TZ - India VIX Volatility ZonesTZ – India VIX Volatility Zones is a long-term volatility analysis indicator designed to visually map important India VIX regimes using clearly defined horizontal zones and labels.

The indicator highlights how market volatility cycles between complacency, normal conditions, elevated risk, and panic phases. These zones are based on historical behavior of India VIX and help traders understand when risk is underpriced or overstretched.

This tool is especially useful for:

Index traders

Options sellers and buyers

Risk management and regime filtering

Long-term volatility study

How It Works

The script plots static, historically significant volatility zones on the India VIX chart and visually separates them using shaded bands and labels.

Volatility Zones Explained

1.Extreme Low Volatility (VIX 8–10)

Indicates market complacency and underpriced risk. Often precedes volatility expansion.

2.Low Volatility (VIX 10–13)

Stable market conditions with controlled movement.

3.Normal Volatility (VIX 13–18)

Healthy market behavior and balanced risk.

4.High Volatility (VIX 18–25)

Rising uncertainty and increased intraday swings.

5.Panic Zone (VIX 25–35+)

High fear environment, usually during major events or crises.

How Traders Can Use This Indicator

Identify volatility regimes before choosing option strategies

Avoid aggressive short-volatility trades during extreme zones

Prepare for volatility expansion during low-VIX phases

Use as a market risk context tool alongside price action

This indicator does not provide buy/sell signals. It is designed for contextual analysis and decision support.

Best Usage

Apply on India VIX (NSE:INDIAVIX)

Works best on Weekly and Monthly timeframes

Can be combined with index charts for volatility-based risk assessment

Disclaimer

This indicator is for educational and analytical purposes only.

It does not constitute financial advice or trade recommendations.

Users should apply proper risk management and confirm signals using additional analysis.

Search in scripts for "Cycle"

FOMC Federal Fund Rate Tracker [MHA Finverse]The FOMC Rate Tracker is a comprehensive indicator that visualizes Federal Reserve interest rate decisions and tracks market behavior during FOMC meeting periods. This tool helps traders analyze historical rate changes and anticipate market movements around Federal Open Market Committee announcements.

Key Features:

• Visual FOMC Periods - Automatically highlights each FOMC meeting period with colored boxes spanning from announcement to the next meeting

• Complete Rate Data - Displays actual rates, forecasts, previous rates, and rate differences for every meeting from 2021-2026

• Multiple Color Modes - Choose between cycle colors for visual distinction or rate difference colors (green for hikes, red for cuts, gray for holds)

• Smart Filtering - Filter periods by rate hikes only, cuts only, no change, or surprise moves to focus on specific market conditions

• Performance Metrics - Track average returns during rate hikes, cuts, and holds to identify historical patterns

• Volatility Analysis - Measure and compare price volatility across different FOMC periods

• Statistical Dashboard - View total hikes, cuts, holds, surprises, and longest hold streaks at a glance

• Built-in Alerts - Get notified 1 day before FOMC meetings, on meeting day, or when rates change

How It Works:

The indicator divides your chart into distinct periods between FOMC meetings, with each period showing a labeled box containing the meeting date, actual rate, forecast, previous rate, and rate difference. Future meetings are marked as "UPCOMING" to help you prepare for scheduled announcements.

Use Cases:

- Analyze how markets typically react to rate hikes vs. cuts

- Identify volatility patterns around FOMC announcements

- Backtest strategies based on monetary policy cycles

- Plan trades around upcoming Federal Reserve meetings

- Study the impact of surprise rate decisions on price action

Customization Options:

- Adjustable box transparency and outlines

- Customizable label sizes and colors

- Toggle individual dashboards on/off

- Filter specific types of rate decisions

- Configure alert preferences

This indicator is ideal for traders who incorporate fundamental analysis and monetary policy into their trading decisions. The historical data provides context for understanding market reactions to Federal Reserve actions.

Intraday Key OpensIntraday Key Opens plots the key session and cycle opening prices: 90-minute cycles opens, New York open, Asia open, and 9:30 US market open. Each line is labeled, color-coded, and can be toggled on/off independently. Designed for intraday traders to quickly identify important price levels and session pivots.

Dani u nedelji + midnight open @mladja123This indicator breaks the weekly timeframe into cycles and marks the midnight open for each day. It helps traders visualize weekly structure, identify key daily openings, and track market rhythm within the week. Perfect for analyzing trend patterns, swing setups, and session-based strategies.

Modern Economic Eras DashboardOverview

This script provides a historical macroeconomic visualization of U.S. markets, highlighting long-term structural "eras" such as the Bretton Woods period, the inflationary 1970s, and the post-2020 "Age of Disorder." It overlays key economic indicators sourced from FRED (Federal Reserve Economic Data) and displays notable market crashes, all in a clean and rescaled format for easy comparison.

Data Sources & Indicators

All data is loaded monthly from official FRED series and rescaled to improve readability:

🔵 Real GDP (FRED:GDP): Total output of the U.S. economy.

🔴 Inflation Index (FRED:CPIAUCSL): Consumer price index as a proxy for inflation.

⚪ Debt to GDP (FRED:GFDGDPA188S): Federal debt as % of GDP.

🟣 Labor Force Participation (FRED:CIVPART): % of population in the labor force.

🟠 Oil Prices (FRED:DCOILWTICO): Monthly WTI crude oil prices.

🟡 10Y Real Yield (FRED:DFII10): Inflation-adjusted yield on 10-year Treasuries.

🔵 Symbol Price: Optionally overlays the charted asset’s price, rescaled.

Historical Crashes

The dashboard highlights 10 major U.S. market crashes, including 1929, 2000, and 2008, with labeled time spans for quick context.

Era Classification

Six macroeconomic eras based on Deutsche Bank’s Long-Term Asset Return Study (2020) are shaded with background color. Each era reflects dominant economic regimes—globalization, wars, monetary systems, inflationary cycles, and current geopolitical disorder.

Best Use Cases

✅ Long-term macro investors studying structural market behavior

✅ Educators and analysts explaining economic transitions

✅ Portfolio managers aligning strategy with macroeconomic phases

✅ Traders using history for cycle timing and risk assessment

Technical Notes

Designed for monthly timeframe, though it works on weekly.

Uses close price and standard request.security calls for consistency.

Max labels/lines configured for broader history (from 1860s to present).

All plotted series are rescaled manually for better visibility.

Originality

This indicator is original and not derived from built-in or boilerplate code. It combines multiple economic dimensions and market history into one interactive chart, helping users frame today's markets in a broader structural context.

Log Regression OscillatorThe Log Regression Oscillator transforms the logarithmic regression curves into an easy-to-interpret oscillator that displays potential cycle tops/bottoms.

🔶 USAGE

Calculating the logarithmic regression of long-term swings can help show future tops/bottoms. The relationship between previous swing points is calculated and projected further. The calculated levels are directly associated with swing points, which means every swing point will change the calculation. Importantly, all levels will be updated through all bars when a new swing is detected.

