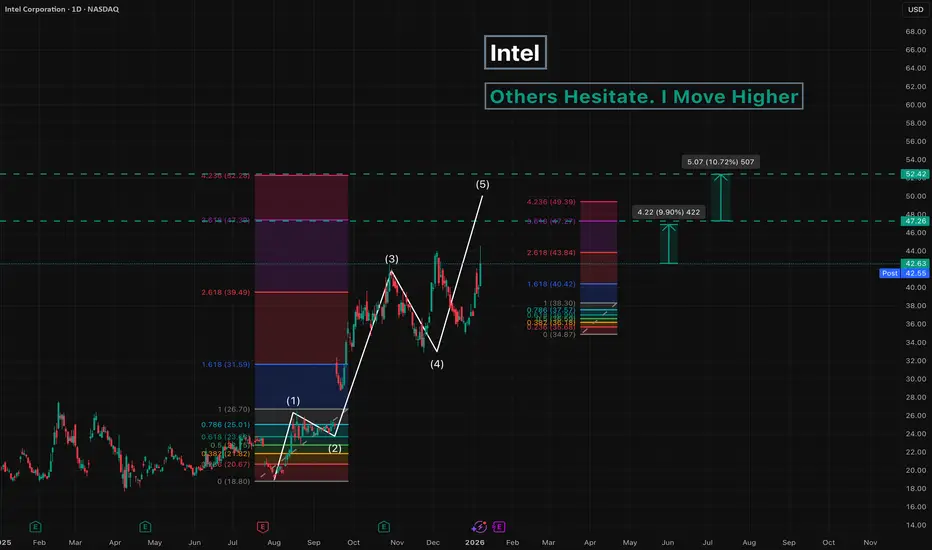

Intel - Others Hesitate. I Move HigherSince August 2025, Intel has been in an uptrend.

Only the final fifth wave remains to be completed.

The upside potential is estimated at 10-23% .

Key targets:

47

52

---

Please subscribe and leave a comment.

You’ll get new information faster than anyone else.

---

Intel

Intel - Here comes the bullish breakout!💾Intel ( NASDAQ:INTC ) will soon break out:

🔎Analysis summary:

During 2025, Intel has over and over again been retesting major support. That was exactly the reason why I told everyone to enter longs here on Intel. Just a couple months later we witnessed a +150% rally and Intel is about to create another bullish breakout soon.

📝Levels to watch:

$45 and $70

SwingTraderPhil

SwingTrading.Simplified. | Investing.Simplified. | #LONGTERMVISION

INTC – What Price and Volume Are Telling Us ?INTC - CURRENT PRICE : 37.40 - 37.60

INTC is currently undergoing a controlled pullback within a broader rising structure, as indicated by the rising trendline support (white dashed line). Notably, the recent price decline is accompanied by diminishing volume, which suggests that selling pressure is losing momentum rather than aggressive distribution.

This type of price-down / volume-down behavior typically reflects profit-taking and short-term exhaustion by sellers, often seen during healthy corrections within an uptrend. As long as price continues to respect the rising trendline, the broader bullish structure remains intact.

From a volume perspective, there is no evidence of panic selling, while prior upswings were supported by higher relative volume — reinforcing the view that buyers remain in control at higher timeframes.

Take note that stochastic oscillator is approaching near oversold zone. In an uptrend, any oversold condition may be considered as a potential buy on dips.

Trading Plan (Price & Volume Based)

Buy on pullback near the rising trendline support

ENTRY PRICE : 36.00 - 37.00 zone

Upside Targets:

🎯 Target 1: 40.00 (near-term resistance)

🎯 Target 2: 44.00 (prior swing high)

🧊 Cut Loss: Below 33.00, which would signal a breakdown of trend support.

Intel (INTC) shares surge following chip unveilingIntel (INTC) shares surge following chip unveiling

Intel (INTC) shares jumped above $44.30 yesterday, marking a 21-month high. The rally was driven by news from CES 2026, where the company unveiled its new Core Ultra Series 3 processors (codenamed Panther Lake). These are Intel’s first consumer chips manufactured using the advanced Intel 18A process technology.

Market participants interpreted the announcement as evidence that Intel’s ambitious turnaround strategy to restore its technological leadership is gaining traction. The launch of the 18A node suggests that Intel is once again capable of competing with TSMC on the leading edge of semiconductor manufacturing.

