Eli Lilly (LLY) Shares Have Surged by Around 30% in NovemberEli Lilly (LLY) Shares Have Surged by Around 30% in November

The price action of Eli Lilly and Company (LLY), the world’s largest pharmaceutical firm, reflects exceptionally strong demand:

→ since the start of the month, LLY shares have risen by roughly 30%;

→ in late November, the company’s market capitalisation exceeded $1 trillion, making Eli Lilly the first pharmaceutical firm in history to reach this level.

Why are Eli Lilly (LLY) Shares Rising?

A key driver has been the strong earnings report published on 30 October.

→ Earnings per share came in far above expectations ($7.02 versus $5.69).

→ Sales of diabetes treatment Mounjaro and obesity drug Zepbound surpassed $10 billion for the quarter.

→ On the back of this success, management raised its revenue outlook, and market participants now expect an even stronger fourth quarter.

At the same time, the chart is signalling that the extraordinary rally may be running out of steam.

Technical Analysis of Eli Lilly (LLY) Shares

For more than a year, LLY’s price action followed a downward channel. If this channel is extended upward twofold after the bullish breakout (which occurred following the earnings release), we can see that the price has reached the upper boundary of the expanded channel — a level often viewed as a potential target for buyers.

Note that after breaking above the psychological $1,000 level, the rally initially slowed (1), but then accelerated sharply this week (2) — a possible sign of FOMO and the climax of the November uptrend.

Additionally → the RSI indicator is deep in overbought territory and is pointing lower.

Given these factors, it is reasonable to assume that LLY shares are vulnerable to a pullback, which could intensify if investors begin taking profits on long positions.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Trade ideas

Eli Lilly Hits $1 Trillion Milestone on GLP-1 BoomEli Lilly & Co. (NYSE: NYSE:LLY ) briefly crossed the $1 trillion market-cap threshold, becoming the first health-care company in history to reach the valuation. Shares traded around $1,059 as demand for its GLP-1 weight-loss and diabetes drugs exploded, driving extraordinary revenue growth and solidifying its global leadership.

Historic Breakthrough for Health-Care

Eli Lilly’s rise into the trillion-dollar tier places it beside mega-caps typically dominated by technology firms. Its 36% year-to-date surge has been powered by transformative changes in global health trends, particularly the widespread adoption of GLP-1 therapies. Investors see Lilly as the clear frontrunner in a market undergoing rapid medical, cultural, and financial shifts.

Mounjaro and Zepbound Drive Massive Revenue

Third-quarter earnings highlighted unprecedented growth:

Mounjaro: $6.52B revenue (+109% YoY)

Zepbound: $3.59B revenue (+184% YoY)

These drugs are expanding faster than nearly any product in pharmaceutical history. Analysts expect continued momentum as insurance adoption widens, regulatory approvals expand, and Lilly prepares to launch oral GLP-1 versions—an innovation that could reshape accessibility.

Legacy of Innovation

Founded in 1876, Eli Lilly has delivered breakthroughs for a century—from insulin to Prozac to early polio vaccines. But its modern dominance began in 2022 when tirzepatide (Mounjaro) gained approval, offering dual-hormone therapy that reshaped diabetes and weight-loss treatment. Zepbound extended that dominance into obesity care, capturing global demand at scale.

Rivals such as Novo Nordisk and Pfizer are accelerating efforts, with the obesity-drug market expected to exceed $150 billion by the 2030s. Still, Lilly maintains the strongest growth trajectory.

Technical Outlook

LLY trades at all-time highs after breaking above the $969 resistance zone. Price action remains firmly bullish, targeting psychological levels at $1,100 and $1,200. Any retracement should find support at $969, keeping the broader uptrend intact.

Eli Lilly: The Trillion-Dollar Cure for Market Volatility?Eli Lilly has officially shattered the Silicon Valley ceiling, becoming the first healthcare company to achieve a $1 trillion market capitalization. While tech giants like Nvidia grapple with bubble concerns and doubts about AI monetization, Lilly has delivered tangible, recurring revenue through its dominance of GLP-1. This milestone is not merely a pharmaceutical victory; it represents a fundamental shift in market leadership from speculative tech to essential biopharma.

