DOPT---

## 🔍 **DOPT - Daily Open & Price Time Markers**

This script is designed to support directional bias development and price behavior analysis around key time-based reference points on the **1H and 4H timeframes**.

### ✨ **What It Does**

- **1800 Open Marker** (6 PM NY time): Plots the **daily open** from 1800 in **black dotted lines**.

- **0000 Open Marker** (Midnight NY time): Plots the **midnight open** in **blue dotted lines**.

- **Day Letters**: Each 1800 open is labeled with the corresponding **day of the week** (e.g., M, T, W...), helping visually segment your chart.

- **Hour Labels**: Select specific candles (e.g., 0000 = '0', 0800 = '8') to be labeled above the bar. These are fully customizable.

- **Candle Midpoints**: Option to mark the **50% level** of a specific candle (good for CE or CRT references).

- **CRT High/Low Tracking**: Ability to plot **extended high and low lines** from a selected candle back (e.g., for CRT modeling).

- **4H Timeframe Candle Numbering**: Helpful when analyzing sequences on the 4-hour timeframe. Candles are numbered `1`, `5`, and `9` for reference.

---

### 🧠 **How I Use It**

- I mostly use this on the **1-hour timeframe** to decide **directional bias** for the day:

- If price **closes above 1800 open**, I consider that a **green daily close** — potential bullish sentiment.

- If price **closes below**, I treat it as a **red daily close** — potential bearish behavior.

- Price often uses these opens as **support/resistance**, so I watch for reactions there.

- On the **4H**, the candle numbers help track structure and flow.

- Combine with CRT tools to mark **key candle highs/lows** and their **equilibrium (50%)** — great for refining entries or understanding how price is respecting a particular candle.

---

### ⚠️ **Note on Daylight Savings**

This is a **daylight saving time-dependent script**. When DST kicks in or out, you’ll need to **adjust the time inputs** accordingly to keep the opens accurate (e.g., 1800 might shift to 1700 depending on the season).

---

### 🔁 **Backtesting & Reference**

- The **1800 and 0000 opens** are plotted for **as far back** as your chart loads, making it great for backtesting historical reactions.

- The CRT marking tools only go back **50 candles max**, so use that for recent structure only.

---

Search in scripts for "backtesting"

RSI + Stochastic + WMA StrategyThis script is designed for TradingView and serves as a trading strategy (not just a visual indicator). It's intended for backtesting, strategy optimization, or live trading signal generation using a combination of popular technical indicators.

📊 Indicators Used in the Strategy:

Indicator Description

RSI (Relative Strength Index) Measures momentum; identifies overbought (>70) or oversold (<30) conditions.

Stochastic Oscillator (%K & %D) Detects momentum reversal points via crossovers. Useful for timing entries.

WMA (Weighted Moving Average) Identifies the trend direction (used as a trend filter).

📈 Trading Logic / Strategy Rules:

📌 Long Entry Condition (Buy Signal):

All 3 conditions must be true:

RSI is Oversold → RSI < 30

Stochastic Crossover Upward → %K crosses above %D

Price is above WMA → Confirms uptrend direction

👉 Interpretation: Market was oversold, momentum is turning up, and price confirms uptrend — bullish entry.

📌 Short Entry Condition (Sell Signal):

All 3 conditions must be true:

RSI is Overbought → RSI > 70

Stochastic Crossover Downward → %K crosses below %D

Price is below WMA → Confirms downtrend direction

👉 Interpretation: Market is overbought, momentum is turning down, and price confirms downtrend — bearish entry.

🔄 Strategy Execution (Backtesting Logic):

The script uses:

pinescript

Copy

Edit

strategy.entry("LONG", strategy.long)

strategy.entry("SHORT", strategy.short)

These are Pine Script functions to place buy and sell orders automatically when the above conditions are met. This allows you to:

Backtest the strategy

Measure win/loss ratio, drawdown, and profitability

Optimize indicator settings using TradingView Strategy Tester

📊 Visual Aids (Charts):

Plots WMA Line: Orange line for trend direction

Overbought/Oversold Zones: Horizontal lines at 70 (red) and 30 (green) for RSI visualization

⚡ Strategy Type Summary:

Category Setting

Strategy Type Momentum Reversal + Trend Filter

Timeframe Flexible (Works best on 1H, 4H, Daily)

Trading Style Swing/Intraday

Risk Profile Medium to High (due to momentum triggers)

Uses Leverage Possible (adjust risk accordingly)

Multi-Timeframe MACD Strategy ver 1.0Multi-Timeframe MACD Strategy: Enhanced Trend Trading with Customizable Entry and Trailing Stop

This strategy utilizes the Moving Average Convergence Divergence (MACD) indicator across multiple timeframes to identify strong trends, generate precise entry and exit signals, and manage risk with an optional trailing stop loss. By combining the insights of both the current chart's timeframe and a user-defined higher timeframe, this strategy aims to improve trade accuracy, reduce exposure to false signals, and capture larger market moves.

Key Features:

Dual Timeframe Analysis: Calculates and analyzes the MACD on both the current chart's timeframe and a user-selected higher timeframe (e.g., Daily MACD on a 1-hour chart). This provides a broader market context, helping to confirm trends and filter out short-term noise.

Configurable MACD: Fine-tune the MACD calculation with adjustable Fast Length, Slow Length, and Signal Length parameters. Optimize the indicator's sensitivity to match your trading style and the volatility of the asset.

Flexible Entry Options: Choose between three distinct entry types:

Crossover: Enters trades when the MACD line crosses above (long) or below (short) the Signal line.

Zero Cross: Enters trades when the MACD line crosses above (long) or below (short) the zero line.

Both: Combines both Crossover and Zero Cross signals, providing more potential entry opportunities.

Independent Timeframe Control: Display and trade based on the current timeframe MACD, the higher timeframe MACD, or both. This allows you to focus on the information most relevant to your analysis.

Optional Trailing Stop Loss: Implements a configurable trailing stop loss to protect profits and limit potential losses. The trailing stop is adjusted dynamically as the price moves in your favor, based on a user-defined percentage.

No Repainting: Employs lookahead=barmerge.lookahead_off in the request.security() function to prevent data leakage and ensure accurate backtesting and real-time signals.

Clear Visual Signals (Optional): Includes optional plotting of the MACD and Signal lines for both timeframes, with distinct colors for easy visual identification. These plots are for visual confirmation and are not required for the strategy's logic.

Suitable for Various Trading Styles: Adaptable to swing trading, day trading, and trend-following strategies across diverse markets (stocks, forex, cryptocurrencies, etc.).

Fully Customizable: All parameters are adjustable, including timeframes, MACD Settings, Entry signal type and trailing stop settings.

How it Works:

MACD Calculation: The strategy calculates the MACD (using the standard formula) for both the current chart's timeframe and the specified higher timeframe.

Trend Identification: The relationship between the MACD line, Signal line, and zero line is used to determine the current trend for each timeframe.

Entry Signals: Buy/sell signals are generated based on the selected "Entry Type":

Crossover: A long signal is generated when the MACD line crosses above the Signal line, and both timeframes are in agreement (if both are enabled). A short signal is generated when the MACD line crosses below the Signal line, and both timeframes are in agreement.

Zero Cross: A long signal is generated when the MACD line crosses above the zero line, and both timeframes agree. A short signal is generated when the MACD line crosses below the zero line and both timeframes agree.

Both: Combines Crossover and Zero Cross signals.

Trailing Stop Loss (Optional): If enabled, a trailing stop loss is set at a specified percentage below (for long positions) or above (for short positions) the entry price. The stop-loss is automatically adjusted as the price moves favorably.

Exit Signals:

Without Trailing Stop: Positions are closed when the MACD signals reverse according to the selected "Entry Type" (e.g., a long position is closed when the MACD line crosses below the Signal line if using "Crossover" entries).

With Trailing Stop: Positions are closed if the price hits the trailing stop loss.

Backtesting and Optimization: The strategy automatically backtests on the chart's historical data, allowing you to assess its performance and optimize parameters for different assets and timeframes.

Example Use Cases:

Confirming Trend Strength: A trader on a 1-hour chart sees a bullish MACD crossover on the current timeframe. They check the MTF MACD strategy and see that the Daily MACD is also bullish, confirming the strength of the uptrend.

Filtering Noise: A trader using a 15-minute chart wants to avoid false signals from short-term volatility. They use the strategy with a 4-hour higher timeframe to filter out noise and only trade in the direction of the dominant trend.

Dynamic Risk Management: A trader enters a long position and enables the trailing stop loss. As the price rises, the trailing stop is automatically adjusted upwards, protecting profits. The trade is exited either when the MACD reverses or when the price hits the trailing stop.

