Intradayscanner – Institutional Interest (vs. RSP)This indicator measures volatility-adjusted Relative Residual Strength (RRS) of any symbol versus RSP (the Invesco S&P 500® Equal Weight ETF) to surface potential institutional interest overlooked by cap-weighted benchmarks.

Equal-weighted benchmark: Uses RSP instead of SPY, so each S&P 500 component carries equal influence—highlighting broad institutional flows beyond the largest names.

ATR normalization: Computes a “Divergence Index” by dividing RSP’s price move by its ATR(14), then adjusts the symbol’s move by that index and rescales by its own ATR(14). This isolates true outperformance.

Residual focus: RRS represents the portion of a symbol’s move unexplained by broad-market action, making it easier to spot when institutions rotate into specific stocks.

Visualization: Plots RRS as green/red histogram bars and overlays a 14-period EMA for trend smoothing.

Search in scripts for "spy"

Daily GEX Zones & Dashboard by JCThis script plots daily options-driven gamma zones alongside a live sentiment dashboard to help traders visualize dealer positioning, support/resistance clusters, and expected price behavior.

Features:

📅 Date-based GEX Zones: Automatically draws GEX Resistance, GEX Support, Max Pain Zone, and Zero Gamma Line for a specific trading day.

📊 Gamma Flow Dashboard: Displays real-time GEX, DEX, Vanna, and Charm flows using intuitive dropdowns (Negative, Neutral, Positive) — no manual number typing.

🔢 Combo ID Calculation: Combines your gamma flow selections into a single Combo ID, quantifying net positioning pressure.

🎯 Automatic Bias Classification: Instantly highlights whether the day’s gamma structure is likely Pinned/Stable, Unpinned/Wild, Choppy, or Trap/Expansion — color-coded for quick reading.

📈 Zero Gamma Lines: Plots two critical levels where gamma flips from long to short, providing valuable confluence for intraday support/resistance.

How to Use:

1️⃣ Pick your target date (e.g., current day) to activate the GEX boxes.

2️⃣ Enter the day’s Resistance Wall, Support Wall, Max Pain, and Zero Gamma levels from your option chain analysis.

3️⃣ Use the radio-style dropdowns to select sentiment for GEX, DEX, Vanna, and Charm based on your interpretation of open interest, hedging, dealer flow, and market structure.

4️⃣ The dashboard will auto-calculate your Combo ID and bias class.

Designed for:

SPX, SPY, QQQ, NVDA, or any high-liquidity underlying with active options flow.

Active day traders, gamma scalpers, and market makers tracking dealer positioning.

Tip:

Combine with price action levels, VWAP, and intraday structure for high probability trade zones.

All SMAs Bullish/Bearish Screener (Enhanced)All SMAs Bullish/Bearish Screener Enhanced: Uncover High-Conviction Trend Alignments with Confidence

Description:

Are you ready to elevate your trading from mere guesswork to precise, data-driven decisions? The "All SMAs Bullish/Bearish Screener Enhanced" is not just another indicator; it's a sophisticated, yet user-friendly, trend-following powerhouse designed to cut through market noise and pinpoint high-probability trading opportunities. Built on the foundational strength of comprehensive Moving Average confluence and fortified with critical confirmation signals from Momentum, Volume, and Relative Strength, this script empowers you to identify truly robust trends and manage your trades with unparalleled clarity.

The Power of Multi-Factor Confluence: Beyond Simple Averages

In the unpredictable world of financial markets, true strength or weakness is rarely an isolated event. It's the harmonious alignment of multiple technical factors that signals a high-conviction move. While our original "All SMAs Bullish/Bearish Screener" intelligently identified stocks where price was consistently above or below a full spectrum of Simple Moving Averages (5, 10, 20, 50, 100, 200), this Enhanced version takes it a crucial step further.

We've integrated a powerful three-pronged confirmation system to filter out weaker signals and highlight only the most compelling setups:

Momentum (Rate of Change - ROC): A strong trend isn't just about price direction; it's about the speed and intensity of that movement. Positive momentum confirms that buyers are still aggressively pushing price higher (for bullish signals), while negative momentum validates selling pressure (for bearish signals).

Volume: No trend is truly trustworthy without the backing of smart money. Above-average volume accompanying an "All SMAs" alignment signifies strong institutional participation and conviction behind the move. It separates genuine trend starts from speculative whims.

Relative Strength Index (RSI): This versatile oscillator ensures the trend isn't just "there," but that it's developing healthily. We use RSI to confirm a bullish bias (above 50) or a bearish bias (below 50), adding another layer of confidence to the direction.

When the price aligns above ALL six critical SMAs, and is simultaneously confirmed by robust positive momentum, healthy volume, and a bullish RSI bias, you have an exceptionally strong "STRONGLY BULLISH" signal. This confluence often precedes sustained upward moves, signaling prime accumulation phases. Conversely, a "STRONGLY BEARISH" signal, where price is below ALL SMAs with negative momentum, confirming volume, and a bearish RSI bias, indicates powerful distribution and potential for significant downside.

How to Use This Enhanced Screener:

Add to Chart: Go to TradingView's Pine Editor, paste the script, and click "Add to Chart."

Customize Parameters: Fine-tune the lengths of your SMAs, RSI, Momentum, and Volume averages via the indicator's settings. Experiment to find what best suits your trading style and the assets you trade.

Choose Your Timeframe Wisely:

Daily (1D) and 4-Hour (240 min) are highly recommended. These timeframes cut through intraday noise and provide more reliable, actionable signals for swing and position trading.

Shorter timeframes (e.g., 15min, 60min) can be used by advanced day traders for very short-term entries, but be aware of increased volatility and noise.

Visual Confirmation:

Green/Red Triangles: Appear on your chart, indicating confirmed bullish or bearish signals.

Background Color: The chart background will subtly turn lime green for "STRONGLY BULLISH" and red for "STRONGLY BEARISH" conditions.

On-Chart Status Table: A clear table displays the current signal status ("STRONGLY BULLISH/BEARISH," or "SMAs Mixed") for immediate feedback.

Set Up Alerts (Your Primary Screener Tool): This is the game-changer! Create custom alerts on TradingView based on the "Confirmed Bullish Trade" and "Confirmed Bearish Trade" conditions. Receive instant notifications (email, pop-up, mobile) for any stock in your watchlist that meets these stringent criteria. This allows you to scan the entire market effortlessly and act decisively.

Strategic Stop-Loss Placement: The Trader's Lifeline

Even the most robust signals can fail. Protecting your capital is paramount. For this trend-following strategy, your stop-loss should be placed where the underlying trend structure is broken.

For a "STRONGLY BULLISH" Trade: Place your stop-loss just below the most recent significant swing low (higher low). This is the last point where buyers stepped in to support the price. If price breaks below this, your bullish thesis is invalidated.

For a "STRONGLY BEARISH" Trade: Place your stop-loss just above the most recent significant swing high (lower high). If price breaks above this, your bearish thesis is invalidated.

Alternatively, consider placing your stop-loss just below the 20-period SMA (for bullish trades) or above the 20-period SMA (for bearish trades). A significant close beyond this intermediate-term average often indicates a critical shift in momentum. Always ensure your chosen stop-loss adheres to your pre-defined risk per trade (e.g., 1-2% of capital).

Disciplined Profit Booking: Maximizing Gains

Just as important as knowing when you're wrong is knowing when to take profits.

Trailing Stop-Loss: As your trade moves into profit, trail your stop-loss upwards (for longs) or downwards (for shorts). You can trail it using:

Previous Swing Lows/Highs: Move your stop to just below each new higher low (for longs) or just above each new lower high (for shorts).

A Moving Average (e.g., 10-period or 20-period SMA): If price closes below your chosen trailing SMA, exit. This allows you to ride the trend while protecting accumulated profits.

Target Levels: Identify potential resistance levels (for longs) or support levels (for shorts) using pivot points, previous highs/lows, or Fibonacci extensions. Consider taking partial profits at these levels and letting the rest run with a trailing stop.