Macroeconomics: The Flight to Quality

The Federal Reserve’s pivot is fueling this ascent. New York Fed President John Williams signaled imminent rate cuts, raising December cut expectations to 70%. Lower rates disproportionately benefit capital-intensive sectors like pharma, which require massive upfront R&D and manufacturing spend. Investors, wary of tech volatility, are treating Lilly as a "defensive growth" asset—a rare hybrid offering the stability of healthcare with the explosive growth of software.

Science & Innovation: The Dual-Agonist Revolution

Lilly’s valuation rests on **tirzepatide** (branded as Mounjaro and Zepbound). Unlike previous drugs that target a single hormone, tirzepatide mimics both GIP and GLP-1, delivering superior efficacy in weight loss and blood sugar control. This scientific leap has rendered competitors’ single-agonist drugs vulnerable. Furthermore, Lilly is already stress-testing its own dominance with **retatrutide**, a triple-agonist candidate showing even higher potency, effectively cannibalizing its own portfolio before rivals can catch up.

Business Models: Disrupting the Middlemen

Lilly is aggressively rewriting the pharmaceutical distribution playbook. The launch of **LillyDirect** bypasses traditional Pharmacy Benefit Managers (PBMs). By partnering directly with Walmart to offer cash-pay options for Zepbound vials, Lilly captures margin previously lost to intermediaries. This Direct-to-Consumer (DTC) model exerts immense pressure on insurers to cover these drugs, leveraging patient demand as a battering ram against restrictive formularies.

Geostrategy: Manufacturing Sovereignty

Management recognizes that demand is useless without supply. Lilly has committed over $27 billion to manufacturing expansion, predominantly in the US and Europe (Ireland and Germany). This strategy reduces reliance on fragile Asian supply chains, insulating the company from US-China geopolitical friction. By onshoring active pharmaceutical ingredient (API) production, Lilly positions itself as a national security asset, aligning corporate growth with Western industrial policy.

Technology & Cyber: AI-Driven Discovery

Lilly is moving beyond traditional wet labs. The company’s **TuneLab initiative** utilizes federated AI learning. This allows biotech partners to train models on Lilly’s proprietary data without exposing the underlying IP. Additionally, partnerships with Isomorphic Labs aim to accelerate small molecule discovery. This "tech-forward" approach reduces the years-long timeline of drug discovery, turning R&D into a computational problem rather than a biological guessing game.

Management & Leadership: The Ricks Doctrine

CEO David Ricks has executed a masterclass in capital allocation. While peers engaged in share buybacks, Ricks poured capital into manufacturing capacity ahead of approval. His leadership style is characterized by "preemptive scale"—building the factory before the drug is approved. This risk appetite allowed Lilly to meet the explosive demand for Zepbound faster than competitors, securing market share through sheer logistical brute force.

Patent Analysis: Building the Moat

Lilly is fiercely defending its IP territory. The company has launched legal offensives against compounding pharmacies attempting to sell unauthorized versions of tirzepatide. Simultaneously, they are layering patents on delivery mechanisms and combination therapies. The transition from auto-injectors to vials also serves a strategic patent function, complicating the regulatory pathway for future biosimilars.

Conclusion

Eli Lilly has successfully decoupled itself from the broader healthcare index. By combining Silicon Valley-style innovation with industrial-scale manufacturing, it has created a $1 trillion moat. As the Fed eases policy, Lilly stands ready to deploy cheap capital to further widen the gap against its rivals.

