SNAP Options Ahead of EarningsIf you haven`t sold the top on SNAP:

Now analyzing the options chain and the chart patterns of SNAP prior to the earnings report this week,

I would consider purchasing the 10usd strike price Calls with

an expiration date of 2026-6-18,

for a premium of approximately $0.36.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Signalsgroup

MSFT Microsoft Corporation Options Ahead of EarningsIf you missed buying MSFT when they took a 49% stake in OpenAI:

Nor sold the recent double top:

Now analyzing the options chain and the chart patterns of MSFT Microsoft Corporation prior to the earnings report this week,

I would consider purchasing the 475usd strike price Calls with

an expiration date of 2026-2-20,

for a premium of approximately $14.60.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

LAES SEALSQ Corp Options Ahead of EarningsAnalyzing the options chain and the chart patterns of LAES SEALSQ Corp prior to the earnings report next week,

I would consider purchasing the 5usd strike price Calls with

an expiration date of 2027-1-15,

for a premium of approximately $0.62.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

POET Technologies Options Ahead of EarningsAnalyzing the options chain and the chart patterns of POET Technologies prior to the earnings report this week,

I would consider purchasing the 17usd strike price Calls with

an expiration date of 2028-1-21,

for a premium of approximately $0.82.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

MU Micron Technology Options Ahead of EarningsIf you haven`t bought MU before the rally:

Now analyzing the options chain and the chart patterns of MU Micron Technology prior to the earnings report next week,

I would consider purchasing the 247.5usd strike price Calls with

an expiration date of 2025-12-19,

for a premium of approximately $8.10.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Geopolitics Alert: Greenland, Tariffs & Potential VIX Surge 2026As President Donald Trump ramps up his aggressive foreign policy in early 2026, fresh tariff threats against European allies are stoking fears of a trade war escalation, potentially driving market volatility higher and pushing the VIX (fear gauge) into overdrive.

Trump's January 17 announcement of 10% tariffs starting February 1—rising to 25% by June—on eight European nations (Denmark, Norway, Sweden, France, Germany, the UK, the Netherlands, and Finland) unless they facilitate a U.S. "purchase" of Greenland has sent shockwaves through global markets.

This move, tied to his long-standing obsession with annexing the Arctic territory for national security reasons, risks severe retaliatory measures from the EU, including tariffs on up to $108 billion in U.S. goods.

The standoff is intensifying: European leaders are holding emergency summits, deploying troops to Greenland to assert sovereignty, and rejecting Trump's demands outright, with Danish officials calling it "blackmail."

Trump has not ruled out military options, linking his threats to a perceived Nobel Peace Prize snub, which could fracture NATO alliances and trigger broader geopolitical turmoil.

On X, traders are buzzing about immediate impacts—S&P futures dipping, VIX spiking from 13 to potentially 40 in a flash, and crypto liquidations exceeding $1B amid risk-off sentiment.

Oil prices are already edging higher on China data, but Greenland tensions add uncertainty, pushing safe havens like gold while hammering stocks and autos.

These risks—trade retaliation, alliance breakdowns, and failed annexation attempts—could cascade into major market disruptions, echoing past tariff shocks that tanked equities.

With no deal in sight for Greenland (public support in the U.S. is low at 17%, and force is even less favored), volatility looks set to surge.

Hedging with VIX futures or options isn't a bad idea for protection—better safe than sorry in this high-stakes game.

SNAP: 2026 Bull Case Driven by AI and AR InnovationIf you haven`t sold the double top on SNAP:

nor bought the dip afterwards:

As we enter 2026, Snap Inc. (SNAP) presents a compelling bullish case for investors willing to bet on a social media turnaround story.

Trading around $7.53 with a market cap of approximately $13 billion, the stock is down 91% from its 2021 all-time high, yet it boasts a rock-bottom valuation—price-to-sales near 2.2x, one of its cheapest since the 2017 IPO.

