Channel Based Zigzag [HeWhoMustNotBeNamed]🎲 Concept

Zigzag is built based on the price and number of offset bars. But, in this experiment, we build zigzag based on different bands such as Bollinger Band, Keltner Channel and Donchian Channel. The process is simple:

🎯 Derive bands based on input parameters

🎯 High of a bar is considered as pivot high only if the high price is above or equal to upper band.

🎯 Similarly low of a bar is considered as pivot low only if low price is below or equal to lower band.

🎯 Adding the pivot high/low follows same logic as that of regular zigzag where pivot high is always followed by pivot low and vice versa.

🎯 If the new pivot added is of same direction as that of last pivot, then both pivots are compared with each other and only the extreme one is kept. (Highest in case of pivot high and lowest in case of pivot low)

🎯 If a bar has both pivot high and pivot low - pivot with same direction as previous pivot is added to the list first before adding the pivot with opposite direction.

🎲 Use Cases

Can be used for pattern recognition algorithms instead of standard zigzag. This will help derive patterns which are relative to bands and channels.

Example: John Bollinger explains how to manually scan double tap using Bollinger Bands in this video: www.youtube.com This modified zigzag base can be used to achieve the same using algorithmic means.

🎲 Settings

Few simple configurations which will let you select the band properties. Notice that there is no zigzag length here. All the calculations depend on the bands.

With bands display, indicator looks something like this

Note that pivots do not always represent highest/lowest prices. They represent highest/lowest price relative to bands.

As mentioned many times, application of zigzag is not for buying at lower price and selling at higher price. It is mainly used for pattern recognition either manually or via algorithms. Lets build new Harmonic, Chart patterns, Trend Lines using the new zigzag?

Search in scripts for "high low"

HH-LL ZZAnother ZigZag, yes...

I believe though this concerns another angle/principle, therefore I wanted to share

How does it work?

Given:

source for level breach -> close

X breaches -> 3

Let's say this is the latest found 'lower low' (LL - blue dot under bar):

This bar has been triggered because 3 bars closed under low of previous 'trigger bar' (TB )

The high and low of this new TB will act as triggers

(aqua blue lines, seen in image above)

Then there are 2 options:

- again 3 bars closes under the latest TB , in that case the TB moves to that new LL.

- 3 bars closes higher than the high of previous TB

The high and low of this new TB act again as trigger

If a new TB LL/HH is found, the script checks previous LL/HH

and searches the highest/lowest point in between.

If necessary, the temporary highest/lowest will be adjusted:

Another example:

The last 2 points can change (repaint).

Yellow coloured lines/labels are set and won't change anymore.

Concluded:

In case of these settings:

source for level breach -> close

X breaches -> 3

once a new TB is found, the high and low act as trigger lines

- when 3 bars closes under that low , a new LL is found, this will be the new TB

- when 3 bars closes above that high , a new HH is found, this will be the new TB

and so on...

Settings:

source for level breach -> close or high/low - H/L

X breaches -> 1 -> 10

line style -> solid, dotted, dashed

show level breaches -> new found TB (blue/lime coloured)

show Support/Resistance (lines at the right)

repaint warning can be removed

show labels / lines

This ZZ can be used for Harmonic patterns, Trend evaluation, support/resistance,...

In this script, I also used new features

- text_font_family = font.family_monospace -> link

- display=display.pane -> link

Cheers!

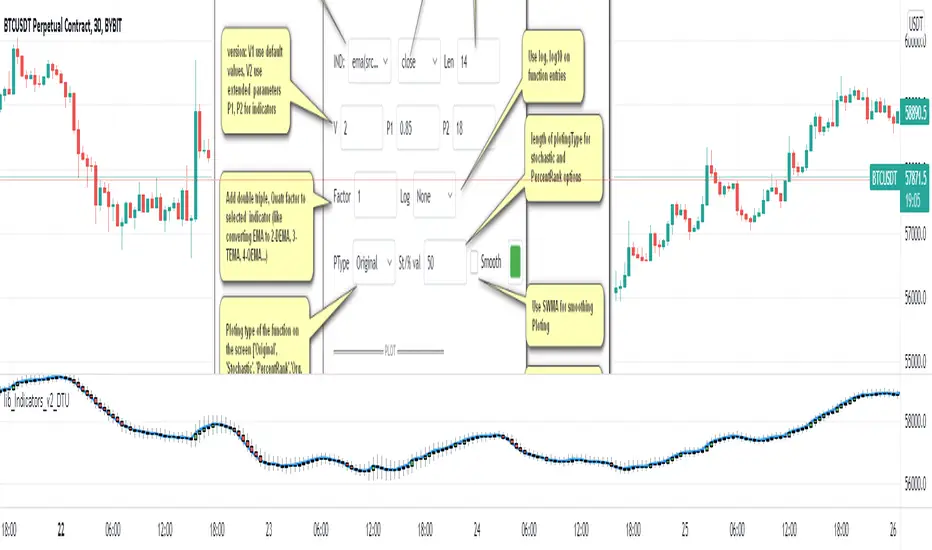

lib_Indicators_v2_DTULibrary "lib_Indicators_v2_DTU"

This library functions returns included Moving averages, indicators with factorization, functions candles, function heikinashi and more.

Created it to feed as backend of my indicator/strategy "Indicators & Combinations Framework Advanced v2 " that will be released ASAP.

This is replacement of my previous indicator (lib_indicators_DT)

I will add an indicator example which will use this indicator named as "lib_indicators_v2_DTU example" to help the usage of this library

Additionally library will be updated with more indicators in the future

NOTES:

Indicator functions returns only one series :-(

plotcandle function returns candle series

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma(src,len,offset=0.85,sigma=6)', //Arnaud Legoux Moving Average

ama = 'ama(src,len,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', //Accumulation/distribution index.

cma = 'cma(src,len)', //Corrective Moving average

dema = 'dema(src,len)', //Double EMA (Same as EMA with 2 factor)

ema = 'ema(src,len)', //Exponential Moving Average

gmma = 'gmma(src,len)', //Geometric Mean Moving Average

hghst = 'highest(src,len)', //Highest value for a given number of bars back.

hl2ma = 'hl2ma(src,len)', //higest lowest moving average

hma = 'hma(src,len)', //Hull Moving Average.

lgAdt = 'lagAdapt(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre(src,len)', //Ehler's Laguerre filter

lsrcp = 'lesrcp(src,len)', //lowest exponential esrcpanding moving line

lexp = 'lexp(src,len)', //lowest exponential expanding moving line

linrg = 'linreg(src,len,loffset=1)', //Linear regression

lowst = 'lowest(src,len)', //Lovest value for a given number of bars back.