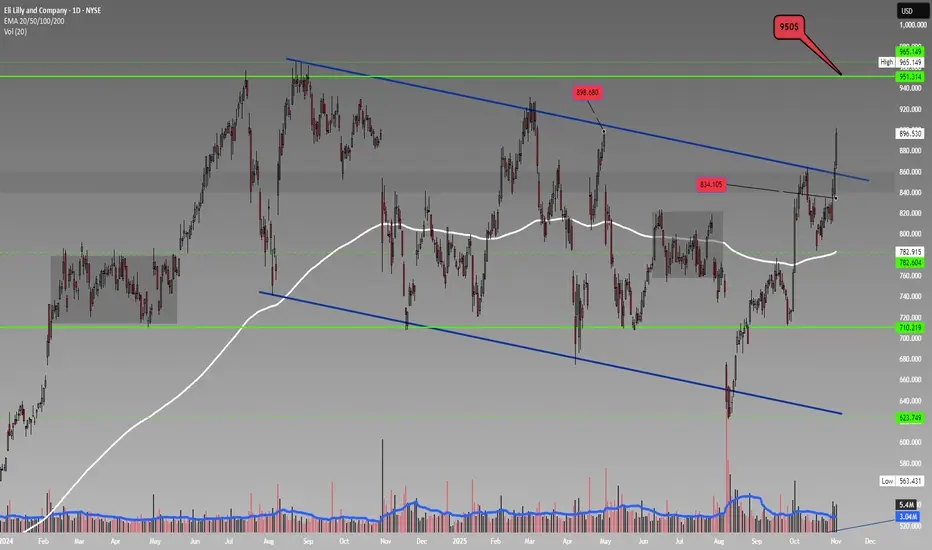

Eli Lilly’s $1T Breakout at 1060 | End of the Supercycle?Eli Lilly (LLY) – Macro Elliott Wave, Fibonacci & Historic $1 Trillion Milestone

LLY has now reached a critical long-term inflection point, advancing directly into the 2.618 Fibonacci extension , completing the projection of a full five-wave Elliott Wave cycle. This precise alignment establishes the 1060 region as a high-confidence macro top zone.

At today’s high of 1060 , LLY also achieved a historic milestone - crossing the $1 Trillion market-cap threshold , becoming the first medical company in history to reach this valuation. This achievement underscores the extraordinary scale of the preceding multi-year impulse and reinforces the significance of the current structural level.

With price holding at these unprecedented highs, the market is operating deep within a premium zone , where long-cycle reversals typically begin. While the bullish structure remains intact for now, the confluence of Fibonacci exhaustion, wave completion, and valuation extremity creates a strong, affirmative expectation that LLY is entering its macro topping phase.

The broader corrective roadmap follows a classical A–B–C structure , with downside levels anchored to key long-term Fibonacci retracements:

• The 0.236 retracement at ~245 forms the primary target for the anticipated Wave A leg, aligning with prior institutional accumulation and structural demand.

• The 0.382 retracement at ~98 represents the major macro demand zone and the high-probability destination for full cycle re-pricing via Wave C.

Taken together - the completed Elliott Wave structure, extreme Fibonacci extension, and the unprecedented $1T milestone - LLY stands at one of the most significant macro levels in its history. The next major move is expected to guide the market from its expansionary phase into a multi-year structural correction, with clearly defined downside objectives.

What do YOU think happens next?

Breakout or fake-out? Drop your prediction below!

👇 We are replying to every comment - let’s talk charts .

Smash the 👍 if this helped, hit 🔔 to catch the next setup,

and FOLLOW for more high-probability wave + SMC plays.

⚠️ Disclaimer

This content is for educational and informational purposes only and does not constitute financial, investment, or trading advice. All analyses reflect personal opinions based on publicly available data and chart structures. Markets involve risk, and you should always perform your own research or consult a licensed financial professional before making any trading decisions. Past performance does not guarantee future results.

"LLY's Bear Market Mode ON | Crash Incoming"“ LLY is gearing up for a sharp correction down to the $35–$17 zone — a critical reset that could flush out weak hands before the next explosive bull run. Stay sharp, this is where big opportunities form. ⚠️

🔥 Summary:

Eli Lilly (LLY) looks ready for a major market reset after completing a historic five-wave climb. This could be the start of a long-term corrective Wave 2 , potentially wiping out years of gains before the next explosive super-cycle takes off. The bull run isn’t over — but it’s taking a serious pause. ⚠️📉

🌊 Wave Theory Outlook

LLY’s multi-decade Elliott structure shows a completed Cycle Wave 1 peaking near the 2.618 extension zone around $1029. Historically, such extensions often mark exhaustion.

Next comes Wave 2 , which could retrace deep into the $35–$17 zone (the 0.618–0.786 Fibonacci region and prior structural base). Expect a complex W-X-Y pattern , shaking weak hands before a powerful Wave 3 bull expansion later this decade.

📉 Price Action & Smart Money Context

The chart shows exhaustion wicks, momentum divergence, and slowing volume — classic signs of distribution .

Smart money is likely off-loading near the highs , preparing to reload at discount levels once liquidity below 2020–2022 lows is taken.

