Is Red Cat the Drone King America Has Been Waiting For?Red Cat Holdings (RCAT) stands at the epicenter of a transformative moment in defense technology. The December 2025 FCC ban on Chinese drone manufacturers DJI and Autel has effectively eliminated Red Cat's primary competition, creating a protected market for domestic producers. With Q3 fiscal 2025 revenue surging 646% year-over-year and a balance sheet fortified with over $212 million in cash, Red Cat has positioned itself as the primary beneficiary of America's pivot toward sovereign defense supply chains. The company's "Blue UAS" certification and inclusion on NATO's procurement catalog provide immediate access to both domestic and allied defense markets at a critical moment of global rearmament.

The company's technological architecture differentiates it from competitors through integrated systems spanning air, land, and sea domains. The "Arachnid" family, including the Black Widow quadcopter, Edge 130 hybrid VTOL, and FANG strike drone, creates a closed-loop ecosystem enhanced by partnerships with Palantir for GPS-denied navigation and Doodle Labs for anti-jamming communications. Red Cat's Visual SLAM technology enables autonomous operation in contested electromagnetic environments, directly addressing Pentagon requirements under the Replicator initiative for "attritable mass" autonomous systems. The recent partnership with Apium Swarm Robotics advances one-to-many drone control, multiplying the combat effectiveness of individual operators.

Strategic acquisitions of FlightWave and Teal Drones have rapidly expanded Red Cat's capabilities while maintaining strict supply chain sovereignty. The company's selection as a finalist for the Army's Short Range Reconnaissance Tranche 2 program validates its tactical systems for infantry deployment. With NATO allies ramping up defense spending and the Ukraine conflict demonstrating voracious demand for small unmanned systems, Red Cat faces a multi-year secular tailwind. The convergence of regulatory protection, technological differentiation, financial strength, and geopolitical necessity positions Red Cat not merely as a defense contractor but as a cornerstone of America's robotic warfare infrastructure for the coming decade.

Manufacturing

Can Japan's Steel Giant Win the Green War?Nippon Steel Corporation stands at a critical crossroads, executing a radical transformation from domestic Japanese producer to global materials powerhouse. The company targets 100 million tons of global crude steel capacity under its "2030 Medium- to Long-term Management Plan," seeking 1 trillion yen in annual underlying business profit. However, this ambition collides with formidable obstacles: the politically contested $14.1 billion U.S. Steel acquisition faces bipartisan opposition despite Japan's allied status, while the strategic withdrawal from China, including dissolving a 20-year joint venture with Baosteel, signals a decisive "de-risking" pivot toward Western security frameworks.

The company's future hinges on its aggressive Indian expansion through the AM/NS India joint venture, which plans to triple capacity to 25-26 million tons by 2030, capturing the subcontinent's infrastructure boom and favorable demographics. Simultaneously, NSC is weaponizing its intellectual property dominance in electrical steel critical for EV motors through unprecedented patent litigation, even suing major customer Toyota to protect proprietary technology. This technological moat, exemplified by brands like "HILITECORE" and "NSafe-AUTOLite," positions NSC as an indispensable supplier in the global automotive lightweighting and electrification revolution.

Yet existential threats loom large. The "NSCarbolex" decarbonization strategy requires massive capital expenditures of 868 billion yen for electric arc furnaces alone, while bridging to unproven hydrogen direct reduction technology by 2050. Europe's Carbon Border Adjustment Mechanism threatens to tax NSC's exports into oblivion, forcing accelerated retirement of coal-based assets. The March 2025 cyberattack on subsidiary NSSOL exposed digital vulnerabilities as operational technology converges with IT systems. The NSC faces a strategic trilemma: balancing growth in protected markets, ensuring security through supply chain decoupling, and making sustainability investments that threaten near-term solvency. Success demands flawless execution across geopolitical, technological, and financial dimensions, simultaneously a precarious bet on reshaping the global steel order.

Is Europe's Industrial Crown Jewel Being Quietly Dismantled?Volkswagen Group, once the symbol of German engineering dominance and post-war European recovery, is experiencing what can only be described as a structural dismantling rather than a cyclical downturn. The company faces a perfect storm of challenges: geopolitical vulnerability exposed by the Nexperia semiconductor crisis, where China demonstrated escalation of dominance over critical supply chains, catastrophic labor cost disadvantages ($3,307 per vehicle in Germany versus $597 in China), and a complete failure of its CARIAD software division that consumed €12 billion with little to show for it. The result is unprecedented: 35,000 German job cuts by 2030, the first factory closures in 87 years, and Golf production moving to Mexico.

