MarkdownUtilsLibrary "MarkdownUtils"

This library shows all of CommonMark's formatting elements that are currently (2024-03-30)

available in Pine Script® and gives some hints on how to use them.

The documentation will be in the tooltip of each of the following functions. It is also

logged into Pine Logs by default if it is called. We can disable the logging by setting `pLog = false`.

mediumMathematicalSpace()

Medium mathematical space that can be used in e.g. the library names like `Markdown Utils`.

Returns: The medium mathematical space character U+205F between those double quotes " ".

zeroWidthSpace()

Zero-width space.

Returns: The zero-width character U+200B between those double quotes "".

stableSpace(pCount)

Consecutive space characters in Pine Script® are replaced by a single space character on output.

Therefore we require a "stable" space to properly indent text e.g. in Pine Logs. To use it in code blocks

of a description like this one, we have to copy the 2(!) characters between the following reverse brackets instead:

# > <

Those are the zero-width character U+200B and a space.

Of course, this can also be used within a text to add some extra spaces.

Parameters:

pCount (simple int)

Returns: A zero-width space combined with a space character.

headers(pLog)

Headers

```

# H1

## H2

### H3

#### H4

##### H5

###### H6

```

*results in*

# H1

## H2

### H3

#### H4

##### H5

###### H6

*Best practices*: Add blank line before and after each header.

Parameters:

pLog (bool)

paragrahps(pLog)

Paragraphs

```

First paragraph

Second paragraph

```

*results in*

First paragraph

Second paragraph

Parameters:

pLog (bool)

lineBreaks(pLog)

Line breaks

```

First row

Second row

```

*results in*

First row\

Second row

Parameters:

pLog (bool)

emphasis(pLog)

Emphasis

With surrounding `*` and `~` we can emphasize text as follows. All emphasis can be arbitrarily combined.

```

*Italics*, **Bold**, ***Bold italics***, ~~Scratch~~

```

*results in*

*Italics*, **Bold**, ***Bold italics***, ~~Scratch~~

Parameters:

pLog (bool)

blockquotes(pLog)

Blockquotes

Lines starting with at least one `>` followed by a space and text build block quotes.

```

Text before blockquotes.

> 1st main blockquote

>

> 1st main blockquote

>

>> 1st 1-nested blockquote

>

>>> 1st 2-nested blockquote

>

>>>> 1st 3-nested blockquote

>

>>>>> 1st 4-nested blockquote

>

>>>>>> 1st 5-nested blockquote

>

>>>>>>> 1st 6-nested blockquote

>

>>>>>>>> 1st 7-nested blockquote

>

> 2nd main blockquote, 1st paragraph, 1st row\

> 2nd main blockquote, 1st paragraph, 2nd row

>

> 2nd main blockquote, 2nd paragraph, 1st row\

> 2nd main blockquote, 2nd paragraph, 2nd row

>

>> 2nd nested blockquote, 1st paragraph, 1st row\

>> 2nd nested blockquote, 1st paragraph, 2nd row

>

>> 2nd nested blockquote, 2nd paragraph, 1st row\

>> 2nd nested blockquote, 2nd paragraph, 2nd row

Text after blockquotes.

```

*results in*

Text before blockquotes.

> 1st main blockquote

>

>> 1st 1-nested blockquote

>

>>> 1st 2-nested blockquote

>

>>>> 1st 3-nested blockquote

>

>>>>> 1st 4-nested blockquote

>

>>>>>> 1st 5-nested blockquote

>

>>>>>>> 1st 6-nested blockquote

>

>>>>>>>> 1st 7-nested blockquote

>

> 2nd main blockquote, 1st paragraph, 1st row\

> 2nd main blockquote, 1st paragraph, 2nd row

>

> 2nd main blockquote, 2nd paragraph, 1st row\

> 2nd main blockquote, 2nd paragraph, 2nd row

>

>> 2nd nested blockquote, 1st paragraph, 1st row\

>> 2nd nested blockquote, 1st paragraph, 2nd row

>

>> 2nd nested blockquote, 2nd paragraph, 1st row\

>> 2nd nested blockquote, 2nd paragraph, 2nd row

Text after blockquotes.

*Best practices*: Add blank line before and after each (nested) blockquote.

Parameters:

pLog (bool)

lists(pLog)

Paragraphs

#### Ordered lists

The first line starting with a number combined with a delimiter `.` or `)` starts an ordered

list. The list's numbering starts with the given number. All following lines that also start

with whatever number and the same delimiter add items to the list.

#### Unordered lists

A line starting with a `-`, `*` or `+` becomes an unordered list item. All consecutive items with

the same start symbol build a separate list. Therefore every list can only have a single symbol.

#### General information

To start a new list either use the other delimiter or add some non-list text between.

List items in Pine Script® allow line breaks but cannot have paragraphs or blockquotes.

Lists Pine Script® cannot be nested.

```

1) 1st list, 1st item, 1st row\

1st list, 1st item, 2nd row

1) 1st list, 2nd item, 1st row\

1st list, 2nd item, 2nd row

1) 1st list, 2nd item, 1st row\

1st list, 2nd item, 2nd row

1. 2nd list, 1st item, 1st row\

2nd list, 1st item, 2nd row

Intermediary text.

1. 3rd list

Intermediary text (sorry, unfortunately without proper spacing).

8. 4th list, 8th item

8. 4th list, 9th item

Intermediary text.

- 1st list, 1st item

- 1st list, 2nd item

* 2nd list, 1st item

* 2nd list, 2nd item

Intermediary text.

+ 3rd list, 1st item

+ 3rd list, 2nd item

```

*results in*

1) 1st list, 1st item, 1st row\

1st list, 1st item, 2nd row

1) 1st list, 2nd item, 1st row\

1st list, 2nd item, 2nd row

1) 1st list, 2nd item, 1st row\

1st list, 2nd item, 2nd row

1. 2nd list, 1st item, 1st row\

2nd list, 1st item, 2nd row

Intermediary text.

1. 3rd list

Intermediary text (sorry, unfortunately without proper spacing).

8. 4th list, 8th item

8. 4th list, 9th item

Intermediary text.

- 1st list, 1st item

- 1st list, 2nd item

* 2nd list, 1st item

* 2nd list, 2nd item

Intermediary text.

+ 3rd list, 1st item

+ 3rd list, 2nd item

Parameters:

pLog (bool)

code(pLog)

### Code

`` `Inline code` `` is formatted like this.

To write above line we wrote `` `` `Inline code` `` ``.

And to write that line we added another pair of `` `` `` around that code and

a zero-width space of function between the inner `` `` ``.

### Code blocks

can be formatted like that:

~~~

```

export method codeBlock() =>

"code block"

```

~~~

Or like that:

```

~~~

export method codeBlock() =>

"code block"

~~~

```

To write ````` within a code block we can either surround it with `~~~`.

Or we "escape" those ````` by only the zero-width space of function (stableSpace) in between.

To escape \` within a text we use `` \` ``.

Parameters:

pLog (bool)

horizontalRules(pLog)

Horizontal rules

At least three connected `*`, `-` or `_` in a separate line build a horizontal rule.

```

Intermediary text.

---

Intermediary text.

***

Intermediary text.

___

Intermediary text.

```

*results in*

Intermediary text.

---

Intermediary text.

***

Intermediary text.

___

Intermediary text.

*Best practices*: Add blank line before and after each horizontal rule.

Parameters:

pLog (bool)

tables(pLog)

Tables

A table consists of a single header line with columns separated by `|`

and followed by a row of alignment indicators for either left (`---`, `:---`), centered (`:---:`) and right (`---:`)

A table can contain several rows of data.

The table can be written as follows but hasn't to be formatte like that. By adding (stableSpace)

on the correct side of the header we could even adjust the spacing if we don't like it as it is. Only around

the column separator we should only use a usual space on each side.

```

Header 1 | Header 1 | Header 2 | Header 3

--- | :--- | :----: | ---:

Left (Default) | Left | Centered | Right

Left (Default) | Left | Centered | Right

```

*results in*

Header 1 | Header 1 | Header 2 | Header 3

--- | :--- | :----: | ---:

Left (Default) | Left | Centered | Right

Left (Default) | Left | Centered | Right

Parameters:

pLog (bool)

links(pLog)

## Links.

### Inline-style

` (Here should be the link to the TradingView homepage)`\

results in (Here should be the link to the TradingView homepage)

` (Here should be the link to the TradingView homepage "Trading View tooltip")`\

results in (Here should be the link to the TradingView homepage "Trading View tooltip")

### Reference-style

One can also collect all links e.g. at the end of a description and use a reference to that as follows.

