FEAM — 5E ADVANCED MATERIALS. August 27, 2025.NASDAQ:FEAM #FEAM — 5E ADVANCED MATERIALS (NASDAQ:FEAM) Insider Purchase Analysis | Basic Materials | Specialty Chemicals | USA | NASDAQ | August 27, 2025.

Overview: This report examines the recent insider purchases of FEAM shares on August 25, 2025, in the context of the company's operational focus on boron and lithium production. FEAM, a critical minerals developer with assets in California, has faced significant share price depreciation amid market challenges in the lithium sector. The insider activity, coupled with a concurrent public offering, signals potential confidence in near-term catalysts. We provide a comprehensive analysis for institutional consideration.

1. Insider Trading Context

Buyers and Transaction Details: On August 25, 2025, BEP Special Situations IV LLC (a director-affiliated entity) purchased 100,000 shares at $3.50 per share, increasing its holdings to 7,597,349 shares.

Similarly, Ascend Global Investment Fund SPC - Strategic Segregated Portfolio (potentially related) acquired 100,000 shares at the same price, bringing combined indirect beneficial ownership to 7,830,646 shares.

Additionally, CEO Paul Weibel III bought 1,628 shares, and CFO Joshua Malm purchased 1,425 shares, both at $3.50. These transactions coincide with the closing of an $8.31 million public offering of common stock at $3.50 per share, raising capital for operational advancements.

Size and Significance: The director/fund purchases represent the bulk of the activity, totaling ~$350,000 per entity, while executive buys are smaller (~$5,000–$6,000 each). Insider ownership stands at 79.00%, with recent transactions boosting it by 1.16%. Top holders include Bluescape Energy Partners LLC (37.45% of outstanding shares).

Bullish Signal Interpretation: Insider buys at depressed prices, especially amid a capital raise, often indicate confidence in undervaluation or upcoming catalysts. This aligns with FEAM's focus on boron (stable pricing at ~$757/MT in the U.S.) and lithium (recovering demand from EVs).

The stock rose 7.82% on August 26, 2025, post-announcement, suggesting market recognition of this vote of confidence. High insider ownership (79%) reduces agency risks and aligns interests with shareholders.

Charts:

• (1D)

• (5D)

• (1H)

Insider Trades:

FEAM Ownership:

SEC From 4:

www.sec.gov

www.sec.gov

2. Technical Analysis

Chart Overview (1-Year View): FEAM has been in a prolonged downtrend since September 2024, declining from ~$24 to $4.20 by August 2025, reflecting sector pressures.

A sharp drop in December 2024 (from $20 to $10) marked a breakdown below key support, followed by consolidation around $4–$6. The descending trendline (purple) connects highs from October 2024 onward, acting as resistance. Moving averages show bearish alignment: SMA20 ($3.57), SMA50 ($3.92), SMA200 ($6.34). Volume trends indicate spikes during sell-offs (e.g., December 2024, March 2025), with recent August 2025 volume elevated on the offering news.

Chart Overview (1-Month View): Short-term volatility is evident, with a bounce from $3.50 lows in late June to $5.00 highs in mid-August, followed by a pullback to $3.42. Candlestick patterns include a bullish engulfing on August 7–11 (green candles with volume spike), but recent red candles suggest profit-taking. RSI (14) at 38.40 indicates approaching oversold territory, potentially signaling a reversal if buying momentum builds.

Key Levels and Indicators:

• Support: $3.00 (psychological floor, recent lows), $2.82 (52-week low).

• Resistance: $4.00 (near-term), $5.00 (mid-August high), $6.00 (SMA200 convergence).

• Trendlines: Bearish descending channel intact; a break above $4.00 could invalidate.

• RSI/MACD: RSI neutral-to-oversold (38.40); MACD not shown but implied convergence on pullback suggests potential bullish crossover if volume supports.

• Volume and Patterns: Average volume 35K; recent spikes (e.g., 131K on August 27) correlate with news. No clear reversal patterns yet, but insider buys at $3.50 may establish a base.

➖➖➖

3. News & Fundamental Drivers

➖ Latest News: On August 25, 2025, FEAM closed an $8.31 million public offering to fund project development, including its Fort Cady boron-lithium project. An updated technical report was released on August 12, 2025, highlighting resource estimates. The company presented at the Sidoti Micro-Cap Conference on May 22, 2025.

