Market Delta [Makit0]MARKET DELTA INDICATOR v0.5 beta

Market Delta is suitable for daytrading on intraday timeframes, is a volume based indicator which allows to see the UP VOLUME vs the DOWN VOLUME, the DELTA (difference) and the CUMULATIVE DELTA (cumulative sum of difference) between them

This indicator is based on contracts volume (data avaiable), not in ask/bid volume (data not avaiable)

The up/down volume is calculated at each candle as follows:

- calculate the ticks of the range, top wick and bottom wick

- calculate the ticks up and ticks down to get the total ticks of the candle

- calculate the volume per tick as total volume divided by total ticks

- calculate the up and down volume as volume per tick multiplied by up ticks and down ticks

The delta is calculated as volume up minus volume down

The cumulative delta is a cumulative sum of delta and is resetted to 0 twice a day at the globex open and at the us cash open

By default the indicator plots the 'CANDLE MODE' which is useful for charting the cumulative volume to find out support and resistance zones where the volume is rejected or pass thru, as the volume moves so does the price, price always follows the volume, price goes away from where volume dries and price auctions comfortable where is plenty of volume, in a way PRICE FEEDS ON VOLUME

An indication about the plotting style in the volume, delta and cumulative delta modes: I can't use histogram as intended due a bug at autoresizing the scale in the candle mode, so the styles used are areabr and circles.

FEATURES

- Plot volume in one of four modes: Volume Up/Down, Delta, Cumulative Delta, Cumulative Delta as Candles

- Cumulative delta resetted twice a day (globex and cash open)

- Show a base line at 0

SETTINGS

- Mode: select one of the four volume output modes: Volume, Delta, Cumulative Delta and Candles. Candles by default

- Show zero line: show/hide the zero base line. False by default.

HOW TO SETTING UP THE INDICATOR:

BE AWARE, by default the indicator settings are configured for using the Cumulative Delta Candle Mode

- Candles Mode Settings: configured by default, mode candles and zero line off

- Volume, Delta, Cumulative Delta Mode Settings: select the mode you want and switch on/off the zero line

GOOD LUCK AND HAPPY TRADING

Search in scripts for "文华财经tick价格"

Trading Range Indicator - TRISimple script made to identify trading ranges in any timeframe

The oscillator bounces between 1 and 0. 1 means that the current asset is in a trading range and 0 meaning it is not.

The determination of a trading range is determined by the following:

ATR(14)40 and RSI<60

ADX<25

Due to all 3 having to be fulfilled in order for the oscillator to show there is a trading range, this causes a problem where 2 of the conditions are fulfilled and therefore still shows 0 on the oscillator, however, the asset could very well be in a trading range.

So what in the world do you use this for if there is such a significant margin of error?

Since all 3 conditions need to be fulfilled in order for it to be considered a trading range, this gives a very strong indicator of said trading ranges. So if a person is looking at individual stock tickers or the SPY index ticker, then when the oscillator reads a 1, it could be ideal to open an Iron Condor on said ticker. This means that this indicator is not well suiting for traditional long and short stock positions, but rather it is made for options traders who by using an Iron Condor can make money of a range-bound market.

Acc/Dist. Cloud with Fractal Deviation Bands by @XeL_ArjonaACCUMULATION / DISTRIBUTION CLOUD with MORPHIC DEVIATION BANDS

Ver. 2.0.beta.23:08:2015

by Ricardo M. Arjona @XeL_Arjona

DISCLAIMER

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The embedded code and ideas within this work are FREELY AND PUBLICLY available on the Web for NON LUCRATIVE ACTIVITIES and must remain as is.

Pine Script code MOD's and adaptations by @XeL_Arjona with special mention in regard of:

Buy (Bull) and Sell (Bear) "Power Balance Algorithm by Vadim Gimelfarb published at Stocks & Commodities V. 21:10 (68-72).

Custom Weighting Coefficient for Exponential Moving Average (nEMA) adaptation work by @XeL_Arjona with contribution help from @RicardoSantos at TradingView @pinescript chat room.

Morphic Numbers (PHI & Plastic) Pine Script adaptation from it's algebraic generation formulas by @XeL_Arjona

Fractal Deviation Bands idea by @XeL_Arjona

CHANGE LOG:

ACCUMULATION / DISTRIBUTION CLOUD: I decided to change it's name from the Buy to Sell Pressure. The code is essentially the same as older versions and they are the center core (VORTEX?) of all derived New stuff which are:

MORPHIC NUMBERS: The "Golden Ratio" expressed by the result of the constant "PHI" and the newer and same in characteristics "Plastic Number" expressed as "PN". For more information about this regard take a look at: HERE!

CUSTOM(K) EXPONENTIAL MOVING AVERAGE: Some code has cleaned from last version to include as custom function the nEMA , which use an additional input (K) to customise the way the "exponentially" is weighted from the custom array. For the purpose of this indicator, I implement a volatility algorithm using the Average True Range of last 9 periods multiplied by the morphic number used in the fractal study. (Golden Ratio as default) The result is very similar in response to classic EMA but tend to accelerate or decelerate much more responsive with wider bars presented in trending average.

FRACTAL DEVIATION BANDS: The main idea is based on the so useful Standard Deviation process to create Bands in favor of a multiplier (As John Bollinger used in it's own bands) from a custom array, in which for this case is the "Volume Pressure Moving Average" as the main Vortex for the "Fractallitly", so then apply as many "Child bands" using the older one as the new calculation array using the same morphic constant as multiplier (Like Fibonacci but with other approach rather than %ratios). Results are AWSOME! Market tend to accelerate or decelerate their Trend in favor of a Fractal approach. This bands try to catch them, so please experiment and feedback me your own observations.

EXTERNAL TICKER FOR VOLUME DATA: I Added a way to input volume data for this kind of study from external tickers. This is just a quicky-hack given that currently TradingView is not adding Volume to their Indexes so; maybe this is temporary by now. It seems that this part of the code is conflicting with intraday timeframes, so You are advised.

This CODE is versioned as BETA FOR TESTING PROPOSES. By now TradingView Admins are changing lot's of things internally, so maybe this could conflict with correct rendering of this study with special tickers or timeframes. I will try to code by itself just the core parts of this study in order to use them at discretion in other areas. ALL NEW IDEAS OR MODIFICATIONS to these indicator(s) are Welcome in favor to deploy a better and more accurate readings. I will be very glad to be notified at Twitter or TradingView accounts at: @XeL_Arjona

Short Squeeze Screener _ SYLGUYO//@version=5

indicator("Short Squeeze Screener — Lookup Table", overlay=false)

// ===========================

// TABLEAU INTERNE DES DONNÉES

// ===========================

// Exemple : remplace par tes données réelles

var string tickers = array.from("MARA", "BBBYQ", "GME")

var float short_float_data = array.from(28.5, 47.0, 22.3)

var float dtc_data = array.from(2.3, 15.2, 5.4)

var float oi_growth_data = array.from(12.0, 22.0, 4.0)

var float pcr_data = array.from(0.75, 0.45, 1.1)

// ===========================

// CHARGEMENT DU TICKER COURANT

// ===========================

string t = syminfo.ticker

var float short_f = na

var float dtc = na

var float oi = na

var float pcr = na

// Trouve le ticker dans la base

for i = 0 to array.size(tickers) - 1

if array.get(tickers, i) == t

short_f := array.get(short_float_data, i)

dtc := array.get(dtc_data, i)

oi := array.get(oi_growth_data, i)

pcr := array.get(pcr_data, i)

// ===========================

// SCORE SHORT SQUEEZE

// ===========================

score = 0

score += (short_f >= 30) ? 1 : 0

score += (dtc >= 7) ? 1 : 0

score += (oi >= 10) ? 1 : 0

score += (pcr <= 1) ? 1 : 0

plot(score, "Short Squeeze Score", linewidth=2)

Market Trend & Breadth Checklist [Kulturdesken]Description

Concept & Inspiration This indicator serves as a disciplined "Pre-Flight Checklist" for swing traders, combining two powerful methodologies into one objective dashboard.

The Foundation (@kulturdesken): The core checklist structure is inspired by the workflow of @kulturdesken, utilizing the QQQE (Nasdaq 100 Equal Weighted Index). By focusing on the equal-weighted index rather than the market-cap weighted QQQ, we avoid distortions caused by mega-cap stocks and gauge the true price trend of the average stock.

The Enhancement (StockBee): To further filter out "hollow rallies," we integrated Pradeep Bonde’s (StockBee) "Market Monitor" logic. This adds a layer of analysis based on the Total US Universe (Wilshire 5000) to ensure market breadth is expanding, not just price.

Why StockBee Logic Was Added While QQQE tells us if the average price is trending, the StockBee logic tells us if the market structure is healthy. We added the "Universe" checks (Total US Market Breadth) because price trends can sometimes be deceptive during low-volume corrections.

By incorporating the Market Monitor concept (specifically checking if the % of stocks above their 50-day Moving Average is rising), this tool acts as a "Traffic Light." It prevents the trader from entering aggressive long positions even if QQQE is green, provided the underlying participation (Market Breadth) is weak.

How It Works (The 7 Checks)

1. Price Momentum (Kulturdesken): QQQE > Rising 5 SMA

Verifies short-term momentum is aggressive (Price > 5SMA) and the 5SMA itself is curling up.