The "Log Regression Oscillator" transforms the calculated levels, where the top level is regarded as 100 and the bottom level as 0. The price values are displayed in between and calculated as a ratio between the top and bottom, resulting in a clear view of where the price is situated.

The main picture contains the Logarithmic Regression Alternative on the chart to compare with this published script.

Included are the levels 30 and 70. In the example of Bitcoin, previous cycles showed a similar pattern: the bullish parabolic was halfway when the oscillator passed the 30-level, and the top was very near when passing the 70-level.

🔹 Proactive

A "Proactive" option is included, which ensures immediate calculations of tentative unconfirmed swings.

Instead of waiting 300 bars for confirmation, the "Proactive" mode will display a gray-white dot (not confirmed swing) and add the unconfirmed Swing value to the calculation.

The above example shows that the "Calculated Values" of the potential future top and bottom are adjusted, including the provisional swing.

When the swing is confirmed, the calculations are again adjusted, showing a red dot (confirmed top swing) or a green dot (confirmed bottom swing).

🔹 Dashboard

When less than two swings are available (top/bottom), this will be shown in the dashboard.

The user can lower the "Threshold" value or switch to a lower timeframe.

🔹 Notes

Logarithmic regression is typically used to model situations where growth or decay accelerates rapidly at first and then slows over time, meaning some symbols/tickers will fit better than others.

Since the logarithmic regression depends on swing values, each new value will change the calculation. A well-fitted model could not fit anymore in the future.

Users have to check the validity of swings; for example, if the direction of swings is downwards, then the dataset is not fitted for logarithmic regression.

In the example above, the "Threshold" is lowered. However, the calculated levels are unreliable due to the swings, which do not fit the model well.

Here, the combination of downward bottom swings and price accelerates slower at first and faster recently, resulting in a non-fit for the logarithmic regression model.

Note the price value (white line) is bound to a limit of 150 (upwards) and -150 (down)

In short, logarithmic regression is best used when there are enough tops/bottoms, and all tops are around 100, and all bottoms around 0.

Also, note that this indicator has been developed for a daily (or higher) timeframe chart.

🔶 DETAILS

In mathematics, the dot product or scalar product is an algebraic operation that takes two equal-length sequences of numbers (arrays) and returns a single number, the sum of the products of the corresponding entries of the two sequences of numbers.

The usual way is to loop through both arrays and sum the products.

In this case, the two arrays are transformed into a matrix, wherein in one matrix, a single column is filled with the first array values, and in the second matrix, a single row is filled with the second array values.

After this, the function matrix.mult() returns a new matrix resulting from the product between the matrices m1 and m2.

Then, the matrix.eigenvalues() function transforms this matrix into an array, where the array.sum() function finally returns the sum of the array's elements, which is the dot product.

dot(x, y)=>

if x.size() > 1 and y.size() > 1

m1 = matrix.new()

m2 = matrix.new()

m1.add_col(m1.columns(), y)

m2.add_row(m2.rows (), x)

m1.mult (m2)

.eigenvalues()

.sum()

🔶 SETTINGS

Threshold: Period used for the swing detection, with higher values returning longer-term Swing Levels.

Proactive: Tentative Swings are included with this setting enabled.

Style: Color Settings

Dashboard: Toggle, "Location" and "Text Size"

Altcoin Relative Macro StrengthAltcoin Relative Macro Strength

Overview

The Altcoin Relative Macro Strength indicator measures the altcoin market's price performance relative to global macroeconomic conditions. By comparing TOTAL3ES (total altcoin market capitalization excluding Bitcoin, Ethereum and stable coins) against a composite macro trend, the indicator identifies periods of relative overvaluation and undervaluation.

Methodology

Global Macro Trend Calculation:

The macro trend synthesizes three primary components:

- ISM PMI – A proxy for the business cycle phase

- Global Liquidity – An aggregate measure of major central bank balance sheets and broad money supply

- IWM (Russell 2000) – Small-cap equity exposure, reflecting risk-on/risk-off market sentiment

Global Liquidity is calculated as:

Fed Balance Sheet - Reverse Repo - Treasury General Account + U.S. M2 + China M2

The final Global Macro Trend is:

ISM PMI × Global Liquidity × IWM

Theoretical Framework:

The global macro trend integrates liquidity expansion/contraction with business cycle dynamics and small-cap equity performance. The inclusion of IWM reflects altcoins' tendency to behave as high-beta risk assets, exhibiting sensitivity similar to small-cap equities. This composite exhibits strong directional correlation with altcoin market movements, capturing the risk-on/risk-off dynamics that drive altcoin performance.

Interpretation

Primary Signal:

The histogram displays the rolling percentage change of TOTAL3ES relative to the global macro trend (default: 21-period average). Positive divergence indicates altcoins are outperforming macro conditions; negative divergence suggests underperformance relative to the underlying economic and risk environment.

Data Tables:

Alts/Macro Change – Percentage deviation of the altcoin market's average value from the Global Macro Trend's average over the specified period

Macro Trend – Directional assessment of the macro trend based on slope and trend agreement:

🔵 BULLISH ▲ – Positive slope with upward trend

⚪ NEUTRAL → – Slope and trend direction disagree

🟣 BEARISH ▼ – Negative slope with downward trend

Macro Slope – Percentage rate of change in the global macro trend

Altcoin Valuation – Relative valuation category based on TOTAL3/Macro deviation:

🟢 Extreme Discount / Deep Discount / Discount

🟡 Fair Value

🔴 Premium / Large Premium / Extreme Premium

TOTAL3ES Mcap – Current total altcoin market capitalization (in billions)

Visual Components:

📊 Histogram: Alts/Macro Change

🟢 Green = Positive deviation (altcoins outperforming)

🔴 Red = Negative deviation (altcoins underperforming)

📈 Macro Slope Line

Color-coded to match trend assessment

Scaled for visibility (adjustable in settings)

Application

This indicator is designed to identify mean reversion opportunities by highlighting periods when the altcoin market materially diverges from fundamental macro and risk conditions. Extreme positive values may indicate overvaluation; extreme negative values may signal undervaluation relative to the prevailing economic and risk appetite backdrop.

Strategy Considerations:

- Identify extremes: Look for periods when the histogram reaches elevated positive or negative levels

- Assess valuation: Use the Altcoin Valuation reading to gauge relative over/undervaluation

Confirm with risk sentiment: Check whether macro conditions and risk appetite support or contradict current price levels

- Mean reversion: Consider that significant deviations from trend historically tend to revert

Note: This indicator identifies relative valuation based on macro conditions and risk sentiment—it does not predict price direction or timing.

