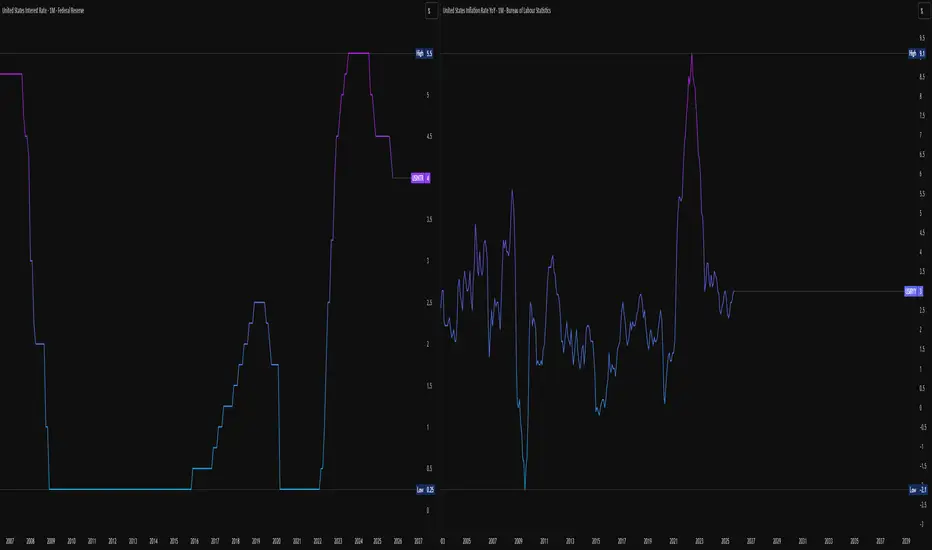

Real Rates, Policy Transition & Cross-Asset Bias (Update)Macro Overview

Global monetary policy remains in a transitional phase, not yet a true easing cycle.

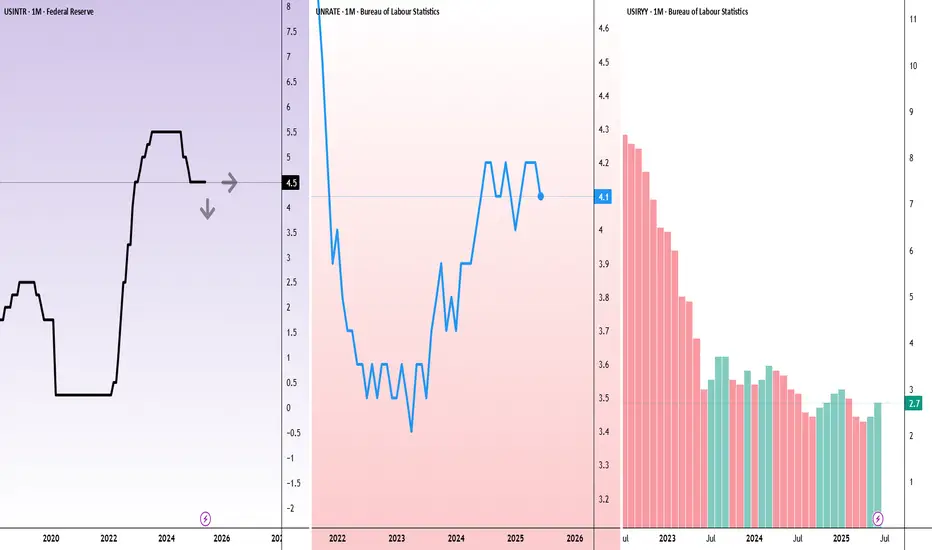

The Federal Reserve executed a hawkish 25 bps cut (4.25% → 4.00%), maintaining its QT program and signaling that further reductions are not guaranteed.

The ECB held rates steady amid slightly higher inflation, while the BoE remains restrictive.

Liquidity conditions, according to the latest H.4.1, confirm a net weekly drain, not an injection — contradicting market narratives of a “pivot.”

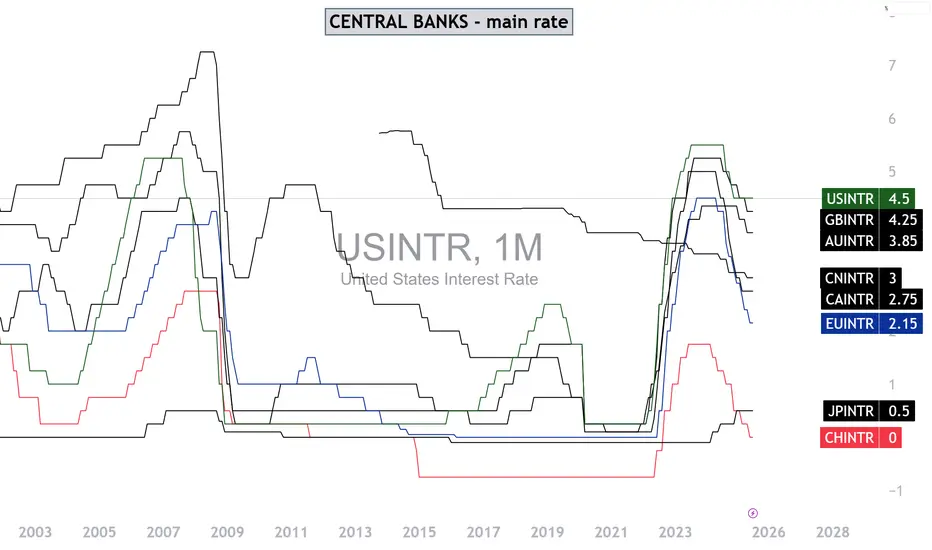

🏛️ Global Monetary Conditions (latest data)

United States 🇺🇸

Inflation (YoY): 3.0% (Sep 2025)

Policy Rate: 4.00% (after 25 bps cut)

Real Rate: ≈ +1.0%

Comment: The Fed delivered a hawkish cut; QT remains active. H.4.1 shows liquidity withdrawal (RRP and TGA up, reserves down).

Stance: Restrictive bias maintained.

Euro Area 🇪🇺

Inflation (YoY, flash): 2.1% (Oct 2025)

ECB Deposit Rate: 2.00% (unchanged)

Real Rate: ≈ –0.1%

Stance: Neutral; ECB focuses on currency and fiscal stability.

