The Earnings Playbook: How to Navigate Each Quarter Like a ProTraders are in the heat of the earnings season and euphoria is sweeping every corner of the market.

The charts twitch, traders stop talking about the Fed for five minutes ( not this week, though ), and online forums turn into a parade of watch-me-trade sessions.

It’s that glorious stretch when companies pop open the books and reveal what’s really been happening behind the scenes.

For professional investors, it’s data heaven. For retail traders, it’s emotional cardio. Stocks can rise 20% on a single upbeat forecast — or plummet before your coffee cools. The trick isn’t just to survive it. It’s to navigate it like a pro.

💼 Know the Seasons (and the Mood Swings)

Earnings season comes four times a year — January, April, July, and October — and each has its own flavor.

Q1 (April): That’s the hangover quarter. Holiday sales meet new-year cost cuts. Traders recalibrate expectations and reality collides with ambition.

Q2 (July): The mid-year checkup. CEOs brag about “momentum,” analysts start sharpening their red pencils. Markets get twitchy.

Q3 (October): The credibility test. Guidance revisions and cautious tones dominate. If the year’s been good, this is where the victory laps start.

Q4 (January): The scoreboard reveal. Everyone tallies their annual wins and losses, and traders begin to bet on who carries the next year’s momentum.

Each cycle has a similar rhythm: hype, reaction, digestion, and speculation. Think of it like a four-act play.

📊 Mind the Gap

One thing to keep in mind whenever you find yourself in the earnings bonanza: the actual numbers matter less than the narrative. ( Looking at you, Oracle NYSE:ORCL )

A company can beat on revenue, miss on profit, and still rally — if the CEO sells a compelling story about the next quarter. Conversely, it can post record earnings and tank because analysts wanted even more.

The pros know to look beyond the headline EPS. They dig into guidance, margins, and segment performance. Is revenue growing because of genuine demand, or just creative accounting? Are margins improving, or did the company quietly cut R&D?

Markets don’t price what’s happened — they price what’s next. That’s especially true for growth stocks like t echnology companies .

🎯 Don’t Chase the Knee-Jerk

Every earnings season has its share of instant overreactions — the “up 10% at open, down 8% by lunch” kind of chaos. That’s when seasoned traders sit back and let volatility do the heavy lifting.

Smart money avoids buying into the frenzy or shorting into despair. Instead, they wait for the second move — when dust settles, algorithms calm down, and humans return to their desks.

🧠 Build Your Own Playbook

To trade earnings season like a pro, you need a plan. Here’s how the veterans prep:

Start early. Check the earnings calendar and mark high-impact names in your portfolio or watchlist.

Study the setup. Look at how the stock’s performed heading into earnings. A big pre-report rally can mean expectations are too high.

Focus on guidance. Earnings beats are old news — future commentary moves markets.

Use position sizing. Never bet the farm on one report. Even the best setups can go sideways.

Don’t forget the macro. Rate cuts, inflation prints, or a stray tweet from the US President can overshadow the best earnings beat.

🕹️ The Big Picture: Earnings as Market GPS

Earnings season is the market’s health check because it tells you which sectors are thriving, which are limping, and how CEOs feel about the future (watch the language: “headwinds” and “volatility” are polite ways of saying buckle up).

Taken together, earnings trends shape the broader narrative — from interest rate expectations to sector rotations. In other words, earnings season is where short-term trading meets long-term investing.

Now go and prepare for the next batch of earnings — Big Tech is on deck this week with Apple NASDAQ:AAPL and Amazon NASDAQ:AMZN reporting today.

Off to you : What’s your strategy this earnings season? Buying the hype or waiting to buy the dip? Share your thoughts in the comments!

Community ideas

Trading Bots: The Future of the Markets?Let’s be real, the idea of a trading bot sounds like the holy grail.

Set it up, go to bed, and wake up to profit.

If only it were that simple.

Most bots don’t fail because of bad code, they fail because of bad logic.

A bot is only as good as the rules you give it.

What a Trading Bot Actually Does

A bot doesn’t predict the market, it reacts to it.

It follows a defined strategy:

Buy when X happens, sell when Y is confirmed, cut losses if price breaks Z.

That’s all.

No fear. No greed. No “maybe I’ll wait for one more candle.”

The power of bots isn’t in magic,it’s in consistency.

They do what most traders can’t: follow the plan exactly as written, every single time.

Why Most Bots Fail

The truth?

Most traders plug in random bots they find online without understanding what’s inside.

They win a few trades, feel invincible… and then lose it all when volatility spikes.

The reason isn’t the bot, it’s the lack of testing and understanding.

If you don’t know your system’s weak spots, you’ll eventually find them the hard way.

That’s why backtesting matters.

Backtesting: Your First Line of Defense

Backtesting shows how your logic performs over hundreds of trades — across bull, bear, and sideways markets.

It reveals your system’s strengths, weaknesses, and drawdowns before you risk a dollar.

A good backtest should tell you:

Your average win rate and risk/reward ratio.

How your system handles volatility.

How often it hits consecutive losses.

Whether your edge actually holds over time.

If your bot looks good in backtests and performs similarly in live conditions — you’re onto something real.

*Example of one of our indicator

How Bots Can Enhance Your Trading

You don’t have to hand everything over to automation.

In fact, many great traders use bots to handle the mechanical side, while keeping the decision-making human.

Here are a few examples:

Trade Execution: Let the bot enter trades instantly after your setup triggers.

Risk Management: Bots can move stop-losses, take partial profits, or scale positions automatically.

Signal Filtering: Use automation to scan hundreds of pairs and alert you only when conditions align.

Backtesting Sandbox: Test new ideas safely with data before deploying them live.

Bots don’t replace traders, they multiply efficiency.

They free your mind from execution so you can focus on refinement.

The Real Lesson

A trading bot isn’t a shortcut.

It’s a mirror, it reflects your discipline, your rules, and your logic.

If your plan is solid, a bot will make it unstoppable.

If your plan is weak, it’ll just lose money faster.

Automation doesn’t fix bad habits, it exposes them.

So learn the logic, test it hard, then let the system do what humans struggle with most: follow the plan.

How to enter a successful futures tradeDrop everything and let me show you how to enter a successful long position with the lowest possible risk.

You need to understand that the market maker usually acts against us at major support areas on the chart — like the 100 EMA, 0.618 Fibonacci level, or a trendline.

To make this clearer, let’s take TAO as an example and I’ll explain why.

TAO has strong momentum and a large market cap,

so don’t apply what I’m about to say to meme coins, for example.

Now let’s go step by step on how to enter a futures position after choosing the coin 👇

1. First, wait for a bullish pattern to form — like a triangle — and for the coin to break it upwards with increasing long momentum.

2. The price will then retest the trendline, encouraging people to enter with larger positions, and those who missed the first breakout will likely place buy orders at the retest zone.

3. Then, the market surprises them — it drops back inside the triangle, giving a small bounce at the lower side.

4. But it doesn’t stop there — it continues dropping, breaking below the triangle and closing below the 100 EMA on the 4-hour chart.

This makes you panic and close your long position.

Others start entering shorts thinking it’s a real breakdown.

5. That’s when the market reverses sharply upward,

trapping short traders in losses,

while long traders who exited too early also lose.

In the end, only those who placed buy orders slightly below the strong support level (not directly on it, like under the 100 EMA) — and of course the market maker — end up winning.

So basically, the long traders lose, the short traders lose,

and only a small percentage of smart traders and the market maker win.

Small things to pay attention to 👇

-Your entry point should be slightly below the support, not too far below it.

(That support could be the 100 EMA, below the triangle pattern, or the 0.618 Fibonacci level, as we mentioned.)

-Don’t use high leverage — x5 should be your maximum.

-Place your stop loss 5% below your entry zone,

which equals about 25% loss if you’re using x5 leverage.

And with that, you’ve got yourself a long setup with over a 90% success rate,

and you can apply the same logic in reverse when taking a short position.

