$SPX Hi, we are back with another one: SP:SPX !!!

As we can see we have SP:SPX sitting at $6796.30 with and expectation for a 65% pump.

That would bring us around $9-$10K per 1 SP:SPX .

Wouldn't that be incredible if we can see this by 2026 -2028 ?

What a time to be alive no ?

Don't forget to comment like and share for good luck :) !!!

Trade ideas

SPX500 - 5000 & 5500 PUT, exp June 2026📉👍

SPX500 short with 5000 & 55000 PUT exp June 2026.

Take your pick...

AI hype & capital overcommitment

China beginning to catch up in GPU compute capability, pulling away capital from nvidia

Degrading consumer credit (BNPL, Auto loans, housing)

Increased govermant debt, geo-political decoupling

China rare earth mineral threats

Possible overturn on the Trumps tarrifs by the supreme court, requiring repatriations to be paid back to foreign countries

SPX QuantSignals V3 0DTE – High-Conviction PUT Alert SPX 0DTE Signal | 2025-11-13

Market Context:

SPX faces heavy selling pressure after a -1.22% intraday drop, with RSI at an extreme 8.1 (oversold zone). Despite Katy AI’s neutral 50% confidence, momentum and sentiment indicate short-term downside continuation.

AI Insight (QuantSignals V3):

Confidence: 72% (Medium)

Predicted Range: $6769 → $6667 (-1.5%)

Gamma Risk: Low

Flow Intel: Neutral

Signal Type: 0DTE PUT

Trade Setup:

🎯 Strike: 6770 PUT (Exp. 2025-11-13)

💵 Entry: $15.30

🎯 Target 1: $22.80 (+50%)

🎯 Target 2: $30.60 (+100%)

🛑 Stop Loss: $10.70 (-30%)

📏 Position Size: 2% (Low-Moderate Risk)

🕒 Exit By: 2:00 PM ET (Time Decay Risk)

Technical Summary:

EMA alignment: Bearish

RSI: 8.1 (Extreme Oversold)

MACD: -6.23 (Bearish)

Support: $6667.58 (Katy stop)

Resistance: $6869.91 (session high)

Key Notes:

⚠️ Katy’s model predicts upside, but real-time technicals override AI summary.

⚡ Momentum + sentiment confirm short-term PUT bias.

📉 Use tight stop & scale profits fast — 0DTE = fast decay.

SPX 1H – Rejection at Parabolic Midline | 11/13 UpdateSPX rejected cleanly from the 10/28–10/29 supply zone and the parabolic midline (blue). The lower parabolic channel on 11/10 ( check the chart ) - this level that flipped from support to resistance after Nov 10.

Currently, price is testing the 10/24 High R zone (~6774) with strong downside momentum shown on Heikin Ashi

Key Levels:

Resistance: 6830–6870 (midline + prior rejection block)

Suport 1: 6780 (10/24 High R)

Support 2: 6720–6650 (10/2–10/9 & 9/16–11/7 demand zones)

Scenarios:

Bounce: If 6780 holds, expect a short-term relief rally toward 6830–6850 (mean reversion).

Breakdown: A 1H close below 6775 opens room for 6720 and possibly 6650.

Overall momentum remains bearish after rejection from the parabolic curve. Bulls must reclaim 6830+ to shift structure.

S&P500 (US500): Important Breakout & Bullish Continuation

US500 likely completely a correctional movement,

breaking a resistance line of a bullish flag pattern on a 4H time frame.

I think that a bullish wave is going to start soon

and the market will reach at least to 6917 level.

❤️Please, support my work with like, thank you!❤️

I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

SPX500 TIME TO BUY NOWSPX500 is in a clear upwards channel and has broken the last bit of resistance (white line shown) - this is a clear confirmation that the next target will be the next resistance zone to the upside shown above (this is a great buy trade opportunity) - Time to buy!