United Kingdom 🇬🇧

Inflation (YoY): 3.8% (Sep 2025)

Bank Rate: 4.00%

Real Rate: ≈ +0.2%

Stance: Restrictive; inflation remains well above target, limiting policy flexibility.

Brazil 🇧🇷

Inflation (YoY): 5.17% (Sep 2025)

Selic Rate: 15.00%

Real Rate: ≈ +9.8%

Stance: Active easing cycle under high nominal yields; strong carry-trade appeal.

Japan 🇯🇵

Inflation (YoY): 2.9% (Sep 2025)

Policy Rate: 0.50%

Real Rate: ≈ –2.4%

Stance: Ultra-loose, but with tightening bias emerging.

Data Note:

CFTC COT reports remain unavailable during the U.S. government shutdown.

Liquidity assessment must rely on the H.4.1 report, yield curves, and repo dynamics instead of position data.

💧 Liquidity Context (Federal Reserve)

Despite the rate cut, the Fed’s balance sheet continues to contract:

• Securities holdings: –7.1B

• Reverse Repo (RRP): +10.2B

• Treasury General Account (TGA): +50B

• Reserve balances: –85B

→ Net Liquidity: –59B (weekly)

Liquidity conditions are tighter, not looser.

Interpretation:

The Fed’s “insurance cut” contrasts with actual quantitative tightening and a measurable liquidity drain.

💡 Macro Bias Summary

Equities (NASDAQ / S&P500) – Neutral to slightly bullish tactically. The rate cut provides short-term relief, but QT and liquidity contraction limit upside potential.

Commodities (Gold / Oil / Copper) – Mixed bias. Gold capped by higher real yields; oil and copper remain driven by global demand expectations.

USD (DXY) – Bullish bias. Rate differentials and liquidity drain favor the dollar in the short term.

EUR/USD – Bearish bias. Euro policy stable, but U.S. remains tighter in real terms; spread still favors USD.

Crypto (BTC / ETH) – Range-bound and liquidity sensitive. Speculative flows remain correlated to net liquidity trends.

🧭 Cycle Interpretation

We remain in a prolonged transition, not a clean easing phase.

Real rates are positive, balance-sheet runoff continues, and central banks remain cautious after two years of inflation pressure.

The macro liquidity cycle is not yet expansionary, and risk assets should be traded selectively, not directionally.

Quote

“Fade the rhetoric, trade the flows — until net liquidity turns up decisively, ‘easing’ is a headline, not a condition.”

Trade ideas

$USINTR -Fed Delivers Rate Cut (October/2025)ECONOMICS:USINTR

October/2025

source: Federal Reserve

- The Federal Reserve lowered the federal funds rate by 25 bps to a target range of 3.75%–4.00% at its October 2025 meeting, in line with market expectations.

The move followed a similar cut in September,

bringing borrowing costs to their lowest level since 2022.

Policymakers cited increasing downside risks to employment in recent months while inflation has moved up since earlier in the year and remains somewhat elevated.

The Fed said it will continue to monitor the implications of incoming information for the economic outlook and would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of its goals.

In addition, the central bank decided to conclude the reduction of its aggregate securities holdings on December 1.

Fed Update: The Dissenting VoteSo I've covered last week's interest rate cut , but a word came out that there was a dissenting vote.

11 FOMC Members voted for a standard 25 bps cut.

1 FOMC Member (Steven Mirren - a Trump appointee recently from the White House) voted for a more aggressive 50 bps cut.

This matters because Mirren, with access to non-public White House data , saw something concerning enough to warrant a much larger stimulus. The question is, what does the WH know that justifies a double-sized cut? This dissent underscores the underlying economic risks Powell alluded to.

Impact & Outlook

Today markets sold off on the reduced certainty of future rate cuts. The hope for a quick series of cuts has been dampened.

The Fed is now firmly in a "meeting-by-meeting" mode. I do not expect a pre-set easing path. Future decisions will hinge entirely on incoming data, especially inflation reports and jobs numbers.

Powell pointed to policy uncertainty (tariffs, etc.) causing businesses to postpone hiring and investment, and a sharp drop in immigration reducing labor supply.

Implications

USD: Bullish. A patient Fed with a restrictive stance supports the dollar.

Equities: Bearish in the short term. The removal of the "Fed put" narrative and heightened uncertainty could lead to continued volatility and pressure on growth stocks.

Treasuries: Yields may stabilize or rise slightly as expectations for deeper cuts are priced out.

The Fed is walking a tightrope, and it really tells to prepare for heightened volatility driven by each new data point.

FOMC: Interest Rate Cut🏛️ Research Notes

Based on Chair Powell's press conference from September 17 '25, the FOMC decided to lower the federal funds rate by 1/4 percentage point. Since I’ve chosen to expand my research to include economic performance, I want to document the reasoning behind this decision.

Dual Considerations

Employment: The labor market has softened. The unemployment rate edged up to 4.3%, job gains slowed significantly (to just 29,000 per month over the past three months), and downside risks to employment have increased.

Inflation: Inflation remains elevated relative to the Fed’s 2% target. Total PCE inflation was 2.7% over the past 12 months, and core PCE was 2.9%. Recent tariff policies have also contributed to upward pressure on prices.

Shift in Risk Balance

The Fed noted that risks to employment are tilted to the downside, while risks to inflation are tilted to the upside. This creates a tension between the two parts of the dual mandate.

Given the increased downside risks to employment, the Committee judged it appropriate to ease monetary policy to support the labor market.

Economic Slowdown

GDP growth moderated to around 1.5% in the first half of 2025, down from 2.5% in 2024.

Consumer spending slowed, though business investment improved.

Housing activity remained weak.

Response to Evolving Conditions

The Fed aims to avoid letting a one-time price increase (e.g., from tariffs) become persistent inflation, while also supporting employment.

The rate cut is seen as a step toward a more neutral policy stance to better balance the competing risks.

The Fed remains data-dependent and is not committed to a preset policy path. The Fed cut rates primarily due to rising downside risks in the labor market, even though inflation remains above target. The decision reflects careful balancing between supporting employment and preventing inflation from becoming entrenched.