➖ Earnings Reports: Fiscal Q3 2025 (ended March 31, 2025, reported May 15, 2025) showed EPS of -$1.68, missing estimates of -$1.31 by $0.37. TTM EPS stands at -$16.11, with no sales reported (pre-commercial stage). ROA -44.56%, ROE -82.77%, reflecting development-phase losses. Next earnings expected September 8, 2025.

➖ Sector Outlook: The boron market is projected to grow from $3.63B in 2025 at >4% CAGR, driven by glass, ceramics, and agriculture demand. Lithium supply currently outpaces demand, stabilizing prices in 2025, but EV battery growth forecasts >400 GWh demand by year-end, with potential shortages ahead.

Catalysts include U.S. tariffs on imports, FEAM's domestic production advantages, and project milestones (e.g., commercial boron output).

➖➖➖

4. Trade Setup & Forecast

Replicating Insider Trade: Assuming entry mirroring insiders at ~$3.50 (current price $3.42 offers a slight discount).

Entry Price: $3.42–$3.50.

Price Targets:

➡️ Short-term (1–3 months): $4.50 (break above resistance, +31.6%).

➡️ Mid-term (3–6 months): $6.00 (SMA200 test, +75.4%).

➡️ Long-term (6–12 months): $10.00 (channel breakout, +192.4%).

We recommend a Strong Buy with 25–35% potential upside over the next 6 months, targeting $4.50–$4.75 on project milestones.

Disclaimer: This report is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.

Insider

Oil Target 62$: Sentiment Shifts Amid Geopolitical TensionsWe’re in a non-standard situation for oil markets — with the White House now openly threatening military action against Venezuela.

This dramatically increases the value of oil options sentiment.

You don’t need to be a PhD in geopolitics to understand:

A military operation = major supply disruption risk = price volatility on steroids.

And the market is already pricing it in.

Over the last two days, key levels like 58–60–72 have started appearing more and more in CME options flow — clear signs of positioning for extreme moves.

But here’s what matters most:

The trades that were placed before the Venezuela news broke.

That’s where we focus.

And if I had to summarize:

Two days ago, some guys were actively building spreads targeting 60–62 — betting on a pullback.

📌 Why?

These spreads are aggressive — they can generate 2x–3x returns from just a $2–$3 move, even if price doesn’t fully reach the target.

In short:

They’re not waiting for perfection.

They’re ready for explosion.

🔥 Final Take:

Yes, the option market has been extremely active over the past 48 hours — one of the busiest periods lately.

But beyond the noise, there’s a growing signal:

Oil is primed to explode.

And this "Venezuela narrative"?

It’s looking less like talk — and more like a setup for real movement. Big money is involved

The main question: will it explode before or after the New Year?

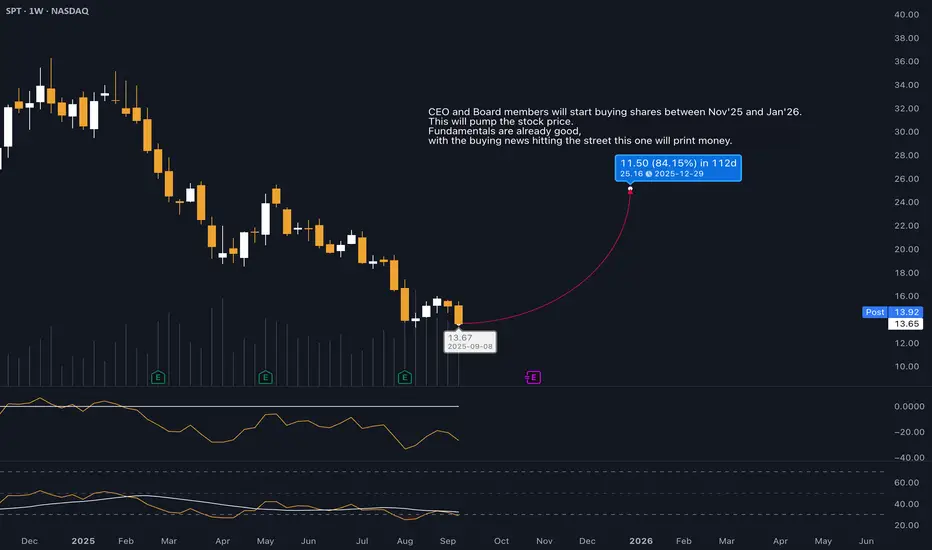

SPT will hit 25 USD (+80%) in next 4 monthsRead the Sec filing 26th August, 2025.

CEO and Board members will end their share selling plans and instead they will start buying shares. This change needs some weeks to get approved by SEC.