2. Daily Trend Structure: Daily Buy Signal

Verifies a "stacked" bullish alignment where Price > 10 SMA > 20 SMA.

3. Macro Trend: Weekly Buy Signal

Verifies the Weekly Price > 10 WMA > 20 WMA (Weighted Moving Averages).

4. Universe Breadth (StockBee/McClellan): Summation Uptrend

We aggregate Nasdaq + NYSE data to create a "Total Universe" McClellan Summation Index.

Check: Is the Summation Index rising? (Indicates long-term money flow entering the system).

5. Short-Term Thrust: Oscillator Positive

Uses the "Total Universe" McClellan Oscillator.

Check: Is the Oscillator > 0? (Indicates immediate buying pressure is dominant).

6. Leadership: Net Highs/Lows

Check: Are Net New Highs (Highs minus Lows) trending positive?

7. Performance Filter (Manual): Traction Check

A psychological guardrail. If you toggle this off in settings (indicating you are losing money/getting stopped out), the checklist forces a "WAIT" signal, protecting you from overtrading during choppy conditions.

Settings & Customization

Data Feeds: The script is pre-configured with USI (United States Indices) and INDEX tickers to ensure accurate breadth data, but these can be customized in the settings.

Main Ticker: Defaults to QQQE.

Disclaimer: This tool is for educational purposes and market analysis only. It does not constitute financial advice. Past performance is not indicative of future results.

Morning ORB FVG Trigger✅ Overview

Morning ORB FVG Trigger is a complete intraday trading framework built around:

A Morning Opening Range Breakout (ORB)

The first Fair Value Gap (FVG) after that breakout

Strict risk management and position sizing

Optional HTF trend filter (Daily / Weekly / Monthly)

Optional Daily ATR filter to avoid extreme days

The script is designed for futures / indices / FX on intraday charts up to 15 minutes and for traders who want a clean, mechanical entry framework with clear risk.

🧠 Core idea

Define a morning opening range (e.g. 09:30–09:45).

Wait for a clean breakout above/below that range.

After the breakout, wait for the first FVG in breakout direction,

confirmed by the next candle (no immediate full reclaim).

Use a chosen stop logic + R:R factor to build risk/reward boxes.

Calculate position size based on your account risk.

(Optional) Only take trades:

In the direction of the HTF EMA trend (D/W/M).

On days where the morning range is within a band of the Daily ATR.

You can also disable all signals/boxes and use the script just as a visual ORB tool.

⏰ 1. ORB / Morning Range

Inputs (Main section)

Morning Range Session

Time window of the opening range in exchange time

Example: 09:30–09:45 for a 15-minute ORB.

You can type custom ranges (e.g. 09:30–09:35 for a 5-minute ORB).

Risk/Reward (TP factor)

Multiplier for the take-profit distance relative to the stop.

2.0 = TP is 2× the stop distance

1.5 = TP is 1.5× the stop distance

Show ORB range

If enabled, draws:

ORB high/low lines

ORB labels (e.g. 15min ORB high / low)

Optional midline

Extend ORB lines to the right (bars)

How many bars to extend the ORB high/low horizontally beyond the ORB itself.

Trade box width (bars)

Horizontal width (in bars) of:

Red risk box (entry–stop)

Green reward box (entry–TP)

Implementation details

The ORB is always calculated on 1-minute data internally, so it stays precise even on 5m/15m charts.

The script only works on intraday timeframes up to 15 minutes.

📦 2. FVG Block

Group: “FVG”

Threshold %

Minimum size of an FVG in % of price.

0 = every FVG

Higher values = only larger gaps

Auto threshold (from volatility)

If enabled, the minimum FVG size is derived from historical volatility

instead of a fixed percentage.

Allow breakout FVG partly inside ORB

Off (default): the FVG must lie fully outside the ORB.

On: the breakout FVG itself may still overlap the ORB a bit,

as long as it is the first one attached to the breakout move.

Enable FVG entry signals, boxes & alerts

On: full system – FVG detection, entry labels, risk/TP boxes, alerts.

Off: no entries, no risk/TP boxes, no alerts.

You only get the ORB and (optionally) the HTF dashboard, so you can trade your own setups.

Entry mode

Entry mode (Mid / Edge / NextOpen)

Mid – Entry at the midpoint of the FVG.

Edge – Long at the upper FVG edge, short at the lower FVG edge.

NextOpen – No limit order in the gap. Entry is placed at the next bar open after FVG confirmation.

Edge offset (ticks)

Additional offset for Edge entries:

Long:

+ticks = a bit above the FVG (more conservative)

-ticks = deeper into the FVG (more aggressive)

Short:

+ticks = a bit below the FVG

-ticks = deeper into the FVG

FVG detection logic

Uses a LuxAlgo-style 3-candle FVG pattern (gap between candle 1 and 3).

Only one FVG is taken: the first valid FVG after the ORB breakout in breakup direction.

The FVG candle is the middle bar; the script:

Detects the FVG on the previous bar.

Waits for the current bar to confirm it:

Bullish: current low must stay above the lower FVG boundary

Bearish: current high must stay below the upper FVG boundary

Only then an entry signal is generated.

🛑 3. Stop Logic

Group: “Stop Logic”

Stop mode (PrevBar / Pivot / FVG Candle)

PrevBar – Stop at the low/high of the candle before the FVG

(tight/aggressive).

FVG Candle – Stop at the low/high of the FVG candle itself

(medium).

Pivot – Stop at the most recent swing high/low

using pivotLeft / pivotRight pivots (more conservative).

Ticks (stop buffer)

Offset (in ticks) from the selected stop level.

> 0 = further away (more room, more risk)

< 0 = closer (tighter stop)

Pivot left / Pivot right

Number of candles left/right to define a swing high/low

when using Pivot stop mode.

Typical intraday values: 2–3.

The script also sanity-checks the stop:

if the calculated stop would be invalid (e.g. above entry in a long), it moves it by a minimal distance (2 ticks) to keep a valid risk.

📈 4. HTF Trend Filter (Daily / Weekly / Monthly)

Group: “HTF Trend Filter”

Enable HTF trend filter

If enabled, trades are only allowed:

Long when at least 2 of D/W/M closes are above their EMA

Short when at least 2 of D/W/M closes are below their EMA

EMA length (D/W/M)

EMA length for all three higher timeframes (Daily, Weekly, Monthly).

This helps focus entries in the direction of the dominant higher-timeframe trend.

📊 5. ATR Filter (Daily)

Group: “ATR Filter (Daily)”

Use daily ATR filter

If enabled, the height of the ORB (ORB high – ORB low) must be within

a band of the Daily ATR to allow any signals.

Daily ATR length

ATR period on the Daily timeframe.

Min ORB size vs ATR

Lower bound:

Example: 0.3 → ORB must be at least 0.3 × Daily ATR

0.0 = no minimum.

Max ORB size vs ATR

Upper bound:

Example: 1.5 → ORB must be ≤ 1.5 × Daily ATR

0.0 = no maximum.

If the ORB is too small (choppy) or too large (exhausted move), no breakout or FVG signal will be generated on that day.

🧭 6. HTF Dashboard & Signal Labels

Group: “HTF Trend Dashboard”

Show HTF dashboard

Draws a small label at the top of the chart showing:

HTF Trend (EMA X)

D: UP/FLAT/DOWN

W: UP/FLAT/DOWN

M: UP/FLAT/DOWN

Dashboard position

Top Right, Top Center, Top Left – places the dashboard at the top.

Over Risk Info – no top dashboard; instead, the HTF trend info is shown as a label near the risk box when a new signal appears.

Lookback (bars) for top anchor

How many bars to use to determine the top price level for dashboard placement.

Show HTF trend above risk box on signal

Only relevant if Dashboard position = Over Risk Info.

When enabled, a small HTF label appears near the risk box for each new trade.

Signal label vertical offset (ticks)

Vertical spacing between risk info label and HTF label.

Minimum spacing HTF/Risk (ticks)

Ensures a minimum vertical distance so the two labels don’t overlap.

HTF signal label X offset (bars)

Horizontal offset (left/right) relative to the risk info label.

⏳ 7. ORB–FVG Filters (Session & Time Window)

Group: “ORB FVG Filter”

Only same session day

If enabled, FVG entries are only allowed on the same calendar day

as the ORB. When the date changes, all state & drawings are reset.

Limit hours after ORB

Enables a time window after the ORB end.

Trading window after ORB (hours)

Length of that window in hours.

Example: 2.0 → FVG signals only in the first 2 hours after ORB end.

💰 8. Risk Management & Position Sizing

Group: “Risk Management”

Calculate position size

If enabled, the script computes suggested mini and micro contract size for you.

Account size

Your trading account size (in account currency).

Risk mode

Percent – risk is a % of account size (Account risk %).

Fixed amount – risk is a fixed dollar amount (Fixed risk ($)).

Account risk %

Risk per trade as a percentage of account size (e.g. 1.0 for 1%).

Fixed risk ($)

Fixed risk per trade in dollars when using Fixed amount mode.

Micro factor (vs mini)

How much a micro contract is worth relative to a mini.

Example:

0.1 → one micro moves 1/10 of one mini.

