Nth Order Differencing Oscillator Perform higher order differencing through convolution, the result is equivalent to cascading N momentum oscillators of periods P :

mom(mom(mom(mom(x,P)...,P)

Settings

length - Period of the oscillator, indicate the lag to use (equivalent to the period in a momentum oscillator)

order - Differencing order, indicate how many times differencing is performed (number of times a momentum oscillator is cascaded)

src - Input of the indicator

Usage

Differencing consists in subtracting an input to a previous input, this is what the momentum oscillator performs. This is often done in order to remove longer-term variations in the price. Differencing also induces a 90-degree phase shift for all sinusoids in a signal, this is why oscillators can have this leading effect, as such higher differencing can sometimes help have a faster and more visible lead.

In red the indicator with period 50 and differencing order 2, below a momentum oscillator of the same period.

It is important to note that differencing is an operation that increases noise, in fact, you might have seen some oscillators use the median price hl2 instead of the closing price, this is because the median price contains less noise than the closing price, as such more differencing require a smoother input.

Here both the sma and the oscillator period are equal to 20 with a differencing order of 5.

In time series analysis the order of differencing is chosen depending on the order of integration, more simply put we should choose a differencing order that responds to the question: "How many time should I differentiate my time series so that the result is stationary?", for stocks prices this differencing order should be 1.

Technically speaking differencing orders higher than 3 might be overkill, as higher orders return noisier outputs that might no longer be representative of the original input.

here a period of 14 with differencing order of 20 is used, we can see more periodic results but they are not really representative of the closing prices.

Details

Simple differencing is actually achieved thought convolution, if we take a first-order difference x - x(1) , we can see that this is equivalent to 1*x + -1*x(1) , the coefficients are 1 and -1, for the momentum oscillator the difference is that the coefficients include 0 values. So we only need a function generating the coefficients of our Nth order difference oscillator, in order to get them lets analyze the impulse response of a cascaded change function.

Here 5 change function are cascaded, the coefficients are: (1,-5,10,-10,5,-1)

If you look at these coefficients and the ones of higher/lower order differences we can deduce various things

The impulse response is symmetric

The first coefficient is always 1 and the last always -1

The number of coefficients increase with higher differencing orders

The sign of the current coefficient is different from the sign of the previous one

From the shape of the impulse response, we can deduce that the coefficients of an Nth order differencing operator is a windowed series of 1,-1,1...,-1 , and that's actually the case, for an Nth order differencing operator the values of this window are given by the Nth row of the Pascal triangle.

There are various ways to get the values in the row of the Pascal triangle, one involving using the combination formula, however, we can do it way faster by using the recursive formula used in line number 13. Now that we have our coefficients we only need to separate them with 0 values and that's all.

Conclusion

We can see that oscillators are noisier than the original input signal, this is can be a desired effect in order to make lagging indicators more reactive, but it can also be overlooked due to the results appearing leading the price or just looking more predictable, however, we should note that higher-order differencing does not provide a consistent nor reliable solution toward minimizing lag, nor does classical oscillators.

The indicator is not useful, but if for some reason you require a lot of differencing operations to be done and don't want to use consecutive change or mom functions, then this script might results useful to you.

Search in scripts for "oscillator"

Range Oscillator (Zeiierman)█ Overview

Range Oscillator (Zeiierman) is a dynamic market oscillator designed to visualize how far the price is trading relative to its equilibrium range. Instead of relying on traditional overbought/oversold thresholds, it uses adaptive range detection and heatmap coloring to reveal where price is trading within a volatility-adjusted band.

The oscillator maps market movement as a heat zone, highlighting when the price approaches the upper or lower range boundaries and signaling potential breakout or mean-reversion conditions.

Highlights

Adaptive range detection based on ATR and weighted price movement.

Heatmap-driven coloring that visualizes volatility pressure and directional bias.

Clear transition zones for detecting trend shifts and equilibrium points.

█ How It Works

⚪ Range Detection

The indicator identifies a dynamic price range using two main parameters:

Minimum Range Length: The number of bars required to confirm that a valid range exists.

Range Width Multiplier: Expands or contracts the detected range proportionally to the ATR (Average True Range).

This approach ensures that the oscillator automatically adapts to both trending and ranging markets without manual recalibration.

⚪ Weighted Mean Calculation

Instead of a simple moving average, the script calculates a weighted equilibrium mean based on the size of consecutive candle movements:

Larger price changes are given greater weight, emphasizing recent volatility.

⚪ Oscillator Formula

Once the range and equilibrium mean are defined, the oscillator computes:

Osc = 100 * (Close - Mean) / RangeATR

This normalizes price distance relative to the dynamic range size — producing consistent readings across volatile and quiet periods.

█ Heatmap Logic

The Range Oscillator includes a built-in heatmap engine that color-codes each oscillator value based on recent price interaction intensity:

Strong Bullish Zones: Bright green — price faces little resistance upward.

Weak Bullish Zones: Muted green — uptrend continuation but with minor hesitation.

Transition Zones: Blue — areas of uncertainty or trend shift.

Weak Bearish Zones: Maroon — downtrend pressure but soft momentum.

Strong Bearish Zones: Bright red — strong downside continuation with low resistance.

Each color band adapts dynamically using:

Number of Heat Levels: Controls granularity of the heatmap.

Minimum Touches per Level: Defines how reactive or “sensitive” each color zone is.

█ How to Use

⚪ Trend & Momentum Confirmation

When the oscillator stays above +0 with green coloring, it suggests sustained bullish pressure.

Similarly, readings below –0 with red coloring, it suggests sustained bearish pressure.

⚪ Range Breakouts

When the oscillator line breaks above +100 or below –100, the price is exceeding its normal volatility range, often signaling breakout potential or exhaustion extremes.

⚪ Mean Reversion Trades

Look for the oscillator to cross back toward zero after reaching an extreme. These transitions (often marked by blue tones) can identify early reversals or range resets.

⚪ Divergence

Use oscillator peaks and troughs relative to price action to spot hidden strength or weakness before the next move.

█ Settings

Minimum Range Length: Number of bars needed to confirm a valid range.

Range Width Multiplier: Expands or contracts range width based on ATR.

Number of Heat Levels: Number of gradient bands used in the oscillator.

Minimum Touches per Level: Sensitivity threshold for when a zone becomes “hot.”

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Pivot Oscillator█ OVERVIEW

Pivot Oscillator is a versatile oscillator that measures market strength by comparing the current price to local price pivots. Values are scaled by ATR, normalized to a 0–100 range, and displayed along with an SMA line.

Oscillator: generates signals suitable for pullback strategies.

SMA line: serves as a momentum indicator.

█ CONCEPTS

Pivot Oscillator is designed with dual functionality:

- Oscillator & signals: ideal for pullback strategies, detecting local highs/lows and short-term reversals.

- SMA (Momentum): shows stable market-side dominance and filters price impulses.

Calculation logic:

- Oscillator = closing price − pivot line (derived from average high/low pivots).

Scaled by ATR and normalized to 0–100:

50 – bullish dominance,

< 50 – bearish dominance.

SMA is computed from smoothed oscillator values and serves as a momentum indicator.

█ FEATURES

Pivot Calculation:

- Pivot Length (lenSwing) – the number of bars used to identify local pivots (highs/lows). Higher values filter only larger extremes, while lower values make the oscillator react faster to local highs and lows.

- Pivot Level (pivotLevel) – determines the position of the pivot line between the average low and high pivots. A value of 0.5 places the pivotLine exactly halfway between the average high and low pivots; values closer to 0 or 1 shift the line toward the low or high pivots, respectively.

- Pivot Lookback (lookback) – the number of recent pivots used to calculate the average pivot, which smooths the pivotLine and reduces noise caused by individual extremes.

