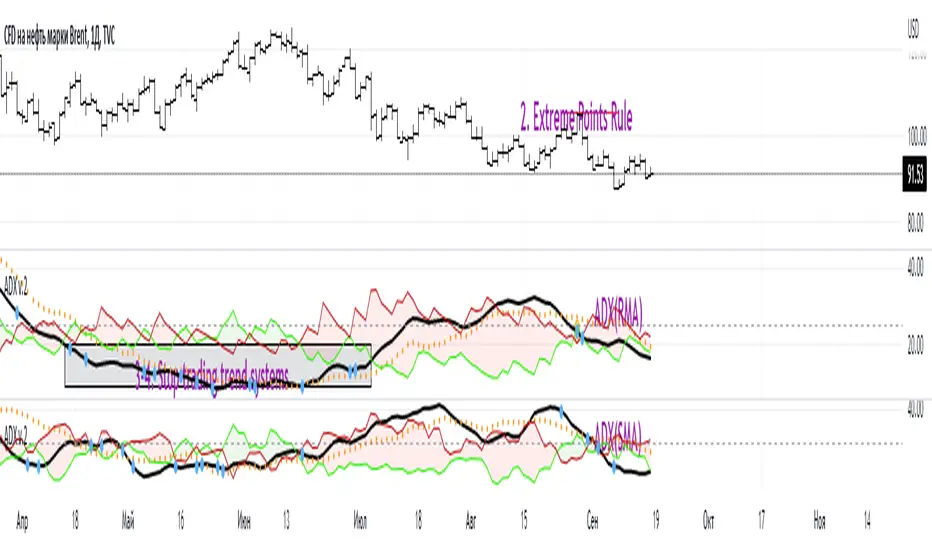

ADX W. Wilders(DI+, DI-, DX, ADXR, Equilibrium Point)The reason for publishing the script was the lack of display of important components in the standard ADX indicator, such as DI+, DI-, DX , ADXR, and the absence of a choice of methods for calculating moving averages in the indicator.

According to the book by the author of the ADX indicator, W. Wilder, the indicator components were calculated using the SMA formula, however, the RMA moving average is used in the code of the built-in indicator in TradingView, which shows excellent results, but this is not a classic calculation method. In addition to SMA and RMA, there are also EMA , HMA , WMA , VWMA moving averages to choose from. Added the ability to display lines ADX , ADXR , DX , DI+, DI- and Equilibrium points (when DI+ and DI- are equal or intersect).

ADX Trading Rules

1. Trade the intersections of DI+ and DI-

2. Extreme Point Rule(EPR). EPR is formed when DI+, DI- (Equilibrium point) crosses, forming a trend reversal point at the extremum of the current bar. In the example on the ADX RMA chart, the DI- line is above DI+. Being in a short position at the reverse intersection of the DI- and DI + lines, it is necessary to take the high price of the crossing bar for the reversal point, upon breakdown of which, turn to long. In this example, the breakdown did not take place and the short position remained active, despite the intersection of the DI+ lines over DI-. This rule is an excellent filter that removes unnecessary transactions in the trading system.

3. DI+ > ADX and DI- > ADX. Stop trading trend-following systems.

4. If ADXR > 25, the trading system will be profitable. With ADXR < 20, trend-following systems need to stop trading. Many mistakenly use ADX values instead of ADXR . The author explicitly pointed to ADXR in his book.

5. Equilibrium Point - balance points. The accumulation of these points on the chart means the presence of a flat in the market. Accumulation often appears on a declining ADX after a top has been established on the ADX indicator. The smaller the distance between the points, the less significant movements occurred in the market.

6. For intraday trading of cryptocurrencies use can the following ADX settings:

DI Length = 100

ADX Smoothing = 14

MA Type = VWMA

Flat Zone = 30

P.S. Fragment from an interview with W. Wilder:

OH: You are probably best known for inventing the Relative Strength Index ( RSI ), Average Directional Index ( ADX ) and Average True Range (ATR). Which of these is the most powerful tool for a trader?

WW: The ADX .

OH: Is it the indicator you are most proud of?

WW: I guess so.

Search in scripts for "rma"

Forex Midpoint Stratejisi For Nasdaq English Knowledge:

Midpoint Strategy;

The general calculation method is a strategy that helps determine direction by the intersection of a MA line and the value obtained by dividing the lowest and highest price in the specified length range.

Başlangıç Periyodu: The data length of the Midpoint Line.

Kaydırma Seviyesi: The number of steps forward or backward of the Midpoint Line.

Yüzde Seviyesi: the amount of vertical scrolling.

Uzunluk: The length of the MA line

represents.

This strategy is prepared for the Nasdaq 5-minute period. It needs to be optimized for use on other instruments.

There are take profit and stop loss levels within the codes. Friends who want to use it can remove the invisibility from the relevant sections. Also, I removed the midpoint and the MA line so that it does not crowd the image, you can add it if you want.

Thank you.

Turkish Knowledge:

Midpoint Stratejisi;

Genel hesaplama yöntemi, belirlenen uzunluk aralığındaki en düşük ve en yüksek fiyatın ikiye bölümü ile elde edilen değer ve bir ortalama çizgisinin kesişimleriyle yön belirlemeye yardımcı bir stratejidir.

Başlangıç Period: Midpoint Çizgisinin veri uzunluğunu.

Kaydırma Seviyesi: Midpoint Çizgisinin ileri veya geri adım sayısını.

Yüzde Seviyesi: dikey kaydırma miktarını.

Uzunluk: Ortalama çizgisinin uzunluğunu

temsil etmektedir.

Bu strateji Nasdaq 5 dakikalık periot için hazırlanmıştır. Diğer enstrümanlarda kullanılması için optimize edilmesi gerekir.

Kodların içinde Kar alma , zarar durdurma seviyeleri mevcuttur. Kullanmak isteyen arkadaşlar ilgili bölümlerden görünmezliği kaldırabilirler. ayrıca midpoint ve ortalama çizgisinide görüntü kalabalığı yapmaması için ben kaldırdım isterseniz siz ekleyebilirsiniz.

Teşekkürler.

