NFP report for Friday September 5 - DECISIVE!While the month of September on the stock market has seen the least favorable performance statistics, and the market is eagerly awaiting the Federal Reserve's (FED) monetary policy decision on Wednesday September 17, a decisive macro-economic figure is published this Friday September 5.

The US NFP report is updated during the trading session on Friday September 5, and is the last monthly report on US employment before the FED meeting on September 17.

1) No pivot, technical pivot, healthy real pivot, unhealthy real pivot: the choice the FED has to make on September 17 is a real headache

Tariffs have been in place since August 7 and have begun to affect US producer and consumer prices. US inflation will remain closer to the 3% than the 2% threshold for several months, and it will take some time for the situation to normalize, probably from the beginning of 2026.

The FED is therefore in an uncomfortable position, as it also has the task of ensuring full employment, and the situation of the US labor market has deteriorated in recent months. If the NFP report on the US labor market on Friday September 5 confirms this deterioration, the FED will have no choice but to make at least a “technical” pivot. A cut in the federal funds rate to adjust to the weak labor market and neutralize any out-of-control rise in the unemployment rate in good time.

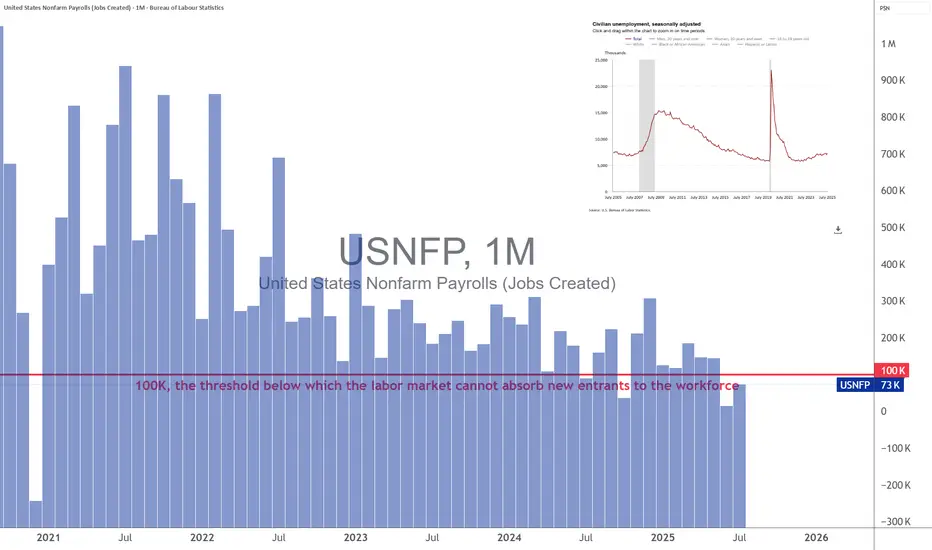

2) The US labor market has been on a worrying trajectory for the past 3 months, and the FED's warning thresholds are not far off

For three months running, the number of net new jobs created in the USA has been insufficient to absorb the new arrivals in the labor force. This minimum threshold is set at 100K net job creations per month, and the consensus figure for Friday September 5 is still below this threshold.

As for the number of unemployed in the US, it could hit a new 4-year high with the Friday September 5 NFP report.

3) The elements of the NFP report for Friday September 5 should therefore make it possible to set for good the likelihood of monetary action by the FED on September 17

This Friday, the market will therefore be looking at three figures from this Friday's NFP report:

- Unemployment rate

- The number of net new jobs created

- Wage growth, the link between inflation and the labour market.

Any upward tick in the unemployment rate to 4.3% of the working population, or any figure below 100K for net job creation, will make the scenario of a US federal funds rate cut on Wednesday September 17 all but certain.

DISCLAIMER:

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only. The presented idea (including market commentary, market data and observations) is not a work product of any research department of Swissquote or its affiliates. This material is intended to highlight market action and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is advisable to seek professional advice from licensed advisor before making any financial decisions.