Disclaimer:

The MACD is a lagging indicator and can produce false signals, especially in ranging markets. This strategy is for educational and informational purposes only and should not be considered financial advice. Backtest and optimize the strategy thoroughly, combine it with other technical analysis tools, and always implement sound risk management practices before using it with real capital. Past performance is not indicative of future results. Conduct your own due diligence and consider your risk tolerance before making any trading decisions.

*Auto Backtest & Optimize EngineFull-featured Engine for Automatic Backtesting and parameter optimization. Allows you to test millions of different combinations of stop-loss and take profit parameters, including on any connected indicators.

⭕️ Key Futures

Quickly identify the optimal parameters for your strategy.

Automatically generate and test thousands of parameter combinations.

A simple Genetic Algorithm for result selection.

Saves time on manual testing of multiple parameters.

Detailed analysis, sorting, filtering and statistics of results.

Detailed control panel with many tooltips.

Display of key metrics: Profit, Win Rate, etc..

Comprehensive Strategy Score calculation.

In-depth analysis of the performance of different types of stop-losses.

Possibility to use to calculate the best Stop-Take parameters for your position.

Ability to test your own functions and signals.

Customizable visualization of results.

Flexible Stop-Loss Settings:

• Auto ━ Allows you to test all types of Stop Losses at once(listed below).

• S.VOLATY ━ Static stop based on volatility (Fixed, ATR, STDEV).

• Trailing ━ Classic trailing stop following the price.

• Fast Trail ━ Accelerated trailing stop that reacts faster to price movements.

• Volatility ━ Dynamic stop based on volatility indicators.

• Chandelier ━ Stop based on price extremes.

• Activator ━ Dynamic stop based on SAR.

• MA ━ Stop based on moving averages (9 different types).

• SAR ━ Parabolic SAR (Stop and Reverse).

Advanced Take-Profit Options:

• R:R: Risk/Reward ━ sets TP based on SL size.

• T.VOLATY ━ Calculation based on volatility indicators (Fixed, ATR, STDEV).

Testing Modes:

• Stops ━ Cyclical stop-loss testing

• Pivot Point Example ━ Example of using pivot points

• External Example ━ Built-in example how test functions with different parameters

• External Signal ━ Using external signals

⭕️ Usage

━ First Steps:

When opening, select any point on the chart. It will not affect anything until you turn on Manual Start mode (more on this below).

The chart will immediately show the best results of the default Auto mode. You can switch Part's to try to find even better results in the table.

Now you can display any result from the table on the chart by entering its ID in the settings.

Repeat steps 3-4 until you determine which type of Stop Loss you like best. Then set it in the settings instead of Auto mode.

* Example: I flipped through 14 parts before I liked the first result and entered its ID so I could visually evaluate it on the chart.

Then select the stop loss type, choose it in place of Auto mode and repeat steps 3-4 or immediately follow the recommendations of the algorithm.

Now the Genetic Algorithm at the bottom right will prompt you to enter the Parameters you need to search for and select even better results.

Parameters must be entered All at once before they are updated. Enter recommendations strictly in fields with the same names.

Repeat steps 5-6 until there are approximately 10 Part's left or as you like. And after that, easily pour through the remaining Parts and select the best parameters.

━ Example of the finished result.

━ Example of use with Takes

You can also test at the same time along with Take Profit. In this example, I simply enabled Risk/Reward mode and immediately specified in the TP field Maximum RR, Minimum RR and Step. So in this example I can test (3-1) / 0.1 = 20 Takes of different sizes. There are additional tips in the settings.

━

* Soon you will start to understand how the system works and things will become much easier.

* If something doesn't work, just reset the engine settings and start over again.

* Use the tips I have left in the settings and on the Panel.

━ Details:

Sort ━ Sorting results by Score, Profit, Trades, etc..

Filter ━ Filtring results by Score, Profit, Trades, etc..

Trade Type ━ Ability to disable Long\Short but only from statistics.

BackWin ━ Backtest Window Number of Candle the script can test.

Manual Start ━ Enabling it will allow you to call a Stop from a selected point. which you selected when you started the engine.

* If you have a real open position then this mode can help to save good Stop\Take for it.

1 - 9 Сheckboxs ━ Allow you to disable any stop from Auto mode.

Ex Source - Allow you to test Stops/Takes from connected indicators.

Connection guide:

//@version=6

indicator("My script")

rsi = ta.rsi(close, 14)

buy = not na(rsi) and ta.crossover (rsi, 40) // OS = 40

sell = not na(rsi) and ta.crossunder(rsi, 60) // OB = 60

Signal = buy ? +1 : sell ? -1 : 0

plot(Signal, "🔌Connector🔌", display = display.none)

* Format the signal for your indicator in a similar style and then select it in Ex Source.

⭕️ How it Works

Hypothesis of Uniform Distribution of Rare Elements After Mixing.

'This hypothesis states that if an array of N elements contains K valid elements, then after mixing, these valid elements will be approximately uniformly distributed.'

'This means that in a random sample of k elements, the proportion of valid elements should closely match their proportion in the original array, with some random variation.'

'According to the central limit theorem, repeated sampling will result in an average count of valid elements following a normal distribution.'

'This supports the assumption that the valid elements are evenly spread across the array.'

'To test this hypothesis, we can conduct an experiment:'

'Create an array of 1,000,000 elements.'

'Select 1,000 random elements (1%) for validation.'

'Shuffle the array and divide it into groups of 1,000 elements.'

'If the hypothesis holds, each group should contain, on average, 1~ valid element, with minor variations.'

* I'd like to attach more details to My hypothesis but it won't be very relevant here. Since this is a whole separate topic, I will leave the minimum part for understanding the engine.

Practical Application

To apply this hypothesis, I needed a way to generate and thoroughly mix numerous possible combinations. Within Pine, generating over 100,000 combinations presents significant challenges, and storing millions of combinations requires excessive resources.

I developed an efficient mechanism that generates combinations in random order to address these limitations. While conventional methods often produce duplicates or require generating a complete list first, my approach guarantees that the first 10% of possible combinations are both unique and well-distributed. Based on my hypothesis, this sampling is sufficient to determine optimal testing parameters.

Most generators and randomizers fail to accommodate both my hypothesis and Pine's constraints. My solution utilizes a simple Linear Congruential Generator (LCG) for pseudo-randomization, enhanced with prime numbers to increase entropy during generation. I pre-generate the entire parameter range and then apply systematic mixing. This approach, combined with a hybrid combinatorial array-filling technique with linear distribution, delivers excellent generation quality.

My engine can efficiently generate and verify 300 unique combinations per batch. Based on the above, to determine optimal values, only 10-20 Parts need to be manually scrolled through to find the appropriate value or range, eliminating the need for exhaustive testing of millions of parameter combinations.

For the Score statistic I applied all the same, generated a range of Weights, distributed them randomly for each type of statistic to avoid manual distribution.

Score ━ based on Trade, Profit, WinRate, Profit Factor, Drawdown, Sharpe & Sortino & Omega & Calmar Ratio.

⭕️ Notes

For attentive users, a little tricks :)

To save time, switch parts every 3 seconds without waiting for it to load. After 10-20 parts, stop and wait for loading. If the pause is correct, you can switch between the rest of the parts without loading, as they will be cached. This used to work without having to wait for a pause, but now it does slower. This will save a lot of time if you are going to do a deeper backtest.

Sometimes you'll get the error “The scripts take too long to execute.”

For a quick fix you just need to switch the TF or Ticker back and forth and most likely everything will load.

The error appears because of problems on the side of the site because the engine is very heavy. It can also appear if you set too long a period for testing in BackWin or use a heavy indicator for testing.

Manual Start - Allow you to Start you Result from any point. Which in turn can help you choose a good stop-stick for your real position.

* It took me half a year from idea to current realization. This seems to be one of the few ways to build something automatic in backtest format and in this particular Pine environment. There are already better projects in other languages, and they are created much easier and faster because there are no limitations except for personal PC. If you see solutions to improve this system I would be glad if you share the code. At the moment I am tired and will continue him not soon.

Also You can use my previosly big Backtest project with more manual settings(updated soon)

Supertrend TP SL (PRO)2. Main Components:

Supertrend Indicator:

Theoretical basis: The Supertrend indicator is based on two main concepts: Average True Range (ATR) and Factor. ATR measures the extent of price fluctuations in a given period of time, while Factor determines the sensitivity of the indicator to price changes.

Mechanism of operation: The indicator calculates two possible lines: one line representing the potential support level and another line representing the potential resistance level. The selection of the appropriate line depends on the current price direction. When the price is above the line, the indicator is considered to be in an uptrend, and vice versa.