Best Regards:

Ceciliones🎯

Halloween Special: The Risk “Treats” That Keep You Alive!🧠 If October has a lesson, it’s this: fear is useful, panic is fatal. Great traders don’t fight the monsters; they contain them.

Here’s my Halloween mindset & risk playbook:

🧪 Keep your “lifeline” small: Risk a fixed 1% per trade until your balance moves ±10%, then recalibrate. This makes loss streaks survivable and hot streaks meaningful.

⏰ Set a nightly curfew: a max daily loss (e.g., 3R or 3%). Hit it? Close the platform. No “one last trade.” Curfews save accounts.

🛑 Define your invalidation before you enter: If that level prints, you’re out, no arguments, no “maybe it comes back.” Plans beat feelings.

🎯 Hunt asymmetry: If you can’t see at least 2R cleanly (preferably 3R), pass. You don’t need more trades; you need better trades.

🧟 Kill the zombie trade: the one you’re babysitting, nudging stops, praying. If you’re managing hope more than risk, exit and reset.

🧘 Protect your mind equity: Two back-to-back losses? Take a 20-minute break. After a big win? Journal before you click again. Calmness compounds.

📜 Make a ritual: pre-trade checklist → position size → entry → stop → targets → log. Rituals turn uncertainty into routine, and routine into consistency.

What’s your #1 rule that keeps the “revenge-trading demon” out of your account❓

⚠️ Disclaimer: This is not financial advice. Always do your own research and manage risk properly.

📚 Stick to your trading plan regarding entries, risk, and management.

Good luck!

All Strategies Are Good; If Managed Properly!

~Richard Nasr

VBL Vbl is breaks this trend line , target is high ,

Quarterly results, yearly result increasing, revenue,PAT increasing, new partnership with carlsberg in south africa , p a potential multibagger

The Billy Big Balls MomentA trader reached out to me by direct message here on Trading View highlighting a challenge that many of us face from time to time. We’re talking about self sabotage. That moment you know what to do - but do something entirely different and get a result that frustrates the **** out of you.

Follow along, I hope this helps.

BUT FIRST

NOTE – This is a post on mindset and emotion. It’s not a trade idea or strategy designed to make you money. My intention is to help you preserve your capital, focus, and composure so you can trade your own system with calm and confidence.

Here's a scenario you might be familiar with...

You nail a sequence of trades.

Precision. Flow. Everything lines up.

And then something flips.

You start pushing harder, sizing up, breaking your own rules.

A few minutes later, you’re staring at a screen wondering,

“What the hell just happened?”

It’s not lack of discipline nor is it a technical problem.

You have an emotional pattern that hasn’t been mapped out yet.

This pattern has roots into your subconscious and it’s sabotaging your efforts.

WHATS REALLY HAPPENING AND WHERE DOES THE DRIVER REALLY COME FROM

When you start winning, your brain gets flooded with dopamine , the chemical of reward and anticipation.

If your nervous system has ever learned that success leads to loss, losing control, losing safety, losing connection it quietly associates “winning” with risk .

The mind says, “Let’s keep this going.” Deeper down though is the silent warning … “This isn’t safe.”

Doesn’t sound logical right? It’s not. It’s emotional. Deeply embedded in your psyche and activated whenever the mind feels that familiar feeling again.

The mind wants to go forward - the body wants to intervene. And so you get an internal split. A moment of pressure that your mind just has to resolve. And the fastest way the subconscious knows to relieve that pressure… is to end the win.

So you do something impulsive, not because you want to fail,

but because deep down, you're trying to protect yourself or believe or not, you might be even trying to punish yourself.

Weird stuff happens in the subconscious.

That’s why the sabotage happens right after a run of success.

It’s not logic breaking down.

It’s the mind trying to restore an emotional equilibrium.

HOW TO CATCH IT BEFORE IT HAPPENS

Listen. The moment you size up impulsively is not random.

It’s a repeatable signal that your emotional system has been triggered.

You can’t fix what you can’t see - so start tracking it.

1. Notice your signature cue.

For some, it’s tension in the chest or a fidgety feeling of restlessness.

For others, it’s the need to “just check one more chart.”

For you it might be something else. Pay attention and start to become aware of what comes up for you.

2. Map the pattern

Keep a short log : what happens right before you go rogue?

Notice the time of day, physical tension, thoughts.

You are looking for a repeatable sequence.

3. Identify your threshold

There’s always a tipping point where clarity narrows: your breath shortens, attention tunnels or you start fantasising about bigger gains.

That’s your signal.

4. Interrupt the pattern and create a recovery plan (as you notice the cues)

Physically step away from the desk.

Exhale through the mouth long, slow, 6 seconds.

Let your eyes rest on something still . This shifts the nervous system out of fight-or-flight and back into focus.

This isn’t about controlling emotion.

Its about expanding your capacity so emotion doesn't control you.

Next time you’re on a hot streak, notice where focus ends and thrill begins.

That’s the edge that makes or breaks the run.

Why Your Next Trade Means Nothing

🧠 The Notebook Process #2 — Understanding the True Nature of Trading.

Some laws govern everything we do, and trading is no exception, even if it often feels like pure chaos.

Every tick looks random. Every trade feels unique. Yet beneath that noise, a hidden law quietly shapes your results. It’s one of the cornerstones of statistics, and it rules every trading account on Earth: The Central Limit Theorem.

Don’t worry, no math coming your way: just an intuitive truth you can plug directly into your trading mindset.

📖 The Nature of Trading.

Your true profitability, your average win or loss, only begins to emerge and, more importantly, stabilize after a large number of trades.

That’s it. That’s the law.

A single trade? Meaningless. Ten trades? Still noise.

Hundreds of trades? That’s where the truth starts to show. What you see after enough repetitions isn’t randomness anymore: it’s your edge revealing itself.

That’s the Law of Large Numbers and the Central Limit Theorem in motion: pure science.

☑️ What This Means for Traders.

Your system’s real strength, its expectancy, only appears through repetition.

A handful of trades? Still luck. Pure variance, random ups and downs that mean nothing.

A few hundred? Now you’re seeing skill: the signal rising above the noise. In plain English:

“A trading journey can only be evaluated after a large number of trades. That’s why your process matters more than your last result, no matter how good or bad it looked.”

And that’s exactly what The Notebook Process #1 was about: 👉 Evaluate in blocks, not single trades.

💸 Let’s Put the Law to Work:

1️⃣ Take your trading record and compute: Average win, Average loss, and Win rate.

2️⃣ Calculate your expectancy using this simple formula:

(Avg Win × Win Rate) – (Avg Loss × (1 – Win Rate))

3️⃣ That number tells you how much you make (or lose) per trade on average, and more importantly, what you can expect to make in the future.

If it’s positive, you’re trading with an edge. Keep going: reproducibility is what makes it stable.

If it’s negative, stop immediately. The bleeding won’t stop until the math changes.

That’s it. Pure math applied to trading: and believe me, you don’t want to fight this law.

🌍 The Gravity of Trading.

The difference between a trader who understands and one who only tries isn’t talent, it’s focus.

Focus on expectancy, not the win rate, not the reward to risk ratio.

It might seem basic, but so is gravity, and like gravity, it governs you whether you believe in it or not.

Fair Value Gaps: The Market Secret You Shouldn’t IgnoreEver scrolled through a chart and spotted a weird empty space in the candles — like the market just skipped a beat? That’s a Fair Value Gap (FVG). It’s one of those subtle price imbalances smart traders love to hunt for. Understanding how these gaps form and how price reacts around them can seriously level up your chart-reading game.

What Is a Fair Value Gap in Trading?

A Fair Value Gap happens when there’s a sudden surge in buying or selling pressure that causes price to move so fast, it doesn’t fully balance out between buyers and sellers. In simple terms, it’s an imbalance — a zone where the market skipped over potential orders.

When you hear traders talking about FVG in trading, they’re referring to those little pockets of unfilled liquidity left behind during strong moves.

So, what is FVG in trading, and why does it matter? Because price often comes back to those areas later to “rebalance” — filling the gap before continuing in the original direction. That’s the core logic behind Fair Value Gap trading.

