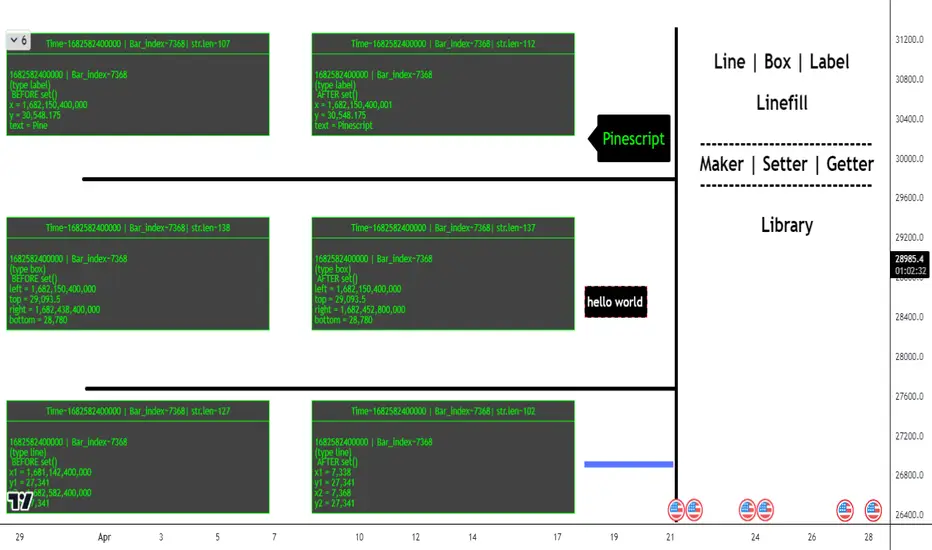

ObjectHelpersLibrary "ObjectHelpers"

Line | Box | Label | Linefill -- Maker, Setter, Getter Library

TODO: add table functionality

set(object)

set all params for `line`, `box`, `label`, `linefill` objects with 1 function

***

## Overloaded

***

```

method set(line Line, int x1=na, float y1=na, int x2=na, float y2=na,string xloc=na,string extend=na,color color=na,string style=na,int width=na,bool update=na) => line

```

### Params

- **Line** `line` - line object | `required`

- **x1** `int` - value to set x1

- **y1** `float` - value to set y1

- **x2** `int` - value to set x2

- **y2** `float` - value to set y2

- **xloc** `int` - value to set xloc

- **yloc** `int` - value to set yloc

- **extend** `string` - value to set extend

- **color** `color` - value to set color

- **style** `string` - value to set style

- **width** `int` - value to set width

- **update** `bool` - value to set update

***

```

method set(box Box,int left=na,float top=na,int right=na, float bottom=na,color bgcolor=na,color border_color=na,string border_style=na,int border_width=na,string extend=na,string txt=na,color text_color=na,string text_font_family=na,string text_halign=na,string text_valign=na,string text_wrap=na,bool update=false) => box

```

### Params

- **Box** `box` - box object

- **left** `int` - value to set left

- **top** `float` - value to set top

- **right** `int` - value to set right

- **bottom** `float` - value to set bottom

- **bgcolor** `color` - value to set bgcolor

- **border_color** `color` - value to set border_color

- **border_style** `string` - value to set border_style

- **border_width** `int` - value to set border_width

- **extend** `string` - value to set extend

- **txt** `string` - value to set _text

- **text_color** `color` - value to set text_color

- **text_font_family** `string` - value to set text_font_family

- **text_halign** `string` - value to set text_halign

- **text_valign** `string` - value to set text_valign

- **text_wrap** `string` - value to set text_wrap

- **update** `bool` - value to set update

***

```

method set(label Label,int x=na,float y=na, string txt=na,string xloc=na,color color=na,color textcolor=na,string size=na,string style=na,string textalign=na,string tooltip=na,string text_font_family=na,bool update=false) => label

```

### Paramas

- **Label** `label` - label object

- **x** `int` - value to set x

- **y** `float` - value to set y

- **txt** `string` - value to set text add`"+++"` to the _text striing to have the current label text concatenated to the location of the "+++")

- **textcolor** `color` - value to set textcolor

- **size** `string` - value to set size

- **style** `string` - value to set style (use "flip" ,as the style to have label flip to top or bottom of bar depending on if open > close and vice versa)

- **text_font_family** `string` - value to set text_font_family

- **textalign** `string` - value to set textalign

- **tooltip** `string` - value to set tooltip

- **update** `bool` - update label to next bar

***

```

method set(linefill Linefill=na,line line1=na,line line2=na,color color=na) => linefill

```

### Params

- **linefill** `linefill` - linefill object

- **line1** `line` - line object

- **line2** `line` - line object

- **color** `color` - color

Parameters:

object (obj)

Returns: `line`, `box`, `label`, `linefill`

method set(Line, x1, y1, x2, y2, xloc, extend, color, style, width, update)

set the location params of a line with 1 function auto detects time or bar_index for xloc param

Namespace types: series line

Parameters:

Line (line) : `line` - line object | `required`

x1 (int) : `int` - value to set x1

y1 (float) : `float` - value to set y1

x2 (int) : `int` - value to set x2

y2 (float) : `float` - value to set y2

xloc (string) : `int` - value to set xloc

extend (string) : `string` - value to set extend

color (color) : `color` - value to set color

style (string) : `string` - value to set style

width (int) : `int` - value to set width

update (bool) : `bool` - value to set update

Returns: `line`

method set(Box, left, top, right, bottom, bgcolor, border_color, border_style, border_width, extend, txt, text_color, text_font_family, text_halign, text_valign, text_wrap, update)

set the location params of a box with 1 function

Namespace types: series box

Parameters:

Box (box) : `box` - box object | `required`

left (int) : `int` - value to set left

top (float) : `float` - value to set top

right (int) : `int` - value to set right

bottom (float) : `float` - value to set bottom

bgcolor (color) : `color` - value to set bgcolor

border_color (color) : `color` - value to set border_color

border_style (string) : `string` - value to set border_style

border_width (int) : `int` - value to set border_width

extend (string) : `string` - value to set extend

txt (string) : `string` - value to set _text

text_color (color) : `color` - value to set text_color

text_font_family (string) : `string` - value to set text_font_family

text_halign (string) : `string` - value to set text_halign

text_valign (string) : `string` - value to set text_valign

text_wrap (string) : `string` - value to set text_wrap

update (bool) : `bool` - value to set update

Returns: `box`

method set(Label, x, y, txt, xloc, color, textcolor, size, style, textalign, tooltip, text_font_family, update)

set the location params of a label with 1 function auto detects time or bar_index for xloc param

Namespace types: series label

Parameters:

Label (label) : `label` | `required`

x (int) : `int` - value to set x

y (float) : `float` - value to set y

txt (string) : `string` - value to set text add`"+++"` to the _text striing to have the current label text concatenated to the location of the "+++")

xloc (string)

color (color)

textcolor (color) : `color` - value to set textcolor

size (string) : `string` - value to set size

style (string) : `string` - value to set style (use "flip" ,as the style to have label flip to top or bottom of bar depending on if open > close and vice versa)

textalign (string) : `string` - value to set textalign

tooltip (string) : `string` - value to set tooltip

text_font_family (string) : `string` - value to set text_font_family

update (bool) : `bool` - update label to next bar

Returns: `label`

method set(Linefill, line1, line2, color)

change the 1 or 2 of the lines in a linefill object

Namespace types: series linefill

Parameters:

Linefill (linefill)

line1 (line) : `line` - line object

line2 (line) : `line` - line object

color (color) : `color` - color

Returns: `linefill`

get(object)

get all of the location variables for `line`, `box`, `label` objects or the line objects from a `linefill`

***

## Overloaded

***

```

method get(line Line) =>

```

### Params

- **Line** `line` - line object | `required`

***

```

method get(box Box) =>

```

### Params

- **Box** `box` - box object | `required`

***

```

method get(label Label) =>

```

### Paramas

- **Label** `label` - label object | `required`

***

```

method get(linefill Linefill) =>

```

### Params

- **Linefill** `linefill` - linefill object | `required`

Parameters:

object (obj)

Returns: ` `

method get(Line)

Gets the location paramaters of a Line

Namespace types: series line

Parameters:

Line (line) : `line` - line object

Returns:

method get(Box)

Gets the location paramaters of a Box

Namespace types: series box

Parameters:

Box (box) : `box` - box object

Returns:

method get(Label)

Gets the `x`, `y`, `text` of a Label

Namespace types: series label

Parameters:

Label (label) : `label` - label object

Returns:

method get(Linefill)

Gets `line 1`, `line 2` from a Linefill

Namespace types: series linefill

Parameters:

Linefill (linefill) : `linefill` - linefill object

Returns:

method set_x(Line, x1, x2)

set the `x1`, `x2` of a line

***

### Params

- **Line** `line` - line object | `required`

- **x1** `int` - value to set x1 | `required`

- **x2** `int` - value to set x2 | `required`

Namespace types: series line

Parameters:

