Is $5T reasonable for NVDA?

• Mechanically, yes: The market only needs ~10% near-term appreciation from today’s levels to print $5T. That’s within one strong quarter or a guidance beat.

• Fundamentally, the math works if (a) FY26–27 revenue tracks the guide/Street trajectory (TTM already $165B with Q3 guide $54B), (b) non-GAAP GMs hover low-to-mid-70s, and (c) opex discipline holds. Under those, forward EPS path supports ~35× at $5T, a premium but not outlandish for a category-defining compute platform.

• Free-cash optionality: With ~$48B net cash and massive FCF, NVDA can keep funding buybacks (already $60B fresh authorization) and capacity, smoothing cycles.

________________________________________

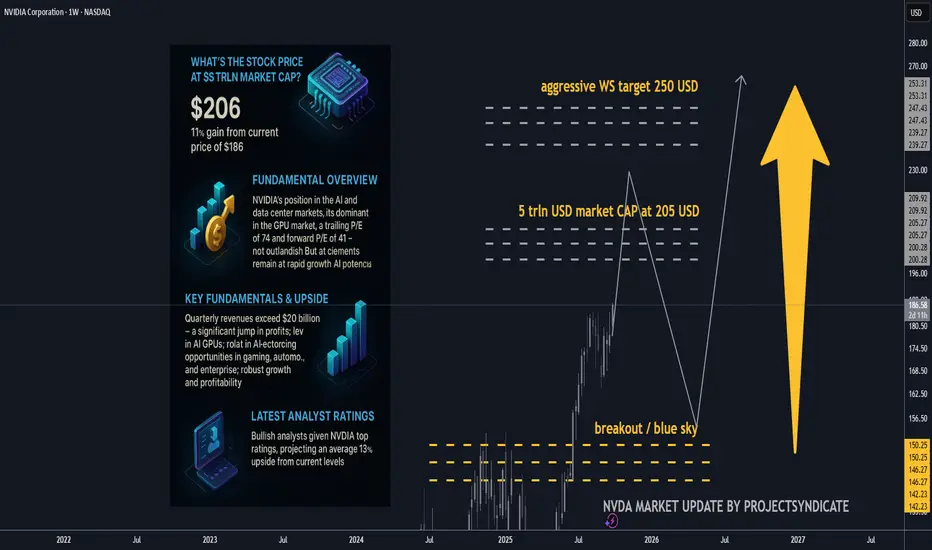

• Stock price at $5T market cap: ≈ $205.8 per share (on ~24.3B shares).

• Gain needed from $186.6: +$19.2 (~+10.3%).

The quick math (market cap ⇒ price)

• Shares outstanding (basic): ~24.3 B (as of Aug 22, 2025, per 10-Q).

• Stock @ $5T market cap: $5,000,000,000,000 ÷ 24.3B ≈ $205.8/share.

• From today’s price $186.6: needs +$19.2 or ~+10.3%.

That also implies P/E (TTM) at $5T of roughly ~56× (using TTM EPS ~3.68). Today’s trailing P/E is ~50–53× depending on feed.

________________________________________

Core fundamentals snapshot 🧩

Latest quarter (Q2 FY26, reported Aug 27, 2025)

• Revenue: $46.7B (+56% y/y; +6% q/q).

• Data Center revenue: $41.1B (+56% y/y).

• GAAP gross margin: 72.4%; non-GAAP 72.7%; Q3 guide ~73.3–73.5%.

• GAAP EPS: $1.08 (non-GAAP: $1.05; excl. $180M inventory release: $1.04).

TTM scale & profitability

• Revenue (TTM): ~$165.2B.

• Net income (TTM): ~$86.6B.

• Diluted EPS (TTM): ~$3.5–3.7.

• Cash & marketable securities: $56.8B; debt: ~$8.5–10.6B ⇒ net cash ≈ $48B.

Capital returns

• $24.3B returned in 1H FY26; new $60B buyback authorization (no expiration). Remaining buyback capacity ~$71B as of Aug 26.

________________________________________

Valuation read (today vs. $5T)

Using widely watched metrics:

• P/E (TTM): ~50–53× today; at $5T it rises to ~56× (assuming flat TTM EPS).

• Forward P/E: Street FY27 EPS ≈ $5.91 → ~31–33× today; ~35× at $5T — still below many AI hyper-growth narratives that trade at 40–50× forward when growth visibility is high.

• EV/EBITDA (TTM): EV ≈ market cap – net cash. Today EV ~$4.45T; EBITDA TTM ≈ $98–103B ⇒ EV/EBITDA ~43–45×; at $5T EV/EBITDA drifts to ~48–50×.

