wave cycle is here defined as a complete two-part move between a swing high and a swing low, or a swing low and a swing high. The first swing high or swing low will set the course for the sequence of wave cycles that follow; for example a chart that begins with a swing low will form its first complete wave cycle upon the formation of the first complete swing high and vice versa.

Figure 1.

Fibonacci Retracement and Extension Ratios

The Fibonacci sequence is a series of numbers in which each number is the sum of the two preceding numbers, starting with 0 and 1. For example 0 + 1 = 1, 1 + 1 = 2, 1 + 2 = 3, and so on. Ultimately, we could go on forever but the first few numbers in the sequence are as follows: 0 , 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144.

The extension ratios are calculated by dividing each number in the sequence by the number preceding it. For example 0/1 = 0, 1/1 = 1, 2/1 = 2, 3/2 = 1.5, 5/3 = 1.6666..., 8/5 = 1.6, 13/8 = 1.625, 21/13 = 1.6153..., 34/21 = 1.6190..., 55/34 = 1.6176..., 89/55 = 1.6181..., 144/89 = 1.6179..., and so on. The retracement ratios are calculated by inverting this process and dividing each number in the sequence by the number proceeding it. For example 0/1 = 0, 1/1 = 1, 1/2 = 0.5, 2/3 = 0.666..., 3/5 = 0.6, 5/8 = 0.625, 8/13 = 0.6153..., 13/21 = 0.6190..., 21/34 = 0.6176..., 34/55 = 0.6181..., 55/89 = 0.6179..., 89/144 = 0.6180..., and so on.

1.618 is considered to be the 'golden ratio', found in many natural phenomena such as the growth of seashells and the branching of trees. Some now speculate the universe oscillates at a frequency of 0,618 Hz, which could help to explain such phenomena, but this theory has yet to be proven.

Traders and analysts use Fibonacci retracement and extension indicators, consisting of horizontal lines representing different Fibonacci ratios, for identifying potential levels of support and resistance. Fibonacci ranges are typically drawn from left to right, with retracement levels representing ratios inside of the current range and extension levels representing ratios extended outside of the current range. If the current wave cycle ends on a swing low, the Fibonacci range is drawn from peak to trough. If the current wave cycle ends on a swing high the Fibonacci range is drawn from trough to peak.

Harmonic Patterns

The concept of harmonic patterns in trading was first introduced by H.M. Gartley in his book "Profits in the Stock Market", published in 1935. Gartley observed that markets have a tendency to move in repetitive patterns, and he identified several specific patterns that he believed could be used to predict future price movements.

Since then, many other traders and analysts have built upon Gartley's work and developed their own variations of harmonic patterns. One such contributor is Larry Pesavento, who developed his own methods for measuring harmonic patterns using Fibonacci ratios. Pesavento has written several books on the subject of harmonic patterns and Fibonacci ratios in trading. Another notable contributor to harmonic patterns is Scott Carney, who developed his own approach to harmonic trading in the late 1990s and also popularised the use of Fibonacci ratios to measure harmonic patterns. Carney expanded on Gartley's work and also introduced several new harmonic patterns, such as the Shark pattern and the 5-0 pattern.

The bullish and bearish Gartley patterns are the oldest recognized harmonic patterns in trading and all the other harmonic patterns are ultimately modifications of the original Gartley patterns. Gartley patterns are fundamentally composed of 5 points, or 4 waves.

Bullish and Bearish Shark Patterns

• Bullish shark patterns are fundamentally composed of three troughs and two peaks, with the second peak being higher than the first peak and the second trough being higher than the first trough. The third trough must be lower than the second trough but can be above or below the first trough providing it meets the ratio requirements.

• Bearish shark patterns are fundamentally composed of three peaks and two troughs, with the second trough being lower than the first trough and the second peak being lower than the first peak. The third peak must be higher than the second peak but can be above or below the first peak providing it meets the ratio requirements.

The ratio measurements recommended by Scott Carney, who originated the pattern, are as follows:

• Wave 1 of the pattern, referred to as OX, has no specific ratio requirements.

• Wave 2 of the pattern, referred to as XA, has no specific ratio requirements.

• Wave 3 of the pattern, referred to as AB, should extend to at least 113%, but no further than 161.8% of the range set by wave 2.

• Wave 4 of the pattern, referred to as BC, should extend to at least 161.8%, but no further than 224% of the range set by wave 3.

• The last measure, referred to as XC, is that of wave 4 as a ratio of the range set by wave 1, which should extend to at least 88.6%, but no further than 113%.