Line (line) : `line` - line object

x1 (int) : `int` - value to set x1

x2 (int) : `int` - value to set x2

Returns: `line`

method set_y(Line, y1, y2)

set `y1`, `y2` of a line

***

### Params

- **Line** `line` - line object | `required`

- **y1** `float` - value to set y1 | `required`

- **y2** `float` - value to set y2 | `required`

Namespace types: series line

Parameters:

Line (line) : `line` - line object

y1 (float) : `float` - value to set y1

y2 (float) : `float` - value to set y2

Returns: `line`

method Line(x1, y1, x2, y2, extend, color, style, width)

Similar to `line.new()` but can detect time or bar_index for xloc param and has defaults for all params but `x1`, `y1`, `x2`, `y2`

***

### Params

- **x1** `int` - value to set

- **y1** `float` - value to set

- **x2** `int` - value to set

- **y2** `float` - value to set

- **extend** `string` - extend value to set line

- **color** `color` - color to set line

- **style** `string` - style to set line

- **width** `int` - width to set line

Namespace types: series int, simple int, input int, const int

Parameters:

x1 (int) : `int` - value to set

y1 (float) : `float` - value to set

x2 (int) : `int` - value to set

y2 (float) : `float` - value to set

extend (string) : `string` - extend value to set line

color (color) : `color` - color to set line

style (string) : `string` - style to set line

width (int) : `int` - width to set line

Returns: `line`

method Box(left, top, right, bottom, extend, border_color, bgcolor, text_color, border_width, border_style, txt, text_halign, text_valign, text_size, text_wrap)

similar to box.new() with the but can detect xloc param and has defaults for everything but location params

***

### Params

- **left** `int` - value to set

- **top** `float` - value to set

- **right** `int` - value to set

- **bottom** `float` - value to set

- **extend** `string` - extend value to set box

- **border_color** `color` - color to set border

- **bgcolor** `color` - color to set background

- **text_color** `color` - color to set text

- **border_width** `int` - width to set border

- **border_style** `string` - style to set border

- **txt** `string` - text to set

- **text_halign** `string` - horizontal alignment to set text

- **text_valign** `string` - vertical alignment to set text

- **text_size** `string` - size to set text

- **text_wrap** `string` - wrap to set text

Namespace types: series int, simple int, input int, const int

Parameters:

left (int) : `int` - value to set

top (float) : `float` - value to set

right (int) : `int` - value to set

bottom (float) : `float` - value to set

extend (string) : `string` - extend value to set box

border_color (color) : `color` - color to set border

bgcolor (color) : `color` - color to set background

text_color (color) : `color` - color to set text

border_width (int) : `int` - width to set border

border_style (string) : `string` - style to set border

txt (string) : `string` - text to set

text_halign (string) : `string` - horizontal alignment to set text

text_valign (string) : `string` - vertical alignment to set text

text_size (string) : `string` - size to set text

text_wrap (string) : `string` - wrap to set text

Returns: `box`

method Label(txt, x, y, yloc, color, textcolor, style, size, textalign, text_font_family, tooltip)

Similar to label.new() but can detect time or bar_index for xloc param and has defaults for all params but x, y, txt, tooltip \n

***

### Params

- **txt** `string` - string to set

- **x** `int` - value to set

- **y** `float` - value to set

- **yloc** `string` - y location to set

- **color** `color` - label color to set

- **textcolor** `color` - text color to set

- **style** `string` - style to set

- **size** `string` - size to set

- **textalign** `string` - text alignment to set

- **text_font_family** `string` - font family to set

- **tooltip** `string` - tooltip to set

Namespace types: series string, simple string, input string, const string

Parameters:

txt (string) : `string` - string to set

x (int) : `int` - value to set

y (float) : `float` - value to set

yloc (string) : `string` - y location to set

color (color) : `color` - label color to set

textcolor (color) : `color` - text color to set

style (string) : `string` - style to set

size (string) : `string` - size to set

textalign (string) : `string` - text alignment to set

text_font_family (string) : `string` - font family to set

tooltip (string) : `string` - tooltip to set

Returns: `label`

obj

Fields:

obj (series__string)

Search in scripts for "top"

Order Blocks Volume Delta 3D | Flux ChartsGENERAL OVERVIEW:

Order Blocks Volume Delta 3D by Flux Charts is a rule-based order block and volume delta visualization tool. It detects bullish and bearish order blocks using a profile-of-price approach: the indicator finds the most actively traded price area (Point of Control, or POC) between a swing high/low and the Break of Structure (BOS), then anchors the order block to the earliest still-valid candle that traded through that POC band. From there, it tracks all candles that continue to interact with that zone and overlays both 2D and 3D volume delta views directly inside the order block.

Unlike traditional order block tools that simply use candle bodies or wicks, this indicator is volume-aware. It lets you optionally pull volume from a lower timeframe feed (for example, using 1-minute data while watching a 5-minute chart) to build a much more accurate picture of how buyers and sellers actually traded inside the zone. This makes every block not just a price box, but a volume story: which side dominated, where, and by how much.

All order blocks printed by this indicator are confirmed: BOS and retests are evaluated strictly on closed candles. Nothing is drawn or alerted on partially formed bars, which helps avoid repaint-style flicker and keeps the signals clean and stable.

What is the theory behind the indicator?:

The core idea behind Order Blocks Volume Delta 3D is that not all price levels inside an order block are equal. Some prices are barely touched, while others act like magnets where candles repeatedly trade and heavy volume passes through.

The indicator first finds a swing high or swing low, waits for a clear Break of Structure (BOS), then scans the candles between the swing point and the BOS to find the price level that was touched the most. That level is treated as the POC.

From all candles in the swing-to-BOS range that interact with this POC band, the indicator looks for the earliest candle that is not already mitigated and uses that as the anchor candle for the order block:

The top of the block equals the anchor candle’s high (for a bearish OB) or the top of its wick zone.

The bottom equals the anchor candle’s low (for a bullish OB) or the bottom of its wick zone.

This “earliest valid POC-touching candle” rule makes it easier to visualize how price and volume developed from the very start of a meaningful zone, while ignoring POC touches that are already fully mitigated by the time the structure is confirmed. On top of that, each candle is split into bullish and bearish volume. If you choose a lower timeframe volume input, the tool aggregates lower timeframe candles into your chart timeframe, giving a more granular bull-versus-bear breakdown for each bar. The result is

an order block that not only shows where price moved but also which side pushed it, how aggressively, and how that balance shifted over time.

ORDER BLOCKS VOLUME DELTA 3D FEATURES:

The Order Blocks Volume Delta 3D indicator includes 4 main features:

1. Order Blocks

2. Volume Delta

3. 3D Visualization

4. Alerts

ORDER BLOCKS:

🔹What is an Order Block

An order block is a price zone where a clear displacement move began after liquidity was taken. It usually forms around the last consolidation or cluster of candles before price breaks structure with a strong move.

In this indicator, order blocks are defined as structured zones that:

Begin at the earliest unmitigated candle that interacted with the most-touched price level (POC) between swing and BOS.

Extend through the full wick range of that anchor candle.

Stretch forward in time, tracking how price continues to trade through, respect, retest, or invalidate the zone.

Are only printed once the BOS is fully confirmed on closed candles (confirmed order blocks only).

Example of bullish and bearish order blocks anchored at the earliest unmitigated candle in the POC zone:

🔹How are Order Blocks detected

The indicator uses a step-by-step, rules-based process to detect bullish and bearish order blocks. The logic is designed to match discretionary Smart Money concepts but with strict, repeatable rules.

Step 1: Detect swing highs and swing lows

Swing High: a candle whose high is higher than the highs of surrounding candles.

Swing Low: a candle whose low is lower than the lows of surrounding candles.

The Swing Length input controls how many candles are checked to the left and right.

Example of swing high and swing low detection:

Step 2: Confirm Break of Structure (BOS)

Once a swing is confirmed, the indicator waits for price to break past that swing:

Bullish BOS: price closes above a previous swing high.

Bearish BOS: price closes below a previous swing low.

To avoid “live” flicker, BOS logic is evaluated based on the previous closed candle. The order block is only confirmed once the BOS candle has fully closed and the next bar has opened. This is one of the reasons the script only shows confirmed, non-repainting order blocks.

Example of bullish BOS and bearish BOS:

Step 3: Build the POC range between swing and BOS

Between the swing candle and the BOS candle, the indicator:

Scans all candles in that range.

Tracks every price level touched using binning (POC bins).

Counts how many times each price band was touched by candle wicks.

The bin with the highest touch count becomes the POC band. This is where price traded most often, not necessarily where volume was highest.

Example of the POC band between swing and BOS.

Step 4 – Anchor the order block to the earliest valid POC candle

From all candles in the swing-to-BOS range, the indicator finds the earliest candle whose high/low overlaps the POC band and whose zone is not already mitigated. That candle becomes the anchor candle for the order block:

For a bearish OB, the block spans the anchor candle’s full wick range, with its top at the high.

For a bullish OB, the block spans the anchor candle’s full wick range, with its bottom at the low.

