CVD - Cumulative Volume Delta Candles█ OVERVIEW

This indicator displays cumulative volume delta in candle form. It uses intrabar information to obtain more precise volume delta information than methods using only the chart's timeframe.

█ CONCEPTS

Bar polarity

By bar polarity , we mean the direction of a bar, which is determined by looking at the bar's close vs its open .

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 bars at the lower timeframe of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This script uses a LTF to access intrabars. The lower the LTF, the more intrabars are analyzed, but the less chart bars can display CVD information because there is a limit to the total number of intrabars that can be analyzed.

Volume delta

The volume delta concept divides a bar's volume in "up" and "down" volumes. The delta is calculated by subtracting down volume from up volume. Many calculation techniques exist to isolate up and down volume within a bar. The simplest techniques use the polarity of interbar price changes to assign their volume to up or down slots, e.g., On Balance Volume or the Klinger Oscillator . Others such as Chaikin Money Flow use assumptions based on a bar's OHLC values. The most precise calculation method uses tick data and assigns the volume of each tick to the up or down slot depending on whether the transaction occurs at the bid or ask price. While this technique is ideal, it requires huge amounts of data on historical bars, which usually limits the historical depth of charts and the number of symbols for which tick data is available.

This indicator uses intrabar analysis to achieve a compromise between the simplest and most precise methods of calculating volume delta. In the context where historical tick data is not yet available on TradingView, intrabar analysis is the most precise technique to calculate volume delta on historical bars on our charts. Our Volume Profile indicators use it. Other volume delta indicators in our Community Scripts such as the Realtime 5D Profile use realtime chart updates to achieve more precise volume delta calculations, but that method cannot be used on historical bars, so those indicators only work in real time.

This is the logic we use to assign intrabar volume to up or down slots:

• If the intrabar's open and close values are different, their relative position is used.

• If the intrabar's open and close values are the same, the difference between the intrabar's close and the previous intrabar's close is used.

• As a last resort, when there is no movement during an intrabar and it closes at the same price as the previous intrabar, the last known polarity is used.

Once all intrabars making up a chart bar have been analyzed and the up or down property of each intrabar's volume determined, the up volumes are added and the down volumes subtracted. The resulting value is volume delta for that chart bar.

█ FEATURES

CVD Candles

Cumulative Volume Delta Candles present volume delta information as it evolves during a period of time.

This is how each candle's levels are calculated:

• open : Each candle's' open level is the cumulative volume delta for the current period at the start of the bar.

This value becomes zero on the first candle following a CVD reset.

The candles after the first one always open where the previous candle closed.

The candle's high, low and close levels are then calculated by adding or subtracting a volume value to the open.

• high : The highest volume delta value found in intrabars. If it is not higher than the volume delta for the bar, then that candle will have no upper wick.

• low : The lowest volume delta value found in intrabars. If it is not lower than the volume delta for the bar, then that candle will have no lower wick.

• close : The aggregated volume delta for all intrabars. If volume delta is positive for the chart bar, then the candle's close will be higher than its open, and vice versa.

The candles are plotted in one of two configurable colors, depending on the polarity of volume delta for the bar.

CVD resets

The "cumulative" part of the indicator's name stems from the fact that calculations accumulate during a period of time. This allows you to analyze the progression of volume delta across manageable chunks, which is often more useful than looking at volume delta cumulated from the beginning of a chart's history.

You can configure the reset period using the "CVD Resets" input, which offers the following selections:

• None : Calculations do not reset.

• On a fixed higher timeframe : Calculations reset on the higher timeframe you select in the "Fixed higher timeframe" field.

• At a fixed time that you specify.

• At the beginning of the regular session .

• On a stepped higher timeframe : Calculations reset on a higher timeframe automatically stepped using the chart's timeframe and following these rules:

Chart TF HTF

< 1min 1H

< 3H 1D

<= 12H 1W

< 1W 1M

>= 1W 1Y

The indicator's background shows where resets occur.

Intrabar precision

The precision of calculations increases with the number of intrabars analyzed for each chart bar. It is controlled through the script's "Intrabar precision" input, which offers the following selections:

• Least precise, covering many chart bars

• Less precise, covering some chart bars

• More precise, covering less chart bars

• Most precise, 1min intrabars

As there is a limit to the number of intrabars that can be analyzed by a script, a tradeoff occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

Total volume candles

You can choose to display candles showing the total intrabar volume for the chart bar. This provides you with more context to evaluate a bar's volume delta by showing it relative to the sum of intrabar volume. Note that because of the reasons explained in the "NOTES" section further down, the total volume is the sum of all intrabar volume rather than the volume of the bar at the chart's timeframe.

Total volume candles can be configured with their own up and down colors. You can also control the opacity of their bodies to make them more or less prominent. This publication's chart shows the indicator with total volume candles. They are turned off by default, so you will need to choose to display them in the script's inputs for them to plot.

Divergences

Divergences occur when the polarity of volume delta does not match that of the chart bar. You can identify divergences by coloring the CVD candles differently for them, or by coloring the indicator's background.

Information box

An information box in the lower-left corner of the indicator displays the HTF used for resets, the LTF used for intrabars, and the average quantity of intrabars per chart bar. You can hide the box using the script's inputs.

█ INTERPRETATION

The first thing to look at when analyzing CVD candles is the side of the zero line they are on, as this tells you if CVD is generally bullish or bearish. Next, one should consider the relative position of successive candles, just as you would with a price chart. Are successive candles trending up, down, or stagnating? Keep in mind that whatever trend you identify must be considered in the context of where it appears with regards to the zero line; an uptrend in a negative CVD (below the zero line) may not be as powerful as one taking place in positive CVD values, but it may also predate a movement into positive CVD territory. The same goes with stagnation; a trader in a long position will find stagnation in positive CVD territory less worrisome than stagnation under the zero line.

After consideration of the bigger picture, one can drill down into the details. Exactly what you are looking for in markets will, of course, depend on your trading methodology, but you may find it useful to:

• Evaluate volume delta for the bar in relation to price movement for that bar.

• Evaluate the proportion that volume delta represents of total volume.

• Notice divergences and if the chart's candle shape confirms a hesitation point, as a Doji would.

• Evaluate if the progress of CVD candles correlates with that of chart bars.

• Analyze the wicks. As with price candles, long wicks tend to indicate weakness.

Always keep in mind that unless you have chosen not to reset it, your CVD resets for each period, whether it is fixed or automatically stepped. Consequently, any trend from the preceding period must re-establish itself in the next.

█ NOTES

Know your volume

Traders using volume information should understand the volume data they are using: where it originates and what transactions it includes, as this can vary with instruments, sectors, exchanges, timeframes, and between historical and realtime bars. The information used to build a chart's bars and display volume comes from data providers (exchanges, brokers, etc.) who often maintain distinct feeds for intraday and end-of-day (EOD) timeframes. How volume data is assembled for the two feeds depends on how instruments are traded in that sector and/or the volume reporting policy for each feed. Instruments from crypto and forex markets, for example, will often display similar volume on both feeds. Stocks will often display variations because block trades or other types of trades may not be included in their intraday volume data. Futures will also typically display variations.

Note that as intraday vs EOD variations exist for historical bars on some instruments, differences may also exist between the realtime feeds used on intraday vs 1D or greater timeframes for those same assets. Realtime reporting rules will often be different from historical feed reporting rules, so variations between realtime feeds will often be different from the variations between historical feeds for the same instrument. The Volume X-ray indicator can help you analyze differences between intraday and EOD volumes for the instruments you trade.

If every unit of volume is both bought by a buyer and sold by a seller, how can volume delta make sense?

Traders who do not understand the mechanics of matching engines (the exchange software that matches orders from buyers and sellers) sometimes argue that the concept of volume delta is flawed, as every unit of volume is both bought and sold. While they are rigorously correct in stating that every unit of volume is both bought and sold, they overlook the fact that information can be mined by analyzing variations in the price of successive ticks, or in our case, intrabars.

Our calculations model the situation where, in fully automated order handling, market orders are generally matched to limit orders sitting in the order book. Buy market orders are matched to quotes at the ask level and sell market orders are matched to quotes at the bid level. As explained earlier, we use the same logic when comparing intrabar prices. While using intrabar analysis does not produce results as precise as when individual transactions — or ticks — are analyzed, results are much more precise than those of methods using only chart prices.

Not only does the concept underlying volume delta make sense, it provides a window on an oft-overlooked variable which, with price and time, is the only basic information representing market activity. Furthermore, because the calculation of volume delta also uses price and time variations, one could conceivably surmise that it can provide a more complete model than ones using price and time only. Whether or not volume delta can be useful in your trading practice, as usual, is for you to decide, as each trader's methodology is different.

