AUD/USD – Bullish Reversal from Demand Zone | 2H Chart Analysis Busy: 🔹 AUD/USD – Bullish Reversal from Demand Zone | 2H Chart Analysis 🔹

Price has respected a key demand zone with support from the Ichimoku cloud.

Bullish price action suggests a potential breakout & retest setup targeting 0.6580 and 0.6615.

- Entry Zone: 0.6530 – 0.6540

- Stop Loss: 0.6490

- TP1: 0.6580

- TP2: 0.6615

- Risk:Reward: 1:2 or better

📊 If the price confirms breakout above 0.6550 with a retest, this setup can play out cleanly.

#AUDUSD #Ichimoku #ForexAnalysis #TradingView #BreakoutSetup

Busy: AUD/USD – Bullish Reversal from Demand Zone | 2H Chart Analysis

Technology

BROADCOM 6-year Channel Up in need of a correction.Broadcom Inc. (AVGO) has been trading within a 6-year Channel Up since the start of the COVID crash with the price is currently on its top (Higher Highs trend-line).

Our point of interest currently is the 1W RSI Bearish Divergence, being on Lower Highs since September against the price's Higher Highs. This kind of Bearish Divergence that high inside such a long-term pattern is an indication of a potential trend reversal.

The last correction (January - March 2025) pulled back all the way to the 1W MA100 (green trend-line) and the one before (January - October 2022) to the 1W MA200 (orange trend-line). The former was more aggressive (-44.72% against -38.65%) and faster. Both reached the bottom of the Channel Up.

As a result, even a -38.65% correction from the current levels would come very close to the bottom of the pattern by Q3 2026, approaching also the 1W MA200, which fulfils most prior pull-back conditions of the Channel Up.

Given this data, our long-term Target on Broadcom from now on is $240. The most optimal buy signal for our next long-term buy will be when the 1W RSI hits its 6-year Support Zone, which happened both on the March 2025 and October 2022 bottoms.

---

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

---

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

META entering Bear Cycle territory.Meta Platforms (META) has been on a steady decline since its August All Time High (ATH) that is lately accelerating. The reason the breaking below its 1W MA50 (blue trend-line) last week for the first time since April 2025. That was the time that the market formed the bottom of the Tariff War Crisis.

The key characteristic here (and most worrisome) is the Huge Bearish Divergence of the 1W RSI (Lower Highs) against the price's Higher Highs since February 2024. This indicates a loss of strength for the bullish trend and potential reversal.

The same kind of RSI Bearish Divergence was seen in 2017 - 2018, leading to the eventual July 2018 market Top and strong multi-month correction to the 0.236 Fibonacci retracement level that found Support exactly on the 1W MA250 (red trend-line).

Just like then, the stock price has reached now the top of its historic Channel Up, the pattern that has been trading within since its IPO and only broke once marginally at the bottom of the 2022 Inflation Crisis.

As a result, given the strong similarities between the two fractals, META may be entering a Bear Cycle (since the 1W MA50 break) that could last for about a year. Our 0.236 Fibonacci Target is $480.

---

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

---

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

ASTS 4H: space internet or orbital dream?AST SpaceMobile (ASTS) is consolidating above the $61–69 zone, right near the 0.618 Fibonacci level of its last major rally. On the 4H chart, momentum shows early reversal signs: falling volume on pullbacks, stochastic turning up, and buyers defending local lows. The bullish setup holds as long as price stays above $61, with upside targets at $100 and $135 where the extension projection aligns.

Fundamentally , as of November 2025, ASTS stands out as one of the most promising yet capital-intensive players in the satellite telecom industry. The company completed deployment of its BlueWalker test constellation and is preparing for commercial rollout of direct-to-cell satellite connectivity. Successful phone-to-satellite calls using standard smartphones - validated with AT&T and Vodafone - mark a true technological milestone, positioning ASTS as a potential first-mover in global space-based mobile internet.

