Counter-trend long on Iridium Communications Inc (Ticker IRDM)

NASDAQ:IRDM

Technicals:

- September - January the price failed to break through the support zone 16.80 - 18.00

- strong weekly candle closed above 19.90 ressistance (there since Jul 2018)

- 20.10 - 20.40 can still be retested

- upswing to close Sep 8th weekly candle looks logical

- best-case scenario targets long-term bear trend upper resistance line

- take care of 24.20 - 25.40 resistance zone - partial close preferred

- scenario invalidated if two bars close below 19.00 - price can retest support zone 16.80 - 17.80

Fundamentals:

- company emerged from bankruptcy and has successfully returned to profitability.

- business model centers on providing connectivity via its orbital satellite constellation for tasks such as tracking shipping containers at sea and monitoring pipelines for both government and private-sector clients

- has long-term, fixed-price contracts with the U.S. Department of Defense.

- due to the modern state of its satellite fleet, free cash flow is being directed toward share buybacks and dividends rather than capital expenditures on new rocket launches.

but:

- competition with Starlink for the retail user segment and partial dependency on third-party aerospace companies for orbital satellite deployment.

Conclusion:

- fundamentally, the company is a prominent representative of the aerospace industry during its "renaissance" era (which is now and potentially has bright future).

- with effective management, the stock price has the potential for multi-bagger growth over time.

- the technical setup remains in a bearish trend.

- t here are two distinct positions available: one for high-risk traders and another for patient, long-term investors. For short-term traders, the risk of a further drawdown or a retest of support zones remains high. For long-term traders or investors, an entry price within the $16.00 – $22.00 range is considered attractive.

but:

- the upcoming earnings report on Feb 12th will be the primary catalyst determining the price direction in the short-to-medium term.

# - - - - -

Position - Buy Long ⬆️

# - - - - -

✅ Entry Point 1 Short Term - 21.19

🛑 SL Short Term - 19.75

🤑 TP Short Term - 24.15

⚙️ Risk/Reward - 1 : 2.05 👌

⌛️ Timeframe - 2 weeks 🗓

# - - - - -

✅ Entry Point 2 Middle Term - 20.20

🛑 SL Long term - 18.50

🤑 TP Long Term - 27.95

⚙️ Risk/Reward - 1 : 4.15 👌

⌛️ Timeframe - 3-4 months 🗓

# - - - - -

Good Luck! ☺️

Space

Northrop Grumman: Architecting the Future of AI Warfare

Northrop Grumman (NOC) is redefining the defense sector by fusing lethal hardware with digital intelligence. While the delivery of the 1,500th F-35 center fuselage cements its manufacturing legacy, the company’s valuation thesis is shifting. Investors must now analyze Northrop as a master architect of space militarization, autonomous systems, and AI-driven command structures.

Geopolitics and Geostrategy

Global conflicts now demand seamless integration across land, sea, air, and space. Northrop’s Integrated Battle Command System (IBCS) serves as the central nervous system for this new reality. It connects disparate sensors and shooters, creating a unified shield against hypersonic threats. As the space militarization market expands, nations require robust ground systems to command orbital assets. Northrop dominates this geostrategic niche, securing critical infrastructure that nations cannot afford to lose.

Technology and Innovation

The company’s "BattleOne" initiative represents a quantum leap in military logic. This digital ecosystem accelerates decision-making by fusing data from satellites and terrestrial sensors. It utilizes advanced artificial intelligence to predict enemy movements and optimize response times. Northrop is not merely selling weapons; it is selling decision dominance. This move toward software-defined warfare creates a high competitive moat against legacy hardware manufacturers.

Industry Trends: The Rise of Autonomous Mass

The U.S. Air Force currently prioritizes "Collaborative Combat Aircraft" (CCA) to fly alongside manned fighters. Northrop is aggressively targeting this sector with platforms like the "Lumberjack." This one-way attack drone delivers kinetic capabilities at an affordable price point. Furthermore, their ANCILLARY vertical take-off drone eliminates the need for traditional runways. These innovations align perfectly with the industry trend toward "affordable mass" and distributed lethality.

Electronic Warfare and Cyber Security

Nations fight modern warfare in the electromagnetic spectrum. Northrop’s electronic warfare (EW) solutions actively jam enemy communications while shielding friendly networks. These systems integrate cyber resilience directly into the hardware architecture. As adversaries develop sophisticated jamming techniques, Northrop’s multispectral capabilities become non-negotiable for the Pentagon. This ensures recurring revenue streams for constant software and hardware upgrades.

Business Models and Economics

Management is adapting its business model to match tightening fiscal environments. The shift toward platforms like Lumberjack signals a pivot from low-volume, high-cost units to high-volume, lower-cost attrition assets. This diversification protects the balance sheet against potential budget cuts to expensive flagship programs. By balancing the massive F-35 supply chain with agile drone production, the company optimizes its revenue mix.