For Pine Script™ coders

As our latest Polarity Divergences publication, this script uses the recently released request.security_lower_tf() Pine Script™ function discussed in this blog post . It works differently from the usual request.security() in that it can only be used at LTFs, and it returns an array containing one value per intrabar. This makes it much easier for programmers to access intrabar information.

Look first. Then leap.

Search in scripts for "文华财经tick价格"

Grid Bot AutoThis script is an auto-adjusting grid bot simulator. This is an improved version of the original Grid Bot Simulator. The grid bot is best used for ranging/choppy markets. Prices are divided into grids, or trade zones, that will trigger signals each time a new zone is entered. During ranging markets, each transaction is followed by a “take profit.” As the market starts to trend, transactions are stacked (compare to DCA ), until the market consolidates. No signals are triggered above the Upper Limit or Below the Lower Limit. Unlike the previous version, the upper and lower limits are calculated automatically. Grid levels are determined by four factors: Smoothing, Laziness, Elasticity, and Grid Intervals.

Smoothing:

A moving average (or linear regression) is applied to each close price as a basis. Options for smoothing are Linear Regression, Simple Moving Average, Exponential Moving Average, Volume-Weighted Moving Average, Triple-Exponential Moving Average.

Laziness:

Laziness is the percentage change required to reach the next level. If laziness is 1.5, the price must move up or down by 1.5% before the grid will change. This concept is based on Alex Grover’s Efficient Trend Step. This allows the grids to be based on even price levels, as opposed to jagged moving averages.

Elasticity:

Elasticity is the degree of “stickiness” to the current price trend. If the smoothing line remains above (or below) the current grid center without reverting but still not enough to reach the next grid level, the grid line will start to curve toward the next grid level. Elasticity is added to (or subtracted from) the gridline by a factor of minimum system ticks for the current pair. Elasticity of zero will keep the gridlines horizontal. If elasticity is too high, the grid will distort.

Grid Intervals:

Grid intervals are the percentage of space between each grid.

Laziness = 4%, Elasticity = 0. Price must move at least 4% before reaching the next level. With zero elasticity, gridlines are straight.

Laziness = 5%, Elasticity = 100. For each bar at a new grid level, the grid will start “curve” toward the next price level (up if price is greater than the middle grid, down if less than middle grid). Elasticity is calculated by the user-inputted “Elasticity” multiplied by the minimum tick for the current pair (ELSTX = syminfo.mintick * iELSTX)

Try experimenting with different combinations of the Smoothing Length, Smoothing Type, Laziness, Elasticity, and Grid Intervals to find the optimum settings for each chart. Lower-priced pairs (e.g. XRP/ADA/DODGE) will require lower Elasticity. Also note that different exchanges may have different minimum tick values. For example, minimum tick for BITMEX:XBTUSD and BYBIT:BTCUSD is .5, but BINANCE:BTCUSDT and COINBASE:BTCUSD is .01.

s3.tradingview.com

DODGEUSDT, 5min. Laziness: 4%, Elasticity 2.5

Number of Grids: 2. Laziness: 3.75%. Elasticity: 150. Grid Interval 2%.

Settings Overview

Smoothing Length : Smoothing period

Smoothing Type : Linear Regression, Simple Moving Average, Exponential Moving Average, Volume-Weighted Moving Average, Triple-Exponential Moving Average

Laziness : Percentage required for price to move until it reaches the next level. If price does not reach the next level (up or down), the grid will remain the same as previous grid (because it’s lazy).

Elasticity : Amount of curvature toward the next grid, based on the current price trend. As elasticity increases, gridlines will curve up or down by a factor of the number of ticks since the last grid change.

Grid Interval : Percent between grid levels.

Number of Grids : Number of grids to show.

Cooldown : Number of bars to wait to prevent consecutive signals.

Grid Line Transparency : Lower transparencies brighten the gridlines; higher transparencies dim the gridlines. To hide the gridlines completely, enter 100.

Fill Transparency: Lower transparencies brighten the fill box; higher transparencies dim the fill box. To hide the fill box completely, enter 100.

Signal Size : Make signal triangles large or small.

Reset Buy/Sell Index When Grids Change : When a new grid is formed, resetting the index may prevent false signals (experimental)

Use Highs/Lows for Signals : If enabled, signals are triggered as soon as the price touches the next zone. If disabled, signals are triggered after bar closes. Enable this for “Once Per Bar alerts. Disable for “Once Per Bar Close” alerts.

Show Min Tick : If checked, syminfo.mintick is displayed in upper-righthand corner. Useful for estimating Laziness.

Reverse Fill Colors : Default fill for fill boxes is green after buy and red after sell. Check this box to reverse.

Note: The Grid Bot Simulator scripts are experimental and works in progress. Please feel free to comment or contact me if you have suggestions/complaints.

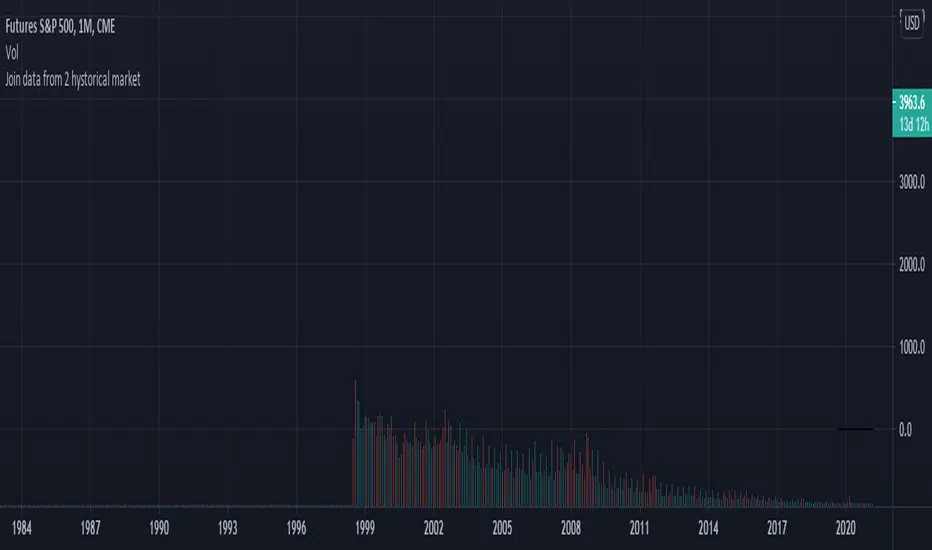

Join data and union of 2 hystorical markets

How to create a union from two contiguous Tradingview tickers (series)

Francesco Marzolo March 18, 2021

Go to the older ticker of the two, for example CME: SP1! and open it on Tradingview.

On the graph thus created, add this script.

In the indicator settings select the same ticker as the chart in Symbol1

while in Symbol2 the ticker from which to retrieve the most recent data, for example: SPX500

The operation this script does is examine each bar of the two tickers, where there is a value for the second it holds this one, where it does not exist in second ticker it keeps the value of the first one. This new series is called Merge. So now in the chart there will be 4 series:

- that of the original chart without script

- the same series loaded via script (Symbol1)

- series 2 of "new" data (Symbol2)

- the Merge series that "prefers" the Symbol2 data if present, otherwise it shows Symbol1

So now you have to change the visibility of the 4 series to see the differences:

- turn off the visibility of the chart indicator

- turn off the Symbol1 series in the script properties (old data only)

- switch off the Symbol2 series as well (only new data)

- switch on the Merge series (new data if existing, old if not present in the new ticker)

Compare (RSI) MACDHere I've created an indicator which can be used together with my "Compare (RSI) Ticker 3x" Indicator.

It makes it much easier to see the movements between the "RSI Ticker 1" and "RSI Ticker 2/3".

- The white line is the "MACD" of Ticker 1, which is the difference between the "RSI Ticker 1" and "RSI Ticker 2/3".

- The purple line is the "Signal" line, an EMA of the "MACD". (Length is adjustable)

- The "0-line" is the "RSI Ticker 2/3" line, when Ticker 2 is chosen, this will be blue coloured, when Ticker 3 is chosen it will be red.

Because 2 MACD in 1 indicator is way too messy, you only can choose the comparison against Ticker 2 OR Ticker 3.

- In "Settings" > "Inputs" you can enable/disable the second or third Ticker

(If Ticker 2 is enabled, Ticker 3 is disabled and vice versa)

- The second Ticker has multiple choices

- The third you can type any Ticker you want, for example CRYPTOCAP:BNB, BINANCE:ETHUSDT, NASDAQ_DLY:NDX or whatever,

just start typing and you'll see the possibilities (You also can choose between "Cryptocurrencies", "Index", "Forex", ...)

- When the "MACD" crosses the "0-line", arrows will appear, white ones for "MACD", purple ones for the "Signal" line.

- The "Histogram" makes it easier to see the difference between "MACD" and "Signal" line.