The technological surrender is perhaps most revealing. VW is investing $5.8 billion in American startup Rivian and $700 million in Chinese EV maker XPeng—not as strategic partnerships, but as desperate attempts to acquire the software and platform capabilities it failed to develop internally. The company that once provided technology to Chinese joint ventures now buys entire vehicle platforms from a Chinese startup founded in 2014. Meanwhile, its profit engine has collapsed: Porsche's operating profit plummeted 99% to just €40 million in Q3 2024, while VW's China market share eroded from 17% to under 13%, with only 4% share in the critical EV segment.

This isn't just corporate restructuring—it's a fundamental transfer of power. VW's "In China, For China" strategy, which moves 3,000 engineers to Hefei and creates a separate technological ecosystem under Chinese jurisdiction, effectively places the company's intellectual property and future development under the control of a systemic rival. The patent analysis confirms the shift: while BYD has built a moat of 51,000 patents focused on battery and EV technology, much of VW's portfolio protects legacy internal combustion engines—stranded assets in an electric future. What we're witnessing is not Germany adapting to competition, but Europe losing control of its most important manufacturing sector, with the engineering and innovation increasingly done by Chinese hands, on Chinese soil, under Chinese rules.

Is Germany's Economic Success Just an Illusion?Germany's benchmark DAX 40 index surged 30% over the past year, creating an impression of robust economic health. However, this performance masks a troubling reality: the index represents globally diversified multinationals whose revenues originate largely outside Germany's struggling domestic market. Behind the DAX's resilience lies fundamental decay. GDP fell 0.3% in Q2 2025, industrial output reached its lowest level since May 2020, and manufacturing declined 4.8% year-over-year. The energy-intensive sector suffered even steeper contraction at 7.5%, revealing that high input costs have become a structural, long-term threat rather than a temporary challenge.

The automotive sector exemplifies Germany's deeper crisis. Once-dominant manufacturers are losing ground in the electric vehicle transition, with their European market share in China plummeting from 24% in 2020 to just 15% in 2024. Despite leading global R&D spending at €58.4 billion in 2023, German automakers remain trapped at Level 2+ autonomy while competitors pursue full self-driving solutions. This technological lag stems from stringent regulations, complex approval processes, and critical dependencies on Chinese rare earth materials, which could trigger €45-75 billion in losses and jeopardize 1.2 million jobs.

Germany's structural rigidities compound these challenges. Federal fragmentation across 16 states paralyzes digitalization efforts, with the country ranking below the EU average in digital infrastructure despite ambitious sovereignty initiatives. The nation serves as Europe's fiscal anchor, contributing €18 billion net to the EU budget in 2024, yet this burden constrains domestic investment capacity. Meanwhile, demographic pressures persist, though immigration has stabilized the workforce; highly skilled migrants disproportionately consider leaving, threatening to transform a demographic solution into brain drain. Without radical reform to streamline bureaucracy, pivot R&D toward disruptive technologies, and retain top talent, the disconnect between the DAX and Germany's foundational economy will only widen.

Can Memory Chips Become Geopolitical Weapons?Micron Technology has executed a strategic transformation from commodity memory producer to critical infrastructure provider, positioning itself at the intersection of AI computing demands and U.S. national security interests. The company's fiscal 2025 performance demonstrates this pivot's success, with data center revenue surging 137% year-over-year to comprise 56% of total sales. Gross margins expanded to 45.7% as the company captured pricing power across both its advanced High-Bandwidth Memory (HBM) portfolio and traditional DRAM products. This dual-margin expansion stems from an unusual market dynamic: capacity reallocation toward specialized AI chips has created artificial supply constraints in legacy memory, driving price increases exceeding 30% in some segments. In contrast, HBM3E capacity through 2026 is already sold out.

Micron's technological leadership centers on power efficiency and manufacturing innovation that translate directly into customer economics. The company's HBM3E solutions deliver bandwidth exceeding 1.2 TB/s while consuming 30% less power than competing 8-high configurations—a critical advantage for hyperscale operators managing electricity costs across massive data center footprints. This efficiency edge is reinforced by scientific advances in manufacturing, particularly the mass production deployment of 1γ DRAM using Extreme Ultraviolet lithography. This node transition delivers over 30% more bits per wafer than previous generations while reducing power consumption by 20%, creating structural cost advantages that competitors must match through heavy R&D investment.

The company's unique position as America's sole HBM manufacturer has transformed it from a component supplier to a strategic national asset. Micron's $200 billion U.S. expansion plan, supported by $6.1 billion in CHIPS Act funding, aims to produce 40% of its DRAM capacity domestically within a decade. This geostrategic positioning grants preferential access to U.S. hyperscalers and government projects requiring secure, domestically sourced components, a competitive moat independent of immediate technological specifications. Combined with a robust intellectual property portfolio covering 3D memory stacking and secure boot architectures, Micron has established multiple defensive layers that transcend typical semiconductor industry cycles, validating an investment thesis for sustained high-margin growth through structural rather than cyclical drivers.

