Volatility Regimes | GainzAlgo📊 OVERVIEW:

=========

This is a comprehensive ATR-based trading system designed for professional

traders who need advanced volatility analysis, precise trade management, and

intelligent market regime detection. The indicator combines multiple proven

volatility concepts into one powerful, customizable tool.

⭐ WHY THIS SYSTEM IS UNIQUE AND WORTHY OF PUBLICATION:

====================================================

This is not simply a collection of ATR-based indicators placed together.

It represents a unified volatility analysis framework where each component

is specifically designed to work in concert with the others, creating a

complete trading workflow that cannot be replicated by using multiple

separate indicators.

🔗 SYNERGISTIC INTEGRATION - How Components Work Together:

🧠 1. CONTEXT-AWARE ANALYSIS

The Volatility Regime Detection acts as the "brain" of the system,

classifying market conditions into 4 distinct phases. Every other

component then adapts its behavior based on this regime classification:

- ATR Bands expand/contract with regime changes

- Stop Loss distances automatically adjust (tighter in compression,

wider in high volatility)

- Take Profit targets scale proportionally to current regime

- Signal sensitivity filters itself based on market phase

📐 2. UNIFIED VOLATILITY FOUNDATION

All calculations share a single ATR baseline calculation, ensuring

internal consistency across the entire system. When ATR changes, every

element updates in perfect synchronization:

- Bands recalculate from the same ATR value

- Risk management levels use the same volatility measurement

- Regime classification and signals reference identical data

🛡️ 3. INTEGRATED RISK MANAGEMENT

The system doesn't just show WHERE to enter - it calculates HOW MUCH

to risk:

- Dynamic Stop Loss adapts to current ATR automatically

- Position Size Calculator uses the dynamic stop to compute exact quantities

- Take Profit levels scale proportionally, maintaining optimal risk:reward

✅ 4. TWO-STAGE SIGNAL CONFIRMATION

The alert system creates a logical progression:

Step 1: Volatility Breakout → Market energy is building

Step 2: Trend Confirmation → Direction confirmed with volatility support

This prevents false breakouts by requiring both volatility AND direction.

🏦 5. PROFESSIONAL WORKFLOW INTEGRATION

The system mirrors how institutional traders analyze markets:

Phase 1: Assess regime → What's the market doing?

Phase 2: Identify setup → Where's the opportunity?

Phase 3: Calculate risk → What's my exposure?

Phase 4: Set targets → Where do I take profit?

Phase 5: Monitor regime → When do conditions change?

❌ WHY NOT USE SEPARATE INDICATORS?

- Separate ATR Bands: Don't know about regime changes, remain static

- Separate Regime Indicator: Doesn't automatically adjust stop/targets

- Separate Position Calculator: Doesn't know your actual ATR-based stop

- Manual Integration: Requires constant mental calculation and cross-referencing

🧮 DETAILED CALCULATION METHODOLOGY:

=================================

📏 ATR (AVERAGE TRUE RANGE) CALCULATION:

- True Range = Maximum of:

1. Current High - Current Low

2. Absolute value of (Current High - Previous Close)

3. Absolute value of (Current Low - Previous Close)

- ATR = Simple Moving Average of True Range over specified period (default: 14)

📊 DYNAMIC ATR BANDS:

- Upper Band = Current Close + (ATR × Band Multiplier)

- Lower Band = Current Close - (ATR × Band Multiplier)

- Band 1: 1.0× ATR (closest support/resistance)

- Band 2: 2.0× ATR (intermediate zone)

- Band 3: 3.0× ATR (extended zone)

🌡️ VOLATILITY REGIME CLASSIFICATION:

Step 1: Calculate ATR Baseline

- Baseline ATR = SMA or EMA of ATR over long period (default: 50 bars)

- This represents "normal" volatility for the instrument

Step 2: Calculate ATR Ratio

- ATR Ratio = Current ATR ÷ Baseline ATR

- Example: If current ATR = 70 and baseline = 50, ratio = 1.40

Step 3: Classify Regime Based on Ratio

- COMPRESSION: Ratio < 0.70 (ATR is 30% below normal)

Market consolidating, volatility contracting, energy building

- EXPANSION: Ratio between 1.15 and 1.40 (ATR is 15-40% above normal)

Volatility breaking out, early phase of directional movement

- HIGH VOLATILITY: Ratio > 1.40 (ATR is 40%+ above normal)

Strong sustained trend with high participation

- EXHAUSTION: ATR declining after high volatility period

Requires: Previous high ratio + declining ATR over X bars (default: 5)

Trend maturity, potential reversal or consolidation approaching

🛑 DYNAMIC STOP LOSS CALCULATION:

- For Long Positions: Stop Loss = Entry Price - (ATR × SL Multiplier)

- For Short Positions: Stop Loss = Entry Price + (ATR × SL Multiplier)

- Default Multiplier: 2.0× ATR

- Adjusts automatically: Wider in high volatility, tighter in compression

🎯 TAKE PROFIT LEVELS:

- TP1 = Entry Price ± (ATR × TP1 Multiplier)

- TP2 = Entry Price ± (ATR × TP2 Multiplier)

- TP3 = Entry Price ± (ATR × TP3 Multiplier)

- Direction (+ or -) depends on trade direction

📦 POSITION SIZE CALCULATION:

Formula: Position Size = Account Risk Amount ÷ Stop Loss Distance

Step-by-step:

1. Risk Amount = Account Size × (Risk Percentage ÷ 100)

2. Stop Distance = |Entry Price - Stop Loss Price|

3. Position Size = Risk Amount ÷ Stop Distance

📈 ATR PERCENTILE RANKING:

- >80% = Extremely high volatility

- 20-80% = Normal volatility range

- <20% = Extremely low volatility

🌀 VOLATILITY CONTRACTION PATTERN:

Detects extended low-volatility periods indicating imminent breakout.

🧭 TREND DETECTION SIGNALS:

Bullish: Price > MA AND Current ATR > ATR MA

Bearish: Price < MA AND Current ATR > ATR MA

⚡ VOLATILITY BREAKOUT SIGNALS:

Triggered when ATR exceeds its moving average by a defined threshold.

🧩 CORE FEATURES:

==============

1. ATR BANDS (Dynamic Support/Resistance)

2. VOLATILITY REGIME DETECTION

3. DYNAMIC STOP LOSS SYSTEM

4. MULTIPLE TAKE PROFIT LEVELS

5. SUPPORT & RESISTANCE LEVELS

6. RISK MANAGEMENT CALCULATOR

7. ATR PERCENTILE RANKING

8. VOLATILITY CONTRACTION PATTERN

9. TREND DETECTION SIGNALS

10. VOLATILITY BREAKOUT SIGNALS

⚙️ RECOMMENDED SETTINGS BY TRADING STYLE:

======================================

DAY TRADING • SWING TRADING • POSITION TRADING • SCALPING

📘 HOW TO USE THIS INDICATOR:

==========================

STEP 1: Identify Market Regime

STEP 2: Wait for Entry Signal

STEP 3: Set Stop Loss

STEP 4: Set Take Profits

STEP 5: Position Sizing

STEP 6: Monitor & Manage

🔔 ALERT SYSTEM:

=============

Alerts for volatility breakouts, trend changes, regime transitions,

ATR band crossings, contraction completion, and percentile extremes.