Settings

Lookback Period – 21 bars (default) – Number of bars for calculating rolling averages

Macro Slope Scale – 3.0 (default) – Multiplier for macro slope line visibility

BTC - VERI - Valuation & Entity Ratio IndexVERI: Valuation & Entity Ratio IndexObservation-only.

Data: IntoTheBlock.

Overview & Philosophy

The name VERI is derived from the Latin Veritas (Truth). In a crypto market often driven by deceptive speculative noise, this indicator seeks to establish the "On-Chain Truth" of a price trend.

It operates on the thesis that price action is only sustainable when verified by high-conviction capital flows.VERI is a fundamental composite oscillator that fuses Entity Behavior (Who is holding?) with Network Valuation (Is the price fair?) to identify Bitcoin market cycle extremes.

The "Alpha"

Why this Composite stands out: on-chain metrics often tell only half the story.

MVRV tells you if the price is cheap, but not if anyone is actually buying.

Whale Activity tells you if large players are moving, but not if they are accumulating at a value discount.

VERI fuses these two dimensions into a single Z-Score. It identifies the rare, high-probability moments where Smart Money Conviction intersects with Deep Value.

Methodology

The Mathematics of VERI: The indicator constructs a composite index using three fundamental metrics from IntoTheBlock:

The "Who" (Entity Ratio) : We calculate the flow ratio between Whales (>1% supply holders) and Retail (<0.1% supply holders). A rising ratio indicates supply is transferring from weak hands to strong hands.

The "Why" (Valuation Multiplier) : We utilize the MVRV (Market Value to Realized Value) ratio. To isolate value opportunities, we use the inverse (1 / MVRV).

The Fusion : These factors are multiplied to create the raw VERI index.

Normalization & Inversion

We apply a rolling Z-Score (standard deviation from the mean) and invert the result.

How to Interpret the Indicator

Because the output is inverted, the visual logic matches price action intuitively:

🟥 Distribution Zone (High Values > 1.5):

The Signal: "Low Conviction Overvaluation."

Context: The price is historically expensive relative to the cost basis (High MVRV), and Whales are distributing coins to Retail.Implication: Historically precedes macro tops or deep corrections.

🟩 Accumulation Zone (Low Values < -1.5):

The Signal: "High Conviction Undervaluation."Context: The price is historically cheap (Low MVRV), and Whales are aggressively accumulating relative to Retail.

Implication: Historically precedes macro bottoms and generational entry points.

Zero Line : Represents the historical baseline. A crossover of the zero line often confirms a regime shift (e.g., from Bear to Bull).

Visual Guide & Features

Dynamic Coloring: The line turns Red in the Distribution Zone, Blue in the Accumulation Zone, and Orange during neutral trends.

Zone Labels: Static labels are pinned to the left side of the chart for immediate context.

The "Data Check" Monitor (Status Table): Since this indicator relies on third-party fundamental data, we have included a diagnostic table in the bottom-right corner.

Data Check Monitor Guide

STATUS: LIVE (Green): The indicator is functioning correctly. All data feeds (Whales, Retail, MVRV) are being retrieved successfully.

STATUS: WAIT (Red): The indicator cannot retrieve data. This might happen for some reasons, e.g. your TradingView plan may not support IntoTheBlock integration.

Settings

Lookback Period (Default: 365): The window used for Z-Score normalization. We use a full year to smooth out seasonal volatility.

Smoothing (Default: 7): A 7-day smoothing is applied to the signal to filter out daily noise.

Zone Thresholds: Users can customize the specific Z-Score levels for the Distribution and Accumulation bands.

Disclaimer

This script is for research and educational purposes only. It uses historical on-chain data to visualize market structure and does not constitute financial advice. Past performance of whale entities does not guarantee future results.

Tags

bitcoin, btc, on-chain, mvrv, whales, valuation, fundamentals, cycle, oscillator, veri

BTC Energy + HR + Longs + M2

BTC Energy Ratio + Hashrate + Longs + M2

The #1 Bitcoin Macro Weapon on TradingView 🚀🔥

If you’re tired of getting chopped by fakeouts, ETF noise, and Twitter hopium — this is the one chart that finally puts you on the right side of every major move.

What you’re looking at:

Orange line → Bitcoin priced in real-world mining energy (Oil × Gas + Uranium × Coal) × 1000

→ The true fundamental floor of BTC

Blue line → Scaled hashrate trend (miner strength & capex lag)

Green line → Bitfinex longs EMA (leveraged bull sentiment)

Purple line → Global M2 money supply (US+EU+CN+JP) with 10-week lead (the liquidity wave BTC rides)

Why this indicator prints money:

Most tools react to price.

This one predicts where price is going based on energy, miners, leverage, and liquidity — the only four things that actually drive Bitcoin long-term.

It has nailed:

2022 bottom at ~924 📉

2024 breakout above 12,336 🚀

2025 top at 17,280 🏔️

And right now it’s flashing generational accumulation at ~11,500 (Nov 2025)

13 permanent levels with right-side labels — no guessing what anything means:

20,000 → 2021 Bull ATH

17,280 → 2025 ATH

15,000 → 2024 High Resist

14,000 → Overvalued Zone

13,000 → 2024 Breakout

12,336 → Bull/Bear Line (the most important level)

12,000 → 2024 Volume POC

10,930 → Key Support 2024

9,800 → Strong Buy Fib

8,000 → Deep Support 2023

6,000 → 2021 Mid-Cycle

4,500 → 2023 Accum Low

924 → 2022 Bear Low

Live dashboard tells you exactly what to do — no thinking required:

Current ratio (updates live)

Hashrate + 24H %

Longs trend

Risk Mode → Orange vs Hashrate (RISK ON / RISK OFF)

180-day correlation

RSI

13-tier Zone + SIGNAL (STRONG BUY / ACCUMULATE / HOLD / DISTRIBUTE / EXTREME SELL)

Dead-simple rules that actually work:

Weekly timeframe = cleanest view

Blue peaking + orange holding support → miner pain = next leg up

Green spiking + orange failing → overcrowded longs = trim

Purple rising → liquidity coming in = ride the wave

Risk Mode = RISK OFF → price is cheap vs miners → buy

Set these 3 alerts and walk away:

Ratio > 12,336 → Bull confirmed → add

Ratio > 14,000 → Start scaling out

Ratio < 9,800 → Generational buy → back up the truck

No repainting • Fully open-source • Forced daily data • Works on any TF

Energy is the only real backing Bitcoin has.

Hashrate lag is the best leading indicator.

Longs show greed.

M2 is the tide.

This chart combines all four — and right now it’s screaming ACCUMULATE.

Load it. Trust it.

Stop trading hope. Start trading reality.

