Pair Correlation Master [Macro]The Main Idea

Trading represents a constant battle between Systemic Flows (the whole market moving together) and Idiosyncratic Moves (one specific asset moving on its own).

This tool allows you to monitor a "basket" of 4 assets simultaneously (e.g., the major USD pairs). It answers the most important question in forex and multi-asset trading: "Is this move happening because the Dollar is weak, or because the Euro is strong?"

It separates the "Signal" (the unique move) from the "Noise" (the herd movement).

1. The Chart Lines: The "Race" (Macro Trend)

Think of the lines on your chart as a long-distance race. They visualize the performance of all 4 assets over the last 200 candles (adjustable).

- Bunched Together: If all lines are moving in the same direction, the market is highly correlated. (e.g., "The Dollar is selling off everywhere").

- Fanning Out: If the lines are spreading apart, specific currencies are outperforming others.

- The Zero Line: This is the starting line.

--- Above 0: The pair is in a macro uptrend.

--- Below 0: The pair is in a macro downtrend.

2. The Dashboard: The "Health Check" (Micro Data)

The table in the top right gives you the immediate statistics for right now.

- A. The Z-Score (The Rubber Band)

This measures how "stretched" price is compared to its normal behavior.

- White (< 2.0): Normal trading activity.

- Orange (> 2.0): The price is stretching. Warning sign.

- Red (> 3.0): Critical Stretch. The rubber band is pulled to its limit. Statistically, a pullback or pause is highly likely.

B. The Star (★)

The script automatically calculates the average behavior of your group. If one asset is behaving completely differently from the rest, it marks it with a Star (★).

- Example: EURUSD, GBPUSD, and NZDUSD are flat, but AUDUSD is rallying hard. AUDUSD gets the ★. This is where the unique opportunity lies.

🎯 Best Uses: 4H & Daily Timeframes

This indicator is tuned for "Macro" analysis. It works best on the "4-Hour" and "Daily" charts to filter out intraday noise and capture swing trading moves.

- Strategy 1: The "Rubber Band" Snap (Mean Reversion)

- Setup: Look for a Z-Score in the RED (> 3.0) on the Daily timeframe.

- Action: This indicates an unsustainable move. Look for reversals or exhaustion patterns to trade against the trend back toward the mean.

- Strategy 2: The "Lone Wolf" (Trend Following)

- Setup: Look for the asset with the Star (★).

- Action: If the whole basket is flat (Balanced), but the Star asset is breaking out, that creates a high-quality trend trade because that specific currency has its own catalyst (News/Earnings).

- Strategy 3: Systemic Flows (Basket Trading)

- Setup: The dashboard footer says "⚠️ SYSTEMIC MOVE."

- Action: This means everything is moving together (e.g., a massive USD crash). Don't look for unique setups; just join the trend on the strongest pair.

Dashboard Footer Key

The bottom of the table summarizes the current state of the market for you:

- Balanced / Rangebound: The market is quiet. Good for range trading.

- Focus: : Trade this specific pair. It is moving independently.

- Systemic Move: The whole basket is moving violently. Trade the momentum.

p.s. Suggestion - apply and use on the chart rather than an oscillator.

Statistics

Range-scannerThis indicator shows you the range of the chart based on your specifications in minutes. For example, if you set 30 minutes, the indicator will show you the range of the last 30 minutes in real time, as well as the high and low prices for the same period.

NeuralFlow Forecast Engine™ | SPY Weekly NeuralFlow Forecast Engine™ | SPY Weekly

AI-adaptive market equilibrium & expansion mapping. NeuralFlow doesn’t forecast by direction — it forecasts by where markets prefer to stabilize.

NeuralFlow Forecast Engine™ is a proprietary Artificial Intelligence framework trained to identify where price is statistically inclined to rebalance and where expansion zones historically exhaust rather than extend.

What the Bands Represent

Band Layer Meaning

AI Equilibrium (white core) Primary weekly balance zone where price is most likely to mean-revert

Predictive Rails (aqua / purple) High-confidence corridor of institutional flow containment

Outer Zones (green / red) Expansion limits where continuation historically decays

Extreme Zones (top/bottom) Rare deviation envelope where auction completion is statistically favored

NeuralFlow operates on proprietary, institution-grade Artificial Intelligence models trained specifically to map statistical rebalancing behavior, not trader predictions or sentiment. No discretionary drawing. No correlations. No lagging overlays.

This engine updates only when underlying structure changes — not when candles fluctuate intraday.

⚠ Risk & Use Notice

NeuralFlow Forecast Engine™ provides AI-derived structural zones, not trade signals or financial advice.

Markets can behave outside modeled distributions, especially during macro catalysts, thin liquidity, or surprise volatility events.

By loading or using this indicator, the user acknowledges full responsibility for any trades or outcomes based on its interpretation.

Educational & analytical use only. Not financial advice.

Optimal Trading ReplayOptimal Trading Replay

---------------------------------------------------------

This indicator helps you visualize your executed trades directly on the TradingView chart.

// Features:

// - Imports your trade list (CSV-style text input)

// - Plots entries, exits, and direction arrows

// - Draws P&L summary boxes on chart

// - Useful for replay, journaling, and verification

NQ H1 Stats+NQ H1 Stats - Detailed Prob & Excursion Indicator

Overview

NQ H1 Stats - Detailed Prob & Excursion is a specialized statistical overlay indicator for TradingView, tailored for the Nasdaq futures (NQ) on a 1-hour timeframe. It provides real-time insights into the probability of price returning to the hourly open after sweeping the previous hour's high (PHH) or low (PHL), based on historical data segmented by hour and 20-minute intervals. The indicator visualizes these sweeps with lines, labels, circles, background fills, and "excursion zones" (also called "Magic Boxes") that highlight median/mean extensions post-sweep, along with percentile lines (75th, 90th, 95th) for gauging potential "pain" or extreme moves. This tool is designed for intraday traders focusing on liquidity sweeps, or mean-reversion setups, helping to quantify edge based on empirical probabilities and volatility excursions.

The data is hardcoded from extensive historical analysis of NQ behavior (e.g., probabilities range from ~7% to ~91%, with sample sizes up to 2000+ per segment), making it a backtested reference rather than dynamic learning. It emphasizes visual clarity during active hours, with options to filter for Regular Trading Hours (RTH: 09:00–15:59 ET) or high-probability (>70%) events only. Note: This is an educational tool for analyzing market structure; it does not predict future performance or provide trading signals/advice. Past data does not guarantee future results, and users should backtest on current conditions (as of December 2025 data availability) and use at their own risk, in compliance with TradingView's house rules.

Key Features

• Sweep Detection & Probability Labels: Identifies when price breaks PHH (upside) or PHL (downside), displaying a centered label with probability of returning to the hourly open, sample size (N), time of sweep, and a checkmark (✅) if the open is retested post-sweep.

• Visual Lines & Markers: Draws hourly open (h.o.), PHH, and PHL lines with customizable styles/colors; adds small circles on sweep bars for quick spotting.

• Breakout→Open Background Fill: Shaded zone from sweep bar until price returns to open, visualizing extension duration and retracement.

• Excursion (Pain) Zone - "Magic Box": Post-sweep box showing median/mean extension percentages, colored dynamically by probability (green high, orange mid, red low); includes dashed lines for 75th/90th/95th percentiles to mark statistical extremes.

• Time-Segmented Data: Probabilities and excursions vary by hour (0-23) and 20-min segments (0-19 min: _0, 20-39: _1, 40-59: _2), capturing intraday nuances (e.g., higher probs in early/late hours).

• Filters for Focus: RTH-only mode hides non-session elements; high-prob-only shows >70% events to reduce noise.

• Alerts: Triggers on PHH/PHL sweeps with messages for chart checks.