But once the new purchase plans are approved - i expect this to happen until the end of the year - and this news hits the street this stock will pump like crazy.

We will see at least 20 USD, im expecting even 25 USD.

Fundamentals are already good. Revenue is growing. Social media managers love Sprout Social already. Big companies will follow in future and start using Sprout Social.

F&G Annuities & Life Inc — Insider Activity ReportSergio Richi Premium ✅

NYSE:FG — F&G Annuities & Life Inc (NASDAQ:FG) Insider Activity Report | Financial | Insurance-Life |USA | NASDAQ | September 04, 2025.

Price (Sept 4, 2025) : $34.99

Insider Activity

CEO Chris Blunt just bought 7,000 shares at $34.02 on Sept 2. That pushes his 2025 insider buys to $2.5M+. No insider sales on record. When the CEO keeps writing checks into weakness, that’s conviction you don’t ignore.

(SEC Form 4)

www.sec.gov

1. Company Overview

FG is a life insurance and annuities player, majority-owned by Fidelity National Financial. Core business: retirement security through annuities, life insurance, and pension risk transfers. Rising rates have juiced demand for fixed-index annuities. Q2 revenue: $1.35B (+12.6% YoY), with sales momentum accelerating.

Dividend just bumped to $0.22/share (2.5% yield).

2. The Setup

• Stock is down ~15% YTD but holding a strong base near $34 support.

• Heavy institutional ownership (95.71%) and recent inflows from funds like BlackRock, DFA, and Millennium.

• Catalysts ahead: Q3 earnings in November, sector tailwinds from higher-for-longer rates, and annuity demand from aging demographics.

Charts:

• (1D)

Insider Trades:

FG seasonality:

FG Hedge Fund Flows:

FG Ownership:

3. The Trade:

Entry : $34–35

🎯 Take Profit 1: $40.85 (+16.75%)

🎯 Take Profit 2: $43.70 (+24.89%)

My View

The CEO is doubling down, institutions are scaling in, and fundamentals are firm. Risk/reward skews bullish — I see a 16–25% move higher as the base case, with upside surprise if annuity sales keep beating.

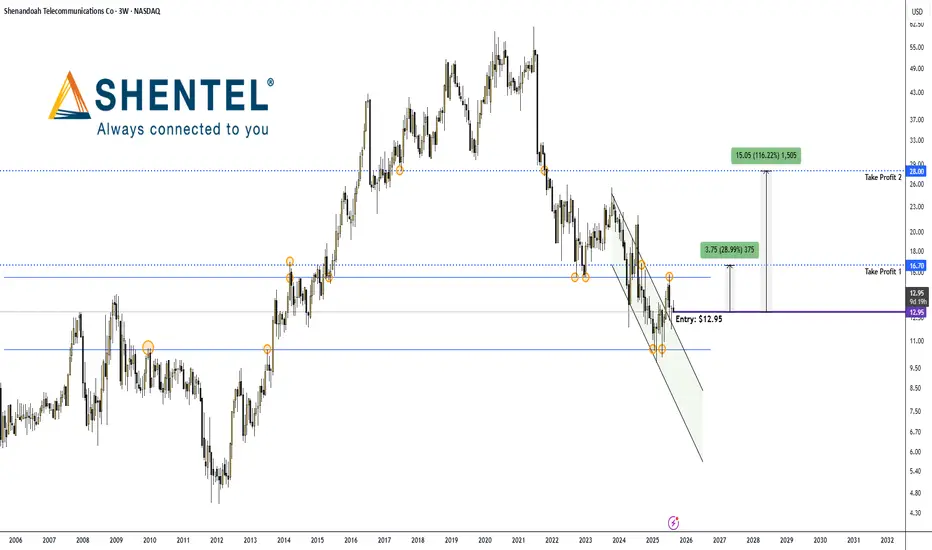

Shenandoah Telecommunications Co — September 02, 2025Sergio Richi Premium ✅

NASDAQ:SHEN — Shenandoah Telecommunications Co (NASDAQ:SHEN) Insider Activity Report | Communication Services | Telecom Services |USA | NASDAQ | September 02, 2025.

Price (Sept 2, 2025) : $12.95

Insider Activity

ECP ControlCo, a 10% owner tied to Energy Capital Partners, has been steadily loading up on SHEN since May. From late May through August 29, they picked up 864K+ shares worth over $11M, pushing their stake above 3.3M shares (~6.1% of the float). The buying wasn’t symbolic—this is real money, consistently deployed on a stock that’s been under pressure.