Bullish and Bearish FVGs

There are two main types of Fair Value Gaps — bullish and bearish:

Bullish Fair Value Gap (bullish FVG): Forms during a strong upward move, when aggressive buyers push price higher, leaving a void below. Price might later dip back into that zone before continuing upward.

Bearish Fair Value Gap (bearish FVG): Forms in a sell-off, when sellers dominate and the market drops quickly, skipping over potential buy orders. Later, price often retraces upward to “fill” that gap.

Both can act as magnets for liquidity — areas where smart money likes to re-enter the market.

Fair Value Gap Example

Let’s say Bitcoin jumps from $110,000 to $120,000 in a single bullish candle, with almost no trading in between. That sudden move leaves a Fair Value Gap — the zone between the candle’s high and low where little to no trading took place.

If the market later pulls back to that range and finds support before bouncing, you’ve just witnessed a textbook Fair Value Gap example in action.

Using a Fair Value Gap Indicator

You can spot these zones manually by looking for three-candle structures — one candle that “leaves the gap” and two surrounding it that don’t overlap. But if you prefer automation, you can use a Fair Value Gap indicators:

Fair Value Gap Trading Strategies

Fair Value Gap trading isn’t about chasing price — it’s about waiting for the market to come back to you. Within Smart Money Concepts, traders often combine FVGs with CHoCH (Change of Character) to confirm a potential shift in structure before entering.

A common approach is to mark recent FVGs, identify the broader trend, and wait for price to revisit a gap in line with that trend.

In a bullish trend , traders look for bullish FVGs below current price as potential demand zones — ideally after a CHoCH confirms that buyers are stepping back in.

In a bearish trend , they watch for bearish FVGs above current price as potential supply zones, again validated by a CHoCH showing a shift in control.

Still, it’s important to remember — these setups are not guarantees. The market doesn’t owe you a fill. Use FVGs and CHoCH as part of the Smart Money framework, not as standalone signals. Always manage risk and make your own trading decisions based on your personal strategy and comfort level.

Final Thoughts

So, what is a Fair Value Gap really? It’s not magic — just the market showing where it moved too fast. Learning to read Fair Value Gaps gives you insight into liquidity, momentum, and potential reversals. Whether you use a Fair Value Gap indicator or mark them by hand, mastering FVG in trading can give you a serious edge in spotting high-probability zones.

Just keep in mind — no indicator or setup replaces good judgment.

Observe, adapt, and let the charts speak for themselves.

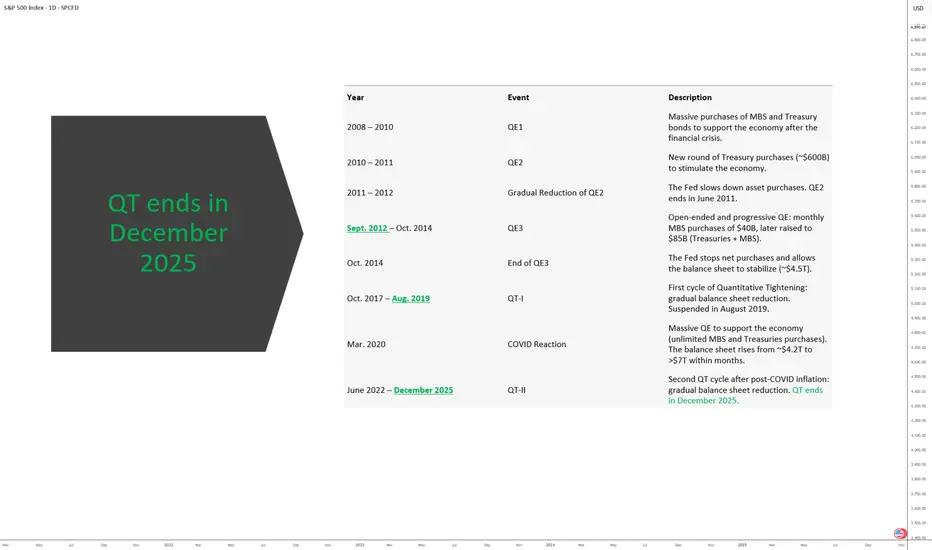

Fed Overview: The Good and the Not So GoodDriven by an euphoric phase, the S&P 500 has approached 7,000 points, nearing its 2000 valuation record, with six consecutive months of gains without retracement.

The key question for investors is now clear: has the Federal Reserve provided enough justification for this confidence, or does Jerome Powell’s caution mark the beginning of the end of this euphoric phase?

1) A Fed slowing the pace without complacency

On Wednesday, October 29, the Fed announced another 25-basis-point rate cut, bringing the federal funds rate into the 3.75%–4.00% range. This is the second consecutive reduction, aimed at countering the labor market slowdown.

However, the FOMC vote revealed strong internal divisions: one member wanted a deeper cut, another preferred no change. This reflects the delicate balance between supporting employment and avoiding renewed inflationary pressure.

Another key signal: the Fed decided to pause its balance sheet reduction (quantitative tightening) starting December 1st, in order to preserve financial system liquidity, as credit markets show early signs of stress. Powell clarified that this pause does not imply a lasting return to an expansionary stance.

Finally, Powell cooled expectations for another rate cut in December, stating that “nothing is guaranteed.” Money markets now price roughly a 70% chance of a hold in December, down from nearly 90% odds of a cut before the meeting.

2) Between monetary realism and market excess

The Fed is not ruling out further easing, but it refuses to fuel a bullish rally in the S&P 500 that is now considered excessive relative to fundamentals.

Current valuations rely heavily on expectations of continued rate cuts. If that narrative weakens, the likelihood of a technical correction in the S&P 500 rises.

At this stage, however, the index has not yet signaled a reversal.

DISCLAIMER:

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only. The presented idea (including market commentary, market data and observations) is not a work product of any research department of Swissquote or its affiliates. This material is intended to highlight market action and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is advisable to seek professional advice from licensed advisor before making any financial decisions.

This content is not intended to manipulate the market or encourage any specific financial behavior.

Swissquote makes no representation or warranty as to the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The views expressed are those of the consultant and are provided for educational purposes only. Any information provided relating to a product or market should not be construed as recommending an investment strategy or transaction. Past performance is not a guarantee of future results.

Swissquote and its employees and representatives shall in no event be held liable for any damages or losses arising directly or indirectly from decisions made on the basis of this content.

The use of any third-party brands or trademarks is for information only and does not imply endorsement by Swissquote, or that the trademark owner has authorised Swissquote to promote its products or services.

Swissquote is the marketing brand for the activities of Swissquote Bank Ltd (Switzerland) regulated by FINMA, Swissquote Capital Markets Limited regulated by CySEC (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the CSSF, Swissquote Ltd (UK) regulated by the FCA, Swissquote Financial Services (Malta) Ltd regulated by the Malta Financial Services Authority, Swissquote MEA Ltd. (UAE) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) licensed by the Hong Kong Securities and Futures Commission (SFC) and Swissquote South Africa (Pty) Ltd supervised by the FSCA.

Products and services of Swissquote are only intended for those permitted to receive them under local law.

All investments carry a degree of risk. The risk of loss in trading or holding financial instruments can be substantial. The value of financial instruments, including but not limited to stocks, bonds, cryptocurrencies, and other assets, can fluctuate both upwards and downwards. There is a significant risk of financial loss when buying, selling, holding, staking, or investing in these instruments. SQBE makes no recommendations regarding any specific investment, transaction, or the use of any particular investment strategy.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The vast majority of retail client accounts suffer capital losses when trading in CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital Assets are unregulated in most countries and consumer protection rules may not apply. As highly volatile speculative investments, Digital Assets are not suitable for investors without a high-risk tolerance. Make sure you understand each Digital Asset before you trade.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainties.

The use of Internet-based systems can involve high risks, including, but not limited to, fraud, cyber-attacks, network and communication failures, as well as identity theft and phishing attacks related to crypto-assets.