S&P 500 H1 | Bullish Bounce off Key SupportMomentum: Bullish

Price is currently above the ichimoku cloud.

Buy entry: 6,849.07

- Strong overlap support

- 50% Fib retracement

- 100% Fib projection

Stop Loss: 6,814.5

- Swing low support

Take Profit: 6,883.1

- Strong overlap resistance

Stratos Markets Limited (tradu.com/uk ), Stratos Europe Ltd (tradu.com/eu ):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 70% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Global LLC (tradu.com/en ): Losses can exceed deposits.

Bullish continuation in play?S&P500 (US500) has bounced off the pivot and could potentially rise to the 1st resistance.

Pivot: 6,827.13

1st Support: 6,745.48

1st Resistance: 7,006.51

Disclaimer:

The opinions given above constitute general market commentary and do not constitute the opinion or advice of IC Markets or any form of personal or investment advice.

Any opinions, news, research, analyses, prices, other information, or links to third-party sites contained on this website are provided on an "as-is" basis, are intended to be informative only, and are not advice, a recommendation, research, a record of our trading prices, an offer of, or solicitation for, a transaction in any financial instrument and thus should not be treated as such. The information provided does not involve any specific investment objectives, financial situation, or needs of any specific person who may receive it. Please be aware that past performance is not a reliable indicator of future performance and/or results. Past performance or forward-looking scenarios based upon the reasonable beliefs of the third-party provider are not a guarantee of future performance. Actual results may differ materially from those anticipated in forward-looking or past performance statements. IC Markets makes no representation or warranty and assumes no liability as to the accuracy or completeness of the information provided, nor any loss arising from any investment based on a recommendation, forecast, or any information supplied by any third party.

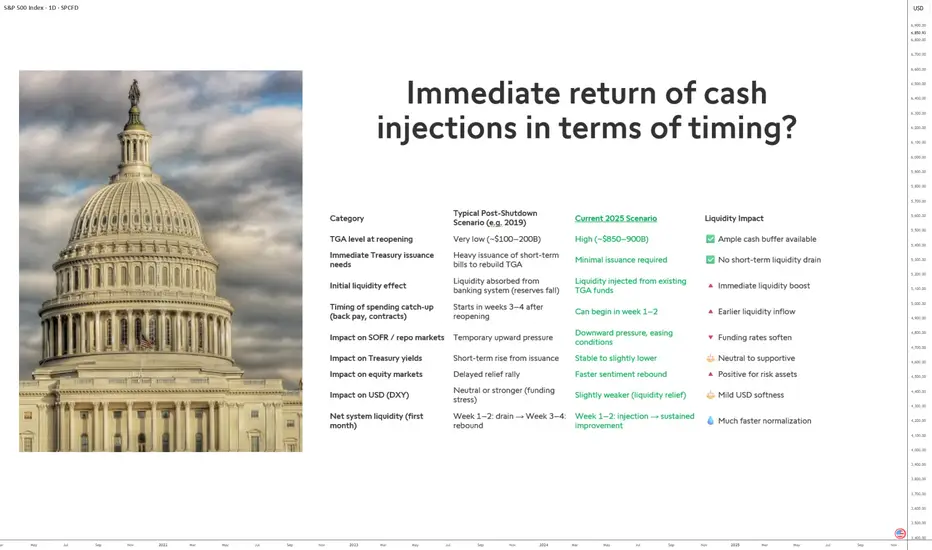

End of the 2025 Shutdown: Immediate Impact on LiquidityThe reopening of the U.S. government at the end of the 2025 shutdown is expected to trigger a swift return of liquidity to financial markets. This recurring phenomenon will have a distinct magnitude this time due to the specific conditions of the U.S. Treasury General Account (TGA) and the current federal funding structure.