Loss of Confluence: If the "STRONGLY BULLISH/BEARISH" condition ceases to be met (e.g., RSI crosses below 50, or volume drops significantly), this can be a signal to reduce or exit your position, even if your stop-loss hasn't been hit.

The "All SMAs Bullish/Bearish Screener Enhanced" is your comprehensive partner in navigating the markets. By combining robust trend identification with critical confirmation signals and disciplined risk management, you're equipped to make smarter, more confident trading decisions. Add it to your favorites and unlock a new level of precision in your trading journey!

#PineScript #TradingView #SMA #MovingAverage #TrendFollowing #StockScreener #TechnicalAnalysis #Bullish #Bearish #QQQ #Momentum #Volume #RSI #SPY #TradingStrategy #Enhanced #Signals #Analysis #DayTrading #SwingTrading

SPX Psych Levels for /ES Futures (Fair Value)Overview

This indicator displays S&P 500 psychological levels adjusted for ES futures fair value premium. These levels act as powerful magnets for price action due to the convergence of technical trading and options market dynamics.

What is Fair Value Premium?

Simply put, its the difference between the SPX price and the ES futures price. This changes dynamically based on interest rate, dividends, and time to expiration.

Why Psych Levels are Increasingly Important

Psychological levels are round numbers where traders naturally place orders. These obvious levels attract stop losses, profit targets, and breakout orders from both retail and institutional traders. Algorithms often target these same levels, creating a self-fulfilling prophecy of support and resistance. Importantly, this effect has been exacerbated by the options market.

Using May 2025 as an example, SPX options averaged 3.46 million contracts a day ≈US $1.8 trillion notional, dwarfing trading in SPY or ES/MES futures. 0-day-to-expiry (0DTE) trades hit a record-high 61% share of all SPX volume, making the options complex the primary arena for intraday price discovery.

Strikes at psychological numbers (ending in 00 and 50) captured 66% of total open interest and 58% of 0DTE volume for the entire month. This massive concentration at round number strikes creates powerful hedging flows:

Dealer Gamma Hedging: As price approaches these levels, market makers must dynamically hedge their options exposure, creating reflexive buying/selling pressure

Pin Risk: Options dealers face maximum uncertainty at these levels near expiration, leading to increased hedging activity

Charm Flows: Time decay accelerates near these levels, forcing position adjustments

How It Works

The indicator automatically:

Calculates the fair value premium between ES futures and SPX using real-time interest rate data, dividends, and time to expiration

Adjusts SPX round numbers by this premium to show where they appear on ES charts

Updates once daily at futures session open (5PM CT) to maintain stable reference points throughout the trading session

Key Features

All TradingView Native: All calculations performed automatically using data available within TradingView - no external data feeds or manual updates required

Multiple Level Increments: Display major (100-point), intermediate (50-point), and minor (25-point) psychological levels

Margin of Error Zones: Optional ±2.5 point zones accounting for fair value calculation variance

Full Customization: Colors, line styles, and widths for each level type

Fair Value Info Table: Displays current contract, fair value calculation, interest rate, and days to expiration

Automatic Contract Detection: Works on ES1!/MES1! continuous contracts and automatically detects the current front month contract

Important Notes

This indicator does not access any options data. It identifies levels where options activity naturally concentrates based on market structure. The power comes from understanding that these obvious levels create predictable dealer hedging flows, making them high-probability reaction zones.

Trading Applications

These levels can be used as dynamic areas of interest to be incorporated into a complete trading strategy.

Supply & Demand MTF[E7T]This is not your average supply and demand tool. it’s a powerful, flexible indicator that helps traders spot high-probability opportunities by adapting to real-time market conditions. It uses a smart combination of volatility (ATR), volume, and price action to identify key zones where the market is likely to react. Perfect for scalpers and swing traders alike, this strategy brings together adaptive zone detection, trend bias (pivot line), two-tiered signals (S1 and S2), volume filtering, built-in Fibonacci targets, and even a debug mode for transparency and performance tracking.

KEY FEATURES

1. ADAPTIVE ZONE DETECTION; This feature highlights areas where price is likely to bounce or reversebullish demand zones and bearish supply zones. Instead of using fixed levels, it adjusts based on market volatility.

HOW IT WORKS:

Uses Average True Range (ATR) to measure volatility.

TWO MODES:

Low Volatility Mode: Makes zones tighter for calm markets.

High Volatility Mode: Expands zones during choppy or fast-moving conditions.

Plots red boxes for supply zones and blue for demand zones. Zones extend until broken or naturally expire.

WHY IT MATTERS: Traditional zone indicators often fall short in fast-changing conditions. This one adjusts automatically, helping you stay one step ahead.

EXAMPLE: On a 4H BTCUSD chart, a demand zone will form at a key support level and adjust its size depending on whether the market is quiet or volatile.

2. MARKET BIAS PIVOT LINE; This dynamic line helps you quickly see whether the market is trending up or down so you can trade in the direction of strength.

HOW IT WORKS:

Based on recent swing highs and lows (default: last 4 bars).

Line is green when price is above (bullish), red when below (bearish).

Updates live and can be turned on/off in settings.

WHY IT MATTERS: It’s a built-in trend filter. Use it to avoid fighting the market.

EXAMPLE: If SPY is above a green pivot and enters a demand zone, it’s a solid bullish setup.

3. DUAL ENTRY SIGNALS (S1 and S2) The strategy gives you two signal types depending on your risk style:

S1 SIGNALS: Early entry, based on basic confirmation (like a bullish engulfing pattern).

S2 SIGNALS: Stronger entry, requiring solid candle confirmation, volume spike, and close near the zone.

HOW IT WORKS:

S1 = good for aggressive traders or small size entries.

S2 = better for high-conviction trades and bigger position sizes.

Both signals follow your selected market mood (bullish or bearish).

WHY IT MATTERS: Flexibility! Most indicators only offer one signal style. This one gives you choice.

EXAMPLE: In EURUSD, S1 might show up when price taps a demand zone and forms a small bullish candle. If volume increases and the next candle closes strong, S2 confirms the entry.

4. VOLUME CONFIRMATION This filters out weak signals by checking for real buying/selling interest.

HOW IT WORKS:

Compares current volume to previous bar and a 10–14 bar average.

Adjustable volume thresholds for S1 and S2.

Can be disabled for markets with unreliable volume (like certain forex pairs).

WHY IT MATTERS: It adds a layer of quality control. High-volume moves usually mean higher conviction.

EXAMPLE: On AAPL, an S2 will only trigger if volume jumps by 1.3x the average, signaling strong seller presence.

5. BUILT-IN FIBONACCI TARGETS (TP1, TP2, SL) No more guessing exits. The strategy draws take profit (TP) and stop loss (SL) levels automatically based on zone size.

HOW IT WORKS:

TP1 = 2.12x the zone height

TP2 = 3.3x the zone height

SL = 1x the zone height (all adjustable)

These are shown as dashed (TP) and solid (SL) lines with labels

WHY IT MATTERS: Reduces emotional decision-making. Helps you plan trades with consistent risk/reward.

Example: In GOLD, if the demand zone is $20 tall, TP1 would be ~$42.40 higher, TP2 ~$66 higher, and SL $20 lower.

6. FULLY CUSTOMIZABLE INPUTS Tweak the settings to match your style and asset type.

KEY INPUTS:

Market Mood: Choose bullish (1) or bearish (2)

Timeframe Filter: Focus only on reliable zones (30M or 4H) or can disable to show on every timeframe

Zone Limit: Limit how many zones show (e.g., max 4)

Breakout Buffer: Defines how much price must move to break a zone

Zone Opacity: Make zones more/less visible

WHY IT MATTERS: This lets you dial in the indicator for scalping, swing trading, crypto, stocks, or forex.

Example: A scalper might use tighter zones and a low breakout buffer, while a swing trader prefers more zones and higher volatility mode.