Origins of Modern Trade Wars in the World MarketIntroduction

The term trade war refers to an economic conflict between nations characterized by the imposition of tariffs or other trade barriers against each other. In essence, it is a battle for economic dominance fought through policy, not arms. While trade wars have existed since the rise of mercantilism in the 16th century, the modern trade war is a more complex phenomenon, deeply rooted in globalization, technological advancement, and national security concerns.

In today’s interconnected world, trade wars affect not just the warring nations but also global supply chains, financial markets, and consumer prices. The origins of modern trade wars can be traced to a combination of historical protectionism, geopolitical rivalry, and the changing structure of the global economy. This essay explores the evolution of trade wars, their causes, major examples, and the underlying forces shaping them in the 21st century.

Historical Background: From Protectionism to Globalization

Trade conflicts have long been tools of economic strategy. In the early centuries of global commerce, nations viewed trade surpluses as a measure of power. The 17th and 18th centuries saw the rise of mercantilism, where colonial powers such as Britain, France, and Spain imposed trade barriers to protect their domestic industries and accumulate wealth.

In the 19th century, industrial revolutions and colonial expansion spread free trade ideas, most notably through the British-led global trade system. However, the Great Depression of the 1930s reversed this progress. The U.S. Smoot-Hawley Tariff Act (1930), which raised tariffs on thousands of goods, triggered a global retaliatory cycle, deepening the depression.

After World War II, world leaders sought to prevent such destructive economic nationalism. They created institutions like the General Agreement on Tariffs and Trade (GATT) in 1947, which later evolved into the World Trade Organization (WTO) in 1995. These institutions aimed to promote global trade liberalization, reducing tariffs and establishing dispute resolution mechanisms.

Yet, even as globalization accelerated, protectionist instincts never disappeared. By the early 21st century, trade wars had transformed from simple tariff conflicts into strategic economic weapons, targeting technology, security, and intellectual property.

The Rise of the Modern Trade War

Modern trade wars differ from historical ones in both scale and motivation. They are not merely about tariffs or market access — they reflect deeper struggles over technological supremacy, economic sovereignty, and geopolitical power.

The post-Cold War world initially saw unprecedented economic cooperation. The 1990s and early 2000s were marked by open markets, rapid global trade growth, and the rise of multinational corporations. Countries like China and India emerged as manufacturing powerhouses, while the U.S. and Europe focused on innovation and services.

However, the same globalization that integrated economies also created vulnerabilities. Wealth inequality widened, industrial jobs in developed economies disappeared, and dependency on foreign supply chains increased. These developments laid the groundwork for nationalist economic movements and the resurgence of trade conflicts.

Key Triggers of Modern Trade Wars

1. Globalization’s Backlash

Globalization, once hailed as a force for prosperity, became politically controversial. Many Western workers felt displaced by cheaper imports and outsourcing. Factories in the U.S. and Europe shut down as companies moved production to low-cost countries like China and Vietnam. This economic discontent fueled protectionist policies, with leaders promising to “bring back jobs” and “protect national industries.”

2. The U.S.–China Rivalry

No relationship defines the modern trade war era more than the rivalry between the United States and China. For decades, the U.S. supported China’s integration into the world economy, hoping economic liberalization would lead to political openness. However, as China’s technological and military strength grew, Washington began viewing Beijing as a strategic competitor.

In 2018, under President Donald Trump, the U.S. imposed tariffs on over $360 billion worth of Chinese goods, accusing China of unfair trade practices, currency manipulation, and intellectual property theft. China retaliated with tariffs on American products like soybeans, automobiles, and chemicals. The conflict disrupted global supply chains and forced multinational companies to rethink their dependence on China.

The U.S.–China trade war marked a turning point: trade policy was now a tool of geopolitical containment rather than mere economic correction.

3. Technology and National Security

Another defining feature of modern trade wars is the fusion of technology with national security concerns. Nations increasingly view technology — particularly in areas like semiconductors, 5G, and artificial intelligence — as strategic assets.

For instance, the U.S. imposed sanctions on Huawei, China’s leading telecom firm, citing espionage risks. It also restricted semiconductor exports to China, aiming to curb its access to advanced chips. In response, China accelerated its “Made in China 2025” policy, seeking self-sufficiency in high-tech sectors.

This represents a shift from tariffs to tech-based trade restrictions, signaling that modern trade wars are as much about digital dominance as about trade balances.

4. Supply Chain Security and Reshoring

The COVID-19 pandemic and subsequent global disruptions exposed how dependent nations had become on foreign suppliers. Shortages of essential goods, from medical equipment to microchips, triggered a wave of economic nationalism. Countries began promoting reshoring (bringing production home) and friend-shoring (trading with allies instead of rivals).

This policy direction — seen in the U.S. CHIPS Act and India’s Production-Linked Incentive (PLI) schemes — reflects the idea that economic independence is a form of security, even if it reduces efficiency.

5. Energy and Resource Control

Energy politics also play a major role in modern trade wars. The Russia–Ukraine conflict (2022) led to Western sanctions against Moscow, which retaliated by cutting energy supplies to Europe. This sparked global price surges in oil, gas, and food commodities, proving that trade and geopolitics are inseparable.

Resource nationalism — countries restricting exports of vital minerals like lithium, rare earths, or fertilizers — has become another front in trade conflicts, particularly as nations race to secure green energy resources.

Major Examples of Modern Trade Wars

1. U.S.–China Trade War (2018–Present)

This remains the most significant trade conflict of the 21st century. It began with tariffs but expanded into technology bans, export controls, and investment restrictions. While both nations signed a Phase One Trade Agreement in 2020, tensions persist, especially in technology and defense sectors. The conflict has reshaped global trade flows, encouraging companies to diversify production to countries like Vietnam, India, and Mexico.

2. U.S.–European Union Disputes

Though allies, the U.S. and EU have engaged in repeated trade disputes — from Boeing vs. Airbus subsidies to digital taxes on U.S. tech giants like Google and Apple. Tariffs on steel, aluminum, and agricultural goods have also flared intermittently, reflecting underlying competition for global industrial leadership.

3. Japan–South Korea Trade Restrictions (2019)

In Asia, Japan and South Korea clashed when Japan restricted exports of key materials used in semiconductors, citing national security. The dispute was partly rooted in historical grievances but had serious consequences for tech industries worldwide.

4. Russia and Western Sanctions

Following the annexation of Crimea in 2014 and the 2022 invasion of Ukraine, Western countries imposed unprecedented economic sanctions on Russia. Moscow retaliated by banning exports and redirecting trade to Asia. This confrontation effectively created a bifurcated global trading system, dividing economies along political lines.

Economic and Market Impacts

Modern trade wars have profound consequences for the world economy:

Rising Costs and Inflation:

Tariffs increase the cost of imported goods, leading to inflation. Consumers ultimately bear the burden through higher prices.

Disrupted Supply Chains:

Global manufacturing relies on integrated networks. Trade barriers force companies to relocate or diversify production, often at higher costs.

Market Volatility:

Stock markets react sharply to trade tensions. For example, during the 2018–2019 U.S.–China dispute, global equities saw major sell-offs amid uncertainty.

Shifting Investment Patterns:

Countries like India, Vietnam, and Mexico have gained foreign investment as companies seek alternatives to China, illustrating the realignment of global supply chains.

Reduced Global Growth:

The International Monetary Fund (IMF) estimates that prolonged trade wars could shave off 0.5–1% of global GDP, dampening investment and productivity.

Geopolitical Dimensions

Trade wars are increasingly intertwined with geopolitical rivalries. Economic measures have replaced traditional warfare as a tool of statecraft. Sanctions, export bans, and tariffs are now used to coerce adversaries or reward allies.

For example, the U.S. uses trade policy to contain China, while China leverages its dominance in rare earth minerals to influence global industries. Similarly, Europe’s green transition policies also carry a strategic dimension — reducing dependence on Russian energy and Chinese solar components.

The emergence of trade blocs like BRICS, ASEAN, and the Indo-Pacific Economic Framework reflects nations’ attempts to secure regional economic influence in a multipolar world.