• P/S (TTM): ~27× today (at $4.5T) and ~30× at $5T on $165.2B TTM revenue.

• FCF yield: TTM FCF range $60.9–72.0B ⇒ ~1.35–1.60% today; ~1.22–1.44% at $5T.

Takeaway: $5T doesn’t require a heroic repricing — it’s ~10% above spot and implies ~35× forward earnings if consensus holds. That’s rich vs. the S&P (~22.5× forward) but arguably reasonable given NVDA’s growth, margins, and quasi-platform status in AI compute.

________________________________________

What must be true to justify $5T (and beyond) ✅

1. AI capex “supercycle” persists/expands. Citi now models $490B hyperscaler AI capex in 2026 (up from $420B) and trillions through 2029–30. A sustained 40–50% NVDA wallet share across compute+networking underwrites revenue momentum and margin sustainment.

2. Annual product cadence holds. Blackwell today → Rubin in 2026 with higher power & bandwidth, widening the perf gap vs. AMD MI450 — supports pricing power and mix.

3. Margins stay “mid-70s” non-GAAP. Company guides ~73.3–73.5% near term; sustaining 70%+ through transitions offsets any unit price compression.

4. Networking, software & systems scale. NVLink/Spectrum, NVL systems and CUDA/Enterprise subscriptions deepen the moat and smooth cyclicality; attach expands TAM (improves EV/EBITDA vs. pure-GPU lens).

5. China/export workarounds do not derail mix. Q2 had no H20 China sales; guidance and commentary frame this as manageable with non-China demand and limited H20 redirection.

________________________________________

A contrarian check (where the model could break) 🧨

• Power & grid bottlenecks. Even bulls (Citi) note AI buildouts imply tens of GW of incremental power; slippage in datacenter electrification can defer GPU racks, elongating deployments (and revenue recognition).

• Debt-funded AI spend. Rising share of AI DC capex is being levered (Oracle’s $18B bonds; neoclouds borrowing against NVDA GPUs). If credit windows tighten, orders could wobble.

• Customer consolidation & vertical ASICs. Hyperscalers iterating custom silicon could cap NVDA’s mix/price in some workloads; edge inference may fragment.

• China policy volatility. Export rules already forced product pivots; rebounds are uncertain and not fully in NVDA’s control.

• Multiple risk. At ~50× TTM and >40× EV/EBITDA, any growth decel (unit or pricing) can de-rate the multiple faster than earnings make up the gap.

Bottom line of the bear case: If AI capex normalizes faster (say +10–15% CAGR instead of +25–35%), forward EPS still grows, but the stock would likely need multiple compression (toward ~25–30× forward), making $5T less sticky near-term.

________________________________________

Street positioning (latest bullish calls) 📣

• KeyBanc: $250 (Overweight) — Rubin cycle deepens moat → ~+34% implied upside.

• Barclays: $240 (Overweight) — AI infra wave; higher multiple to 35×. ~+29% upside.

• Bank of America: $235 (Buy). ~+26% upside.

• Bernstein: $225 (Outperform). ~+21% upside.

• Citi: $210 (Buy) — reiterates annual cadence & rising AI capex.

• Morgan Stanley: $206–210 (Overweight). ~+11–13% upside; 33× CY25 EPS framework.

• Consensus: Avg 12-mo PT ~$211, ~+13% from here.

________________________________________

________________________________________

Extra color you can trade on 🎯

• Where bulls may be too conservative:

o Networking/NVLink attach could outgrow GPUs as Blackwell/Rubin systems standardize on NVIDIA fabric, defending blended margins longer.

o Software monetization (CUDA ecosystem, NIMs, enterprise inference toolchains) is still under-modeled in many sell-side DCFs.

• Where bulls may be too aggressive:

o China rebound timing & magnitude.

o Power/real-estate constraints delaying deployments into 2026.

o Credit-driven AI capex — watch for any signs of tightening in private credit / neocloud financing that uses GPUs as collateral.

________________________________________

________________________________________

Sources: NVIDIA IR & 10-Q; Yahoo Finance stats; StockAnalysis (TTM financials); company Q2 FY26 press release and CFO commentary; recent analyst notes from KeyBanc, Citi, Barclays, BofA, Morgan Stanley; financial media coverage (WSJ/FT).

• Mechanically, yes: The market only needs ~10% near-term appreciation from today’s levels to print $5T. That’s within one strong quarter or a guidance beat.

• Fundamentally, the math works if (a) FY26–27 revenue tracks the guide/Street trajectory (TTM already $165B with Q3 guide $54B), (b) non-GAAP GMs hover low-to-mid-70s, and (c) opex discipline holds. Under those, forward EPS path supports ~35× at $5T, a premium but not outlandish for a category-defining compute platform.