- The source of this indicator is adjustable

- When the second chosen Ticker is the same as the first Ticker, of course you will be seeing lines

(because there is no difference between the 2 Tickers, the EMA is visible though)

If you use both "Compare (RSI) Ticker 3x" AND "Compare (RSI) MACD", of course be aware that you have the same Ticker 2 or 3 in each indicator!

YM Ultimate SNIPER# YM Ultimate SNIPER - Documentation & Trading Guide

## 🎯 Unified GRA + DeepFlow | YM-Optimized for Low Volatility

**TARGET: 3-7 High-Confluence Trades per Day**

> **Philosophy:** *YM's lower volatility is not a weakness—it's our edge. Predictability + precision = consistent profits.*

---

## ⚡ QUICK REFERENCE CARD

```

┌─────────────────────────────────────────────────────────────────────────────┐

│ YM ULTIMATE SNIPER - QUICK REFERENCE │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ 💰 YM BASICS: │

│ ═════════════ │

│ • 1 tick = 1 point = $5/contract │

│ • Typical daily range: 150-400 points │

│ • 30-40% less volatile than NQ │

│ • More institutional, less retail noise │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ 🎯 TIER THRESHOLDS (YM-OPTIMIZED): │

│ ══════════════════════════════════ │

│ S-TIER: 50+ pts = $250+/contract → HOLD (Institutional sweep) │

│ A-TIER: 25-49 pts = $125-245/contract → SWING (Strong momentum) │

│ B-TIER: 12-24 pts = $60-120/contract → SCALP (Quick grab) │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ ⏰ SESSION WINDOWS: │

│ ═══════════════════ │

│ LDN → 3:00-5:00 AM ET (European flow) │

│ NY → 9:30-11:30 AM ET (US opening drive) │

│ PWR → 3:00-4:00 PM ET (End-of-day rebalancing) │

│ │

│ Expected Trades: 1-2 LDN | 2-3 NY | 1-2 PWR = 4-7 total │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ 📊 CONFLUENCE SCORING (MAX 10 POINTS): │

│ ═══════════════════════════════════════ │

│ Tier Signal: S=3, A=2, B=1 points │

│ In Active Zone: +2 points │

│ POC Aligned: +1 point (POC at body extreme) │

│ Imbalance Support:+1 point (supporting IMB nearby) │

│ Strong Volume: +1 point (2x+ average) │

│ Strong Delta: +1 point (70%+ dominance) │

│ CVD Momentum: +1 point (CVD trending with signal) │

│ │

│ MINIMUM SCORE: 5/10 to show signal (adjustable) │

│ IDEAL SCORE: 7+/10 for highest probability │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ 🚨 SIGNAL TYPES: │

│ ═════════════════ │

│ S🎯 / A🎯 / B🎯 → GRA Tier Signals (Full confluence) │

│ Z🎯 → Zone Entry (At DFZ zone + delta + volume) │

│ SP → Single Print (Institutional impulse) │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ ✓ ENTRY CHECKLIST: │

│ ═══════════════════ │

│ □ Signal appears (check Score ≥5) │

│ □ Session active (LDN!/NY!/PWR!) │

│ □ Table: Vol GREEN, Delta colored, Body GREEN │

│ □ CVD arrow (▲/▼) matches direction │

│ □ Note stop/target lines on chart │

│ □ Check Zone status (bonus if IN ZONE) │

│ □ Execute at signal candle close │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ 🎯 POSITION SIZING BY TIER: │

│ ═══════════════════════════ │

│ S-TIER (50+ pts): Full size, hold 2-5 min, target 2.5:1 R:R │

│ A-TIER (25-49): 75% size, hold 1-3 min, target 2.0:1 R:R │

│ B-TIER (12-24): 50% size, hold 30-90 sec, target 1.5:1 R:R │

│ │

├─────────────────────────────────────────────────────────────────────────────┤

│ │

│ ⛔ DO NOT TRADE WHEN: │

│ ════════════════════ │

│ ✗ Session shows "---" │

│ ✗ Score < 5/10 │

│ ✗ Vol shows RED (<1.8x) │

│ ✗ Delta < 62% │

│ ✗ Multiple conflicting signals │

│ ✗ Just before major news (FOMC, NFP, etc.) │

│ │

└─────────────────────────────────────────────────────────────────────────────┘

```

---

## 📋 WHY YM? LEVERAGING LOW VOLATILITY

### The YM Advantage

Most traders avoid YM because "it doesn't move enough." This is precisely why it's perfect for precision scalping:

| Factor | NQ | YM | Advantage |

|--------|----|----|-----------|

| **Daily Range** | 300-600 pts | 150-400 pts | More predictable moves |

| **Tick Value** | $5/tick (4 ticks/pt) | $5/tick (1 tick/pt) | Simpler math |

| **Retail Noise** | High | Low | Cleaner signals |

| **Whipsaws** | Frequent | Rare | Fewer fakeouts |

| **Trend Persistence** | Short | Long | Easier holds |

| **Fill Quality** | Variable | Consistent | Better execution |

### Why 3-7 Trades is the Sweet Spot

```

YM SESSION BREAKDOWN:

════════════════════

LONDON (3-5 AM ET): 1-2 trades

├── Why: European institutions positioning for US open

├── Character: Slow build-up, clean trends

└── Best signals: Zone entries + A/B tier

NY OPEN (9:30-11:30 AM ET): 2-3 trades

├── Why: Highest volume, most institutional activity

├── Character: Initial balance formation, breakouts

└── Best signals: S/A tier, zone confluence

POWER HOUR (3-4 PM ET): 1-2 trades

├── Why: End-of-day rebalancing, MOC orders

├── Character: Mean reversion or trend acceleration

└── Best signals: Zone entries, B tier quick scalps

TOTAL: 4-7 high-quality setups per day

```

---

## 🔧 YM-SPECIFIC OPTIMIZATIONS

This unified indicator has been specifically tuned for YM's characteristics:

### Tier Thresholds

| Tier | NQ (Original) | YM (Optimized) | Rationale |

|------|---------------|----------------|-----------|

| S-Tier | 100 pts | **50 pts** | YM's daily range is ~50% of NQ |

| A-Tier | 50 pts | **25 pts** | Proportional scaling |

| B-Tier | 20 pts | **12 pts** | Still 5%+ of typical daily range |

### Filter Adjustments

| Filter | NQ Value | YM Value | Why |

|--------|----------|----------|-----|

| Volume Ratio | 1.5x | **1.8x** | Higher bar = less retail noise |

| Delta Threshold | 60% | **62%** | Tighter for cleaner signals |

| Body Ratio | 70% | **72%** | More conviction required |

| Range Multiplier | 1.3x | **1.4x** | Bigger move = real signal |

| Gap ATR% | 30% | **25%** | Smaller gaps still significant |

| Zone Age | 50 bars | **75 bars** | Zones last longer in slow market |

### Why These Changes Work

1. **Higher Volume Bar**: YM has more institutional flow. Requiring 1.8x volume ensures we're catching real moves, not retail chop.

2. **Tighter Delta**: With less noise, we can demand clearer buyer/seller dominance before entering.

3. **Longer Zone Life**: YM trends persist longer. A zone that would be stale in NQ is still viable in YM.

4. **Smaller Gap Threshold**: YM gaps are naturally smaller. 25% of ATR in YM is significant institutional activity.

---

## 📊 CONFLUENCE SCORING SYSTEM

The unified indicator uses a 10-point confluence scoring system to filter for only the highest-probability setups:

### Score Breakdown

```

CONFLUENCE SCORE CALCULATION:

═════════════════════════════

BASE POINTS (Tier):

├── S-Tier signal: +3 points

├── A-Tier signal: +2 points

└── B-Tier signal: +1 point

BONUS POINTS:

├── Inside Active Zone (DFZ): +2 points

│ └── Price within bull/bear zone = institutional level

│

├── POC Alignment: +1 point

│ └── POC at body extreme = strong conviction

│

├── Imbalance Support: +1 point

│ └── Supporting imbalance within 1 ATR

│

├── Strong Volume (2x+): +1 point

│ └── Exceptional institutional participation

│

├── Strong Delta (70%+): +1 point

│ └── Clear one-sided aggression

│

└── CVD Momentum: +1 point

└── CVD trending with signal direction

MAXIMUM POSSIBLE: 10 points