By requiring the anchor to be the earliest unmitigated interaction with POC, the script avoids building blocks from price action that has already been fully traded through and is less relevant.

Step 5: Extend and manage the order block

Once created, the block:

Extends to the right by a configurable number of candles (Extend Zones).

Continues until it is invalidated by wick or close, depending on the chosen method.

Can show retest labels when price revisits the zone after creation.

Is included or excluded from display depending on the Show Nearest and Hide Invalidated Zones settings.

Example of active and invalidated OB.

🔹Order Block Settings

◇ Swing Length

Swing Length controls how sensitive swing highs and lows are.

Lower Swing Length: Swings form more frequently, which leads to more frequent BOS events and order block formations.

Higher Swing Length: Only larger, more meaningful swings are detected, which leads to less frequent BOS events and less order block formations.

◇ Invalidation

Invalidation determines how an order block is considered “mitigated” or no longer valid.

Wick: For bullish OBs, if price wicks completely through the bottom of the zone, the order block is invalidated. For bearish OBs, if price wicks completely through the top, the order block is invalidated.

Close: For bullish OBs, the block is invalidated only when a candle closes below the bottom. For bearish OBs, it is invalidated only when a candle closes above the top.

Example of wick invalidation:

Example of close invalidation:

◇ Show Nearest

Show Nearest limits how many active order blocks are displayed based on proximity to current price. For example, a value of 2 will display only the two nearest bullish order blocks and two nearest bearish order blocks.

Chart with Show Nearest set to 3:

◇ Extend Zones

Extend Zones define how many candles forward each order block should project beyond the right most candle on the chart.

Chart with Extend Zones set to 10:

◇ Retest Labels

When enabled, the indicator prints labels on every clean retest of an active order block, as long as that block remains valid. Key points:

A retest label is only printed once the retest candle has fully closed – you always see confirmed retests, not intrabar tests.

Retest labels are positioned on the actual retest candle so you can visually see which bar interacted with the zone.

In addition, if multiple retests occur in quick succession, the indicator applies a built-in three-candle buffer between retests. That means only the first valid retest within each three-bar window is labeled (and can trigger an alert), helping to reduce clutter while still highlighting meaningful interactions with the zone.

Example of retest labels on bullish and bearish order blocks.

◇ Hide Invalidated Zones

Hide Invalidated Zones controls whether mitigated/invalidated blocks stay drawn.

Enabled: Only currently valid, unmitigated order blocks are shown (subject to Show Nearest)

Disabled: Both active and invalidated order blocks are displayed.

VOLUME DELTA:

🔹What is Volume Delta

Volume delta measures the difference between buying and selling volume. Instead of only showing “how much volume traded”, it separates volume into bullish and bearish components.

In this indicator:

Bullish volume = volume from candles (or lower timeframe candles) that closed higher.

Bearish volume = volume from candles that closed lower.

Delta % shows how dominant one side was compared to the total.

Example of bullish and bearish order blocks with volume delta and total volume.

🔹How is Volume Delta calculated?

The indicator uses a flexible, timeframe-aware volume engine.

1. Choose a Volume Delta Timeframe.

If the selected timeframe is equal to or higher than the chart timeframe, the indicator simply uses chart-volume per candle.

If the selected timeframe is lower than the chart timeframe (for example, 1‑minute volume on a 5‑minute chart), the indicator pulls all lower timeframe candles for each chart bar and sums them.

2. Split each bar into bull and bear volume.

For each contributing candle:

If close > open → its volume is added to bullish volume.

If close < open → its volume is added to bearish volume.

If close == open → its volume is split evenly between bullish and bearish.

3. Aggregate for each order block.

For each order block:

The indicator loops once from the swing candle to the BOS candle.

It records every candle that touches the POC band.

For each touching candle, it adds its bull and bear volumes (either directly from chart candles or from aggregated lower timeframe candles).

Total volume = bullish volume + bearish volume

Delta % = (bullish volume or bearish volume / total volume ) * 100, depending on which side is dominant.

🔹Volume Delta Settings:

◇ Display Style

Display Style controls how the volume delta is drawn inside each order block:

Horizontal:

Bullish and bearish fills extend horizontally from left to right.

The filled strip sits along the base of the block, with a bull vs bear gradient.

Vertical:

Bullish and bearish fills stretch vertically inside the zone.

The bullish percentage controls how much of the block is filled with the “dominant” color.

Example of Horizontal display style.

Example of Vertical display style.

◇ Volume Delta Timeframe

Volume Delta Timeframe tells the indicator whether to use chart volume or lower timeframe volume. When set to a lower timeframe, the indicator aggregates all lower timeframe candles that fall inside each chart bar, splitting their volume into bullish and bearish components before summing.

Using a lower timeframe:

Increases precision for how volume truly behaved inside each bar.

Helps reveal hidden absorption and aggressive flows that a higher timeframe candle might hide.

Example of volume delta based on chart timeframe.

Example of volume delta based on lower timeframe than chart(same OB as above)

◇ Display Total Volume

When enabled, the indicator prints the total volume for each order block as a label positioned inside the zone, near the bottom-right corner. This total is the sum of bullish and bearish volume used in the delta calculation and gives you a quick sense of how “heavy” the trading was in that block compared to others.

Example of total volume label inside multiple order blocks.

◇ Show Delta %

Show Delta % draws a small text label on the strip of the block that displays the dominant side’s percentage. For example, a bullish block might show “72%” if 72% of all volume inside that POC band came from bullish volume.

Example of Delta %:

3D VISUALIZATION:

The 3D Visualization feature turns each order block into a 3D plot.

🔹What the 3D Visualization does:

Wraps the order block with side faces and a top face to create a 3D bar effect.

Uses delta percentages to tilt the top face toward the dominant side.

Projects blocks into the future using Extend Zones, making the 3D blocks visually stand out.

🔹How it works:

The front face of the OB shows the standard 2D zone.

The side face extends forward in time based on the 3D depth setting.

The top face is angled depending on the Display Style and bull vs bear delta, making strong bullish blocks “rise” and strong bearish blocks “sink”.

🔹How the 3D depth setting affects visuals

Lower 3D depth:

Shorter side faces.

Subtle 3D effect.

Higher 3D depth:

Longer side faces projecting further into the future.

Stronger 3D effect that visually highlights key zones.

Example of lower 3D depth:

Example of higher 3D depth:

ALERTS:

The indicator supports alert conditions through TradingView’s AnyAlert() engine, allowing you to set alerts for the following:

New Bullish Order Block formed

New Bearish Order Block formed

Bullish OB Retest

Bearish OB Retest

Important alert behavior:

Order block alerts only fire when a new block is confirmed (after BOS closes and the next bar opens).

Retest alerts only fire when a retest candle has completely finished, matching the behavior of the visual retest labels.

IMPORTANT NOTES:

3D faces for order blocks are built using polylines. In some situations, especially when an order block’s starting point (its left edge) is beyond the chart’s left-most visible bar, the top 3D face may appear slightly irregular, skewed, or incomplete. This is purely a drawing limitation related to how the chart engine handles off-screen polyline points. Once the starting point of that order block comes into view (by zooming out or scrolling back), the 3D top face corrects itself and the visual becomes fully consistent. This issue affects only the 3D top face drawing, not the actual order-block box itself. The underlying zone, prices, and volume calculations remain accurate at all times.

If all conditions are met to create a new order block but the resulting zone would overlap an existing active order block, the new block is intentionally not created. A built-in guard prevents overlapping active zones to keep the structure clean and easier to interpret.

3D face drawing is implemented using an adaptive polyline method, which can be relatively calculation-heavy on certain symbols, timeframes, or chart histories. In some cases this may lead to calculation timeout error from TradingView.

UNIQUENESS:

This indicator is unique because it:

Anchors each order block to the earliest unmitigated candle that traded through the most-touched POC band between swing and BOS, rather than a generic “last up/down candle” or a random volume spike.

Builds a dedicated volume engine that can pull either chart timeframe volume or aggregated lower timeframe volume, then splits it into bull and bear components.

Adds 3D visualization on top of standard zones, turning each OB into a visually weighted slab rather than a flat rectangle.

Provides clean toggles (Show Nearest, Hide Invalidated Zones, Extend Zones, Display Style, Delta %, and total volume labels) so you can dial the indicator from extremely minimal to fully detailed, depending on your trading workflow.

Combined, these features make the indicator not just an order block plotter, but a complete volume‑informed structure tool tailored for traders who want to see where price actually traded and whether bulls or bears truly controlled the move inside each order block.

High/Low Location Frequency [LuxAlgo]The High/Low Location Frequency tool provides users with probabilities of tops and bottoms at user-defined periods, along with advanced filters that offer deep and objective market information about the likelihood of a top or bottom in the market.

