VKTX Viking Therapeutics Exploding Higher TodayVKTX surges higher today after pulling back again near 200-day EMA. Not sure what the news is that's driving the big move higher. The news I did find talks about the following:

1) Viking Therapeutics completed a drug clinical trial stage earlier than expected last week

2) VKTX is on lists of hot stocks to buy for 2026 and could be a takeover, acquisition target

3) VKTX is recommended by 15 Wall Street Ranked analysis who give stock 12-month consensus average price target of $92

4) VKTX is on lists of stocks with high short interest (over 20% short interest) TO BUY because they are vulnerable to getting short-squeezed

Let's talk about the 4th item above. Just imagine VKTX continues to move higher on good news about clinical trials or possibly getting acquired by a larger company. This would push the stock even higher and will force traders who have big short positions on the stock to quickly cover, creating a snowball effect that frantically drives VKTX even higher and completely surges! This is reminiscent of what happened to Game Stop (GME) a few years back. I hope that this happens because I am long on several rather large call option positions on VKTX!

Whatever you all decide to do..... Good Luck!

Pharmaceuticals

RXRX monthly close.www.tradingview.com

RXRX MC. Touched the lower BB, but got bought heavily. IMHO price is going to reclaim the 20ma MA in the upcoming month(s). Sell volume is dropping while buy volume is increasing. Institutions keep on buying as well. Shake out before breakout!

Looking to pickup at $476$476 is the buy area target $715. It's best to wait for support to hit before jumping into this one.

Good luck!

Eli Lilly and Company: Path to Sustained Market LeadershipEli Lilly and Company has achieved a market valuation approaching one trillion U.S. dollars by the close of 2025, underpinned by a comprehensive corporate strategy that integrates advanced scientific research, targeted technology acquisitions, and adaptive global partnerships. This performance, marked by a substantial year-over-year share appreciation, positions the firm as a preeminent participant in the international pharmaceutical sector and underscores structural advantages in innovation-driven capital markets.

Core Therapeutic Franchises and Pipeline Expansion

The company's cardiometabolic portfolio, centered on dual GIP/GLP-1 receptor agonists, continues to serve as the principal engine of revenue growth. Products indicated for type 2 diabetes and chronic weight management recorded quarterly sales exceeding ten billion dollars in 2025, reflecting robust demand in large-scale metabolic disease populations. Ongoing clinical investigation into the neurobiological effects of these molecules has yielded preliminary evidence of modulation within central reward pathways, suggesting potential future applications in neuropsychiatric conditions characterized by dysregulated appetite control. Such findings reinforce the intellectual property protections surrounding the franchise and broaden its therapeutic scope.

In parallel, Eli Lilly is advancing capabilities in central nervous system disorders through specialized drug-delivery technologies. A recent multibillion-dollar licensing agreement with a South Korean biotechnology enterprise grants exclusive access to an engineered bispecific antibody platform designed to enhance macromolecular transport across the blood-brain barrier. This acquisition complements prior collaborations in the same domain and materially strengthens the company's competitive positioning in Alzheimer’s disease, Parkinson’s disease, and related neurodegenerative indications.

Global Research Collaborations and Supply-Chain Resilience

Strategic alliances with leading Asian biotechnology organizations form a key component of Eli Lilly’s innovation sourcing model. These partnerships provide access to proprietary platform technologies, expand the firm's intellectual property base beyond North American origination, and foster diversified scientific talent networks. By establishing collaborative development nodes within geopolitically aligned jurisdictions, the company enhances resilience in high-value biopharmaceutical supply chains while accelerating the maturation of next-generation therapeutic modalities.

Capital Market Dynamics and Transatlantic Divergence

Eli Lilly operates within a U.S. financial ecosystem that currently represents approximately three-quarters of global developed-market equity indices, an environment particularly conducive to large-capitalization growth enterprises. This structural weighting, combined with concentrated domestic healthcare spending and investor preference for scalable innovation platforms, has facilitated accelerated valuation expansion. In contrast, European peers contend with more fragmented national markets and differing risk appetite conventions among institutional investors, resulting in divergent capital allocation outcomes across the Atlantic.

