Is the Fortress of Precision Oncology Crumbling?In late 2025, the global diagnostics industry is poised for a potential paradigm shift as rumors circulate regarding Abbott Laboratories' advanced negotiations to acquire Exact Sciences. A favorable macroeconomic pivot catalyzes this potential consolidation; the Federal Reserve’s decision to cut interest rates has thawed the "capital winter," enabling cash-rich conglomerates like Abbott to leverage debt for high-value acquisitions. While Exact Sciences has demonstrated financial fortitude with record Q3 2025 revenue of $851 million and a transition to significant profitability, the proposed deal is interpreted as a strategic necessity rather than a simple exit. Abbott seeks a durable post-pandemic growth engine, while Exact Sciences requires a partner with a "fortress balance sheet" to navigate an era of "exponential risk".

Despite its market leadership, Exact Sciences is contending with deepening vulnerabilities that threaten its independence. The company’s intellectual property moat has been breached following a critical defeat in patent litigation against Geneoscopy, which invalidated key claims protecting Cologuard and opened the door to immediate competition. Furthermore, the company faces significant geopolitical exposure due to a heavy reliance on Chinese supply chains for essential chemical precursors, a fragility that could be catastrophic in the event of heightened U.S.-China tensions. In a defensive maneuver, Exact Sciences has already begun diversifying its technological bets by licensing Freenome’s blood-based screening technology, effectively hedging against the potential erosion of its own stool-based testing monopoly.

The merger’s long-term value thesis rests on scaling innovation and unlocking international markets. Exact Sciences holds a promising pipeline, including Cologuard Plus, which improves specificity to 94% and the multi-cancer early detection tool, Cancerguard. However, the company has historically struggled to export Cologuard due to high costs and incompatible foreign screening guidelines. An acquisition would allow Exact Sciences to leverage Abbott’s massive global infrastructure to bypass these barriers, "friend-shore" vulnerable supply chains, and navigate complex regulatory frameworks like the EU’s Medical Device Regulation. Ultimately, this transaction represents a flight to safety, merging Exact’s scientific innovation with Abbott’s logistical power to secure the future of cancer diagnostics.

Intellectualproperty

Can One Shot Silence a Disease Forever?Benitec Biopharma has emerged from clinical obscurity to platform validation with unprecedented Phase 1b/2a trial results showing a 100% response rate across all six patients treated with BB-301, their gene therapy for Oculopharyngeal Muscular Dystrophy (OPMD). This rare genetic disorder, characterized by progressive swallowing difficulties that can lead to fatal aspiration pneumonia, has no approved pharmaceutical treatments. Benitec's proprietary "Silence and Replace" approach uses DNA-directed RNA interference to simultaneously shut down production of the toxic mutant protein while delivering a functional replacement, a sophisticated dual-action mechanism delivered via a single AAV9 vector injection. The clinical data revealed dramatic improvements, with one patient experiencing an 89% reduction in swallowing burden, essentially normalizing their eating experience. The FDA's subsequent Fast Track Designation for BB-301 underscores the regulatory conviction in this approach.

The company's strategic positioning extends well beyond a single asset. November 2025 marked a transformative capital event with a $100 million raise at $13.50 per share, nearly triple the $4.80 pricing from just 18 months prior, anchored by a $20 million direct investment from Suvretta Capital, which now controls approximately 44% of outstanding shares. This institutional validation, coupled with a fortress balance sheet providing runway into 2028-2029, has fundamentally de-risked the investment thesis. The manufacturing partnership with Lonza ensures scalable, GMP-compliant production while avoiding geopolitical supply chain risks that plague competitors reliant on Chinese CDMOs. With robust IP protection extending into the 2040s and Orphan Drug Designation providing additional market exclusivity, Benitec operates in a competitive vacuum, as no other clinical-stage programs target OPMD.