` `\

results in .

` `\

results in .

` `\

results in .

` (../tradingview/scripts/readme)`\

results in (../tradingview/scripts/readme).

### URLs and email

URLs are also identified by the protocol identifier, email addresses by `@`. They can also be surrounded by `<` and `>`.

Input | Result

--- | ---

`Here should be the link to the TradingView homepage` | Here should be the link to the TradingView homepage

`` |

`support@tradingview.com` | support@tradingview.com

`` |

## Images

We can display gif, jp(e)g and png files in our documentation, if we add `!` before a link.

### Inline-style:

`! (Here should be the link to the favicon of the TradingView homepage "Trading View icon")`

results in

! (Here should be the link to the favicon of the TradingView homepage "Trading View icon")\

### Reference-style:

`! `

results in

!

## References for reference-style links

Even though only the formatted references are visible here in the output, this text is also followed

by the following references with links in the style

` : Referenced link`

```

: Here should be the link to the TradingView homepage "Trading view text-reference tooltip"

: Here should be the link to the TradingView homepage "Trading view number-reference tooltip"

: Here should be the link to the TradingView homepage "Trading view self-reference tooltip"

: Here should be the link to the favicon of the TradingView homepage "Trading View icon (reference)"

```

: Here should be the link to the TradingView homepage "Trading view text-reference tooltip"

: Here should be the link to the TradingView homepage "Trading view number-reference tooltip"

: Here should be the link to the TradingView homepage "Trading view self-reference tooltip"

: Here should be the link to the favicon of the TradingView homepage "Trading View icon (reference)"

Parameters:

pLog (bool)

taskLists(pLog)

Task lists.

Other Markdown implementations can also display task lists for list items like `- ` respective `- `.

This can only be simulated by inline code `` ´ ` ``.

Make sure to either add a line-break `\` at the end of the line or a new paragraph by a blank line.

### Task lists

` ` Finish library

` ` Finish library

Parameters:

pLog (bool)

escapeMd(pLog)

Escaping Markdown syntax

To write and display Markdown syntax in regular text, we have to escape it. This can be done

by adding `\` before the Markdown syntax. If the Markdown syntax consists of more than one character

in some cases also the character of function can be helpful if a command consists of

more than one character if it is placed between the separate characters of the command.

Parameters:

pLog (bool)

test()

Calls all functions of above script.

Search in scripts for "order"

Liquidity Finder🔵 Introduction

The concept of "liquidity pool" or simply "liquidity" in technical analysis price action refers to areas on the price chart where stop losses accumulate, and the market, by reaching those areas and collecting liquidity (Stop Hunt), provides the necessary energy to move the price. This concept is prominent in the "ICT" and "Smart Money" styles. Imagine, as depicted below, the price is at a support level. The general trader mentality is that there is "demand" for the asset at this price level, and this demand will outweigh "supply" as before. So, it is likely that the price will increase. As a result, they start buying and place their stop loss below the support area.

Stop Hunt areas are essentially traders' "stop loss" levels. These are the liquidity that institutional and large traders need to fill their orders. Consequently, they penetrate the price below support areas or above resistance areas to touch their stop loss and fill their orders, and then the price trend reverses.

Cash zones are generally located under "Swings Low" and above "Swings High." More specifically, they can be categorized as support levels or resistance levels, above Double Top and Triple Top patterns, below Double Bottom and Triple Bottom patterns, above Bearish Trend lines, and below Bullish Trend lines.

Double Top and Triple Top :

Double Bottom and Triple Bottom :

Bullish Trend line and Bearish Trend line :

🔵 How to Use

To optimally use this indicator, you can adjust the settings according to the symbol, time frame, and your needs. These settings include the "sensitivity" of the "liquidity finder" function and the swing periods related to static and dynamic liquidity lines.

"Statics Liquidity Line Sensitivity" is a number between 0 and 0.4. Increasing this number decreases the sensitivity of the "Statics Liquidity Line Detection" function and increases the number of lines identified. The default value is 0.3.

"Dynamics Liquidity Line Sensitivity" is a number between 0.4 and 1.95. Increasing this number increases the sensitivity of the "Dynamics Liquidity Line Detection" function and decreases the number of lines identified. The default value is 1.

"Statics Period Pivot" is set to 8 by default. By changing this number, you can specify the period for the static liquidity line pivots.

"Dynamics Period Pivot" is set to 3 by default. By changing this number, you can specify the period for the dynamic liquidity line pivots.

🔵 Settings

Access to adjust the inputs of Static Dynamic Liquidity Line Sensitivity, Dynamics Liquidity Line Sensitivity, Statics Period Pivot, and Dynamics Period Pivot is possible from this section.

Additionally, you can enable or disable liquidity lines as needed using the buttons for "Show Statics High Liquidity Line," "Show Statics Low Liquidity Line," "Show Dynamics High Liquidity Line," and "Show Dynamics Low Liquidity Line."

Candle Color By OHLC ComparisonThis indicator is designed to help you recognize the price movements within a candle/bar more quickly and easily. Typically, candle coloring is based on the opening and closing prices, but in this indicator, I followed the OHLC values in reverse order: starting with closing, low, high, and then opening. Each of these is compared with the value in the previous candle. I assigned the least importance to the opening, hence did not include it in the color determination. To make the colors memorable, I used a rainbow-like color scale; with purple representing the highest value and maroon the lowest. You can also change the colors if you wish. Additionally, if you want to set alarms, I assigned values to the candles; the highest being 16 and the lowest 1. A thicker barchart provides a better visual representation.

For instance, consider the monthly chart of the NASDAQ 100. After a prolonged positive trend, when our indicator shows a negative maroon bar (representing a low value) for the first time, it could signal a change in the trend direction. In this scenario, the appearance of the maroon bar serves as a crucial alert for investors to review their current positions or prepare for a potential downtrend. This indicator provides users with a significant advantage in identifying such critical turning points and assists them in quickly adapting to market dynamics.

[imba]lance algo🟩 INTRODUCTION

Hello, everyone!

Please take the time to review this description and source code to utilize this script to its fullest potential.

🟩 CONCEPTS

This is a trend indicator. The trend is the 0.5 fibonacci level for a certain period of time.

A trend change occurs when at least one candle closes above the level of 0.236 (for long) or below 0.786 (for short). Also it has massive amout of settings and features more about this below.

With good settings, the indicator works great on any market and any time frame!

A distinctive feature of this indicator is its backtest panel. With which you can dynamically view the results of setting up a strategy such as profit, what the deposit size is, etc.

Please note that the profit is indicated as a percentage of the initial deposit. It is also worth considering that all profit calculations are based on the risk % setting.

🟩 FEATURES

First, I want to show you what you see on the chart. And I’ll show you everything closer and in more detail.

1. Position

2. Statistic panel

3. Backtest panel

Indicator settings:

Let's go in order:

1. Strategies

This setting is responsible for loading saved strategies. There are only two preset settings, MANUAL and UNIVERSAL. If you choose any strategy other than MANUAL, then changing the settings for take profits, stop loss, sensitivity will not bring any results.

