V2 BUY LOW, BUY MORE, SELL HIGH Strategy w Buffett Meter-LITE__________________________________________________________________________

V2 Buy Low, Buy More, Sell High With Buffett Meter (LITE – JTMarketAI)

__________________________________________________________________________

Category: Quantitative Momentum & Liquidity Flow

Author: JTMarketAI

Architecture: Non-Repainting

This strategy accumulates into validated pullbacks during fear cycles, scales intelligently as price declines into liquidity support, and exits when momentum weakens after meaningful run-ups. It uses synthetic higher-timeframe OHLC data (non-repainting), liquidity imbalance confirmation, adaptive KAMA trend logic, RSI validation, and a live Buffett macro valuation gauge.

This is a patient, conviction-based accumulation engine designed for equities.

It is not a scalp bot.

__________________________________________________________________________

Core Features

__________________________________________________________________________

Non-repainting (confirmed bars only)

Synthetic HTF OHLC (no lookahead)

Dynamic trailing exit preserves ~80–87% of peak profit

Bull vs Bear liquidity dominance and flow imbalance

Rolling lowest-low tracking (LLL)

NY-session alignment (default)

Buffett Macro Meter integration

Technical Highlights

Flow-confidence derived from volume-order pressure

Adaptive KAMA smoothing for lower-lag confirmation

Daily > Weekly > Monthly synthetic aggregation

LLL progression display for trend exhaustion

Fully profiler-optimized

Supports averaging down when pyramiding enabled

__________________________________________________________________________

Why It Does Not Repaint

__________________________________________________________________________

All state updates occur only on confirmed bars

All trades are recorded and remembered to not disappear

Synthetic HTFs built without lookahead

Persistent arrays freeze historical values

Trailing highs updated only after confirmation

No forward-reference to future bars

__________________________________________________________________________

Lite Edition Notes

__________________________________________________________________________

Manual trading focused

Live trades (Dark Blue) Preview period trades (aqua entries)

On strategy start date, if preview trades are profitable, live trades begin.

Buffett Meter enabled. Nice for monitoring volume bar-by-bar for day trading.

Visual dashboard included

No alerts, automation, or webhooks (PRO unlocks TradersPost.io auto-trading)

__________________________________________________________________________

Limitations

__________________________________________________________________________

Best on intraday equities (1m–4h) V2 uses virtual volume to enable Daily Charts.

Designed for stock market tickers only.

High-resource if full visuals enabled

Avoid extremely low-volume tickers. Nice cyclical wave tickers like TSLA are best.

Does not guard against after-hours gaps or major news moves

Does not prevent tickers from racing towards 0.

__________________________________________________________________________

Warnings

__________________________________________________________________________

Contrarian scaling requires discipline and patience

Expect longer-duration trades, not rapid scalps

Use on quality tickers unlikely to permanently collapse

Confirm price behavior outside cash session

Test manually before automating anything

Not suitable for every market environment or asset

Notes on Philosophy

This strategy attempts to accumulate when markets overshoot lower, and distribute after recovery momentum fades. It reflects a patient, value-driven approach built on the principle of buying fear and reducing exposure into strength.

__________________________________________________________________________

Disclaimer

__________________________________________________________________________

For research and educational use only. Not financial advice. Past performance does not guarantee future results. Test thoroughly and use appropriate risk management.

Volume

51 By GoldmanMrBaNNa✅ Indicator Description

This indicator checks the Higher Timeframe (HTF) trend and only allows trades in that direction on the Lower Timeframe (LTF).

Example:

If 15-minute timeframe gives a BUY signal, then on the 1-minute timeframe the indicator will only show BUY signals.

If 15-minute timeframe gives a SELL signal, then on the 1-minute timeframe the indicator will only show SELL signals.

It filters small-timeframe trades and keeps entries aligned with major market direction.

Built for clean, directional scalping such as 1:3 / 1:4 risk-reward setups.

Adaptive Averaging Concept [NeuraAlgo]Adaptive Averaging Concept

A Quant-Engineered Dynamic Position Sizing & Optimization Framework

Adaptive Averaging Concept™ is a next-generation, research-driven trading framework that combines multistage entries, ATR-based intelligent scaling, real-time sentiment filtering, and a fully automated optimization engine.

It is designed for traders who want precision execution, adaptive risk control, and an architecture capable of learning from market structure.

🔹 Core Concept

Unlike traditional averaging or DCA methods, this engine uses Adaptive Averaging — a controlled, mathematically tuned accumulation system that adjusts entries based on volatility, trend conditions, and signal confidence.

Each additional entry intelligently recalculates average price and updates a volatility-sensitive dynamic Take Profit.

🔹 Main Features

1. Intelligent Multi-Stage Entry System

Initial entries triggered by SMA crossover, rising volume, or Always-On mode

Secondary entries triggered only when price retraces by a volatility-adjusted threshold

Every added position recalculates:

Total quantities

Capital distribution

Average price

Adaptive Take Profit (ATR-based)

2. Adaptive Risk & Position Management

ATR-driven take-profit using Exit Sensitivity

ATR-driven add-entry logic using Exit Tuner

Dynamic or Fixed lot sizing

Capital-per-entry control

Automatic minimum lot protection

3. High-Level Market Filters

Trend Filter

A volatility-normalized EMA slope filter that identifies:

1.Bullish trend

2.Bearish trend

3.Neutral trend

Sentiment Cloud Filter

A structural sentiment engine analyzing:

1.Micro-gaps

2.Bull and bear pressure

3.Range compression

4.Market regime bias

Trades only execute when filters align with your directional bias.

4. NeuraAlgo Optimization Engine

The strategy includes a built-in optimizer allowing you to test & tune with no loops and no external computation.

You can automatically optimize:

Smooth Period (ATR)

Exit Sensitivity

Exit Tuner

SMA Period

Trend Filter Length

Trend Filter Smooth

Sentiment Cloud Period

Optimization Goals:

Maximize Winrate

Maximize Net Profits

This allows the strategy to self-configure based on live market conditions.

Here, the optimization is finally complete.

🔹 Summary

Adaptive Averaging Concept™ is not a simple indicator or basic DCA script.

It is a complete quant-grade execution engine capable of dynamically adjusting its behavior to volatility, price structure, trend strength, and sentiment.

Engineered for traders who demand:

High-precision entry logic

Adaptive position sizing

Volatility-calibrated exits

Smart accumulation

Built-in optimization

Professional-grade backtesting

It is a powerful framework suitable for swing traders, intraday traders, and automated system developers.

Hanzo Strategy - Volume & Smart Money📊 HANZO STRATEGY - Complete Description

## 🎯 Strategy Overview

The **Hanzo Strategy** is an advanced institutional trading system that combines Volume Profile analysis, Smart Money Concepts, and Price Action patterns to identify high-probability trade setups. This strategy is specifically designed for trading Gold (XAUUSD), NAS100, and US30 on the 15-minute timeframe.

---

## 🧠 Core Trading Philosophy

The Hanzo Strategy operates on the principle that **institutional money leaves footprints** in the market through:

- Volume accumulation at key price levels

- Liquidity sweeps and stop hunts

- Order block formations

- Strategic wick rejections at support/resistance

By identifying these institutional behaviors and combining them with precise volume analysis, the strategy aims to trade **with** the smart money, not against it.