How It Works

• Data Foundation: Uses pre-computed maps for probabilities (prob_high_taken/prob_low_taken), sample sizes, and excursions (mean, median, p75/p90/p95 as percentages of open). Data is initialized on the first bar via f_init_high_data() and f_init_low_data(), covering 24 hours with 3 segments each (e.g., key "9_1" for 09:20-09:39). Probabilities represent historical likelihood of price returning to open after sweep; excursions quantify average/rare extensions (e.g., 0.156% mean = 0.156% of open price).

• Period Detection: On new 1H bars (new_period_bar), resets visuals, draws lines for open/PHH/PHL extending 1 hour forward, and labels if enabled. Uses request.security on standard ticker for real OHLC, bypassing chart transformations (e.g., Heikin Ashi).

• Sweep Logic: On each bar, checks if real high > PHH or real low < PHL. If so, fetches segment-specific data (hour + floor(minute/20)), displays probability label centered mid-hour. Skips if filtered (RTH-only or <70% prob).

• Excursion Visualization: If enabled, draws "Magic Box" from 1-min to 58-min into the hour, bounded by mean/median levels (top/bottom adjusted for high/low sweep). Adds percentile lines with labels (e.g., "75%") at right end. Box color reflects prob strength for quick bias assessment.

• Retest Check: Monitors for open retest post-sweep (high/low cross open, or gap scenarios from prev bar). Adds ✅ to label if hit on subsequent bars (skips sweep bar to avoid false positives). Stops background fill on retest or at 58-min mark.

• Background Fill: Activates on sweep, shades until retest, using user color.

• Cleanup & Performance: Manages labels in arrays, clears on new periods; no excess drawing beyond max counts (500 lines/labels/boxes).

This setup "meshes" statistical backtesting with real-time visualization: Hardcoded data provides empirical probabilities/excursions (reducing subjectivity in breakouts), while dynamic elements (lines, fills, boxes) overlay structure on the chart. It helps traders assess if a sweep is "high-edge" (e.g., >70% prob of revert) or likely to run (low prob, high excursion), blending historical context with current price action for informed decisions.

Settings and Customization

Inputs are grouped for ease:

1. Settings:

o Show RTH Only (9:00-15:59): Restricts to main session (default: false; tooltip: for RTH-focused stats).

o Show High Prob Only (>70%): Filters low-prob sweeps visually (default: false; tooltip: highlights confidence).

2. Visuals:

o Show Line Labels: Toggle "h.o."/ "phh"/ "phl" (default: true).

o Period Open Line Color: Gray 50% (default).

o Previous High/Low Line Colors: Gray 100% (default).

o Open Line Style/Width: Dotted/1 (default; options: Solid/Dotted/Dashed).

3. Breakout→Open Background:

o Show Breakout→Open Background: Toggle fill (default: true).

o Fill Color: Teal 85% (default).

4. Breakout Circles:

o Show Breakout Circles: Toggle (default: true).

o PHH/PHL Break Circle Colors: White 20% (default).

5. Info Label Style:

o Text Size: Small (default; options: Auto/Tiny/Normal/Large/Huge).

o Label Text Color: White (default).

o Low/Mid/High Probability Colors: Red 20%/Orange 20%/Green 20% (default).

6. Excursion (Pain) Zone:

o Show Excursion Zone: Toggle Magic Box (default: true).

o Excursion Box Color: Gray 75% (default; dynamic overrides).

o 75th/90th/95th Percentile Lines: Orange 30%/Red 30%/Dark Red 100% (default).

No additional tables/plots; all elements are lines/labels/boxes for overlay focus.

Usage Tips

• Breakout Trading: Watch for sweeps with high prob (>70%, green label) as potential fades back to open; low prob (red) may signal runs—use excursion box for targets (e.g., exit at 90th percentile for extremes).

• Time Awareness: Probabilities peak in open hours (e.g., 09:00 ~90%+ for initial sweeps) and drop in off-hours; segments capture momentum shifts (e.g., _2 often lower prob).

• RTH Focus: Enable for cleaner stats during high-liquidity sessions; disable for 24/7 view.

• Visual Filtering: Use high-prob-only in volatile conditions to avoid noise; combine with volume or other indicators for confirmation.

• Alerts Integration: Set TradingView alerts on sweeps; check label for prob/N before acting.

• Chart Setup: Best on 1H or lower NQ charts; adjust text size for readability on mobiles.

• Backtesting: Manually review historical sweeps against data maps to validate; update hardcoded values if new data emerges (as of 2025).

Limitations

• Fixed Data: Hardcoded stats may not reflect recent market changes (e.g., post-2025 volatility shifts); not adaptive.

• Reactive Only: Detects sweeps after they occur; no predictive signals.

• Timeframe Specific: Locked to 1H logic; may not translate to other assets/TFs without recoding data.

• Visual Clutter: On busy charts, labels/boxes may overlap—toggle off selectively.

• No Live Stats: Sample sizes are historical; real-time N/prob not updated.

• Gaps & Extremes: Handles gaps in retest logic, but rare events (e.g., news) may exceed 95th percentile.

Disclaimer

This indicator is for informational and educational purposes only. Trading involves significant risk of loss and is not suitable for all investors. The hardcoded data represents past NQ performance and does not guarantee future outcomes. No claims of profitability are made—results depend on market conditions, user strategy, and risk management. Consult a financial advisor before trading, and backtest extensively. Abiding by TradingView rules, this tool provides no investment recommendations.

TMT Support & Resistance - Hitesh NimjeTMT Support & Resistance - HiteshNimje Indicator

Overview

The TMT Support & Resistance indicator is a professional pivot point analysis tool that automatically calculates and displays key support and resistance levels across multiple timeframe perspectives. It offers various pivot point calculation methods and provides customizable visual elements for comprehensive technical analysis.

Key Features

Pivot Point Calculation Methods

1. Traditional Pivot Points

Standard pivot point calculation using Previous Period High, Low, and Close

Creates P, S1, S2, S3, R1, R2, R3 levels

Most widely used method for day trading and swing trading

2. Fibonacci Pivot Points

Incorporates Fibonacci retracement levels (38.2%, 61.8%)

Uses traditional pivot as base with Fibonacci extensions

Popular among traders following Fibonacci analysis

3. Woodie Pivot Points

Alternative calculation method with different weighting

Emphasizes opening price in calculations

Preferred by some intraday traders

4. Classic Pivot Points

Similar to traditional but with different level calculations

Balanced approach to support/resistance identification

Timeframe Options

* Auto: Automatically selects optimal timeframe based on chart timeframe

Intraday ≤15min → Daily

Intraday >15min → Weekly

Daily → Monthly

* Fixed Timeframes: Daily, Weekly, Monthly, Quarterly, Yearly

* Extended Periods: Biyearly, Triyearly, Quinquennially, Decennially

Level Management System

Support Levels (Blue Colored)

* TMT Support 1 (S1): First major support level

* TMT Support 2 (S2): Second support level

* TMT Support 3 (S3): Third support level

* TMT Support 4 (S4): Fourth support level (Traditional/Camarilla only)

* TMT Support 5 (S5): Fifth support level (Traditional/Camarilla only)

Resistance Levels (Black Colored)

* TMT Resistance 1 (R1): First major resistance level

* TMT Resistance 2 (R2): Second resistance level

* TMT Resistance 3 (R3): Third resistance level

* TMT Resistance 4 (R4): Fourth resistance level (Traditional/Camarilla only)

* TMT Resistance 5 (R5): Fifth resistance level (Traditional/Camarilla only)

Central Pivot (Orange Colored)

* Pivot Point (P): Central price level used for S/R calculations

Customization Options

Display Settings

* Show Labels: Toggle pivot level identification labels

* Show Prices: Display actual price values next to levels

* Labels Position: Choose between Left or Right positioning

* Line Width: Adjustable thickness (1-100 pixels) for all pivot lines

Data Source Options

* Use Daily-based Values:

ON: Uses official daily OHLC values for calculations

OFF: Uses intraday data with extended hours consideration

* Number of Pivots Back: Historical pivot display (1-200 levels)

Color Customization

* Individual color selection for each support/resistance level

* Default colors: Supports (Blue), Resistances (Black), Pivot (Orange)