DYOR • NFA • For entertainment purposes only 😎

#bitcoin #macro #energy #hashrate #m2 #cycle #riskon #riskoff

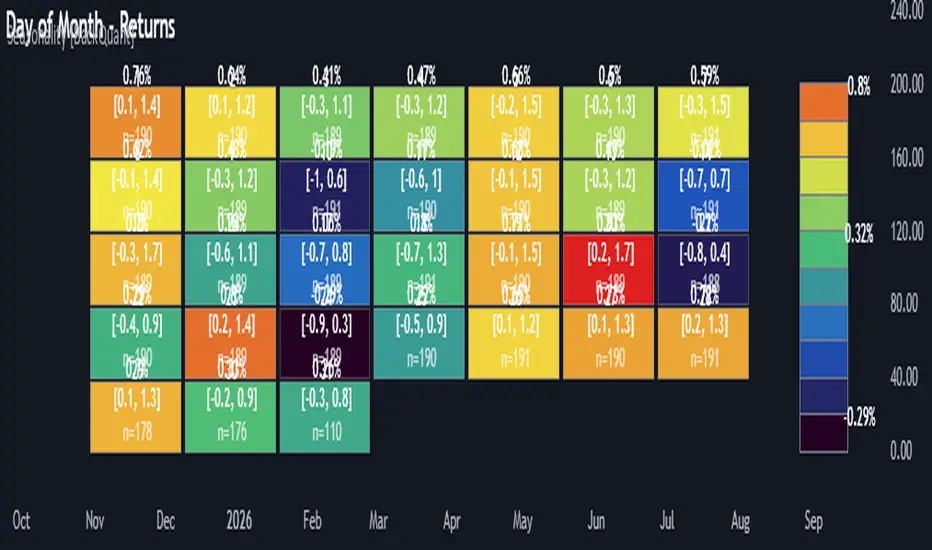

Multi-Mode Seasonality Map [BackQuant]Multi-Mode Seasonality Map

A fast, visual way to expose repeatable calendar patterns in returns, volatility, volume, and range across multiple granularities (Day of Week, Day of Month, Hour of Day, Week of Month). Built for idea generation, regime context, and execution timing.

What is “seasonality” in markets?

Seasonality refers to statistically repeatable patterns tied to the calendar or clock, rather than to price levels. Examples include specific weekdays tending to be stronger, certain hours showing higher realized volatility, or month-end flow boosting volumes. This tool measures those effects directly on your charted symbol.

Why seasonality matters

It’s orthogonal alpha: timing edges independent of price structure that can complement trend, mean reversion, or flow-based setups.

It frames expectations: when a session typically runs hot or cold, you size and pace risk accordingly.

It improves execution: entering during historically favorable windows, avoiding historically noisy windows.

It clarifies context: separating normal “calendar noise” from true anomaly helps avoid overreacting to routine moves.

How traders use seasonality in practice

Timing entries/exits : If Tuesday morning is historically weak for this asset, a mean-reversion buyer may wait for that drift to complete before entering.

Sizing & stops : If 13:00–15:00 shows elevated volatility, widen stops or reduce size to maintain constant risk.

Session playbooks : Build repeatable routines around the hours/days that consistently drive PnL.

Portfolio rotation : Compare seasonal edges across assets to schedule focus and deploy attention where the calendar favors you.

Why Day-of-Week (DOW) can be especially helpful

Flows cluster by weekday (ETF creations/redemptions, options hedging cadence, futures roll patterns, macro data releases), so DOW often encodes a stable micro-structure signal.

Desk behavior and liquidity provision differ by weekday, impacting realized range and slippage.

DOW is simple to operationalize: easy rules like “fade Monday afternoon chop” or “press Thursday trend extension” can be tested and enforced.

What this indicator does

Multi-mode heatmaps : Switch between Day of Week, Day of Month, Hour of Day, Week of Month .

Metric selection : Analyze Returns , Volatility ((high-low)/open), Volume (vs 20-bar average), or Range (vs 20-bar average).

Confidence intervals : Per cell, compute mean, standard deviation, and a z-based CI at your chosen confidence level.

Sample guards : Enforce a minimum sample size so thin data doesn’t mislead.

Readable map : Color palettes, value labels, sample size, and an optional legend for fast interpretation.

Scoreboard : Optional table highlights best/worst DOW and today’s seasonality with CI and a simple “edge” tag.

How it’s calculated (under the hood)

Per bar, compute the chosen metric (return, vol, volume %, or range %) over your lookback window.

Bucket that metric into the active calendar bin (e.g., Tuesday, the 15th, 10:00 hour, or Week-2 of month).

For each bin, accumulate sum , sum of squares , and count , then at render compute mean , std dev , and confidence interval .

Color scale normalizes to the observed min/max of eligible bins (those meeting the minimum sample size).

How to read the heatmap

Color : Greener/warmer typically implies higher mean value for the chosen metric; cooler implies lower.

Value label : The center number is the bin’s mean (e.g., average % return for Tuesdays).

Confidence bracket : Optional “ ” shows the CI for the mean, helping you gauge stability.

n = sample size : More samples = more reliability. Treat small-n bins with skepticism.

Suggested workflows

Pick the lens : Start with Analysis Type = Returns , Heatmap View = Day of Week , lookback ≈ 252 trading days . Note the best/worst weekdays and their CI width.

Sanity-check volatility : Switch to Volatility to see which bins carry the most realized range. Use that to plan stop width and trade pacing.

Check liquidity proxy : Flip to Volume , identify thin vs thick windows. Execute risk in thicker windows to reduce slippage.

Drill to intraday : Use Hour of Day to reveal opening bursts, lunchtime lulls, and closing ramps. Combine with your main strategy to schedule entries.

Calendar nuance : Inspect Week of Month and Day of Month for end-of-month, options-cycle, or data-release effects.

Codify rules : Translate stable edges into rules like “no fresh risk during bottom-quartile hours” or “scale entries during top-quartile hours.”

Parameter guidance

Analysis Period (Days) : 252 for a one-year view. Shorten (100–150) to emphasize the current regime; lengthen (500+) for long-memory effects.

Heatmap View : Start with DOW for robustness, then refine with Hour-of-Day for your execution window.

Confidence Level : 95% is standard; use 90% if you want wider coverage with fewer false “insufficient data” bins.

Min Sample Size : 10–20 helps filter noise. For Hour-of-Day on higher timeframes, consider lowering if your dataset is small.

Color Scheme : Choose a palette with good mid-tone contrast (e.g., Red-Green or Viridis) for quick thresholding.

Interpreting common patterns

Return-positive but low-vol bins : Favorable drift windows for passive adds or tight-stop trend continuation.

Return-flat but high-vol bins : Opportunity for mean reversion or breakout scalping, but manage risk accordingly.

High-volume bins : Better expected execution quality; schedule size here if slippage matters.

Wide CI : Edge is unstable or sample is thin; treat as exploratory until more data accumulates.

Best practices

Revalidate after regime shifts (new macro cycle, liquidity regime change, major exchange microstructure updates).

Use multiple lenses: DOW to find the day, then Hour-of-Day to refine the entry window.