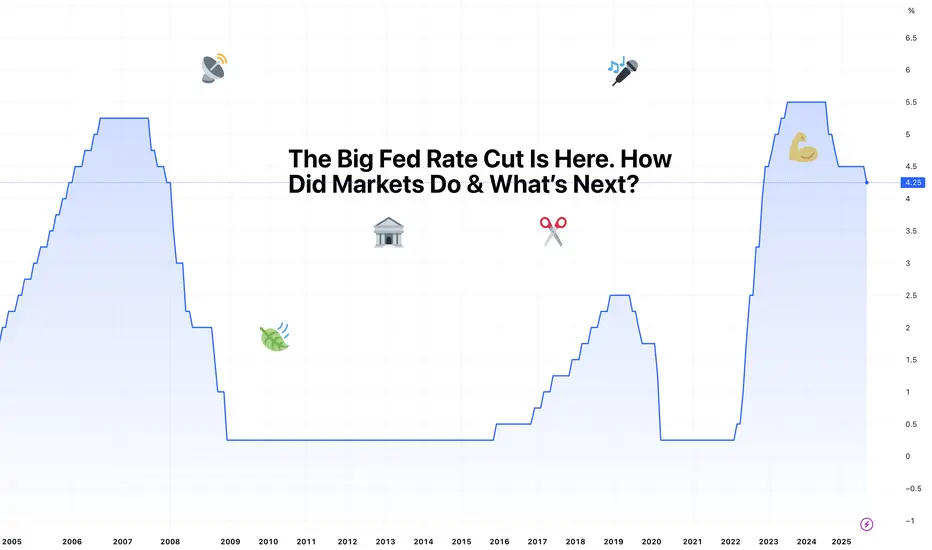

The Big Fed Rate Cut Is Here. How Did Markets Do & What’s Next?“ Best we can do is 25bps ,” officials, probably, when they gathered to lower the federal funds rate. It wasn’t the 50 basis points some of you had expected. But you also didn’t expect to hear that two more trims are most likely coming by year end.

Let’s talk about that and what it means for your trading.

🎤 Powell Delivers

The Federal Reserve finally trimmed rates for the first time in nine months, cutting the federal-funds rate by 25 basis points to 4%–4.25%. This was hardly a surprise.

Markets had already fully priced in a quarter-point move. But the real twist was the Fed boss hinting at two more cuts this year. With just two FOMC meetings on the calendar, it’s pretty clear: unless something changes dramatically, traders should expect a cut at both.

The decision wasn’t unanimous. Newly minted, Trump-appointed Fed governor Stephen Miran wanted to go big or go home with a 50bps slash. Powell, though, balanced his message by saying risks to the labor market had grown while inflation was still running at 2.9% (way above target).

What does this mean? The Fed’s dual mandate of price stability and full employment is officially leaning toward protecting jobs at the risk of flaring up inflation.

💵 Dollar Takes a Dive

The immediate reaction was classic. A weaker dollar is the natural byproduct of lower rates, and the greenback obliged by sliding against major peers.

The FX:EURUSD pushed toward $1.19, its highest in four years, while the FX:GBPUSD tested $1.37 and the FX:USDJPY sank below ¥146.

For forex traders, this was textbook: lower yields make the dollar less attractive, especially compared to rivals with steadier or higher returns. But that was a reaction to the initial shock.

By early Thursday the dollar bounced back, because markets love to overreact before correcting, but the broader trend is still tilted bearish .

📈 Stocks: Buy the Rumor, Sell the News

Stocks were less enthusiastic. The S&P 500 SP:SPX hovered near flat, the Nasdaq Composite NASDAQ:IXIC slipped 0.3% for a second straight loss, and the Dow Jones TVC:DJI managed to buck the trend with a 260-point climb.

The takeaway? Traders had already bought the rumor of rate cuts, jammed their cash into equities, so when Powell delivered the expected 25bps, it wasn’t enough to light another fire.

The bigger hope lies in those promised future cuts, which could set the stage for another push higher – especially if Big Tech earnings hold up through the third quarter. (For the record, earnings season is almost here.)

Thursday's futures contracts were showing a big jump ahead of the opening bell with Nasdaq futures up by more than 1%.

🟡 Gold Shines, Then Stumbles

Gold OANDA:XAUUSD did what gold usually does when the Fed loosens policy: it powered up. Bullion was surfing on the high point of its all-time record of $3,700, before sliding back under $3,640.

What’s the logic behind rising gold prices and a falling dollar? In a low-yield environment, non-yielding assets like gold look more attractive, and a weaker dollar only sweetens the deal for overseas buyers.

Still, this week’s whipsaw reminded everyone that gold is no straight line up – momentum is there, but so are the bears guarding resistance.

🟠 Bitcoin Shrugs

Crypto was more muted. Bitcoin BITSTAMP:BTCUSD slipped 1.2% after the cut, dipping toward $115,000, only to bounce back above $116,000 the next morning.

For the orange coin, the Fed story is just background noise. Institutional inflows and ETF demand remain the key drivers, and traders are still gauging whether crypto wants to behave like a risk asset or play its “digital gold” role.

Still, the OG coin remains off its $124,000 record from mid-August , the market seems caught between consolidation and correction.

⚖️ The Balancing Act

The Fed’s challenge is clear: unemployment is rising, job gains are slowing , and payrolls have been revised lower for months.

At the same time, inflation has crept back up, with core prices still well above target. Cutting too much risks reigniting price pressures; cutting too little risks a labor-market slide that could snowball into recession.

Powell chose the middle ground – a modest 25bps – and teased with two more to calm investor nerves.

👀 What’s Next?

Markets now have a new playbook: watch every jobs report ECONOMICS:USNFP , every CPI ECONOMICS:USCPI release, and every Powell presser between now and December.

If job creation continues to cool, the Fed will likely follow through with the cuts. If inflation heats up, those cuts may get scaled back. And if both trends stall, expect chop – the dreaded sideways trade that tests everyone’s patience.

What can you do in this situation? One message is to stay nimble. The dollar’s longer-term weakness is reshuffling the forex space, gold is on the cusp of a breakout, and stocks remain in record territory. And crypto is doing its usual unpredictable mood swinging.