Revenue for the first nine months of 2025 reached roughly $55M, almost double last year’s level, but operating losses still exceed $300M due to high manufacturing and launch costs. The company holds about $180M in cash versus ~$260M in debt, continuing to rely on strategic partnerships and funding programs to maintain liquidity. The key upcoming catalyst is the commercial network activation in 2026 in cooperation with AT&T, Vodafone, and Rakuten, which could dramatically change valuation if successful.

With investor attention shifting back to space communications, competition with Starlink and Lynk Global is heating up, but ASTS’s advantage lies in using standard smartphones without extra hardware. Risks remain - high capital needs, launch delays, and dependency on partner timelines - yet the reward potential is extraordinary if execution holds.

Tactically, staying above $61 keeps the bullish structure alive with $100 and $135 as primary targets. A breakdown below $60 would negate the setup.

They’ve already connected phones to space - now let’s see if they can connect revenue to profit.

GOOGLE Bull Cycle running out of steam. Be ready to sell.It's been exactly 2 months (September 05, see chart below) when we last had a look at Google (GOOG) giving a strong break-out Buy Signal that methodically hit our $275 Target:

This time we look at the stock from a much longer term perspective on the 1W time-frame, where it is approaching the top (Higher Highs trend-line) of the Channel Up that started on the COVID crash (March 2020).

This is a major Sell Alert as the 1W RSI is also printing a Double Top formation similar to the November 15 2021 Top. Given that +125% rallies have been the most common long-term sequences of this pattern, we believe that any price above $300 is a major Sell for Google.

The strongest long-term Support and Target of correction sequences/ Bearish Legs has been the 1W MA200 (orange trend-line) and this is our Target for 2026. We estimate that a potential contact with the 1W MA200 can be made at around $180 (also marginally above the 0.5 Fibonacci level from the bottom of the previous correction). A contact with the 1W MA200 will be our next long-term Buy on Google.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

AMAZON flashing a massive 5-year Sell Signal.More than 5 months ago (May 28, see chart below), we gave a strong buy signal on Amazon Inc. (AMZN), which last Friday hit our $255 Target:

This time we come across a massive Sell Signal on the 1W time-frame as the price hit (and is so far being rejected on) the 5-year Higher Highs trend-line that started back on the August 31 2020 Top.

We can see that during that period of time, Amazon had started a Triple Top formation that eventually led to the final rejection and the start of the 2022 Bear Cycle. Until we can talk about such a correction, we can expect at least a pull-back to its 1W MA50 (blue trend-line) as all of those 2020/21 rejections did. As a result, our medium-term Target on Amazon is $220.

Notice also the similarities between the 1W RSI sequences between the two fractals (2020/21 and 2024/25), both forming Lower Highs patterns.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Is IBM Building an Unbreakable Cryptographic Empire?IBM has positioned itself at the strategic intersection of quantum computing and national security, leveraging its dominance in post-quantum cryptography to create a compelling investment thesis. The company led the development of two of the three NIST-standardized post-quantum cryptographic algorithms (ML-KEM and ML-DSA), effectively becoming the architect of global quantum-resistant security. With government mandates like NSM-10 requiring federal systems to migrate by the early 2030s, and the looming threat of "harvest now, decrypt later" attacks, IBM has transformed geopolitical urgency into a guaranteed, high-margin revenue stream. The company's quantum division has already generated nearly $1 billion in cumulative revenue since 2017—more than tenfold that of specialized quantum startups—demonstrating that quantum is a profitable business segment today, not merely an R&D cost center.

IBM's intellectual property moat further reinforces its competitive advantage. The company holds over 2,500 quantum-related patents globally, substantially outpacing Google's approximately 1,500, and secured 191 quantum patents in 2024 alone. This IP dominance ensures future licensing revenue as competitors inevitably require access to foundational quantum technologies. On the hardware front, IBM maintains an aggressive roadmap with clear milestones: the 1,121-qubit Condor processor demonstrated manufacturing scale in 2023, while researchers recently achieved a breakthrough by entangling 120 qubits in a stable "cat state." The company targets deployment of Starling, a fault-tolerant system capable of running 100 million quantum gates on 200 logical qubits, by 2029.