You can also save your customized strategies, this is discussed in a separate paragraph “🟩HOW TO SAVE A STRATEGY”

2. Sensitive

Responsible for the time period in bars to create Fibonacci levels

3. Start calculating date

This is the time to start backtesting strategies

4. Position group

Show checkbox - is responsible for displaying positions

Fill checkbox - is responsible for filling positions with background

Risk % - is responsible for what percentage of the deposit you are willing to lose if there is a stop loss

BE target - here you can choose when you reach which take profit you need to move your stop loss to breakeven

Initial deposit- starting deposit for profit calculation

5. Stoploss group

Fixed stoploss % checkbox - If choosed: stoploss will be calculated manually depending on the setting below( formula: entry_price * (1 - stoploss percent)) If NOT choosed: stoploss will be ( formula: fibonacci level(0.786/0.236) * (1 + stoploss percent))

6. Take profit group

This group of settings is responsible for how far from the entry point take profits will be and what % of the position to fix

7. RSI

Responsible for configuring the built-in RSI. Suitable bars will be highlighted with crosses above or below, depending on overbought/oversold

8. Infopanels group

Here I think everything is clear, you can hide or show information panels

9. Developer mode

If enabled, all events that occur will be shown, for example, reaching a take profit or stop loss with detailed information about the unfixed balance of the position

🟩 HOW TO USE

Very simple. All you need is to wait for the trend to change to long or short, you will immediately see a stop loss and four take profits, and you will also see prices. Like in this picture:

🟩 ALERTS

There are 3 types of alerts:

1. Long signal

2. Short signal

3. Any alert() function call - will be send to you json with these fields

{

"side": "LONG",

"entry": "64.454",

"tp1": "65.099",

"tp2": "65.743",

"tp3": "66.388",

"tp4": "67.032",

"winrate": "35.42%",

"strategy": "MANUAL",

"beTargetTrigger": "1",

"stop": "64.44"

}

🟩 HOW TO SAVE A STRATEGY

First, you need to make sure that the “MANUAL” strategy is selected in the strategy settings.

After this, you can start selecting parameters that will show the largest profit in the statistics panel.

I have highlighted what you need to pay attention to when choosing a strategy

Let's assume you have set up a strategy. The main question is how to preserve it?

Let’s say the strategy turned out with the following parameters:

Next we need to find this section of code:

// STRATS

selector(string strategy_name) =>

strategy_settings = Strategy_settings.new()

switch strategy_name

"MANUAL" =>

strategy_settings.sensitivity := 18

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

"UNIVERSAL" =>

strategy_settings.sensitivity := 20

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

// "NEW STRATEGY" =>

// strategy_settings.sensitivity := 20

// strategy_settings.risk_percent := 1

// strategy_settings.break_even_target := "1"

// strategy_settings.tp1_percent := 1

// strategy_settings.tp1_percent_fix := 40

// strategy_settings.tp2_percent := 2

// strategy_settings.tp2_percent_fix := 30

// strategy_settings.tp3_percent := 3

// strategy_settings.tp3_percent_fix := 20

// strategy_settings.tp4_percent := 4

// strategy_settings.tp4_percent_fix := 10

// strategy_settings.fixed_stop := false

// strategy_settings.sl_percent := 0.0

strategy_settings

// STRATS

Let's uncomment on the latest strategy called "NEW STRATEGY" rename it to "SOL 5m" and change the sensitivity:

// STRATS

selector(string strategy_name) =>

strategy_settings = Strategy_settings.new()

switch strategy_name

"MANUAL" =>

strategy_settings.sensitivity := 18

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

"UNIVERSAL" =>

strategy_settings.sensitivity := 20

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

"SOL 5m" =>

strategy_settings.sensitivity := 15

strategy_settings.risk_percent := 1

strategy_settings.break_even_target := "1"

strategy_settings.tp1_percent := 1

strategy_settings.tp1_percent_fix := 40

strategy_settings.tp2_percent := 2

strategy_settings.tp2_percent_fix := 30

strategy_settings.tp3_percent := 3

strategy_settings.tp3_percent_fix := 20

strategy_settings.tp4_percent := 4

strategy_settings.tp4_percent_fix := 10

strategy_settings.fixed_stop := false

strategy_settings.sl_percent := 0.0

strategy_settings

// STRATS

Now let's find this code:

strategy_input = input.string(title = "STRATEGY", options = , defval = "MANUAL", tooltip = "EN:\nTo manually configure the strategy, select MANUAL otherwise, changing the settings won't have any effect\nRU:\nЧтобы настроить стратегию вручную, выберите MANUAL в противном случае изменение настроек не будет иметь никакого эффекта")

And let's add our new strategy there, it turned out like this:

strategy_input = input.string(title = "STRATEGY", options = , defval = "MANUAL", tooltip = "EN:\nTo manually configure the strategy, select MANUAL otherwise, changing the settings won't have any effect\nRU:\nЧтобы настроить стратегию вручную, выберите MANUAL в противном случае изменение настроек не будет иметь никакого эффекта")

That's all. Our new strategy is now saved! It's simple! Now we can select it in the list of strategies:

Relative Volume Candles [QuantVue]In the words of Dan Zanger, "Trying to trade without using volume is like trying to drive a few hundred miles without putting gas in your tank. Trying to trade without chart patterns is like leaving without having an idea how to get there!"

Volume tends to show up at the beginning and the end of trends. As a general rule, when a stock goes up on low volume, it's seen as negative because it means buyers aren't committed. When a stock goes down on low volume, it means that not many people are trying to sell it, which is positive.

The Relative Volume Candles indicator is based on the Zanger Volume Ratio and designed to help identify key volume patterns effortlessly, with color coded candles and wicks.

The indicator is designed to be used on charts less than 1 Day and calculates the average volume for the user selected lookback period at the given time of day. From there a ratio of the current volume vs the average volume is used to determine the candle’s colors.

The candles wicks are color coded based on whether or not the volume ratio is rising or falling.

So when is it most important to have volume? When prices break out of a consolidation pattern like a bull flag or cup and handle pattern, volume plays a role. When a stock moves out of a range, volume shows how committed buyers are to that move.

Note in order to see this indicator you will need to change the visual order. This is done by selecting the the 3 dots next to the indicator name, scrolling down to visual order and selecting bring to front.

Indicator Features

🔹Selectable candle colors

🔹Selectable ratio levels

🔹Custom lookback period***

***TradingView has a maximum 5,000 bar lookback for most plans. If you are on a lower time frame chart and you select a lookback period larger than 5,000 bars the indicator will not show and you will need to select a shorter lookback period or move to a higher time frame chart.

Give this indicator a BOOST and COMMENT your thoughts!

We hope you enjoy.

Cheers!

AI SuperTrend - Strategy [presentTrading]

█ Introduction and How it is Different

The AI Supertrend Strategy is a unique hybrid approach that employs both traditional technical indicators and machine learning techniques. Unlike standard strategies that rely solely on traditional indicators or mathematical models, this strategy integrates the power of k-Nearest Neighbors (KNN), a machine learning algorithm, with the tried-and-true SuperTrend indicator. This blend aims to provide traders with more accurate, responsive, and context-aware trading signals.

*The KNN part is mainly referred from @Zeiierman.

BTCUSD 8hr performance

ETHUSD 8hr performance

█ Strategy, How it Works: Detailed Explanation

SuperTrend Calculation

Volume-Weighted Moving Average (VWMA): A VWMA of the close price is calculated based on the user-defined length (len). This serves as the central line around which the upper and lower bands are calculated.

Average True Range (ATR): ATR is calculated over a period defined by len. It measures the market's volatility.

Upper and Lower Bands: The upper band is calculated as VWMA + (factor * ATR) and the lower band as VWMA - (factor * ATR). The factor is a user-defined multiplier that decides how wide the bands should be.

KNN Algorithm

Data Collection: An array (data) is populated with recent n SuperTrend values. Corresponding labels (labels) are determined by whether the weighted moving average price (price) is greater than the weighted moving average of the SuperTrend (sT).

Distance Calculation: The absolute distance between each data point and the current SuperTrend value is calculated.

Sorting & Weighting: The distances are sorted in ascending order, and the closest k points are selected. Each point is weighted by the inverse of its distance to the current point.

Classification: A weighted sum of the labels of the k closest points is calculated. If the sum is closer to 1, the trend is predicted as bullish; if closer to 0, bearish.

Signal Generation

Start of Trend: A new bullish trend (Start_TrendUp) is considered to have started if the current trend color is bullish and the previous was not bullish. Similarly for bearish trends (Start_TrendDn).

Trend Continuation: A bullish trend (TrendUp) is considered to be continuing if the direction is negative and the KNN prediction is 1. Similarly for bearish trends (TrendDn).