In a nutshell, Powell gave markets a gift in the form of liquidity, but as history reminds us, the Fed giveth and the Fed taketh away.

👉 Off to you : What’s your strategy in this market? Now that you have the cut (and two more likely on the way), are you bullish or bearish? Share your thoughts in the comments!

$USINTR - Fed Cuts Rates as Expected (September/2025)ECONOMICS:USINTR

September/2025

source: Federal Reserve

- The Federal Reserve cut the federal funds rate by 25bps, bringing it to the 4.00%–4.25% range, in line with expectations.

It is the first reduction in borrowing costs since December. Policymakers noted that recent indicators suggest that growth of economic activity moderated in the first half of the year.

Job gains have slowed, and the unemployment rate has edged up but remains low.

Inflation has moved up and remains somewhat elevated.

Recessions usually follow interest rate cutsFrom a historical perspective, it looks like recessions follow periods after the feds rate is cut.

Periods of technical recessions, where the technical definition is two negative GDP quarters):

Jan 1974 – Jun 1974 (Q1 & Q2 ’74)

Jan 1975 – Jun 1975 (Q1 & Q2 ’75)

Jan 1980 – Jun 1980 (Q1 & Q2 ’80)

Jul 1981 – Dec 1981 (Q3 & Q4 ’81)

Jul 1990 – Dec 1990 (Q3 & Q4 ’90)

Jan 2001 – Jun 2001 (Q1 & Q2 ’01)

Jul 2008 – Dec 2008 (Q3 & Q4 ’08)

Jan 2020 – Jun 2020 (Q1 & Q2 ’20)

Also with the stock market at ATHs it will be very interesting to see what occurs post rate cuts that are forecasted for the remainder of 2025, assets would like be super charged for a bullish tear.

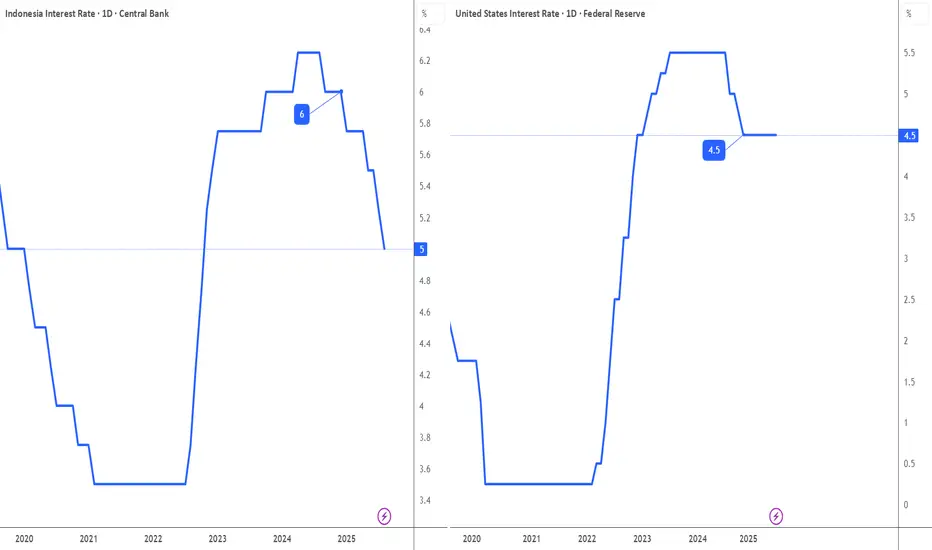

What To Watch This WeekThe Federal Reserve (US) and Bank of Indonesia will announce their policy rate.

While Bank of Indonesia is expected to maintain rate at 5%, most Investors expect The Fed will (finally) cut rate to 4.25% from current 4.5% (since Dec'24).

This week might starts a 1-2 years Bullish Cycle for all assets.

If Powell will cut rate, before he steps out.

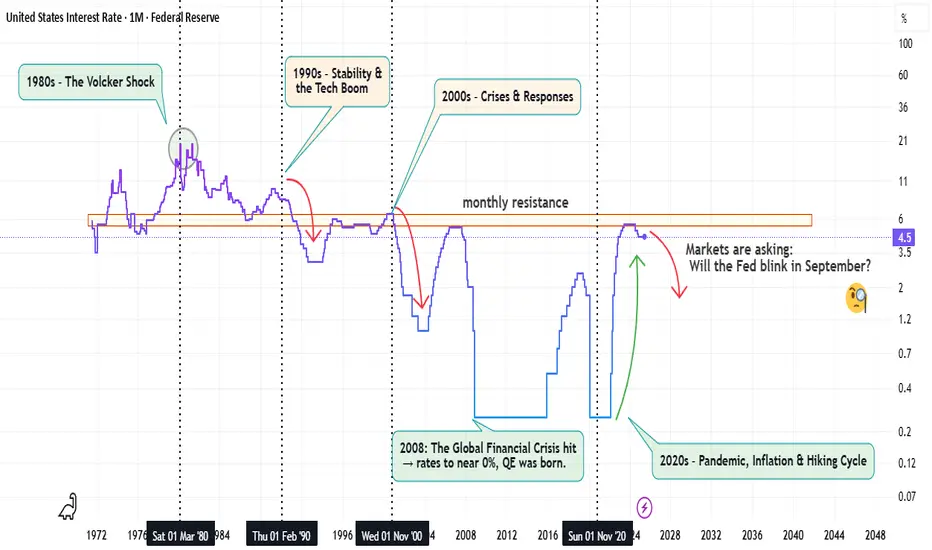

Interest Rates: The Hidden Driver of Markets📈 U.S. Interest Rates: From the Volcker Era to Today & Why September Could Be a Turning Point

When people talk about “the Fed,” they often forget just how much its decisions shape every asset class — from stocks and bonds to real estate and crypto. To understand the setup for September 2025, we need to look back. Because history doesn’t repeat… but it sure does rhyme.

🔙 The Journey Since the 1980s

1980s – The Volcker Shock

Paul Volcker took interest rates above 20% to crush runaway inflation. Painful? Yes. But it restored credibility and anchored inflation expectations for decades.

1990s – Stability & the Tech Boom

Rates gradually declined. Cheap(er) credit fueled the U.S. expansion and helped ignite the dot-com bubble.

