ATR %Overview

Shows the Average True Range (ATR) as a percentage of a chosen price basis. Useful for a quick, apples-to-apples view of current volatility across symbols and timeframes. The value is displayed in a clean table at the bottom-right of the chart.

What it shows

Basis can be: Close, EMA(len), SMA(len), or VWAP.

Data timeframe can be the Chart timeframe or a Daily aggregation.

Inputs

ATR length (len) – ATR lookback.

Percent basis – Close / EMA / SMA / VWAP.

Data timeframe – Chart (uses the current chart TF) or Daily (computes ATR and basis from daily data).

Decimals – number of decimal places to display.

Text / Background / Frame colors – customize the table appearance.

Notes

In Daily mode, ATR and basis are taken from daily data and update on daily close.

VWAP is available only in Chart mode (Daily + VWAP will show n/a by design).

The script overlays the chart but does not plot lines—only a compact info box.

Use cases

Compare volatility across coins/stocks quickly using ATR% instead of raw ATR.

Switch basis to match your style (e.g., EMA for trend-aware scaling, VWAP for intraday context).

Set Daily to track higher-timeframe volatility while trading lower TFs.

Disclaimer

For educational purposes only. Not financial advice. Trading involves risk.

Average True Range (ATR)

Deadband Hysteresis Supertrend [BackQuant]Deadband Hysteresis Supertrend

A two-stage trend tool that first filters price with a deadband baseline, then runs a Supertrend around that baseline with optional flip hysteresis and ATR-based adverse exits.

What this is

A hybrid of two ideas:

Deadband Hysteresis Baseline that only advances when price pulls far enough from the baseline to matter. This suppresses micro noise and gives you a stable centerline.

Supertrend bands wrapped around that baseline instead of raw price. Flips are further gated by an extra margin so side changes are more deliberate.

The goal is fewer whipsaws in chop and clearer regime identification during trends.

How it works (high level)

Deadband step — compute a per-bar “deadband” size from one of four modes: ATR, Percent of price, Ticks, or Points. If price deviates from the baseline by more than this amount, move the baseline forward by a fraction of the excess. If not, hold the line.

Centered Supertrend — build upper and lower bands around the baseline using ATR and a user factor. Track the usual trailing logic that tightens a band while price moves in its favor.

Flip hysteresis — require price to exceed the active band by an extra flip offset × ATR before switching sides. This adds stickiness at the boundary.

Adverse exit — once a side is taken, trigger an exit if price moves against the entry by K × ATR .

If you would like to check out the filter by itself:

What it plots

DBHF baseline (optional) as a smooth centerline.

DBHF Supertrend as the active trailing band.

Candle coloring by trend side for quick read.

Signal markers 𝕃 and 𝕊 at flips plus ✖ on adverse exits.

Inputs that matter

Price Source — series being filtered. Close is typical. HL2 or HLC3 can be steadier.

Deadband mode — ATR, Percent, Ticks, or Points. This defines the “it’s big enough to matter” zone.

ATR Length / Mult (DBHF) — only used when mode = ATR. Larger values widen the do-nothing zone.

Percent / Ticks / Points — alternatives to ATR; pick what fits your market’s convention.

Enter Mult — scales the deadband you must clear before the baseline moves. Increase to filter more noise.

Response — fraction of the excess applied to baseline movement. Higher responds faster; lower is smoother.

Supertrend ATR Period & Factor — traditional band size controls; higher factor widens and flips less often.

Flip Offset ATR — extra ATR buffer required to flip. Useful in choppy regimes.

Adverse Stop K·ATR — per-trade danger brake that forces an exit if price moves K×ATR against entry.

UI — toggle baseline, supertrend, signals, and bar painting; choose long and short colors.

How to read it

Green regime — candles painted long and the Supertrend running below price. Pullbacks toward the baseline that fail to breach the opposite band often resume higher.

Red regime — candles painted short and the Supertrend running above price. Rallies that cannot reclaim the band may roll over.

Frequent side swaps — reduce sensitivity by increasing Enter Mult, using ATR mode, raising the Supertrend factor, or adding Flip Offset ATR.

Use cases

Bias filter — allow entries only in the direction of the current side. Use your preferred triggers inside that bias.

Trailing logic — treat the active band as a dynamic stop. If the side flips or an adverse K·ATR exit prints, reduce or close exposure.

Regime map — on higher timeframes, the combination baseline + band produces a clean up vs down template for allocation decisions.

Tuning guidance

Fast markets — ATR deadband, modest Enter Mult (0.8–1.2), response 0.2–0.35, Supertrend factor 1.7–2.2, small Flip Offset (0.2–0.5 ATR).

Choppy ranges — widen deadband or raise Enter Mult, lower response, and add more Flip Offset so flips require stronger evidence.

Slow trends — longer ATR periods and higher Supertrend factor to keep you on side longer; use a conservative adverse K.

Included alerts

DBHF ST Long — side flips to long.

DBHF ST Short — side flips to short.

Adverse Exit Long / Short — K·ATR stop triggers against the current side.

Strengths

Deadbanded baseline reduces micro whipsaws before Supertrend logic even begins.

Flip hysteresis adds a second layer of confirmation at the boundary.

Optional adverse ATR stop provides a uniform risk cut across assets and regimes.

Clear visuals and minimal parameters to adjust for symbol behavior.

Putting it together

Think of this tool as two decisions layered into one view. The deadband baseline answers “does this move even count,” then the Supertrend wrapped around that baseline answers “if it counts, which side should I be on and where do I flip.” When both parts agree you tend to stay on the correct side of a trend for longer, and when they disagree you get an early warning that conditions are changing.

When the baseline bends and price cannot reclaim the opposite band , momentum is usually continuing. Pullbacks into the baseline that stall before the far band often resolve in trend.

When the baseline flattens and the bands compress , expect indecision. Use the Flip Offset ATR to avoid reacting to the first feint. Wait for a clean band breach with follow through.

When an adverse K·ATR exit prints while the side has not flipped , treat it as a risk event rather than a full regime change. Many users cut size, re-enter only if the side reasserts, and let the next flip confirm a new trend.

Final thoughts

Deadband Hysteresis Supertrend is best read as a regime lens. The baseline defines your tolerance for noise, the bands define your trailing structure, and the flip offset plus adverse ATR stop define how forgiving or strict you want to be at the boundary. On strong trends it helps you hold through shallow shakeouts. In choppy conditions it encourages patience until price does something meaningful. Start with settings that reflect the cadence of your market, observe how often flips occur, then nudge the deadband and flip offset until the tool spends most of its time describing the move you care about rather than the noise in between.