Moving_AveragesLibrary "Moving_Averages"

This library contains majority important moving average functions with int series support. Which means that they can be used with variable length input. For conventional use, please use tradingview built-in ta functions for moving averages as they are more precise. I'll use functions in this library for my other scripts with dynamic length inputs.

ema(src, len)

Exponential Moving Average (EMA)

Parameters:

src : Source

len : Period

Returns: Exponential Moving Average with Series Int Support (EMA)

alma(src, len, a_offset, a_sigma)

Arnaud Legoux Moving Average (ALMA)

Parameters:

src : Source

len : Period

a_offset : Arnaud Legoux offset

a_sigma : Arnaud Legoux sigma

Returns: Arnaud Legoux Moving Average (ALMA)

covwema(src, len)

Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

covwma(src, len)

Coefficient of Variation Weighted Moving Average (COVWMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Moving Average (COVWMA)

dema(src, len)

DEMA - Double Exponential Moving Average

Parameters:

src : Source

len : Period

Returns: DEMA - Double Exponential Moving Average

edsma(src, len, ssfLength, ssfPoles)

EDSMA - Ehlers Deviation Scaled Moving Average

Parameters:

src : Source

len : Period

ssfLength : EDSMA - Super Smoother Filter Length

ssfPoles : EDSMA - Super Smoother Filter Poles

Returns: Ehlers Deviation Scaled Moving Average (EDSMA)

eframa(src, len, FC, SC)

Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

Parameters:

src : Source

len : Period

FC : Lower Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

SC : Upper Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

Returns: Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

ehma(src, len)

EHMA - Exponential Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Exponential Hull Moving Average (EHMA)

etma(src, len)

Exponential Triangular Moving Average (ETMA)

Parameters:

src : Source

len : Period

Returns: Exponential Triangular Moving Average (ETMA)

frama(src, len)

Fractal Adaptive Moving Average (FRAMA)

Parameters:

src : Source

len : Period

Returns: Fractal Adaptive Moving Average (FRAMA)

hma(src, len)

HMA - Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Hull Moving Average (HMA)

jma(src, len, jurik_phase, jurik_power)

Jurik Moving Average - JMA

Parameters:

src : Source

len : Period

jurik_phase : Jurik (JMA) Only - Phase

jurik_power : Jurik (JMA) Only - Power

Returns: Jurik Moving Average (JMA)

kama(src, len, k_fastLength, k_slowLength)

Kaufman's Adaptive Moving Average (KAMA)

Parameters:

src : Source

len : Period

k_fastLength : Number of periods for the fastest exponential moving average

k_slowLength : Number of periods for the slowest exponential moving average

Returns: Kaufman's Adaptive Moving Average (KAMA)

kijun(_high, _low, len, kidiv)

Kijun v2

Parameters:

_high : High value of bar

_low : Low value of bar

len : Period

kidiv : Kijun MOD Divider

Returns: Kijun v2

lsma(src, len, offset)

LSMA/LRC - Least Squares Moving Average / Linear Regression Curve

Parameters:

src : Source

len : Period

offset : Offset

Returns: Least Squares Moving Average (LSMA)/ Linear Regression Curve (LRC)

mf(src, len, beta, feedback, z)

MF - Modular Filter

Parameters:

src : Source

len : Period

beta : Modular Filter, General Filter Only - Beta

feedback : Modular Filter Only - Feedback

z : Modular Filter Only - Feedback Weighting

Returns: Modular Filter (MF)

rma(src, len)

RMA - RSI Moving average

Parameters:

src : Source

len : Period

Returns: RSI Moving average (RMA)

sma(src, len)

SMA - Simple Moving Average

Parameters:

src : Source

len : Period

Returns: Simple Moving Average (SMA)

smma(src, len)

Smoothed Moving Average (SMMA)

Parameters:

src : Source

len : Period

Returns: Smoothed Moving Average (SMMA)

stma(src, len)

Simple Triangular Moving Average (STMA)

Parameters:

src : Source

len : Period

Returns: Simple Triangular Moving Average (STMA)

tema(src, len)

TEMA - Triple Exponential Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Exponential Moving Average (TEMA)

thma(src, len)

THMA - Triple Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Hull Moving Average (THMA)

vama(src, len, volatility_lookback)

VAMA - Volatility Adjusted Moving Average

Parameters:

src : Source

len : Period

volatility_lookback : Volatility lookback length

Returns: Volatility Adjusted Moving Average (VAMA)

vidya(src, len)

Variable Index Dynamic Average (VIDYA)

Parameters:

src : Source

len : Period

Returns: Variable Index Dynamic Average (VIDYA)

vwma(src, len)

Volume-Weighted Moving Average (VWMA)

Parameters:

src : Source

len : Period

Returns: Volume-Weighted Moving Average (VWMA)

wma(src, len)

WMA - Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Weighted Moving Average (WMA)

zema(src, len)

Zero-Lag Exponential Moving Average (ZEMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Exponential Moving Average (ZEMA)

zsma(src, len)

Zero-Lag Simple Moving Average (ZSMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Simple Moving Average (ZSMA)

evwma(src, len)

EVWMA - Elastic Volume Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Elastic Volume Weighted Moving Average (EVWMA)

tt3(src, len, a1_t3)

Tillson T3

Parameters:

src : Source

len : Period

a1_t3 : Tillson T3 Volume Factor

Returns: Tillson T3

gma(src, len)

GMA - Geometric Moving Average

Parameters:

src : Source

len : Period

Returns: Geometric Moving Average (GMA)

wwma(src, len)

WWMA - Welles Wilder Moving Average

Parameters:

src : Source

len : Period

Returns: Welles Wilder Moving Average (WWMA)

ama(src, _high, _low, len, ama_f_length, ama_s_length)

AMA - Adjusted Moving Average

Parameters:

src : Source

_high : High value of bar

_low : Low value of bar

len : Period

ama_f_length : Fast EMA Length

ama_s_length : Slow EMA Length

Returns: Adjusted Moving Average (AMA)

cma(src, len)

Corrective Moving average (CMA)

Parameters:

src : Source

len : Period

Returns: Corrective Moving average (CMA)

gmma(src, len)

Geometric Mean Moving Average (GMMA)

Parameters:

src : Source

len : Period

Returns: Geometric Mean Moving Average (GMMA)

ealf(src, len, LAPercLen_, FPerc_)

Ehler's Adaptive Laguerre filter (EALF)

Parameters:

src : Source

len : Period

LAPercLen_ : Median Length

FPerc_ : Median Percentage

Returns: Ehler's Adaptive Laguerre filter (EALF)

elf(src, len, LAPercLen_, FPerc_)

ELF - Ehler's Laguerre filter

Parameters:

src : Source

len : Period

LAPercLen_ : Median Length

FPerc_ : Median Percentage

Returns: Ehler's Laguerre Filter (ELF)

edma(src, len)

Exponentially Deviating Moving Average (MZ EDMA)

Parameters:

src : Source

len : Period

Returns: Exponentially Deviating Moving Average (MZ EDMA)

pnr(src, len, rank_inter_Perc_)

PNR - percentile nearest rank

Parameters:

src : Source

len : Period

rank_inter_Perc_ : Rank and Interpolation Percentage

Returns: Percentile Nearest Rank (PNR)

pli(src, len, rank_inter_Perc_)