🔶 USAGE

There are four different time periods that traders can select for analysis of probabilities:

HOUR OF DAY: Probability of occurrence of top and bottom prices for each hour of the day

DAY OF WEEK: Probability of occurrence of top and bottom prices for each day of the week

DAY OF MONTH: Probability of occurrence of top and bottom prices for each day of the month

MONTH OF YEAR: Probability of occurrence of top and bottom prices for each month

The data is displayed as a dashboard, which users can position according to their preferences. The dashboard includes useful information in the header, such as the number of periods and the date from which the data is gathered. Additionally, users can enable active filters to customize their view. The probabilities are displayed in one, two, or three columns, depending on the number of elements.

🔹 Advanced Filters

Advanced Filters allow traders to exclude specific data from the results. They can choose to use none or all filters simultaneously, inputting a list of numbers separated by spaces or commas. However, it is not possible to use both separators on the same filter.

The tool is equipped with five advanced filters:

HOURS OF DAY: The permitted range is from 0 to 23.

DAYS OF WEEK: The permitted range is from 1 to 7.

DAYS OF MONTH: The permitted range is from 1 to 31.

MONTHS: The permitted range is from 1 to 12.

YEARS: The permitted range is from 1000 to 2999.

It should be noted that the DAYS OF WEEK advanced filter has been designed for use with tickers that trade every day, such as those trading in the crypto market. In such cases, the numbers displayed will range from 1 (Sunday) to 7 (Saturday). Conversely, for tickers that do not trade over the weekend, the numbers will range from 1 (Monday) to 5 (Friday).

To illustrate the application of this filter, we will exclude results for Mondays and Tuesdays, the first five days of each month, January and February, and the years 2020, 2021, and 2022. Let us review the results:

DAYS OF WEEK: `2,3` or `2 3` (for crypto) or `1,2` or `1 2` (for the rest)

DAYS OF MONTH: `1,2,3,4,5` or `1 2 3 4 5`

MONTHS: `1,2` or `1 2`

YEARS: `2020,2021,2022` or `2020 2021 2022`

🔹 High Probability Lines

The tool enables traders to identify the next period with the highest probability of a top (red) and/or bottom (green) on the chart, marked with two horizontal lines indicating the location of these periods.

🔹 Top/Bottom Labels and Periods Highlight

The tool is capable of indicating on the chart the upper and lower limits of each selected period, as well as the commencement of each new period, thus providing traders with a convenient reference point.

🔶 SETTINGS

Period: Select how many bars (hours, days, or months) will be used to gather data from, max value as default.

Execution Window: Select how many bars (hours, days, or months) will be used to gather data from

🔹 Advanced Filters

Hours of day: Filter which hours of the day are excluded from the data, it accepts a list of hours from 0 to 23 separated by commas or spaces, users can not mix commas or spaces as a separator, must choose one

Days of week: Filter which days of the week are excluded from the data, it accepts a list of days from 1 to 5 for tickers not trading weekends, or from 1 to 7 for tickers trading all week, users can choose between commas or spaces as a separator, but can not mix them on the same filter.

Days of month: Filter which days of the month are excluded from the data, it accepts a list of days from 1 to 31, users can choose between commas or spaces as separator, but can not mix them on the same filter.

Months: Filter months to exclude from data. Accepts months from 1 to 12. Choose one separator: comma or space.

Years: Filter years to exclude from data. Accepts years from 1000 to 2999. Choose one separator: comma or space.

🔹 Dashboard

Dashboard Location: Select both the vertical and horizontal parameters for the desired location of the dashboard.

Dashboard Size: Select size for dashboard.

🔹 Style

High Probability Top Line: Enable/disable `High Probability Top` vertical line and choose color

High Probability Bottom Line: Enable/disable `High Probability Bottom` vertical line and choose color

Top Label: Enable/disable period top labels, choose color and size.

Bottom Label: Enable/disable period bottom labels, choose color and size.

Highlight Period Changes: Enable/disable vertical highlight at start of period

Williams Vix Fix BB + RVI & Squeeze (Keltner) filtered BBW + %BLegend:

- When line touches or crosses red band it is Top signal (Williams Vix Fix)

- When line touches or crosses blue band it is Bottom signal (Williams Vix Fix)

- Red dot at the top of indicator is a Top signal (Relative Volatility Index)

- Blue dot at the top of indicator is a Bottom signal (Relative Volatility Index)

- Gray dot at the bottom of indicator is a Keltner Squeeze signal (filtered by either BBW or %B)

- Silver dot at the bottom of indicator is a weaker Keltner Squeeze signal (Doesn't meet either BBW or %B filter)

- Purple is a 'Half Squeeze' only 1 Bollinger Band crossed the Keltner Channel

This is an attempt to make use of the main features of all 6 of these Volatility tools :

- Williams Vix Fix + Bollinger Bands

- Relative Volatility Index (RVI)

- The crossing of Keltner Channel by the Bollinger Bands (Squeeze)

Conditions to Help Filter Keltner Squeeze:

- When the Bollinger Bands Width (BBW) value is lower than the lowest value within a period plus a margin of error (percentage)

- When the %B value reaches the alert level detailed in LazyBears indicator. ()

If it meets one of these 2 filters and there is a Keltner Channel Squeeze than gray color or else if the squeeze doesn’t meet one of the 2 filters than silver color (weaker Squeeze).

The goal is to find the best tool to find bottoms and top relative to volatility and filter the squeeze.

The idea is that both Williams Vix Fix + Bollinger Bands and Relative Volatility Index both already give the main volatility bottom and top so combining them to compare and validate the signals makes sense. (Note: Bottom signal is more accurate than top). In addition, I added the squeeze to show the potential breakout pressure and to compliment bottom and top signals.

For ideas on how to continue this work :

I encourage ideas to combine the Williams Vix Fix and Relative Volatility Index for volatility top and bottom (with probability would be awesome)

And I encourage ideas to filter Keltner Channel Volatility Squeeze using both the BBW or %B or other volatility squeeze indicators or a combination of all of them.

Also, I encourage people to post their top parameters for the BBW and %B to filter the Keltner Squeeze in the comments or to send me them by chat relative to this indicator.

Half the battle is making the indicator, while the other half is tuning the parameters.

The current parameters are one of the least aggressive, and act as a mild filter.

Note: You can also change the threshold for RVI top and bottom.

And this work builds on my last indicator:

If you have ideas on this work or have ideas on potential combinations please message me, I always want to learn or get perspective on how it can be improved.

Sharing is how we get better (Parameter tuning, ideas, discussion)

I don’t reinvent the wheel, just trying to make the wheel better.

Momentum Day Trading ToolkitMomentum Day Trading Toolkit

Complete User Guide

Table of Contents

Overview

Quick Start

The Dashboard

Module 1: 5 Pillars Screener

Module 2: Gap & Go

Module 3: Bull Flag / Flat Top

Module 4: Float Rotation

Module 5: R2G / G2R

Module 6: Micro Pullback

Signal Reference

Quality Score

Settings Guide

Alerts Setup

Trading Workflows

Troubleshooting

Overview

The Momentum Day Trading Toolkit combines 6 powerful indicators into one unified system for day trading momentum stocks.

ModulePurpose① 5 PillarsConfirms stock is "in play"② Gap & GoPre-market levels & gap analysis③ Bull Flag / Flat TopClassic breakout patterns④ Float RotationMeasures true interest level⑤ R2G / G2RTracks prior close crosses⑥ Micro PullbackPrecision continuation entries

All modules work together - the dashboard shows you everything at a glance, and you can enable/disable any module you don't need.

Quick Start

Step 1: Add to Chart

Add the indicator to any stock chart

Recommended timeframes: 1-minute, 5-minute, or 15-minute

Step 2: Check the Dashboard (Top Right)

Look for:

Status = Current state (Scanning, Entry Signal, etc.)

Quality Score = Setup rating out of 10

Green checkmarks (✓) = Criteria passing

Step 3: Watch for Entry Signals

Triangles, circles, diamonds below bars = Entry signals

Arrows = R2G/G2R crosses

Step 4: Set Alerts

Right-click chart → Add Alert

Select "Momentum Day Trading Toolkit"

Choose your alert condition

The Dashboard

The dashboard in the top-right corner gives you instant analysis:

┌─────────────────────────────┐

│ MOMENTUM TOOLKIT │

├─────────────────────────────┤

│ Status │ 🎯 ENTRY SIGNAL │

│ Day │ 🟢 GREEN │

│ Gap │ +8.5% 🔥 │

│ RVol │ 3.2x ✓ │

│ Rotation │ 1.45x 🔥 │

│ Float │ 5.2M 🔥 │

│ Change │ +12.3% ✓ │

│ Pattern │ BULL FLAG! │

│ EMA 9/20 │ Above Both ✓ │

│ VWAP │ Above ✓ │

│ Prior Cl │ 5.91 │

│ PM High │ 9.11 ✓ │

│ Price │ 9.46 ✓ │

└─────────────────────────────┘

Dashboard Row Reference

RowWhat It ShowsGood ValuesStatusCurrent state🎯 ENTRY SIGNALDayGreen/Red vs prior close🟢 GREENGapGap % from prior close🔥 (5%+) or 🔥🔥 (10%+)RVolRelative volume✓ (2x+) or ✓✓ (5x+)RotationFloat rotation🔥 (1x) or 🔥🔥 (2x+)FloatFloat in millions🔥 (<5M) or Low (<10M)ChangeDaily % change✓ (meets minimum)PatternPattern statusBREAKOUT!EMA 9/20Trend positionAbove Both ✓VWAPVWAP positionAbove ✓Prior CloseKey R2G levelReference pricePM HighPre-market high✓ = Above itPriceCurrent price✓ = In range

Status Messages

StatusMeaningActionScanning...Looking for setupsWait✅ ALL PILLARSStock qualifiesWatch for pattern⏳ PATTERN FORMINGSetup developingGet ready🎯 ENTRY SIGNALSignal triggeredExecute trade

Module 1: 5 Pillars Screener

What It Does

Confirms the stock meets basic criteria to be worth trading.

