Super Z strategy - Thanks to Rafael Zioni//Original script

//https://www.tradingview.com/script/wYknDlLx-super-Z/

This is a test for verifying if this interesting study works well.

The author, thanks to him!!!, advise a possible repaint because the script uses security function.

Refer to tradingview.com for more info on repainting:

www.tradingview.com

QUOTE:

We can see repainting in the following cases:

1- Strategies using calc_on_every_tick=true. A strategy with parameter calc_on_every_tick = false may also be prone to repainting, but to a lesser degree.

(this is not the case, ndr).

2- Using security for requesting data from a resolution higher than the resolution of the chart’s main symbol (i.e. do not use ion weelky chart if you set 1440 (1Day) in inputs)

NOTE: Thanks again to Rafael Zioni. If he requires to delete this strategy, I'll do immediately.

Search in scripts for "the script"

Trend spider glueThis script works on all market types.

This script will show you when to long, short, exit (stop loss) and Take profit.

Signals take into account various elements such as momentum, volume , moving averages and long term trend analysis. Stop loss function is included to show you when a signal is invalidated.

Use this strategy strictly, patiently and with discipline to prevent unneeded losses, this will result in long term consistent profits.

This script has been set to work best on the intraday time frames, however it also works on the longer timeframes. Use the settings tab to dilute the indicators to ur own market.

Lastly, this indicator will not give signals if the market is not trending.

PM me here to get a free trial for the indicator !

HAPPY TRADING <3

Version 2 will be coming soon which will integerate more elements to allow for more accurate signals and faster stop losses !

disclaimer: although this indicator is taking many elements into account and is highly accurate the market is never certain, we are not responsible for any losses the script may result in as we are not financial advisors.

[astropark] Super Stochastic RSI [strategy]Dear Followers,

today a new Scalper Tool , which works great on 3 minutes and 5 minutes timeframes !

I called it " Super Stochastic RSI ", as it is based on StochRSI and inherits some basic functionality from it.

If you check its settings, you will see that you can have 3 different buy-sell sources (first two are active by default):

STRONG BUY/SELL : buy when green area deeply falls into oversold zone and sell when red area gets into overbought zone (you can set and edit at which level oversold and overbought zones start);

K/D CROSSES : buy when k-line cross above d-line and sell viceversa (you can set and edit specific cross ranges for both buy and sell);

WEAK BUY/SELL : buy when green area at least go below 50 level and sell when red area at least goes above 50 level (you can edit both levels); these conditions are highlighted as background color and are very useful for taking (at least partial) profits in trades.

By default the script will be placed as oscillator on a specific pane below the chart, but

> you can disable the oscillator plot by enabling the "hide all plot" option

> and place it as overlay on chart by clicking on the black arrow at then end on the indicator name in chart and selecting "move to -> existing pane above"

This strategy can trigger till 10 buy or 10 sell signals in a row before reverting, so use a proper money management .

Strategy results are calculated on 20 trading days using 1000$ as initial capital and working at 10x leverage.

The user who wants to use this strategy, especially via an automated bot, must always set a stoploss at 3-5% from entry point or use a proper risk management strategy .

This is not the "Holy Grail", so use it with caution.

This script will let you backtest the strategy and find best settings for your preferred market.

The alarms script version of this indicator, which will let you set all notifications you may need in order to be alerted on each triggered signals, can be found here below:

This is a premium indicator , so send me a private message in order to get access to this script .

[Strategy]-=The Script=- On Fire - Leverage EditionStrategy version of =The Scrip=- On Fire - Leverage Edition

Back-test period starts 01-01-2018

The settings used

• Strategy Period 3h and Chart Period 7 minute

DISCLAIMER:

The creators of these script are not financial advisors, and as such, this script is not financial advice. Anything seen or used within this script is here simply for educational purposes and it is up to you to decide what to do with this information and results. Please do your own research and verify any outcome made before deciding to act upon them. Do not commit any of your own resources to any trading or cryptocurrency activities without first verifying the accuracy of the information and know that your decisions are your own.

Chart Formation DetectionThis script is designed to recognise a chart formation that is bullish. However, the script is optimised to default as using a very accurate formation.

This script works best on the 1-15 minute time frames. Anything higher is subject to macroeconomic events as apposed to high-frequency-trading algorithms which we are relying on in order for this script to work.

This seems to work very well on certain instruments as apposed to others(e.g. gold seems to work better than the US30). You will find what you like the best and develop your own uses for these indicators.

GMAE Original (By Kevin Manrrique)This script is called GMAE Original by me (Kevin Manrrique). I'm publishing this to the public because we are all traders and we need to support each other as a TVcommunity. This is something I built for fun. This script uses a series of EMA's. NO REPAINT, NO LAGGING! It works better for short-term trends as you can see. Please leave the copyright on the script at all times even if you rebuild it. If you need any help or have questions please inbox me privately. If you interested in joining up and building an indicator or strategy please inbox me as well. Thank you and I hope you enjoy this script as much as I do.

Remember there are no holy grails. The only holy grail there is are indicators built together to stop faulty signals and be as accurate as possible and this is one of them.

Sincerely,

Kevin Manrrique

Dhanesh_CustomTrendlineLogicUsed framma in getting the trades.

You can also define the custom horizontal and an inclined trendline breaking of which can trigger the trade. Enjoy the script.

Volumemetrix Variance StrategyThe “Volumemetrix Variance Strategy” is an advanced Pine Script strategy designed to identify trade entries and exits using a combination of volume profile analysis, candle structure, and volatility filters. It constructs a dynamic volume profile over a specified lookback period to identify critical price levels such as the Point of Control (PoC), Value Area High (VAH), and Value Area Low (VAL). These levels represent zones of high trading activity that often act as support and resistance. The script smooths and adjusts these levels across different timeframes to align short-term market structure with higher-timeframe trends. It incorporates a variety of filters to exclude doji candles, detect continuation or rejection patterns, and confirm alignment with higher timeframe candle direction (e.g., 4-hour bullish or bearish bias).