Management and Leadership

Executive leadership demonstrates strategic agility by embracing digital engineering. They are successfully navigating the transition from a hardware-first mindset to an AI-centric strategy. Their ability to deliver on legacy contracts while funding speculative high-tech ventures instills confidence. Leadership is effectively positioning the firm to capture the lion's share of the Joint All-Domain Command and Control (JADC2) budget.

Conclusion

Northrop Grumman has evolved beyond the definition of a traditional defense contractor. It stands as a technology powerhouse integrating space, AI, and autonomous systems. The company effectively monetizes the complexity of modern warfare. For investors, NOC represents a strategic play on the convergence of silicon and steel in the 21st century.

ASTS 4H: space internet or orbital dream?AST SpaceMobile (ASTS) is consolidating above the $61–69 zone, right near the 0.618 Fibonacci level of its last major rally. On the 4H chart, momentum shows early reversal signs: falling volume on pullbacks, stochastic turning up, and buyers defending local lows. The bullish setup holds as long as price stays above $61, with upside targets at $100 and $135 where the extension projection aligns.

Fundamentally , as of November 2025, ASTS stands out as one of the most promising yet capital-intensive players in the satellite telecom industry. The company completed deployment of its BlueWalker test constellation and is preparing for commercial rollout of direct-to-cell satellite connectivity. Successful phone-to-satellite calls using standard smartphones - validated with AT&T and Vodafone - mark a true technological milestone, positioning ASTS as a potential first-mover in global space-based mobile internet.

Revenue for the first nine months of 2025 reached roughly $55M, almost double last year’s level, but operating losses still exceed $300M due to high manufacturing and launch costs. The company holds about $180M in cash versus ~$260M in debt, continuing to rely on strategic partnerships and funding programs to maintain liquidity. The key upcoming catalyst is the commercial network activation in 2026 in cooperation with AT&T, Vodafone, and Rakuten, which could dramatically change valuation if successful.

With investor attention shifting back to space communications, competition with Starlink and Lynk Global is heating up, but ASTS’s advantage lies in using standard smartphones without extra hardware. Risks remain - high capital needs, launch delays, and dependency on partner timelines - yet the reward potential is extraordinary if execution holds.

Tactically, staying above $61 keeps the bullish structure alive with $100 and $135 as primary targets. A breakdown below $60 would negate the setup.

They’ve already connected phones to space - now let’s see if they can connect revenue to profit.

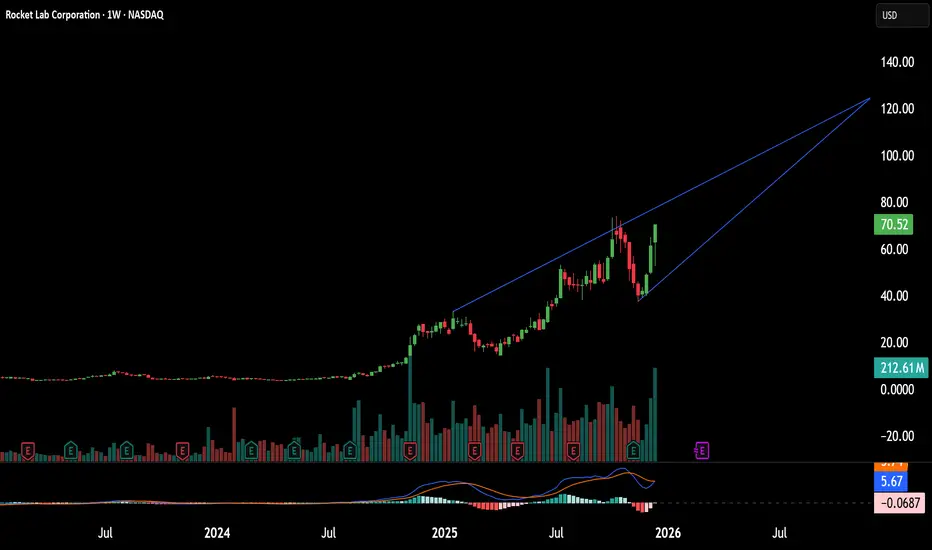

Can a Small-Sat Pioneer Become a Defense Superpower?Rocket Lab has transformed from a niche small-satellite launch provider into a strategic national security asset, closing 2025 with 21 successful Electron launches and a remarkable 175% stock surge. The company's evolution culminated in an $816 million Space Development Agency contract to build 18 satellites for hypersonic missile threat detection, signaling its emergence as a primary defense contractor. This vertical integration strategy positions Rocket Lab as a critical player in an era where supply chain sovereignty has become paramount for military readiness.

The technological centerpiece of Rocket Lab's 2026 ambitions is the Neutron rocket, a medium-lift vehicle capable of carrying 13,000 kilograms to low Earth orbit. Set for its maiden test flight in mid-2026, Neutron features the innovative "Hungry Hippo" fairing design and 3D-printed Archimedes engines, targeting the lucrative mega-constellation market currently dominated by SpaceX's Falcon 9. This technological leap, combined with over 550 global patents covering critical propulsion and structural innovations, creates a formidable intellectual property moat that competitors cannot easily replicate.