According to media reports, several analysts have raised their price targets for INTC shares, as the new technology opens up the prospect for Intel to secure contract manufacturing orders from major players such as Nvidia and Apple.

Technical analysis of INTC shares

On 3 December, when analysing the INTC chart, we:

→ identified a broad long-term price channel;

→ highlighted the importance of the $20 level, which appeared to act as support from institutional investors;

→ noted that the line dividing the upper half of the channel into two quarters could function as resistance.

As indicated by the red arrow, this line has indeed acted as a reliable barrier to further upside. Volume analysis is particularly noteworthy: on two occasions when INTC shares rallied towards this level, we observed:

→ a surge in trading volumes;

→ followed by a subsequent pullback.

It is possible that the move above the psychological $40 level, combined with positive news flow, generated FOMO-driven demand. Institutional traders may be using this demand to lock in profits on long positions accumulated around the $20 zone.

Given the long upper wick on yesterday’s candlestick, we could assume that the identified resistance line may hold, and that a third attempt to break above it could once again result in a pullback.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Intel aiming to previous two bottomsIntel is probably aiming to harvest a lot of liquidity from the previous two bottoms.

INTC Weakness Exposed — Are Sellers Still In Control?🔥 INTC Bearish Profit Play — Smart Money Thief Mode Activated?

📌 Asset

INTC — Intel Corporation

NASDAQ Exchange | Stock Market Profit Playbook

🕒 Swing Trade / Day Trade Setup

🧠 Market Bias

📉 Primary Bias: Bearish

Price structure shows weak momentum, failed bullish continuation, and distribution behavior near resistance. This setup favors controlled downside continuation rather than aggressive longs.

🎯 Trade Plan (Bearish Thief Setup)

🔑 Entry

📍 Flexible Entry Zone

➡️ Any favorable price level aligned with bearish confirmation

(Structure break, rejection, or weak bounce)

🛑 Stop Loss

⚠️ Thief-Style SL: 38.00

Dear Ladies & Gentlemen (Thief OGs),

This stop-loss level is NOT a recommendation.

Risk management is your own responsibility — trade at your own risk and adjust according to your strategy.

🎯 Take Profit Zones

Primary Target 🎯

✅ TP-1: 34.00

Extended Target (Escape With Profits) 💰

🚀 TP-2: 31.00

📌 Why TP-2 matters:

Strong historical support zone

Oversold conditions likely to appear

Potential trap & reaction bounce

Broader market correlation suggests profit-taking is wise here

Dear Ladies & Gentlemen (Thief OGs),

These targets are NOT mandatory.

Secure profits based on your own plan and risk tolerance.

🔍 Technical Breakdown (Clean & Professional)

📉 Lower-High Structure intact

❌ Failed bullish continuation

📊 Weak volume on pullbacks

🧠 Distribution near resistance

🔄 Correlation with tech sector weakness

This supports a sell-the-rally / continuation downside approach rather than bottom-fishing.

🔗 Related Pairs & Correlation Watchlist

Keep an eye on these correlated instruments 👇

NASDAQ:NDX (Nasdaq-100)

➝ Tech weakness usually accelerates downside in INTC

NASDAQ:SOXX (Semiconductor ETF)

➝ Sector confirmation strengthens bearish conviction

NASDAQ:NVDA / NASDAQ:AMD

➝ Relative strength comparison — INTC underperformance adds pressure

TVC:DXY (US Dollar Index)

➝ Strong USD often pressures equities, especially tech

📌 If these pairs remain weak, INTC downside probability increases.

🧠 Master Trader Notes

This is NOT financial advice

No prediction — only reaction

Capital preservation > hero trades

Take profits when market offers them

If anything here feels aggressive, scale down — the market will always give another setup.

✨ “If you find value in my analysis, a 👍 and 🚀 boost is much appreciated — it helps me share more setups with the community!”

⚠️ Disclaimer

This is a thief-style trading strategy just for fun.

Educational & entertainment purposes only.