🎨 CUSTOMIZATION:

==============

All visuals, thresholds, multipliers, colors, alerts, and risk parameters

can be fully customized.

⚠️ IMPORTANT DISCLAIMER:

=====================

This indicator is a volatility analysis tool and does NOT provide financial advice.

Past performance does not guarantee future results.

All trading involves substantial risk.

All trading decisions are the sole responsibility of the user.

ATR

ATR Bands (MA Distance)ATR Bands (MA Distance) plots volatility-based bands at a multiple of ATR away from a selected moving average.

Unlike percentage envelopes or standard deviation bands, this indicator measures distance from the moving average using ATR, representing the market’s normal “breathing range” rather than statistical probability.

Key Features

The center line is a selectable moving average (EMA, SMA, RMA/Wilder, or WMA).

Upper and lower bands are calculated as:

Moving Average ± ATR × Multiplier

Band width automatically adapts to changing market volatility.

Designed for consistent use across different markets and timeframes without parameter re-optimization.

Non-repainting: all values are calculated only from confirmed historical bars.

Intended Use

ATR Bands (MA Distance) is best used as a context and preparation tool , not as a direct entry or exit signal.

Typical use cases include:

Identifying areas where price is extended relative to its recent volatility.

Visualizing normal vs. stretched price distance from the moving average.

Supporting range-based analysis or trade preparation when combined with other indicators (e.g., oscillators).

Important Notes / How NOT to Use

This indicator does NOT generate buy or sell signals by itself .

Touching or crossing a band does not imply an automatic reversal.

In strong trending markets, price may stay outside the bands for extended periods.

ATR Bands should not be interpreted as overbought/oversold levels on their own.

This indicator does NOT repaint. Once a bar is closed, its values will not change.

For best results:

Use ATR Bands as a preparation zone, then wait for confirmation from your own entry logic.

Disable or ignore band-based mean-reversion ideas during strong trend conditions.

Concept Summary (Short)

ATR Bands (MA Distance) visualize how far price has moved from its moving average in terms of volatility, without repainting and without relying on percentage deviation or statistical assumptions.

Optional Short Description (Preview)

Volatility-based, non-repainting ATR bands plotted at a distance from a moving average.

Designed for market context and trade preparation — not standalone signals.

Opening Range candle percent of ATRIt takes the opening range of the first candle - 5, 10, 15 or whatever minute - and finds what percent of the ATR that is. So if the opening candle high is 15 and low is 14, its range is 1. If the ATR (daily or whatever you want) is 2, then the opening candle's range is 50% of the ATR.

The percentage is displayed on right in a blue box.

The indicator is used in reversal strategies, since opening candles that eat up a large amount of the daily ATR have a higher probability of reversing.

Indicator made with ChatGPT.

ATR-Normalized VWMA DeviationThis indicator measures how far price deviates from the Volume-Weighted Moving Average ( VWMA ), normalized by market volatility ( ATR ). It identifies significant price reversal points by combining price structure and volatility-adjusted deviation behavior.

The core idea is to use VWMA as a dynamic trend anchor, then measure how far price travels away from it relative to recent volatility . This helps highlight when price has stretched too far and may be due for a reversal or pullback.

How it works:

VWMA deviation is calculated as the difference between price and the VWMA.

That deviation is divided by ATR (Average True Range) to normalize for current volatility.

The script tracks the highest and lowest normalized deviations over the chosen lookback period.

It also tracks price structure (highest/lowest highs/lows) over the same period.

A reversal signal is generated when a historical extreme in deviation aligns with a price structure extreme, and a confirmed reversal candle forms.

You get visual signals and color highlights where these conditions occur.

Settings explained:

Lookback period defines how many bars the script uses to find recent extremes.

ATR length controls how volatility is measured.

VWMA length controls how the volume-weighted moving average is calculated.

Signal filters help refine entries based on price vs deviation behavior.

Display options let you customize how signals and levels appear on the chart.

This indicator is especially useful for spotting potential turning points where price has moved far from VWMA relative to volatility, suggesting possible exhaustion or overextension.

Tips for use:

Combine with broader trend context (higher timeframe support/resistance).

Use with risk management rules (position sizing, stops) — signals are guides, not guaranteed entries.

Adjust lookback and ATR settings based on your trading timeframe and asset volatility.

SVP + candle + Max volume [midst]

SVP + DALY CANDLE + MAX VOLUME

A comprehensive trading indicator that combines Session Volume Profile (SVP), Higher Timeframe (HTF) Candles, and Intrabar Max Volume Price Detection into one powerful tool. Perfect for traders who want to understand price action, volume distribution, and key levels all in one place.

KEY FEATURES

Session Volume Profile

• Real-time volume distribution across price levels for the current session

• Point of Control (POC) - identifies the price with the highest traded volume

• Value Area High (VAH) & Low (VAL) - shows where 70% of the volume occurred (customizable percentage)

• Color-coded volume bars - distinguish between up volume (bullish) and down volume (bearish)

• Value area highlighting - clearly see the most important price zones

Higher Timeframe Candle Display

• Visual daily (or custom timeframe) candle overlaid on your current chart

• OHLC labels - see Open, High, Low, and Close prices clearly marked

• Fully customizable colors - separate colors for bullish/bearish bodies, borders, and wicks

• Adjustable positioning - move the candle and labels to your preferred location

Max Volume Price Detection

• Identifies the exact price level with maximum volume within each bar

• Uses Lower Timeframe (LTF) data for precise volume analysis (Premium+ required)

• Simple mode fallback - works on all TradingView plans

• Previous max volume marker - displays previous bar's max volume as a reference dot

• Real-time calculation - updates as each bar forms

ATR Table

• Dynamic ATR-based stop levels - automatically calculates potential stop-loss levels

• Multiple smoothing methods - RMA, SMA, EMA, WMA

• Customizable multiplier - adjust for your risk tolerance

• Clean table display - shows ATR value, high stop, and low stop

PERFECT FOR

Day traders analyzing intrabar volume distribution

Swing traders wanting HTF context on lower timeframes

Volume profile traders looking for key support/resistance levels

Price action traders seeking high-probability entry zones

HOW TO USE

Volume Profile Analysis

POC often acts as a magnet for price. VAH/VAL are key support/resistance levels. High volume nodes indicate strong price acceptance, while low volume nodes suggest potential breakout zones.

HTF Candle Context

See daily range while trading on 5m-1h charts. Daily open often acts as pivot point. Daily high/low are key levels to watch.

Max Volume Price

Black line shows where most volume traded in each bar. Previous max volume (dot) helps identify institutional activity. Clusters of max volume create strong support/resistance. Can possibly indicate a Wick bounce

ATR Stops

Use ATR-based levels for logical stop placement. Adjust multiplier based on market volatility.

SETTINGS & CUSTOMIZATION

Positioning

Control the global offset to move both candle and profile together. Fine-tune with individual offsets for candle and profile spacing.

Volume Profile

Adjustable number of rows (50-500) for granular or simplified view. Customizable width and placement (left/right). Value Area percentage control. Full color customization for all volume components.

HTF Candle

Any timeframe selection (default: Daily). Full color customization for bull/bear candles. Adjustable candle width. Toggle OHLC labels on/off. Control label distance and line widths.

Max Volume Price

Choose between Simple (all plans) or LTF mode (Premium+). Auto or manual LTF resolution. Custom color and line width. Toggle current and previous markers independently.