Can a Small-Cap Survive the AI Data Revolution?Applied Optoelectronics (AAOI) represents a high-stakes investment proposition at the intersection of artificial intelligence infrastructure and geopolitical supply chain realignment. The small-cap optical networking company has positioned itself as a vertically integrated manufacturer of advanced optical transceivers, leveraging proprietary laser technology to serve hyperscale data centers, driving the AI boom. With 77.94% year-over-year revenue growth reaching $368.23 million in FY 2024, AAOI has successfully re-engaged a major hyperscale customer and begun shipping 400G datacenter transceivers, marking a potential turnaround from its 2017 customer loss that previously crushed its stock performance.

The company's strategic pivot centers on transitioning from lower-margin products to high-performance 800G and 1.6T transceivers while simultaneously relocating manufacturing capacity from China to Taiwan and the United States. This supply chain realignment, formalized through a 15-year lease for a New Taipei City facility signed in September 2025, positions AAOI to benefit from domestic sourcing preferences and potential government incentives like the CHIPS Act. The optical transceiver market, valued at $13.6 billion in 2024 and projected to reach $25 billion by 2029, is driven by substantial tailwinds, including AI workloads, 5G deployment, and hyperscale data center expansion.

However, AAOI's financial foundation remains precarious despite impressive revenue growth. The company reported a net loss of $155.72 million in 2024 and carries over $211 million in debt while facing ongoing share dilution from equity offerings that increased outstanding shares from 25 million to 62 million. Customer concentration risk persists as a fundamental vulnerability, with data centers representing 79.39% of revenue. External scrutiny has questioned the viability of the Taiwan expansion, with some reports characterizing the 800G production story as an "optical illusion" and raising concerns about the readiness of manufacturing facilities.

The investment thesis ultimately hinges on execution risk and competitive positioning in a rapidly evolving technology landscape. While AAOI's vertical integration and proprietary laser technology provide differentiation against giants like Broadcom and Lumentum, emerging co-packaged optics (CPO) technology threatens to disrupt traditional pluggable transceivers. The company's success depends on successfully ramping 800G production, operationalizing the Taiwan facility, achieving consistent profitability, and maintaining its re-engaged hyperscale customer relationships. For investors, AAOI represents a classic high-risk, high-reward opportunity, where strategic execution could deliver significant returns; however, financial vulnerabilities and operational challenges present substantial downside risks.

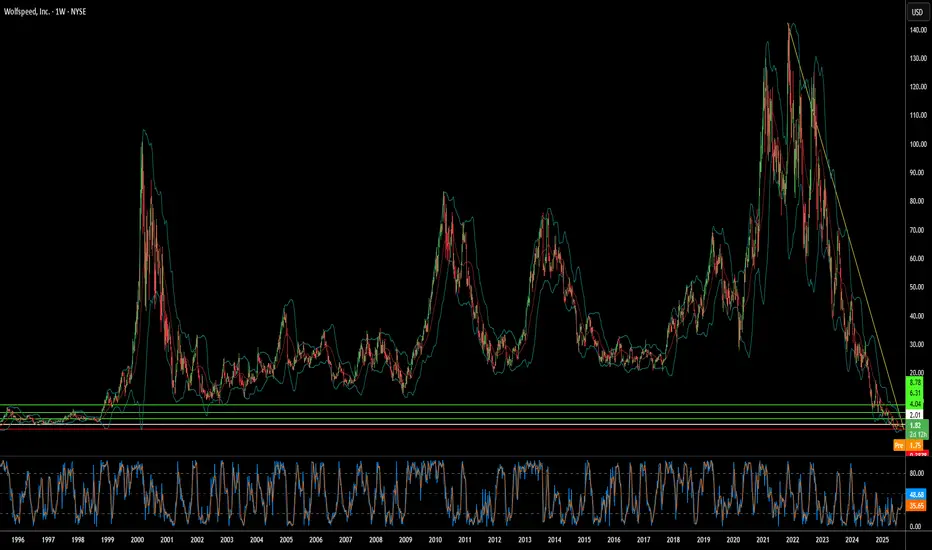

Can Silicon Carbide Save a Bankrupt Chip Giant?Wolfspeed's dramatic 60% stock surge following court approval of its Chapter 11 restructuring plan signals a potential turning point for the struggling semiconductor company. The bankruptcy resolution eliminates 70% of Wolfspeed's $6.5 billion debt burden and reduces interest obligations by 60%, freeing up billions in cash flow for operations and new fabrication facilities. With 97% creditor support backing the plan, investors appear confident that the financial overhang has been cleared, positioning the company for a cleaner emergence from bankruptcy.