pcnl = 'percntl(src,len)', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli(src,len)', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema(src,len)', //Range EMA (REMA)

rma = 'rma(src,len)', //Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma(src,len)', //Smoothed Moving Average

smma = 'smma(src,len)', //Smoothed Moving Average

supr2 = 'super2(src,len)', //Ehler's super smoother, 2 pole

supr3 = 'super3(src,len)', //Ehler's super smoother, 3 pole

strnd = 'supertrend(src,len,period=3)', //Supertrend indicator

swma = 'swma(src,len)', //Sine-Weighted Moving Average

tema = 'tema(src,len)', //Triple EMA (Same as EMA with 3 factor)

tma = 'tma(src,len)', //Triangular Moving Average

vida = 'vida(src,len)', //Variable Index Dynamic Average

vwma = 'vwma(src,len)', //Volume Weigted Moving Average

wma = 'wma(src,len)', //Weigted Moving Average

angle = 'angle(src,len)', //angle of the series (Use its Input as another indicator output)

atr = 'atr(src,len)', //average true range. RMA of true range.

bbr = 'bbr(src,len,mult=1)', //bollinger %%

bbw = 'bbw(src,len,mult=2)', //Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci(src,len)', //commodity channel index

cctbb = 'cctbbo(src,len)', //CCT Bollinger Band Oscilator

chng = 'change(src,len)', //Difference between current value and previous, source - source .

cmo = 'cmo(src,len)', //Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog(src,len)', //The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve(src,len)', //Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl(src,len)', //Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count = 'count(src,len)', //green avg - red avg

dev = 'dev(src,len)', //ta.dev() Measure of difference between the series and it's ta.sma

fall = 'falling(src,len)', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr(src,len,mult=2)', //Keltner Channels Range

kcw = 'kcw(src,len,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd(src,len)', //macd

mfi = 'mfi(src,len)', //Money Flow Index

nvi = 'nvi()', //Negative Volume Index

obv = 'obv()', //On Balance Volume

pvi = 'pvi()', //Positive Volume Index

pvt = 'pvt()', //Price Volume Trend

rise = 'rising(src,len)', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc(src,len)', //Rate of Change

rsi = 'rsi(src,len)', //Relative strength Index

smosc = 'smi_osc(src,len,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig(src,len,fast=5, slow=34)', //smi Signal

stdev = 'stdev(src,len)', //Standart deviation

trix = 'trix(src,len)' , //the rate of change of a triple exponentially smoothed moving average.

tsi = 'tsi(src,len)', //True Strength Index

vari = 'variance(src,len)', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc(src,len)', //Williams %R

wad = 'wad()', //Williams Accumulation/Distribution.

wvad = 'wvad()' //Williams Variable Accumulation/Distribution.

}

f_func(string, float, simple, float, float, float, simple) f_func Return selected indicator value with different parameters. New version. Use extra parameters for available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

Returns: float Return calculated indicator value

fn_heikin(float, float, float, float) fn_heikin Return given src data (open, high,low,close) as heikin ashi candle values

Parameters:

float : o_ open value

float : h_ high value

float : l_ low value

float : c_ close value

Returns: float heikin ashi open, high,low,close vlues that will be used with plotcandle

fn_plotFunction(float, string, simple, bool) fn_plotFunction Return input src data with different plotting options

Parameters:

float : src_ indicator src_data or any other series.....

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

Returns: float

fn_funcPlotV2(string, float, simple, float, float, float, simple, string, simple, bool, bool) fn_funcPlotV2 Return selected indicator value with different parameters. New version. Use extra parameters fora available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return calculated indicator value

fn_factor(string, float, simple, float, float, float, simple, simple, string, simple, bool, bool) fn_factor Return selected indicator's factorization with given arguments

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

simple : int fact_ Add double triple, Quatr factor to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return result of the function

fn_plotCandles(string, simple, float, float, float, simple, string, simple, bool, bool, bool) fn_plotCandles Return selected indicator's candle values with different parameters also heikinashi is available

Parameters:

string : FuncType_ indicator from the indicator list

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

bool : plotheikin_ Use Heikin Ashi on Plot

Returns: float

[MF] Auto Fibonacci LevelsDescription:

Automatically draw Fibonacci Pivot levels based on the previous (day's, week's or month's)

Range ( High-Low ). The HLC3 is used as the default Pivot level.

Unlike the "Auto Fibonacci Levels", this variation does not update

Levels on current day even if the price goes past the R3/S3 levels.

Timeframes: 1D, 1W, 1M

Range = (High - Low) - From previous Day, Week or month.

FIB LEVELS:

- Yellow = Pivot and Pivot Zone (HLC3 by default)

- red = R1,S1 Levels 0.236 * Range

- Green = R2,S2 Levels 0.368 * Range

- Lime = R3,S3 Levels 0.618 * Range

- Blue = R4,S4 Levels 0.786 * Range

- Gray = R5,S5 Levels 1.000 * Range

- Lime = R6,S6 Levels 1.236 * Range

- Red = R7,S7 Levels 1.382 * Range

- Blue = R8,S8 Levels 1.618 * Range

- Green = R9,S9 Levels 2.000 * Range

CLASSIC LEVELS:

- Yellow = Pivot and Pivot Zone (HLC3)

- Green = R1,S1 Levels (Pivot*2 - Low), (Pivot*2 - High)

- Lime = R2,S2 Levels ( Pivot + Range), ( Pivot - Range)

- Lime = R3,S3 Levels (High + 2*( Pivot - Low)), (Low - 2*(High - Pivot ))

- Blue = R4,S4 Levels (High + 3*( Pivot - Low)), (Low - 3*(High - Pivot ))

Refrences:

- Auto Daily Fib Levels R3.0 by JustUncleL

- Auto Fib by TheYangGuizi

- Monthly Dynamic Range Levels (Fibonaci) V0 by RicardoSantos

Modifications:

- Added next FIB Levels. (changes during the current cycle)

- Added FIB 0.236 Levels

- Added Option to change the colors of the Fib Levels

- Changed Default colors to the colors of Tradingview

- Upgraded to Version4 Pinescript

supertrendHere is an extensive library on different variations of supertrend.

Library "supertrend"

supertrend : Library dedicated to different variations of supertrend

supertrend_atr(length, multiplier, atrMaType, source, highSource, lowSource, waitForClose, delayed) supertrend_atr: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

length : : ATR Length

multiplier : : ATR Multiplier

atrMaType : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

source : : Default is close. Can Chose custom source

highSource : : Default is high. Can also use close price for both high and low source

lowSource : : Default is low. Can also use close price for both high and low source

waitForClose : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

delayed : : if set to true lags supertrend atr stop based on target levels.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_bands(bandType, maType, length, multiplier, source, highSource, lowSource, waitForClose, useTrueRange, useAlternateSource, alternateSource, sticky) supertrend_bands: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

bandType : : Type of band used - can be bb, kc or dc

maType : : Moving Average type for Bands. This can be sma, ema, hma, rma, wma, vwma, swma

length : : Band Length

multiplier : : Std deviation or ATR multiplier for Bollinger Bands and Keltner Channel

source : : Default is close. Can Chose custom source

highSource : : Default is high. Can also use close price for both high and low source

lowSource : : Default is low. Can also use close price for both high and low source

waitForClose : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

useTrueRange : : Used for Keltner channel. If set to false, then high-low is used as range instead of true range

useAlternateSource : - Custom source is used for Donchian Chanbel only if useAlternateSource is set to true

alternateSource : - Custom source for Donchian channel

sticky : : if set to true borders change only when price is beyond borders.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_zigzag(length, history, useAlternateSource, alternateSource, source, highSource, lowSource, waitForClose, atrlength, multiplier, atrMaType) supertrend_zigzag: Zigzag pivot based supertrend