Risk Info label

For each new trade, a label is shown above the boxes with:

Stop distance in price and $ risk per mini

Max risk allowed for the trade

Suggested mini and micro size

Text like:

Suggested: 2 mini

Suggested: 5 micro

or Suggested: no trade

This makes the script especially useful for prop-firm rules or strict risk discipline.

🎨 9. Visual Style (Boxes, Labels, ORB Lines)

Group: “Box & Label Style (Trade)”

Label font size (Very small, Small, Normal, Large)

Entry label BG / text color

Stop label BG / text color

TP label BG / text color

Risk info BG / text color

Risk box color (entry–stop zone)

Reward box color (entry–TP zone)

Group: “ORB Style”

ORB high line color

ORB low line color

ORB line width

ORB label font size

ORB label background color

ORB label text color

Show ORB midline

ORB midline color / width / style (Solid / Dashed / Dotted)

⚠️ 10. Alerts

Group: “Alerts”

The script defines three alert conditions:

Long entry FVG breakout

Triggered when a new long signal appears.

Short entry FVG breakout

Triggered when a new short signal appears.

FVG entry (long/short)

Generic alert for any new signal (long or short).

To use them:

Add the indicator to the chart.

Open the Alerts dialog → “Condition”.

Select this script and one of the alert conditions.

Set your preferred expiration and notification settings.

Alerts only fire when Enable FVG entry signals, boxes & alerts is on.

🧩 11. How the trading logic flows (summary)

Build ORB on 1-minute data during the selected session.

Optionally reject the day if ORB is outside the ATR bounds.

Wait for a breakout (close above high or below low), respecting HTF trend filter.

After breakout, look for the first valid FVG in that direction:

Outside the ORB (unless breakout FVG allowed inside)

Confirmed by the next candle (no full reclaim)

Once confirmed:

Compute entry, stop, target.

Draw risk/reward boxes and all labels.

Optionally show HTF signal label over the risk info.

Trigger alerts if enabled.

If you disable FVG signals, only steps 1–3 (plus dashboard) are effectively active.

⚠️ 12. Notes & Disclaimer

Script is intended for intraday trading up to 15-minute timeframes.

All signals are mechanical and do not guarantee profitability.

Always backtest and forward-test on your own data before risking real money.

This script is for educational purposes only and is not financial advice.

🚀 Quick-start guide

Add the script to your chart

Use an intraday timeframe ≤ 15 minutes (1m, 3m, 5m, 15m).

Works best on liquid indices, futures, FX and large-cap stocks.

Set the Morning Range

In “Morning Range Session” choose the exchange’s opening window.

Examples

US index futures (CME): 08:30–08:45 or 08:30–08:35

US stocks (NYSE/Nasdaq): 09:30–09:45 or 09:30–09:35

The ORB is always calculated on 1-minute data internally, so the range stays accurate on higher intraday charts.

Keep the default filters at first

HTF Trend Filter: ON

EMA length = 20

This will only allow trades in the direction of the dominant D/W/M trend.

ATR Filter: OFF (optional; you can enable later once you’re comfortable).

Use the full trade system

In the FVG group leave

“Enable FVG entry signals, boxes & alerts” = ON

Entry mode: Mid

Stop mode: FVG Candle or PrevBar

Risk/Reward: 2.0 as a starting point.

Set your risk

Turn on “Calculate position size”.

Enter your Account size and choose either:

Risk mode = Percent (e.g. 1.0 = 1% per trade), or

Risk mode = Fixed amount (e.g. $250 per trade).

The risk info label will show:

Stop distance in price and $/contract

Max allowed risk

Suggested mini and micro contract size.

Enable alerts (optional)

Open the Alerts dialog → Condition: this script.

Choose one of:

Long entry FVG breakout

Short entry FVG breakout

FVG entry (long/short)

Choose “Once per bar” or “Once per bar close”, and your preferred notification type.

Replay & journal

Use the TradingView bar replay tool to step through past days.

Focus on:

How the ORB defines the structure.

How the first confirmed FVG outside the ORB behaves.

Whether the risk/TP levels fit your own style and product.

🎛 Recommended settings & profiles

These are starting points, not rules. Always adapt to the instrument and your own risk tolerance.

1. Conservative / Trend-following

Timeframe: 5m or 15m

Morning Range Session: 15-minute ORB around the cash or futures open

FVG

Threshold %: 0.05–0.1 (filter out very small gaps)

Auto threshold: OFF (keep it simple)

Allow breakout FVG partly inside ORB: OFF

Enable FVG entry signals/boxes/alerts: ON

Entry mode: Mid

Stop Logic

Stop mode: Pivot

Pivot left/right: 2–3

Stop buffer: +1–2 ticks

HTF Trend Filter

Enabled: ON

EMA length: 20

ATR Filter

Enabled: ON

Daily ATR length: 14

Min ORB vs ATR: 0.3–0.4

Max ORB vs ATR: 1.2–1.5

Risk Management

Risk mode: Percent

Account risk: 0.5–1.0%

Idea: Only trade when the higher-timeframe trend supports the move and the opening range is of a “normal” size for the current volatility.

2. Balanced / Intraday directional

Timeframe: 3m or 5m

FVG

Threshold %: 0.02–0.05

Auto threshold: ON (lets the script adapt to volatility)

Allow breakout FVG partly inside ORB: ON

(first breakout FVG may partly sit inside the ORB)

Entry mode: Edge

Edge offset (ticks): 0 or +1

Stop Logic

Stop mode: FVG Candle

Stop buffer: 0–1 ticks

HTF Trend Filter

Enabled: ON

ATR Filter

Enabled: OFF (optional)

Risk Management

Risk mode: Percent

Account risk: 1.0–1.5% (if this fits your plan)

Idea: Slightly more aggressive entries at the gap edge, still aligned with HTF trend, but with more flexibility on ATR.

3. Aggressive / Scalping around the ORB

Timeframe: 1m or 3m

FVG

Threshold %: 0.0–0.02

Auto threshold: ON

Allow breakout FVG partly inside ORB: ON

Entry mode: NextOpen or Edge with a negative offset (deeper into the gap)

Stop Logic

Stop mode: PrevBar

Stop buffer: 0 or -1 tick

HTF Trend Filter

Enabled: OFF (or ON but treat as soft guidance)

ATR Filter

Enabled: OFF

Risk Management

Risk mode: Percent

Account risk: lower, e.g. 0.25–0.5% per trade

Idea: More trades and tighter stops. Best for experienced traders who understand the limitations of scalping and whipsaw risk.

Final reminder

All of these are templates, not guarantees:

Always check how the system behaves on your market and session.

Start on replay and demo before trading real money.

Adjust filters (HTF, ATR, thresholds) until the signals fit your personal approach.

ATR Risk Display - Multi FuturesWhat This Does

I got tired of manually calculating my ATR stops and risk for different futures contracts, especially when switching between ES, NQ, and their micro versions. This indicator automatically detects what futures symbol you're trading and shows you the exact tick count and dollar risk for your stop loss.

The Problem It Solves

If you trade futures with ATR-based stops, you know the hassle:

Different contracts have different tick values

You need to calculate position risk in dollars

Switching between symbols means redoing all the math

Renko charts make it even more confusing since ATR needs to come from regular candles

This handles all of that automatically.

Key Features

Auto-detects futures symbols - ES, NQ, YM, RTY, GC, CL, and all the micros (MES, MNQ, etc.)

Shows everything you need in one line: ATR(timeframe) × multiplier = X ticks ($XXX)

Works on Renko charts - pulls ATR from regular timeframe charts (super important if you use Renko)

Adjustable position sizing - set your contract count and see total risk instantly

Clean, minimal display - just the info you need, no clutter

How to Use

Add it to any futures chart

Set your preferred ATR timeframe (I use 5-minute)

Set your ATR multiplier (I use 1.5x for my stops)

Set your contract size

That's it - the indicator handles the rest

The display will show something like: "ES ATR(5) × 1.5 = 12 ticks ($150)"

Settings Explained

ATR Timeframe: What timeframe to calculate ATR from (always uses regular candles, even on Renko)

ATR Multiplier: How many ATRs for your stop (1.5 is common, 2.0 for wider stops)

Number of Contracts: Your position size for risk calculation

Auto-Detect Symbol: Leave on unless you want to manually override

Supported Futures

Full size: ES, NQ, YM, RTY, GC, CL, ZB, ZN, 6E, 6J

Micros: MES, MNQ, MYM, M2K, MGC, MCL

Notes

Made this primarily for my own ES trading but figured others might find it useful

The tick values are based on standard CME specs

If you trade other futures, you can modify the code to add them

Works great alongside level indicators for risk management

Why This Exists

I use ATR trailing stops on all my trades and got tired of doing mental math every time I switched between charts or contracts. Especially useful if you trade both full-size and micro contracts - the risk difference is huge and easy to mess up.

Hope this helps your trading! Feel free to suggest improvements.

Michael's FVG Detector═══════════════════════════════════════

Michael's FVG Detector

═══════════════════════════════════════

A clean and efficient Fair Value Gap (FVG) indicator for TradingView that helps traders identify market imbalances with precision.

───────────────────────────────────────

Overview

───────────────────────────────────────

Fair Value Gaps (FVGs) are price inefficiencies that occur when there's a gap between the wicks of candlesticks, indicating rapid price movement with minimal trading activity. These gaps often act as support/resistance zones where price may return to "fill the gap."

