(MVD) Meta-Volatility Divergence (DAFE) Meta-Volatility Divergence (MVD)

Reveal the Hidden Tension in Volatility.

The Meta-Volatility Divergence (MVD) indicator is a next-generation tool designed to expose the disagreement between multiple volatility measures—helping you spot when the market’s “volatility engines” are out of sync, and a regime shift or volatility event may be brewing.

What Makes MVD Unique?

Multi-Source Volatility Analysis:

Unlike traditional volatility indicators that rely on a single measure, MVD fuses four distinct volatility signals:

ATR (Average True Range): Captures the average range of price movement.

Stdev (Standard Deviation): Measures the dispersion of closing prices.

Range: The average difference between high and low.

VoVix: A proprietary “volatility of volatility” metric, quantifying the difference between fast and slow ATR, normalized by ATR’s own volatility.

Divergence Engine:

The core MVD line (yellow) represents the mean absolute deviation (MAD) of these volatility measures from their average. When the line is flat, all volatility measures are in agreement. When the line rises, it means the market’s volatility signals are diverging—often a precursor to regime shifts, volatility expansions, or hidden stress.

Dynamic Z-Score Normalization:

The MVD line is normalized as a Z-score, so you can easily spot when current divergence is rare or extreme compared to recent history.

Visual Clarity:

Yellow center line: Tracks the real-time divergence of volatility measures.

Green dashed thresholds: Mark the ±2.00 Z-score levels, highlighting when divergence is unusually high and action may be warranted.

Dashboard: Toggleable panel shows all key metrics (ATR, Stdev, VoVix, MVD Z) and your custom branding.

Compact Info Label : For mobile or minimalist users, a single-line summary keeps you informed without clutter.

What Makes The MVD line move?

- The MVD line rises when the included volatility measures (ATR, Stdev, Range, VoVix) are moving in different directions or at different magnitudes. For example, if ATR is rising but Stdev is falling, the line will move up, signaling disagreement.

- The line falls or flattens when all volatility measures are in sync, indicating a consensus in the market’s volatility regime.

- VoVix adds a unique dimension, making the indicator especially sensitive to sudden changes in volatility structure that most tools miss.

Inputs & Settings

ATR Length: Sets the lookback for ATR calculation. Shorter = more sensitive, longer = smoother.

Stdev Length: Sets the lookback for standard deviation. Adjust for your asset’s volatility.

Range Length: Sets the lookback for the average high-low range.

MVD Lookback: Controls the window for Z-score normalization. Higher values = more historical context, lower = more responsive.

Show Dashboard: Toggle the full dashboard panel on/off.

Show Compact Info Label: Toggle the mobile-friendly info line on/off.

Tip:

Adjust these settings to match your asset’s volatility and your trading timeframe. There is no “one size fits all”—tuning is key to extracting the most value from MVD.

How to make MVD work for you:

Threshold Crosses: When the MVD line crosses above or below the green dashed thresholds (±2.00), it signals that volatility measures are diverging more than usual. This is a heads-up that a volatility event, regime shift, or hidden market stress may be developing.

Not a Buy/Sell Signal: A threshold cross is not a direct buy or sell signal. It is an indication that the market’s volatility structure is changing. Use it as a filter, confirmation, or alert in combination with your own strategy and risk management.

Dashboard & Info Line: Use the dashboard for a full view of all metrics, or the info label for a quick glance—especially useful on mobile.

Chart: MNQ! on 5min frames

ATR: 14

StDev L: 11

Range L: 13

MDV LB: 13

Important Note

MVD is a market structure and volatility regime tool.

It is designed to alert you to potential changes in market conditions, not to provide direct trade entries or exits. Always combine with your own analysis and risk management.

Meta-Volatility Divergence:

See the market’s hidden tension. Anticipate the next wave.

For educational purposes only. Not financial advice. Always use proper risk management.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Search in scripts for "电力行业+股票+11年涨幅"

Multi VWAPsMulti VWAPs Inspired by Biran Shannon and his book:

"MAXIMUM TRADING GAINS WITH ANCHORED VWAP . The Perfect Combination of Price, Time & Volume."

(ISBN 9798986868004)

A comprehensive VWAP (Volume Weighted Average Price) indicator that combines multiple timeframes and sessions in one view. Perfect for day trading and swing trading across different markets.

Features:

• Multiple VWAP Timeframes:

- Daily VWAP

- Weekly VWAP

- Monthly VWAP

- Quarterly VWAP

- Yearly VWAP

• Session-specific VWAPs:

- London Session (3:00 AM - 11:30 AM NY time)

- New York Session (9:30 AM - 4:00 PM NY time)

• Additional Indicators:

- Midnight Price Line (Previous day's closing price)

- 5-Day Moving Average

- 50-Day Moving Average

• Customization Options:

- Toggle individual VWAPs and indicators

- Customize colors for each component

- Adjustable label positioning

- MA smoothing settings

- Option to show/hide previous day's midnight price

• Smart Features:

- Auto-adjusting calculations based on timeframe

- Clear session boundaries

- Optimized for all chart timeframes

- Clean label system

Perfect for:

• Day traders tracking multiple timeframe momentum

• Swing traders using longer-term VWAPs

• Session traders focusing on London/NY hours

• Multi-timeframe analysis

• Price action trading with VWAP support/resistance

This indicator combines essential trading tools in one clean interface, helping you make informed decisions without cluttering your chart.

EMA SuiteFor strategies with moving averages, of course. My preference is to use Fibonacci values, but it can be configured with any setup. When working on a single timeframe, it allows adding averages or groups of averages from other timeframes, I’ve used this for scalping. The indicator is designed to be dynamic and adaptable. By editing the script, it’s easy to add or remove averages.

Larger averages might slow down loading, and a color palette selector could be added since manually setting 11 values is tedious.

I’m open to any suggestions

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Hippo Battlefield - Bulls VS Bears 20 bars## Hippo Battlefield – Bulls VS Bears (20 Bars)

**What it is**

A multi-dimensional momentum-and-sentiment oscillator that combines classic Bull/Bear Power with ATR- or peak-normalization, then layers on RSI and MACD-derived metrics into:

1. **A colored bar series** showing net Bull+Bear Power strength over the last 20 bars,

2. **A dynamic table** of each of those 20 BBP values (grouped into four 5-bar “quartals”), with symbols, per-bar change, and rolling averages, and

3. **A composite “Weighted BBP” histogram** blending normalized RSI, MACD, and BBP into a single view.

---

### Key Inputs

- **Length (EMA)** – look-back for the underlying EMA (default 60)

- **Normalization Length** – look-back window for peak-normalization (default 60)

- **Use ATR for Norm.** – toggle ATR-based normalization vs. highest-abs(BBP)

- **Show Tables** – toggle the bottom-right 21×11 grid of raw and average BBP values

---

### What You See

#### 1. Colored Bars (Overlay = false)

- Bars are colored by normalized BBP intensity:

- Extreme Bull (≥+10): deep blue

- Strong Bull (+5 to +10): green/yellow

- Weak Bull (+0 to +5): dark green

- Weak Bear (–0 to –5): dark red

- Strong Bear (–5 to –10): pink/red

- Extreme Bear (<–10): magenta

#### 2. Bottom-Right Table (20 Bars of Data)

- Divided into four columns (0–4, 5–9, 10–14, 15–19 bars ago) and one “average” row.

- Each cell shows:

1. Bar index (1–20),

2. Normalized BBP value (to four decimals),

3. Direction symbol (↑/↓/=),

4. Bar-to-bar change (± value),

5. A separator “|”.

- At the very bottom, each column’s 5-bar average is displayed as “Avg: X.XXXX” with a dot marker.

#### 3. Top-Center Mini-Table

- When ≥20 bars have elapsed, shows the date at 20 bars ago and the average BBP across the full 20-bar window.

#### 4. Normalized RSI Line

- Rescales the classic 14-period RSI into a –20…+20 band to align with BBP.

#### 5. MACD Lines (Hidden) & Composite Histogram

- MACD and signal lines are calculated but not plotted by default.

- A “Weighted BBP” histogram combines:

- 20% normalized RSI,

- 20% average of (MACD + signal + normalized BBP),

- 60% normalized BBP

- Plotted as columns, color-coded by strength using the same palette as the main bars.