Trade logic is built around detecting crossovers and breakouts relative to the PoC and value areas. The system can trigger entries based on several configurable behaviors: breakout, retake, bounce, reversal, or rejection near key volume zones. It supports flexible entry conditions for long, short, or both sides of the market, as well as a range of customizable settings for time-based trading restrictions, end-of-day position closures, and alert-based data capture. For execution, the script includes integrated risk management—users can specify take-profit and stop-loss levels, enable moving (trailing) stops, and even apply a “power curve” model to dynamically adjust trailing stops using exponential decay logic that adapts to price progress.

Overall, the Volumemetrix Variance Strategy is a hybrid between a quantitative volume-based strategy and a volatility-adaptive trade manager. It combines fixed range volume profiling with multi-timeframe confirmation, candle pattern validation, and adaptive exit logic. Its architecture allows for detailed trade automation, alert generation for external systems, and real-time control over parameters such as ATR scaling, entry delay, or bar confirmation. The result is a high-granularity framework for both backtesting and live execution that seeks to capture statistically favorable setups around liquidity concentration zones.

v2.0—Tristan's Multi-Indicator Reversal Strategy🎯 Multi-Indicator Reversal Strategy - Optimized for High Win Rates

A powerful confluence-based strategy that combines RSI, MACD, Williams %R, Bollinger Bands, and Volume analysis to identify high-probability reversal points . Designed to let winners run with no stop loss or take profit - positions close only when opposite signals occur.

Also, the 3 hour timeframe works VERY well—just a lot less trades.

📈 Proven Performance

This strategy has been backtested and optimized on multiple blue-chip stocks with 80-90%+ win rates on 1-hour timeframes from Aug 2025 through Oct 2025:

✅ V (Visa) - Payment processor

✅ MSFT (Microsoft) - Large-cap tech

✅ WMT (Walmart) - Retail leader

✅ IWM (Russell 2000 ETF) - Small-cap index

✅ NOW (ServiceNow) - Enterprise software

✅ WM (Waste Management) - Industrial services

These stocks tend to mean-revert at extremes, making them ideal candidates for this reversal-based approach. I only list these as a way to show you the performance of the script. These values and stock choices may change over time as the market shifts. Keep testing!

🔑 How to Use This Strategy Successfully

Step 1: Apply to Chart

Open your desired stock (V, MSFT, WMT, IWM, NOW, WM recommended)

Set timeframe to 1 Hour

Apply this strategy

Check that the Williams %R is set to -20 and -80, and "Flip All Signals" is OFF (can flip this for some stocks to perform better.)

Step 2: Understand the Signals

🟢 Green Triangle (BUY) Below Candle:

Multiple indicators (RSI, Williams %R, MACD, Bollinger Bands) show oversold conditions

Enter LONG position

Strategy will pyramid up to 10 entries if more buy signals occur

Hold until red triangle appears

🔴 Red Triangle (SELL) Above Candle:

Multiple indicators show overbought conditions

Enter SHORT position (or close existing long)

Strategy will pyramid up to 10 entries if more sell signals occur

Hold until green triangle appears

🟣 Purple Labels (EXIT):

Shows when positions close

Displays count if multiple entries were pyramided (e.g., "Exit Long x5")

Step 3: Let the Strategy Work

Key Success Principles:

✅ Be Patient - Signals don't occur every day, wait for quality setups

✅ Trust the Process - Don't manually close positions, let opposite signals exit

✅ Watch Pyramiding - The strategy can add up to 10 positions in the same direction

✅ No Stop Loss - Positions ride through drawdowns until reversal confirmed

✅ Session Filter - Only trades during NY session (9:30 AM - 4:00 PM ET)

⚙️ Winning Settings (Already Set as Defaults)

INDICATOR SETTINGS:

- RSI Length: 14

- RSI Overbought: 70

- RSI Oversold: 30

- MACD: 12, 26, 9 (standard)

- Williams %R Length: 14

- Williams %R Overbought: -20 ⭐ (check this! And adjust to your liking)

- Williams %R Oversold: -80 ⭐ (check this! And adjust to your liking)

- Bollinger Bands: 20, 2.0

- Volume MA: 20 periods

- Volume Multiplier: 1.5x

SIGNAL REQUIREMENTS:

- Min Indicators Aligned: 2

- Require Divergence: OFF

- Require Volume Spike: OFF

- Require Reversal Candle: OFF

- Flip All Signals: OFF ⭐

RISK MANAGEMENT:

- Use Stop Loss: OFF ⭐⭐⭐

- Use Take Profit: OFF ⭐⭐⭐

- Allow Pyramiding: ON ⭐⭐⭐

- Max Pyramid Entries: 10 ⭐⭐⭐

SESSION FILTER:

- Trade Only NY Session: ON

- NY Session: 9:30 AM - 4:00 PM ET

**⭐ = Critical settings for success**

## 🎓 Strategy Logic Explained

### **How It Works:**

1. **Multi-Indicator Confluence**: Waits for at least 2 out of 4 technical indicators to align before generating signals

2. **Oversold = Buy**: When RSI < 30, Williams %R < -80, price below lower Bollinger Band, and/or MACD turning bullish → BUY signal

3. **Overbought = Sell**: When RSI > 70, Williams %R > -20, price above upper Bollinger Band, and/or MACD turning bearish → SELL signal

4. **Pyramiding Power**: As trend continues and more signals fire in the same direction, adds up to 10 positions to maximize gains

5. **Exit Only on Reversal**: No arbitrary stops or targets - only exits when opposite signal confirms trend change

6. **Session Filter**: Only trades during liquid NY session hours to avoid overnight gaps and low-volume periods

### **Why No Stop Loss Works:**

Traditional reversal strategies fail because they:

- Get stopped out too early during normal volatility

- Miss the actual reversal that happens later

- Cut winners short with tight take profits

This strategy succeeds because it:

- ✅ Rides through temporary noise

- ✅ Captures full reversal moves

- ✅ Uses multiple indicators for confirmation

- ✅ Pyramids into winning positions

- ✅ Only exits when technical picture completely reverses

---

## 📊 Understanding the Display

**Live Indicator Counter (Top Corner / end of current candles):**

Bull: 2/4

Bear: 0/4

(STANDARD)