```

### Score Interpretation

| Score | Quality | Action | Expected Win Rate |

|-------|---------|--------|-------------------|

| 8-10 | 🥇 Elite | Full size, hold for target | 75-80% |

| 6-7 | 🥈 Strong | Standard size, manage actively | 65-70% |

| 5 | 🥉 Valid | Reduced size, quick scalp | 55-60% |

| <5 | ⚫ Filtered | No signal shown | N/A |

### Adjusting Minimum Score

- **Conservative (Score ≥6)**: Fewer trades, higher win rate

- **Standard (Score ≥5)**: Balanced approach, 3-7 trades/day

- **Aggressive (Score ≥4)**: More trades, requires active management

---

## 📐 SIGNAL TYPES EXPLAINED

### 1. GRA Tier Signals (S🎯, A🎯, B🎯)

These are the primary signals from the merged GRA system:

```

TIER SIGNAL REQUIREMENTS:

═══════════════════════════

ALL must be TRUE:

├── ✓ Point movement meets tier threshold

├── ✓ Volume ≥ 1.8x average

├── ✓ Delta ≥ 62% (buy or sell dominance)

├── ✓ Body ≥ 72% of candle range

├── ✓ Range ≥ 1.4x average

├── ✓ Small opposite wick (<50% of body)

├── ✓ CVD confirms direction (if enabled)

├── ✓ Active session (LDN/NY/PWR)

└── ✓ Confluence Score ≥ minimum (default 5)

```

### 2. Zone Entry Signals (Z🎯)

When price enters a DeepFlow zone with confirmation:

```

ZONE ENTRY REQUIREMENTS:

═══════════════════════════

ALL must be TRUE:

├── ✓ Price inside fresh/tested zone (not broken)

├── ✓ Delta ≥ 62% in zone direction

├── ✓ Volume ≥ 1.5x average

└── ✓ Active session

NOTE: Z🎯 only appears when NOT already showing tier signal

(prevents duplicate signals on same candle)

```

### 3. Single Print Markers (SP)

Mark institutional impulse candles for future S/R:

```

SINGLE PRINT REQUIREMENTS:

═══════════════════════════

ALL must be TRUE:

├── ✓ Range ≥ 1.6x average

├── ✓ Body ≥ 72% of range

├── ✓ Volume ≥ 1.8x average

├── ✓ Delta ≥ 62% confirms direction

└── ✓ Active session

USE: Horizontal lines at high/low act as future S/R

```

---

## 🎯 TRADING STRATEGIES

### Strategy 1: Zone + Tier Confluence (Highest Probability)

```

THE ULTIMATE YM SETUP:

═══════════════════════

Setup:

1. Active DeepFlow zone exists (green box below for long)

2. Price pulls back INTO the zone

3. Tier signal fires INSIDE the zone (S🎯/A🎯)

4. Score shows 7+/10

Entry: Signal candle close

Stop: Below zone bottom (for longs)

Target: Based on tier (1.5-2.5:1 R:R)

Why It Works:

• Zone = institutional limit orders

• Tier signal = momentum confirmation

• Double confirmation = high probability

Expected Win Rate: 70-75%

```

### Strategy 2: Pure Tier Signal with POC Stop

```

SNIPER TIER TRADE:

══════════════════

Setup:

1. Tier signal appears (preferably A or S)

2. Score ≥ 5/10

3. Note POC level on signal candle

4. Red/green stop/target lines appear

Entry: Signal candle close

Stop: Beyond POC (shown on chart)

Target: Auto-calculated based on tier

Key: POC placement matters

• POC near candle bottom (longs) = STRONG

• POC in middle = weaker signal

• POC at extreme = possible exhaustion

Expected Win Rate: 60-65%

```

### Strategy 3: Zone Bounce (Continuation)

```

ZONE BOUNCE TRADE:

══════════════════

Setup:

1. Fresh zone created during session

2. Price leaves zone, moves in zone direction

3. Price returns to test zone (within 15 bars)

4. Z🎯 signal appears or rejection candle forms

Entry: At CE line (middle of zone)

Stop: Beyond zone edge

Target: Previous swing high/low

Why It Works:

• Zones represent unfilled orders

• First retest often finds support/resistance

• Lower volatility = cleaner bounces

Expected Win Rate: 55-60%

```

### Strategy 4: Single Print Scalp

```

SINGLE PRINT SCALP:

═══════════════════

Setup:

1. Single Print (SP) marker appears

2. Note the gold/purple lines at high/low

3. Wait for price to return to SP level

4. Look for rejection or tier signal at level

Entry: At SP line with confirmation

Stop: Beyond the SP line

Target: Quick 1:1 or to next structure

Why It Works:

• SP = price moved too fast, orders unfilled

• Price often returns to "fill" these levels

• YM's slower pace makes retests likely

Expected Win Rate: 55-60%

```

---

## 📊 TABLE LEGEND

| Field | Reading | Color Meaning |

|-------|---------|---------------|

| **Pts** | Current candle points | Gold/Green/Yellow = Tiered |

| **Tier** | S/A/B/X | Tier color or white |

| **Vol** | Volume ratio | 🟢 ≥1.8x, 🔴 <1.8x |

| **Delta** | Buy/Sell % | 🟢 Buy dom, 🔴 Sell dom |

| **Body** | Body % of range | 🟢 ≥72%, 🔴 <72% |

| **CVD** | Trend direction | ▲ Bullish, ▼ Bearish |

| **Sess** | Active session | 🟡 LDN!/NY!/PWR!, ⚫ --- |

| **POC** | Point of Control | 🟡 Gold price level |

| **Zone** | Zone position | 🟢 BUY⬚, 🔴 SELL⬚, ⚫ --- |

| **Zones** | Active zone count | #B/#S format |

| **Score** | Confluence score | 🟢 7+, 🟡 5-6, ⚫ <5 |

| **IMB** | Recent imbalances | Count in last 10 bars |

| **R:R** | Risk/Reward | 🟢 On signal, ⚫ No signal |

---

## ⏰ SESSION-SPECIFIC PLAYBOOKS

### London Session (3:00-5:00 AM ET)

```

CHARACTER: Slow, methodical, trend-building

VOLUME: Medium (50-70% of NY)

BEST SETUPS: Zone entries, A/B tier with zones

PLAYBOOK:

• Enter on zone retests

• Expect 15-25 pt moves

• Don't fight early direction

• Watch for pre-NY positioning

TYPICAL TRADES: 1-2

```

### NY Open (9:30-11:30 AM ET)

```

CHARACTER: Fast, volatile, high-conviction

VOLUME: Highest of day

BEST SETUPS: S/A tier, zone confluence

PLAYBOOK:

• First 15 min: Observe Initial Balance

• 9:45-10:15: Best setups form

• S-tier signals = ride the wave

• Be aggressive on high scores

TYPICAL TRADES: 2-3

```

### Power Hour (3:00-4:00 PM ET)

```

CHARACTER: Rebalancing, MOC orders

VOLUME: Medium-high (70-80% of NY)

BEST SETUPS: B tier scalps, zone entries

PLAYBOOK:

• Watch for mean reversion setups

• Quick scalps around POC levels

• Don't hold through close

• Take profits at 1:1 R:R

TYPICAL TRADES: 1-2

```

---

## 🔧 RECOMMENDED SETTINGS

### Conservative (Fewer, Better Trades)

| Setting | Value | Notes |

|---------|-------|-------|

| Min Confluence Score | 6 | Only strong setups |

| Min Volume Ratio | 2.0 | Higher bar |

| Delta Threshold | 65% | Stricter dominance |

| Max Zones | 8 | Less clutter |

### Standard (Balanced)

| Setting | Value | Notes |

|---------|-------|-------|

| Min Confluence Score | 5 | Default |

| Min Volume Ratio | 1.8 | Default |

| Delta Threshold | 62% | Default |

| Max Zones | 12 | Default |

### Aggressive (More Opportunities)

| Setting | Value | Notes |

|---------|-------|-------|

| Min Confluence Score | 4 | More signals |

| Min Volume Ratio | 1.5 | Lower bar |

| Delta Threshold | 60% | Looser |

| Max Zones | 15 | More context |

---

## 🚨 ALERT SETUP

Configure these alerts in TradingView:

| Alert | Priority | Action |

|-------|----------|--------|

| 🎯 YM S-TIER LONG/SHORT | 🔴 CRITICAL | Drop everything, check immediately |

| 🎯 YM A-TIER LONG/SHORT | 🟠 HIGH | Evaluate within 15 seconds |

| 🎯 YM B-TIER LONG/SHORT | 🟡 MEDIUM | Check if available |

| 🎯 YM ZONE BUY/SELL | 🟢 STANDARD | Good context entry |

| 📦 NEW ZONE | 🔵 INFO | Mark on mental map |

| ⭐ SINGLE PRINT | 🔵 INFO | Note for future S/R |

| SESSION OPEN | ⚪ INFO | Prepare to trade |

### Alert Message Format

```

🎯 YM A-LONG | YM1! @ 42,150 | 68%B | Score: 7/10 | IN ZONE | POC: 42,125 | Stop: 42,098 | SWING