1) A fiscal context unlike previous shutdowns

In past episodes, notably in 2019, the U.S. Treasury exited the shutdown with very low cash balances—typically between $100 and $200 billion. To rebuild this buffer, it had to issue large amounts of short-term Treasury bills, which drained liquidity from the banking system as investors used reserves to buy the securities.

In 2025, the situation is reversed. The Treasury holds a high cash balance—estimated between $850 and $900 billion—because the federal government’s account at the Fed (the TGA) was replenished at the end of September. This provides ample room to finance near-term public spending without issuing new debt. The result is an absence of pressure on money markets and stable bank reserves.

2) Liquidity injections from day one

With abundant cash reserves, the Treasury can promptly resume pending payments—federal salaries, public contracts, and suspended programs. These payments act as direct liquidity injections into the financial system, starting within the first weeks following the end of the shutdown.

In previous reopenings, this process began only after three to four weeks. In 2025, it could start as early as week one or two, significantly shortening the normalization timeline for market liquidity.

3) Moderate but positive market effects

This faster liquidity return should lead to:

• unchanged or slightly lower bond yields, given steady demand and the absence of additional issuance;

• a slightly weaker dollar, reflecting easier financing conditions.

Overall, this points to a quicker and more orderly normalization of the monetary system compared to 2019, potentially supporting risk assets in the short term.

DISCLAIMER:

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only. The presented idea (including market commentary, market data and observations) is not a work product of any research department of Swissquote or its affiliates. This material is intended to highlight market action and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is advisable to seek professional advice from licensed advisor before making any financial decisions.

This content is not intended to manipulate the market or encourage any specific financial behavior.

Swissquote makes no representation or warranty as to the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The views expressed are those of the consultant and are provided for educational purposes only. Any information provided relating to a product or market should not be construed as recommending an investment strategy or transaction. Past performance is not a guarantee of future results.

Swissquote and its employees and representatives shall in no event be held liable for any damages or losses arising directly or indirectly from decisions made on the basis of this content.

The use of any third-party brands or trademarks is for information only and does not imply endorsement by Swissquote, or that the trademark owner has authorised Swissquote to promote its products or services.

Swissquote is the marketing brand for the activities of Swissquote Bank Ltd (Switzerland) regulated by FINMA, Swissquote Capital Markets Limited regulated by CySEC (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the CSSF, Swissquote Ltd (UK) regulated by the FCA, Swissquote Financial Services (Malta) Ltd regulated by the Malta Financial Services Authority, Swissquote MEA Ltd. (UAE) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) licensed by the Hong Kong Securities and Futures Commission (SFC) and Swissquote South Africa (Pty) Ltd supervised by the FSCA.

Products and services of Swissquote are only intended for those permitted to receive them under local law.

All investments carry a degree of risk. The risk of loss in trading or holding financial instruments can be substantial. The value of financial instruments, including but not limited to stocks, bonds, cryptocurrencies, and other assets, can fluctuate both upwards and downwards. There is a significant risk of financial loss when buying, selling, holding, staking, or investing in these instruments. SQBE makes no recommendations regarding any specific investment, transaction, or the use of any particular investment strategy.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The vast majority of retail client accounts suffer capital losses when trading in CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital Assets are unregulated in most countries and consumer protection rules may not apply. As highly volatile speculative investments, Digital Assets are not suitable for investors without a high-risk tolerance. Make sure you understand each Digital Asset before you trade.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainties.

The use of Internet-based systems can involve high risks, including, but not limited to, fraud, cyber-attacks, network and communication failures, as well as identity theft and phishing attacks related to crypto-assets.

US500 Recovery on Imminent US Government Shutdown DealFundamental Analysis

The US500 is driven by strong Q3 earnings and a recovery in risk sentiment due to the imminent resolution of the US government shutdown. Market odds for a December Fed rate cut are high, boosting equity valuations. However, index gains are uneven, highly concentrated in the "Magnificent 7" tech mega-caps.