Trading Logic

Long Condition: If Start_TrendUp or TrendUp is true, a long position is entered.

Short Condition: If Start_TrendDn or TrendDn is true, a short position is entered.

Exit Condition: Dynamic trailing stops are used for exits. If the trend does not continue as indicated by the KNN prediction and SuperTrend direction, an exit signal is generated.

The synergy between SuperTrend and KNN aims to filter out noise and produce more reliable trading signals. While SuperTrend provides a broad sense of the market direction, KNN refines this by predicting short-term price movements, leading to a more nuanced trading strategy.

Local picture

█ Trade Direction

The strategy allows traders to choose between taking only long positions, only short positions, or both. This is particularly useful for adapting to different market conditions.

█ Usage

ToolTips: Explains what each parameter does and how to adjust them.

Inputs: Customize values like the number of neighbors in KNN, ATR multiplier, and moving average type.

Plotting: Visual cues on the chart to indicate bullish or bearish trends.

Order Execution: Based on the generated signals, the strategy will execute buy/sell orders.

█ Default Settings

The default settings are selected to provide a balanced approach, but they can be modified for different trading styles and asset classes.

Initial Capital: $10,000

Default Quantity Type: 10% of equity

Commission: 0.1%

Slippage: 1

Currency: USD

By combining both machine learning and traditional technical analysis, this strategy offers a sophisticated and adaptive trading solution.

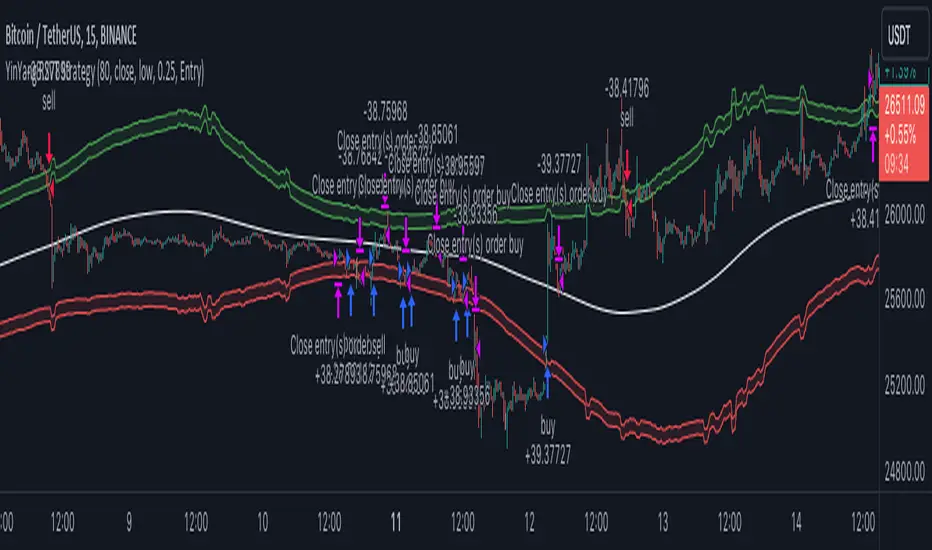

YinYang RSI Volume Trend StrategyThere are many strategies that use RSI or Volume but very few that take advantage of how useful and important the two of them combined are. This strategy uses the Highs and Lows with Volume and RSI weighted calculations on top of them. You may be wondering how much of an impact Volume and RSI can have on the prices; the answer is a lot and we will discuss those with plenty of examples below, but first…

How does this strategy work?

It’s simple really, when the purchase source crosses above the inner low band (red) it creates a Buy or Long. This long has a Trailing Stop Loss band (the outer low band that's also red) that can be adjusted in the Settings. The Stop Loss is based on a % of the inner low band’s price and by default it is 0.1% lower than the inner band’s price. This Stop Loss is not only a stop loss but it can also act as a Purchase Available location.

You can get back into a trade after a stop loss / take profit has been hit when your Reset Purchase Availability After condition has been met. This can either be at Stop Loss, Entry or None.

It is advised to allow it to reset in case the stop loss was a fake out but the call was right. Sometimes it may trigger stop loss multiple times in a row, but you don’t lose much on stop loss and you gain lots when the call is right.

The Take Profit location is the basis line (white). Take Profit occurs when the Exit Source (close, open, high, low or other) crosses the basis line and then on a different bar the Exit Source crosses back over the basis line. For example, if it was a Long and the bar’s Exit Source closed above the basis line, and then 2 bars later its Exit Source closed below the basis line, Take Profit would occur. You can disable Take Profit in Settings, but it is very useful as many times the price will cross the Basis and then correct back rather than making it all the way to the opposing zone.

Longs:

If for instance your Long doesn’t need to Take Profit and instead reaches the top zone, it will close the position when it crosses above the inner top line (green).

Please note you can change the Exit Source too which is what source (close, open, high, low) it uses to end the trades.

The Shorts work the same way as the Long but just opposite, they start when the purchase source crosses under the inner upper band (green).

Shorts:

Shorts take profit when it crosses under the basis line and then crosses back.

Shorts will Stop loss when their outer upper band (green) is crossed with the Exit Source.

Short trades are completed and closed when its Exit Source crosses under the inner low red band.

So, now that you understand how the strategy works, let’s discuss why this strategy works and how it is profitable.

First we will discuss Volume as we deem it plays a much bigger role overall and in our strategy:

As I’m sure many of you know, Volume plays a huge factor in how much something moves, but it also plays a role in the strength of the movement. For instance, let’s look at two scenarios:

Bitcoin’s price goes up $1000 in 1 Day but the Volume was only 10 million

Bitcoin’s price goes up $200 in 1 Day but the Volume was 40 million

If you were to only look at the price, you’d say #1 was more important because the price moved x5 the amount as #2, but once you factor in the volume, you know this is not true. The reason why Volume plays such a huge role in Price movement is because it shows there is a large Limit Order battle going on. It means that both Bears and Bulls believe that price is a good time to Buy and Sell. This creates a strong Support and Resistance price point in this location. If we look at scenario #2, when there is high volume, especially if it is drastically larger than the average volume Bitcoin was displaying recently, what can we decipher from this? Well, the biggest take away is that the Bull’s won the battle, and that likely when that happens we will see bullish movement continuing to happen as most of the Bears Limit Orders have been fulfilled. Whereas with #2, when large price movement happens and Bitcoin goes up $1000 with low volume what can we deduce? The main takeaway is that Bull’s pressured the price up with Market Orders where they purchased the best available price, also what this means is there were very few people who were wanting to sell. This generally dictates that Whale Limit orders for Sells/Shorts are much higher up and theres room for movement, but it also means there is likely a whale that is ready to dump and crash it back down.

You may be wondering, what did this example have to do with YinYang RSI Volume Trend Strategy? Well the reason we’ve discussed this is because we use Volume multiple times to apply multiplications in our calculations to add large weight to the price when there is lots of volume (this is applied both positively and negatively). For instance, if the price drops a little and there is high volume, our strategy will move its bounds MUCH lower than the price actually dropped, and if there was low volume but the price dropped A LOT, our strategy will only move its bounds a little. We believe this reflects higher levels of price accuracy than just price alone based on the examples described above.

Don’t believe us?

Here is with Volume NOT factored in (VWMA = SMA and we remove our Volume Filter calculation):

Which produced -$2880 Profit

Here is with our Volume factored in:

Which produced $553,000 (55.3%)

As you can see, we wen’t from $-2800 profit with volume not factored to $553,000 with volume factored. That's quite a big difference! (Please note previous success does not predict future success we are simply displaying the $ amounts as example).

Now how about RSI and why does it matter in this strategy?

As I’m sure most of you are aware, RSI is one of the leading indicators used in trading. For this reason we figured it would only make sense to incorporate it into our calculations. We fiddled with RSI for quite awhile and sometimes what logically seems to be the right way to use it isn’t. Now, because of this, our RSI calculation is a little odd, but basically what we’re doing is we calculate the RSI, then turn it into a percentage (between 0-1) that can easily be multiplied to the price point we need. The price point we use is the difference between our high purchase zone and our low purchase zone. This allows us to see how much price movement there is between zones. We multiply our zone size with our RSI multiplication and we get the amount we will add +/- to our basis line (white line). This officially creates the NEW high and low purchase zones that we are actually using and displaying in our trades.