Executive Leadership and Technology Adoption

Under the direction of Chief Executive Officer David Ricks, Eli Lilly has institutionalized the integration of advanced computational tools throughout the research and decision-making processes. Specialized large-language models and frontier artificial intelligence systems are routinely employed to augment hypothesis generation and data interpretation, supported by investments in high-throughput robotic experimentation infrastructure. This disciplined yet exploratory approach to emerging technologies reflects a broader organizational commitment to maintaining leadership in computationally assisted drug discovery.

Evolution Toward Platform-Centric Development

The company has transitioned from asset-specific transactions to the systematic acquisition of foundational technology platforms capable of yielding multiple product candidates. Recent investments in blood-brain barrier transport modalities and downstream applications in oncology illustrate this paradigm. By prioritizing versatile, proprietary enabling technologies, Eli Lilly establishes durable competitive barriers and aligns its research and development expenditure with long-term industry trends favoring multi-indication pipelines.

Intellectual Property Strategy and Risk Mitigation

Comprehensive patent estates surrounding the incretin mimetic class, coupled with proactive manufacturing capacity expansion, preserve pricing autonomy and market exclusivity in high-volume cardiometabolic indications. Concurrent investment in novel mechanisms—of which blood-brain barrier penetration is a prime example—serves to replenish the development pipeline and offset eventual patent expirations on current revenue-generating products. This forward-looking intellectual property management underpins investor confidence in the sustainability of the company’s growth trajectory.

In summary, Eli Lilly’s ascent to near-trillion-dollar valuation reflects the successful execution of an integrated strategy encompassing scientific excellence, strategic technology acquisition, international collaboration, and rigorous capital allocation—positioning the enterprise for continued leadership in global biopharmaceutical innovation.

ELI LILLY to soon start a correction towards $700.Eli Lilly (LLY) has made new All Time Highs (ATH) this month, extending the impressive rally since the August Low near the 1W MA200 (orange trend-line).

The multi-year trend remains bullish within a Fibonacci Channel Up but practically the stock hasn't gotten out of its range since the July 2024 High, breaking in August below even its 1W MA100 (green trend-line).

This prolonged sideways trading resembles the July 2015 - July 2018 3-year consolidation phase, which broke upwards only after a 2nd test of the 1W MA200. Even the 1M RSI patterns between the two sequences are similar. Based on this (1M RSI), which is about to break above its MA for the first time since July 2024, we are in similar levels as February 2017.

As a result, we expect LLY to start a rather smooth correction towards its 1W MA200 again, targeting $700, where the next long-term buy opportunity may potentially emerge.

---

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

---

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Novo Nordisk Setup – Is This the Pharma Sector’s Strongest Play?🚀 NVO "Novo Nordisk" – Wealth Strategy Map (Swing/Day Trade)

📈 Trade Plan (Bullish Setup)

Trend Confirmation: The bullish trend is supported by Dow Theory accumulation phase 📊.

Candle Signal: A Heikin Ashi Doji has formed, adding confluence to the setup.

Indicator Alert: LSMA (Least Squares Moving Average) line has confirmed a breakout, reinforcing the bullish case.

🎯 Entry Strategy (Layering Style)

This plan uses a layered entry approach — placing multiple buy-limit orders across price levels to scale into the trade:

Layered Buys: 54.00 → 55.00 → 56.00 → 57.00

(⚡ You can expand your limit layers further depending on your own preference and risk appetite.)

✅ This layered method allows flexibility, smoothing entries instead of relying on a single price level.

🛡️ Risk Management

Stop Loss Idea: Suggested protective stop near 52.00 🔒.

📢 Note: Risk is personal! Adjust your SL to fit your risk tolerance, capital, and trading style.