The broader implications position Benitec as a platform leader rather than a single-product company. The "Silence and Replace" architecture addresses a fundamental limitation of traditional gene therapy: it can treat autosomal dominant disorders where toxic mutant proteins render simple gene replacement ineffective. This unlocks an entire class of previously undruggable genetic diseases. The company's leadership, including CEO Dr. Jerel Banks (who brings both M.D./Ph.D. credentials and biotechnology equity research experience) and board member Dr. Sharon Mates (who guided Intra-Cellular Therapies to a $14.6 billion acquisition by J&J), suggests preparation for either commercial scale-up or strategic acquisition. With potential pricing power in the $2-3 million range per treatment based on comparable gene therapies, and an enterprise value of approximately $250 million against a multi-billion dollar revenue opportunity, Benitec represents a compelling asymmetric risk-reward profile at the vanguard of curative genetic medicine.

Can One Company Control Computing's Future?Google has executed a strategic transformation from a digital advertising platform to a full-stack technology infrastructure provider, positioning itself to dominate the next era of computation through proprietary hardware and breakthrough scientific discoveries. The company's vertical integration strategy centers on three pillars: custom Tensor Processing Units (TPUs) for AI workloads, quantum computing breakthroughs with verifiable advantages, and Nobel Prize-winning drug discovery capabilities through AlphaFold. This approach creates formidable competitive barriers by controlling foundational computational infrastructure rather than relying on commodity hardware.

The TPU strategy exemplifies Google's infrastructure lock-in model. By designing specialized chips optimized for machine learning tasks, Google achieved superior energy efficiency and performance scaling compared to general-purpose processors. The company's multibillion-dollar deal with Anthropic, deploying up to one million TPUs, transforms a potential cost center into a profit generator while locking competitors into Google's ecosystem. This technical dependence makes migration to rival platforms financially prohibitive, ensuring Google monetizes a significant portion of the generative AI market through its cloud services regardless of which AI models succeed.

Google's quantum computing achievement represents a paradigm shift from theoretical benchmarks to practical utility. The Willow chip's "Verifiable Quantum Advantage" demonstrates a 13,000-times speedup over classical supercomputers in physics simulations, with immediate applications in molecular structure mapping for drug discovery and materials science. Meanwhile, AlphaFold delivers quantifiable economic impact, reducing Phase I drug development costs by approximately 30% from over $100 million to $70 million per candidate. Isomorphic Labs has secured nearly $3 billion in pharmaceutical partnerships, validating this high-margin revenue stream independent of advertising.

The geopolitical implications are profound. Google holds the second-highest number of quantum technology patents globally, with strategic IP covering essential scaling technologies like chip tiling and error correction. This intellectual property portfolio creates a technical chokepoint, positioning Google as a mandatory licensing partner for nations seeking to deploy quantum technology. Combined with the dual-use nature of quantum computing for both commercial and military applications, Google's dominance extends beyond market competition to national security infrastructure. This convergence of proprietary hardware, scientific breakthroughs, and IP control justifies premium valuations as Google transitions from cyclical advertising dependence to an indispensable deep-tech infrastructure provider.

Is IBM Building an Unbreakable Cryptographic Empire?IBM has positioned itself at the strategic intersection of quantum computing and national security, leveraging its dominance in post-quantum cryptography to create a compelling investment thesis. The company led the development of two of the three NIST-standardized post-quantum cryptographic algorithms (ML-KEM and ML-DSA), effectively becoming the architect of global quantum-resistant security. With government mandates like NSM-10 requiring federal systems to migrate by the early 2030s, and the looming threat of "harvest now, decrypt later" attacks, IBM has transformed geopolitical urgency into a guaranteed, high-margin revenue stream. The company's quantum division has already generated nearly $1 billion in cumulative revenue since 2017—more than tenfold that of specialized quantum startups—demonstrating that quantum is a profitable business segment today, not merely an R&D cost center.