The Role of the WTO and Global Governance

The World Trade Organization (WTO), once the central arbiter of global trade disputes, has struggled to keep pace with modern challenges. Its mechanisms are slow, and its rules were designed for a different era — one dominated by goods, not digital or technology trade.

The paralysis of the WTO’s Appellate Body since 2019 has allowed nations to act unilaterally, bypassing multilateral dispute resolution. This vacuum has emboldened major economies to engage in aggressive trade policies without fear of meaningful retaliation through international law.

The Future of Global Trade Relations

Looking ahead, trade wars are unlikely to disappear — they are evolving. The new era of “geo-economic competition” will revolve around:

Technology control: Chip manufacturing, AI, and green tech will be the new battlegrounds.

Economic security: Nations will prioritize resilience over efficiency.

Regional trade networks: Supply chains will become more localized and politically aligned.

Digital trade rules: The next frontier of regulation will involve data sovereignty and cyber-exports.

While globalization will not end, it is shifting toward fragmented globalization, where countries trade selectively based on security and political alignment.

Conclusion

The origins of modern trade wars lie in a complex interplay of history, politics, and economics. What began as a quest to protect domestic industries has evolved into a multidimensional struggle for technological dominance, national security, and geopolitical power.

In today’s world, trade wars are not just about tariffs or deficits — they are about who controls the future of global innovation, energy, and information. The challenge for policymakers is to balance national interests with global stability, ensuring that competition does not destroy cooperation.

Ultimately, while trade wars may bring short-term political victories, history shows that economic nationalism rarely produces lasting prosperity. True progress will depend on rebuilding trust, reforming global trade institutions, and recognizing that in a deeply interconnected world, economic conflict anywhere can trigger consequences everywhere.

The Pillars of Global Trade Dynamics1. The Economic Foundation: Supply, Demand, and Comparative Advantage

At the heart of global trade lies the principle of comparative advantage, introduced by David Ricardo in the early 19th century. This concept explains why nations trade — even when one nation can produce everything more efficiently than another. Instead of self-sufficiency, countries specialize in producing goods where they have a lower opportunity cost, leading to mutual benefit through exchange.

For example, if India focuses on software services and textiles while importing advanced machinery from Germany, both countries benefit from efficiency and specialization. This principle underpins global trade structures and ensures that resources — from labor to capital — are utilized optimally.

Global supply and demand dynamics also play a critical role. When consumer preferences shift or production costs change, global trade adjusts rapidly. The pandemic, for instance, disrupted both supply chains and demand patterns, forcing the world to reconsider its dependence on certain countries and industries. Similarly, rising middle-class consumption in Asia has altered global demand, turning countries like India, China, and Indonesia into consumption powerhouses.

Economic interdependence has deepened as well. A smartphone assembled in China, using components from South Korea, software from the United States, and raw materials from Africa, showcases how global production networks interlink economies. This interdependence creates efficiencies but also vulnerabilities, as seen during trade disruptions, geopolitical tensions, or shipping crises.

2. Policy and Governance: The Regulatory Pillars of Trade

Trade doesn’t occur in a vacuum; it is guided and regulated by policies, agreements, and global institutions. The World Trade Organization (WTO), International Monetary Fund (IMF), and World Bank form the triad of international governance that promotes free and fair trade.

These institutions were established after World War II to prevent the economic nationalism that contributed to the Great Depression and global conflict. The WTO, for instance, provides a platform to settle disputes and negotiate trade liberalization, ensuring countries abide by agreed-upon rules.

However, in the 21st century, trade policy has become a strategic weapon. Tariffs, sanctions, and subsidies are now tools of economic diplomacy. Trade wars, such as the U.S.–China conflict, illustrate how policy decisions ripple across the global economy — raising costs, shifting supply chains, and altering investment flows.

Moreover, regional trade agreements (RTAs) such as the European Union (EU), North American Free Trade Agreement (now USMCA), and the Regional Comprehensive Economic Partnership (RCEP) have reshaped trade patterns. These blocs promote intra-regional cooperation and reduce barriers, allowing countries to integrate economically and enhance competitiveness.

In contrast, protectionist policies — often driven by domestic political pressures — can distort markets and fragment global trade. The balance between globalization and protectionism remains one of the defining policy challenges of our era.

3. Technological Advancement: The Catalyst of Modern Trade

Technology has revolutionized every facet of global trade — from production and logistics to finance and communication. The digital revolution, automation, and artificial intelligence (AI) have made trade faster, more efficient, and more data-driven.

In logistics, innovations like real-time tracking, blockchain-based shipping records, and automated ports have streamlined global supply chains. The containerization revolution in the mid-20th century was one of the earliest technological breakthroughs that drastically cut transport costs and boosted trade volumes.

In manufacturing, technologies such as robotics, 3D printing, and Internet of Things (IoT) are reshaping the global distribution of production. Countries with advanced infrastructure and technological expertise now dominate high-value segments of the global value chain, while developing economies specialize in labor-intensive manufacturing.

Furthermore, the digital economy has expanded trade beyond physical goods. Digital services — from cloud computing and fintech to online education — are now significant components of international commerce. A freelancer in the Philippines, a software firm in India, and a design studio in the U.S. can collaborate seamlessly in real time, thanks to digital trade platforms.

However, this technological leap also brings challenges. Automation threatens traditional manufacturing jobs in developing nations, while data localization laws and digital protectionism create new trade barriers. As the world moves toward digital globalization, ensuring inclusive access and digital equity becomes a new trade priority.

4. Financial and Monetary Systems: The Flow of Global Capital

Trade cannot function without finance. The global financial system — encompassing currency exchange, cross-border payments, and investment flows — acts as the bloodstream of trade. The U.S. dollar, long the dominant reserve currency, facilitates most international transactions, while central banks and financial institutions provide the credit and liquidity necessary for trade expansion.

Trade finance — letters of credit, guarantees, and export financing — ensures that exporters get paid and importers receive goods. The stability of global finance directly impacts trade volumes. For instance, during the 2008 global financial crisis, liquidity dried up, leading to a sharp contraction in global trade.

Exchange rate fluctuations also affect trade competitiveness. A weaker currency makes exports cheaper and imports costlier, influencing trade balances. Hence, countries often intervene in foreign exchange markets to maintain favorable trade positions — a practice sometimes criticized as “currency manipulation.”

Additionally, capital mobility — the ability of investors to move funds across borders — has made financial markets more intertwined with trade. Foreign direct investment (FDI) fuels industrial growth, infrastructure, and technology transfer, while portfolio investments reflect global confidence in economies.

As digital currencies and blockchain-based payment systems evolve, the future of global trade finance may shift toward decentralization. Central Bank Digital Currencies (CBDCs) could make international payments faster and cheaper, redefining the global monetary order.

5. Infrastructure and Logistics: The Physical Backbone of Trade

Trade relies heavily on physical connectivity — ports, roads, railways, and airports form the arteries of global commerce. Efficient infrastructure determines how fast and cost-effectively goods move from producers to consumers.

Maritime transport carries around 80–90% of world trade by volume. Hence, modern ports like Shanghai, Singapore, and Rotterdam serve as critical global trade hubs. The expansion of the Panama and Suez Canals, along with new infrastructure projects like China’s Belt and Road Initiative (BRI), reflects the growing emphasis on connectivity.

Poor infrastructure, on the other hand, remains a major bottleneck in developing countries. Delays, congestion, and high logistics costs reduce competitiveness and deter investment. Therefore, trade infrastructure investment is not just an economic necessity — it’s a strategic imperative for sustainable development.

The logistics revolution has also introduced new efficiencies. Just-in-time (JIT) inventory systems, global freight management software, and last-mile delivery innovations have minimized waste and improved responsiveness. Yet, as the pandemic revealed, these lean systems can also be fragile when global shocks occur.

6. Geopolitical and Social Factors: The Human Dimension of Trade

Global trade is deeply intertwined with geopolitics. Trade routes, resource control, and economic influence are often used as instruments of national power. Countries form alliances or impose sanctions based on strategic interests, shaping the flow of trade and investment.