Monthly VWAPDescription

This indicator identifies potential mean reversion opportunities by tracking price deviations from monthly VWAP with dynamic volatility-adjusted thresholds.

Core Logic:

The indicator monitors when price moves significantly away from monthly VWAP and looks for potential reversal opportunities. It uses ATR-based dynamic thresholds that adapt to current market volatility, combined with volume confirmation to filter out weak signals.

Key Features:

Adaptive Thresholds: ATR-based bands that adjust to market volatility

Volume Confirmation: Requires average volume spike to validate signals

Monthly Reset: VWAP anchors reset each month for fresh reference levels

Visual Clarity: Color-coded deviation line with background highlights for active signals

Info Panel: Shows days from anchor and current price context vs fair value

Signal Generation:

Buy Signal: Price below monthly VWAP by threshold amount with elevated volume

Sell Signal: Price above monthly VWAP by threshold amount with elevated volume

Neutral: Price within threshold range or insufficient volume

Best Used For:

Mean reversion strategies in ranging markets

Identifying potential oversold/overbought conditions

Understanding price position relative to monthly fair value

HalfTrend Histogram (MTF)This indicator shows the halftrend on a histogram (rather than a line on the chart) and has an option for Multi timeframe (MTF).

It uses the logic of the original halftrend coded by Everget.

The halftrend is a trend-following indicator that uses volatility to to determine change in bias.

Double Median ATR Bands | MisinkoMasterThe Double Median ATR Bands is a version of the SuperTrend that is designed to be smoother, more accurate while maintaining a good speed by combining the HMA smoothing technique and the median source.

How does it work?

Very simple!

1. Get user defined inputs:

=> Set them up however you want, for the result you want!

2. Calculate the Median of the source and the ATR

=> Very simple

3. Smooth the median with √length (for example if median length = 9, it would be smoothed over the length of 3 since 3x3 = 9)

4. Add ATR bands like so:

Upper = median + (atr*multiplier)

Lower = median - (atr*multiplier)

Trend Logic:

Source crossing over the upper band = uptrend

Source crossing below the lower band = downtrend

Enjoy G´s!

2ATR / Close %Certainly. Here is the English version of the indicator description you requested.

---

### **2ATR Stop-Loss Ratio**

This indicator provides a straightforward calculation of **what percentage a 2ATR (Average True Range) move represents relative to the current price**. It's a specialized tool designed to help traders set dynamic, volatility-based stop-loss levels.

---

### **Purpose of the Indicator**

Many traders use a **2ATR** as their standard for setting a stop-loss, believing it's a good measure of a stock's typical movement. However, it can be difficult to quickly determine the exact percentage a 2ATR drop represents from the current price. This indicator solves that problem by giving you a clear, single number that shows the **anticipated percentage loss before you even enter a position**.

---

### **How It Works**

The indicator is calculated using a simple formula:

**(2 * ATR(20) / Current Price) * 100**

* `ATR(20)`: The Average True Range over the last 20 periods. This period can be customized in the indicator's settings.

* `Current Price`: The closing price at the time of calculation.

---

### **How to Use It**

* **Assess Risk**: A higher number on the indicator means greater volatility, indicating a wider stop-loss range.

* **Set a Stop-Loss**: If the indicator shows **3%**, it means a 2ATR move is roughly a 3% change from the current price. This gives you a clear understanding of the potential loss.

* **Adjust Position Size**: If the potential percentage loss is larger than you're comfortable with, you can use this information to reduce your position size, effectively managing your risk.

This tool is especially useful for trading highly volatile stocks, as it helps you establish a clear and effective risk management strategy.

NY Anchored VWAP and Auto SMANY Anchored VWAP and Auto SMA

This script is a versatile trading indicator for the TradingView platform that combines two powerful components: a New York-anchored Volume-Weighted Average Price (VWAP) and a dynamic Simple Moving Average (SMA). Designed for traders who utilize VWAP for intraday trend analysis, this tool provides a clear visual representation of average price and volatility-adjusted moving averages, generating automated alerts for key crossover signals.

Indicator Components

1. NY Anchored VWAP

The VWAP is a crucial tool that represents the average price of a security adjusted for volume. This version is "anchored" to the start of the New York trading session, resetting at the beginning of each new session. This provides a clean, session-specific anchor point to gauge market sentiment and trend. The VWAP line changes color to reflect its slope:

Green: When the VWAP is trending upwards, indicating a bullish bias.

Red: When the VWAP is trending downwards, indicating a bearish bias.

2. Auto SMA

The Auto SMA is a moving average with a unique twist: its lookback period is not fixed. Instead, it dynamically adjusts based on market volatility. The script measures volatility using the Average True Range (ATR) and a Z-Score calculation.

When volatility is expanding, the SMA's length shortens, making it more sensitive to recent price changes.

When volatility is contracting, the SMA's length lengthens, smoothing out the price action to filter out noise.

This adaptive approach allows the SMA to react appropriately to different market conditions.

Suggested Trading Strategy

This indicator is particularly effective when used on a one-minute chart for identifying high-probability trade entries. The core of the strategy is to trade the crossover between the VWAP and the Auto SMA, with confirmation from a candle close.

The strategy works best when the entry signal aligns with the overall bias of the higher timeframe market structure. For example, if the daily or 4-hour chart is in an uptrend, you would look for bullish signals on the one-minute chart.

Bullish Entry Signal: A potential entry is signaled when the VWAP crosses above the Auto SMA, and is confirmed when the one-minute candle closes above both the VWAP and the SMA. This indicates a potential continuation of the bullish momentum.

Bearish Entry Signal: A potential entry is signaled when the VWAP crosses below the Auto SMA, and is confirmed when the one-minute candle closes below both the VWAP and the SMA. This indicates a potential continuation of the bearish momentum.

The built-in alerts for these crossovers allow you to receive notifications without having to constantly monitor the charts, ensuring you don't miss a potential setup.

Triple Tap Sniper Triple Tap Sniper v3 – EMA Retest Precision System

Triple Tap Sniper is a precision trading tool built around the 21, 34, and 55 EMAs, designed to capture high-probability retests after EMA crosses. Instead of chasing the first breakout candle, the system waits for the first pullback into the EMA21 after a trend-confirming cross — the spot where professional traders often enter.

🔑 Core Logic

EMA Alignment → Trend defined by EMA21 > EMA34 > EMA55 (bullish) or EMA21 < EMA34 < EMA55 (bearish).

Cross Detection → Signals are only armed after a fresh EMA cross.

Retest Entry → Buy/Sell signals fire only on the first retest of EMA21, with trend still intact.