If you found that confusing, here are some examples to why it is an important calculation for this strategy:

Before RSI factored in:

Which produced 27.8% Profit

After RSI factored in:

Which produced 553% Profit

As you can see, the RSI makes not only the purchase zones more accurate, but it also greatly increases the profit the strategy is able to make. It also helps ensure an relatively linear profit slope so you know it is reliable with its trades.

This strategy can work on pretty much anything, but you should tweak the values a bit for each pair you are trading it with for best results.

We hope you can find some use out of this simple but effective strategy, if you have any questions, comments or concerns please let us know.

HAPPY TRADING!

TradingToolsLibraryLibrary "TradingToolsLibrary"

Easily create advanced entries, exits, filters and qualifiers to simulate strategies. Supports DCA (Dollar Cost Averaging) Lines, Stop Losses, Take Profits (with trailing or without) & ATR.

method deepCopy(this)

This creates a deep copy instead of a shallow copy of an entry_position. This does NOT deep copy the self_pyramiding_positions array reference, since only the master entry_position needs this to track the rest of its copies for efficiency reasons. This is to prevent a feedback loop.

Namespace types: entry_position

Parameters:

this (entry_position)

Returns: entry_position

method precision_fix(this, precision)

Convert a floating point number to a precise floating point number with digit precision to avoid floating point errors in quantity calculations.

Namespace types: series float, simple float, input float, const float

Parameters:

this (float)

precision (int)

Returns: float

xSellBuyMidInterpolation(_x, _high, _low, _sellRange, _buyRange)

Creates an interpolation for a sell range and buy range but with an emphasis on reaching the _low the closer to the middle of the _sell and _buy range you go.

Parameters:

_x (float) : is the value you want to use to control interpolation bewteen the _high and _low value. This will return the lowest percentage at the mid between high and low and highest percentage at the _high and _low.

_high (float)

_low (float)

_sellRange (float)

_buyRange (float)

Returns: an interpolated float between the _high and _low supplied.

xSellBuyInterpolation(_x, _high, _low, _sellRange, _buyRange)

Creates an interpolation a sell range and buy range

Parameters:

_x (float) : is the value you want to use to control interpolation bewteen the _high and _low value.

_high (float)

_low (float)

_sellRange (float)

_buyRange (float)

Returns: an interpolated float between the _high and _low supplied.

activate_entries_and_exits(_entries, _exits, _filters, _qualifiers, _equity)

Determines activation for entries or exits. Does not place the actual orders.

Parameters:

_entries (entry_position )

_exits (exit_position )

_filters (filter )

_qualifiers (qualifier )

_equity (equity_management)

Returns: void

create_entries_and_exits(_entries, _exits, _equity)

Creates actual entry and exit orders if activated

Parameters:

_entries (entry_position )

_exits (exit_position )

_equity (equity_management)

Returns: void

filter

Fields:

disabled (series__bool)

filter_for_entries_or_exits (series__string)

filter_for_groups (series__string)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

expire_condition_activate_value (series__string)

expire_condition_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_operator (series__string)

qualifier

Fields:

disabled (series__bool)

qualify_for_entries_or_exits (series__string)

qualify_for_groups (series__string)

disqualify (series__bool)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

expire_after_x_bars (series__integer)

use_expire_after_x_bars (series__bool)

use_expire_condition (series__bool)

use_override_expire_condition (series__bool)

expire_condition_operator (series__string)

expire_condition_source (series__float)

expire_compare_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_activate_value (series__string)

active (series__bool)

expire_after_bars_bar_index (series__integer)

expire_after_bars_bar_index_prior (series__integer)

expire_bar_count (series__integer)

expire_bar_changed (series__bool)

entry_position

Fields:

disabled (series__bool)

activate (series__bool)

active (series__bool)

override_occured (series__bool)

passDebug (array__bool)

initial_activation_price (series__float)

dca_done (series__bool)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

use_cash (series__bool)

use_percent_equity (series__bool)

percent_equity_amount (series__float)

cash_amount (series__float)

position_size (series__float)

total_position_size (series__float)

prior_total_position_size (series__float)

equity_remaining (series__float)

prior_equity_remaining (series__float)

initial_equity (series__float)

use_martingale (series__bool)

martingale_win_ratio (series__float)

martingale_lose_ratio (series__float)

martingale_win_limit (series__integer)

martingale_lose_limit (series__integer)

martingale_limit_reset_mode (series__string)

use_dynamic_percent_equity (series__bool)

dynamic_percent_equity_amount (series__float)

initial_dynamic_percent_equity_amount (series__float)

dynamic_percent_equity_source (series__float)

dynamic_percent_equity_min (series__float)

dynamic_percent_equity_max (series__float)

dynamic_percent_equity_source_sell_range (series__float)

dynamic_percent_equity_source_buy_range (series__float)

dynamic_equity_interpolation_method (series__string)

total_bars (series__integer)

bar_index_at_activate (series__integer)

bars_since_active (series__integer)

time_at_activate (series__integer)

time_since_active (series__integer)

bar_index_at_activated (series__integer)

bar_index_at_pyramid_change (series__integer)

name (series__string)

id (series__string)

group (series__string)

pyramiding_limit (series__integer)

self_pyramiding_limit (series__integer)

self_pyramiding_positions (array__|entry_position|#OBJ)

new_pyramid_cancels_dca (series__bool)

num_active_long_positions (series__integer)

num_active_short_positions (series__integer)

num_active_positions (series__integer)

position_remaining (series__float)

prior_position_remaining (series__float)

direction (series__string)

allow_flip_position (series__bool)

flip_occurred (series__bool)

ignore_flip (series__bool)

use_dca (series__bool)

dca_use_limit (series__bool)

dca_num_positions (series__integer)

dca_positions (array__float)

dca_deviation_percentage (series__float)

dca_scale (series__float)

dca_percentages (series__string)

dca_close_cancels (series__bool)

dca_active_positions (series__integer)

use_atr_deviation (series__bool)

dca_atr_length (series__integer)

dca_atr_mult (series__float)

dca_atr_updates_dca_positions (series__bool)

close_price_at_order (series__float)

dca_use_deviation_atr_min (series__bool)

dca_position_quantities (array__float)

use_dca_dynamic_percent_equity (series__bool)

dca_in_use (array__bool)

dca_activated (array__bool)

dca_money_used (array__float)

dca_lines (array__line)

dca_color (series__color)

show_dca_lines (series__bool)

atr_value (series__float)

atr_value_at_activation (series__float)

use_cooldown_bars (series__bool)

cooldown_bars (series__integer)

cooldown_bar_changed (series__bool)

cooldown_bar_index (series__integer)

cooldown_bar_index_prior (series__integer)

cooldown_bar_change_count (series__integer)

expire_condition_activate_value (series__string)

expire_condition_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_operator (series__string)

exit_position

Fields:

disabled (series__bool)

id (series__string)

group (series__string)

exit_for_entries (series__string)

exit_for_groups (series__string)

total_bars (series__integer)

name (series__string)

condition (series__bool)

dynamic_condition (series__bool)

use_dynamic_condition (series__bool)

use_override_default_condition (series__bool)

dynamic_condition_operator (series__string)

dynamic_condition_source (series__float)

dynamic_compare_source (series__float)

dynamic_condition_source_prior (series__float)

dynamic_compare_source_prior (series__float)

use_dynamic_compare_source (series__bool)

dynamic_condition_activate_value (series__string)

activate (series__bool)

active (series__bool)

reset_equity (series__bool)

use_limit (series__bool)

use_alerts (series__bool)

reset_entry_cooldowns (series__bool)

prevent_new_entries_on_partial_close (series__bool)

show_activation_zone (series__bool)

use_average_position (series__bool)

source_value (series__float)

trigger_x_times (series__integer)

amount_of_times_triggered (series__integer)

quantity_percent (series__float)

trade_qty (series__float)

exit_amount (series__float)

entries_exiting_for (array__|entry_position|#OBJ)

atr_value (series__float)

update_atr (series__bool)

use_activate_after_bars (series__bool)