7. DEBUG MODE (Optional) Get under the hood and see exactly how the strategy works.

HOW IT WORKS:

Shows metrics like ATR, volatility mode, memory usage, signal win rate, etc.

Plots visual lines showing zone age and success rate (TP1 hit tracking)

WHY IT MATTERS: Very few indicators show their math. This one does—great for power users who want to optimize.

EXAMPLE: You might discover that signals perform best in high volatility mode during news events, helping you adjust settings accordingly.

HOW TO USE IT

1. Add it to your TradingView chart (30M or 4H timeframes recommended).

2. Adjust inputs:

Market Mood = 1 (bullish) or 2 (bearish)

Pick your Volatility Mode

Set Zone Collector Limit (3–4 works well)

Use Timeframe Filter for better signals

3. Watch for S1 and S2:

S1 = quicker trades, lighter risk

S2 = stronger confirmation, bigger trades

4. Use the Pivot Line for trade direction.

5. Manage exits with auto TP/SL levels.

6. Turn on Debug Mode if you want detailed stats.

WORKS VERY WELL WITHOUT REPAINTING

Why It’s a Game-Changer; IT takes the guesswork out of zone trading. It’s not just smart—it’s adaptive. From volatility and volume to dynamic signals and exit plans, everything adjusts based on what the market is doing. And with a built-in trend filter and real-time debug info, it’s like having a trading co-pilot that’s always alert.

Why It’s Different Most zone indicators are basic. This one isn’t. Here’s why:

Adaptive zones that change with the market

Dual signal system (S1/S2) for flexibility

Volume confirmation to filter noise

Built-in Fibonacci targets for clean exits

Debug mode that shows you how it works

YOU CAN SET ALERTS WITHOUT repainting

THIS isn’t just another tool—it’s a smarter, more responsive way to trade.

Mongoose Conflict Risk Radar v1.1 (Separate Panel) description

The Mongoose Capital: Risk Rotation Index is a macro market sentiment tool designed to detect elevated risk conditions by aggregating signals across key asset classes.

This script evaluates trend strength across 8 ETFs representing major risk-on and risk-off flows:

GLD – Gold

VIXY – Volatility

TLT – Long-Term Bonds

SPY – S&P 500

UUP – U.S. Dollar Index

EEM – Emerging Markets

SLV – Silver

FXI – China Large-Cap

Each asset is assigned a binary signal based on price position vs. its 21-period SMA (or a crossover for bonds). The signals are then totaled into a composite Risk Rotation Score, plotted as a bar graph.

How to Use

0–2 = Low risk-on behavior

3–4 = Caution / Mixed regime

5–8 = Elevated conflict or macro stress

Use this as a macro confirmation layer for trend entries, risk reduction, or allocation shifts.

Alerts

Set alerts when the index exceeds 5 to track major rotations into defensive assets.

ORB IndicatorORB – Opening Range Breakout Strength (Applies to First 2 Bars Only)

The ORB (Opening Range Breakout) indicator is a momentum-based tool designed to highlight potential long trade opportunities during the first two candles of the regular trading session. It’s built to detect early strength by filtering for clean bullish price action and relative outperformance against a benchmark index.

🔍 Signal Criteria

A blue triangle is plotted at the close of the candle if the following conditions are met:

The candle is bullish (close > open)

The body makes up at least 60% of the total candle range

The candle occurs during the first or second bar after session start (default: 9:30 AM)

The candle shows greater range strength (in %) than a benchmark symbol (e.g., QQQ or SPY), scaled by a configurable multiplier

⚙️ Customizable Settings

Benchmark Ticker: Choose any symbol (default: NASDAQ:QQQ)

Range Multiplier: Adjust the strength threshold relative to the benchmark’s range

Session Start Time: Set the hour and minute to match your market’s open

📈 Features

Visual signal: blue triangle below the bar

Alert-ready: Get notified instantly when a valid ORB setup appears

Executes only at bar close to ensure confirmed signal

Distribution & Accumulation Days# Distribution & Accumulation Days Indicator

## Overview

This powerful institutional activity tracker identifies **Distribution Days** (selling pressure) and **Accumulation Days** (buying pressure) based on the proven methodology used by Investor's Business Daily (IBD). Perfect for detecting when "smart money" institutions are actively buying or selling, helping you align your trades with institutional flow.

## What It Does

- **Distribution Days**: Identifies days when price drops significantly on higher volume (institutional selling)

- **Accumulation Days**: Identifies days when price rises significantly on higher volume (institutional buying)

- **Real-time Counting**: Tracks the number of each type over your specified lookback period

- **Net Analysis**: Shows whether buying or selling pressure is dominant

## Key Features

### 🎯 **Customizable Threshold**

- Set your own price change percentage (default 0.2%) to filter out minor moves

- Focus only on significant institutional activity

### 📊 **Moving Average Filter**

- Optional MA filter to eliminate noise during strong downtrends

- Choose from SMA, WMA, or EMA

- Only counts signals when price is above the moving average

### 📈 **Visual Markers**

- **Red 'D'** markers above bars = Distribution (selling pressure)

- **Green 'A'** markers below bars = Accumulation (buying pressure)

- Numbers show current count within your lookback period

### 📋 **Information Dashboard**

Real-time table displays:

- Total Distribution Days in period

- Total Accumulation Days in period

- Net difference (positive = more buying, negative = more selling)

## How to Use

### Market Analysis

- **4-5 Distribution Days** in 25 sessions = Potential market weakness

- **Multiple Accumulation Days** after decline = Potential bottom formation

- **Net positive** = Institutional buying dominance

- **Net negative** = Institutional selling dominance

### Trade Setup

- Look for accumulation clusters near support levels for long entries

- Watch for distribution clusters near resistance for potential short setups

- Use in conjunction with your existing technical analysis

## Settings

| Parameter | Description | Default |

|-----------|-------------|---------|

| Days Back | Lookback period for counting | 25 |

| Price Change Threshold | Minimum % move required | 0.2% |

| Moving Average Filter | Enable/disable MA filter | Off |

| MA Type | SMA, WMA, or EMA | EMA |

| MA Length | Moving average period | 50 |

## Best Practices

- Use on **daily timeframe only** (automatically restricts to daily)

- Works best on major indices (SPY, QQQ, IWM) and liquid stocks

- Combine with support/resistance levels for better entries

- Monitor both individual counts and net difference for complete picture

## Important Notes

- Based on proven IBD methodology used by professional traders

- Requires significant volume confirmation - price moves without volume are ignored

- Most effective when used as part of a complete trading system

- Works only on daily charts (designed for institutional timeframe analysis)

---

*This indicator helps you see the market through institutional eyes. When the big players are buying or selling, you'll know.*

**Tags**: Distribution, Accumulation, IBD, Institutional, Volume Analysis, Smart Money, Market Structure

Yelober - Sector Rotation Detector# Yelober - Sector Rotation Detector: User Guide

## Overview

The Yelober - Sector Rotation Detector is a TradingView indicator designed to track sector performance and identify market rotations in real-time. It monitors key sector ETFs, calculates performance metrics, and provides actionable stock recommendations based on sector strength and weakness.

## Purpose

This indicator helps traders identify when capital is moving from one sector to another (sector rotation), which can provide valuable trading opportunities. It also detects risk-off conditions in the market and highlights sectors with abnormal trading volume.

## Table Columns Explained

### 1. Sector

Displays the sector name being monitored. The indicator tracks six primary sectors plus the S&P 500:

- Energy (XLE)

- Financial (XLF)

- Technology (XLK)

- Consumer Staples (XLP)

- Utilities (XLU)

- Consumer Discretionary (XLY)

- S&P 500 (SPY)

### 2. Perf %

Shows the daily percentage performance of each sector ETF. Values are color-coded:

- Green: Positive performance

- Red: Negative performance

Positive values display with a "+" sign (e.g., +1.25%)

### 3. RSI

Displays the Relative Strength Index value for each sector, which helps identify overbought or oversold conditions:

- Values above 70 (highlighted in red): Potentially overbought

- Values below 30 (highlighted in green): Potentially oversold

- Values between 30-70 (highlighted in blue): Neutral territory

### 4. Vol Ratio

Shows the volume ratio, which compares today's volume to the average volume over the lookback period:

- Values above 1.5x (highlighted in yellow): Indicates abnormally high trading volume

- Values below 1.5x (highlighted in blue): Normal trading volume

This helps identify sectors with unusual activity that may signal important price movements.