- Oscillator calculation: closing price − pivotLine (average of pivots computed from the above parameters).

The pivotLine is then scaled by ATR and normalized to a 0–100 range.

ATR Scaling:

- ATR period (atrLen)

- Multipliers (multUp / multDown) for upper and lower scaling.

Dynamic Colors:

- Oscillator > 50 → green (bullish)

- Oscillator < 50 → red (bearish)

SMA Line (Momentum):

- Smoothed oscillator (SMA) serves as a momentum indicator.

- Dynamic color indicates direction of SMA.

- Helps identify dominant market side and trend.

Overbought / Oversold Zones:

- Configurable OB/OS levels for both oscillator and SMA.

- Dynamic band colors: change depending on SMA relative to maOverbought / maOversold.

- Provides visual confirmation for potential corrections or strong momentum.

Gradients & Visualization:

- Oscillator and SMA gradients (3 layers) with adjustable transparency.

- Gradient visualization for OB/OS zones and oscillator.

- Full customization of colors, line width, and transparency.

Signals:

- Oscillator leaving oversold zone → long signal

- Oscillator leaving overbought zone → short signal

- OB/OS band colors dynamically reflect SMA levels for additional confirmation.

Alerts:

- OB/OS cross alerts.

█ HOW TO USE

Add the indicator to your TradingView chart → Indicators → search for “Pivot Oscillator”.

Parameter Configuration:

- Pivot Settings: pivot length, pivot level, pivot lookback.

- ATR Settings: ATR period, scaling multipliers.

- Threshold Levels: OB/OS levels for oscillator and SMA.

- Signal Settings: SMA length, extra smoothing.

- Style Settings: bullish/bearish colors, OB/OS lines, midline, text colors.

- Gradient Settings: enable/disable gradients and transparency.

Signal Interpretation:

BUY (Long):

- Oscillator leaves the oversold zone (OS crossover).

- OB/OS band color may additionally confirm the signal when SMA < maOversold.

SELL (Short):

- Oscillator leaves the overbought zone (OB crossunder).

- OB/OS band color may additionally confirm the signal when SMA > maOverbought.

█ APPLICATIONS

Pivot Oscillator and SMA can be scaled for different strategies:

- Pullback strategies: oscillator detects local highs/lows.

- Momentum / Trend: SMA shows market-side dominance and trend direction.

Adjust pivot and ATR parameters:

- Lower settings: faster reaction, suitable for scalping or intraday trading.

- Higher settings: more stable readings, suitable for swing trading or longer timeframes.

█ NOTES

- In strong trends, the oscillator may remain in extreme zones for extended periods – reflects dominance, not necessarily a reversal.

- OB/OS levels should be adapted to the instrument and pivot/ATR settings.

- Works best when combined with other tools: support/resistance, market structure, and volume analysis.

BTC Regime Oscillator (MC + Spread) [1D]ONLY SUPPOSED TO BE USED FOR BTC PERPS, AND SPOT LEVERAGING:

This is a risk oscillator that measures whether Bitcoin’s price is supported by real capital or is running ahead of it, and converts that into a simple risk-regime oscillator.

It's built with market cap, and FDV, and Z-scores compressed to -100 <-> 100

I created this indicator because I got tired of FOMO Twitter and Wall Street games.

DO NOT USE THIS AS A BEGIN-ALL-AND-END-ALL. YOU NEED TO USE THIS AS A CONFIRMATION INDICATOR, AND ON HTF ONLY (1D>) IF YOU USE THIS ON LOWER TIMEFRAMES, YOU ARE FEEDING YOUR MONEY TO A LOW-LIFE DING BAT ON WALL STREET. HERE IS HOW IT WORKS:

This indicator is Split up by

A) Market Cap

--> Represents real money in BTC

--> Ownership capital

--> If MC is rising, money is entering BTC

B) FDV (Fully Diluted Valuation)

--> For BTC: price(21M) (21,000,000)

--> Represents the theoretical valuation

--> Since BTC really has a fixed cap, FDV mostly tracks the price

C) Oscillators

Both MC and FDV are:

--> Logged (to handle scale)

--> Normalized (Z-score)

--> Compressed to -100 <-> 100

HERE ARE THREE THINGS YOU ARE GOING TO SEE ON THE CHART

A) The market cap oscillator (MC OSC)

--> Normalized trend of real capital

RISING: Indicates capital inflow

FALLING: Indicates capital outflow

B) FDV Oscillator

--> Normalized trend of valuation pressure

ABOVE MC: Price is ahead of capital

BELOW MC: Capital is keeping up

!!!! FDV IS CONTEXT NOT SIGNALS !!!!

C) Spread = (FDV - MC)

--> The difference between valuation and capital

(THIS IS THE CORE SIGNAL)

NEGATIVE: Capital is gonna lead price

NEAR 0: Balanced

POSITIVE: Price leads capital

(THIS MEANS STRESS FOR BTC, NOT DILLUTION!)

WHAT DOES -60, 0, 60 MEAN?:

--> These are meant to serve as risk zones, not buy/sell dynamics; this is not the same as an RSI oscillator.

A) 0 level

--> Price and capital are balanced

--> No structural stress

(TRADE WITH NORMAL POSITION SIZE, AND NORMAL EXPECTATIONS)

B) Below -60 (Supportive/Compressed)

--> BTC is relatively cheap to recent history

--> Capital supports price well

(ALWAYS REMEMBER TO CONFIRM THIS WITH WHAT THE CHART IS TELLING YOU)

--> Press trends

--> Use higher ATRs

--> Pullbacks are better here

C) Above 60 (Overextension, or fragile)

--> BTC is expensive relative to recent history

--> Price is ahead of capital

(ALWAYS REMEMBER TO CONFIRM THIS WITH WHAT THE CHART IS TELLING YOU)

--> Reduce leverage, use smaller ATR

--> Use lower ATRs, TP faster

--> Do not chase breakouts

--> Expect volatility and whipsaws

"Can I press trades right now? Or do I need to hog my capital?"

CONDITIONS:

Spread Less than 0 and below -60 = Press trades

Spread near 0 = Normal trading conditions

Spread is Greater than 0 or above 60+ = Capital protection

OI Volume Oscillator Cross DynamicsThe OI Volume Oscillator Cross Dynamics is a custom indicator designed to analyze the relationship between Open Interest (OI) and Volume Oscillator in the cryptocurrency markets. This tool aims to assist traders in identifying potential market sentiment shifts, enabling them to make informed trading decisions based on the dynamic interplay of these key market components.

Key Components:

Open Interest (OI): This component represents the total number of outstanding derivative contracts, such as futures and options, that have not been settled. Open Interest provides insights into market participation and trader commitment, offering a broader perspective on the flow of money into the market.

Volume Oscillator: The Volume Oscillator is a momentum indicator that showcases the difference between two volume moving averages. It is instrumental in identifying bullish or bearish market trends by providing insights into buying and selling pressure in the market.

Functional Dynamics:

Crossover Analysis: The indicator identifies points where the Volume Oscillator crosses above or below the Open Interest, marking potential shifts in market sentiment. These crossover points are visually represented, making them easily identifiable for analysis.

Visual Cues: The indicator uses visual shapes and colors to enhance interpretability. Bullish crossovers are marked with green upward triangles, while bearish crossovers are represented by red downward triangles.

Customization: The indicator allows for customization of the Volume Oscillator’s sensitivity through a multiplier, enabling traders to adjust the indicator according to their trading strategy and market outlook.

Usage Guidelines:

Bullish Scenario: A crossover of the Volume Oscillator above the Open Interest is interpreted as a bullish signal, indicating potential upward price movement due to increased buying pressure or trading activity.

Bearish Scenario: A crossover of the Volume Oscillator below the Open Interest is seen as a bearish signal, suggesting potential downward price movement due to increased selling pressure or reduced trading activity.