2000s – Crises & Responses

Early 2000s: Post-dot-com crash, the Fed cut rates sharply.

2008: The Global Financial Crisis hit → rates to near 0%, QE was born.

2010s – The Low-Rate Era

This was the decade of “easy money.” Stocks soared, housing recovered, and crypto emerged in a world shaped by monetary stimulus.

2020s – Pandemic, Inflation & Hiking Cycle

2020: Zero rates + record stimulus.

2022 onward: Inflation surged → the Fed started its most aggressive hiking cycle since the Volcker era.

📊 Where We Stand in 2025

Current rates: at multi-decade highs.

Inflation: cooled off, but still above the Fed’s 2% target.

Growth: showing cracks (manufacturing weakness, slowing jobs data).

Markets are asking: Will the Fed blink in September?

🌍 Why September Matters

Pause Scenario: The Fed holds steady. Markets breathe, risk assets stabilize.

Cut Scenario: If growth data worsens, even a small cut could spark rallies across risk-on assets.

Hike Scenario (unlikely): Would shock markets and hit crypto hardest.

💡 Impact by Asset Class

Stocks: Lower rates = higher valuations. Tech especially sensitive.

Bonds: A cut means yields fall, prices rise.

Dollar: A pause/cut could weaken the dollar → bullish for commodities & crypto.

Crypto: The big winner if liquidity returns. Historically, Bitcoin thrives when real rates fall. Altcoins even more so.

⚡ My Personal View

I don’t see the Fed risking a fresh hike here. Inflation’s not dead, but neither is growth. My base case:

September pause with dovish signals.

First rate cut possible late 2025 if data keeps softening.

For crypto, that means:

Neutral short-term.

Bullish medium-term if liquidity trickles back into the system.

🚀 Every market cycle is shaped by rates. From the Volcker shock to the birth of Bitcoin, the Fed has always been in the driver’s seat. September might not be “the” moment, but it could be the beginning of a major narrative shift.

❓What’s your call — pause, cut, or surprise hike? And how do you see crypto reacting? Drop your thoughts

Central Banks, the Great Paradox of 2025This year 2025 reveals a paradox in the floating exchange market (Forex), a paradox I can describe as rare. The foundation of currency movements in the foreign exchange market lies in the divergence of monetary policies. In other words, it is the difference in the trajectory of interest rates among the world’s main central banks that usually drives the long-term trend of major USD pairs on Forex.

But this year 2025 shows a rare configuration: the divergence of monetary policies has had almost no effect on FX.

Why? Because the US dollar is (by far) the weakest currency in FX in 2025, even though the Fed has not touched its interest rate and this rate remains the highest among the major central banks, as shown in the main chart of this analysis.

1) In 2025, the divergence of monetary policies has not influenced FX

The table below compares the evolution of the interest rates of the major central banks as well as their inflation status. Except for the Bank of Japan, all major central banks have cut their interest rates several times this year as inflation targets were reached or approached.

The Fed alone has not touched the federal funds rate, and its rate is now the highest among all central banks.

The table below was prepared by analyst Vincent Ganne for Swissquote and offers a comparison of the monetary policies of major central banks in 2025.

The infographic below, sourced from Bloomberg, compares the evolution of central bank interest rates worldwide in 2025.

2) Here is the paradox: the US dollar is the weakest FX currency this year (down 10%) despite the favorable US rates

Not only is the US dollar the only major FX currency that has fallen in 2025, but this decline is significant — a 10% drop.

This fall of the US dollar is in total contradiction with the divergence of monetary policies, which should have led to a stronger dollar against a basket of major currencies. The question now is what trend the US dollar will take if the Fed eventually decides to cut its rate at the end of the year.

3) Ultimately, the role of monetary policy divergence is temporarily suspended as the US economy faces structural uncertainties

• Tariffs and their impact on US economic growth prospects

• Rising US public debt and the fiscal/budgetary policy of the Trump Administration (“Big Beautiful Bill”)

These two structural challenges have neutralized the divergence of monetary policies for this year, but it should regain its influence in 2026, potentially allowing a rebound of the US dollar on FX.

DISCLAIMER:

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only. The presented idea (including market commentary, market data and observations) is not a work product of any research department of Swissquote or its affiliates. This material is intended to highlight market action and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is advisable to seek professional advice from licensed advisor before making any financial decisions.

This content is not intended to manipulate the market or encourage any specific financial behavior.

Swissquote makes no representation or warranty as to the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The views expressed are those of the consultant and are provided for educational purposes only. Any information provided relating to a product or market should not be construed as recommending an investment strategy or transaction. Past performance is not a guarantee of future results.

Swissquote and its employees and representatives shall in no event be held liable for any damages or losses arising directly or indirectly from decisions made on the basis of this content.

The use of any third-party brands or trademarks is for information only and does not imply endorsement by Swissquote, or that the trademark owner has authorised Swissquote to promote its products or services.

Swissquote is the marketing brand for the activities of Swissquote Bank Ltd (Switzerland) regulated by FINMA, Swissquote Capital Markets Limited regulated by CySEC (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the CSSF, Swissquote Ltd (UK) regulated by the FCA, Swissquote Financial Services (Malta) Ltd regulated by the Malta Financial Services Authority, Swissquote MEA Ltd. (UAE) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) licensed by the Hong Kong Securities and Futures Commission (SFC) and Swissquote South Africa (Pty) Ltd supervised by the FSCA.

Products and services of Swissquote are only intended for those permitted to receive them under local law.

All investments carry a degree of risk. The risk of loss in trading or holding financial instruments can be substantial. The value of financial instruments, including but not limited to stocks, bonds, cryptocurrencies, and other assets, can fluctuate both upwards and downwards. There is a significant risk of financial loss when buying, selling, holding, staking, or investing in these instruments. SQBE makes no recommendations regarding any specific investment, transaction, or the use of any particular investment strategy.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The vast majority of retail client accounts suffer capital losses when trading in CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital Assets are unregulated in most countries and consumer protection rules may not apply. As highly volatile speculative investments, Digital Assets are not suitable for investors without a high-risk tolerance. Make sure you understand each Digital Asset before you trade.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainties.

The use of Internet-based systems can involve high risks, including, but not limited to, fraud, cyber-attacks, network and communication failures, as well as identity theft and phishing attacks related to crypto-assets.