With monthly active users (MAUs) approaching 1 billion and daily active users (DAUs) at 477 million (up 8% YoY in Q3 2025), SNAP’s scale is undervalued compared to peers like Meta or Pinterest, setting the stage for a potential rebound if execution aligns.

Key tailwinds include SNAP’s aggressive push into AI and AR technologies.

Recent partnerships, such as the $400 million deal with Perplexity AI for enhanced search features in Snapchat, signal innovation that could boost user engagement and ad revenue.

The upcoming 2026 launch of lightweight AR Specs glasses aims to capitalize on augmented reality commerce, while Snapchat+ subscriptions are already generating ~$700 million in annual recurring revenue.

Q3 2025 results showed 10% revenue growth to $1.507 billion and positive free cash flow of $93 million, hinting at improving margins amid cost-cutting efforts. Analysts’ consensus 12-month target sits at $9.86, implying ~30% upside, with some optimistic calls reaching $13–16.

On X (formerly Twitter), sentiment leans bullish for 2026: many traders call it a “buy & forget” stock at current levels, with several predicting targets of $17+ in the coming months and $40+ by year-end.

Others highlight parallels to Spotify’s (SPOT) 10x run post-profit inflection, noting SNAP’s forward P/E compression to 17x. Reddit discussions emphasize non-U.S. user growth and emerging revenue streams (AI features, AR commerce, subscriptions) as key catalysts for a potential 2–3x winner.

Of course, risks persist: Regulatory pressures (e.g., age restrictions in the UK and Australia) and competition from TikTok could cap growth, while recent insider sales add caution.

Still, with Q4 2025 earnings on February 3 potentially serving as a catalyst, SNAP’s asymmetric upside makes it a speculative buy for those eyeing tech recovery plays in 2026.

If AI/AR bets pay off, this stock could snap back strongly.

JBL Jabil Options Ahead of EarningsIf you haven`t bought JBL before the rally:

Now analyzing the options chain and the chart patterns of JBL Jabil prior to the earnings report this week,

I would consider purchasing the 220usd strike price Puts with

an expiration date of 2025-12-19,

for a premium of approximately $8.45.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

U Unity Potential Buyout Soon?!If you missed my previous signal on U (Unity):

Now Unity Technologies (NYSE: U) just caught fire — surging 12.5% in a single day — on a massive uptick in volume that should have every sharp trader watching closely. With $39.1M in volume against a daily average of 9.4M shares, something is clearly brewing beneath the surface.

But this isn’t just about technicals — the options market is lighting up with unusual activity, and there’s fundamental buyout potential that’s getting harder to ignore.

🔍 Options Traders Are Making Bold Bets

Yesterday: Traders loaded up on January 16 $37 strike calls — deep out-of-the-money, high-risk, high-reward plays.

Today: A massive $3.5 million bet was placed on the $30 strike calls, also expiring January 16.

These aren’t casual bets. This is smart money positioning for a potential takeover or major catalyst, and the timeline is clear: January 2025.

📈 Why a Buyout Could Be Back on the Table

Let’s rewind. On August 9, 2022, AppLovin (APP) made an unsolicited offer to acquire Unity in an all-stock deal worth $17.5B, valuing Unity shares at $58.85 — an 18% premium at the time. Unity rejected the deal.

Fast forward to today:

AppLovin's market cap has exploded — now sitting at a jaw-dropping $127B, up 3,800% since late 2022.

Unity, meanwhile, is a shadow of its former self, trading far below its ATH of $201.12 (November 2021), with ongoing struggles in monetization and competition.

But this disparity creates a prime M&A setup:

AppLovin now has the firepower and strategic incentive to revisit the acquisition — with Unity’s depressed valuation, it’s arguably a bargain.

The AI + gaming narrative is red hot. Combining Unity’s engine with AppLovin’s ad and monetization capabilities could be the synergy Wall Street loves.

🎯 The Trade Setup

Unity just broke out with conviction on high volume — this could be the first leg of a larger move.

Options flow suggests bullish sentiment into early 2025.