show_activate_after_bars (series__bool)

activate_after_bars (series__integer)

activate_after_bars_bar_changed (series__bool)

activate_after_bars_bar_index (series__integer)

activate_after_bars_bar_index_prior (series__integer)

activate_after_bars_bar_change_count (series__integer)

all_conditions_pass (series__bool)

use_close_if_profit_only (series__bool)

profit_value (series__float)

exit_type (series__string)

exit_modifier (series__string)

update_atr_with_new_pyramid (series__bool)

percentage (series__float)

activation_percentage (series__float)

atr_multiplier (series__float)

use_cancel_if_percent (series__bool)

cancel_if_percent (series__float)

activation_value (series__float)

activation_value_crossed (series__bool)

exit_value (series__float)

hypo_long_exit_value (series__float)

hypo_short_exit_value (series__float)

close_exit_value (series__float)

debug (series__float)

expire_condition_activate_value (series__string)

expire_condition_source (series__float)

expire_condition_source_prior (series__float)

expire_compare_source (series__float)

expire_compare_source_prior (series__float)

use_expire_compare_source (series__bool)

expire_condition_operator (series__string)

equity_management

Fields:

equity (series__float)

prior_equity (series__float)

position_used (series__float)

prior_position_used (series__float)

prevent_future_entries (series__bool)

minimum_order_size (series__float)

decimal_rounding_precision (series__integer)

direction (series__string)

show_order_info_in_comments (series__bool)

show_order_info_in_labels (series__bool)

allow_longs (series__bool)

allow_shorts (series__bool)

override_occured (series__bool)

flip_occured (series__bool)

num_concurrent_wins (series__integer)

num_concurrent_losses (series__integer)

first_entry (|entry_position|#OBJ)

num_win_trades (series__integer)

num_losing_trades (series__integer)

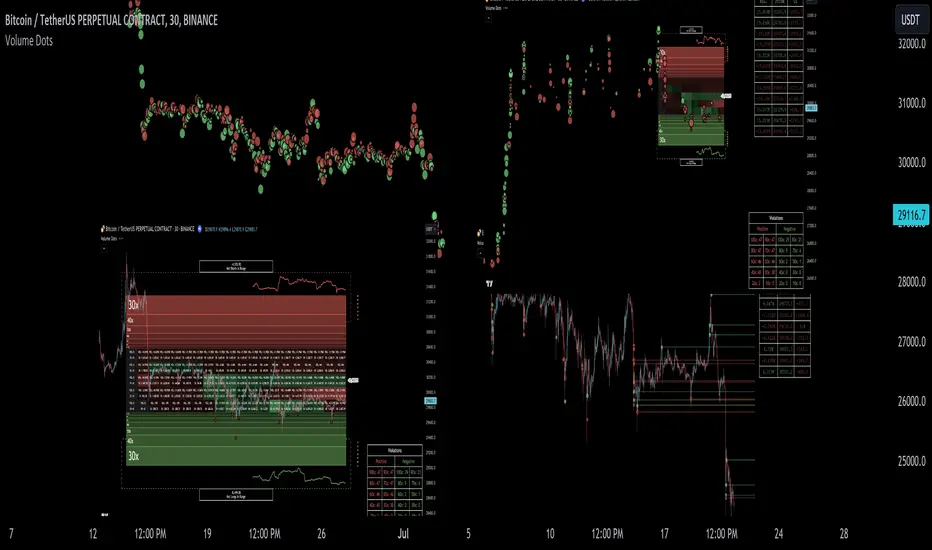

Liquidation Ranges + Volume/OI Dots [Kioseff Trading]Hello!

Introducing a multi-faceted indicator "Liquidation Ranges + Volume Dots" - this indicator replicates the volume dot tools found on various charting platforms and populates a liquidation range on crypto assets!

Features

Volume/OI dots populated according to user settings

Size of volume/OI dots corresponds to degree of abnormality

Naked level volume dots

Fixed range capabilities for volume/OI dots

Visible time range capabilities for volume/OI dots

Lower timeframe data used to discover iceberg orders (estimated using 1-minute data)

S/R lines drawn at high volume/OI areas

Liquidation ranges for crypto assets (10x - 100x)

Liquidation ranges are calculated using a popular crypto exchange's method

# of violations of liquidation ranges are recorded and presented in table

Pertinent high volume/OI price areas are recorded and presented in table

Personalized coloring for volume/OI dots

Net shorts / net long for the price range recorded

Lines shows reflecting net short & net long increases/decreases

Configurable volume/OI heatmap (displayed between liquidation ranges)

And some more (:

Liquidation Range

The liquidation range component of the indicator uses a popular crypto exchange's calculation (for liquidation ranges) to populate the chart for where 10x - 100x leverage orders are stopped out.

The image above depicts features corresponding to net shorts and net longs.

The image above shows features corresponding to liquidation zones for the underlying coin.

The image above shows the option to display volume/oi delta at the time the corresponding grid was traded at.

The image above shows an instance of using the "fixed range" feature for the script.

*The average price of the range is calculated to project liquidation zones.

*Heatmap is calculated using OI (or volume) delta.

Huge thank you to Pine Wizard @DonovanWall for his range filter code!

Price ranges are automatically detected using his calculation (:

Volume / OI Dots

Similar to other charting platforms, the volume/OI dots component of the indicator distinguishes "abnormal" changes in volume/OI; the detected price area is subsequently identified on the chart.

The detection method uses percent rank and calculates on the last bar of the chart. The "agelessness" of detection is contingent on user settings.

The image above shows volume dots in action; the size of each volume dot corresponds to the amount of volume at the price area.

Smaller dots = lower volume

Larger dots = higher volume

The image above exemplifies the highest aggression setting for volume/OI dot detection.

The table oriented top-right shows the highest volume areas (discovered on the 1-minute chart) for the calculated period.

The open interest change and corresponding price level are also shown. Results are listed in descending order but can also be listed in order of occurrence (most relevant).

Additionally, you can use the visible time range feature to detect volume dots.

The feature shows and explains how the visible range feature works. You select how many levels you want to detect and the script will detect the selected number of levels.

For instance, if I select to show 20 levels, the script will find the 20 highest volume/OI change price areas and distinguish them.

The image above shows a narrower price range.

The image above shows the same price range; however, the script is detecting the highest OI change price areas instead of volume.

* You can also set a fixed range with this feature

* Naked levels can be used

Additionally, you can select for the script to show only the highest volume/ OI change price area for each bar. When active, the script will successively identify the highest volume / OI change price area for the most recent bars.

Naked Levels

The image above shows and explains how naked levels can be detected when using the script.

And that's pretty much it!

Of course, there're a few more features you can check out when you use the script that haven't been explained here (:

Thank you again to @DonovanWall

Thank you to @Trendoscope for his binary insertion sort library (:

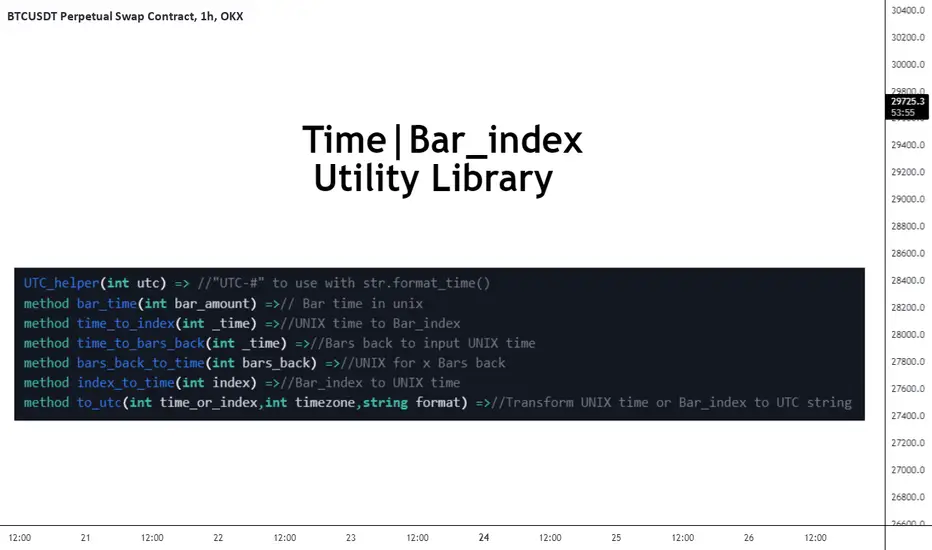

Thank you to @PineCoders for their time library

Thank you for checking this out!

improved volumeIt is an indicator that displays the trading volume.