Customizable inputs:

atrPeriod: Allows the trader to specify the time period for calculating the ATR. Shorter periods make the indicator more sensitive to price changes, while longer periods reduce its sensitivity.

factor: Allows the adjustment of the factor. Higher values make the indicator less likely to give false signals, but they may also delay entry signals.

Risk Management:

Take Profit and Stop Loss Orders:

TPPoints: Specifies the distance between the entry price and the take profit level. This distance is expressed in points, and is converted to an actual price value using syminfo.mintick (the smallest possible price movement of the traded asset).

SLPoints: Specifies the distance between the entry price and the stop loss level.

Importance: These orders allow the trader to specify the maximum loss he is willing to take and the profit target he is aiming to achieve, which helps in effective risk management.

Activate/Disable Trades:

isLongEnabled: Allows buy trades to be enabled or disabled, which allows the trader to trade in one direction only (for example, only trade in the uptrend during a bull market).

isShortEnabled: Allows sell trades to be enabled or disabled.

isTakeProfitEnabled: Allows take profit orders to be enabled or disabled. The trader may wish to disable them if he prefers to manage his trades manually.

isStopLossEnabled: Allows you to enable or disable stop loss orders. Although disabling them may seem tempting in some cases, it is a very risky move.

Visual Customization:

Line Style and Width:

lineStyle: Allows the trader to choose the style of lines used to draw TP and SL levels (Solid, Dashed, Dotted).

lineWidth: Sets the thickness of the lines.

Label Size:

labelSize: Allows you to set the size of the labels that display TP and SL levels (Small, Normal, Large).

Colors:

bullColor, bearColor, tpColor, slColor: Allows the trader to customize the colors of the different elements on the chart, making visual analysis easier.

3. Strategy Logic:

Determining Entry Signals: The strategy relies on the Supertrend indicator to determine entry signals. When the Supertrend trend changes from bearish to bullish, a buy trade is triggered (if isLongEnabled is enabled). When the trend changes from bullish to bearish, a sell trade is triggered (if isShortEnabled is enabled).

Order Execution: Once the entry signal is triggered, the strategy automatically places buy or sell orders.

Trade Management: After opening a trade, the strategy monitors the price and automatically triggers Take Profit and Stop Loss orders if the price reaches the specified levels.

Visualization: The strategy displays useful information on the chart, such as TP and SL lines, entry and exit signals, which helps the trader understand the strategy’s behavior and evaluate its performance.

4. Advanced Tips:

Optimizing Settings: The strategy’s performance can be improved by adjusting different input values. For example, the trader can experiment with different values for atrPeriod and factor to improve the accuracy of Supertrend signals.

Combining Indicators: This strategy can be combined with other indicators to improve the accuracy of entry signals. For example, the Relative Strength Index (RSI) can be used to confirm Supertrend signals.

Time Analysis: The strategy’s performance can be analyzed over different time periods to evaluate its effectiveness in various market conditions.

Strategy Testing: Before using the strategy in real trading, it should be tested on historical data (Backtesting) to evaluate its performance and determine the optimal settings.

5. Associated Risks:

False Signals: The Supertrend indicator may sometimes give false signals, especially in volatile markets.

Losses: Even with the use of stop loss orders, the trader may be exposed to significant losses.

Over-optimization: Over-optimization of settings on historical data may lead to misleading results. The trader should be careful about generalizing the results to future data.

Over-reliance on automation: The automated strategy should not be relied upon completely. The trader should monitor the trades and make appropriate decisions when necessary.

6. Disclaimer:

I am not a licensed financial advisor. This strategy is provided for educational and illustrative purposes only and should not be considered as investment advice. Trading in financial markets involves significant risks and you may lose your invested capital. Before making any investment decisions, consult a qualified financial advisor and conduct your own research. You alone are responsible for your trading decisions and their results. By using this strategy, you acknowledge and agree that I am not responsible for any losses or damages you may incur.

2. المكونات الرئيسية:

مؤشر Supertrend:

الأساس النظري: يعتمد مؤشر Supertrend على مفهومين رئيسيين هما: متوسط المدى الحقيقي (Average True Range - ATR) ومعامل الضرب (Factor). ATR يقيس مدى تقلبات الأسعار في فترة زمنية محددة، بينما Factor يحدد مدى حساسية المؤشر لتغيرات الأسعار.

آلية العمل: يقوم المؤشر بحساب خطين محتملين: خط يمثل مستوى الدعم المحتمل وخط آخر يمثل مستوى المقاومة المحتمل. يعتمد اختيار الخط المناسب على اتجاه السعر الحالي. عندما يكون السعر أعلى من الخط، يعتبر المؤشر في اتجاه صاعد، والعكس صحيح.

المدخلات القابلة للتخصيص:

atrPeriod: يتيح للمتداول تحديد الفترة الزمنية لحساب ATR. الفترات الأقصر تجعل المؤشر أكثر حساسية لتغيرات الأسعار، بينما الفترات الأطول تقلل من حساسيته.

factor: يسمح بتعديل معامل الضرب. القيم الأعلى تجعل المؤشر أقل عرضة لإعطاء إشارات خاطئة، ولكنها قد تؤخر أيضًا إشارات الدخول.

إدارة المخاطر:

أوامر جني الأرباح وإيقاف الخسارة:

TPPoints: يحدد المسافة بين سعر الدخول ومستوى جني الأرباح. يتم التعبير عن هذه المسافة بالنقاط (Points)، ويتم تحويلها إلى قيمة سعرية فعلية باستخدام syminfo.mintick (أصغر حركة سعرية ممكنة للأصل المتداول).

SLPoints: يحدد المسافة بين سعر الدخول ومستوى إيقاف الخسارة.

الأهمية: تتيح هذه الأوامر للمتداول تحديد الحد الأقصى للخسارة التي يرغب في تحملها والهدف الربحي الذي يسعى لتحقيقه، مما يساعد على إدارة المخاطر بشكل فعال.

تفعيل/تعطيل الصفقات:

isLongEnabled: يسمح بتفعيل أو تعطيل صفقات الشراء، مما يمكن المتداول من التداول في اتجاه واحد فقط (على سبيل المثال، التداول فقط في الاتجاه الصاعد خلال سوق صاعدة).

isShortEnabled: يسمح بتفعيل أو تعطيل صفقات البيع.

isTakeProfitEnabled: يسمح بتفعيل أو تعطيل أوامر جني الأرباح. قد يرغب المتداول في تعطيلها إذا كان يفضل إدارة صفقاته يدويًا.

isStopLossEnabled: يسمح بتفعيل أو تعطيل أوامر إيقاف الخسارة. على الرغم من أن تعطيلها قد يبدو مغريًا في بعض الحالات، إلا أنه يعتبر خطوة محفوفة بالمخاطر للغاية.

التخصيص المرئي:

نمط وعرض الخطوط:

lineStyle: يتيح للمتداول اختيار نمط الخطوط المستخدمة لرسم مستويات TP و SL (Solid, Dashed, Dotted).

lineWidth: يحدد سمك الخطوط.

حجم الملصقات:

labelSize: يسمح بتحديد حجم الملصقات التي تعرض مستويات TP و SL (Small, Normal, Large).

الألوان:

bullColor, bearColor, tpColor, slColor: تتيح للمتداول تخصيص ألوان العناصر المختلفة على الرسم البياني، مما يسهل عملية التحليل البصري.

3. منطق عمل الاستراتيجية:

تحديد إشارات الدخول: تعتمد الاستراتيجية على مؤشر Supertrend لتحديد إشارات الدخول. عندما يتغير اتجاه Supertrend من هابط إلى صاعد، يتم تفعيل صفقة شراء (إذا كانت isLongEnabled مفعلة). وعندما يتغير الاتجاه من صاعد إلى هابط، يتم تفعيل صفقة بيع (إذا كانت isShortEnabled مفعلة).

تنفيذ الأوامر: بمجرد تفعيل إشارة الدخول، تقوم الاستراتيجية بوضع أوامر الشراء أو البيع تلقائيًا.

إدارة الصفقات: بعد فتح الصفقة، تقوم الاستراتيجية بمراقبة السعر وتفعيل أوامر جني الأرباح وإيقاف الخسارة تلقائيًا في حالة وصول السعر إلى المستويات المحددة.

التمثيل المرئي: تعرض الاستراتيجية معلومات مفيدة على الرسم البياني، مثل خطوط TP و SL وإشارات الدخول والخروج، مما يساعد المتداول على فهم سلوك الاستراتيجية وتقييم أدائها.