Technical Analysis

The index is in a well-defined upward channel, with dynamic support at the EMA 21. The RSI is bullish but nearing overbought territory, though all major moving averages signal a "buy." Short-term volatility (VIX) is low, supporting a continued grind higher. Key levels are 6,805 Support and 6,920 Resistance.

Sentiment Analysis

Optimism prevails following the drop in the VIX, indicating subsiding turbulence. Funds are positioning for a low-volatility climb. However, caution exists regarding high valuations in tech and signs of rotation into defensive sectors. Commentators view recent dips as routine corrections.

Outlook

The year-end target remains near 7,000, contingent on sustained macroeconomic stability and continued Fed dovishness. Pullbacks are expected to be buying opportunities given solid corporate profitability and continued AI enthusiasm. The core uptrend remains intact barring major policy or geopolitical surprises.

Analysis by Terence Hove, Senior Financial Market Strategist at Exness

US500: Breaking Out of the Falling ChannelUS500: Breaking Out of the Falling Channel

The US500 index has finally broken out from its falling channel, signaling a potential continuation of the broader bullish trend.

After a strong recovery from recent lows, price action suggests a possible pullback to retest the breakout zone before targeting higher levels.

If momentum continues, we could see buyers pushing the index toward the 6,875 resistance zone first — and if that level gives way, the next target sits around 6,985.

Key levels to watch:

🎯Target 1: 6,875

🎯Target 2: 6,985

You may find more details in the chart!

Thank you and Good Luck!

❤️PS: Please support with a like or comment if you find this analysis useful for your trading day❤️

SPX500 Bullish Plan in Motion with SMA + Kijun Confirmation🚀 US500/SPX500 INDEX MARKET SWING TRADE MASTERCLASS 🎯

📊 ASSET: S&P 500 Index (US500 | SPX500)

Timeframe: 4H-Daily | Strategy Type: Swing Trade | Market Context: Bullish Pullback Confirmation

🎲 TRADE SETUP: THE "THIEF PROTOCOL" STRATEGY ⚡

✅ TECHNICAL CONFIRMATION

🔹 Primary Signal: Simple Moving Average (SMA) Pullback Retest

🔹 Secondary Confirmation: Kijun-sen (Ichimoku MA) Retest

🔹 Market Structure: Higher Lows Formation + Bullish Consolidation

🔹 Bias: LONG with Layered Entry Methodology

💰 ENTRY STRATEGY: MULTI-LAYER LIMIT ORDER APPROACH

The "Thief Layering Method" - Stack multiple buy limit orders for optimal risk distribution:

🟢 Layer 1 Entry: $6,750.00 - Initial Probe Entry (30% Position Allocation)

🟢 Layer 2 Entry: $6,800.00 - Aggressive Add (35% Position Allocation)

🟢 Layer 3 Entry: $6,850.00 - Final Confirmation Entry (35% Position Allocation)

Entry Flexibility: Adjust layers based on your account size & risk tolerance. Spread entries across pullback zones for superior fill pricing.

🛑 STOP LOSS MANAGEMENT

Recommended SL Level: $6,720.00 - Placed below the support trendline + SMA confluence

⚠️ IMPORTANT DISCLAIMER: Dear Traders! This is YOUR trading journey. We strongly recommend adjusting stop loss based on YOUR risk management rules. Account sizing is crucial - never risk more than 2-3% per trade. Your SL placement = YOUR decision, YOUR responsibility. Use proper position sizing ALWAYS.

🎯 PROFIT TARGET ZONES

Primary Target: $7,050.00 ⚡

📊 Technical Reasoning: This level represents strong resistance confluence zone, historical supply level in overbought territory, and creates a risk/reward sweet spot of 1:3+ return potential. Alert: Trap zone exists here - smart money reversal area confirmed.

Exit Strategy Recommendation: Close 50% of position at $7,000-7,020 to lock partial profits. Hold remaining 50% with trailing stop or until $7,050 for maximum upside capture. Lock profits incrementally to secure gains.