* Full color picker integration for all levels

Technical Features

Smart Display Logic

* Intraday Charts: Automatically uses daily-based calculations when intraday data is insufficient

* Multi-timeframe Compatibility: Adapts to chart timeframe and pivot timeframe differences

* Extended Hours Handling: Incorporates extended trading hours when enabled on chart

Dynamic Level Management

* Real-time Updates: Levels update as new data becomes available

* Historical Tracking: Maintains configurable number of historical pivot periods

* Automatic Cleanup: Removes old pivot graphics when limit is exceeded

Visual Elements

* Time-based Lines: Lines extend across full time periods for clear visual reference

* Price Labels: Contextual information showing level names and prices

* Professional Styling: Clean, professional appearance suitable for any trading style

Use Cases

Day Trading Applications

* Session Management: Use daily pivots for intraday trading decisions

* Range Trading: Camarilla levels excellent for range-bound strategies

* Breakout Confirmation: Use pivot breaks as entry/exit signals

Swing Trading Applications

* Weekly/Monthly Pivots: Identify key levels for multi-day positions

* Trend Analysis: Track how price interacts with higher timeframe pivots

* Risk Management: Set stop-losses and take-profits at pivot levels

Long-term Trading Applications

* Quarterly/Yearly Pivots: Major institutional levels for position trading

* Support/Resistance Maps: Create comprehensive price level roadmap

* Market Structure Analysis: Understand price behavior around key levels

Benefits for Traders

Professional Analysis

* Multiple Methodologies: Choose pivot calculation that matches trading style

* Timeframe Flexibility: Analyze from multiple temporal perspectives

* Historical Context: See how price has historically responded to pivot levels

Risk Management

* Level Identification: Clear visual reference for stop-loss placement

* Position Sizing: Use pivot distances for risk/reward calculations

* Entry Timing: Identify optimal entry points near support/resistance

Market Understanding

* Psychological Levels: Understand where market participants react

* Volume Confirmation: Cross-reference pivot levels with volume data

* Trend Continuation: Identify pivot levels that may continue or reverse trends

Technical Specifications

* Pine Script Version: 6

* Overlay: True (displays on price chart)

* Performance: Optimized for up to 200 historical pivot periods

* Compatibility: All trading instruments and timeframes

* Data Source: OHLC-based pivot calculations with security function integration

Trading Strategy Integration

1. Support/Resistance Trading: Enter trades at S1/R1 with stops beyond S2/R2

2. Pivot Bounce Strategy: Trade bounces from established pivot levels

3. Range Trading: Use Camarilla pivots for tight range strategies

4. Breakout Strategy: Enter breakouts with confirmation from pivot breaks

5. Multiple Timeframe Analysis: Combine daily, weekly, and monthly pivots for comprehensive analysis

This indicator serves as a comprehensive support and resistance analysis tool, providing traders with institutional-quality pivot point analysis across multiple calculation methods and timeframes. It combines professional-grade pivot point calculations with intuitive customization options, making it suitable for traders of all experience levels and trading styles.

TRADING DISCLAIMER

RISK WARNING

Trading involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge, and financial resources.

NO FINANCIAL ADVICE

This indicator is provided for educational and informational purposes only. It does not constitute:

* Financial advice or investment recommendations

* Buy/sell signals or trading signals

* Professional investment advice

* Legal, tax, or accounting guidance

LIMITATIONS AND DISCLAIMERS

Technical Analysis Limitations

* Pivot points are mathematical calculations based on historical price data

* No guarantee of accuracy of price levels or calculations

* Markets can and do behave irrationally for extended periods

* Past performance does not guarantee future results

* Technical analysis should be used in conjunction with fundamental analysis

Data and Calculation Disclaimers

* Calculations are based on available price data at the time of calculation

* Data quality and availability may affect accuracy

* Pivot levels may differ when calculated on different timeframes

* Gaps and irregular market conditions may cause level failures

* Extended hours trading may affect intraday pivot calculations

Market Risks

* Extreme market volatility can invalidate all technical levels

* News events, economic announcements, and market manipulation can cause gaps

* Liquidity issues may prevent execution at calculated levels

* Currency fluctuations, inflation, and interest rate changes affect all levels

* Black swan events and market crashes cannot be predicted by technical analysis

USER RESPONSIBILITIES

Due Diligence

* You are solely responsible for your trading decisions

* Conduct your own research before using this indicator

* Verify calculations with multiple sources before trading

* Consider multiple timeframes and confirm levels with other technical tools

* Never rely solely on one indicator for trading decisions

Risk Management

* Always use proper risk management and position sizing

* Set appropriate stop-losses for all positions

* Never risk more than you can afford to lose

* Consider the inherent risks of leverage and margin trading

* Diversify your portfolio and trading strategies

Professional Consultation

* Consult with qualified financial advisors before trading

* Consider your tax obligations and legal requirements

* Understand the regulations in your jurisdiction

* Seek professional advice for complex trading strategies

LIMITATION OF LIABILITY

Indemnification

The creator and distributor of this indicator shall not be liable for:

* Any trading losses, whether direct or indirect

* Inaccurate or delayed price data

* System failures or technical malfunctions

* Loss of data or profits

* Interruption of service or connectivity issues

No Warranty

This indicator is provided "as is" without warranties of any kind:

* No guarantee of accuracy or completeness

* No warranty of uninterrupted or error-free operation

* No warranty of merchantability or fitness for a particular purpose

* The software may contain bugs or errors

Maximum Liability

In no event shall the liability exceed the purchase price (if any) paid for this indicator. This limitation applies regardless of the theory of liability, whether contract, tort, negligence, or otherwise.

REGULATORY COMPLIANCE

Jurisdiction-Specific Risks

* Regulations vary by country and region

* Some jurisdictions prohibit or restrict certain trading strategies

* Tax implications differ based on your location and trading frequency

* Commodity futures and options trading may have additional requirements

* Currency trading may be regulated differently than stock trading

Professional Trading

* If you are a professional trader, ensure compliance with all applicable regulations

* Adhere to fiduciary duties and best execution requirements

* Maintain required records and reporting

* Follow market abuse regulations and insider trading laws

TECHNICAL SPECIFICATIONS

Data Sources

* Calculations based on TradingView data feeds

* Data accuracy depends on broker and exchange reporting

* Historical data may be subject to adjustments and corrections

* Real-time data may have delays depending on data providers

Software Limitations

* Internet connectivity required for proper operation

* Software updates may change calculations or functionality

* TradingView platform dependencies may affect performance

* Third-party integrations may introduce additional risks

MONEY MANAGEMENT RECOMMENDATIONS

Conservative Approach

* Risk only 1-2% of capital per trade

* Use position sizing based on volatility

* Maintain adequate cash reserves

* Avoid over-leveraging accounts

Portfolio Management

* Diversify across multiple strategies

* Don't put all capital into one approach

* Regularly review and adjust trading strategies

* Maintain detailed trading records

FINAL LEGAL NOTICES

Acceptance of Terms

* By using this indicator, you acknowledge that you have read and understood this disclaimer

* You agree to assume all risks associated with trading

* You confirm that you are legally permitted to trade in your jurisdiction

Updates and Changes

* This disclaimer may be updated without notice

* Continued use constitutes acceptance of any changes

* It is your responsibility to stay informed of updates

Governing Law

* This disclaimer shall be governed by the laws of the jurisdiction where the indicator was created

* Any disputes shall be resolved in the appropriate courts

* Severability clause: If any part of this disclaimer is invalid, the remainder remains enforceable

REMEMBER: THERE ARE NO GUARANTEES IN TRADING. THE MAJORITY OF RETAIL TRADERS LOSE MONEY. TRADE AT YOUR OWN RISK.

Contact Information:

* Creator: Hitesh_Nimje

* Phone: Contact@8087192915

* Source: Thought Magic Trading

© HiteshNimje - All Rights Reserved

This disclaimer should be prominently displayed whenever the indicator is shared, sold, or distributed to ensure users are fully aware of the risks and limitations involved in trading.