PLI - Percentile Linear Interpolation

Parameters:

src : Source

len : Period

rank_inter_Perc_ : Rank and Interpolation Percentage

Returns: Percentile Linear Interpolation (PLI)

rema(src, len)

Range EMA (REMA)

Parameters:

src : Source

len : Period

Returns: Range EMA (REMA)

sw_ma(src, len)

Sine-Weighted Moving Average (SW-MA)

Parameters:

src : Source

len : Period

Returns: Sine-Weighted Moving Average (SW-MA)

vwap(src, len)

Volume Weighted Average Price (VWAP)

Parameters:

src : Source

len : Period

Returns: Volume Weighted Average Price (VWAP)

mama(src, len)

MAMA - MESA Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: MESA Adaptive Moving Average (MAMA)

fama(src, len)

FAMA - Following Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Following Adaptive Moving Average (FAMA)

hkama(src, len)

HKAMA - Hilbert based Kaufman's Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Hilbert based Kaufman's Adaptive Moving Average (HKAMA)

AMASling - All Moving Average Sling ShotThis indicator modifies the SlingShot System by Chris Moody to allow it to be based on 'any' Fast and Slow moving average pair. Open Long / Close Long / Open Short / Close Short alerts can be generated for automated bot trading based on the SlingShot strategy:

• Conservative Entry = Fast MA above Slow MA, and previous bar close below Fast MA, and current price above Fast MA

• Conservative Entry = Fast MA below Slow MA, and previous bar close above Fast MA, and current price below Fast MA

• Aggressive Entry = Fast MA above Slow MA, and price below Fast MA

• Aggressive Exit = Fast MA below Slow MA, and price above Fast MA

Entries and exits can also be made based on moving average crossovers, I initially put this in to make it easy to compare to a more standard strategy, but upon backtesting combining crossovers with the SlingShot appeared to produce better results on some charts.

Alerts can also be filtered to allow long deals only when the fast moving average is above the slow moving average (uptrend) and short deals only when the fast moving average is below the slow moving averages (downtrend).

If you have a strategy that can buy based on External Indicators you can use the 'Backtest Signal' which plots the values set in the 'Long / Short Signals' section.

The Fast, Slow and Signal Moving Averages can be set to:

• Simple Moving Average (SMA)

• Exponential Moving Average (EMA)

• Weighted Moving Average (WMA)

• Volume-Weighted Moving Average (VWMA)

• Hull Moving Average (HMA)

• Exponentially Weighted Moving Average (RMA) (SMMA)

• Linear regression curve Moving Average (LSMA)

• Double EMA (DEMA)

• Double SMA (DSMA)

• Double WMA (DWMA)

• Double RMA (DRMA)

• Triple EMA (TEMA)

• Triple SMA (TSMA)

• Triple WMA (TWMA)

• Triple RMA (TRMA)

• Symmetrically Weighted Moving Average (SWMA) ** length does not apply **

• Arnaud Legoux Moving Average (ALMA)

• Variable Index Dynamic Average (VIDYA)

• Fractal Adaptive Moving Average (FRAMA)

'Backtest Signal' and 'Deal State' are plotted to display.none, so change the Style Settings for the chart if you need to see them for testing.

Yes I did choose the name because 'It's Amasling!'

pandas_taLibrary "pandas_ta"

Level: 3

Background

Today is the first day of 2022 and happy new year every tradingviewers! May health and wealth go along with you all the time. I use this chance to publish my 1st PINE v5 lib : pandas_ta

This is not a piece of cake like thing, which cost me a lot of time and efforts to build this lib. Beyond 300 versions of this script was iterated in draft.

Function

Library "pandas_ta"

PINE v5 Counterpart of Pandas TA - A Technical Analysis Library in Python 3 at github.com

The Original Pandas Technical Analysis (Pandas TA) is an easy to use library that leverages the Pandas package with more than 130 Indicators and Utility functions and more than 60 TA Lib Candlestick Patterns.

I realized most of indicators except Candlestick Patterns because tradingview built-in Candlestick Patterns are even more powerful!

I use this to verify pandas_ta python version indicators for myself, but I realize that maybe many may need similar lib for pine v5 as well.

Function Brief Descriptions (Pls find details in script comments)

bton --> Binary to number

wcp --> Weighted Closing Price (WCP)

counter --> Condition counter

xbt --> Between

ebsw --> Even Better SineWave (EBSW)

ao --> Awesome Oscillator (AO)

apo --> Absolute Price Oscillator (APO)

xrf --> Dynamic shifted values

bias --> Bias (BIAS)

bop --> Balance of Power (BOP)

brar --> BRAR (BRAR)

cci --> Commodity Channel Index (CCI)

cfo --> Chande Forcast Oscillator (CFO)

cg --> Center of Gravity (CG)

cmo --> Chande Momentum Oscillator (CMO)

coppock --> Coppock Curve (COPC)

cti --> Correlation Trend Indicator (CTI)

dmi --> Directional Movement Index(DMI)

er --> Efficiency Ratio (ER)

eri --> Elder Ray Index (ERI)

fisher --> Fisher Transform (FISHT)

inertia --> Inertia (INERTIA)

kdj --> KDJ (KDJ)

kst --> 'Know Sure Thing' (KST)

macd --> Moving Average Convergence Divergence (MACD)

mom --> Momentum (MOM)

pgo --> Pretty Good Oscillator (PGO)

ppo --> Percentage Price Oscillator (PPO)

psl --> Psychological Line (PSL)

pvo --> Percentage Volume Oscillator (PVO)

qqe --> Quantitative Qualitative Estimation (QQE)

roc --> Rate of Change (ROC)

rsi --> Relative Strength Index (RSI)

rsx --> Relative Strength Xtra (rsx)

rvgi --> Relative Vigor Index (RVGI)

slope --> Slope

smi --> SMI Ergodic Indicator (SMI)

sqz* --> Squeeze (SQZ) * NOTE: code sufferred from very strange error, code was commented.