IBM's intellectual property moat further reinforces its competitive advantage. The company holds over 2,500 quantum-related patents globally, substantially outpacing Google's approximately 1,500, and secured 191 quantum patents in 2024 alone. This IP dominance ensures future licensing revenue as competitors inevitably require access to foundational quantum technologies. On the hardware front, IBM maintains an aggressive roadmap with clear milestones: the 1,121-qubit Condor processor demonstrated manufacturing scale in 2023, while researchers recently achieved a breakthrough by entangling 120 qubits in a stable "cat state." The company targets deployment of Starling, a fault-tolerant system capable of running 100 million quantum gates on 200 logical qubits, by 2029.

Financial performance validates IBM's strategic pivot. Q3 2025 results showed revenue of $16.33 billion (up 7% year-over-year) with EPS of $2.65, beating forecasts, while adjusted EBITDA margins expanded by 290 basis points. The company generated a record $7.2 billion in year-to-date free cash flow, confirming its successful transition toward high-margin software and consulting services. The strategic partnership with AMD to develop quantum-centric supercomputing architectures further positions IBM to deliver integrated solutions at exascale for government and defense clients. Analysts project IBM's forward P/E ratio may converge with peers like Nvidia and Microsoft by 2026, implying potential share price appreciation to $338-$362, representing a unique dual thesis of proven profitability today combined with validated high-growth quantum optionality tomorrow.

Can a Wristband Read Your Mind Before You Move?Wearable Devices Ltd. (NASDAQ: WLDS) is pioneering a radical shift in human-computer interaction through its proprietary neural input interface technology. Unlike invasive brain-computer interfaces or basic gesture-recognition systems, the company's Mudra Band and Mudra Link decode subtle neuromuscular signals at the wrist, enabling users to control digital devices through intent rather than physical touch. What distinguishes WLDS from competitors like Meta's surface electromyography (sEMG) solutions is its patented capability to measure not just gestures, but quantifiable physical forces, including weight, torque, and applied pressure, opening applications far beyond consumer electronics into industrial quality control, extended reality (XR) environments, and mission-critical defense systems.

The company's strategic value lies not in hardware sales but in its planned evolution into a neural data intelligence platform. WLDS is executing a four-phase roadmap that transitions from consumer adoption (Phases 1-2) to data monetization through its Large Motor-Unit Action Potential Model (LMM), a continuously learning biosignal platform expected to launch by 2026. This proprietary dataset, generated from millions of user interactions, positions WLDS to offer high-margin licensing services to OEMs and enterprise clients, particularly in predictive health monitoring and cognitive analytics. With partnerships including Qualcomm and TCL-RayNeo, the company is building the infrastructure for what it envisions as the industry-standard neural interaction platform.

However, WLDS operates in a market defined by extraordinary potential and substantial execution risk. The global brain-computer interface market is projected to reach $6.2 billion by 2030, yet current wireless neural interface revenues remain modest at an estimated $1.5 billion by 2035, suggesting either a massive untapped opportunity or significant adoption barriers. The company's lean 26-34 person operation, $522,000 in 2024 revenue, and extreme stock volatility (Beta: 3.58, 52-week range: $1.00-$14.67) underscore its early-stage profile. Success hinges entirely on converting consumer adoption into the proprietary biosignal data required to train the LMM platform, which in turn must prove sufficiently valuable to command enterprise licensing agreements at scale.

WLDS represents a calculated bet on the convergence of AI, wearable computing, and neurotechnology, a company that could either establish the foundational infrastructure for touchless interaction across XR, healthcare, and defense sectors or struggle to bridge the gap between technological capability and market validation. Its military contracts and robust IP portfolio covering force-measurement capabilities provide technical credibility, but the path to ubiquitous platform adoption (Phase 4) requires flawless execution across consumer seeding, data accumulation, and B2B conversion, a multiyear journey with no guarantee of arrival.

Can Vertical Integration Ground a Flying Dream?Joby Aviation faces a critical convergence of structural vulnerabilities that threaten its ambitious air taxi vision. The company pursues an all-in vertical integration strategy, controlling everything from manufacturing to operations, which demands extraordinary capital expenditure. With quarterly losses exceeding $324 million and cash reserves depleting rapidly, Joby must continually raise equity financing, perpetually diluting shareholders. This high-burn model collides with a punishing macroeconomic environment where elevated interest rates dramatically increase the cost of capital for pre-revenue ventures, multiplying financial pressure at precisely the wrong moment.