Red-colored candle bars indicate a decrease in trading volume.

Green-colored candle bars indicate an increase in trading volume.

The transparent yellow cloud above the volume bars represents the 21-bar moving average volume, which shows the average volume over the specified period. (You can change the number of bars and the type of moving average from the indicator settings.)

This allows for easier comparison between the current trading volume and the average volume.

In the price scale section, there are 4 target levels. They represent the following in ascending order: Average volume, Average volume multiplied by 2, Average volume multiplied by 3, Average volume multiplied by 4.

Additionally, you can use the alarm feature based on these average volume levels.

Grid Spot Trading Algorithm V2 - The Quant ScienceGrid Spot Trading Algorithm V2 is the last grid trading algorithm made by our developer team.

Grid Spot Trading Algorithm V2 is a fixed 10-level grid trading algorithm. The grid is divided into an accumulation area (red) and a selling area (green).

In the accumulation area, the algorithm will place new buy orders, selling the long positions on the top of the grid.

BUYING AND SELLING LOGIC

The algorithm places up to 5 limit orders on the accumulation section of the grid, each time the price cross through the middle grid. Each single order uses 20% of the equity.

Positions are closed at the top of the grid by default, with the algorithm closing all orders at the first sell level. The exit level can be adjusted using the user interface, from the first level up to the fifth level above.

CONFIGURING THE ALGORITHM

1) Add it to the chart: Add the script to the current chart that you want to analyze.

2) Select the top of the grid: Confirm a price level with the mouse on which to fix the top of the grid.

3) Select the bottom of the grid: Confirm a price level with the mouse on which to fix the bottom of the grid.

4) Wait for the automatic creation of the grid.

USING THE ALGORITHM

Once the grid configuration process is completed, the algorithm will generate automatic backtesting.

You can add a stop loss that destroys the grid by setting the destruction price and activating the feature from the user interface. When the stop loss is activated, you can view it on the chart.

loxxfftLibrary "loxxfft"

This code is a library for performing Fast Fourier Transform (FFT) operations. FFT is an algorithm that can quickly compute the discrete Fourier transform (DFT) of a sequence. The library includes functions for performing FFTs on both real and complex data. It also includes functions for fast correlation and convolution, which are operations that can be performed efficiently using FFTs. Additionally, the library includes functions for fast sine and cosine transforms.

Reference:

www.alglib.net

fastfouriertransform(a, nn, inversefft)

Returns Fast Fourier Transform

Parameters:

a (float ) : float , An array of real and imaginary parts of the function values. The real part is stored at even indices, and the imaginary part is stored at odd indices.

nn (int) : int, The number of function values. It must be a power of two, but the algorithm does not validate this.

inversefft (bool) : bool, A boolean value that indicates the direction of the transformation. If True, it performs the inverse FFT; if False, it performs the direct FFT.

Returns: float , Modifies the input array a in-place, which means that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution. The transformed data will have real and imaginary parts interleaved, with the real parts at even indices and the imaginary parts at odd indices.

realfastfouriertransform(a, tnn, inversefft)

Returns Real Fast Fourier Transform

Parameters:

a (float ) : float , A float array containing the real-valued function samples.

tnn (int) : int, The number of function values (must be a power of 2, but the algorithm does not validate this condition).

inversefft (bool) : bool, A boolean flag that indicates the direction of the transformation (True for inverse, False for direct).

Returns: float , Modifies the input array a in-place, meaning that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution.

fastsinetransform(a, tnn, inversefst)

Returns Fast Discrete Sine Conversion

Parameters:

a (float ) : float , An array of real numbers representing the function values.

tnn (int) : int, Number of function values (must be a power of two, but the code doesn't validate this).

inversefst (bool) : bool, A boolean flag indicating the direction of the transformation. If True, it performs the inverse FST, and if False, it performs the direct FST.

Returns: float , The output is the transformed array 'a', which will contain the result of the transformation.

fastcosinetransform(a, tnn, inversefct)

Returns Fast Discrete Cosine Transform

Parameters:

a (float ) : float , This is a floating-point array representing the sequence of values (time-domain) that you want to transform. The function will perform the Fast Cosine Transform (FCT) or the inverse FCT on this input array, depending on the value of the inversefct parameter. The transformed result will also be stored in this same array, which means the function modifies the input array in-place.

tnn (int) : int, This is an integer value representing the number of data points in the input array a. It is used to determine the size of the input array and control the loops in the algorithm. Note that the size of the input array should be a power of 2 for the Fast Cosine Transform algorithm to work correctly.

inversefct (bool) : bool, This is a boolean value that controls whether the function performs the regular Fast Cosine Transform or the inverse FCT. If inversefct is set to true, the function will perform the inverse FCT, and if set to false, the regular FCT will be performed. The inverse FCT can be used to transform data back into its original form (time-domain) after the regular FCT has been applied.

Returns: float , The resulting transformed array is stored in the input array a. This means that the function modifies the input array in-place and does not return a new array.

fastconvolution(signal, signallen, response, negativelen, positivelen)

Convolution using FFT

Parameters:

signal (float ) : float , This is an array of real numbers representing the input signal that will be convolved with the response function. The elements are numbered from 0 to SignalLen-1.

signallen (int) : int, This is an integer representing the length of the input signal array. It specifies the number of elements in the signal array.

response (float ) : float , This is an array of real numbers representing the response function used for convolution. The response function consists of two parts: one corresponding to positive argument values and the other to negative argument values. Array elements with numbers from 0 to NegativeLen match the response values at points from -NegativeLen to 0, respectively. Array elements with numbers from NegativeLen+1 to NegativeLen+PositiveLen correspond to the response values in points from 1 to PositiveLen, respectively.

negativelen (int) : int, This is an integer representing the "negative length" of the response function. It indicates the number of elements in the response function array that correspond to negative argument values. Outside the range , the response function is considered zero.

positivelen (int) : int, This is an integer representing the "positive length" of the response function. It indicates the number of elements in the response function array that correspond to positive argument values. Similar to negativelen, outside the range , the response function is considered zero.

Returns: float , The resulting convolved values are stored back in the input signal array.

fastcorrelation(signal, signallen, pattern, patternlen)

Returns Correlation using FFT

Parameters:

signal (float ) : float ,This is an array of real numbers representing the signal to be correlated with the pattern. The elements are numbered from 0 to SignalLen-1.

signallen (int) : int, This is an integer representing the length of the input signal array.

pattern (float ) : float , This is an array of real numbers representing the pattern to be correlated with the signal. The elements are numbered from 0 to PatternLen-1.

patternlen (int) : int, This is an integer representing the length of the pattern array.

Returns: float , The signal array containing the correlation values at points from 0 to SignalLen-1.

tworealffts(a1, a2, a, b, tn)

Returns Fast Fourier Transform of Two Real Functions

Parameters:

a1 (float ) : float , An array of real numbers, representing the values of the first function.

a2 (float ) : float , An array of real numbers, representing the values of the second function.

a (float ) : float , An output array to store the Fourier transform of the first function.

b (float ) : float , An output array to store the Fourier transform of the second function.

tn (int) : float , An integer representing the number of function values. It must be a power of two, but the algorithm doesn't validate this condition.

Returns: float , The a and b arrays will contain the Fourier transform of the first and second functions, respectively. Note that the function overwrites the input arrays a and b.

█ Detailed explaination of each function

Fast Fourier Transform

The fastfouriertransform() function takes three input parameters:

1. a: An array of real and imaginary parts of the function values. The real part is stored at even indices, and the imaginary part is stored at odd indices.

2. nn: The number of function values. It must be a power of two, but the algorithm does not validate this.

3. inversefft: A boolean value that indicates the direction of the transformation. If True, it performs the inverse FFT; if False, it performs the direct FFT.