4. نصائح متقدمة:

تحسين الإعدادات: يمكن تحسين أداء الاستراتيجية من خلال تعديل قيم المدخلات المختلفة. على سبيل المثال، يمكن للمتداول تجربة قيم مختلفة لـ atrPeriod و factor لتحسين دقة إشارات Supertrend.

الجمع بين المؤشرات: يمكن دمج هذه الاستراتيجية مع مؤشرات أخرى لتحسين دقة إشارات الدخول. على سبيل المثال، يمكن استخدام مؤشر القوة النسبية (RSI) لتأكيد إشارات Supertrend.

التحليل الزمني: يمكن تحليل أداء الاستراتيجية على مدى فترات زمنية مختلفة لتقييم مدى فعاليتها في ظروف السوق المتنوعة.

اختبار الاستراتيجية: قبل استخدام الاستراتيجية في التداول الحقيقي، يجب اختبارها على بيانات تاريخية (Backtesting) لتقييم أدائها وتحديد الإعدادات المثلى.

5. المخاطر المرتبطة:

الإشارات الخاطئة: قد يعطي مؤشر Supertrend إشارات خاطئة في بعض الأحيان، خاصة في الأسواق المتقلبة.

الخسائر: حتى مع استخدام أوامر إيقاف الخسارة، قد يتعرض المتداول لخسائر كبيرة.

التحسين المفرط: قد يؤدي التحسين المفرط للإعدادات على بيانات تاريخية إلى نتائج مضللة. يجب أن يكون المتداول حذرًا بشأن تعميم النتائج على البيانات المستقبلية.

الاعتماد الزائد على الأتمتة: يجب عدم الاعتماد بشكل كامل على الاستراتيجية الآلية. يجب على المتداول مراقبة الصفقات واتخاذ القرارات المناسبة عند الضرورة.

6. إخلاء المسؤولية:

أنا لست مستشارًا ماليًا مرخصًا. هذه الاستراتيجية مقدمة لأغراض تعليمية وتوضيحية فقط، ولا ينبغي اعتبارها نصيحة استثمارية. التداول في الأسواق المالية ينطوي على مخاطر كبيرة، وقد تخسر رأس المال المستثمر. قبل اتخاذ أي قرارات استثمارية، استشر مستشارًا ماليًا مؤهلاً وقم بإجراء بحثك الخاص. أنت وحدك المسؤول عن قراراتك التجارية ونتائجها. باستخدام هذه الاستراتيجية، فإنك تقر وتوافق على أنني لست مسؤولاً عن أي خسائر أو أضرار قد تتكبدها.

FVG Breakout Lite by tradingbauhausExplanation of "FVG Breakout Lite by tradingbauhaus"

This script is a trading strategy built for TradingView that helps you spot and trade "Fair Value Gaps" (FVGs)—price areas where the market moved quickly, leaving a gap that might act as support or resistance later. It’s designed to catch breakout opportunities when the price moves strongly in one direction, with extra filters to make trades more reliable. Here’s how it works and how you can use it:

What It Does

1. Finds Fair Value Gaps (FVGs):

A "Bullish FVG" happens when the price jumps up quickly, leaving a gap below where it didn’t trade much (e.g., today’s low is higher than the high from two bars ago).

A "Bearish FVG" is the opposite: the price drops fast, leaving a gap above (e.g., today’s high is lower than the low from two bars ago).

The script draws colored boxes on your chart to show these gaps: green for bullish, red for bearish.

2. Spots Breakouts:

It looks for "strong" FVGs by comparing them to a trend (based on the highest highs and lowest lows over a set period).

If a bullish gap forms above the recent highs, or a bearish gap below the recent lows, it’s marked as a breakout opportunity.

3. Adds a Volume Check:

Trades only happen if the market’s volume is higher than usual (e.g., 1.2x the average volume over the last 20 bars). This helps ensure the breakout has real momentum behind it.

4. Trades Automatically:

Long Trades (Buy): If a bullish breakout FVG forms and volume is high, it buys at the current price.

Short Trades (Sell): If a bearish breakout FVG forms with high volume, it sells short.

Each trade comes with a stop loss (to limit losses) and a take profit (to lock in gains), both adjustable by you.

5. Shows Mitigation Lines (Optional):

If you turn on "Display Mitigation Zones," it draws lines at the edge of each breakout FVG. These lines show where the price might return to "fill" the gap later, helping you see key levels.

6. Includes Webull Costs:

The script factors in real trading fees from Webull, like tiny SEC and FINRA fees for selling, and a daily margin cost if you’re borrowing money to trade. These don’t show up on the chart but affect the strategy’s performance in backtesting.

How to Use It

1. Add to Your Chart:

Copy the script into TradingView’s Pine Editor, click "Add to Chart," and it’ll start drawing FVGs and running the strategy.

2. Customize Settings:

Trend Period (Default: 25): How many bars it looks back to define the trend. Longer periods mean fewer but stronger signals.

Volume Lookback (Default: 20) & Volume Threshold (Default: 1.2): Adjust how it measures "high volume." Increase the threshold for stricter trades.

Stop Loss % (Default: 1.5%) & Take Profit % (Default: 3%): Set how much you’re willing to lose or aim to gain per trade.

Margin Rate % (Default: 8.74%): Webull’s rate for borrowing money—lower it if your account qualifies for a better rate.

Display Mitigation Zones (Default: On): Toggle this to see or hide the gap lines.

Colors: Change the green (bullish) and red (bearish) shades to suit your chart.

3. Backtest It:

Go to the "Strategy Tester" tab in TradingView to see how it performs on past data. It’ll show trades, profits, losses, and Webull fees included.

4. Watch It Work:

Green boxes mean bullish FVGs; red boxes mean bearish FVGs. If volume spikes and the price breaks out, you’ll see trades happen automatically.

What to Expect

Visuals: You’ll see colored boxes for FVGs and optional lines showing where they start. These help you spot key price zones even if you’re not trading.

Trades: It’s selective—only trades when FVGs align with a breakout and volume confirms it. Expect fewer trades but with higher potential.

Risk: The stop loss keeps losses in check, while the take profit aims for a 2:1 reward-to-risk ratio by default (3% gain vs. 1.5% loss).

Costs: Webull’s fees are small but baked into the results, so you’re seeing a realistic picture of profits.

Tips for Users

Test it on a small timeframe (like 5-minute charts) for day trading or a larger one (like daily) for swing trading.

Play with the volume threshold—if you get too few trades, lower it (e.g., 1.1); if too many, raise it (e.g., 1.5).

Watch how price reacts to the mitigation lines—they’re often support or resistance zones traders target.

This strategy is lightweight, focused, and built for traders who like breakouts with a bit of confirmation. It’s not foolproof (no strategy is!), but it gives you a clear way to trade FVGs with some smart filters.

Trend Vanguard StrategyHow to Use:

Trend Vanguard Strategy is a multi-feature Pine Script strategy designed to identify market pivots, draw dynamic support/resistance, and generate trade signals via ZigZag breakouts. Here’s how it works and how to use it:

ZigZag Detection & Pivot Points

The script locates significant swing highs and lows using configurable Depth, Deviation, and Backstep values.

It then connects these pivots with lines (ZigZag) to highlight directional changes and prints labels (“Buy,” “Sell,” etc.) at key turning points.

Support & Resistance Trendlines

Pivot highs and lows are used to draw dashed S/R lines in real-time.

When price crosses these lines, the script triggers a breakout signal (long or short).

EMA Overlays

Up to four EMAs (with customizable lengths and colors) can be overlaid on the chart for added trend confirmation.

Enable/disable each EMA independently via the settings.

Repaint Option

Turning on “Smooth Indicator Lines” (repaint) uses future data to refine past pivots.

This can make historical signals look cleaner but does not reflect true historical conditions.

Turning it off ensures signals remain fixed once they appear.

Strategy Entries & Exits

On each new ZigZag “Buy” or “Sell” signal, the script closes any open position and flips to the opposite side (if desired).

Works with the built-in TradingView Strategy engine for backtesting.

Additional Inputs (Placeholders)

Volume Filter and RSI Filter settings exist but are not fully implemented in the current code. Future versions may incorporate these filters more directly.

How to Use

Add to Chart: Click “Indicators” → “Invite-Only Scripts” (or “My Scripts”) and select “Trend Vanguard Strategy.”

Configure Settings:

Adjust ZigZag Depth, Deviation, and Backstep to fine-tune pivot sensitivity.

Enable or disable each EMA to see how it aligns with market trends.

Toggle “Smooth Indicator Lines” on or off depending on whether you want repainting.

Backtest and Forward Test:

Use TradingView’s “Strategy Tester” tab to review hypothetical performance.

Remember that repainting can alter past signals if enabled.