sqz_pro --> Squeeze PRO(SQZPRO)

xfl --> Condition filter

stc --> Schaff Trend Cycle (STC)

stoch --> Stochastic (STOCH)

stochrsi --> Stochastic RSI (STOCH RSI)

trix --> Trix (TRIX)

tsi --> True Strength Index (TSI)

uo --> Ultimate Oscillator (UO)

willr --> William's Percent R (WILLR)

alma --> Arnaud Legoux Moving Average (ALMA)

xll --> Dynamic rolling lowest values

dema --> Double Exponential Moving Average (DEMA)

ema --> Exponential Moving Average (EMA)

fwma --> Fibonacci's Weighted Moving Average (FWMA)

hilo --> Gann HiLo Activator(HiLo)

hma --> Hull Moving Average (HMA)

hwma --> HWMA (Holt-Winter Moving Average)

ichimoku --> Ichimoku Kinkō Hyō (ichimoku)

jma --> Jurik Moving Average Average (JMA)

kama --> Kaufman's Adaptive Moving Average (KAMA)

linreg --> Linear Regression Moving Average (linreg)

mgcd --> McGinley Dynamic Indicator

rma --> wildeR's Moving Average (RMA)

sinwma --> Sine Weighted Moving Average (SWMA)

ssf --> Ehler's Super Smoother Filter (SSF) © 2013

supertrend --> Supertrend (supertrend)

xsa --> X simple moving average

swma --> Symmetric Weighted Moving Average (SWMA)

t3 --> Tim Tillson's T3 Moving Average (T3)

tema --> Triple Exponential Moving Average (TEMA)

trima --> Triangular Moving Average (TRIMA)

vidya --> Variable Index Dynamic Average (VIDYA)

vwap --> Volume Weighted Average Price (VWAP)

vwma --> Volume Weighted Moving Average (VWMA)

wma --> Weighted Moving Average (WMA)

zlma --> Zero Lag Moving Average (ZLMA)

entropy --> Entropy (ENTP)

kurtosis --> Rolling Kurtosis

skew --> Rolling Skew

xev --> Condition all

zscore --> Rolling Z Score

adx --> Average Directional Movement (ADX)

aroon --> Aroon & Aroon Oscillator (AROON)

chop --> Choppiness Index (CHOP)

xex --> Condition any

cksp --> Chande Kroll Stop (CKSP)

dpo --> Detrend Price Oscillator (DPO)

long_run --> Long Run

psar --> Parabolic Stop and Reverse (psar)

short_run --> Short Run

vhf --> Vertical Horizontal Filter (VHF)

vortex --> Vortex

accbands --> Acceleration Bands (ACCBANDS)

atr --> Average True Range (ATR)

bbands --> Bollinger Bands (BBANDS)

donchian --> Donchian Channels (DC)

kc --> Keltner Channels (KC)

massi --> Mass Index (MASSI)

natr --> Normalized Average True Range (NATR)

pdist --> Price Distance (PDIST)

rvi --> Relative Volatility Index (RVI)

thermo --> Elders Thermometer (THERMO)

ui --> Ulcer Index (UI)

ad --> Accumulation/Distribution (AD)

cmf --> Chaikin Money Flow (CMF)

efi --> Elder's Force Index (EFI)

ecm --> Ease of Movement (EOM)

kvo --> Klinger Volume Oscillator (KVO)

mfi --> Money Flow Index (MFI)

nvi --> Negative Volume Index (NVI)

obv --> On Balance Volume (OBV)

pvi --> Positive Volume Index (PVI)

dvdi --> Dual Volume Divergence Index (DVDI)

xhh --> Dynamic rolling highest values

pvt --> Price-Volume Trend (PVT)

Remarks

I also incorporated func descriptions and func test script in commented mode, you can test the functino with the embedded test script and modify them as you wish.

This is a Level 3 free and open source indicator library.

Feedbacks are appreciated.

This is not the end of pandas_ta lib publication, but it is start point with pine v5 lib function and I will add more and more funcs into this lib for my own indicators.

Function Name List:

bton()

wcp()

count()

xbt()

ebsw()

ao()

apo()

xrf()

bias()

bop()

brar()

cci()

cfo()

cg()

cmo()

coppock()

cti()

dmi()

er()

eri()

fisher()

inertia()

kdj()

kst()

macd()

mom()

pgo()

ppo()

psl()

pvo()

qqe()

roc()

rsi()

rsx()

rvgi()

slope()

smi()

sqz_pro()

xfl()

stc()

stoch()

stochrsi()

trix()

tsi()

uo()

willr()

alma()

wcx()

xll()

dema()

ema()

fwma()

hilo()

hma()

hwma()

ichimoku()

jma()

kama()

linreg()

mgcd()

rma()

sinwma()

ssf()

supertrend()

xsa()

swma()

t3()

tema()

trima()

vidya()

vwap()

vwma()

wma()

zlma()

entropy()

kurtosis()

skew()

xev()

zscore()

adx()

aroon()

chop()

xex()

cksp()

dpo()

long_run()

psar()

short_run()

vhf()

vortex()

accbands()

atr()

bbands()

donchian()

kc()

massi()

natr()

pdist()

rvi()

thermo()

ui()

ad()

cmf()

efi()

ecm()

kvo()

mfi()

nvi()

obv()

pvi()

dvdi()

xhh()

pvt()

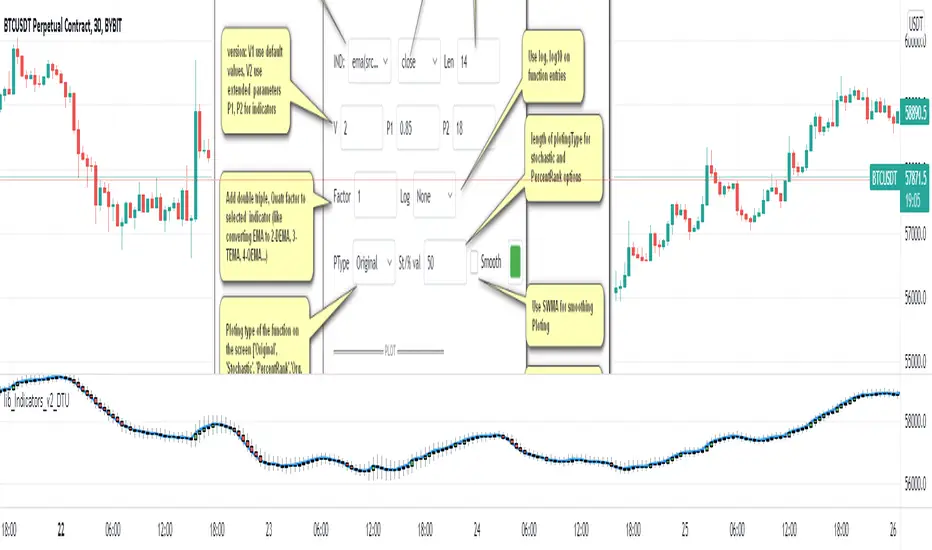

Indicator Functions with Factor and HeikinAshiHello all,

This indicator returns below selected indicators values with entered parameters.

Also you can add factorization, functions candles, function HeikinAshi and more to the plot.