Parameters:

length : : Zigzag Length

history : : number of historical pivots to consider

useAlternateSource : - Custom source is used for Zigzag only if useAlternateSource is set to true

alternateSource : - Custom source for Zigzag

source : : Default is close. Can Chose custom source

highSource : : Default is high. Can also use close price for both high and low source

lowSource : : Default is low. Can also use close price for both high and low source

waitForClose : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrlength : : ATR Length

multiplier : : ATR Multiplier

atrMaType : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

taLibrary "ta"

█ OVERVIEW

This library holds technical analysis functions calculating values for which no Pine built-in exists.

Look first. Then leap.

█ FUNCTIONS

cagr(entryTime, entryPrice, exitTime, exitPrice)

It calculates the "Compound Annual Growth Rate" between two points in time. The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It only takes into account the prices of the two end points — not drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two instruments. Because it annualizes values, the function requires a minimum of one day between the two end points (annualizing returns over smaller periods of times doesn't produce very meaningful figures).

Parameters:

entryTime : The starting timestamp.

entryPrice : The starting point's price.

exitTime : The ending timestamp.

exitPrice : The ending point's price.

Returns: CAGR in % (50 is 50%). Returns `na` if there is not >=1D between `entryTime` and `exitTime`, or until the two time points have not been reached by the script.

█ v2, Mar. 8, 2022

Added functions `allTimeHigh()` and `allTimeLow()` to find the highest or lowest value of a source from the first historical bar to the current bar. These functions will not look ahead; they will only return new highs/lows on the bar where they occur.

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `high`.

Returns: (float) The highest value tracked.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `low`.

Returns: (float) The lowest value tracked.

█ v3, Sept. 27, 2022

This version includes the following new functions:

aroon(length)

Calculates the values of the Aroon indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the Aroon-Up and Aroon-Down values.

coppock(source, longLength, shortLength, smoothLength)

Calculates the value of the Coppock Curve indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

longLength (simple int) : (simple int) Number of bars for the fast ROC value (length).

shortLength (simple int) : (simple int) Number of bars for the slow ROC value (length).

smoothLength (simple int) : (simple int) Number of bars for the weigted moving average value (length).

Returns: (float) The oscillator value.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `source`.

dema2(src, length)

An alternate Double Exponential Moving Average (Dema) function to `dema()`, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `src`.

dm(length)

Calculates the value of the "Demarker" indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

ema2(src, length)

An alternate ema function to the `ta.ema()` built-in, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Number of bars (length).

Returns: (float) The exponentially weighted moving average of the `src`.

eom(length, div)

Calculates the value of the Ease of Movement indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

div (simple int) : (simple int) Divisor used for normalzing values. Optional. The default is 10000.

Returns: (float) The oscillator value.

frama(source, length)

The Fractal Adaptive Moving Average (FRAMA), developed by John Ehlers, is an adaptive moving average that dynamically adjusts its lookback period based on fractal geometry.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The fractal adaptive moving average of the `source`.

ft(source, length)

Calculates the value of the Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

ht(source)

Calculates the value of the Hilbert Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

ichimoku(conLength, baseLength, senkouLength)

Calculates values of the Ichimoku Cloud indicator, including tenkan, kijun, senkouSpan1, senkouSpan2, and chikou. NOTE: offsets forward or backward can be done using the `offset` argument in `plot()`.

Parameters:

conLength (int) : (series int) Length for the Conversion Line (Tenkan). The default is 9 periods, which returns the mid-point of the 9 period Donchian Channel.

baseLength (int) : (series int) Length for the Base Line (Kijun-sen). The default is 26 periods, which returns the mid-point of the 26 period Donchian Channel.

senkouLength (int) : (series int) Length for the Senkou Span 2 (Leading Span B). The default is 52 periods, which returns the mid-point of the 52 period Donchian Channel.

Returns: ( [float, float, float, float, float ]) A tuple of the Tenkan, Kijun, Senkou Span 1, Senkou Span 2, and Chikou Span values. NOTE: by default, the senkouSpan1 and senkouSpan2 should be plotted 26 periods in the future, and the Chikou Span plotted 26 days in the past.

ift(source)

Calculates the value of the Inverse Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

kvo(fastLen, slowLen, trigLen)

Calculates the values of the Klinger Volume Oscillator.

Parameters:

fastLen (simple int) : (simple int) Length for the fast moving average smoothing parameter calculation.

slowLen (simple int) : (simple int) Length for the slow moving average smoothing parameter calculation.

trigLen (simple int) : (simple int) Length for the trigger moving average smoothing parameter calculation.

Returns: ( [float, float ]) A tuple of the KVO value, and the trigger value.

pzo(length)

Calculates the value of the Price Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

rms(source, length)

Calculates the Root Mean Square of the `source` over the `length`.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The RMS value.

rwi(length)

Calculates the values of the Random Walk Index.

Parameters:

length (simple int) : (simple int) Lookback and ATR smoothing parameter length.

Returns: ( [float, float ]) A tuple of the `rwiHigh` and `rwiLow` values.

stc(source, fast, slow, cycle, d1, d2)

Calculates the value of the Schaff Trend Cycle indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

fast (simple int) : (simple int) Length for the MACD fast smoothing parameter calculation.

slow (simple int) : (simple int) Length for the MACD slow smoothing parameter calculation.

cycle (simple int) : (simple int) Number of bars for the Stochastic values (length).

d1 (simple int) : (simple int) Length for the initial %D smoothing parameter calculation.

d2 (simple int) : (simple int) Length for the final %D smoothing parameter calculation.

Returns: (float) The oscillator value.

stochFull(periodK, smoothK, periodD)

Calculates the %K and %D values of the Full Stochastic indicator.

Parameters:

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

stochRsi(lengthRsi, periodK, smoothK, periodD, source)

Calculates the %K and %D values of the Stochastic RSI indicator.

Parameters:

lengthRsi (simple int) : (simple int) Length for the RSI smoothing parameter calculation.

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

source (float) : (series int/float) Series of values to process. Optional. The default is `close`.