INTC - Cup and Handle A cup and handle pattern forming on this Weekly timeframe for INTC

Good opportunity to get in on these lows before price goes back up, forming the handle

Using the bars pattern to show my thoughts on potential future price action

Cup and Handles are considered bullish patterns

Intel - This behavior is wonderful!🎉Intel ( NASDAQ:INTC ) respects all structure:

🔎Analysis summary:

Just in the end of 2024, Intel perfectly retested a major long term horizontal support. After we then witnessed bullish confirmation, it was so obvious, that Intel will create a move higher. Now, Intel rallied +120% and is ready for a shorter term correction now.

📝Levels to watch:

$45

SwingTraderPhil

SwingTrading.Simplified. | Investing.Simplified. | #LONGTERMVISION

Intel (NASDAQ: $INTC) Eyes SambaNova AI AcquisitionIntel Corporation (NASDAQ: INTC) is reportedly in advanced discussions to acquire AI chip startup SambaNova Systems, a move that could reshape the competitive dynamics of the enterprise AI hardware market. SambaNova provides full-stack AI solutions, including AI appliances, data-center servers, and software, that compete directly with Nvidia’s DGX systems and other AI-accelerated computing platforms.

Rumors about the deal began circulating in October, but recent reports suggest the acquisition is becoming increasingly likely. The two companies already share deep ties: Intel CEO Lip Bu-Tan currently serves as SambaNova’s executive chairman, while Intel Capital has invested in the startup. SoftBank, which took a stake in Intel earlier this year, is also a SambaNova investor, further tightening strategic alignment.

If Intel proceeds with the acquisition, it would gain immediate access to an AI computing segment where it has fallen behind. Currently, Intel lacks a product equivalent to Nvidia’s DGX racks or emerging competitors like GroqRack. SambaNova’s AI racks are already deployed across finance, healthcare, defense, and government sectors, giving Intel a direct entry point into high-performance enterprise AI markets.

Beyond hardware, SambaNova’s software stack and model-training solutions would enhance Intel’s push toward end-to-end AI platforms, supporting its turnaround strategy in both data-center and edge computing. However, the acquisition would still require regulatory approvals and feasibility studies before moving forward.

Technical Analysis

The INTC chart shows a major breakout above a long-term descending trendline, a bullish structural shift after years of compression. Price currently trades around $38–$40, retesting the trendline from above, which now acts as support. A successful retest could trigger continuation toward the $45–$50 zone, with a broader target near the next major resistance at $65–$70.

Volume expansion during the breakout supports bullish momentum, while RSI remains elevated but not overbought, indicating healthy trend strength. Failure to hold above the trendline could send price back to the mid-$20s, but the technical bias remains bullish as long as it stays above $34.c

INTC | Bottoming Process is Progress | BounceIntel Corp. engages in the design, manufacture, and sale of computer products and technologies. It delivers computer, networking, data storage, and communications platforms. The firm operates through the following segments: Client Computing Group (CCG), Data Center and AI (DCAI), Network and Edge (NEX), Mobileye, Accelerated Computing Systems and Graphics (AXG), Intel Foundry Services (IFS), and All Other. The CCG segment consists of platforms designed for notebooks, 2-in-1 systems, desktops, tablets, phones, wireless and wired connectivity products, and mobile communication components. The DCAI segment delivers solutions to cloud service providers and enterprise customers, along with silicon devices for communications service providers and high-performance computing customers. The NEX segment offers computing system solutions from inflexible fixed-function hardware to general-purpose compute, acceleration, and networking devices running cloud native software on programmable hardware. The Mobileye segment develops driving assistance and self-driving solutions. The AXG segment provides products and technologies designed to help customers solve the toughest computational problems. Its products include CPUs for high-performance computing and GPUs targeted for a range of workloads and platforms, from gaming and content creation on client devices to delivering media and gaming in the cloud, and the most demanding high-performance computing and AI workloads on supercomputers. The IFS segment refers to full stack solutions created from the foundry industry ecosystem. The All Other segment represents results from other non-reportable segments and corporate-related charges. The company was founded by Robert Norton Noyce and Gordon Earle Moore on July 18, 1968, and is headquartered in Santa Clara, CA.

Is Intel’s Apple Deal the Ultimate Pivot?Intel (NASDAQ: INTC) stock soared over 116% this year. Reports suggest Apple may use Intel’s foundry by 2027. We analyze the drivers behind this potential resurrection.