Monitor Live:

Watch for breakout triangles or ZigZag labels to identify potential reversal or breakout trades in real time.

Disclaimer: This script is purely educational and not financial advice. Always combine it with sound risk management and thorough analysis. Enjoy exploring the script, and feel free to experiment with the different settings to match your trading style!

SuperTrend AI Oscillator StrategySuperTrend AI Oscillator Strategy

Overview

This strategy is a trend-following approach that combines the SuperTrend indicator with oscillator-based filtering.

By identifying market trends while utilizing oscillator-based momentum analysis, it aims to improve entry precision.

Additionally, it incorporates a trailing stop to strengthen risk management while maximizing profits.

This strategy can be applied to various markets, including Forex, Crypto, and Stocks, as well as different timeframes. However, its effectiveness varies depending on market conditions, so thorough testing is required.

Features

1️⃣ Trend Identification Using SuperTrend

The SuperTrend indicator (a volatility-adjusted trend indicator based on ATR) is used to determine trend direction.

A long entry is considered when SuperTrend turns bullish.

A short entry is considered when SuperTrend turns bearish.

The goal is to capture clear trend reversals and avoid unnecessary trades in ranging markets.

2️⃣ Entry Filtering with an Oscillator

The Super Oscillator is used to filter entry signals.

If the oscillator exceeds 50, it strengthens long entries (indicating strong bullish momentum).

If the oscillator drops below 50, it strengthens short entries (indicating strong bearish momentum).

This filter helps reduce trades in uncertain market conditions and improves entry accuracy.

3️⃣ Risk Management with a Trailing Stop

Instead of a fixed stop loss, a SuperTrend-based trailing stop is implemented.

The stop level adjusts automatically based on market volatility.

This allows profits to run while managing downside risk effectively.

4️⃣ Adjustable Risk-Reward Ratio

The default risk-reward ratio is set at 1:2.

Example: A 1% stop loss corresponds to a 2% take profit target.

The ratio can be customized according to the trader’s risk tolerance.

5️⃣ Clear Trade Signals & Visual Support

Green "BUY" labels indicate long entry signals.

Red "SELL" labels indicate short entry signals.

The Super Oscillator is plotted in a separate subwindow to visually assess trend strength.

A real-time trailing stop is displayed to support exit strategies.

These visual aids make it easier to identify entry and exit points.

Trading Parameters & Considerations

Initial Account Balance: Default is $7,000 (adjustable).

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 1,032

Visual Aids for Clarity

This strategy includes clear visual trade signals to enhance decision-making:

Green "BUY" labels for long entries

Red "SELL" labels for short entries

Super Oscillator plotted in a subwindow with a 50 midline

Dynamic trailing stop displayed for real-time trend tracking

These visual aids allow traders to quickly identify trade setups and manage positions with greater confidence.

Summary

The SuperTrend AI Oscillator Strategy is developed based on indicators from Black Cat and LuxAlgo.

By integrating high-precision trend analysis with AI-based oscillator filtering, it provides a strong risk-managed trading approach.

Important Notes

This strategy does not guarantee profits—performance varies based on market conditions.

Past performance does not guarantee future results. Markets are constantly changing.

Always test extensively with backtesting and demo trading before using it in live markets.

Risk management, position sizing, and market conditions should always be considered when trading.

Conclusion

This strategy combines trend analysis with momentum filtering, enhancing risk management in trading.

By following market trends carefully, making precise entries, and using trailing stops, it seeks to reduce risk while maximizing potential profits.

Before using this strategy, be sure to test it thoroughly via backtesting and demo trading, and adjust the settings to match your trading style.

MACD Volume Strategy for XAUUSD (15m) [PineIndicators]The MACD Volume Strategy is a momentum-based trading system designed for XAUUSD on the 15-minute timeframe. It integrates two key market indicators: the Moving Average Convergence Divergence (MACD) and a volume-based oscillator to identify strong trend shifts and confirm trade opportunities. This strategy uses dynamic position sizing, incorporates leverage customization, and applies structured entry and exit conditions to improve risk management.

⚙️ Core Strategy Components

1️⃣ Volume-Based Momentum Calculation

The strategy includes a custom volume oscillator to filter trade signals based on market activity. The oscillator is derived from the difference between short-term and long-term volume trends using Exponential Moving Averages (EMAs)

Short EMA (default = 5) represents recent volume activity.

Long EMA (default = 8) captures broader volume trends.

Positive values indicate rising volume, supporting momentum-based trades.

Negative values suggest weak market activity, reducing signal reliability.

By requiring positive oscillator values, the strategy ensures momentum confirmation before entering trades.

2️⃣ MACD Trend Confirmation

The strategy uses the MACD indicator as a trend filter. The MACD is calculated as:

Fast EMA (16-period) detects short-term price trends.

Slow EMA (26-period) smooths out price fluctuations to define the overall trend.

Signal Line (9-period EMA) helps identify crossovers, signaling potential trend shifts.

Histogram (MACD – Signal) visualizes trend strength.

The system generates trade signals based on MACD crossovers around the zero line, confirming bullish or bearish trend shifts.

📌 Trade Logic & Conditions

🔹 Long Entry Conditions

A buy signal is triggered when all the following conditions are met:

✅ MACD crosses above 0, signaling bullish momentum.

✅ Volume oscillator is positive, confirming increased trading activity.

✅ Current volume is at least 50% of the previous candle’s volume, ensuring market participation.

🔻 Short Entry Conditions

A sell signal is generated when:

✅ MACD crosses below 0, indicating bearish momentum.

✅ Volume oscillator is positive, ensuring market activity is sufficient.

✅ Current volume is less than 50% of the previous candle’s volume, showing decreasing participation.

This multi-factor approach filters out weak or false signals, ensuring that trades align with both momentum and volume dynamics.

📏 Position Sizing & Leverage

Dynamic Position Calculation:

Qty = strategy.equity × leverage / close price

Leverage: Customizable (default = 1x), allowing traders to adjust risk exposure.

Adaptive Sizing: The strategy scales position sizes based on account equity and market price.

Slippage & Commission: Built-in slippage (2 points) and commission (0.01%) settings provide realistic backtesting results.

This ensures efficient capital allocation, preventing overexposure in volatile conditions.

🎯 Trade Management & Exits

Take Profit & Stop Loss Mechanism

Each position includes predefined profit and loss targets:

Take Profit: +10% of risk amount.

Stop Loss: Fixed at 10,100 points.

The risk-reward ratio remains balanced, aiming for controlled drawdowns while maximizing trade potential.

Visual Trade Tracking

To improve trade analysis, the strategy includes:

📌 Trade Markers:

"Buy" label when a long position opens.

"Close" label when a position exits.

📌 Trade History Boxes:

Green for profitable trades.

Red for losing trades.

📌 Horizontal Trade Lines:

Shows entry and exit prices.

Helps identify trend movements over multiple trades.

This structured visualization allows traders to analyze past performance directly on the chart.

⚡ How to Use This Strategy

1️⃣ Apply the script to a XAUUSD (Gold) 15m chart in TradingView.

2️⃣ Adjust leverage settings as needed.

3️⃣ Enable backtesting to assess past performance.

4️⃣ Monitor volume and MACD conditions to understand trade triggers.

5️⃣ Use the visual trade markers to review historical performance.

The MACD Volume Strategy is designed for short-term trading, aiming to capture momentum-driven opportunities while filtering out weak signals using volume confirmation.

Forward Curve Visualization ToolProvide the spot symbol and the futures product root, and the script automatically scans all relevant contracts for you—no more tedious manual searches. The result is a clean, intuitive chart showing the live forward curve in real time.

It also detects contango or backwardation conditions (based on spot < F1 < F2 < F3).

Future Features:

Plot historical snapshots of the curve (1 day, 1 week, or 1 month ago) to understand market trends over time.

Display additional metrics such as annualized basis, cost of carry (CoC), and even volume or open interest for deeper insights.

If you trade futures and watch the forward curve, this script will give you the actionable data you need and get more ideas or features you’d like to see. Let’s build them together!

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

MTF Signal XpertMTF Signal Xpert – Detailed Description

Overview:

MTF Signal Xpert is a proprietary, open‑source trading signal indicator that fuses multiple technical analysis methods into one cohesive strategy. Developed after rigorous backtesting and extensive research, this advanced tool is designed to deliver clear BUY and SELL signals by analyzing trend, momentum, and volatility across various timeframes. Its integrated approach not only enhances signal reliability but also incorporates dynamic risk management, helping traders protect their capital while navigating complex market conditions.