The function performs the FFT using the Cooley-Tukey algorithm, which is an efficient algorithm for computing the discrete Fourier transform (DFT) and its inverse. The Cooley-Tukey algorithm recursively breaks down the DFT of a sequence into smaller DFTs of subsequences, leading to a significant reduction in computational complexity. The algorithm's time complexity is O(n log n), where n is the number of samples.

The fastfouriertransform() function first initializes variables and determines the direction of the transformation based on the inversefft parameter. If inversefft is True, the isign variable is set to -1; otherwise, it is set to 1.

Next, the function performs the bit-reversal operation. This is a necessary step before calculating the FFT, as it rearranges the input data in a specific order required by the Cooley-Tukey algorithm. The bit-reversal is performed using a loop that iterates through the nn samples, swapping the data elements according to their bit-reversed index.

After the bit-reversal operation, the function iteratively computes the FFT using the Cooley-Tukey algorithm. It performs calculations in a loop that goes through different stages, doubling the size of the sub-FFT at each stage. Within each stage, the Cooley-Tukey algorithm calculates the butterfly operations, which are mathematical operations that combine the results of smaller DFTs into the final DFT. The butterfly operations involve complex number multiplication and addition, updating the input array a with the computed values.

The loop also calculates the twiddle factors, which are complex exponential factors used in the butterfly operations. The twiddle factors are calculated using trigonometric functions, such as sine and cosine, based on the angle theta. The variables wpr, wpi, wr, and wi are used to store intermediate values of the twiddle factors, which are updated in each iteration of the loop.

Finally, if the inversefft parameter is True, the function divides the result by the number of samples nn to obtain the correct inverse FFT result. This normalization step is performed using a loop that iterates through the array a and divides each element by nn.

In summary, the fastfouriertransform() function is an implementation of the Cooley-Tukey FFT algorithm, which is an efficient algorithm for computing the DFT and its inverse. This FFT library can be used for a variety of applications, such as signal processing, image processing, audio processing, and more.

Feal Fast Fourier Transform

The realfastfouriertransform() function performs a fast Fourier transform (FFT) specifically for real-valued functions. The FFT is an efficient algorithm used to compute the discrete Fourier transform (DFT) and its inverse, which are fundamental tools in signal processing, image processing, and other related fields.

This function takes three input parameters:

1. a - A float array containing the real-valued function samples.

2. tnn - The number of function values (must be a power of 2, but the algorithm does not validate this condition).

3. inversefft - A boolean flag that indicates the direction of the transformation (True for inverse, False for direct).

The function modifies the input array a in-place, meaning that the transformed data (the FFT result for direct transformation or the inverse FFT result for inverse transformation) will be stored in the same array a after the function execution.

The algorithm uses a combination of complex-to-complex FFT and additional transformations specific to real-valued data to optimize the computation. It takes into account the symmetry properties of the real-valued input data to reduce the computational complexity.

Here's a detailed walkthrough of the algorithm:

1. Depending on the inversefft flag, the initial values for ttheta, c1, and c2 are determined. These values are used for the initial data preprocessing and post-processing steps specific to the real-valued FFT.

2. The preprocessing step computes the initial real and imaginary parts of the data using a combination of sine and cosine terms with the input data. This step effectively converts the real-valued input data into complex-valued data suitable for the complex-to-complex FFT.

3. The complex-to-complex FFT is then performed on the preprocessed complex data. This involves bit-reversal reordering, followed by the Cooley-Tukey radix-2 decimation-in-time algorithm. This part of the code is similar to the fastfouriertransform() function you provided earlier.

4. After the complex-to-complex FFT, a post-processing step is performed to obtain the final real-valued output data. This involves updating the real and imaginary parts of the transformed data using sine and cosine terms, as well as the values c1 and c2.

5. Finally, if the inversefft flag is True, the output data is divided by the number of samples (nn) to obtain the inverse DFT.

The function does not return a value explicitly. Instead, the transformed data is stored in the input array a. After the function execution, you can access the transformed data in the a array, which will have the real part at even indices and the imaginary part at odd indices.

Fast Sine Transform

This code defines a function called fastsinetransform that performs a Fast Discrete Sine Transform (FST) on an array of real numbers. The function takes three input parameters:

1. a (float array): An array of real numbers representing the function values.

2. tnn (int): Number of function values (must be a power of two, but the code doesn't validate this).

3. inversefst (bool): A boolean flag indicating the direction of the transformation. If True, it performs the inverse FST, and if False, it performs the direct FST.

The output is the transformed array 'a', which will contain the result of the transformation.

The code starts by initializing several variables, including trigonometric constants for the sine transform. It then sets the first value of the array 'a' to 0 and calculates the initial values of 'y1' and 'y2', which are used to update the input array 'a' in the following loop.

The first loop (with index 'jx') iterates from 2 to (tm + 1), where 'tm' is half of the number of input samples 'tnn'. This loop is responsible for calculating the initial sine transform of the input data.

The second loop (with index 'ii') is a bit-reversal loop. It reorders the elements in the array 'a' based on the bit-reversed indices of the original order.

The third loop (with index 'ii') iterates while 'n' is greater than 'mmax', which starts at 2 and doubles each iteration. This loop performs the actual Fast Discrete Sine Transform. It calculates the sine transform using the Danielson-Lanczos lemma, which is a divide-and-conquer strategy for calculating Discrete Fourier Transforms (DFTs) efficiently.

The fourth loop (with index 'ix') is responsible for the final phase adjustments needed for the sine transform, updating the array 'a' accordingly.

The fifth loop (with index 'jj') updates the array 'a' one more time by dividing each element by 2 and calculating the sum of the even-indexed elements.

Finally, if the 'inversefst' flag is True, the code scales the transformed data by a factor of 2/tnn to get the inverse Fast Sine Transform.

In summary, the code performs a Fast Discrete Sine Transform on an input array of real numbers, either in the direct or inverse direction, and returns the transformed array. The algorithm is based on the Danielson-Lanczos lemma and uses a divide-and-conquer strategy for efficient computation.

Fast Cosine Transform

This code defines a function called fastcosinetransform that takes three parameters: a floating-point array a, an integer tnn, and a boolean inversefct. The function calculates the Fast Cosine Transform (FCT) or the inverse FCT of the input array, depending on the value of the inversefct parameter.

The Fast Cosine Transform is an algorithm that converts a sequence of values (time-domain) into a frequency domain representation. It is closely related to the Fast Fourier Transform (FFT) and can be used in various applications, such as signal processing and image compression.

Here's a detailed explanation of the code:

1. The function starts by initializing a number of variables, including counters, intermediate values, and constants.

2. The initial steps of the algorithm are performed. This includes calculating some trigonometric values and updating the input array a with the help of intermediate variables.

3. The code then enters a loop (from jx = 2 to tnn / 2). Within this loop, the algorithm computes and updates the elements of the input array a.

4. After the loop, the function prepares some variables for the next stage of the algorithm.

5. The next part of the algorithm is a series of nested loops that perform the bit-reversal permutation and apply the FCT to the input array a.

6. The code then calculates some additional trigonometric values, which are used in the next loop.

7. The following loop (from ix = 2 to tnn / 4 + 1) computes and updates the elements of the input array a using the previously calculated trigonometric values.

8. The input array a is further updated with the final calculations.

9. In the last loop (from j = 4 to tnn), the algorithm computes and updates the sum of elements in the input array a.

10. Finally, if the inversefct parameter is set to true, the function scales the input array a to obtain the inverse FCT.

The resulting transformed array is stored in the input array a. This means that the function modifies the input array in-place and does not return a new array.

Fast Convolution

This code defines a function called fastconvolution that performs the convolution of a given signal with a response function using the Fast Fourier Transform (FFT) technique. Convolution is a mathematical operation used in signal processing to combine two signals, producing a third signal representing how the shape of one signal is modified by the other.

The fastconvolution function takes the following input parameters:

1. float signal: This is an array of real numbers representing the input signal that will be convolved with the response function. The elements are numbered from 0 to SignalLen-1.

2. int signallen: This is an integer representing the length of the input signal array. It specifies the number of elements in the signal array.