(SEC Form 4)

www.sec.gov

(SEC Form 4)

www.sec.gov

1. Company Overview

Shenandoah Telecommunications (Shentel) runs fiber broadband, video, and voice services across Virginia, West Virginia, Maryland, and Pennsylvania. Its flagship brand Glo Fiber is expanding fast, with 40%+ YoY revenue growth. Q2 2025 showed revenue at $88.6M (+3.2% YoY), with adjusted EBITDA up 21.9%. Despite a small net loss, the operating trend is improving.

Market cap sits just over $700M, with insiders holding ~11% and institutions ~65%.

2. Why It Matters

• Fiber-to-the-home growth is the story: Q2 Glo Fiber up 40.5%.

• Rural broadband subsidies add a tailwind.

• Institutional inflows are showing up: Southeastern Asset Mgmt (+151%), Longleaf (+151%), RBC (+184%), Two Sigma (+119%), Invesco (+104%).

• Short interest is modest (~4.4% float).

Charts:

• (3W)

Insider Trades:

SHEN seasonality:

SHEN Hedge Fund Flows:

SHEN Ownership:

3. The setup:

SHEN has been trading heavy but looks like it found a floor around $13. Insider conviction plus institutional inflows give me confidence this is a buy-the-weakness play.

Entry : $12.95–$13.35

🎯 Take Profit 1: $16.70 (+29%)

🎯 Take Profit 2: $28.00 (+116%)

My Take

Insiders are writing 8-figure checks into a depressed tape, institutions are scaling in, and fiber growth is compounding.

Atlassian Corporation — September 02, 2025Sergio Richi Premium ✅

NASDAQ:TEAM #AtlassianCorporation — Atlassian Corporation (NASDAQ:TEAM) Insider Activity Report | Technology | Software - Application | USA | NASDAQ | September 02, 2025.

Price (Sept 2, 2025) : $172.66

On August 28, Director Scott Belsky bought 1,455 shares at $173.00 (~$252K). This is his first disclosed purchase. Unlike CEO sales under pre-arranged 10b5-1 plans, this was an open-market buy—at levels that insiders view as undervalued following strong FY25 results.

(SEC Form 4)

www.sec.gov

1. Company Profile / Overview:

Atlassian Corporation (NASDAQ: TEAM) is a global leader in enterprise collaboration and productivity software. Its flagship products include Jira, Confluence, Trello, and Bitbucket, serving more than 300,000 organizations worldwide.

Atlassian’s strategy is anchored in:

• Cloud transition – shifting its massive install base from on-prem to recurring cloud revenues.

• AI integration – with over 2.3 million active AI users and a strategic partnership with Google Cloud to scale adoption.

• Enterprise expansion – record multi-million-dollar contracts, deeper penetration into Fortune 500.

• Financial strength – FY25 revenue hit $5.22B (+19.7% YoY), with cloud revenue up 26%. Free cash flow reached $1.4B, giving the company flexibility for reinvestment and M&A.

Insiders own ~37% of the stock, institutions ~53%—a rare alignment of interests between management and Wall Street.

2. Institutional Flows (Q2 2025):

• FMR (Fidelity): +74%

• D.E. Shaw: +321%

• Two Sigma: +285%

• Vanguard: +2.6% (largest holder at 17.4M shares)

Net effect: significant inflows despite a -30% YTD drawdown.

Charts:

• (2W)

TEAM seasonality:

TEAM Hedge Fund Flows:

TEAM Ownership:

3. The setup:

TEAM has defended the $170 support zone. Belsky’s buy at $173 validates this level as institutional demand. A breakout above $190 could accelerate momentum, with the next resistance in the $220–235 range.

Entry : $172–173

🎯 Take Profit 1: $235 (+36.1%)

🎯 Take Profit 2: $273 (+58.0%)

Insider conviction, institutional accumulation, and strong AI/Cloud fundamentals line up with a bullish long-term setup. Risk/reward skews heavily to the upside. I’m targeting +36–58% upside in the next 6–12 months as TEAM extends its global uptrend.

Strategic Education Inc. — September 02, 2025Sergio Richi Premium ✅

NASDAQ:STRA #StrategicEducation — Strategic Education Inc. (NASDAQ:STRA) Insider Activity Report | Consumer Defensive | Education & Training Services | USA | NASDAQ | September 02, 2025.

Price (Sept 2, 2025) : $82.12

On August 29th, Daniel Jackson, EVP & CFO of Strategic Education, stepped in with a 1,900-share open-market buy at $81.50 (~$155K). His total stake now tops 104K shares. It’s not the size of the purchase that matters here — it’s the timing: the transaction followed a Q2 earnings beat (EPS $1.52 vs. $1.42 est.) and nearly 8% YoY revenue growth, driven primarily by their Education Technology Services.