Self-Organized Criticality - Avalanche DistributionHere's all you need to know: This indicator applies Self-Organized Criticality (SOC) theory to financial markets, measuring the power-law exponent (alpha) of price drawdown distributions. It identifies whether markets are in stable Gaussian regimes or critical states where large cascading moves become more probable.

Self-Organized Criticality

SOC theory, introduced by Per Bak, Tang, and Wiesenfeld (1987), describes how complex systems naturally evolve toward critical (fragile) states. An example is a sand pile: adding grains creates avalanches whose sizes follow a power-law distribution rather than a normal distribution.

Financial markets exhibit similar behavior. Price movements aren't purely random walks—they display:

Fat-tailed distributions (more extreme events than Gaussian models predict)

Scale invariance (no characteristic avalanche size)

Intermittent dynamics (periods of calm punctuated by large cascades)

Power-Law Distributions

When a system is in a critical state, the probability of an avalanche of size s follows:

P(s) ∝ s^(-α)

Where:

α (alpha) is the power-law exponent

Higher α → distribution resembles Gaussian (large events rare)

Lower α → heavy tails dominate (large events common)

This indicator estimates α from the empirical distribution of price drawdowns.

Mathematical Method

1. Avalanche Detection

The indicator identifies local price peaks (highest point in a lookback window), then measures the percentage drawdown to the next trough. A dynamic ATR-based threshold filters out noise—small drops in calm markets count, but the bar rises in volatile periods.

2. Logarithmic Binning

Avalanche sizes are sorted into logarithmically-spaced bins (e.g., 1-2%, 2-4%, 4-8%) rather than linear bins. This captures power-law behavior across multiple scales - a 2% drop and 20% crash both matter. The indicator creates 12 adaptive bins spanning from your smallest to largest observed avalanche.

3. Bin-to-Bin Ratio Estimation

For each pair of adjacent bins, we calculate:

α ≈ log(N₁/N₂) / log(s₂/s₁)

Where N₁ and N₂ are avalanche counts, s₁ and s₂ are bin sizes.

Example: If 2% drops happen 4× more often than 4% drops, then α ≈ log(4)/log(2) ≈ 2.0.

We get 8-11 independent estimates and average them. This is more robust than fitting one line through all points—outliers can't dominate.

4. Rolling Window Analysis

Alpha recalculates using only recent avalanches (default: last 500 bars). Old data drops out as new avalanches occur, so the indicator tracks regime shifts in real-time.

Regime Classification

🟢 Gaussian α ≥ 2.8 Normal distribution behavior; large moves are rare outliers

🟡 Transitional 1.8 ≤ α < 2.8 Moderate fat tails; system approaching criticality

🟠 Critical 1.0 ≤ α < 1.8 Heavy tails; large avalanches increasingly common

🔴 Super-Critical α < 1.0 Extreme tail risk; system prone to cascading failures

What Alpha Tells You

Declining alpha → Market moving toward criticality; tail risk increasing

Rising alpha → Market stabilizing; returns to normal distribution

Persistent low alpha → Sustained fragility; heightened crash probability

Supporting Metrics

Heavy Tail %: Concentration of total drawdown in largest 10% of events

Populated Bins: Data coverage quality (11-12 out of 12 is ideal)

Avalanche Count: Sample size for statistical reliability

Limitations

This is a distributional measure, not a timing indicator. Low alpha indicates increased systemic risk but doesn't predict when a cascade will occur. Only that the probability distribution has shifted toward larger events.

How This Differs from the Per Bak Fragility Index

The SOC Avalanche Distribution calculates the power-law exponent (alpha) directly from price drawdown distributions - a pure mathematical analysis requiring only price data. The Per Bak Fragility Index aggregates external stress indicators (VIX, SKEW, credit spreads, put/call ratios) into a weighted composite score.

Technical Notes

Default settings optimized for daily and weekly timeframes on major indices

Requires minimum 200 bars of history for stable estimates

ATR-based dynamic sizing prevents scale-dependent bias

Alerts available for regime transitions and super-critical entry

References

Bak, P., Tang, C., & Wiesenfeld, K. (1987). Self-organized criticality: An explanation of the 1/f noise. Physical Review Letters.

Sornette, D. (2003). Why Stock Markets Crash: Critical Events in Complex Financial Systems. Princeton University Press.

Jenkins OscillatorAn oscillator designed to capture price movement relative to recent intra-candle volatility. Z-score normalization is applied to smoothed price and therefore should be read in terms of standard deviation AND direction.

MNQ Momentum Suite – Intraday Confluence Dashboard (1-5M)MNQ Momentum Suite is a multi-factor intraday momentum dashboard designed primarily for MNQ / NQ on the 1M–5M timeframes during the New York session.

Instead of staring at 3–4 separate indicators, this script combines them into one clean pane

DMI / ADX → who’s in control (+DI vs –DI) and how strong the move is

Momentum MA Slope (T3 or EMA) → directional bias and trend quality

Squeeze Logic (BB vs Keltner) → volatility compression & expansion zones

Composite Momentum Score (–4 to +4) → single number capturing total confluence

Color-coded Dashboard Table → instant Bull / Bear / Flat status for each component

Core Components

1️⃣ Composite Momentum (Main Histogram)

Score range : –4 to +4

Built from 4 building blocks :

DMI direction (Bull/Bear)

ADX strength above threshold

MA slope direction (up/down)

Squeeze direction (after it fires)

Interpretation:

+3 / +4 → strong bullish confluence

+1 / +2 → mild bullish bias

0 → mixed / no edge

–1 / –2 → mild bearish bias

–3 / –4 → strong bearish confluence

2️⃣ DMI / ADX Block

Uses ta.dmi() under the hood.

DI spread histogram (teal/orange) shows which side is in control.

White ADX line measures trend strength – higher = cleaner moves, low = chop.

3️⃣ Momentum MA Slope (T3 / EMA)

User can choose T3 or EMA for the slope engine.

Slope histogram color:

Aqua → MA sloping up (bull-friendly)

Fuchsia → MA sloping down (bear-friendly)

4️⃣ Squeeze (BB vs Keltner)

Yellow dots mark when Bollinger Bands are inside Keltner Channels (volatility squeeze).

When the squeeze releases and price closes on one side of both BB basis and Keltner basis, the script flags a bullish or bearish squeeze fire that feeds the composite score.

Dashboard Table (Top-Right) : The table gives a fast, text-based read of the environment:

DMI Dir – Bull / Bear / Flat

ADX – Numeric trend strength

Slope – Up / Down / Flat based on chosen MA

Squeeze – Building / Fired Up / Fired Down / Idle

Row text is color-coded:

Green when that metric is bull-friendly

Red when it is bear-friendly

Gray/white when neutral

This makes it very easy to glance at the table and see if the environment is mostly green (long-friendly) or mostly red (short-friendly).

Session & Histogram Controls

Use NY Session Filter?

When enabled, all logic is focused on the defined NY session (default 09:30–16:00 exchange time).

how Histograms Only in NY Session?

true → plots only during the NY session (good for live trading focus).

false → plots on all bars, including overnight, so you can study past days and pre-/post-market behavior.

Alerts

Two built-in alert conditions are provided:

Strong Bull Momentum – Composite ≥ 3 during the session.

Strong Bear Momentum – Composite ≤ –3 during the session.

Use these as “heads-up” momentum pings, then confirm with your own price-action, VWAP, HTF levels, and liquidity zones.

Recommended Use

Primary instruments: MNQ / NQ futures, but it can be applied to any intraday symbol.

Primary timeframes: 1M to 5M.

Designed as a confluence and filter tool, not a stand-alone entry system.

Works especially well combined with:

VWAP

10 EMA

Pre-NY and RTH highs/lows

FVG/IFVG and liquidity zones

As with any tool, this is not financial advice and does not guarantee results. Always combine with risk management and your own playbook.

