BHEL has a very strong order book (~₹ 1.96 trn) which gives solid revenue visibility.

CRISIL

+2

Bharat Heavy Electricals Limited

+2

FY 2024–25 saw record order inflows (~₹ 92,500 crore), indicating strong demand pipeline.

Bharat Heavy Electricals Limited

+1

Profit recovered: BHEL’s Q2 showed strong profit growth and margin improvement, which is boosting sentiment.

Business Standard

Capital structure: According to CRISIL, BHEL’s financial risk profile is improving with manageable debt.

CARE Ratings

Risks / Bear Case:

Operational issues: In some quarters (like Q1 FY26), the company reported widening losses, suggesting execution or cost problems.

Investing.com South Africa

Margin pressure: Despite order flow, expenses and cost control remain a concern.

Outlook Business

Long execution cycle: Many orders have long execution timelines (several years), which exposes BHEL to project risk and working capital stress.

CARE Ratings

Regulatory / tax risk: There could be headwinds if financial or operational assumptions (like working capital or project delivery) go wrong.

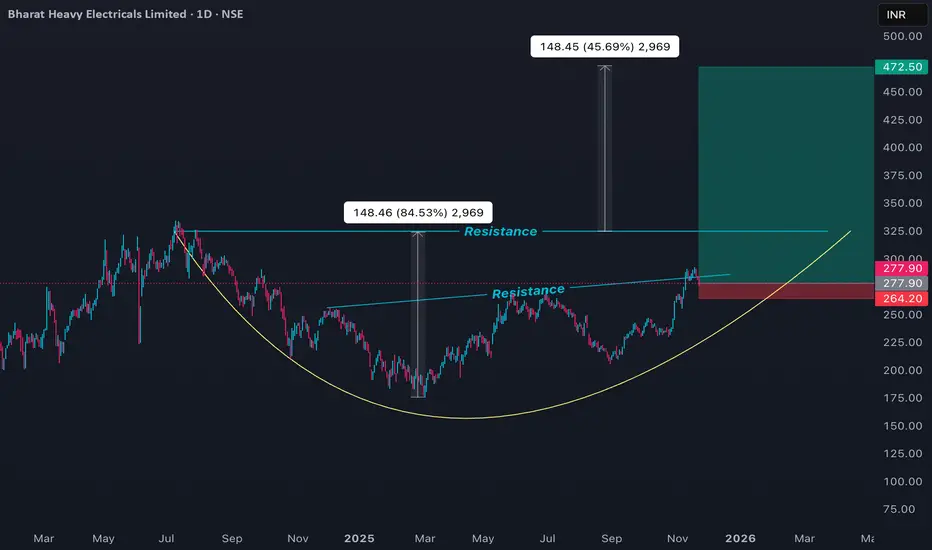

Price Outlook:

Short to medium term: The large order book could drive more consistent revenue and profit, making BHEL a turnaround / value recovery play.

Potential entry zone: If BHEL can sustain execution and improve margins, it’s a candidate for accumulation, especially on price weakness.

Catalyst watch: Execution on existing orders, quarterly profits, and working-capital improvements will be key to re-rating.

Conclusion:

BHEL is showing signs of a structural recovery: strong order flow plus improving execution could drive meaningful upside — but risks remain around margin volatility and project execution. It’s a balanced play: not a rapid growth bet, but a value-oriented infrastructure turnaround.

CRISIL

+2

Bharat Heavy Electricals Limited

+2

FY 2024–25 saw record order inflows (~₹ 92,500 crore), indicating strong demand pipeline.

Bharat Heavy Electricals Limited

+1

Profit recovered: BHEL’s Q2 showed strong profit growth and margin improvement, which is boosting sentiment.

Business Standard

Capital structure: According to CRISIL, BHEL’s financial risk profile is improving with manageable debt.

CARE Ratings

Risks / Bear Case:

Operational issues: In some quarters (like Q1 FY26), the company reported widening losses, suggesting execution or cost problems.

Investing.com South Africa

Margin pressure: Despite order flow, expenses and cost control remain a concern.

Outlook Business

Long execution cycle: Many orders have long execution timelines (several years), which exposes BHEL to project risk and working capital stress.

CARE Ratings

Regulatory / tax risk: There could be headwinds if financial or operational assumptions (like working capital or project delivery) go wrong.

Price Outlook:

Short to medium term: The large order book could drive more consistent revenue and profit, making BHEL a turnaround / value recovery play.

Potential entry zone: If BHEL can sustain execution and improve margins, it’s a candidate for accumulation, especially on price weakness.

Catalyst watch: Execution on existing orders, quarterly profits, and working-capital improvements will be key to re-rating.

Conclusion:

BHEL is showing signs of a structural recovery: strong order flow plus improving execution could drive meaningful upside — but risks remain around margin volatility and project execution. It’s a balanced play: not a rapid growth bet, but a value-oriented infrastructure turnaround.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.