Geopolitics & Geostrategy: The Stability Premium

In a volatile world, Intel offers a "stability premium." TSMC’s concentration in Taiwan risks Western supply chains. The US government now holds a ~10% stake in Intel. This actively incentivizes domestic production to secure the grid. Apple chooses Intel to hedge against geopolitical friction. This move aligns with US strategic interests, treating Intel as a sovereign asset.

Management & Leadership: The Tan Effect

CEO Lip-Bu Tan drives a massive cultural shift. He replaced Pat Gelsinger’s engineering vision with operational discipline. Tan prioritizes customer listening, an area where Intel historically struggled. This pivot is paying off. Securing Apple proves Intel is shedding its "arrogant" legacy. It is becoming a true service-oriented foundry.

Technology & Innovation: The 18A-P Advantage

The deal relies on Intel’s **18A-P process technology**. Apple aims to use this for entry-level M-series chips. This validates Intel's aggressive manufacturing roadmap. Additionally, the Trump administration invested $150 million in xLight. This startup develops next-gen lithography lasers to aid chipmaking. It reinforces the ecosystem surrounding Intel’s manufacturing capabilities.

Business Models: The Foundry Pivot

Intel is transforming from a product company to a hybrid foundry. Analysts estimate the Apple deal could generate ~$1 billion annually. However, the "Apple Seal of Approval" is worth far more. It signals to giants like Qualcomm that Intel is ready. It also creates leverage against TSMC’s pricing power.

Final Verdict: The Apple rumors convert Intel into a legitimate turnaround play. US geopolitical interests align with the new leadership. Validated technology suggests Intel’s worst days are likely over.

Bullish Thesis for INTC Intel Stock in 2025If you haven`t bought INTC before the previous earnings:

Now Intel INTC is positioned for a potential turnaround and upside by the end of 2025, driven by strategic leadership changes, foundry business expansion, AI innovation, and favorable geopolitical dynamics. Here’s why INTC could head higher this year:

1. Leadership Transformation and Strategic Vision

The appointment of Lip-Bu Tan as CEO in March 2025 has injected new optimism into Intel’s prospects. Tan is a respected semiconductor industry veteran, and his arrival was met with a 10% jump in INTC’s share price, reflecting renewed investor confidence in the company’s direction.

2. Foundry Business Expansion and Government Support

Intel’s pivot toward a foundry-centric model is gaining momentum. The company is leveraging its U.S.-based manufacturing footprint to attract domestic and international clients, especially as geopolitical tensions and trade restrictions make U.S. chip production more attractive.

There is speculation about strategic partnerships, such as TSMC potentially acquiring a stake in Intel’s foundry operations, which could accelerate technology transfers and client wins.

The U.S. government is likely to continue supporting domestic semiconductor manufacturing through incentives and tariffs, directly benefiting Intel’s foundry ambitions.

3. AI and Next-Gen Product Launches

Intel is aggressively targeting the AI and data center markets. The upcoming Jaguar Shores and Panther Lake CPUs, built on the advanced 18A process node, are set for release in the second half of 2025. These chips will be available not only for Intel’s own products but also for external clients like Amazon and Microsoft, expanding the addressable market.

Intel’s renewed focus on AI accelerators and competitive cost structures could help it regain share in high-growth segments.

4. Financial Resilience and Market Position

Despite recent setbacks, Intel remains a dominant player in the PC CPU market and continues to generate substantial revenue, outpacing some key competitors in the latest quarter.

Analysts have revised their short-term price targets upward, with some projecting INTC could reach as high as $62—a potential upside of over 170% from current levels.

Forecasts for 2025 suggest an average price target in the $40–$45 range, with bullish scenarios pointing even higher if execution on foundry and AI strategies meets expectations.

5. Technical and Sentiment Factors

While technical analysis currently signals caution, the $18.50–$20 zone has provided strong support, and any positive news on foundry contracts or AI wins could catalyze a breakout from current consolidation patterns.

Market sentiment has shifted more positively following the CEO change and strategic announcements, suggesting the potential for a sustained rebound if Intel delivers on its promises.