The financial trajectory underscores this transformation: analysts project 52.2% EPS growth for 2026, reaching $0.27 per share and dramatically outpacing traditional aerospace giants like Lockheed Martin (0.6%) and Northrop Grumman (-7.6%). A potential SpaceX IPO at $1.5 trillion valuation could trigger sector-wide revaluation, with Rocket Lab standing as the only publicly traded, vertically integrated alternative. Wall Street has responded accordingly, raising price targets to $90 as the company bridges the gap between startup agility and aerospace titan scale, with defense contracts poised to dominate its revenue mix.

FJET - Cycles Don’t Lie - Structure Is Repeating Again!Markets don’t move randomly.

They move in cycles , and AMEX:FJET just completed another one.

📊 Technical Analysis

FJET has now officially broken above the falling red channel, confirming the end of the corrective phase and the start of the next impulse leg.📈

This is important, because the structure has been repeating with precision:

• An impulse move

• Followed by a curved correction

• A retest of demand

• Then a break in structure that launches the next expansion

In the previous completed cycle, FJET rallied from around $6.4 to nearly $31 , delivering a ~400% surge before entering correction.

🏹This time, price once again respected the $10- $11 demand zone , formed a rounded base, and has now flipped momentum bullish by reclaiming and breaking above the descending channel marked in red.

With structure already broken to the upside, the bias shifts from anticipation to trend-following.

⚔️As long as price holds above the former channel and demand remains intact, the path of least resistance points toward continuation and a potential push toward new all-time highs.

💡 Bigger Picture (Fundamentals)

Starfighters Space is already operational, running the world’s only commercial fleet of Mach 2-capable F-104 aircraft, not a prototype, not a concept.

🛰️ The company has secured strategic validation from NASA, Lockheed Martin, GE Aerospace, and the U.S. Air Force , a level of credibility rarely seen at this stage.

Following its public listing, FJET now has fresh capital to support expansion, R&D, and continued development of its STARLAUNCH platform.

🎯 Its focus sits at the intersection of small-satellite deployment and hypersonic testing, two of the fastest-growing segments in aerospace and defense.

The business model is built around a supersonic air-launch approach, designed to reduce both launch costs and timelines compared to traditional methods.

📈 Finally, post-IPO market interest remains strong, suggesting attention is shifting from hype to structure, exactly where durable trends tend to form.

📘 Bottom line

FJET has completed another corrective phase, respected demand, and broken structure to the upside, just as it has done before major expansions.

With fundamentals supporting real operations, real contracts, and real demand, this is no longer a story built on speculation.

From here, the focus shifts to trend-following, structure management, and risk control, letting the cycle play out, not forcing it.

📌 Always do your own research and speak with your financial advisor before investing.

📚 Stick to your trading plan, entry, risk management, and execution.

All Strategies Are Good, If Managed Properly!

~ Richard Nasr

Disclaimer: I have been paid $800 by CDMG, funded by Starfighters Space, to disseminate this message.

FJET - Post-IPO Structure Is Taking Shape!After its public debut, Starfighters Space ( AMEX:FJET ) delivered exactly what strong listings tend to do:

an impulsive expansion 📈, followed by a healthy correction 📉, and now the early signs of structure forming.

This phase is where real opportunities usually start to emerge.

📊 Technical Analysis

Cycles are clearly repeating on FJET.🔄

In the previous cycle, FJET printed a strong impulse move from around $6.4 to approximately $31, representing a ~400% expansion🚀 .

That rally was followed by a curved correction , after which price retested the $10 demand zone and used it as a base for continuation.

🔄Now, we are seeing the same structure forming again.

FJET is currently trading within another curved correction , gradually rotating lower toward a newly formed demand zone between $10 and $11 . Importantly, this correction is unfolding with decreasing downside momentum, suggesting absorption rather than aggressive selling.

🏹The key trigger remains the last high marked in blue around $16.

A clean break and hold above this level would confirm bullish continuation and signal the start of the next impulse move, with the potential to push FJET toward new all-time highs above $31.

⚔️As long as the $10 demand zone holds, the structure continues to favor continuation over reversal.

💡 Bigger Picture

Now that FJET is officially public📊, the narrative has shifted from anticipation to execution.

Starfighters Space is not a speculative concept, it’s an operating aerospace company:

- Flying missions out of NASA’s Kennedy Space Center👩🚀

- Operating the world’s only commercial Mach 2-capable fleet

- Backed by validation from NASA, Lockheed Martin, GE, and the U.S. Air Force🛩

Post-IPO phases like this are often where institutions begin evaluating structure, liquidity, and follow-through, not at the highs, but during consolidation.

📘 Bottom line

FJET has moved past the chaos of its debut and is now building a base.🪨

If demand continues to hold and momentum rebuilds, this consolidation could be the pause before the next expansion.

This is the phase where patience matters most.

📌 Always do your own research and speak with your financial advisor before investing.

📚 Stick to your trading plan, entry, risk management, and execution.