### 5. Trend

Displays the current price trend direction with symbols:

- ▲ (green): Uptrend (today's close > yesterday's close)

- ▼ (red): Downtrend (today's close < yesterday's close)

- ◆ (gray): Neutral (today's close = yesterday's close)

## Summary & Recommendations Section

The summary section provides:

1. **Sector Rotation Detection**: Identifies when there's a significant performance gap (>2%) between the strongest and weakest sectors.

2. **Risk-Off Mode Detection**: Alerts when defensive sectors (Consumer Staples and Utilities) are positive while Technology is negative, which often signals investors are moving to safer assets.

3. **Strong Volume Detection**: Indicates when any sector shows abnormally high trading volume.

4. **Stock Recommendations**: Suggests specific stocks to consider for long positions (from the strongest sectors) and short positions (from the weakest sectors).

## Example Interpretations

### Example 1: Sector Rotation

If you see:

- Technology: -1.85%

- Financial: +2.10%

- Summary shows: "SECTOR ROTATION DETECTED: Rotation from Technology to Financial"

**Interpretation**: Capital is moving out of tech stocks and into financial stocks. This could be due to rising interest rates, which typically benefit banks while pressuring high-growth tech companies. Consider looking at financial stocks like JPM, BAC, and WFC for potential long positions.

### Example 2: Risk-Off Conditions

If you see:

- Consumer Staples: +0.80%

- Utilities: +1.20%

- Technology: -1.50%

- Summary shows: "RISK-OFF MODE DETECTED"

**Interpretation**: Investors are seeking safety in defensive sectors while selling growth-oriented tech stocks. This often occurs during market uncertainty or ahead of economic concerns. Consider reducing exposure to high-beta stocks and possibly adding defensive names like PG, KO, or NEE.

### Example 3: Volume Spike

If you see:

- Energy: +3.20% with Volume Ratio 2.5x (highlighted in yellow)

- Summary shows: "STRONG VOLUME DETECTED"

**Interpretation**: The energy sector is making a strong move with significantly higher-than-average volume, suggesting conviction behind the price movement. This could indicate the beginning of a sustained trend in energy stocks. Consider names like XOM, CVX, and COP.

## How to Use the Indicator

1. Apply the indicator to any chart (works best on daily timeframes).

2. Customize settings if needed:

- Timeframe: Choose between intraday (60 or 240 minutes), daily, or weekly

- Lookback Period: Adjust the historical comparison period (default: 20)

- RSI Period: Modify the RSI calculation period (default: 14)

3. To refresh the data: Click the settings icon, increase the "Click + to refresh data" counter, and click "OK".

4. Identify opportunities based on sector performance, RSI levels, volume ratios, and the summary recommendations.

This indicator helps traders align with market rotation trends and identify which sectors (and specific stocks) may outperform or underperform in the near term.

SHYY TFC SPX Sectors list This script provides a clean, configurable table displaying real-time data for the major SPX sectors, key indices, and market sentiment indicators such as VIX and the 10-year yield (US10Y).

It includes 16 columns with two rows:

* The top row shows the sector/asset symbol.

* The bottom row shows the most recent daily close price.

Each price cell is dynamically color-coded based on:

* Direction (green/red) during regular trading hours

* Separate colors during extended hours (pre-market or post-market)

* VIX values greater than 30 trigger a distinct background highlight

Users can fully control the position of the table on the chart via input settings. This flexibility allows traders to place the table in any screen corner or center without overlapping key price action.

The script is designed for:

* Monitoring broad market health at a glance

* Understanding sector performance in real-time

* Spotting risk-on/risk-off behavior (via SPY, QQQ, VIX, US10Y)

Unlike traditional watchlists, this table visually encodes directional movement and trading session context (regular vs. extended hours), making it highly actionable for intraday, swing, or macro-level analysis.

All data is pulled using `request.security()` on daily candles and uses pure Pine logic without external dependencies.

To use:

1. Add the indicator to your chart.

2. Adjust the table position via the input dropdown.

3. Read sector strength or weakness directly from the table.

Options Betting Range - FixedOptions Betting Range

Options Betting Range is a powerful TradingView indicator designed to streamline options trading by visualizing high-probability price ranges for key symbols. With automated trendlines and clear labels, it empowers traders to make precise, data-driven decisions based on customizable prediction and execution dates.

## Key Features

Broad S&P 500 Coverage: Supports most S&P 500 stock symbols, excluding those with insufficient options volume for reliable data, alongside major ETFs and indices like SPY, IWM, QQQ, DIA, TLT, ^GSPC, ^IXIC, ^RUT, ^NDX, and ^SOX.

Automated Trendlines: Plots dashed and solid trendlines to mark high/low price boundaries, triggered only on specified prediction dates for clean, uncluttered charts.

Customizable Inputs: Configure prediction and execution dates to align with your trading strategy.

Clear Visuals: Color-coded labels (green for highs, purple for lows) display price ranges and percentage spreads for rapid decision-making.

Single-Execution Logic: Draws trendlines once per prediction date, ensuring chart clarity and efficiency.

## How It Works

Based on the latest daily open interest data, the indicator calculates swing ranges for different strike dates, drawing trendlines and labels to visualize potential price boundaries for options trading.

## Why Use It?

Streamlined Analysis: Automates range visualization, saving time and reducing manual charting.

Strategic Clarity: Objective price levels minimize emotional bias and enhance trade planning.

Versatile Application: Ideal for day traders, swing traders, and options strategists across multiple markets.

## Tips for Best Use

Regular Updates: To maintain the accuracy of options betting ranges, periodically update the indicator. On the view page, hover over the indicator name and click the blue whirlwind icon to complete the update.

## Get Started

Add Options Betting Range to your TradingView chart, select a supported symbol, and customize your prediction/execution dates. Leverage the visualized price ranges to execute precise options trading strategies with confidence.

BBS – Bond Breadth Signal"When bonds scream, breadth collapses, and fear spikes — BBS listens."

🧠 BBS – Bond Breadth Signal

A reversal timing tool built on macro conviction, not price noise.

The Bond Breadth Signal (BBS) was developed to identify major market inflection points by combining four key market stress indicators:

1) 10-Year Yield ROC – Measures sharp moves in the bond market

2) Z-Score of the 10Y – Captures statistical extremes

3) NSHF (Net Highs–Lows) – Signals internal market strength or weakness

4) TLT ROC + VIX – Confirmations of flight to safety and volatility-driven fear

When all conditions align, BBS marks either a For-Sure Buy or For-Sure Sell — these are rare, high-confidence signals designed to cut through noise and focus on true market dislocations.

🔧 Features:

-Background color and signal arrows on confirmation days

-Signals remain visually active for 3 days for added clarity

-Fully adjustable thresholds and alert toggles

-Plot panel for yield, TLT, NSHF, VIX, and Z-score visuals

This tool isn’t designed to fire every day. It’s meant to wait for those moments when the market truly bends — not just wiggles.

Best used on major indices (SPY, QQQ, IWM) to assess macro turning points.

Single MA Pullback – Producers TradeHow to Use the “Single MA Pullback – Producers Trade” Indicator

This indicator helps options traders identify high-probability CALL and PUT signals based on price reacting to a single moving average.

⸻

✅ How It Works

• Select your preferred MA type (EMA, SMA, WMA, VWMA) and length.

• A Buy signal (CALL) is generated when price crosses above the MA.

• A Sell signal (PUT) is generated when price crosses below the MA.

