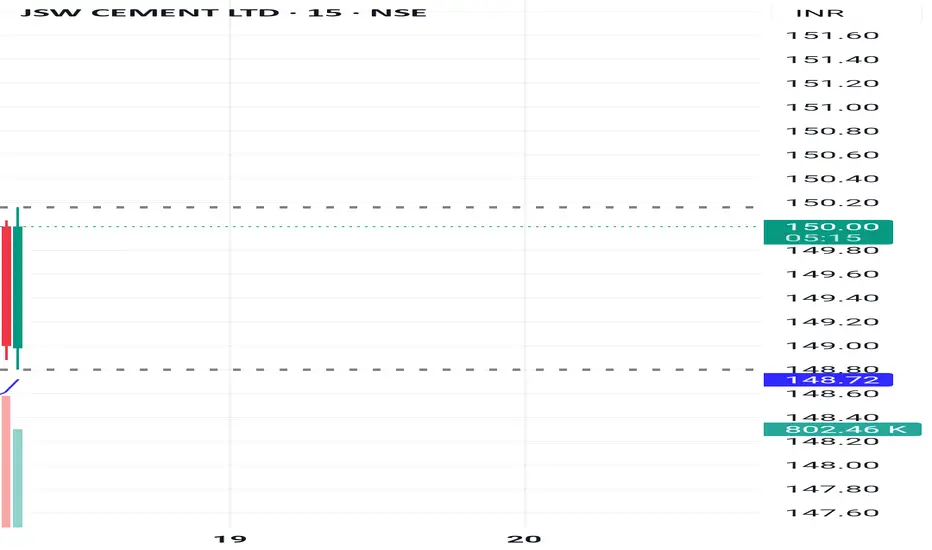

JSWCEMENT – Watching Breakout LevelsPrice is approaching a key resistance zone around ₹160.

A clear breakout above ₹160 with strong volume can indicate bullish momentum.

Traders generally watch for follow-through candles and retests after a breakout.

Support remains near the ₹142 zone.

Observing volume confirmation is crucial to differentiate between true breakout and false breakout.

⚠️ Disclaimer: This is for educational purposes only. I am not SEBI registered. Please do your own analysis before making trading or investing decisions.

Trade ideas

JSW CEMENTJSW Cement Ltd. (currently trading at ₹151) is a fast-growing player in India’s cement industry, with a strong focus on sustainability and industrial integration. Backed by the JSW Group, the company operates 8 state-of-the-art manufacturing units with a total grinding capacity of 20.6 MTPA across India and the UAE. It is the country’s leading producer of Ground Granulated Blast Furnace Slag (GGBS), contributing significantly to green construction and infrastructure.

JSW Cement Ltd. – FY22–FY25 Snapshot

Sales – ₹4,820 Cr → ₹5,720 Cr → ₹6,820 Cr → ₹8,120 Cr Growth driven by GGBS volumes, regional expansion, and infra demand

Net Profit – ₹-55 Cr → ₹120 Cr → ₹300 Cr → ₹420 Cr Profitability turnaround supported by margin mix and scale

Operating Performance – Weak → Moderate → Strong → Strong EBITDA margins improving with GGBS-led contribution

Dividend Yield (%) – 0.00% → 0.00% → 0.00% → 0.00% No payouts; reinvestment-focused strategy

Equity Capital – ₹1,363 Cr (post IPO) Stable structure post listing; no dilution expected

Total Debt – ₹4,070 Cr → ₹4,800 Cr → ₹5,300 Cr → ₹5,750 Cr Elevated leverage due to aggressive capex cycle

Fixed Assets – ₹6,850 Cr → ₹7,420 Cr → ₹8,100 Cr → ₹9,200 Cr Capex focused on Rajasthan integrated unit, Punjab grinding, and Shiva Cement expansion

Institutional Interest & Ownership Trends

Promoter holding stands at 85.00% via JSW Group, with gradual dilution expected. FIIs and DIIs have initiated coverage post IPO, with neutral-to-positive outlooks. Delivery volumes reflect cautious accumulation by infra and ESG-focused funds.

Business Growth Verdict

JSW Cement is scaling rapidly across green cement and GGBS segments Margins improving due to product mix and regional diversification Debt remains elevated but aligned with capex intensity Capex supports long-term competitiveness and pan-India footprint

Management Con Call

Management emphasized strategic entry into North India via Rajasthan plant, with incentives offsetting limestone costs GGBS continues to be a key profit driver, contributing 60–75% of EBITDA despite forming ~34% of revenue2 Capex of ₹5,600 Cr planned for FY26–FY28, with focus on integrated units and grinding capacity FY26 outlook includes 19% revenue CAGR and 31% EBITDA CAGR, with PAT expected to reach ₹300 Cr from FY25 loss1

Final Investment Verdict

JSW Cement Ltd. offers a high-growth industrial story built on sustainability, integration, and regional expansion. Its leadership in GGBS, aggressive capex, and strategic entry into high-margin geographies make it suitable for accumulation by investors seeking exposure to green infrastructure and scalable cement platforms.

JSW Cement: Company Profile & Sector Analysis

🙀🧐Conclusion 🧐🙀

🤔While JSW Cement demonstrates ambition and operational scale in India’s vibrant cement sector, its financial health is tempered by high leverage and modest returns. Strong governance, strategic debt management, and transparent reporting will be critical as the company seeks market leadership among robust peers. Long-term investors should closely monitor improvements in cash flows and efficiency, given sector opportunities and competitive dynamics.

🧐The cement sector shows strong growth led by robust leaders; JSW Cement is a promising but highly leveraged mid-cap facing profitability and liquidity challenges. Sector fundamentals remain resilient, but JSW’s turnaround depends on prudent financial and governance reforms

🌺🌺About JSW Cement🌺🌺

JSW Cement is a prominent Indian cement manufacturer, recently listed on BSE and NSE in August 2025. The company aims to rapidly expand its production capacity and footprint across key markets with a focus on sustainable manufacturing and innovative processes.

🤯Cement Sector Growth & Future Potential🤯

- India’s cement demand driven by government infrastructure push and urbanization.

- Sector CAGR expected at 7-9% over the next five years with rapid capacity additions.

- Companies investing in green cement, alternative fuels, and digital operations.

- Consolidation and entry of large players signal a highly competitive future market landscape.

🧐Financials Snapshot (FY25)🧐

- Revenue: ₹6,028 crore

- Operating Margin: 15.3%

- EBITDA Margin: 16%

- Net Margin: 1%

- Market Cap: ₹7,400 crore

- Free Cash Flow: Negative

😶🌫️Key Ratios😶🌫️

- Debt/Equity Ratio: 2.6 (sector high)

- Return on Equity (ROE): 0.6% (below industry average)

- Return on Capital Employed (ROCE): 8%

- Current Ratio: 0.65

- Dividend Payout: 0%

👷🏻 Peer Analysis👷🏻

- UltraTech Cement, Shree Cement, and Ambuja Cement lead with stronger margins and lower debt.

- JSW Cement’s leverage (high debt) impacts profitability and shareholder returns.

- Sector leaders maintain ROE and ROCE above 10-13%; JSW lags in these metrics.

- Free cash flow in JSW Cement lags behind top peers due to high investment and operational pressures.

- Margins are competitive but net profitability is limited compared to industry best.

- JSW Cement is positioned as a mid-cap, growth-oriented player with room for efficiency improvement.

- Company’s focus on expansion adds long-term growth potential.

- Peer companies show higher liquidity and sustainable dividend payout records.