Detailed Explanation of How It Works:

Trend Detection via Moving Averages

Dual Moving Averages:

MTF Signal Xpert computes two moving averages—a fast MA and a slow MA—with the flexibility to choose from Simple (SMA), Exponential (EMA), or Hull (HMA) methods. This dual-MA system helps identify the prevailing market trend by contrasting short-term momentum with longer-term trends.

Crossover Logic:

A BUY signal is initiated when the fast MA crosses above the slow MA, coupled with the condition that the current price is above the lower Bollinger Band. This suggests that the market may be emerging from a lower price region. Conversely, a SELL signal is generated when the fast MA crosses below the slow MA and the price is below the upper Bollinger Band, indicating potential bearish pressure.

Recent Crossover Confirmation:

To ensure that signals reflect current market dynamics, the script tracks the number of bars since the moving average crossover event. Only crossovers that occur within a user-defined “candle confirmation” period are considered, which helps filter out outdated signals and improves overall signal accuracy.

Volatility and Price Extremes with Bollinger Bands

Calculation of Bands:

Bollinger Bands are calculated using a 20‑period simple moving average as the central basis, with the upper and lower bands derived from a standard deviation multiplier. This creates dynamic boundaries that adjust according to recent market volatility.

Signal Reinforcement:

For BUY signals, the condition that the price is above the lower Bollinger Band suggests an undervalued market condition, while for SELL signals, the price falling below the upper Bollinger Band reinforces the bearish bias. This volatility context adds depth to the moving average crossover signals.

Momentum Confirmation Using Multiple Oscillators

RSI (Relative Strength Index):

The RSI is computed over 14 periods to determine if the market is in an overbought or oversold state. Only readings within an optimal range (defined by user inputs) validate the signal, ensuring that entries are made during balanced conditions.

MACD (Moving Average Convergence Divergence):

The MACD line is compared with its signal line to assess momentum. A bullish scenario is confirmed when the MACD line is above the signal line, while a bearish scenario is indicated when it is below, thus adding another layer of confirmation.

Awesome Oscillator (AO):

The AO measures the difference between short-term and long-term simple moving averages of the median price. Positive AO values support BUY signals, while negative values back SELL signals, offering additional momentum insight.

ADX (Average Directional Index):

The ADX quantifies trend strength. MTF Signal Xpert only considers signals when the ADX value exceeds a specified threshold, ensuring that trades are taken in strongly trending markets.

Optional Stochastic Oscillator:

An optional stochastic oscillator filter can be enabled to further refine signals. It checks for overbought conditions (supporting SELL signals) or oversold conditions (supporting BUY signals), thus reducing ambiguity.

Multi-Timeframe Verification

Higher Timeframe Filter:

To align short-term signals with broader market trends, the script calculates an EMA on a higher timeframe as specified by the user. This multi-timeframe approach helps ensure that signals on the primary chart are consistent with the overall trend, thereby reducing false signals.

Dynamic Risk Management with ATR

ATR-Based Calculations:

The Average True Range (ATR) is used to measure current market volatility. This value is multiplied by a user-defined factor to dynamically determine stop loss (SL) and take profit (TP) levels, adapting to changing market conditions.

Visual SL/TP Markers:

The calculated SL and TP levels are plotted on the chart as distinct colored dots, enabling traders to quickly identify recommended exit points.

Optional Trailing Stop:

An optional trailing stop feature is available, which adjusts the stop loss as the trade moves favorably, helping to lock in profits while protecting against sudden reversals.

Risk/Reward Ratio Calculation:

MTF Signal Xpert computes a risk/reward ratio based on the dynamic SL and TP levels. This quantitative measure allows traders to assess whether the potential reward justifies the risk associated with a trade.

Condition Weighting and Signal Scoring

Binary Condition Checks:

Each technical condition—ranging from moving average crossovers, Bollinger Band positioning, and RSI range to MACD, AO, ADX, and volume filters—is assigned a binary score (1 if met, 0 if not).

Cumulative Scoring:

These individual scores are summed to generate cumulative bullish and bearish scores, quantifying the overall strength of the signal and providing traders with an objective measure of its viability.

Detailed Signal Explanation:

A comprehensive explanation string is generated, outlining which conditions contributed to the current BUY or SELL signal. This explanation is displayed on an on‑chart dashboard, offering transparency and clarity into the signal generation process.

On-Chart Visualizations and Debug Information

Chart Elements:

The indicator plots all key components—moving averages, Bollinger Bands, SL and TP markers—directly on the chart, providing a clear visual framework for understanding market conditions.

Combined Dashboard:

A dedicated dashboard displays key metrics such as RSI, ADX, and the bullish/bearish scores, alongside a detailed explanation of the current signal. This consolidated view allows traders to quickly grasp the underlying logic.

Debug Table (Optional):

For advanced users, an optional debug table is available. This table breaks down each individual condition, indicating which criteria were met or not met, thus aiding in further analysis and strategy refinement.

Mashup Justification and Originality

MTF Signal Xpert is more than just an aggregation of existing indicators—it is an original synthesis designed to address real-world trading complexities. Here’s how its components work together:

Integrated Trend, Volatility, and Momentum Analysis:

By combining moving averages, Bollinger Bands, and multiple oscillators (RSI, MACD, AO, ADX, and an optional stochastic), the indicator captures diverse market dynamics. Each component reinforces the others, reducing noise and filtering out false signals.

Multi-Timeframe Analysis:

The inclusion of a higher timeframe filter aligns short-term signals with longer-term trends, enhancing overall reliability and reducing the potential for contradictory signals.

Adaptive Risk Management:

Dynamic stop loss and take profit levels, determined using ATR, ensure that the risk management strategy adapts to current market conditions. The optional trailing stop further refines this approach, protecting profits as the market evolves.

Quantitative Signal Scoring:

The condition weighting system provides an objective measure of signal strength, giving traders clear insight into how each technical component contributes to the final decision.

How to Use MTF Signal Xpert:

Input Customization:

Adjust the moving average type and period settings, ATR multipliers, and oscillator thresholds to align with your trading style and the specific market conditions.

Enable or disable the optional stochastic oscillator and trailing stop based on your preference.

Interpreting the Signals:

When a BUY or SELL signal appears, refer to the on‑chart dashboard, which displays key metrics (e.g., RSI, ADX, bullish/bearish scores) along with a detailed breakdown of the conditions that triggered the signal.

Review the SL and TP markers on the chart to understand the associated risk/reward setup.

Risk Management:

Use the dynamically calculated stop loss and take profit levels as guidelines for setting your exit points.

Evaluate the provided risk/reward ratio to ensure that the potential reward justifies the risk before entering a trade.

Debugging and Verification:

Advanced users can enable the debug table to see a condition-by-condition breakdown of the signal generation process, helping refine the strategy and deepen understanding of market dynamics.

Disclaimer:

MTF Signal Xpert is intended for educational and analytical purposes only. Although it is based on robust technical analysis methods and has undergone extensive backtesting, past performance is not indicative of future results. Traders should employ proper risk management and adjust the settings to suit their financial circumstances and risk tolerance.

MTF Signal Xpert represents a comprehensive, original approach to trading signal generation. By blending trend detection, volatility assessment, momentum analysis, multi-timeframe alignment, and adaptive risk management into one integrated system, it provides traders with actionable signals and the transparency needed to understand the logic behind them.

Enhanced Bollinger Bands Strategy with SL/TP// Title: Enhanced Bollinger Bands Strategy with SL/TP

// Description:

// This strategy is based on the classic Bollinger Bands indicator and incorporates Stop Loss (SL) and Take Profit (TP) levels for automated trading. It identifies potential long and short entry points based on price crossing the lower and upper Bollinger Bands, respectively. The strategy allows users to customize several parameters to suit different market conditions and risk tolerances.

// Key Features:

// * **Bollinger Bands:** Uses Simple Moving Average (SMA) as the basis and calculates upper and lower bands based on a user-defined standard deviation multiplier.

// * **Customizable Parameters:** Offers extensive customization, including SMA length, standard deviation multiplier, Stop Loss (SL) in pips, and Take Profit (TP) in pips.

// * **Long/Short Position Control:** Allows users to independently enable or disable long and short positions.

// * **Stop Loss and Take Profit:** Implements Stop Loss and Take Profit levels based on pip values to manage risk and secure profits. Entry prices are set to the band levels on signals.

// * **Visualizations:** Provides options to display Bollinger Bands and entry signals on the chart for easy analysis.

// Strategy Logic:

// 1. **Bollinger Bands Calculation:** The strategy calculates the Bollinger Bands using the specified SMA length and standard deviation multiplier.

// 2. **Entry Conditions:**

// * **Long Entry:** Enters a long position when the closing price crosses above the lower Bollinger Band and the `Enable Long Positions` setting is enabled.