Expect liquidity sweeps, imbalance fills, and a long-term accumulation base forming near the orange demand zone before the next breakout.

💰 Fundamental Alignment

Despite incredible fundamentals — obesity and diabetes drug leadership, global demand growth, and innovation — valuation gravity always returns .

A deep correction would align price with sustainable earnings and provide institutional re-entry opportunities at fair value.

🧠 Traders ,

"the charts are whispering — a major LLY correction is loading.

Our projections highlight the $35–$17 zone as the key accumulation region before the next super-cycle.

Stay alert, plan your levels, and don’t fight the wave. 🌊📉

Where do you think LLY bottoms out? Share your thoughts below 👇”

— Team FIBCOS

#LLY #EliLilly #BearMarket #Correction #WaveTheory #SmartMoney #ElliottWave #Fibcos #TechnicalAnalysis #PriceAction #Investing #PharmaStocks #StockMarket #MarketCycle #ChartAnalysis #Bearish #Wave2 #TradingView #StockAlert #MarketReset

Eli Lilly Drug Shows New Potential in Curbing Food CravingsEli Lilly’s GLP-1 weight-loss drug tirzepatide — sold as Mounjaro and Zepbound — may do more than suppress appetite. A new Nature Medicine report shows that in one patient with severe binge-eating behavior, the drug appeared to silence food-craving signals in the brain’s reward center. This is the first direct recording of brain activity in a person receiving tirzepatide, offering rare insight into how GLP-1 drugs may reduce “food noise.”

Researchers from the University of Pennsylvania monitored the brain activity of four patients undergoing deep-brain stimulation for loss-of-control eating disorders. Only one was already taking tirzepatide. During electrode monitoring, her nucleus accumbens — the core craving region — showed no binge-triggering activity, and she experienced no food preoccupation. The other three patients showed the usual spikes in brain activity before cravings. While the findings cannot be generalized due to the small sample size, researchers believe this opens a door for exploring GLP-1 drugs as potential treatments for certain eating disorders.

Technically, Eli Lilly’s stock continues its strong bullish structure. Price recently broke above a major resistance zone at $960, pushing into new all-time highs. With this breakout, the market may wait for a clean retest of former resistance — now support — before another upward continuation. The next psychological levels to watch remain $1,100 and $1,200, which could act as future resistance zones if momentum continues.

$LLY probably back to $1000Took full profits on NYSE:LLY , did not want to see this overshoot and a reversal. Short term it's going back to $1000 first, probably.

LLY NOV 2025LLY extending in markup, demand absorption at 935-885 support.

Upside target 1120; downside 885 then 740 if it fails.

#LLY #globaltrade #investment #investing #stockmarket #wealth #realestate #markets #economy #finance #money #forex #trading #price #business #currency

LLY Hits Major Resistance: Breakout to $1300 or Pullback Ahead?LLY is moving inside a strong long-term ascending channel, and the price has now reached the upper resistance boundary of the purple channel.

This is a major decision zone:

Either a breakout occurs and momentum continues strongly upward,

or the price gets rejected and pulls back inside the channel.

Bullish Scenario (Breakout)

A confirmed breakout above the upper channel line can start a strong rally.

Bullish Targets:

• $1150

• $1220

• $1300 (only if the breakout is solid)

Bearish Scenario (More likely on first touch)

LLY reached the top after a very sharp rally, so a pullback is logical.

Bearish Targets:

• $1050

• $980 (mid-channel)

• $900 (bottom of the purple channel)

Stop Loss

• Long positions: Below $1050

• Short positions: Above $1135

Eli Lilly and Company: Path to Sustained Market LeadershipEli Lilly and Company has achieved a market valuation approaching one trillion U.S. dollars by the close of 2025, underpinned by a comprehensive corporate strategy that integrates advanced scientific research, targeted technology acquisitions, and adaptive global partnerships. This performance, marked by a substantial year-over-year share appreciation, positions the firm as a preeminent participant in the international pharmaceutical sector and underscores structural advantages in innovation-driven capital markets.