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

supertrend(factor, atrLength, wicks)

Calculates the values of the SuperTrend indicator with the ability to take candle wicks into account, rather than only the closing price.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is false.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

szo(source, length)

Calculates the value of the Sentiment Zone Oscillator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

t3(source, length, vf)

Calculates the value of the Tilson Moving Average (T3).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

t3Alt(source, length, vf)

An alternate Tilson Moving Average (T3) function to `t3()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

tema(source, length)

Calculates the value of the Triple Exponential Moving Average (TEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

tema2(source, length)

An alternate Triple Exponential Moving Average (TEMA) function to `tema()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

trima(source, length)

Calculates the value of the Triangular Moving Average (TRIMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `source`.

trima2(src, length)

An alternate Triangular Moving Average (TRIMA) function to `trima()`, which allows a "series int" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `src`.

trix(source, length, signalLength, exponential)

Calculates the values of the TRIX indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

signalLength (simple int) : (simple int) Length for smoothing the signal line.

exponential (simple bool) : (simple bool) Condition to determine whether exponential or simple smoothing is used. Optional. The default is `true` (exponential smoothing).

Returns: ( [float, float, float ]) A tuple of the TRIX value, the signal value, and the histogram.

uo(fastLen, midLen, slowLen)

Calculates the value of the Ultimate Oscillator.

Parameters:

fastLen (simple int) : (series int) Number of bars for the fast smoothing average (length).

midLen (simple int) : (series int) Number of bars for the middle smoothing average (length).

slowLen (simple int) : (series int) Number of bars for the slow smoothing average (length).

Returns: (float) The oscillator value.

vhf(source, length)

Calculates the value of the Vertical Horizontal Filter.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

vi(length)

Calculates the values of the Vortex Indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the viPlus and viMinus values.

vzo(length)

Calculates the value of the Volume Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

williamsFractal(period)

Detects Williams Fractals.

Parameters:

period (int) : (series int) Number of bars (length).

Returns: ( [bool, bool ]) A tuple of an up fractal and down fractal. Variables are true when detected.

wpo(length)

Calculates the value of the Wave Period Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

█ v7, Nov. 2, 2023

This version includes the following new and updated functions:

atr2(length)

An alternate ATR function to the `ta.atr()` built-in, which allows a "series float" `length` argument.

Parameters:

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The ATR value.

changePercent(newValue, oldValue)

Calculates the percentage difference between two distinct values.

Parameters:

newValue (float) : (series int/float) The current value.

oldValue (float) : (series int/float) The previous value.

Returns: (float) The percentage change from the `oldValue` to the `newValue`.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

highestSince(cond, source)

Tracks the highest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the highest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `high`.

Returns: (float) The highest `source` value since the last time the `cond` was `true`.

lowestSince(cond, source)

Tracks the lowest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the lowest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `low`.

Returns: (float) The lowest `source` value since the last time the `cond` was `true`.

relativeVolume(length, anchorTimeframe, isCumulative, adjustRealtime)

Calculates the volume since the last change in the time value from the `anchorTimeframe`, the historical average volume using bars from past periods that have the same relative time offset as the current bar from the start of its period, and the ratio of these volumes. The volume values are cumulative by default, but can be adjusted to non-accumulated with the `isCumulative` parameter.

Parameters:

length (simple int) : (simple int) The number of periods to use for the historical average calculation.

anchorTimeframe (simple string) : (simple string) The anchor timeframe used in the calculation. Optional. Default is "D".

isCumulative (simple bool) : (simple bool) If `true`, the volume values will be accumulated since the start of the last `anchorTimeframe`. If `false`, values will be used without accumulation. Optional. The default is `true`.

adjustRealtime (simple bool) : (simple bool) If `true`, estimates the cumulative value on unclosed bars based on the data since the last `anchor` condition. Optional. The default is `false`.

Returns: ( [float, float, float ]) A tuple of three float values. The first element is the current volume. The second is the average of volumes at equivalent time offsets from past anchors over the specified number of periods. The third is the ratio of the current volume to the historical average volume.

rma2(source, length)

An alternate RMA function to the `ta.rma()` built-in, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The rolling moving average of the `source`.

supertrend2(factor, atrLength, wicks)

An alternate SuperTrend function to `supertrend()`, which allows a "series float" `atrLength` argument.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is `false`.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

vStop(source, atrLength, atrFactor)

Calculates an ATR-based stop value that trails behind the `source`. Can serve as a possible stop-loss guide and trend identifier.

Parameters:

source (float) : (series int/float) Series of values that the stop trails behind.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

atrFactor (float) : (series int/float) The multiplier of the ATR value. Affects the maximum distance between the stop and the `source` value. A value of 1 means the maximum distance is 100% of the ATR value. Optional. The default is 1.

Returns: ( [float, bool ]) A tuple of the volatility stop value and the trend direction as a "bool".

vStop2(source, atrLength, atrFactor)

An alternate Volatility Stop function to `vStop()`, which allows a "series float" `atrLength` argument.

Parameters:

source (float) : (series int/float) Series of values that the stop trails behind.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

atrFactor (float) : (series int/float) The multiplier of the ATR value. Affects the maximum distance between the stop and the `source` value. A value of 1 means the maximum distance is 100% of the ATR value. Optional. The default is 1.

Returns: ( [float, bool ]) A tuple of the volatility stop value and the trend direction as a "bool".

Removed Functions:

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

trima2(src, length)

An alternate Triangular Moving Average (TRIMA) function to `trima()`, which allows a

"series int" length argument.

My:HTF O/H/L/C█ MY Higher Time Frame Open / High / Low / Close

This indicator shows one line per Higher Time Frame Price of Interest.

We are interested to know whether we are currently seeing support or resistance at previous daily / weekly / monthly price of interest.

Each price of interest can be displayed or hidden in the configuration. Each line has a label attached to it with the (short) label on it to help identifying what is this line.

Price of interest with (short) label :

Current Daily Open (CDO)

Current Daily High (CDH)

Current Daily Low (CDL)

Previous Daily Open (PDO)

Previous Daily High (PDH)

Previous Daily Low (PDL)

Previous Daily Close (PDC)

Current Weekly Open (CWO)

Current Weekly High (CWH)

Current Weekly Low (CWL)

Previous Weekly Open (PWO)

Previous Weekly High (PWH)

Previous Weekly Low (PWL)

Previous Weekly Close (PWC)

Current Monthly Open (CMO)

Current Monthly High (CMH)

Current Monthly Low (CML)

Previous Monthly Open (PMO)

Previous Monthly High (PMH)

Previous Monthly Low (PML)

Previous Monthly Close (PMC)

Volume EffectivenessI have been trying to work with volume as an indicator for quite some time, as it holds qualities as a 'leading indicator'.

However, please note that any indicator which to some extent predict a future trend has its issues as it can be misleading.

But, in some datasets in a selected timeframe the leading properties of volume as an indicator are useful.

So this script is not too complicated. It shows a numeric which resembles the 'effectiveness of volume' in moving price.