#### 6. Middle Reference Line

- A horizontal zero line to anchor over/under-zero readings.

---

### How to Use It

- **Trend confirmation**: Strong blue/green bars alongside a rising histogram suggest bull conviction; strong reds/magentas signal bear dominance.

- **Divergence spotting**: Watch for price making new highs/lows while BBP or the histogram fails to follow.

- **Quartal analysis**: The 5-bar group averages can reveal whether recent momentum is accelerating or waning.

- **Cross-indicator weighting**: Because RSI, MACD, and raw BBP all feed into the final histogram, you get a smoothed, blended view of momentum shifts.

---

**Tip:** Tweak the EMA and normalization length to suit your preferred timeframe (e.g. shorter for intraday scalps, longer for swing trades). Enable/disable the table if you prefer a cleaner pane.

Clenow MomentumClenow Momentum Method

The Clenow Momentum Method, developed by Andreas Clenow, is a systematic, quantitative trading strategy focused on capturing medium- to long-term price trends in financial markets. Popularized through Clenow’s book, Stocks on the Move: Beating the Market with Hedge Fund Momentum Strategies, the method leverages momentum—an empirically observed phenomenon where assets that have performed well in the recent past tend to continue performing well in the near future.

Theoretical Foundation

Momentum investing is grounded in behavioral finance and market inefficiencies. Investors often exhibit herding behavior, underreact to new information, or chase trends, causing prices to trend beyond fundamental values. Clenow’s method builds on academic research, such as Jegadeesh and Titman (1993), which demonstrated that stocks with high returns over 3–12 months outperform those with low returns over similar periods.

Clenow’s approach specifically uses **annualized momentum**, calculated as the rate of return over a lookback period (typically 90 days), annualized to reflect a yearly percentage. The formula is:

Momentum=(((Close N periods agoCurrent Close)^N252)−1)×100

- Current Close: The most recent closing price.

- Close N periods ago: The closing price N periods back (e.g., 90 days).

- N: Lookback period (commonly 90 days).

- 252: Approximate trading days in a year for annualization.

This metric ranks stocks by their momentum, prioritizing those with the strongest upward trends. Clenow’s method also incorporates risk management, diversification, and volatility adjustments to enhance robustness.

Methodology

The Clenow Momentum Method involves the following steps:

1. Universe Selection:

- A broad universe of liquid stocks is chosen, often from major indices (e.g., S&P 500, Nasdaq 100) or global exchanges.

- Filters should exclude illiquid stocks (e.g., low average daily volume) or those with extreme volatility.

2. Momentum Calculation:

- Stocks are ranked based on their annualized momentum over a lookback period (typically 90 days, though 60–120 days can be common tests).

- The top-ranked stocks (e.g., top 10–20%) are selected for the portfolio.

3. Volatility Adjustment (Optional):

- Clenow sometimes adjusts momentum scores by volatility (e.g., dividing by the standard deviation of returns) to favor stocks with smoother trends.

- This reduces exposure to erratic price movements.

4. Portfolio Construction:

- A diversified portfolio of 10–25 stocks is constructed, with equal or volatility-weighted allocations.

- Position sizes are often adjusted based on risk (e.g., 1% of capital per position).

5. Rebalancing:

- The portfolio is rebalanced periodically (e.g., weekly or monthly) to maintain exposure to high-momentum stocks.

- Stocks falling below a momentum threshold are replaced with higher-ranked candidates.

6. Risk Management:

- Stop-losses or trailing stops may be applied to limit downside risk.

- Diversification across sectors reduces concentration risk.

Implementation in TradingView

Key features include:

- Customizable Lookback: Users can adjust the lookback period in pinescript (e.g., 90 days) to align with Clenow’s methodology.

- Visual Cues: Background colors (green for positive, red for negative momentum) and a zero line help identify trend strength.

- Integration with Screeners: TradingView’s stock screener can filter high-momentum stocks, which can then be analyzed with the custom indicator.

Strengths

1. Simplicity: The method is straightforward, relying on a single metric (momentum) that’s easy to calculate and interpret.

2. Empirical Support: Backed by decades of academic research and real-world hedge fund performance.

3. Adaptability: Applicable to stocks, ETFs, or other asset classes, with flexible lookback periods.

4. Risk Management: Diversification and periodic rebalancing reduce idiosyncratic risk.

5. TradingView Integration: Pine Script implementation enables real-time visualization, enhancing decision-making for stocks like NVDA or SPY.

Limitations

1. Mean Reversion Risk: Momentum can reverse sharply in bear markets or during sector rotations, leading to drawdowns.

2. Transaction Costs: Frequent rebalancing increases trading costs, especially for retail traders with high commissions. This is not as prevalent with commission free trading becoming more available.

3. Overfitting Risk: Over-optimizing lookback periods or filters can reduce out-of-sample performance.

4. Market Conditions: Underperforms in low-momentum or highly volatile markets.

Practical Applications

The Clenow Momentum Method is ideal for:

Retail Traders: Use TradingView’s screener to identify high-momentum stocks, then apply the Pine Script indicator to confirm trends.

Portfolio Managers: Build diversified momentum portfolios, rebalancing monthly to capture trends.

Swing Traders: Combine with volume filters to target short-term breakouts in high-momentum stocks.

Cross-Platform Workflow: Integrate with Python scanners to rank stocks, then visualize on TradingView for trade execution.

Comparison to Other Strategies

Vs. Minervini’s VCP: Clenow’s method is purely quantitative, while Minervini’s Volatility Contraction Pattern (your April 11, 2025 query) combines momentum with chart patterns. Clenow is more systematic but less discretionary.

Vs. Mean Reversion: Momentum bets on trend continuation, unlike mean reversion strategies that target oversold conditions.

Vs. Value Investing: Momentum outperforms in bull markets but may lag value strategies in recovery phases.

Conclusion

The Clenow Momentum Method is a robust, evidence-based strategy that capitalizes on price trends while managing risk through diversification and rebalancing. Its simplicity and adaptability make it accessible to retail traders, especially when implemented on platforms like TradingView with custom Pine Script indicators. Traders must be mindful of transaction costs, mean reversion risks, and market conditions. By combining Clenow’s momentum with volume filters and alerts, you can optimize its application for swing or position trading.

SMT SwiftEdge PowerhouseSMT SwiftEdge Powerhouse: Precision Trading with Divergence, Liquidity Grabs, and OTE Zones

The SMT SwiftEdge Powerhouse is a powerful trading tool designed to help traders identify high-probability entry points during the most active market sessions—London and New York. By combining Smart Money Technique (SMT) Divergence, Liquidity Grabs, and Optimal Trade Entry (OTE) Zones, this script provides a unique and cohesive strategy for capturing market reversals with precision. Whether you're a scalper or a swing trader, this indicator offers clear visual signals to enhance your trading decisions on any timeframe.

What Does This Script Do?

This script integrates three key concepts to identify potential trading opportunities:

SMT Divergence:

SMT Divergence compares the price action of two correlated assets (e.g., Nasdaq and S&P 500 futures) to detect hidden market reversals. When one asset makes a higher high while the other makes a lower high (bearish divergence), or one makes a lower low while the other makes a higher low (bullish divergence), it signals a potential reversal. This technique leverages institutional "smart money" behavior to anticipate market shifts.

Liquidity Grabs:

Liquidity Grabs occur when price breaks above recent highs or below recent lows on higher timeframes (5m and 15m), often triggering stop-loss orders from retail traders. These breakouts are identified using pivot points and confirm institutional activity, setting the stage for a reversal. The script focuses on liquidity grabs during the London and New York sessions for maximum market activity.

Optimal Trade Entry (OTE) Zones:

OTE Zones are Fibonacci-based retracement areas (e.g., 61.8%) calculated after a liquidity grab. These zones highlight where price is likely to retrace before continuing in the direction of the reversal, offering a high-probability entry point. The script adjusts the width of these zones using the Average True Range (ATR) to adapt to market volatility.

By combining these components, the script identifies when institutional activity (liquidity grabs) aligns with market reversals (SMT divergence) and pinpoints precise entry points (OTE zones) during high-liquidity sessions.

Why Combine These Components?