```

---

## ⚠️ COMMON MISTAKES TO AVOID

| Mistake | Why It's Bad | Solution |

|---------|-------------|----------|

| Trading outside sessions | Low volume = noise | Wait for LDN/NY/PWR |

| Ignoring score | Low scores = low probability | Require ≥5/10 |

| Fighting the zone | Zones are institutional | Trade WITH zones |

| Oversizing B-tier | Quick scalps, not holds | 50% size max |

| Holding through news | Volatility spike | Exit before FOMC, NFP |

| Chasing after signal | Entry on close only | Miss it = wait for next |

| Ignoring POC position | Middle POC = indecision | Strong = extreme POC |

---

## 📈 DAILY TRADE JOURNAL TEMPLATE

```

DATE: ___________

SESSION: □ LDN □ NY □ PWR

TRADE 1:

├── Time: _______

├── Signal: S🎯 / A🎯 / B🎯 / Z🎯

├── Score: ___/10

├── Entry: _______

├── Stop: _______

├── Target: _______

├── In Zone: □ Yes □ No

├── Result: +/- ___ pts ($_____)

└── Notes: _______________________

TRADE 2:

DAILY SUMMARY:

├── Total Trades: ___

├── Win Rate: ___%

├── Net P/L: $_____

├── Best Setup: _______

└── Improvement: _______________________

```

---

## 🏆 GOLDEN RULES FOR YM

> **"YM rewards patience. Wait for the confluence—it's worth it."**

> **"Low volatility means you can size up. One good trade beats five forced trades."**

> **"Score 7+ is your edge. Anything less is gambling."**

> **"The zone + tier combo is your bread and butter. Master it."**

> **"Leave every trade with money. YM gives you time to manage."**

---

## 📊 VISUAL GUIDE

```

PERFECT YM SNIPER SETUP:

═══════════════════════════════════════════════════════════════════

│ Current Price

│

┌─────────────────────────┴────────────────────────────┐

│ BEARISH ZONE (Red) │

│- - - - - - - CE Line (Entry for shorts) - - - - - - │

│ │

└──────────────────────────────────────────────────────┘

│

══════════════════╪══════════════════ SP High (Purple)

│

┌─────────────────────┤

│█████████████████████│ ← A🎯 LONG Signal

│█████████████████████│ Score: 8/10

│ ●──────────────────│ ← POC (Gold) near bottom = STRONG

│█████████████████████│

│█████████████████████│

└─────────────────────┤

│

══════════════════╪══════════════════ SP Low (Purple)

│

┌─────────────────────────┴────────────────────────────┐

│ BULLISH ZONE (Green) │

│- - - - - - - CE Line (Entry for longs) - - - - - - -│

│██████████████████████████████████████████████████████│

└──────────────────────────────────────────────────────┘

│

Stop Loss

CONFLUENCE CHECK:

✓ A-Tier signal (+2)

✓ At edge of bullish zone (+2)

✓ POC at bottom of candle (+1)

✓ Strong volume 2.3x (+1)

✓ Delta 72% buyers (+1)

✓ CVD bullish (+1)

TOTAL: 8/10 = ELITE SETUP

ACTION: Full size LONG at signal candle close

STOP: Below zone bottom

TARGET: 2:1 R:R (auto-calculated)

```

---

## 🔧 TROUBLESHOOTING

| Issue | Cause | Fix |

|-------|-------|-----|

| No signals appearing | Score too high | Lower min score to 4-5 |

| Too many signals | Score too low | Raise min score to 6+ |

| Zones cluttering chart | Max zones high | Reduce to 8-10 |

| POC not showing | Tiered filter on | Check "POC Only Tiered" |

| Session not highlighting | Wrong timezone | Verify timezone setting |

| Alerts not firing | Not configured | Set up in TradingView alerts |

---

## 📝 PINE SCRIPT V6 TECHNICAL NOTES

This indicator uses advanced features:

- **User Defined Types (UDT)**: Clean state management for zones/imbalances

- **`request.security_lower_tf()`**: Intrabar volume analysis

- **Dynamic Array Management**: Efficient memory for drawings

- **Confluence Scoring Engine**: Multi-factor signal qualification

- **Auto Stop/Target**: Dynamic risk management calculation

**Minimum TradingView Plan:** Pro (for intrabar data access)

---

*© Alexandro Disla - YM Ultimate SNIPER*

*Pine Script v6 | TradingView*

*Unified GRA v5 + DeepFlow Zones | YM-Optimized*

Gamma Levels w/AlertsPlots Gamma Levels for identifying Market Positioning. Has alert function on the specific levels.

---To apply to different tickers You Must:

1. apply to chart layout

2. input ticker specific levels

3. Save as an INDICATOR TEMPLATE titled same as ticker (check the remember symbol box)

Now when switching to different tickers, simply open that template

Volatility-Targeted Momentum Portfolio [BackQuant]Volatility-Targeted Momentum Portfolio

A complete momentum portfolio engine that ranks assets, targets a user-defined volatility, builds long, short, or delta-neutral books, and reports performance with metrics, attribution, Monte Carlo scenarios, allocation pie, and efficiency scatter plots. This description explains the theory and the mechanics so you can configure, validate, and deploy it with intent.

Table of contents

What the script does at a glance

Momentum, what it is, how to know if it is present

Volatility targeting, why and how it is done here

Portfolio construction modes: Long Only, Short Only, Delta Neutral

Regime filter and when the strategy goes to cash

Transaction cost modelling in this script

Backtest metrics and definitions

Performance attribution chart

Monte Carlo simulation

Scatter plot analysis modes

Asset allocation pie chart

Inputs, presets, and deployment checklist

Suggested workflow

1) What the script does at a glance

Pulls a list of up to 15 tickers, computes a simple momentum score on each over a configurable lookback, then volatility-scales their bar-to-bar return stream to a target annualized volatility.

Ranks assets by raw momentum, selects the top 3 and bottom 3, builds positions according to the chosen mode, and gates exposure with a fast regime filter.

Accumulates a portfolio equity curve with risk and performance metrics, optional benchmark buy-and-hold for comparison, and a full alert suite.

Adds visual diagnostics: performance attribution bars, Monte Carlo forward paths, an allocation pie, and scatter plots for risk-return and factor views.

2) Momentum: definition, detection, and validation

Momentum is the tendency of assets that have performed well to continue to perform well, and of underperformers to continue underperforming, over a specific horizon. You operationalize it by selecting a horizon, defining a signal, ranking assets, and trading the leaders versus laggards subject to risk constraints.

Signal choices . Common signals include cumulative return over a lookback window, regression slope on log-price, or normalized rate-of-change. This script uses cumulative return over lookback bars for ranking (variable cr = price/price - 1). It keeps the ranking simple and lets volatility targeting handle risk normalization.

How to know momentum is present .

Leaders and laggards persist across adjacent windows rather than flipping every bar.

Spread between average momentum of leaders and laggards is materially positive in sample.

Cross-sectional dispersion is non-trivial. If everything is flat or highly correlated with no separation, momentum selection will be weak.

Your validation should include a diagnostic that measures whether returns are explained by a momentum regression on the timeseries.

Recommended diagnostic tool . Before running any momentum portfolio, verify that a timeseries exhibits stable directional drift. Use this indicator as a pre-check: It fits a regression to price, exposes slope and goodness-of-fit style context, and helps confirm if there is usable momentum before you force a ranking into a flat regime.

3) Volatility targeting: purpose and implementation here

Purpose . Volatility targeting seeks a more stable risk footprint. High-vol assets get sized down, low-vol assets get sized up, so each contributes more evenly to total risk.

Computation in this script (per asset, rolling):

Return series ret = log(price/price ).

Annualized volatility estimate vol = stdev(ret, lookback) * sqrt(tradingdays).

Leverage multiplier volMult = clamp(targetVol / vol, 0.1, 5.0).

This caps sizing so extremely low-vol assets don’t explode weight and extremely high-vol assets don’t go to zero.

Scaled return stream sr = ret * volMult. This is the per-bar, risk-adjusted building block used in the portfolio combinations.

Interpretation . You are not levering your account on the exchange, you are rescaling the contribution each asset’s daily move has on the modeled equity. In live trading you would reflect this with position sizing or notional exposure.

4) Portfolio construction modes

Cross-sectional ranking . Assets are sorted by cr over the chosen lookback. Top and bottom indices are extracted without ties.

Long Only . Averages the volatility-scaled returns of the top 3 assets: avgRet = mean(sr_top1, sr_top2, sr_top3). Position table shows per-asset leverages and weights proportional to their current volMult.

Short Only . Averages the negative of the volatility-scaled returns of the bottom 3: avgRet = mean(-sr_bot1, -sr_bot2, -sr_bot3). Position table shows short legs.

Delta Neutral . Long the top 3 and short the bottom 3 in equal book sizes. Each side is sized to 50 percent notional internally, with weights within each side proportional to volMult. The return stream mixes the two sides: avgRet = mean(sr_top1,sr_top2,sr_top3, -sr_bot1,-sr_bot2,-sr_bot3).

Notes .