Measurement Tolerances

In general, tolerance in measurements refers to the allowable variation or deviation from a specific value or dimension. It is the range within which a particular measurement is considered to be acceptable or accurate. In this script I have applied this concept to the measurement of harmonic pattern ratios to increase to the frequency of pattern occurrences.

For example, the AB measurement of Gartley patterns is generally set at around 61.8%, but with such specificity in the measuring requirements the patterns are very rare. We can increase the frequency of pattern occurrences by setting a tolerance. A tolerance of 10% to both downside and upside, which is the default setting for all tolerances, means we would have a tolerable measurement range between 51.8-71.8%, thus increasing the frequency of occurrence.

█ FEATURES

Inputs

• AB Lower Tolerance

• AB Upper Tolerance

• BC Lower Tolerance

• BC Upper Tolerance

• XC Lower Tolerance

• XC Upper Tolerance

• Pattern Color

• Label Color

• Show Projections

• Extend Current Projection Lines

█ LIMITATIONS

All green and red candle calculations are based on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. This may cause some unexpected behaviour on some markets and timeframes. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with.

█ NOTES

Here is a link to Scott's harmonic patterns webpage for those who may be interested: harmonictrader.com

Bullish Shark Harmonic Patterns [theEccentricTrader]█ OVERVIEW

This indicator automatically draws bullish Shark harmonic patterns and price projections derived from the ranges that constitute the patterns.

█ CONCEPTS

Green and Red Candles

• A green candle is one that closes with a close price equal to or above the price it opened.

• A red candle is one that closes with a close price that is lower than the price it opened.

Swing Highs and Swing Lows

• A swing high is a green candle or series of consecutive green candles followed by a single red candle to complete the swing and form the peak.

• A swing low is a red candle or series of consecutive red candles followed by a single green candle to complete the swing and form the trough.

Peak and Trough Prices (Basic)

• The peak price of a complete swing high is the high price of either the red candle that completes the swing high or the high price of the preceding green candle, depending on which is higher.

• The trough price of a complete swing low is the low price of either the green candle that completes the swing low or the low price of the preceding red candle, depending on which is lower.

Historic Peaks and Troughs

The current, or most recent, peak and trough occurrences are referred to as occurrence zero. Previous peak and trough occurrences are referred to as historic and ordered numerically from right to left, with the most recent historic peak and trough occurrences being occurrence one.

Range

The range is simply the difference between the current peak and current trough prices, generally expressed in terms of points or pips.

Support and Resistance

• Support refers to a price level where the demand for an asset is strong enough to prevent the price from falling further.

• Resistance refers to a price level where the supply of an asset is strong enough to prevent the price from rising further.

Support and resistance levels are important because they can help traders identify where the price of an asset might pause or reverse its direction, offering potential entry and exit points. For example, a trader might look to buy an asset when it approaches a support level , with the expectation that the price will bounce back up. Alternatively, a trader might look to sell an asset when it approaches a resistance level , with the expectation that the price will drop back down.

It's important to note that support and resistance levels are not always relevant, and the price of an asset can also break through these levels and continue moving in the same direction.

Upper Trends

• A return line uptrend is formed when the current peak price is higher than the preceding peak price.

• A downtrend is formed when the current peak price is lower than the preceding peak price.

• A double-top is formed when the current peak price is equal to the preceding peak price.

Lower Trends

• An uptrend is formed when the current trough price is higher than the preceding trough price.

• A return line downtrend is formed when the current trough price is lower than the preceding trough price.

• A double-bottom is formed when the current trough price is equal to the preceding trough price.

Muti-Part Upper and Lower Trends

• A multi-part return line uptrend begins with the formation of a new return line uptrend, or higher peak, and continues until a new downtrend, or lower peak, completes the trend.

• A multi-part downtrend begins with the formation of a new downtrend, or lower peak, and continues until a new return line uptrend, or higher peak, completes the trend.

• A multi-part uptrend begins with the formation of a new uptrend, or higher trough, and continues until a new return line downtrend, or lower trough, completes the trend.

• A multi-part return line downtrend begins with the formation of a new return line downtrend, or lower trough, and continues until a new uptrend, or higher trough, completes the trend.

Wave Cycles

A wave cycle is here defined as a complete two-part move between a swing high and a swing low, or a swing low and a swing high. The first swing high or swing low will set the course for the sequence of wave cycles that follow; for example a chart that begins with a swing low will form its first complete wave cycle upon the formation of the first complete swing high and vice versa.