(SEC Form 4)

www.sec.gov

Insiders rarely commit fresh capital unless they see value that the market is missing. What stands out: institutions have been quietly adding — Marshfield Associates increased by 12,500 shares, and American Century expanded their stake earlier in the quarter. Insider ownership sits near 3.3%, and inflows continue despite a flat YTD chart.

1. Company at a glance:

• Runs Strayer University, Capella University, Torrens (AU/NZ), plus Sophia Learning & Workforce Edge.

• Focused on affordable, flexible, employer-aligned higher ed.

• Q2 revenue ~$300M, cash position $133.6M, dividend $0.60/qtr (~3% yield).

Market cap around $2B.

2. Catalysts on the horizon:

• Dividend payable Sept 15.

• Next earnings Oct 29 — potential follow-through if enrollment momentum stabilizes.

• Expanding EdTech footprint — Sophia & Workforce Edge gaining traction in B2B partnerships.

• Protocol adoption in Australia/NZ could re-accelerate international enrollment.

Charts:

• (5D)

Insider Trades:

STRA seasonality:

STRA Hedge Fund Flows:

STRA Ownership:

3. The setup:

Entry: $81.50–$82.06 (aligned with insider buy).

🎯 Take Profit 1: $111.00 (+35.27%)

🎯 Take Profit 2: $119.00 (+45.02%)

Base case: 35–45% upside in 6–12 months.

Bull case: test $119 on stronger EdTech growth + enrollment recovery.

AI c3ai Bullish Reversal Ahead of EarningsAI C3.ai has been in the spotlight recently, following a series of notable developments that set the stage for a potential bullish reversal. The company recently announced that founder and CEO Thomas Siebel is stepping down due to health reasons. While this initially caused some market jitters, it coincides with a broader operational transformation that could act as a catalyst for a turnaround.

Earlier this month, C3ai reported preliminary fiscal first-quarter revenues below expectations, raising short-term concerns. However, the company continues to invest in AI-driven solutions and expand strategic partnerships, including a notable collaboration with Eletrobras in Brazil. These moves demonstrate that the firm is actively diversifying its offerings and positioning itself as a leading player in enterprise AI.

From an options market perspective, there is evidence of bullish sentiment building ahead of earnings. The $25 strike price out-of-the-money calls expiring on September 19 suggest that traders are betting on a near-term upside, signaling expectations of a possible recovery or positive surprise in the upcoming earnings report.

Leadership changes, while initially unsettling, often create opportunities for strategic shifts. A new CEO could accelerate operational efficiency, focus on high-growth initiatives, and highlight C3ai’s AI innovation, which has been a core strength of the company. Combined with ongoing product launches and partnership expansions, these factors could serve as a catalyst for a technical and fundamental reversal in the stock.

Traders may want to watch key support levels and the $25 strike options activity closely, as these indicators suggest that a bullish reversal could be on the horizon. With a renewed leadership team and continued AI innovation, C3.ai has the potential to regain momentum in the weeks leading up to earnings.

BTC - The Reason 8,000 is Possible There is already speculation and news coming out about plans of a large drop, and I imagine if this occurs there will be much hysteria and conspiracy about it.

Bitcoin is massively dominated by leverage trading. In fact, the majority of buys (or sells respectively) are leveraged.

Even Microstrategy for example, is leveraging its BTC to buy more BTC - and what happens when the value of the asset drops too low when leveraging is used? Well, we will find out. But normally this means bankruptcy / liquidation.

In futures trading, this is liquidation or stop losses being hit on those positions.

Since the price of BTC has been moving up, sideways, up, sideways, up, sideways - we could see for years the intentionality in this chart.

The market has been accumulating long positions / leveraged buys, holding the price up and continuing to attract money into the market cap (leveraged) and keep the orders in tact.

As a consequence, this leaves behind a trail, like a series of dominos, of leveraged sell orders.

These sell orders are in the form of long stop losses or liquidations. In essence, we have an explosive chain reaction ready to set off in the chart - an automatic, natural consequence to how the chart has been moving the last 2 years.

The argument may be that Bitcoins market cap is stabilized by a “floor”, possibly by ETF holdings, spot holdings, ETC - however, this is not the case. Many of these spot holdings themselves are leveraged with BTC to procure more BTC.