---

## 🔑 Key Components

### 1️⃣ **Fixed Range Volume Profile (FRVP)**

- **What it does:** Analyzes the last 2 days of price action and calculates where the most volume traded

- **Point of Control (POC):** The price level with the highest trading volume - acts as a magnet for price

- **How we use it:** Price tends to revert to POC. When price is far from POC and starts moving toward it, we prepare for entries

- **Visual:** Yellow cross line on the chart marking the POC

### 2️⃣ **Wick Cluster Detection**

- **What it does:** Automatically identifies price levels where multiple candle wicks have rejected (2-6+ wicks)

- **Why it matters:** Multiple rejections at the same level indicate strong institutional support/resistance

- **Upper wick clusters:** Resistance zones where price was rejected downward

- **Lower wick clusters:** Support zones where price was rejected upward

- **Visual:** Dashed lines (red for resistance, green for support)

### 3️⃣ **Session Volatility Boxes**

- **London Session (8:00-16:00 UTC+3):** Captures European market volatility range

- **New York Session (13:30-20:00 UTC+3):** Captures US market volatility range

- **How we use it:** These ranges often act as support/resistance for the rest of the day

- **Visual:** Blue box for London, Orange box for New York

### 4️⃣ **Smart Money Zones**

**Order Blocks:**

- Strong institutional areas where banks and hedge funds placed large orders

- **Bullish Order Block:** Area where smart money bought heavily before a strong upward move

- **Bearish Order Block:** Area where smart money sold heavily before a strong downward move

- **Visual:** Green/Red filled boxes with "Bull OB" or "Bear OB" labels

**Liquidity Sweeps:**

- Price breaks above recent high or below recent low, then quickly reverses

- This is a "stop hunt" - institutions triggering retail stops before moving in the real direction

- **Bullish Sweep:** Price dips below support, grabs stops, then reverses up

- **Bearish Sweep:** Price pops above resistance, grabs stops, then reverses down

- **Visual:** Triangle markers (green up = bullish, red down = bearish)

### 5️⃣ **Engulfing Pattern Recognition**

- **Bullish Engulfing:** Large green candle fully engulfs the previous red candle - shows strong buying pressure

- **Bearish Engulfing:** Large red candle fully engulfs the previous green candle - shows strong selling pressure

- **How we use it:** Confirmation signal when combined with other factors

- **Visual:** Small circles below/above candles

### 6️⃣ **Trend Bias Indicator**

- Dynamically calculates market bias based on price position relative to POC

- **Bullish:** Price > 0.2% above POC

- **Neutral:** Price within 0.2% of POC

- **Bearish:** Price > 0.2% below POC

- **Visual:** Label at top of chart showing current bias

---

## 📈 Entry Signal Logic

The strategy generates **LONG** and **SHORT** signals based on confluence of multiple factors:

### 🟢 LONG ENTRY CONDITIONS:

1. **POC Break:** Price crosses above POC from below + Trend Bias is Bullish

**OR**

2. **Support Bounce:** Price touches a lower wick cluster + Bullish Engulfing pattern forms

3. **Additional Filter:** Trend Bias must NOT be Bearish

### 🔴 SHORT ENTRY CONDITIONS:

1. **POC Break:** Price crosses below POC from above + Trend Bias is Bearish

**OR**

2. **Resistance Rejection:** Price touches an upper wick cluster + Bearish Engulfing pattern forms

3. **Additional Filter:** Trend Bias must NOT be Bullish

---

## 🎯 Risk Management

### Stop Loss:

- **Calculation:** 2 × ATR(14) from entry price

- **Logic:** Uses Average True Range to adapt to current market volatility

- **Example:** If ATR = 10 points, stop loss is 20 points away

### Take Profit:

- **Calculation:** 3 × ATR(14) from entry price

- **Risk:Reward Ratio:** 1:1.5 (risking 2 ATR to make 3 ATR)

- **Example:** If ATR = 10 points, take profit is 30 points away

### Position Sizing:

- **Default:** 2% of account equity per trade

- **Adjustable:** Can be modified in strategy settings

---

## ⚙️ Strategy Settings & Customization

### Volume Profile Settings:

- **Lookback Days:** How many days to analyze (default: 2)

- **Profile Rows:** Resolution of volume calculation (default: 24)

- **POC Distance Threshold:** Minimum distance from POC for "far from POC" status (default: 0.3%)

### Wick Cluster Settings:

- **Min Wicks for Cluster:** How many wicks needed to form a cluster (default: 3)

- **Lookback Bars:** How far back to search for wicks (default: 50)

- **Tolerance %:** How close wicks must be to cluster together (default: 0.15%)

### Session Settings:

- **London Session:** 08:00-16:00 (adjustable)

- **New York Session:** 13:30-20:00 (adjustable)

- **UTC Offset:** Timezone adjustment (default: +3)

### Smart Money Settings:

- **Order Block Lookback:** How far back to search for order blocks (default: 20)

- **Toggle On/Off:** Can enable/disable order blocks and liquidity sweeps independently

---

## 📊 Performance Metrics Display

The strategy includes a real-time **Information Table** (top-right corner) showing:

| Metric | Description |

|--------|-------------|

| **Trend Bias** | Current market direction (Bullish/Neutral/Bearish) |

| **POC Price** | Current Point of Control price level |

| **Distance from POC** | How far current price is from POC (%) |

| **ATR (14)** | Current volatility measurement |

| **High Wick Clusters** | Number of resistance clusters detected |

| **Low Wick Clusters** | Number of support clusters detected |

| **Current Signal** | Active signal (LONG/SHORT/None) |

---

## 🚨 Alert System

The strategy can send alerts for:

1. **LONG Signal Triggered** - When all conditions met for long entry

2. **SHORT Signal Triggered** - When all conditions met for short entry

3. **Price Touching Support Cluster** - Warning that price at key support

4. **Price Touching Resistance Cluster** - Warning that price at key resistance

**Alert Frequency:** Once per bar (prevents spam)

---

## 📅 Best Trading Timeframes & Instruments

### ✅ Recommended Timeframes:

- **Primary Entry:** 15-minute chart

- **Trend Confirmation:** 30-minute or 1-hour chart

- **Higher Timeframe Filter:** 4-hour for major trend direction

### ✅ Recommended Instruments:

1. **Gold (XAUUSD)** - High volatility, respects key levels well

2. **NAS100 (US Tech 100)** - Strong trends, good liquidity

3. **US30 (Dow Jones)** - Reliable institutional participation

4. **EUR/USD, GBP/USD** - Can work on major forex pairs with adjustments

### ⏰ Best Trading Sessions:

- **London Open (08:00-12:00 UTC+3)** - High volatility, clear directional moves

- **New York Open (13:30-17:00 UTC+3)** - Strongest moves, highest volume

- **Overlap (13:30-16:00 UTC+3)** - Best liquidity and movement

### ⚠️ Avoid Trading:

- Asian session (low volatility)

- Major news events (first 15 minutes after high-impact news)

- Sundays and holidays (low liquidity)

---

## 💡 Pro Trading Tips

### 1. **Multiple Timeframe Confirmation**

- Check 1-hour chart for overall trend before taking 15-minute signals

- Only take LONG signals if 1-hour is bullish

- Only take SHORT signals if 1-hour is bearish

### 2. **POC Strategy**

- Best entries occur when price returns to POC after being far away

- Wait for POC touch + confirmation pattern (engulfing, order block)

- POC acts as support in uptrends, resistance in downtrends

### 3. **Wick Cluster Strategy**

- Strongest signals occur when wick clusters align with POC

- Look for 4+ wicks at the same level for highest probability

- Recent clusters (formed in last 2 days) are stronger than old ones

### 4. **Order Block Strategy**

- Fresh order blocks (just formed) are more powerful

- Wait for price to return to order block zone before entering

- Best when order block + wick cluster occur at same level

### 5. **London/NY Box Strategy**

- If price breaks above session high → look for LONG pullback entries

- If price breaks below session low → look for SHORT pullback entries

- Price often returns to session mid-point before continuing

### 6. **Risk Management Rules**

- **Never risk more than 2% per trade**

- **Don't trade more than 3 positions simultaneously**

- **If 2 losses in a row, reduce size to 1% or stop for the day**

- **Move stop to breakeven after 1:1 profit reached**

### 7. **High-Probability Setups**

Look for **CONFLUENCE** - the more factors aligned, the better:

✅ **BEST LONG SETUP:**

- Price at lower wick cluster (support)

- Price at/near POC

- Bullish order block present

- Bullish engulfing pattern forms

- Trend Bias = Bullish

- 1-hour chart = uptrend

✅ **BEST SHORT SETUP:**

- Price at upper wick cluster (resistance)

- Price at/near POC

- Bearish order block present

- Bearish engulfing pattern forms

- Trend Bias = Bearish

- 1-hour chart = downtrend

---

## 📈 Performance Expectations

### Typical Win Rate:

- **Conservative Trading (high confluence only):** 55-65% win rate

- **Moderate Trading (good setups):** 45-55% win rate

- **Aggressive Trading (all signals):** 35-45% win rate

### Typical Risk:Reward:

- **Average R:R:** 1:1.5 (with 2 ATR stop and 3 ATR target)