• Visual arrows mark each signal, and a label suggests an option contract with strike and expiration.

⸻

🧠 Features

• Strike prices are automatically calculated ~1% out of the money.

• Expiration dates target the next Friday, based on the current day of the week.

• Symbol-specific strike rounding (e.g., 1 for SPY/XSP, 5 for most stocks).

⸻

📆 Expiration Date Notes

• Expiration dates shown in the label are based on a best-estimate to the next Friday.

• Depending on the time of day or day of week, the date may be off by one day.

• Always verify expiration dates on your trading platform before placing a trade.

⸻

📌 Important Tip on Expiration

A further out expiration is almost always a better idea — especially for:

• Avoiding time decay (theta)

• Holding through small pullbacks

• Letting your trade develop with less pressure

Even when the label suggests a short-dated contract, you can manually choose a longer expiration (e.g., 2–3 weeks out) for added safety and flexibility.

⸻

📈 Trading Suggestions

1. Green arrow = CALL setup. Red arrow = PUT setup.

2. Labels include trade type, strike price, and suggested expiration.

3. Confirm the signal with volume, price structure, or catalyst.

4. Manage your risk with proper sizing and optional stop-loss/target planning.

$ADD LevelsThis Pine Script is designed to track and visualize the NYSE Advance-Decline Line (ADD). The Advance-Decline Line is a popular market breadth indicator, showing the difference between advancing and declining stocks on the NYSE. It’s often used to gauge overall market sentiment and strength.

1. //@version=5

This line tells TradingView to use Pine Script v5, the latest and most powerful version of Pine.

2. indicator(" USI:ADD Levels", overlay=false)

• This creates a new indicator called ” USI:ADD Levels”.

• overlay=false means it will appear in a separate pane, not on the main price chart.

3. add = request.security(...)

This fetches real-time data from the symbol USI:ADD (Advance-Decline Line) using a 1-minute timeframe. You can change the timeframe if needed.

add_symbol = input.symbol(" USI:ADD ", "Market Breadth Symbol")

add = request.security(add_symbol, "1", close)

4. Key Thresholds

These define the market sentiment zones:

Zone. Value. Meaning

Overbought +1500 Extremely bullish

Bullish +1000 Generally bullish trend

Neutral ±500 Choppy, unclear market

Bearish -1000 Generally bearish trend

Oversold -1500 Extremely bearish

5. Plot the ADD Line hline(...)

Draws static lines at +1500, +1000, +500, -500, -1000, -1500 for reference so you can visually assess where ADD stands.

6. Horizontal Threshold Lines bgcolor(...)

• Green background if ADD > +1500 → extremely bullish.

• Red background if ADD < -1500 → extremely bearish.

7. Background Highlights alertcondition(...)

• Green background if ADD > +1500 → extremely bullish.

• Red background if ADD < -1500 → extremely bearish.

8. Alert Conditions. alertcondition(...)

Lets you create automatic alerts for:

• USI:ADD being very high or low.

• Crosses above +1000 (bullish trigger).

• Crosses below -1000 (bearish trigger).

You can use these to trigger trades or monitor sentiment shifts.

Summary: When to Use It

• Use this script in a market breadth dashboard.

• Combine it with price action and volume analysis.

• Monitor for ADD crosses to signal potential market reversals or momentum.

RRC Sniper SetupRRC Sniper Setup, this looks at candles this way:

Go to Market Scanner

Create New Scan → "RRC Sniper Setup"

Add filters listed below with timeframe logic (e.g. 1m/5m)

Run scan on:

Your Watchlist

SPY 500

QQQ 100

AI/Momentum names

1. Reclaim Filter

Find price breaking back above a key level (VWAP or EMA113)

Last 1m Close > EMA 113 (1m)

OR

Last 5m Close > VWAP

2. Retrace Filter

Price pulls back into the zone and holds within a tight range

Current Price < VWAP * 1.0025

AND

Current Price > VWAP * 0.9975

AND

Volume (Current Candle) < Volume (Previous Candle)

✅ 3. Confirm Filter

Price begins moving back up with confirmation candle and volume

Last Candle Close > Last Candle Open

AND

Volume (Current Candle) > Volume (Previous Candle)

Multi-Session ORBThe Multi-Session ORB Indicator is a customizable Pine Script (version 6) tool designed for TradingView to plot Opening Range Breakout (ORB) levels across four major trading sessions: Sydney, Tokyo, London, and New York. It allows traders to define specific ORB durations and session times in Central Daylight Time (CDT), making it adaptable to various trading strategies.

Key Features:

1. Customizable ORB Duration: Users can set the ORB duration (default: 15 minutes) via the inputMax parameter, determining the time window for calculating the high and low of each session’s opening range.

2. Flexible Session Times: The indicator supports user-defined session and ORB times for:

◦ Sydney: Default ORB (17:00–17:15 CDT), Session (17:00–01:00 CDT)

◦ Tokyo: Default ORB (19:00–19:15 CDT), Session (19:00–04:00 CDT)

◦ London: Default ORB (02:00–02:15 CDT), Session (02:00–11:00 CDT)

◦ New York: Default ORB (08:30–08:45 CDT), Session (08:30–16:00 CDT)

3. Session-Specific ORB Levels: For each session, the indicator calculates and tracks the high and low prices during the specified ORB period. These levels are updated dynamically if new highs or lows occur within the ORB timeframe.

4. Visual Representation:

◦ ORB high and low lines are plotted only during their respective session times, ensuring clarity.

◦ Each session’s lines are color-coded for easy identification:

▪ Sydney: Light Yellow (high), Dark Yellow (low)

▪ Tokyo: Light Pink (high), Dark Pink (low)

▪ London: Light Blue (high), Dark Blue (low)

▪ New York: Light Purple (high), Dark Purple (low)

◦ Lines are drawn with a linewidth of 2 and disappear when the session ends or if the timeframe is not intraday (or exceeds the ORB duration).

5. Intraday Compatibility: The indicator is optimized for intraday timeframes (e.g., 1-minute to 15-minute charts) and only displays when the chart’s timeframe multiplier is less than or equal to the ORB duration.

How It Works:

• Session Detection: The script uses the time() function to check if the current bar falls within the user-defined ORB or session time windows, accounting for all days of the week.

• ORB Logic: At the start of each session’s ORB period, the script initializes the high and low based on the first bar’s prices. It then updates these levels if subsequent bars within the ORB period exceed the current high or fall below the current low.

• Plotting: ORB levels are plotted as horizontal lines during the respective session, with visibility controlled to avoid clutter outside session times or on incompatible timeframes.

Use Case:

Traders can use this indicator to identify key breakout levels for each trading session, facilitating strategies based on price action around the opening range. The flexibility to adjust ORB and session times makes it suitable for various markets (e.g., forex, stocks, or futures) and time zones.

Limitations:

• The indicator is designed for intraday timeframes and may not display on higher timeframes (e.g., daily or weekly) or if the timeframe multiplier exceeds the ORB duration.

• Time inputs are in CDT, requiring users to adjust for their local timezone or market requirements.

• If you need to use this for GC/CL/SPY/QQQ you have to adjust the times by one hour.

This indicator is ideal for traders focusing on session-based breakout strategies, offering clear visualization and customization for global market sessions.

Symbol Seasonality Matrix (w/ BTC Base) Symbol Seasonality Matrix (w/ BTC Base)

Compare monthly performance between Bitcoin and any symbol across time

🧠 Overview

This indicator provides a side-by-side monthly return table of Bitcoin (BTCUSD from Bitfinex) and any selected symbol (e.g., ETH, stocks, etc.). It visualizes seasonality patterns, historical performance shifts, and relative trends in a clean matrix layout with dynamic line overlays.

⚙️ Mechanism

BTC Benchmarking:

BTC monthly returns are always shown as a benchmark against the selected chart symbol.

Monthly ROI Calculation:

For each month, the indicator tracks the open and close price and calculates the monthly return using:

(close_end - close_start) / close_start × 100%

It stores both price and return for BTC and the chart symbol.