Regulatory friction compounds these economic headwinds. The FAA has requested additional safety documentation, pushing U.S. commercial deployment potentially beyond 2027 and severely undermining financial projections. While Joby has achieved technical milestones like preparing for Type Inspection Authorization flight testing, the market correctly recognizes that hardware readiness cannot overcome bureaucratic inertia. The company's $125 million Blade acquisition, intended to fast-track market entry, now sits idle as an expensive, non-performing asset awaiting regulatory clearance. Meanwhile, Joby faces over $100 million in potential liabilities from Aerosonic's trade secret lawsuit regarding critical air data probes, with the court already denying Joby's motion to dismiss.

The confluence of these challenges creates a severe risk-adjusted valuation problem. Analysts project an average 30% downside from current trading levels, with bearish targets suggesting potential declines exceeding 65%. Joby's international pivot to Dubai and Japan represents a geopolitical hedge against FAA delays but introduces regulatory complexity by reversing the preferred certification sequence. The company's acquisitions of autonomous flight technology (Xwing) and hybrid power systems (H2Fly) may diffuse engineering focus away from core certification objectives. With profitability unlikely before 2027-2028 and existential threats spanning legal, regulatory, and financial domains, the market is rationally discounting Joby's prospects despite its technical achievements.

Can Quantum Annealing Reshape Global Power?D-Wave Quantum Inc. has emerged as a distinctive player in commercial quantum computing by focusing on immediate utility through quantum annealing rather than waiting for fault-tolerant gate systems. The company's Advantage2™ system, featuring over 4,400 qubits, delivers production-grade solutions for complex optimization problems today, generating measurable ROI for clients like Ford Otosan, which reduced vehicle production scheduling from 30 minutes to under five minutes. This hybrid strategy of monetizing mature annealing technology while developing gate-model capabilities positions D-Wave to capture revenue now while hedging technological risk for the future. The quantum computing market's projected growth to $20.20 billion by 2030 (41.8% CAGR) and JPMorgan Chase's $1.5 trillion initiative, which explicitly includes quantum as a critical security technology, validate this sector beyond speculative investment.

D-Wave's recent scientific milestone, demonstrating "beyond-classical computation" on a magnetic materials simulation published in Science, marks a pivotal moment. The Advantage2™ prototype completed in minutes what would have required nearly one million years on classical supercomputers like Frontier, representing the first quantum supremacy claim on a commercially relevant, real-world problem. While classical researchers dispute aspects of the claim, the peer-reviewed validation drives enterprise confidence and accelerates bookings across manufacturing, pharmaceuticals, and energy sectors. Japan Tobacco's proof-of-concept using D-Wave's quantum-AI workflow generated drug candidates with superior properties compared to classical methods, addressing the pharmaceutical industry's 90%+ failure rate crisis.

Geopolitically, D-Wave has strategically embedded itself in European digital sovereignty initiatives, co-founding Italy's Q-Alliance to establish what aims to be the world's most powerful quantum hub. This dual-vendor partnership with IonQ provides Italy and the EU immediate access to D-Wave's production-ready annealing technology while hedging against future gate-model capabilities. Additional strategic deployments include Swiss Quantum Technology's €10 million investment and extended partnerships with Aramco Europe. The company's concentrated portfolio of 208 patent families in superconducting annealing creates defensible IP barriers, though significant risks remain: wider-than-expected losses despite 40% revenue growth, the Advantage2™ system's high cost barrier to adoption, and critical dependence on rare helium-3 supplies subject to geopolitical volatility.