- **Breakeven adjusted:** Often improves to 1:2+ when stop moved to BE

### Monthly Trade Frequency (15M chart):

- **Gold:** 60-100 signals per month

- **NAS100:** 50-80 signals per month

- **US30:** 40-70 signals per month

---

## 🎓 Strategy Philosophy Summary

The Hanzo Strategy is built on three core principles:

1. **Follow the Volume** - Trade where institutions are active

2. **Respect the Levels** - Key support/resistance zones matter

3. **Confirm with Price Action** - Wait for confirmation before entering

This is NOT a holy grail - it requires:

- ✅ Discipline to wait for proper setups

- ✅ Patience to let trades play out

- ✅ Risk management to protect capital

- ✅ Emotional control to handle losses

---

## 🛠️ How to Use This Strategy

### Step 1: Initial Setup

1. Add strategy to 15-minute chart

2. Check that all components are visible (POC, clusters, boxes, etc.)

3. Adjust colors if needed for your chart theme

### Step 2: Daily Routine

1. **Pre-Market (before 8:00 AM):**

- Check POC location

- Note wick clusters from previous days

- Mark London/NY session boxes from yesterday

2. **London Session (8:00-16:00):**

- Watch for POC interactions

- Monitor for order blocks forming

- Wait for confluence setups

3. **NY Session (13:30-20:00):**

- Highest activity period

- Best signal quality

- More aggressive entries allowed

### Step 3: Trade Execution

1. Wait for signal label (LONG or SHORT) to appear

2. Check confluence factors (minimum 3)

3. Enter immediately or on next candle

4. Set stop loss at 2 × ATR from entry

5. Set take profit at 3 × ATR from entry

6. Move stop to breakeven at +1.5 ATR profit

### Step 4: Trade Management

- **Don't move stop closer** (let trade breathe)

- **Can trail stop** after 2:1 profit reached

- **Can take partial profits** at 1.5:1 and let rest run

- **Journal every trade** for future improvement

---

## ⚠️ Important Disclaimers

1. **Past performance does not guarantee future results**

2. **This strategy involves risk** - only trade with money you can afford to lose

3. **Backtest thoroughly** on your specific instruments before live trading

4. **Start small** - test with minimum position sizes first

5. **Market conditions change** - what works today may not work tomorrow

6. **Use proper risk management** - this is the #1 key to long-term success

---

## 🎯 Quick Reference Checklist

Before taking any trade, ask yourself:

- ✅ Is there a clear LONG or SHORT signal?

- ✅ Are we in London or NY session?

- ✅ Is price at/near POC or wick cluster?

- ✅ Is trend bias aligned with my direction?

- ✅ Is there an order block or engulfing pattern?

- ✅ Is my risk:reward at least 1:1.5?

- ✅ Am I risking no more than 2% of my account?

**If 5+ are YES → Take the trade!**

**If 3 or fewer YES → Skip and wait for better setup!**

---

## 🚀 Final Words

The Hanzo Strategy is a professional-grade trading system that combines institutional analysis with precise technical execution. Success comes not from taking every signal, but from taking only the **highest probability setups** with proper risk management.

**Trade smart. Trade safe. Trade like an institution.**

📊 **Good luck and profitable trading!** 📊

Rawa_Trade_System_Vol_AdxThe strategy must be configured for each instrument separately; the basic configuration uses a trailing stop, a 4H timeframe, and excludes margin trading.

D.Y Volume Swing Strategy📌 Summary of the Daniel.Yer Volume Strategy

This strategy is based on identifying the "opening volume peak" at the start of each trading day, using a user-defined sampling window.

After the sampling period ends, the strategy looks for breakouts above the daily high or below the daily low, provided they occur with a strong high-volume candle that meets the user-set threshold.

When a breakout appears in one direction, the strategy waits for an opposite-direction confirmation candle (Reversal Confirmation) and then enters a smart counter-breakout trade.

Each trade includes dynamic Stop-Loss and Take-Profit levels calculated from recent price structure, with the option to multiply stop distance according to user preference.

The strategy also gives full control over entering long only, short only, or both, as well as choosing whether trades occur exclusively from the high/low or without restrictions.

The strategy can be tested on any timeframe and evaluated across four trading directions:

✔ Buy from High

✔ Sell from High

✔ Buy from Low

✔ Sell from Low

EVS BTC V1Overview

The "EVS BTC V1" is a momentum-based trading strategy designed for Bitcoin (BTC) or similar volatile assets on TradingView. It combines Exponential Moving Averages (EMAs) for trend direction, volume confirmation to filter for strong moves, and an optional Relative Strength Index (RSI) filter to avoid overextended entries. The strategy uses a trailing stop for exits to lock in profits dynamically. It's set up for backtesting with an initial capital of $10,000, risking 10% of equity per trade, and accounting for 0.1% commissions.This is a crossover strategy: it goes long on bullish EMA crossovers with high volume (and RSI not overbought) and short on bearish crossunders (with high volume and RSI not oversold). It's overlayed on the main price chart for easy visualization.Key Parameters (User-Adjustable)Fast EMA Period: 9 (default) – Shorter-term trend line.

Slow EMA Period: 21 (default) – Longer-term trend line.

Volume Multiplier: 1.5 (default) – Requires volume to be 1.5x the 20-period average for signal validation.

Use RSI Filter?: Enabled (default) – Optional toggle to apply RSI conditions.

RSI Period: 14 (default), with overbought threshold at 70 and oversold at 30.

Trailing Stop Profit: 50 points (default) – Activates trailing once this profit level is hit.

Trailing Stop Offset: 20 points (default) – Distance from the high/low to trail the stop-loss.

Indicators UsedEMAs: 9-period (fast, blue line) and 21-period (slow, red line) on close prices.

Volume Filter: Compares current volume to a 20-period SMA; signals only trigger if volume exceeds the average by the multiplier (highlighted in yellow bars).

RSI: 14-period on close; plotted in purple on a sub-panel if enabled, with dashed horizontal lines at 70 (overbought) and 30 (oversold).

Entry RulesEntries are triggered only when all conditions align on a bar close:Direction

Conditions

Long (Buy)

- Fast EMA crosses over Slow EMA (bullish trend shift).

- Volume is "high" (> 1.5x 20-period avg).

- RSI < 70 (not overbought; skipped if filter disabled).

Short (Sell)

- Fast EMA crosses under Slow EMA (bearish trend shift).

- Volume is "high" (> 1.5x 20-period avg).

- RSI > 30 (not oversold; skipped if filter disabled).

On entry: Places a market order using 10% of current equity.

Alerts: Fires a one-time alert per bar (e.g., "Long Signal: EMA Crossover + High Volume!").

Exit RulesNo fixed take-profit or stop-loss on entry.

Uses a trailing stop for both long and short positions:Trails the stop-loss 20 points below the highest high (for longs) or 20 points above the lowest low (for shorts), but only activates after 50 points of unrealized profit.

This allows winners to run while protecting gains dynamically.

Positions close automatically on opposite signals or trailing stop hits (no pyramiding; only one position per direction at a time).

VisualizationMain Chart: Blue fast EMA and red slow EMA lines. Green background tint on long signals, red on short signals.

Volume Sub-Panel: Gray columns for normal volume, yellow for high-volume bars; zero line for reference.

RSI Sub-Panel (if enabled): Purple RSI line with overbought/oversold dashed lines.

Strengths and ConsiderationsStrengths: Simple, trend-following with volume to avoid weak signals; RSI adds mean-reversion protection; trailing stops suit trending markets like BTC.

Risks: Whipsaws in sideways markets (EMA crossovers can false-signal); volume filter may miss low-volume breakouts; trailing parameters (50/20 points) assume a specific price scale (e.g., BTC/USD in dollars—adjust for other pairs).

Best For: Higher timeframes (e.g., 1H or 4H) on volatile crypto pairs. Backtest on historical data to tune parameters.