🎯 Profit Target

Target Zone: 66.00 (area of heavy resistance + possible overbought levels ⚡).

⚠️ Note: Exiting before the “crowd trap” forms is key — take profits wisely when conditions match your own plan.

🔗 Related Pairs to Watch

NYSE:NVO (Primary)

NYSE:LLY (Eli Lilly) 🧬 – Correlated pharma sector, often mirrors biotech sentiment.

SP:SPX / AMEX:SPY 📊 – Broader market direction can impact large-cap pharma momentum.

$USD/SEK 💱 – Novo Nordisk is Danish; currency fluctuations sometimes influence investor flow.

Keeping an eye on these correlated assets can improve timing and risk management.

✨ “If you find value in my analysis, a 👍 and 🚀 boost is much appreciated — it helps me share more setups with the community!”

#NVO #NovoNordisk #Stocks #SwingTrade #DayTrade #StockMarket #Bullish #HeikinAshi #DowTheory #TradingStrategy #PharmaStocks #LayeredEntries #RiskManagement

Can Machines Rewrite the DNA of Discovery?Recursion Pharmaceuticals is redefining the boundaries of biotech by positioning itself not as a traditional drug developer, but as a deep-technology platform built on artificial intelligence and automation. Its mission: to collapse the pharmaceutical industry’s notoriously slow and costly research model - one that can demand up to $3 billion and 14 years for a single approved drug. Through its integrated platform, Recursion aims to transform this inefficiency into a scalable engine for global health innovation, where value is driven not by one-off products but by the speed and reproducibility of discovery itself.

At the core of this transformation lies BioHive-2, a proprietary supercomputer powered by NVIDIA’s DGX H100 architecture. This computational behemoth fuels Recursion’s ability to iterate biological experiments at a pace that competitors cannot match. In collaboration with MIT’s CSAIL, Recursion co-developed Boltz-2, a biomolecular foundation model capable of predicting protein structures and binding affinities in seconds rather than weeks. By open-sourcing Boltz-2, the company has effectively shaped the scientific ecosystem around its standards, granting access to the community while retaining the true moat: its proprietary biological data and infrastructure.

Beyond its technological might, Recursion’s growing clinical pipeline provides proof of concept for its AI-driven discovery process. Early successes, including REC-617 (a CDK7 inhibitor) and REC-994 (for cerebral cavernous malformations), illustrate how computational prediction can rapidly yield viable drug candidates. The company’s ability to compress the time-to-market curve doesn’t merely improve profitability; it fundamentally redefines which diseases can be economically targeted, potentially democratizing innovation in previously neglected therapeutic spaces.

Yet with such power comes strategic responsibility. Recursion now operates at the intersection of biosecurity, data sovereignty, and geopolitics. Its commitment to rigorous compliance frameworks and aggressive global IP expansion underscores its dual identity as both a scientific and strategic asset. As investors and regulators watch closely, Recursion’s long-term value will hinge on its ability to transform computational speed into clinical success - turning the once-impossible dream of AI-driven drug discovery into an operational reality.

HIMS THROUGH LABOR DAYThis is my speculative technical analysis of what I believe could unravel with $HIMS.

$45.00 has been crossed twice, and I believe this is where the line on the sand is drawn. A Strong close above this mark and we could see $47.40, $48.94, and then a gap fill to $50.00 which is a big psychological level.

An area where I would expect some price consolidation before picking direction once again.