Core Therapeutic Franchises and Pipeline Expansion

The company's cardiometabolic portfolio, centered on dual GIP/GLP-1 receptor agonists, continues to serve as the principal engine of revenue growth. Products indicated for type 2 diabetes and chronic weight management recorded quarterly sales exceeding ten billion dollars in 2025, reflecting robust demand in large-scale metabolic disease populations. Ongoing clinical investigation into the neurobiological effects of these molecules has yielded preliminary evidence of modulation within central reward pathways, suggesting potential future applications in neuropsychiatric conditions characterized by dysregulated appetite control. Such findings reinforce the intellectual property protections surrounding the franchise and broaden its therapeutic scope.

In parallel, Eli Lilly is advancing capabilities in central nervous system disorders through specialized drug-delivery technologies. A recent multibillion-dollar licensing agreement with a South Korean biotechnology enterprise grants exclusive access to an engineered bispecific antibody platform designed to enhance macromolecular transport across the blood-brain barrier. This acquisition complements prior collaborations in the same domain and materially strengthens the company's competitive positioning in Alzheimer’s disease, Parkinson’s disease, and related neurodegenerative indications.

Global Research Collaborations and Supply-Chain Resilience

Strategic alliances with leading Asian biotechnology organizations form a key component of Eli Lilly’s innovation sourcing model. These partnerships provide access to proprietary platform technologies, expand the firm's intellectual property base beyond North American origination, and foster diversified scientific talent networks. By establishing collaborative development nodes within geopolitically aligned jurisdictions, the company enhances resilience in high-value biopharmaceutical supply chains while accelerating the maturation of next-generation therapeutic modalities.

Capital Market Dynamics and Transatlantic Divergence

Eli Lilly operates within a U.S. financial ecosystem that currently represents approximately three-quarters of global developed-market equity indices, an environment particularly conducive to large-capitalization growth enterprises. This structural weighting, combined with concentrated domestic healthcare spending and investor preference for scalable innovation platforms, has facilitated accelerated valuation expansion. In contrast, European peers contend with more fragmented national markets and differing risk appetite conventions among institutional investors, resulting in divergent capital allocation outcomes across the Atlantic.

Executive Leadership and Technology Adoption

Under the direction of Chief Executive Officer David Ricks, Eli Lilly has institutionalized the integration of advanced computational tools throughout the research and decision-making processes. Specialized large-language models and frontier artificial intelligence systems are routinely employed to augment hypothesis generation and data interpretation, supported by investments in high-throughput robotic experimentation infrastructure. This disciplined yet exploratory approach to emerging technologies reflects a broader organizational commitment to maintaining leadership in computationally assisted drug discovery.

Evolution Toward Platform-Centric Development

The company has transitioned from asset-specific transactions to the systematic acquisition of foundational technology platforms capable of yielding multiple product candidates. Recent investments in blood-brain barrier transport modalities and downstream applications in oncology illustrate this paradigm. By prioritizing versatile, proprietary enabling technologies, Eli Lilly establishes durable competitive barriers and aligns its research and development expenditure with long-term industry trends favoring multi-indication pipelines.

Intellectual Property Strategy and Risk Mitigation

Comprehensive patent estates surrounding the incretin mimetic class, coupled with proactive manufacturing capacity expansion, preserve pricing autonomy and market exclusivity in high-volume cardiometabolic indications. Concurrent investment in novel mechanisms—of which blood-brain barrier penetration is a prime example—serves to replenish the development pipeline and offset eventual patent expirations on current revenue-generating products. This forward-looking intellectual property management underpins investor confidence in the sustainability of the company’s growth trajectory.

In summary, Eli Lilly’s ascent to near-trillion-dollar valuation reflects the successful execution of an integrated strategy encompassing scientific excellence, strategic technology acquisition, international collaboration, and rigorous capital allocation—positioning the enterprise for continued leadership in global biopharmaceutical innovation.

Eli Lilly and Company (LLY)Initiate short bias around $1020-1060.

Targets:

Target 1: $840

Target 2: $740

Options Position:

Buy Dec 19 $800 Put @ $2.44

Take partial profits once price reaches $840 area to lock gains.

$LLYThe technical structure for NYSE:SMR presents a compelling case of a strong, sustained uptrend, characterized by a rhythmic pattern of sharp advances followed by periods of consolidation. This behavior is the hallmark of a healthy, momentum-driven bull move.