The integration of SMT Divergence, Liquidity Grabs, and OTE Zones creates a robust trading system for several reasons:

Synergy of Institutional Signals: SMT Divergence and Liquidity Grabs both reflect "smart money" behavior—divergence shows hidden reversals, while liquidity grabs confirm institutional intent to trap retail traders. Together, they provide a strong foundation for identifying high-probability setups.

Session-Based Precision: Focusing on the London and New York sessions ensures signals occur during periods of high volatility and liquidity, increasing their reliability.

Precision Entries with OTE: After confirming a setup with divergence and liquidity grabs, OTE zones provide a clear entry area, reducing guesswork and improving trade accuracy.

Adaptability: The script works on any timeframe, with adjustable settings for signal sensitivity, session times, and Fibonacci levels, making it versatile for different trading styles.

This combination makes the script unique by aligning institutional insights with actionable entry points, tailored to the most active market hours.

How to Use the Script

Setup:

Add the script to your chart (works on any timeframe, e.g., 1m, 5m, 15m).

Configure the settings in the indicator's inputs:

Session Settings: Adjust the start/end times for London and New York sessions (default: London 8-11 UTC, New York 13-16 UTC). You can disable session restrictions if desired.

Asset Settings: Set the primary and secondary assets for SMT Divergence (default: NQ1! and ES1!). Ensure the assets are correlated.

Signal Settings: Adjust the lookback period, ATR period, and signal sensitivity (Low/Medium/High) to control the frequency of signals.

OTE Settings: Choose the Fibonacci level for OTE zones (default: 61.8%).

Visual Settings: Enable/disable OTE zones, SMT labels, and debug labels for troubleshooting.

Interpreting Signals:

Blue Circles: Indicate a liquidity grab (price breaking a 5m or 15m pivot high/low), marking the start of a potential setup.

Blue OTE Zones: Appear after a liquidity grab, showing the retracement area (e.g., 61.8% Fibonacci level) where price is likely to enter for a reversal trade. The label "OTE Trigger 5m/15m" confirms the direction (Short/Long) and session.

Green/Red Entry Boxes: Mark precise entry points when price enters the OTE zone and confirms the SMT Divergence. Green boxes indicate a long entry, red boxes a short entry.

Trading Example:

On a 1m chart, a blue circle appears when price breaks a 5m pivot high during the London session.

A blue OTE zone forms, showing a retracement area (e.g., 61.8% Fibonacci level) with the label "OTE Trigger 5m/15m (Short, London)".

Price retraces into the OTE zone, and a red "Short Entry" box appears, confirming a bearish SMT Divergence.

Enter a short trade at the red box, with a stop-loss above the OTE zone and a take-profit at the next support level.

Originality and Utility

The SMT SwiftEdge Powerhouse stands out by merging SMT Divergence, Liquidity Grabs, and OTE Zones into a single, session-focused indicator. Unlike traditional indicators that focus on one aspect of price action, this script combines institutional reversal signals with precise entry zones, tailored to the most active market hours. Its adaptability across timeframes, customizable settings, and clear visual cues make it a versatile tool for traders seeking to capitalize on smart money movements with confidence.

Tips for Best Results

Use on correlated assets like NQ1! (Nasdaq futures) and ES1! (S&P 500 futures) for accurate SMT Divergence.

Test on lower timeframes (1m, 5m) for scalping or higher timeframes (15m, 1H) for swing trading.

Adjust the "Signal Sensitivity" to "High" for more signals or "Low" for fewer, high-quality setups.

Enable "Show Debug Labels" if signals are not appearing as expected, to troubleshoot pivot points and liquidity grabs.

The Mayan CalendarThis indicator displays the current date in the Mayan Calendar, based on real-time UTC time. It calculates and presents:

🌀 Long Count (Baktun.Katun.Tun.Uinal.Kin) – A linear count of days since the Mayan epoch (August 11, 3114 BCE).

🔮 Tzolk'in Date – A 260-day sacred cycle combining a number (1–13) and one of 20 day names (e.g., 4 Ajaw).

🌾 Haab' Date – A 365-day civil cycle divided into 18 months of 20 days + 5 "nameless" days (Wayeb').

The calculations follow Smithsonian standards and align with the Maya Calendar Converter from the National Museum of the American Indian:

👉 maya.nmai.si.edu

The results are shown in a table overlay on your chart's top-right corner. This indicator is great for symbolic traders, astro enthusiasts, or anyone interested in ancient timekeeping systems woven into financial timeframes. Enjoy, time travelers! ⌛

MACD [AlchimistOfCrypto]🌠 MACD Optimized with Python – Decoding the Chaos of Markets 🌠

Category: Trend Analysis 📈

"Like the dynamic systems studied in chaos theory, financial markets appear unpredictable at first glance. Yet, as Edward Lorenz demonstrated, even in apparent chaos reside harmonious mathematical structures. The MACD (Moving Average Convergence Divergence) represents this quest for order within disorder—a mathematical formulation that extracts coherent signals from price noise. By combining moving averages of different periods, this indicator reveals hidden cycles and precise moments when market energy shifts, like a pendulum obeying the immutable laws of physics."

📊 Technical Overview

The MACD Optimized with Python is a revolutionary take on the classic Moving Average Convergence Divergence indicator. Powered by Python-driven optimizations 🐍, it adapts to specific timeframes, delivering razor-sharp signals for traders seeking to navigate the market’s chaos with precision.

⚙️ How It Works

- Python-Optimized Parameters 🔧: Unlike the standard MACD (12,26,9), our version uses mathematically tailored parameters for each timeframe:

- 1H: 11/38/27

- 4H: 9/98/27

- 1D: 45/90/29

- 1W: 9/16/3

- 2W: 5/20/5

- Intuitive Visuals 🎨:

- Crossovers marked by colored dots 🟢🔴 for clear entry/exit signals.

- Histogram with a color gradient 🌈 to show direction and momentum intensity.

- Customizable Signals 🎯: Choose to display long, short, or both signals to match your trading style.

🚀 How to Use This Indicator

1. Select Your Timeframe ⏰: Choose the timeframe aligned with your trading horizon (1H, 4H, 1D, 1W, or 2W).

2. Spot Crossovers 🔍: Watch for the MACD line (green) crossing the signal line (red) to identify potential trend changes.

3. Confirm with Divergence ✅: Combine crossovers with price-MACD divergence for high-probability trend reversal signals.

📅 Release Notes

Unlock the hidden order of markets with this Python-optimized MACD. Stay tuned for future enhancements! ✨

🏷️ Tags

#Trading #TechnicalAnalysis #MACD #TrendAnalysis #Python #MultiTimeframe #Divergence #Momentum #TradingStrategy #RiskManagement #Forex #Stocks #Crypto #ChaosTheory #OptimizedTrading

Collatz Conjecture - DolphinTradeBot1️⃣ Overview

Every positive number follows its own unique path to reach 1 according to the Collatz rule.

Some numbers reach the end quickly and directly.

Others rise significantly before crashing down sharply.

Some get stuck within a certain range for a while before finally reaching 1.

Each number follows a different pattern — the number of steps it takes, how high it climbs, or which values it passes through cannot be predicted in advance.

This is a structure that appears chaotic but ultimately leads to order:

Every number reaches 1, but the way it gets there is entirely uncertain.

2️⃣ How Is It Work?

The rule is simple:

▪️ If the number is even → divide it by two.

▪️ If it’s odd → multiply it by three and add one.

Repeat this process at each step.

Example :

Let’s say the starting number is 7:

7 → 22 → 11 → 34 → 17 → 52 → 26 → 13 → 40 → 20 → 10 → 5 → 16 → 8 → 4 → 2 → 1

It reaches 1 in 17 steps.

And from there, it always enters the same cycle:

4 → 2 → 1 → 4 → 2 → 1...

3️⃣ Why Is It Worth Learning?

🎯 This indicator isn’t just mathematical fun—it’s a thought experiment for those who dare to question market behavior.

▪️ It’s fun.

Watching numbers behave in unpredictable ways from a simple rule set is surprisingly enjoyable.

▪️ It shows how hard it is to teach a computer what randomness really is .

The Collatz process can be used to simulate chaotic behavior and may even inspire creative ways to introduce complexity into your code.

▪️ It makes you think — especially in financial markets.

The patternless, yet rule-based structure of Collatz can help train your mind to recognize that not all unpredictability is random. It’s a great mental model for navigating complex systems like price action.