The 5 Pillars

PillarDefaultWhy It MattersRelative Volume2x+ (5x for "strong")Confirms unusual interestDaily Change5%+Stock is movingPrice Range$1-$20Sweet spot for momentumFloat Size<20M sharesLower float = bigger moves

Visual Indicator

Green background appears when ALL pillars pass

Dashboard Shows

Individual pillar status with ✓ checkmarks

Quality score includes pillar factors

Settings

SettingDefaultDescriptionMin RVol2.0xMinimum relative volumeStrong RVol5.0xVolume for full qualificationMin Change5%Minimum daily moveMin Price$1Minimum stock priceMax Price$20Maximum stock priceMax Float20MMaximum float size

Module 2: Gap & Go

What It Does

Analyzes pre-market gaps and displays key price levels.

Key Levels Displayed

LevelColorDescriptionPrior CloseOrangeYesterday's close - THE key levelPM HighGreenPre-market high - breakout levelPM LowRedPre-market low - support

Gap Classification

Gap SizeRatingMeaning5-9.9%🔥 QualifyingWorth watching10%+🔥🔥 StrongHigh priority

Entry Signal

Small green triangle = PM High Breakout

How to Trade

Stock gaps up in pre-market

Wait for market open

Look for break above PM High

Enter on breakout with stop below PM Low

Settings

SettingDefaultDescriptionMin Gap %5%Qualifying gap thresholdStrong Gap %10%Strong gap thresholdShow PM LevelsONDisplay PM high/low lines

Module 3: Bull Flag / Flat Top

What It Does

Detects classic continuation patterns and signals breakouts.

Bull Flag Pattern

▲ BREAKOUT (Entry Signal)

│

┌────┴────┐

│ Pullback │ ← 2-5 red candles

│ (flag) │ Max 50% retrace

└─────────┘

│

┌────┴────┐

│ Pole │ ← 3+ green candles

│ (move) │ Strong momentum

└─────────┘

Flat Top Pattern

═══════════════ Resistance (2+ touches)

│

▲ BREAKOUT above resistance

Entry Signals

SignalShapeColorPatternBull Flag Breakout▲ TriangleLimeFlag breaks upFlat Top Breakout◆ DiamondAquaResistance breaks

How to Trade Bull Flag

See 3+ green candles (the pole)

Price pulls back 2-5 red candles

Pullback stays above 50% of move

Enter on break above pullback high

Stop below pullback low

Settings

SettingDefaultDescriptionMin Pole Candles3Green candles neededMax Pullback5Max red candles allowedMax Retrace50%Max pullback depthFT Touches2Resistance touches neededFT Lookback10Bars to check for resistance

Module 4: Float Rotation

What It Does

Tracks how many times the entire float has traded hands today.

The Formula

Rotation = Cumulative Day Volume ÷ Float

Rotation Levels

RotationEmojiMeaning0.5x—Half float traded1.0x🔥FULL rotation - significant!2.0x🔥🔥Double rotation - extreme3.0x+🔥🔥🔥Triple rotation - rare event

Why It Matters

High rotation = Extreme interest

Everyone who owns shares has likely traded

Often precedes explosive moves

Shows "real" demand beyond just volume

Dashboard Shows

Current rotation level

Fire emojis for milestones

Settings

SettingDefaultDescriptionFloat SourceAutoAuto-detect or manualManual Float10MIf auto fails, use thisAlert Level1.0xAlert when rotation hits this

Module 5: R2G / G2R

What It Does

Tracks when price crosses the prior day's close - a key psychological level.

Red to Green (R2G) 🟢

Prior Close ─────────────────

↗ CROSS TO GREEN

↗

(opened red)

Stock opened below prior close (red)

Crosses above prior close (green)

BULLISH signal

Green to Red (G2R) 🔴

(opened green)

↘

↘ CROSS TO RED

Prior Close ─────────────────

Stock opened above prior close (green)

Crosses below prior close (red)

BEARISH signal

Entry Signals

SignalShapeColorMeaningR2G↑ ArrowLimeCrossed to greenG2R↓ ArrowRedCrossed to red

Why R2G Matters

Bears who shorted get squeezed

Creates FOMO buying

Prior close becomes support

Momentum often continues

Dashboard Shows

Current day status (🟢 GREEN / 🔴 RED)

Whether R2G or G2R occurred (R2G ✓ or G2R ✓)

Settings

SettingDefaultDescriptionRequire Opposite OpenONR2G needs red openShow Prior CloseONDisplay the line

Module 6: Micro Pullback

What It Does

Finds precision entries on brief 1-3 candle pullbacks after strong moves.

The Pattern

▲ ENTRY (break pullback high)

│

┌──┴───┐

│ 1-3 │ ← Micro pullback (brief!)

│ red │ Stop = low of this

└──────┘

│

┌──┴───┐

│ 3+ │ ← Strong move

│green │ Momentum building

└──────┘

Why Micro Pullbacks Work

Tight stop = Pullback low is close

Momentum intact = Only paused briefly

Early entry = Catch continuation early

Clear trigger = Break of pullback high

Entry Signal

SignalShapeColorMicro Pullback Entry● CircleYellow

How to Trade

See 3+ green candles (strong move)

1-3 red candles (brief pause)

Pullback stays above 50% retrace

Enter when green candle breaks pullback high

Stop at pullback low

Settings

SettingDefaultDescriptionMin Green Candles3Candles before pullbackMax Pullback3Max red candlesMax Retrace50%Max pullback depth

Signal Reference

All Entry Signals (Below Bar)

ShapeColorSignalModule▲ Large TriangleLimeBull Flag BreakoutPatterns◆ DiamondAquaFlat Top BreakoutPatterns● CircleYellowMicro Pullback EntryMicro PB▲ Small TriangleGreenPM High BreakoutGap & Go↑ ArrowLimeRed to GreenR2G/G2R

Warning Signals (Above Bar)

ShapeColorSignalModule↓ ArrowRedGreen to RedR2G/G2R

Optional Forming Signals (Disabled by Default)

ShapeColorSignal🚩 FlagFaded LimeBull Flag Forming● CircleFaded YellowMicro PB Forming

Enable "Show 'Forming' Markers" in settings to see these

Quality Score

The quality score (0-10) rates the overall setup strength.

Scoring Breakdown

FactorPointsRVol 5x++2RVol 2x++1Daily change 5%++1Low float (<20M)+1Strong gap (10%+)+2Qualifying gap (5%+)+1Rotation 1x++2Rotation 0.5x++1Above EMA 20+1

Score Interpretation

ScoreGradeAction8-10A+Best setups - full position6-7AGood setups - standard size4-5BAverage - reduced size0-3CWeak - skip or paper trade

Settings Guide

Module Toggles

Turn each module ON/OFF:

SettingDefaultDescription① 5 Pillars ScreenerONStock qualification② Gap & Go AnalysisONGap & level analysis③ Bull Flag / Flat TopONPattern detection④ Float RotationONRotation tracking⑤ R2G / G2R TrackerONPrior close crosses⑥ Micro PullbackONPullback entries

Visual Settings

SettingDefaultDescriptionShow DashboardONDisplay info tableTable SizeNormalSmall/Normal/LargeShow Entry SignalsONDisplay entry shapesShow 'Forming' MarkersOFFShow pattern formingShow Key LevelsONPrior close, PM levelsShow EMA 9/20ONTrend EMAsShow VWAPONVWAP line

Recommended Presets

Minimal (Clean Chart)

Show Dashboard: ON

Show Entry Signals: ON

Show 'Forming' Markers: OFF

Show Key Levels: OFF

Show EMA: OFF

Show VWAP: OFF

Standard (Balanced)

All defaults

Full Analysis

All settings ON

Alerts Setup

Available Alerts

AlertTriggerAny Bullish EntryAny entry signal firesBull Flag BreakoutBull flag breaks outFlat Top BreakoutFlat top breaks outMicro Pullback EntryMicro PB triggersPM High BreakoutBreaks above PM highRed to GreenR2G crossGreen to RedG2R crossFloat RotationHits rotation level5 Pillars PassAll pillars qualifyPattern FormingPattern starts formingHigh Quality EntryEntry with score 7+/10

How to Set Alerts

Right-click on chart

Select "Add Alert"

Condition: "Momentum Day Trading Toolkit"

Select alert type from dropdown

Set expiration and notifications

Click "Create"

Recommended Alerts

For Active Trading:

Any Bullish Entry

High Quality Entry

For Watchlist Monitoring:

5 Pillars Pass

Float Rotation

Trading Workflows

Workflow 1: Full Qualification

Step 1: 5 PILLARS

└─→ Wait for "✅ ALL PILLARS" status

Step 2: CHECK SETUP

└─→ Quality score 6+?