Even so, the vast majority of the market cap is market maker liquidity allowing retail traders to leverage trade the asset and other cryptocurrency - and the exchanges aren’t legislated to disclose where the stop losses are located or how much liquidity is contained here.

So if we think popular heat map and liquidation platforms are accurate, think again. The only way to really understand this, is to look at the price movement on HTF.

There are longs held since 12,000, and stop losses respectively held sub 10,000.

I suspect the true “floor price” of BTC is between 7,000 to 8,000 - that’s the total percentage of stable spot holding liquidity vs leveraged liquidity. Leveraged liquidity has no incentive to be stable, it moves in and out, market makers make their money via bankrupting / liquidating traders, or forcing them into stopped out positions.

For me, the last 1-2 years, this has never been an IF, but a WHEN. And WHEN this chain reaction occurs, those reading this can understand the reason is not a black swan (although that may serve as some initial excuse) - but rather a very natural phenomenon in a unique market that we mistakingly treat as a stable market that these events simple cannot happen in.

I’ll be very clear when I say - it’s possible BTC drops to 8,000, extremely fast, possibly in a matter of days or even hours, and quickly returns to ATH positions.

The real warning here I want to get across, is that a flash crash as I am describing, will only go so low as the stop loss orders are active. Ultimately there are no incentives or plans to destroy or bring BTC to zero.

When this flush happens, the big players (market makers) will be filling in the buy orders at those low prices with the liquidity returned from retail longs.

DO NOT SELL AT A MASSIVE LOSS. This is the biggest warning I have to get across with these posts, and would be the most devastating conclusion - believing BTC will go to nothing.

DXY is breaking down a major multi month bearish pattern and over the next 3-5 year period will be absorbing liquidity towards the lows. A falling dollar = bull market for BTC and equities.

This move up on BTC WAS NEVER A BULL MARKET - it was a bearish retest. This explains the erratic, up only nature of the move zoomed out - and all these justifications to explain that this is the “norm” it’s dangerous to traders. It’s not the norm of a bull market, it’s the norm of a bearish retest.

What do you do with this information?

If you are me, and by no means am I suggesting this, you can short the market and try to align yourselves with the big players.

If you’re a believer in the future of BTC, you can do nothing - not letting any fast drop or hysteria shake you or drive you to making an emotional decision to sell or change your mind.

This has never been a doom and gloom scenario for you all - it’s a reality check, a warning, and an opportunity to prepare yourselves for something you may not yet believe is possible unless you’ve been watching this market unfold since it’s very inception. In those cases, you will certainly remember flash crashes and stop hunts - and they have never changed, nor has the nature of the exchanges or market - it’s month more calculated now with big players invested in capitalizing to the fullest on the flaws of it all.

I wish you all the best.

AI Insider Trading Before the Buyout? $5.8Million block of callsOn Friday, after the close, C3. ai announced CEO Thomas Siebel is stepping down, with a new leadership team taking over. The stock dropped almost 14% on the news, slashing its market cap and potentially making it irresistible for a takeover bid. They are looking for a new CEO!

Why this matters:

1. Perfect M&A Timing: C3. ai has proven AI tech, including contracts with the U.S. Department of Defense. The right acquirer could turn this into the next Palantir-style success story. Leadership changes often make buyouts easier.

2. Valuation Reset: The 14% drop gives strategic buyers a cheaper entry point, exactly when they might be circling.

3. Massive Call Buying Before News: Just last week, someone dropped $5.8M on Sept 19 $25 strike calls. That’s a high-conviction, short-dated bet. Nobody throws around that kind of money without expecting a big move, possibly insider knowledge of a deal or major contract.

4. Strategic Fit: Defense contractors or big tech companies could instantly expand their AI footprint by acquiring C3.ai.

Palantir built its empire by combining cutting-edge data analytics with deep government and defense relationships. C3. ai is following a similar blueprint and may be earlier in the curve:

1. Strong Defense Footprint: C3. ai already holds contracts with the U.S. Department of Defense and other government agencies, positioning it in the same secure, high-margin niche that powered Palantir’s growth.

2. Mission-Critical AI Solutions: Just like Palantir’s Gotham and Foundry platforms became embedded in government workflows, C3. ai’s AI suite is designed for enterprise and defense applications that are hard to replace once integrated.

3. Massive TAM (Total Addressable Market): The AI defense and enterprise analytics market is projected to grow exponentially over the next decade, mirroring the macro tailwinds Palantir rode after 2020.

4. Sticky Contracts: Government and defense clients tend to lock in long-term, high-value contracts once a system is deployed, creating predictable recurring revenue streams.