The company's recovery prospects are bolstered by its leadership position in silicon carbide (SiC) technology, a critical component for electric vehicles and renewable energy systems. Wolfspeed's unique capability to produce 200mm SiC wafers at scale, combined with its vertically integrated supply chain and substantial patent portfolio, provides competitive advantages in a rapidly growing market. Global EV sales exceeded 17 million units in 2024, with projections of 20-30% annual growth, while each new electric vehicle requires more SiC chips for improved efficiency and faster charging capabilities.

Geopolitical factors further strengthen Wolfspeed's strategic position, with the U.S. CHIPS Act providing up to $750 million in funding for domestic SiC manufacturing capacity. As the U.S. government classifies silicon carbide as critical for national security and clean energy, Wolfspeed's fully domestic supply chain becomes increasingly valuable amid rising export controls and cybersecurity concerns. However, the company faces intensifying competition from well-funded Chinese rivals, including a new Wuhan facility capable of producing 360,000 SiC wafers annually.

Despite these favorable tailwinds, significant risks remain that could derail the recovery. Current shareholders face severe dilution, retaining only 3-5% of the restructured equity, while execution challenges persist regarding ramping the novel 200mm fabrication technology. The company continues operating at a loss with high enterprise value relative to current financial performance, and expanding global SiC capacity from competitors threatens to pressure pricing and market share. Wolfspeed's turnaround represents a high-stakes bet on whether technological leadership and strategic government support can overcome financial restructuring challenges in a competitive marketplace.

The timing is right for FEIM - high tight flag before earningsFEIM manufactures technology for timing things. They're an old company that's found newfound relevance with big budgets going to rockets and satellites and military tech that requires absolute precision timing.

THe fundamentals are great and the chart shows a high tight flag pattern getting ready for earnings.

FEIM releases earnings on Thursday, 9/11. I'm planning on prepping to buy if they release positive earnings because it could jump to the next stage of its flag.

Is Samsung's Chip Bet Paying Off?Samsung Electronics is navigating a complex global landscape, marked by intense technological competition and shifting geopolitical alliances. A recent $16.5 billion deal to supply advanced chips to Tesla, confirmed by Elon Musk, signals a potential turning point. This contract, set to run until late 2033, underscores Samsung's strategic commitment to its foundry business. The agreement will dedicate Samsung's new Texas fabrication plant to producing Tesla's next-generation AI6 chips, a move Musk himself highlighted for its significant strategic importance. This partnership aims to bolster Samsung's position in the high-stakes semiconductor sector, particularly in advanced manufacturing and AI.

The deal's economic and technological implications are substantial. Samsung's foundry division has faced profitability challenges, experiencing estimated losses exceeding $3.6 billion in the first half of the year. This large-scale contract is expected to help mitigate those losses, providing a much-needed revenue stream. From a technological standpoint, Samsung aims to accelerate its 2-nanometer (2nm) mass production efforts. While its 3nm process faced yield hurdles, the Tesla collaboration, with Musk's direct involvement in optimizing efficiency, could be crucial for improving 2nm yields and attracting future clients like Qualcomm. This pushes Samsung to remain at the forefront of semiconductor innovation.

Beyond the immediate financial and technological gains, the Tesla deal holds significant geopolitical and geostrategic weight. The dedicated Texas fab enhances U.S. domestic chip production capabilities, aligning with American goals for supply chain resilience. This deepens the U.S.-South Korea semiconductor alliance. For South Korea, the deal strengthens its critical tech exports and may provide leverage in ongoing trade negotiations, particularly concerning potential U.S. tariffs. While Samsung still trails TSMC in foundry market share and faces fierce competition in High-Bandwidth Memory (HBM) from SK Hynix, this strategic alliance with Tesla positions Samsung to solidify its recovery and expand its influence in the global high-tech arena.

LMT sky high rocket stock LMT has been experiencing some intense changes in geopolitical conflict for next week. Leading analysts to observe closely LMT price behavior according to avg volume. We’re al expecting LMT to rise just above $520 by next week in order to accommodate some liquidity. Keep buying if not yet more.

US-China Rift: India's Golden Hour?Heightened trade tensions between the United States and China, characterized by substantial US tariffs on Chinese goods, inadvertently create a favorable environment for India. The significant difference in tariff rates—considerably lower for Indian imports than Chinese ones—positions India as an attractive alternative manufacturing base for corporations seeking to mitigate costs and geopolitical risks when supplying the US market. This tariff advantage presents a unique strategic opening for the Indian economy.