Pro Filters →

📊 Higher Timeframe Confirmation: Aligns signals with larger trend.

📈 ATR Volatility Filter: Blocks weak signals in low-vol chop.

📏 EMA Spread Filter: Ignores tiny “fake crosses.”

🕯️ Price Action Filter: Requires a proper wick rejection for valid entries.

🚀 Why Use Triple Tap Sniper?

✅ Filters out most false signals from sideways markets.

✅ Focuses only on clean trend continuations after pullbacks.

✅ Beginner-friendly visuals (Buy/Sell labels) + alert-ready for automation.

✅ Flexible: works across multiple timeframes & asset classes (stocks, crypto, forex).

⚠️ Notes

This is a signal indicator, not a full strategy. For backtesting and optimization, convert to a strategy and adjust filters per market/timeframe.

No indicator guarantees profits — use with sound risk management.

Perfect Price-Anchored % Fib Grid This indicator generates support and resistance levels anchored to a fixed price of your choice.

You can also specify a percentage for the indicator to calculate potential highs and lows.

Commonly used values are 3.5% or 7%, as well as smaller decimal versions like 0.35% or 0.7%, depending on the volatility you expect.

In addition, the indicator can highlight potential stop-run levels in multiples of 27 — ranging from 0 up to 243. This automatically places the 243 GB range directly onto your chart.

The tool is versatile and can be applied not only to equities, but also to ES futures and Forex markets.

Sentinel 5 — OHL daybreak signals [KedArc Quant]Overview

Sentinel 5 plots the first-bar high/low of each trading session and gives clean, rules-based signals in two ways:

1) OHL Setups at the close of the first bar (Open equals/near High for potential short; Open equals/near Low for potential long).

2) Breakout Signals later in the session when price breaks the first-bar High/Low, with optional body/penetration filters.

Basic workflow

1. Wait for the first session bar to finish.

*If O≈H (optionally by proximity) → short setup. •

*If O≈L → long setup. • If neither happens, optionally allow later breakouts.

2. Optional: Act only on breakouts that penetrate a minimum % of that bar’s range/body.

3. Skip the day automatically if the first bar is abnormally large (marubozu-like / extreme ATR / outsized vs yesterday).

Signals & Markers

Markers on the chart:

▲ O=L (exact) / O near L (proximity) – long setup at first-bar close.

▼ O=H (exact) / O near H (proximity) – short setup at first-bar close.

▲ Breakout Long – later bar breaks above first-bar High meeting your penetration rule.

▼ Breakout Short – later bar breaks below first-bar Low meeting your penetration rule.

ATR% | Volatility NormalizerThis indicator measures true volatility by expressing the Average True Range (ATR) as a percentage of price. Unlike basic ATR plots, which show raw values, this version normalizes volatility to make it directly comparable across instruments and timeframes.

How it works:

Uses True Range (High–Low plus gaps) to capture actual market movement.

Normalizes by dividing ATR by the chosen price base (default: Close).

Multiplies by 100 to output a clean ATR% line.

Smoothing is flexible: choose from RMA, SMA, EMA, or WMA.

Optional Feature:

For comparison, you can toggle an auxiliary line showing the average absolute close-to-close % move, highlighting the difference between simplified and true volatility.

Why use it:

Track regime shifts: identify when volatility expands or contracts in % terms.

Compare volatility across different markets (equities, crypto, forex, commodities).

Integrate into risk management: position sizing, stop placement, or volatility filters for entries.

Interpretation:

Rising ATR% → expanding volatility, potential breakouts or unstable ranges.

Falling ATR% → contracting volatility, possible consolidation or range-bound conditions.

Sudden spikes → market “shocks” worth paying attention to.

Dynamic Chandelier Exit Trader [KedArc Quant])Dynamic Chandelier Exit Trader (DCET)

The Dynamic Chandelier Exit Trader (DCET) builds upon the classical Chandelier Exit indicator by combining volatility-based stop placement with risk-reward exit logic. It is designed to provide clear buy/sell flip signals, making it adaptable across multiple trading environments.

Market Suitability

The DCET is most effective under the following market conditions:

1. Trending Markets (Upward or Downward)

- Strong performance when price is in a clear directional trend.

- Buy signals align with uptrends, sell signals align with downtrends.

- Works well on stocks, forex pairs, and crypto during trending phases.

2. Breakout Environments:

- Captures moves when price breaks out of consolidations.

- ATR-based stop dynamically adjusts to volatility expansion.

- Effective for traders who like catching the first move after breakouts.

3. Sideways / Range-Bound Markets:

- DCET tends to generate more frequent flip signals in sideways conditions.

- May lead to whipsaws, but can still be used with reduced ATR length or by combining with a trend filter (e.g., moving average direction).

4. All Markets (with Adjustments):

- Works universally but requires tuning.

- In highly volatile markets (e.g., crypto), a higher ATR multiplier may reduce false signals.

- In stable, slower-moving markets (e.g., large-cap equities), smaller ATR multipliers improve responsiveness.

ATR Extension from Moving Average, with Robust Sigma Bands

# ATR Extension from Moving Average, with Robust Sigma Bands

**What it does**

This indicator measures how far price is from a selected moving average, expressed in **ATR multiples**, then overlays **robust sigma bands** around the long run central tendency of that extension. Positive values mean price is extended above the MA, negative values mean price is extended below the MA. The signal adapts to volatility through ATR, which makes comparisons consistent across symbols and regimes.

**Why it can help**

* Normalizes distance to an MA by ATR, which controls for changing volatility

* Uses the **bar’s extreme** against the MA, not just the close, so it captures true stretch

* Computes a **median** and **standard deviation** of the extension over a multi-year window, which yields simple, intuitive bands for trend and mean-reversion decisions

---

## Inputs

* **MA length**: default 50, options 200, 64, 50, 20, 9, 4, 3

* **MA timeframe**: Daily or Weekly. The MA is computed on the chosen higher timeframe through `request.security`.

* **MA type**: EMA or SMA

* **Years lookback**: 1 to 10 years, default 5. This sets the sample for the median and sigma calculation, `years * 365` bars.

* **Line width**: visual width of the plotted extension series

* **Table**: optional on-chart table that displays the current long run **median** and **sigma** of the extension, with selectable text size

**Fixed parameters in this release**

* **ATR length**: 20 on the daily timeframe

* **ATR type**: classic ATR. ADR percent is not enabled in this version.

---

## Plots and colors

* **Main plot**: “Extension from 50d EMA” by default. Value is in **ATR multiples**.