For example, if a small volume creates a large price change - the Volume Effectiveness indicator will be high and show a spike

Whereas, if a large volume creates a small price change - the Volume Effectiveness indicator will be low

I used 3 metrics to represent Volume Effectiveness (these are different colors on the bar chart)

One price difference is the absolute(high - low) for each bar

Another is the absolute(open - close)

The 'open-close' is smaller than the 'high-low', so note this when viewing the bar charts

The final metric depends on if the open is greater than the close or vice-versa

But it considers the 'absolute(high-low)' and the difference between the open and the high (or low) and the close and the low (or high)

So the final metric is the largest of the 3 metrics and is generally the most useful of the 3 however, the other 2 are displayed to provide a better understanding of what 'Volume Effectiveness' displays

Note, I use absolute values so they are only positive, i.e. there are no negative values to represent a price drop within a bar

So, why is this indicator useful - its because volume is a leading indicator

A decreasing volume tends to suggest a price change is coming

Also, when the volume within a bar is very small, its Volume Effectiveness tends to go very high

That means a small trade volume creates a relatively large change in price

This is ideal conditions for a big pump (or big dump - although this indicator seems to work better before pumps)

A large spike in the Volume Effectiveness is commonly/sometimes preceding a big pump

So watch this indicator - and if there is a big spike - evaluate other market conditions to consider getting into position

Large spikes in the Volume Effectiveness can precede big price changes and therefore can provide a leading indication before a pump or dump

Timeframe is important - I found on the daily timeframe this indicator did not provide sufficient lead to be useful. Similarly on the <15min timeframe the spikes were not highly correlated with pumps/dumps

However, in medium timeframes (15mins, 1hour, 4hours) this indicator can be useful for predicting sizeable price changes.

HhLl-OscilatorSimple oscillator which checks how many highs and how many lows the price is making. Parameters are as explained below:

lookback - Checks how many highs and lows it is making in these many bars. Sum of all highs and lows are taken for plotting.

periods - Initial period to check high and lows

multiples - Number of multiples on initial period for which highs and lows are checked

colorCandles - CandleColor based on the oscillator

If periods is 20 and multiples is 5 and loopback is 10

Indicator checks for last 10 bars how many highs/lows are made for 20, 40, 60, 80 and 100 periods. Sum of all highs and lows are plotted on the oscillator overlay

Expanded Floor PivotsHello Everyone,

The Expanded Floor Pivots is introduced in the book "Secrets of a Pivot Boss: Revealing Proven Methods for Profiting in the Market " by Franklin Ochoa. He added four new levels: S4, R4, BC and TC. There are many great ideas in the book, such using these levels, following trend, time price opportunity and much more. (Thanks to @tonyjab for pushing me to read this book)

The definition/formula of the levels defined in the book:

r1 = 2 * pivot - Low

r2 = pivot + (High - Low)

r3 = r1 + (High - Low)

r4 = r3 + (r2 - r1)

tc = (pivot - bc) + pivot

pivot = (High + Low + Close) / 3

bc = (High + Low) / 2

s1 = 2 * pivot - High

s2 = pivot - (High - Low)

s3 = s1 - (High - Low)

s4 = s3 - (s1 - s2)

The area between TC and BC is used as Pivot Channel, (blue area in the chart). you can see how it helps on identifying the trend.

Options:

By default the script decides Higher Time Frame but if you want you can set HTF as you wish.

You can choose line style as: Solid, Circles or Cross

and also you have option to show only last period or all historical levels.

Enjoy!

Volume Profile Free Ultra SLI (100 Levels Value Area VWAP) - RRBVolume Profile Free Ultra SLI by RagingRocketBull 2019

Version 1.0

This indicator calculates Volume Profile for a given range and shows it as a histogram consisting of 100 horizontal bars.

This is basically the MAX SLI version with +50 more Pinescript v4 line objects added as levels.

It can also show Point of Control (POC), Developing POC, Value Area/VWAP StdDev High/Low as dynamically moving levels.

Free accounts can't access Standard TradingView Volume Profile, hence this indicator.

There are several versions: Free Pro, Free MAX SLI, Free Ultra SLI, Free History. This is the Free Ultra SLI version. The Differences are listed below:

- Free Pro: 25 levels, +Developing POC, Value Area/VWAP High/Low Levels, Above/Below Area Dimming

- Free MAX SLI: 50 levels, 2x SLI modes for Buy/Sell or even higher res 150 levels

- Free Ultra SLI: 100 levels, packed to the limit, 2x SLI modes for Buy/Sell or even higher res 300 levels

- Free History: auto highest/lowest, historic poc/va levels for each session

Features:

- High-Res Volume Profile with up to 100 levels (line implementation)

- 2x SLI modes for even higher res: 300 levels with 3x vertical SLI, 100 buy/sell levels with 2x horiz SLI

- Calculate Volume Profile on full history

- POC, Developing POC Levels

- Buy/Sell/Total volume modes

- Side Cover

- Value Area, VAH/VAL dynamic levels

- VWAP High/Low dynamic levels with Source, Length, StdDev as params

- Show/Hide all levels

- Dim Non Value Area Zones

- Custom Range with Highlighting

- 3 Anchor points for Volume Profile

- Flip Levels Horizontally

- Adjustable width, offset and spacing of levels

- Custom Color for POC/VA/VWAP levels, Transparency for buy/sell levels

WARNING:

- Compilation Time: 1 min 20 sec

Usage:

- specify max_level/min_level/spacing (required)

- select range (start_bar, range length), confirm with range highlighting

- select volume type: Buy/Sell/Total

- select mode Value Area/VWAP to show corresponding levels

- flip/select anchor point to position the buy/sell levels

- use Horiz Buy/Sell SLI mode with 100 or Vertical SLI with 300 levels if needed

- use POC/Developing POC/VA/VWAP High/Low as S/R levels. Usually daily values from 1-3 days back are used as levels for the current day.

SLI:

use SLI modes to extend the functionality of the indicator:

- Horiz Buy/Sell 2x SLI lets you view 100 Buy/Sell Levels at the same time

- Vertical Max_Vol 3x SLI lets you increase the resolution to 300 levels

- you need at least 2 instances of the indicator attached to the same chart for SLI to work

1) Enable Horiz SLI:

- attach 2 indicator instances to the chart

- make sure all instances have the same min_level/max_level/range/spacing settings

- select volume type for each instance: you can have a buy/sell or buy/total or sell/total SLI. Make sure your buy volume instance is the last attached to be displayed on top of sell/total instances without overlapping.

- set buy_sell_sli_mode to true for indicator instances with volume_type = buy/sell, for type total this is optional.

- this basically tells the script to calculate % lengths based on total volume instead of individual buy/sell volumes and use ext offset for sell levels

- Sell Offset is calculated relative to Buy Offset to stack/extend sell after buy. Buy Offset = Zero - Buy Length. Sell Offset = Buy Offset - Sell Length = Zero - Buy Length - Sell Length

- there are no master/slave instances in this mode, all indicators are equal, poc/va levels are not affected and can work independently, i.e. one instance can show va levels, another - vwap.