This indicator automatically detects and visualizes both bullish and bearish FVGs on any timeframe, making it easy to spot potential trading opportunities.

───────────────────────────────────────

Features

───────────────────────────────────────

Core Functionality

Automatic FVG Detection : Identifies Fair Value Gaps in real-time as they form

Bullish & Bearish FVGs : Detects both upward and downward price gaps

3-Candle Pattern : Uses classic FVG logic (current candle low > high from 2 bars ago for bullish, vice versa for bearish)

Gap Size Display : Shows the exact size of each FVG in ticks directly on the box

Confirmed Bars Only : Only draws FVGs on confirmed bars to prevent repainting

Customization

Color Settings : Fully customizable colors for bullish and bearish FVGs with transparency control

Text Color : Configurable color for the tick size labels

Default Styling : Comes with sensible defaults (20% transparency, dark gray labels)

Performance Optimization

Smart Cleanup : Automatically removes boxes outside the visible chart area

Efficient Rendering : Maintains optimal performance even on lower timeframes

No Repainting : Uses confirmed bars only for reliable signals

───────────────────────────────────────

How It Works

───────────────────────────────────────

Detection Logic

Bullish FVG:

Current bar's low is higher than the high from 2 bars ago

Creates an upward gap that price left behind during bullish momentum

Bearish FVG:

Current bar's high is lower than the low from 2 bars ago

Creates a downward gap that price left behind during bearish momentum

Visual Display

Each detected FVG is displayed as:

A semi-transparent colored box spanning the gap area

The box extends from bar -2 to the current bar

Gap size in ticks shown at the bottom-left of each box

Singular/plural formatting ("1 tick" vs "X ticks")

───────────────────────────────────────

Performance Notes

───────────────────────────────────────

Cleanup runs every 50 bars to maintain optimal performance

Only creates boxes on confirmed bars (no real-time repainting)

Efficiently manages memory by removing off-screen boxes

Suitable for both manual and automated trading strategies

───────────────────────────────────────

Disclaimer

───────────────────────────────────────

This indicator is for educational and informational purposes only. It is not financial advice. Always do your own research and risk management before making trading decisions.

───────────────────────────────────────

Author : Michael

Version : 1.0

License : Free for personal use

Last Updated : November 2025

Info de Vela 1m1-Minute Candle Info Dashboard (Real-Time)

Overview

This is a lightweight, real-time dashboard designed specifically for 1-minute (1m) scalping. It provides critical, non-lagging data about the current 1-minute candle, helping you make split-second decisions on stop-loss placement and risk assessment.The table updates on every tick without flickering or repainting.

Key Features (Real-Time Table)

The dashboard displays three key metrics about the current 1m candle:Time Remaining: A simple countdown timer showing the exact seconds remaining until the current candle closes (e.g., "00:34").Dist. to Extreme (Ticks): This is the core function for scalping. It calculates the distance (in ticks) from the current price to the furthest extreme of the candle (i.e., max(high - close, close - low)). This is ideal for traders who base their stop-loss on the current candle's range.Total Candle Range (Ticks): Displays the full high-to-low range of the current candle in ticks, giving you an instant read on volatility.

How to Use

This tool is designed to solve one problem: speed.Instead of manually measuring the distance for your stop-loss on every candle, you can instantly read the exact tick value from the table. This allows you to calculate your position size (lotage) much faster, which is essential in a fast-moving 1m environment.

REQUIREMENT:This indicator is designed to work ONLY on the 1-minute (1m) timeframe. It will display an error and show no data on any other chart.

Enhanced MA Crossover Pro📝 Strategy Summary: Enhanced MA Crossover Pro

This strategy is an advanced, highly configurable moving average (MA) crossover system designed for algorithmic trading. It uses the crossover of two customizable MAs (a "Fast" MA 1 and a "Slow" MA 2) as its core entry signal, but aggressively integrates multiple technical filters, time controls, and dynamic position management to create a robust and comprehensive trading system.

💡 Core Logic

Entry Signal: A bullish crossover (MA1 > MA2) generates a Long signal, and a bearish crossover (MA1 < MA2) generates a Short signal. Users can opt to use MA crossovers from a Higher Timeframe (HTF) for the entry signal.

Confirmation/Filters: The basic MA cross signal is filtered by several optional indicators (see Filters section below) to ensure trades align with a broader trend or momentum context.

Position Management: Trades are managed with a sophisticated system of Stop Loss, Take Profit, Trailing Stops, and Breakeven stops that can be fixed, ATR-based, or dynamically adjusted.

Risk Management: Daily limits are enforced for maximum profit/loss and maximum trades per day.

⚙️ Key Features and Customization

1. Moving Averages

Primary MAs (MA1 & MA2): Highly configurable lengths (default 8 & 20) and types: EMA, WMA, SMA, or SMMA/RMA.

Higher Timeframe (HTF) MAs: Optional MAs calculated on a user-defined resolution (e.g., "60" for 1-hour) for use as an entry signal or as a trend confirmation filter.

2. Multi-Filter System

The entry signal can be filtered by the following optional conditions:

SMA Filter: Price must be above a 200-period SMA for long trades, and below it for short trades.

VWAP Filter: Price must be above VWAP for long trades, and below it for short trades.

RSI Filter: Long trades are blocked if RSI is overbought (default 70); short trades are blocked if RSI is oversold (default 30).

MACD Filter: Requires the MACD Line to be above the Signal Line for long trades (and vice versa for short trades).

HTF Confirmation: Requires the HTF MA1 to be above HTF MA2 for long entries (and vice versa).

3. Dynamic Stop and Target Management (S/L & T/P)

The strategy provides extensive control over exits:

Stop Loss Methods:

Fixed: Fixed tick amount.

ATR: Based on a multiple of the Average True Range (ATR).

Capped ATR: ATR stop limited by a maximum fixed tick amount.

Exit on Close Cross MA: Position is closed if the price crosses back over the chosen MA (MA1 or MA2).

Breakeven Stop: A stop can be moved to the entry price once a trigger distance (fixed ticks or Adaptive Breakeven based on ATR%) is reached.

Trailing Stop: Can be fixed or ATR-based, with an optional feature to auto-tighten the trailing multiplier after the breakeven condition is met.

Profit Target: Can be a fixed tick amount or a dynamic target based on an ATR multiplier.

4. Time and Session Control

Trading Session: Trades are only taken between defined Start/End Hours and Minutes (e.g., 9:30 to 16:00).

Forced Close: All open positions are closed near the end of the session (e.g., 15:45).

Trading Days: Allows specific days of the week to be enabled or disabled for trading.

5. Risk and Position Limits

Daily Profit/Loss Limits: The strategy tracks daily realized and unrealized PnL in ticks and will close all positions and block new entries if the user-defined maximum profit or maximum loss is hit.

Max Trades Per Day: Limits the number of executed trades in a single day.

🎨 Outputs and Alerts

Plots: Plots the MA1, MA2, SMA, VWAP, and HTF MAs (if enabled) on the chart.

Shapes: Plots visual markers (BUY/SELL labels) on the bar where the MA crossover occurs.

Trailing Stop: Plots the dynamic trailing stop level when a position is open.

Alerts: Generates JSON-formatted alerts for entry ({"action":"buy", "price":...}) and exit ({"action":"exit", "position":"long", "price":...}).

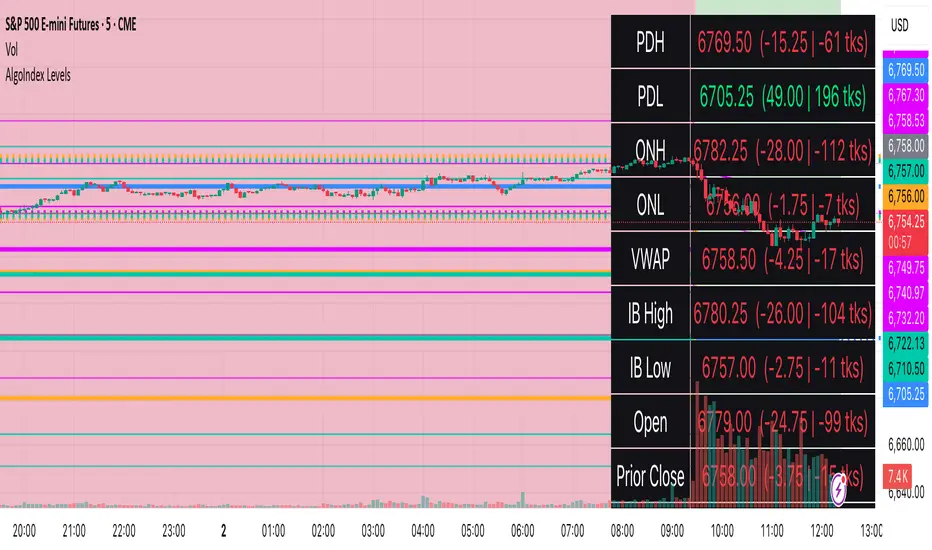

RTH Levels: VWAP + PDH/PDL + ONH/ONL + IBAlgo Index — Levels Pro (ONH/ONL • PDH/PDL • VWAP±Bands • IB • Gaps)

Purpose. A session-aware, non-repainting levels tool for intraday decision-making. Designed for futures and indices, with clean visuals, alerts, and a one-click Minimal Mode for screenshot-ready charts.