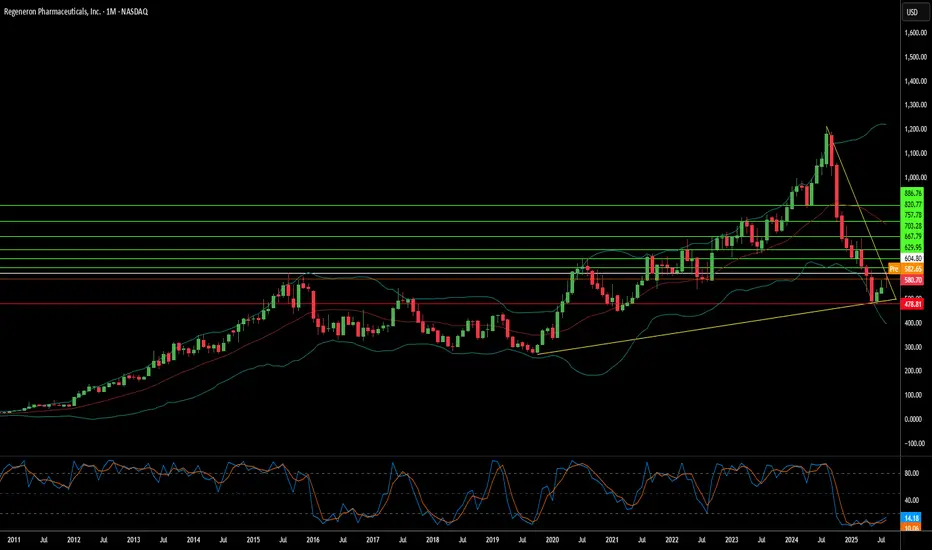

Can Innovation Survive Manufacturing Chaos?Regeneron Pharmaceuticals stands at a fascinating crossroads, embodying the paradox of modern biotechnology: extraordinary scientific achievement shadowed by operational vulnerability. The company has successfully transformed from a blockbuster-dependent enterprise into a diversified biopharmaceutical powerhouse, driven by two key engines. Dupixent continues its remarkable ascent, achieving 22% growth and reaching $4.34 billion in Q2 2025. Meanwhile, the strategic transition from legacy Eylea to the superior Eylea HD demonstrates forward-thinking market positioning, despite apparent revenue declines.

The company's innovation engine supports its aggressive R&D strategy, investing 36.1% of revenue, nearly double the industry average, into discovery and development. This approach has yielded tangible results, with Lynozyfic's FDA approval marking Regeneron's first breakthrough in blood cancer, achieving a competitive 70% response rate in multiple myeloma. The proprietary VelociSuite technology platform, particularly VelocImmune and Veloci-Bi, creates a sustainable competitive moat that competitors cannot easily replicate, enabling the consistent generation of fully human antibodies and differentiated bispecific therapies.

However, Regeneron's scientific triumphs are increasingly threatened by third-party manufacturing dependencies that have created critical vulnerabilities. The FDA's second rejection of odronextamab, despite strong European approval and compelling clinical data, is due to manufacturing issues at an external facility, rather than scientific deficiencies. This same third-party bottleneck has delayed crucial Eylea HD enhancements, potentially allowing competitors to gain market share during a pivotal transition period.

The broader strategic landscape presents both opportunities and risks that extend beyond manufacturing concerns. Although the company's strong victories in intellectual property cases against Amgen and Samsung Bioepis showcase effective legal defenses, the proposed 200% drug tariffs and industry-wide cybersecurity breaches, such as the Cencora incident impacting 27 pharmaceutical companies, highlight significant systemic vulnerabilities. Regeneron's fundamental strengths-its technological platforms, diverse pipeline spanning oncology to rare diseases, and proven ability to commercialize breakthrough therapies-position it for long-term success, provided it can resolve the operational dependencies that threaten to derail its scientific achievements.

Zydus Lifesciences: Premium Valuation, Solid OutlookZydus Lifesciences Ltd. (NSE: ZYDUSLIFE), one of India’s most respected pharmaceutical giants, is at a crucial juncture where technical breakout signals align with solid fundamental strength. Let’s dive deeper into its techno-fundamental outlook.