Financial performance validates IBM's strategic pivot. Q3 2025 results showed revenue of $16.33 billion (up 7% year-over-year) with EPS of $2.65, beating forecasts, while adjusted EBITDA margins expanded by 290 basis points. The company generated a record $7.2 billion in year-to-date free cash flow, confirming its successful transition toward high-margin software and consulting services. The strategic partnership with AMD to develop quantum-centric supercomputing architectures further positions IBM to deliver integrated solutions at exascale for government and defense clients. Analysts project IBM's forward P/E ratio may converge with peers like Nvidia and Microsoft by 2026, implying potential share price appreciation to $338-$362, representing a unique dual thesis of proven profitability today combined with validated high-growth quantum optionality tomorrow.

DDOG: interesting macro potential Interesting large multi-year VCP formation. Earnings are on Nov 6. While there’s still a chance that the correction from the June highs isn’t fully complete and that price is currently in a higher-degree bounce (running flat correction), I’ll be on the lookout for a potential (gap-up) earnings breakout.

If such a move occurs—especially if supported by a strong and positive catalyst—I’ll be watching for a delayed-reaction setup for a possible entry.

Chart:

Macro view:

Bullish potential detected for QOREntry conditions:

(i) breach of the upper confines of the Darvas box formation for ASX:QOR

- i.e.: above high of $0.705 of 14th August (most conservative entry), and

(ii) swing up of indicators such as DMI/RSI.

Stop loss for the trade (based upon the Darvas box formation) would be:

(i) below the support level from the low of 5th September (i.e.: below $0.565).

AMD Is it approaching a multi-year top and turning into a Sell ?Almost 8 months ago (March 07, see chart below) we made a bold call (for the time) on Advanced Micro Devices (AMD), expecting it to bottom on its 1M MA100 (red trend-line) and then rebound, targeting $320:

Well the Bullish Leg of its 6-year Channel Up had been even more aggressive than we expected and is already approaching its top (Higher Highs trend-line), much earlier than we expected.

This is technically the right time to book the amazing +240% profits from the April 07 bottom, as the 1W RSI just hit its 6-year Resistance, which has marked the Channel's two Tops.

Even though the Bullish Leg can technically extend as high as +287% on the 1.236 Fibonacci extension (like the previous did), the focus of a long-term investor should now be to buy (much) lower, preferably as close to the 1M MA100 as possible.

The last two Higher Lows of the Channel Up have been priced just above the 0.786 Fibonacci retracement level, so our fair long-term Target is currently at $110.00.

So do you also think AMD is approaching the end of the (long-term) road and is gradually turning into a Sell?

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

PALANTIR sitting on a Buy Zone. Target $220.Palantir (PLTR) has been trading within a Channel Up since early May and is currently consolidating on its bottom (Higher Lows trend-line). while holding he 1D MA50 (red trend-line). The 4H MA50 (blue trend-line) - 1D MA50 range has been technically the most optimal buy zone of this pattern.

With the 4H RSI exhibiting a Bull Flag similar to May - June, we expect the stock to aim for at least its 2.618 Fibonacci extension at $220.00. If broken, it may extend for an end-of-year rally to $255.00 completing a +80% Bullish Leg similar to the Channel's first.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Tech & Rates: The Unstoppable Force Driving USD/JPY SkywardThe USD/JPY exchange rate has exhibited a clear upward trend, recently touching a one-week high before a slight pull-back to around 151.74. This sustained yen weakness reflects a convergence of factors across global finance, domestic Japanese policy, and international relations. Traders must analyze these multi-faceted pressures to accurately forecast future movements.