▪️ Just like price movements in financial markets, this ancient problem remains unsolved.

Despite its simplicity, the Collatz conjecture has resisted proof for decades — a reminder that even the most basic-looking systems can hide deep complexity.

4️⃣ How To Use?

Super easy — in the indicator’s settings, there’s just one input field.

Enter any positive number, and you’ll see the pattern it follows on its way to 1.

You can also observe how many steps it takes and which values it visits in the info box at the top center of the chart.

5️⃣ Some Examples

You Can Observe the Chaos in the Following Examples⤵️

For Input Number → 12

For Input Number → 13

For Input Number → 14

For Input Number → 32768

For Input Number → 47

MA Deviation// -----------------------------------------------------------------------------

// MA Deviation Marking & Alert (MA Divergence)

// -----------------------------------------------------------------------------

// Short Title: MA Deviation Radar

// Author: zhipeng luo

// Version: 1.0

// Date: 2025-04-11

// -----------------------------------------------------------------------------

// Overview:

// This indicator identifies and highlights price bars where the closing price

// deviates significantly from its Simple Moving Average (SMA) by a user-defined

// percentage. It visually marks these bars on the chart and provides

// configurable alert conditions for threshold breaches.

//

// How it Works:

// 1. Calculates the Simple Moving Average (SMA) based on the 'MA Period' input.

// 2. Computes the percentage deviation of the closing price from the SMA value.

// Formula: `((Close - SMA) / SMA) * 100`

// 3. Compares the calculated deviation percentage against the positive and

// negative 'Threshold (%)' input values.

// 4. Marks the background of the price bars when a threshold is exceeded:

// - Red Background: Price deviation is greater than the positive threshold.

// - Green Background: Price deviation is less than the negative threshold.

// 5. Includes an optional, non-visible plot of the MA line itself.

// 6. Offers three distinct alert conditions for automation and notifications.

//

// Features:

// - Customizable Simple Moving Average period.

// - Adjustable deviation threshold percentage.

// - Clear visual signals using background colors on the main chart.

// - Built-in Alert Conditions:

// - MA Positive Deviation Alert (Triggers when price > MA + Threshold %)

// - MA Negative Deviation Alert (Triggers when price < MA - Threshold %)

// - MA Deviation Alert - Any (Triggers on either positive or negative breach)

//

// How to Use:

// - Identify Potential Extremes: Useful for spotting potential overbought (large

// positive deviation) or oversold (large negative deviation) conditions

// which might precede price corrections or mean reversion.

// - Gauge Trend Extension: Extreme deviations can sometimes indicate that a

// trend is overextended and might be due for a pause or reversal.

// - Parameter Tuning: Adjust the 'MA Period' and '(Threshold %)' settings to

// suit the specific asset, timeframe, and volatility characteristics you

// are analyzing. Lower thresholds yield more signals; higher thresholds

// focus on more significant deviations.

// - Alerts: Set up alerts via the TradingView alert menu using the provided

// conditions ("MA Positive Deviation Alert", "MA Negative Deviation Alert",

// "MA Deviation Alert - Any") to get notified of potential setups.

//

// Parameters:

// - MA Period (Default: 200): The lookback period for the SMA calculation.

// - (Threshold %) (Default: 7.0): The percentage deviation (positive and

// negative) from the MA required to trigger a background signal and alert.

//

// Alerts & Important Note:

// Three alert conditions corresponding to the signals are available:

// 1. "MA Positive Deviation Alert"

// 2. "MA Negative Deviation Alert"

// 3. "MA Deviation Alert - Any"

//

// ***Please Note:*** The value shown after "( {{plot_0}}%)" or

// "( {{plot_0}}%)" in the default alert message refers to the

// **Moving Average value** (`plot_0`), not the actual deviation percentage.

// The alert *triggers correctly* based on the deviation percentage crossing

// the threshold, but the number displayed by the `{{plot_0}}` placeholder

// in the message is the MA's value at that time due to the script's

// internal plot order.

//

// Disclaimer: This indicator is provided for informational and analytical

// purposes only. It does not constitute financial advice or a recommendation

// to buy or sell any asset. Always conduct your own research and use proper

// risk management. Trading involves significant risk.

// -----------------------------------------------------------------------------

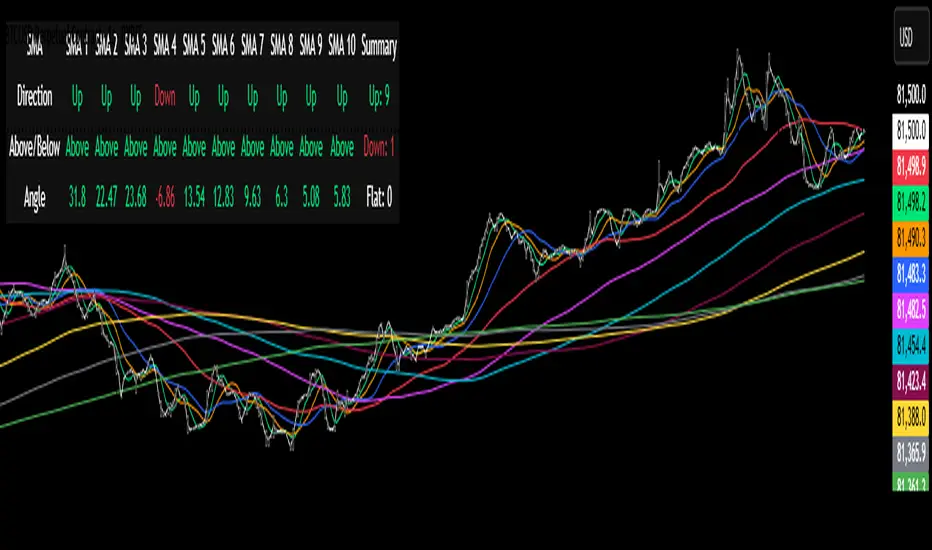

Multi-SMA Dashboard (10 SMAs)Description:

This script, "Multi-SMA Dashboard (10 SMAs)," creates a dashboard on a TradingView chart to analyze ten Simple Moving Averages (SMAs) of varying lengths. It overlays the chart and displays a table with each SMA’s direction, price position relative to the SMA, and angle of movement, providing a comprehensive trend overview.

How It Works:

1. **Inputs**: Users define lengths for 10 SMAs (default: 5, 10, 20, 50, 100, 150, 200, 250, 300, 350), select a price source (default: close), and customize table appearance and options like angle units (degrees/radians) and debug plots.

2. **SMA Calculation**: Computes 10 SMAs using the `ta.sma()` function with user-specified lengths and price source.

3. **Direction Determination**: The `sma_direction()` function checks each SMA’s trend:

- "Up" if current SMA > previous SMA.

- "Down" if current SMA < previous SMA.

- "Flat" if equal (no strength distinction).

4. **Price Position**: Compares the price source to each SMA, labeling it "Above" or "Below."

5. **Angle Calculation**: Tracks the most recent direction change point for each SMA and calculates its angle (atan of price change over time) in degrees or radians, based on the `showInRadians` toggle.

6. **Table Display**: A 12-column table shows:

- Columns 1-10: SMA name, direction (Up/Down/Flat), Above/Below status, and angle.

- Column 11: Summary of Up, Down, and Flat counts.

- Colors reflect direction (lime for Up/Above, red for Down/Below, white for Flat).

7. **Debug Option**: Optionally plots all SMAs and price for visual verification when `debug_plots_toggle` is enabled.

Indicators Used:

- Simple Moving Averages (SMAs): 10 user-configurable SMAs ranging from short-term (e.g., 5) to long-term (e.g., 350) periods.

The script runs continuously, updating the table on each bar, and overlays the chart to assist traders in assessing multi-timeframe trend direction and momentum without cluttering the view unless debug mode is active.

London Breakout Tracker - Box Style📊 London Breakout Tracker (Pine Script v6)

This script is designed to track the Asian session range and identify breakout opportunities when the London session begins. It highlights high-probability trade setups and helps avoid fakeouts or overly wide ranges.

🧱 1. Session Time Definitions (Adjusted for Kenyan Time)

The Asian session is defined as:

3:00 AM to 11:00 AM (Kenyan Time)

🔐 2. Asian Session High & Low

During the Asian session:

The script tracks the highest high and lowest low to define the range.