* **Reference lines**:

* `median` line, black dashed

* +2σ orange, +3σ red

* −2σ blue, −3σ green

---

## How it is calculated

1. **Moving average** on the selected higher timeframe: EMA or SMA of `close`.

2. **Extreme-based distance** from MA, as a percent of price:

* If `close > MA`, use `(high − MA) / close * 100`

* Else, use `(low − MA) / close * 100`

3. **ATR percent** on the daily timeframe: `ATR(20) / close * 100`

4. **ATR multiples**: extension percent divided by ATR percent

5. **Robust center and spread** over the chosen lookback window:

* Center: **median** of the ATR-multiple series

* Spread: **standard deviation** of that series

* Bands: center ± 1σ, 2σ, 3σ, with 2σ and 3σ drawn

This design yields an intuitive unit scale. A value of **+2.0** means price is about 2 ATR above the selected MA by the most stretched side of the current bar. A value of **−3.0** means roughly 3 ATR below.

---

## Practical use

* **Trend continuation**

* Sustained readings near or above **+1σ** together with a rising MA often signal healthy momentum.

* **Mean reversion**

* Spikes into **±2σ** or **±3σ** can identify stretched conditions for fade setups in range or late-trend environments.

* **Regime awareness**

* The **median** moves slowly. When median drifts positive for many months, the market spends more time extended above the MA, which often marks bullish regimes. The opposite applies in bearish regimes.

**Notes**

* The MA can be set to Weekly while ATR remains Daily. This is deliberate, it keeps the normalization stable for most symbols.

* On very short intraday charts, the extension remains meaningful since it references the session’s extreme against a higher-timeframe MA and a daily ATR.

* Symbols with short histories may not fill the lookback window. Bands will adapt as data accrues.

---

## Table overlay

Enable **Table → Show** to see:

* “ATR from \”

* Current **median** and **sigma** of the extension series for your lookback

---

## Recommended settings

* **Swing equities**: 50 EMA on Daily, 5 to 7 years

* **Index trend work**: 200 EMA on Daily, 10 years

* **Position trading**: 20 or 50 EMA on Weekly MA, 5 to 10 years

---

## Interpretation examples

* Reading **+2.7** with price above a rising 50 EMA, near prior highs

* Strong trend extension, consider pyramiding in trend systems or waiting for a pullback if you are a mean-reverter.

* Reading **−2.2** into multi-month support with flattening MA

* Stretch to the downside that often mean-reverts, size entries based on your system rules.

---

## Credits

The concept of measuring stretch from a moving average in ATR units has a rich community history. This implementation and its presentation draw on ideas popularized by **Jeff Sun**, **SugarTrader**, and **Steve D Jacobs**. Thanks to each for their contributions to ATR-based extension thinking.

---

## License

This script and description are distributed under **MPL-2.0**, consistent with the header in the source code.

---

## Changelog

* **v1.0**: Initial public release. Daily ATR normalization, EMA or SMA on D or W timeframe, robust median and sigma bands, optional table.

---

## Disclaimer

This tool is for educational use only. It is not financial advice. Always test on your own data and strategies, then manage risk accordingly.

ATR SL/TPStop Loss Finder ATR

A Stop Loss Finder ATR indicator is a dynamic risk management tool leveraging the Average True Range (ATR) to identify and track optimal stop-loss levels based on current market volatility.

A stop hunt indicator is a technical tool designed to identify potential instances where large market participants, often referred to as "smart money," deliberately move the price to trigger a large number of stop-loss orders, creating a temporary price distortion before reversing the trend. These indicators aim to help traders detect these events to either avoid being stopped out or to enter trades in the direction of the anticipated reversal.

For example, a long wick below support with high volume may signal a bullish stop-hunt , indicating that the price has been driven down to trigger sell-stop orders before reversing upward. Conversely, a long wick above resistance with high volume may signal a bearish stop-hunt , suggesting the price was pushed up to trigger buy-stop orders before reversing downward. The presence of such wicks is often associated with candlestick patterns like hammers or shooting stars.

Unlike fixed stop-losses, this indicator adapts its distance from the current price using a customizable ATR multiplier, ensuring that stop-loss levels are neither too tight (prone to being triggered by normal market noise) nor too wide (exposing capital to excessive risk) . The core function calculates the true range—considering the current high-low range, gaps up, and gaps down—over a user-defined period (typically 14 bars), then applies a multiplier to generate a volatility-adjusted stop-loss distance . This approach allows the indicator to dynamically widen stops during high-volatility periods and tighten them during calm markets, providing a more responsive and context-aware exit strategy.

EMA多空趋势信号The EMA multi-period moving average combination retains the Fibonacci sequence 144 for moving support and resistance. It also integrates 1ATR to facilitate users to set take-profit and stop-loss.

Range TableThe Range Table indicator calculates and displays the Daily Average True Range (ATR), the current day's True Range (TR), and two customizable ATR percentage values in a clean table format. It provides values in ticks, points, and USD, helping traders set stop-loss buffers based on market volatility.

**Features:**

- Displays the Daily ATR (14-period) and current day's True Range (TR) with its percentage of the Daily ATR.

- Includes two customizable ATR percentages (default: 75% and 10%, with the second disabled by default).

- Shows values in ticks, points, and USD based on the symbol's tick size and point value.

- Customizable table position, background color, text color, and font size.

- Toggle visibility for the table and percentage rows via input settings.

**How to Use:**

1. Add the indicator to your chart.

2. Adjust the table position, colors, and font size in the input settings.

3. Enable or disable the 75% and 10% ATR rows or customize their percentages.

4. Use the displayed values to set stop-loss or take-profit levels based on volatility.

**Ideal For:**

- Day traders and swing traders looking to set volatility-based stop-losses.

- Users analyzing tick, point, and USD-based risk metrics.

**Notes:**

- Ensure your chart is set to a timeframe that aligns with the daily ATR calculations.

- USD values are approximate if `syminfo.pointvalue` is unavailable.

Developed by FlyingSeaHorse.