TECHNICAL NOTES

Maximum 5000 bars lookback for volume calculations

Works on all timeframes

LTF max volume requires TradingView Premium or higher

Optimized for performance with efficient array operations

For best results, use on liquid instruments with reliable volume data

Most effective on intraday charts (5min-1hour) for day trading and scalping strategies

For Entertainment and information only

Created by midst

Weighted ATRWeighted ATR is a volatility indicator that computes True Range and smooths it using a selectable kernel (native Wilder ATR, SMA, EMA, WMA, VWMA, or HMA). It outputs a single volatility line in price units for risk sizing, stop distances, and regime filtering.

SMA MAD Trend [Alpha Extract]A sophisticated trend identification system that combines Simple Moving Average with Mean Absolute Deviation methodology to create adaptive Super Trend-style bands with advanced strength filtering and gradient visualization. Utilizing ADX-based trend strength validation and slope analysis for signal quality enhancement, this indicator delivers institutional-grade trend detection with dynamic ATR-based ribbon visualization and comprehensive strength measurement. The system's dual-filter architecture eliminates false signals during weak or choppy market conditions while maintaining sensitivity to genuine trend establishment and reversal events.

🔶 Advanced SMA-MAD Band Construction

Implements innovative Mean Absolute Deviation calculation around Simple Moving Average baseline to create volatility-adaptive bands with ratcheting logic for trend persistence. The system calculates MAD by measuring absolute price deviations from the mean, then applies configurable multipliers to generate upper and lower bands that adjust to changing market conditions while preventing premature band violations.

// Core SMA-MAD Framework

SMA_Value = ta.sma(close, SMA_Length)

Mean = ta.sma(close, MAD_Length)

Abs_Deviation = abs(close - Mean)

MAD_Value = ta.sma(Abs_Deviation, MAD_Length)

// Adaptive Bands

Upper_Band = SMA_Value + MAD_Factor * MAD_Value

Lower_Band = SMA_Value - MAD_Factor * MAD_Value

🔶 Intelligent Dual-Filter System

Features comprehensive trend validation using ADX strength measurement and slope analysis to eliminate low-conviction signals during ranging or consolidating markets. The system calculates normalized slope strength using ATR scaling and combines with ADX threshold analysis, generating filtered trend states that distinguish genuine trends from temporary price fluctuations.

🔶 Dynamic Trend Strength Engine

Implements sophisticated strength calculation combining slope intensity and ADX readings to produce normalized 0-100% strength scores with gradient colour intensity modulation. The system normalizes slope by minimum threshold and ADX by configurable level, multiplying factors to create composite strength measurement that drives visual feedback intensity across all indicator elements.

🔶 Super Trend-Style Direction Logic

Utilizes classic Super Trend methodology adapted for SMA-MAD bands, where trend direction flips occur on opposite band violations with persistent state maintenance. The system tracks previous band levels with ratcheting behaviour that adjusts bands only when price movement or new calculations warrant changes, preventing oscillation during normal volatility.

🔶 ATR-Based Ribbon Visualization

Provides dynamic ribbon overlay using ATR-scaled width around the trend line with opacity modulation based on trend strength for intuitive conviction assessment. The system creates upper and lower ribbon bounds at configurable ATR multiples, filling the channel with gradient-adjusted transparency that increases during strong trends and fades during weak conditions.

🔶 Multi-Dimensional Visual Architecture

Provides complete chart integration through trend line overlay, ATR ribbon fills, candle colouring, background glow, and transition signal labels with configurable visibility toggles. The system enables traders to customize display density from minimal (trend line only) to comprehensive (all visual elements) while maintaining consistent colour scheme and strength-based intensity across components.

🔶 Slope Strength Validation

Calculates ATR-normalized slope over configurable lookback periods to measure trend line momentum and filter sideways price action. The system compares absolute slope against minimum threshold requirements, preventing trend signals when price movement relative to the trend line lacks sufficient directional conviction regardless of band position.

🔶 Signal Generation Framework

Generates trend change signals when filtered direction state transitions from bearish to bullish or vice versa, with label placement and alert integration. The system implements state persistence that maintains previous trend until both ADX and slope filters confirm directional change, reducing whipsaw signals while capturing genuine reversals with minimal lag.

🔶 Performance Optimization Framework

Utilizes efficient calculation methods with optimized variable management and configurable parameters for balance between responsiveness and stability. The system includes intelligent state tracking with NA handling for initial bars and smooth gradient calculations that maintain performance across extended historical periods and real-time updates.

This indicator delivers sophisticated trend identification through Mean Absolute Deviation methodology combined with dual-strength filtering for superior signal quality. Unlike traditional Super Trend indicators that rely solely on ATR bands, the SMA-MAD approach uses statistical deviation measurement while incorporating ADX strength and slope validation to eliminate false signals during choppy conditions. The system's gradient-based visual feedback, ATR ribbon visualization, comprehensive dashboard, and multi-dimensional filtering make it essential for traders seeking reliable trend-following approaches with clear conviction measurement across cryptocurrency, forex, and equity markets. The combination of adaptive bands, strength-based transparency, and intelligent filtering creates an institutional-grade trend system suitable for systematic trading strategies.

Volatility State Index [Interakktive]The Volatility State Index (VSI) classifies market volatility into three behavioral states: Expansion, Decay, and Transition. It answers one question visually: Is volatility supporting price movement, withdrawing, or unstable?

Unlike traditional volatility indicators that show levels or bands, VSI diagnoses the current volatility regime so traders can adapt their approach accordingly.

█ WHAT IT DOES

• Classifies volatility into three states: Expansion (teal), Decay (grey), Transition (amber)

• Measures volatility momentum as a percentage rate-of-change

• Applies stability filtering to detect unstable/choppy conditions

• Uses persistence logic to prevent state flickering

• Exports state data for use in alerts and strategies

█ WHAT IT DOES NOT DO

• NO buy/sell signals

• NO entry/exit recommendations

• NO alerts (v1 is diagnostic only)

• NO performance claims

This is a volatility diagnostic tool, not a trading system.

█ HOW IT WORKS

The VSI processes volatility through a five-stage pipeline:

STAGE 1 — Base Volatility

Calculates ATR as the foundation for volatility measurement.

STAGE 2 — Smoothing

Applies EMA smoothing to reduce noise in the volatility series.

STAGE 3 — Volatility Momentum

Computes the percentage rate-of-change of smoothed volatility:

Volatility Momentum (%) = ((Current ATR - Previous ATR) / Previous ATR) × 100

Positive values indicate expanding volatility; negative values indicate contracting volatility.

STAGE 4 — Stability Filter

Tracks how frequently volatility momentum changes direction. Frequent sign changes indicate unstable, choppy conditions.

Stability Score = 1 - (Average Flip Rate)

Low stability forces the Transition state regardless of momentum level.

STAGE 5 — State Classification

Combines momentum thresholds and stability to determine the final state:

• Expansion: Momentum ≥ +5% (default threshold)

• Decay: Momentum ≤ -5% (default threshold)

• Transition: Between thresholds OR low stability

A persistence filter requires states to hold for multiple bars before confirming, preventing visual noise.

█ INTERPRETATION

EXPANSION (Teal)

Volatility is increasing in a sustained way. Price moves are becoming larger.