5. Potential for Commercial Expansion: Palantir went from mostly government to a healthy commercial mix. C3. ai could follow the same path, leveraging its defense credibility to win private-sector deals.

6. Strategic Acquisition Target: Big tech and defense primes would love to own a proven AI platform with federal clearance — just as Palantir’s unique positioning has made it a darling of Wall Street and a fortress against competition.

In short: C3. ai today could be where Palantir was a few years ago!

If acquired or scaled correctly, the upside could be just as explosive!

UNH bear flag and gapsUNH has been top of my radar for a bullish reversal. With 2 major gaps to fill after the epic collapse in share price this ticker has a lot of potential. Currently sitting in what appears to be a bear flag, it is holding above the monthly 200EMA (overlayed on this 4H chart). However price recently rejected off the daily 21ema (overlayed on this 4H chart) and if the bear flag is any indicator price may head lower for another liquidity sweep before the inevitable bullish reversal.

A side note: insiders have been buying $millions since the share price collapsed which is always a good indicator of what's to come.

Plug Power: A Mirage or a Miracle?Plug Power (NASDAQ: PLUG), a key innovator in hydrogen energy solutions, recently experienced a significant surge in its stock value. This upturn is largely attributed to a strong vote of confidence from within the company: Chief Financial Officer Paul Middleton substantially increased his stake by acquiring an additional 650,000 shares. This decisive investment, following an earlier purchase, clearly signals robust conviction in Plug Power's future growth trajectory, despite prior market challenges. Analysts also reflect this cautious optimism, with an average one-year price target that suggests a significant upside potential from the current valuation.

A major catalyst for the renewed interest stems from Plug Power's expanded strategic collaboration with Allied Green Ammonia (AGA). This partnership includes a new 2-gigawatt (GW) electrolyzer project in Uzbekistan, part of a substantial $5.5 billion green chemical production facility. This facility will produce sustainable aviation fuel, green urea, and green diesel, positioning Plug Power's technology as foundational to large-scale decarbonization efforts. This initiative, backed by the Government of Uzbekistan, further solidifies a broader 5 GW partnership between Plug Power and AGA across two continents, highlighting the company's capability to deliver industrial-scale green hydrogen solutions.

While these strategic wins are promising, Plug Power continues to navigate financial headwinds. The company has faced recent revenue declines and currently reports significant annual losses and cash burn. To address capital needs, it is seeking shareholder approval to issue more shares. However, the substantial, multi-gigawatt contracts secured, particularly with Allied Green, underscore a strong future revenue pipeline. These projects affirm the critical demand for Plug Power's technology and its pivotal role in the evolving green hydrogen economy, emphasizing that the successful execution of these large-scale ventures will be key to long-term financial stability and sustained growth.

SHORT META Ahead of Earnings Report Based on Insider Selling"Meta Platforms Insider Sold Shares Worth $22,132,922"

Mark Zuckerberg, 10% Owner, Director, Chair of Board and Chief Executive Officer, on January 15, 2025, sold 35,921 shares in [eta Platforms. Following the Form 4 filing with the SEC, Zuckerberg has control over a total of 353,696 shares of the company, with 353,696 controlled indirectly.

Jennifer Newstead, Chief Legal Officer of Meta Platforms sold 905 shares of Class A Common Stock on January 14, 2025, at a price of $604.54 per share, totaling $547,108. Following the transaction, Newstead directly owns 31,105 shares of Meta Platforms.

Jennifer Newstead, Chief Legal Officer of Meta Platforms, sold 905 shares of Class A Common Stock on January 21, 2025, at a price of $618.0 per share, totaling $559,290. Following the transaction, Newstead directly owns 30,200 shares of Meta Platforms.

The sales were conducted under a Rule 10b5-1 trading plan adopted on November 30, 2023.

Olivan Javier, Chief Operating Officer of Meta Platforms, sold 413 shares of Class A Common Stock on January 21, 2025, at a price of $618.0 per share, totaling $255,234. Following the transaction, Javier directly owns 16,275 shares and indirectly owns 95,287 shares through various entities.

The sale was conducted under a Rule 10b5-1 trading plan adopted on August 30, 2023.

Platinum Insider Stays in the Game, Anticipating Higher PricesA platinum Insider hasn't changed portfolio yet, so there's still potential for more growth.

Let me remind you, on September 4th, an insider came into the Platinum market and went long, which caused the price of Platinum (and other precious metals) to go up.