// * **Short Entry:** Enters a short position when the closing price crosses below the upper Bollinger Band and the `Enable Short Positions` setting is enabled.

// 3. **Exit Conditions:**

// * **Stop Loss:** Exits the position if the price reaches the Stop Loss level, calculated based on the input `Stop Loss (Pips)`.

// * **Take Profit:** Exits the position if the price reaches the Take Profit level, calculated based on the input `Take Profit (Pips)`.

// Input Parameters:

// * **SMA Length (length):** The length of the Simple Moving Average used to calculate the Bollinger Bands (default: 20).

// * **Standard Deviation Multiplier (mult):** The multiplier applied to the standard deviation to determine the width of the Bollinger Bands (default: 2.0).

// * **Enable Long Positions (enableLong):** A boolean value to enable or disable long positions (default: true).

// * **Enable Short Positions (enableShort):** A boolean value to enable or disable short positions (default: true).

// * **Pip Value (pipValue):** The value of a pip for the traded instrument. This is crucial for accurate Stop Loss and Take Profit calculations (default: 0.0001 for most currency pairs). **Important: Adjust this value to match the specific instrument you are trading.**

// * **Stop Loss (Pips) (slPips):** The Stop Loss level in pips (default: 10).

// * **Take Profit (Pips) (tpPips):** The Take Profit level in pips (default: 20).

// * **Show Bollinger Bands (showBands):** A boolean value to show or hide the Bollinger Bands on the chart (default: true).

// * **Show Entry Signals (showSignals):** A boolean value to show or hide entry signals on the chart (default: true).

// How to Use:

// 1. Add the strategy to your TradingView chart.

// 2. Adjust the input parameters to optimize the strategy for your chosen instrument and timeframe. Pay close attention to the `Pip Value`.

// 3. Backtest the strategy over different periods to evaluate its performance.

// 4. Use the `Enable Long Positions` and `Enable Short Positions` settings to customize the strategy for specific market conditions (e.g., only long positions in an uptrend).

// Important Notes and Disclaimers:

// * **Backtesting Results:** Past performance is not indicative of future results. Backtesting results can be affected by various factors, including market volatility, slippage, and transaction costs.

// * **Risk Management:** This strategy is provided for informational and educational purposes only and should not be considered financial advice. Always use proper risk management techniques when trading. Adjust Stop Loss and Take Profit levels according to your risk tolerance.

// * **Slippage:** The strategy takes into account slippage by specifying a slippage parameter on the `strategy` declaration. However, real-world slippage may vary.

// * **Market Conditions:** The performance of this strategy can vary significantly depending on market conditions. It may perform well in trending markets but poorly in ranging or choppy markets.

// * **Pip Value Accuracy:** **Ensure the `Pip Value` is correctly set for the specific instrument you are trading. Incorrect pip value will result in incorrect stop loss and take profit placement.** This is critical.

// * **Broker Compatibility:** The strategy's performance may vary depending on your broker's execution policies and fees.

// * **Disclaimer:** I am not a financial advisor, and this script is not financial advice. Use this strategy at your own risk. I am not responsible for any losses incurred while using this strategy.

Bollinger Bounce Reversal Strategy – Visual EditionOverview:

The Bollinger Bounce Reversal Strategy – Visual Edition is designed to capture potential reversal moves at price extremes—often termed “bounce points”—by using a combination of technical indicators. The strategy integrates Bollinger Bands, MACD, and volume analysis, and it provides rich on‑chart visual cues to help traders understand its signals and conditions. Additionally, the strategy enforces a maximum of 5 trades per day and uses fixed risk management parameters. This publication is intended for educational purposes and offers a systematic, transparent approach that you can further adjust to fit your market or risk profile.

How It Works:

Bollinger Bands:

A 20‑period simple moving average (SMA) and a user‑defined standard deviation multiplier (default 2.0) are used to calculate the Bollinger Bands.

When the price reaches or crosses these bands (i.e. falls below the lower band or rises above the upper band), it suggests that the price is in an extreme, potentially oversold or overbought, state.

MACD Filter:

The MACD (calculated with standard lengths, e.g. 12, 26, 9) provides momentum information.

For a bullish (long) signal, the MACD line should be above its signal line; for a bearish (short) signal, the MACD line should be below.

Volume Confirmation:

The strategy uses a 20‑period volume moving average to determine if current volume is strong enough to validate a signal.

A signal is confirmed only if the current volume is at or above a specified multiple (by default, 1.0×) of this moving average, ensuring that the move is supported by increased market participation.

Visual Cues:

Bollinger Bands and Fill: The basis (SMA), upper, and lower Bollinger Bands are plotted, and the area between the upper and lower bands is filled with a semi‑transparent color.

Signal Markers: When a long or short signal is generated, corresponding markers (labels) appear on the chart.

Background Coloring: The chart’s background changes color (green for long signals and red for short signals) on the bars where signals occur.

Information Table: An on‑chart table displays key indicator values (MACD, signal line, volume, average volume) and the number of trades executed that day.

Entry Conditions:

Long Entry:

A long trade is triggered when the previous bar’s close is below the lower Bollinger Band and the current bar’s close crosses above it, combined with a bullish MACD condition and strong volume.

Short Entry:

A short trade is triggered when the previous bar’s close is above the upper Bollinger Band and the current bar’s close crosses below it, with a bearish MACD condition and high volume.

Risk Management:

Daily Trade Limit: The strategy restricts trading to no more than 5 trades per day.

Stop-Loss and Take-Profit:

For each position, a stop loss is set at a fixed percentage away from the entry price (typically 2%), and a take profit is set to target a 1:2 risk-reward ratio (typically 4% from the entry price).

Backtesting Setup:

Initial Capital: $10,000

Commission: 0.1% per trade

Slippage: 1 tick per bar

These realistic parameters help ensure that backtesting results reflect the conditions of an average trader.

Disclaimer:

Past performance is not indicative of future results. This strategy is experimental and provided solely for educational purposes. It is essential to backtest extensively and paper trade before any live deployment. All risk management practices are advisory, and you should adjust parameters to suit your own trading style and risk tolerance.

Conclusion:

By combining Bollinger Bands, MACD, and volume analysis, the Bollinger Bounce Reversal Strategy – Visual Edition provides a clear, systematic method to identify potential reversal opportunities at price extremes. The added visual cues help traders quickly interpret signals and assess market conditions, while strict risk management and a daily trade cap help keep trading disciplined. Adjust and refine the settings as needed to better suit your specific market and risk profile.

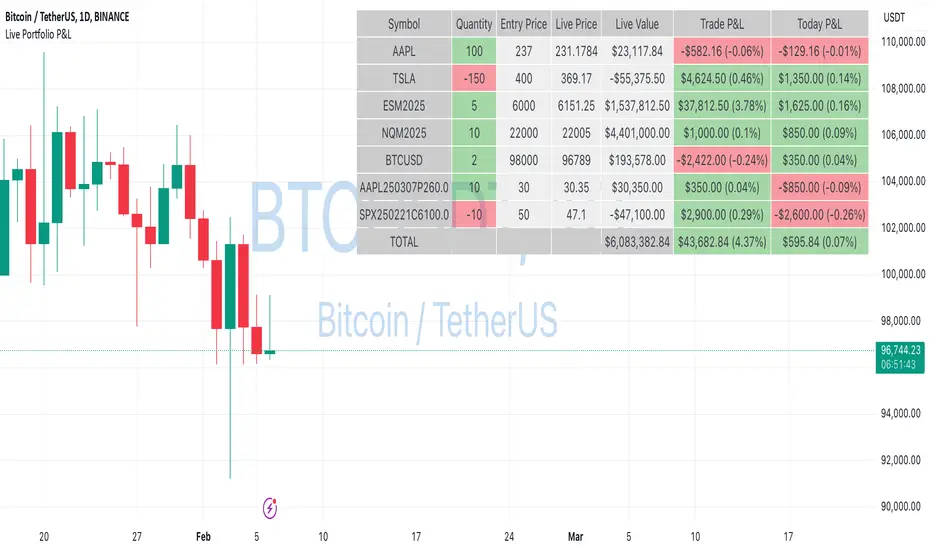

Live Portfolio P<his script calculates live P&L (Profit & Loss) for up to 40 instruments — stocks, ETFs, options, futures, and Forex pairs supported by TradingView. Instead of juggling numerous inputs, you paste your portfolio in CSV format into a single text field, and the script handles the rest. It parses each position and displays a comprehensive table showing the symbol, current price, position value, total P&L, and today’s P&L—all updated in real time.

Key Features

CSV Portfolio Input – Effortlessly import all your positions at once without filling in multiple fields. You can export the position from your broker, save it in the required format, and paste it into this script.