[Top] Simple ATR TP/SLSimple TP/SL from ATR (Locked per Bar) - Advanced Position Management Tool

What This Indicator Does:

Automatically calculates and displays Take Profit (TP) and Stop Loss (SL) levels based on Average True Range (ATR)

Locks ATR values and direction signals at the start of each bar to prevent repainting and provide consistent levels

Offers multiple direction detection modes including real-time candle-based positioning for dynamic trading approaches

Displays entry, TP, and SL levels as clean horizontal lines that extend from the current bar

Original Features That Make This Script Unique:

Bar-Locked ATR System: ATR values are captured and frozen at bar open, ensuring levels remain stable throughout the bar's progression

Multi-Modal Direction Detection: Four distinct modes for determining TP/SL positioning - Trend Following (EMA-based), Bullish Only, Bearish Only, and real-time Candle Based

Real-Time Candle Flipping: In Candle Based mode, TP/SL levels flip immediately when the current candle changes from bullish to bearish or vice versa

Persistent Line Management: Uses efficient line object management to prevent ghost lines and maintain clean visual presentation

Flexible Base Price Selection: Choose between Open (static), Close (dynamic), or midpoint (H+L)/2 for entry level calculation

How The Algorithm Works:

ATR Calculation: Captures ATR value at each bar open using specified length parameter, maintaining consistency throughout the bar

Direction Determination: Uses different methods based on selected mode - EMA crossover for trend following, or real-time candle color for dynamic positioning

Level Calculation: TP level = Base Price + (Direction × TP Multiplier × ATR), SL level = Base Price - (Direction × SL Multiplier × ATR)

Visual Management: Creates persistent line objects once, then updates their positions every bar for optimal performance

Direction Modes Explained:

Trend Following: Uses 5-period and 12-period EMA relationship to determine trend direction (locked at bar open)

Bullish Only: Always places TP above and SL below entry (traditional long setup)

Bearish Only: Always places TP below and SL above entry (traditional short setup)

Candle Based: Dynamically adjusts based on current candle direction - flips in real-time as candle develops

Key Input Parameters:

ATR Length: Period for ATR calculation (default 14) - longer periods provide smoother volatility measurement

TP Multiplier: Take profit distance as multiple of ATR (default 1.0) - higher values target larger profits

SL Multiplier: Stop loss distance as multiple of ATR (default 1.0) - higher values allow more room for price movement

Base Price: Reference point for level calculations - Open for static entry, Close for dynamic tracking

Direction Mode: Method for determining whether TP goes above or below entry level

How To Use This Indicator:

For Position Sizing: Use the displayed SL distance to calculate appropriate position size based on your risk tolerance

For Entry Timing: Wait for price to approach the entry level before taking positions

For Risk Management: Set your actual stop loss orders at or near the displayed SL level

For Profit Taking: Use the TP level as initial profit target, consider scaling out at this level

Mode Selection: Choose Candle Based for scalping and quick reversals, Trend Following for swing trading

Visual Style Customization:

Line Colors: Customize TP line color (default teal) and SL line color (default orange) for easy identification

Line Widths: Adjust TP/SL line thickness (1-5) and entry line thickness (1-3) for visibility preferences

Clean Display: Lines extend 3 bars forward from current bar and update position dynamically

Best Practices:

Use on clean charts without multiple overlapping indicators for clearest visual interpretation

Combine with volume analysis and key support/resistance levels for enhanced decision making

Adjust ATR length based on your trading timeframe - shorter for scalping, longer for position trading

Test different TP/SL multipliers based on the volatility characteristics of your chosen instruments

Consider using Trend Following mode during strong trending periods and Candle Based during ranging markets

Chicago 17:00-19:00 Overnight RangeThis indicator will map out range high and range low of previous 17:00 - 19:00 of the chart. It can also display mid range if needed

Opening Range — Chicago 17:00-19:00 (Customizable)Maps opening 2 hour range of Chicago timezone with the range high range low and medium zone. It can be customized to fit your needs

ATR x2 AUTODescription:

This indicator automatically plots ATR-based horizontal levels for each of the most recent candles, helping traders visualize potential stop-loss hunting zones, breakout areas, or price reaction points.

It works by taking the Average True Range (ATR) over a customizable period and multiplying it by a user-defined factor (default: ×2). For each of the last N candles (default: 5), it calculates and draws:

Below green candles (bullish) → A horizontal line placed ATR × multiplier below the candle’s low.

Above red candles (bearish) → A horizontal line placed ATR × multiplier above the candle’s high.

Doji candles → No line is drawn.

Each line extends to the right indefinitely, allowing traders to monitor how price reacts when returning to these ATR-based levels. This makes the tool useful for:

Identifying likely stop-loss clusters below bullish candles or above bearish candles.

Anticipating liquidity sweeps and fakeouts.

Supporting breakout or reversal strategies.

Key Features:

Customizable ATR length, multiplier, number of recent candles, and line thickness.

Separate colors for bullish and bearish candle levels.

Automatic real-time updates for each new bar.

Clean overlay on the main price chart.

Inputs:

ATR Length → Period used for ATR calculation.

Multiplier → Factor applied to the ATR distance.

Number of Candles → How many recent candles to track.

Line Thickness and Colors → Full visual customization.

Usage Tip:

These levels can be combined with key market structure points such as support/resistance, trendlines, or the 200 EMA to anticipate high-probability price reactions.

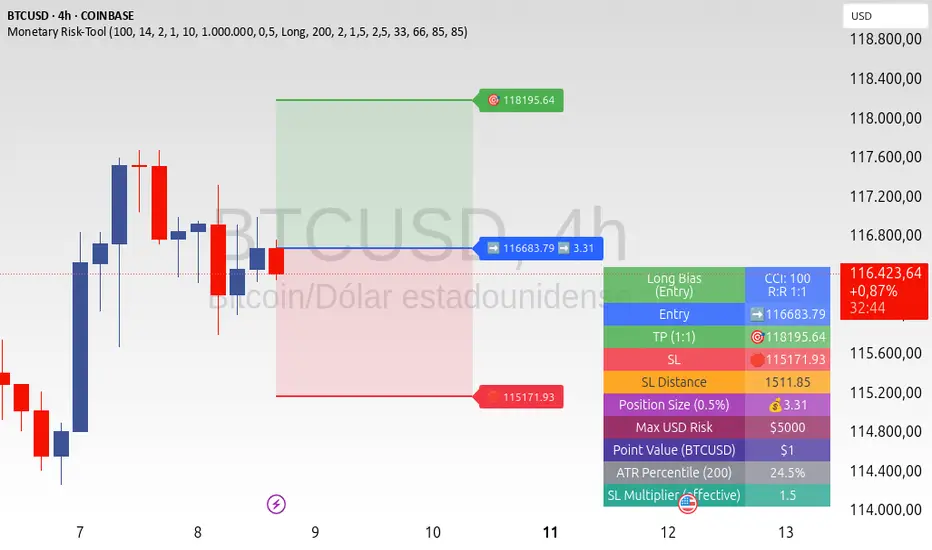

ATR+CCI Monetary Risk Tool - TP/SL⚙️ ATR+CCI Monetary Risk Tool — Volatility-aware TP/SL & Position Sizing

Exact prices (no rounding), ATR-percentile dynamic stops, and risk-budget sizing for consistent execution.