VERSION:

Version 1: returns series only source and Length with already defined default values

Version 2: returns series with source, Length, p1 and p2 parameters according to the indicator definition (ex: )

PARAMETERS p1 p2

for defining multi arguments (See indicators list) indicator input value usable with verison=V2 selected.. ex: for alma( src , len ,offset=0.85,sigma=6), set source=source, len=length, p1=0.85 an p2=6

FACTOR:

Add double triple, Quadruple factors to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

1-Original

2-Double

3-Triple

4-Quadruple

LOG

Log: Use log, log10 on function entries

PLOTTING:

PType: Plotting type of the function on the screen

Original :use original values

Org. Range (-1,1): usable for indicators between range -1 and 1

Stochastic: Convert indicator values by using stochastic calculation between -1 & 1. (use AT/% length to better view)

PercentRank: Convert indicator values by using Percent Rank calculation between -1 & 1. (use AT/% length to better view)

ST/%: length for plotting Type for stochastic and Percent Rank options

Smooth: Use SWMA for smoothing the function

DISPLAY TYPES

Plot Candles: Display the selected indicator as candle by implementing values

Plot Ind: Display result of indicator with selected source

HeikinAshi: Display Selected indicator candles with Heikin Ashi calculation

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma( src , len ,offset=0.85,sigma=6)', // Arnaud Legoux Moving Average

ama = 'ama( src , len ,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', // Accumulation/distribution index.

cma = 'cma( src , len )', //Corrective Moving average

dema = 'dema( src , len )', // Double EMA (Same as EMA with 2 factor)

ema = 'ema( src , len )', // Exponential Moving Average

gmma = 'gmma( src , len )', //Geometric Mean Moving Average

hghst = 'highest( src , len )', //Highest value for a given number of bars back.

hl2ma = 'hl2ma( src , len )', //higest lowest moving average

hma = 'hma( src , len )', // Hull Moving Average .

lgAdt = 'lagAdapt( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre( src , len )', //Ehler's Laguerre filter

lsrcp = 'lesrcp( src , len )', //lowest exponential esrcpanding moving line

lexp = 'lexp( src , len )', //lowest exponential expanding moving line

linrg = 'linreg( src , len ,loffset=1)', // Linear regression

lowst = 'lowest( src , len )', //Lovest value for a given number of bars back.

pcnl = 'percntl( src , len )', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli( src , len )', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema( src , len )', //Range EMA (REMA)

rma = 'rma( src , len )', //Moving average used in RSI . It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma( src , len )', // Smoothed Moving Average

smma = 'smma( src , len )', // Smoothed Moving Average

supr2 = 'super2( src , len )', //Ehler's super smoother, 2 pole

supr3 = 'super3( src , len )', //Ehler's super smoother, 3 pole

strnd = 'supertrend( src , len ,period=3)', //Supertrend indicator

swma = 'swma( src , len )', //Sine-Weighted Moving Average

tema = 'tema( src , len )', // Triple EMA (Same as EMA with 3 factor)

tma = 'tma( src , len )', //Triangular Moving Average

vida = 'vida( src , len )', // Variable Index Dynamic Average

vwma = 'vwma( src , len )', // Volume Weigted Moving Average

wma = 'wma( src , len )', //Weigted Moving Average

angle = 'angle( src , len )', //angle of the series (Use its Input as another indicator output)

atr = 'atr( src , len )', // average true range . RMA of true range.

bbr = 'bbr( src , len ,mult=1)', // bollinger %%

bbw = 'bbw( src , len ,mult=2)', // Bollinger Bands Width . The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci( src , len )', // commodity channel index

cctbb = 'cctbbo( src , len )', // CCT Bollinger Band Oscilator

chng = 'change( src , len )', //Difference between current value and previous, source - source.

cmo = 'cmo( src , len )', // Chande Momentum Oscillator . Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog( src , len )', //The cog (center of gravity ) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve( src , len )', // Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl( src , len )', // Correlation coefficient . Describes the degree to which two series tend to deviate from their ta. sma values.

count = 'count( src , len )', //green avg - red avg

dev = 'dev( src , len )', //ta.dev() Measure of difference between the series and it's ta. sma

fall = 'falling( src , len )', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr( src , len ,mult=2)', // Keltner Channels Range

kcw = 'kcw( src , len ,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd( src , len )', // macd

mfi = 'mfi( src , len )', // Money Flow Index

nvi = 'nvi()', // Negative Volume Index

obv = 'obv()', // On Balance Volume

pvi = 'pvi()', // Positive Volume Index

pvt = 'pvt()', // Price Volume Trend

rise = 'rising( src , len )', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc( src , len )', // Rate of Change

rsi = 'rsi( src , len )', // Relative strength Index

smosc = 'smi_osc( src , len ,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig( src , len ,fast=5, slow=34)', //smi Signal

stdev = 'stdev( src , len )', //Standart deviation

trix = 'trix( src , len )' , //the rate of change of a triple exponentially smoothed moving average .

tsi = 'tsi( src , len )', //True Strength Index

vari = 'variance( src , len )', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta. sma ), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc( src , len )', // Williams %R

wad = 'wad()', // Williams Accumulation/Distribution .

wvad = 'wvad()' //Williams Variable Accumulation/Distribution

I will update the indicator list when I will update the library

Thanks to tradingview, @RodrigoKazuma for their open source indicators

lib_Indicators_v2_DTULibrary "lib_Indicators_v2_DTU"

This library functions returns included Moving averages, indicators with factorization, functions candles, function heikinashi and more.

Created it to feed as backend of my indicator/strategy "Indicators & Combinations Framework Advanced v2 " that will be released ASAP.

This is replacement of my previous indicator (lib_indicators_DT)

I will add an indicator example which will use this indicator named as "lib_indicators_v2_DTU example" to help the usage of this library

Additionally library will be updated with more indicators in the future

NOTES:

Indicator functions returns only one series :-(

plotcandle function returns candle series

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma(src,len,offset=0.85,sigma=6)', //Arnaud Legoux Moving Average

ama = 'ama(src,len,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', //Accumulation/distribution index.

cma = 'cma(src,len)', //Corrective Moving average

dema = 'dema(src,len)', //Double EMA (Same as EMA with 2 factor)

ema = 'ema(src,len)', //Exponential Moving Average

gmma = 'gmma(src,len)', //Geometric Mean Moving Average

hghst = 'highest(src,len)', //Highest value for a given number of bars back.

hl2ma = 'hl2ma(src,len)', //higest lowest moving average

hma = 'hma(src,len)', //Hull Moving Average.

lgAdt = 'lagAdapt(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre(src,len)', //Ehler's Laguerre filter

lsrcp = 'lesrcp(src,len)', //lowest exponential esrcpanding moving line

lexp = 'lexp(src,len)', //lowest exponential expanding moving line

linrg = 'linreg(src,len,loffset=1)', //Linear regression

lowst = 'lowest(src,len)', //Lovest value for a given number of bars back.