These are stored in variables: asianHigh and asianLow.

🧊 3. Box Drawing for the Asian Range

Once the Asian session ends:

A visual box is drawn around the session using box.new().

This box spans from the session start to end bars and from the high to low.

It helps visually see the range price must break out from.

🚨 4. Breakout Signals

After the Asian session:

A Long Breakout signal is generated if:

The candle closes above the Asian High.

A Short Breakout signal is generated if:

The candle closes below the Asian Low.

This corresponds to 00:00 to 08:00 UTC

These are shown with:

✅ Green up label for long breakouts

❌ Red down label for short breakouts

🧯 5. Fakeout Detection

If price breaks out but closes back inside the Asian range, it’s marked as a Fakeout:

Long Fakeout: Price breaks above high, then closes back below.

Short Fakeout: Price breaks below low, then closes back above.

These are marked with orange X-crosses above or below candles.

⚠️ 6. Wide Range Filter

If the Asian session range is too wide (e.g. > 40 pips), a gray background is drawn.

This warns you not to trade that day since breakouts from wide ranges are unreliable.

📣 7. Alert Conditions

The script can trigger alerts in TradingView when:

🔔 A Long or Short Breakout occurs

⚠️ A Fakeout is detected

You can set these up via the TradingView alert system.

🎯 Overall Purpose:

The script helps you:

Clearly see the Asian session range

Identify breakout opportunities at the London open

Avoid trading during fakeouts or wide-range sessions

Get alerted when breakout/fakeout conditions occur

2013-2025 Moon Phases & Mercury RetrogradesIndicator Description: 2013-2025 Moon Phases & Mercury Retrogrades

This Pine Script (version 5) indicator overlays key astrological events on a TradingView chart, specifically tracking full moons, new moons, and Mercury retrograde periods from 2013 to 2025. It is designed to help traders and astrology enthusiasts visualize these celestial events alongside price action, potentially identifying correlations or patterns.

Features:

New Moons:

Visualization: Plotted as small white circles above the price bars.

Data: Includes 156 specific new moon dates from January 11, 2013, to December 20, 2025.

Purpose: Marks the start of the lunar cycle, often associated with new beginnings or shifts in energy.

Full Moons:

Visualization: Plotted as small orange circles above the price bars.

Data: Includes 157 specific full moon dates from January 27, 2013, to December 15, 2025.

Purpose: Highlights the peak of the lunar cycle, often linked to heightened emotions or market volatility in astrological analysis.

Mercury Retrogrades:

Visualization: Displayed as a light red background highlight across the chart.

Data: Covers 39 Mercury retrograde periods, with precise start and end timestamps from February 23, 2013, to November 29, 2025.

Purpose: Indicates periods traditionally associated with communication issues, delays, or reversals, which some traders monitor for potential market impacts.

Technical Details:

Overlay: The indicator is set to overlay=true, meaning it displays directly on the price chart rather than in a separate pane.

Date Matching: Uses a helper function is_date(y, m, d) to check if the current chart date matches any of the predefined event dates, leveraging TradingView's year, month, and dayofmonth variables.

Visualization Methods:

plotshape: Used for new moons (white circles) and full moons (orange circles), positioned above bars for clear visibility.

bgcolor: Used for Mercury retrograde periods, applying a semi-transparent red highlight (transparency level 85) to the background during active retrograde periods.

Time Range: Spans from January 2013 to December 2025, providing a comprehensive 13-year view of these astrological events.

Usage:

Add the script to your TradingView chart to see new moons, full moons, and Mercury retrograde periods overlaid on your chosen symbol and timeframe.

The white and orange circles appear on specific dates, while the red background highlights extend across the duration of each Mercury retrograde period.

Useful for traders incorporating astrology into their analysis or anyone interested in tracking these celestial events alongside financial data.

Notes:

The script assumes accurate date data as provided; users should verify dates against astronomical sources if precision is critical.

The transparency of the Mercury retrograde background can be adjusted by modifying the value in color.new(color.red, 85) (0 = fully opaque, 100 = fully transparent).

Best viewed on daily or higher timeframes for clarity, though it works on any timeframe supported by TradingView.

This indicator provides a visual tool to explore the potential influence of lunar phases and Mercury retrograde periods on market behavior, blending astrology with technical analysis in a clear, customizable format.

LUX CLARA - EMA + VWAP (No ATR Filter) - v6EMA STRAT SHOUT OUTOUTLIERSSSSS

Overview:

an intraday strategy built around two core principles:

Trend Confirmation using the 50 EMA (Exponential Moving Average) in relation to the VWAP (Volume-Weighted Average Price).

Entry Signals triggered by the 8 EMA crossing the 50 EMA in the direction of that confirmed trend.

Key Logic:

Bullish Trend if the 50 EMA is above VWAP. Only long entries are allowed when the 8 EMA crosses above the 50 EMA during that bullish phase.

Bearish Trend if the 50 EMA is below VWAP. Only short entries are allowed when the 8 EMA crosses below the 50 EMA during that bearish phase.

Intraday Focus: Trades are restricted to a user-defined session window (default 7:30 AM–11:30 AM), aligning entries/exits with peak intraday liquidity.

Exit Rule: Positions close automatically when the 8 EMA crosses back in the opposite direction of the entry.

Why It Works:

EMA + VWAP helps detect both immediate momentum (EMAs) and overall institutional bias (VWAP).

By confining trades to a set intraday window, the strategy aims to capture morning volatility while avoiding choppy afternoon or overnight sessions.

Customization:

Users can adjust EMA lengths, session times, or incorporate stops/targets for additional risk management.

It can be tested on various symbols and intraday timeframes to gauge performance and robustness.

MACD Volume Strategy (BBO + MACD State, Reversal Type)Overview

MACD Volume Strategy (BBO + MACD State, Reversal Type) is a momentum-based reversal system that combines MACD crossover logic with volume filtering to enhance signal accuracy and minimize noise. It aims to identify structural trend shifts and manage risk using predefined parameters.

※This strategy is for educational and research purposes only. All results are based on historical simulations and do not guarantee future performance.

Strategy Objectives

Identify early trend transitions with high probability

Filter entries using volume dynamics to validate momentum

Maintain continuous exposure using a reversal-style model

Apply a consistent 1:1.5 risk-to-reward ratio per trade

Key Features

Integrated MACD and volume oscillator filtering

Zero repainting (all signals confirmed on closed candles)

Automatic position flipping for seamless direction shifts

Stop-loss and take-profit based on recent structural highs/lows

Trading Rules

Long Entry Conditions

MACD crosses above the zero line (BBO Buy arrow)

Volume oscillator is positive (short EMA > long EMA)

MACD is above the signal line

Close any existing short and enter a new long

Short Entry Conditions

MACD crosses below the zero line (BBO Sell arrow)

Volume oscillator is positive

MACD is below the signal line

Close any existing long and enter a new short

Exit Rules

Take Profit (TP) = Entry ± (risk distance × 1.5)

Stop Loss (SL) = Recent swing low (for long) or high (for short)

Early Exit = Triggered when a reversal signal appears (flip logic)

Risk Management Parameters

Pair: ETH/USD

Timeframe: 10-minute

Starting Capital: $3,000

Commission: 0.02%

Slippage: 2 pip

Risk per Trade: 5% of account equity (adjusted for sustainable practice)

Total Trades: 312 (backtest on selected dataset)

※Risk parameters are fully configurable and should be adjusted to suit each trader's personal setup and broker conditions.

Parameters & Configurations

Volume Short Length: 6

Volume Long Length: 12

MACD Fast Length: 11

MACD Slow Length: 21

Signal Smoothing: 10

Oscillator MA Type: SMA

Signal Line MA Type: SMA

Visual Support

Green arrow = Long entry

Red arrow = Short entry

MACD lines, signal line, and histogram

SL/TP markers plotted directly on the chart

Strategic Advantages & Uniqueness

Volume filtering eliminates low-participation, weak signals

Structurally aligned SL/TP based on recent market pivots

No repainting — decisions are made only on closed candles

Always in the market due to the reversal-style framework

Inspirations & Attribution

This strategy is inspired by the excellent work of:

Bitcoinblockchainonline – “BBO_Roxana_Signals MACD + vol”

Leveraging MACD zero-line cross and volume oscillator for intuitive signal generation.