What it suggests:

• Breakouts are more likely to follow through

• Stops may need wider placement

• Trend-following approaches tend to work better

• Mean-reversion weakens

DECAY (Grey)

Volatility is decreasing. Price is compressing into tighter ranges.

What it suggests:

• Breakouts are more likely to fail

• Ranges tend to hold

• Trend-following underperforms

• Mean-reversion strengthens

TRANSITION (Amber)

Volatility behavior is unclear or unstable. This is NOT neutral — it is uncertainty.

What it suggests:

• Mixed signals — one bar huge, next bar dead

• Higher whipsaw risk

• Reduced conviction in either direction

• Consider waiting for clarity

The key insight: Amber is a warning, not a middle ground. It appears when volatility cannot decide what it wants to do.

█ VISUAL DESIGN

The indicator uses a state-first histogram design:

• Histogram height shows volatility momentum percentage

• Histogram color shows the classified state

• Zero line provides visual anchor

• Optional momentum line for confirmation

• Optional background tint (default OFF for clean charts)

The visual hierarchy prioritizes instant state recognition. A trader should understand the volatility environment in under one second without reading numbers.

█ INPUTS

Core Settings

• ATR Length: Base volatility measurement period (default: 14)

• Smoothing Length: EMA smoothing applied to ATR (default: 10)

• Momentum Length: Rate-of-change lookback (default: 10)

State Classification

• Expansion Threshold (%): Momentum above this = Expansion (default: 5.0)

• Decay Threshold (%): Momentum below this = Decay (default: -5.0)

• Persistence Bars: Bars required to confirm state change (default: 3)

• Stability Lookback: Window for stability calculation (default: 20)

• Stability Threshold: Below this = forced Transition (default: 0.5)

Visual Settings

• Show State Histogram: Toggle main display (default: ON)

• Show Momentum Line: Thin confirmation line (default: OFF)

• Show Zero Line: Baseline reference (default: ON)

• Show Background Tint: Subtle state coloring (default: OFF)

█ DATA WINDOW EXPORTS

When enabled, the following values are exported:

• ATR (Raw)

• ATR (Smoothed)

• Volatility Momentum (%)

• Stability Score (0-1)

• State (-1/0/1): Decay = -1, Transition = 0, Expansion = 1

• Is Expansion (0/1)

• Is Decay (0/1)

• Is Transition (0/1)

These exports allow VSI to be used as a filter in Pine Script strategies or alert conditions.

█ ORIGINALITY

While ATR and volatility indicators are common, VSI is original because it:

1. Classifies volatility into behavioral states rather than showing raw levels

2. Applies momentum analysis to volatility itself (rate-of-change of ATR)

3. Uses stability filtering to detect genuinely unstable conditions

4. Implements persistence logic to prevent state flickering

5. Provides a state-first visual design optimized for instant recognition

VSI is state-first: it classifies volatility regimes (Expansion/Decay/Transition) rather than plotting volatility level alone, using momentum and stability to reduce false regime reads.

This is not a modified ATR or Bollinger Band — it is a volatility regime classifier.

█ SUITABLE MARKETS

Works on: Stocks, Futures, Forex, Crypto

Timeframes: All timeframes — state classification adapts accordingly

Best on: Instruments with consistent volatility patterns

█ RELATED

• Market Efficiency Ratio — measures price path efficiency

• Effort-Result Divergence — compares volume effort to price result

█ DISCLAIMER

This indicator is for educational purposes only. It does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own analysis before making trading decisions.

Session ATR Progression Tracker📊 Session ATR Progression Tracker - SIYL Regression Trading Tool

Track how much of your instrument's 7-day Average True Range (ATR) has been covered during the current trading session. This indicator is specifically designed for regression traders who follow the "Stay In Your Lane" (SIYL) methodology, helping you identify when the probability of mean reversion significantly increases. If you are interested in more on that check out Rod Casselli and tradersdevgroup.com.

🎯 Key Features:

• Real-time ATR Coverage Percentage - See at a glance what percentage of the 7-day ATR has been covered in the current session

• SIYL-Optimized Thresholds - See at a glance when the instrument has achieved 80% and 100% ATR coverage, the proven thresholds where mean reversion probability increases (customizable)

• Flexible Session Modes:

- Daily: Resets at calendar day change

- Session: Uses exchange-defined trading sessions

- Custom Session: Set your exact session start/end times (perfect for futures traders and international markets)

• Visual Alerts - Color-coded display (gray → orange → red) and optional background highlighting

• Repositionable Display - Choose from 9 screen positions to avoid chart clutter

• Session Markers - Green triangles mark the start of each new session

• Detailed Stats - View current range, ATR value, session high/low, and session status

💡 Why Use This Indicator?

This tool is built around a proven concept: regression trading becomes significantly more effective once a session has achieved at least 80% of its 7-day ATR. At this threshold, the probability of price reverting to mean increases substantially, creating higher-probability trade setups for SIYL practitioners.

Benefits for regression traders:

- Identify optimal entry points when mean reversion probability is highest (≥80% ATR coverage)

- Avoid premature regression entries before adequate range has been established

- Recognize when daily moves have "earned their range" and are ripe for reversal

- Time fade-the-move and counter-trend strategies with statistical backing

- Improve win rates by trading only after proven probability thresholds are met

⚙️ Setup Instructions:

1. Add the indicator to your chart

2. Select your preferred "Reset Mode" (recommend "Custom Session" for futures/international markets)

3. If using Custom Session, enter your session times in 24-hour format (e.g., 0930-1600 for US stocks, 1700-1600 for CME futures)

4. Adjust alert thresholds if desired (default: 80% and 100% - proven SIYL thresholds)

5. Position the display where it's most visible on your chart

📈 Works Across All Markets:

Stocks • Futures • Forex • Indices • Crypto • Commodities

Perfect for regression traders, mean reversion specialists, and SIYL practitioners who want to trade with probability on their side by entering only after the session has "earned its range."

---

Tip: For futures contracts with overnight sessions that span calendar days (like MES, MNQ, MYM), use "Custom Session" mode with your exchange's official session times for accurate tracking.

TRV & nTRV - Trimmed Range VolatilityGrid bots require stable volatility measurement - ATR becomes misleading when gaps and sudden spikes distort the average. TRV (Trimmed Range Volatility) is an advanced version of ATR: it filters outliers at the extremes (highest and lowest ranges) and remains unaffected by gaps. This provides real-time, accurate volatility measurement for grid bot setup.Grid bots require stable volatility measurement - ATR becomes misleading when gaps and sudden spikes distort the average. TRV (Trimmed Range Volatility) is an advanced version of ATR: it filters outliers at the extremes (highest and lowest ranges) and remains unaffected by gaps. This provides real-time, accurate volatility measurement for grid bot setup.

Why We Developed TRV?

When a gap or sudden spike occurs in the morning, this extreme movement affects standard ATR calculations for an extended period. Even if the price moves sideways for the rest of the day, ATR remains elevated. This causes grid bots to operate with unnecessarily wide spacing and execute fewer trades.