⚠️ CRITICAL REMINDER: Your profit target = YOUR choice! This TP represents technical confluence, but market conditions evolve. Trade YOUR plan, manage YOUR risk, protect YOUR capital.

🌍 CORRELATED PAIRS TO WATCH 🔗

📈 PRIMARY CORRELATIONS

1️⃣ QQQ (Nasdaq-100 ETF) - 0.99 Correlation 💻

This is the tech-heavy composition that typically leads SPX rallies. Current focus remains on AI/Mag7 momentum and overall growth stock sentiment. Key watch: QQQ strength = SPX bullish confirmation signal. When QQQ breaks out, SPX follows closely.

2️⃣ IWM (Russell 2000 ETF) - 0.95 Correlation 📍

Small-cap composition with high tariff sensitivity. Current status shows small-cap underperformance zones vulnerable to trade policy shifts. Trading tip: IWM weakness = Sector rotation risk, so watch for divergence from SPX strength.

3️⃣ DXY (US Dollar Index) - Inverse/Mixed Correlation 💵

Recent positive correlation emerging in 2025 market dynamics. Current dynamic shows dollar strength now sometimes supports equities due to policy-driven factors. Risk factor alert: DXY spike above 108 = potential SPX headwind to monitor.

📊 SECONDARY WATCH PAIRS

SPY (S&P 500 ETF) - Mirror of SPX, use for volume confirmation and institutional positioning.

DIA (Dow Jones ETF) - Large-cap value barometer, less tech-sensitive than QQQ, shows rotation signals.

VIX (Volatility Index) - Above 25 = caution mode, below 15 = complacency warning.

📱 KEY CORRELATION INSIGHTS FOR THIS TRADE

🔴 RED FLAGS - Watch These Closely:

VIX spiking above 30 signals potential fear spike. DXY breaking above 108 creates dollar strength pressure. QQQ failing to confirm breakout indicates tech weakness divergence. IWM hitting new lows signals broad market weakness.

🟢 GREEN LIGHTS - Trade Confirmation:

QQQ and SPX moving in sync above SMA is bullish. IWM holding key support levels confirms breadth. DXY consolidating means no headwind pressure building. VIX below 20 indicates low fear environment.

🎯 TRADE PSYCHOLOGY & EXECUTION TIPS

✅ Pre-Trade Checklist:

Confirm SMA pullback on 4H chart before entry. Verify Kijun retest on Ichimoku indicator. Check QQQ alignment for correlation confirmation. Monitor DXY to avoid strong dollar days. Set alerts at all 3 entry layers for execution readiness.

✅ During Trade Management:

Take partial profit at 50% move up to secure gains. Move SL to breakeven after hitting first target. Trail stop every 50-pip move in your favor. Document your execution for journal review and performance tracking.

🔥 TRADE EXECUTION SUMMARY

Signal Type: Bullish Pullback Retest ✅ Confirmed

Entry Method: 3-Layer Limit Orders 🎯 Optimized for Best Fill Pricing

SL Level: $6,720.00 🛑 Defined and Placed Below Support

TP Level: $7,050.00 🎯 Defined at Resistance Confluence

Risk/Reward Ratio: 1:3+ 💰 Favorable Trade Structure

Best Tradeable Window: Next 48-72 Hours ⏰ Active Setup Zone

Good Luck, Traders! 🚀 Trade Smart. Trade Safe. Trade Often.

Remember: Your SL = Your Protection | Your TP = Your Goal | Your Risk = Your Responsibility

#SPX500 #SwingTrade #TechnicalAnalysis #TradingIdea #S&P500 #MarketAnalysis #TradeSetup #RiskManagement

S&P500 H1 | Bullish Bounce off Key SupportMomentum: Bullish

Price is currently above the ichimoku cloud.