Table Structure:

Each year is split into two halves:

2023 (Jan ~ Jun) and 2023 (Jul ~ Dec) for clarity.

Color Coding:

Green for positive months

Red for negative months

Monthly trend lines and labels drawn in consistent colors

Background shading per month helps track seasonality

Plot Modes:

regular: raw price

percent: relative % change from the start of selected period

normalized: base=1 scaling to compare trends

Time Range Selector:

You can define start time and end time for comparison — all logic, including table, plots, and highlights, will focus only on this window.

🧭 How to Use

Set the time range:

Choose a meaningful window such as the past 3 years or 2018–2021 to study behavior.

Compare Symbol vs BTC:

Load BTCUSD in a separate chart for baseline.

Switch to ETHUSD, SPY, or any altcoin/equity to view overlayed performance.

Analyze Seasonality:

Look for months with repeated strong/weak performance (e.g., BTC strong in October).

Compare how your asset aligns with BTC trends or diverges.

Choose View Mode:

Use percent to adjust Y-axis scaling and directly compare relative movements.

Use normalized to detect trend correlation without caring about price level.

🔍 Why It’s Useful

Spot seasonal alpha and align entries with favorable months

See if a symbol outperforms or underperforms BTC consistently

Get price-to-return context visually, not just via numbers

Quickly compare assets in real scale or normalized scale

📌 Tip

Try publishing this to a layout with multiple tickers (ETH, SOL, AAPL) to instantly switch comparisons.

Pair with volume-based or macro indicators to layer signals.

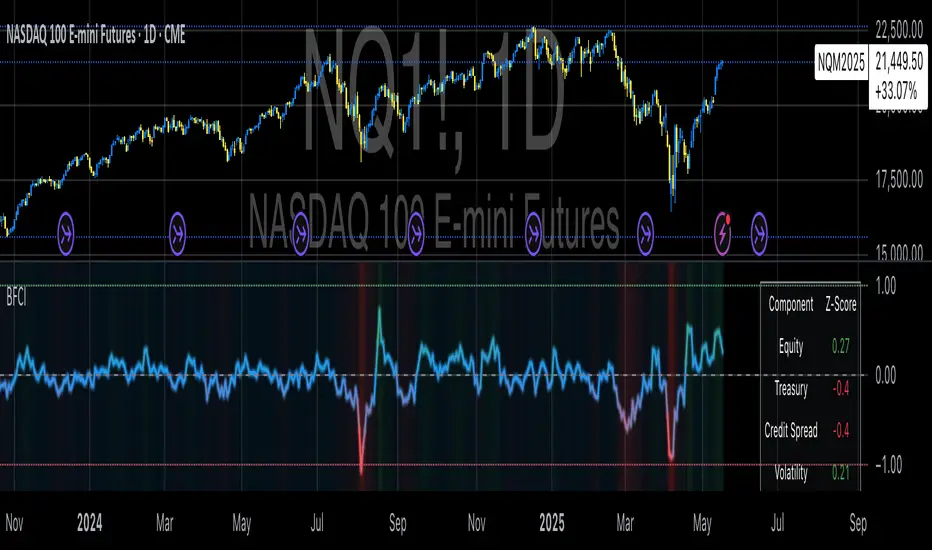

Bloomberg Financial Conditions Index (Proxy)The Bloomberg Financial Conditions Index (BFCI): A Proxy Implementation

Financial conditions indices (FCIs) have become essential tools for economists, policymakers, and market participants seeking to quantify and monitor the overall state of financial markets. Among these measures, the Bloomberg Financial Conditions Index (BFCI) has emerged as a particularly influential metric. Originally developed by Bloomberg L.P., the BFCI provides a comprehensive assessment of stress or ease in financial markets by aggregating various market-based indicators into a single, standardized value (Hatzius et al., 2010).

The original Bloomberg Financial Conditions Index synthesizes approximately 50 different financial market variables, including money market indicators, bond market spreads, equity market valuations, and volatility measures. These variables are normalized using a Z-score methodology, weighted according to their relative importance to overall financial conditions, and then aggregated to produce a composite index (Carlson et al., 2014). The resulting measure is centered around zero, with positive values indicating accommodative financial conditions and negative values representing tighter conditions relative to historical norms.

As Angelopoulou et al. (2014) note, financial conditions indices like the BFCI serve as forward-looking indicators that can signal potential economic developments before they manifest in traditional macroeconomic data. Research by Adrian et al. (2019) demonstrates that deteriorating financial conditions, as measured by indices such as the BFCI, often precede economic downturns by several months, making these indices valuable tools for predicting changes in economic activity.

Proxy Implementation Approach

The implementation presented in this Pine Script indicator represents a proxy of the original Bloomberg Financial Conditions Index, attempting to capture its essential features while acknowledging several significant constraints. Most critically, while the original BFCI incorporates approximately 50 financial variables, this proxy version utilizes only six key market components due to data accessibility limitations within the TradingView platform.

These components include:

Equity market performance (using SPY as a proxy for S&P 500)

Bond market yields (using TLT as a proxy for 20+ year Treasury yields)

Credit spreads (using the ratio between LQD and HYG as a proxy for investment-grade to high-yield spreads)

Market volatility (using VIX directly)

Short-term liquidity conditions (using SHY relative to equity prices as a proxy)

Each component is transformed into a Z-score based on log returns, weighted according to approximated importance (with weights derived from literature on financial conditions indices by Brave and Butters, 2011), and aggregated into a composite measure.

Differences from the Original BFCI

The methodology employed in this proxy differs from the original BFCI in several important ways. First, the variable selection is necessarily limited compared to Bloomberg's comprehensive approach. Second, the proxy relies on ETFs and publicly available indices rather than direct market rates and spreads used in the original. Third, the weighting scheme, while informed by academic literature, is simplified compared to Bloomberg's proprietary methodology, which may employ more sophisticated statistical techniques such as principal component analysis (Kliesen et al., 2012).

These differences mean that while the proxy BFCI captures the general direction and magnitude of financial conditions, it may not perfectly replicate the precision or sensitivity of the original index. As Aramonte et al. (2013) suggest, simplified proxies of financial conditions indices typically capture broad movements in financial conditions but may miss nuanced shifts in specific market segments that more comprehensive indices detect.

Practical Applications and Limitations

Despite these limitations, research by Arregui et al. (2018) indicates that even simplified financial conditions indices constructed from a limited set of variables can provide valuable signals about market stress and future economic activity. The proxy BFCI implemented here still offers significant insight into the relative ease or tightness of financial conditions, particularly during periods of market stress when correlations among financial variables tend to increase (Rey, 2015).

In practical applications, users should interpret this proxy BFCI as a directional indicator rather than an exact replication of Bloomberg's proprietary index. When the index moves substantially into negative territory, it suggests deteriorating financial conditions that may precede economic weakness. Conversely, strongly positive readings indicate unusually accommodative financial conditions that might support economic expansion but potentially also signal excessive risk-taking behavior in markets (López-Salido et al., 2017).

The visual implementation employs a color gradient system that enhances interpretation, with blue representing neutral conditions, green indicating accommodative conditions, and red signaling tightening conditions—a design choice informed by research on optimal data visualization in financial contexts (Few, 2009).

References

Adrian, T., Boyarchenko, N. and Giannone, D. (2019) 'Vulnerable Growth', American Economic Review, 109(4), pp. 1263-1289.

Angelopoulou, E., Balfoussia, H. and Gibson, H. (2014) 'Building a financial conditions index for the euro area and selected euro area countries: what does it tell us about the crisis?', Economic Modelling, 38, pp. 392-403.

Aramonte, S., Rosen, S. and Schindler, J. (2013) 'Assessing and Combining Financial Conditions Indexes', Finance and Economics Discussion Series, Federal Reserve Board, Washington, D.C.