All Strategies Are Good, If Managed Properly!

~ Richard Nasr

Disclaimer: I have been paid $800 by CDMG, funded by Starfighters Space, to disseminate this message.

LHX Analysis: $1B Space Deal Signals GrowthThe Strategic Pivot

L3Harris Technologies (NYSE: LHX) is redefining the defense landscape. While the stock has climbed 38.6% year-to-date, recent developments suggest the rally is just beginning. The catalyst is a massive $843 million contract with the Space Development Agency (SDA). This deal confirms L3Harris as a primary player in modern warfare infrastructure. With projected revenues hitting $22 billion and free cash flow nearing $2.7 billion, the fundamentals are robust. This analysis dissects the strategic drivers behind this growth.

Geopolitics & Geostrategy: The High Ground

Modern conflict has shifted to orbit. Major powers are actively militarizing space to secure communications and surveillance advantages. The SDA contract for infrared satellites places L3Harris at the center of this geopolitical contest. Governments demand persistent missile warning capabilities to counter hypersonic threats from rivals. L3Harris provides the "eyes in the sky" necessary for national survival. This geostrategic necessity ensures long-term demand for their orbital assets.

Industry Trends: From Armor to Dat

The defense industry is moving away from heavy manufacturing toward intelligence and connectivity. Tanks and ships are vulnerable without secure data links. L3Harris specializes in this exact niche: avionics, electronic warfare, and sensing. They are not building the metal shell; they are building the brain. This trend favors agile tech integrators over traditional heavy metal defense contractors. The market values high-margin electronics over low-margin hardware.

Technology & Science: Infrared Precision

The science behind the new SDA contract is critical. These satellites utilize advanced infrared sensors to track heat signatures from missile launches. Developing these sensors requires elite engineering and physics capabilities. L3Harris has mastered the suppression of "background noise" in space to detect small targets. This scientific edge creates a high barrier to entry for competitors. Few companies possess the technical heritage to execute this level of precision engineering.

Business Models & Economics: Cash Flow Efficiency

L3Harris operates on a highly efficient financial model. The company generated nearly $2.7 billion in free cash flow (FCF) recently. This liquidity allows them to fund internal Research and Development (R&D) without relying on expensive debt. In a high-interest-rate macroeconomic environment, cash is king. Their ability to self-fund innovation while paying dividends makes them attractive to institutional investors. The economic engine here is stability combined with growth.

Cyber & High-Tech: Hardened Systems

Space assets are prime targets for cyberattacks. L3Harris integrates "cyber-resilience" directly into its satellite architecture. They do not just build communication radios; they build encrypted networks that withstand jamming and spoofing. This convergence of hardware and cybersecurity is a key selling point. Defense clients pay a premium for systems that operate reliably in contested electronic environments.

Management & Leadership: Organic Discipline

The leadership team at L3Harris is executing a disciplined strategy. Instead of relying solely on expensive acquisitions, they are driving "organic growth." The recent financial report highlights this internal efficiency. Management focuses on operational excellence and clearing supply chain bottlenecks. This focus has improved margins and delivery times. Investors trust leadership that delivers on promises without overleveraging the balance sheet.

Patent Analysis: Protecting Intellectual Property

A review of the sector suggests L3Harris holds a "moat" of intellectual property. Their patent portfolio likely covers proprietary sensor integration and waveform technologies. These patents legally protect their market share in tactical communications. Competitors cannot easily replicate their avionics suites without infringing on protected tech. This IP fortress secures future revenue streams and keeps margins high.

Forecast: The Trajectory

L3Harris is currently undervalued relative to its potential. The $843 million contract is a signal, not an anomaly. As global tensions rise, the premium on space-based intelligence will increase. The company’s focus on high-tech sensors, strong cash flow, and strategic positioning makes it a formidable stock. Traders should view the current price as an entry point before the full value of these space contracts materializes in 2026 earnings.

FJET - From Private Skies to Public Markets!!Most retail investors never had access to the biggest space winners.🌌

SpaceX went from a private valuation near $46B to over $800B without ever giving the public a chance to participate.

This time, the door is open❗️

Starfighters Space, Inc. AMEX:FJET has officially entered the public markets, giving everyday investors exposure to a real aerospace company… Not a concept, not a slide deck; but one already flying missions out of NASA’s Kennedy Space Center.

📊 Technical Analysis

Following its public debut, FJET delivered a strong impulsive move 📈, confirming aggressive buyer interest.

After a healthy correction into demand, buyers stepped in again, keeping the structure intact.

Price has now broken and held above the $10 area , confirming bullish continuation and validating the higher-timeframe structure.

🔁 From here, the expectation is a shallow pullback / consolidation , followed by continuation in line with the scenario marked in purple.

🏹 The $20 zone represents the first target , and upon reaching it, I will be watching for further upside , at which point I’ll post an updated outlook.

💡 Bigger Picture

This isn’t a speculative space idea, it’s an operating aerospace company 💼with rare credentials:

- World’s only commercial Mach 2-capable fleet of Lockheed F-104 Starfighters.