2) Enable Vertical SLI:

- attach the first instance and evaluate the full range to roughly determine where is the highest max_vol/poc level i.e. 0..20000, poc is in the bottom half (third, middle etc) or

- add more instances and split the full vertical range between them, i.e. set min_level/max_level of each corresponding instance to 0..10000, 10000..20000 etc

- make sure all instances have the same range/spacing settings

- an instance with a subrange containing the poc level of the full range is now your master instance (bottom half). All other instances are slaves, their levels will be calculated based on the max_vol/poc of the master instance instead of local values

- set show_max_vol_sli to true for the master instance. for slave instances this is optional and can be used to check if master/slave max_vol values match and slave can read the master's value. This simply plots the max_vol value

- you can also attach all instances and set show_max_vol_sli to true in all of them - the instance with the largest max_vol should become the master

Auto/Manual Ext Max_Vol Modes:

- for auto vertical max_vol SLI mode set max_vol_sli_src in all slave instances to the max_vol of the master indicator: "VolumeProfileFree_MAX_RRB: Max Volume for Vertical SLI Mode". It can be tricky with 2+ instances

- in case auto SLI mode doesn't work - assign max_vol_sli_ext in all slave instances the max_vol value of the master indicator manually and repeat on each change

- manual override max_vol_sli_ext has higher priority than auto max_vol_sli_src when both values are assigned, when they are 0 and close respectively - SLI is disabled

- master/slave max_vol values must match on each bar at all times to maintain proper level scale, otherwise slave's levels will look larger than they should relative to the master's levels.

- Max_vol (red) is the last param in the long list of indicator outputs

- the only true max_vol/poc in this SLI mode is the master's max_vol/poc. All poc/va levels in slaves will be irrelevant and are disabled automatically. Slaves can only show VWAP levels.

- VA Levels of the master instance in this SLI mode are calculated based on the subrange, not the whole range and may be inaccurate. Cross check with the full range.

WARNING!

- auto mode max_vol_sli_src is experimental and may not work as expected

- you can only assign auto mode max_vol_sli_src = max_vol once due to some bug with unhandled exception/buffer overflow in Tradingview. Seems that you can clear the value only by removing the indicator instance

- sometimes you may see a "study in error state" error when attempting to set it back to close. Remove indicator/Reload chart and start from scratch

- volume profile may not finish to redraw and freeze in an ugly shape after an UI parameter change when max_vol_sli_src is assigned a max_vol value. Assign it to close - VP should redraw properly, but it may not clear the assigned max_vol value

- you can't seem to be able to assign a proper auto max_vol value to the 3rd slave instance

- 2x Vertical SLI works and tested in both auto/manual, 3x SLI - only manual seems to work (you can have a mixed mode: 2nd instance - auto, 3rd - manual)

Notes:

- This code uses Pinescript v3 compatibility framework

- This code is 20x-30x faster (main for cycle is removed) especially on lower tfs with long history - only 4-5 sec load/redraw time vs 30-60 sec of the old Pro versions

- Instead of repeatedly calculating the total sum of volumes for the whole range on each bar, vol sums are now increased on each bar and passed to the next in the range making it a per range vs per bar calculation that reduces time dramatically

- 100 levels consist of 50 main plot levels and 50 line objects used as alternate levels, differences are:

- line objects are always shown on top of other objects, such as plot levels, zero line and side cover, it's not possible to cover/move them below.

- all line objects have variable lengths, use actual x,y coords and don't need side cover, while all plot levels have a fixed length of 100 bars, use offset and require cover.

- all key properties of line objects, such as x,y coords, color can be modified, objects can be moved/deleted, while this is not possible for static plot levels.

- large width values cause line objects to expand only up/down from center while their length remains the same and stays within the level's start/end points similar to an area style.

- large width values make plot levels expand in all directions (both h/v), beyond level start/end points, sometimes overlapping zero line, making them an inaccurate % length representation, as opposed to line objects/plot levels with area style.

- large width values translate into different widths on screen for line objects and plot levels.

- you can't compensate for this unwanted horiz width expansion of plot levels because width uses its own units, that don't translate into bars/pixels.

- line objects are visible only when num_levels > 50, plot levels are used otherwise

- Since line objects are lines, plot levels also use style line because other style implementations will break the symmetry/spacing between levels.

- if you don't see a volume profile check range settings: min_level/max_level and spacing, set spacing to 0 (or adjust accordingly based on the symbol's precision, i.e. 0.00001)

- you can view either of Buy/Sell/Total volumes, but you can't display Buy/Sell levels at the same time using a single instance (this would 2x reduce the number of levels). Use 2 indicator instances in horiz buy/sell sli mode for that.

- Volume Profile/Value Area are calculated for a given range and updated on each bar. Each level has a fixed length. Offsets control visible level parts. Side Cover hides the invisible parts.

- Custom Color for POC/VA/VWAP levels - UI Style color/transparency can only change shape's color and doesn't affect textcolor, hence this additional option

- Custom Width - UI Style supports only width <= 4, hence this additional option

- POC is visible in both modes. In VWAP mode Developing POC becomes VWAP, VA High and Low => VWAP High and Low correspondingly to minimize the number of plot outputs

- You can't change buy/sell level colors from input (only transparency) - this requires 2x plot outputs => 2x reduces the number of levels to fit the max 64 limit. That's why 2 additional plots are used to dim the non Value Area zones

- You can change level transparency of line objects. Due to Pinescript limitations, only discrete values are supported.

- Inverse transp correlation creates the necessary illusion of "covered" line objects, although they are shown on top of the cover all the time

- If custom lines_transp is set the illusion will break because transp range can't be skewed easily (i.e. transp 0..100 is always mapped to 100..0 and can't be mapped to 50..0)

- transparency can applied to lines dynamically but nva top zone can't be completely removed because plot/mixed type of levels are still used when num_levels < 50 and require cover

- transparency can't be applied to plot levels dynamically from script this can be done only once from UI, and you can't change plot color for the past length bars

- All buy/sell volume lengths are calculated as % of a fixed base width = 100 bars (100%). You can't set show_last from input to change it

- Range selection/Anchoring is not accurate on charts with time gaps since you can only anchor from a point in the future and measure distance in time periods, not actual bars, and there's no way of knowing the number of future gaps in advance.

- Adjust Width for Log Scale mode now also works on high precision charts with small prices (i.e. 0.00001)

- in Adjust Width for Log Scale mode Level1 width extremes can be capped using max deviation (when level1 = 0, shift = 0 width becomes infinite)

- There's no such thing as buy/sell volume, there's just volume, but for the purposes of the Volume Profile method, assume: bull candle = buy volume, bear candle = sell volume

P.S. I am your grandfather, Luke! Now, join the Dark Side in your father's steps or be destroyed! Once more the Sith will rule the Galaxy, and we shall have peace...

PivotBoss Outside Reversal SetupPATTERN SUMMARY

1. The engulfing bar of a bullish outside reversal setup has a low that is below the prior bar's low (L < L ) and a

close that is above the prior bar's high (C > H ).

2. The engulfing bar of a bearish outside reversal setup has a high that is above the prior bar's high (H > H )

and a close that is below the prior bar's low (C < L ).