CapitalFlowsResearch: Sensitivity AnalysisCapitalFlowsResearch: Sensitivity Analysis — Driver–Price Beta Gauge

CapitalFlowsResearch: Sensitivity Analysis is built to answer a very specific macro question:

“How sensitive is this price to moves in that driver, right now?”

The indicator compares bar-to-bar changes in a chosen “price” asset with a chosen “driver” (such as an equity index, yield, or cross-asset benchmark), and from that relationship derives a rolling measure of effective beta. That beta is then converted into a “band width” value, representing how much the price typically moves for a standardised shock in the driver, under current conditions.

You can choose whether the driver’s moves are treated in basis points, absolute terms, or percent changes, and optionally smooth the resulting band with a configurable moving average to emphasise structural shifts over noise. The two plotted lines—current band width and its moving average—form a simple yet powerful gauge of how tightly the price is currently “geared” to the driver.

In practice, this makes Sensitivity Analysis a compact tool for:

Tracking when a contract becomes more or less responsive to a key macro factor.

Comparing sensitivity across instruments or timeframes.

Framing expected move scenarios (“if the driver does X, this should roughly do Y”).

All of this is done without exposing the detailed beta or volatility math inside the script.

CapitalFlowsResearch: Returns Regime MapCapitalFlowsResearch: Returns Regime Map — Two-Asset Behaviour & Correlation Lens

CapitalFlowsResearch: Returns Regime Map is a two-asset regime overlay that shows how a primary market and a linked macro series are really moving together over short rolling windows. Instead of just eyeballing two separate charts, the tool classifies each bar into one of four states based on the combined direction of recent returns:

Up / Up

Up / Down

Down / Up

Down / Down

These states are calculated from aggregated, windowed returns (using configurable return definitions for each asset), then painted directly onto the price chart as background regimes. On top of that, the indicator monitors the correlation of the same return streams and can optionally tint periods where correlation sits within a user-defined “low-correlation” band—highlighting moments when the usual relationship between the two series is weak, unstable, or breaking down.

In practice, this turns the chart into a compact co-movement map: you can see at a glance whether price and rates (or any two chosen markets) are trending together, diverging in a meaningful way, or moving in choppy, low-conviction fashion. It’s especially powerful for macro traders who need to frame trades in terms of “risk asset vs. rates,” “index vs. volatility,” or similar pairs—while keeping the actual construction details of the regime logic abstracted.

CapitalFlowsResearch: CB LevelsCapitalFlowsResearch: CB Levels — Policy Path Mapping for STIR & Rates Traders

CapitalFlowsResearch: CB Levels provides a structured, policy-anchored framework for interpreting short-term interest rate futures. Instead of treating STIR pricing as an abstract number, the indicator converts central bank settings—such as the official cash rate, expected hike/cut increments, and basis adjustments—into a clear ladder of explicit rate levels. These levels are then projected directly onto the price chart as horizontal reference bands.

The tool automatically builds a series of future policy steps (e.g., +25bp, +50bp, –25bp, etc.) based on user-defined increments and direction, allowing traders to visualise where the current contract sits relative to hypothetical central bank actions. By plotting settlement levels and multiple forward steps, the script creates a transparent “policy grid” that traders can anchor against when evaluating mispricings, risk/reward asymmetry, or scenario outcomes.

Discreet labels—placed periodically to avoid clutter—identify each policy step in bp terms, making the chart readable even when zoomed out. Whether the mode is set to Cuts or Hikes, the tool instantly recalibrates the entire ladder, offering a consistent structure for comparing different contracts or central bank paths.

In practice, CB Levels acts as a policy-path overlay for futures traders, helping them contextualise market pricing relative to central bank intent, quantify potential repricing ranges, and understand where key inflection levels lie—without revealing the underlying calculation methods that generate the steps.

CapitalFlowsResearch: Vol RangesCapitalFlowsResearch: Vol Ranges — Multi-Timeframe ATR Expansion Map

CapitalFlowsResearch: Vol Ranges creates a structured volatility “roadmap” by projecting expected price extensions across multiple timeframes using ATR-based ranges. Instead of relying on a single ATR reading, the tool pulls in higher-timeframe volatility measures—such as daily and monthly expansions—and uses them to build a set of reference levels that anchor the current market against where it should trade under normal volatility conditions.

The script does two things simultaneously:

Projects volatility-derived target bands

It computes a set of upper and lower expansion levels (e.g., +100%, +50%, –50%, –100%) around prior closing levels on different timeframes. These levels act as structural markers for expected movement, allowing traders to quickly recognise when price is behaving within typical bounds or pressing into statistically stretched territory.

Displays a live dashboard for interpretation

A fully configurable on-chart table displays:

Recent volatility readings

Today's reference ranges

Distance from current price to each expansion level

Whether today's movement is expanding or contracting relative to prior volatility

This gives traders a compact situational summary without cluttering the price chart.

Optional high-timeframe projection lines can also be plotted directly on the chart, updating once per new day or new month, making it easy to visually align intraday price action with broader volatility structure.

In practical terms, Vol Ranges functions as a multi-timeframe volatility compass—highlighting when markets are trading inside normal ranges, when they are beginning to stretch, and when they may be entering conditions supportive of momentum or reversal behaviour. All core mechanics remain abstracted, preserving the proprietary nature of the volatility framework.

CapitalFlowsResearch: CS CorrelationCapitalFlowsResearch: CS Correlation — Multi-Asset Correlation Radar

CapitalFlowsResearch: CS Correlation provides a real-time view of how closely a chosen “base” market is moving relative to a basket of other assets. Instead of relying on a single method, the tool allows you to transform each series (price, log-price, normalized score, or short-term returns) before correlation is calculated. This gives traders the flexibility to analyse relationships on the basis most relevant to their strategy—whether they care about trend alignment, return co-movement, or standardized behaviour.

Each comparison asset is evaluated independently using a rolling lookback window, producing a clean set of correlation lines that update bar-by-bar. The tool is deliberately modular: symbols can be switched on or off individually, and the chart remains uncluttered while still capturing broad cross-asset dynamics. A compact on-chart legend displays the latest correlation reading for each active symbol, making it easy to interpret at a glance.

Conceptually, the indicator helps highlight when normally-linked assets begin to diverge, when new relationships begin to strengthen, or when markets move into low-correlation regimes often associated with macro shifts, liquidity changes, or turning points. It functions as a correlation heatmap in time-series form, offering structural insight without exposing the underlying computation or weighting logic.

CapitalFlowsResearch: PEMA ThresholdCapitalFlowsResearch: PEMA Threshold — Forward Regime Projection

CapitalFlowsResearch: PEMA Threshold extends the logic of the standard PEMA framework by not only identifying when price is in an extended regime, but also calculating the exact price levels where the next regime flip would occur. Instead of waiting for a signal to trigger, the tool projects the thresholds forward in real time, showing traders the points at which the current regime would shift from positive to negative extension (or vice versa).

Conceptually, the script takes the behaviour of price around its moving equilibrium and determines how far price would need to travel for the underlying extension score to breach its upper or lower band. These projected “flip prices” can be displayed as guide lines or labelled directly on the chart, providing a live map of where key behavioural shifts would take place.

This transforms PEMA from a reactive overlay into an anticipatory one—helping traders plan entries, stops, and scenario paths with a clear understanding of where the market’s statistical pressure points sit, without exposing the underlying calculations.

Shezab AlgoLabs EMA Trend UtilityOverview

This tool is a clean and practical EMA trend utility built to help traders quickly understand market direction, trend regime, and momentum shifts. It plots a fast EMA and slow EMA using a branded color theme and highlights transitions between bullish and bearish conditions. The script also includes optional visual crossover markers to make regime changes easier to spot.

How it works

The relationship between the fast and slow EMA is used to classify the trend environment:

When the fast EMA is above the slow EMA, the market is considered in a bullish phase.

When the fast EMA is below the slow EMA, the market is considered in a bearish phase.