• Free-cash optionality: With ~$48B net cash and massive FCF, NVDA can keep funding buybacks (already $60B fresh authorization) and capacity, smoothing cycles.

________________________________________

• Stock price at $5T market cap: ≈ $205.8 per share (on ~24.3B shares).

• Gain needed from $186.6: +$19.2 (~+10.3%).

The quick math (market cap ⇒ price)

• Shares outstanding (basic): ~24.3 B (as of Aug 22, 2025, per 10-Q).

• Stock @ $5T market cap: $5,000,000,000,000 ÷ 24.3B ≈ $205.8/share.

• From today’s price $186.6: needs +$19.2 or ~+10.3%.

That also implies P/E (TTM) at $5T of roughly ~56× (using TTM EPS ~3.68). Today’s trailing P/E is ~50–53× depending on feed.

________________________________________

Core fundamentals snapshot 🧩

Latest quarter (Q2 FY26, reported Aug 27, 2025)

• Revenue: $46.7B (+56% y/y; +6% q/q).

• Data Center revenue: $41.1B (+56% y/y).

• GAAP gross margin: 72.4%; non-GAAP 72.7%; Q3 guide ~73.3–73.5%.

• GAAP EPS: $1.08 (non-GAAP: $1.05; excl. $180M inventory release: $1.04).

TTM scale & profitability

• Revenue (TTM): ~$165.2B.

• Net income (TTM): ~$86.6B.

• Diluted EPS (TTM): ~$3.5–3.7.

• Cash & marketable securities: $56.8B; debt: ~$8.5–10.6B ⇒ net cash ≈ $48B.

Capital returns

• $24.3B returned in 1H FY26; new $60B buyback authorization (no expiration). Remaining buyback capacity ~$71B as of Aug 26.

________________________________________

Valuation read (today vs. $5T)

Using widely watched metrics:

• P/E (TTM): ~50–53× today; at $5T it rises to ~56× (assuming flat TTM EPS).

• Forward P/E: Street FY27 EPS ≈ $5.91 → ~31–33× today; ~35× at $5T — still below many AI hyper-growth narratives that trade at 40–50× forward when growth visibility is high.

• EV/EBITDA (TTM): EV ≈ market cap – net cash. Today EV ~$4.45T; EBITDA TTM ≈ $98–103B ⇒ EV/EBITDA ~43–45×; at $5T EV/EBITDA drifts to ~48–50×.

• P/S (TTM): ~27× today (at $4.5T) and ~30× at $5T on $165.2B TTM revenue.

• FCF yield: TTM FCF range $60.9–72.0B ⇒ ~1.35–1.60% today; ~1.22–1.44% at $5T.

Takeaway: $5T doesn’t require a heroic repricing — it’s ~10% above spot and implies ~35× forward earnings if consensus holds. That’s rich vs. the S&P (~22.5× forward) but arguably reasonable given NVDA’s growth, margins, and quasi-platform status in AI compute.

________________________________________

What must be true to justify $5T (and beyond) ✅

1. AI capex “supercycle” persists/expands. Citi now models $490B hyperscaler AI capex in 2026 (up from $420B) and trillions through 2029–30. A sustained 40–50% NVDA wallet share across compute+networking underwrites revenue momentum and margin sustainment.

2. Annual product cadence holds. Blackwell today → Rubin in 2026 with higher power & bandwidth, widening the perf gap vs. AMD MI450 — supports pricing power and mix.

3. Margins stay “mid-70s” non-GAAP. Company guides ~73.3–73.5% near term; sustaining 70%+ through transitions offsets any unit price compression.

4. Networking, software & systems scale. NVLink/Spectrum, NVL systems and CUDA/Enterprise subscriptions deepen the moat and smooth cyclicality; attach expands TAM (improves EV/EBITDA vs. pure-GPU lens).

5. China/export workarounds do not derail mix. Q2 had no H20 China sales; guidance and commentary frame this as manageable with non-China demand and limited H20 redirection.

________________________________________

A contrarian check (where the model could break) 🧨

• Power & grid bottlenecks. Even bulls (Citi) note AI buildouts imply tens of GW of incremental power; slippage in datacenter electrification can defer GPU racks, elongating deployments (and revenue recognition).

• Debt-funded AI spend. Rising share of AI DC capex is being levered (Oracle’s $18B bonds; neoclouds borrowing against NVDA GPUs). If credit windows tighten, orders could wobble.

• Customer consolidation & vertical ASICs. Hyperscalers iterating custom silicon could cap NVDA’s mix/price in some workloads; edge inference may fragment.

• China policy volatility. Export rules already forced product pivots; rebounds are uncertain and not fully in NVDA’s control.