Conclusion:

The OI Volume Oscillator Cross Dynamics indicator is designed to provide traders with a nuanced perspective of market activity through the combined analysis of Open Interest and Volume Oscillator. Its design aims to offer valuable insights, allowing for a strategic approach to trading based on the observed market dynamics.

The code is open source and utilizes Binance info but you can alter the code to meet your needs to go beyond just Bitcoin if needed.

Lyapunov Hodrick-Prescott Oscillator w/ DSL [Loxx]Lyapunov Hodrick-Prescott Oscillator w/ DSL is a Hodrick-Prescott Channel Filter that is modified using the Lyapunov stability algorithm to turn the filter into an oscillator. Signals are created using Discontinued Signal Lines.

What is the Lyapunov Stability?

As soon as scientists realized that the evolution of physical systems can be described in terms of mathematical equations, the stability of the various dynamical regimes was recognized as a matter of primary importance. The interest for this question was not only motivated by general curiosity, but also by the need to know, in the XIX century, to what extent the behavior of suitable mechanical devices remains unchanged, once their configuration has been perturbed. As a result, illustrious scientists such as Lagrange, Poisson, Maxwell and others deeply thought about ways of quantifying the stability both in general and specific contexts. The first exact definition of stability was given by the Russian mathematician Aleksandr Lyapunov who addressed the problem in his PhD Thesis in 1892, where he introduced two methods, the first of which is based on the linearization of the equations of motion and has originated what has later been termed Lyapunov exponents (LE). (Lyapunov 1992)

The interest in it suddenly skyrocketed during the Cold War period when the so-called "Second Method of Lyapunov" (see below) was found to be applicable to the stability of aerospace guidance systems which typically contain strong nonlinearities not treatable by other methods. A large number of publications appeared then and since in the control and systems literature. More recently the concept of the Lyapunov exponent (related to Lyapunov's First Method of discussing stability) has received wide interest in connection with chaos theory . Lyapunov stability methods have also been applied to finding equilibrium solutions in traffic assignment problems.

In practice, Lyapunov exponents can be computed by exploiting the natural tendency of an n-dimensional volume to align along the n most expanding subspace. From the expansion rate of an n-dimensional volume, one obtains the sum of the n largest Lyapunov exponents. Altogether, the procedure requires evolving n linearly independent perturbations and one is faced with the problem that all vectors tend to align along the same direction. However, as shown in the late '70s, this numerical instability can be counterbalanced by orthonormalizing the vectors with the help of the Gram-Schmidt procedure (Benettin et al. 1980, Shimada and Nagashima 1979) (or, equivalently with a QR decomposition). As a result, the LE λi, naturally ordered from the largest to the most negative one, can be computed: they are altogether referred to as the Lyapunov spectrum.

The Lyapunov exponent "λ" , is useful for distinguishing among the various types of orbits. It works for discrete as well as continuous systems.

λ < 0

The orbit attracts to a stable fixed point or stable periodic orbit. Negative Lyapunov exponents are characteristic of dissipative or non-conservative systems (the damped harmonic oscillator for instance). Such systems exhibit asymptotic stability; the more negative the exponent, the greater the stability. Superstable fixed points and superstable periodic points have a Lyapunov exponent of λ = −∞. This is something akin to a critically damped oscillator in that the system heads towards its equilibrium point as quickly as possible.

λ = 0

The orbit is a neutral fixed point (or an eventually fixed point). A Lyapunov exponent of zero indicates that the system is in some sort of steady state mode. A physical system with this exponent is conservative. Such systems exhibit Lyapunov stability. Take the case of two identical simple harmonic oscillators with different amplitudes. Because the frequency is independent of the amplitude, a phase portrait of the two oscillators would be a pair of concentric circles. The orbits in this situation would maintain a constant separation, like two flecks of dust fixed in place on a rotating record.

λ > 0

The orbit is unstable and chaotic. Nearby points, no matter how close, will diverge to any arbitrary separation. All neighborhoods in the phase space will eventually be visited. These points are said to be unstable. For a discrete system, the orbits will look like snow on a television set. This does not preclude any organization as a pattern may emerge. Thus the snow may be a bit lumpy. For a continuous system, the phase space would be a tangled sea of wavy lines like a pot of spaghetti. A physical example can be found in Brownian motion. Although the system is deterministic, there is no order to the orbit that ensues.

For our purposes here, we transform the HP by applying Lyapunov Stability as follows:

output = math.log(math.abs(HP / HP ))

You can read more about Lyapunov Stability here: Measuring Chaos

What is. the Hodrick-Prescott Filter?

The Hodrick-Prescott (HP) filter refers to a data-smoothing technique. The HP filter is commonly applied during analysis to remove short-term fluctuations associated with the business cycle. Removal of these short-term fluctuations reveals long-term trends.

The Hodrick-Prescott (HP) filter is a tool commonly used in macroeconomics. It is named after economists Robert Hodrick and Edward Prescott who first popularized this filter in economics in the 1990s. Hodrick was an economist who specialized in international finance. Prescott won the Nobel Memorial Prize, sharing it with another economist for their research in macroeconomics.

This filter determines the long-term trend of a time series by discounting the importance of short-term price fluctuations. In practice, the filter is used to smooth and detrend the Conference Board's Help Wanted Index (HWI) so it can be benchmarked against the Bureau of Labor Statistic's (BLS) JOLTS, an economic data series that may more accurately measure job vacancies in the U.S.

The HP filter is one of the most widely used tools in macroeconomic analysis. It tends to have favorable results if the noise is distributed normally, and when the analysis being conducted is historical.

What are DSL Discontinued Signal Line?

A lot of indicators are using signal lines in order to determine the trend (or some desired state of the indicator) easier. The idea of the signal line is easy : comparing the value to it's smoothed (slightly lagging) state, the idea of current momentum/state is made.

Discontinued signal line is inheriting that simple signal line idea and it is extending it : instead of having one signal line, more lines depending on the current value of the indicator.

"Signal" line is calculated the following way :

When a certain level is crossed into the desired direction, the EMA of that value is calculated for the desired signal line

When that level is crossed into the opposite direction, the previous "signal" line value is simply "inherited" and it becomes a kind of a level

This way it becomes a combination of signal lines and levels that are trying to combine both the good from both methods.

In simple terms, DSL uses the concept of a signal line and betters it by inheriting the previous signal line's value & makes it a level.

Included:

Bar coloring

Alerts

Signals

Loxx's Expanded Source Types

Uptrick: Trend SMA Oscillator### In-Depth Analysis of the "Uptrick: Trend SMA Oscillator" Indicator

---

#### Introduction to the Indicator

The "Uptrick: Trend SMA Oscillator" is an advanced yet user-friendly technical analysis tool designed to help traders across all levels of experience identify and follow market trends with precision. This indicator builds upon the fundamental principles of the Simple Moving Average (SMA), a cornerstone of technical analysis, to deliver a clear, visually intuitive overlay on the price chart. Through its strategic use of color-coding and customizable parameters, the Uptrick: Trend SMA Oscillator provides traders with actionable insights into market dynamics, enhancing their ability to make informed trading decisions.

#### Core Concepts and Methodology

1. **Foundational Principle – Simple Moving Average (SMA):**

- The Simple Moving Average (SMA) is the heart of the Uptrick: Trend SMA Oscillator. The SMA is a widely-used technical indicator that calculates the average price of an asset over a specified number of periods. By smoothing out price data, the SMA helps to reduce the noise from short-term fluctuations, providing a clearer picture of the overall trend.

- In the Uptrick: Trend SMA Oscillator, two SMAs are employed:

- **Primary SMA (oscValue):** This is applied to the closing price of the asset over a user-defined period (default is 14 periods). This SMA tracks the price closely and is sensitive to changes in market direction.