🔹 Fundamental Snapshot

CMP (25 Aug 2025): ₹1,023

Market Cap: ~₹1 lakh crore

P/E Ratio: ~22.4 (slightly above historical average of ~21.6)

P/B Ratio: ~4.2–4.7

Dividend Yield: ~1.1%

ROE / ROCE: 21.2% / 24.3%

Debt-to-Equity: 0.13 (low leverage)

Current Ratio: 1.9 (healthy liquidity)

EPS (TTM): ~₹45.4

Growth Metrics:

Revenue CAGR (5Y): ~10%

Profit CAGR (5Y): ~26%

Profit CAGR (3Y): ~2% (showing a slowdown recently)

Valuation Insight:

Intrinsic value estimates range from ₹748–₹814, implying the stock trades 25–27% above fair value.

👉 Fundamentally, Zydus is financially strong and consistently profitable, but valuation is on the premium side.

🔹 Technical Analysis

The daily chart (shown above) highlights a large Inverse Head & Shoulders (H&S) formation, typically a bullish reversal pattern.

Left Shoulder: Nov 2024

Head: Apr 2025 (major bottom around ₹800.5)

Right Shoulder: Aug 2025

Neckline Breakout: Around ₹1,000–1,010

Key Levels

Reversal Zone (Support): ₹977–₹993

Immediate Resistance (R1): ₹1,100

Next Resistance (R2): ₹1,150

Major Resistance (R3): ₹1,240

📈 Technical Outlook:

The breakout above the neckline suggests momentum towards ₹1,100–₹1,150 in the short term, with the potential to test ₹1,240 in the medium term if volumes support it.

🔹 Techno-Fundamental View

Valuation: Trading at a premium, about 25% above intrinsic value, though supported by a strong balance sheet and product pipeline.

Profitability: ROE and ROCE remain strong, both above 20%.

Balance Sheet: Very low debt and solid liquidity provide financial strength.

Growth: Long-term CAGR is healthy, but recent three-year profit growth has slowed.

Technical Setup: Inverse Head & Shoulders breakout signals bullish momentum.

Upside Targets: ₹1,100 → ₹1,150 → ₹1,240.

Risk Zone: A breakdown below ₹977 would invalidate the bullish pattern.

🔹 Conclusion

Zydus Lifesciences presents a compelling techno-fundamental story:

Fundamentally strong with robust financial ratios, prudent balance sheet, and a global growth strategy.

Technically bullish, as the inverse Head & Shoulders suggests a strong reversal with clear upside targets.

However, with the stock trading above intrinsic value estimates, new investors should approach with caution—preferably on dips near the ₹977–₹993 support zone. For existing investors, this breakout could unlock the next leg towards ₹1,150–₹1,240.

Teva long positionTeva looks like a student who failed an exam and now desperately tries to cover the gaps literally, the gap around 21.4.

On the chart we see a clear breakout of the descending channel followed by a neat retest from above, suggesting the stock is ready to get back into a long-term uptrend.

Volumes in the 17–17.5 zone act like a safety cushion, preventing the price from dropping too sharply.

Technically the next target is gap closure in the 21–22 area, which may unlock the path to higher levels.

From the fundamental side, Teva also has some cards to play: the pharmaceutical sector remains in focus due to rising demand for medicines and biotech solutions, and the company has been cleaning up its balance sheet while expanding new business lines. Altogether, both technicals and fundamentals point in the same direction , buyers are not ready to give up just yet.

Eli Lilly (LLY) – Pharma Giant at a Key Price LevelHi,

Eli Lilly & Co. is one of the world’s largest pharmaceutical companies, founded in 1876 and headquartered in Indianapolis. It operates in over 125 countries and is best known for blockbuster treatments in diabetes, obesity, oncology, and immunology. Recent growth has been driven largely by its GLP-1 class drugs Mounjaro and Zepbound, which have quickly become industry leaders in the weight-loss and diabetes markets.

Recent Fundamentals (Q2 2025)

Revenue: $15.56 B (+38% YoY)

- EPS: $6.31 (beat expectations)

- Mounjaro sales: $5.2 B

- Zepbound sales: $3.38 B

- Full-year guidance: Revenue $60–62 B, EPS $21.75–$23.00

- Margins: Gross margin ~82.6%, net margin ~25.9%

- Profitability: ROE ~75.5%, ROIC ~29.6%

While fundamentals remain strong, the recent Phase III data for the oral weight-loss pill orforglipron came in below expectations, sparking a ~14% drop, the stock’s steepest one-day decline in decades. Analysts have since trimmed long-term sales forecasts for this product.