Can Machines Rewrite the DNA of Discovery?Recursion Pharmaceuticals is redefining the boundaries of biotech by positioning itself not as a traditional drug developer, but as a deep-technology platform built on artificial intelligence and automation. Its mission: to collapse the pharmaceutical industry’s notoriously slow and costly research model - one that can demand up to $3 billion and 14 years for a single approved drug. Through its integrated platform, Recursion aims to transform this inefficiency into a scalable engine for global health innovation, where value is driven not by one-off products but by the speed and reproducibility of discovery itself.

At the core of this transformation lies BioHive-2, a proprietary supercomputer powered by NVIDIA’s DGX H100 architecture. This computational behemoth fuels Recursion’s ability to iterate biological experiments at a pace that competitors cannot match. In collaboration with MIT’s CSAIL, Recursion co-developed Boltz-2, a biomolecular foundation model capable of predicting protein structures and binding affinities in seconds rather than weeks. By open-sourcing Boltz-2, the company has effectively shaped the scientific ecosystem around its standards, granting access to the community while retaining the true moat: its proprietary biological data and infrastructure.

Beyond its technological might, Recursion’s growing clinical pipeline provides proof of concept for its AI-driven discovery process. Early successes, including REC-617 (a CDK7 inhibitor) and REC-994 (for cerebral cavernous malformations), illustrate how computational prediction can rapidly yield viable drug candidates. The company’s ability to compress the time-to-market curve doesn’t merely improve profitability; it fundamentally redefines which diseases can be economically targeted, potentially democratizing innovation in previously neglected therapeutic spaces.

Yet with such power comes strategic responsibility. Recursion now operates at the intersection of biosecurity, data sovereignty, and geopolitics. Its commitment to rigorous compliance frameworks and aggressive global IP expansion underscores its dual identity as both a scientific and strategic asset. As investors and regulators watch closely, Recursion’s long-term value will hinge on its ability to transform computational speed into clinical success - turning the once-impossible dream of AI-driven drug discovery into an operational reality.

Can Silicon Nanowires Redefine America's Battery Future?Amprius Technologies has positioned itself at the convergence of breakthrough materials science and national security imperatives, developing the world's highest energy density lithium-ion batteries through proprietary silicon nanowire technology. The company's batteries deliver up to 450 Wh/kg with targets exceeding 500 Wh/kg - nearly double the performance of conventional graphite-based cells - by solving silicon's historical expansion problems through a unique rooted nanowire architecture that allows internal expansion without structural degradation.

The strategic value extends beyond pure technology metrics. Amprius has secured $50 million in federal funding under Biden's Bipartisan Infrastructure Law and maintains critical defense contracts, including repeat orders totaling over $50 million from unmanned aerial systems manufacturers. This government backing reflects the company's role in domestic supply chain security, as its 100% silicon anode technology reduces reliance on graphite imports while establishing gigawatt-hour manufacturing capacity in Colorado. The Department of Energy's investment essentially validates Amprius as a strategic national asset in the race for advanced battery independence.

Financially, the company has demonstrated rapid acceleration with H1 2025 revenue of $26.4 million already surpassing all of 2024, while achieving a crucial 9% positive gross margin that signals viable unit economics. However, the path to mass market viability remains challenging, with estimated capital expenditures of $120-150 million per GWh of capacity highlighting the complexity of scaling nanowire manufacturing. Wall Street maintains unanimous "Strong Buy" ratings with price targets above $11.67, though recent insider selling following the stock's 1,100% surge raises questions about current valuation versus near-term execution risks.

The company's hybrid manufacturing strategy - leveraging over 1.8 GWh of international contract capacity while building domestic production - reflects a calculated approach to managing capital requirements while capturing immediate high-margin defense and aerospace opportunities. Success hinges on the operational launch of their Colorado facility in H1 2025 and the ability to translate their performance advantages into cost-competitive production for broader electric vehicle markets.

Can Single-Use Robotics Topple Surgical Giants?Microbot Medical Inc. (NASDAQ: MBOT) has experienced a dramatic stock surge from $0.85 to $4.67, driven by the convergence of multiple strategic milestones that signal a potential disruption in the surgical robotics market. The company's flagship LIBERTY® Endovascular Robotic System received FDA 510(k) clearance in September 2025, marking the first single-use, remotely operated robotic solution for peripheral endovascular procedures. This breakthrough represents more than regulatory approval; it validates a fundamentally different business model that challenges the capital-intensive approach dominating the industry.