Domestic Japanese Fiscal Expansion

Japan's new Prime Minister, Sanae Takaichi, is preparing an aggressive economic stimulus package likely exceeding last year's $13.9$ trillion yen ($92.19$ billion). This expansionary fiscal policy aims to counter rising inflation and support household incomes. Markets anticipated this policy shift, contributing to the yen's $2.6\%$ decline this month, its biggest monthly drop since July. A combination of significant fiscal spending and a challenging relationship with the central bank typically weighs heavily on a currency.

Geopolitical Instability and Safe Havens

Global political risk typically favors the U.S. dollar, cementing its position as the world's primary reserve currency. The ongoing $\mathbf{U.S.}$ $\mathbf{government}$ $\mathbf{shutdown}$, now into its third week, injects domestic uncertainty. This standoff complicates the Fed’s data-driven decision-making, potentially reinforcing expectations for rate cuts, which can weaken the dollar. Despite this, the dollar index (DXY) remains resilient at $98.84$. A brief drop in gold prices recently triggered market volatility and a rebalancing of safe-haven assets, briefly allowing the yen to climb. Yet, the persistent US political gridlock maintains a background risk premium that supports the dollar as the ultimate haven.

Geostrategy and Technology Competition

Geostrategic competition, especially involving China, supports the USD through capital flow redirection. Diversification and resilience strategies in global supply chains lead to investment shifts toward Southeast Asia and other strategic areas, often bypassing the yen. Furthermore, the dollar benefits from the High-Tech sector's dominance. High-tech and cyber security, and the associated intellectual property (IP), including patent families, are key drivers of economic growth. A country's strength in technology, quantified by international patents, significantly impacts its currency's global competitiveness and valuation, often bolstering the dollar’s perceived "soft power" relative to the yen. (www.worldscientific.com)

Conclusion and Outlook

The primary drivers of the USD/JPY's ascent are the widening interest rate differential and Japan’s expansionary fiscal outlook. While a short-term correction occurred due to safe-haven rebalancing, the structural forces remain dollar-positive. The US government shutdown presents a risk, but its historical impact on the dollar has typically been modest and short-lived. Traders should expect USD/JPY to test new highs, especially if the new Japanese fiscal policy exacerbates bond market concerns.

TESLA New Bullish Leg to $600 has started.Last time we took a look at Tesla (TSLA) more than a month ago (September 11, see chart below), we gave a massive buy signal that worked out instantly, as we saw the resemblances between the recent Triangle accumulation pattern and that of late 2024, setting a $600 long-term Target:

This time we take a better look at the Channel Up that has emerged. Technically it looks like a Bearish Leg (red Channel Down) has ended and with the 1D MA50 (blue trend-line) holding, a new Bullish Leg has been initiated.

The previous Bullish Leg, which by the way started after a 1D MA100 (green trend-line) hold, rose by +59.26%. This puts the next Higher High technically above our $600 long-term Target.

Notice also how the 1D MACD is about to form a new Bullish Cross, with all previous ones being a strong Buy Signal. At the same time, the 1D RSI found support and bounced on its 5-month Higher Lows trend-line.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

SentinelOne | S | Long at $17.04SentinelOne NYSE:S : a cybersecurity company that uses an autonomous AI-powered platform to performs real-time threat detection, prevention, and remediation across endpoints, cloud, and IoT.

Technical Analysis

Price is consolidating along my historical simple moving average (a regression to the mean). This is after a meteoric rise in 2021 to $78.53 (just after the IPO) and then collapse to $12.43 in 2023. While near-term ups and downs may persist for a bit, usually a price consolidation near the historical simple moving average eventually leads to a major move. The simple moving average band is getting tighter, signaling the potential for a move out of the zone "soon". Given the grow, niche, and need, the future may be bright with this one.