Buy entry: 6,811.61

- Pullback support

- 50% Fib retracement

- 100% Fib projection

Stop Loss: 6,773.85

- Swing low support

Take Profit: 6,848.7

- Overlap resistance

Stratos Markets Limited (tradu.com/uk ):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 68% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Stratos Europe Ltd (tradu.com/eu ):

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 70% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

SPX since 1877 & 1896 & 1932-2021 & beyond. Waddup MM !!! 9 Years & 18 months. I choose the first largest three crashes as a base for cycles nothing more nothing less.

WADDUP MARKET MAKERS, CAN YOU SHARE THE PROBABILITIES OF YOUR ALGOS ;-) .

Blue adjusted for time = Action in June. Red and green = Action in July . It is like a

puzzle. Waddup MMs share the knowledge.

Congress Set to End Shutdown | SPX500 Holds Strong Above 6877SPX500 | Overview

U.S. Congress Poised to Get Back to Work

The U.S. government is on the verge of reopening, potentially restoring pay to federal workers and reviving key economic data releases that have been halted for weeks — leaving the Federal Reserve operating with limited visibility.

Renewed optimism over a resolution in Washington has boosted investor sentiment, supporting further upside in U.S. equities.

Technically:

The SPX500 has pushed higher and is now stabilized above the pivot level at 6877, indicating continuation of the bullish trend toward 6918 and 6941, with potential to reach new all-time highs (ATH) if momentum persists.

However, if the price closes a 1H candle below 6866, it would signal short-term weakness, leading to a bearish correction toward 6844 and 6814.

Pivot Line: 6877

Resistance: 6918 · 6941 · 6991

Support: 6845 · 6814 · 6797

Important Breakout - US500Hello traders,

The US500 failed to create a new lower low, and the price broke the lower high — confirming a change of character (ChoCH)!

So, I expect a bullish move ahead 🚀

🎯 Target: 6890.0

SPX – Recovery Momentum Gradually ReturningThe U.S. stock market is regaining its upward rhythm after a period of correction, as investor sentiment improves notably on hopes that the U.S. government shutdown will soon end .

At the same time, the U.S. Dollar Index has stalled and bond yields have slightly declined , creating favorable conditions for capital to return to large-cap equities.

On the 4H chart, SPX maintains a steady ascending channel structure , and the sharp rebound from the 6,800 zone signals that buyers are regaining control.

The current setup suggests the index could continue rising toward the 7,000 level, before a minor technical pullback — a healthy move to build momentum for the next leg higher toward the upper boundary of the channel.

With market sentiment turning increasingly positive , supported by bullish forecasts from major institutions like UBS (targeting S&P 500 at 7,500 by 2026), the short-term bullish bias for SPX remains intact.

As long as 6,800 holds firm, the uptrend structure stays valid, reflecting growing confidence that the U.S. market recovery cycle is far from over.

$SPX: DIP BUYNG IS THE RULE FOR NOW The strategy of buying on dips has proven effective once again, underscoring the current strength of the market. The 10- and 20-day moving averages are no longer relevant as support or resistance levels; instead, their slopes indicate the short-term trend. We will focus on the 20-day simple moving average (SMA), which remains in a positive slope. The key moving average for maintaining the upward trend is the 50-day SMA. The S&P 500 has easily recovered above the 0.618 Fibonacci retracement level and is just 73 points away from its all-time high; it appears quite feasible to set a new record.

However, there is a slight concern regarding the technology sector, which seems to be carrying more weight in the market. If the end of the shutdown is indeed approaching, the uncertainty will likely conclude with the release of economic data. Therefore, given this display of market strength, a wait-and-see approach may develop, which could lead to sideways trading—a situation that could be quite frustrating.

SPX What's it Gonna Be? Pop or Drop?Fellow SPX traders, followers and gamblers!

Do we have a bullish flag on the 30min or will it fake break the other way?

Pop or Drop be ready either way!