What it plots

• PDH/PDL (RTH-only) – Prior Regular Trading Hours high/low, computed intraday and frozen at the RTH close (no 24h mix-ups, no repainting).

• ONH/ONL – Prior Overnight high/low, held throughout RTH.

• RTH VWAP with ±σ bands – Volume-weighted variance, reset each RTH.

• Initial Balance (IB) – First N minutes of RTH, plus 1.5× / 2.0× extensions after IB completes.

• Today’s RTH Open & Prior RTH Close – With gap detection and “gap filled” alert.

• Killzone shading – NY Open (09:30–10:30 ET) and Lunch (11:15–13:30 ET).

• Values panel (top-right) – Each level with live distance in points & ticks.

• Right-edge level tags – With anti-overlap (stagger + vertical jitter).

• Price-scale tags – Native trackprice markers that always “stick” to the axis.

⸻

New in v6.4

• Minimal Mode: one click for a clean look (thinner lines, VWAP bands/IB extensions hidden, on-chart right-edge labels off; price-scale tags remain).

• Theme presets: Dark Hi-Contrast / Light Minimal / Futures Classic / Muted Dark.

• Anti-overlap controls: horizontal staggering, vertical jitter, and baseline offset to keep tags readable even when levels cluster.

⸻

Quick start (2 minutes)

1. Add to chart → keep defaults.

2. Sessions (ET):

• RTH Session default: 09:30–16:00 (US equities cash hours).

• Overnight Session default: 18:00–09:29.

Adjust for your market if you use different “day” hours (e.g., many use 08:20–13:30 ET for COMEX Gold).

3. Theme & Minimal Mode: pick a Theme Preset; enable Minimal Mode for screenshots.

4. Visibility: toggle PD/ON/VWAP/IB/References/Panel to taste.

5. Right-edge labels: turn Show Right-Edge Labels on. If they crowd, tune:

• Anti-overlap: min separation (ticks)

• Horizontal offset per tag (bars)

• Vertical jitter per step (ticks)

• Right-edge baseline offset (bars)

6. Alerts: open Add alert → Condition: and pick the events you want.

⸻

How levels are computed (no repainting)

• PDH/PDL: Intraday H/L are accumulated only while in RTH and saved at RTH close for “yesterday’s” values.

• ONH/ONL: Accumulated across the defined Overnight window and then held during RTH.

• RTH VWAP & ±σ: Volume-weighted mean and standard deviation, reset at the RTH open.

• IB: First N minutes of RTH (default 60). Extensions (1.5×/2.0×) appear after IB completes.

• Gaps: Today’s RTH open vs prior RTH close; “Gap Filled” triggers when price trades back to prior close.

⸻

Practical playbooks (how to trade around the levels)

1) PDH/PDL interactions

• Rejection: Price taps PDH/PDL then closes back inside → mean-reversion toward VWAP/IB.

• Acceptance: Close/hold beyond PDH/PDL with momentum → continuation to next HTF/IB target.

• Alert: PD Touch/Break.

2) ONH/ONL “taken”

• Often one ON extreme is taken during RTH. ONH Taken / ONL Taken → check if it’s a clean break or sweep & reclaim.

• Sweep + reclaim near VWAP can fuel rotations through the ON range.

3) VWAP ±σ framework

• Balanced: First tag of ±1σ often reverts toward VWAP.

• Trend: Persistent trade beyond ±1σ + IB break → target ±2σ/±3σ.

• Alerts: VWAP Cross and VWAP Reject (cross then immediate fail back).

4) IB breaks

• After IB completes, a clean IB break commonly targets 1.5× and sometimes 2.0×.

• Quick return inside IB = possible fade back to the opposite IB edge/VWAP.

• Alerts: IB Break Up / Down.

5) Gaps

• Gap-and-go: Opening drive away from prior close + VWAP support → trend until IB completion.

• Gap-fill: Weak open and VWAP overhead/underfoot → trade toward prior close; manage on Gap Filled alert.

Pro tip: Stack confluences (e.g., ONL sweep + VWAP reclaim + IB hold) and respect your execution rules (e.g., require a 5-minute close in direction, or your order-flow confirmation).

⸻

Inputs you’ll actually touch

• Sessions (ET): Session Timezone, RTH Session, Overnight Session.

• Visibility: toggles for PD/ON/VWAP/IB/Ref/Panel.

• VWAP bands: set σ multipliers (±1/±2/±3).

• IB: duration (minutes) and extension multipliers (1.5× / 2.0×).

• Style & Theme: Theme Preset, Main Line Width, Trackprice, Minimal Mode, and anti-overlap controls.

⸻

Alerts included

• PD Touch/Break — High ≥ PDH or Low ≤ PDL

• ONH Taken / ONL Taken — First in-RTH take of ONH/ONL

• VWAP Cross — Close crosses VWAP

• VWAP Reject — Cross then immediate fail back

• IB Break Up / Down — Break of IB High/Low after IB completes

• Gap Filled — Price trades back to prior RTH close

Setup: Add alert → Condition: Algo Index — Levels Pro → choose event → message → Notify on app/email.

⸻

Panel guide

The top-right panel shows each level plus live distance from last price:

LevelValue (Δpoints | Δticks)

Coloring: green if level is below current price, red if above.

⸻

Styling & screenshot tips

• Use Theme Preset that matches your chart.

• For dark charts, “Dark Hi-Contrast” with Main Line Width = 3 works well.

• Enable Trackprice for crisp axis tags that always stick to the right edge.

• Turn on Minimal Mode for cleaner screenshots (no VWAP bands or IB extensions, on-chart tags off; price-scale tags remain).

• If tags crowd, increase min separation (ticks) to 30–60 and horizontal offset to 3–5; add vertical jitter (4–12 ticks) and/or push tags farther right with baseline offset (bars).

⸻

Behavior & limitations

• Levels are computed incrementally; tables refresh on the last bar for efficiency.

• Right-edge labels are placed at bar_index + offset and do not track extra right-margin scrolling (TradingView limitation). The price-scale tags (from trackprice) do track the axis.

• “RTH” is what you define in inputs. If your market uses different day hours, change the session strings so PDH/PDL reflect your definition of “yesterday’s session.”

⸻

FAQ

Q: My PDH/PDL don’t match the daily chart.

A: By design this uses RTH-only highs/lows, not 24h daily bars. Adjust sessions if you want a different definition.

Q: Right-edge tags overlap or don’t sit at the far right.

A: Increase min separation / horizontal offset / vertical jitter and/or push tags farther with baseline offset. If you want markers that always hug the axis, rely on Trackprice.

Q: Can I change killzones?

A: Yes—edit the session strings in settings or request a version with user inputs for custom windows.

⸻

Disclaimer

Educational use only. This is not financial advice. Always apply your own risk management and confirmation rules.

⸻

Enjoy it? Please ⭐ the script and share screenshots using Minimal Mode + a Theme Preset that fits your style.

NightWatch 24/5 [theUltimator5]NightWatch 24/5 is a comprehensive indicator designed to seamlessly display both regular and overnight trading (BOATS exchange) into a single chart. Current TV limitations don't allow both overnight trading and regular exchanges to appear on the same chart due to timeframe visibility settings. We can either select between RTH (Regular Trading Hours) or ETH (Extended Trading Hours). There is no option to show 24 hour charts when looking at a stock. This indicator attempts to solve this issue.

Please read the entire description thoroughly because this indicator takes a little bit of setup to work properly!

---IMPORTANT-- -

This indicator MUST be used over a liquid cryptocurrency chart, like Bitcoin. It requires access to something that trades 24/7 and has volume data for all periods. Bitcoin on Coinbase is the best option. Please select Bitcoin as your main ticker before adding this indicator to the chart.

-------------------

This indicator combines the price of both the regular trading hours and the overnight trading to create a single price line and volume candles. You can select view settings to either overlay the price on the chart, or have it below the chart. Volume can be toggled on or off as well.

Default settings:

Ticker = GME

Overlay Candles on Main Chart = true

Display Data = Both Price and Volume

Show Status Table = true

Here is an explanation for each of these settings:

Ticker - Type in the ticker you want to track overnight and intraday data for

Overlay Candles on Main chart - This will push the price candles onto the main chart area instead of below it. Volume candles will remain in their own separate pane below. This is useful if you want to track both price and volume without adding the indicator twice.

Display Data - This determines what data to show. Volume, price, or both volume and price.

Show Status Table - This toggles on or off the table that shows the ticker name, current session, and the price (change) of the ticker since the most recent daily close.

If you overlay the price onto the chart, the price of the stock you are looking at will likely be a VERY different price than the crypto it is overlaying against. There are a couple workarounds. You can either zoom into the chart around the price of the stock you are looking at (time consuming), or you can go into your object tree and drag the indicator up into the main chart area. This will overlay the price onto the crypto while maintaining it's own unique y-axis.

After you move the indicator up, you can add the indicator back a second time, then change the settings to only show the volume candles. You can then toggle off the table on one of the two so you don't see duplicate tables. This is the setting I am showing in my chart above. The indicator is added twice with the price being pulled up into the same window as Bitcoin, then a second instance below showing just volume.