A renewed takeover offer could easily push the stock back toward the $50–60 zone, if not higher.

🧠 Final Thoughts

Unity is no stranger to volatility, but when volume spikes, options explode, and a cash-rich suitor like AppLovin is thriving, traders should sit up and pay attention.

We may be watching the early stages of a buyout story 2.0 unfold — and Wall Street might be starting to price it in.

📌 Watch Unity (U) closely in the coming weeks. The market may be whispering — or shouting — "Takeover incoming."

AAPL Poised for Continued GrowthIf you haven`t bought AAPL before the rally:

What to consider now:

1. AI-Driven iPhone Upgrade CycleApple’s integration of Apple Intelligence, its proprietary AI platform, is set to catalyze a significant iPhone replacement cycle. Posts on X highlight positive sentiment around AI-driven demand, with estimates suggesting a 40% year-over-year surge in iPhone shipments in China during May 2024, signaling strong consumer interest. New AI features, such as on-device processing for enhanced privacy and functionality, are expected to drive accelerated hardware upgrades. Analysts, including Bernstein, project these features could boost upgrade rates, with even a 1% increase in upgrades driving meaningful revenue growth. With the iPhone 15 and future iterations leveraging AI, Apple is likely to capture pent-up demand, as noted by industry observers who see long-term revenue growth from its 7% year-over-year increase in active installed base.

2. Strong Ecosystem and Services GrowthApple’s ecosystem—spanning iPhones, iPads, Macs, and wearables—continues to drive customer loyalty and recurring revenue. The company reported record services growth in Q2 2025, with revenue reaching $95.4 billion, up 5% year-over-year. Services like Apple Music, iCloud, and Apple TV+ benefit from the growing active device base, which ensures sticky, high-margin revenue streams. This ecosystem strength mitigates concerns about short-term iPhone sales fluctuations, as Apple captures upgrade revenue over time. The seamless integration of hardware and services creates a moat that competitors struggle to replicate, reinforcing AAPL’s long-term growth potential.

3. Technical Bullish MomentumFrom a technical perspective, AAPL exhibits strong bullish patterns across multiple timeframes. TradingView analyses point to a rising bullish channel, with higher highs and higher lows signaling sustained upward momentum. Key bullish patterns, such as an ascending wedge and triangle, are forming around current price levels, suggesting potential breakouts. For instance, if AAPL clears $203.21 with volume, it could target $204.98 or higher, with some analyses eyeing $240 as a near-term resistance. Technical indicators like a rising RSI and MACD convergence further support short-term bullish momentum. Despite recent consolidation, reduced volatility and a strong setup pattern indicate AAPL is primed for a breakout.

4. Analyst Optimism and Market SentimentAnalyst sentiment remains overwhelmingly positive, with a consensus “Buy” rating and a 12-month price target of $228.85, implying a 14.05% upside from the current price of $200.66 as of June 2025. Hedge funds like Third Point see “significant” upside, driven by AI features that could meaningfully boost earnings. Bernstein’s raised price target to $240 reflects confidence in Apple’s ability to monetize AI through hardware and services. Posts on X also highlight investor optimism, with AAPL’s $350 billion market cap increase in a single day underscoring strong market confidence in its AI-driven growth chapter.

5. Global Expansion and Emerging MarketsApple’s growth in emerging markets, particularly India and China, bolsters its bullish case. Improved guidance for December 2023, driven by iPhone 15 adoption and India’s market potential, signals untapped opportunities. Apple’s ability to penetrate these high-growth regions, combined with its premium brand appeal, positions it to capture a larger share of global smartphone and tech markets.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

VKTX Viking Therapeutics Potential Buyout Soon?!If you haven`t bought VKTX before the previous rally:

If GLP-1 obesity drugs are a multi-hundred-billion-dollar opportunity, a successful VK2735 (injectable + oral) could justify a valuation far north of where VKTX trades today—if it makes it to market.

My bullish thesis:

1. GLP-1 Momentum + “Mini Lilly / Novo” Narrative

VKTX is seen as a “pure play” on the global obesity and metabolic-disease boom.