- **Smoothing SMA (oscV):** This second SMA is applied to the primary SMA, further smoothing the data and helping to filter out minor price movements that might otherwise be mistaken for trend reversals. The default period for this smoothing is 50, but it can be adjusted to suit the trader's preference.

2. **Color-Coding for Trend Visualization:**

- One of the most distinctive features of this indicator is its use of color to represent market trends. The indicator’s line changes color based on the relationship between the primary SMA and the smoothing SMA:

- **Bullish (Green):** The line turns green when the primary SMA is equal to or greater than the smoothing SMA, indicating that the market is in an upward trend.

- **Bearish (Red):** Conversely, the line turns red when the primary SMA falls below the smoothing SMA, signaling a downward trend.

- This color-coded system provides traders with an immediate, easy-to-interpret visual cue about the market’s direction, allowing for quick decision-making.

#### Detailed Explanation of Inputs

1. **Bullish Color (Default: Green #00ff00):**

- This input allows traders to customize the color that represents bullish trends on the chart. The default setting is green, a color commonly associated with upward market movement. However, traders can adjust this to any color that suits their visual preferences or matches their overall chart theme.

2. **Bearish Color (Default: Red RGB: 245, 0, 0):**

- The bearish color input determines the color of the line when the market is trending downwards. The default setting is a vivid red, signaling caution or selling opportunities. Like the bullish color, this can be customized to fit the trader’s needs.

3. **Line Thickness (Default: 5):**

- This setting controls the thickness of the line plotted by the indicator. The default thickness of 5 makes the line prominent on the chart, ensuring that the trend is easily visible even in complex or crowded chart setups. Traders can adjust the thickness to make the line thinner or thicker, depending on their visual preferences.

4. **Primary SMA Period (Value 1 - Default: 14):**

- The primary SMA period defines how many periods (e.g., days, hours) are used to calculate the moving average based on the asset’s closing prices. The default period of 14 is a balanced setting that offers a good mix of responsiveness and stability, but traders can adjust this depending on their trading style:

- **Shorter Periods (e.g., 5-10):** These make the indicator more sensitive, capturing trends more quickly but also increasing the likelihood of reacting to short-term price fluctuations or "noise."

- **Longer Periods (e.g., 20-50):** These smooth the data more, providing a more stable trend line that is less prone to whipsaws but may be slower to respond to trend changes.

5. **Smoothing SMA Period (Value 2 - Default: 50):**

- The smoothing SMA period determines how much the primary SMA is smoothed. A longer smoothing period results in a more gradual, stable line that focuses on the broader trend. The default of 50 is designed to smooth out most of the short-term fluctuations while still being responsive enough to detect significant trend shifts.

- **Customization:**

- **Shorter Smoothing Periods (e.g., 20-30):** Make the indicator more responsive, better for fast-moving markets or for traders who want to capture quick trends.

- **Longer Smoothing Periods (e.g., 70-100):** Enhance stability, ideal for long-term traders looking to avoid reacting to minor price movements.

#### Unique Characteristics and Advantages

1. **Simplicity and Clarity:**

- The Uptrick: Trend SMA Oscillator’s design prioritizes simplicity without sacrificing effectiveness. By relying on the widely understood SMA, it avoids the complexity of more esoteric indicators while still providing reliable trend signals. This simplicity makes it accessible to traders of all levels, from novices who are just learning about technical analysis to experienced traders looking for a straightforward, dependable tool.

2. **Visual Feedback Mechanism:**

- The indicator’s use of color to signify market trends is a particularly powerful feature. This visual feedback mechanism allows traders to assess market conditions at a glance. The clarity of the green and red color scheme reduces the mental effort required to interpret the indicator, freeing the trader to focus on strategy execution.

3. **Adaptability Across Markets and Timeframes:**

- One of the strengths of the Uptrick: Trend SMA Oscillator is its versatility. The basic principles of moving averages apply equally well across different asset classes and timeframes. Whether trading stocks, forex, commodities, or cryptocurrencies, traders can use this indicator to gain insights into market trends.

- **Intraday Trading:** For day traders who operate on short timeframes (e.g., 1-minute, 5-minute charts), the oscillator can be adjusted to be more responsive, capturing quick shifts in momentum.

- **Swing Trading:** Swing traders, who typically hold positions for several days to weeks, will find the default settings or slightly adjusted periods ideal for identifying and riding medium-term trends.

- **Long-Term Trading:** Position traders and investors can adjust the indicator to focus on long-term trends by increasing the periods for both the primary and smoothing SMAs, filtering out minor fluctuations and highlighting sustained market movements.

4. **Minimal Lag:**

- One of the challenges with moving averages is lag—the delay between when the price changes and when the indicator reflects this change. The Uptrick: Trend SMA Oscillator addresses this by allowing traders to adjust the periods to find a balance between responsiveness and stability. While all SMAs inherently have some lag, the customizable nature of this indicator helps traders mitigate this effect to align with their specific trading goals.

5. **Customizable and Intuitive:**

- While many technical indicators come with a fixed set of parameters, the Uptrick: Trend SMA Oscillator is fully customizable, allowing traders to tailor it to their trading style, market conditions, and personal preferences. This makes it a highly flexible tool that can be adjusted as markets evolve or as a trader’s strategy changes over time.

#### Practical Applications for Different Trader Profiles

1. **Day Traders:**

- **Use Case:** Day traders can customize the SMA periods to create a faster, more responsive indicator. This allows them to capture short-term trends and make quick decisions. For example, reducing the primary SMA to 5 and the smoothing SMA to 20 can help day traders react promptly to intraday price movements.

- **Strategy Integration:** Day traders might use the Uptrick: Trend SMA Oscillator in conjunction with volume-based indicators to confirm the strength of a trend before entering or exiting trades.

2. **Swing Traders:**

- **Use Case:** Swing traders can use the default settings or slightly adjust them to smooth out minor price fluctuations while still capturing medium-term trends. This approach helps in identifying the optimal points to enter or exit trades based on the broader market direction.

- **Strategy Integration:** Swing traders can combine this indicator with oscillators like the Relative Strength Index (RSI) to confirm overbought or oversold conditions, thereby refining their entry and exit strategies.

3. **Position Traders:**

- **Use Case:** Position traders, who hold trades for extended periods, can extend the SMA periods to focus on long-term trends. By doing so, they minimize the impact of short-term market noise and focus on the underlying trend.

- **Strategy Integration:** Position traders might use the Uptrick: Trend SMA Oscillator in combination with fundamental analysis. The indicator can help confirm the timing of entries and exits based on broader economic or corporate developments.

4. **Algorithmic and Quantitative Traders:**

- **Use Case:** The simplicity and clear logic of the Uptrick: Trend SMA Oscillator make it an excellent candidate for algorithmic trading strategies. Its binary output—bullish or bearish—can be easily coded into automated trading systems.

- **Strategy Integration:** Quant traders might use the indicator as part of a larger trading system that incorporates multiple indicators and rules, optimizing the SMA periods based on historical backtesting to achieve the best results.

5. **Novice Traders:**

- **Use Case:** Beginners can use the Uptrick: Trend SMA Oscillator to learn the basics of trend-following strategies.

The visual simplicity of the color-coded line helps novice traders quickly understand market direction without the need to interpret complex data.

- **Educational Value:** The indicator serves as an excellent starting point for those new to technical analysis, providing a practical example of how moving averages work in a real-world trading environment.

#### Combining the Indicator with Other Tools

1. **Relative Strength Index (RSI):**

- The RSI is a momentum oscillator that measures the speed and change of price movements. When combined with the Uptrick: Trend SMA Oscillator, traders can look for instances where the RSI shows divergence from the price while the oscillator confirms the trend. This can be a powerful signal of an impending reversal or continuation.