Shows how many indicators currently align bullish/bearish

"STANDARD" = normal reversal mode (buy oversold, sell overbought)

"FLIPPED" = momentum mode if you toggle that setting

Visual Indicators:

🔵 Blue background = NY session active (trading window)

🟡 Yellow candle tint = Volume spike detected

💎 Aqua diamond = Bullish divergence (price vs RSI)

💎 Fuchsia diamond = Bearish divergence

⚡ Advanced Tips

Optimizing for Different Stocks:

If Win Rate is Low (<50%):

Try toggling "Flip All Signals" to ON (switches to momentum mode)

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Test on different timeframe (4-hour or daily)

If Too Few Signals:

Decrease "Min Indicators Aligned" to 2

Turn OFF all requirement filters

Widen Williams %R bands to -15 and -85

If Too Many False Signals:

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Turn ON "Require Volume Spike"

Reduce Max Pyramid Entries to 5

Stock Selection Guidelines:

Best Suited For:

Large-cap stable stocks (V, MSFT, WMT)

ETFs (IWM, SPY, QQQ)

Stocks with clear support/resistance

Mean-reverting instruments

Avoid:

Ultra low-volume penny stocks

Extremely volatile crypto (try traditional settings first)

Stocks in strong one-directional trends lasting months

🔄 The "Flip All Signals" Feature

If backtesting shows poor results on a particular stock, try toggling "Flip All Signals" to ON:

STANDARD Mode (OFF):

Buy when oversold (reversal strategy)

Sell when overbought

May work best for: V, MSFT, WMT, IWM, NOW, WM

FLIPPED Mode (ON):

Buy when overbought (momentum strategy)

Sell when oversold

May work best for: Strong trending stocks, momentum plays, crypto

Test both modes on your stock to see which performs better!

📱 Alert Setup

Create alerts to notify you of signals:

📊 Performance Expectations

With optimized settings on recommended stocks:

Typical results we are looking for:

Win Rate: 70-90%

Average Winner: 3-5%

Average Loser: 1-3%

Signals Per Week: 1-3 on 1-hour timeframe

Hold Time: Several hours to days

Remember: Past performance doesn't guarantee future results. Always use proper risk management.

ES cuhthis strategy uses laggard rsi to compute the best parameters to go long and tp at key levels. the overall trend strength within the rsi laggard indicator is what is used to automate the calculations within the script. enjoy and paramter optimize

Hilly 3.0 Advanced Crypto Scalping Strategy - 1 & 5 Min ChartsHow to Use

Copy the Code: Copy the script above.

Paste in TradingView: Open TradingView, go to the Pine Editor (bottom of the chart), paste the code, and click “Add to Chart.”

Check for Errors: Verify no errors appear in the Pine Editor console. The script uses Pine Script v5 (@version=5).

Select Timeframe:

1-Minute Chart: Use defaults (emaFastLen=7, emaSlowLen=14, rsiLen=10, rsiOverbought=80, rsiOversold=20, slPerc=0.5, tpPerc=1.0, useCandlePatterns=false, patternLookback=10).

5-Minute Chart: Adjust to emaFastLen=9, emaSlowLen=21, rsiLen=14, rsiOverbought=75, rsiOversold=25, slPerc=0.8, tpPerc=1.5, useCandlePatterns=true, patternLookback=10.

Apply to Chart: Use a liquid crypto pair (e.g., BTC/USDT, ETH/USDT on Binance or Coinbase).

Verify Signals:

Green “BUY” or “EMA BUY” labels and triangle-up arrows below candles for bullish signals (EMA crossovers, bullish engulfing, hammer, doji, morning star, three white soldiers, double bottom).

Red “SELL” or “EMA SELL” labels and triangle-down arrows above candles for bearish signals (EMA crossovers, bearish engulfing, shooting star, doji, evening star, three black crows, double top).

Green/red background highlights for signal candles.

Backtest: Use TradingView’s Strategy Tester to evaluate performance over 1–3 months, checking Net Profit, Win Rate, and Drawdown.

Demo Test: Run on a demo account to confirm signal visibility and performance before trading with real funds.

Hilly 2.0 Advanced Crypto Scalping Strategy - 1 & 5 Min ChartsHow to Use

Copy the Code: Copy the script above.

Paste in TradingView: Open TradingView, go to the Pine Editor (bottom of the chart), paste the code, and click “Add to Chart.”

Check for Errors: Verify no errors appear in the Pine Editor console. The script uses Pine Script v5 (@version=5).

Select Timeframe:

1-Minute Chart: Use defaults (emaFastLen=7, emaSlowLen=14, rsiLen=10, rsiOverbought=80, rsiOversold=20, slPerc=0.5, tpPerc=1.0, useCandlePatterns=false).

5-Minute Chart: Adjust to emaFastLen=9, emaSlowLen=21, rsiLen=14, rsiOverbought=75, rsiOversold=25, slPerc=0.8, tpPerc=1.5, useCandlePatterns=true.

Apply to Chart: Use a liquid crypto pair (e.g., BTC/USDT, ETH/USDT on Binance or Coinbase).

Verify Signals:

Green “BUY” or “EMA BUY” labels and triangle-up arrows below candles.

Red “SELL” or “EMA SELL” labels and triangle-down arrows above candles.

Green/red background highlights for signal candles.

Arrows use size.normal for consistent visibility.

Backtest: Use TradingView’s Strategy Tester to evaluate performance over 1–3 months, checking Net Profit, Win Rate, and Drawdown.

Demo Test: Run on a demo account to confirm signal visibility and performance before trading with real funds.

System 0530 - Stoch RSI Strategy with ATR filterStrategy Description: System 0530 - Multi-Timeframe Stochastic RSI with ATR Filter

Overview:

This strategy, "System 0530," is designed to identify trading opportunities by leveraging the Stochastic RSI indicator across two different timeframes: a shorter timeframe for initial signal triggers (assumed to be the chart's current timeframe, e.g., 5-minute) and a longer timeframe (15-minute) for signal confirmation. It incorporates an ATR (Average True Range) filter to help ensure trades are taken during periods of adequate market volatility and includes a cooldown mechanism to prevent rapid, successive signals in the same direction. Trade exits are primarily handled by reversing signals.