Fed rate cut timing: September or October? The Jackson Hole Symposium has set the stage for renewed downside pressure on the U.S. dollar, as investors increasingly position for a 25-basis point Fed rate cut in September.

However, Morgan Stanley assigns only a 50% probability to such a move, suggesting that a September cut is far from guaranteed.

Market focus is also turning to the prospects of a rate cut in October too. The market is assigning only a small chance of two cuts in a row by the Fed.

Perhaps Morgan Stanely’s outlook implies the Fed may delay the widely expected September cut until October instead.

In practice, the market impact could be similar either way. With a softer dollar and stronger equities if Powell signals in September that easing is on the way the following month.

Markets Eye Policy, Positioning, and PerformanceCME_MINI:NQ1! CME_MINI:ES1! CME_MINI:MNQ1! COMEX:GC1! FRED:FEDFUNDS

Happy 4th of August, Traders!

As we head into the new week, here’s a look at what’s on the calendar:

Key Economic Data Releases

Monday:

• Factory Orders (MoM) – June

• Supply: 3-Month Bill Auction, 6-Month Bill Auction

Tuesday:

• Trade Balance (June), Exports (June), Imports (June)

• S&P Services PMI (July), ISM Non-Manufacturing PMI (July)

• Atlanta Fed GDPNow (Q3) – Prelim

• Supply: 52-Week Bill Auction, 3-Year Note Auction

Wednesday:

• German Factory Orders (MoM) – June

• Crude Oil Inventories

• FOMC Member Daly speaks at 11:45 CT

• Fed Governor Cook speaks at 1:00 CT

• Supply: 17-Week Bill Auction, 10-Year Note Auction

Thursday:

• Bank of England Interest Rate Decision

• BoE MPC Meeting Minutes, Inflation Letter, MPC Vote

• BoE Governor Bailey speaks at 8:15 CT

• FOMC Member Bostic at 9:00 CT

• Supply: 30-Year Bond Auction

Crude Oil Update

OPEC+ V8 members have announced an additional 547K bpd unwinding of voluntary cuts. Notably, crude prices have not reacted significantly to the expected OPEC+ figures. As we’ve previously highlighted, the market's focus remains firmly on demand-side factors. Despite geopolitical shocks, trade tensions, and recession concerns, crude oil prices have remained relatively stable—trading within a consistent range for over two and a half years since August 2022. According to Amena Bakr at Kpler, the V8 will meet again on September 7th to potentially reassess the reinstatement of 1.65 million bpd of cuts, currently scheduled to remain in place until the end of 2026.

Earnings Recap

With over half of S&P 500 companies having reported Q2 earnings, YoY earnings growth is now projected at 9.8%, compared to the 5.8% estimate as of July 1, per LSEG data cited by Reuters. More than 80% of reporting companies have surpassed analyst profit expectations—well above the 76% average from the past four quarters.

Macro Outlook

Fed Vice Chair Williams provided further insight into the central bank’s posture ahead of the September FOMC meeting, stating he remains open-minded but continues to believe that modestly restrictive policy is warranted. Williams also emphasized that the notable downward revisions to May and June payrolls were the key takeaway from Friday’s jobs report, reinforcing the theme of softening labor market momentum.

In addition, the Fed announced on Friday that Governor Lisa Cook will resign from the Board effective August 8. A replacement is expected to be named in the coming days, though it is not anticipated to materially alter the policy outlook in the near term.

Looking ahead, if both inflation and unemployment tick higher between now and the September FOMC meeting, it would represent a worst-case scenario for the Fed. The August NFP report due on the first Friday of September and July and August 2025 inflation reports are key data points to monitor before the next FOMC Meeting on September 17th, 2025.

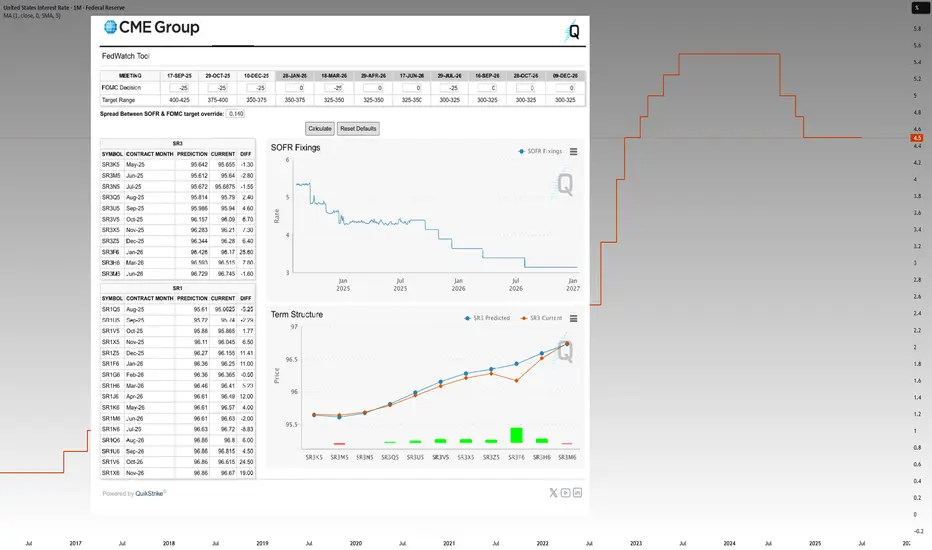

Although equity futures sold off on Friday following a disappointing jobs report, market pricing has adjusted notably. Participants now expect the Fed to deliver three rate cuts in 2025 and two cuts of 25bps each in 2026. This marks a shift from pre-NFP expectations of two cuts in 2025 and three cuts in 2026, per CME FedWatch Tool.

Market Implications:

On the back of rate cut expectations, in our analysis, this may help sustain upside in the equities complex. Although, it may be prudent to adjust portfolio and re-balance strategically according to sectors that may continue to outperform namely tech, AI, defense stocks, commodities and USD per our analysis.

$USINTR -Feds Leaves Rates Steady (July/2025)ECONOMICS:USINTR

July/2025

source: Federal Reserve

- The Federal Reserve held rates steady at 4.25%–4.50% for a fifth straight meeting, defying President Trump’s demands for cuts even after positive GDP growth .