- Operating directly out of NASA’s Kennedy Space Center.

- Strategic validation from NASA, Lockheed Martin, GE, and the U.S. Air Force.🛩

- Pioneering a hypersonic air-launch platform designed to dramatically reduce the cost and timeline of microsatellite deployment.

- Successfully completed a $40M Regulation A+ raise , transitioning from private capital into the public markets.

Recent history shows that real aerospace IPOs tend to move early:

Voyager, Firefly, Karman, and AIRO all saw sharp post-listing expansions.

In this sector, the first phase after going public often matters the most.

📘 Bottom line

FJET offers something rare:

💎Early exposure to a credible aerospace company right after it entered the public markets, before full institutional positioning and before the story became widely crowded.

📡Whether you approach it as a technical setup, a newly public aerospace play, or a longer-term space infrastructure narrative, this is a name worth keeping on the radar.

⚠️ Always do your own research and speak with your financial advisor before investing.

📚 Stick to your trading plan, entry, risk management, and execution.

All strategies are good; if managed properly.

~ Richard Nasr

Disclaimer: I have been paid $800 by CDMG, funded by Starfighters Space, to disseminate this message.

Rocket Lab’s Strategic Ascent: Beyond the NumbersRocket Lab (NASDAQ: RKLB) has solidified its status as a cornerstone of the modern space economy. Following a turbulent period that saw shares retrace nearly 50%, the stock has staged a commanding recovery, rallying roughly 111% year-to-date. This resurgence is not merely a product of market speculation; it reflects a convergence of geopolitical necessity, operational maturity, and favorable macroeconomic shifts.

Geostrategy and Defense Dynamics

The company’s recent momentum is deeply rooted in shifting geopolitical realities. The successful STP-S30 mission for the U.S. Space Force, launched five months ahead of schedule, underscores Rocket Lab’s critical role in national security. In an era where orbital assets are vulnerable to kinetic and cyber threats, the ability to rapidly replace satellites is a strategic deterrent. Rocket Lab provides the "responsive space" capability that Western defense planners demand.

Furthermore, the dedicated launch for the Japan Aerospace Exploration Agency (JAXA) highlights a strengthening of allied aerospace integration. As nations like Japan seek to diversify launch providers away from domestic bottlenecks, Rocket Lab has emerged as the preferred neutral partner. This expands its total addressable market beyond U.S. borders, insulating it from single-market risks.

Industry Trends and Valuation Benchmarks

A massive sector-wide repricing is underway, catalyzed by reports of a potential SpaceX IPO in 2026 at a $1.5 trillion valuation. This news has fundamentally altered how investors assess the space industry’s long-term economics. SpaceX’s valuation serves as a powerful anchor, validating the orbital economy’s scale.

As the only other publicly traded, vertically integrated launch provider with a proven track record, Rocket Lab is the primary beneficiary of this sentiment shift. Capital that once flowed into speculative pre-revenue SPACs is consolidating into proven operators. Rocket Lab’s business model, which combines launch services with high-margin space systems, offers investors a tangible hedge against the capital-intensive nature of pure launch plays.

Operational Excellence and Culture

Corporate culture remains Rocket Lab’s hidden alpha. While the broader aerospace sector struggles with chronic delays, Rocket Lab’s delivery of the STP-S30 mission ahead of schedule speaks to a unique internal ethos. This "execution-first" culture sharply contrasts with competitors who rely on PowerPoint engineering.

Management’s ability to navigate high-tech manufacturing challenges while maintaining launch cadence has built a reservoir of institutional trust. This reliability is a defensive moat. In the launch business, reputation is currency; Rocket Lab’s consistency allows it to command pricing power and secure long-term government contracts that competitors cannot access.

Technology and the Neutron Horizon

The upcoming Neutron rocket represents a technological inflection point. Scheduled for its maiden flight in the first half of 2026, Neutron moves the company from a small-lift niche to medium-lift dominance. This vehicle targets the lucrative constellation deployment market, currently a SpaceX monopoly.

From a patent and science perspective, Neutron’s design—featuring unique carbon composite structures and reusable fairings—signals a leap in material science application. These proprietary engineering solutions create high barriers to entry. By securing intellectual property around rapid reusability and automated manufacturing, Rocket Lab protects its margins against commoditization.

Conclusion

Rocket Lab’s recovery is structural, not accidental. It is driven by a unique intersection of defense utility, superior execution, and a repricing of the space sector’s potential. As the company prepares for the Neutron era, it is shedding its label as a "small launch" provider and emerging as a diversified aerospace prime.

THE RETURN BREAK OF REI TO $0,032There is a good chance we are going to see a new break on REI as we saw before.

We will follow the coin for new volume.

Rocket Lab to new all time highs as more things go to spaceRocket Lab build rockets. CEO has an extremely bright aura. Hard to find a better story-driven pure space play with SpaceX being private. I like Rocket Lab and invested because as more and more things fly and go to space, it has the wind at its back.