Supports Various Asset Classes – Works with any instrument that TradingView provides data for, including futures, options, and Forex.

Up to 40 Instruments – Track a broad and diverse set of holdings in one place.

Real-Time Updates – Get immediate feedback on live price changes, total value, and current P&L.

Today’s P&L – Monitor your daily performance to gauge short-term trends.

CSV is consumed in the following format:

Symbol (supported TradingView instruments)

Entry Price

Quantity (negative for short position)

Lot Size (for futures/options, it might not be one)

For example:

AAPL,237,100,1

TSLA,400,-150,1

ESM2025,6000,5,50

Planned Enhancements

Multi-Currency Support – Automatically convert and display your positions’ values in different currencies.

Advanced Metrics – Get deeper insights with calculations for drawdown, Sharpe ratio, and more.

Risk Management Tools – Set stop-loss and take-profit levels and receive alerts when thresholds are hit.

Option Greeks & Margin Calculations – Manage complex option strategies and track margin requirements.

Questions for You

What additional features would you like to see?

Are there any specific metrics or analytics you’d find especially valuable?

How might this script fit into your current trading workflow?

Feel free to share your thoughts and suggestions. Your feedback will help shape future updates and make this tool even more helpful for traders like you!

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Daily COC Strategy with SHERLOCK WAVESThis indicator implements a unique trading strategy known as the "Daily COC (Candle Over Candle) Strategy" enhanced with "SHERLOCK WAVES" for pattern recognition. It's designed for traders looking to capitalize on specific candlestick formations with a negative risk-reward ratio, with the aim of achieving a high win rate (over 70%) through numerous trading opportunities, despite each trade having a higher risk relative to the reward.

Key Features:

Pattern Recognition: Identifies a setup based on three consecutive candles - a red candle followed by a shooting star, then an entry candle that does not break below the shooting star's low.

Negative Risk/Reward Trade Selection: Focuses on entries where the potential stop loss is greater than the take profit, banking on a high win rate to offset the individual trade's negative risk-reward ratio.

Visual Signals:

Green Label: Marks potential entry points at the high of the candle before the entry.

Green Dot: Indicates a winning trade closure.

Red Dot: Signals a losing trade closure.

Blue Circle: Warns when the current candle is within 2% of breaking above the previous candle's high, suggesting a potential setup is developing.

Green Circle: Plots the take profit level.

Red Circle: Plots the stop loss level.

Dynamic Statistics: A live updating label showing the number of trades, wins, losses, open trades, current account balance, and win percentage.

Customizable Parameters:

Risk % per Trade: Adjust the percentage of your account balance you're willing to risk on each trade.

Initial Account Balance: Set your starting balance for tracking performance.

Start Date for Strategy: Define when the strategy should start calculating from, allowing for backtesting.

Alerts:

An alert condition is set for when a potential trade setup is developing, helping traders prepare for entries.

Usage Tips:

This strategy is predicated on the idea that a high win rate can compensate for the negative risk-reward ratio of individual trades. It might not suit all market conditions or traders' risk profiles.

Use this strategy in conjunction with other analysis methods to validate trade setups.

Note: Always backtest thoroughly before applying to live markets. Consider this tool as part of a broader trading strategy, not a standalone solution. Monitor your win rate and adjust your risk management accordingly to ensure the strategy remains profitable over time.

This description now correctly explains the purpose behind the negative risk-reward ratio in the context of your trading strategy.

Statistical Arbitrage Pairs Trading - Long-Side OnlyThis strategy implements a simplified statistical arbitrage (" stat arb ") approach focused on mean reversion between two correlated instruments. It identifies opportunities where the spread between their normalized price series (Z-scores) deviates significantly from historical norms, then executes long-only trades anticipating reversion to the mean.

Key Mechanics:

1. Spread Calculation: The strategy computes Z-scores for both instruments to normalize price movements, then tracks the spread between these Z-scores.

2. Modified Z-Score: Uses a robust measure combining the median and Median Absolute Deviation (MAD) to reduce outlier sensitivity.

3. Entry Signal: A long position is triggered when the spread’s modified Z-score falls below a user-defined threshold (e.g., -1.0), indicating extreme undervaluation of the main instrument relative to its pair.

4. Exit Signal: The position closes automatically when the spread reverts to its historical mean (Z-score ≥ 0).

Risk management:

Trades are sized as a percentage of equity (default: 10%).

Includes commissions and slippage for realistic backtesting.

hector mena Breakout Trading with ATR, RSI and MA CrossTitle: Breakout Trading Strategy with ATR, RSI, and Moving Average Cross

Description (English):

This script combines key technical indicators—ATR (Average True Range), RSI (Relative Strength Index), and Moving Averages—to provide a comprehensive breakout trading strategy. It is designed to help traders identify significant breakout levels and confirm signals with momentum and trend analysis.

How It Works:

ATR for Breakout Levels:

The ATR is used to calculate dynamic breakout levels by adjusting the highest resistance and lowest support levels with a customizable multiplier. This ensures that breakout levels adapt to market volatility.

RSI for Momentum Confirmation:

The RSI identifies overbought and oversold conditions, providing an additional layer of confirmation for breakouts. A breakout accompanied by an RSI signal can indicate stronger momentum.

Moving Average Cross for Trend Validation:

Two simple moving averages (short-term and long-term) are included to validate the trend. A crossover suggests a potential change in trend, aligning with breakout signals.

Why Combine These Indicators?

The ATR ensures breakout levels are realistic and volatility-adjusted.

The RSI avoids false signals by confirming if the price has momentum during a breakout.

Moving Average crossovers add trend-following confirmation, helping traders align with market direction.

The combination provides a robust framework to filter out false signals and improve the reliability of trading decisions.

Key Features:

Breakout Levels: Upper and lower breakout levels dynamically calculated using ATR.

RSI Confirmation: Visual overbought (70) and oversold (30) levels and RSI plot.

Trend Validation: Short and long-term moving averages plotted on the chart with crossover signals.

Visual Alerts: Clear "BUY" and "SELL" labels for actionable signals.

Custom Alerts: Configurable alerts for breakouts and moving average crossovers.

How to Use It:

Adjust the parameters (ATR length, multiplier, RSI length, and moving averages) based on your trading strategy.

Look for "BUY" signals when:

Price breaks above the resistance level, and RSI indicates oversold conditions.

Moving averages cross bullishly.

Look for "SELL" signals when:

Price breaks below the support level, and RSI indicates overbought conditions.

Moving averages cross bearishly.

Use alerts for automated notifications about potential trades.

Notes:

This script is intended for educational purposes. Use it alongside proper risk management techniques and backtesting.

Always test in demo mode before applying it to live trading.

[blackcat] L2 Waveband Trading█ OVERVIEW

The Waveband Trading script calculates trading signals based on a modified Relative Strength Index (RSI)-like system combined with specific price action criteria. It plots two lines representing different smoothed RSI-like indicators and marks potential buying opportunities labeled as "S" for stronger trends and "B" for weaker but still favorable ones.

█ LOGICAL FRAMEWORK

The script begins by defining the waveband_trading_signals function which computes RSI-like metrics and determines buy signals under certain conditions. The main sections include input parameter definitions, function calls, data processing within the function, and plot commands for visual representation. Data flows from historical OHLCV data to various technical computations like EMAs and SMAs before being evaluated against user-defined thresholds to generate trade signals.

█ CUSTOM FUNCTIONS

Waveband Trading Signals:

• Purpose: Computes waveband trading signals using a customized version of the RSI indicator.

• Parameters:

— overboughtLevel: Threshold level indicating market overbought condition.

— oversoldLevel: Threshold level indicating market oversold condition.

— strongHoldLevel: Strong hold condition threshold between neutral and overbought states.

— moderateHoldLevel: Moderate hold condition threshold below strong hold level.

• [b>Returns: A tuple containing:

— k: Smoothed RSI-like metric.

— d: Further smoothed version of 'k'.

— buySignalStrong: Boolean indicating a strong trend buy signal.

— buySignalWeak: Boolean indicating a weak but promising buy signal.

█ KEY POINTS AND TECHNIQUES

• Utilizes EMA and SMA functions to smooth out price variations effectively.

• Employs crossover logic between fast ('k') and slow ('d') indicators to identify entry points.

• Incorporates volume checks ensuring increasing interest in trades aligns with upwards momentum.

• Leverages predefined threshold levels allowing flexibility to adapt to varying market conditions.

• Uses the new labeling feature ( label.new ) introduced in Pine Script v5 for marking significant chart events visually.

█ EXTENDED KNOWLEDGE AND APPLICATIONS