Absorption PROOF - Absorption PRO (Clean & Smart)Ultra-clean, high-precision absorption reversal strategy.Detects institutional buying/selling pressure using volume-weighted delta proxy and VWAP deviation zones.Smart RSI + early-session range filter automatically separates valid range-bound reversals from trend exhaustion.Green/Red circles → High-probability entries (fully tradable)

Small crosses + colored zones → Rejected signals (avoid)

Blue dotted lines → Session range ±100% deviation levels (optional)

By default: only signals and rejection zones displayed — zero clutter.Minimalist, professional, and deadly accurate on futures & forex (1m–15m).Less noise. Better trades.

MTF EMA Hariss 369The strategy has been prepared in a simplistic manner and easy to understand the concept by any novice trader.

Indicators used:

Current Time frame 20 EMA- Gives clear look about current time frame dynamic support and resistance and trend as well.

Higher Time Frame 20 EMA: Gives macro level trend, support and resistance

Kama: Capture volatility and trend direction.

RVOL: Main factor of price movement.

Buy when price closes above current time frame 20 ema and current time frame 20 ema is above higher time frame 20 ema. Stop loss just below the low of last candle. One can use current time frame 20 ema, higher time frame 20 ema or kama as stop loss depending upon type of asset class and risk appetite. The ideal way is to keep 20 ema as trailing sl if one wants to trail with trend.

Sell when price closes below current time frame 20 ema and current time frame 20 ema is lower than higher time frame 20 ema. Stop loss just above high of last candle.

Ideal target is 1.5 or 2 times of stop loss.

Entry and exit time depends on trading style. Eg. if you want to enter and exit in 5 min time frame, then choose 15 min or 1h as higher time frame as trend filter. Buy and sell signals are also plotted based on this strategy. One should always go with the higher time frame trend. Opting higher time frame trend filter always filters out market noises.

HMA+RVOL Strategy Hariss 369The Hull Moving Average (HMA) is a smooth, fast, and highly responsive moving average created by Alan Hull. It reduces lag significantly while still maintaining smoothness, making it one of the most popular tools for trend detection and entries. It is widely used for trend filter. Hull Moving Average(HMA) with RVOL strengthens the trend as volume is prime factor of price movement.

Trading with HMA: Simple method is buy when price closes above HMA , stop less below the low of last candle and target is 1.5 or 2 times of stop loss. The reverse is for sell. The HMA automatically turns to green on bull trend and red on bear trend for better visual confirmation.

Adding RVOL to HMA is better method of trading. Buy signal is initiated when price closes above HMA and RVOL is greater than 1.2. Sell signal is initiated when price closes below 89 HMA and rovl is greater than 1.2. One can change the value of RVOL according to trading style and type asset being traded.

It is a back tested strategy.

ai cruhsera pullback strategy to donchain lower and upperbands.. best for cypro lower timeframe scalping..

Volume weighted average price band strategy [Kevin-Patrick]VWAP Bands strategy, Credit

VWAP Machine Learning Bands is an advanced indicator designed to enhance trading analysis by integrating VWAP with a machine learning-inspired adaptive smoothing approach. This tool helps traders identify trend-based support and resistance zones, predict potential price movements, and generate dynamic trade signals.

Key Features

Adaptive ML VWAP Calculation: Uses a dynamically adjusted SMA-based VWAP model with volatility sensitivity for improved trend analysis.

Forecasting Mechanism: The 'Forecast' parameter shifts the ML output forward, providing predictive insights into potential price movements.

Volatility-Based Band Adjustments: The 'Sigma' parameter fine-tunes the impact of volatility on ML smoothing, adapting to market conditions.

Multi-Tier Standard Deviation Bands: Includes two levels of bands to define potential breakout or mean-reversion zones.

Dynamic Trend-Based Colouring: The VWAP and ML lines change colour based on their relative positions, visually indicating bullish and bearish conditions.

Custom Signal Detection Modes: Allows traders to choose between signals from Band 1, Band 2, or both, for more tailored trade setups.

+ Strategy setting by Kevin-Patrick

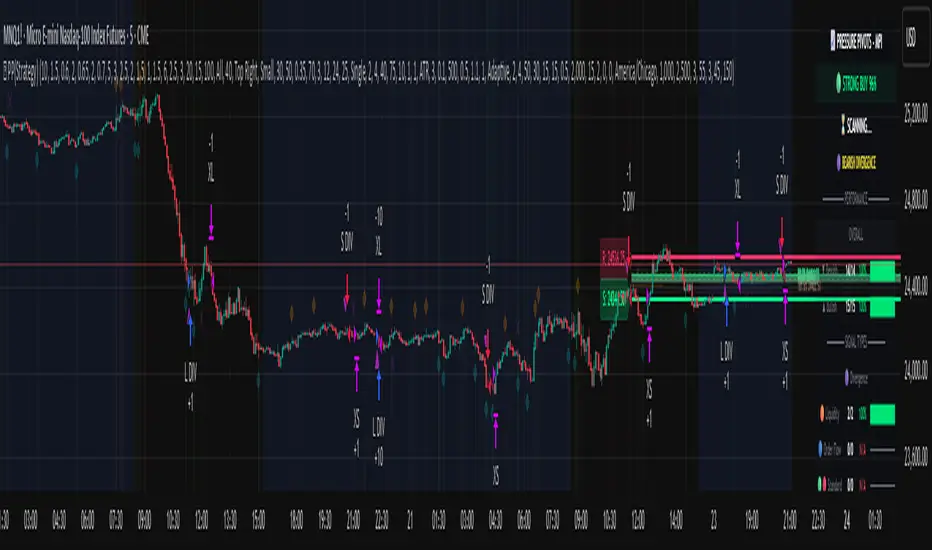

Pressure Pivots - MPI (Strategy)⇋ PRESSURE PIVOTS — MARKET PRESSURE INDEX STRATEGY

A comprehensive reversal trading system that combines order flow pressure analysis, multi-factor confluence detection, and adaptive machine learning to identify high-probability turning points in liquid markets.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

CORE INNOVATION: MARKET PRESSURE INDEX (MPI)

Traditional indicators measure price movement. The Market Pressure Index measures the force behind the movement.

How MPI Works:

Every bar tells two stories through volume distribution:

• Buy Pressure: Volume × (Close - Low) / (High - Low)

• Sell Pressure: Volume × (High - Close) / (High - Low)

• Net Pressure: Buy Pressure - Sell Pressure

This raw pressure is then normalized against baseline activity to create the bounded MPI (-1.0 to +1.0):

• Smooth Pressure: EMA(Net Pressure, period)

• Baseline Activity: SMA(|Net Pressure|, period × 2)

• MPI: (Smooth Pressure / Baseline) × Sensitivity

What MPI Reveals:

MPI > +0.7: Extreme buy pressure → Exhaustion potential

MPI = +0.2 to +0.7: Healthy bullish momentum

MPI = -0.2 to +0.2: Neutral/balanced pressure

MPI = -0.7 to -0.2: Healthy bearish momentum

MPI < -0.7: Extreme sell pressure → Exhaustion potential

Why It Works:

Two bars can both move 10 points, but if one closes at the high on high volume (aggressive buying) and the other closes mid-range on average volume (weak buying), only MPI distinguishes between sustainable momentum and exhaustion. This volume-weighted pressure analysis reveals conviction behind price moves—the key to timing reversals.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

SEVEN-FACTOR CONFLUENCE SYSTEM

MPI extremes alone aren't enough. The system requires multiple independent confirmations through weighted scoring:

1. DIVERGENCE (Weight: 3.0) — Premium Signal Type: DIV

Price makes new high but MPI makes lower high (or inverse for bullish)

• Detection: Tracks pivots with 5-bar lookback, compares price vs MPI at pivot points

• Signal: Purple triangles, highest weight (pressure weakening while price extends)

2. LIQUIDITY SWEEP (Weight: 2.5) — Premium Signal Type: LIQ

Price breaks swing high/low within 0.3 ATR then reverses

• Detection: Break within tolerance + close back through level

• Signal: Orange triangles, second-highest weight (stop hunt reversal)