🧠 What this indicator is

A risk-first planning tool. It doesn’t generate orders; it gives you clean, objective levels (Entry, SL, TP) and position size derived from your risk budget. It shows only the latest setup to keep charts readable, and a compact on-chart table summarizing the numbers you actually act on.

✨ What makes it different

Dynamic SL by regime (ATR percentile): Instead of a fixed multiple, the SL multiplier adapts to the current volatility percentile (low / medium / high). That helps avoid tight stops in noisy markets and over-wide stops in quiet markets.

Risk budgeting, not guesswork: Size is computed from Account Balance × Max Risk % divided by SL distance × point value. You risk the same dollars across assets/timeframes.

Precision that matches your instrument: Entry, TP, SL, and SL Distance are displayed as exact prices (no rounding), truncated to syminfo.mintick so they align with broker/exchange precision.

Symbol-aware point value: Uses syminfo.pointvalue so you don’t maintain tick tables.

Non-repaint option: Work from closed bars to keep the plan stable.

🔧 How to use (quick start)

Add to chart and pick your timeframe and symbol.

In settings:

Set Account Balance (USD) and Max Risk per Trade (%).

Choose R:R (1:1 … 1:5).

Pick ATR Period and CCI Period (defaults are sensible).

Keep Dynamic ATR ON to adapt SL by regime.

Keep Use closed-bar values ON to avoid repaint when planning.

Read the labels (Entry/TP/SL) and the table (SL Distance, Position Size, Max USD Risk, ATR Percentile, effective SL Mult).

Combine with your entry trigger (price action, levels, momentum, etc.). This indicator handles risk & targets.

📐 How levels are computed

Bias: CCI ≥ 0 ⇒ long, otherwise short.

ATR Percentile: Percent rank of ATR(atrPeriod) over a lookback window.

Effective SL Mult:

If percentile < Low threshold ⇒ use Low SL Mult (tighter).

If between thresholds ⇒ use Base SL Mult.

If percentile > High threshold ⇒ use High SL Mult (wider).

Stop-Loss: SL = Entry ± ATR × SL_Mult (minus for long, plus for short).

Take-Profit: TP = Entry ± (Entry − SL) × R (R from the R:R dropdown).

Position Size:

USD Risk = Balance × Risk%

Contracts = USD Risk ÷ (|Entry − SL| × PointValue)

For futures, quantity is floored to whole contracts.

Exact prices: Entry/TP/SL and SL Distance are not rounded; they’re truncated to mintick so what you see matches valid price increments.

📊 What you’ll see on chart

Latest Entry (blue), TP (green), SL (red) with labels (optional emojis: ➡️ 🎯 🛑).

Info Table with:

Bias, Entry, TP, SL (exact, truncated to mintick)

SL Distance (exact, truncated)

Position Size (contracts/units)

Max USD Risk

Point Value

ATR Percentile and effective SL Mult

🧪 Practical examples

High-volatility session (e.g., XAUUSD, 1H): ATR percentile is high ⇒ wider SL, smaller size. Reduces churn from normal noise during macro events.

Range-bound market (e.g., EURUSD, 4H): ATR percentile low ⇒ tighter SL, better R:R. Helps you avoid carrying unnecessary risk.

Index swing planning (e.g., ES1!, Daily): Non-repaint levels + risk budgeting = consistent sizing across days/weeks, easier to review and journal.

🧭 Why traders should use it

Consistency: Same dollar risk regardless of instrument or volatility regime.

Clarity: One-trade view forces focus; you see the numbers that matter.

Adaptivity: Stops calibrated to the market’s current behavior, not last month’s.

Discipline: A visible checklist (SL distance, size, USD risk) before you hit buy/sell.

🔧 Input guide (practical defaults)

CCI Period: 100 by default; use as a bias filter, not an entry signal.

ATR Period: 14 by default; raise for smoother, lower for more reactive.

ATR Percentile Lookback: 200 by default (stable regime detection).

Percentile thresholds: 33/66 by default; widen the gap to change how often regimes switch.

SL Mults: Start ~1.5 / 2.0 / 2.5 (low/base/high). Tune by asset.

Risk % per trade: Common pro ranges are 0.25–1.0%; adjust to your risk tolerance.

R:R: Start with 1:2 or 1:3 for balanced skew; adapt to strategy edge.

Closed-bar values: Keep ON for planning/live; turn OFF only for exploration.

💡 Best practices

Combine with your entry logic (structure, momentum, liquidity levels).

Review ATR percentile and effective SL Mult across sessions so you understand regime shifts.

For futures, remember size is floored to whole contracts—safer by design.

Journal trades with the table snapshot to improve risk discipline over time.

⚠️ Notes & limitations

This is not a strategy; it does not place orders or alerts.

No slippage/commissions modeled here; build a strategy() version for backtests that mirror your broker/exchange.

Displayed non-price metrics use two decimals; prices and SL Distance are exact (truncated to mintick).

📎 Disclaimer

For educational purposes only. Not financial advice. Markets involve risk. Test thoroughly before trading live.

Mutanabby_AI | Fresh Algo V24Mutanabby_AI | Fresh Algo V24: Advanced Multi-Mode Trading System

Overview

The Mutanabby_AI Fresh Algo V24 represents a sophisticated evolution of multi-component trading systems that adapts to various market conditions through advanced operational configurations and enhanced analytical capabilities. This comprehensive indicator provides traders with multiple signal generation approaches, specialized assistant functions, and dynamic risk management tools designed for professional market analysis across diverse trading environments.

Primary Signal Generation Framework

The Fresh Algo V24 operates through two fundamental signal generation approaches that accommodate different market perspectives and trading philosophies. The Trending Signals Mode serves as the primary trend-following mechanism, combining Wave Trend Oscillator analysis with Supertrend directional signals and Squeeze Momentum breakout detection. This mode incorporates ADX filtering that requires values exceeding 20 to ensure sufficient trend strength exists before signal activation, making it particularly effective during sustained directional market movements where momentum persistence creates profitable trading opportunities.

The Contrarian Signals Mode provides an alternative approach targeting reversal opportunities through extreme market condition identification. This mode activates when the Wave Trend Oscillator reaches critical threshold levels, specifically when readings surpass 65 indicating potential bearish reversal conditions or drop below 35 suggesting bullish reversal opportunities. This methodology proves valuable during overextended market phases where mean reversion becomes statistically probable.