In conclusion:

Intel’s combination of visionary leadership, foundry expansion, AI innovation, and favorable geopolitical trends sets the stage for a potential stock price recovery by the end of 2025. With analyst targets and investor sentiment turning more bullish, INTC presents a compelling case for upside as it executes its turnaround strategy

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

Intel Corporation and Apple Rumors Ignite a Bullish SurgeIntel Corporation (NASDAQ: NASDAQ:INTC ) jumped more than 10% on Friday as fresh speculation pointed to Apple potentially becoming a major new customer. The rally followed a social media post by TF International Securities analyst Ming-Chi Kuo, who suggested industry surveys indicate Apple could begin sourcing processors from Intel as early as 2027. The possibility marks one of the most meaningful shifts in Intel’s long-term manufacturing prospects in several years.

Investors reacted quickly because a deal with Apple would strengthen confidence in Intel’s turnaround strategy. Despite a strong year—where shares have doubled in value—Intel continues to face questions about its ability to secure durable, high-volume contracts. Apple, known for its vertically integrated chip ecosystem, would represent a major validation of Intel’s foundry ambitions. While neither company has publicly commented, the speculation alone has reinforced bullish sentiment surrounding Intel’s expanding customer pipeline.

Intel’s recent performance is underpinned by several high-profile partnerships, including collaborations with Nvidia (NVDA) in advanced chip manufacturing. These deals, combined with ongoing restructuring efforts, have pushed investor confidence higher. Yet the company remains far from its historical highs, and long-term execution remains the central focus for the market.

Technical Analysis

Intel trades in a strong bullish structure, now pressing against a key descending trendline that has acted as resistance for months. Price is breaking above this level with clear momentum, signaling a possible shift into a broader upward continuation. The next resistance sits at $50, followed by a major level at $68 if bullish pressure sustains. On the downside, support rests at $32, with deeper support at $25 if the trend cools. Current momentum favors the bulls as long as price holds above the breakout zone.

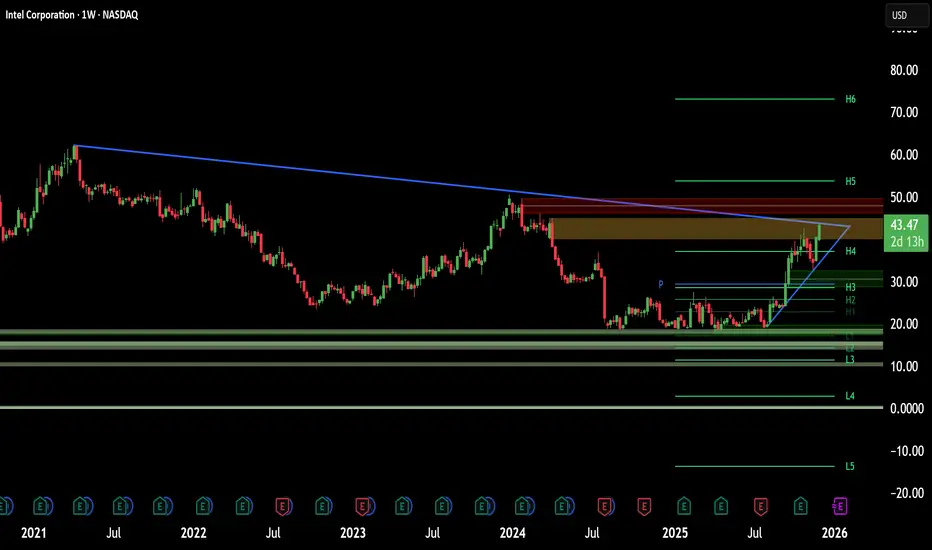

INTC long-term TAIntel is strong, it's a beautiful reversal of a downtrend on a long-term trend. Current uptrend is in correction and there's a distribution going on mid-term, which means now is not the best time to enter but considering strong weekly reversal INTC is something you should keep an eye on and pick up. The blue line for the support has been standing so far, we will see if it's going to be the lowest target in this correction.

Intel (NASDAQ: $INTC) Rises After CEO’s Chinese SpeechIntel (NASDAQ: NASDAQ:INTC ) gained momentum in Wednesday’s trading session after CEO Lip-Bu Tan delivered a speech in Chinese during Intel’s 40th-anniversary celebration in the Chinese market. While the content of the speech was important, the fact that Tan used Chinese for the address made the biggest impact. Investors viewed the gesture as a strategic cultural connection and a positive signal for Intel’s presence in China, helping push shares higher by more than 2%.