Combine with your core setup signals; treat seasonality as a filter or weight, not a standalone trigger.

Test across assets/timeframes—edges are instrument-specific and may not transfer 1:1.

Limitations & notes

History-dependent: short histories or sparse intraday data reduce reliability.

Not causal: a hot Tuesday doesn’t guarantee future Tuesday strength; treat as probabilistic bias.

Aggregation bias: changing session hours or symbol migrations can distort older samples.

CI is z-approximate: good for fast triage, not a substitute for full hypothesis testing.

Quick setup

Use Returns + Day of Week + 252d to get a clean yearly map of weekday edge.

Flip to Hour of Day on intraday charts to schedule precise entries/exits.

Keep Show Values and Confidence Intervals on while you calibrate; hide later for a clean visual.

The Multi-Mode Seasonality Map helps you convert the calendar from an afterthought into a quantitative edge, surfacing when an asset tends to move, expand, or stay quiet—so you can plan, size, and execute with intent.

The Mayan CalendarThis indicator displays the current date in the Mayan Calendar, based on real-time UTC time. It calculates and presents:

🌀 Long Count (Baktun.Katun.Tun.Uinal.Kin) – A linear count of days since the Mayan epoch (August 11, 3114 BCE).

🔮 Tzolk'in Date – A 260-day sacred cycle combining a number (1–13) and one of 20 day names (e.g., 4 Ajaw).

🌾 Haab' Date – A 365-day civil cycle divided into 18 months of 20 days + 5 "nameless" days (Wayeb').

The calculations follow Smithsonian standards and align with the Maya Calendar Converter from the National Museum of the American Indian:

👉 maya.nmai.si.edu

The results are shown in a table overlay on your chart's top-right corner. This indicator is great for symbolic traders, astro enthusiasts, or anyone interested in ancient timekeeping systems woven into financial timeframes. Enjoy, time travelers! ⌛

Logarithmic Regression AlternativeLogarithmic regression is typically used to model situations where growth or decay accelerates rapidly at first and then slows over time. Bitcoin is a good example.

𝑦 = 𝑎 + 𝑏 * ln(𝑥)

With this logarithmic regression (log reg) formula 𝑦 (price) is calculated with constants 𝑎 and 𝑏, where 𝑥 is the bar_index .

Instead of using the sum of log x/y values, together with the dot product of log x/y and the sum of the square of log x-values, to calculate a and b, I wanted to see if it was possible to calculate a and b differently.

In this script, the log reg is calculated with several different assumed a & b values, after which the log reg level is compared to each Swing. The log reg, where all swings on average are closest to the level, produces the final 𝑎 & 𝑏 values used to display the levels.

🔶 USAGE

The script shows the calculated logarithmic regression value from historical swings, provided there are enough swings, the price pattern fits the log reg model, and previous swings are close to the calculated Top/Bottom levels.

When the price approaches one of the calculated Top or Bottom levels, these levels could act as potential cycle Top or Bottom.

Since the logarithmic regression depends on swing values, each new value will change the calculation. A well-fitted model could not fit anymore in the future.

Swings are based on Weekly bars. A Top Swing, for example, with Swing setting 30, is the highest value in 60 weeks. Thirty bars at the left and right of the Swing will be lower than the Top Swing. This means that a confirmation is triggered 30 weeks after the Swing. The period will be automatically multiplied by 7 on the daily chart, where 30 becomes 210 bars.

Please note that the goal of this script is not to show swings rapidly; it is meant to show the potential next cycle's Top/Bottom levels.

🔹 Multiple Levels

The script includes the option to display 3 Top/Bottom levels, which uses different values for the swing calculations.

Top: 'high', 'maximum open/close' or 'close'

Bottom: 'low', 'minimum open/close' or 'close'

These levels can be adjusted up/down with a percentage.

Lastly, an "Average" is included for each set, which will only be visible when "AVG" is enabled, together with both Top and Bottom levels.

🔹 Notes

Users have to check the validity of swings; the above example only uses 1 Top Swing for its calculations, making the Top level unreliable.

Here, 1 of the Bottom Swings is pretty far from the bottom level, changing the swing settings can give a more reliable bottom level where all swings are close to that level.

Note the display was set at "Logarithmic", it can just as well be shown as "Regular"

In the example below, the price evolution does not fit the logarithmic regression model, where growth should accelerate rapidly at first and then slows over time.

Please note that this script can only be used on a daily timeframe or higher; using it at a lower timeframe will show a warning. Also, it doesn't work with bar-replay.

🔶 DETAILS

The code gathers data from historical swings. At the last bar, all swings are calculated with different a and b values. The a and b values which results in the smallest difference between all swings and Top/Bottom levels become the final a and b values.

The ranges of a and b are between -20.000 to +20.000, which means a and b will have the values -20.000, -19.999, -19.998, -19.997, -19.996, ... -> +20.000.

As you can imagine, the number of calculations is enormous. Therefore, the calculation is split into parts, first very roughly and then very fine.

The first calculations are done between -20 and +20 (-20, -19, -18, ...), resulting in, for example, 4.

The next set of calculations is performed only around the previous result, in this case between 3 (4-1) and 5 (4+1), resulting in, for example, 3.9. The next set goes even more in detail, for example, between 3.8 (3.9-0.1) and 4.0 (3.9 + 0.1), and so on.

1) -20 -> +20 , then loop with step 1 (result (example): 4 )

2) 4 - 1 -> 4 +1 , then loop with step 0.1 (result (example): 3.9 )

3) 3.9 - 0.1 -> 3.9 +0.1 , then loop with step 0.01 (result (example): 3.93 )

4) 3.93 - 0.01 -> 3.93 +0.01, then loop with step 0.001 (result (example): 3.928)

This ensures complicated calculations with less effort.

These calculations are done at the last bar, where the levels are displayed, which means you can see different results when a new swing is found.

Also, note that this indicator has been developed for a daily (or higher) timeframe chart.

🔶 SETTINGS

Three sets

High/Low

• color setting

• Swing Length settings for 'High' & 'Low'

• % adjustment for 'High' & 'Low'

• AVG: shows average (when both 'High' and 'Low' are enabled)

Max/Min (maximum open/close, minimum open/close)

• color setting

• Swing Length settings for 'Max' & 'Min'

• % adjustment for 'Max' & 'Min'

• AVG: shows average (when both 'Max' and 'Min' are enabled)

Close H/Close L (close Top/Bottom level)

• color setting

• Swing Length settings for 'Close H' & 'Close L'

• % adjustment for 'Close H' & 'Close L'

• AVG: shows average (when both 'Close H' and 'Close L' are enabled)

Show Dashboard, including Top/Bottom levels of the desired source and calculated a and b values.

Show Swings + Dot size

Intellect_city - Halvings Bitcoin CycleWhat is halving?