The script also provides optional:

Colored bars reflecting trend direction

Crossover labels to highlight momentum shifts

Background cloud to visually emphasize trending or neutral conditions

Optional alerts for crossover events

These visual features help traders recognize potential trend transitions without implying a complete trading system.

How to use it

This tool is designed as a supplemental decision aid. Traders can combine it with their preferred structure analysis, volume tools, oscillators, or confirmation methods. The crossover markers and alerts highlight shifts in trend behavior but are informational rather than mechanical buy/sell signals. Users should apply their own risk-management and entry criteria.

Originality

This script goes beyond a standard EMA by combining multiple elements into a single, cohesive trend-clarification tool:

• regime coloring

• optional cloud regions

• crossover markers

• visual dynamic styling using a unified aesthetic palette

It is not a mashup of existing scripts; all components are integrated specifically to support traders who prefer a simple-yet-clear visual framework for understanding trend behavior.

Position Size Tool [Riley]Automatically determine number of shares for an entry. Quantity based on a stop set at the low of day for long positions or a stop set at the high of the day for short positions. As well as inputs like account balance risk per trade. Also includes a user-defined maximum for percentage of daily dollar volume to consume with entry.

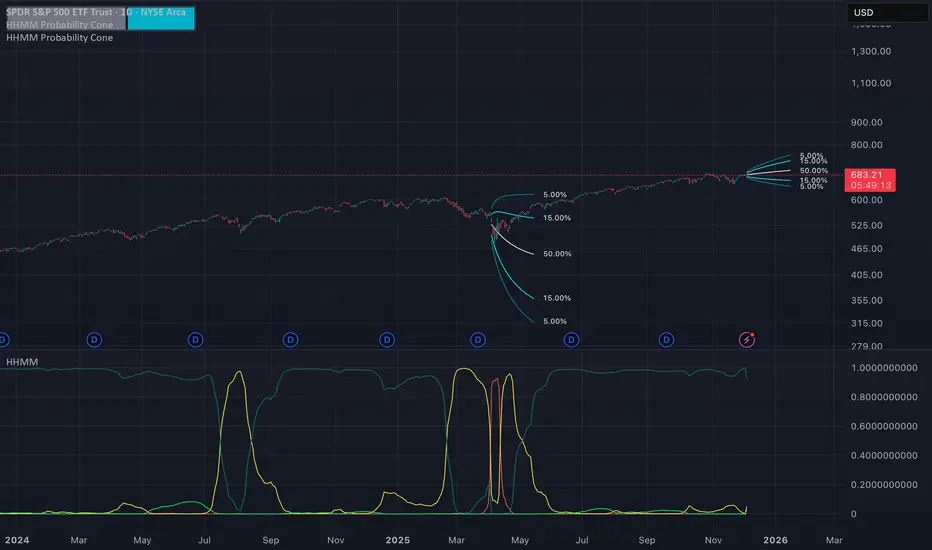

Hierarchical Hidden Markov Model - Probability Cone

The Hierarchical Hidden Markov Model - Probability Cone Indicator employs Hierarchical Hidden Markov Models for forecasting future price movements in financial markets. HHMMs are statistical tools that predict transitions between hidden states, such as different market regimes, based on observed data. This makes them valuable for understanding market behaviours and projecting future price trajectories. As discussed in the Hierarchical Hidden Markov Model indicator, HHMMs predict future states and their associated outputs based on the current state and model parameters. This tool is fundamentally very similar to the traditional HMM . The application of the HHMM for generating a probability cone forecast is therefore also fundamentally the same between HMM and HHMM. Despite their significant similarity I will go through the same fundamental examples of how probability cone is generated for the HHMM as I did for the HMM probability cone .

As you might know by now the probability cone indicator uses the knowledge about the current identified "state" or "regime" and with the help of transition probabilities, emission probabilities and initial probabilities generate a probabilistic forecast of the expected future price movements. To better understand the behind the Probability Cone we encourage you to use and learn about our free version of the Probability Cone as well as for even deeper understanding the Probability Cone Pro.

WHAT ARE REGIME DEPENDENT FORECASTS

We established that the indicator creates probabilistic forecasts of future price movements dependent on the current identified "state" or market "regime" via the Hidden Markov Model. In the image below we can see an example.

In this example we can see 4 different probability cones forecasting a 70% and 90% probability range (15% and 5% quantiles respectively). What you may notice is that the 4 probability cones look vastly different, despite using the same probability ranges as well as being generated from the same model trained on virtually the same data. What allows for this difference in the forecast, is conditioning the forecast on the current most likely identified state by the HHMM.

The first most cone is generating a forecast taking into account that the model identified the current market condition to be a extremely low in volatility this is a characteristic of the state identified by the light green coloured posterior probability. The second cone is significantly wider as well as has a negative drift, this is the case because that state identified by the red posterior probability is characterised by the most extreme volatility along with significant negative returns. The cone after that remains quite wide however is again associated with positive returns, this is characteristic of the state that the model identified via a high yelow coloured posterior probability. The last probability cone is again generated from a state that is characterised by quite low volatility albeit not the lowest. We can also see the state associated with that behaviour is identified by the high dark green posterior probability which is the highest at that time.

NOTE! Those are within sample forecasts, you can find more information on the difference between within sample model fit and out of sample prediction in the HHMM indicator description

This indicator also allows you to specify whether you wish to display probability based labels at the edges of the cone or whether you would prefer to display percent change based labels. With percent change labels you get the exact percentage value of the probabilistic increase or decrease of the price. See the example below

BARS BACK OFFSET vs DATE BASED OFFSET

The cones position can be offset by specifying the number of bars we wish to move it back similarly as with the rest of probability cone indicators. This indicator has however an additional, date based offset implemented. A user can therefore specify the position of the cone by specifying a date in the settings. The advantage of using the date based offset is that once it is turned on the user can also slide the cone up and down the chart with their mouse without having to manually adjust the date in the settings.

DIFFICULTIES WITH GENERATING FORECASTS (advanced):

The estimation of the probability cone, gets more difficult the more complex the model gets. A simple normal distribution probability cone can scale the distribution over time by simply multiplying the drift by the number of time steps and the volatility by the square root of time steps we wish to forecast for. More complex distributions often have to rely on mode advanced methods like convolutions, monte carlo or other kinds of approximations.

To estimate the probability cone forecast for the Hierarchial Hidden Markov Model, the indicator integrates two primary methodologies: Gaussian approximation and importance sampling. The Gaussian approximation is utilised for estimating the central 90% of future prices. This method provides a quick and efficient estimation within this central range, capturing the most likely price movements. The gaussian approximation will result in a forecast with an equal mean and variance as the true forecast, it will however not accurately reflect higher moments like skewness and kurtosis. For that reason the tail quantiles, which represent extreme price movements beyond the central range (90%), are estimated via importance sampling. This approach ensures a more accurate estimation of the skewness and kurtosis associated with extreme scenarios. While importance sampling leverages the flexibility of Monte Carlo as well as attempts to increase its efficiency by sampling from more precise areas of the distribution, the importance sampling may still underestimate most extreme quantiles associated with the lowest probabilities which is an inherent limitation of the indicator.

Example of gaussian approximation cone for probabilities above 5% (90% range):

Example of importance sampling cone for tail probabilities lower than 5% (beyond 90% range):

WARNING!

As per usual understand that the probabilities are estimations and best guesses based on the historical data and the patterns identified by the model and do not represent the true probability which is unknown in reality.

Settings:

- Source: Data source used for the model

- Forecast Period: Number of bars ahead for generating forecasts.

- Simulation Number: Number of Monte Carlo simulations to run in the case of importance sampling

-Body Probability: Specifies the inner range of the probability cone. The probability specifies the ammount of observations that are expected to fall outside of this range

- Tail Probability: Specifies the outter range of the probability cone. When this probability is under 5%, importance sampling will turn on

- Lock Cone: When ticked on, the cone will be locked at its current position.