Now, prices are getting close to his target levels. This is important because it shows the market's future direction. The Insider know when to get in and when to get out. And we can watch them to see what he is doing.

If you don't have the time or inclination to read stock reports, just follow us. We cover all the important stuff and provide valuable insights every day.

FTMUSD Trade setupAccumulate in this area, FTM is primed in Q4 2024 - Q1 2025. Sonic will generate new ATH's.

Platinum is about to skyrocket and soar by 20%!Platinum's insider was discovered!

He was last seen at it on March 7th of this year, and platinum prices have jumped by 20% since then!

Now, his target price is between $1100 and $1200 , representing a greater than 20% increase. There's some significant momentum going on there.

We are keeping a close eye on it.

3 Reasons Why Insider Selling Wont EndInsider selling is like a mole rat on a farm

they are hard if not impossible to

get rid of infact, some farming

experts say mole are good for the soil

fertility

i was watering a ground where a mole

had made a tunnel,

and i noticed that where the moles

had not drilled into the ground

the vegetables are not growing well

as compared to where the moles had

drilled underground tunnels

Its a very similar concept

when it comes to trading the

only difference here is that:

1-Insider selling gives you a map of what to do

2-Insider selling is public information

3-Insider selling helps you as a trader

In insider selling is good because it will

help you find the right trades

Watch this video again to learn more

about this

Also rocket boost this content to learn more.

Disclaimer:Trading is risky you will lose money

wether you like it or not

and so because of this please

learn risk management and

profit taking strategies

before you engage in trading.

SNOW - Major long opportunity! Look for this to enterThis is super interesting and we could be near a great level to get in for a longer term hold.

Many confluences on this one so keep this one on the list!

Happy Trading :)

COPPER! Is the party over?Targets met. Activity in an options portfolio that was poised to rise before the market rose (INSIDER) resold 4.14 calls into the market. Made 400% on that strike. How about that? Is it worth studying options strategies and tracking the activity of the big players?

Trade Idea: Go Long Up To 1100$Rationale:

COT sentiment

The last COT report shows that Commercials' net short positions have been decreasing, which could indicate a shift in sentiment towards the bullish side.

The COT report can be used as a tool to gauge the market sentiment of traders. When Commercials' net short positions decrease, it could signal a potential shift in sentiment towards the bullish side. This could be due to factors such as improving economic conditions, increased demand for platinum, or geopolitical events that could impact the price of platinum.

Option Sentiment

There has been a significant increase in insider option activity, with a notable number of calls being purchased at 100$ strike price. This bullish sentiment has been further corroborated by the options open interest, which has also increased.

Technical Analysis

From a technical perspective, Platinum breakthroug range.

"PANW" Palo Alto Networks - Insider TradingPANW is being bought by US Parliament member Nancy Pelosi, she bought twice in past month.

The current price is in perfect Golden Zone on Daily chart. If we go past ATH there is no actual telling where it will go up to next, we might just move sideways for now to reset RSI or even start moving up at any time. But it also might just drop down a bit.

Palo Alto Networks, a cybersecurity company that provides advanced firewall and cloud security solutions. Palo Alto Networks offers a range of products and services aimed at protecting organizations from cyber threats, including next-generation firewalls, cloud security, endpoint protection, and threat intelligence services. The company is known for its focus on innovation and its commitment to helping businesses secure their digital assets against evolving cyber threats.

Bullish What's going on with IDEA/USDT?50 & 200 about to cross

Volume Steadily Increasing

Rebounding from the .5 fib

Low Market_Cap with High Potential

If you zoom out with this one you can see since the price bottomed out it's been at a record high volume leading me to believe something is going on with this token that we're gonna find out later in time

NVDA: $194M Insider LiquidationNVIDIA is presenting potentially lucrative short-term trading opportunities, specifically for derivatives. A months-long ascending triangle is visible on the hourly and daily charts; a second, smaller ascending triangle is potentially forming at the time of this idea.

I believe, and am hopeful for, that the smaller ascending triangle will prove invalid and complete the double-top "M" pattern with selling pressure draining NVDA to the $430 range which falls around the respective 61.8% Fibonacci retracement level. However, I think it would be reckless to count out a potential rebound around $470 which is where the second ascending triangle's support will be tested.

If the $430 support is reached, I believe this will be the time to enter a long call option as I suspect the asset will be retesting the $500 resistance. However, insider liquidation is a major concern especially since the total offload within the last 30 days is equal to $194.3M USD. A link to the SEC filings is posted below.

NASDAQ:NVDA

www.sec.gov