The halving timer shows when the next Bitcoin halving will occur, as well as the dates of past halvings. This event occurs every 210,000 blocks, which is approximately every 4 years. Halving reduces the emission reward by half. The original Bitcoin reward was 50 BTC per block found.

Why is halving necessary?

Halving allows you to maintain an algorithmically specified emission level. Anyone can verify that no more than 21 million bitcoins can be issued using this algorithm. Moreover, everyone can see how much was issued earlier, at what speed the emission is happening now, and how many bitcoins remain to be mined in the future. Even a sharp increase or decrease in mining capacity will not significantly affect this process. In this case, during the next difficulty recalculation, which occurs every 2014 blocks, the mining difficulty will be recalculated so that blocks are still found approximately once every ten minutes.

How does halving work in Bitcoin blocks?

The miner who collects the block adds a so-called coinbase transaction. This transaction has no entry, only exit with the receipt of emission coins to your address. If the miner's block wins, then the entire network will consider these coins to have been obtained through legitimate means. The maximum reward size is determined by the algorithm; the miner can specify the maximum reward size for the current period or less. If he puts the reward higher than possible, the network will reject such a block and the miner will not receive anything. After each halving, miners have to halve the reward they assign to themselves, otherwise their blocks will be rejected and will not make it to the main branch of the blockchain.

The impact of halving on the price of Bitcoin

It is believed that with constant demand, a halving of supply should double the value of the asset. In practice, the market knows when the halving will occur and prepares for this event in advance. Typically, the Bitcoin rate begins to rise about six months before the halving, and during the halving itself it does not change much. On average for past periods, the upper peak of the rate can be observed more than a year after the halving. It is almost impossible to predict future periods because, in addition to the reduction in emissions, many other factors influence the exchange rate. For example, major hacks or bankruptcies of crypto companies, the situation on the stock market, manipulation of “whales,” or changes in legislative regulation.

---------------------------------------------

Table - Past and future Bitcoin halvings:

---------------------------------------------

Date: Number of blocks: Award:

0 - 03-01-2009 - 0 block - 50 BTC

1 - 28-11-2012 - 210000 block - 25 BTC

2 - 09-07-2016 - 420000 block - 12.5 BTC

3 - 11-05-2020 - 630000 block - 6.25 BTC

4 - 20-04-2024 - 840000 block - 3.125 BTC

5 - 24-03-2028 - 1050000 block - 1.5625 BTC

6 - 26-02-2032 - 1260000 block - 0.78125 BTC

7 - 30-01-2036 - 1470000 block - 0.390625 BTC

8 - 03-01-2040 - 1680000 block - 0.1953125 BTC

9 - 07-12-2043 - 1890000 block - 0.09765625 BTC

10 - 10-11-2047 - 2100000 block - 0.04882813 BTC

11 - 14-10-2051 - 2310000 block - 0.02441406 BTC

12 - 17-09-2055 - 2520000 block - 0.01220703 BTC

13 - 21-08-2059 - 2730000 block - 0.00610352 BTC

14 - 25-07-2063 - 2940000 block - 0.00305176 BTC

15 - 28-06-2067 - 3150000 block - 0.00152588 BTC

16 - 01-06-2071 - 3360000 block - 0.00076294 BTC

17 - 05-05-2075 - 3570000 block - 0.00038147 BTC

18 - 08-04-2079 - 3780000 block - 0.00019073 BTC

19 - 12-03-2083 - 3990000 block - 0.00009537 BTC

20 - 13-02-2087 - 4200000 block - 0.00004768 BTC

21 - 17-01-2091 - 4410000 block - 0.00002384 BTC

22 - 21-12-2094 - 4620000 block - 0.00001192 BTC

23 - 24-11-2098 - 4830000 block - 0.00000596 BTC

24 - 29-10-2102 - 5040000 block - 0.00000298 BTC

25 - 02-10-2106 - 5250000 block - 0.00000149 BTC

26 - 05-09-2110 - 5460000 block - 0.00000075 BTC

27 - 09-08-2114 - 5670000 block - 0.00000037 BTC

28 - 13-07-2118 - 5880000 block - 0.00000019 BTC

29 - 16-06-2122 - 6090000 block - 0.00000009 BTC

30 - 20-05-2126 - 6300000 block - 0.00000005 BTC

31 - 23-04-2130 - 6510000 block - 0.00000002 BTC

32 - 27-03-2134 - 6720000 block - 0.00000001 BTC

90cycle @joshuuu90 minute cycle is a concept about certain time windows of the day.

This indicator has two different options. One uses the 90 minute cycle times mentioned by traderdaye, the other uses the cls operational times split up into 90 minutes session.

e.g. we can often see a fake move happening in the 90 minute window between 2.30am and 4am ny time.

The indicator draws vertical lines at the start/end of each session and the user is able to only display certain sessions (asia, london, new york am and pm)

For the traderdayes option, the indicator also counts the windows from 1 to 4 and calls them q1,q2,q3,q4 (q-quarter)

⚠️ Open Source ⚠️

Coders and TV users are authorized to copy this code base, but a paid distribution is prohibited. A mention to the original author is expected, and appreciated.

⚠️ Terms and Conditions ⚠️

This financial tool is for educational purposes only and not financial advice. Users assume responsibility for decisions made based on the tool's information. Past performance doesn't guarantee future results. By using this tool, users agree to these terms.

inverse_fisher_transform_adaptive_stochastic█ Description

The indicator is the implementation of inverse fisher transform an indicator transform of the adaptive stochastic (dominant cycle), as in the Cycle Analytics for Trader pg. 198 (John F. Ehlers). Indicator transformation in brief means reshaping the indicator to be more interpretable. The inverse fisher transform is achieved by compressing values near the extremes many extraneous and irrelevant wiggles are removed from the indicator, as cited.

█ Inverse Fisher Transform

input = 2*(adaptive_stoc - .5)

output = e(2*k*input) -1 / e(2*k*input) +1

█ Feature:

iFish i.e. output value

trigger i.e. previous 1 bar of iFish * 0.90

if iFish crosses above the trigger, consider a buy indicated with the green line

while, iFish crosses below the trigger, consider a sell indicate by the red line

in addition iFish needs to be greater than the previous iFish

timing marketIntraday time cycle . it is valid for nifty and banknifty .just add this on daily basis . ignore previous day data

BTC Pi MultipleThe Pi Multiple is a function of 350 and 111-day moving average. When both intersect and the 111-day MA crosses above, it has historically coincided with a cycle top with a 3-day margin.

With the Pi Multiple, this intersection is visible when the line crosses zero upwards.

The indicator is called the Pi Multiple because 350/111 is close to Pi. It is based on the Pi Cycle Top Indicator developed by Philip Swift and has been modified for better readability by David Bertho.

Cycle Dynamic Composite AverageThis MA uses the formula of simple cycle indicator to find 2 cycles periods length's .