- Offset Cone Based on Date: When ticked on, the position of the cone will be determined by the selected date.

- Offset: When "Offset Cone Based on Date" is turned off, you can use offset setting to specify the position of the cone projection.

- Date: When "Offset Cone Based on Date" is turned on, you can use the date setting to specify the date from which the forecast starts.

- Reestimate Model Every N Bars: This is especially useful if you wish to use the indicator on lower timeframes where model estimation might take longer than for the new datapoint to arrive. In that case you can specify after how many bars the model should be reestimated.

- Training Period: Length of historical data used to train the HMM.

- Expectation Maximization Iterations: Number of iterations for the EM algorithm.

- Cone Colors: Customizable colors for the probability cone, when approximation is on and when importance sampling is on

NY 8-11 Statistical Bias NQ 【Donkey】This indicator analyzes historical session patterns to predict directional bias during the NY 8:00-11:00 AM trading window for Micro NQ futures.

Simple Logic:

Monitors 3 sessions: Asian (20:00-02:00), London (02:00-08:00), NY (08:00-11:00)

Identifies current pattern based on: ranges, opening positions, and sweep behaviors

Searches database of 2.080 historical sessions for matching patterns

Displays statistical probability: "X% reached HIGH" vs "Y% reached LOW"

Shows expected drawdown levels for risk management

Example: If pattern shows "77% HIGH bias" → historically, 77 out of 100 similar sessions reached London high during NY 8-11 window.

Key Features

✅ Statistical Database:2.080 real sessions analyzed, 236 unique patterns

✅ 4-Level Pattern Matching: Finds best match with minimum 25 occurrences

✅ Live Bias Display: Shows HIGH% vs LOW% probability in real-time table

✅ Risk Management Zones: Visual drawdown levels (50%, 75%, 90%) + stop-loss suggestion

✅ No Repainting: Calculations made in real-time, no look-ahead bias

✅ Session Visualization: Color-coded boxes for Asian/London/NY ranges

How Pattern Matching Works

5 Components Analyzed:

Asian Range: Above/Below average

London Open: Above/Below Asian 50%

London Sweep: H, L, DH (double high→low), DL (double low→high), N (none)

London Range: Above/Below average

NY Open: Above/Below London 50%

Cascade Search (finds best available match):

Level 1: All 5 components (most specific)

Level 2: 4 components (drops London Range)

Level 3: 3 components (core pattern)

Level 4: 2 components (minimal pattern)

Validity: Only displays patterns with ≥25 historical occurrences.

Interpretation

Bias Table Shows:

Pattern match level (1-4) and historical count

Session characteristics (ranges, sweeps, positions)

TOTAL HIGH % = probability of reaching London high

TOTAL LOW % = probability of reaching London low

Bias strength: ⭐⭐⭐ STRONG (≥70%), ⭐⭐ MEDIUM (60-69%), ⭐ WEAK (<60%)

Drawdown Zones (for winning trades):

🟢 Green: 50% of winners stayed within this level

🟡 Yellow: 75% of winners stayed within this level

🟠 Orange: 90% of winners stayed within this level

🔴 Red Line: Suggested stop-loss (95th percentile + buffer)

Settings

Fully Customizable:

Timezone selection (auto-detects sessions correctly)

Minimum session threshold (default: 25)

Toggle boxes, lines, labels, drawdown zones

Complete color customization

Table size and position

Best Use Cases

✅ Optimal Setup:

Instrument: Micro NQ (MNQ) futures

Timeframe: Only 1-minute

Timezone: America/New_York

Historical data: 8+ years loaded

✅ Trading Approach:

Wait for pattern confirmation (≥25 sessions)

Prefer STRONG bias (≥70%) for higher confidence

Use drawdown zones for stop placement

Combine with price action confirmation

Avoid major news events (FOMC, NFP)

⚠️ Required Disclaimers

IMPORTANT RISK WARNINGS:

Past Performance ≠ Future Results: Historical statistics do NOT guarantee future outcomes

Not Financial Advice: Educational tool for statistical analysis only

Risk of Loss: Futures trading involves substantial risk of loss

No Guarantees: Individual trades WILL result in losses regardless of percentages shown

Requires Knowledge: Best for traders familiar with session analysis and risk management

Instrument-Specific: Optimized for Micro NQ - test before using elsewhere

Never risk more than you can afford to lose. Always use proper risk management.

Hidden Markov Model - Probability Cone

The Hidden Markov Model - Probability Cone Indicator employs Hidden Markov Models (HMMs) for forecasting future price movements in financial markets. HMMs are statistical tools that predict transitions between hidden states, such as different market regimes, based on observed data. This makes them valuable for understanding market behaviours and projecting future price trajectories. As discussed in the Hidden Markov Model indicator, HMMs predict future states and their associated outputs based on the current state and model parameters.

The probability cone indicator therefore uses the knowledge about the current identified "state" or "regime" and with the help of transition probabilities, emission probabilities and initial probabilities generate a probabilistic forecast of the expected future price movements. To better understand the behind the Probability Cone we encourage you to use and learn about our free version of the Probability Cone as well as for even deeper understanding the Probability Cone Pro.

WHAT ARE REGIME DEPENDENT FORECASTS

As mentioned above the indicator creates probabilistic forecasts of future price movements dependent on the current identified "state" or market "regime" via the Hidden Markov Model. In the image below we can see an example.

In this example we can see 3 different probability cones forecasting a 70% and 90% probability range (15% and 5% quantiles respectively). What you may notice is that the 3 probability cones look vastly different, despite using the same probability ranges as well as being generated from the same model trained on virtually the same data. What allows for this difference in the forecast is conditioning the forecast on the current most likely identified state by the HMM.

The first most wide cone is generating a forecast taking into account that the model identified the current market condition to be a very volatile which is a characteristic of the state identified by the orange coloured posterior probability. The second cone is significantly more narrow as that state identified by the purple posterior probability is characterised by lower volatility. Nevertheless, the last probability cone is generated from the state that is characterised by the lowest volatility, we can also see the light blue posterior probability to be the highest at that time.

The indicator also allows you to specify whether you wish to display probability based labels at the edges of the cone or whether you would prefer to display percent change based labels. With percent change labels you get the exact percentage value of the probabilistic increase or decrease of the price. See the example below

BARS BACK OFFSET vs DATE BASED OFFSET

The cones position can be offset by specifying the number of bars we wish to move it back similarly as with the rest of probability cone indicators. This indicator has however an additional, date based offset implemented. A user can therefore specify the position of the cone by specifying a date in the settings. The advantage of using the date based offset is that once it is turned on the user can also slide the cone up and down the chart with their mouse without having to manually adjust the date in the settings.

DIFFICULTIES WITH GENERATING FORECASTS (advanced):

The estimation of the probability cone, gets more difficult the more complex the model gets. A simple normal distribution probability cone can scale the distribution over time by simply multiplying the drift by the number of time steps and the volatility by the square root of time steps we wish to forecast for. More complex distributions often have to rely on mode advanced methods like convolutions, monte carlo or other kinds of approximations.

To estimate the probability cone forecast for the Hidden Markov Model, the indicator integrates two primary methodologies: Gaussian approximation and importance sampling. The Gaussian approximation is utilized for estimating the central 90% of future prices. This method provides a quick and efficient estimation within this central range, capturing the most likely price movements. The gaussian approximation will result in a forecast with an equal mean and variance as the true forecast, it will however not accurately reflect higher moments like skewness and kurtosis. For that reason the tail quantiles, which represent extreme price movements beyond the central range (90%), are estimated via importance sampling. This approach ensures a more accurate estimation of the skewness and kurtosis associated with extreme scenarios. While impoortance sampling leverages the flexibility of monte carlo as well as attempts to increase its efficiency by sampling from more precise areas of the distribution, the importance sampling may still underestimate most extreme quantiles associated with the lowest probabilties which is an inherent limitation of the indicator.