HasanRifat – “MACD Fake Filter ”

Introduced a signal filter using MACD wave height averaging to reduce false positives.

This strategy builds upon those ideas to create a more automated, risk-aware, and technically adaptive system.

Summary

MACD Volume Strategy is a clean, logic-first automated trading system built for precision-seeking traders. It avoids discretionary bias and provides consistent signal logic under backtested historical conditions.

100% mechanical — no discretionary input required

Designed for high-confidence entries

Can be extended with filters, alerts, or trailing stops

※Strategy performance depends on market context. Past performance is not indicative of future results. Use with proper risk management and careful configuration.

DAMA OSC - Directional Adaptive MA OscillatorOverview:

The DAMA OSC (Directional Adaptive MA Oscillator) is a highly customizable and versatile oscillator that analyzes the delta between two moving averages of your choice. It detects trend progression, regressions, rebound signals, MA cross and critical zone crossovers to provide highly contextual trading information.

Designed for trend-following, reversal timing, and volatility filtering, DAMA OSC adapts to market conditions and highlights actionable signals in real-time.

Features:

Support for 11 custom moving average types (EMA, DEMA, TEMA, ALMA, KAMA, etc.)

Customizable fast & slow MA periods and types

Histogram based on percentage delta between fast and slow MA

Trend direction coloring with “Green”, “Blue”, and “Red” zones

Rebound detection using close or shadow logic

Configurable thresholds: Overbought, Oversold, Underbought, Undersold

Optional filters: rebound validation by candle color or flat-zone filter

Full visual overlay: MA lines, crossover markers, rebound icons

Complete alert system with 16 preconfigured conditions

How It Works:

Histogram Logic:

The histogram measures the percentage difference between the fast and slow MA:

hist_value = ((FastMA - SlowMA) / SlowMA) * 100

Trend State Logic (Green / Blue / Red):

Green_Up = Bullish acceleration

Blue_Up (or Red_Up, depending the display settings) = Bullish deceleration

Blue_Down (or Green_Down, depending the display settings) = Bearish deceleration

Red_Down = Bearish acceleration

Rebound Logic:

A rebound is detected when price:

Crosses back over a selected MA (fast or slow)

After being away for X candles (rebound_backstep)

Optional: filtered by histogram zones or candle color

Inputs:

Display Options:

Show/hide MA lines

Show/hide MA crosses

Show/hide price rebounds

Enable/disable blue deceleration zones

DAMA Settings:

Fast/Slow MA type and length

Source input (close by default)

Overbought/Oversold levels

Underbought/Undersold levels

Rebound Settings:

Use Close and/or Shadow

Rebound MA (Fast/Slow)

Candle color validation

Flat zone filter rebounds (between UnderSold and UnderBought)

Available MA type:

SMA (Simple MA)

EMA (Exponential MA)

DEMA (Double EMA)

TEMA (Triple EMA)

WMA (Weighted MA)

HMA (Hull MA)

VWMA (Volume Weighted MA)

Kijun (Ichimoku Baseline)

ALMA (Arnaud Legoux MA)

KAMA (Kaufman Adaptive MA)

HULLMOD (Modified Hull MA, Same as HMA, tweaked for Pine v6 constraints)

Notes:

**DEMA/TEMA** reduce lag compared to EMA, useful for faster reaction in trending markets.

**KAMA/ALMA** are better suited to noisy or volatile environments (e.g., BTC).

**VWMA** reacts strongly to volume spikes.

**HMA/HULLMOD** are great for visual clarity in fast moves.

Alerts Included (Fully Configurable):

Golden Cross:

Fast MA crosses above Slow MA

Death Cross:

Fast MA crosses below Slow MA

Bullish Rebound:

Rebound from below MA in uptrend

Bearish Rebound:

Rebound from above MA in downtrend

Bull Progression:

Transition into Green_Up with positive delta

Bear Progression:

Transition into Red_Down with negative delta

Bull Regression:

Exit from Red_Down into Blue/Green with negative delta

Bear Regression:

Exit from Green_Up into Blue/Red with positive delta

Crossover Overbought:

Histogram crosses above Overbought

Crossunder Overbought:

Histogram crosses below Overbought

Crossover Oversold:

Histogram crosses above Oversold

Crossunder Oversold:

Histogram crosses below Oversold

Crossover Underbought:

Histogram crosses above Underbought

Crossunder Underbought:

Histogram crosses below Underbought

Crossover Undersold:

Histogram crosses above Undersold

Crossunder Undersold:

Histogram crosses below Undersold

Credits:

Created by Eff_Hash. This code is shared with the TradingView community and full free. do not hesitate to share your best settings and usage.

ZigZag█ Overview

This Pine Script™ library provides a comprehensive implementation of the ZigZag indicator using advanced object-oriented programming techniques. It serves as a developer resource rather than a standalone indicator, enabling Pine Script™ programmers to incorporate sophisticated ZigZag calculations into their own scripts.

Pine Script™ libraries contain reusable code that can be imported into indicators, strategies, and other libraries. For more information, consult the Libraries section of the Pine Script™ User Manual.

█ About the Original

This library is based on TradingView's official ZigZag implementation .

The original code provides a solid foundation with user-defined types and methods for calculating ZigZag pivot points.

█ What is ZigZag?

The ZigZag indicator filters out minor price movements to highlight significant market trends.

It works by:

1. Identifying significant pivot points (local highs and lows)

2. Connecting these points with straight lines

3. Ignoring smaller price movements that fall below a specified threshold

Traders typically use ZigZag for:

- Trend confirmation

- Identifying support and resistance levels

- Pattern recognition (such as Elliott Waves)

- Filtering out market noise

The algorithm identifies pivot points by analyzing price action over a specified number of bars, then only changes direction when price movement exceeds a user-defined percentage threshold.

█ My Enhancements

This modified version extends the original library with several key improvements:

1. Support and Resistance Visualization

- Adds horizontal lines at pivot points

- Customizable line length (offset from pivot)

- Adjustable line width and color

- Option to extend lines to the right edge of the chart

2. Support and Resistance Zones

- Creates semi-transparent zone areas around pivot points

- Customizable width for better visibility of important price levels

- Separate colors for support (lows) and resistance (highs)

- Visual representation of price areas rather than just single lines

3. Zig Zag Lines

- Separate colors for upward and downward ZigZag movements

- Visually distinguishes between bullish and bearish price swings

- Customizable colors for text

- Width customization

4. Enhanced Settings Structure

- Added new fields to the Settings type to support the additional features

- Extended Pivot type with supportResistance and supportResistanceZone fields

- Comprehensive configuration options for visual elements

These enhancements make the ZigZag more useful for technical analysis by clearly highlighting support/resistance levels and zones, and providing clearer visual cues about market direction.

█ Technical Implementation

This library leverages Pine Script™'s user-defined types (UDTs) to create a robust object-oriented architecture:

- Settings : Stores configuration parameters for calculation and display

- Pivot : Represents pivot points with their visual elements and properties

- ZigZag : Manages the overall state and behavior of the indicator

The implementation follows best practices from the Pine Script™ User Manual's Style Guide and uses advanced language features like methods and object references. These UDTs represent Pine Script™'s most advanced feature set, enabling sophisticated data structures and improved code organization.

For newcomers to Pine Script™, it's recommended to understand the language fundamentals before working with the UDT implementation in this library.