Is Rocket Lab the Future of Space Commerce?Rocket Lab (RKLB) is rapidly ascending as a pivotal force in the burgeoning commercial space industry. The company's vertically integrated model, spanning launch services, spacecraft manufacturing, and component production, distinguishes it as a comprehensive solutions provider. With key operations and launch sites in both the U.S. and New Zealand, Rocket Lab leverages a strategic geographic presence, particularly its strong U.S. footprint. This dual-nation capability is crucial for securing sensitive U.S. government and national security contracts, aligning perfectly with the U.S. imperative for resilient, domestic space supply chains in an era of heightened geopolitical competition. This positions Rocket Lab as a trusted partner for Western allies, mitigating supply chain risks for critical missions and bolstering its competitive edge.

The company's growth is inextricably linked to significant global shifts. The space economy is projected to surge from $630 billion in 2023 to $1.8 trillion by 2035, driven by decreasing launch costs and increasing demand for satellite data. Space is now a critical domain for national security, compelling governments to rely on commercial entities for responsive and reliable access to orbit. Rocket Lab's Electron rocket, with over 40 launches and a 91% success rate, is ideally suited for the burgeoning small satellite market, vital for Earth observation and global communications. Its ongoing development of Neutron, a reusable medium-lift rocket, promises to further reduce costs and increase launch cadence, targeting the expansive market for mega-constellations and human spaceflight.

Rocket Lab's strategic acquisitions, such as SolAero and Sinclair Interplanetary, enhance its in-house manufacturing capabilities, allowing greater control over the entire space value chain. This vertical integration not only streamlines operations and reduces lead times but also establishes a significant barrier to entry for competitors. While facing stiff competition from industry giants like SpaceX and emerging players, Rocket Lab's diversified approach into higher-margin space systems and its proven reliability position it strongly. Its strategic partnerships further validate its technological prowess and operational excellence, ensuring a robust position in an increasingly competitive landscape. As the company explores new frontiers like on-orbit servicing and in-space manufacturing, Rocket Lab continues to demonstrate the strategic foresight necessary to thrive in the dynamic new space race.

LONG-TERM $ASTSYou can't spell Sats without ASTS

This will be a trillion dollar company - here's the next few years, cheers!

GE Aerospace: How to go to the moon!GE's stock is soaring due to strong earnings and optimistic future guidance from its aerospace division.

1. Blowout Earnings: GE Aerospace reported earnings per share of $1.75, far exceeding analysts' expectations of $1.10.

2. Surging Orders: The company saw a 46% increase in orders last quarter, signaling strong demand for its products.

3. Revenue Growth: GE generated $10.8 billion in revenue, beating forecasts of $10 billion.

4. Wall Street Optimism: Analysts are raising price targets, with some predicting the stock could climb even higher.

5. Industry Momentum: The aerospace sector is experiencing a boom, with GE positioned as a key player.

I'm betting we are close to a pullback and then catapult to New ATH!

To the Moon: Space Isn't Just for Billionaires. It's for You TooTo your parents, getting involved in space meant joining NASA, becoming an astronaut, or — more realistically — building a scale model of the Saturn V and telling them you wanted to be "just like Neil Armstrong."

Today? You don’t need a PhD, perfect vision, or the ability to survive on dehydrated ice cream. The economics of orbit is accessible from your screen through the shares of publicly listed companies.

While billionaires are busy trying to out-flex each other in orbit, there’s a rapidly growing group of public companies that you can use as a launchpad to space exposure.

Let's explore (pun intended) how space is no longer science fiction only — it's an economic sector you can trade.

🚀 SpaceX: The Giant with a Gravitational Field

First, let’s get this out of the way: SpaceX is still private. Elon Musk’s rocket-powered unicorn dominates the headlines — and deservedly so. The company is launching Starlink satellites by the hundreds, winning NASA contracts, and discussing building cities on Mars where we can move and grow space potatoes.

But unless you have deep VC connections or you run a private equity fund, you can’t buy SpaceX stock yet. (Cue the tiny violin.) According to private-market estimates, SpaceX boasts a valuation of $350 billion, making it the world’s most expensive private company.

What you can do is invest in companies that supply, compete with, or benefit from the SpaceX era. Here are a few ideas.

🛸 Rocket Lab NASDAQ:RKLB : The Mini-SpaceX

If SpaceX is the Goliath of orbital launches, Rocket Lab is the David — except instead of a slingshot, it's using the Electron rocket and prepping the bigger Neutron.

Rocket Lab specializes in small satellite launches — think communications, Earth observation, climate monitoring. The company is cheaper, faster, and more frequent than the heavy-lifters like Falcon 9 by SpaceX. If you’re bullish on the boom in low-Earth orbit activity, Rocket Lab could be the small-cap rocket you can strap your portfolio to.

Bonus points — it’s not just a launch company. Rocket Lab, valued at around $10 billion, is expanding into satellite manufacturing, in-orbit services, and deep space missions.