1. Pattern Analysis: Sequential Bull Flags

The chart reveals the successful completion and continuation of a classic bullish pattern sequence:

The First Bull Flag: This pattern likely began with a powerful upward move (the "flagpole"), followed by a brief, shallow, and downward-sloping consolidation period (the "flag"). The successful breakout above this first flag confirmed the pattern and signaled the resumption of the uptrend. Your note that this first pattern "has been a success" is a key observation that sets a bullish precedent.

The Emerging Second Bull Flag: Following the initial breakout, the price action appears to be forming a second, successive bull flag. This pattern represents a temporary pause and period of profit-taking within a larger uptrend. It indicates that after a strong leg up, the market is catching its breath, allowing overbought conditions to ease before the next potential advance. We are currently in the "waiting" phase for this second pattern to fully reveal itself and confirm with a breakout.

2. Fibonacci Retracement: Mapping the Pullback and Target

Applying Fibonacci retracement levels to the most significant prior upswing provides a mathematical framework for understanding the corrections and projecting future targets.

The current consolidation within the second bull flag has already respected key Fibonacci levels, finding support and reversing near them:

0.236 Level ($44.30): This shallow level was easily passed, indicating a healthy correction.

0.382 Level ($36.18): This is a common retracement zone in a strong trend, and the price action here likely provided a key support area.

0.500 Level ($29.62): A deeper, but still within the normal, retracement level. Holding above this level would be considered a sign of continued strength.

The analysis points to the 0.618 Fibonacci retracement level at $23.05 as the primary target for the overall pattern. This level is a deep retracement and often acts as a critical support or resistance zone. In this context, it represents a significant profit-taking objective once the second bull flag completes its breakout and resumes the upward trajectory.

3. The Overall Narrative and Key Levels to Watch

The story for NYSE:SMR is one of a powerful, structured uptrend building energy for its next move.

The Bullish Narrative: The successful first bull flag established a pattern of "burst and consolidate." The formation of a second such pattern suggests the trend is well-organized and has further to run. The measured move projection from the second flag, upon a breakout, aligns with the $23.05 (0.618 Fib) target.

The Outlook After the Target: It is prudent to anticipate that upon reaching the $23.05 target, the stock will likely experience a significant pullback or period of extended consolidation. This is a typical market behavior as traders lock in profits at a major Fibonacci level.

Conclusion and Strategy:

Confirmation Trigger: A decisive breakout above the resistance trendline of the current, second bull flag pattern is needed to confirm the next leg up is beginning.

Primary Target: The initial upside target for this next leg is projected at the $23.05 level.

Risk Management: A break below the support trendline of the second flag would invalidate the short-term bullish pattern and suggest a deeper correction is underway.

In summary, NYSE:SMR is exhibiting technically sound bullish behavior. The focus is now on the completion of the second bull flag, with a breakout setting the stage for a move toward the $23.05 Fibonacci target, after which a pullback is considered a high probability.

NYSE:LLY has confirmed a bull flag pattern which suggest a bull run. NYSE:LLY has strong fundamentals. stop loss for NYSE:LLY is 0.236 (787.55). take profit is 1,100 and 1,200 reparaphase and make it longer please

Of course. Here is a detailed and repurposed technical analysis of NYSE:LLY (Eli Lilly) based on the points you provided, expanded to provide a more comprehensive market perspective.

Technical & Fundamental Analysis of NYSE:LLY : Positioning for a Continued Advance

A combined technical and fundamental assessment of Eli Lilly ( NYSE:LLY ) reveals a powerfully bullish setup, suggesting the stock is poised for a significant continuation of its established uptrend. The convergence of a confirmed chart pattern and robust underlying fundamentals creates a high-conviction narrative for further gains.

1. Technical Outlook: The Confirmed Bull Flag Pattern

The primary technical feature on the chart is the confirmation of a Bull Flag pattern. This pattern is one of the most reliable continuation signals in technical analysis and typically forms after a strong, near-vertical advance (the flagpole).

Pattern Structure: The formation began with a sharp upward move (the flagpole), followed by a period of consolidation characterized by a slight downward or sideways drift on lower volume (the flag). This consolidation represents a brief pause and profit-taking phase within a larger bullish trend.

Confirmation: The pattern is considered "confirmed" once the price breaks out above the upper trendline of the flag consolidation with conviction, ideally accompanied by a surge in trading volume. This breakout signals that the period of consolidation has ended and the prior uptrend is resuming.