--LIMITATIONS--

Since the indicator requires the use of a 24 hour market ticker like Bitcoin, it DOES NOT display extended hours data. The price and volume data STOPS at 16:00 EST then resumes back up at 20:00 EST when BOATS opens. At 04:00, the price and volume then stops until 09:30, when the regular trading hours begin. This causes a flat line in the price during those periods. Unfortunately, there is no current workaround to this issue.

If Bitcoin becomes illiquid (or whatever crypto you choose), it will only populate data for the ticker you want if there is data available for that crypto at the same time period. A gap in Bitcoin volume will show a gap in trade activity for your ticker.

LTA - Futures Contract Size CalculatorLTA - Futures Contract Size Calculator

This indicator helps futures traders calculate the potential stop-loss (SL) value for their trades with ease. Simply input your entry price, stop-loss price, and number of contracts, and the indicator will compute the ticks moved, price movement, and total SL value in USD.

Key Features:

Supports a wide range of futures contracts, including:

Index Futures: E-mini S&P 500 (ES), Micro E-mini S&P 500 (MES), E-mini Nasdaq-100 (NQ), Micro E-mini Nasdaq-100 (MNQ)

Commodity Futures: Crude Oil (CL), Gold (GC), Micro Gold (MGC), Silver (SI), Micro Silver (SIL), Platinum (PL), Micro Platinum (MPL), Natural Gas (NG), Micro Natural Gas (MNG)

Bond Futures: 30-Year T-Bond (ZB)

Currency Futures: Euro FX (6E), Japanese Yen (6J), Australian Dollar (6A), British Pound (6B), Canadian Dollar (6C), Swiss Franc (6S), New Zealand Dollar (6N)

Displays key metrics in a clean table (bottom-right corner):

Instrument, Entry Price, Stop-Loss Price, Number of Contracts, Tick Size, Ticks Moved, Price Movement, and Total SL Value.

Automatically calculates based on the selected instrument’s tick size and tick value.

User-friendly interface with a dark theme for better visibility.

How to Use:

Add the indicator to your chart.

Select your instrument from the dropdown (ensure it matches your chart’s symbol, e.g., "NG1!" for NATURAL GAS (NG)).

Input your Entry Price, Stop-Loss Price, and Number of Contracts.

View the results in the table, including the Total SL Value in USD.

Ideal For:

Futures traders looking to quickly assess stop-loss risk.

Beginners and pros trading indices, commodities, bonds, or currencies.

Note: Ensure your chart symbol matches the selected instrument for accurate calculations. For best results, test with a few contracts and price levels to confirm the output.

This description is tailored for TradingView’s audience, providing a clear overview of the indicator’s functionality, supported instruments, and usage instructions. It also includes a note to help users avoid common pitfalls (e.g., mismatched symbols). If you’d like to adjust the tone, add more details, or include specific TradingView tags (e.g., , ), let me know!

E9 MM Nuke signalScript identifies wickless candles on a specified higher timeframe and plots them on a lower timeframe (If desired), such as 15 minutes. It includes options to adjust the margin for error (e.g. 5 tick wick), higher timeframe, and toggle the volume filter with period adjustment.

Wickless candles signal strong market sentiment shifts, indicating areas of significant buying or selling pressure. These areas can become key levels of support or resistance, making them crucial to monitor for potential price revisits.

Why Price Revisits Wickless Areas

Manipulators often create artificial wickless candles to deceive traders. However, genuine market movements can also produce wickless candles, indicating a strong consensus among market participants. In either case, the price is likely to revisit these areas as traders and investors react to the perceived market sentiment shift.

Key Features:

Margin Input:

Description: Allows users to specify the margin in 0.01 tick increments to account for small wicks due to spread issues.

Example: A margin of 0.05 ticks means the script will consider candles wickless if the high is within 0.05 ticks of the open and the low is within 0.05 ticks of the open.

Volume Filter:

Description: Users can enable or disable a volume filter to consider only candles with a volume greater than the average volume over a specified period.

Default: Enabled by default.

Volume Period Input: Users can specify the period for calculating the average volume (e.g., 9 periods).

Higher Timeframe Input:

Description: Allows users to select the higher timeframe on which to identify wickless candles.

Options: H4 ("240"), Daily ("D"), Weekly ("W"), Monthly ("M").

Plotting:

Bearish Wickless Candles: Plotted with a red circle and a "🐻" emoji above the bar.

Bullish Wickless Candles: Plotted with a green circle and a "🐂" emoji below the bar.

Swing Structure Scanner [LuxAlgo]The Swing Structure Scanner Indicator is a dashboard type indicator which displays a Consolidated "High/Low-Only" view of swing structure, with the capability to retrieve and display swing points from up to 6 different tickers and timeframes at once.

🔶 USAGE

This indicator displays swing structure data from up to 6 unique tickers or timeframes; Each graph represents the current swing structure retrieved from the requested chart/s.

Each swing graph displays the current live swing point positioning relative to the previous swing points. By analyzing the different formations, patterns can more easily be recognized and found across multiple tickers or timeframes at once.

This indicator serves as a nifty tool for confluence recognition, whether that's confluence throughout market tickers, or confluence through higher timeframes on the same ticker.

Alternatively, viewing the relative positioning of each swing point to each other, should give a clearer idea when higher lows or lower highs are formed. This can potentially indicate a newly forming trend, as well as serving as a warning to watch for breakouts.

The swing length can be changed to align with each individual's strategy, as well as a display look back can be adjusted to show more or less swing points at one time.

The display is fairly customizable, it is not fixed to 6 symbols at all times and can be minimized to only display the number of symbols needed; Additionally, the display can be set to vertical mode or horizontal(default) to utilize as needed.

Note: Hover over the swing point in the dashboard to get a readout of the exact price level of the swing point.

🔶 SETTINGS

Swing Length: Set the swing length for the structure calculations.

Swing Display Lookback: Sets the number of swing points (Pairs) to display in each Swing Graph display.

Symbols: Sets the Timeframe and Symbol for each Swing Graph.

Vertical Display: Display the Swing Graphs up and down, rather than side to side.

Scaling Factor: Scales the entire indicator up or down, to fit your needs.

Universal Ratio Trend Matrix [InvestorUnknown]The Universal Ratio Trend Matrix is designed for trend analysis on asset/asset ratios, supporting up to 40 different assets. Its primary purpose is to help identify which assets are outperforming others within a selection, providing a broad overview of market trends through a matrix of ratios. The indicator automatically expands the matrix based on the number of assets chosen, simplifying the process of comparing multiple assets in terms of performance.

Key features include the ability to choose from a narrow selection of indicators to perform the ratio trend analysis, allowing users to apply well-defined metrics to their comparison.

Drawback: Due to the computational intensity involved in calculating ratios across many assets, the indicator has a limitation related to loading speed. TradingView has time limits for calculations, and for users on the basic (free) plan, this could result in frequent errors due to exceeded time limits. To use the indicator effectively, users with any paid plans should run it on timeframes higher than 8h (the lowest timeframe on which it managed to load with 40 assets), as lower timeframes may not reliably load.

Indicators:

RSI_raw: Simple function to calculate the Relative Strength Index (RSI) of a source (asset price).

RSI_sma: Calculates RSI followed by a Simple Moving Average (SMA).

RSI_ema: Calculates RSI followed by an Exponential Moving Average (EMA).

CCI: Calculates the Commodity Channel Index (CCI).

Fisher: Implements the Fisher Transform to normalize prices.

Utility Functions:

f_remove_exchange_name: Strips the exchange name from asset tickers (e.g., "INDEX:BTCUSD" to "BTCUSD").

f_remove_exchange_name(simple string name) =>

string parts = str.split(name, ":")

string result = array.size(parts) > 1 ? array.get(parts, 1) : name

result

f_get_price: Retrieves the closing price of a given asset ticker using request.security().

f_constant_src: Checks if the source data is constant by comparing multiple consecutive values.

Inputs:

General settings allow users to select the number of tickers for analysis (used_assets) and choose the trend indicator (RSI, CCI, Fisher, etc.).

Table settings customize how trend scores are displayed in terms of text size, header visibility, highlighting options, and top-performing asset identification.

The script includes inputs for up to 40 assets, allowing the user to select various cryptocurrencies (e.g., BTCUSD, ETHUSD, SOLUSD) or other assets for trend analysis.

Price Arrays:

Price values for each asset are stored in variables (price_a1 to price_a40) initialized as na. These prices are updated only for the number of assets specified by the user (used_assets).