Evidence of this shift is already apparent, with major players like Apple reportedly exploring increased iPhone imports from India and even accelerating shipments ahead of tariff deadlines. This trend extends beyond Apple, as other global electronics manufacturers, including Samsung and potentially even some Chinese firms, evaluate shifting production or export routes through India. Such moves stand to significantly bolster India's "Make in India" initiative and enhance its role within global electronics value chains.

The potential influx of manufacturing activity, investment, and exports translates into substantial tailwinds for India's benchmark Nifty 50 index. Increased economic growth, higher corporate earnings for constituent companies (especially in manufacturing and logistics), greater foreign investment, and positive market sentiment are all likely outcomes. However, realizing this potential requires India to address persistent challenges related to infrastructure, policy stability, and ease of doing business, while also navigating competition from other low-tariff nations and seeking favorable terms in ongoing trade negotiations with the US.

Vietnam's Shadow Over Nike's Swoosh?Nike's recent stock dip illuminates the precarious balance of global supply chains in an era of trade tensions. The article reveals a direct correlation between the proposed US tariffs on Asian imports, particularly from Vietnam – Nike's primary manufacturing hub – and a significant drop in the company's stock value. This immediate market reaction underscores the financial risks associated with Nike's deep reliance on its extensive factory network in Vietnam, which produces a substantial portion of its footwear, apparel, and equipment.

Despite robust revenues, Nike operates with relatively thin profit margins, leaving limited capacity to absorb increased costs from tariffs. The competitive nature of the athletic wear industry further restricts Nike's ability to pass these costs onto consumers through significant price hikes without risking decreased demand. Analysts suggest that only a fraction of the tariff burden can likely be transferred, forcing Nike to explore alternative, potentially less appealing, mitigation strategies such as product downgrades or extended design cycles.

Ultimately, the article highlights Nike's significant challenges in navigating the current trade landscape. While historically cost-effective, the deep entrenchment of its manufacturing in Vietnam now presents a considerable vulnerability. Shifting production elsewhere, particularly back to the US, proves complex and expensive due to the specialized nature of footwear manufacturing and the lack of domestic infrastructure. The future financial health of the athleticwear giant hinges on its ability to adapt to these evolving geopolitical and economic pressures.

Is Apple's Empire Built on Sand?Apple Inc., a tech titan valued at over $2 trillion, has built its empire on innovation and ruthless efficiency. Yet, beneath this dominance lies a startling vulnerability: an overreliance on Taiwan Semiconductor Manufacturing Company (TSMC) for its cutting-edge chips. This dependence on a single supplier in a geopolitically sensitive region exposes Apple to profound risks. While Apple’s strategy has fueled its meteoric rise, it has also concentrated its fate in one precarious basket—Taiwan. As the world watches, the question looms: what happens if that basket breaks?

Taiwan’s uncertain future under China’s shadow amplifies these risks. If China moves to annex Taiwan, TSMC’s operations could halt overnight, crippling Apple’s ability to produce its devices. Apple’s failure to diversify its supplier base left its trillion-dollar empire on a fragile foundation. Meanwhile, TSMC’s attempts to hedge by opening U.S. factories introduce new complications. If Taiwan falls, the U.S. could seize these assets, potentially handing them to competitors like Intel. This raises unsettling questions: Who truly controls the future of these factories? And what becomes of TSMC’s investments if they fuel a rival’s ascent?

Apple’s predicament is a microcosm of a global tech industry tethered to concentrated semiconductor production. Efforts to shift manufacturing to India or Vietnam pale against China’s scale, while U.S. regulatory scrutiny—like the Department of Justice’s probe into Apple’s market dominance—adds further pressure. The U.S. CHIPS Act seeks to revive domestic manufacturing, but Apple’s grip on TSMC muddies the path forward. The stakes are clear: resilience must now trump efficiency, or the entire ecosystem risks collapse.

As Apple stands at this crossroads, the question echoes: Can it forge a more adaptable future, or will its empire crumble under the weight of its design? The answer may not only redefine Apple but also reshape the global balance of tech and power. What would it mean for us all if the chips—both literal and figurative—stopped falling into place?

EUR/USD soars as eurozone CPI higher than expectedThe euro has charged out of the gates and posted strong gains on Monday. In the North American session, EUR/USD is trading at 1.0484, up 1.06%. With today's sharp gains, the euro has ended a three-day slide.

Inflation in the eurozone eased to 2.4% y/y in February, down from 2.5% in January but above the market estimate of 2.3%. Monthly, inflation jumped 0.5%, the fastest pace since April 2024 and after a January decline of 0.3%. It was the same story for core CPI, which slowed to 2.6% y/y, down from 2.7% in January but above the market estimate of 2.5%.