2. The Powerful Fundamental Backdrop

The bullish technical structure is significantly reinforced by NYSE:LLY 's strong fundamentals. The company is a leader in the pharmaceutical sector, with a highly promising portfolio. Key drivers include:

Blockbuster Drugs: Massive commercial success and future potential from drugs like Mounjaro and Zepbound in the GLP-1 space for diabetes and weight loss.

Robust Pipeline: A strong and innovative research and development pipeline that promises future growth.

Solid Financials: Consistent revenue growth and profitability.

This fundamental strength provides a solid foundation for the stock's upward move, suggesting that the trend is supported by tangible business performance and not merely speculative sentiment. This reduces the risk of the pattern being a false signal.

3. Trade Management Strategy: Risk and Reward

A clear plan for managing the trade is crucial. Based on the bull flag's measured move target and Fibonacci levels, a structured approach would be:

Stop-Loss (Risk Management): To protect capital in the event of a pattern failure or a sudden market reversal, a logical stop-loss level is placed below the 0.236 Fibonacci retracement level at $787.55. This level acts as a key support; a break below it would invalidate the immediate bullish premise and suggest a deeper pullback is underway.

Profit-Taking Targets (Reward Zones): The measured move projection of the bull flag pattern provides clear upside objectives.

Primary Target: $1,100. This is the initial projected price target based on the technical pattern and represents a key psychological and resistance zone.

Extended Target: $1,200. If buying momentum remains exceptionally strong and the stock breaks through the $1,100 level with ease, a further extension toward the $1,200 area becomes probable. This would likely represent a more euphoric or parabolic phase of the move.

Synthesis and Market Outlook

In summary, NYSE:LLY presents a high-probability bullish setup where technicals and fundamentals are in strong alignment. The confirmed bull flag breakout indicates the continuation of a powerful uptrend, with clearly defined levels for managing risk and securing profits.

Key Levels to Watch:

Support (Stop-Loss): $787.55

Resistance (Target 1): $1,100

Resistance (Target 2): $1,200

Traders and investors should monitor the stock's behavior at these key levels. A hold above the flag's resistance, now turned support, combined with strong fundamental tailwinds, keeps the bullish thesis firmly intact.

ELI LILLY to soon start a correction towards $700.Eli Lilly (LLY) has made new All Time Highs (ATH) this month, extending the impressive rally since the August Low near the 1W MA200 (orange trend-line).

The multi-year trend remains bullish within a Fibonacci Channel Up but practically the stock hasn't gotten out of its range since the July 2024 High, breaking in August below even its 1W MA100 (green trend-line).

This prolonged sideways trading resembles the July 2015 - July 2018 3-year consolidation phase, which broke upwards only after a 2nd test of the 1W MA200. Even the 1M RSI patterns between the two sequences are similar. Based on this (1M RSI), which is about to break above its MA for the first time since July 2024, we are in similar levels as February 2017.

As a result, we expect LLY to start a rather smooth correction towards its 1W MA200 again, targeting $700, where the next long-term buy opportunity may potentially emerge.

---

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

---

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Eli Lilly and Company breakoutEli Lilly and Company NYSE:LLY price has broken above the previous resistance near $950 and is now charging toward the top of its long-term ascending channel.

The next key level sits around $1,076.

Eli Lilly Testing $1000 — Breakout or Fakeout?After consolidating for over a year inside a descending channel, LLY has rallied back to the top resistance zone around $1000.

Bullish Case:

• Breakout above $1000 = start of new uptrend.

• Targets: $1100 → $1200.

Bearish Case:

• Rejection at $1000 could pull price back to $850–$800, or even $700 (channel bottom).

Conclusion:

LLY is at a make-or-break point — a confirmed breakout could send it to new all-time highs, while rejection would trigger a correction back into the channel.

$LLY: Decision Zone — Wedge Breakout or Retest of 685Eli Lilly (LLY) rebounded off the long-term trendline and weekly demand box (≈622–686) and is compressing inside a descending wedge.

Bullish path (blue): a clean break and retest of wedge resistance opens room toward the prior extension/marker near ~970.

Bearish path (red): rejection at the wedge cap could send price back to the green trendline for a higher-low around ~685 before another attempt up.