Still, two governors dissented in favor of a cut—the first such dual dissent since 1993.

Policymakers observed that, fluctuations in net exports continue to influence the data, and recent indicators point to a moderation in economic activity during the first half of the year.

The unemployment rate remains low, while Inflation somewhat elevated.

Latest on Fed rate cut debateThe Fed isn’t expected to cut rates this week, but this FOMC meeting should still be very interesting.

Powell will need to address growing pressure from board members Waller and Bowman, who’ve both called for cuts, citing limited inflation impact from tariffs.

Still, Powell is just one of 12 votes on the FOMC, and there’s little sign of broader support for a cut.

With the labour market steady and early signs of tariff-driven inflation, the Fed has reason to hold. The rate decision is due Wednesday at 2 p.m. ET, followed by Powell’s press conference at 2:30 p.m. ET.

This decision will further widen the rift between the Fed and President Trump, whose frustration has grown in recent weeks, with renewed attacks on Powell’s leadership.

The tension has drawn international attention. On Monday, the IMF issued a warning about political interference in central banks, which can pose a threat to global financial stability.

$USINTR -Fed Keeps Rates Uncut (June/2025)ECONOMICS:USINTR

June/2025

source: Federal Reserve

- The Federal Reserve left the federal funds rate unchanged at 4.25%–4.50% for a fourth consecutive meeting in June 2025, in line with expectations, as policymakers take a cautious stance to fully evaluate the economic impact of President Trump’s policies, particularly those related to tariffs, immigration, and taxation. However, officials are still pricing in two rate cuts this year.

Mr. LATE drop the RATE!!"Jerome Powell aspires to be remembered as a heroic Federal Reserve chair, akin to Tall Paul #VOLKER.

However, Volker was largely unpopular during much of his tenure.

The primary function of the Federal Reserve is to finance the federal #government and ensure liquidity in US capital markets.

Controlling price inflation should not rely on costly credit.

Instead, it should be achieved by stimulating growth and productivity through innovation and by rewarding companies that wisely allocate capital, ultimately leading to robust cash flows... innovation thrives on affordable capital.

While innovation can lead to misallocations and speculative errors, this is a normal aspect of the process.

(BUT it is crucial that deposits and savings are always insured and kept separate from investment capital.)

By maintaining higher interest rates for longer than necessary, J POW is negatively impacting innovators, capital allocators, small businesses that need cheap capital to function effectively, job creators, and the overall growth environment.

Addressing price inflation is a far more favorable situation than allowing unemployment to soar to intolerable levels.

"Losing my job feels like a depression".

But if I have to pay more for eggs, I can always opt for oats.

Rate Cuts and Risky Bets: When the Fed Rolls Out the Red Carpet🎬 The Fed’s June Meeting Is Around the Corner

Mark your calendars: June 17–18 is when the Federal Reserve's Federal Open Market Committee (FOMC) convenes next. With the benchmark interest rate ECONOMICS:USINTR currently holding steady at 4.25% – 4.50%, investors and policymakers alike are keenly awaiting any signals of a shift in monetary policy.

Market expectations suggest a cautious approach, with futures markets indicating a modest probability of rate cuts in the latter half of the year. That said, the upcoming meeting could offer some juicy insights into the Fed's outlook — yes, in this economy.

🤝 Trump vs. Powell: The Sequel No One Asked For

President Donald Trump and Fed Chair Jerome Powell recently had their first face-to-face meeting during Trump’s second term, rekindling a familiar tension. Trump criticized Powell for maintaining high interest rates, saying it puts the US at an economic disadvantage compared to countries like China.

Not too surprising, Trump’s tone, that is. As a matter of fact, it’s way softer than when the President called the Fed chair a “major loser.”

Anyway, Powell was holding back at the meeting, saying that the Fed is independent and that monetary policy decisions are based on objective economic data, not political pressure.

Despite Trump's public and private criticisms, Powell remains steadfast in his approach, focusing on long-term economic stability over short-term political considerations.

📉 Inflation, Employment, and the Tightrope Walk

Inflation has decreased significantly from its peak of 9.1% in 2022 to 2.3% in April 2025 , nearing the Fed's 2% target. However, the labor market remains robust, with unemployment rates at historically low levels.

The Fed faces a delicate balancing act: cutting rates too soon could reignite inflation, while maintaining high rates might dampen economic growth. This tightrope walk requires careful analysis of incoming data and a measured approach to policy adjustments.

🛍️ Market Reactions: Bulls, Bytes, and Bullion

If rate cuts are the rumor, the S&P 500 SP:SPX is already buying the headline. The index clawed back all of its early-year slump and now sits just above the flatline. Traders are clearly pricing in a friendlier Fed, even if Jerome Powell hasn’t sent out the official RSVP yet.

Gold OANDA:XAUUSD , meanwhile, has been doing what it does best — quietly flexing in the corner as uncertainty swirls. Prices bounced back above $3,300 in late May, reminding everyone that when central banks blink, bullion blings. A rate cut could weaken the dollar — and gold’s inverse relationship with the greenback suddenly looks like a playbook move.

Speaking of the dollar, the dollar index TVC:DXY has been wobbling like it’s just finding its feet. With inflation softening and tariff noise all over the place, the buck has lost some swagger . Traders are already rotating out of safe havens and into riskier plays, including…

Yep, Bitcoin ( BTCUSD ).

Crypto’s original bad boy is back on the move, orbiting near $110,000 after rewriting its all-time high book in May.

A dovish Fed can technically pour more rocket fuel into the rally, especially as sovereign adoption and ETF flows keep pumping ( $9 billion in just five weeks?! ). In the land of easy money, Bitcoin doesn’t just survive — it thrives.

The takeaway? Markets love a dovish pivot. Whether you're holding stocks, stacking sats, or eyeing gold bars, the Fed’s next move could be the difference between breakout and breakdown.

🧠 What to Keep in Mind

As the June Fed meeting approaches, traders should consider the following strategies:

Diversification: Maintain a diversified portfolio to mitigate risks associated with interest rate volatility.

Equity Exposure: Evaluate exposure to sectors sensitive to interest rates, such as the good old tech space and throw in some financials — banks love rate moves.