Viking’s lead program, VK2735, is a dual GLP-1/GIP receptor agonist being developed in both injectable and oral form for obesity and related metabolic disorders.

Phase 1 and Phase 2 data for the injectable version have already shown meaningful weight loss with an encouraging safety/tolerability profile, which is why it advanced into large Phase 3 obesity trials.

An oral version of VK2735 is in Phase 2 obesity trials and, in the VENTURE oral study, delivered up to ~12.2% mean weight loss at 13 weeks, with a clear dose response.

2. Rapid Trial Execution = Strong Momentum & Upcoming Catalysts

Another big talking point is how fast Viking is executing on its trials, which bulls see as a leading indicator of future news flow:

Viking recently announced completion of enrollment in its Phase 3 VANQUISH-1 VK2735 obesity trial, with ~4,650 patients (above the original 4,500 target).

The company highlighted VK2735 data at ObesityWeek 2025 and continues to position both injectable and oral formulations as core programs.

Management has reiterated that VK2735 oral and injectable programs are moving forward on schedule, with more data expected as Phase 3 and longer-duration studies mature.

3. Short Interest + “Squeeze Fuel” Angle

VKTX has a high short interest, which Twitter traders love to highlight:

Recent data shows around 22–23% of the float short, with days to cover >5 based on average volume.

For many momentum and options traders, this is exactly the kind of setup they look for:

High short interest = a lot of investors betting against the stock.

Any positive surprise (trial data, partnership, M&A rumor, or a strong breakout on the chart) could force shorts to cover.

If that happens during a period of high retail interest, the price action can get violent to the upside.

4. Analyst Targets + Big Pharma Takeover Speculation

Analyst consensus is currently Strong Buy, with an average price target around $95+.

On top of that, there’s constant speculation that VKTX could become a takeover target:

The GLP-1 market is being dominated by Eli Lilly (Zepbound, Mounjaro) and Novo Nordisk (Wegovy, Ozempic).

Many large pharma companies without a strong obesity franchise might prefer buying a late-stage asset rather than starting from scratch.

VK2735, with Phase 3 obesity trials underway and promising oral data, is the kind of asset that fits that narrative.

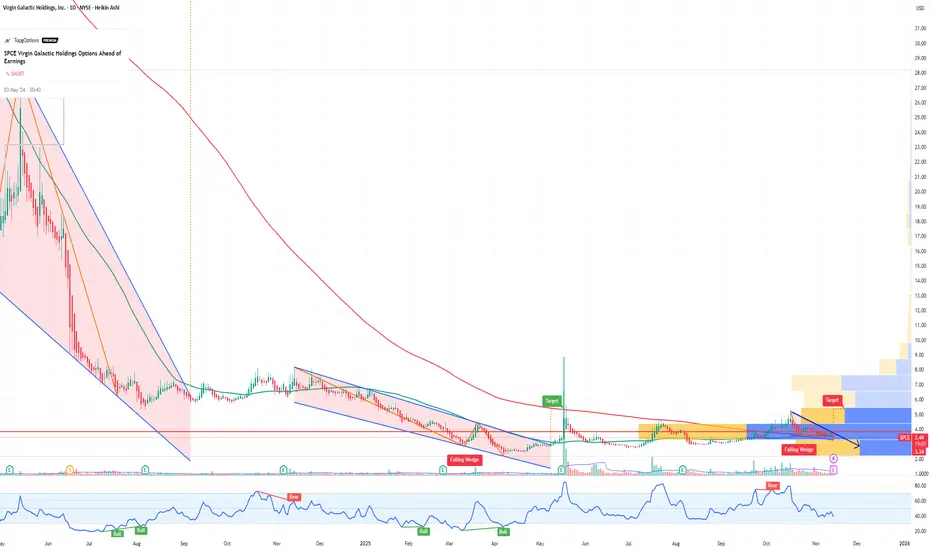

SPCE Virgin Galactic Holdings Options Ahead of EarningsIf you haven`t sold SPCE before the share dilution:

Now analyzing the options chain and the chart patterns of SPCE Virgin Galactic Holdings prior to the earnings report this week,

I would consider purchasing the 3.50usd strike price Puts with

an expiration date of 2025-11-14,

for a premium of approximately $0.37.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

RDDT Reddit Options Ahead of EarningsAnalyzing the options chain and the chart patterns of RDDT Reddit prior to the earnings report this week,

I would consider purchasing the 210usd strike price Calls with

an expiration date of 2025-11-7,

for a premium of approximately $11.00.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

WDC Western Digital Corporation Options Ahead of EarningsIf you haven`t bought WDC before the rally:

Now analyzing the options chain and the chart patterns of WDC Western Digital Corporation prior to the earnings report this week,

I would consider purchasing the 160usd strike price Calls with

an expiration date of 2025-11-21,

for a premium of approximately $4.35.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

NEM Newmont Corporation Options Ahead of EarningsAnalyzing the options chain and the chart patterns of NEM Newmont Corporation prior to the earnings report this week,

I would consider purchasing the 87usd strike price Puts with

an expiration date of 2025-10-24,

for a premium of approximately $2.18.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

VIX The Calm Before the Next Wave of Volatility! Recession RisksAfter last week’s sharp selloff across equities and crypto, followed by a swift recovery on Monday, many traders are once again lulled into a sense of comfort. But beneath the surface, volatility is quietly building — and the VIX is starting to tell the story.

From Panic to Complacency — Too Fast

Friday’s market crash revealed how fragile sentiment still is. We saw broad-based liquidations, risk-off flows, and a short spike in volatility as traders scrambled for protection. Then, as if nothing happened, Monday brought a sharp rebound — driven by short-covering, dip-buying algos, and a belief that the correction was “overdone.”

Geopolitical Flashpoints: U.S.-China Tensions

The ongoing conflict between the U.S. and China over critical metals exports has intensified. China controls a large portion of rare earth metals, essential for electronics, batteries, and defense technology. Recent U.S. threats to impose sanctions or tariffs on key exports, coupled with potential Chinese retaliatory measures, have created uncertainty for supply chains.

Markets hate uncertainty. Every news cycle mentioning trade escalation acts like a volatility catalyst, as investors hedge against unexpected economic shocks. This alone can drive the VIX higher, even if the S&P 500 has short-term rallies.

Trump Tariff Threats and Market Psychology

Adding fuel to the fire, former President Trump has repeatedly hinted at renewed tariff measures. While the headlines may seem political theater, history shows that even the anticipation of tariffs can disrupt equities and spark short-term volatility spikes.

Friday’s selloff can be partially attributed to traders pricing in these geopolitical and policy risks, which are not reflected in earnings reports or fundamentals — making hedging through VIX-linked products increasingly attractive.

Earnings and Economic Signals

Beyond geopolitics, the earnings season will likely reveal weak spots across sectors. Companies exposed to global supply chains, tech hardware, and industrials may report margins under pressure. This combination — disappointing earnings and global trade uncertainty — often precedes volatility expansions.

Historical patterns show that VIX rises ahead of earnings dispersion and macro shocks, as investors scramble for protection against downside surprises.

Potential upside target: 25+ if earnings disappoint and SPX breaks below $6000

SPY S&P 500 etf Oversold on the RSI ! 2025 Price Target ! The SPDR S&P 500 ETF Trust (SPY) is flashing a major buy signal, with its Relative Strength Index (RSI) currently sitting at 28.33 — firmly in oversold territory. Historically, every time SPY has entered oversold levels on the RSI, institutional buyers have stepped in aggressively, driving sharp rebounds in the following weeks and months.

The last time SPY dipped below the 30 RSI threshold was during market pullbacks in 2022 and 2023 — both of which were followed by significant rallies as institutions capitalized on discounted valuations. The current setup is no different. With earnings growth stabilizing, inflation cooling, and the Federal Reserve signaling a potential shift toward rate cuts in the second half of the year, the backdrop for a recovery is aligning perfectly.