Figure 1.

Fibonacci Retracement and Extension Ratios

The Fibonacci sequence is a series of numbers in which each number is the sum of the two preceding numbers, starting with 0 and 1. For example 0 + 1 = 1, 1 + 1 = 2, 1 + 2 = 3, and so on. Ultimately, we could go on forever but the first few numbers in the sequence are as follows: 0 , 1, 1, 2, 3, 5, 8, 13, 21, 34, 55, 89, 144.

The extension ratios are calculated by dividing each number in the sequence by the number preceding it. For example 0/1 = 0, 1/1 = 1, 2/1 = 2, 3/2 = 1.5, 5/3 = 1.6666..., 8/5 = 1.6, 13/8 = 1.625, 21/13 = 1.6153..., 34/21 = 1.6190..., 55/34 = 1.6176..., 89/55 = 1.6181..., 144/89 = 1.6179..., and so on. The retracement ratios are calculated by inverting this process and dividing each number in the sequence by the number proceeding it. For example 0/1 = 0, 1/1 = 1, 1/2 = 0.5, 2/3 = 0.666..., 3/5 = 0.6, 5/8 = 0.625, 8/13 = 0.6153..., 13/21 = 0.6190..., 21/34 = 0.6176..., 34/55 = 0.6181..., 55/89 = 0.6179..., 89/144 = 0.6180..., and so on.

1.618 is considered to be the 'golden ratio', found in many natural phenomena such as the growth of seashells and the branching of trees. Some now speculate the universe oscillates at a frequency of 0,618 Hz, which could help to explain such phenomena, but this theory has yet to be proven.

Traders and analysts use Fibonacci retracement and extension indicators, consisting of horizontal lines representing different Fibonacci ratios, for identifying potential levels of support and resistance. Fibonacci ranges are typically drawn from left to right, with retracement levels representing ratios inside of the current range and extension levels representing ratios extended outside of the current range. If the current wave cycle ends on a swing low, the Fibonacci range is drawn from peak to trough. If the current wave cycle ends on a swing high the Fibonacci range is drawn from trough to peak.

Harmonic Patterns

The concept of harmonic patterns in trading was first introduced by H.M. Gartley in his book "Profits in the Stock Market", published in 1935. Gartley observed that markets have a tendency to move in repetitive patterns, and he identified several specific patterns that he believed could be used to predict future price movements.

Since then, many other traders and analysts have built upon Gartley's work and developed their own variations of harmonic patterns. One such contributor is Larry Pesavento, who developed his own methods for measuring harmonic patterns using Fibonacci ratios. Pesavento has written several books on the subject of harmonic patterns and Fibonacci ratios in trading. Another notable contributor to harmonic patterns is Scott Carney, who developed his own approach to harmonic trading in the late 1990s and also popularised the use of Fibonacci ratios to measure harmonic patterns. Carney expanded on Gartley's work and also introduced several new harmonic patterns, such as the Shark pattern and the 5-0 pattern.

The bullish and bearish Gartley patterns are the oldest recognized harmonic patterns in trading and all the other harmonic patterns are ultimately modifications of the original Gartley patterns. Gartley patterns are fundamentally composed of 5 points, or 4 waves.

Bullish and Bearish Shark Patterns

• Bullish shark patterns are fundamentally composed of three troughs and two peaks, with the second peak being higher than the first peak and the second trough being higher than the first trough. The third trough must be lower than the second trough but can be above or below the first trough providing it meets the ratio requirements.

• Bearish shark patterns are fundamentally composed of three peaks and two troughs, with the second trough being lower than the first trough and the second peak being lower than the first peak. The third peak must be higher than the second peak but can be above or below the first peak providing it meets the ratio requirements.

The ratio measurements recommended by Scott Carney, who originated the pattern, are as follows:

• Wave 1 of the pattern, referred to as OX, has no specific ratio requirements.

• Wave 2 of the pattern, referred to as XA, has no specific ratio requirements.

• Wave 3 of the pattern, referred to as AB, should extend to at least 113%, but no further than 161.8% of the range set by wave 2.

• Wave 4 of the pattern, referred to as BC, should extend to at least 161.8%, but no further than 224% of the range set by wave 3.

• The last measure, referred to as XC, is that of wave 4 as a ratio of the range set by wave 1, which should extend to at least 88.6%, but no further than 113%.