From a valuation perspective, the stock trades at a premium (~41× P/E, ~10.7× P/S), leaving little room for major disappointments.

Technicals

Technically speaking, the price has arrived in the zone where I’ve been patiently waiting to share it as an idea. This is a good area from where to start building positions if you’re interested.

There are quite a few technical confluence factors aligning here, but be ready to grab it also around $500 if the market offers it. Let that be your guide:

- If you’re not willing to hold long-term, don’t touch it.

- If you’re not willing to buy more at lower prices, don’t touch it.

Good luck,

Vaido

Ironwood Pharmaceuticals | IRWD | Long at $0.61Ironwood Pharma NASDAQ:IRWD stock dropped ~89% in the past year due to disappointing Phase 3 Apraglutide trial results, FDA requiring an additional trial, weak Q1 2025 earnings (-$0.14 EPS vs. -$0.04 expected), high debt ($599.48M), and analyst downgrades. So why would I be interested in swing trading this company? The chart. The price has entered my "crash" simple moving average zone, which often results in a reversal - even if temporary. Also, Linzess (GI drug) revenue is steady, and I thoroughly believe that alone pushes the fair value near $0.95, if not higher. Thus, at $0.61, NASDAQ:IRWD is in a personal buy zone with the potential for additional declines before future rise.

Target:

$0.95 (+55.7%)

Novo Nordisk (Revised) | NVO | Long at $47.78**This is a revised analysis from February 5, 2025: I am still in that position, but added significantly more below $50**

Novo Nordisk NYSE:NVO is now trading at valuations before its release of Wegovy and Ozempic... From a technical analysis perspective, it's within my "major crash" simple moving average zone (gray lines). When a company's stock price enters this region (especially large and healthy companies) I always grab shares - either for a temporary future bounce or a long-term hold. While currently trading near $47 a share, I think worst case scenario here in 2025 is near $38-$39. Tariffs may cause a recession in the second half of 2025, so no company would be immune.

As mentioned above, I am still a holder at $86.74. However, I went in much heavier within my "major crash" simple moving average band and have a final entry planned near $38-$38 (if it drops there). My current cost average is near $55.00.

Why do I still have faith in NYSE:NVO ? Because no one else does right now, yet it generated $42 billion in revenue, $14 billion in profits, and has significant cash flow YoY. The company has a massive pipeline, despite Wegovy and Ozempic competition, and I think the market is undervaluing its position in the pharmaceutical industry.

Revised Targets in 2028:

$60.00 (+25.6%)

$70.00 (+46.5%)

$80.00 (+67.4%)

KALV FDA approval rallyKALV received FDA approval this week for a new drug, has $220mln in cash, and just bounced off the daily 21EMA (overlayed on this 4H chart).

Recently rejected off the monthly 100ema two times (overlayed on this 4H chart). Breakout beyond the monthly 100ema and first target is $20. Numerous price target increases, most notably, one at $27 and another increased from $32 to $40.

Bearish Divergence on Weekly tf.FEROZ Update

Closed at 362.90 (20-06-2025)

There is a Bearish Divergence on Weekly tf.

So important to Cross the Strong Resistance Zone

around 380 - 410.

Crossing this level with good volumes may lead

it towards further upside around 500.

Important Supports are around 330 - 333 & then

around 260 - 265.

Potential outside week and bearish potential for TLXEntry conditions:

(i) lower share price for ASX:TLX below the level of the potential outside week noted on 2nd June (i.e.: below the level of $24.91).

Stop loss for the trade would be:

(i) above the high of the outside week on 5th June (i.e.: above $27.40), should the trade activate.