The CDCA is the result of 8 different ma to control and filter the price. The regression line is the signal , don t need to look candles, but just the cross between MA and reg lin.

VB Sigma Smart Momentum IndicatorVB Sigma Smart Momentum Indicator (VBSSMI)

The VBSSMI provides a consolidated decision-support framework that surfaces market participation, trend integrity, and liquidity conditions in a single visual environment. The tool integrates four analytical modules: MCDX Flow Mapping, Donchian Regime Layers, Banker Flow Modeling, and Chop Zone Trend Classification. Together, these components convert raw price movement into an actionable interpretation of who is in control, whether momentum is durable, and what phase the instrument is currently cycling through.

How to Use the Indicator (Practical Workflow)

1. Start with Institutional / Banker Flow (Pink/Red/Yellow/Green Candles)

This is the primary signal layer. It tells you when high-capacity participants are increasing, reducing, or reversing risk.

Yellow Candle — Entry Bias

Indicates a potential institutional initiation when their trend metric crosses above their accumulation threshold.

Operational signal: instrument enters “monitor for entry” state.

Green Candle — Accumulation State

Fund-trend > bullbearline.

Operational signal: trend integrity improving; pullbacks are generally buyable.

White Candle — Distribution / Cooling

Fund-trend weakening but not broken.

Operational signal: tighten stops; momentum deteriorating.

Red Candle — Exit / Trend Failure

Fund-trend < bullbearline.

Operational signal: momentum regime invalidated; avoid long risk.

Blue Candle — Weak Rebound

A temporary uptick within broader weakness.

Operational signal: do not mistake this for a durable reversal.

2. Validate alignment with Flow Chips (Retail / Trader / Institutional)

These three flow columns (MCDX layers) answer: who is actually participating?

Retailer Flow (Locked Chips – Green)

High values imply retail conviction, often late-cycle.

Good for confirming trend strength, not timing entries.

Trader Zone Flow (Float Chips – Yellow)

When this spikes, volatility and tactical positioning increase.

Signal: strong short-term engagement, supports breakout/trend continuation.

Institutional Flow (Profitable Chips – Red/Pink)

This is the “true north” of momentum.

Rising values = institutions controlling price discovery.

Signal: long setups have statistical tailwind.

The operational guidance is straightforward:

Institutional Flow > Trader Flow > Retail Flow

is the healthiest configuration for sustainable upside momentum.

3. Confirm Breakout / Breakdown Conditions with Donchian Regime Columns

The vertical Donchian stack illustrates trend regime in a time-compressed format.

Bright Blue/Cyan

Structure expanding upward (breakout cluster).

Dark Purple/Red

Structure breaking downward (breakdown cluster).

Mixed Columns

Transitional or indecisive conditions.

Interpret it as a “momentum backdrop”:

If Donchian columns and Banker Flow candles disagree, avoid entries.

4. Consult the Chop Zone Strip Before Committing Capital

The Chop Zone uses EMA angle to determine whether the market is trending or congested.

Greens/Blues → Trend phase (favorable environment for continuation trades).

Yellows/Oranges/Reds → High noise probability; expect false signals.

Operationally:

Never enter breakout setups during yellow/orange/red chop.

5. Final Decision Framework (Checklist)

A long setup typically requires:

Green or Yellow Banker Flow Candle

Institutional Flow rising

Donchian columns in bullish regime colors

Chop Zone in a trend color (not red/yellow/orange)

A short setup is the exact inverse.

Recommended Use Cases

Momentum trading

Swing position building

Institutional-flow confirmation

Trend-filtering before deploying breakout systems

Screening for strong/weak symbols in multi-asset rotation strategies

Election Year GainsShows the yearly gains of the chart in U.S. Election years.

Use the options to turn on other years in the cycle.

For use with the 12M chart.

Will show non-sensical data with other intervals.

Titan V40.0 Optimal Portfolio ManagerTitan V40.0 Optimal Portfolio Manager

This script serves as a complete portfolio management ecosystem designed to professionalize your entire investment process. It is built to replace emotional guesswork with a structured, mathematically driven workflow that guides you from discovering broad market trends to calculating the exact dollar amount you should allocate to each asset. Whether you are managing a crypto portfolio, a stock watchlist, or a diversified mix of assets, Titan V40.0 acts as your personal "Portfolio Architect," helping you build a scientifically weighted portfolio that adapts dynamically to market conditions.

How the 4-Step Workflow Operates

The system is organized into four distinct operational modes that you cycle through as you analyze the market. You simply change the "Active Workflow Step" in the settings to progress through the analysis.

You begin with the Macro Scout, which is designed to show you where capital is flowing in the broader economy. This mode scans 15 major sectors—ranging from Technology and Energy to Gold and Crypto—and ranks them by relative strength. This high-level view allows you to instantly identify which sectors are leading the market and which are lagging, ensuring you are always fishing in the right pond.

Once you have identified a leading sector, you move to the Deep Dive mode. This tool allows you to select a specific target sector, such as Semiconductors or Precious Metals, and instantly scans a pre-loaded internal library of the top 20 assets within that industry. It ranks these assets based on performance and safety, allowing you to quickly cherry-pick the top three to five winners that are outperforming their peers.

After identifying your potential winners, you proceed to the Favorites Monitor. This step allows you to build a focused "bench" of your top candidates. by inputting your chosen winners from the Deep Dive into the Favorites slots in the settings, you create a dedicated watchlist. This separates the signal from the noise, letting you monitor the Buy, Hold, or Sell status of your specific targets in real-time without the distraction of the rest of the market.

The final and most powerful phase is Reallocation. This is where the script functions as a true Portfolio Architect. In this step, you input your current portfolio holdings alongside your new favorites. The script treats this combined list as a single "unified pool" of candidates, scoring every asset purely on its current merit regardless of whether you already own it or not. It then generates a clear Action Plan. If an asset has a strong trend and a high score, it issues a BUY or ADD signal with a specific target dollar amount based on your total equity. If an asset is stable but not a screaming buy, it issues a MAINTAIN signal to hold your position. If a trend has broken, it issues an EXIT signal, advising you to cut the position to zero to protect capital.

Smart Logic Under the Hood

What makes Titan V40.0 unique is its "Regime Awareness." The system automatically detects if the broad market is in a Risk-On (Bull) or Risk-Off (Bear) state using a global proxy like SPY or BTC. In a Risk-On regime, the system is aggressive, allowing capital to be fully deployed into high-performing assets. In a Risk-Off regime, the system automatically forces a "Cash Drag," mathematically reducing allocation targets to keep a larger portion of your portfolio in cash for safety.

Furthermore, the scoring engine uses Risk-Adjusted math. It does not simply chase high returns; it actively penalizes volatility. A stock that is rising steadily will be ranked higher than a stock that is wildly erratic, even if their total returns are similar. This ensures that your "Maintenance" positions—assets you hold that are doing okay but not spectacular—still receive a proper allocation target, preventing you from being forced to sell good assets prematurely while ensuring you are effectively positioned for the highest probability of return.