Growth

www.tradingview.com

820% growth expected in earnings per share between 2024 ($0.05) to 2027 ($0.46)

75% revenue growth projected between 2024 ($821 million) to 2027 ($1.4 billion)

Health

Debt-to-equity: 0 (perfection)

Altman's Z Score \ Bankruptcy Risk: 3.3 (extremely low risk)

Quick Ratio: 1.7 (they are able to pay current bills without relying on debt)

Insiders

Warning: Lots of selling and no buying...

openinsider.com

Action

SentinelOne NYSE:S is an extremely healthy company with very high-growth potential. However, the cybersecurity landscape is highly competitive, but NYSE:S is forming a niche with AI-powered tools. While insider selling is a red flag, that is all I can see here besides competition (or the company secretly falling apart behind the scenes). That's the risk we all take as investors. Thus, at $17.04, NYSE:S is in a personal buy zone.

Targets into 2028

$24.00 (+40.8%)

$27.50 (+61.4%)

Can Memory Chips Become Geopolitical Weapons?Micron Technology has executed a strategic transformation from commodity memory producer to critical infrastructure provider, positioning itself at the intersection of AI computing demands and U.S. national security interests. The company's fiscal 2025 performance demonstrates this pivot's success, with data center revenue surging 137% year-over-year to comprise 56% of total sales. Gross margins expanded to 45.7% as the company captured pricing power across both its advanced High-Bandwidth Memory (HBM) portfolio and traditional DRAM products. This dual-margin expansion stems from an unusual market dynamic: capacity reallocation toward specialized AI chips has created artificial supply constraints in legacy memory, driving price increases exceeding 30% in some segments. In contrast, HBM3E capacity through 2026 is already sold out.

Micron's technological leadership centers on power efficiency and manufacturing innovation that translate directly into customer economics. The company's HBM3E solutions deliver bandwidth exceeding 1.2 TB/s while consuming 30% less power than competing 8-high configurations—a critical advantage for hyperscale operators managing electricity costs across massive data center footprints. This efficiency edge is reinforced by scientific advances in manufacturing, particularly the mass production deployment of 1γ DRAM using Extreme Ultraviolet lithography. This node transition delivers over 30% more bits per wafer than previous generations while reducing power consumption by 20%, creating structural cost advantages that competitors must match through heavy R&D investment.

The company's unique position as America's sole HBM manufacturer has transformed it from a component supplier to a strategic national asset. Micron's $200 billion U.S. expansion plan, supported by $6.1 billion in CHIPS Act funding, aims to produce 40% of its DRAM capacity domestically within a decade. This geostrategic positioning grants preferential access to U.S. hyperscalers and government projects requiring secure, domestically sourced components, a competitive moat independent of immediate technological specifications. Combined with a robust intellectual property portfolio covering 3D memory stacking and secure boot architectures, Micron has established multiple defensive layers that transcend typical semiconductor industry cycles, validating an investment thesis for sustained high-margin growth through structural rather than cyclical drivers.

NVIDIA Next stop.. $200For a long time we've been calling for a $200 Target on NVIDIA Corporation (NVDA). That was our main Target for the Bull Cycle that started in November 2022. The stock is very close to this level and the short-term pattern that can get to it is this Channel Up.

Supported by the 1H MA100 (green trend-line), NVIDIA has been posting Bullish Legs of around +10% since the September 05 Low. The confirmation signal for those Legs has been a 1H MACD Bullish Cross.

Given that we formed one yesterday, we expect the price to be on such a Bullish Leg already. The 'weakest' of those sequences has been +9.58%, which if repeated, lands marginally above the $200 psychological level.

Time to hit it?