█ Usage Example

//@version=6

indicator("ZigZag Example", overlay = true, shorttitle = 'ZZA', max_bars_back = 5000, max_lines_count = 500, max_labels_count = 500, max_boxes_count = 500)

import andre_007/ZigZag/1 as ZIG

var group_1 = "ZigZag Settings"

//@variable Draw Zig Zag on the chart.

bool showZigZag = input.bool(true, "Show Zig-Zag Lines", group = group_1, tooltip = "If checked, the Zig Zag will be drawn on the chart.", inline = "1")

// @variable The deviation percentage from the last local high or low required to form a new Zig Zag point.

float deviationInput = input.float(5.0, "Deviation (%)", minval = 0.00001, maxval = 100.0,

tooltip = "The minimum percentage deviation from a previous pivot point required to change the Zig Zag's direction.", group = group_1, inline = "2")

// @variable The number of bars required for pivot detection.

int depthInput = input.int(10, "Depth", minval = 1, tooltip = "The number of bars required for pivot point detection.", group = group_1, inline = "3")

// @variable registerPivot (series bool) Optional. If `true`, the function compares a detected pivot

// point's coordinates to the latest `Pivot` object's `end` chart point, then

// updates the latest `Pivot` instance or adds a new instance to the `ZigZag`

// object's `pivots` array. If `false`, it does not modify the `ZigZag` object's

// data. The default is `true`.

bool allowZigZagOnOneBarInput = input.bool(true, "Allow Zig Zag on One Bar", tooltip = "If checked, the Zig Zag calculation can register a pivot high and pivot low on the same bar.",

group = group_1, inline = "allowZigZagOnOneBar")

var group_2 = "Display Settings"

// @variable The color of the Zig Zag's lines (up).

color lineColorUpInput = input.color(color.green, "Line Colors for Up/Down", group = group_2, inline = "4")

// @variable The color of the Zig Zag's lines (down).

color lineColorDownInput = input.color(color.red, "", group = group_2, inline = "4",

tooltip = "The color of the Zig Zag's lines")

// @variable The width of the Zig Zag's lines.

int lineWidthInput = input.int(1, "Line Width", minval = 1, tooltip = "The width of the Zig Zag's lines.", group = group_2, inline = "w")

// @variable If `true`, the Zig Zag will also display a line connecting the last known pivot to the current `close`.

bool extendInput = input.bool(true, "Extend to Last Bar", tooltip = "If checked, the last pivot will be connected to the current close.",

group = group_1, inline = "5")

// @variable If `true`, the pivot labels will display their price values.

bool showPriceInput = input.bool(true, "Display Reversal Price",

tooltip = "If checked, the pivot labels will display their price values.", group = group_2, inline = "6")

// @variable If `true`, each pivot label will display the volume accumulated since the previous pivot.

bool showVolInput = input.bool(true, "Display Cumulative Volume",

tooltip = "If checked, the pivot labels will display the volume accumulated since the previous pivot.", group = group_2, inline = "7")

// @variable If `true`, each pivot label will display the change in price from the previous pivot.

bool showChgInput = input.bool(true, "Display Reversal Price Change",

tooltip = "If checked, the pivot labels will display the change in price from the previous pivot.", group = group_2, inline = "8")

// @variable Controls whether the labels show price changes as raw values or percentages when `showChgInput` is `true`.

string priceDiffInput = input.string("Absolute", "", options = ,

tooltip = "Controls whether the labels show price changes as raw values or percentages when 'Display Reversal Price Change' is checked.",

group = group_2, inline = "8")

// @variable If `true`, the Zig Zag will display support and resistance lines.

bool showSupportResistanceInput = input.bool(true, "Show Support/Resistance Lines",

tooltip = "If checked, the Zig Zag will display support and resistance lines.", group = group_2, inline = "9")

// @variable The number of bars to extend the support and resistance lines from the last pivot point.

int supportResistanceOffsetInput = input.int(50, "Support/Resistance Offset", minval = 0,

tooltip = "The number of bars to extend the support and resistance lines from the last pivot point.", group = group_2, inline = "10")

// @variable The width of the support and resistance lines.

int supportResistanceWidthInput = input.int(1, "Support/Resistance Width", minval = 1,

tooltip = "The width of the support and resistance lines.", group = group_2, inline = "11")

// @variable The color of the support lines.

color supportColorInput = input.color(color.red, "Support/Resistance Color", group = group_2, inline = "12")

// @variable The color of the resistance lines.

color resistanceColorInput = input.color(color.green, "", group = group_2, inline = "12",

tooltip = "The color of the support/resistance lines.")

// @variable If `true`, the support and resistance lines will be drawn as zones.

bool showSupportResistanceZoneInput = input.bool(true, "Show Support/Resistance Zones",

tooltip = "If checked, the support and resistance lines will be drawn as zones.", group = group_2, inline = "12-1")

// @variable The color of the support zones.

color supportZoneColorInput = input.color(color.new(color.red, 70), "Support Zone Color", group = group_2, inline = "12-2")

// @variable The color of the resistance zones.

color resistanceZoneColorInput = input.color(color.new(color.green, 70), "", group = group_2, inline = "12-2",

tooltip = "The color of the support/resistance zones.")

// @variable The width of the support and resistance zones.

int supportResistanceZoneWidthInput = input.int(10, "Support/Resistance Zone Width", minval = 1,

tooltip = "The width of the support and resistance zones.", group = group_2, inline = "12-3")

// @variable If `true`, the support and resistance lines will extend to the right of the chart.

bool supportResistanceExtendInput = input.bool(false, "Extend to Right",

tooltip = "If checked, the lines will extend to the right of the chart.", group = group_2, inline = "13")

// @variable References a `Settings` instance that defines the `ZigZag` object's calculation and display properties.

var ZIG.Settings settings =

ZIG.Settings.new(

devThreshold = deviationInput,

depth = depthInput,

lineColorUp = lineColorUpInput,

lineColorDown = lineColorDownInput,

textUpColor = lineColorUpInput,

textDownColor = lineColorDownInput,

lineWidth = lineWidthInput,

extendLast = extendInput,

displayReversalPrice = showPriceInput,

displayCumulativeVolume = showVolInput,

displayReversalPriceChange = showChgInput,

differencePriceMode = priceDiffInput,

draw = showZigZag,

allowZigZagOnOneBar = allowZigZagOnOneBarInput,

drawSupportResistance = showSupportResistanceInput,

supportResistanceOffset = supportResistanceOffsetInput,

supportResistanceWidth = supportResistanceWidthInput,

supportColor = supportColorInput,

resistanceColor = resistanceColorInput,

supportResistanceExtend = supportResistanceExtendInput,

supportResistanceZoneWidth = supportResistanceZoneWidthInput,

drawSupportResistanceZone = showSupportResistanceZoneInput,

supportZoneColor = supportZoneColorInput,

resistanceZoneColor = resistanceZoneColorInput

)

// @variable References a `ZigZag` object created using the `settings`.

var ZIG.ZigZag zigZag = ZIG.newInstance(settings)

// Update the `zigZag` on every bar.

zigZag.update()

//#endregion

The example code demonstrates how to create a ZigZag indicator with customizable settings. It:

1. Creates a Settings object with user-defined parameters

2. Instantiates a ZigZag object using these settings

3. Updates the ZigZag on each bar to detect new pivot points

4. Automatically draws lines and labels when pivots are detected

This approach provides maximum flexibility while maintaining readability and ease of use.

ZRK 30m This TradingView indicator draws alternating 30-minute boxes aligned precisely to real clock times (e.g., 10:00, 10:30, 11:00), helping traders visually segment intraday price action. It highlights every other 30-minute block with customizable colors, line styles, and opacity, allowing users to clearly differentiate between trading intervals. The boxes automatically adjust based on the chart’s timeframe, maintaining accuracy on 1-minute to 60-minute charts. Optional time labels can also be displayed for additional context. This tool is useful for identifying patterns, measuring volatility, or applying breakout strategies based on defined, consistent time windows across global trading sessions.

Custom TABI Model with LayersCustom Top and Bottom Indicator (TABI) (Is a Trend Adaptive Blow-Off Indicator) -

User Guide & Description

Introduction

The TABI (Trend Adaptive Blow-Off Indicator) is a refined, multi-layered RSI tool designed to enhance trend analysis, detect momentum shifts, and highlight overbought/oversold conditions with a more nuanced, color-coded approach. This indicator is useful for traders seeking to identify key reversal points, confirm trend strength, and filter trade setups more effectively than traditional RSI.

By incorporating volume-based confirmation and divergence detection, TABI aims to reduce false signals and improve trade timing.

How It Works

TABI builds on the Relative Strength Index (RSI) by introducing:

A smoothed RSI calculation for better trend readability.

11 color-coded RSI levels, allowing traders to visually distinguish weak, neutral, and extreme conditions.

Volume-based confirmation to detect high-conviction moves.

Bearish & Bullish Divergence Detection, inspired by Market Cipher methods, to spot potential reversals early.

Overbought & Oversold alerts, with optional candlestick color changes to highlight trade signals.