• Multiple risk. At ~50× TTM and >40× EV/EBITDA, any growth decel (unit or pricing) can de-rate the multiple faster than earnings make up the gap.

Bottom line of the bear case: If AI capex normalizes faster (say +10–15% CAGR instead of +25–35%), forward EPS still grows, but the stock would likely need multiple compression (toward ~25–30× forward), making $5T less sticky near-term.

________________________________________

Street positioning (latest bullish calls) 📣

• KeyBanc: $250 (Overweight) — Rubin cycle deepens moat → ~+34% implied upside.

• Barclays: $240 (Overweight) — AI infra wave; higher multiple to 35×. ~+29% upside.

• Bank of America: $235 (Buy). ~+26% upside.

• Bernstein: $225 (Outperform). ~+21% upside.

• Citi: $210 (Buy) — reiterates annual cadence & rising AI capex.

• Morgan Stanley: $206–210 (Overweight). ~+11–13% upside; 33× CY25 EPS framework.

• Consensus: Avg 12-mo PT ~$211, ~+13% from here.

________________________________________

________________________________________

Extra color you can trade on 🎯

• Where bulls may be too conservative:

o Networking/NVLink attach could outgrow GPUs as Blackwell/Rubin systems standardize on NVIDIA fabric, defending blended margins longer.

o Software monetization (CUDA ecosystem, NIMs, enterprise inference toolchains) is still under-modeled in many sell-side DCFs.

• Where bulls may be too aggressive:

o China rebound timing & magnitude.

o Power/real-estate constraints delaying deployments into 2026.

o Credit-driven AI capex — watch for any signs of tightening in private credit / neocloud financing that uses GPUs as collateral.

________________________________________

________________________________________

Sources: NVIDIA IR & 10-Q; Yahoo Finance stats; StockAnalysis (TTM financials); company Q2 FY26 press release and CFO commentary; recent analyst notes from KeyBanc, Citi, Barclays, BofA, Morgan Stanley; financial media coverage (WSJ/FT).

Note

🎁Please hit the like button and🎁Leave a comment to support our team!

Note

short summary of the detailed overview:🚀 NVDA Stock: Path to $5 Trillion Market Cap

🖥️ 1. Current Market Cap: $4.5T — trading at ~$186/share.

📈 2. $5T Target Price: ~$206/share → needs ~+10% gain.

💰 3. Earnings Power: TTM EPS ~$3.7; Forward EPS FY27 ~$5.9.

🔢 4. Valuation Check: P/E (TTM) ~50× today → ~56× at $5T; Forward P/E ~31–33× today → ~35× at $5T.

💹 5. Revenue Momentum: TTM revenue ~$165B; Q2 FY26 revenue $46.7B (+56% y/y).

💎 6. Profitability: Non-GAAP gross margins ~73%; net income TTM ~$86B.

💵 7. Capital Returns: $24B returned in 1H FY26; $60B fresh buyback authorized, ~$71B capacity left.

⚡ 8. Growth Drivers: AI data center capex supercycle, Rubin (2026) GPU launch, NVLink/Spectrum networking, CUDA ecosystem.

🛑 9. Risks: Power/grid bottlenecks, debt-funded AI spend, custom silicon by hyperscalers, export restrictions.

📊 10. Analyst Consensus: Avg PT ~$211 (+13% upside). KeyBanc tops at $250 (+34% upside).

Trade active

taplink.cc/black001

🔱Syndicate Black MT4/MT5

⚡️Gold/FX Auto-Trading bot

🔱100%/week max DD <10%

📕verified 500%+ gains

🏧GOLD EA target 100%+ gains/week

🚀supercharge your trading

💎75% win rate gold signals

t.me/syndicategold001

🔱Syndicate Black MT4/MT5

⚡️Gold/FX Auto-Trading bot

🔱100%/week max DD <10%

📕verified 500%+ gains

🏧GOLD EA target 100%+ gains/week

🚀supercharge your trading

💎75% win rate gold signals

t.me/syndicategold001

Related publications

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

taplink.cc/black001

🔱Syndicate Black MT4/MT5

⚡️Gold/FX Auto-Trading bot

🔱100%/week max DD <10%

📕verified 500%+ gains

🏧GOLD EA target 100%+ gains/week

🚀supercharge your trading

💎75% win rate gold signals

t.me/syndicategold001

🔱Syndicate Black MT4/MT5

⚡️Gold/FX Auto-Trading bot

🔱100%/week max DD <10%

📕verified 500%+ gains

🏧GOLD EA target 100%+ gains/week

🚀supercharge your trading

💎75% win rate gold signals

t.me/syndicategold001

Related publications

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.