News supporting the bullish path:

1- Mounjaro (tirzepatide) UK price hike: Lilly will lift UK list prices by up to ~170% from Sept 1, 2025 (e.g., highest doses from ~£122 to ~£330), with pharmacies flagging stockpiling/shortages. This supports revenue/ASP but may draw scrutiny.

2- Phase 3 ATTAIN-2 (orforglipron, oral GLP-1): trial met primary & key secondary endpoints in patients with obesity/overweight and Type-2 diabetes; company guiding to global regulatory submissions this year. Reports cite ~10.5% mean weight loss at the top dose. Sentiment tailwind for the obesity franchise.

Invalidation: weekly close below ~622.

Not financial advice :)

LLY - Massive Bullflag in a Multi-year uptrendLLY will absolutely outperform in the next couple of months.

Pair a technically flawless chart with a huge bullflag breakout with positive headwind "Google: Trump announces deals with Eli Lilly, Novo Nordisk to slash weight loss drug prices, offer some Medicare coverage" and coming QE and you have a star in the making.

First targets for profit-taking marked in the charts if you want to swing trade this beast in the next 6-12 months.

Eli Lilly (LLY) Weekly Chart – Double Top Patterns & Major SuppoLLY has formed consecutive double top patterns within a broad descending channel.

Price recently tested a long-term major support zone and bounced strongly, signaling renewed buying interest. If this momentum holds, a move toward the major resistance near $973 is possible, aligning with the upper trend-line.

RSI remains in recovery territory, suggesting potential for further upside before overbought conditions appear.

Eli Lilly ($LLY) – Brief AnalysisNYSE:LLY The stock remains in a downward channel (resistance ~772–780 $, support ~720–709 $, key risk level — 680 $).

Current price (~752 $) is around the middle of the channel (Fib 0.5). There’s pressure from the upper boundary.

Entry points:

750–755 $ (aggressive, with retracement risk)

Above 780 $ (confirmed breakout, targets 800–858 $)

Around 720 $ (defensive entry on rebound)

Targets: 800 → 858 → 900 $

Stop-loss: below 680 $.

With positive GLP-1 news (Zepbound, Mounjaro, new projects), an upside breakout looks the most likely scenario.

LLY DAILY OUTLOOKLLY has been rising strongly with high volume for the past three days! It closed above its long-term downtrend. Let’s see if it can reach $950.

If you already hold a position, taking some profits could be considered. If it falls below $835, the situation might change.

💬 Remember: Profit looks best in your pocket money that’s not in your pocket isn’t yours yet!

Wishing everyone successful trades and good profits!

LLY Bullish Breakout: Retest or Continuation Toward 950–1000Eli Lilly (LLY) just cleared the key ceiling at 865 with a wide-range bullish day, closing near 896.53 and printing a session high at 901.34. The breakout resolves an ascending triangle and comes with expanding volatility and volume—classic continuation behavior in a dominant uptrend. With price above the 20/60/120-day MAs and bands widening, momentum favors the upside while acknowledging short-term overbought conditions.

Primary path: treat 865–880 as the new Demand zone (polarity flip). A clean retest that holds this band and shows a bullish candle is a higher-probability entry, aiming first for 925, then the psychological markers at 950 and ultimately the measured move area around 980–1000. For traders preferring strength, a daily close through 902 would signal continuation in price discovery, using 880–865 as the first check on risk.

If buyers fail to defend the breakout, a decisive close back below 860 invalidates the bullish thesis and opens room for a deeper shakeout. Until then, dips into 865–880 are potential buys, while strength above 902 can be used to add or initiate, with partial profit-taking into 950 and 980–1000 to respect the expanded volatility.

This is a study, not financial advice. Manage risk and invalidations.

Imminent bullish breakoutThe price has been moving within a descending channel for several months, and following the recent earnings report, it's accelerating upward — now positioned just below the upper boundary.

A confirmed close above $880 would set the next target at $935, followed by a potential move beyond $1000.

Keep an eye on the healthcare sector — it's poised to surprise in the coming year.

LLY | This Healthcare Co. Is a Great Pick | LONGEli Lilly & Co. engages in the discovery, development, manufacture, and sale of pharmaceutical products. The firm's products consist of diabetes, oncology, immunology, neuroscience, and other products and therapies. The company was founded by Eli Lilly in May 1876 and is headquartered in Indianapolis, IN.