US Recessions - ShadingThis indicator shades the chart background during every U.S. recession as dated by the National Bureau of Economic Research (NBER). Recessions are defined using NBER’s business cycle peak-to-trough months, and the script shades from the peak month through the trough month (inclusive) using monthly boundaries.

What it does

* Applies a shaded overlay on your chart **only during recession periods**.

* Works on any symbol and any timeframe (crypto, equities, FX, commodities, bonds, indices).

* Includes options to:

- Toggle shading on/off

- Choose your preferred shading colour

- Adjust transparency for readability

Why this overlay is important for analysing any asset class

Even if you trade or invest in assets that aren’t directly tied to U.S. GDP (like crypto or commodities), U.S. recessions often coincide with major shifts in:

-Risk appetite (risk-on vs risk-off behaviour)

-Liquidity conditions (credit availability, financial stress)

-Interest-rate expectations and central bank response

-Earnings expectations and corporate defaults

-Volatility regimes (large, sustained changes in volatility)

Having recession shading directly on the price chart helps you quickly see whether price action is happening in a historically “normal” expansion environment, or in a macro regime where behaviour can change dramatically. This is particularly useful in a deeper analysis like comparing GOLD to SPX. This chart makes it clear how in recessions the S&P bleeds against Gold therefor making the concept more visual and better for understanding.

Of course this is just an example of how it can be used, there are plenty of other factors which can be overlayed like unemployment and interest rates for an even better understanding.

Please DM majordistribution.inc on Instagram for any info - FREE - NO Course

BTC - StableFlow: Pit-Stop & Refuel EngineBTC – StableFlow: Pit-Stop & Refuel Engine | RM

Strategic Context: The Institutional Gas Station In the high-speed race of the crypto markets, Stablecoins (USDT, USDC, DAI) represent the Fuel, and Bitcoin is the Race Car. Most traders only look at the car's speed (Price), but they ignore the gas tank. The StableFlow Engine is a telemetry dashboard designed to monitor the "Fuel Pressure" within the ecosystem, identifying exactly when the car is being refueled and when it is running on empty.

The Telemetry Logic: How to Read the Race

The indicator operates on a Relative Velocity model. We aren't just looking at how many Stablecoins exist; we are measuring the Acceleration of Stablecoin Market Cap relative to the Acceleration of BTC Price.

1. The Fuel Reservoir (The Histogram)

• Cyan Zones (Refuel): The gas station is open. Institutional "Dry Powder" is flowing into stables faster than it is being spent on BTC. The tank is filling up.

• Orange Zones (Exhaust): The "Overdrive." The car is driving faster than the gas can be pumped. Price is outperforming the stablecoin supply—this is unsustainable and usually precedes a stall.

2. Lap Transitions (The Grey Lines)

These vertical markers signify a Regime Shift . They trigger the moment the momentum crosses the zero-axis, visually distinguishing the transition between a "Net-Refueling" period and a "Net-Exhaustion" period. While not used as direct entry signals, they define the Macro Lap we are currently in.

Operational Playbook: The Pit-Stop Signals

We don't just buy because the tank is full; we buy when the car exits the pits and begins to accelerate. This is captured by our proprietary Pit-Stop Pips.

• Blue Pip (Pit-Stop Buy): Triggered when the Refuel momentum has peaked and is now rotating back into the market. The refuel is complete; the car is rejoining the race with a full tank.

• Red Pip (Exhaust Sell): Triggered when the price acceleration has overextended relative to its fuel source and begins to "roll over." The tank is near empty; time for a tactical pull-back.

Settings & Calibration: The Pit Wall Dashboard

Signal Mode & Logic The engine features a dual-mode signaling system to adapt to different market conditions (or your personal preferred logic):

• Consecutive Mode: Best for high-velocity trends. Fires a pip after n bars of momentum reversal (Default: 2 bars).

• Percentage (%) Mode: Best for structural fades. Fires a pip when the momentum retraces by a specific percentage (e.g., 15%) from its local peak, regardless of the bar count.

Recommended Calibration

While the engine is versatile across various timeframes, the Weekly (1W) chart is the preferred setting for identifying high-conviction macro signals. Lower timeframes provide tactical speed, but the 1W frame offers significantly cleaner signals by filtering out the daily market noise.

Weekly (1W) — The Macro Signal (Preferred): * Velocity Lookback: 20 | Smoothing: 5.

Peak Lookback: 25 (Represents roughly half a year of telemetry data). This is a good starting point for identifying major cycle rotations.

Daily (1D) — The Tactical Pulse: * Velocity Lookback: 20 | Smoothing: 5.

Peak Lookback: 25 (Represents one trading month of telemetry). Useful for active swing traders looking for entry/exit timing within an established macro trend.

Technical Documentation

Data Sourcing & Aggregation The script utilizes request.security to aggregate a "Big Three" Stablecoin Market Cap (USDT + USDC + DAI). This prevents "False Exhaustion" signals caused by capital simply migrating between different stablecoin assets.

Mathematical Foundation The core engine calculates the Rate of Change (ROC) for the Aggregate Stablecoin Supply and BTC Price over a synchronized lookback window.

Formula Logic: Fuel Pressure = EMA ( ROC(Stables) - ROC(BTC) )

The Pit-Stop Pips utilize a local peak-finding algorithm via ta.highest and ta.lowest within a rolling 25-bar window to calculate the Relative Retracement Magnitude . This ensures signals are mathematically tied to the volatility of the current market regime.

The Dual-Fuel Framework: StableFlow x Liquisync

The StableFlow Engine is designed to function as the tactical counterpart to the Liquisync: Macro Pulse Engine . While Liquisync monitors the Global Supply Line (the "Tanker Truck" of M2 Liquidity moving from Central Banks toward the track with a 60-day lead), StableFlow measures the Immediate Fuel Pressure (the "Dry Powder" already in the pit lane, ready to be pumped into the car).

By using both indicators in tandem, you can follow the Dual-Fuel Strategy: Liquisync identifies the fundamental macro regime, while StableFlow identifies the specific "Refuel" and "Exhaustion" pivots within that regime. We will be providing a comprehensive breakdown of this synchronized telemetry in our upcoming Substack Masterclass: The Dual-Fuel Architecture.

Risk Disclaimer & Credits

The StableFlow is a thematic macro tool tracking on-chain liquidity proxies. Stablecoin data is subject to exchange reporting delays. This is not financial advice; it is a telemetry model for institutional education. Rob Maths is not liable for losses incurred via use of this model.

Tags:

indicator, bitcoin, btc, stablecoins, usdt, flow, liquidity, macro, refuel, institutional, robmaths, Rob Maths