Important note for the trade:

- Observe market reaction at two key areas illustrated in the chart above, should the trade activate ($24.79 and $24.47), which could act as support against the short trade.

Play on LevelsSEARL

Closed at 86.99 (27-06-2025)

Monthly Closing above 83 is a +ve sign.

Immediate Resistance is around 93 - 95

& then around 105 - 114 is a Very Important

Zone that needs to Sustain for further upside.

This time if 61 is broken, it may take further

selling pressure.

Play on levelsMonthly closing above 66 is actually

an important Support.

Retest of Trendline done.

Weekly Support is around 71 - 68.

Immediate Resistance is around 91 - 92.

If this level is sustained, we may witness 96 - 97

Novartis | NVS | Long at $99.00As one of the largest pharmaceutical companies in the world, Novartis NYSE:NVS is poised to grow well into 2027. It's trading at a 17x P/E, earnings are forecast to grow 7% per year, it has low debt, and has been raising its dividend over the past few years (3.8%). The price on the daily chart is nearing the historical simple moving average line and may be poised for another move up. However, entry into the lower $90's or even $80's is still not off the table and, in my view, a great opportunity. Thus, at $99.00, NYSE:NVS is in a personal buy zone.

Target #1 = $110.00

Target #2 = $120.00

Though Bullish on Monthly tf, butGLAXO Closed at 390.42 (23-05-2025)

Though Bullish on Monthly tf, but weekly bearish

divergence has started appearing.

Important Support level is around 367 - 372; but

important to Sustain 388 - 390 atleast for further upside.

Immediate Resistance is around 410 - 420

Breaking 300 will bring more selling pressure.

Can Lilly Redefine Weight Loss Market Leadership?Eli Lilly is rapidly emerging as a dominant force in the burgeoning weight loss drug market, presenting a significant challenge to incumbent leader Novo Nordisk. Lilly has demonstrated remarkable commercial success despite its key therapy, Zepbound (tirzepatide), entering the market well after Novo Nordisk's Wegovy (semaglutide). Zepbound's substantial revenue in 2024 underscores its rapid adoption and strong competitive standing, leading market analysts to project Eli Lilly's obesity drug sales will surpass Novo Nordisk's within the next few years. This swift ascent highlights the impact of a highly effective product in a market with immense unmet demand.

The success of Eli Lilly's tirzepatide, the active ingredient in both Zepbound and the diabetes treatment Mounjaro, stems from its dual mechanism targeting GLP-1 and GIP receptors, offering potentially enhanced clinical benefits. The company's market position was further solidified by a recent U.S. federal court ruling that upheld the FDA's decision to remove tirzepatide from the drug shortage list. This legal victory effectively halts compounding pharmacies from producing unauthorized, cheaper versions of Zepbound and Mounjaro, thereby protecting Lilly's market exclusivity and ensuring the integrity of the supply chain for the approved product.

Looking ahead, Eli Lilly's pipeline includes the promising oral GLP-1 receptor agonist, orforglipron. Positive Phase 3 trial results indicate its potential as a convenient, non-injectable alternative with comparable efficacy to existing therapies. As a small molecule, orforglipron offers potential advantages in manufacturing scalability and cost, which could significantly expand access globally if approved. Eli Lilly is actively increasing its manufacturing capacity to meet anticipated demand for its incretin therapies, positioning itself to capitalize on the vast and growing global market for weight management solutions.

A Long-term Bullish Trend ?With an upcoming Earnings report we can observe rather uncertain future behavior.

But since the trend has been bearish for a longer period of time and the price is "nearly" at the same position which was achieved for the first time in early April in 2019, we can, mostly based only on the technical analysis and Earnings report, determine quite confidently that the price is ready to rise.

Important data:

EPS Estimate: -$3.12

Revenue Estimate: $106 million to $166.7 million

Notable developments:

Cost-cutting initiative = Targeting $1.1B in reductions by 2027

By the end of 2024 $9.5 billion allocated in investments