TRV Advantages:

✅ Unaffected by Gaps: Opening gaps don't distort the calculation

✅ Extreme Point Elimination: Filters the largest and smallest outlier candles

✅ Real-Time Accuracy: Shows current market volatility

✅ Grid Bot Optimization: Enables tighter and more efficient grid spacing

✅ Comparison Capability: Compare different stocks and timeframes with nTRV

Grid Bot Usage:

The TRV value is used directly to calculate the number of grid lines:

(Resistance - Support) / TRV = Number of Grid Lines

Example:

Resistance: $110

Support: $90

TRV: $2

Grid Count: (110-90)/2 = 10 grid lines

Features:

Two Filtering Modes: Manual (enter number) or Percentage-Based (automatic ratio)

Four Indicators in One: nTRV, TRV, ATR, and nATR all displayed on the same panel

nTRV: Normalized value (percentage-based, for stock comparison)

TRV: Absolute value (currency-based, for grid calculation)

ATR & nATR Included: Standard ATR and nATR for direct comparison with TRV

Comprehensive Analysis: Compare filtered (TRV) vs unfiltered (ATR) volatility side-by-side

Default: 10% top, 10% bottom outlier elimination

Conclusion:

TRV is an advanced version of ATR specifically designed for grid bot traders. By filtering outlier movements, it provides more stable and reliable volatility measurement. The indicator includes both TRV (filtered) and ATR (unfiltered) on the same chart, giving traders a comprehensive view to make informed decisions. This dual-display approach enables more efficient grid strategies and increased trading frequency.

Combined: Net Volume, RSI & ATR# Combined: Net Volume, RSI & ATR Indicator

## Overview

This custom TradingView indicator overlays **Net Volume** and **RSI (Relative Strength Index)** on the same chart panel, with RSI scaled to match the visual range of volume spikes. It also displays **ATR (Average True Range)** values in a table.

## Key Features

### Net Volume

- Calculates buying vs selling pressure by analyzing lower timeframe data

- Displays as a **yellow line** centered around zero

- Automatically selects optimal timeframe or allows manual override

- Shows net buying pressure (positive values) and selling pressure (negative values)

### RSI (Relative Strength Index)

- Traditional 14-period RSI displayed as a **blue line**

- **Overlays directly on the volume chart** - scaled to match volume spike heights

- Includes **70/30 overbought/oversold levels** (shown as dotted red/green lines)

- Adjustable scale factor to fine-tune visual sizing relative to volume

- Optional **smoothing** with multiple moving average types (SMA, EMA, RMA, WMA, VWMA)

- Optional **Bollinger Bands** around RSI smoothing line

- **Divergence detection** - identifies regular bullish/bearish divergences with labels

### ATR (Average True Range)

- Displays current ATR value in a **table at top-right corner**

- Configurable period length (default: 50)

- Multiple smoothing methods: RMA, SMA, EMA, or WMA

- Helps assess current market volatility

## Use Cases

- **Momentum & Volume Confirmation**: See if RSI trends align with net volume flows

- **Divergence Trading**: Automatically spots when price makes new highs/lows but RSI doesn't

- **Volatility Assessment**: Monitor ATR for position sizing and stop-loss placement

- **Overbought/Oversold + Volume**: Identify exhaustion when RSI hits extremes with volume spikes

## Customization

All components can be toggled on/off independently. RSI scale factor allows you to adjust how prominent the RSI line appears relative to volume bars.

IDWM Master StructureExecutive Summary

The IDWM Master Structure is a Multi-Timeframe (MTF) trading tool designed to force discipline by aligning traders with the "Parent" trend. It functions by locking onto the "Completed Auction" of a higher timeframe candle (like a Daily or Weekly bar) and projecting that structure onto your lower timeframe chart. Its primary goal is to define the "Dealing Range"—the hard boundaries where value was previously established—so you don't get lost in the noise of smaller price movements.

1. The Principle of Completed Auctions (Hierarchy)

Most technical indicators curve dynamically with every price tick. This script acts differently because it relies on "Settled Arguments." A closed Daily candle represents a finished battle between buyers and sellers; the High and Low are the historical results of that battle.

To enforce this, the script automatically selects a "Parent" timeframe based on your view:

Scalping (charts below 15 minutes) uses the 4-Hour Auction.

Intraday trading (15 minutes to 4 Hours) uses the Daily Auction.

Swing trading (Daily chart) uses the Weekly Auction.

2. Liquidity Pools & The Sticky Range

The High and Low lines drawn by the indicator are not just support and resistance; they represent Liquidity Pools. In market theory, stop-losses (Sell Stops below Lows, Buy Stops above Highs) accumulate at these edges.

Smart money often pushes price just past these lines to grab this liquidity (a "Stop Hunt") before reversing direction. To account for this, the script uses a "Sticky Range" mechanism. It refuses to redraw the box simply because price touched the line. Instead, it uses an Average True Range (ATR) Buffer. A new structure is only formed if the candle closes decisively outside the range plus this volatility buffer. This ensures you are trading real breakouts, not liquidity sweeps.

3. Internal Range Mechanics (Premium vs. Discount)

Inside the Master Box, the script applies Equilibrium Theory to help with trade location.

The most important internal line is the Equilibrium (EQ), which marks the exact 50% point of the range.

Premium Zone (Above EQ): Price is mathematically "expensive" relative to the recent range. Algorithms generally look to establish Short positions here.

Discount Zone (Below EQ): Price is considered "cheap." Algorithms generally look to establish Long positions here.

It also plots the Master Open, which acts as a "Line in the Sand." If price is currently trading above the Master Open, the higher timeframe candle is Green (Bullish), suggesting longs have a higher probability. If below, the candle is Red (Bearish).

4. Wick Theory (Failed Auctions)

The script places special emphasis on the wicks of the Master Candle because a wick represents a "Failed Auction"—a price level the market tried to explore but ultimately rejected.

The indicator highlights the background of the wick area (from the High to the Body). On a retest, these zones often act as supply or demand blocks because the market remembers the previous failure.

It also calculates the "Consequent Encroachment," which is the 50% midpoint of the wick. The rule of thumb here is that if a candle body can close past 50% of a wick, the rejection is nullified, and price will likely travel to fill the entire wick.

5. Energy Expansion (Breakout Targets)

Market energy transfers from Consolidation (inside the box) to Expansion (the breakout). When the price finally breaks the "Sticky Range" (confirming via the ATR buffer), the script projects where that energy will go.

It uses the height of the previous range to calculate Fibonacci extensions. Specifically, it targets the 1.618 Extension, often called the "Golden Ratio." This is a statistically significant level where expansion moves tend to exhaust themselves and reverse.

6. Safety Protocol: Live Detection

A dashboard monitors the state of the parent candle. If the text turns Magenta with a warning symbol, it means the Higher Timeframe candle is "Live" (still forming).

Trading off a live structure is considered higher risk because the "Auction" isn't finished—the High or Low can still shift. The safest approach is to trade when the dashboard indicates a standard, locked, historical structure.

Hash SupertrendHash Supertrend is a visually enhanced Supertrend-based indicator designed by Hash Capital Research, tuned specifically for crypto trend trading on Solana (SOL) and Bitcoin (BTC). It combines institutional-style color coding, an optional session time filter, and production-ready alerts for systematic and discretionary traders alike.

What This Indicator Is

Hash Supertrend is a trend-following volatility band indicator built on TradingView’s native ta.supertrend() function.