└─→ Above EMA and VWAP?

Step 3: WAIT FOR ENTRY

└─→ Bull Flag, Flat Top, or Micro PB signal

Step 4: EXECUTE

└─→ Enter on signal

└─→ Stop below pattern low

└─→ Target 2:1 minimum

Workflow 2: Gap & Go

Step 1: PRE-MARKET

└─→ Stock gaps 5%+ (shows in Gap row)

Step 2: MARKET OPEN

└─→ Note PM High level (green line)

Step 3: WAIT FOR BREAK

└─→ PM High Breakout signal (small triangle)

Step 4: CONFIRM

└─→ R2G if opened red (double confirmation)

└─→ RVol 2x+

Step 5: EXECUTE

└─→ Enter on PM High break

└─→ Stop below PM Low

Workflow 3: Micro Pullback Scalp

Step 1: FIND MOMENTUM

└─→ Stock moving, 3+ green candles

Step 2: WAIT FOR PAUSE

└─→ 1-3 red candles (brief pullback)

Step 3: ENTRY

└─→ Yellow circle signal appears

Step 4: QUICK TRADE

└─→ Enter at signal

└─→ Tight stop at pullback low

└─→ Quick target (1:1 to 2:1)

Troubleshooting

Q: Lines are moving/jumping on real-time chart?

A: This was fixed in latest version. Make sure you have the newest code. Lines now lock in place at market open.

Q: Too many signals, chart is cluttered?

A:

Turn off "Show 'Forming' Markers"

Disable modules you don't need

Use "Minimal" visual preset

Q: No signals appearing?

A:

Check if "Show Entry Signals" is ON

Make sure relevant module is enabled

Stock may not meet pattern criteria

Q: Dashboard shows wrong float?

A:

TradingView float data isn't available for all stocks

Switch Float Source to "Manual"

Enter correct float in millions

Q: PM High/Low not showing?

A:

Only appears during market hours

Needs pre-market data to calculate

Check if "Show Key Levels" is ON

Q: Quality score seems wrong?

A:

Score updates in real-time

Check individual factors in dashboard

RVol and rotation change throughout day

Q: Alert not triggering?

A:

Make sure alert is set on correct symbol

Check alert hasn't expired

Verify condition is set correctly

Quick Reference Card

Entry Signals

▲ Lime Triangle = Bull Flag Breakout

◆ Aqua Diamond = Flat Top Breakout

● Yellow Circle = Micro Pullback

▲ Green Triangle = PM High Break

↑ Lime Arrow = R2G (bullish)

↓ Red Arrow = G2R (bearish)

Dashboard Quick Read

🎯 = Entry signal active

✅ = All pillars pass

🟢 = Day is green

🔥 = Strong (gap/rotation)

✓ = Criteria met

✗ = Criteria failed

Quality Score

8-10 = A+ (Best)

6-7 = A (Good)

4-5 = B (Average)

0-3 = C (Weak)

Key Levels

Orange Line = Prior Close (R2G level)

Green Line = PM High (breakout level)

Red Line = PM Low (support)

Purple Line = VWAP

Yellow/Orange = EMA 9/20

Happy Trading! 🎯📈

For questions or issues, use TradingView's comment section on the indicator page.

Smart Money Volume Matrix [Ata]Smart Money Volume Matrix

The Smart Money Volume Matrix (SMV Matrix) is an advanced volume-spread analysis (VSA) dashboard and charting tool designed to identify significant market anomalies by analyzing the relationship between price extremes and volume flow.

Unlike traditional indicators that rely solely on moving averages or oscillators, this tool performs a "Snapshot Analysis" of a defined lookback period (default: 100 bars) to rank price action based on Order Flow Dominance. It isolates the Top 10 Highest and Lowest Close prices and scrutinizes the volume behind them to categorize market sentiment into four distinct phases: Distribution, No Demand, Absorption, and Exhaustion.

Core Logic & Methodology

The script operates on a Zero-Lag Snapshot Engine. It does not print historical signals bar-by-bar; instead, it evaluates the current market structure relative to the recent history (Lookback Period).

1. Ranking Engine: The script scans the lookback period to find the Top 10 Highest Closes and Top 10 Lowest Closes.

2. Volume Classification: For each ranked bar, it calculates the "Intrabar Buy/Sell Volume" (or approximates it using candle geometry if Intrabar data is unavailable).

3. Dominance Detection: It compares Buying Volume vs. Selling Volume to determine who is in control at critical price levels.

Signal Classifications (VSA Logic)

The indicator generates labels on the chart and updates the dashboard table based on the following logic:

1. At Price Tops (Resistance Areas):

- Distribution (Supply): High Price + High Total Volume + Sellers Dominant.

Interpretation: Indicates heavy institutional selling into rising prices. Often precedes a reversal.

- Buy Climax: High Price + High Total Volume + Buyers Dominant.

Interpretation: Extreme buying frenzy. While bullish, it often marks a "trap" or temporary top due to exhaustion.

- No Demand: High Price + Low Volume.

Interpretation: Prices drifted higher but lack institutional participation. A sign of weakness.

2. At Price Bottoms (Support Areas):

- Absorption: Low Price + High Total Volume + Buyers Dominant.

Interpretation: Institutional money is absorbing selling pressure (passive buying). A strong sign of accumulation.

- Panic Sell: Low Price + High Total Volume + Sellers Dominant.

Interpretation: Extreme fear. High volume at lows typically indicates capitulation and potential hands-changing.

- Exhaustion: Low Price + Low Volume.

Interpretation: Selling pressure has dried up. The market may float upward due to lack of sellers.

Key Features

- Dashboard Matrix Table:

Displays the exact Close Price, Buy/Sell Volume, and Market State (Group) for the Top 10 ranking bars.

Smart Footer: Automatically detects the active "Resistance Zone" (derived from G1 Distribution levels) and "Support Zone" (derived from G3 Absorption levels) and reports the current price status relative to these zones (e.g., "Testing Resistance", "Breakout", "At Support").

- Smart Zones (Auto S/R):

Automatically draws Support and Resistance boxes extending into the future based on the most significant volume clusters found in the rankings. Includes logic to detect "Flips" (e.g., when Support breaks, it is labeled as a flip to Resistance).

- Average Trend Channels:

Calculates a Linear Regression trend line based specifically on the coordinates of the Top 10 Highs and Top 10 Lows, providing a "Best Fit" channel for the current market structure.

- Visual Clarity:

Labels utilize a "Smart Stacking" algorithm to prevent overlap on the chart. Guide lines connect labels to their respective candles for precise identification.

Settings & Configuration

- Matrix Settings: Lookback Period (default 100 bars) and Top Rank Count.

- Volume Engine: Choose between "Intrabar (Precise)" for accurate order flow or "Geometry (Approx)" for standard volume estimation.

- Visuals: Toggle Table, Labels, Lines, Zones, and Trend Lines. Adjust transparency and font sizes.

IMPORTANT NOTE ON SNAPSHOT LOGIC

This indicator is designed as a Real-Time Dashboard. It continuously updates the "Top 10" list as new candles form. Therefore, a label that appears on a candle may disappear if that candle falls out of the Top 10 ranking or leaves the lookback window. This is intended behavior to ensure the chart always reflects the current most critical levels, rather than a historical record of past signals. It is best used for live market analysis rather than historical back testing.

Disclaimer: This tool is for educational and analytical purposes only. Volume analysis is subjective and should be used in conjunction with other methods of technical analysis.

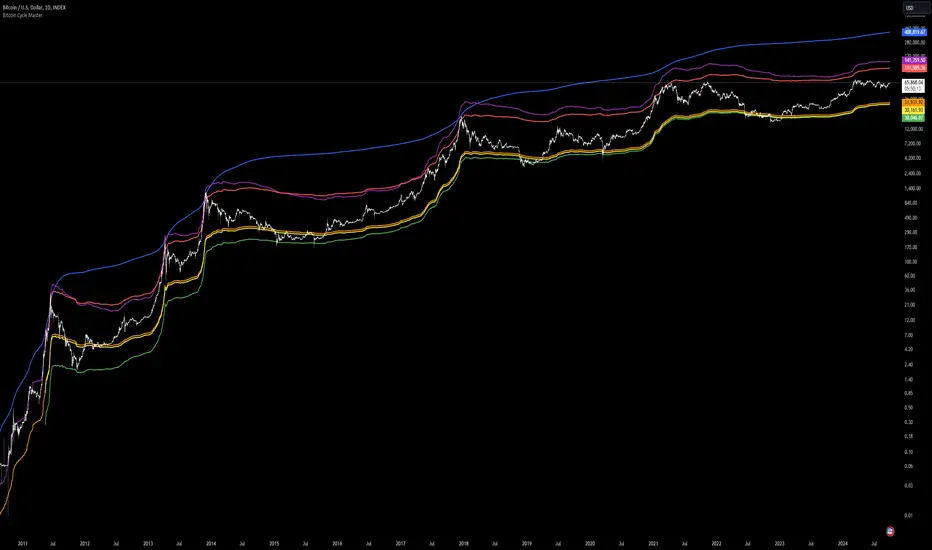

Puell Multiple Variants [OperationHeadLessChicken]Overview

This script contains three different, but related indicators to visualise Bitcoin miner revenue.