pcnl = 'percntl(src,len)', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli(src,len)', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema(src,len)', //Range EMA (REMA)

rma = 'rma(src,len)', //Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma(src,len)', //Smoothed Moving Average

smma = 'smma(src,len)', //Smoothed Moving Average

supr2 = 'super2(src,len)', //Ehler's super smoother, 2 pole

supr3 = 'super3(src,len)', //Ehler's super smoother, 3 pole

strnd = 'supertrend(src,len,period=3)', //Supertrend indicator

swma = 'swma(src,len)', //Sine-Weighted Moving Average

tema = 'tema(src,len)', //Triple EMA (Same as EMA with 3 factor)

tma = 'tma(src,len)', //Triangular Moving Average

vida = 'vida(src,len)', //Variable Index Dynamic Average

vwma = 'vwma(src,len)', //Volume Weigted Moving Average

wma = 'wma(src,len)', //Weigted Moving Average

angle = 'angle(src,len)', //angle of the series (Use its Input as another indicator output)

atr = 'atr(src,len)', //average true range. RMA of true range.

bbr = 'bbr(src,len,mult=1)', //bollinger %%

bbw = 'bbw(src,len,mult=2)', //Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci(src,len)', //commodity channel index

cctbb = 'cctbbo(src,len)', //CCT Bollinger Band Oscilator

chng = 'change(src,len)', //Difference between current value and previous, source - source .

cmo = 'cmo(src,len)', //Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog(src,len)', //The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve(src,len)', //Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl(src,len)', //Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count = 'count(src,len)', //green avg - red avg

dev = 'dev(src,len)', //ta.dev() Measure of difference between the series and it's ta.sma

fall = 'falling(src,len)', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr(src,len,mult=2)', //Keltner Channels Range

kcw = 'kcw(src,len,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd(src,len)', //macd

mfi = 'mfi(src,len)', //Money Flow Index

nvi = 'nvi()', //Negative Volume Index

obv = 'obv()', //On Balance Volume

pvi = 'pvi()', //Positive Volume Index

pvt = 'pvt()', //Price Volume Trend

rise = 'rising(src,len)', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc(src,len)', //Rate of Change

rsi = 'rsi(src,len)', //Relative strength Index

smosc = 'smi_osc(src,len,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig(src,len,fast=5, slow=34)', //smi Signal

stdev = 'stdev(src,len)', //Standart deviation

trix = 'trix(src,len)' , //the rate of change of a triple exponentially smoothed moving average.

tsi = 'tsi(src,len)', //True Strength Index

vari = 'variance(src,len)', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc(src,len)', //Williams %R

wad = 'wad()', //Williams Accumulation/Distribution.

wvad = 'wvad()' //Williams Variable Accumulation/Distribution.

}

f_func(string, float, simple, float, float, float, simple) f_func Return selected indicator value with different parameters. New version. Use extra parameters for available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

Returns: float Return calculated indicator value

fn_heikin(float, float, float, float) fn_heikin Return given src data (open, high,low,close) as heikin ashi candle values

Parameters:

float : o_ open value

float : h_ high value

float : l_ low value

float : c_ close value

Returns: float heikin ashi open, high,low,close vlues that will be used with plotcandle

fn_plotFunction(float, string, simple, bool) fn_plotFunction Return input src data with different plotting options

Parameters:

float : src_ indicator src_data or any other series.....

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

Returns: float

fn_funcPlotV2(string, float, simple, float, float, float, simple, string, simple, bool, bool) fn_funcPlotV2 Return selected indicator value with different parameters. New version. Use extra parameters fora available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return calculated indicator value

fn_factor(string, float, simple, float, float, float, simple, simple, string, simple, bool, bool) fn_factor Return selected indicator's factorization with given arguments

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

simple : int fact_ Add double triple, Quatr factor to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return result of the function

fn_plotCandles(string, simple, float, float, float, simple, string, simple, bool, bool, bool) fn_plotCandles Return selected indicator's candle values with different parameters also heikinashi is available

Parameters:

string : FuncType_ indicator from the indicator list

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

bool : plotheikin_ Use Heikin Ashi on Plot

Returns: float

supertrendHere is an extensive library on different variations of supertrend.

Library "supertrend"

supertrend : Library dedicated to different variations of supertrend

supertrend_atr(length, multiplier, atrMaType, source, highSource, lowSource, waitForClose, delayed) supertrend_atr: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

length : : ATR Length

multiplier : : ATR Multiplier

atrMaType : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

source : : Default is close. Can Chose custom source

highSource : : Default is high. Can also use close price for both high and low source

lowSource : : Default is low. Can also use close price for both high and low source

waitForClose : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

delayed : : if set to true lags supertrend atr stop based on target levels.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_bands(bandType, maType, length, multiplier, source, highSource, lowSource, waitForClose, useTrueRange, useAlternateSource, alternateSource, sticky) supertrend_bands: Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Parameters:

bandType : : Type of band used - can be bb, kc or dc

maType : : Moving Average type for Bands. This can be sma, ema, hma, rma, wma, vwma, swma

length : : Band Length

multiplier : : Std deviation or ATR multiplier for Bollinger Bands and Keltner Channel

source : : Default is close. Can Chose custom source

highSource : : Default is high. Can also use close price for both high and low source

lowSource : : Default is low. Can also use close price for both high and low source

waitForClose : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

useTrueRange : : Used for Keltner channel. If set to false, then high-low is used as range instead of true range

useAlternateSource : - Custom source is used for Donchian Chanbel only if useAlternateSource is set to true

alternateSource : - Custom source for Donchian channel

sticky : : if set to true borders change only when price is beyond borders.

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

supertrend_zigzag(length, history, useAlternateSource, alternateSource, source, highSource, lowSource, waitForClose, atrlength, multiplier, atrMaType) supertrend_zigzag: Zigzag pivot based supertrend

Parameters:

length : : Zigzag Length

history : : number of historical pivots to consider

useAlternateSource : - Custom source is used for Zigzag only if useAlternateSource is set to true

alternateSource : - Custom source for Zigzag

source : : Default is close. Can Chose custom source

highSource : : Default is high. Can also use close price for both high and low source

lowSource : : Default is low. Can also use close price for both high and low source

waitForClose : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

atrlength : : ATR Length

multiplier : : ATR Multiplier

atrMaType : : Moving Average type for ATR calculation. This can be sma, ema, hma, rma, wma, vwma, swma

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

Swing Stock Market Multi MA Correlation This is a swing strategy adapted to stock market using correlation with either SP500 or Nasdaq, so its best to trade stocks from this region.