2. **Moving Average Convergence Divergence (MACD):**

- The MACD is another popular trend-following momentum indicator. By using it alongside the Uptrick: Trend SMA Oscillator, traders can confirm the strength of a trend and identify potential entry and exit points with greater confidence. For example, a bullish crossover on the MACD that coincides with the Uptrick: Trend SMA Oscillator turning green can be a strong buy signal.

3. **Volume Indicators:**

- Volume is often considered the fuel behind price movements. Using volume indicators like the On-Balance Volume (OBV) or Volume Weighted Average Price (VWAP) in conjunction with the Uptrick: Trend SMA Oscillator can help traders confirm the validity of a trend. A trend identified by the oscillator that is supported by increasing volume is typically more reliable.

4. **Fibonacci Retracement:**

- Fibonacci retracement levels are used to identify potential reversal levels in a trending market. When the Uptrick: Trend SMA Oscillator indicates a trend, traders can use Fibonacci retracement levels to find potential entry points that align with the broader trend direction.

#### Implementation in Different Market Conditions

1. **Trending Markets:**

- The Uptrick: Trend SMA Oscillator excels in trending markets, where it provides clear signals on the direction of the trend. In a strong uptrend, the line will remain green, helping traders stay in the trade for longer periods. In a downtrend, the red line will signal the continuation of bearish conditions, prompting traders to stay short or avoid long positions.

2. **Sideways or Range-Bound Markets:**

- In range-bound markets, where price oscillates within a confined range without a clear trend, the Uptrick: Trend SMA Oscillator may produce more frequent changes in color. While this could indicate potential reversals at the range boundaries, traders should be cautious of false signals. It may be beneficial to pair the oscillator with a volatility indicator to better navigate such conditions.

3. **Volatile Markets:**

- In highly volatile markets, where prices can swing rapidly, the sensitivity of the Uptrick: Trend SMA Oscillator can be adjusted by modifying the SMA periods. A shorter SMA period might capture quick trends, but traders should be aware of the increased risk of whipsaws. Combining the oscillator with a volatility filter or using it in a higher time frame might help mitigate some of this risk.

#### Final Thoughts

The "Uptrick: Trend SMA Oscillator" is a versatile, easy-to-use indicator that stands out for its simplicity, visual clarity, and adaptability. It provides traders with a straightforward method to identify and follow market trends, using the well-established concept of moving averages. The indicator’s customizable nature makes it suitable for a wide range of trading styles, from day trading to long-term investing, and across various asset classes.

By offering immediate visual feedback through color-coded signals, the Uptrick: Trend SMA Oscillator simplifies the decision-making process, allowing traders to focus on execution rather than interpretation. Whether used on its own or as part of a broader technical analysis toolkit, this indicator has the potential to enhance trading strategies and improve overall performance.

Its accessibility and ease of use make it particularly appealing to novice traders, while its adaptability and reliability ensure that it remains a valuable tool for more experienced market participants. As markets continue to evolve, the Uptrick: Trend SMA Oscillator remains a timeless tool, rooted in the fundamental principles of technical analysis, yet flexible enough to meet the demands of modern trading.

Smart Money Oscillator [ChartPrime]The "Smart Money Oscillator " is a premium and discount zone oscillator with BOS and CHoCH built in for further analysis of price action. This indicator works by first determining the the premium and discount zones by using pivot points and high/lows. The top of this oscillator represents the current premium zone while the bottom half of this oscillator represents the discount zone. This oscillator functionally works like a stochastic oscillator with more sophisticated upper and lower bounds generated using smart money concept theories. We have included a moving average to allow the user to visualize the currant momentum in the oscillator. Another key feature we have included lagging divergences to help traders visualize potential reversal conditions.

Understanding the concepts of Premium and Discount zones, as well as Break of Structure (BoS) and Change of Character (CHoCH), is crucial for traders using the Smart Money Oscillator. These concepts are rooted in market structure analysis, which involves studying price levels and movements.

Premium Zone is where the price is considered to be relatively high or 'overbought'. In this zone, prices have risen significantly and may indicate that the asset is becoming overvalued, potentially leading to a reversal or slowdown in the upward trend.

The Discount Zone represents a 'discount' or 'oversold' area. Here, prices have fallen substantially, suggesting that the asset might be undervalued. This could be an indicator of a potential upward reversal or a pause in the downward trend.

Break of Structure (BoS) is about the continuation of a trend. In a bullish trend, a BoS is identified by the break of a recent higher high. In a bearish trend, it's the break of a recent Lower Low. BoS indicates that the trend is strong and likely to continue in its current direction. It's a sign of strength in the prevailing trend, whether up or down.

Change of Character (CHoCH) is an indication of a potential end to a trend. It occurs when there's a significant change in the market's behavior, contradicting the current trend. For example, in an uptrend characterized by higher highs and higher lows, a CHoCH may occur if a new high is formed but then is followed by an impulsive move downwards. This suggests that the bullish trend may be weakening and a bearish reversal could be imminent. CHoCH is essentially a sign of trend exhaustion and potential reversal.

With each consecutive BoS, the signal line of the oscillator will deepen in color. This allows you to visually see the strength of the current trend. The maximum strength of the trend is found by keeping track of the maximum number of consecutive BoS's within a window of 10. This calculation excludes periods without any BoS's to allow for a more stable max.

Quick Update is a feature that implements a more aggressive algorithm to update the highs and lows. Instead of updating the pivot points exclusively to update the range levels, it will attempt to use the current historical highs/lows to update the bounds. This results in a more responsive range at the cost of stability. There are pros and cons for both settings. With Quick Update disabled, the indicator will allow for strong reversals to register without the indicator maxing out. With Quick Update enabled, the indicator will show shorter term extremes with the risk of the signal being pinned to the extremities during strong trends or large movements. With Quick Update disabled, the oscillator prioritizes stability, using a more historical perspective to set its bounds. When Quick Update is enabled, the oscillator becomes more responsive, adjusting its bounds rapidly to reflect the latest market movements.

The Scale Offset feature allows the indicator to break the boundaries of the oscillator. This can be useful when the market is breaking highs or lows allowing the user to identify extremities in price. With Scale Offset disabled the oscillator will always remain inside of the boundaries because the extremities will be updated instantly. When this feature is enabled it will update the boundaries one step behind instead of updating it instantly. This allows the user to more easily see overbought and oversold conditions at the cost of incurring a single bar lag to the boundaries. Generally this is a good idea as this behavior makes the oscillator more sensitive to recent price spikes or drops, reflecting sudden market movements more accurately. It accentuates the extremities of the market conditions, potentially offering a more aggressive analysis. The main trade-off with the Scale Offset feature is between sensitivity and potential overreaction. It offers a more immediate and exaggerated reflection of market conditions but might also lead to misinterpretations in certain scenarios, especially in highly volatile markets.

Divergence is used to predict potential trend reversals. It occurs when the price of an asset and the reading of an oscillator move in opposite directions. This discrepancy can signal a weakening of the current trend and possibly indicate a potential reversal.

Divergence doesn't always lead to a trend reversal, but it's a warning sign that the current trend might be weakening. Divergence can sometimes give false signals, particularly in strongly trending markets where the oscillator may remain in overbought or oversold conditions for extended periods. The lagging nature of using pivot points to calculate divergences means that all divergences are limited by the pivot look forward input. The upside of using a longer look forward is that the divergences will be more accurate. The obvious con here is that it will be more delayed and might be useless by the time it appears. Its recommended to use the built in divergences as a way to learn how these are formed so you can make your own in real time.

By default, the oscillator uses a smoothing of 3 to allow for a more price like behavior while still being rather smooth compared to raw price data. Conversely, you can increase this value to make this indicator behave smoother. Something to keep in mind is that the amount of delay from real time is equal to half of the smoothing period.