How It Works:

1. Signal Initiation (e.g., 5-Minute Timeframe):

Long Signal Wait: A potential long entry is considered when the 5-minute Stochastic RSI %K line crosses above its %D line, AND the %K value at the time of the cross is at or below a user-defined oversold level (default: 30).

Short Signal Wait: A potential short entry is considered when the 5-minute Stochastic RSI %K line crosses below its %D line, AND the %K value at the time of the cross is at or above a user-defined overbought level (default: 70). When these conditions are met, the strategy enters a "waiting state" for confirmation from the 15-minute timeframe.

2. Signal Confirmation (15-Minute Timeframe):

Once in a waiting state, the strategy looks for confirmation on the 15-minute Stochastic RSI within a user-defined number of 5-minute bars (wait_window_5min_bars, default: 5 bars).

Long Confirmation:

The 15-minute Stochastic RSI %K must be greater than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be below a user-defined threshold (stoch_15min_long_entry_level, default: 40).

Short Confirmation:

The 15-minute Stochastic RSI %K must be less than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be above a user-defined threshold (stoch_15min_short_entry_level, default: 60).

3. Filters:

ATR Volatility Filter: If enabled, trades are only confirmed if the current ATR value (converted to ticks) is above a user-defined minimum threshold (min_atr_value_ticks). This helps to avoid taking signals during periods of very low market volatility. If the ATR condition is not met, the strategy continues to wait for the condition to be met within the confirmation window, provided other conditions still hold.

Signal Cooldown Filter: If enabled, after a signal is generated, the strategy will wait for a minimum number of bars (min_bars_between_signals) before allowing another signal in the same direction. This aims to reduce overtrading.

4. Entry and Exit Logic:

Entry: A strategy.entry() order is placed when all trigger, confirmation, and filter conditions are met.

Exit: This strategy primarily uses reversing signals for exits. For example, if a long position is open, a confirmed short signal will close the long position and open a new short position. There are no explicit take profit or stop loss orders programmed into this version of the script.

Key User-Adjustable Parameters:

Stochastic RSI Parameters: RSI Length, Stochastic RSI Length, %K Smoothing, %D Smoothing.

Signal Trigger & Confirmation:

5-minute %K trigger levels for long and short.

15-minute %K confirmation thresholds for long and short.

Wait window (in 5-minute bars) for 15-minute confirmation.

Filters:

Enable/disable and configure the Signal Cooldown filter (minimum bars between signals).

Enable/disable and configure the ATR Volatility filter (ATR period, minimum ATR value in ticks).

Strategy Parameters:

Leverage Multiplier (Note: This primarily affects theoretical position sizing for backtesting calculations in TradingView and does not simulate actual leveraged trading risks).

Recommendations for Users:

Thorough Backtesting: Test this strategy extensively on historical data for the instruments and timeframes you intend to trade.

Parameter Optimization: Experiment with different parameter settings to find what works best for your trading style and chosen markets. The default values are starting points and may not be optimal for all conditions.

Understand the Logic: Ensure you understand how each component (Stochastic RSI on different timeframes, ATR filter, cooldown) interacts to generate signals.

Risk Management: Since this version does not include explicit stop-loss orders, ensure you have a clear risk management plan in place if trading this strategy live. You might consider manually adding stop-loss orders through your broker or using TradingView's separate strategy order settings for stop-loss if applicable.

Disclaimer:

This strategy description is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Trading involves significant risk of loss. Always do your own research and understand the risks before trading.

Anomaly Counter-Trend StrategyA mean-reversion style strategy that automatically spots unusually large price moves over a configurable lookback period and takes the opposite side, with full risk-management, commission and slippage modeling—built in Pine Script® v6.

🔎 Overview

ACTS monitors the percent-change over the past N minutes and, when that move exceeds your chosen threshold, enters a counter-trend position (short on a strong rise; long on a sharp fall). It’s ideal for markets that often “overshoot” and snap back, and can be applied on any symbol or timeframe.

⚙️ Key Features

Anomaly Detection: Detect abnormal price swings based on a user-defined % change over a lookback period.

Counter-Trend Entries: Auto-enter short on rise anomalies, long on fall anomalies (with seamless flat↔reverse transitions).

Risk Management: Configurable stop-loss and take-profit in ticks per trade.

Realistic Modeling: Simulates commissions (0.05 % default), slippage (2 ticks), and percent-of-equity sizing.

Immediate Bar-Close Execution: Orders processed on bar close for faster fills.

Visual Aids: Optional on-chart BUY/SELL triangles and background highlights during anomaly periods.

⚙️ Inputs

Input Default Description

Percentage Threshold (%) 2.00 Min % move over lookback to trigger an anomaly.

Lookback Period (Minutes) 15 Number of minutes over which to measure change.

Stop Loss (Ticks) 100 Distance from entry for stop-loss exit.

Take Profit (Ticks) 200 Distance from entry for take-profit exit.

Plot Trade Signal Shapes (on/off) true Show BUY/SELL triangles on chart.

Highlight Anomaly Background true Shade background during anomaly bars.

📊 How to Use

Add to Chart: Apply the script to any ticker & timeframe.

Tune: Adjust your percentage threshold and lookback to match each instrument’s volatility.

Review Backtest: Check built-in strategy performance (drawdown, Sharpe, etc.) under the Strategy Tester tab.

Go Live: Once optimized, link to alerts or your trade execution system.

⚠️ Disclaimer

This script is provided “as-is” for educational purposes and backtesting only. Past performance does not guarantee future results. Always backtest thoroughly, manage your own risk, and consider market conditions before live trading.

Enjoy experimenting—and may your counter-trend entries catch the next big snapback!

Breadth-Driven Swing StrategyWhat it does

This script trades the S&P 500 purely on market breadth extremes:

• Data source : INDEX:S5TH = % of S&P 500 stocks above their own 200-day SMA (range 0–100).

• Buy when breadth is washed-out.