The rise of geoeconomics — where economic tools are used for geopolitical aims — marks a major shift. Energy trade, for instance, has been a central element in international relations, with oil-producing nations wielding significant influence. Similarly, rare earth minerals — vital for electronics and renewable technologies — have become a new front in global trade rivalries.

Social factors are equally important. Labor standards, human rights, and environmental sustainability now shape consumer choices and corporate strategies. The ESG (Environmental, Social, and Governance) movement has pushed multinational corporations to adopt responsible sourcing and ethical production practices.

Moreover, trade influences societies by transforming employment patterns, income distribution, and cultural exchange. While globalization has lifted millions out of poverty, it has also widened inequalities in some regions. Thus, social equity and inclusivity have become essential considerations in modern trade policy.

7. Sustainability and the Green Trade Transition

The future of global trade depends on its ability to align with sustainability. As climate change intensifies, nations and businesses are rethinking supply chains, energy sources, and production methods. The concept of “green trade” emphasizes reducing carbon footprints, promoting renewable energy, and developing circular economies.

Green policies — such as the European Union’s Carbon Border Adjustment Mechanism (CBAM) — are reshaping trade norms. Exporters to such markets now face carbon pricing, pushing industries to adopt cleaner technologies. Similarly, green finance and ESG-focused investments are channeling capital toward sustainable trade infrastructure.

Sustainability is no longer an optional pillar but a central force defining competitiveness and resilience in global trade.

Conclusion: Interconnected Pillars for a Shared Future

The pillars of global trade dynamics — economic principles, policy frameworks, technology, finance, infrastructure, geopolitics, and sustainability — together uphold the vast structure of global commerce. Each pillar is interdependent, reinforcing and influencing the others.

The coming decades will witness a reconfiguration of trade networks — driven by technological innovation, climate imperatives, and shifting geopolitical alignments. The challenge lies in ensuring that trade remains inclusive, sustainable, and equitable — balancing efficiency with resilience, and growth with environmental stewardship.

Ultimately, global trade is more than an economic process; it is a reflection of human collaboration and interdependence. As nations navigate the complexities of the 21st century, strengthening these foundational pillars will determine not just the direction of commerce, but the shared prosperity of the global community.

How Currency Valuations Impact Exporters and ImportersIntroduction

Currency valuation is one of the most powerful forces shaping global trade dynamics. Every day, trillions of dollars’ worth of goods, services, and investments cross borders, and the exchange rates between currencies determine how much value each participant gains or loses. A small shift in the rupee, dollar, euro, or yen can have a massive impact on exporters’ earnings, importers’ costs, and even a country’s overall trade balance.

For exporters and importers, understanding currency valuation is not just a financial technicality — it is a survival strategy. Whether a company sells machinery to Europe, imports raw materials from China, or outsources services to the U.S., fluctuations in exchange rates directly affect profitability, competitiveness, and strategic planning.

This essay explores how currency valuations influence exporters and importers, the mechanisms behind exchange rate movements, their implications on pricing, profitability, and policy decisions, and how businesses can manage the risks associated with currency fluctuations.

Understanding Currency Valuation

Currency valuation refers to the market-determined worth of one currency relative to another. It is usually expressed as an exchange rate — for example, ₹83 per U.S. dollar means that one dollar can be exchanged for 83 Indian rupees.

Exchange rates fluctuate due to a combination of factors such as:

Inflation differentials

Interest rate variations

Trade balances

Foreign investment flows

Central bank policies

Market speculation

When a currency appreciates, its value rises compared to others, meaning it can buy more foreign currency. When it depreciates, it loses value, meaning more domestic currency is needed to buy the same amount of foreign currency.

These movements, while often subtle on a daily basis, can have profound effects on international trade.

Impact on Exporters

Exporters earn revenue in foreign currencies but often bear costs in their home currency. Therefore, currency depreciation usually benefits exporters, while currency appreciation tends to hurt them. Let’s explore both situations.

1. Currency Depreciation: A Competitive Advantage

When a country’s currency depreciates, its goods and services become cheaper in foreign markets. For example, if the Indian rupee weakens from ₹75 to ₹85 per U.S. dollar, an American buyer can now buy more Indian products for the same amount of dollars.

This creates several benefits for exporters:

Price Competitiveness: Products appear cheaper abroad, boosting demand.

Higher Profits: Exporters earn more in domestic currency when converting foreign sales revenue.

Market Expansion: Depreciation can help penetrate new markets or outcompete suppliers from stronger-currency nations.

For instance, India’s textile and IT service exporters often benefit when the rupee weakens against the dollar. Their revenues in dollars translate into higher rupee earnings, improving margins even if prices remain constant.

2. Currency Appreciation: A Profit Squeeze

When a domestic currency strengthens, exporters face a dual challenge:

Their products become more expensive for foreign buyers, reducing competitiveness.

Their foreign revenues shrink in domestic terms.

For example, if the rupee appreciates from ₹85 to ₹75 per dollar, the same $1 million export sale now converts into ₹75 million instead of ₹85 million — a clear loss in rupee terms.

Unless exporters hedge their exposure or increase prices (which may hurt demand), their profit margins shrink significantly.

Industries that rely heavily on exports — such as automobiles, textiles, or pharmaceuticals — are particularly sensitive to such changes.

3. Long-Term Effects on Export Strategy

Persistent currency appreciation can force exporters to rethink their strategy:

Shift production abroad to reduce currency exposure.

Focus on higher value-added goods where price sensitivity is lower.

Increase use of financial hedging instruments.

On the other hand, a consistently weak currency can encourage export-led growth but might raise inflation due to costlier imports (like energy or components).

Impact on Importers

Importers face the opposite situation. They pay for foreign goods and services in foreign currencies but sell them domestically in their local currency. Hence, currency appreciation generally benefits importers, while currency depreciation hurts them.

1. Currency Appreciation: Lower Import Costs

When the domestic currency strengthens, importers gain purchasing power. They can buy more goods from abroad for the same amount of domestic currency.

For example, if the rupee appreciates from ₹83 to ₹78 per dollar, a $10,000 machine from the U.S. costs ₹7.8 lakh instead of ₹8.3 lakh.

The benefits include:

Reduced Import Costs: Lower costs for raw materials, equipment, or finished goods.

Lower Inflation: Cheaper imports can reduce overall price pressures in the domestic economy.

Improved Margins: Importers or retailers can either lower their selling prices or increase profit margins.

Industries such as electronics, oil, and automobiles — which rely heavily on imports — often welcome currency appreciation.

2. Currency Depreciation: Costly Imports

Depreciation has the opposite effect. The domestic currency buys fewer foreign goods, increasing import costs.

For example, if the rupee depreciates from ₹83 to ₹88 per dollar, that same $10,000 machine now costs ₹8.8 lakh.

This can lead to:

Higher Input Costs: Import-dependent manufacturers face rising costs of raw materials or components.

Inflationary Pressure: Costlier imports can push up consumer prices, especially for fuel or food.

Profit Margin Squeeze: Importers may struggle to pass higher costs to consumers, hurting profitability.

A prolonged depreciation phase can thus make it difficult for import-driven sectors like energy, technology, and healthcare to maintain stable pricing structures.

Exchange Rate Pass-Through: Linking Valuation to Pricing

The concept of exchange rate pass-through (ERPT) explains how much of the currency movement is reflected in the final price of goods.

Full Pass-Through: Exporters/importers adjust prices completely in line with exchange rate changes.

Partial Pass-Through: Companies absorb part of the exchange rate impact to remain competitive.

For example, if the rupee weakens 10% but an exporter only raises prices abroad by 5%, the remaining 5% is absorbed in margins.

The degree of pass-through depends on market conditions, demand elasticity, and brand power. Highly competitive markets (like garments) show low pass-through, while niche products or monopolistic services show higher pass-through.

Case Examples

1. Indian IT and Pharmaceutical Exporters

When the rupee depreciates, these sectors thrive because they earn in dollars but spend in rupees. During 2020–2023, rupee weakness benefited companies like Infosys, TCS, and Sun Pharma, improving operating margins despite global volatility.