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

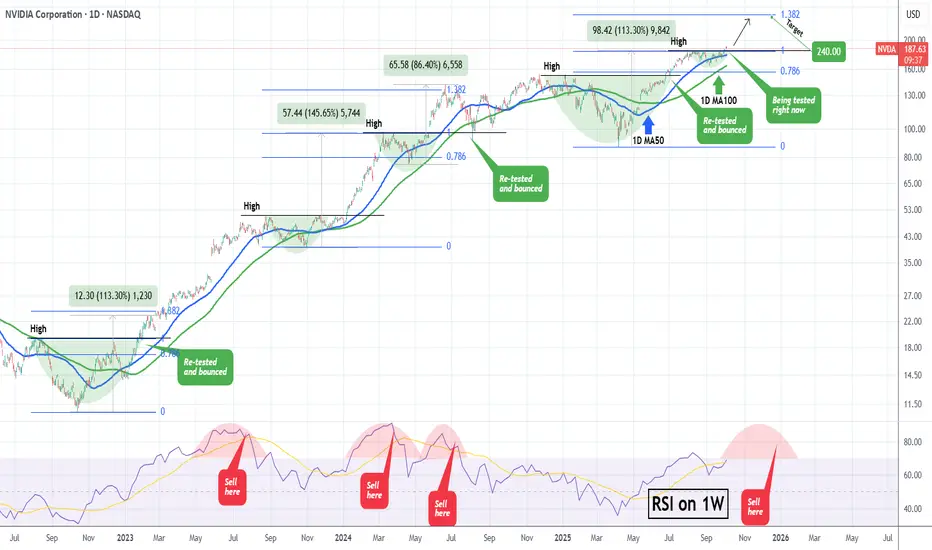

NVIDIA What happens when it retests a Resistance after a break?NVIDIA Corporation (NVDA) has been on a strong rise since the mid-term September 05 Low and this week finally broke above its previous $184 High. During the current Bull Cycle (since the October 2022 bottom), every time the price broke above a previous High and re-tested it as a Support, it started a secondary rally to new Highs.

Technically, as long as the 1D MA100 (green trend-line) holds, we should see at least a 1.382 Fibonacci extension test, similar to the February 2023 and June 2024 Highs. As a result, once the current former High / Resistance level finishes getting re-tested, we expect an end-of-the-year rally to $240.

Additionally, we will keep an eye on the 1W RSI. Typically, once it gets massively overbought above 85.00 and then starts to decline within an Arc peak formation, the time to Sell is after the middle of that Arc.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

SMCI ready to test the top of the Triangle at $63.50.Supermicro Computer Inc. (SMCI) has been trading within a 1-year Ascending Triangle but since August 06 it has been 'trapped' within its 1D MA50 (blue trend-line) and 1D MA200 (orange trend-line).

A closing above the 1D MA50, technically confirms the new Bullish Leg, targeting the top of the Ascending Triangle a $63.50.

If it then closes a full 1W candle above it, we will have a technical bullish break-out, targeting the All Time High (ATH) at $123.00.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Can Silicon Nanowires Redefine America's Battery Future?Amprius Technologies has positioned itself at the convergence of breakthrough materials science and national security imperatives, developing the world's highest energy density lithium-ion batteries through proprietary silicon nanowire technology. The company's batteries deliver up to 450 Wh/kg with targets exceeding 500 Wh/kg - nearly double the performance of conventional graphite-based cells - by solving silicon's historical expansion problems through a unique rooted nanowire architecture that allows internal expansion without structural degradation.

The strategic value extends beyond pure technology metrics. Amprius has secured $50 million in federal funding under Biden's Bipartisan Infrastructure Law and maintains critical defense contracts, including repeat orders totaling over $50 million from unmanned aerial systems manufacturers. This government backing reflects the company's role in domestic supply chain security, as its 100% silicon anode technology reduces reliance on graphite imports while establishing gigawatt-hour manufacturing capacity in Colorado. The Department of Energy's investment essentially validates Amprius as a strategic national asset in the race for advanced battery independence.