• Sell when breadth is overheated.

It is long-only by design; shorting and ATR trailing stops have been removed to keep the logic minimal and transparent.

⸻

Signals in plain English

1. Long entry

A. A 200-EMA trough in breadth is printed and the trough value is ≤ 40 %.

or

B. A 5-EMA trough appears, its prominence passes the user threshold, and the lowest breadth reading in the last 20 bars is ≤ 20 %.

(Toggle this secondary trigger on/off with “ Enter also on 5-EMA trough ”.)

2. Exit (close long)

First 200-EMA peak whose breadth value is ≥ 70 %.

3. Risk control

A fixed stop-loss (% of entry price, default 8 %) is attached to every long trade.

⸻

Key parameters (defaults shown)

• Long EMA length 200 • Short EMA length 5

• Peak prominence 0.5 pct-pts • Trough prominence 3 pct-pts

• Peak level 70 % • Trough level 40 % • 5-EMA trough level 20 %

• Fixed stop-loss 8 %

• “Enter also on 5-EMA trough” = true (allows additional entries on extreme momentum reversals)

Feel free to tighten or relax any of these thresholds to match your risk profile or account for different market regimes.

⸻

How to use it

1. Load the script on a daily SPX / SPY chart.

(The price chart drives order execution; the breadth series is pulled internally and does not need to be on the chart.)

2. Verify the breadth feed.

INDEX:S5TH is updated after each session; your broker must provide it.

3. Back-test across several cycles.

Two decades of daily data is recommended to see how the rules behave in bear markets, range markets, and bull trends.

4. Adjust position sizing in the Properties tab.

The default is “100 % of equity”; change it if you prefer smaller allocations or pyramiding caps.

⸻

Why it can help

• Breadth signals often lead price, allowing entries before index-level momentum turns.

• Simple, rule-based exits prevent “waiting for confirmation” paralysis.

• Only one input series—easy to audit, no black-box math.

Trade-offs

• Relies on a single breadth metric; other internals (advance/decline, equal-weight returns, etc.) are ignored.

• May sit in cash during shallow pullbacks that never push breadth ≤ 40 %.

• Signals arrive at the end of the session (breadth is EoD data).

⸻

Disclaimer

This script is provided for educational purposes only and is not financial advice. Markets are risky; test thoroughly and use your own judgment before trading real money.

ストラテジー概要

本スクリプトは S&P500 のマーケットブレッド(内部需給) だけを手がかりに、指数をスイングトレードします。

• ブレッドデータ : INDEX:S5TH

(S&P500 採用銘柄のうち、それぞれの 200 日移動平均線を上回っている銘柄比率。0–100 %)

• 買い : ブレッドが極端に売られたタイミング。

• 売り : ブレッドが過熱状態に達したタイミング。

余計な機能を削り、ロングオンリー & 固定ストップ のシンプル設計にしています。

⸻

シグナルの流れ

1. ロングエントリー

• 条件 A : 200-EMA がトラフを付け、その値が 40 % 以下

• 条件 B : 5-EMA がトラフを付け、

・プロミネンス条件を満たし

・直近 20 本のブレッドス最小値が 20 % 以下

• B 条件は「5-EMA トラフでもエントリー」を ON にすると有効

2. ロング決済

最初に出現した 200-EMA ピーク で、かつ値が 70 % 以上 のバーで手仕舞い。

3. リスク管理

各トレードに 固定ストップ(初期価格から 8 %)を設定。

⸻

主なパラメータ(デフォルト値)

• 長期 EMA 長さ : 200 • 短期 EMA 長さ : 5

• ピーク判定プロミネンス : 0.5 %pt • トラフ判定プロミネンス : 3 %pt

• ピーク水準 : 70 % • トラフ水準 : 40 % • 5-EMA トラフ水準 : 20 %

• 固定ストップ : 8 %

• 「5-EMA トラフでもエントリー」 : ON

相場環境やリスク許容度に合わせて閾値を調整してください。

⸻

使い方

1. 日足の SPX / SPY チャート にスクリプトを適用。

2. ブレッドデータの供給 (INDEX:S5TH) がブローカーで利用可能か確認。

3. 20 年以上の期間でバックテスト し、強気相場・弱気相場・レンジ局面での挙動を確認。

4. 資金配分 は プロパティ → 戦略実行 で調整可能(初期値は「資金の 100 %」)。

⸻

強み

• ブレッドは 価格より先行 することが多く、天底を早期に捉えやすい。

• ルールベースの出口で「もう少し待とう」と迷わずに済む。

• 入力 series は 1 本のみ、ブラックボックス要素なし。

注意点・弱み

• 単一指標に依存。他の内部需給(A/D ライン等)は考慮しない。

• 40 % を割らない浅い押し目では機会損失が起こる。

• ブレッドは終値ベースの更新。ザラ場中の変化は捉えられない。

⸻

免責事項

本スクリプトは 学習目的 で提供しています。投資助言ではありません。

実取引の前に必ず自己責任で十分な検証とリスク管理を行ってください。

Vinicius Setup ATR

Description:

This script is a strategy based on the Supertrend indicator combined with volume analysis, candle strength, and RSI. Its goal is to identify potential entry points for buy and sell trades based on technical criteria, without promising profitability or guaranteed results.

Script Components:

Supertrend: Used as the main trend compass. When the trend is positive (direction = 1), buy signals are considered; when negative (direction = -1), sell signals are considered.

Volume: Entries are only validated if the volume is above the average of the last 20 candles, adjusted with a 1.2 multiplier.

Candle Body: The candle body must be larger than a certain percentage of the ATR, ensuring sufficient strength and volatility.

RSI: Used as a filter to avoid trades in extreme overbought or oversold zones.

Support and Resistance: Identified based on simple pivots (5 periods before and after).

Customizable Parameters:

ATR Length and Multiplier: Controls the sensitivity of the Supertrend.

RSI Period: Adjusts the relative strength filter.

Minimum Volume and Candle Body: Settings to validate entry signals.

Entry Conditions:

Buy: Positive trend + strong candle + high volume + RSI below 70.