2. Oil and Gold Importers

India imports most of its crude oil and gold. When the rupee weakens, import bills rise sharply, widening the current account deficit and creating inflationary pressure. This shows how currency valuation directly influences macroeconomic stability.

3. Japanese Yen and Export Competitiveness

Japan has long relied on a weak yen to maintain export competitiveness in automobiles and electronics. When the yen strengthens sharply, companies like Toyota or Sony face reduced foreign earnings, prompting shifts in production to other regions.

Macroeconomic Implications

1. Trade Balance Effects

Currency depreciation tends to boost exports and reduce imports, improving the trade balance. Conversely, appreciation may widen trade deficits.

However, the J-Curve effect suggests that after depreciation, the trade deficit may initially worsen (as import bills rise before export volumes adjust) before eventually improving.

2. Inflation and Interest Rates

A weaker currency can stoke inflation through higher import costs, prompting central banks to raise interest rates. A stronger currency can have a disinflationary effect, allowing for looser monetary policy.

Hence, exporters and importers must watch not just exchange rates but also central bank reactions.

3. Investment Flows

Stable currency values attract foreign investment, while volatile or overvalued currencies deter it. Export-oriented economies like China and South Korea often manage currency levels strategically to maintain competitiveness.

Risk Management and Hedging Strategies

Given the volatility in currency markets, exporters and importers use various tools to manage risk:

Forward Contracts: Lock in future exchange rates to avoid uncertainty.

Options and Futures: Provide flexibility to benefit from favorable moves while limiting losses.

Natural Hedging: Matching foreign currency revenues and expenses (e.g., using dollar earnings to pay dollar liabilities).

Diversification: Expanding trade across multiple markets to reduce dependency on one currency.

A disciplined hedging strategy protects profit margins and ensures financial stability despite volatile exchange rates.

Policy and Central Bank Interventions

Governments and central banks often intervene in foreign exchange markets to prevent excessive currency swings.

Managed Float Systems: Authorities allow market forces to determine exchange rates but step in during volatility.

Reserve Management: Buying or selling foreign reserves to influence currency supply.

Export Incentives and Import Duties: Used to balance the impact of currency movements on trade sectors.

For example, the Reserve Bank of India (RBI) actively manages rupee liquidity to avoid sharp fluctuations that could harm exporters or spike import costs.

The Balance Between Exporters and Importers

While a weaker currency aids exporters, it hurts importers and raises inflation. Conversely, a stronger currency benefits importers and consumers but reduces export competitiveness.

Thus, an optimal exchange rate — not too strong, not too weak — is crucial. The goal for policymakers is to maintain stability rather than favor one side.

In the long run, productivity, innovation, and diversification are more sustainable sources of competitiveness than currency manipulation.

Conclusion

Currency valuation stands at the crossroads of global trade, linking the fortunes of exporters, importers, investors, and entire economies. A fluctuating exchange rate is more than a number on a financial screen — it is a reflection of economic strength, investor confidence, and trade competitiveness.

For exporters, a weaker domestic currency can mean opportunity; for importers, it can mean challenge — and vice versa. But those who understand the mechanics of currency valuation, hedge their risks, and adapt strategically can turn volatility into advantage.

In a globalized era, exchange rate literacy is as essential as market knowledge. Whether you’re shipping goods overseas or sourcing materials from abroad, managing currency exposure is not merely financial prudence — it’s the foundation of resilient international business.

Understanding Global Market SensitivitiesIntroduction

In an increasingly interconnected world, the global financial system behaves like a finely tuned orchestra—each instrument (country, industry, currency, or commodity) affects the harmony of the whole. When one note goes off-key, the impact resonates far beyond borders. These reactions, known as global market sensitivities, refer to how markets respond to changes in economic indicators, geopolitical tensions, interest rates, and investor sentiment.

Understanding these sensitivities is essential for investors, traders, and policymakers because even a minor shock in one part of the world can ripple across continents. Whether it’s a central bank rate decision in the U.S., a natural disaster in Asia, or an oil supply disruption in the Middle East, the effects are quickly transmitted through the arteries of global trade and finance.

1. What Are Global Market Sensitivities?

Global market sensitivities describe how financial markets react to internal and external stimuli—events or decisions that influence economic expectations, trade flows, and capital movement.

In simple terms, they are the emotional and structural responses of global markets to changing realities. These sensitivities are not random; they are shaped by a complex network of factors such as interest rates, inflation, political stability, supply-chain disruptions, and investor psychology.

For instance:

A spike in U.S. inflation may lead to fears of tighter monetary policy, strengthening the dollar but weakening emerging market currencies.

A conflict in the Middle East might cause oil prices to surge, impacting transportation, manufacturing costs, and inflation worldwide.

Thus, global market sensitivities are a mirror reflecting the pulse of the world economy.

2. The Role of Economic Indicators

Economic data releases are among the strongest triggers of global market movements. The most influential indicators include:

Gross Domestic Product (GDP) — Reflects a nation’s economic health. A strong GDP growth rate signals expansion, attracting investment and strengthening currency.

Consumer Price Index (CPI) — Measures inflation. Rising CPI data can pressure central banks to raise interest rates, which impacts global equity and bond markets.

Unemployment Rate — Indicates labor market strength. Lower unemployment often signals robust consumer spending, while rising unemployment hints at a slowdown.

Purchasing Managers’ Index (PMI) — Reveals the pace of industrial and service activity, providing an early indication of economic direction.

Each of these indicators can cause significant short-term volatility and long-term adjustments in asset allocation. For example, a surprising jump in U.S. inflation data might trigger a global equity sell-off as investors anticipate aggressive rate hikes.

3. The Sensitivity to Monetary Policy

Central banks, particularly the U.S. Federal Reserve, the European Central Bank (ECB), and the Bank of Japan (BoJ), play a pivotal role in global market reactions. Their decisions on interest rates, liquidity, and quantitative easing ripple across the financial world.

When central banks tighten monetary policy:

Bond yields rise.

Stock valuations often fall.

The domestic currency strengthens.

Emerging markets see capital outflows.

Conversely, when they loosen policy through rate cuts or asset purchases, risk assets like equities and commodities usually rally.

The 2020–2021 pandemic period is a perfect example. Central banks worldwide slashed interest rates and flooded economies with liquidity, triggering a global bull run in equities, real estate, and even cryptocurrencies. But when inflation surged in 2022, the reversal of these policies caused sharp corrections.

4. Geopolitical Events and Market Sensitivity

Geopolitical events—wars, trade conflicts, sanctions, and elections—often spark sudden and unpredictable market movements.

Trade Wars: The 2018 U.S.-China trade tensions disrupted global supply chains, increased tariffs, and caused stock market volatility worldwide.

Wars and Conflicts: The Russia-Ukraine war led to energy price spikes, global inflation, and shifts in commodity trade routes.

Elections and Policy Changes: The uncertainty surrounding major elections (like the U.S. Presidential race) often results in cautious trading and market rebalancing.

Markets dislike uncertainty. When geopolitics introduce unpredictability, investors typically move capital to “safe-haven assets” such as gold, the U.S. dollar, or U.S. Treasury bonds. These shifts highlight how sensitive global capital is to changes in stability and governance.

5. Currency Market Sensitivities

The foreign exchange (forex) market is perhaps the most sensitive of all. Currency movements respond instantly to changes in macroeconomic expectations, trade balances, and interest rate differentials.

For example:

If the U.S. Federal Reserve hikes rates while the European Central Bank holds steady, the USD tends to appreciate against the EUR.

Conversely, if China reports stronger-than-expected manufacturing growth, Asian currencies might gain due to improved trade sentiment.

Currency sensitivity also impacts export-import competitiveness. A stronger domestic currency makes exports expensive but reduces import costs—shaping the trade balance and corporate profitability.

6. Commodity Market Sensitivities

Commodities like oil, gold, copper, and wheat are highly sensitive to global demand, supply shocks, and geopolitical risk.