The LIBERTY® System's disruptive potential lies in its unique value proposition: a disposable robotic platform that eliminates the multi-million-dollar upfront costs that have limited robotic adoption to less than 1% of endovascular procedures. The system demonstrated a 92% reduction in physician radiation exposure and achieved a 100% success rate in clinical trials with zero device-related adverse events. By offering universal compatibility with existing instruments and requiring no dedicated operating room infrastructure, Microbot is positioning itself to capture a massive underserved market segment—smaller hospitals, ambulatory surgery centers, and clinics that have been previously excluded from robotic innovation due to cost barriers.

Strategic elements supporting this momentum include a robust intellectual property portfolio with 12 granted patents and 57 pending applications, particularly a modularity patent that could expand the addressable market from 2.5 million to over 6 million procedures annually. The company secured up to $92.2 million in financing through a sophisticated multi-tranche structure, providing critical operational runway for its Q4 2025 U.S. commercial launch. Despite maintaining R&D operations in Israel during ongoing geopolitical tensions, Microbot has demonstrated operational resilience by keeping all development activities on schedule.

The company's "procedure-based" strategy, reinforced by acquisitions such as Nitiloop Ltd.'s FDA-cleared microcatheters, positions it to create comprehensive solution kits rather than competing solely on robotic hardware. While analysts maintain a consensus price target of $12.24 compared to the current $3.42 trading price, the ultimate test will be market adoption rates and commercial execution in a space where established players like Intuitive Surgical have built formidable ecosystems around high-cost capital equipment models.

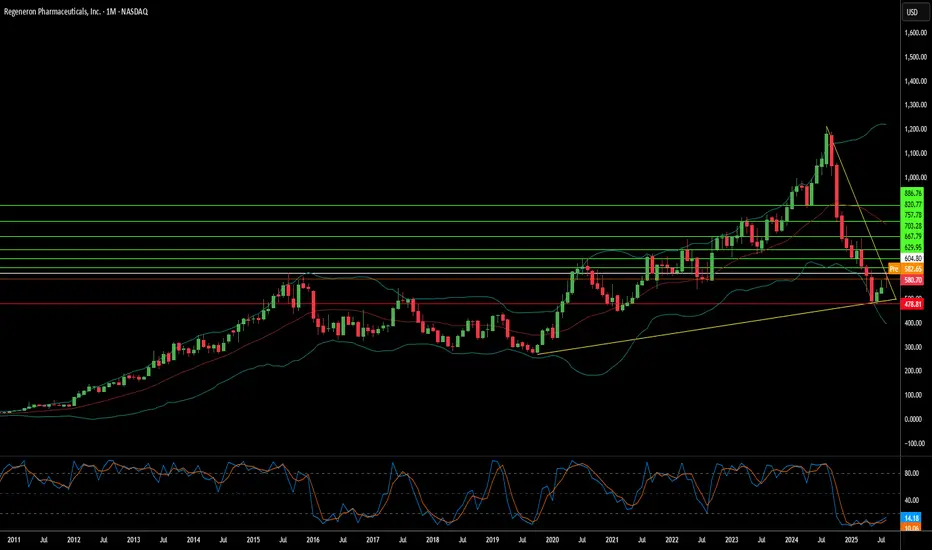

Can Innovation Survive Manufacturing Chaos?Regeneron Pharmaceuticals stands at a fascinating crossroads, embodying the paradox of modern biotechnology: extraordinary scientific achievement shadowed by operational vulnerability. The company has successfully transformed from a blockbuster-dependent enterprise into a diversified biopharmaceutical powerhouse, driven by two key engines. Dupixent continues its remarkable ascent, achieving 22% growth and reaching $4.34 billion in Q2 2025. Meanwhile, the strategic transition from legacy Eylea to the superior Eylea HD demonstrates forward-thinking market positioning, despite apparent revenue declines.