Arregui, N., Elekdag, S., Gelos, G., Lafarguette, R. and Seneviratne, D. (2018) 'Can Countries Manage Their Financial Conditions Amid Globalization?', IMF Working Paper No. 18/15.

Brave, S. and Butters, R. (2011) 'Monitoring financial stability: A financial conditions index approach', Economic Perspectives, Federal Reserve Bank of Chicago, 35(1), pp. 22-43.

Carlson, M., Lewis, K. and Nelson, W. (2014) 'Using policy intervention to identify financial stress', International Journal of Finance & Economics, 19(1), pp. 59-72.

Few, S. (2009) Now You See It: Simple Visualization Techniques for Quantitative Analysis. Analytics Press, Oakland, CA.

Hatzius, J., Hooper, P., Mishkin, F., Schoenholtz, K. and Watson, M. (2010) 'Financial Conditions Indexes: A Fresh Look after the Financial Crisis', NBER Working Paper No. 16150.

Kliesen, K., Owyang, M. and Vermann, E. (2012) 'Disentangling Diverse Measures: A Survey of Financial Stress Indexes', Federal Reserve Bank of St. Louis Review, 94(5), pp. 369-397.

López-Salido, D., Stein, J. and Zakrajšek, E. (2017) 'Credit-Market Sentiment and the Business Cycle', The Quarterly Journal of Economics, 132(3), pp. 1373-1426.

Rey, H. (2015) 'Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence', NBER Working Paper No. 21162.

VWAP Adaptive (RelVol-Adjusted)This indicator provides an Adaptive VWAP that adjusts volume weighting using RelVol (Relative Volume at Time), offering a more accurate and context-aware price reference during sessions with irregular volume behavior.

Classic VWAP calculates the average price weighted by raw volume, without considering the time of day. This becomes a serious limitation during major market events such as CPI releases, FOMC announcements, NFP, or large-cap earnings. These events often trigger massive volume spikes within one or two candles. As a result, the classic VWAP gets pulled toward those extreme prices and becomes permanently skewed for the rest of the session.

In such conditions, classic VWAP becomes unreliable. It no longer reflects fair value and often misleads traders relying on it for dynamic support, resistance, or reversion signals.

This Adaptive VWAP improves on that by using RelVol, which compares the current volume to the average volume seen at the same time over previous sessions. It gives more weight to price when volume is typical for that moment, and adjusts the influence when volume is statistically abnormal. This reduces the impact of isolated volume spikes and stabilizes the VWAP path, even in high-volatility environments.

For example, on SPY 1-minute or 5-minute charts during a CPI release, a massive spike in volume and price can occur within a single candle. Classic VWAP will immediately anchor itself to that spike. Adaptive VWAP using RelVol softens that effect and maintains a more realistic trajectory.

Key features:

- Adaptive VWAP weighted by time-adjusted Relative Volume (RelVol)

- Designed to maintain VWAP reliability during macroeconomic events

- Flexible anchoring: Session, Week, Month, Quarter, Earnings, etc.

- Optional display of Classic VWAP for comparison

- Up to 3 customizable deviation bands (standard deviation or percentage)

This tool is ideal for intraday traders who need a VWAP that remains usable and unbiased, even in volatile sessions. It adds robustness to VWAP-based strategies by incorporating time-sensitive volume normalization.

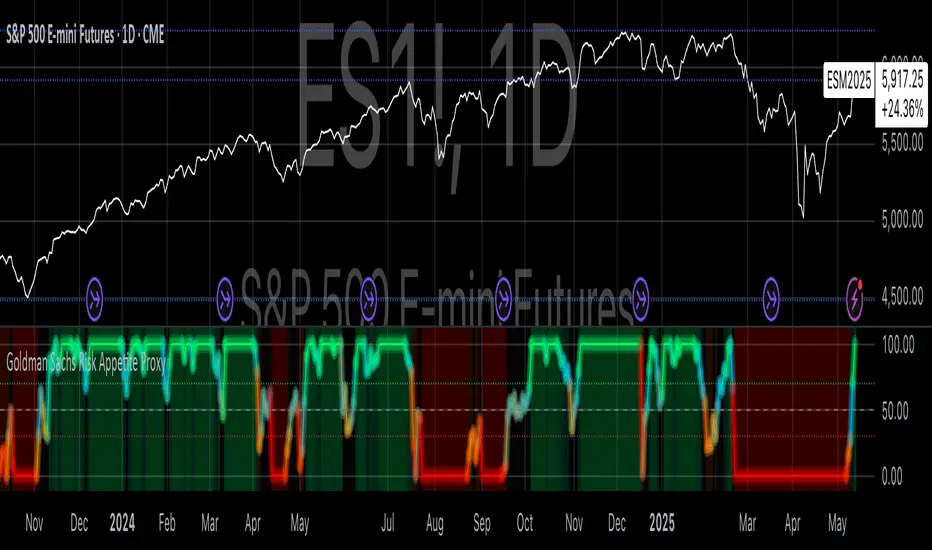

Goldman Sachs Risk Appetite ProxyRisk appetite indicators serve as barometers of market psychology, measuring investors' collective willingness to engage in risk-taking behavior. According to Mosley & Singer (2008), "cross-asset risk sentiment indicators provide valuable leading signals for market direction by capturing the underlying psychological state of market participants before it fully manifests in price action."

The GSRAI methodology aligns with modern portfolio theory, which emphasizes the importance of cross-asset correlations during different market regimes. As noted by Ang & Bekaert (2002), "asset correlations tend to increase during market stress, exhibiting asymmetric patterns that can be captured through multi-asset sentiment indicators."

Implementation Methodology

Component Selection

Our implementation follows the core framework outlined by Goldman Sachs research, focusing on four key components:

Credit Spreads (High Yield Credit Spread)

As noted by Duca et al. (2016), "credit spreads provide a market-based assessment of default risk and function as an effective barometer of economic uncertainty." Higher spreads generally indicate deteriorating risk appetite.

Volatility Measures (VIX)

Baker & Wurgler (2006) established that "implied volatility serves as a direct measure of market fear and uncertainty." The VIX, often called the "fear gauge," maintains an inverse relationship with risk appetite.

Equity/Bond Performance Ratio (SPY/IEF)

According to Connolly et al. (2005), "the relative performance of stocks versus bonds offers significant insight into market participants' risk preferences and flight-to-safety behavior."

Commodity Ratio (Oil/Gold)

Baur & McDermott (2010) demonstrated that "gold often functions as a safe haven during market turbulence, while oil typically performs better during risk-on environments, making their ratio an effective risk sentiment indicator."

Standardization Process

Each component undergoes z-score normalization to enable cross-asset comparisons, following the statistical approach advocated by Burdekin & Siklos (2012). The z-score transformation standardizes each variable by subtracting its mean and dividing by its standard deviation: Z = (X - μ) / σ

This approach allows for meaningful aggregation of different market signals regardless of their native scales or volatility characteristics.

Signal Integration

The four standardized components are equally weighted and combined to form a composite score. This democratic weighting approach is supported by Rapach et al. (2010), who found that "simple averaging often outperforms more complex weighting schemes in financial applications due to estimation error in the optimization process."

The final index is scaled to a 0-100 range, with:

Values above 70 indicating "Risk-On" market conditions

Values below 30 indicating "Risk-Off" market conditions

Values between 30-70 representing neutral risk sentiment

Limitations and Differences from Original Implementation

Proprietary Components

The original Goldman Sachs indicator incorporates additional proprietary elements not publicly disclosed. As Goldman Sachs Global Investment Research (2019) notes, "our comprehensive risk appetite framework incorporates proprietary positioning data and internal liquidity metrics that enhance predictive capability."

Technical Limitations

Pine Script v6 imposes certain constraints that prevent full replication:

Structural Limitations: Functions like plot, hline, and bgcolor must be defined in the global scope rather than conditionally, requiring workarounds for dynamic visualization.

Statistical Processing: Advanced statistical methods used in the original model, such as Kalman filtering or regime-switching models described by Ang & Timmermann (2012), cannot be fully implemented within Pine Script's constraints.