It’s optimized and visually styled for:

High-volatility crypto pairs (especially SOL/USDT, SOL/USD, BTC/USDT, BTC/USD)

Timeframes typically used by crypto traders (from 5m scalping to 4H swing and 1D trend following)

The script is an indicator, not a strategy:

It does not place trades or show backtest results.

It provides clear trend states, flips, and alerts that you can plug into your own execution stack or manual trading.

Key Features

✅ Tuned for Crypto (Solana & Bitcoin)

Parameters are chosen to respond well to the volatility profile of SOL and BTC, reducing noise while still catching strong moves.

✅ Non-repainting Supertrend Core

Uses TradingView’s built-in ta.supertrend — values may move intrabar as the bar forms, but once a bar closes, the historical line and signals do not repaint.

✅ Fluorescent Trend Visualization

Bright green for bullish phases

Bright red for bearish phases

Adaptive color intensity based on user setting

✅ Glow Layer & Trend Zones

Glow effect around the Supertrend line for instant visual recognition

Optional filled zones between price and line for “trend cloud” style visualization

✅ Time Filter (Session Control)

Option to only mark signals during specific hours for those wanting to integrate with webhooks

Designed for traders who avoid certain sessions (e.g., low-liquidity hours)

✅ Signal Dots & Alerts

Tiny green dots for bullish flips

Tiny red dots for bearish flips

Professional, preconfigured alerts for:

Long Entry

Short Entry

Any Trend Change

Filtered signals outside trading hours (for monitoring only)

The core logic is built on:

ATR Length (ATR Length) Default: 16

Lower values (7–10): more sensitive, more signals, more noise

Higher values (12–20): smoother, fewer but stronger trend signals

Factor (Factor) Default: 3.11

Lower values (1.5–2.5): tighter bands, earlier entries, higher whipsaws

Higher values (3.0–4.0+): wider bands, later entries, stronger trend confirmation

The indicator reads direction from ta.supertrend and classifies:

Bullish Trend: direction < 0

Bearish Trend: direction > 0

A trend flip happens when direction changes sign:

longSignal: Supertrend flips from above price to below price (bearish → bullish)

shortSignal: Supertrend flips from below price to above price (bullish → bearish)

Clean Industry DataClean Industry Data – Overview

Clean Industry Data is a utility tool designed to give traders an instant, structured view of key fundamental and volatility metrics directly on the chart. The script displays a compact, customizable information panel containing:

Industry & Sector

Market Cap and Free-Float Market Cap

Free-Float Percentage

Average Daily Rupee Volume

Relative Volume (R.Vol) based on daily volume

% from 10 / 21 / 50 EMAs (calculated on daily closes)

ADR (14-day) with threshold-based indicators

ATR (current timeframe) with colour-coded risk cues

All volume-based statistics are anchored to daily data, ensuring the values remain consistent across all timeframes. The display table supports flexible positioning, custom background/text colours, and adjustable text size.

This script is ideal for traders who want a quick, accurate snapshot of a stock’s liquidity, volatility, and broader classification — without digging through multiple menus or external sources.

Simple Price ChannelSimple Price Channel

This indicator plots a basic volatility-based channel around a moving average.

Features:

Midline using Simple Moving Average (SMA)

Upper & lower bands using ATR or true range

Channel fill for easy trend visualisation

This script is designed for educational and analytical purposes only.

It does not provide signals, alerts, or financial advice.

Position Sizing Calculator (Real-Time) - Futures Edition█ SUMMARY

The following indicator is a Position Sizing Calculator based on Average True Range (ATR), originally developed by market technician J. Welles Wilder Jr., intended for real-time trading.

This script utilizes the user's account size, acceptable risk percentage, and a stop-loss distance based on ATR to dynamically calculate the appropriate position size for each trade in real time.

█ BACKGROUND

Developed for use on the Micro E-mini Nasdaq-100 futures (MNQ), this script provides traders with continuously updated dynamic position sizes. It enables traders to instantly determine the exact number of contracts to use when entering a trade while staying within their acceptable risk tolerance.

This real-time position sizing tool helps traders make well-informed decisions when planning trade entries and calculating maximum stop-loss levels, ultimately enhancing risk management.

█ USER INPUTS

Trading Account Size: Total dollar value of the user's trading account.

Acceptable Risk (%): Maximum percentage of the trading account that the user is willing to risk per trade.

ATR Multiplier for Stop-Loss: Multiplier used to determine the distance of the stop-loss from the current price, based on the ATR value.

ATR Length: The length of the lookback period used to calculate the ATR value.

Show Target Risk Row: Toggle to hide/show the Target Risk Row

SL Levels Display: Option to see Both, Long Only, Short Only, or None of the Stop Loss Level Values.

Contract Point Value ($): Point value per contract. Tooltip highlights common values.

Tick Size: Minimum Price Movement (Default set to 0.25)

Minimum Contracts: Override the Minimum Contracts per trade to a user selected value.

(May Exceed User's Target Risk)

TR-ATR-DATR+MAs shows the Range of selected Candle + 3 Moving Averages

True Range

Avg True Range

Daily Range

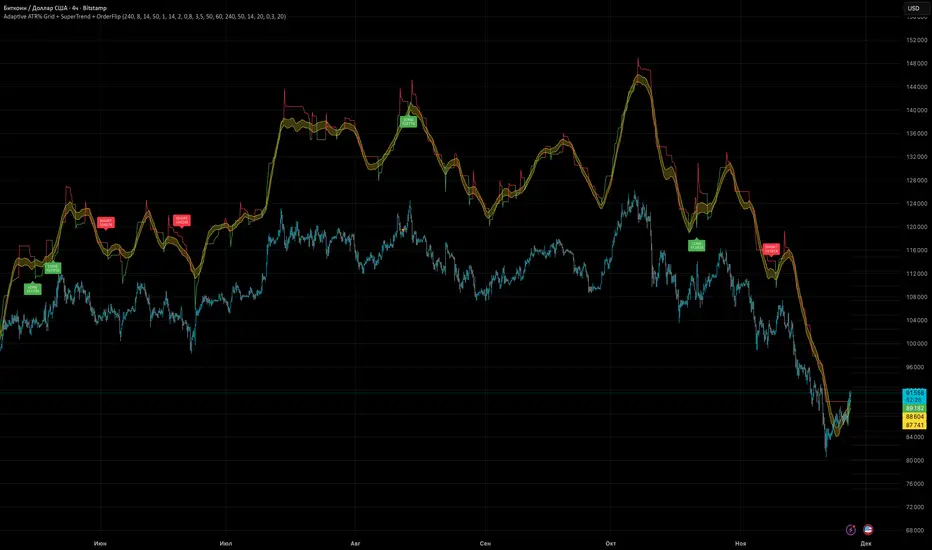

Adaptive ATR% Grid + SuperTrend + OrderFlipDescription:

This indicator combines multiple technical analysis tools to identify key price levels and trading signals:

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

OrderFlip – identifies price reversal points relative to a moving average with ATR-based sensitivity, optionally filtered by OBV and DMI.

MTF Confirmation – multi-timeframe trend verification using EMA to reduce false signals.

Signal Labels – "LONG" and "SHORT" labels appear on the chart with an offset from the price for better visibility.

JSON Alerts – ready-to-use format for automated alerts, including price, SuperTrend direction, Fair Zone, and ATR%.