We have included a verity of alerts in this indicator. Here is a list of all of the available alerts: Bullish BOS, Bearish BOS, Bullish CHoCH, Bearish CHoCH, Bullish Divergence, Hidden Bullish Divergence, Bearish Divergence, Hidden Bearish Divergence, Cross Over Average, Cross Under Average.

Below are all of the inputs and their tooltips to get you started:

Settings:

Smoothing: Specifies the degree of smoothing applied to the oscillator. Higher values result in smoother but potentially less responsive signals.

Average Length: Sets the length of the moving average applied to the oscillator, affecting its sensitivity and smoothness.

Pivot Length: Specifies the forward-looking length for pivot points, affecting how the oscillator anticipates future price movements. This directly impacts the delay in finding a pivot.

Max Length: Sets the maximum length to consider for calculating the highest values in the oscillator.

Min Length: Defines the minimum length for calculating the lowest values in the oscillator.

Quick Update: Activates a faster update mode for the oscillator's extremities, which may result in less stable range boundaries.

Scale Offset: When enabled, delays updating minimum and maximum values to enhance signal directionality, allowing the signal to occasionally exceed normal bounds.

Candle Color: Enables coloring of candles based on the current directional signal of the oscillator.

Labels:

Enable BOS/CHoCH Labels: Activates the display of BOS (Break of Structure) and CHoCH (Change of Character) labels on the chart.

Visual Padding: Turns on additional visual padding at the top and bottom of the chart to accommodate labels. Determines the amount of visual padding added to the chart for label display.

Divergence:

Divergence Pivot: Defines the number of bars to the right of the pivot in divergence calculations, influencing the oscillator's responsiveness.

Divergence Pivot Forward: Directly impacts latency. Longer periods results in more accurate results at the sacrifice of delay.

Upper Range: Sets the upper range limit for divergence calculations, influencing the oscillator's sensitivity to larger trends.

Lower Range: Determines the lower range limit for divergence calculations, affecting the oscillator's sensitivity to shorter trends.

Symbol: Allows selection of the label style for divergence indicators, with options for text or symbolic representation.

Regular Bullish: Activates the detection and marking of regular bullish divergences in the oscillator.

Hidden Bullish: Enables the identification and display of hidden bullish divergences.

Regular Bearish: Turns on the feature to detect and highlight regular bearish divergences.

Hidden Bearish: Activates the functionality for detecting and displaying hidden bearish divergences.

Color:

Bullish: Determines the minimum/maximum color gradient for bullish signals, impacting the chart's visual appearance.

Bearish: Defines the minimum/maximum color gradient for bearish signals, affecting their visual representation.

Average: Specifies the color for the average line of the oscillator, enhancing chart readability.

CHoCH: Sets the color for bullish/bearish CHoCH (Change of Character) signals.

Premium/Discount: Determines the color for the premium/discount zone in the oscillator's visual representation.

Text Color: Sets the color for the text in BoS/CHoCH labels.

Regular Bullish: Defines the color used to represent regular bullish divergences.

Hidden Bullish: Specifies the color for hidden bullish divergences.

Regular Bearish: Determines the color for hidden bearish divergences.

Divergence Text Color: Specifies the color for the text in divergence labels.

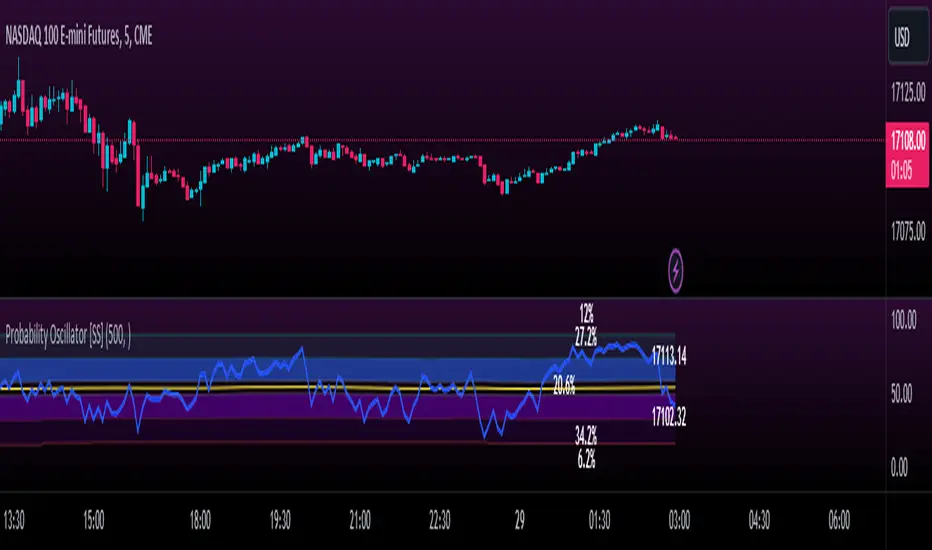

Momentum Probability Oscillator [SS]This is the momentum based probability indicator.

What it does?

This takes the average of MFI, Stochastics and RSI and plots it out as an independent oscillator.

It then tracks bullish vs bearish instances. Bullish is defined as a greater move from open to high than open to low and inverse for bearish.

It stores this data and these averages and plots these levels as a graph.

The graph depicts the max bullish values at the top, the min bearish values at the bottom and the averages in between:

It will plot the average "threshold" value in yellow:

The threshold value is key. A ticker trading above the threshold is generally bullish. Below is bearish.

The threshold value frequently acts as support and resistance levels (see below):

Resistance:

Support:

The indicator also shows you the amount of time a ticker has spent in each region, over a defined lookback period (defaulted to 500):

When you see that cumulatively, more time has been spent in a bullish range or a bearish range, it can help you ascertain the prevailing sentiment at that time.

The indicator will also calculate the average price range based on the underlying oscillator value. It does this through use of ATR based techniques, as its not usually possible to calculate a price from an oscillator:

This is intended as a general reference and not a precise target, as it is using ATR as opposed to the actual technical value itself.

As this is an oscillator, you can use it to look for divergences as well. The advantage to having it formulated in this way is:

a) You get the power of all 3 indicators (stochastics, MFI and RSI) in one and

b) You are adding context to the underlying technical reading. The indicator is plotting out the average, max and min ranges for the selected ticker and performing assessments based on these ranges that add context to the current PA.

You also have the ability to see the specific technical levels associated with each specific technical indicator. If you open up the settings menu and select "Show Table", this will appear:

This will show you the exact values of each of the technicals the indicator is using in its range assessment.

And that is basically the bulk of the indicator!

I use this predominately on the smaller timeframes, especially when there is a lot of chop, to ascertain the overall sentiment.

I also will reference it on the 1 hour to see what the prevailing sentiment is and whether the stock is at an area of technical resistance or support. For example, here is what I referenced on SPY today:

QUICK NOTE:

It works best with RTH (regular trading hours) turned on and ETH (extended trading hours) turned off!

That's it!

Hopefully you like it and leave your comments and suggestions below!

Ultimate Oscillator + Realtime DivergencesUltimate Oscillator (UO) + Realtime Divergences + Alerts + Lookback periods.

This version of the Ultimate Oscillator adds the following 5 additional features to the stock UO by Tradingview:

- Optional divergence lines drawn directly onto the oscillator in realtime

- Configurable alerts to notify you when divergences occur, as well as centerline crossovers.

- Configurable lookback periods to fine tune the divergences drawn in order to suit different trading styles and timeframes.

- Background colouring option to indicate when the UO has crossed the centerline, or optionally when both the UO and an external oscillator, which can be linked via the settings, have both crossed their centerlines.

- Alternate timeframe feature allows you to configure the oscillator to use data from a different timeframe than the chart it is loaded on.