Investors focused on the fact that CPI was higher than expected and on the hot monthly CPI figure. As a result, the euro has soared as the European Central Bank could delay rate-cut plans with inflation surprising on the upside. The ECB is also concerned about sticky services inflation, which fell from 3.9% to 3.7% but remains much higher than the inflation target of 2%.

The ECB lowered rates in January and meets next on March 6. There is little doubt that the ECB will trim rates by a quarter-point but after that the rate path is unclear. The eurozone economy is sluggish and hasn't shown much response to the five rate cuts from the ECB since it started its easing cycle last June. The economy could use additional rate cuts but the ECB remains concerned about the upward risk of inflation and today's CPI report hasn't put those worries to rest.

Europe's manufacturing sector is stuck in the doldrums, with contractions in Germany, Italy, France and even Spain, which has been the eurozone's bright spot. Still, there is some optimism among manufacturers, as Germany quickly formed a government and there is the possibility of an end to the war in Ukraine.

EUR/USD is testing resistance at 1.0483. Above, there is resistance at 1.0590

1.0421 and 1.0314 are the next support lines

Euro rally ends, Eurozone GDP expected to accelerateThe euro is steady on Friday after jumping 0.7% a day earlier. In the European session, EUR/USD is trading at 1.0581, down 0.06% at the time of writing.

The eurozone wraps up the week with the GDP and job growth reports and the market is expecting an improvement. Third-quarter GDP is expected to improve to 0.4% q/q from o.2% in the second quarter. Job growth if forecast to tick upwards to 0.2% q/q, up from 0.1% in Q2.

In France, the political chaos continues. A no-confidence vote passed this week and has left the country without a functioning government. Prime Minister Michel Barnier resigned on Thursday after just three months in office. President Emmanuel Macron said he will name a new prime minister shortly but the political crisis could push up French interest rates and the country's large debt.

Germany, once the powerful locomotive of the eurozone, has faltered badly and has hampered growth in the eurozone. This week's German manufacturing data was dismal. The Manufacturing PMI remains mired in contraction and was unchanged at 43.0 in November. Factory orders for October declined by 1.5% after a 7.2% gain a month earlier. On Friday, industrial production fell 1% in October, after a 2% decline in September and shy of the market estimate of 1.2%.

The German Services PMI slipped into contraction in November and there is political instability, as the coalition German government collapsed in November. A snap election has been scheduled for Feb. 23, 2025.

The US wraps up the week with the nonfarm payroll report. With inflation largely contained, the employment growth is once again a key release can move the US dollar. The November report is expected to rise to a respectable 200 thousand, after a weak gain of 12 thousand in October, which was driven downwards by hurricanes and work stoppages at Boeing.

EUR/USD faces resistance at 1.0615 and 1.0644

1.0562 and 1.0533 are providing support

BMW (BMW): Navigating Through Uncertainty in the Auto MarketThe German automotive industry is currently facing significant challenges, from rising production costs and the transition to electric vehicles to increased competition from China. Despite these hurdles, we believe that most of the negative factors are already priced into the market.

From a technical perspective, we’re zooming out to get a broader view of BMW. Ignoring the COVID-19 dip, BMW has been ranging between 55€ and 113€ for an extended period. We anticipate that this range will continue, as markets tend to range 70% of the time. Right now, BMW is at a critical level, either bottoming out for the fourth time or, more likely, preparing to break below and collect the sell-side liquidity that has accumulated over the past three years.

Our plan is simple: We’re monitoring this closely, with alerts set to notify us if the stock dips below this level. Should this occur, we’re looking at a potential entry near 62€. We will update you with our strategy once this scenario unfolds.

Japanese yen slides as political drama continuesThe yen is sharply lower on Wednesday. In the European session, the USD/JPY is trading at 144.82 at the time of writing, up 0.89%.

In Japan, the dust is yet to settle on the political drama. On Tuesday, the new Prime Minister, Shigeru Ishiba, appointed Katsunobu Kato as finance minister. Kato is a supporter of “Abenomics” which advocates monetary easing. This could complicate the BoJ’s plans to tighten policy and the yen has responded with sharp losses today.

Ishiba is on record for supporting a tighter policy but may have chosen Kato to ease concerns that Ishiba will make a significant shift in monetary policy with a snap election on October 27. The election will be followed by the next BoJ meeting on October 31, with the BoJ expected to maintain its policy settings.