3. The engulfing bar is usually 5 to 25 percent larger than the size of the average bar in the lookback period.

PATTERN PSYCHOLOGY

The power behind this pattern lies in the psychology behind the traders involved in this setup. If you have

ever participated in a breakout at support or resistance only to have the market reverse sharply against you, then

you are familiar with the market dynamics of this setup. What exactly is going on at these levels? To understand

this concept is to understand the outside reversal pattern. Basically, market participants are testing the waters

above resistance or below support to make sure there is no new business to be done at these levels. When no

initiative buyers or sellers participate in range extension, responsive participants have all the information they

need to reverse price back toward a new area of perceived value.

As you look at a bullish outside reversal pattern, you will notice that the current bar's low is lower than the

prior bar's low. Essentially, the market is testing the waters below recently established lows to see if a downside

follow-through will occur. When no additional selling pressure enters the market, the result is a flood of buying

pressure that causes a springboard effect, thereby shooting price above the prior bar's highs and creating the

beginning of a bullish advance.

If you recall the child on the trampoline for a moment, you'll realize that the child had to force the bounce

mat down before he could spring into the air. Also, remember Jennifer the cake baker? She initially pushed price

to $20 per cake, which sent a flood of orders into her shop. The flood of buying pressure eventually sent the price

of her cakes to $35 apiece. Basically, price had to test the $20 level before it could rise to $35.

Let's analyze the outside reversal setup in a different light for a moment. One of the reasons I like this setup

is because the two-bar pattern reduces into the wick reversal setup, which we covered earlier in the chapter. If

you are not familiar with candlestick reduction, the idea is simple. You are taking the price data over two or more

candlesticks and combining them to create a single candlestick. Therefore, you will be taking the open, high, low,

and close prices of the bars in question to create a single composite candlestick.

Take a look at Figure 2.13, which illustrates the candlestick reduction of the outside reversal setup.

Essentially, taking the highest high and the lowest low over the two-bar period gives you the range of the

composite candlestick. Then, taking the opening price of the first candle and the closing price of the last candle

will finish off the composite candlestick. Depending on the structure of the bars of the outside reversal setup, the

result of the candlestick reduction will usually be the transformation into a wick reversal setup, which we know to

be quite powerful. Therefore, in many cases the physiology of the outside reversal pattern basically demonstrates

the inherent psychological traits of the wick reversal pattern. This is just another level of analysis that reinforces

my belief in the outside reversal setup.

Session Fibonacci Tracker with Dynamic Range FreezeSession Fibonacci Tracker with Dynamic Range Freeze

This indicator plots Fibonacci retracement and extension levels based on session high/low ranges with a unique "freeze" mechanism that locks levels during volatility and recalculates only when price returns to the established range.

How It Works:

The indicator uses a three-stage process to maintain stable Fibonacci levels:

Range Establishment: At the start of each session (default 1800 ET), the indicator tracks the session high and low. Fibonacci levels are calculated with dynamic anchoring - when price is above the session open, 0 anchors at the high with 1 at the low; when below, 0 anchors at the low with 1 at the high.

Freeze Mechanism: Once the range is established, it immediately freezes. If a candle closes outside this range, the Fibonacci levels remain locked at their current values even as new session highs or lows form. This prevents levels from constantly recalculating during trending moves.

Recalculation: The frozen range only updates when price action (high or low) touches back inside the established range. At this point, levels recalculate based on the current session high/low, then freeze again.

Key Features:

Customizable Fibonacci levels: All retracement (0.236, 0.382, 0.500, 0.618, 0.786) and extension levels (-1.0, -0.618, -0.272, 1.272, 1.618, 2.0) can be enabled/disabled and adjusted to custom values

Time-based line extension prevents historical buffer overflow errors

Works across all timeframes

Session start time fully customizable

Visual status indicator shows whether levels are frozen or active

All lines and labels are fully customizable (colors, width, labels, prices)

Use Cases:

This indicator is particularly useful for traders who want stable reference levels during volatile periods. Traditional Fibonacci tools recalculate with every new extreme, making them difficult to use as support/resistance during trends. This implementation keeps levels stable until price returns to consolidation, providing consistent reference points for entries, exits, and stop placement.

Settings:

Session Settings: Configure session start time (default 1800 ET)

Fibonacci Levels: Enable/disable and customize each retracement level value

Extension Levels: Enable/disable and customize each extension level value

Visual Settings: Adjust line extension, width, labels, and price display

Colors: Customize colors for open line, 0 level, 1 level, retracements, and extensions

FVG PilotWhat it does

Automatically detects and draws Fair Value Gaps (FVGs) on the chart.

Removes an FVG as soon as it’s invalidated (bullish FVG invalid if price closes below its lower bound; bearish FVG invalid if price closes above its upper bound).

Triggers alerts only during Silver Bullet (SB) sessions in Europe/Berlin time when a new FVG is created.

Optionally draws two thin vertical lines at the start and end of each SB session so you can see the windows at a glance.

Runs on confirmed bars to avoid repainting.

How FVGs are detected

Wick mode (default):

Bullish FVG when low > high → gap [high , low]

Bearish FVG when high < low → gap [high, low ]

Body mode (optional): uses candle bodies instead of wicks:

Bullish FVG when current body low > prior body high

Bearish FVG when current body high < prior body low

Silver Bullet sessions (Europe/Berlin)

Three configurable session windows (default examples):

SB1: 10:00–11:00

SB2: 02:00–03:00

SB3: 07:00–08:00

Alerts for new FVGs fire only inside these windows.

Session lines: a thin vertical line is drawn on the first bar inside a session (start) and on the first bar after a session (end).

Inputs

Show Bullish / Bearish FVGs

Use Bodies (instead of wicks)

Minimum FVG size (in ticks)

Box opacity

SB sessions: enable/disable each window and set times (Europe/Berlin)

Session line toggle + color/width

Alerts included

SB (Berlin): Bullish FVG created – fires only during SB sessions

SB (Berlin): Bearish FVG created – fires only during SB sessions

Bullish FVG invalidated – fires when a bullish FVG is invalidated (no time filter)

Bearish FVG invalidated – fires when a bearish FVG is invalidated (no time filter)

How to set alerts (TradingView)

Click Create Alert.

Condition: choose this indicator, then pick one of the alert conditions above.

Select your alert options (once per bar close is recommended), then Create.

Tips

If you don’t see boxes, reduce Minimum FVG size or lower opacity (e.g., 70–85).

Body mode is stricter; start with wicks if you want more signals.

SB windows use Europe/Berlin and automatically account for DST.

The script respects platform limits for drawings; if your chart is cluttered, zoom in or reduce active sessions.

Smart Money Concepts [MHA Finverse]A comprehensive Smart Money Concepts (SMC) indicator designed to identify institutional trading behavior and market structure shifts. This tool helps traders align with "smart money" by detecting key supply and demand zones, structural breaks, and liquidity patterns.