Inflation Hedges: Consider assets like gold or silver to hedge against unexpected inflationary pressures.

🧾 Conclusion: Navigating Uncertainty

The June Fed meeting isn’t just another calendar event — it’s a market-defining moment dressed in central bank jargon. With politics heating up and inflation cooling down, Powell’s next move could either pump more cash into the risk rally or throw cold water on the party.

Yes, the noise is loud. Yes, the data is messy. But through it all, one thing holds: staying nimble beats being early. Whether you're riding the S&P 500, hodl’ing Bitcoin, or hugging gold like a doomsday prepper, this is the time to trade the chart, not the chatter.

Off to you : Are you in the rate-cut camp or you think there’s more ground to cover before Powell and his squad tune the pitch down? Comment below!

$USINTR -Fed Keeps Rates Unchanged (May/2025)ECONOMICS:USINTR

May/2025

source: Federal Reserve

- The Federal Reserve kept the funds rate at 4.25%–4.50% range for a third consecutive meeting as officials adopt a wait-and-see approach amid concerns about the effects of President Trump’s tariffs.

Policymakers noted that uncertainty about the economic outlook has increased further and that the risks of higher unemployment and higher inflation have risen.

4/8/25 - one more i keep staring at. i'll keep it short!One more from me tonight, friends,

I keep staring at this chart which plots (the scatter-like print) ST rates vs. S&P earnings yield and also shows the S&P adjusted by M2 (purple).

I believe one or the other is likely true.

1/ we're in the middle of a mega bull run that began in '09 and never really ended, given low rates, tons of tech-led innovation (with cash flows) and the current correction is a pause (similar to the GREEN ARROW in '98) before continuing much higher and with rates remaining high and potentially even headed incrementally higher as stocks climb the wall of worry.

2/ we're undergoing a WTF growth scare, a geopol reordering, inability to look through for many months (or even a year) and causing such a financial meltdown that rates will be forced to head back to zero and stocks maybe undergo another 20-30% lower (the FROWNY FACES).

My guess is it's #1.

- the current spat is Trump-induced.

- it's not a meltdown of credit markets (well... yet...)

- there's not a fake _____ (event of any sort) causing freak out

- and also... unlike dotcom, which ran HARD, we've had some pullbacks along the way in this recent multi-year run, testing the thesis... notably mar '20 and end '22. these tech leaders are v cash generative and there's a good reason to believe they'll continue to gain strength

all this would translate into a massive run into '28, if #1 is correct.

so now that we're in pure correlation 1, margin call territory etc. etc. we have the "can't look through, need help or some resolution event"

so once that resolution comes. we probably boot, rally, retest. and rip.

hard to do this on leverage b/c V might not be the shape of recovery (at least that's not how i'd play it, i still prefer to use deep ITM LEAPS for some flex)

but let's see.

this chart has my attention once again.

V

Recession indicatorUS Federal Fund's Rate - US 2-Year T-Bond Yield

Only two times since 1989 this indicator has hound a ceiling at 2. We've been living the third time for some months now.

However, no indications of an incoming recession whatsoever (?)

$USINTR - U.S Interest Rates (March/2025)ECONOMICS:USINTR

March/2025

source: Federal Reserve

- The Fed keep the funds rate unchanged at 4.25%-4.5%,

but signaled expectations of slower economic growth and rising inflation.

The statement also noted that uncertainty around the economic outlook has increased, but officials still anticipate only two quarter-point rate reductions in 2025.

Crypto market is just waiting for that.Hi.

I expect the federal reserve rate to finally start to decline as early as October.

Three targets for this possible reduction.

I expect the crypto market to react very well.

2/18/25 - general mkt observationsi'd rather be sippin' pina coladas on the balcony at this stage than continue at the beach party with clear skies darkening. think i've just been there, done that enough to not want to play the last minute FAFO game as much as one can possibly avoid it.

so when i look out over the next 12 months... yup... let me stop right there... i don't think we can do that and i get the sense that everyone is doing just this. do i think we'll end the year higher on the index vs. where we stand today? yes. but do i think we just keep chugging along in the clown car in the same fashion as last year. no.

there are a lot of things that changed in the last 3 months. take for instance, how volatile the tape has become (once again) on trump's shower or toilet tweets. less taco bell, more pepto pls. but the reality is, we're just trading the tape we're presented to. any emotional reaction you have to any of it is a disadvantage to your pnl and a benefit to the zero sum other guy *well* computer. DOGE matters. dollar dominance and signaling matters. rates matter. tariffs matter. china matters. all of a sudden, the soup might include a bat. nah. that's for a fairy tale.

take a look at this chart.

i've plotted ST rates vs. S&P earnings yield and flipped on some haikin ashi action for the candles to show trends as more obvious. while we could argue about infinite topics in the >12 month context for each of these... simply put... ST rates look... competitive. even in the fake video game we all play, we get to choose different doors, weapons, opinions to follow. opportunity cost matters.

and so when i see the rolling over of this trend PLUS dominance of market cap weighted S&P vs. equal weight S&P (SPXEW/SPY)... this also tells me there's an embedded premium in these "will survive better than the others" boats. Bitcoin dominance (BTC.d in trading view) shows you the same thing. Everyone has been chitcoinin' but realizes now the zero-sum game of 99% of these things and the conclusion is... "settle into USDT and BTC". ultimately, that purple line (back to the trad mkts) indicates we might be reaching a point where growth is unclear, the path is unclear... and therefore... any relevant catalyst (like a headline about China-Taiwan... EVEN IF IT WON'T HAPPEN) could throw these markets off 5-10% easily. maybe that's all we get. maybe there's something else. right now we don't have that catalyst.

it's getting a bit spooky out here. we will keep playing our earnings game. liking what we like

BTC

,

NXT

,

UBER

, tsm... incubating a few others like

EVVTY

,

BLDE

, mu. i can't HELP but to keep my cash balance awkwardly high.

i don't mind jumping back in the pool. but my swimsuit is dry. the pina colada is chilly. and the whispy air coming in off the rocky ocean sends a feel-good shiver up my spine.

something's off, but in a good way. opportunity is coming. be vigilant. risk manage. know what you own. know what you want to own if/when/for how much.

have a good week.

V