Manufacturing continues to sputter in both the US and Japan. The Japanese manufacturing PMI eased to a revised 49.7 in September, down from 49.8 in August and above the market estimate of 49.6. This was the third straight month of contraction in factory activity, with a strong decrease in export orders. Business confidence dropped to its lowest since December 2022, as manufacturers don’t see a light at the end of the tunnel for the troubled manufacturing sector.

In the US, the ISM manufacturing PMI was unchanged in September at 47.2, below the market estimate of 47.5. The contraction in manufacturing has extended for six straight months. New orders decreased in September, demand remains weak and manufacturers face uncertainty over the Federal Reserve’s monetary policy and the upcoming US election.

USD/JPY has pushed above resistance at 143.69 and 144.41. Above, there is resistance at 145.25

There is support at 142.85 and 142.13

Ford (F): Waiting for the right moment after recent bounceAfter being stopped out at break-even with profits already taken on NYSE:F , we are now observing the chart again. We're pleased that we didn't buy any shares as the anticipated bounce did not materialize. However, Ford did bounce almost exactly at point X, which is where wave 2 should not have dropped below—it briefly wicked under before pumping back up. This is something we can respect, as we haven't been stuck below the designated level for an extended time.

From a technical perspective, the plan is clear, but Ford is highly impacted by the current political climate, as car companies are in the spotlight right now. Despite this, we are planning for a push upwards after the recent dip. Ideally, we should not revisit the $9.64 level or, even better, avoid the wave (ii) level. Multiple levels need to be flipped for us to be confident that there's enough strength for future success. We've marked the "Ideal Entry Point" with a green dot, and it should be clear what we want to see.

For now, we're standing on the sidelines, letting it develop and play out. If our scenario unfolds as anticipated, we can capitalize on it.

Plan the trade and trade the plan.

NIO (NIO): 55% Increase but Bearish Trends Still LoomA while back, we analyzed NIO, and recently, we’ve seen a considerable 55% increase in the stock price. However, despite this rise, nothing truly convinces us that this bearish trend has ended or that a sustainable upward movement is underway.

The critical factor here is that none of the key levels that need to be breached for a trend reversal have been crossed. Specifically, we’re looking at the current Wave ((iv)) level around $6.04. If this level isn’t breached, it’s likely that we could see further declines, possibly dipping into the $2.99 range—or even lower, potentially as far as $1. It may seem dramatic, but considering NIO has already dropped up to 62% since January, repeating such a decline isn’t out of the question.

In conclusion, the market remains quite weak, and we’re still cautious about the possibility of more significant setbacks. Always remember, it’s okay to stay on the sidelines and not invest in everything that catches your eye. 🤝

Euro jumps to 10-day highThe euro has posted strong gains on Monday. EUR/USD is trading at 1.1126 in the North American session at the time of writing, up 0.49% today. The euro is at its highest level since Sept. 6.

It’s a quiet day on the data calendar, with no tier-1 events. In the US, the Empire State Manufacturing index rebounded to 11.5 in September, much higher than the August reading of -4.7 and the market estimate of -3.9. This was a shocker as the manufacturer index had contracted nine straight times before today’s reading.

Tuesday will be busier, with German ZEW economic sentiment index and US retail sales. German ZEW economic sentiment plunged to 19.2 in August, down from 41.8 in July. The market estimate for September stands at 17.1. US retail sales are expected to fall to 2.2% y/y in August, down from 2.7% in July.

This week’s key event is the Federal Reserve meeting on Wednesday, with a 25 basis-point cut practically guaranteed. Will the Fed opt for an oversize 50-bps cut or play it safe with a 25-bps move? The rate cut odds continue to swing wildly. After last week’s producer price index reading, the odds of a 50-bps point cut soared to 41%, up from just 13% before the release, according to the CME’s FedWatch tool. That has increased to 59% today.

The uncertainty over what the Fed will do could last right up to the wire. The Fed is in a quandary as it needs to balance the risk of inflation moving higher against the recent weakness in the labor market. A modest 25-bps cut may not be sufficient to improve the employment picture, while a 50 bps cut might send a message that the Fed believes the economy is in deep trouble.

EUR/USD is testing resistance at 1.118. Above, there is resistance at 1.1160

There is support at 1.1060 and 1.1018

US30 | Trade ideaKey Points:

Tesla: Shares fell 1.6% after a report that the company plans to produce a six-seat Model Y in China by late 2025.

Boeing: Dropped 7.3% following a downgrade from Wells Fargo to "underweight" from "equal weight."

Nvidia: Slumped nearly 10%, wiping out a record $279 billion in market value, marking the largest single-day decline for a U.S. company.

U.S. Manufacturing: Edged up in August from an eight-month low but remained subdued, according to ISM data.