Features:

Fully compatible with Pine Script v6

Lines and signals are fixed on the chart, do not shift with new bars

Configurable grid, ATR, SuperTrend, and filter parameters

Works with MTF analysis and classic indicators (OBV/DMI)

Usage:

Best used with additional indicators and risk management strategies. ATR% Grid is ideal for both positional trading and intraday setups.

перевод на русский

Описание:

Этот индикатор объединяет несколько методов технического анализа для выявления ключевых уровней цены и сигналов на покупку/продажу:

Сетка ATR% (ATR% Grid) – автоматическое построение уровней поддержки и сопротивления на основе текущей цены и волатильности (ATR). Позволяет видеть потенциальные цели и зоны входа/выхода.

SuperTrend – классический трендовый индикатор с адаптивным множителем ATR, который корректируется на основе средней волатильности.

OrderFlip – определение моментов разворота цены относительно скользящей средней с учетом ATR, с возможностью фильтрации по OBV и DMI.

MTF-подтверждение – проверка направления тренда на нескольких таймфреймах с помощью EMA, чтобы снизить ложные сигналы.

Сигнальные метки – на графике появляются "LONG" и "SHORT" с отступом от цены для наглядности.

JSON Alerts – готовый формат для автоматических уведомлений, включающий цену, направление SuperTrend, Fair Zone и ATR%.

Особенности:

Поддержка Pine Script v6

Линии и сигналы закреплены на графике, не двигаются при обновлении свечей

Настраиваемые параметры сетки, ATR, SuperTrend и фильтров

Совместимость с MTF-анализом и классическими индикаторами OBV/DMI

Рекомендации:

Используйте в сочетании с другими индикаторами и стратегиями управления риском. Сетка ATR% отлично подходит для позиционной торговли и интрадей.

ATR% Grid – automatic plotting of support and resistance levels based on current price and volatility (ATR). Useful for identifying potential targets and entry/exit zones.

SuperTrend – a classic trend indicator with an adaptive ATR multiplier that adjusts based on average volatility.

OTT Volatility [RunRox]📊 OTT Volatility is an indicator developed by the RunRox team to pinpoint the most optimal time to trade across different markets.

OTT stands for Optimal Trade Time Volatility and is designed primarily for markets without a fixed trading session, such as cryptocurrencies that trade 24/7. At the same time, it works equally well on any other market.

🔶 The concept is straightforward. The indicator takes a specified number of historical periods (Samples) and statistically evaluates which hours of the day or which days show the highest volatility for the selected asset.

As a result, it highlights time windows with elevated volatility where traders can focus on searching for trade setups and building positions.

🔶 As the core volatility metric, the indicator uses ATR (Average True Range) to measure intraday volatility. Then it calculates the average ATR value over the last N Samples, creating a statistically stable estimate of typical volatility for the selected asset.

🔶 Statistically, during these highlighted periods the market shows higher-than-average volatility.

This means that in these time windows price is more likely to be subject to stronger moves and potential manipulation, making them attractive for active trade execution and position management.

⚠️ However, historical behavior does not guarantee future results.

These periods should be treated only as zones where volatility has a higher probability of being above normal, not as a promise of movement.

As shown in the screenshot above, the indicator also projects potential future volatility based on historical data. This helps you better plan your trading hours and align your activity with periods where volatility is statistically expected to be higher or lower.

🔶 Current Volatility – as shown in the screenshot above, you can also monitor the real-time volatility of the market without any statistical averaging.

On top of that, you can overlay the current volatility on top of the statistical volatility levels, which makes it easy to see whether the market is now trading in a high- or low-volatility regime relative to its usual behavior.

4 display modes – you can choose any visualization style that fits your trading workflow:

Absolute – displays the raw volatility values.

Relative – shows volatility relative to its typical levels.

Average Centered – centers volatility around its average value.

Trim Low Value – filters out low-volatility noise and highlights only more significant moves.

This indicator helps you define the most effective trading hours on any market by relying on historical volatility statistics.

Use it to quickly see when your market tends to be more active and to structure your trading sessions around those periods.

✅ We hope this tool becomes a useful part of your trading toolkit and helps you improve the quality of your decisions and timing.

Average True Range % infoATR% is a modified version of the classic Average True Range indicator that displays price volatility as a percentage of the instrument's value, rather than in absolute values. This allows you to easily compare the volatility of different assets (e.g., Bitcoin vs Tesla stock) regardless of their price.

Main Features

1. ATR% Chart

The red line shows the average volatility from the last N candles (default 14), expressed as a percentage. For example:

ATR% = 2.5% means that the average daily move is approximately 2.5% of the asset's value

Higher values = greater volatility (higher profit potential, but also greater risk)

Lower values = lower volatility (calmer market)

2. Volatility Trend Analysis

The indicator automatically detects whether volatility is rising, falling, or stable:

Up arrow (↑) - volatility is rising (price becomes more "nervous")

Down arrow (↓) - volatility is falling (market is calming down)

Horizontal arrow (⮆) - volatility is stable (within ±3% of the moving average)

3. Information Table

In the upper right corner of the chart you will see Current ATR% value and Trend arrow with color coding:

- Green = rising volatility

- Red = falling volatility

- Gray = stable volatility

Parameters to Configure

Indicator Length (default: 14) - How many candles back to include in calculations:

Lower values (5-10): more sensitive to sudden changes, reacts faster

Higher values (20-30): more smoothed, shows long-term volatility picture

Trend Length (default: 10) - Period to analyze whether volatility is rising/falling:

Lower values: faster trend change signals

Higher values: more reliable, but slower signals

Sample Interpretations

ATR% Volatility Asset Type/Situation

< 1% Very low Stable blue-chip stocks, calm market

1-3% Low-medium Typical stocks, normal conditions

3-5% Medium-high Volatile stocks, cryptocurrencies at rest

5-10% High Cryptocurrencies, penny stocks

> 10% Extremely high Market panic, crash, pump & dump

Đại Ka 3 ATR BandsĐại Ka 3 ATR Bands – The ultimate single-slot indicator that replaces three separate ATR plots.

Designed specifically for ICT/SMC traders in 2025:

• Light red band (±0.5 ATR) → fake moves, Judas Swing, Turtle Soup zone

• Gray band (±1.0 ATR) → normal price action

• Light green band (±2.0 ATR) → real displacement zone → Silver Bullet, SFT, high-probability entries

How to use:

– Price stuck inside red band → expect reversal/fakeout

– Price breaks and closes outside green band + volume spike → enter aggressively in that direction (85%+ win-rate inside Killzones)

Default ATR(14), subtle fills for instant visual filtering of real vs fake moves.

Perfect companion for Order Blocks, FVG, Breaker Blocks and NY/London Killzones.

Free forever – coded with love by Đại Ka & Vietnamese ICT crew.

Momentum Tide [Alpha Extract]A sophisticated momentum-based trend identification system that measures normalized price deviation from an EMA baseline using ATR scaling and hyperbolic tangent smoothing for precise trend state classification. Utilizing advanced signal processing with configurable neutral bands and slope sensitivity adjustments, this indicator delivers institutional-grade momentum analysis with continuous strength measurement and visual trend confirmation. The system's three-state classification (bullish, bearish, neutral) combined with dynamic color intensity scaling provides comprehensive market momentum assessment across varying volatility conditions.