This indicator adds additional features onto the stock Ultimate Oscillator by Tradingview, whose core calculations remain unchanged. Namely the configurable option to automatically and clearly draw divergence lines onto the oscillator for you as they occur in realtime. It also has the addition of unique alerts, so you can be notified as divergences occur without spending all day watching the charts. Furthermore, this version of the Ultimate Oscillator comes with configurable lookback periods, which can be configured in order to adjust the length of the divergences, in order to suit shorter or higher timeframe trading approaches.

The Ultimate Oscillator

Tradingview describes the Ultimate Oscillator as follows:

“The Ultimate Oscillator indicator (UO) indicator is a technical analysis tool used to measure momentum across three varying timeframes. The problem with many momentum oscillators is that after a rapid advance or decline in price, they can form false divergence trading signals. For example, after a rapid rise in price, a bearish divergence signal may present itself, however price continues to rise. The ultimate Oscillator attempts to correct this by using multiple timeframes in its calculation as opposed to just one timeframe which is what is used in most other momentum oscillators.”

More information on the history, use cases and calculations of the Ultimate Oscillator can be found here: www.tradingview.com

What are divergences?

Divergence is when the price of an asset is moving in the opposite direction of a technical indicator, such as an oscillator, or is moving contrary to other data. Divergence warns that the current price trend may be weakening, and in some cases may lead to the price changing direction.

There are 4 main types of divergence, which are split into 2 categories;

regular divergences and hidden divergences. Regular divergences indicate possible trend reversals, and hidden divergences indicate possible trend continuation.

Regular bullish divergence: An indication of a potential trend reversal, from the current downtrend, to an uptrend.

Regular bearish divergence: An indication of a potential trend reversal, from the current uptrend, to a downtrend.

Hidden bullish divergence: An indication of a potential uptrend continuation.

Hidden bearish divergence: An indication of a potential downtrend continuation.

Setting alerts.

With this indicator you can set alerts to notify you when any/all of the above types of divergences occur, on any chart timeframe you choose.

Configurable lookback values.

You can adjust the default lookback values to suit your prefered trading style and timeframe. If you like to trade a shorter time frame, lowering the default lookback values will make the divergences drawn more sensitive to short term price action.

How do traders use divergences in their trading?

A divergence is considered a leading indicator in technical analysis , meaning it has the ability to indicate a potential price move in the short term future.

Hidden bullish and hidden bearish divergences, which indicate a potential continuation of the current trend are sometimes considered a good place for traders to begin, since trend continuation occurs more frequently than reversals, or trend changes.

When trading regular bullish divergences and regular bearish divergences, which are indications of a trend reversal, the probability of it doing so may increase when these occur at a strong support or resistance level . A common mistake new traders make is to get into a regular divergence trade too early, assuming it will immediately reverse, but these can continue to form for some time before the trend eventually changes, by using forms of support or resistance as an added confluence, such as when price reaches a moving average, the success rate when trading these patterns may increase.

Typically, traders will manually draw lines across the swing highs and swing lows of both the price chart and the oscillator to see whether they appear to present a divergence, this indicator will draw them for you, quickly and clearly, and can notify you when they occur.

Disclaimer: This script includes code from the stock UO by Tradingview as well as the Divergence for Many Indicators v4 by LonesomeTheBlue.

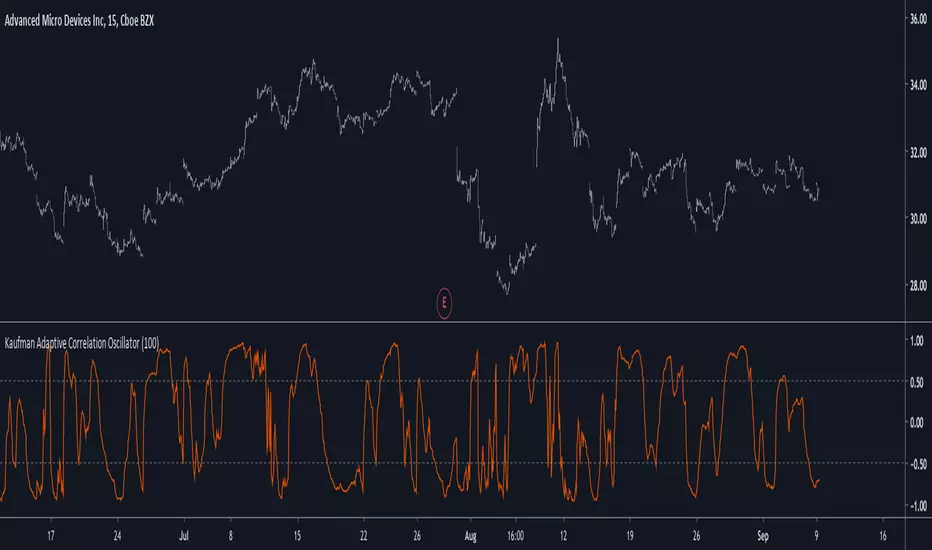

Kaufman Adaptive Correlation OscillatorIntroduction

The correlation oscillator is a technical indicator that measure the linear relationship between the market closing price and a simple increasing line, the indicator is in a (-1,1) range and rise when price is up-trending and fall when price is down-trending. Another characteristic of the indicator is its inherent smoothing which provide a noise free (to some extent) oscillator.

Such indicator use simple moving averages as well as estimates of the standard deviation for its calculation, but we can easily make it adaptive, this is why i propose this new technical indicator that create an adaptive correlation oscillator based on the Kaufman adaptive moving average.

The Indicator

The length parameter control the period window of the moving average, larger periods return smoother results while having a low kurtosis, which mean that values will remain around 1 or -1 a longer period of time. Pre-filtering apply a Kaufman adaptive moving average to the input, which allow for a smoother output.

No pre-filtering in orange, pre-filtering in yellow, period = 100 for both oscillators.

If you are not aware of the Kaufman adaptive moving average, such moving average return more reactive results when price is trending and smoother results when price is ranging, this also apply for the proposed indicator.

Conclusion

Classical correlation coefficients could use this approach, therefore the linear relationships between any variables could be measured. The fact that the indicator is adaptive add a certain potential, however such combination make the indicator have the drawback of kama + the correlation oscillator, which might appear at certain points.

Thanks for reading !

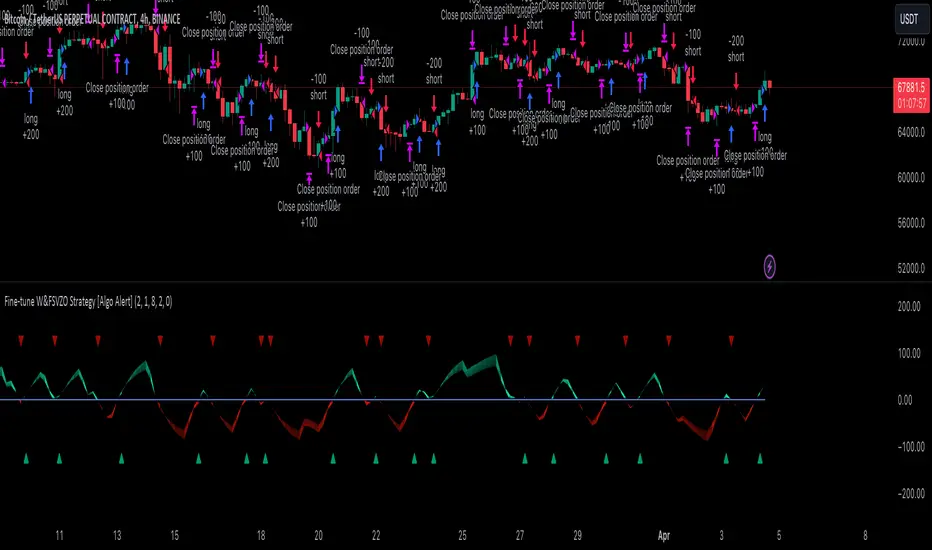

Fine-tune Inputs: Fourier Smoothed Volume zone oscillator WFSVZ0Use this Strategy to Fine-tune inputs for the (W&)FSVZ0 Indicator.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame.