The company's innovation engine supports its aggressive R&D strategy, investing 36.1% of revenue, nearly double the industry average, into discovery and development. This approach has yielded tangible results, with Lynozyfic's FDA approval marking Regeneron's first breakthrough in blood cancer, achieving a competitive 70% response rate in multiple myeloma. The proprietary VelociSuite technology platform, particularly VelocImmune and Veloci-Bi, creates a sustainable competitive moat that competitors cannot easily replicate, enabling the consistent generation of fully human antibodies and differentiated bispecific therapies.

However, Regeneron's scientific triumphs are increasingly threatened by third-party manufacturing dependencies that have created critical vulnerabilities. The FDA's second rejection of odronextamab, despite strong European approval and compelling clinical data, is due to manufacturing issues at an external facility, rather than scientific deficiencies. This same third-party bottleneck has delayed crucial Eylea HD enhancements, potentially allowing competitors to gain market share during a pivotal transition period.

The broader strategic landscape presents both opportunities and risks that extend beyond manufacturing concerns. Although the company's strong victories in intellectual property cases against Amgen and Samsung Bioepis showcase effective legal defenses, the proposed 200% drug tariffs and industry-wide cybersecurity breaches, such as the Cencora incident impacting 27 pharmaceutical companies, highlight significant systemic vulnerabilities. Regeneron's fundamental strengths-its technological platforms, diverse pipeline spanning oncology to rare diseases, and proven ability to commercialize breakthrough therapies-position it for long-term success, provided it can resolve the operational dependencies that threaten to derail its scientific achievements.

Royalties and Copyright: How DAOs Will Facilitate These in Web3So the reality of the NFT marketplace right now is that there is no way to technically enforce royalty payments for artists since it's up to the platform to decide to honor that or not. (Search the phrase online and you'll see that it's the talk of the industry right now - this includes the original artist for those monkey jpegs too, btw - she was left out of the equity deal and basically got nothing.) There might be a way to close this loophole at some point but for now, it's something both artists and collectors need to be mindful of if they really care about the ideals of Web3.

The blockchain can be a double-edged sword in this way - on one hand, everyone has more autonomy and freedom to do what they want, but it's probably unwise to assume everyone will be doing things in good faith. Some platforms are already advertising them ripping artists off as a 'discount". And there's nothing stopping them from undercutting other platforms who actually are honoring the royalties in good faith.

If mp3 pirating apps and other Web2 content sites are any indication, we know that the tech industry as a whole tends to be more sympathetic to the one doing the undercutting than the ones honoring the deals...because "disruption" or something. There's an inherent distrust of collective action as a whole in the ethos of Silicon Valley right now, though that's another issue altogether. Either way, a lot of the money made in Web2 were done on the backs of artists and creatives basically doing things for free. That is how the business model works, at the end of the day.

But this is also the reason why we have fake-news, false advertising, dystopian narratives everywhere, and why many techies don't get the status/prestige they think they deserve despite making so much money, working long hours, and screaming a lot on social media. There's 0 chance that you'll leave a positive legacy if you're constantly screwing over the folks who're writing the songs, after all.

The "Web3" movement is more fragile than a lot of people think, since once you start looking into the details you realize how easily this whole thing could just become another iteration of Web2 with crypto-buzzwords thrown on top. Bitcoin is already there, Ethereum also on its way (we'll see if the merge will help them act together), Dogecoin wants to do the right thing but doesn't know how. Aside from the good doggie Doge (🐕🥰), the recession taking these projects down a peg or two wouldn't be a bad thing, imo - it'll open up avenues for more serious projects in the altcoin category to emerge. (I do like Tezos in this regard, which I covered a few times here too.)