The selection metric is raw momentum, the execution stream is volatility-scaled returns. This separation is deliberate. It avoids letting volatility dominate ranking while still enforcing risk parity at the return contribution stage.

If everything rallies together and dispersion collapses, Long Only may behave like a single beta. Delta Neutral is designed to extract cross-sectional momentum with low net beta.

5) Regime filter

A fast EMA(12) vs EMA(21) filter gates exposure.

Long Only active when EMA12 > EMA21. Otherwise the book is set to cash.

Short Only active when EMA12 < EMA21. Otherwise cash.

Delta Neutral is always active.

This prevents taking long momentum entries during obvious local downtrends and vice versa for shorts. When the filter is false, equity is held flat for that bar.

6) Transaction cost modelling

There are two cost touchpoints in the script.

Per-bar drag . When the regime filter is active, the per-bar return is reduced by fee_rate * avgRet inside netRet = avgRet - (fee_rate * avgRet). This models proportional friction relative to traded impact on that bar.

Turnover-linked fee . The script tracks changes in membership of the top and bottom baskets (top1..top3, bot1..bot3). The intent is to charge fees when composition changes. The template counts changes and scales a fee by change count divided by 6 for the six slots.

Use case: increase fee_rate to reflect taker fees and slippage if you rebalance every bar or trade illiquid assets. Reduce it if you rebalance less often or use maker orders.

Practical advice .

If you rebalance daily, start with 5–20 bps round-trip per switch on liquid futures and adjust per venue.

For crypto perp microcaps, stress higher cost assumptions and add slippage buffers.

If you only rotate on lookback boundaries or at signals, use alert-driven rebalances and lower per-bar drag.

7) Backtest metrics and definitions

The script computes a standard set of portfolio statistics once the start date is reached.

Net Profit percent over the full test.

Max Drawdown percent, tracked from running peaks.

Annualized Mean and Stdev using the chosen trading day count.

Variance is the square of annualized stdev.

Sharpe uses daily mean adjusted by risk-free rate and annualized.

Sortino uses downside stdev only.

Omega ratio of sum of gains to sum of losses.

Gain-to-Pain total gains divided by total losses absolute.

CAGR compounded annual growth from start date to now.

Alpha, Beta versus a user-selected benchmark. Beta from covariance of daily returns, Alpha from CAPM.

Skewness of daily returns.

VaR 95 linear-interpolated 5th percentile of daily returns.

CVaR average of the worst 5 percent of daily returns.

Benchmark Buy-and-Hold equity path for comparison.

8) Performance attribution

Cumulative contribution per asset, adjusted for whether it was held long or short and for its volatility multiplier, aggregated across the backtest. You can filter to winners only or show both sides. The panel is sorted by contribution and includes percent labels.

9) Monte Carlo simulation

The panel draws forward equity paths from either a Normal model parameterized by recent mean and stdev, or non-parametric bootstrap of recent daily returns. You control the sample length, number of simulations, forecast horizon, visibility of individual paths, confidence bands, and a reproducible seed.

Normal uses Box-Muller with your seed. Good for quick, smooth envelopes.

Bootstrap resamples realized returns, preserving fat tails and volatility clustering better than a Gaussian assumption.

Bands show 10th, 25th, 75th, 90th percentiles and the path mean.

10) Scatter plot analysis

Four point-cloud modes, each plotting all assets and a star for the current portfolio position, with quadrant guides and labels.

Risk-Return Efficiency . X is risk proxy from leverage, Y is expected return from annualized momentum. The star shows the current book’s composite.

Momentum vs Volatility . Visualizes whether leaders are also high vol, a cue for turnover and cost expectations.

Beta vs Alpha . X is a beta proxy, Y is risk-adjusted excess return proxy. Useful to see if leaders are just beta.

Leverage vs Momentum . X is volMult, Y is momentum. Shows how volatility targeting is redistributing risk.

11) Asset allocation pie chart

Builds a wheel of current allocations.

Long Only, weights are proportional to each long asset’s current volMult and sum to 100 percent.

Short Only, weights show the short book as positive slices that sum to 100 percent.

Delta Neutral, 50 percent long and 50 percent short books, each side leverage-proportional.

Labels can show asset, percent, and current leverage.

12) Inputs and quick presets

Core

Portfolio Strategy . Long Only, Short Only, Delta Neutral.

Initial Capital . For equity scaling in the panel.

Trading Days/Year . 252 for stocks, 365 for crypto.

Target Volatility . Annualized, drives volMult.

Transaction Fees . Per-bar drag and composition change penalty, see the modelling notes above.

Momentum Lookback . Ranking horizon. Shorter is more reactive, longer is steadier.

Start Date . Ensure every symbol has data back to this date to avoid bias.

Benchmark . Used for alpha, beta, and B&H line.

Diagnostics

Metrics, Equity, B&H, Curve labels, Daily return line, Rolling drawdown fill.

Attribution panel. Toggle winners only to focus on what matters.

Monte Carlo mode with Normal or Bootstrap and confidence bands.

Scatter plot type and styling, labels, and portfolio star.

Pie chart and labels for current allocation.

Presets

Crypto Daily, Long Only . Lookback 25, Target Vol 50 percent, Fees 10 bps, Regime filter on, Metrics and Drawdown on. Monte Carlo Bootstrap with Recent 200 bars for bands.

Crypto Daily, Delta Neutral . Lookback 25, Target Vol 50 percent, Fees 15–25 bps, Regime filter always active for this mode. Use Scatter Risk-Return to monitor efficiency and keep the star near upper left quadrants without drifting rightward.

Equities Daily, Long Only . Lookback 60–120, Target Vol 15–20 percent, Fees 5–10 bps, Regime filter on. Use Benchmark SPX and watch Alpha and Beta to keep the book from becoming index beta.

13) Suggested workflow

Universe sanity check . Pick liquid tickers with stable data. Thin assets distort vol estimates and fees.

Check momentum existence . Run on your timeframe. If slope and fit are weak, widen lookback or avoid that asset or timeframe.

Set risk budget . Choose a target volatility that matches your drawdown tolerance. Higher target increases turnover and cost sensitivity.

Pick mode . Long Only for bull regimes, Short Only for sustained downtrends, Delta Neutral for cross-sectional harvesting when index direction is unclear.

Tune lookback . If leaders rotate too often, lengthen it. If entries lag, shorten it.

Validate cost assumptions . Increase fee_rate and stress Monte Carlo. If the edge vanishes with modest friction, refine selection or lengthen rebalance cadence.

Run attribution . Confirm the strategy’s winners align with intuition and not one unstable outlier.

Use alerts . Enable position change, drawdown, volatility breach, regime, momentum shift, and crash alerts to supervise live runs.

Important implementation details mapped to code

Momentum measure . cr = price / price - 1 per symbol for ranking. Simplicity helps avoid overfitting.

Volatility targeting . vol = stdev(log returns, lookback) * sqrt(tradingdays), volMult = clamp(targetVol / vol, 0.1, 5), sr = ret * volMult.

Selection . Extract indices for top1..top3 and bot1..bot3. The arrays rets, scRets, lev_vals, and ticks_arr track momentum, scaled returns, leverage multipliers, and display tickers respectively.

Regime filter . EMA12 vs EMA21 switch determines if the strategy takes risk for Long or Short modes. Delta Neutral ignores the gate.

Equity update . Equity multiplies by 1 + netRet only when the regime was active in the prior bar. Buy-and-hold benchmark is computed separately for comparison.

Tables . Position tables show current top or bottom assets with leverage and weights. Metric table prints all risk and performance figures.

Visualization panels . Attribution, Monte Carlo, scatter, and pie use the last bars to draw overlays that update as the backtest proceeds.

Final notes

Momentum is a portfolio effect. The edge comes from cross-sectional dispersion, adequate risk normalization, and disciplined turnover control, not from a single best asset call.

Volatility targeting stabilizes path but does not fix selection. Use the momentum regression link above to confirm structure exists before you size into it.

Always test higher lag costs and slippage, then recheck metrics, attribution, and Monte Carlo envelopes. If the edge persists under stress, you have something robust.

RSI ExtremesRSI Extremes — Educational Indicator (Pine v5)

Per-Tick Dual-RSI Extremes · Real-Time Visualization · Cooldown Logic

Overview

RSI Extremes is a real-time educational indicator built to show where the Relative Strength Index (RSI) reaches its most extreme levels during every tick of live price action.

Instead of using only the candle close, it continuously tracks both RSI(low) and RSI(high) to reveal how deeply each bar stretches into demand or supply extremes.

This tool is meant solely for study and visualization, helping you understand how RSI behaves intrabar when price wicks expand. It produces no signals, no alerts, and no trade suggestions — it’s a microscope for momentum pressure.

Core Idea

Standard RSI hides a lot of the wick-based stress in price because it calculates from close values only.