3. ORDER FLOW IMBALANCE (Weight: 2.0) — Premium Signal Type: OF

Aggressive buying/selling 50% above normal

• Detection: EMA(aggressive volume) vs SMA(imbalance) threshold

• Signal: Aqua triangles, institutional positioning

4. VELOCITY EXHAUSTION (Weight: 1.5)

Parabolic move (2+ ATRs in 3 bars) + extreme MPI

• Detection: |3-bar price change / ATR| > threshold + MPI > ±0.5

• Indicates: Momentum deceleration, blow-off top/bottom

5. WICK REJECTION (Weight: 1.5)

Single bar: wick > 60% of range, or sequence: 2 bars with 40% + 30% wicks

• Detection: Shooting stars (bearish) or hammers (bullish)

• Indicates: Intrabar rejection, battle won by opposing side

6. VOLUME SPIKE (Weight: 1.0)

Volume > 20-bar average × multiplier (default: 2.0x)

• Detection: Participation surge confirmation

• Lowest weight: Can be manipulated, better as confirmation

7. POSITION FACTOR (Weight: 1.0)

At 10-bar highest (bearish) or lowest (bullish)

• Detection: Structural positioning for reversal

• Base requirement: Must be at extreme to score

Scoring Logic:

Premium Signals (DIV/LIQ/OF): Must score ≥6.0 (default premiumThreshold)

Standard Signals (STD): Must score ≥4.0 (default standardThreshold)

Example Scoring:

Divergence (3.0) + Liquidity Sweep (2.5) + Volume (1.0) = 6.5 → FIRES (DIV signal)

Recent High (1.0) + Wick (1.5) + Volume (1.0) + Velocity (1.5) = 5.0 → FIRES (STD signal)

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ADAPTIVE LEARNING ENGINE

Unlike static strategies, this system learns from every trade and optimizes itself.

Performance Tracking:

Every trade records:

• Entry Score: Confluence level at entry

• Signal Type: DIV / LIQ / OF / STD

• Win/Loss: Boolean outcome

• R-Multiple: (Exit - Entry) / (Entry - Stop)

• MAE: Maximum Adverse Excursion (worst drawdown)

• MFE: Maximum Favorable Excursion (best profit reached)

Three Adaptive Parameters:

1. Signal Threshold Adaptation

If Win Rate < Target (45%): RAISE threshold → fewer signals, better quality

If Win Rate > Target + 10% AND good R: LOWER threshold → more signals, profitable

2. Stop Distance Adaptation

If Avg MAE > 0.85 AND WR < 50%: WIDEN stops → reduce premature exits

If Avg MAE < 0.4 AND WR > 55%: TIGHTEN stops → reduce risk

3. Target Distance Adaptation

If Avg MFE > Target × 1.5: EXTEND targets → capture more of runners

If Avg MFE < Target × 0.7: SHORTEN targets → take profits faster

Signal Type Filtering:

The system tracks performance by type (DIV/LIQ/OF/STD):

• If Type WR < 40% AND Avg R < 0.8: Type DISABLED

• If Type WR ≥ 40% OR Avg R ≥ 0.8: Type RE-ENABLED

Example: If OF signals consistently lose while DIV signals win, system automatically stops taking OF signals and focuses on DIV.

Warmup Period:

First 30 trades (default) gather baseline data with relaxed thresholds. After warmup, full adaptation activates.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPLETE POSITION MANAGEMENT

Dynamic Position Sizing:

Base Contracts = (Equity × Risk%) / (Stop Distance × Point Value)

Then multiplied by:

• Score Bonus: Up to +50% for highest-scoring signals

• Signal Type Bonus: DIV signals +50%, LIQ signals +30%

• Streak Multiplier: After 3 losses: 50% reduction, After 3 wins: 25% increase

Example: High-scoring DIV signal on winning streak = 3-4× larger position than weak STD signal on losing streak

Entry Modes:

Single Entry: Full size at once, exit at TP2 (or partial at TP1)

Tiered Entry: 40% at TP1 (2R), 60% at TP2 (4R adaptive)

Stop Management (3 Modes):

Structural: Beyond recent 20-bar swing high/low + buffer

ATR: Fixed ATR multiplier (default: 2.0 ATR, then adapts)

Hybrid: Attempt structural, fallback to ATR if invalid

Plus:

• Breakeven: Move stop to entry ± 1 tick when 1R reached

• Trailing: Activate when 1.5R reached, trail 0.8R behind price

• Max Loss Override: Cap dollar risk regardless of calculation

Target Management:

Fixed Mode: TP1 = 2R, TP2 = 4R

Adaptive Mode: TP1 = 2R fixed, TP2 adapts based on MFE analysis

Partial Exits: Default 50% at TP1, remainder at TP2 or trailing stop

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

COMPREHENSIVE RISK CONTROLS

Daily Limits:

• Max Daily Loss: $2,000 default → HALT trading

• Max Daily Trades: 15 default → prevent overtrading

• Max Concurrent: 2 positions → limit correlation risk

Session Controls:

• Trading Hours: Specify start/end times + timezone

• Weekend Block: Optional (avoid crypto weekend volatility)

Prop Firm Protection (Live Trading Only):

• Daily Loss Limit: Stricter of general or prop limit ($1,000 default)

• Trailing Drawdown: Tracks high water mark, HALTS if breach ($2,500 default)

• Reset on Reload: Optional high water mark reset

Liquidity Filter (Optional):

• Time-Based: Avoid first/last X minutes of session

• Volume-Based: Require minimum volume ratio (0.5× average default)

Market Regime Filter (Optional):

• ADX-Based: Only trade when ADX > threshold (trending)

• Block: Consolidation (ADX < 20) or Transitional regimes

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

REAL-TIME DASHBOARD

MPI Gauge Section:

Shows current pressure: 🟢 STRONG BUY (+0.5 to +1.0), 🟩 BUY PRESSURE (+0.2 to +0.5), ⚪ NEUTRAL (-0.2 to +0.2), 🟥 SELL PRESSURE (-0.5 to -0.2), 🔴 STRONG SELL (-1.0 to -0.5)

Signal Status Section:

• Active Signals: "🔴 DIV SELL" (purple background), "🟢 LIQ BUY" (orange), "🔵 OF SELL" (aqua), "🟢 STD BUY" (green)

• Warnings: "⚠️ BEAR WARNING" / "⚠️ BULL WARNING" (yellow) — setup forming, not full signal

• Scanning: "⏳ SCANNING..." (gray) — no signal active

• Confidence Bar: Visual score display "██████░░░░" showing confluence strength

Divergence Indicator:

"🟣 BEARISH DIVERGENCE" or "🟡 BULLISH DIVERGENCE" when detected

Performance Statistics:

• Overall Win Rate: Wins/Total with visual bar (lime ≥70%, yellow 50-70%, red <50%)

• Directional: Bearish vs Bullish win rates separately

• By Signal Type: DIV / LIQ / OF / STD individual performance tracking

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

KEY PARAMETERS EXPLAINED

🎯 Pressure Engine:

• MPI Period (5-50, default: 14): Smoothing period — lower for scalping, higher for position trading

• MPI Sensitivity (0.5-5.0, default: 1.5): Amplification — lower compresses range, higher more extremes

🔍 Detection:

• Wick Threshold (0.3-0.9, default: 0.6): Minimum wick-to-range ratio for rejection

• Volume Spike (1.2-3.0x, default: 2.0): Multiplier above average for spike

• Aggressive Ratio (0.5-0.9, default: 0.65): Close position in range for aggressive orders

• Velocity Threshold (1.0-5.0 ATR, default: 2.0): ATR-normalized move for exhaustion

• MPI Extreme (0.5-0.95, default: 0.7): Level considered overbought/oversold

⚖️ Weights:

• Divergence: 3.0 (highest — pressure weakening)

• Liquidity: 2.5 (second — stop hunts)

• Order Flow: 2.0 (institutional positioning)

• Velocity: 1.5 (momentum exhaustion)

• Wick: 1.5 (rejection patterns)

• Volume: 1.0 (lowest — can be manipulated)

🎚️ Thresholds:

• Premium (4.0-15.0, default: 6.0): Score for DIV/LIQ/OF signals

• Standard (2.0-8.0, default: 4.0): Score for STD signals

• Warning Confluence (1-4, default: 2): Factors for yellow diamond warnings

🧬 Adaptive:

• Enable (true/false, default: true): Master learning switch

• Warmup Trades (5-100, default: 30): Data collection before adaptation

• Lookback (20-200, default: 50): Recent trades for performance calculation

• Adapt Speed (0.05-0.50, default: 0.15): Parameter adjustment rate

• Target Win Rate (30-70%, default: 45%): Optimization goal

• Target R-Multiple (0.5-5.0, default: 1.5): Risk/reward goal

💼 Position:

• Base Risk (0.1-10.0%, default: 1.5%): Equity risked per trade

• Max Contracts (1-100, default: 10): Hard position limit

• DIV Bonus (1.0-3.0x, default: 1.5): Size multiplier for divergence signals

• LIQ Bonus (1.0-3.0x, default: 1.3): Size multiplier for liquidity signals

🛡️ Stops:

• Mode (Structural/ATR/Hybrid, default: ATR): Stop placement method

• ATR Multiplier (0.5-5.0, default: 2.0): Stop distance in ATRs (adapts)

• Breakeven at (0.3-3.0R, default: 1.0R): When to move stop to entry

• Trail Trigger (0.5-5.0R, default: 1.5R): When to activate trailing

• Trail Offset (0.3-3.0R, default: 0.8R): Distance behind price

🎯 Targets:

• Mode (Fixed/Adaptive, default: Fixed): Target placement method

• TP1 (0.5-10.0R, default: 2.0R): First target for partial exit

• TP2 (1.0-15.0R, default: 4.0R): Final target (adapts in adaptive mode)

• Partial % (0-100%, default: 50%): Position percentage to exit at TP1

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

PROFESSIONAL USAGE PROTOCOL

Phase 1: Paper Trading (Weeks 1-4)

• Setup: Default settings, all adaptive features ON, 0.5% base risk

• Goal: 30+ trades for warmup, observe MPI behavior and signal frequency

• Adjust: MPI sensitivity if stuck near neutral or always at extremes

• Threshold: Raise/lower if too many/few signals

Phase 2: Micro Live (Weeks 5-8)

• Requirements: WR >43%, at least one type >55%, Avg R >0.8

• Setup: 10-25% intended size, 0.5-1.0% risk, 1 position max

• Focus: Execution quality, match dashboard performance

• Journal: Screenshot every signal, track outcomes

Phase 3: Full Scale (Month 3+)

• Requirements: WR >45% over 50+ trades, Avg R >1.2, drawdown <15%

• Progression: Months 3-4 (1.0-1.5% risk), 5-6 (1.5-2.0%), 7+ (1.5-2.5%)

• Maintenance: Weekly dashboard review, monthly deep analysis

• Warnings: Reduce size if WR drops >10%, consecutive losses >7, or drawdown >20%

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DEVELOPMENT INSIGHTS

The Pressure Insight: Emerged from analyzing intrabar volume distribution. Within every candlestick, volume accumulates at different price levels. MPI deconstructs this to reveal conviction behind moves.

The Confluence Challenge: Early versions using MPI extremes alone achieved only 42% win rate. The seven-factor confluence system emerged from testing which combinations produced reliable reversals. Divergence + liquidity sweep became the strongest setup (68% win rate in isolation).

The Adaptive Breakthrough: Per-signal-type performance tracking revealed DIV signals winning at 71% while OF signals languished at 38%. Adaptive filtering disabled weak types automatically, recovering win rate from 39% to 54% during the 2022 volatility spike.

The Position Sizing Revelation: Dynamic sizing based on signal quality and recent performance increased Sharpe ratio from 1.2 to 1.9 while decreasing max drawdown from 18% to 12% over 500 trades. Bigger positions on better signals = geometric edge amplification.

The Risk Control Lesson: Testing with $50K accounts revealed catastrophic failure modes: daily loss cascades, overtrading commission bleed, weekend gap blowouts. Multi-layer controls (daily limits, concurrent caps, prop firm protection) became essential.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

LIMITATIONS & ASSUMPTIONS

What This Is NOT:

• NOT a Holy Grail: Typical performance 52-58% WR, 1.3-1.8 avg R, probabilistic edge

• NOT Predictive: Identifies high-probability conditions, doesn't forecast prices

• NOT Market-Agnostic: Best on liquid auction-driven markets (futures, forex, major crypto)

• NOT Hands-Off: Requires oversight for news events, gaps, system anomalies

• NOT Immune to Regime Changes: Adaptive engine helps but cannot predict black swans

Critical Assumptions:

1. Volume reflects intent (valid for regulated markets, violated by wash trading)

2. Pressure extremes mean-revert (true in ranging/exhaustion, fails in paradigm shifts)

3. Stop hunts exist (valid in liquid markets, less in thin/random walk periods)

4. Past patterns persist (valid in stable regimes, fails when structure fundamentally changes)

Works Best On: Major futures (ES, NQ, CL), liquid forex pairs (EUR/USD, GBP/USD), large-cap stocks, BTC

Performs Poorly On: Low-volume stocks, illiquid crypto pairs, news-driven headline events

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

RISK DISCLOSURE

Trading futures, forex, and leveraged instruments involves substantial risk of loss and is not suitable for all investors. Past performance is not indicative of future results. This strategy is provided for educational purposes only and should not be construed as financial advice.

The adaptive engine learns from historical data—there is no guarantee that past relationships will persist. Market conditions change, volatility regimes shift, and black swan events occur. No strategy can eliminate the risk of loss.

Users must validate performance on their specific instruments and timeframes before risking capital. The developer makes no warranties regarding profitability or suitability. Users assume all responsibility for trading decisions and outcomes.

"The market doesn't care about your indicators. It only cares about pressure—who's willing to pay more, who's desperate to sell. Find the exhaustion. Trade the reversal. Let the system learn the rest."

Taking you to school. — Dskyz, Trade with insight. Trade with anticipation.

smart honey 2.0The smart honey 2.0 is a long-only trading strategy based on averaging entries.

At "Entry" you can set to enter a trade at a specified averaging level. The best backtest result at "only 4th averaging".

"Tp" is take profit.

"Sensitivity" controls the frequency of trades - lower sensitivity means fewer, but higher-quality trades.

Settings recommendations

For 1m-5m timeframes, use low sensitivity and take profit values. For higher timeframes, increase the take profit value.

For example, a profitable setting for many coins on a 5-minute timeframe is

Tp = 1.5%

Sensitivity = 2.7

Entry = only 4th averaging

The strategy features a "Blue line" showing liquidity clusters influenced by Sensitivity. Price often bounces off this line.

You can also set alerts for lists of coins, receiving notifications at each new candle about active positions

Hull VWMA Crossover StrategyA simple variation on the Hull Moving Average which reacts faster to high volume events, making it more responsive in those cases than even the standard Hull average -- CREDIT GOES TO Saolof - -- Edited into a strategy with some more options that im going to continue to refine. LMK if theres any features or confluence you want me to add -- cheers!

RSI + 55 EMA + Volume (SL Marked, No Engulfing)This is to help entering in trades by considering 50 EMA and RSI indicators, Volume is used for confirmations

LSI Pro - Enhanced Sweep Lines + Trading StrategyThis is a very powerful and sensitive indicator, it embrace the institutional sweep, signaling the high volumes area with the liquidity areas and levels with bear or bull confirmations.

and more ...

It works very good with most instruments such crypto - forex and stocks.

write me to get access.

Alpha VWAP Regime🔥 Alpha VWAP Regime — Institutional VWAP Strategy (Closed Source)

Alpha VWAP Regime is a multi-layered VWAP trading system that identifies the active market regime and adapts its signals based on institutional liquidity behavior.

This strategy is closed-source because it uses a proprietary combination of VWAP structures, anchored pivot logic, band deviations, and regime detection filters that are not publicly available.

🧠 How the Strategy Works (Conceptual Explanation)

This strategy does not rely on a single VWAP line.

Instead, it builds a VWAP matrix consisting of:

1) Session VWAP

Defines fair value for the current session.

Used to detect intraday directional bias.