Tan used the anniversary event to highlight Intel’s long-term commitment to the Chinese market, emphasizing collaboration, innovation, and partnership during the current surge in artificial intelligence technologies. He called on partners to continue working with Intel to seize new opportunities created by rapid AI growth and evolving semiconductor demand.

The CEO reinforced Intel’s core mission, saying his priority is to create products that solve customers’ most pressing challenges and restore confidence in the broader market. Chinese analysts interpreted the speech as a smart move to appeal directly to local consumers and business partners. While trade restrictions still limit which technologies can be imported into China, the landscape continues to shift along with negotiations and global demand.

Technical Outlook

Intel’s chart currently leans bearish. Price faced rejection at a strong double resistance zone around $39, formed by horizontal resistance and a descending trendline. Bears maintain short-term control unless price breaks above this confluence. If bulls manage a breakout, the next target becomes the previous high near $51. If rejection continues, the next major support sits far lower around $17, making it an important level for long-term buyers.

$INTC is set to go to $50I shared this when Intel was sitting at $23 and I am still bullish.

We pulled back to last quarterly opening price which is $34. I wouldnt be surprised if we bounce from here.

Anyway, sentiment is very positive on Intel so good luck.

First $50 then $100 in a long run.

Intel CEO Takes Charge of AI Division After CTO Joins OpenAiIntel Corporation announced that Chief Executive Officer Lip-Bu Tan will now directly oversee the company’s artificial intelligence operations following the departure of Chief Technology Officer Sachin Katti, who has joined OpenAI. Katti will reportedly lead OpenAI’s compute infrastructure development — a vital role in powering artificial general intelligence (AGI) research and large-scale applications.

The move underscores the fierce competition for top AI talent as chipmakers and AI labs race to develop next-generation computing systems. Intel said in a statement that AI remains a top strategic priority, and the company is doubling down on executing its product roadmap for emerging workloads under Tan’s leadership. However, the transition adds pressure on Intel, which continues to struggle in its foundry business and faces tough competition from Nvidia and AMD in the AI chip segment.

Tan, who became CEO earlier this year, has been reshaping Intel’s leadership structure to accelerate innovation and streamline operations. Analysts view his direct involvement in AI as a signal that Intel aims to close the gap in high-performance computing and reposition itself as a key player in the AI hardware space.

Technical Outlook:

Intel shares are currently trading around $38 after a sharp rally that broke a long-term downtrend line. The chart indicates the stock is now testing major resistance near the $40 level. A breakout and retest above this zone could pave the way for a move toward $68–$70, aligning with the bullish scenario shown. However, if the price fails to hold above the trendline, a correction back toward $28 or even $20 remains possible.

Investors are watching closely as Intel’s leadership changes and AI strategy could determine whether this breakout sustains or fades.

“Intel’s Bullish Structure Building Power for a Breakout Move!”🔥 INTC “Intel Corporation” – The Thief’s Profit Playbook 🕶️💰 (Swing/Day Trade Setup)

⚔️ Plan Overview – Bullish Setup with Thief Precision

The Thief Strategy is in play here — a smart layering entry method designed to steal optimal positions from impatient traders. 🕵️♂️

Our mission: Load, Layer, Loot, and Leave with Profits.

🎯 Entry Plan (Layering Method)

We’re layering multiple buy limits (thief-style) to catch value dips:

Buy Limit Layers: 35.00 💵 → 36.00 💵 → 37.00 💵

(⚙️ You can expand your layers based on your risk tolerance and style — thieves adapt fast.)

💡 Why Layer? Because a pro thief never rushes a vault — we break in step-by-step. This builds position strength while keeping entry efficiency.

🛡️ Stop Loss (Thief’s Escape Hatch)

📉 Stop Loss @34.00

💬 “Dear Ladies & Gentlemen (Thief OG’s) — I’m not recommending you set my SL. You’re the boss of your vault. Manage your own risk, grab the bag, and disappear in profits like a shadow.” 🌑💼

🚀 Target Zone (Profit Extraction Level)

🎯 Main Target: @43.00

📛 Police Barricade @44.00 — strong resistance zone + overbought region + potential bull trap.