👽 Intuitive Machines NASDAQ:LUNR : Houston, We Have a Moonshot

With a ticker symbol NASDAQ:LUNR — obviously leaning into the Moon theme — Intuitive is all about lunar landers and space infrastructure. The company is part of NASA’s Commercial Lunar Payload Services (CLPS) program, helping deliver payloads (science experiments, rovers, tech gizmos) to the Moon.

In the absence of crypto moons, these guys are aiming for the real thing.

But be warned: Intuitive is a true moonshot investment. As recently as March, the company's moon lander, Athena, couldn't pull off a stellar touchdown and its shares nosedived roughly 60%. Year to date, the stock is down 55%.

The startup is pioneering in a market that doesn’t quite exist yet at scale. Revenues are coming in phases, tied to contracts, with success as lumpy as a Moon crater. In a nutshell? It's a high-risk, high-reward kind of ride.

Still — if you're looking for an early, pure-play exposure to the Moon economy, Intuitive Machines, valued at just $1.5 billion, is basically as close as you can get.

🌟 Northrop Grumman NYSE:NOC : The Silent Space Titan

While Rocket Lab and Intuitive Machines get the Reddit buzz, Northrop Grumman keeps a low profile, winning contracts and building stuff that actually gets yeeted into space.

The company is deeply involved in NASA’s Artemis program, manufacturing boosters for the Space Launch System (SLS) — the rocket that’s supposed to return humans to the Moon. It also makes satellite systems, missile defense tech, and stealthy aerospace goodies for the US government.

Northrop isn’t going to quadruple overnight on a meme rally — it’s worth just under $70 billion. But it provides serious, steady exposure to the high-stakes space game — with dividends. It’s the choice for traders who like their moonshots with a side of mature risk management.

✨ Lockheed Martin NYSE:LMT : Space Cowboys in Business Suits

Lockheed Martin isn’t just the F-35 fighter jet company. It also builds the Orion spacecraft — NASA’s chosen ride for deep space missions, including Mars (if Elon doesn’t get there first).

Lockheed’s space division covers everything from weather satellites to missile warning systems. The company, worth around $111 billion, has been in the space race before Jeff Bezos came up with Blue Origin and way before Musk founded SpaceX.

Think of Lockheed like the expert-level astronaut: calm, collected, and still racking up mission hours while everyone else is learning which button not to press.

💫 Boeing NYSE:BA : Sometimes Up, Sometimes… Not So Much

Boeing’s Starliner capsule is supposed to ferry astronauts to the International Space Station. Supposed to. It’s been delayed more times than your average budget airline flight.

The astronauts that were stuck in space for nine months? Riding a Starliner that failed during docking (the mission was supposed to be a ten-day roundtrip). So Musk’s SpaceX had to intervene and bring those two space explorers back to earth in March.

Still, despite technical hiccups and PR headaches, Boeing remains heavily involved in the space economy. It builds rockets, satellites, and space station modules. Even when it trips, it trips forward — thanks to government contracts and industrial clout.

If you can stomach some turbulence, Boeing, worth $134 billion, offers another angle on the space trade.

🌙 RTX NYSE:RTX : Watching the Skies

You may not think "space" when you hear RTX (formerly Raytheon), but you should. The company builds sensors, satellites, and missile tracking systems — vital components of the US space and defense apparatus.

Space isn’t just about launching astronauts and rovers; it's about surveillance, communications, and security. RTX, valued at a whopping $168 billion, plays behind the scenes, helping make space a battlefield for signals, not soldiers.

Steady, profitable, and sneakily important, RTX is the stealth bomber of space stocks.

🪐 Other Orbit-Worthy Notables

Outside of the headliners, there’s a growing constellation of companies playing critical roles in space commerce:

Redwire NYSE:RDW : In-space manufacturing and tech solutions.

Blacksky Technology NYSE:BKSY : Real-time satellite imagery and analytics.

Virgin Galactic NYSE:SPCE : Richard Branson’s waning dream of space tourism, working to make suborbital flights a regular experience (careful, though, the stock is down 99.9% from peak).

☄️ Your Portfolio Doesn't Have to Stay on Earth

Space is no longer just a billionaire’s playground or a sci-fi dream. It's an investable theme — one that covers exploration, infrastructure, defense, data, and connectivity.

Sure, the sector is volatile. There will be delays, explosions (hopefully unmanned), stock swings, and moments where it all seems like an expensive science experiment. But there’s also real innovation, massive contracts, and a trillion-dollar economy forming right above our heads.

The thing is, while the biggest names in tech make the headlines and get daily coverage , you won’t see those space companies featured on the front page of big financial journals or covered in the weekly take of your financial podcast.

Traders who are serious about catching the big moves before they blast off should keep one tool close: the earnings calendar . These companies’ quarterly reports highlight progress, revenue, profit or loss figures, and present forward-looking guidance to act as a compass to traders and investors.

The economics of space isn’t just exciting because it’s shiny and futuristic — it’s exciting because the groundwork is being laid quietly, deal by deal, launch by launch. And the traders who are paying attention before the crowd shows up? They’re the ones best positioned for lift-off.