Oil prices often surge during geopolitical crises or supply disruptions (e.g., OPEC decisions, wars in oil-producing regions).

Gold, considered a safe-haven asset, rallies during times of uncertainty, inflation, or currency depreciation.

Industrial metals like copper and aluminum respond to global manufacturing data and infrastructure spending.

For investors and policymakers, understanding these sensitivities helps in forecasting inflation trends and industrial performance, since commodity costs directly affect production and consumer prices.

7. Interconnected Financial Systems

Today’s global markets are deeply interconnected through cross-border investments, supply chains, and digital financial systems.

A single event in one market can rapidly influence others:

A drop in Chinese manufacturing output can lower global metal prices.

A surge in U.S. bond yields can draw funds away from emerging markets.

European energy crises can trigger global shifts toward alternative energy investments.

This interdependence is both a strength and a weakness—it enhances global growth but also increases vulnerability to contagion effects. The 2008 financial crisis and 2020 pandemic shock illustrated how tightly woven these systems have become.

8. The Role of Technology and High-Frequency Trading

Modern markets are far more sensitive than those of the past due to algorithmic trading, AI-driven models, and instant information flow.

High-frequency trading systems can react to economic news within milliseconds, amplifying volatility. Social media and online news platforms also shape sentiment faster than traditional media. A single tweet from a political leader or a corporate executive can move billions in market capitalization.

This technological sensitivity adds a new dimension to global financial behavior—markets now respond not only to fundamentals but also to the speed of perception and reaction.

9. Emerging Markets and Capital Flow Sensitivity

Emerging economies such as India, Brazil, and Indonesia are especially vulnerable to shifts in global investor sentiment.

When global liquidity is high and risk appetite strong, these markets attract capital inflows seeking higher returns. However, when global rates rise or crises occur, these funds often exit rapidly, causing currency depreciation and stock market declines—a phenomenon known as “hot money” reversal.

For example, during the Fed’s 2013 “Taper Tantrum,” several emerging markets faced currency crises as investors pulled funds back to U.S. assets. This highlights the importance of global monetary sensitivity for developing economies.

10. Investor Sentiment and Behavioral Sensitivity

Markets are not purely rational—they are deeply psychological. Fear, greed, and herd mentality drive short-term market movements more than data.

Fear leads to sell-offs during crises.

Greed fuels rallies and bubbles during optimism.

Herd behavior causes investors to follow trends even when fundamentals don’t support them.

This emotional sensitivity explains why markets often overreact to news before stabilizing. Understanding behavioral dynamics is essential for traders aiming to anticipate volatility rather than react to it.

11. Risk Management in a Sensitive Global Market

In a world of interlinked sensitivities, risk management becomes critical. Investors and policymakers must monitor not only domestic data but also global developments.

Some strategies include:

Diversification: Spreading investments across geographies, sectors, and asset classes to reduce exposure.

Hedging: Using derivatives like futures or options to protect against currency and commodity fluctuations.

Scenario Analysis: Stress-testing portfolios under various global event assumptions (e.g., rate hikes, trade wars, pandemics).

Institutional investors also use “Value at Risk (VaR)” and sensitivity analysis to measure potential portfolio losses under different global conditions.

12. Case Studies of Market Sensitivity

a) The COVID-19 Pandemic (2020)

Global markets crashed in March 2020 as lockdowns halted economic activity. Equities plunged, oil prices briefly turned negative, and gold soared. Central bank interventions eventually reversed the panic, illustrating the delicate balance of confidence and liquidity in global systems.

b) The Russia-Ukraine Conflict (2022)

This geopolitical crisis disrupted energy and food supply chains, spiking inflation worldwide. It also led to currency instability and a renewed focus on energy independence across Europe.

c) The U.S. Inflation Surge (2022–2023)

The Federal Reserve’s aggressive rate hikes to tame inflation caused a global reallocation of capital—from risk assets to safer bonds—revealing the powerful global sensitivity to American monetary policy.

13. The Future of Global Market Sensitivities

Looking ahead, the world is entering a phase of “multi-polar market sensitivity.” Power is no longer concentrated in a single economy like the U.S.—China, India, and the EU are equally influential in shaping global sentiment.

Key future drivers include:

Energy transition and climate policy.

Technological disruption (AI, automation, and fintech).

Demographic shifts and consumption patterns.

Geopolitical realignments in trade and defense.

In this landscape, adaptability and awareness will be more valuable than prediction.

Conclusion

Global market sensitivities remind us that the world economy operates as a living organism—responsive, reactive, and interconnected. Every policy decision, natural event, or innovation sends ripples across borders, influencing trade, prices, and investment flows.

For investors, understanding these sensitivities is not merely an academic exercise; it’s a survival skill. The ability to interpret global signals, assess risk exposure, and anticipate reactions gives traders a powerful edge in navigating uncertainty.

As global systems evolve, one truth remains constant: markets move not only on numbers, but on how the world feels about them.

The Concept of Competitive DevaluationIntroduction

In the complex world of international trade and global finance, currency valuation plays a central role in determining the economic health of nations. A country’s currency value not only affects its imports and exports but also influences investment flows, inflation, and overall competitiveness in the global market. Among the many policies that governments use to influence exchange rates, one particularly controversial and strategic move is competitive devaluation—sometimes referred to as a “currency war.”

Competitive devaluation occurs when countries deliberately lower the value of their own currencies in order to gain a trade advantage over others. The main goal is simple: to make exports cheaper and imports more expensive, thereby boosting domestic production and improving the trade balance. While the concept seems straightforward, its implications are far-reaching, affecting everything from global trade relationships to inflation and geopolitical stability.

Understanding Devaluation

Before delving into competitive devaluation, it is crucial to understand what “devaluation” itself means.

Devaluation refers to a deliberate downward adjustment in the value of a country’s currency relative to other currencies. This policy is typically implemented by nations with a fixed or pegged exchange rate system, where the value of the currency is tied to another currency, such as the U.S. dollar or the euro.

For instance, if India were to officially lower the rupee’s exchange rate from ₹80 per U.S. dollar to ₹90 per U.S. dollar, it would mean the rupee has been devalued. This makes Indian exports cheaper for foreign buyers but makes imports costlier for domestic consumers.

Devaluation is generally used to:

Boost exports by making goods cheaper abroad.

Reduce imports by making foreign goods more expensive.

Correct trade imbalances or current account deficits.

Support domestic industries and employment.

However, when multiple countries start engaging in devaluation simultaneously to outcompete one another, the practice turns into competitive devaluation—a self-reinforcing cycle that can destabilize global trade.

Defining Competitive Devaluation

Competitive devaluation is a situation where several countries intentionally devalue their currencies to gain an upper hand in international trade. It’s often described as a “race to the bottom” because every country tries to make its currency weaker to outcompete others.

The basic logic is that if one country devalues its currency, its exports become cheaper on global markets. Other countries, fearing a loss of export competitiveness, may respond by devaluing their own currencies. This leads to a chain reaction of devaluations that can distort trade relationships and create volatility in financial markets.

In essence, competitive devaluation reflects an international tug-of-war where each country attempts to export more and import less by manipulating exchange rates—often at the expense of its trading partners.

Historical Background

The concept of competitive devaluation isn’t new; it has appeared in different forms throughout economic history.

1. The Great Depression (1930s)

During the Great Depression, countries abandoned the gold standard and devalued their currencies to stimulate exports. Britain devalued the pound in 1931, followed by the U.S. in 1933, and many others soon after. This wave of devaluations led to what economists termed “beggar-thy-neighbor” policies—where one nation’s gain in trade came at the expense of others, worsening global economic instability.

2. Post–World War II Period

Under the Bretton Woods System (1944–1971), exchange rates were fixed to the U.S. dollar, and the dollar was pegged to gold. Devaluations were rare but highly significant. For example, Britain devalued the pound by 14% in 1967, and France followed with smaller adjustments. However, competitive devaluation pressures contributed to the eventual collapse of the Bretton Woods system in 1971, when the U.S. dollar was floated.

3. The Modern Era (2008–Present)