Sell: Negative trend + strong candle + high volume + RSI above 30.

Exit Conditions:

The trade is closed upon the appearance of an opposite signal.

Notes:

This is a technical system with no profit guarantees.

It is recommended to test with realistic capital values and parameters suited to your risk management.

The script is not optimized for specific profitability, but rather to support study and the construction of setups with objective criteria.

Reversal & Breakout Strategy with ORB### Reversal & Breakout Strategy with ORB

This strategy combines three distinct trading approaches—reversals, trend breakouts, and opening range breakouts (ORB)—into a single, cohesive system. The goal is to capture high-probability setups across different market conditions, leveraging a mashup of technical indicators for confirmation and risk management. Below, I’ll explain why this combination works, how the components interact, and how to use it effectively.

#### Why the Mashup?

- **Reversals**: Identifies overextended moves using RSI (overbought/oversold) and SMA50 crosses, filtered by VWAP and SMA200 trend direction. This targets mean-reversion opportunities in trending markets.

- **Breakouts**: Uses EMA9/EMA20 crossovers with VWAP and SMA200 confirmation to catch momentum-driven trend continuations.

- **Opening Range Breakout (ORB)**: Detects early momentum by breaking the high/low of a user-defined opening range (default: 15 bars) with volume confirmation. This adds a time-based edge, ideal for intraday trading.

The synergy comes from blending these methods: reversals catch pullbacks, breakouts ride trends, and ORB exploits early volatility—all filtered by trend (SMA200) and anchored by VWAP for context.

#### How It Works

1. **Indicators**:

- **EMA9/EMA20**: Fast-moving averages for breakout signals.

- **SMA50**: Medium-term trend filter for reversals.

- **SMA200**: Long-term trend direction to align trades.

- **RSI (14)**: Measures overbought (>70) or oversold (<30) conditions.

- **VWAP**: Acts as a dynamic support/resistance level.

- **ATR (14)**: Sets stop-loss distance (default: 1.5x ATR).

- **Volume**: Confirms ORB breakouts (1.5x average volume of opening range).

2. **Entry Conditions**:

- **Long**: Triggers on reversal (SMA50 cross + RSI < 30 + below VWAP + uptrend), breakout (EMA9 > EMA20 + above VWAP + uptrend), or ORB (break above opening range high + volume).

- **Short**: Triggers on reversal (SMA50 cross + RSI > 70 + above VWAP + downtrend), breakout (EMA9 < EMA20 + below VWAP + downtrend), or ORB (break below opening range low + volume).

3. **Risk Management**:

- Risks 5% of equity per trade (based on the initial capital set in the strategy tester).

- Stop-loss: Based on lowest low/highest high over 7 bars ± 1.5x ATR.

- Targets: Two exits at 1:1 and 1:2 risk:reward (50% of position at each).

- Break-even: Stop moves to entry price after the first target is hit.

4. **Backtesting Settings**:

- Commission: Hardcoded at 0.1% per trade (realistic for most brokers).

- Slippage: Hardcoded at 2 ticks (realistic for most markets).

- Tested on datasets yielding 100+ trades (e.g., 2-min or 5-min charts over months).

#### How to Use It

- **Timeframe**: Works best on intraday (2-min, 5-min) or daily charts. Adjust `Opening Range Bars` (e.g., 15 bars = 30 min on 2-min chart) for your timeframe.

- **Settings**:

- Set your initial equity in the TradingView strategy tester’s "Properties" tab under "Initial Capital" (e.g., $10,000). The script automatically risks 5% of this equity per trade.

- Adjust `Stop Loss ATR Multiplier` or `Risk:Reward Targets` based on your risk tolerance.

- Note that commission (0.1%) and slippage (2 ticks) are fixed in the script for backtesting consistency.

- **Execution**: Enter on signal, monitor plotted stop (red) and targets (green/blue). The strategy supports pyramiding (up to 2 positions) for scaling into trends.

#### Backtesting Notes

Results are realistic with commission (0.1%) and slippage (2 ticks) included. For a sufficient sample, test on volatile instruments (e.g., stocks, forex) over 3-6 months on lower timeframes. The default 1.5x ATR stop may seem wide, but it’s justified to avoid premature exits in volatile markets—feel free to tweak it with justification. The script assumes an initial capital of $10,000 in the strategy tester for the 5% risk calculation (e.g., $500 risk per trade); adjust this in the "Properties" tab as needed.

This mashup isn’t just a random mix; it’s a deliberate fusion of complementary strategies, offering traders flexibility across market phases. Questions? Let me know!

RSI + Stochastic + WMA StrategyThis script is designed for TradingView and serves as a trading strategy (not just a visual indicator). It's intended for backtesting, strategy optimization, or live trading signal generation using a combination of popular technical indicators.

📊 Indicators Used in the Strategy:

Indicator Description

RSI (Relative Strength Index) Measures momentum; identifies overbought (>70) or oversold (<30) conditions.

Stochastic Oscillator (%K & %D) Detects momentum reversal points via crossovers. Useful for timing entries.

WMA (Weighted Moving Average) Identifies the trend direction (used as a trend filter).

📈 Trading Logic / Strategy Rules:

📌 Long Entry Condition (Buy Signal):

All 3 conditions must be true:

RSI is Oversold → RSI < 30

Stochastic Crossover Upward → %K crosses above %D

Price is above WMA → Confirms uptrend direction

👉 Interpretation: Market was oversold, momentum is turning up, and price confirms uptrend — bullish entry.

📌 Short Entry Condition (Sell Signal):

All 3 conditions must be true:

RSI is Overbought → RSI > 70

Stochastic Crossover Downward → %K crosses below %D

Price is below WMA → Confirms downtrend direction

👉 Interpretation: Market is overbought, momentum is turning down, and price confirms downtrend — bearish entry.