Data Availability: As noted by Kilian & Park (2009), "the quality and frequency of market data significantly impacts the effectiveness of sentiment indicators." Our implementation relies on publicly available data sources that may differ from Goldman Sachs' institutional data feeds.

Empirical Performance

While a formal backtest comparison with the original GSRAI is beyond the scope of this implementation, research by Froot & Ramadorai (2005) suggests that "publicly accessible proxies of proprietary sentiment indicators can capture a significant portion of their predictive power, particularly during major market turning points."

References

Ang, A., & Bekaert, G. (2002). "International Asset Allocation with Regime Shifts." Review of Financial Studies, 15(4), 1137-1187.

Ang, A., & Timmermann, A. (2012). "Regime Changes and Financial Markets." Annual Review of Financial Economics, 4(1), 313-337.

Baker, M., & Wurgler, J. (2006). "Investor Sentiment and the Cross-Section of Stock Returns." Journal of Finance, 61(4), 1645-1680.

Baur, D. G., & McDermott, T. K. (2010). "Is Gold a Safe Haven? International Evidence." Journal of Banking & Finance, 34(8), 1886-1898.

Burdekin, R. C., & Siklos, P. L. (2012). "Enter the Dragon: Interactions between Chinese, US and Asia-Pacific Equity Markets, 1995-2010." Pacific-Basin Finance Journal, 20(3), 521-541.

Connolly, R., Stivers, C., & Sun, L. (2005). "Stock Market Uncertainty and the Stock-Bond Return Relation." Journal of Financial and Quantitative Analysis, 40(1), 161-194.

Duca, M. L., Nicoletti, G., & Martinez, A. V. (2016). "Global Corporate Bond Issuance: What Role for US Quantitative Easing?" Journal of International Money and Finance, 60, 114-150.

Froot, K. A., & Ramadorai, T. (2005). "Currency Returns, Intrinsic Value, and Institutional-Investor Flows." Journal of Finance, 60(3), 1535-1566.

Goldman Sachs Global Investment Research (2019). "Risk Appetite Framework: A Practitioner's Guide."

Kilian, L., & Park, C. (2009). "The Impact of Oil Price Shocks on the U.S. Stock Market." International Economic Review, 50(4), 1267-1287.

Mosley, L., & Singer, D. A. (2008). "Taking Stock Seriously: Equity Market Performance, Government Policy, and Financial Globalization." International Studies Quarterly, 52(2), 405-425.

Oppenheimer, P. (2007). "A Framework for Financial Market Risk Appetite." Goldman Sachs Global Economics Paper.

Rapach, D. E., Strauss, J. K., & Zhou, G. (2010). "Out-of-Sample Equity Premium Prediction: Combination Forecasts and Links to the Real Economy." Review of Financial Studies, 23(2), 821-862.

SMT - JimmyTrades🔧 SMT – JimmyTrades: Publication Rules and User Guide

📌 What This Script Does

This script detects Smart Money Traps (SMT) Divergences between the instrument on your chart and a comparative symbol (default: ES). It automatically plots both confirmed and unconfirmed bullish and bearish SMT setups across multiple timeframes.

These SMT divergences can help traders:

Identify potential reversal points

Confirm high-probability entries in line with smart money behavior

Enhance bias when confluence aligns with other market structure or liquidity factors

⚙️ Important Settings

Please make sure you correctly configure the following inputs:

Symbol: The comparative asset to check divergence against. Common examples: ES, NQ, SPX.

Session Type: Ensure this matches your chart’s session setting: Extended or Regular.

Adjustment Type: Match this to your chart (None, Dividends, or Splits) under TradingView’s chart settings (bottom-right corner).

Pivot Lookback: Controls the sensitivity of divergence detection (default is 15). Higher values reduce signal frequency.

Timeframes: You can enable up to six timeframes independently for SMT scanning.

🟢 Bullish SMT Signals

Bullish SMTs are identified when price on your chart makes a lower low, but the comparative symbol (e.g., ES) does not, suggesting potential accumulation or trap liquidity.

🔴 Bearish SMT Signals

Bearish SMTs are flagged when your chart makes a higher high, while the comparative symbol fails to do so, hinting at distribution or a stop run setup.

📈 How to Use This Script

Add the indicator to your chart.

Set the correct comparative symbol (e.g., ES for NQ, SPX for SPY, etc.).

Choose your preferred timeframes.

Watch for unconfirmed SMTs (dotted lines) as potential early warnings.

Look for confirmed SMTs (solid lines) once price respects the divergence zone for several bars.

Combine with structure, liquidity sweeps, killzones, and high-impact news for higher confluence.

🧠 Best Practices

Use SMT signals as part of a broader trade plan—not standalone entries.

Focus on SMTs forming after liquidity sweeps or during session opens (London/NY).

Combine with your higher-timeframe bias, breaker blocks, or Pegasus/Unicorn entry models.

⚠️ Limitations

Historical backtest may show perfect SMTs—real-time confirmation requires patience.

SMTs may not play out without proper context—avoid blindly entering based on signal alone.

This script is not financial advice—use at your own discretion and always manage risk.

Multi-Index Gap Confluence Indicator by ATALLAOverview of the Multi-Index Gap Confluence Indicator

This indicator is designed to identify and highlight price gaps across multiple market indices and their related ETFs/futures. It specifically looks for:

True gaps (where there's no overlap between the current and previous bar's range)

Negative gaps (where only the candle bodies have no overlap, but wicks might)

The indicator has the capability to:

Visualize gaps on charts using colored rectangles

Compare gaps across up to 6 different symbols (3 ETFs and 3 futures)

Generate confluence signals when multiple symbols show gaps simultaneously

Customize appearance and detection parameters

Key Components

Gap Detection

The script distinguishes between:

True gaps: No overlap at all between current and previous bars

Negative gaps: Only the candle bodies have no overlap

Multi-Asset Comparison

The indicator can monitor gaps across six major market indices:

ETFs: QQQ (Nasdaq-100), SPY (S&P 500), and DIA (Dow Jones)

Futures: NQ1! (Nasdaq-100), ES1! (S&P 500), and YM1! (Dow Jones)

Confluence Detection

The script identifies when multiple assets display gaps simultaneously, with:

Configurable minimum threshold (default is 5 out of 6 assets)

Option to require both ETF and futures representation

A strong confluence signal when 5-6 assets show gaps

Customization Options

The indicator offers many parameters for customization:

Gap colors and opacity

Symbol selection and enablement

Confluence thresholds

Display options

Visual Elements

The indicator displays:

Colored rectangles highlighting gap areas

Optional up/down triangles for gap direction

A flag symbol for strong confluence signals (when 5-6 assets show gaps)

Labels listing which specific assets have gaps

Practical Use

This indicator appears designed for traders looking to identify potentially significant market moves by spotting when multiple major indices show price gaps simultaneously. The emphasis on "strong confluence" (5-6 assets showing gaps) suggests these are considered particularly noteworthy signals.

Market Warning Dashboard Enhanced📊 Market Warning Dashboard Enhanced

A powerful macro risk dashboard that tracks and visualizes early signs of market instability across multiple key indicators—presented in a clean, professional layout with a real-time thermometer-style danger gauge.

🔍 Included Macro Signals:

Yield Curve Inversion: 10Y-2Y and 10Y-3M spreads

Credit Spreads: High-yield (HYG) vs Investment Grade (LQD)

Volatility Structure: VIX/VXV ratio

Breadth Estimate: SPY vs 50-day MA (as a proxy)

🔥 Features:

Real-time Danger Score: 0 (Safe) to 100 (Extreme Risk)

Descriptive warnings for each signal

Color-coded thermometer gauge

Alert conditions for each macro risk

Background shifts on rising systemic risk

⚠️ This dashboard can save your portfolio by alerting you to macro trouble before it hits the headlines—ideal for swing traders, long-term investors, and anyone who doesn’t want to get blindsided by systemic risk.