This content is not intended to manipulate the market or encourage any specific financial behavior.

Swissquote makes no representation or warranty as to the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The views expressed are those of the consultant and are provided for educational purposes only. Any information provided relating to a product or market should not be construed as recommending an investment strategy or transaction. Past performance is not a guarantee of future results.

Swissquote and its employees and representatives shall in no event be held liable for any damages or losses arising directly or indirectly from decisions made on the basis of this content.

The use of any third-party brands or trademarks is for information only and does not imply endorsement by Swissquote, or that the trademark owner has authorised Swissquote to promote its products or services.

Swissquote is the marketing brand for the activities of Swissquote Bank Ltd (Switzerland) regulated by FINMA, Swissquote Capital Markets Limited regulated by CySEC (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the CSSF, Swissquote Ltd (UK) regulated by the FCA, Swissquote Financial Services (Malta) Ltd regulated by the Malta Financial Services Authority, Swissquote MEA Ltd. (UAE) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) licensed by the Hong Kong Securities and Futures Commission (SFC) and Swissquote South Africa (Pty) Ltd supervised by the FSCA.

Products and services of Swissquote are only intended for those permitted to receive them under local law.

All investments carry a degree of risk. The risk of loss in trading or holding financial instruments can be substantial. The value of financial instruments, including but not limited to stocks, bonds, cryptocurrencies, and other assets, can fluctuate both upwards and downwards. There is a significant risk of financial loss when buying, selling, holding, staking, or investing in these instruments. SQBE makes no recommendations regarding any specific investment, transaction, or the use of any particular investment strategy.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The vast majority of retail client accounts suffer capital losses when trading in CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital Assets are unregulated in most countries and consumer protection rules may not apply. As highly volatile speculative investments, Digital Assets are not suitable for investors without a high-risk tolerance. Make sure you understand each Digital Asset before you trade.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainties.

The use of Internet-based systems can involve high risks, including, but not limited to, fraud, cyber-attacks, network and communication failures, as well as identity theft and phishing attacks related to crypto-assets.

Trade ideas

Non farm payrollsIf the number of jobs created falls below that red line, I think odds of a recession increases.

Yes, stock markets are seen to tumble when that happens.

If they tumble enough, it could signal the start of bull eras for gold, silver and other commodities.

Macro Outlook: Trade War Jitters, Deficit, NFP FridayAlthough there is a headline fatigue and markets have been stabilizing with the worst of trade war story behind us, the fact is that uncertainty still looms. President Trump announced over the weekend that he will double down on US steel and aluminum tariffs from 25% to 50% effective June 4th.

Highlight this week is US Jobs data this Friday. A key point to determine the resilience of the US labor market. With FED Chair Powell speaking today and FED speakers scheduled throughout the week, it will be key to watch how they shape markets' probability of rate cuts?

As we previously explained, ongoing uncertainty and dragging trade concerns present more risks until resolved. Here are some key points to consider:

It remains to be seen whether the trade deficit will continue to worsen or begin to reverse. April trade data, along with any policy shifts such as a reversal on reciprocal tariffs, will be important to monitor. These indicators will provide insight into how businesses are interpreting ongoing trade uncertainty. The key question is whether they will continue front-loading inventory in anticipation of future disruptions, or if the focus will shift toward restructuring supply chains and reining in spending as part of a longer-term strategic adjustment.

At the same time, consumer spending remains resilient, supporting overall demand. However, pressure may be building on business balance sheets, particularly businesses with poor cash flow to manage front loading inventory spending as the trade environment remains volatile. If consumer spending begins to weaken, businesses may be forced to cut costs, scale back investment, or offer steep discounts to clear excess inventory. This could lead to a cycle of margin compression, especially if firms attempt to pass higher costs onto price-sensitive consumers, potentially suppressing demand further.

Conversely, if businesses choose to absorb rising costs to maintain competitive pricing, they face deteriorating margins but may be betting on continued strength in consumer credit, household savings buffers as evident. Consumer confidence, despite being low, is not an accurate indicator in times of uncertainty. Here, we should watch what consumers do and not the sentiment.