🔄 Strategy Execution (Backtesting Logic):

The script uses:

pinescript

Copy

Edit

strategy.entry("LONG", strategy.long)

strategy.entry("SHORT", strategy.short)

These are Pine Script functions to place buy and sell orders automatically when the above conditions are met. This allows you to:

Backtest the strategy

Measure win/loss ratio, drawdown, and profitability

Optimize indicator settings using TradingView Strategy Tester

📊 Visual Aids (Charts):

Plots WMA Line: Orange line for trend direction

Overbought/Oversold Zones: Horizontal lines at 70 (red) and 30 (green) for RSI visualization

⚡ Strategy Type Summary:

Category Setting

Strategy Type Momentum Reversal + Trend Filter

Timeframe Flexible (Works best on 1H, 4H, Daily)

Trading Style Swing/Intraday

Risk Profile Medium to High (due to momentum triggers)

Uses Leverage Possible (adjust risk accordingly)

Optimized Auto-Detect Strategy (MA, ATR, Trend, RSI) Overview

This script is designed for traders seeking a trend-following approach that adapts to different currency pairs (e.g., EURUSD, NZDUSD, XAUUSD). It combines moving average crossovers with ATR-based stops, optional trend filters, and RSI filters to help reduce false signals and capture larger moves.

Key Features

1. Auto-Detect Logic

- Automatically applies different moving average periods and ATR multipliers based on the symbol (e.g., XAUUSD, EURUSD, NZDUSD).

- Makes it easy to switch charts without manually adjusting parameters each time.

2. ATR-Based Stop

- Uses the Average True Range (ATR) to set dynamic stop-loss levels, adapting to each market’s volatility.

3. Optional Trend Filter

- Filters out trades if price is below the 200 SMA for longs (and above for shorts), aiming to avoid choppy, range-bound markets.

4. Optional RSI Filter

- Only enters long if RSI is above a certain threshold (e.g., 50), or short if below another threshold, reducing entries during low momentum.

5. Partial Exit & Trailing/Break-Even

- Locks in partial profit at a chosen R:R (e.g., 1:1), then either trails the remaining position or moves the stop to break-even.

- This helps capture additional gains if the trend extends beyond the initial target.

6. Customizable Parameters

- You can toggle on/off each filter (Trend, RSI) and adjust the ATR multiplier, MA periods, partial exit levels, etc.

- Allows easy optimization for different pairs or timeframes.

How to Use

1. Add to Chart: Click “Add to chart” in the Pine Editor.

2. Configure Inputs: In the script’s settings, toggle the filters you want (Trend Filter, RSI Filter, etc.) and set your desired ATR multiplier, RSI thresholds, partial exit ratio, etc.

3. Strategy Tester: Check the performance under the “Strategy Tester” tab. Adjust parameters if needed.

4. Realistic Settings: Consider adding spreads/commissions in the “Properties” tab for more accurate backtests, especially if you trade pairs with higher spreads (like XAUUSD).

Disclaimer

No Guarantee: This script does not guarantee profits. Markets are unpredictable, and results may vary with market conditions.

For Educational Purposes: Always do your own research and forward testing. Past performance does not indicate future results.

GOLD Volume-Based Entry StrategyShort Description:

This script identifies potential long entries by detecting two consecutive bars with above-average volume and bullish price action. When these conditions are met, a trade is entered, and an optional profit target is set based on user input. This strategy can help highlight momentum-driven breakouts or trend continuations triggered by a surge in buying volume.

How It Works

Volume Moving Average

A simple moving average of volume (vol_ma) is calculated over a user-defined period (default: 20 bars). This helps us distinguish when volume is above or below recent averages.

Consecutive Green Volume Bars

First bar: Must be bullish (close > open) and have volume above the volume MA.

Second bar: Must also be bullish, with volume above the volume MA and higher than the first bar’s volume.

When these two bars appear in sequence, we interpret it as strong buying pressure that could drive price higher.

Entry & Profit Target

Upon detecting these two consecutive bullish bars, the script places a long entry.

A profit target is set at current price plus a user-defined fixed amount (default: 5 USD).

You can adjust this target, or you can add a stop-loss in the script to manage risk further.

Visual Cues

Buy Signal Marker appears on the chart when the second bar confirms the signal.

Green Volume Columns highlight the bars that fulfill the criteria, providing a quick visual confirmation of high-volume bullish bars.

Works fine on 1M-2M-5M-15M-30M. Do not use it on higher TF. Due the lack of historical data on lower TF, the backtest result is limited.

Adaptive Fractal Grid Scalping StrategyThis Pine Script v6 component implements an "Adaptive Fractal Grid Scalping Strategy" with an added volatility threshold feature.

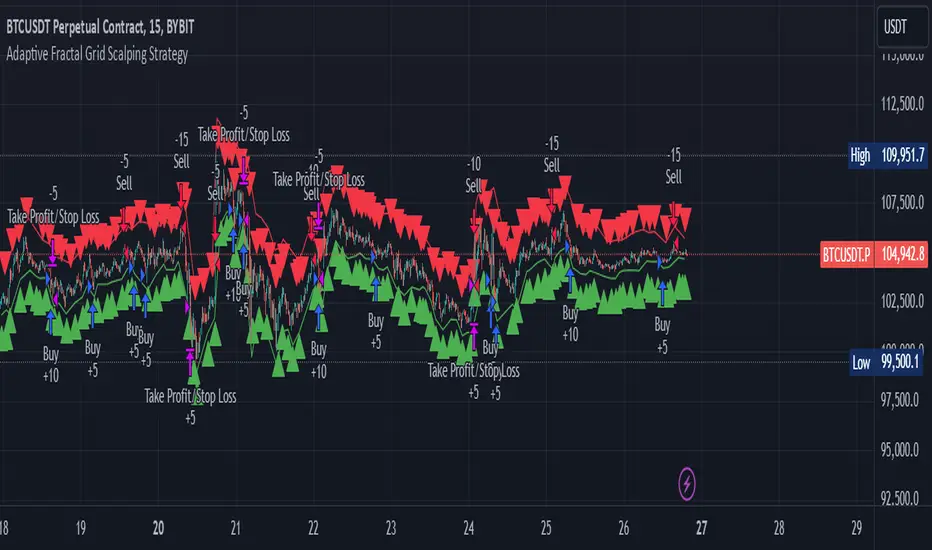

Here's how it works:

Fractal Break Detection: Uses ta.pivothigh and ta.pivotlow to identify local highs and lows.