Measurement Tolerances

In general, tolerance in measurements refers to the allowable variation or deviation from a specific value or dimension. It is the range within which a particular measurement is considered to be acceptable or accurate. In this script I have applied this concept to the measurement of harmonic pattern ratios to increase to the frequency of pattern occurrences.

For example, the AB measurement of Gartley patterns is generally set at around 61.8%, but with such specificity in the measuring requirements the patterns are very rare. We can increase the frequency of pattern occurrences by setting a tolerance. A tolerance of 10% to both downside and upside, which is the default setting for all tolerances, means we would have a tolerable measurement range between 51.8-71.8%, thus increasing the frequency of occurrence.

█ FEATURES

Inputs

• AB Lower Tolerance

• AB Upper Tolerance

• BC Lower Tolerance

• BC Upper Tolerance

• XC Lower Tolerance

• XC Upper Tolerance

• Pattern Color

• Label Color

• Show Projections

• Extend Current Projection Lines

█ LIMITATIONS

All green and red candle calculations are based on differences between open and close prices, as such I have made no attempt to account for green candles that gap lower and close below the close price of the preceding candle, or red candles that gap higher and close above the close price of the preceding candle. This may cause some unexpected behaviour on some markets and timeframes. I can only recommend using 24-hour markets, if and where possible, as there are far fewer gaps and, generally, more data to work with.

█ NOTES

Here is a link to Scott's harmonic patterns webpage for those who may be interested: harmonictrader.com

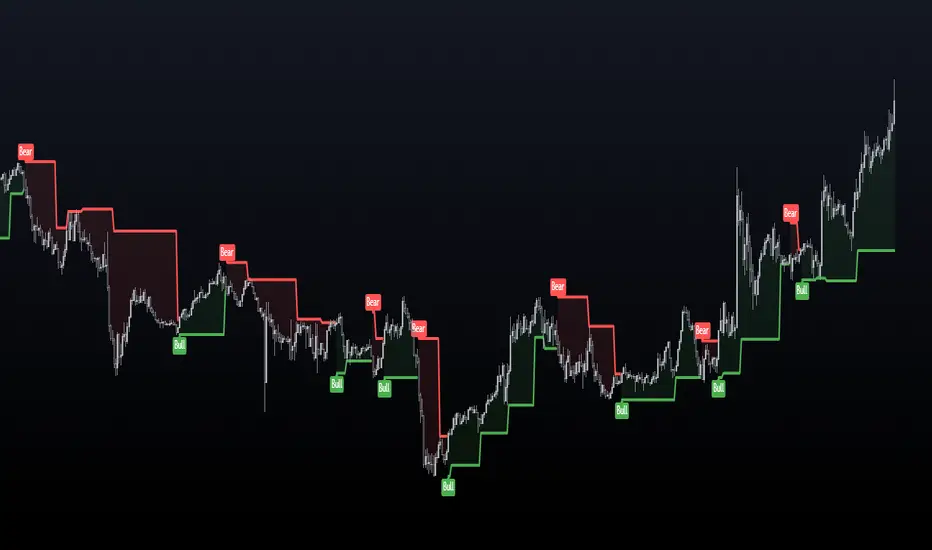

Sushi Trend [HG]🍣 The Sushi Roll, a trading concept conceived at a restaurant by Mark Fisher.

While the indicator itself goes by Sushi Trend, it is completely backed by the idea of Mark Fisher's Sushi Roll Reversal Pattern. No, it has nothing to do with raw fish, it just so happens that somebody was ordering sushi during the discussion of the idea, and that's how it got its name.

📝 Origin

First mentioned in his book, The Logical Trader --- the idea of the Sushi Roll is to serve as an early warning system to identify reversals in the market. Fisher defines the pattern as a series of 10 bars, split into two different sections, seen as 5 and 5. In order for the pattern to be emitted, the 5 bars to the right must completely engulf the 5 bars to the left. It's not a super complex system and is in fact extremely simple to grasp.

📈 Supertrend Similarities

Instead of displaying the pattern in the way Fisher meant for it to be portrayed (as seen in the photo above), I instead turned it into an indicator similar to that of Supertrend while also inheriting the same concepts from the pattern. I did this because the pattern itself has inconsistencies which can be quite noticeable when trading with it after a while. For example, these patterns can occur even during consolidating periods, and even though the pattern is meant to be recognized during trending markets, the engulfing bars can sometimes be left with indecisive directions.

➡️ The Result

Here is the result, visualized to be better in a trending format. (The indicator will not contain the boxes.)