Trend scores for each asset are stored in separate arrays

// declare price variables as "na"

var float price_a1 = na, var float price_a2 = na, var float price_a3 = na, var float price_a4 = na, var float price_a5 = na

var float price_a6 = na, var float price_a7 = na, var float price_a8 = na, var float price_a9 = na, var float price_a10 = na

var float price_a11 = na, var float price_a12 = na, var float price_a13 = na, var float price_a14 = na, var float price_a15 = na

var float price_a16 = na, var float price_a17 = na, var float price_a18 = na, var float price_a19 = na, var float price_a20 = na

var float price_a21 = na, var float price_a22 = na, var float price_a23 = na, var float price_a24 = na, var float price_a25 = na

var float price_a26 = na, var float price_a27 = na, var float price_a28 = na, var float price_a29 = na, var float price_a30 = na

var float price_a31 = na, var float price_a32 = na, var float price_a33 = na, var float price_a34 = na, var float price_a35 = na

var float price_a36 = na, var float price_a37 = na, var float price_a38 = na, var float price_a39 = na, var float price_a40 = na

// create "empty" arrays to store trend scores

var a1_array = array.new_int(40, 0), var a2_array = array.new_int(40, 0), var a3_array = array.new_int(40, 0), var a4_array = array.new_int(40, 0)

var a5_array = array.new_int(40, 0), var a6_array = array.new_int(40, 0), var a7_array = array.new_int(40, 0), var a8_array = array.new_int(40, 0)

var a9_array = array.new_int(40, 0), var a10_array = array.new_int(40, 0), var a11_array = array.new_int(40, 0), var a12_array = array.new_int(40, 0)

var a13_array = array.new_int(40, 0), var a14_array = array.new_int(40, 0), var a15_array = array.new_int(40, 0), var a16_array = array.new_int(40, 0)

var a17_array = array.new_int(40, 0), var a18_array = array.new_int(40, 0), var a19_array = array.new_int(40, 0), var a20_array = array.new_int(40, 0)

var a21_array = array.new_int(40, 0), var a22_array = array.new_int(40, 0), var a23_array = array.new_int(40, 0), var a24_array = array.new_int(40, 0)

var a25_array = array.new_int(40, 0), var a26_array = array.new_int(40, 0), var a27_array = array.new_int(40, 0), var a28_array = array.new_int(40, 0)

var a29_array = array.new_int(40, 0), var a30_array = array.new_int(40, 0), var a31_array = array.new_int(40, 0), var a32_array = array.new_int(40, 0)

var a33_array = array.new_int(40, 0), var a34_array = array.new_int(40, 0), var a35_array = array.new_int(40, 0), var a36_array = array.new_int(40, 0)

var a37_array = array.new_int(40, 0), var a38_array = array.new_int(40, 0), var a39_array = array.new_int(40, 0), var a40_array = array.new_int(40, 0)

f_get_price(simple string ticker) =>

request.security(ticker, "", close)

// Prices for each USED asset

f_get_asset_price(asset_number, ticker) =>

if (used_assets >= asset_number)

f_get_price(ticker)

else

na

// overwrite empty variables with the prices if "used_assets" is greater or equal to the asset number

if barstate.isconfirmed // use barstate.isconfirmed to avoid "na prices" and calculation errors that result in empty cells in the table

price_a1 := f_get_asset_price(1, asset1), price_a2 := f_get_asset_price(2, asset2), price_a3 := f_get_asset_price(3, asset3), price_a4 := f_get_asset_price(4, asset4)

price_a5 := f_get_asset_price(5, asset5), price_a6 := f_get_asset_price(6, asset6), price_a7 := f_get_asset_price(7, asset7), price_a8 := f_get_asset_price(8, asset8)

price_a9 := f_get_asset_price(9, asset9), price_a10 := f_get_asset_price(10, asset10), price_a11 := f_get_asset_price(11, asset11), price_a12 := f_get_asset_price(12, asset12)

price_a13 := f_get_asset_price(13, asset13), price_a14 := f_get_asset_price(14, asset14), price_a15 := f_get_asset_price(15, asset15), price_a16 := f_get_asset_price(16, asset16)

price_a17 := f_get_asset_price(17, asset17), price_a18 := f_get_asset_price(18, asset18), price_a19 := f_get_asset_price(19, asset19), price_a20 := f_get_asset_price(20, asset20)

price_a21 := f_get_asset_price(21, asset21), price_a22 := f_get_asset_price(22, asset22), price_a23 := f_get_asset_price(23, asset23), price_a24 := f_get_asset_price(24, asset24)

price_a25 := f_get_asset_price(25, asset25), price_a26 := f_get_asset_price(26, asset26), price_a27 := f_get_asset_price(27, asset27), price_a28 := f_get_asset_price(28, asset28)

price_a29 := f_get_asset_price(29, asset29), price_a30 := f_get_asset_price(30, asset30), price_a31 := f_get_asset_price(31, asset31), price_a32 := f_get_asset_price(32, asset32)

price_a33 := f_get_asset_price(33, asset33), price_a34 := f_get_asset_price(34, asset34), price_a35 := f_get_asset_price(35, asset35), price_a36 := f_get_asset_price(36, asset36)

price_a37 := f_get_asset_price(37, asset37), price_a38 := f_get_asset_price(38, asset38), price_a39 := f_get_asset_price(39, asset39), price_a40 := f_get_asset_price(40, asset40)

Universal Indicator Calculation (f_calc_score):

This function allows switching between different trend indicators (RSI, CCI, Fisher) for flexibility.

It uses a switch-case structure to calculate the indicator score, where a positive trend is denoted by 1 and a negative trend by 0. Each indicator has its own logic to determine whether the asset is trending up or down.

// use switch to allow "universality" in indicator selection

f_calc_score(source, trend_indicator, int_1, int_2) =>

int score = na

if (not f_constant_src(source)) and source > 0.0 // Skip if you are using the same assets for ratio (for example BTC/BTC)

x = switch trend_indicator

"RSI (Raw)" => RSI_raw(source, int_1)

"RSI (SMA)" => RSI_sma(source, int_1, int_2)

"RSI (EMA)" => RSI_ema(source, int_1, int_2)

"CCI" => CCI(source, int_1)

"Fisher" => Fisher(source, int_1)

y = switch trend_indicator

"RSI (Raw)" => x > 50 ? 1 : 0

"RSI (SMA)" => x > 50 ? 1 : 0

"RSI (EMA)" => x > 50 ? 1 : 0

"CCI" => x > 0 ? 1 : 0

"Fisher" => x > x ? 1 : 0

score := y

else

score := 0

score

Array Setting Function (f_array_set):

This function populates an array with scores calculated for each asset based on a base price (p_base) divided by the prices of the individual assets.

It processes multiple assets (up to 40), calling the f_calc_score function for each.

// function to set values into the arrays

f_array_set(a_array, p_base) =>

array.set(a_array, 0, f_calc_score(p_base / price_a1, trend_indicator, int_1, int_2))

array.set(a_array, 1, f_calc_score(p_base / price_a2, trend_indicator, int_1, int_2))

array.set(a_array, 2, f_calc_score(p_base / price_a3, trend_indicator, int_1, int_2))

array.set(a_array, 3, f_calc_score(p_base / price_a4, trend_indicator, int_1, int_2))

array.set(a_array, 4, f_calc_score(p_base / price_a5, trend_indicator, int_1, int_2))

array.set(a_array, 5, f_calc_score(p_base / price_a6, trend_indicator, int_1, int_2))

array.set(a_array, 6, f_calc_score(p_base / price_a7, trend_indicator, int_1, int_2))

array.set(a_array, 7, f_calc_score(p_base / price_a8, trend_indicator, int_1, int_2))

array.set(a_array, 8, f_calc_score(p_base / price_a9, trend_indicator, int_1, int_2))

array.set(a_array, 9, f_calc_score(p_base / price_a10, trend_indicator, int_1, int_2))

array.set(a_array, 10, f_calc_score(p_base / price_a11, trend_indicator, int_1, int_2))

array.set(a_array, 11, f_calc_score(p_base / price_a12, trend_indicator, int_1, int_2))

array.set(a_array, 12, f_calc_score(p_base / price_a13, trend_indicator, int_1, int_2))

array.set(a_array, 13, f_calc_score(p_base / price_a14, trend_indicator, int_1, int_2))

array.set(a_array, 14, f_calc_score(p_base / price_a15, trend_indicator, int_1, int_2))

array.set(a_array, 15, f_calc_score(p_base / price_a16, trend_indicator, int_1, int_2))

array.set(a_array, 16, f_calc_score(p_base / price_a17, trend_indicator, int_1, int_2))

array.set(a_array, 17, f_calc_score(p_base / price_a18, trend_indicator, int_1, int_2))

array.set(a_array, 18, f_calc_score(p_base / price_a19, trend_indicator, int_1, int_2))

array.set(a_array, 19, f_calc_score(p_base / price_a20, trend_indicator, int_1, int_2))

array.set(a_array, 20, f_calc_score(p_base / price_a21, trend_indicator, int_1, int_2))

array.set(a_array, 21, f_calc_score(p_base / price_a22, trend_indicator, int_1, int_2))

array.set(a_array, 22, f_calc_score(p_base / price_a23, trend_indicator, int_1, int_2))

array.set(a_array, 23, f_calc_score(p_base / price_a24, trend_indicator, int_1, int_2))

array.set(a_array, 24, f_calc_score(p_base / price_a25, trend_indicator, int_1, int_2))

array.set(a_array, 25, f_calc_score(p_base / price_a26, trend_indicator, int_1, int_2))

array.set(a_array, 26, f_calc_score(p_base / price_a27, trend_indicator, int_1, int_2))

array.set(a_array, 27, f_calc_score(p_base / price_a28, trend_indicator, int_1, int_2))

array.set(a_array, 28, f_calc_score(p_base / price_a29, trend_indicator, int_1, int_2))

array.set(a_array, 29, f_calc_score(p_base / price_a30, trend_indicator, int_1, int_2))

array.set(a_array, 30, f_calc_score(p_base / price_a31, trend_indicator, int_1, int_2))

array.set(a_array, 31, f_calc_score(p_base / price_a32, trend_indicator, int_1, int_2))

array.set(a_array, 32, f_calc_score(p_base / price_a33, trend_indicator, int_1, int_2))

array.set(a_array, 33, f_calc_score(p_base / price_a34, trend_indicator, int_1, int_2))

array.set(a_array, 34, f_calc_score(p_base / price_a35, trend_indicator, int_1, int_2))

array.set(a_array, 35, f_calc_score(p_base / price_a36, trend_indicator, int_1, int_2))

array.set(a_array, 36, f_calc_score(p_base / price_a37, trend_indicator, int_1, int_2))

array.set(a_array, 37, f_calc_score(p_base / price_a38, trend_indicator, int_1, int_2))

array.set(a_array, 38, f_calc_score(p_base / price_a39, trend_indicator, int_1, int_2))

array.set(a_array, 39, f_calc_score(p_base / price_a40, trend_indicator, int_1, int_2))

a_array

Conditional Array Setting (f_arrayset):

This function checks if the number of used assets is greater than or equal to a specified number before populating the arrays.