Market Performance:

S&P 500 fell 2.1%

Nasdaq dropped 3.3%

Dow declined 1.5%

This marks the biggest daily percentage decline for these indexes since early August.

Nine out of 11 S&P 500 sectors fell, with technology, energy, communication services, and materials leading the decline.

Market Sentiment: Weakened amid concerns about the Federal Reserve’s interest rate decisions, with September being historically one of the worst months for stock market performance.

Volatility: The CBOE Volatility Index (VIX) jumped 33.2% to 20.72, the highest close since early August.

Trading Volume: Totaled 12.14 billion shares across U.S. exchanges, above the 20-day moving average of nearly 11 billion.

Labor Market: Traders are awaiting labor market reports ahead of the August non-farm payrolls data.

Fed Meeting: Scheduled for Sept. 17-18, with a 63% chance of a 25-basis point rate cut and a 37% chance of a 50-basis point cut, according to the CME FedWatch Tool.

Market Breadth: On the NYSE, declining issues outnumbered advancers by 2.52-to-1, while on the Nasdaq, decliners outnumbered advancers by 3.5-to-1.

India's Nifty 50: A Rising Star in a Geopolitical StormIn 2023, the Indian stock market, represented by the Nifty 50 index, has emerged as a standout performer. Outpacing its U.S. counterpart, the S&P 500, by a significant margin, the Nifty 50 has captured the attention of global investors. Several factors converge to explain this impressive performance, with geopolitical tensions playing a pivotal role.

The Great Manufacturing Shift: India as a Prime Beneficiary

One of the most compelling narratives driving India's economic ascent is the global shift in manufacturing. As the world grapples with heightened geopolitical risks, particularly the escalating tensions between the United States and China, businesses are seeking to diversify their supply chains. India, with its vast market, skilled workforce, and government's "Make in India" initiative, has emerged as a compelling alternative to China for many multinational corporations.

Diversification of Supply Chains: Companies like Apple and Google are actively exploring manufacturing operations in India to reduce their reliance on China. This trend extends to various sectors, including pharmaceuticals, automobiles, and textiles.

Government Support: India's government has proactively created a conducive business environment through infrastructure development, tax incentives, and ease of doing business reforms. These efforts have boosted investor confidence and accelerated the country's industrialization process.

India's Economic Characteristics and Domestic Consumption

India's strong domestic consumption and the rise in manufacturing are major factors in the country's economic expansion. The demand for goods and services is increasing due to the growing middle class and increased disposable incomes. The approach of consumption-led growth enhances the resilience of the Indian economy by acting as a buffer against external shocks.

India's economy boasts several key characteristics:

Rapid Growth: India has consistently been one of the fastest-growing major economies globally.

Large Domestic Market: With a population of over 1.4 billion, India offers a vast consumer base, driving domestic consumption.

Young Population: A large and young workforce provides a demographic dividend, fueling economic potential.

IT and Services Dominance: The IT and services sector is a major contributor to India's GDP, with companies excelling in software development, outsourcing, and business process management.

Agricultural Importance: Agriculture remains a crucial sector, employing a significant portion of the population, although its contribution to GDP is declining.

Challenges and Opportunities

While India's economic trajectory is promising, it faces challenges such as:

Infrastructure Gaps: Improving infrastructure, including transportation, energy, and digital connectivity, is essential for sustained growth.

Poverty and Inequality: Addressing poverty and reducing income inequality remains a priority.

Education and Skill Development: Investing in education and skill development is crucial to enhancing human capital.

Environmental Concerns: One of the main challenges is balancing environmental sustainability with economic growth.

Despite these challenges, India offers immense opportunities for businesses and investors:

Large Consumer Market: The growing middle class presents a lucrative market for consumer goods and services.

Favorable Government Policies: The government's focus on economic reforms and ease of doing business creates a conducive environment for investment.

Digital Transformation: India's rapid adoption of digital technologies presents opportunities in e-commerce, fintech, and digital payments.

The Road Ahead

While the Nifty 50's performance has been impressive, challenges remain. Inflationary pressures, global economic uncertainties, and the potential impact of a prolonged geopolitical standoff could pose risks. However, India's demographic dividend, its digital transformation, and its focus on renewable energy offer promising avenues for long-term growth. Continued focus on infrastructure, education, and skill development will be crucial for realizing its full potential.

In today's complex geopolitical environment, India seems well-placed to take advantage of the opportunities arising from global supply chain disruptions. The performance of the Nifty 50 index reflects India's increasing economic influence and its potential to emerge as a global manufacturing and consumption hub.

(EW) edward lifesciencesblood company, they have a warehouse based here in Utah, only reason I know of the company; as it turns out they did reach an all-time high and drop. Too bad. Wonder what happened? They were doing so well.