Key Features

✅ Color-Coded RSI for Better Readability

The RSI is divided into multi-layered color zones:

🔵 Light Blue: Extremely oversold

🟢 Lime Green: Mild oversold, potential trend reversal

🟡 Yellow & Orange: Neutral, momentum consolidation

🟠 Dark Orange: Caution, overbought conditions developing

🔴 Red: Extreme overbought, possible exhaustion

✅ Divergence Detection

Bearish Divergence: Price makes higher highs, RSI makes lower highs → Potential top signal

Bullish Divergence: Price makes lower lows, RSI makes higher lows → Potential bottom signal

✅ Volume Confirmation Filter

Requires a 50% above-average volume spike for strong buy/sell signals, reducing false breakouts.

✅ Dynamic Labels & Alerts

🚨 Blow-Off Top Warning: If RSI is overbought + volume spikes + divergence detected

🟢 Oversold Bottom Alert: If RSI is oversold + bullish divergence

Candlestick color changes when extreme conditions are met.

How to Use

📌 Entry & Exit Signals

Buy Consideration:

RSI enters Green Zone (oversold)

Bullish divergence detected

Volume confirms the move

Sell Consideration:

RSI enters Red Zone (overbought)

Bearish divergence detected

Volume confirms exhaustion

📌 Trend Confirmation

Use the yellow/orange levels to confirm strong trends before entering counter-trend trades.

📌 Filtering Trade Noise

The RSI smoothing helps reduce false whipsaws, making it easier to read true momentum shifts.

Customization Options

🔧 User-Defined RSI Thresholds

Adjust the overbought/oversold levels to match your trading style.

🔧 Divergence Sensitivity

Modify the lookback period to fine-tune divergence detection accuracy.

🔧 Volume Thresholds

Set custom volume multipliers to control confirmation requirements.

Why This is Unique

🔹 Unlike traditional RSI, TABI visually maps RSI zones into layered gradients, making it easy to spot momentum shifts.

🔹 The multi-layered color scheme adds an intuitive, heatmap-like effect to RSI, helping traders quickly gauge conditions.

🔹 Incorporates CCF-inspired divergence detection and volume filtering, making signals more robust.

🔹 Dynamic labeling system ensures clarity without cluttering the chart.

Alerts & Notifications

🔔 TradingView Alerts Included

🚨 Blow-Off Top Detected → RSI overbought + volume spike + bearish divergence.

🟢 Oversold Bottom Detected → RSI oversold + bullish divergence.

Set alerts to receive notifications without watching the charts 24/7.

Final Thoughts

TABI is designed to simplify RSI analysis, provide better trade signals, and improve decision-making. Whether you're day trading, swing trading, or long-term investing, this tool helps you navigate market conditions with confidence.

🔥 Use it to detect high-probability reversals, confirm trends, and improve trade entries/exits! 🚀

Hierarchical + K-Means Clustering Strategy===== USER GUIDE =====

Hierarchical + K-Means Clustering Strategy

OVERVIEW:

This strategy combines hierarchical clustering and K-means algorithms to analyze market volatility patterns

and generate trading signals. It uses a modified SuperTrend indicator with ATR-based volatility clustering

to identify potential trend changes and market conditions.

KEY FEATURES:

- Advanced volatility analysis using hierarchical clustering and K-means algorithms

- Modified SuperTrend indicator for trend identification

- Multiple filter options including moving average and ADX trend strength

- Volume-based exit mechanism to protect profits

- Customizable appearance settings

SETTINGS EXPLANATION:

1. SuperTrend Settings:

- ATR Length: Period for ATR calculation (default: 11)

- SuperTrend Factor: Multiplier for ATR to determine trend bands (default: 3)

2. Hierarchical Clustering Settings:

- Training Data Length: Number of bars used for clustering analysis (default: 200)

3. Appearance Settings:

- Transparency 1 & 2: Control the opacity of trend lines and fills

- Bullish/Bearish Color: Colors for uptrend and downtrend visualization

4. Time Settings:

- Start Year/Month: Define when the strategy should start executing trades

5. Filter Settings:

- Moving Average Filter: Uses SMA to filter trades (only enter when price is on correct side of MA)

- Trend Strength Filter: Uses ADX to ensure trades are taken in strong trend conditions

6. Volume Stop Loss Settings:

- Volume Ratio Threshold: Controls sensitivity of volume-based exits

- Monitoring Delay Bars: Number of bars to wait before monitoring volume for exit signals

HOW TO USE:

1. Apply the indicator to your chart

2. Adjust settings according to your trading preferences and timeframe

3. Long signals appear when price crosses above the SuperTrend line (▲k marker)

4. Short signals appear when price crosses below the SuperTrend line (▼k marker)

5. The strategy automatically manages exits based on volume balance conditions

INTERPRETATION:

- Green line/area: Bullish trend - consider long positions

- Red line/area: Bearish trend - consider short positions

- Yellow line: Moving average for additional trend confirmation

- Volume balance exits occur when buying/selling pressure equalizes

RECOMMENDED TIMEFRAMES:

This strategy works best on 1H, 4H, and daily charts for most markets.

For highly volatile assets, shorter timeframes may also be effective.

RISK MANAGEMENT:

Always use proper position sizing and consider setting additional stop losses

beyond the strategy's built-in exit mechanisms.

===== END OF USER GUIDE =====

TEMA OBOS Strategy PakunTEMA OBOS Strategy

Overview

This strategy combines a trend-following approach using the Triple Exponential Moving Average (TEMA) with Overbought/Oversold (OBOS) indicator filtering.

By utilizing TEMA crossovers to determine trend direction and OBOS as a filter, it aims to improve entry precision.

This strategy can be applied to markets such as Forex, Stocks, and Crypto, and is particularly designed for mid-term timeframes (5-minute to 1-hour charts).

Strategy Objectives

Identify trend direction using TEMA

Use OBOS to filter out overbought/oversold conditions

Implement ATR-based dynamic risk management

Key Features

1. Trend Analysis Using TEMA

Uses crossover of short-term EMA (ema3) and long-term EMA (ema4) to determine entries.

ema4 acts as the primary trend filter.

2. Overbought/Oversold (OBOS) Filtering

Long Entry Condition: up > down (bullish trend confirmed)

Short Entry Condition: up < down (bearish trend confirmed)

Reduces unnecessary trades by filtering extreme market conditions.

3. ATR-Based Take Profit (TP) & Stop Loss (SL)

Adjustable ATR multiplier for TP/SL

Default settings:

TP = ATR × 5

SL = ATR × 2

Fully customizable risk parameters.

4. Customizable Parameters

TEMA Length (for trend calculation)

OBOS Length (for overbought/oversold detection)

Take Profit Multiplier

Stop Loss Multiplier

EMA Display (Enable/Disable TEMA lines)

Bar Color Change (Enable/Disable candle coloring)

Trading Rules

Long Entry (Buy Entry)

ema3 crosses above ema4 (Golden Cross)

OBOS indicator confirms up > down (bullish trend)

Execute a buy position

Short Entry (Sell Entry)

ema3 crosses below ema4 (Death Cross)

OBOS indicator confirms up < down (bearish trend)

Execute a sell position

Take Profit (TP)

Entry Price + (ATR × TP Multiplier) (Default: 5)

Stop Loss (SL)

Entry Price - (ATR × SL Multiplier) (Default: 2)

TP/SL settings are fully customizable to fine-tune risk management.

Risk Management Parameters

This strategy emphasizes proper position sizing and risk control to balance risk and return.

Trading Parameters & Considerations

Initial Account Balance: $7,000 (adjustable)

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 128

Deep Test Results (2024/11/01 - 2025/02/24)BTCUSD-5M

Total P&L:+1638.20USD

Max equity drawdown:694.78USD

Total trades:128

Profitable trades:44.53

Profit factor:1.45

These settings aim to protect capital while maintaining a balanced risk-reward approach.

Visual Support

TEMA Lines (Three EMAs)

Trend direction is indicated by color changes (Blue/Orange)

ema3 (short-term) and ema4 (long-term) crossover signals potential entries

OBOS Histogram

Green → Strong buying pressure

Red → Strong selling pressure

Blue → Possible trend reversal

Entry & Exit Markers

Blue Arrow → Long Entry Signal