Volatility Clustering: Measures volatility using the Average True Range (ATR).

Adaptive Grid Levels: Dynamically adjusts grid levels based on ATR and user-defined multipliers.

Directional Bias Filter: Uses a Simple Moving Average (SMA) to determine trend direction.

Volatility Threshold: Introduces a new input to specify a minimum ATR value required to activate the strategy.

Trade Execution Logic: Places limit orders at grid levels based on trend direction and fractal levels, but only when ATR exceeds the volatility threshold.

Profit-Taking and Stop-Loss: Implements profit-taking at grid levels and a trailing stop-loss based on ATR.

How to Use

Inputs: Customize the ATR length, SMA length, grid multipliers, trailing stop multiplier, and volatility threshold through the input settings.

Visuals: The script plots fractal points and grid levels on the chart for easy visualization.

Trade Signals: The strategy automatically places buy/sell orders based on the detected fractals, trend direction, and volatility threshold.

Profit and Risk Management: The script includes logic for taking profits and setting stop-loss levels to manage trades effectively.

This strategy is designed to capitalize on micro-movements during high volatility and avoid overtrading during low-volatility trends. Adjust the input parameters to suit your trading style and market conditions.

DCA Simulation for CryptoCommunity v1.1Overview

This script provides a detailed simulation of a Dollar-Cost Averaging (DCA) strategy tailored for crypto traders. It allows users to visualize how their DCA strategy would perform historically under specific parameters. The script is designed to help traders understand the mechanics of DCA and how it influences average price movement, budget utilization, and trade outcomes.

Key Features:

Combines Interval and Safety Order DCA:

Interval DCA: Regular purchases based on predefined time intervals.

Safety Order DCA: Additional buys triggered by percentage price drops.

Interactive Visualization:

Displays buy levels, average price, and profit-taking points on the chart.

Allows traders to assess how their strategy adapts to price movements.

Comprehensive Dashboard:

Tracks money spent, contracts acquired, and budget utilization.

Shows maximum amounts used if profit-taking is active.

Dynamic Safety Orders:

Resets safety orders when a new higher high is established.

Customizable Parameters:

Adjustable buy frequency, safety order settings, and profit-taking levels.

Suitable for traders with varying budgets and risk tolerances.

Default Strategy Settings:

Account Size: Default account size is set to $10,000 to represent a realistic budget for the average trader.

Commission & Slippage: Includes realistic trading fees and slippage assumptions to ensure accurate backtesting results.

Risk Management: Defaults to risking no more than 5% of the account balance per trade.

Sample Size: Optimized to generate a minimum of 100 trades for meaningful statistical analysis. Users can adjust parameters to fit longer timeframes or different datasets.

Usage Instructions:

Configure Your Strategy: Set the base order, safety order size, and buy frequency based on your preferred DCA approach.

Analyze Historical Performance: Use the chart and dashboard to understand how the strategy performs under different market conditions.

Optimize Parameters: Adjust settings to align with your risk tolerance and trading objectives.

Important Notes:

This script is for educational and simulation purposes. It is not intended to provide financial advice or guarantee profitability.

If the strategy's default settings do not meet your needs, feel free to adjust them while keeping risk management in mind.

TradingView limits the number of open trades to 999, so reduce the buy frequency if necessary to fit longer timeframes.

Advanced Position Management [Mr_Rakun]Advanced Position Management

This Pine Script code is for a strategy titled "Advanced Position Management," aimed at effective trade execution and management using multiple take profit levels, trailing stop loss, and dynamic position sizing.

Take Profit Levels: It defines up to three take profit (TP) levels, allowing partial position exits at different price thresholds. The take profit levels and their respective quantities are adjustable using inputs.

Stop Loss and Trailing Stop: The script implements an initial stop loss based on a percentage from the entry price. Additionally, it features a trailing stop that moves based on either a percentage or previous TP levels, dynamically adjusting to maximize gains while protecting profits.

Position Size: The position size is customizable and based on USD value, allowing the trader to manage risk more effectively.

Advantages:

Flexibility: Multiple take profit levels and a dynamic stop loss system allow traders to lock in profits while keeping the position open for further gains.

Risk Management: The initial stop loss and trailing stop help to limit losses and protect profits as the trade moves in the desired direction.

Automation: Once the strategy is deployed, it automatically handles entry, exit, and stop management, reducing the need for constant monitoring.

------ TR ------

Gelişmiş Pozisyon Yönetimi

Bu Pine Script kodu, Gelişmiş Pozisyon Yönetimi için kendi stratejilerinize kolayca entegre edeceğiniz bir risk yönetimidir. Çoklu kâr al seviyeleri, takip eden stop-loss ve dinamik pozisyon büyüklüğü kullanarak işlem yürütme ve yönetiminde etkilidir.

Gelişmiş Pozisyon Yönetimi

Kâr Alma Seviyeleri;

Kod, pozisyonların farklı fiyat seviyelerinde kısmi kapatılmasını sağlayan üç farklı kâr alma (TP) seviyesini tanımlar. Bu kâr alma seviyeleri ve ilgili miktarları, girişlerle ayarlanabilir.

Stop Loss ve Takip Eden Stop;

Koda, giriş fiyatından bir yüzdeye dayalı olarak başlangıçta stop-loss uygulanır. Ayrıca, fiyat hareketine göre kendini ayarlayan takip eden bir stop-loss sistemi bulunur. Ayrıca TP seviyelerini takip eden stop loss özelliğide vardır.

Avantajları:

Esneklik;

Çoklu kâr alma seviyeleri ve dinamik stop-loss sistemi, trader'ların kazançlarını kilitleyip aynı zamanda pozisyonu açık tutmalarına olanak tanır.

Risk Yönetimi;

Başlangıç stop-loss ve takip eden stop, zararı sınırlamaya ve kazançları korumaya yardımcı olur.

Otomasyon;

Strateji bir kez devreye alındığında, giriş, çıkış ve stop yönetimi otomatik olarak gerçekleştirilir, bu da sürekli takip ihtiyacını azaltır.