The classical Puell Multiple : historically, it has been good at signaling Bitcoin cycle tops and bottoms, but due to the diminishing rewards miners get after each halving, it is not clear how you determine overvalued and undervalued territories on it. Here is how the other two modified versions come into play:

Halving-Corrected Puell Multiple : The idea is to multiply the miner revenue after each halving with a correction factor, so overvalued levels are made comparable by a horizontal line across cycles. After experimentation, this correction factor turned out to be around 1.63. This brings cycle tops close to each other, but we lose the ability to see undervalued territories as a horizontal region. The third variant aims to fix this:

Miner Revenue Relative Strength Index (Miner Revenue RSI) : It uses RSI to map miner revenue into the 0-100 range, making it easy to visualise over/undervalued territories. With correct parameter settings, it eliminates the diminishing nature of the original Puell Multiple, and shows both over- and undervalued revenues correctly.

Example usage

The goal is to determine cycle tops and bottoms. I recommend using it on high timeframes, like monthly or weekly . Lower than that, you will see a lot of noise, but it could still be used. Here I use monthly as the example.

The classical Puell Multiple is included for reference. It is calculated as Miner Revenue divided by the 365-day Moving Average of the Miner Revenue . As you can see in the picture below, it has been good at signaling tops at 1,3,5,7.

The problems:

- I have to switch the Puell Multiple to a logarithmic scale

- Still, I cannot use a horizontal oversold territory

- 5 didn't touch the trendline, despite being a cycle top

- 9 touched the trendline despite not being a cycle top

Halving-Corrected Puell Multiple (yellow): Multiplies the Puell Multiple by 1.63 (a number determined via experimentation) after each halving. In the picture below, you can see how the Classical (white) and Corrected (yellow) Puell Multiples compare:

Advantages:

- Now you can set a constant overvalued level (12.49 in my case)

- 1,3,7 are signaled correctly as cycle tops

- 9 is correctly not signaled as a cycle top

Caveats:

- Now you don't have bottom signals anymore

- 5 is still not signaled as cycle top

Let's see if we can further improve this:

Miner Revenue RSI (blue):

On the monthly, you can see that an RSI period of 6, an overvalued threshold of 90, and an undervalued threshold of 35 have given historically pretty good signals.

Advantages:

- Uses two simple and clear horizontal levels for undervalued and overvalued levels

- Signaling 1,3,5,7 correctly as cycle tops

- Correctly does not signal 9 as a cycle top

- Signaling 4,6,8 correctly as cycle bottoms

Caveats:

- Misses two as a cycle bottom, although it was a long time ago when the Bitcoin market was much less mature

- In the past, gave some early overvalued signals

Usage

Using the example above, you can apply these indicators to any timeframe you like and tweak their parameters to obtain signals for overvalued/undervalued BTC prices

You can show or hide any of the three indicators individually

Set overvalued/undervalued thresholds for each => the background will highlight in green (undervalued) or red (overvalued)

Set special parameters for the given indicators: correction factor for the Corrected Puell and RSI period for Revenue RSI

Show or hide halving events on the indicator panel

All parameters and colours are adjustable

Sector Rotation & Money Flow Dashboard📊 Overview

The Sector Rotation & Money Flow Dashboard is a comprehensive market analysis tool that tracks 39 major sector ETFs in real-time, providing institutional-grade insights into sector rotation, momentum shifts, and money flow patterns. This indicator helps traders identify which sectors are attracting capital, which are losing favor, and where the next opportunities might emerge.

Perfect for swing traders, position traders, and investors who want to stay ahead of sector rotation and ride the strongest trends while avoiding weak sectors.

🎯 What This Indicator Does

Tracks 39 Major Sectors: From technology to utilities, cryptocurrencies to commodities

Calculates Multiple Timeframes: 1-week, 1-month, 3-month, and 6-month performance

Advanced Momentum Metrics: Proprietary momentum score and acceleration calculations

Relative Strength Analysis: Compare sector performance against any benchmark index

Money Flow Signals: Visual indicators showing where institutional money is moving

Smart Filtering: Pre-built strategy filters for different trading styles

Trend Detection: Emoji-based visual system for quick trend identification

💡 Key Features

1. Performance Metrics

Multiple timeframe analysis (1W, 1M, 3M, 6M)

Month-over-month change tracking

Relative strength vs benchmark index

2. Advanced Analytics

Momentum Score: Weighted composite of recent performance

Acceleration: Rate of change in momentum (second derivative)

Money Flow Signals: IN/OUT/TURN/WATCH indicators

3. Strategy Preset Filters

🎯 Swing Trade: High momentum opportunities

📈 Trend Follow: Established uptrends

🔄 Mean Reversion: Oversold bounce candidates

💎 Value Hunt: Deep value opportunities

🚀 Breakout: Emerging strength

⚠️ Risk Off: Sectors to avoid

4. Customization

All 39 sector ETFs can be customized

Adjustable benchmark index

Flexible display options

Multiple sorting methods

📋 Settings Documentation

Display Settings

Show Table (Default: On)

Toggles the entire dashboard display

Table Position (Default: Middle Center)

Choose from 9 positions on your chart

Options: Top/Middle/Bottom × Left/Center/Right

Rows to Show (Default: 15)

Number of sectors displayed (5-40)

Useful for focusing on top/bottom performers

Sort By (Default: Momentum)

1M/3M/6M: Sort by specific timeframe performance

Momentum: Weighted recent performance score

Acceleration: Rate of momentum change

1M Change: Month-over-month improvement

RS: Relative strength vs benchmark

Flow: IN First: Prioritize sectors with inflows

Flow: TURN First: Focus on reversal candidates

Recovery Plays: Oversold sectors recovering

Oversold Bounce: Deepest declines with positive signs

Top Gainers/Losers 3M: Best/worst quarterly performers

Best Acc + Mom: Combined strength score

Worst Acc (Topping): Sectors losing momentum

Filter Settings

Strategy Preset Filter (Default: All)

All: No filtering

🎯 Swing Trade: Mom >5, Acc >2, Money flowing in

📈 Trend Follow: Positive 1M & 3M, RS >0

🔄 Mean Reversion: Oversold but improving

💎 Value Hunt: Down >10% with recovery signs

🚀 Breakout: Rapid momentum surge

⚠️ Risk Off: Declining or topping sectors

Custom Flow Filter: Use manual flow filter

Custom Flow Signal Filter (Default: All)

Only active when Strategy Preset = "Custom Flow Filter"

IN Only: Strong inflows

TURN Only: Reversal signals

WATCH Only: Recovery candidates

OUT Only: Outflow sectors

Active Flows Only: Any non-neutral signal

Hide Low Volume ETFs (Default: Off)

Filters out illiquid sectors (future enhancement)

Visual Settings

Show Trend Emojis (Default: On)

🚀 Breakout (Strong 1M + High Acceleration)

🔥 Hot Recovery (From -10% to positive)

💪 Steady Uptrend (All timeframes positive)

➡️ Sideways/Ranging

⚠️ Warning/Topping (Up >15%, now slowing)

📉 Falling (Negative + declining)

🔄 Bottoming (Improving from lows)

Compact Mode (Default: Off)

Removes decimals for cleaner display

Useful when showing many rows

Min Data Points Required (Default: 3)

Minimum data points needed to display a sector

Prevents showing sectors with insufficient data

Relative Strength Settings

RS Benchmark Index (Default: AMEX:SPY)

Index to compare all sectors against

Can use SPY, QQQ, IWM, or any other index

RS Period (Days) (Default: 21)

Lookback period for RS calculation

21 days = 1 month, 63 days = 3 months, etc.

Sector ETF Settings (Groups 1-39)

Each sector has two inputs:

Symbol: The ticker (e.g., "AMEX:XLF")

Name: Display name (e.g., "Financials")

All 39 sectors can be customized to track different ETFs or markets.