RSI Extremes solves this by splitting the measurement into two perspectives:

RSI of LOW (green) → shows how far momentum falls into potential demand exhaustion.

RSI of HIGH (red) → shows how far momentum extends into potential supply exhaustion.

Seeing both together exposes the full oscillation envelope — what RSI looks like between candle opens and closes, not just after the fact.

What Gets Plotted

RSI (Low) — green line representing intrabar downside pressure.

RSI (High) — red line representing intrabar upside pressure.

RSI Ghost (Smoothed) — gray line for soft context only.

Bands: 30 / 50 / 70 visual guides with a shaded 30–70 region.

Markers:

Enter marker when RSI(low) ≤ levelEnter (default 15).

Exit marker when RSI(high) ≥ levelExit (default 85).

Markers appear in real time as soon as a touch occurs and are locked per bar to avoid duplicates.

Inputs & Educational Purpose

Input Description Learning Focus

Source (for ghost smoother) Data used for the ghost RSI. Observe RSI smoothing lag.

RSI Length Period for both RSI(high) and RSI(low). Shorter = faster reaction; longer = smoother.

RSI-based MA Length (ghost) Smoothing for the ghost line. Compare sharp vs smoothed RSI rhythm.

levelEnter (touch or below) Default 15. Study how deep RSI(low) falls during market stress.

levelExit (touch or above) Default 85. Study how high RSI(high) rises during momentum bursts.

Rest period (bars) Cooldown after any event. Encourages post-event observation and prevents overlap.

Real-Time Behavior

Evaluates conditions per tick, not only at bar close.

Uses both real-time detection and bar-close backup for reliability.

Employs per-bar locks to prevent duplicate markers.

Integrates a cooldown so new markers only appear after the rest period.

The result is a clean, stable display of RSI stress points in live price motion — no flicker, no repaint.

How to Study with RSI Extremes

Watch how Enter markers form during sharp sell wicks — these highlight where intrabar RSI(low) dives into extreme territory.

Watch how Exit markers appear during aggressive tops — these show when RSI(high) surges beyond its upper boundary.

Compare both lines to the gray ghost: if the ghost is rising while Enter markers print, you’re seeing a temporary overshoot within strengthening momentum; if it’s falling while Exit markers print, you’re seeing supply exhaustion in weakening momentum.

Use cooldown spacing to examine how long markets take to recover or consolidate after an extreme tick.

Educational Value

Learn how RSI behaves inside a candle rather than only at its close.

Visualize how volatility affects the amplitude of RSI swings.

Understand that extremes don’t mean reversal — they measure intensity, not direction.

Build intuition for momentum saturation and liquidity hunts.

This indicator turns RSI into a real-time stress monitor rather than a delayed oscillator.

Category & Tags

Category: Indicator → Momentum (or Indicator → Educational / Research)

Tags: indicator, rsi, momentum, extremes, enter-exit, levelenter, levelexit, realtime, educational, research, visualization, pine-v5

Disclaimer

This indicator is intended exclusively for educational and research purposes.

It does not issue trade signals or financial advice.

All market activity carries risk; use this tool to learn, not to predict or execute trades.

ICT First Presented FVG with Volume Imbalance [1st P. FVG + VI]The indicator identifies and highlights the first presented Fair Value Gap (FVG) occurringthe morning (09:30–10:00) and afternoon (13:30–14:00) session's first 30 minutes. It includes an optional feature to extend FVG zones when a volume imbalance (V.I.) is detected, providing additional context for areas of potential price inefficiency. This powerful combination helps traders identify significant market structure gaps that often act as support/resistance zones and potential price targets.

What is an FVG?

A Fair Value Gap, often abbreviated as FVG, is a price range on a chart where there is an inefficiency or imbalance in trading. This typically happens when price moves rapidly in one direction, leaving a gap between the wicks or bodies of three consecutive candles. For example, in a bullish move, if the low of the third candle is higher than the high of the first candle, the space between them is the FVG.

What is a Volume Imbalance?

A volume imbalance is a smaller, more precise inefficiency within price action, often visible as a "crack" or thin area in the price delivery. It represents a spot where the volume traded was not balanced between buyers and sellers, often seen as a thin wick or a gap between candle bodies.

FVG + Volume Imbalance:

When you have a fair value gap that contains a volume imbalance, it becomes a more significant area of interest. ICT teaches that you should not ignore a volume imbalance if it’s part of an FVG. In fact, you should use the volume imbalance in conjunction with the FVG to define your trading range more accurately

📊 Volume Imbalance Integration

Toggle Option: Enable/disable volume imbalance detection based on preference

Extended Boundaries: When enabled, FVG boundaries expand to include volume imbalance zones

Accurate Gap Sizing: Total gap calculation includes volume imbalance extensions

Multi-Scenario Support: Handles volume imbalances at start, end, or both sides of FVG formations

📈 Multiple Display Modes

Current Day: Shows only today's FVGs for clean chart analysis

Current Week: Displays all weekly FVGs for broader context

Forward Extension: Extends FVG boxes and CE, Upper/Lower Quadrant lines into the future

📊 Visualization

Bullish FVGs appear in semi-transparent blue or purple zones (depending on session).

Bearish FVGs appear in red or orange zones.

Optional dotted lines mark the CE (midpoint) of each FVG for additional reference.

Quadrant Division: Additional 25%/75% lines for large FVGs (configurable minimum gap size)

🎯 Smart Filtering

First Presentation Only: Only displays the initial FVG in each session, avoiding clutter

Minimum Gap Size: Configurable tick-based thresholds for AM and PM sessions

Core FVG Validation: Ensures only valid Fair Value Gaps are displayed

⚙️ Configuration Options

Display Settings

Show Mode: Current Day or Current Week view

Forward Extension: 1-500 bars projection

Day Labels: Toggle weekday labels in weekly mode

Text Color: Customizable label colors

Volume Imbalance Settings

Include Volume Imbalance: Master toggle for enhanced boundary calculation

Automatic Detection: Identifies imbalance scenarios without additional input

Session-Specific Settings

AM Session (09:30-10:00):

Enable/disable AM FVG detection

Customizable bullish/bearish colors

CE line visibility and coloring

Minimum gap size in ticks

PM Session (13:30-14:00):

Enable/disable PM FVG detection

Customizable bullish/bearish colors

CE line visibility and coloring

Minimum gap size in ticks

Quadrant Settings

Enable/Disable: Toggle quadrant line display

Minimum Gap: Tick threshold for quadrant activation

Line Style: Dotted, dashed, or solid

Color: Customizable quadrant line color

How It Works

FVG Boundary Calculation

Traditional FVG: High to Low (bullish) or Low to High (bearish)

Enhanced FVG: Extended boundaries to include volume imbalance zones when enabled

Total Gap Size: Calculated including any volume imbalance extensions

Volume Imbalance Detection

The indicator identifies volume imbalances by detecting bars where:

Bullish Imbalance: Current bar's body is completely above previous bar's body

Bearish Imbalance: Current bar's body is completely below previous bar's body

⚠️ Disclaimer

This script is a technical visualization tool only.

It does not provide financial advice, signals, or predictions. Always perform independent analysis and manage risk appropriately before making trading decisions.

Quantum Flux Universal Strategy Summary in one paragraph

Quantum Flux Universal is a regime switching strategy for stocks, ETFs, index futures, major FX pairs, and liquid crypto on intraday and swing timeframes. It helps you act only when the normalized core signal and its guide agree on direction. It is original because the engine fuses three adaptive drivers into the smoothing gains itself. Directional intensity is measured with binary entropy, path efficiency shapes trend quality, and a volatility squash preserves contrast. Add it to a clean chart, watch the polarity lane and background, and trade from positive or negative alignment. For conservative workflows use on bar close in the alert settings when you add alerts in a later version.

Scope and intent

• Markets. Large cap equities and ETFs. Index futures. Major FX pairs. Liquid crypto

• Timeframes. One minute to daily

• Default demo used in the publication. QQQ on one hour

• Purpose. Provide a robust and portable way to detect when momentum and confirmation align, while dampening chop and preserving turns

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique concept or fusion. The novelty sits in the gain map. Instead of gating separate indicators, the model mixes three drivers into the adaptive gains that power two one pole filters. Directional entropy measures how one sided recent movement has been. Kaufman style path efficiency scores how direct the path has been. A volatility squash stabilizes step size. The drivers are blended into the gains with visible inputs for strength, windows, and clamps.

• What failure mode it addresses. False starts in chop and whipsaw after fast spikes. Efficiency and the squash reduce over reaction in noise.

• Testability. Every component has an input. You can lengthen or shorten each window and change the normalization mode. The polarity plot and background provide a direct readout of state.

• Portable yardstick. The core is normalized with three options. Z score, percent rank mapped to a symmetric range, and MAD based Z score. Clamp bounds define the effective unit so context transfers across symbols.