2) Anchored VWAP (AVWAP)

Automatically anchored to swing highs and lows (pivot-based).

Tracks where large players accumulated or distributed positions.

3) VWAP Bands (±1σ and ±2σ)

Used as dynamic volatility envelopes:

±1σ = fair-value zone / no-trade area

±2σ = mean-reversion extremes

4) Market Regime Classification (ADX-based)

The strategy determines which environment the market is in:

Trending Regime: ADX above threshold

Ranging Regime: ADX below threshold

Breakout Regime: Volume-based breakout of AVWAP

Each regime activates a different entry model.

📌 Entry Logic (High-Level Overview)

Trend Mode

Triggered only when ADX confirms a trend.

Entries occur near VWAP or −1σ using price-action confirmation.

Mean Reversion Mode

Activated when the market is ranging.

Entries target the ±2σ deviation bands.

Breakout Mode

Triggered by price crossing AVWAP with above-average volume.

Used to catch institutional continuation moves.

ALL Mode

Combines the three models for a full adaptive system.

📉 Exits & Risk Management

All stops and targets use ATR-based volatility sizing

Trend trades aim for larger targets

Mean-reversion trades aim for smaller snapback moves

Breakouts use wider stops but high R:R

🔍 How to Use the Strategy

Load the script on a clean chart

Choose your preferred regime mode (Trend / MR / Breakout / ALL)

Optionally hide VWAP indicators and display signals only

Use realistic position sizing and commissions

Evaluate performance across multiple assets and timeframes

🔒 Why It Is Closed-Source

The code uses:

A custom anchoring engine

Multi-layered regime filters

Dynamic VWAP matrix

Prop logic for bias scoring

These components were built from scratch and form a unique decision model, so the source is protected.

🇸🇦 الشرح العربي لاستراتيجية Alpha VWAP Regime

Alpha VWAP Regime هي استراتيجية تداول مؤسسية متقدمة تعتمد على تحليل السيولة، وتحديد حالة السوق (Market Regime)، ودمج عدة طبقات من VWAP داخل نموذج واحد متكيف.

الهدف من الاستراتيجية هو التداول في المناطق التي يتواجد فيها المال الذكي، وتجنب التداول في المناطق العشوائية أو منخفضة الجودة.

________________________________________

🧠 كيف تعمل الاستراتيجية؟

الاستراتيجية لا تعتمد على VWAP واحد، بل تستخدم “مصفوفة VWAP” كاملة تتكوّن من:

1) VWAP اليومي (Session VWAP)

يُستخدم لتحديد القيمة العادلة خلال الجلسة، وتحديد الاتجاه اللحظي (Intraday Bias).

________________________________________

2) VWAP المثبّت (Anchored VWAP)

يتم تثبيته تلقائيًا على:

• القمم المهمة (Swing Highs)

• القيعان المهمة (Swing Lows)

ويساعد في تحديد مناطق تمركز المؤسسات، ومناطق الانعكاس أو الاختراقات الحقيقية.

________________________________________

3) نطاقات VWAP (±1σ و ±2σ)

تُستخدم كأغلفة ديناميكية للسيولة والتقلب:

• ±1σ = منطقة القيمة العادلة (Fair-Value Zone)

→ غالبًا منطقة غير مناسبة للتداول (No-Trade Zone)

• ±2σ = مناطق التشبّع الحركي (Extremes)

→ مناسبة لاستراتيجيات الانعكاس (Mean Reversion)

________________________________________

4) تصنيف حالة السوق Market Regimes

الاستراتيجية تستخدم مؤشر ADX لتحديد حالة السوق الحالية:

حالة السوق الوصف

Trending اتجاه واضح وقوي

Ranging تذبذب بدون اتجاه

Breakout اختراق مدعوم بحجم تداول

كل Regime يفعّل نموذج دخول مختلف داخل الاستراتيجية.

________________________________________

🎯 نماذج الدخول داخل الاستراتيجية

1) نموذج الاتجاه (Trend Mode)

يعمل فقط عندما يكون السوق في اتجاه حقيقي.

يعتمد على دخول Pullbacks قرب VWAP أو نطاق −1σ مع تأكيد شموعي.

________________________________________

2) نموذج الانعكاس (Mean Reversion Mode)

يعمل فقط عندما يكون السوق متذبذبًا (Range).

الدخول عند لمس ±2σ بهدف العودة نحو VWAP.

________________________________________

3) نموذج الاختراق (Breakout Mode)

يستخدم اختراقات Anchored VWAP

ولكن بشرط وجود حجم تداول أعلى من المتوسط (Volume Confirmation).

________________________________________

4) وضع الدمج (ALL Mode)

يجمع بين النماذج الثلاثة ويجعل الاستراتيجية متكيفة تلقائيًا مع كل حالات السوق.

________________________________________

📉 الخروج وإدارة المخاطر

تستخدم الاستراتيجية نظامًا ديناميكيًا لإدارة المخاطر:

• وقف الخسارة مبني على ATR

• الأهداف مبنية على طبيعة النموذج

• الصفقات الاتجاهية تستهدف R:R أعلى

• صفقات MR أقصر وأسرع

• صفقات Breakout أوسع ولكن مدعومة بزخم قوي

________________________________________

🧩 كيفية استخدام الاستراتيجية

1. ضع الاستراتيجية على رسم بياني نظيف بدون مؤشرات إضافية

2. اختر نموذج الدخول المناسب من الإعدادات

3. فعّل أو أخفِ خطوط VWAP حسب الحاجة

4. استخدم إعدادات مخاطرة واقعية

5. اختبر الاستراتيجية على عدة أسواق وفريمات

________________________________________

🔒 سبب إغلاق الكود

تم إغلاق الكود لأنها تعتمد على:

• محرك تثبيت AVWAP خاص

• نظام Regime Detection متقدم

• مصفوفة VWAP متعددة الطبقات

• منطق دخول/خروج خاص تم تطويره بالكامل

كل ذلك يتطلب حماية الملكية الفكرية، لذا تم نشرها Closed-Source.

TSI.LTA | Base BTC 1DTSI.LTA | Base BTC 1D is a closed‑source trend‑following strategy designed for BTC on the 1D timeframe .

It focuses on participating in the main directional moves of the market while avoiding as much short‑term noise as possible.

📊 The script:

Uses a combination of moving‑average–based filters and volatility bands to define the active trend.

Applies optional volume filters to avoid low‑participation or exhausted moves.

Includes risk‑management controls (Stop Loss, Take Profit, Trailing Stop) that work on a per‑trade basis.

All entries and exits are confirmed at bar close and the script does not repaint .

This makes it suitable for backtesting, alerts and external automation.

█ 💡 CONCEPTS

This strategy is built around a few simple ideas:

1 — Trend first.

Positions are only taken when a group of smoothed trend filters agree on direction.

The goal is to ride larger swings, not to scalp each fluctuation.

2 — Volatility awareness.

Standard‑deviation–based bands help avoid entries in abnormal spikes or during very compressed ranges.

3 — Participation filter.

Optional volume‑based conditions (VWMA, OBV slope, MFI, volume Z‑score) try to ensure that entries occur when the market shows enough activity, not during dead phases.

4 — Risk defined in advance.

Stop‑loss and trailing‑stop inputs are expressed as percentages relative to entry price, so users can align them with their own risk tolerance.

The logic is purposely conservative: it is expected to stay flat during parts of the market where the trend is unclear or participation is weak.

█ ⚙️ FEATURES & INPUTS

This section follows approximately the order of the script’s inputs, so users can read here and then match what they see in the “Inputs” tab.

1 — 📐 Trend filters

These inputs control how the strategy detects the underlying trend:

DEMA / Gaussian / SMMA lengths

Control how fast or slow the trend reacts to price changes.

Shorter lengths → more responsive, more trades, more noise.

Longer lengths → slower reaction, fewer trades, more filtering.

Volatility Bands (SD length & multipliers)

Standard‑deviation bands around the smoothed price series.

They are used to avoid entries during extreme moves or very narrow ranges where a breakout is not yet confirmed.

In practice, these settings let the user choose between a more “aggressive” trend follower (shorter lengths, smaller bands) or a more “patient” one.