Technically, SPY is also approaching key support levels that have held strong in past market corrections. The combination of an oversold RSI and strong institutional appetite at these levels creates a compelling case for a bounce.

My price target for SPY by year-end is $640, representing over 15% upside from current levels. With sentiment stretched to the downside and technical indicators flashing green, SPY looks primed for a sharp and sustained rebound. Now could be the perfect time to position for the next leg higher.

GOOG Alphabet Options Ahead of EarningsIf you haven`t bought GOOG before the previous rally:

Now analyzing the options chain and the chart patterns of GOOG Alphabet prior to the earnings report this week,

I would consider purchasing the 170usd strike price Calls with

an expiration date of 2025-7-18,

for a premium of approximately $4.35.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

RKT Rocket Companies Options Ahead of EarningsIf you haven`t bought RKT before the previous earnings:

Now analyzing the options chain and the chart patterns of RKT Rocket Companies prior to the earnings report this week,

I would consider purchasing the 13usd strike price Calls with

an expiration date of 2026-1-16,

for a premium of approximately $1.37.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

Baidu ($BIDU): China’s Google Is Ready to Break OutIf you haven`t bought BIDU on the previous dip:

What you need to know now:

1. Baidu = The Google of China

Baidu dominates China’s search engine market, holding over 60% market share, making it the Google equivalent in the world's second-largest economy.

Its advertising business is deeply entrenched in Chinese internet infrastructure.

As digital ad spending rebounds in China, Baidu’s core business benefits directly.

2. AI and Autonomous Driving Moonshots

Baidu is China’s national AI champion, pouring billions into next-gen technologies:

Ernie Bot (Baidu’s ChatGPT competitor) is now integrated across its ecosystem and enterprise offerings.

Apollo Go, Baidu’s autonomous driving platform, already operates robo-taxis in multiple Chinese cities and has received licenses for fully driverless operations.

Baidu also provides AI cloud services, competing with Alibaba Cloud and Huawei.

With the Chinese government pushing AI self-sufficiency, Baidu is one of the biggest beneficiaries.

3. Cheap Valuation with High-Tech Exposure

Baidu trades at a forward P/E under 10 and price-to-sales under 2, despite being a major player in AI, cloud, and mobility.

That’s a fraction of what US tech firms with similar ambitions (like Alphabet or Tesla) are valued at.

Over $25 billion in cash and investments on the balance sheet adds a margin of safety.

4. Government Support & Stimulus Tailwinds

The Chinese government is pivoting back toward supporting tech innovation, especially in AI, after years of regulatory crackdowns.

Baidu is aligned with national AI and autonomous driving goals.

If the government ramps up fiscal stimulus, especially in infrastructure and technology, Baidu will likely benefit.

Disclosure: I am part of Trade Nation's Influencer program and receive a monthly fee for using their TradingView charts in my analysis.

IOT Samsara Options Ahead of EarningsIf you haven`t sold IOT before the previous earnings:

Now analyzing the options chain and the chart patterns of IOT Samsara prior to the earnings report this week,

I would consider purchasing the 34.5usd strike price Puts with

an expiration date of 2025-9-5,

for a premium of approximately $2.00.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

AI C3ai Options Ahead of EarningsIf you haven`t bought AI before the previous rally:

Now analyzing the options chain and the chart patterns of AI C3ai prior to the earnings report this week,

I would consider purchasing the 25usd strike price Calls with

an expiration date of 2025-9-19,

for a premium of approximately $0.09!

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.

BBY Best Buy Options Ahead of EarningsIf you haven`t bought BBY before the rally:

Now analyzing the options chain and the chart patterns of BBY Best Buy prior to the earnings report this week,

I would consider purchasing the 70usd strike price Puts with

an expiration date of 2026-1-16,

for a premium of approximately $4.90.

If these options prove to be profitable prior to the earnings release, I would sell at least half of them.