Advanced Filtering Mechanisms

The system incorporates multiple sophisticated filtering mechanisms designed to enhance signal quality and reduce false positive occurrences. The High Volume Filter requires volume expansion confirmation before signal activation, utilizing exponential moving average calculations to ensure institutional participation accompanies price movements. This filter substantially improves signal reliability by eliminating low-conviction breakouts that lack adequate volume support from professional market participants.

The Strong Filter provides additional trend confirmation through 200-period exponential moving average analysis. Long position signals require price action above this benchmark level, while short position signals necessitate price action below it. This ensures strategic alignment with longer-term trend direction and reduces the probability of trading against major market movements that could invalidate shorter-term signals.

Cloud Filter Configuration System

The Fresh Algo V24 offers four distinct cloud filter configurations, each optimized for specific trading timeframes and market approaches. The Smooth Cloud Filter utilizes the mathematical relationship between 150-period and 250-period exponential moving averages, providing stable trend identification suitable for position trading strategies. This configuration generates signals exclusively when price action aligns with cloud direction, creating a more deliberate but highly reliable signal generation process.

The Swing Cloud Filter employs modified Supertrend calculations with parameters specifically optimized for swing trading timeframes. This filter achieves optimal balance between responsiveness and stability, adapting effectively to medium-term price movements while filtering excessive market noise that typically affects shorter-term analytical systems.

For active intraday traders, the Scalping Cloud Filter utilizes accelerated Supertrend calculations designed to capture rapid trend changes effectively. This configuration provides enhanced signal generation frequency suitable for compressed timeframe strategies. The advanced Scalping+ Cloud Filter incorporates Hull Moving Average confirmation, delivering maximum responsiveness for ultra-short-term trading while maintaining signal quality through additional momentum validation processes.

Specialized Assistant Functionality

The system includes two distinct assistant modes that provide supplementary market analysis capabilities. The Trend Assistant Mode activates advanced cloud analysis overlays that display dynamic support and resistance zones calculated through adaptive volatility algorithms. These levels automatically adjust to current market conditions, providing visual guidance for identifying trend continuation patterns and potential reversal areas with mathematical precision.

The Trend Tracker Mode concentrates on long-term trend identification by displaying major exponential moving averages with color-coded fill areas that clarify directional bias. This mode maintains visual simplicity while providing comprehensive trend context evaluation, enabling traders to quickly assess broader market direction and align shorter-term strategies accordingly.

Dynamic Risk Management System

The integrated risk management system automatically adapts across all operational modes, calculating stop loss and take profit targets using Average True Range multiples that adjust to current market volatility. This approach ensures consistent risk parameters regardless of selected operational mode while maintaining relevance to prevailing market conditions.

Stop loss placement occurs at dynamically calculated distances from entry points, while three progressive take profit targets establish at customizable ATR multiples respectively. The system automatically updates these levels upon trend direction changes, ensuring current market volatility influences all risk calculations and maintains appropriate risk-reward ratios throughout trade management.

Comprehensive Market Analysis Dashboard

The sophisticated dashboard provides real-time market analysis including volatility measurements, institutional activity assessment, and multi-timeframe trend evaluation across five-minute through four-hour periods. This comprehensive market context assists traders in selecting appropriate operational modes based on current market characteristics rather than relying exclusively on historical performance data.

The multi-timeframe analysis ensures mode selection considers broader market context beyond the primary trading timeframe, improving overall strategic alignment and reducing conflicts between different temporal market perspectives. The dashboard displays market state classification, volatility percentages, institutional activity levels, current trading session information, and trend pressure indicators with professional formatting and clear visual hierarchy.

Enhanced Trading Assistants

The Fresh Algo V24 includes specialized trading assistant features that complement the primary signal generation system. The Reversal Dot functionality identifies potential reversal points through Wave Trend Oscillator analysis, displaying visual indicators when crossover conditions occur at extreme levels. These reversal indicators provide early warning signals for potential trend changes before they appear in the primary signal system.

The Dynamic Take Profit Labels feature automatically identifies optimal profit-taking opportunities through RSI threshold analysis, marking potential exit points at multiple levels for long positions and corresponding levels for short positions. This automated profit management system helps traders optimize exit timing without requiring constant manual monitoring of technical indicators.

Advanced Alert System

The comprehensive alert system accommodates all operational modes while providing granular notification control for various signal types and risk management events. Traders can configure separate alerts for normal buy signals, strong buy signals, normal sell signals, strong sell signals, stop loss triggers, and individual take profit target achievements.

Cloud crossover alerts notify traders when trend direction changes occur, providing early indication of potential strategy adjustments. The alert system includes detailed trade setup information, timeframe data, and relevant entry and exit levels, ensuring traders receive complete context for informed decision-making without requiring constant chart monitoring.

Technical Foundation Architecture

The Fresh Algo V24 combines multiple proven technical analysis components including Wave Trend Oscillator for momentum assessment, Supertrend for directional bias determination, Squeeze Momentum for volatility analysis, and various exponential moving averages for trend confirmation. Each component contributes specific market insights while the unified system provides comprehensive market evaluation through their mathematical integration.

The multi-component approach reduces dependency on individual indicator limitations while leveraging the analytical strengths of each technical tool. This creates a robust analytical framework capable of adapting to diverse market conditions through appropriate mode selection and parameter optimization, ensuring consistent performance across varying market environments.

Market State Classification

The indicator incorporates advanced market state classification through ADX analysis, distinguishing between trending, ranging, and transitional market conditions. This classification system automatically adjusts signal sensitivity and filtering parameters based on current market characteristics, optimizing performance for prevailing conditions rather than applying static analytical approaches.

The volatility measurement system calculates current market activity levels as percentages, providing quantitative assessment of market energy and helping traders select appropriate operational modes. Institutional activity detection through volume analysis ensures signal generation aligns with professional market participation patterns.

Implementation Strategy Considerations

Successful implementation requires careful matching of operational modes to prevailing market conditions and individual trading objectives. Trending modes demonstrate optimal performance during directional markets with sustained momentum characteristics, while contrarian modes excel during range-bound or overextended market conditions where reversal probability increases.

The cloud filter configurations provide varying degrees of confirmation strength, with smoother settings reducing false signal occurrence at the expense of some responsiveness to price changes. Traders must balance signal quality against signal frequency based on their risk tolerance and available trading time, utilizing the comprehensive customization options to optimize performance for their specific requirements.

Multi-Timeframe Integration

The system provides seamless multi-timeframe analysis through the integrated dashboard, displaying trend alignment across multiple time horizons from five-minute through four-hour periods. This analysis helps traders understand broader market context and avoid conflicts between different temporal perspectives that could compromise trade outcomes.