Its components are

Correlation Candle

Fast moving average to choose from SMA , EMA , SMMA (RMA), WMA and VWMA

Medium moving Average to choose from SMA , EMA , SMMA (RMA), WMA and VWMA

Slow moving average to choose from SMA , EMA , SMMA (RMA), WMA and VWMA

Rules for entry

Long: fast ma > medium ma and medium ma > slow ma

Short: fast ma< medium ma and medium ma < slow ma.

Rules for exit

We exit when we receive an inverse condition.

Caution:

This strategy use no risk management inside, so be careful with it .

If you have any questions, let me know !

+ JMA KDJ with RSI OB/OS SignalsSo, what is the KDJ indicator? If you're familiar with the Stochastic, then you'll know that the two oscillating lines are called the 'K' and 'D' lines. Now you know that this is some sort of implementation of the Stochastic. But, then, what is the J? The 'J' is simply the measure of convergence/divergence of the 'K' and 'D' lines, and the 'J' crossing the 'K' and 'D' lines is representational of the 'K' and 'D' lines themselves crossing. Is this an improvement over simply using the Stochastic as it is? Beats me. I don't use the Stochastic. I stumbled upon the KDJ while surfing around the web, and it sounded cool, so I thought I'd look at it. I do like it a bit more as the 'J' line being far overextended from the other two (usually into overbought/sold territory) does give a clear visual representation of the divergence of the 'K' and 'D' lines, which you might not notice otherwise. So, from that perspective I suppose it is nicer.

But let's get to the good stuff now, shall we? What did I do here?

Well, first thing you're wondering is why there are only two lines when based on my explanation (or your previous experience with the indicator) there should be three. I found this script here on TV, by x4random, who took the 'K' and 'D' lines and made an average of them, so there is only one line instead of the two. So, fewer lines on the indicator, but still the same usefulness. It was in older TV code, so I took it to version4 and cleaned up the code slightly. His indicator included the RSI ob/os plots, and I thought this was neat (even though the RSI being os/ob doesn't tell you much except that the trend is strong, and you should be buying pullback or selling rallies) so I kept them in. His indicator was also the most visually appealing one that I saw on here, so that attracted me too. Credit to x4random for the indicator, though.

Aside from code cleanup and adding the usual bells and whistles (which I will get to) the big thing I did here was change is RMA that he was using for the 'K' and 'D' lines to a Jurik MA's, which smooth a lot of the noise of other moving averages while maintaining responsiveness. This eliminates noise (false signals) while keeping the signals of significance. It took me a while to figure out how to substitute the JMA for the RMA, but thanks to QuantTherapy's "Jurik PPO" indicator I was able to nail down the implementation. One thing you might notice is that there is no input to change signal length. I fiddled with this for a time before sticking to using the period, instead of the signal (thus eliminating the use of the signal input altogether), length to generate the 'K' and 'D' calculations. To make any adjustments other than the period length use the Jurik Power input. You can use the phase input as well, but it has much less of an effect.

Everything else I changed is pretty much cosmetic.

Candle coloring with the option to color candles based on either the 'J' line or the 'KD' line.

color.from_gradients with color inputs to make it beautiful (this is probably my best looking indicator, imo)

plots for when crosses occur (really wish there was a way to plot these over candlesticks! If anyone has any suggestions I'd love to see!)

I think that's about it. Alerts of course.

Enjoy!

Below is a comparison chart of my JMA implementation to the original RMA script.

You can see how much smoother the JMA version is. Both of these had the default period of 55 set, and the JMA version is using the default settings, while the original version is using a length of 3 for the signal line.

Stochastic Momentum Index - SMI🎯 Overview

This is a Stochastic Momentum Index (SMI) indicator that combines stochastic momentum with moving average smoothing to identify trend direction and momentum strength in financial markets. The SMI measures where the current price closes relative to the midpoint of its recent trading range, providing enhanced sensitivity to price momentum.

🧩 Core Components

1. ⚙️ Technical Foundation

📊 Primary Calculation: Uses TradingView's built-in ta.stoch() function

📈 Range-Based: Compares closing price to high-low range over specified period

🎯 Scale: Oscillates between 0-100 with 50 as neutral midpoint

2. 🎛️ Configuration Parameters

📏 SMI Length: Default 101 periods (long-term smoothing)

📊 Source Price: Customizable (default = Close)

📈 MA Length: 30-period moving average applied to SMI

🔄 MA Type: 6 options (EMA, SMA, RMA, WMA, VWMA, HMA)

🎨 Color Themes: 5 visual schemes (Classic, Modern, Robust, Accented, Monochrome)

📈 Signal Interpretation:

🟢 BULLISH: SMI > 50 (price closing in upper half of range)

🔴 BEARISH: SMI < 50 (price closing in lower half of range)

🎯 Neutral Zone: Around 50 indicates balanced momentum

👁️ Visual Features

📈 Signal Line (MA):

Yellow moving average of SMI

Smooths momentum for clearer trend identification

🎯 Reference Lines:

50-level midpoint (white dashed line)

0-100 scale boundaries

🎨 Fill Zones:

🟢 Upper Zone : Bullish momentum area

🔴 Lower Zone : Bearish momentum area

Gradient fills enhance visual clarity

📋 Dashboard Display:

Content: "⬆️ Bullish" or "⬇️ Bearish" indicator

Purpose: Quick market bias assessment

⚡ Trading Applications

📈 Primary Uses:

🎯 Trend Identification

SMI > 50 = Uptrend momentum

SMI < 50 = Downtrend momentum

📊 Momentum Strength

Values near 100 = Strong bullish momentum

Values near 0 = Strong bearish momentum

Values around 50 = Neutral/consolidation

🔄 Mean Reversion

Extreme readings (near 0 or 100) may indicate overbought/oversold conditions

⏰ Timeframe Compatibility:

📅 Long-term: 101-period default suits swing/position trading

📊 Medium-term: Adjust lengths for daily/weekly analysis

⚡ Short-term: Reduce periods for intraday trading

🎨 Customization Options

🔄 Moving Average Types:

📉 EMA: Exponential - responsive to recent changes

📊 SMA: Simple - equal weight to all periods

📈 RMA: Relative - TradingView's special moving average

⚖️ WMA: Weighted - emphasizes recent data

💎 VWMA: Volume-weighted - incorporates volume

🚀 HMA: Hull - reduces lag significantly

🎨 Visual Themes:

🎨 Classic: Green/Red (traditional trading colors)

🚀 Modern: Cyan/Purple (modern aesthetic)

💪 Robust: Amber/Deep Purple (high contrast)