🧠 Play it smart — escape clean with gains at 43.00 before the blue lights flash. 🚨

💬 “Dear Ladies & Gentlemen (Thief OG’s) — not recommending you follow my TP blindly. Make your own move, take your profit, and vanish like a ghost.” 👻💸

🧩 Technical Breakdown

Intel (INTC) forming a strong base accumulation near the $35–37 range.

Volume Profile shows liquidity pockets aligning with the layering zones.

RSI hovering mid-levels → room for upside before overbought conditions hit near $43–44.

EMA Confluence: Price reclaiming short-term EMA — early trend reversal signals in motion.

Fundamental Boost: Intel’s AI chip roadmap and cost-optimization headlines add bullish narrative momentum. ⚙️📈

🌍 Related Pairs to Watch (Correlation & Market Sync)

💠 NASDAQ:NVDA – Leader in AI semis; momentum correlation ~0.78 with INTC.

💠 NASDAQ:AMD – Similar sector swing potential; can mirror INTC lag-moves.

💠 NASDAQ:SMH (VanEck Semiconductor ETF) – Sector strength indicator. A breakout above resistance supports INTC’s upside.

💠 NASDAQ:QQQ / NASDAQ:NDX – Tech-heavy indices; bullish bias strengthens chip sector sentiment.

🧭 Correlation Tip: If NVDA or QQQ rallies strongly while INTC consolidates — that’s your thief’s golden signal to layer your entries quietly before the breakout sparks. ⚡

⚙️ Risk Management Wisdom

Never go all-in; layer your risk like a pro.

Keep your SL tight but mind flexible.

Respect zones — police don’t like thieves hanging around too long. 😎

✨ “If you find value in my analysis, a 👍 and 🚀 boost is much appreciated — it helps me share more setups with the community!”

📜 Disclaimer: This is a Thief-Style Trading Strategy shared for educational & fun purposes only. Not financial advice. Trade wisely — stay stealthy. 🕶️

#INTC #Intel #StockMarket #SwingTrade #DayTrading #ThiefStrategy #LayeredEntries #TechnicalAnalysis #NASDAQ #StocksToWatch #AIStocks #TradingViewCommunity #TradingViewEditorsPick #Semiconductors #NVDA #AMD #QQQ #ProfitPlaybook

$INTC - Best in the sector against Trump tariffsIntel is a semiconductor technology giant, renowned for its x86 processors that dominate the CPU segment, top revenue in Q2 2025 came from PC chips (Client Computing Group, ~$7.9B) and server/AI chips (Data Center & AI, ~$3.9B) . Other revenue includes foundry services ($4.4B) and legacy businesses ($1.1B).

But, for the last 4 years the company has experienced one disaster after another:

- Loss of Market Share & Intensified Competition vs AMDs Ryzen and NVIDIA AI GPUs has been major drivers for last 4 years of decline.

- Gross margin dropped to around 38–39% in 2024—a steep fall from pre‑pandemic levels above 60%, while NVIDIA maintained margins above 75%.

- Intel perpetually lagged in transitioning to advanced nodes (7 nm, 5 nm), resulting in costly delays and reduced competitiveness .

- Credit rating downgrade: In August 2025, Fitch downgraded Intel’s credit rating from BBB+ to BBB (negative outlook) due to weak demand and deteriorating profitability . S&P had already downgraded Intel to BB+, and Moody's also cut its rating in 2024 .

Recent events and price action show its time for a buy at these prices.

- Spin-off of Network & Edge (NEX) group: Intel announced the spin-off of its Network and Edge Group (NEX) into an independent entity focused on critical communications and networks, seeking external investors while retaining a major stake .

- Workforce reduction and factory cancellations: Intel confirmed layoffs of ~24,000 employees (~15% of workforce) and cancellation of chip plant projects in Germany and Poland . New CEO Lip-Bu Tan plans to cut the headcount to ~75,000 by year-end 2025 .

- Executive departures and internal reorganization: Three corporate VPs (Kaizad Mistry, Ryan Russell, Gary Patton) announced retirement from manufacturing operations amid deep restructuring . Intel also cut its manufacturing capacity planning and engineering teams as part of an efficiency-driven reorganization .