In this scenario, firms may delay cost-cutting in the hope that continued strength in consumer spending will support revenues through the rest of the year.

A central tension remains: businesses must navigate a delicate balance between protecting margins and preserving demand. Meanwhile, persistent trade uncertainty and tighter financial conditions may slow capital investment and hiring, further complicating the outlook. Whether firms shift from defensive postures like front-loading toward long-term structural changes in supply chains will hinge on how durable current consumer strength proves to be and how responsive trade policy becomes in the months ahead.

Ongoing front-loading has caused ripples as the trade deficit has further widened. Will this reverse as businesses focus on sales and revenue instead of front-loading inventory?

In our analysis, trade imports, trade balance, consumer spending and corporate profits will be key to monitor despite being lagging indicators.

On the other hand, equally important to watch and monitor goods exports, durable goods to assess and evaluate the other side of the equation.

However, our focus is on imports as manufacturing jobs are at their lowest in US history.

Once the dust has settled and trade deals are locked in, it will be important to note if Exports by Country experience any significant shifts.

What does all this mean for the stock market and futures? In simple terms, the yearly pivot and last month’s high is a major resistance area for index futures. Until this is cleared, we may see a range bound market and two way trade. There is a lot of weak structure to revisit lower. Markets may perhaps retest this before resuming higher. What we would want to see is, last month’s low holding support and this month’s price action trading inside previous month’s range or resuming higher.

If we revisit May Monthly Lows, we may see increased selling pressure come in.

Nonfarm payrolls (jobs created)We are inching closer to a recession and economic turmoil.

Stock markets ALWAYS drop when this happens.

US Unemployed to Employed as Indicator of Job Market HealthIn this chart, we use the following symbols: ECONOMICS:USNFP , FRED:UNEMPLOY

ECONOMICS:USNFP represents the number of jobs created in a month. FRED:UNEMPLOY represents the number of unemployed individuals for a month.

Assuming exactly 1 payroll per person , the ratio 100 * ECONOMICS:USNFP / ( FRED:UNEMPLOY + ECONOMICS:USNFP ) estimates the percentage of previously unemployed individuals who transitioned to employment in the month. If enough jobs are created, the current FRED:UNEMPLOY should equal the previous month's FRED:UNEMPLOY minus ECONOMICS:USNFP , as the jobs created should correspond to the unemployed who found work.

When sufficient jobs are created, the number of unemployed decreases, and the ratio increases. A "healthy" value for this ratio is around 2.5% , indicating that approximately 2.5% of unemployed individuals transition to employment each month .

Conversely, if insufficient jobs are created, the number of unemployed rises, and the ratio decreases. Ratios around 0% or negative values are usually observed during or before recessions, indicating an unhealthy job market .

For last two consecutive months, the ratio has been 0.17% , suggesting an unhealthy job market . Similar patterns were observed before the DotCom and GFC recessions. If this trend continues for several months, it strongly suggests that the US is either on the verge of or already in a recession.

Historically, when the 30-week SMA crosses below the 50-week SMA, it signals a recession. This signal was triggered in June '24.

$USNFP -U.S Non-Farm Payrolls (MoM)$YSNFP (AUGUST/2024)

US Economy Adds Fewer Jobs Than Expected

source: U.S. Bureau of Labor Statistics

- The US economy created 142K jobs in August, more than downwardly revised 89K in July but below market expectations of 160K.

Most job gains occurred in construction and health care while manufacturing employment declined.

Meanwhile, the jobless rate edged lower to 4.2% from 4.3% in July.

U.S. Non Farm Payrolls U.S. Non Farm Payrolls

Rep: 353k ✅ MUCH HIGHER than Expected ✅

Exp: 187k

Prev: 333k

U.S. economy adds 353,000 jobs in January

Based on revised figures we have increased the jobs added to the U.S from 150k in Nov 2023 gradually increasing to 353k for the month of Jan 2024.