Session analysis identifies current trading session characteristics, providing context for expected market behavior patterns and helping traders adjust their approach based on typical session volatility and participation levels. This geographic market awareness enhances strategic decision-making and improves timing for trade execution.

Advanced Visualization Features

The indicator includes sophisticated visualization capabilities through gradient candle coloring based on MACD analysis, providing immediate visual feedback on momentum strength and direction. This enhancement allows rapid market assessment without requiring detailed indicator analysis, improving efficiency for traders managing multiple instruments simultaneously.

The cloud visualization system uses color-coded fill areas to clearly indicate trend direction and strength, with automatic adaptation to selected operational modes. This visual clarity reduces analytical complexity while maintaining comprehensive market information display through professional chart presentation.

Performance Optimization Framework

The Fresh Algo V24 incorporates performance optimization features including signal strength classification, automatic parameter adjustment based on market conditions, and dynamic filtering that adapts to current volatility levels. These optimizations ensure consistent performance across varying market environments while maintaining signal quality standards.

The system automatically adjusts sensitivity levels based on selected operational modes, ensuring appropriate responsiveness for different trading approaches. This adaptive framework reduces the need for manual parameter adjustments while maintaining optimal performance characteristics for each operational configuration.

Conclusion

The Mutanabby_AI Fresh Algo V24 represents a comprehensive solution for professional trading analysis, combining multiple analytical approaches with advanced visualization and risk management capabilities. The system's strength lies in its adaptive multi-mode design and sophisticated filtering mechanisms, providing traders with versatile tools for various market conditions and trading styles.

Success with this system requires understanding the relationship between different operational modes and their optimal application scenarios. The comprehensive dashboard and alert system provide essential market context and trade management support, enabling systematic approach to market analysis while maintaining flexibility for individual trading preferences.

The indicator's sophisticated architecture and extensive customization options make it suitable for traders at all experience levels, from those seeking systematic signal generation to advanced practitioners requiring comprehensive market analysis tools. The multi-timeframe integration and adaptive filtering ensure consistent performance across diverse market conditions while providing clear guidelines for strategic implementation.

ATR%指標概要 / Overview

ATR Percentage (MTF):把 ATR 轉為百分比(ATR%)或保留為絕對值,並在該「波動序列」上套用布林帶。支援多週期(MTF)計算:例如在 5 分圖顯示 4H / D1 的 ATR%。內建白色點狀水平線作為固定門檻(預設 1%)。

ATR Percentage (MTF): Converts ATR to a percentage of price (ATR%) or keeps it as absolute ATR, then applies Bollinger Bands on this volatility series. Supports multi-timeframe (MTF) calculation (e.g., show 4H/D1 ATR% on a 5-min chart). Includes a configurable white dotted horizontal threshold line (default 1%).

⸻

設計目的 / Purpose

• 以 ATR% 衡量相對波動,利於跨品種比較。

Use ATR% for relative volatility to compare across markets.

• 以 布林帶 標示「高/低波動區」,觀察擴張與壓縮。

Use Bollinger Bands on volatility to highlight expansion/squeeze.

• 提供 固定閾值(1%) 作為策略濾網或告警門檻。

Provide a fixed threshold (1%) for filters/alerts.

• 以 MTF 方式,讓低週期策略用高週期波動做濾網。

MTF lets lower-TF strategies filter by higher-TF volatility.

⸻

參數說明 / Inputs

• Use ATR as % of Close:切換 ATR(絕對值)/ ATR%(建議)。

Toggle between absolute ATR and ATR% (recommended).

• ATR Periods:ATR 計算長度(預設 22)。

ATR lookback (default 22).

• Show Bollinger Bands / BB Periods / StdDev:布林帶開關、長度與倍數(預設 20 / 2)。

Bollinger Bands on/off, length, and deviation (default 20 / 2).

• Source Timeframe:計算用週期(如 60、240、D、W;留空/Chart = 跟隨圖表)。

Timeframe used for calculations (e.g., 60, 240, D, W; empty/“Chart” = current).

• Threshold Line (%):白色點線門檻,預設 1.0(即 1%)。

White dotted threshold line, default 1.0 (1%).

提醒:當 非 ATR% 模式時,Threshold 值代表「價格單位」而非百分比。

Note: In non-ATR% mode, the threshold is in price units, not percent.

⸻

訊號解讀 / How to Read

• ATR% > 上軌:波動顯著擴張(趨勢啟動或加速常見)。

ATR% above upper band: significant expansion; often trend ignition/acceleration.

• ATR% < 下軌:波動明顯壓縮(常見於突破前)。

ATR% below lower band: volatility squeeze; often precedes breakouts.

• ATR% 穿越 Threshold(1%):達到固定波動標準,可作策略開關或風控分水嶺。

ATR% crossing the 1% threshold: fixed volatility bar for filters/risk gates.

⸻

內建告警 / Built-in Alerts

• Volatility Breakout (MTF):ATR/ATR% 向上穿越上軌。

Triggers when ATR/ATR% crosses above the upper band.

• Volatility Squeeze (MTF):ATR/ATR% 向下穿越下軌。

Triggers when ATR/ATR% crosses below the lower band.

⸻

使用建議 / Suggested Uses

• 當沖濾網:於 1–5 分圖選擇 4H / D1 作為 Source Timeframe;僅在 ATR% > 1% 且位於中線以上時允許趨勢進場。

Intraday filter: on 1–5m charts, set 4H/D1 as source TF; allow trend entries only when ATR% > 1% and above the midline.

• 突破前偵測:ATR% 長時間貼近下軌 → 留意可能的波動擴張。

Pre-breakout scan: prolonged ATR% near lower band can foreshadow expansion.

• 跨品種比較:用 ATR% 統一指數、外匯、商品的波動刻度。

Cross-asset comparison: ATR% normalizes volatility across indices/FX/commodities.

⸻

已知限制 / Notes

• MTF 對齊:使用 request.security() 對映高週期資料到當前圖表;在歷史回補與即時邊界棒可能略有差異。

MTF alignment: request.security() maps higher-TF data; boundary bars may differ slightly between historical and realtime.

• 百分比分母:ATR% 的分母為同一週期的 close;若需更平滑可改 ATR / SMA(close, N) × 100。

Denominator: ATR% uses same-TF close; for smoother values consider ATR / SMA(close, N) × 100.

• 風險聲明:僅供研究/教育用途,非投資建議,請自行控管風險。

Disclaimer: For research/education only. Not investment advice.

⸻

版本與更新 / Version & Updates

• v1.0:ATR/ATR% + BB(MTF)、1% 白色點線、兩組告警。

v1.0: ATR/ATR% + BB (MTF), 1% white dotted line, two alert conditions.