MEANINGFUL DESCRIPTION:

The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Wavelet & Fourier Smoothed Volume Zone Oscillator (W&)FSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the Discrete Fourier Transform . Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Wavalet and Fourier aproximation with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

When I ndicator/Strategy returns 0 or natural trend , Strategy Closes All it's positions.

ORIGINALITY & USFULLNESS:

Personal combination of Fourier and Wavalet aproximation of a price which results in less noise Volume Zone Oscillator.

The Wavelet Transform is a powerful mathematical tool for signal analysis, particularly effective in analyzing signals with varying frequency or non-stationary characteristics. It dissects a signal into wavelets, small waves with varying frequency and limited duration, providing a multi-resolution analysis. This approach captures both frequency and location information, making it especially useful for detecting changes or anomalies in complex signals.

The Discrete Fourier Transform (DFT) is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 and Strategy closes all it's positions when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

In the next Image you can see that trend is negative on 4h, negative on 12h and positive on 1D. That means trend is negative.

I am sorry, the chart is a bit messy. The idea is to use the indicator over more than 1 Timeframe.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Fourier and Wavelet approximation of a close price are taken from aprox library.

Key Features:

You can tailor the Indicator/Strategy to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Fourier Transform (FFT) , the innovative Double Discrete Fourier Transform (DTF32) and Wavelet soothed Fourier soothed price series to suit your analytical needs.

Image of Wavelet transform with FAST settings, Double Fourier transform with FAST settings. Improved noice reduction with SLOW settings, and standard FSVZO with SLOW settings:

Fast setting are setting by default:

VZO length = 2

NoiceR max Length = 2

Slow settings are:

VZO length = 5 or 7

NoiceR max Length = 8

As you can see fast setting are more volatile. I suggest averaging fast setting on 4h 12h 1d 2d 3d 4d W and M Timeframe to get a clear view on market trend.

What if I want long only when VZO is rising and above 15 not 0?

You have set Setting VzoDifference to 15. That reduces the number of trend changes.

Example of W&FSVZO with VzoDifference 15 than 0:

VZO crossed 0 line but not 15 line and that's why Indicator returns 0 in one case an 1 in another.

What is Smooth length setting?

A way of calculating Bullish or Bearish (W&)FSVZO .

If smooth length is 2 the trend is rising if:

rising = VZO > ta.ema(VZO, 2)

Meaning that we check if VZO is higher that exponential average of the last 2 elements.

If smooth length is 1 the trend is rising if:

rising = VZO_ > VZO_

Use this Strategy to fine-tune inputs for the (W&)FSVZO Indicator.

(Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data)

I suggest using " Close all " input False when fine-tuning Inputs for 1 TimeFrame . When you export data to Excel/Numbers/GSheets I suggest using " Close all " input as True , except for the lowest TimeFrame . I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Wavelet & Fourier Smoothed Volume zone oscillator (W&)FSVZO Indicator id:

USER;e7a774913c1242c3b1354334a8ea0f3c

(only relevant to those that use API requests)

MEANINGFUL DESCRIPTION:

The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Wavelet & Fourier Smoothed Volume Zone Oscillator (W&)FSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the Discrete Fourier Transform. Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Wavalet and Fourier aproximation with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in natural trend.

ORIGINALITY & USFULLNESS:

Personal combination of Fourier and Wavalet aproximation of a price which results in less noise Volume Zone Oscillator.

The Wavelet Transform is a powerful mathematical tool for signal analysis, particularly effective in analyzing signals with varying frequency or non-stationary characteristics. It dissects a signal into wavelets, small waves with varying frequency and limited duration, providing a multi-resolution analysis. This approach captures both frequency and location information, making it especially useful for detecting changes or anomalies in complex signals.

The Discrete Fourier Transform (DFT) is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

In the next Image you can see that trend is positive on 4h, neutral on 12h and positive on 1D. That means trend is positive.

I am sorry, the chart is a bit messy. The idea is to use the indicator over more than 1 Timeframe.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Fourier and Wavelet approximation of a close price are taken from aprox library.

Key Features:

You can tailor the indicator to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Fourier Transform (FFT), the innovative Double Discrete Fourier Transform (DTF32) and Wavelet soothed Fourier soothed price series to suit your analytical needs.

Image of Wavelet transform with FAST settings, Double Fourier transform with FAST settings. Improved noice reduction with SLOW settings, and standard FSVZO with SLOW settings:

Fast setting are setting by default:

VZO length = 2

NoiceR max Length = 2

Slow settings are:

VZO length = 5 or 7

NoiceR max Length = 8

As you can see fast setting are more volatile. I suggest averaging fast setting on 4h 12h 1d 2d 3d 4d W and M Timeframe to get a clear view on market trend.

What if I want long only when VZO is rising and above 15 not 0?

You have set Setting VzoDifference to 15. That reduces the number of trend changes.

Example of W&FSVZO with VzoDifference 15 than 0:

VZO crossed 0 line but not 15 line and that's why Indicator returns 0 in one case an 1 in another.

What is Smooth length setting?

A way of calculating Bullish or Bearish FSVZO.

If smooth length is 2 the trend is rising if:

rising = VZO > ta.ema(VZO, 2)

Meaning that we check if VZO is higher that exponential average of the last 2 elements.

If smooth length is 1 the trend is rising if:

rising = VZO_ > VZO_

Rising is boolean value, meaning TRUE if rising and FALSE if falling.

Mathematical equations presented in Pinescript:

Fourier of the real (x axis) discrete:

x_0 = array.get(x, 0) + array.get(x, 1) + array.get(x, 2)

x_1 = array.get(x, 0) + array.get(x, 1) * math.cos( -2 * math.pi * _dir / 3 ) - array.get(y, 1) * math.sin( -2 * math.pi * _dir / 3 ) + array.get(x, 2) * math.cos( -4 * math.pi * _dir / 3 ) - array.get(y, 2) * math.sin( -4 * math.pi * _dir / 3 )

x_2 = array.get(x, 0) + array.get(x, 1) * math.cos( -4 * math.pi * _dir / 3 ) - array.get(y, 1) * math.sin( -4 * math.pi * _dir / 3 ) + array.get(x, 2) * math.cos( -8 * math.pi * _dir / 3 ) - array.get(y, 2) * math.sin( -8 * math.pi * _dir / 3 )

Euler's Noice reduction with both close and Discrete Furrier approximated price.

w = (dft1*src - dft1 *src ) / math.sqrt(math.pow(math.abs(src- src ),2) + math.pow(math.abs(dft1 - dft1 ),2))

filt := na(filt ) ? 0 : c1 * (w*dft1 + nz(w *dft1 )) / 2.0 /math.abs(dft1 -dft1 ) + c2 * nz(filt ) - c3 * nz(filt )

Usecase:

First option:

Select the preferred version of DFT and noise reduction settings based on your analysis requirements.

Leverage the script to identify Bullish and Bearish trends, shown with green and red triangle.

Combine Different Timeframes to accurately determine market trend.

Second option:

Pull the data with API sockets to automate your trading journey.

plot(close, title="ClosePrice", display=display.status_line)

plot(open, title="OpenPrice", display=display.status_line)

plot(greencon ? 1 : redcon ? -1 : 0, title="position", display=display.status_line)

Use ClosePrice, OpenPrice and "position" titles to easily read and backtest your strategy utilising more than 1 Time Frame.

Indicator id:

USER;e7a774913c1242c3b1354334a8ea0f3c

(only relevant to those that use API requests)