Build Back BetterBuild Back Better is a disaster for the economy. Banks are failing and Inflation is killing middle class America. The wealthy are above inflation rates in a top down economy where they receive their money before the full effect of inflation kicks in at the lower levels. "Trickle Down Economics".

Non Farm Payrolls are down again marking a decisive trend. Fewer jobs being created in the workforce along with flooding Illegal migrants along the border and you have a catastrophe that is just waiting to happen. A third world country in the making.

Is the US Economy Actually adding more jobs than expected?If you have been living under a rock for the past few days, unless you are not an economic savvy, the Bureau of Labor Statistics has released its newest Non-Farm Payrolls much above the expectation. The NFP rose by 263,000 last month, compared with an expected 200,000.

At first, my reaction was that the FED will have to keep raising interest rates, especially as the US dollar reacted to this news by jumping 0.8%. However, I was skeptical as to how NFP jobs increased but the unemployment rate remained steady at 3.7% in an economy that is starting to experience drawdowns from inflation. So I made a research to analyze exactly what is going on.

1. What is happening in the US labor market?

Today the NFP is at ~270,000 jobs, similar to mid-2018 when the labor market was defined as strong. It is much lower than the peak job creation in 2021 but 70,000 extra jobs compared to the expectation is a major difference.

2. What is happening with wage growth in the US labor market?

Wage growth has increased by 0.6% month-over-month. This is way too strong for the FED's target of 2% in inflation. But why is it so high? Well, one of the reasons is that the supply of labor is not coming back. The participation rate remains way below pre-pandemic levels, even when accounting for an aging population. So if labor participation is low, job creation must be low to slow inflation, yet, the labor market appears to be healthy.

Nonetheless, I wrote an analysis in October challenging the FED's data collection on job creation.

"Once consumers have reached their credit limit, they will most likely look for another job. “About 38% of American workers have looked for a second job, while an additional 14% plan to” (LA Time, 2022). This justifies the reasons for more job creation in the U.S. economy as emphasized by the Biden Administration and the Fed, however, it is mostly people looking for a second or third job."

Credit debt is increasing at an all-time high due to inflation. "U.S. households are spending $445 more every month due to inflation" (Lacurci G, 2022). So those who cannot keep up with their bills have to work more jobs or extra time.

This makes total sense, especially when the Household Job Survey shows no jobs added in the past 8 months, while the Establishment Survey shows 2.7 million jobs added, which is the one used by the FED.

Why such a large difference between the Household Job Survey and Establishment Survey?

The answer lies in how the different surveys are run.

For instance, the household survey counts people holding multiple jobs as one employed person. While the establishment survey counts all the jobs created, even if it is a second or third job. Based on the analysis I previously published, at least 700,000 Americans have had a second or third job in the last 12 months to make ends meet.

3. Where are jobs being created and lost?

Being created: leisure, government, education, and healthcare.

Being lost: goods, transportation, retail, construction, and utilities.

Conclusion:

The NFP survey is informing the market about Powell's next decision in December. The strong nominal wage growth and "strong" job creation argue there could be further rate hikes and hawkish talk from grandfather Powell. It is imminent before we will start to see weaknesses in the labor market. It is imperative to understand when will the turnover point of the labor market be and how bad to best position yourself, hence, we can start to see a FED pivot in early 2023 as the labor market weakens.

This is for personal recording but feel free to comment and argue.

NFP 261K is mid!

2016-2017 NFP Average = 168k (Trump Era)

2017-2018 NFP Average = 198k

2018-2019 NFP Average = 164k

2019-2020 NFP Average = -796k (COVID-19)

2020-2021 NFP Average = 474k (Biden Era)

2021-2022 NFP Average = 410k

There was a time when 261k would have been outstanding, but following on from the big job reset in 2019/2020 the average was above 400k.

non farm payroll recession trackerAll official recessions had negative NFP prints the US economy in 2022 is still far from seeing that