- Recent key products/services: Intel launched new Xeon 6 CPUs for AI workloads (e.g. Xeon 6776P) and is preparing Panther Lake CPUs (PCs) for 2025 . It also began 18A node production in Arizona and sold part of its Mobileye stake (~$922M) to boost liquidity .

Price/sales: Intel (0.80), AMD (10.3), NVIDIA (29.6), QCOM (3.68)

Wrap-Up

Intel's last four years have been marked by a series of structural, competitive, and strategic challenges—ranging from manufacturing delays to margin erosion and intense pressure from rivals like AMD and NVIDIA. Yet, the tide may be turning. With decisive actions like major cost-cutting initiatives, new AI-focused products, and progress in advanced node production, Intel is signaling a strategic pivot. Trading at a deep discount relative to peers based on the price-to-sales ratio, the stock reflects much of the past negativity. For investors seeking a long-term turnaround play in the semiconductor sector, now could be the moment to re-evaluate Intel’s potential.

Let’s see if this chip giant can turn the corner. Cheers!

Pablin

INTC Target Hit, Now Showing Another Bullish Setup!INTC - CURRENT PRICE : 41.53

My earlier INTC buy call has reached its projected targets. The previous analysis is shared below for reference.

Technical Highlights

1) New 52-week High – Price has broken into a fresh yearly high, confirming strong bullish momentum.

2) Pennant Breakout – The breakout from a bullish pennant pattern suggests continuation of the prior uptrend, with a potential target of $49 based on the pattern projection.

3) Golden Cross Intact – The 50-day EMA remains above the 200-day EMA, maintaining the long-term bullish bias.

4) RSI in Bullish Territory – RSI remains above 70, indicating strong momentum and persistent buying strength.

ENTRY PRICE : 40.00 - 42.00

FIRST TARGET : 45.00

SECOND TARGET : 49.00

SUPPORT : 36.43 (the low of 23 OCTOBER 2025 candle)

Next Volatility Period: Around November 5th

Hello, fellow traders!

Follow us to get the latest updates quickly.

Have a great day!

-------------------------------------

(INTC 1M Chart)

The price has broken above the 28.93 level, indicating a long-term uptrend.

The basic trading strategy is to buy in the DOM(-60) ~ HA-Low range and sell in the HA-High ~ DOM(60) range.

Accordingly, the resistance zones are 47.33-49.82 and 55.20-56.48.

The 47.33-49.82 range corresponds to the HA-High ~ DOM(60) range formed on the 12M chart.

Therefore, we should consider the overall resistance zone to be 47.33-56.48 and develop a response strategy.

-

(1W chart)

We should examine whether the price can sustain above the downtrend line (1) and rise along the uptrend line (2).

Since the HA-High indicator on the 1W chart is formed at 45.36, the key question is whether the price can rise above 45.36 and maintain its position.

-

(1D chart)

If the upward trend fails along the uptrend line (2), we should check for support near 36.92.

If not, there's a chance the M-Signal indicator on the 1W chart will touch it.

If the price remains above the HA-High ~ DOM (60) range (35.50-36.92) on the 1D chart, a stepwise uptrend is likely.

However, the price must break above the HA-High ~ DOM (60) range on the 1W and 1M charts.

Therefore, the first hurdle is whether the price can rise above 45.36 and maintain its position.

The next period of volatility will be around November 5th.

After this period of volatility, we need to see if the price stays above the downtrend line (1) and rises along the uptrend line.

-

Thank you for reading.

We wish you successful trading.

--------------------------------------------------

INTC Intel Corporation Options Ahead of EarningsIf you haven`t bought the dip on INTC:

Now analyzing the options chain and the chart patterns of INTC Intel Corporation prior to the earnings report this week,

I would consider purchasing the 48usd strike price Calls with

an expiration date of 2026-3-20,

for a premium of approximately $2.75.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Intel - The parabolic bullrun!💸Intel ( NASDAQ:INTC ) rallies significantly:

🔎Analysis summary:

After Intel retested a major support a couple of months ago, we already witnessed an expected rally of about +100%. Considering that the next horizontal resistance is about +25% higher, a bullrun continuation remains totally likely. Intel just perfectly plays out.

📝Levels to watch:

$45

SwingTraderPhil

SwingTrading.Simplified. | Investing.Simplified. | #LONGTERMVISION