Financially, the company has demonstrated rapid acceleration with H1 2025 revenue of $26.4 million already surpassing all of 2024, while achieving a crucial 9% positive gross margin that signals viable unit economics. However, the path to mass market viability remains challenging, with estimated capital expenditures of $120-150 million per GWh of capacity highlighting the complexity of scaling nanowire manufacturing. Wall Street maintains unanimous "Strong Buy" ratings with price targets above $11.67, though recent insider selling following the stock's 1,100% surge raises questions about current valuation versus near-term execution risks.

The company's hybrid manufacturing strategy - leveraging over 1.8 GWh of international contract capacity while building domestic production - reflects a calculated approach to managing capital requirements while capturing immediate high-margin defense and aerospace opportunities. Success hinges on the operational launch of their Colorado facility in H1 2025 and the ability to translate their performance advantages into cost-competitive production for broader electric vehicle markets.

AMAZON Has it found a bottom?Amazon Inc. (AMZN) has been trading within a 4-month Channel Up and is currently pulling back on a Bearish Leg. The 1D MA100 (green trend-line) is just below and last time a similar Channel Up found support on it (May 31 2024), it rebounded for a -0.382 Fibonacci extension top.

As you can see, both patterns are identical, even making their first Higher Lows on their respective 0.618 Fib. Even their 1D RSI fractals are similar and right now we are headed of the 2nd Low (green circle).

As a result, we expect a bullish reversal there, targeting a little under $250 (Fib -0.382 ext).

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

SOXL 1D — With a base like this, the ride’s worth itOn the daily chart of SOXL, since early March, a textbook inverse head and shoulders pattern has formed and is now in its activation phase. The left shoulder sits at $16.67, the head at $7.21, and the right shoulder at $15.11. The symmetry is classic, with volume stabilization and a narrowing range — all the elements are in place.

The key moment was the breakout through the descending daily trendline around $19.00. Price didn’t just pierce the level — it held above it, signaling a phase shift. There was an attempt to break through the 0.5 Fibonacci level at $19.60, which led to a pullback — not on heavy selling, but on decreasing volume. This wasn’t a rejection, it was a pause.

This pullback serves as a retest of the breakout zone and the 20-day moving average. The overall structure remains bullish: price stays above all key EMAs and MAs, RSI climbs past 60, and the candlestick structure is stable. Volume rises during up moves and fades during pullbacks — classic signs of reaccumulation.

The measured target from the pattern is $32.00, calculated from the head-to-neckline height projected from the breakout point. As long as price holds above $18.40, the setup remains intact. A break above $19.60 with confirmation would open the door to acceleration.

This isn’t a momentum play — it’s a setup months in the making. The structure is there, the confirmation is there, and most importantly — the price behavior makes sense. With a base like this, the ride ahead looks worth taking.

META Is this the final rally to $970??Meta Platforms (META) has been rising this month after successfully coming off August's Bull Flag. Technically this is an extension of the very aggressive rebound since the April 07 2025 Trade War bottom. It also took place right above the 1W MA100 (green trend-line).

This is quite similar to the Feb - March 2020 COVID crash, both corrections were -35.39% and -38.52% respectively. At the same time, they were both carried out by Bullish Megaphone patterns with similar 1W RSI sequences.

The Channel Up (green) that followed the COVID crash peaked on its 1.618 Fibonacci extension before turning sideways towards the 1W MA50 (blue trend-line) again.

As a result, given the remarkable symmetry between the two fractals so far, we can expect the current (post Trade War) Channel Up to peak near its 1.618 Fib ext at around $970.00.

-------------------------------------------------------------------------------

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

-------------------------------------------------------------------------------

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

ARM Holdings — reversal pattern signals growth potentialOn the ARM chart an inverted head and shoulders pattern is taking shape with price approaching the neckline around 144–145 and a confirmed breakout above this level could trigger an upward move toward 220 with extended targets at 310–330. In case of a pullback the 128 zone remains key support to preserve the bullish structure. Fundamentally ARM continues to strengthen its role in chip architecture while growing demand in artificial intelligence and mobile technologies drives institutional interest. As long as the pattern holds the bullish scenario stays in play.