// only set values into arrays for USED assets

f_arrayset(asset_number, a_array, p_base) =>

if (used_assets >= asset_number)

f_array_set(a_array, p_base)

else

na

Main Logic

The main logic initializes arrays to store scores for each asset. Each array corresponds to one asset's performance score.

Setting Trend Values: The code calls f_arrayset for each asset, populating the respective arrays with calculated scores based on the asset prices.

Combining Arrays: A combined_array is created to hold all the scores from individual asset arrays. This array facilitates further analysis, allowing for an overview of the performance scores of all assets at once.

// create a combined array (work-around since pinescript doesn't support having array of arrays)

var combined_array = array.new_int(40 * 40, 0)

if barstate.islast

for i = 0 to 39

array.set(combined_array, i, array.get(a1_array, i))

array.set(combined_array, i + (40 * 1), array.get(a2_array, i))

array.set(combined_array, i + (40 * 2), array.get(a3_array, i))

array.set(combined_array, i + (40 * 3), array.get(a4_array, i))

array.set(combined_array, i + (40 * 4), array.get(a5_array, i))

array.set(combined_array, i + (40 * 5), array.get(a6_array, i))

array.set(combined_array, i + (40 * 6), array.get(a7_array, i))

array.set(combined_array, i + (40 * 7), array.get(a8_array, i))

array.set(combined_array, i + (40 * 8), array.get(a9_array, i))

array.set(combined_array, i + (40 * 9), array.get(a10_array, i))

array.set(combined_array, i + (40 * 10), array.get(a11_array, i))

array.set(combined_array, i + (40 * 11), array.get(a12_array, i))

array.set(combined_array, i + (40 * 12), array.get(a13_array, i))

array.set(combined_array, i + (40 * 13), array.get(a14_array, i))

array.set(combined_array, i + (40 * 14), array.get(a15_array, i))

array.set(combined_array, i + (40 * 15), array.get(a16_array, i))

array.set(combined_array, i + (40 * 16), array.get(a17_array, i))

array.set(combined_array, i + (40 * 17), array.get(a18_array, i))

array.set(combined_array, i + (40 * 18), array.get(a19_array, i))

array.set(combined_array, i + (40 * 19), array.get(a20_array, i))

array.set(combined_array, i + (40 * 20), array.get(a21_array, i))

array.set(combined_array, i + (40 * 21), array.get(a22_array, i))

array.set(combined_array, i + (40 * 22), array.get(a23_array, i))

array.set(combined_array, i + (40 * 23), array.get(a24_array, i))

array.set(combined_array, i + (40 * 24), array.get(a25_array, i))

array.set(combined_array, i + (40 * 25), array.get(a26_array, i))

array.set(combined_array, i + (40 * 26), array.get(a27_array, i))

array.set(combined_array, i + (40 * 27), array.get(a28_array, i))

array.set(combined_array, i + (40 * 28), array.get(a29_array, i))

array.set(combined_array, i + (40 * 29), array.get(a30_array, i))

array.set(combined_array, i + (40 * 30), array.get(a31_array, i))

array.set(combined_array, i + (40 * 31), array.get(a32_array, i))

array.set(combined_array, i + (40 * 32), array.get(a33_array, i))

array.set(combined_array, i + (40 * 33), array.get(a34_array, i))

array.set(combined_array, i + (40 * 34), array.get(a35_array, i))

array.set(combined_array, i + (40 * 35), array.get(a36_array, i))

array.set(combined_array, i + (40 * 36), array.get(a37_array, i))

array.set(combined_array, i + (40 * 37), array.get(a38_array, i))

array.set(combined_array, i + (40 * 38), array.get(a39_array, i))

array.set(combined_array, i + (40 * 39), array.get(a40_array, i))

Calculating Sums: A separate array_sums is created to store the total score for each asset by summing the values of their respective score arrays. This allows for easy comparison of overall performance.

Ranking Assets: The final part of the code ranks the assets based on their total scores stored in array_sums. It assigns a rank to each asset, where the asset with the highest score receives the highest rank.

// create array for asset RANK based on array.sum

var ranks = array.new_int(used_assets, 0)

// for loop that calculates the rank of each asset

if barstate.islast

for i = 0 to (used_assets - 1)

int rank = 1

for x = 0 to (used_assets - 1)

if i != x

if array.get(array_sums, i) < array.get(array_sums, x)

rank := rank + 1

array.set(ranks, i, rank)

Dynamic Table Creation

Initialization: The table is initialized with a base structure that includes headers for asset names, scores, and ranks. The headers are set to remain constant, ensuring clarity for users as they interpret the displayed data.

Data Population: As scores are calculated for each asset, the corresponding values are dynamically inserted into the table. This is achieved through a loop that iterates over the scores and ranks stored in the combined_array and array_sums, respectively.

Automatic Extending Mechanism

Variable Asset Count: The code checks the number of assets defined by the user. Instead of hardcoding the number of rows in the table, it uses a variable to determine the extent of the data that needs to be displayed. This allows the table to expand or contract based on the number of assets being analyzed.

Dynamic Row Generation: Within the loop that populates the table, the code appends new rows for each asset based on the current asset count. The structure of each row includes the asset name, its score, and its rank, ensuring that the table remains consistent regardless of how many assets are involved.

// Automatically extending table based on the number of used assets

var table table = table.new(position.bottom_center, 50, 50, color.new(color.black, 100), color.white, 3, color.white, 1)

if barstate.islast

if not hide_head

table.cell(table, 0, 0, "Universal Ratio Trend Matrix", text_color = color.white, bgcolor = #010c3b, text_size = fontSize)

table.merge_cells(table, 0, 0, used_assets + 3, 0)

if not hide_inps

table.cell(table, 0, 1,

text = "Inputs: You are using " + str.tostring(trend_indicator) + ", which takes: " + str.tostring(f_get_input(trend_indicator)),

text_color = color.white, text_size = fontSize), table.merge_cells(table, 0, 1, used_assets + 3, 1)

table.cell(table, 0, 2, "Assets", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, x + 1, 2, text = str.tostring(array.get(assets, x)), text_color = color.white, bgcolor = #010c3b, text_size = fontSize)

table.cell(table, 0, x + 3, text = str.tostring(array.get(assets, x)), text_color = color.white, bgcolor = f_asset_col(array.get(ranks, x)), text_size = fontSize)

for r = 0 to (used_assets - 1)

for c = 0 to (used_assets - 1)

table.cell(table, c + 1, r + 3, text = str.tostring(array.get(combined_array, c + (r * 40))),

text_color = hl_type == "Text" ? f_get_col(array.get(combined_array, c + (r * 40))) : color.white, text_size = fontSize,

bgcolor = hl_type == "Background" ? f_get_col(array.get(combined_array, c + (r * 40))) : na)

for x = 0 to (used_assets - 1)

table.cell(table, x + 1, x + 3, "", bgcolor = #010c3b)

table.cell(table, used_assets + 1, 2, "", bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, used_assets + 1, x + 3, "==>", text_color = color.white)

table.cell(table, used_assets + 2, 2, "SUM", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

table.cell(table, used_assets + 3, 2, "RANK", text_color = color.white, text_size = fontSize, bgcolor = #010c3b)

for x = 0 to (used_assets - 1)

table.cell(table, used_assets + 2, x + 3,

text = str.tostring(array.get(array_sums, x)),

text_color = color.white, text_size = fontSize,

bgcolor = f_highlight_sum(array.get(array_sums, x), array.get(ranks, x)))

table.cell(table, used_assets + 3, x + 3,

text = str.tostring(array.get(ranks, x)),

text_color = color.white, text_size = fontSize,

bgcolor = f_highlight_rank(array.get(ranks, x)))

Risk Radar ProThe "Risk Radar Pro" indicator is a sophisticated tool designed to help investors and traders assess the risk and performance of their investments over a specified period. This presentation will explain each component of the indicator, how to interpret the results, and the advantages compared to traditional metrics.

The "Risk Radar Pro" indicator includes several key metrics:

● Beta

● Maximum Drawdown

● Compound Annual Growth Rate (CAGR)

● Annualized Volatility

● Dynamic Sharpe Ratio

● Dynamic Sortino Ratio

Each of these metrics is dynamically calculated using data from the entire selected period, providing a more adaptive and accurate measure of performance and risk.

1. Start Date