Core Features

Market Structure Analysis

- Real-time Internal Structure: Detects short-term BOS (Break of Structure) and CHoCH (Change of Character) with customizable filters

- Swing Structure: Identifies major trend shifts and structural breaks on higher timeframes

- Adjustable pivot detection with customizable swing point visualization

- Strong/Weak High/Low identification for bias confirmation

Order Blocks (OB)

- Internal and Swing Order Blocks with independent control

- Volume-based metrics showing OB strength and percentage contribution

- Two filtering methods: ATR-based and Cumulative Mean Range

- Flexible mitigation options (Close or High/Low)

- Display up to 20 order blocks per type with auto-cleanup on mitigation

- Color-coded zones with transparency control

Liquidity Detection

- Equal Highs (EQH) and Equal Lows (EQL) identification

- Threshold-based detection using ATR calculation

- Visual confirmation lines connecting equal levels

- Adjustable sensitivity and bar confirmation settings

Fair Value Gaps (FVG)

- Multi-timeframe FVG detection

- Auto-threshold calculation based on price momentum

- Bullish and Bearish gap visualization

- Extendable gap boxes for tracking unfilled imbalances

Premium & Discount Zones

- Automated premium, equilibrium, and discount zone plotting

- Based on current swing range extremes

- Visual representation of optimal entry zones

- Helps identify potential reversal and continuation areas

Multi-Timeframe Levels

- Previous Daily, Weekly, and Monthly High/Low levels

- Customizable line styles (solid, dashed, dotted)

- Independent color controls for each timeframe

- Auto-adjusted labels (PDH, PDL, PWH, PWL, PMH, PML)

Display Modes

- Historical Mode: Shows all past structures and maintains drawing history

- Present Mode: Displays only current active structures for cleaner charts

Visual Themes

- Colored: Full color customization for all elements

- Monochrome: Clean grey-scale design for minimal distraction

Smart Features

- Confluence filter for internal structure to reduce noise

- Automatic candle coloring based on market bias

- 16 pre-configured alert conditions for all major signals

- Efficient rendering with automatic cleanup of broken structures

- Independent control over each feature for modular usage

Use Cases

- Identify institutional entry and exit points through order blocks

- Spot potential reversals at premium/discount zones

- Confirm trend direction with BOS and CHoCH signals

- Find liquidity grabs at equal highs and lows

- Trade imbalances at fair value gaps

- Align entries with multi-timeframe key levels

Settings Organization

All features are neatly organized into logical groups:

- Smart Money Concepts (general settings)

- Real Time Internal Structure

- Real Time Swing Structure

- Order Blocks

- EQH/EQL

- Fair Value Gaps

- Highs & Lows MTF

- Premium & Discount Zones

Note: This indicator works on all timeframes and instruments. For optimal results, combine multiple SMC concepts together to find high-probability setups with confluence.

Credits

Special thanks to Dau_tu_hieu_goc and BigBeluga for their code examples and inspiration that contributed to the development of this indicator.

Disclaimer

This indicator is for educational purposes only and does not constitute financial advice. Trading involves substantial risk of loss. Past performance does not guarantee future results. Always use proper risk management and conduct your own analysis before making trading decisions. The developer is not responsible for any trading losses incurred.

Happy Trading

Session Sweep System – WarRoomXYZ V1WarRoom Session Sweep System v1 is a open-source institutional trading framework built to identify liquidity behavior across Asia, London, and New York sessions.

It combines session-based liquidity mapping, sweep detection, daily expansion modeling, and trend confirmation into a unified, timing-driven system optimized for XAUUSD, FX pairs, indices, and any instrument with session-dependent volatility.

This tool does not attempt to predict direction with arbitrary oscillators.

Instead, it focuses on the underlying market mechanisms that drive price:

liquidity, timing, expansion, and trend alignment.

Below is a detailed explanation of what the script does, how its components work, and how traders can use it effectively.

🔹 1. Session Liquidity Mapping

The script automatically identifies the Asia (00:00–06:00 GMT), London (07:00–12:00 GMT), and New York (13:00–17:00 GMT) sessions and builds real-time session ranges.

Each session creates a liquidity pool.

Trading institutions frequently sweep the high or low of one session before delivering the real move in the next session.

This script captures that behavior by:

►Drawing session range boxes

►Tracking previous session highs/lows

►Highlighting high-probability sweep locations

These ranges are essential reference points for timing entries and exits.

🔹 2. Liquidity Sweep Detection (Buy & Sell Sweeps)

The indicator identifies when price runs a previous session high/low and rejects back inside the range, which is commonly interpreted as a liquidity sweep.

The following sweep types are monitored:

►London sweeping Asia

►New York sweeping London

►Asia sweeping New York

►Daily sweep of PDH/PDL

Sweeps signal that liquidity has been collected and that a potential reversal or continuation is likely.

These are marked clearly on the chart for real-time decision-making.

🔹 3. Killzone Timing Model (GMT Time)

Market manipulation and expansion often occur during specific time windows.

The script highlights these institutional killzones:

►London Killzone: 07:00–10:00 GMT

►New York Killzone: 13:30–15:30 GMT

►NY PM Session: 19:00–21:00 GMT

Sweeps occurring inside these windows carry a significantly higher probability.

The timing layer helps filter out low-quality setups.

🔹 4. Daily Range & ADR Expansion Engine

A dedicated panel displays:

►Current day range

►ADR (Average Daily Range)

►Expansion stage (Early / Developed / Extended)

►PDH/PDL swept or intact

►Overall session bias

This allows traders to understand whether the daily move is likely to continue or reverse.

For example:

►Early expansion → trend continuation likely

►Extended expansion → reversal setups become more probable

This is useful for intraday targets and risk management.

🔹 5. MA Cloud Trend Model (Fast/Slow Structure)

To align liquidity behavior with directional conviction, the script includes a configurable MA engine:

►Fast & slow MA

►MA cloud

►Slope-based trend coloring

►Trend background

►MA cross alerts

The cloud provides trend confirmation without relying on oscillators.

Trades are higher quality when the sweep direction aligns with the MA trend.

🔹 6. How the Components Work Together

The script integrates several institutional concepts into one coherent model:

►Sessions define liquidity pools

►Sweeps identify stop-hunts and reversals

►Killzones define optimal timing

►MA Cloud confirms directional bias

►ADR engine indicates expansion potential

This creates a structured framework:

Sweep → Timing → Trend → Expansion → Execution

Each component strengthens the others, forming a robust decision-making model.

🔹 7. How to Use the Indicator (Practical Guide)

✔ Look for a sweep of a previous session level

When price runs a session high/low and closes back inside, liquidity has likely been collected.

✔ Confirm timing

Sweeps inside London or NY killzones tend to produce the strongest moves.

✔ Confirm trend

Use MA cloud direction and slope:

►Cloud green → long setups preferred

►Cloud red → short setups preferred

✔ Check ADR panel

If the day has already expanded significantly, reversal setups are more likely.

If expansion is still early, continuation setups are favored.

✔ Plan your trade

Common targets include:

►Opposite side of session range