Your turn : Are you already investing in the space economy? Did we miss any names in there? Tell us — what’s your favorite way to reach for the stars? ✨🚀🌔

Breaking: Intuitive Machines ($LUNR) Up 2% In Mondays Premarket The shares of Intuitive Machines, Inc. (NASDAQ: NASDAQ:LUNR ) are up 2.35% in Monday's premarket session. A company that designs, manufactures, and operates space products and services in the United States.

Its space systems and space infrastructure enable scientific and human exploration and utilization of lunar resources to support sustainable human presence on the moon. The company offers lunar access services, such µNova, lunar surface rover services, fixed lunar surface services, lunar orbit delivery services, rideshare delivery services to lunar orbit, as well as content sales and marketing sponsorships.

Technical Outlook

As of the time of writing, shares of Intuitive Machines, Inc. (NASDAQ: NASDAQ:LUNR ) are up 3% in premarket session. Trading in tandem with the 1-month low pivot albeit close to the support point, NASDAQ:LUNR is gaining momentum with a break above the 38.2% Fibonacci retracement point set to be the catalyst to spark a bullish renaissance for NASDAQ:LUNR shares.

Though the Relative Strength Index (RSI) is oversold at 30, NASDAQ:LUNR is looking poised to break the psychological 38.2% Fib level. Intuitive Machines, Inc. earnings is coming up Tuesday, May 13, 2025, before market open.

Analyst Forecast

According to 6 analysts, the average rating for LUNR stock is "Strong Buy." The 12-month stock price forecast is $15.5, which is an increase of 118.62% from the latest price.

UPDATE: Rocket Lab RecoveryMy previous prediction failed hard due to intense political news pressure. Now we look forward at a possible recovery. I want to say a Cup is forming and will guide the price to at least $22 and then hopefully $24. Watch for a retest doing the Handle portion later on.

Can Satellites Redefine Military Power?The strategic chessboard of military technology is undergoing a profound transformation, where Lockheed Martin plays a pivotal role with its advancements in satellite communication systems. The company has recently marked a significant milestone with the successful Early Design Review (EDR) of the MUOS Service Life Extension program, aimed at enhancing secure military communications. This leap forward is not just about maintaining current capabilities but about reimagining how military power can be projected and managed through space.

Lockheed Martin's collaboration with SEAKR Engineering introduces a groundbreaking feature: a reprogrammable payload processor for satellites, which could revolutionize operational flexibility in space. This technology allows for in-orbit adjustments, ensuring satellites can evolve with changing mission requirements without the need for costly replacements. This innovation challenges us to consider the future of warfare, where adaptability and real-time changes could dictate the outcome of conflicts, far beyond the traditional battlefield.

The implications of such technological advancements extend beyond military strategy; they invite a broader conversation about the role of private-sector innovation in national defense. With commercial giants like Starlink reshaping satellite communication, the military must now decide whether to continue investing in proprietary technologies or integrate commercial solutions. This dilemma poses a fascinating question: In an era where technology evolves at breakneck speed, how will traditional military assets adapt to maintain relevance and superiority?

Eternal PainWill Virgin Galactic ever provide share holders with anything but pain?

The board is no help as they continue to issue more shares. However; there is a potential bright future.

Currently the equity value of the company is lower than the liquidation value of the firm. The enormous cash burn is slowing as most of the capex necessary for flights is ready to go. Given their booking backlog, once they start a solid rhythm a lot of cash is going to be generated.

Look at their most recent investor presentation. With conservative estimates when (if) regular flights begin one spaceport will generate $500m per annum in EBIT [ ] With profits and any sort of multiple on earnings the future could be galactic.

My hopium induced reason for owning this since $5.90 is one day in the next 3-5 years this could be a legitimate 100+ bagger. Space is the ultimate growth arena and with SpaceX focused on mars and industrial matters, Blue Origin no where to be found, the moat is large and the industry is wide open.

Can AAL do it?AAL attempted to break outside this channel last week, but price failed to hold above it and now is coming back down inside the trendline.

If price manages to go back above it with volume, this has great potential.

However, nothing to do until we see price pushing above it again.

Could BA be a wrinkle in the market?BA seems to be facing challenges. However, advancements in technology, along with opportunities in space and defense spending, present a gap that could benefit the company. While I don't have a specific time horizon, I see an opportunity to profit by going against the grain. It's a difficult path, but the potential is there.

PL w/ two potential daily gap fillsNeeds a daily close above $2.65 and can easily fill the first small gap into the low $3s and potentially make a bigger move up into the high EUROTLX:4S

MNTS short cover rally preparing to resumesell cycle appears to have been completed. short vol ratio data suggesting we will resume higher soon.

expecting recovery of 2.10 level by q1 2025, at which point the first portion of profits will be secured.. the rest would be held speculatively to 5$-10$ ranges.

lots of bullish macro-economic narrative developments as well to fuel the rally higher.