🔶 Advanced Baseline Deviation Framework

Implements EMA-based baseline calculation with ATR-normalized deviation measurement to create volatility-adjusted momentum signals. The system calculates raw price deviation from the baseline, scales by ATR and slope sensitivity factor, then applies exponential smoothing for stable signal generation with reduced noise and false transitions.

// Core Momentum Calculation

Baseline = ta.ema(close, Baseline_Length)

ATR_Value = ta.atr(ATR_Length)

Raw_Deviation = (close - Baseline) / (ATR_Value * Slope_Scaler)

Signal = ta.ema(Raw_Deviation, Signal_Smoothing)

🔶 Hyperbolic Tangent Normalization Engine

Features sophisticated tanh transformation that clamps raw deviation signals into normalized -1 to +1 range for consistent interpretation across all market conditions. The system applies safe exponential calculations with value capping to prevent overflow while maintaining signal sensitivity, creating bounded momentum readings suitable for systematic threshold analysis.

// Tanh Normalization

Clamped_Signal = tanh(Signal) // Bounded to

Strength = abs(Clamped_Signal) // Momentum intensity

🔶 Three-State Classification System

Implements intelligent trend state determination using configurable neutral band thresholds to reduce whipsaw signals during ranging conditions. The system classifies market as bullish (+1) when momentum exceeds upper neutral band, bearish (-1) below lower neutral band, and neutral (0) within the band, providing clear directional bias with built-in consolidation recognition.

🔶 Dynamic Color Intensity Architecture

Provides advanced visual feedback through momentum strength-based color intensity modulation, where stronger trends display more opaque colors and weaker trends show increased transparency. The system dynamically adjusts color alpha values based on absolute momentum strength, creating intuitive visual representation of trend conviction across baseline, candles, and bars.

🔶 Trend Strength Meter Visualization

Features innovative horizontal gradient meter displaying real-time momentum position across bear-to-bull spectrum with 24-segment resolution. The system creates smooth color transitions from bearish red through neutral gray to bullish green, with arrow indicator showing precise momentum location for instant trend strength assessment without cluttering the price chart.

🔶 Intelligent Flip Detection System

Generates transition markers when trend state changes from neutral/bearish to bullish or neutral/bullish to bearish, with duplicate signal suppression to prevent marker clustering. The system tracks previous signal states and only plots new markers on genuine trend reversals, providing clean entry signal visualization for systematic trading approaches.

snapshot

🔶 Configurable Neutral Band Framework

Implements adjustable neutral zone width using ATR percentage parameters to optimize signal frequency for different trading styles and market conditions. Wider bands reduce flip frequency for position trading while tighter bands increase sensitivity for active trading strategies, enabling customization without code modification.

🔶 Slope Sensitivity Adjustment

Features slope scaler parameter that modulates ATR normalization factor, controlling signal smoothness versus responsiveness trade-off. Higher values create smoother momentum readings with fewer transitions while lower values increase snappiness for faster reaction to price changes, allowing optimization across different volatility regimes and timeframes.

🔶 Comprehensive Visual Integration

Provides multi-dimensional trend visualization through color-coded baseline overlay, momentum-synchronized candle coloring, and bar color modification with configurable display toggles. The system includes optional flip markers and strength meter with position control for complete chart integration without visual overload.

🔶 Performance Optimization Framework

Utilizes efficient calculation methods with optimized table management for strength meter updates and minimal computational overhead for real-time momentum processing. The system includes intelligent state tracking and safe mathematical operations to prevent errors during extreme market conditions while maintaining consistent performance.

🔶 Why Choose Momentum Tide ?

This indicator delivers sophisticated momentum-based trend analysis through normalized deviation measurement and intelligent three-state classification. Unlike traditional momentum oscillators that operate in separate windows, Momentum Tide integrates directly with price action through baseline overlay and candle coloring while providing the analytical depth of bounded momentum measurement. The system's combination of tanh normalization, configurable neutral bands, dynamic color intensity, and innovative strength meter makes it essential for traders seeking adaptive trend-following approaches with clear visual feedback across cryptocurrency, forex, and equity markets. The three-state system naturally filters ranging periods while the momentum strength measurement enables position sizing and confidence assessment for systematic trading strategies.

HTF BIAS FILTER🧭HTF Bias Filter Indicator: 5 in 1 indicator

Technical Overview

The Bias Filter is a comprehensive multi-timeframe tool designed to confirm directional bias using five key indicators before entering a trade. It plots higher-timeframe Moving Averages directly on the chart and provides an immediate status summary via a static dashboard.

The more confluence on the dashboard, the greater the probability of the direction of the trade.

1. 📊 Display Components

A. Plotted Lines

The indicator uses the request.security function to draw Moving Averages from higher timeframes onto your current chart:

1H EMA 21 (Purple): The 21-period Exponential Moving Average calculated on the 1-Hour (60 min) chart. Plotted using a step-line style.

4H EMA 50 (Red): The 50-period Exponential Moving Average calculated on the 4-Hour (240 min) chart. Plotted using a step-line style.

B. Directional Dashboard

A fixed-position summary table is anchored to the bottom-right corner of the chart, providing a quick glance at the current status of all five filters.

2. 🎨 Colour Logic

Each of the five indicators is assigned a colour based on its current directional signal. The more indicators that show the same colour (confluence), the stronger the signal and the higher the likelihood of a high-probability trade.

🟢 Green indicators are signaling UP/BUY (Bullish momentum or trend).

🔴 Red indicators are signaling DOWN/SELL (Bearish momentum or trend).

⚫ Gray indicators are signaling Mixed or flat directions (neutral or undecided).

Note: The dashboard's main header color is determined by a strict confluence logic (All four 4H filters must align for Green/Red), while individual indicator colors follow the simple rules above.

3. 📋 Indicator Breakdown and Logic

The dashboard provides the direction of five different filters.

3.1. Higher-Timeframe (HTF) Trend Indicators

These two signals determine the immediate slope and direction of the primary Moving Averages:

4H EMA 50:

Timeframe: 4-Hour (240 min)

Logic: Compares the current EMA value to the value two bars ago on the 4H chart.

Output: UP ↑, DOWN ↓, or FLAT ⏸

1H EMA 21:

Timeframe: 1-Hour (60 min)

Logic: Compares the current EMA value to the value two bars ago on the 1H chart.

Output: UP ↑, DOWN ↓, or FLAT ⏸

3.2. 4-Hour Confluence Filters

These three indicators provide supplementary confirmation on Volume, Price Position, and Momentum, all calculated on the 4-Hour (240 min) chart:

4H OBV (Smoothed):

Timeframe: 4-Hour (240 min)

Logic: Direction is based on the current value of the 21-bar smoothed On-Balance Volume (OBV) compared to its value nine bars ago.

Output: UP ↑, DOWN ↓, or FLAT ⏸

4H ATR DIR (EMA Proxy):

Timeframe: 4-Hour (240 min)

Logic: Determines the price position by comparing the current Close price against the 4H EMA 50.

Output: BUY 🟢 (Close > EMA 50), SELL 🔴 (Close < EMA 50), or FLAT ⏸️ (Close = EMA 50).

4H RSI (14):

Timeframe: 4-Hour (240 min)

Logic: Momentum check comparing the 14-period Relative Strength Index (RSI) value against the 50 level.

Output: BUY 🟢 (RSI > 50), SELL 🔴 (RSI < 50), or FLAT ⏸️ (RSI = 50).