2 — 📊 Volume filters (optional)

These filters are meant to restrict trades to periods where the market shows meaningful participation:

VWMA filter

Requires price to be aligned with a Volume‑Weighted Moving Average, which de‑emphasizes moves on very low volume.

OBV slope filter

Uses the slope of On‑Balance Volume to check that net volume flow supports the direction of the trade.

MFI band filter

Uses the Money Flow Index to avoid taking new entries in zones that often correspond to exhaustion (extreme values defined by the user).

Volume Z‑Score

Compares current volume to its recent history. Trades can be restricted when volume is unusually low or out of character for that period.

When any of these filters are turned off, the strategy relies only on price‑based trend and volatility logic.

When they are on, trades are more selective and may be fewer.

3 — 🛡️ Risk management

These inputs define how individual trades are managed once entered.

They do not change the trend logic itself:

Stop Loss (%)

A percentage move against the entry price that will close the position.

Typical values on BTC 1D remain in the single‑digit range so that no single trade risks an unrealistic portion of equity.

Take Profit (%)

An optional fixed target that closes the trade when price has moved a chosen percentage in favor.

This can be disabled if the user prefers to let the trend filters perform the exit.

Trailing Stop (%)

A stop that follows the most favorable price reached since entry.

When the “use lower timeframe peak” option is enabled, peaks can be detected on a lower timeframe for more granular trailing, while decisions still occur at the close of the 1D bar.

Fixed SL/TP Price and Activation Date

Allow defining absolute price levels and a date from which they start applying.

This is useful when the user wants structural protection around known price zones.

The combination of these controls determines how deep a pullback the user is willing to tolerate and how much profit they are prepared to give back in order to stay in trends.

4 — 🚫 Filter failure & cooldown

To avoid over‑trading in difficult environments, the script can:

Automatically exit when filters remain unfavorable for a configurable number of bars.

Enter a cooldown period, during which no new trades are taken, even if some conditions improve.

These mechanisms are intended to protect capital during choppy or low‑quality phases rather than force constant exposure.

█ 📚 HOW TO USE

A suggested process for using this strategy as a study tool:

1 — Start on BTC 1D.

Apply the script to BTCUSD or BTC/USDT on the 1D timeframe, with default inputs.

2 — Open the Strategy Tester.

Choose a time window (for example a full halving cycle, a crash + recovery period, or just the most recent bull leg).

3 — Compare with Buy & Hold.

For the same window, look at:

Net profit of the strategy vs Buy & Hold.

Max drawdown of the strategy vs Buy & Hold.

The goal is not to hit a particular number, but to see whether, in that window, the strategy manages to:

Provide a smoother equity curve (lower drawdown),

While still performing at least as well as, or better than, simply holding the asset.

4 — Experiment with risk inputs.

Vary Stop Loss, Trailing Stop and the volume filters.

After each change, re‑check the same two questions above. This should make clear how each input affects the trade‑off between participation and risk.

5 — Forward‑test.

Before using any configuration with real capital, let it run for a while in paper‑trading or demo conditions.

█ 🚧 LIMITATIONS

The strategy is built and tuned primarily for BTC on 1D.

It can be used on other symbols and timeframes, but behavior may differ and requires new testing.

In very tight ranges or during event‑driven gaps, trend logic may enter later than discretionary trading would. This is expected for a conservative trend‑following approach.

Results from historical backtests depend on data quality, broker settings, fees and slippage configured in the Strategy Tester.

█ 📝 NOTES

Signals are generated on bar close.

The script is closed‑source, but the description explains the main ideas so users and moderators can understand what it does and how to use it.

The HUD on the chart is meant as a compact summary of the same statistics available in the Strategy Tester; it simply makes comparisons quicker.

█ ⚠️ DISCLAIMER

This strategy is provided for educational and research purposes only .

It is not financial advice and does not recommend any specific trades, assets, position sizes, or risk levels.

Users are fully responsible for:

Choosing their own risk parameters (Stop Loss, Take Profit, Trailing Stop, position sizing, etc.).

Testing the script on the markets and timeframes they intend to trade.

Verifying that any configuration is appropriate for their capital, risk tolerance and jurisdiction.

Past performance in backtests or examples does not guarantee future results.

Always test carefully before considering any live deployment.

Fractal Break Strategy with Time FilterThis strategy isn't complete yet but just curious how fast they will take it down. It is based off breaks of fractals and then taking the High/Low of the break candle

KELTNER + ADX 전략It's a trend strategy based on the Keltner channel and ADX. It's optimized for the Bitcoin Futures 15 Distribution Chart.

Braid Filter StrategyThis strategy is like a sophisticated set of traffic lights and speed limit signs for trading. It only allows a trade when multiple indicators line up to confirm a strong move, giving it its "Braid Filter" name—it weaves together several conditions.

The strategy is set up to use 100% of your account equity (your trading funds) on a trade and does not "pyramid" (it won't add to an existing trade).

1. The Main Trend Check (The Traffic Lights)

The strategy uses three main filters that must agree before it considers a trade.

A. The "Chad Filter" (Direction & Strength)

This is the heart of the strategy, a custom combination of three different Moving AveragesThese averages have fast, medium, and slow settings (3, 7, and 14 periods).

Go Green (Buy Signal): The fastest average is higher than the medium average, AND the three averages are sufficiently separated (not tangled up, which indicates a strong move).

Go Red (Sell Signal): The medium average is higher than the fastest average, AND the three averages are sufficiently separated.

Neutral (Wait): If the averages are tangled or the separation isn't strong enough.

Key Trigger: A primary condition for a signal is when the Chad Filter changes color (e.g., from Red/Grey to Green).

B. The EMA Trend Bars (Secondary Confirmation)

This is a simpler, longer-term filter using a 34-period Exponential Moving Average (EMA). It checks if the current candle's average price is above or below this EMA.

Green Bars: The price is above the 34 EMA (Bullish Trend).

Red Bars: The price is below the 34 EMA (Bearish Trend).

Trades only happen if the signal direction matches the bar color. For a Buy, the bar must be Green. For a Sell, the bar must be Red.

C. ADX/DI Filter (The Speed Limit Sign)

This uses the Average Directional Index (ADX) and Directional Movement Indicators (DI) to check if a trend is actually in motion and getting stronger.

Must-Have Conditions:

The ADX value must be above 20 (meaning there is a trend, not just random movement).

The ADX line must be rising (meaning the trend is accelerating/getting stronger).

The strategy will only trade when the trend is strong and building momentum.

2. The Trading Action (Entry and Exit)

When all three filters (Chad Filter color change, EMA Trend Bar color, and ADX strength/slope) align, the strategy issues a signal, but it doesn't enter immediately.

Entry Strategy (The "Wait-for-Confirmation" Approach):

When a Buy Signal appears, the strategy sets a "Buy Stop" order at the signal candle's closing price.

It then waits for up to 3 candles (Candles Valid for Entry). The price must move up and hit that Buy Stop price within those 3 candles to confirm the move and enter the trade.

A Sell Signal works the same way but uses a "Sell Stop" at the closing price, waiting for the price to drop and hit it.

Risk Management (Stop Loss and Take Profit):

Stop Loss: To manage risk, the strategy finds a recent significant low (for a Buy) or high (for a Sell) over the last 20 candles and places the Stop Loss there. This is a logical place where the current move would be considered "broken" if the price reaches it.

Take Profit: It uses a fixed Risk:Reward Ratio (set to 1.5 by default). This means the potential profit (Take Profit distance) is $1.50 for every $1.00 of risk (Stop Loss distance).

3. Additional Controls

Time Filter: You can choose to only allow trades during specific hours of the day.

Visuals: It shows a small triangle on the chart where the signal happens and colors the background to reflect the Chad Filter's trend (Green/Red/Grey) and the candle bars to show the EMA trend (Lime/Red).

🎯 Summary of the Strategy's Goal

This strategy is designed to capture strong, confirmed momentum moves. It uses a fast, custom indicator ("Chad Filter") to detect the start of a new move, confirms that move with a slower trend filter (34 EMA), and then validates the move's strength with the ADX. By waiting a few candles for the price to hit the entry level, it aims to avoid false signals.