Method overview in plain language

The strategy computes two smoothed tracks from the chart price source. The fast track and the slow track use gains that are not fixed. Each gain is modulated by three drivers. A driver for directional intensity, a driver for path efficiency, and a driver for volatility. The difference between the fast and the slow tracks forms the raw flux. A small phase assist reduces lag by subtracting a portion of the delayed value. The flux is then normalized. A guide line is an EMA of a small lead on the flux. When the flux and its guide are both above zero, the polarity is positive. When both are below zero, the polarity is negative. Polarity changes create the trade direction.

Base measures

• Return basis. The step is the change in the chosen price source. Its absolute value feeds the volatility estimate. Mean absolute step over the window gives a stable scale.

• Efficiency basis. The ratio of net move to the sum of absolute step over the window gives a value between zero and one. High values mean trend quality. Low values mean chop.

• Intensity basis. The fraction of up moves over the window plugs into binary entropy. Intensity is one minus entropy, which maps to zero in uncertainty and one in very one sided moves.

Components

• Directional Intensity. Measures how one sided recent bars have been. Smoothed with RMA. More intensity increases the gain and makes the fast and slow tracks react sooner.

• Path Efficiency. Measures the straightness of the price path. A gamma input shapes the curve so you can make trend quality count more or less. Higher efficiency lifts the gain in clean trends.

• Volatility Squash. Normalizes the absolute step with Z score then pushes it through an arctangent squash. This caps the effect of spikes so they do not dominate the response.

• Normalizer. Three modes. Z score for familiar units, percent rank for a robust monotone map to a symmetric range, and MAD based Z for outlier resistance.

• Guide Line. EMA of the flux with a small lead term that counteracts lag without heavy overshoot.

Fusion rule

• Weighted sum of the three drivers with fixed weights visible in the code comments. Intensity has fifty percent weight. Efficiency thirty percent. Volatility twenty percent.

• The blend power input scales the driver mix. Zero means fixed spans. One means full driver control.

• Minimum and maximum gain clamps bound the adaptive gain. This protects stability in quiet or violent regimes.

Signal rule

• Long suggestion appears when flux and guide are both above zero. That sets polarity to plus one.

• Short suggestion appears when flux and guide are both below zero. That sets polarity to minus one.

• When polarity flips from plus to minus, the strategy closes any long and enters a short.

• When flux crosses above the guide, the strategy closes any short.

What you will see on the chart

• White polarity plot around the zero line

• A dotted reference line at zero named Zen

• Green background tint for positive polarity and red background tint for negative polarity

• Strategy long and short markers placed by the TradingView engine at entry and at close conditions

• No table in this version to keep the visual clean and portable

Inputs with guidance

Setup

• Price source. Default ohlc4. Stable for noisy symbols.

• Fast span. Typical range 6 to 24. Raising it slows the fast track and can reduce churn. Lowering it makes entries more reactive.

• Slow span. Typical range 20 to 60. Raising it lengthens the baseline horizon. Lowering it brings the slow track closer to price.

Logic

• Guide span. Typical range 4 to 12. A small guide smooths without eating turns.

• Blend power. Typical range 0.25 to 0.85. Raising it lets the drivers modulate gains more. Lowering it pushes behavior toward fixed EMA style smoothing.

• Vol window. Typical range 20 to 80. Larger values calm the volatility driver. Smaller values adapt faster in intraday work.

• Efficiency window. Typical range 10 to 60. Larger values focus on smoother trends. Smaller values react faster but accept more noise.

• Efficiency gamma. Typical range 0.8 to 2.0. Above one increases contrast between clean trends and chop. Below one flattens the curve.

• Min alpha multiplier. Typical range 0.30 to 0.80. Lower values increase smoothing when the mix is weak.

• Max alpha multiplier. Typical range 1.2 to 3.0. Higher values shorten smoothing when the mix is strong.

• Normalization window. Typical range 100 to 300. Larger values reduce drift in the baseline.

• Normalization mode. Z score, percent rank, or MAD Z. Use MAD Z for outlier heavy symbols.

• Clamp level. Typical range 2.0 to 4.0. Lower clamps reduce the influence of extreme runs.

Filters

• Efficiency filter is implicit in the gain map. Raising efficiency gamma and the efficiency window increases the preference for clean trends.

• Micro versus macro relation is handled by the fast and slow spans. Increase separation for swing, reduce for scalping.

• Location filter is not included in v1.0. If you need distance gates from a reference such as VWAP or a moving mean, add them before publication of a new version.

Alerts

• This version does not include alertcondition lines to keep the core minimal. If you prefer alerts, add names Long Polarity Up, Short Polarity Down, Exit Short on Flux Cross Up in a later version and select on bar close for conservative workflows.

Strategy has been currently adapted for the QQQ asset with 30/60min timeframe.

For other assets may require new optimization

Properties visible in this publication

• Initial capital 25000

• Base currency Default

• Default order size method percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Honest limitations and failure modes

• Past results do not guarantee future outcomes

• Economic releases, circuit breakers, and thin books can break the assumptions behind intensity and efficiency

• Gap heavy symbols may benefit from the MAD Z normalization

• Very quiet regimes can reduce signal contrast. Use longer windows or higher guide span to stabilize context

• Session time is the exchange time of the chart

• If both stop and target can be hit in one bar, tie handling would matter. This strategy has no fixed stops or targets. It uses polarity flips for exits. If you add stops later, declare the preference

Open source reuse and credits

• None beyond public domain building blocks and Pine built ins such as EMA, SMA, standard deviation, RMA, and percent rank

• Method and fusion are original in construction and disclosure

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Strategy add on block

Strategy notice

Orders are simulated by the TradingView engine on standard candles. No request.security() calls are used.

Entries and exits

• Entry logic. Enter long when both the normalized flux and its guide line are above zero. Enter short when both are below zero

• Exit logic. When polarity flips from plus to minus, close any long and open a short. When the flux crosses above the guide line, close any short

• Risk model. No initial stop or target in v1.0. The model is a regime flipper. You can add a stop or trail in later versions if needed

• Tie handling. Not applicable in this version because there are no fixed stops or targets

Position sizing

• Percent of equity in the Properties panel. Five percent is the default for examples. Risk per trade should not exceed five to ten percent of equity. One to two percent is a common choice

Properties used on the published chart

• Initial capital 25000

• Base currency Default

• Default order size percent of equity with value 5

• Pyramiding 1

• Commission 0.05 percent

• Slippage 10 ticks

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Dataset and sample size

• Test window Jan 2, 2014 to Oct 16, 2025 on QQQ one hour

• Trade count in sample 324 on the example chart

Release notes template for future updates

Version 1.1.

• Add alertcondition lines for long, short, and exit short

• Add optional table with component readouts

• Add optional stop model with a distance unit expressed as ATR or a percent of price

Notes. Backward compatibility Yes. Inputs migrated Yes.

Untouched ExtremesWhat it is

Untouched Extremes plots horizontal levels at green-candle highs and red-candle lows. Each level is considered “untouched” (clean liquidity) until price revisits it; on the first valid touch the line auto-deletes, keeping only live targets on your chart.

How it works (logic)

Bar close event

If close > open, the script draws a line at that bar’s high and extends it to the right.

If close < open, it draws a line at that bar’s low and extends it to the right.

(Optional) Perfect/almost-dojis can be classified as green or red via settings.

Touch & removal

A green-high line is removed when any later bar’s high ≥ level (optionally within a tick tolerance).

A red-low line is removed when any later bar’s low ≤ level (optionally within a tick tolerance).

You can delay deletion by N bars to make the touch visible before the line disappears.

Housekeeping

Maximum active lines per side and line styling are user-configurable.

Why it’s useful

Untouched highs/lows often coincide with resting liquidity and incomplete price probes. Tracking them helps:

Define targets and magnets price may seek.

Frame mean-reversion rotations after a failed push.

Keep the chart clean: only levels that have not been traded are displayed.

How to use it (trading idea)

Confirmation rule: Treat the line as a level/zone. Price can pierce it; wait for a clear reversal candle pattern (e.g., pin bar, engulfing, strong momentum shift) at or immediately after the touch.

Directional play:

If a bullish reversal pattern forms at/around a red-low line, the working assumption is that price will move toward the first untouched upper line (nearest green-high line above). Many traders use that as the primary target.

Conversely, if a bearish reversal pattern forms at/around a green-high line, expect rotation toward the first untouched lower line.

Risk management: Stops typically go just beyond the level or beyond the pattern’s wick. Consider a fixed R:R (e.g., 1:2) and partials at intermediate levels.

Settings

Doji handling: Choose how to classify close ≈ open bars (Green / Red / Ignore). A small equality margin (ticks) helps with rounding on some symbols.

Touch tolerance (ticks): Counts near-misses as touches if desired.

Deletion delay (bars): Wait N bars after creation before a line becomes eligible for deletion.