📈 Column Explanations

Sector: ETF name/description

1M%: 1-month (21-day) performance

3M%: 3-month (63-day) performance

6M%: 6-month (126-day) performance

Mom: Momentum score (weighted average, recent-biased)

Acc: Acceleration (momentum rate of change)

Δ1M: Month-over-month change

RS: Relative strength vs benchmark

Flow: Money flow signal

↗️ IN: Strong inflows

🔄 TURN: Potential reversal

👀 WATCH: Recovery candidate

↘️ OUT: Outflows

—: Neutral

🎮 Usage Tips

For Swing Traders (3-14 days)

Use "🎯 Swing Trade" filter

Sort by "Acceleration" or "Momentum"

Look for Flow = "IN" and Mom >10

Confirm with positive RS

For Position Traders (2-8 weeks)

Use "📈 Trend Follow" filter

Sort by "RS" or "Best Acc + Mom"

Focus on consistent green across timeframes

Ensure RS >3 for market leaders

For Value Investors

Use "💎 Value Hunt" filter

Sort by "Recovery Plays" or "Top Losers 3M"

Look for improving Δ1M

Check for "WATCH" or "TURN" signals

For Risk Management

Regularly check "⚠️ Risk Off" filter

Sort by "Worst Acc (Topping)"

Review holdings for ⚠️ warning emojis

Exit sectors showing "OUT" flow

Market Regime Recognition

Bull Market: Many sectors showing "IN" flow, positive RS

Bear Market: Widespread "OUT" flows, negative RS

Rotation: Mixed flows, some "IN" while others "OUT"

Recovery: Multiple "TURN" and "WATCH" signals

🔧 Pro Tips

Combine Filters + Sorting: Filter first to narrow candidates, then sort to prioritize

Multi-Timeframe Confirmation: Best setups show alignment across 1M, 3M, and momentum

RS is Key: Sectors outperforming SPY (RS >0) tend to continue outperforming

Acceleration Matters: Positive acceleration often precedes price breakouts

Flow Transitions: "WATCH" → "TURN" → "IN" progression identifies new trends early

Regular Scans:

Daily: Check "Acceleration" sort

Weekly: Review "1M Change"

Monthly: Analyze "RS" shifts

Divergence Signals:

Price up but Acceleration down = Potential top

Price down but Acceleration up = Potential bottom

Sector Pairs Trading: Long sectors with "IN" flow, short sectors with "OUT" flow

⚠️ Important Notes

This indicator makes 40 security requests (maximum allowed)

Best used on Daily timeframe

Data updates in real-time during market hours

Some ETFs may show "—" if data is unavailable

🎯 Common Strategies

"Follow the Flow"

Only trade sectors showing "IN" flow with positive RS

"Rotation Catcher"

Focus on "TURN" signals in sectors down >15% from highs

"Momentum Rider"

Trade top 3 sectors by Momentum score, exit when Acceleration turns negative

"Mean Reversion"

Buy sectors in bottom 20% by 3M performance when Δ1M improves

"Relative Strength Leader"

Maintain positions only in sectors with RS >5

Not financial advice - always do additional research

Log Regression OscillatorThe Log Regression Oscillator transforms the logarithmic regression curves into an easy-to-interpret oscillator that displays potential cycle tops/bottoms.

🔶 USAGE

Calculating the logarithmic regression of long-term swings can help show future tops/bottoms. The relationship between previous swing points is calculated and projected further. The calculated levels are directly associated with swing points, which means every swing point will change the calculation. Importantly, all levels will be updated through all bars when a new swing is detected.

The "Log Regression Oscillator" transforms the calculated levels, where the top level is regarded as 100 and the bottom level as 0. The price values are displayed in between and calculated as a ratio between the top and bottom, resulting in a clear view of where the price is situated.

The main picture contains the Logarithmic Regression Alternative on the chart to compare with this published script.

Included are the levels 30 and 70. In the example of Bitcoin, previous cycles showed a similar pattern: the bullish parabolic was halfway when the oscillator passed the 30-level, and the top was very near when passing the 70-level.

🔹 Proactive

A "Proactive" option is included, which ensures immediate calculations of tentative unconfirmed swings.

Instead of waiting 300 bars for confirmation, the "Proactive" mode will display a gray-white dot (not confirmed swing) and add the unconfirmed Swing value to the calculation.

The above example shows that the "Calculated Values" of the potential future top and bottom are adjusted, including the provisional swing.

When the swing is confirmed, the calculations are again adjusted, showing a red dot (confirmed top swing) or a green dot (confirmed bottom swing).

🔹 Dashboard

When less than two swings are available (top/bottom), this will be shown in the dashboard.

The user can lower the "Threshold" value or switch to a lower timeframe.

🔹 Notes

Logarithmic regression is typically used to model situations where growth or decay accelerates rapidly at first and then slows over time, meaning some symbols/tickers will fit better than others.

Since the logarithmic regression depends on swing values, each new value will change the calculation. A well-fitted model could not fit anymore in the future.

Users have to check the validity of swings; for example, if the direction of swings is downwards, then the dataset is not fitted for logarithmic regression.

In the example above, the "Threshold" is lowered. However, the calculated levels are unreliable due to the swings, which do not fit the model well.

Here, the combination of downward bottom swings and price accelerates slower at first and faster recently, resulting in a non-fit for the logarithmic regression model.

Note the price value (white line) is bound to a limit of 150 (upwards) and -150 (down)

In short, logarithmic regression is best used when there are enough tops/bottoms, and all tops are around 100, and all bottoms around 0.

Also, note that this indicator has been developed for a daily (or higher) timeframe chart.

🔶 DETAILS

In mathematics, the dot product or scalar product is an algebraic operation that takes two equal-length sequences of numbers (arrays) and returns a single number, the sum of the products of the corresponding entries of the two sequences of numbers.

The usual way is to loop through both arrays and sum the products.

In this case, the two arrays are transformed into a matrix, wherein in one matrix, a single column is filled with the first array values, and in the second matrix, a single row is filled with the second array values.

After this, the function matrix.mult() returns a new matrix resulting from the product between the matrices m1 and m2.

Then, the matrix.eigenvalues() function transforms this matrix into an array, where the array.sum() function finally returns the sum of the array's elements, which is the dot product.

dot(x, y)=>

if x.size() > 1 and y.size() > 1

m1 = matrix.new()

m2 = matrix.new()

m1.add_col(m1.columns(), y)

m2.add_row(m2.rows (), x)

m1.mult (m2)

.eigenvalues()

.sum()

🔶 SETTINGS

Threshold: Period used for the swing detection, with higher values returning longer-term Swing Levels.

Proactive: Tentative Swings are included with this setting enabled.

Style: Color Settings

Dashboard: Toggle, "Location" and "Text Size"

VolumeSpreadAnalysisLibrary "VolumeSpreadAnalysis"

A library for Volume Spread Analysis (VSA).

spread(_barIndex)

Calculates the spread of a bar.

Parameters:

_barIndex (int) : (int) The index of the bar.

Returns: (float) The spread of the bar.

volume(_barIndex)

Retrieves the volume of a bar.

Parameters:

_barIndex (int) : (int) The index of the bar.

Returns: (float) The volume of the bar.

body(_barIndex)

Calculates the body of a bar.

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (float) The body size of the bar.

wickUpper(_barIndex)

Calculates the upper wick of a bar (upper shadow).

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (float) The upper wick size of the bar.

wickLower(_barIndex)

Calculates the lower wick of a bar (lower shadow).

Parameters:

_barIndex (simple int) : (int) The index of the bar.

Returns: (float) The lower wick size of the bar.

calcForecastedSMA(_source, _length, _forecastedLevel)

Calculates the forecasted Simple Moving Average (SMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the SMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted SMA value.

calcForecastedEMA(_source, _length, _forecastedLevel)

Calculates the forecasted Exponential Moving Average (EMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the EMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted EMA value.

calcForecastedRMA(_source, _length, _forecastedLevel)

Calculates the forecasted Relative Moving Average (RMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the RMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted RMA value.

calcForecastedWMA(_source, _length, _forecastedLevel)

Calculates the forecasted Weighted Moving Average (WMA).

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the WMA.

_forecastedLevel (float) : (float) The forecasted level to include in the calculation.

Returns: (float) The forecasted WMA value.

calcElapsedTimePercent()

Calculates the elapsed time percent of the current bar.

Returns: (float) The elapsed time percent.

calcForecastedSpread(multiplierAtMidpoints, multiplierAtPeaks)

Calculates the forecasted spread using elapsed time and dynamic multipliers, handling spread's non-linear nature.

Parameters:

multiplierAtMidpoints (float) : (float) The multiplier value at midpoints.

multiplierAtPeaks (float) : (float) The multiplier value at peaks.

Returns: (float) The forecasted spread value.

calcForecastedVolume()

Calculates the forecasted volume using elapsed time, satisfying volume's linear nature.

Returns: (float) The forecasted volume value.

calcForecastedMA(_source, _length, _forecastedSource, _type)

Calculates the forecasted Moving Average (MA) based on the specified type.

Parameters:

_source (float) : (series float) Source data for calculation.

_length (simple int) : (int) The length of the MA.

_forecastedSource (float) : (float) The forecasted level to include in the calculation.

_type (simple string) : (string) The type of the MA ("SMA", "EMA", "SMMA (RMA)", "WMA").

Returns: (float) The forecasted MA value.

calcMA(_source, _length, _type)

Calculates the Moving Average (MA) based on the specified type.