Example of gaussian approximation cone for probabilities above 5% (90% range):

Example of importance sampling cone for tail probabilities lower than 5% (beyond 90% range):

WARNING!

As per usual understand that the probabilities are estimations and best guesses based on the historical data and the patterns identified by the model and do not represent the true probability which is unknown in reality.

Settings:

- Source: Data source used for the model

- Forecast Period: Number of bars ahead for generating forecasts.

- Simulation Number: Number of Monte Carlo simulations to run in the case of importance sampling

-Body Probability: Specifies the inner range of the probability cone. The probability specifies the ammount of observations that are expected to fall outside of this range

- Tail Probability: Specifies the outter range of the probability cone. When this probability is under 5%, importance sampling will turn on

- Lock Cone: When ticked on, the cone will be locked at its current position.

- Offset Cone Based on Date: When ticked on, the position of the cone will be determined by the selected date.

- Offset: When "Offset Cone Based on Date" is turned off, you can use offset setting to specify the position of the cone projection.

- Date: When "Offset Cone Based on Date" is turned on, you can use the date setting to specify the date from which the forecast starts.

- Reestimate Model Every N Bars: This is especially useful if you wish to use the indicator on lower timeframes where model estimation might take longer than for the new datapoint to arrive. In that case you can specify after how many bars the model should be reestimated.

- Training Period: Length of historical data used to train the HMM.

- Expectation Maximization Iterations: Number of iterations for the EM algorithm.

- Cone Colors: Customizable colors for the probability cone, when approximation is on and when importance sampling is on

Watermark | Bar Time | Average Daily RangeMulti Info Panel & Watermark

Multi Info Panel & Watermark is a utility indicator that displays several pieces of chart information in a single, customizable panel. It is designed to support intraday and swing analysis by making key data—such as symbol details, date, and average daily range—easy to see at a glance, as well as providing simple tools for notes and backtesting.

Features

Watermark / Custom Note

Optional text overlay that can be used as a watermark or personal note.

Can display a strategy name, reminder, or any other user-defined label on the chart.

Ticker Info

Shows information about the currently active symbol on the chart (for example, symbol name and other basic details depending on the inputs).

Helps keep track of which market or pair is being analyzed, especially when using multiple charts.

Current Date

Displays the current date directly on the chart.

Useful for screenshots, journaling, and documenting analysis.

Average Daily Range (ADR)

Calculates the average daily range of the active symbol over a user-defined number of recent days.

Helps visualize how much price typically moves in a day, which can support position sizing, target setting, or volatility awareness within your own trading approach.

Open Bar Time Marker

Marks the open time of a selected bar (for example, a session open or a specific reference bar).

Primarily intended as a visual aid for manual backtesting and reviewing historical price action.

Usage

Use the watermark and ticker info to keep your charts labeled and organized.

Refer to the ADR readout to understand typical daily volatility of the instrument you are studying.

Use the date and open bar time marker when creating screenshots, trade journals, or when replaying historical sessions for review.

This script does not generate trading signals and does not guarantee any performance or results. It is provided solely as an informational and visualization tool. Always combine it with your own analysis, risk management, and decision-making. Nothing in this indicator or description should be considered financial advice.

Probability Cone ProProbability Cone Pro is based on the Expected Move Pro . While Expected Move only shows the historical value band on every bar, probability cone extend the period in the future and plot a cone or curve shape of the probable range. It plots the range from bar 1 all the way to any specified number of bars up to 1000.

Probability Cone Pro is an upgraded version of the Probability Cone indicator that uses a Normal Distribution to model the returns. This newer version uses a maximum likelihood estimation for Asymmetric Laplace distribution parameters. Asymmetric Laplace distribution takes into account fatter tails and volatility clustering during low volatility. So it will be thinner in the body (eg: <70% range) and fatter in the tails (>95% range) which fits the stock return better. Despite a better fit users should not blindly follow the probabilities derived from the indicator and should understand that these are very precise estimations of probability based on historical data, not the true probability which is in reality unknown.

When we compare the more peaked asymmetric laplace to the bell curve shaped normal distribution we can see that the asymmetric laplace fits the empirical data (blue histogram) significantly better. The fit is improved in both the body (middle peaked part) as well as in the fatter tails (more of extreme occurrences far from the center)

The area of probability range is based on an inverse cumulative distribution function. The inverse cumulative distribution gives the range of price for given input probability. People can adjust the range by adjusting the input probability in the settings. The entered probability will be shown at the edges of the cone when the “show probability” setting is on.

The indicator allows for specifying the probability for 2 quantiles on each side of the distribution , therefore 4 distinct probability values. The exact probability input is another distinction compared to the Normal Distribution based Probability Cone, in which the probability range is determined by the input of a standard deviation. Additionally now the displayed labels at the edges of the probability cone no longer correspond to the total number of outcomes that are expected to occur within the specific range, instead we chose to display the inverse which is the probability of outcomes outside of the specified range. See comparison below:

Probability cone pro with 68% and 95% ranges also defined by 16% and 2.5% probabilities at the tails on both sides:

Normal Probability cone with 68% and 95% ranges defined by 1st and 2nd standard deviation

SETTINGS:

Bars Back : Number of bars the cone is offset by.

Forecast Bar: Number of bars we forecast the cone for in the future.

Lock Cone : Specify whether we wish t lock the cone to the current bar, so it does not move when new bars arrive.

Show Probability : Specify whether you wish to show the probability labels at the edges of the cone.

Source : Source for computation of log returns whose distribution we forecast

Drift : Whether to take into account the drift in returns or assume 0 mean for the distribution.

Period: The sampling period or lookback for both the drift and the volatility estimation (full distribution estimation).

Up/Down Probabilities: 4 distinct probabilities are specified, 2 for the upper and 2 for the lower side of the distribution.

Expected Move ProExpected Move is the amount that an asset is predicted to increase or decrease from its current price, based on the current levels of volatility.

This Expected Move Pro indicator uses a maximum likelihood estimation for Asymmetric Laplace distribution parameters, and is an upgrade from the regular Expected Move indicator that uses a Normal Distribution. The use of the Asymmetric Laplace distribution ensures a probability range more accurate than the more common expected moves based on a normal distribution assumption for returns. Asymmetric Laplace distribution takes in account fatter tails and volatility clustering during low volatility. So it will be thinner in the body (eg: <70% range) and fatter in the tails (>95% range) which fits the stock return better.

When we compare the more peaked asymmetric laplace to the bell curve shaped normal distribution we can see that the asymmetric laplace fits the empirical data (blue histogram) significantly better. The fit is improved in both the body (middle peaked part) as well as in the fatter tails (more of extreme occurrences far from the center)

EXPECTED MOVE PROBABILITY:

In the expected move settings, the user can specify the range probability they wish to display. In a normal distribution a 1 standard deviation range corresponds to a range within which just under 70% of observations fall. So to specify a 70% probability range one would set 15% probability for both the upper and lower range.

For the more extreme ranges a two tail function is used so the user can only specify one probability. When 5% probability is specified the range will cover 95% and on each side of the range the probability of an occurence that extreme will be 2.5%. In the above Image we can see two tail probabilities specified at 5% and 1%, covering the 95% and 99% ranges respectively.

The indicator also allows for multi timeframe usecases. One can request a daily or perhaps even weekly expected move on an hourly chart, like we see below.

SETTINGS:

Resolution: Specify the timeframe and if you want to use the multi timeframe functionality.

Real Time : Do you wish the expected move to adjust with the current open price or do you wish it to be a forecast based on the yesterdays close. If latter, keep it OFF.

Sample Size : Lookback or the number of bars we sample in the calculation.

Optimization : Keep it on for speed purposes, only slightly higher precision will be achieved without optimization.

Probabilities: One tail - left and right, specify probability for each side of the range, two tail - single probability split in half for each side of the range

Center : Displays the central line which is the central tendency of a distribution / the median

Hide History : Hides expected moves and only the expected move for the current bar remains.

Plot Style Settings : One can adjust the line styles, box styles as well as width and transparency.