S&P500 New Bullish Leg confirmed targeting 7150.The S&P500 index (SPX) offered us, as we mentioned on our last analysis, an excellent buy opportunity last Friday as it hit its 1D MA50 (blue trend-line) and bounced.

Having broken and closed yesterday above its 4H MA50 (red trend-line), it has technically confirmed the new Bullish Leg of the 6-month Channel Up. Based on all previous ones, it should target the 2.5 Fibonacci extension at 7150, which remains our long-term Target for the end of the year.

Notice also how similar the 1D RSI patterns are of October and August. Steady rise is expected for November getting into December.

---

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

---

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Watch out—the current rebound could be a bull trap.Watch out—the current rebound could be a bull trap.

Technical analysis

1. US500 rebounded from the EMA50, with the price forming higher swings, and the multi-period EMAs signal an uptrend.

2. However, price has formed Bearish Divergence with RSI twice already (rarely does it occur more than three times), so this rebound may not be sustainable.

3. In terms of Elliott Wave, this rally might be the final sub-wave before a major correction—potentially an Ending Diagonal, which tends to be a ZigZag structure and often finishes with a throw-over before reversing.

4. If the index holds above 6770 and can make a new high, the upside may be limited, with resistance at the ascending trendline around 7000—near the 161.8% Fibonacci retracement—before a significant pullback begins.

5. Alternatively, if US500 fails to make a new high, it may correct toward 6510 as the first support.

Fundamental Analysis

6. S&P 500 valuations look extended, trading around 28–30x P/E versus a 17–25x long-run average range, while P/S near ~3.3–3.4x sits close to record highs—both materially above historical norms.

7. Inflation remains above target as core CPI is ~3% and sticky, leading to expectations that the Fed may not cut interest rates that much, which might not support risk assets as initially anticipated.

8. Berkshire Hathaway's record cash holdings reflect Warren Buffett's increased caution. He views the current market as expensive or uncertain, thus pausing major investments. This stance aligns with the Buffett Indicator surging to 217%-223%, a level he previously warned was "playing with fire," implying the market is significantly overvalued relative to the economy.

Analysis by: Krisada Yoonaisil, Financial Markets Strategist at Exness

S&P500 Positive sentiment from tech reboundOverview:

Wall Street rallied strongly yesterday, led by tech stocks. The NASDAQ gained +2.27%, and the Magnificent 7 surged +2.79%, with Nvidia (+5.79%) leading after its biggest jump since April. Broader gains were more moderate — the equal-weight S&P 500 rose +0.52%, and Russell 2000 +0.94% — showing the rally was concentrated in large-cap tech.

Drivers of Sentiment:

Tech rebound: Nvidia’s recovery and strong performance in other mega-caps fueled optimism.

Trade optimism: Trump said the US is “pretty close” to trade deals with India and Switzerland, potentially reducing tariffs.

Political progress: The US government funding deal advanced in the Senate, easing shutdown concerns.

Market Takeaway for Today:

S&P 500 likely to open steady to slightly higher, supported by risk-on momentum from tech.

Focus on whether the rally broadens beyond mega-caps — equal-weight S&P lagging suggests narrow leadership.

Short-term tone: Positive sentiment from tech rebound, trade deal hopes, and easing US political risk, but watch for consolidation after strong gains.

Key Support and Resistance Levels

Resistance Level 1: 6866

Resistance Level 2: 6889

Resistance Level 3: 6917

Support Level 1: 6763

Support Level 2: 6736

Support Level 3: 6700

This communication is for informational purposes only and should not be viewed as any form of recommendation as to a particular course of action or as investment advice. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Opinions, estimates and assumptions expressed herein are made as of the date of this communication and are subject to change without notice. This communication has been prepared based upon information, including market prices, data and other information, believed to be reliable; however, Trade Nation does not warrant its completeness or accuracy. All market prices and market data contained in or attached to this communication are indicative and subject to change without notice.