--

When I was in the Bay Area a few years ago, I still remember a few of my friends taking "gigs" where the job was to follow some rich family around and create albums/pictures of them - for their "legacy". Beyond cringey 😬 and usually a mask for the deeper personal issues that was lurking underneath. Not to mention Silicon Valley's obsession with the Singularity, anti-aging products, and artificial-intelligence that is an implicit confession that because they will definitely not be remembered after one generation, everything must be done in order to keep their influence artificially alive. That's the sort of ethos that we're living in right now - and also why I felt like I had to leave that place, just in order to maintain my sanity. (That latter part is TBD but can't imagine how worse it'd be if I was still there, honestly.)

But it's the sort of race-to-the-bottom, screw-the-creator-at-all-costs types of "content" that are perfect candidates for ending up on the trash-pile of history - which will probably include most Web2 platforms and its affiliated leaders right now. If people wanted boredom, hopelessness and gaslighting, all they have to do is go to the status quo - Web3 was supposed to be arbiter to bring something different, not more of the same. Most of the smart ones in the large, powerful institutions saw the writing on the wall and left years ago - the ones still hanging on are probably the first to go when the recession hits and people's priorities start to change.

So what can be done? Well, the good news is that DAOs and blockchains allow us to organize and track things objectively, artists can collectively judge whether or not a platform is doing things in accordance to their interests and needs. In a few years, I think I can see these DAOs - neither a private company nor a traditional union - influencing the market by making recommendations to both artists and collectors out there about which platforms to use...and if the platforms want to actually survive long-term, they have to comply.

This is one very practical application of a DAO (which functions similar to industry associations, trade-unions, performance rights organizations, or standard-settings orgs like ICANN or W3C) and there are many more to come - though it will require the artist to take a more active role in defending their self-interests more than they have in recent history. I know that there's a lot of artists out there who have abandoned all hope at this point - but the time to give up isn't now. Some of history's biggest achievements were done through DAO-like orgs and the idea of it becoming a thing in the near future should be a good thing, over all.

The blockchain is there for us to organize ourselves, hold people and parties accountable, and most importantly GET ARTISTS PAID. That's the thing that will solve the world's "fake news" problem, and the overall malaise and hopelessness that we're experiencing now as a whole. Real art doesn't just parrot an agenda - it tells the truth, after all. The work is just beginning now, if anything.

typed.art

FING_B - CHINA X US G20 - Catalyst Play (Intellectual property)FING_B - CHINA X US G20 - Catalyst Play (Intellectual property)

LSCC - Gateway for video LSCC - $1B Mkt Cap, 1.2B Ent Value, no dividend. Profitable earnings all 2018, not prior. Has IP, growth, strong technology future in smart connectivity, video, and SaS, or high value logic devices. Strong recovery from recent drop at 238 Fibretracement and climbing. About to report strongest earnings, albeit $0.08/share, which is up 700% over prior Q1 yr/yr. Dropped 0.69% on Feb 1 vs NASDAQ avg. down 0.25% and Dow up 0.26% (mostly lg cap). 4Q profitable in 2009, 2013-2014 along with 2018. Current PEG ratio is 1.72. Semiconductor is in top 35% of segments currently. Would have been up 41% if bought at recent low of $5.50 area.

Lattice Semiconductor Corporation is a United States-based company, which develops semiconductor technologies that it monetizes through products, solutions and licenses. The Company operates through two segments: the core Lattice (Core) business, which includes intellectual property (IP) and semiconductor devices, and Qterics, a discrete software-as-a-service business unit in the Lattice legal entity structure. The Company is a provider of customizable smart connectivity solutions based on its low power field programmable gate array (FPGA), video application specific standard product (ASSP), 60 gigahertz millimeter wave, and IP products to the consumer, communications, industrial, computing and automotive markets across the world. Its products include iCE40 Ultra/UltraLite, iCE40 LP/HX/LM, MachXO3, MachXO2, MachXO, HDMI Transmitters, HDMI Receivers, USB Type-C Port Controllers, Port Processors, Analog to HDMI/MHL Converters, MHL Transmitters, UltraGig 6400 and 802.11ad Chipsets.