🌈 Accented: Purple/Magenta (vibrant)

⚫⚪ Monochrome: Light Gray/Dark Gray (minimalist)

🔔 Alert System

🟢 LONG Alert: Triggers when SMI crosses above 50

🔴 SHORT Alert: Triggers when SMI crosses below 50

📧 Format: Includes ticker symbol for easy identification

⚡ Key Advantages

✅ Strengths:

🎯 Clear Signals: Simple >50/<50 threshold for easy interpretation

📊 Range-Bound: Always oscillates 0-100 (no divergence issues)

👁️ Visual Clarity: Color-coded zones make analysis intuitive

🔄 Customizable: Multiple MA types and visual themes

📱 Professional: Clean, organized display suitable for all traders

Momentum RSIMomentum RSI (MRSI | MisinkoMaster)

Momentum RSI is an enhanced version of the classic Relative Strength Index (RSI) developed by J. Welles Wilder. This indicator integrates momentum components directly into the RSI calculation, resulting in a faster, smoother oscillator that helps traders identify trend strength and value zones with greater precision.

Unlike the traditional RSI, which relies on a fixed smoothing approach, the Momentum RSI dynamically incorporates momentum derived from differences between moving averages of RSI values over different lookback periods. This improves signal responsiveness while reducing noise, providing clearer insights for both trend-following and mean-reversion trading strategies.

🔍 Concept & Idea

Momentum RSI aims to improve the original RSI by adding momentum elements that speed up its reaction to price changes without sacrificing smoothness. This hybrid approach helps:

Capture early signals in trending markets

Reduce false signals during sideways or choppy conditions

Highlight overbought and oversold zones more effectively

Provide additional momentum context for more informed trading decisions

By combining RSI with momentum derived from moving average differences, the indicator balances sensitivity and stability for a versatile application across different asset classes and timeframes.

⚙️ How It Works

The Momentum RSI calculation involves several key steps:

Standard RSI Calculation:

The indicator first calculates the classic RSI using user-defined length and smoothing parameters. Users can customize the RSI source price and the smoothing moving average (MA) type applied (options include RMA, SMA, EMA, WMA, DEMA, TEMA, HMA, ALMA).

Momentum Derivation:

Two versions of the RSI are computed with different smoothing lengths—a base RSI and a longer smoothed RSI. The difference between their moving averages represents a momentum component that measures the short-term trend strength.

Additional Momentum:

The difference between shorter-length and longer-length RSI calculations adds another momentum layer, reflecting momentum shifts over different timescales.

Momentum Integration:

These momentum components are combined and added to the previous RSI value, resulting in a momentum-enhanced RSI value (mrsi) that oscillates between 0 and 100.

Trend Detection:

Customizable upper and lower thresholds define long and short signal zones, allowing users to interpret when the market is trending bullish or bearish.

Overbought/Oversold Zones:

Additional thresholds highlight extreme value zones for potential mean-reversion trades.

🧩 Inputs Overview

RSI Length - Controls the primary RSI calculation length (default 20).

Source - Selects the price source for the RSI calculation (default: close).

Smoothing Length - Length used to smooth RSI values with the chosen MA type (default 12).

MA Type - Moving average method used for smoothing (options: RMA, SMA, EMA, WMA, DEMA, TEMA, HMA, ALMA).

ALMA Offset - Offset parameter for ALMA smoothing (applicable only if ALMA is selected).

ALMA Sigma - Sigma parameter for ALMA smoothing (applicable only if ALMA is selected).

Upper Threshold - RSI level above which a bullish (long) signal is triggered (default 55).

Lower Threshold - RSI level below which a bearish (short) signal is triggered (default 45).

Overbought Threshold - RSI level indicating overbought conditions (default 85).

Oversold Threshold - RSI level indicating oversold conditions (default 15).

📌 Usage Notes

Versatile Application: Use Momentum RSI for both trend-following and mean-reversion strategies.

Signal Clarity: The momentum integration reduces noise, helping avoid false breakouts and improving entry timing.

Customization: Adjust smoothing lengths and MA types to match the characteristics of your trading style or the specific asset.

Visual Aids: Background colors, candle coloring, and shape markers facilitate quick interpretation of momentum strength and trend changes.

Threshold Sensitivity: Fine-tune thresholds to balance between early signals and signal reliability.

Intrabar Updates: Signals may update on lower timeframes for responsive trading.

Combine with Other Tools: For best results, use Momentum RSI alongside volume, price action, or other confirmation indicators.

Backtest Before Live Trading: Always validate settings on historical data to ensure suitability for your trading instrument and timeframe.

⚠️ Disclaimer

This script is intended for educational and analytical purposes only and does not constitute financial advice. Trading involves risk, and users should perform their own due diligence before making any trading decisions.

Moving Average Exponential//@version=6

indicator(title="Moving Average Exponential", shorttitle="EMA", overlay=true, timeframe="", timeframe_gaps=true)

len = input.int(9, minval=1, title="Length")

src = input(close, title="Source")

offset = input.int(title="Offset", defval=0, minval=-500, maxval=500, display = display.data_window)

out = ta.ema(src, len)

plot(out, title="EMA", color=color.blue, offset=offset)

// Smoothing MA inputs

GRP = "Smoothing"

TT_BB = "Only applies when 'SMA + Bollinger Bands' is selected. Determines the distance between the SMA and the bands."

maTypeInput = input.string("None", "Type", options = , group = GRP, display = display.data_window)

var isBB = maTypeInput == "SMA + Bollinger Bands"

maLengthInput = input.int(14, "Length", group = GRP, display = display.data_window, active = maTypeInput != "None")

bbMultInput = input.float(2.0, "BB StdDev", minval = 0.001, maxval = 50, step = 0.5, tooltip = TT_BB, group = GRP, display = display.data_window, active = isBB)

var enableMA = maTypeInput != "None"

// Smoothing MA Calculation

ma(source, length, MAtype) =>

switch MAtype

"SMA" => ta.sma(source, length)

"SMA + Bollinger Bands" => ta.sma(source, length)

"EMA" => ta.ema(source, length)

"SMMA (RMA)" => ta.rma(source, length)

"WMA" => ta.wma(source, length)

"VWMA" => ta.vwma(source, length)

// Smoothing MA plots

smoothingMA = enableMA ? ma(out, maLengthInput, maTypeInput) : na

smoothingStDev = isBB ? ta.stdev(out, maLengthInput) * bbMultInput : na

plot(smoothingMA, "EMA-based MA", color=color.yellow, display = enableMA ? display.all : display.none, editable = enableMA)

bbUpperBand = plot(smoothingMA + smoothingStDev, title = "Upper Bollinger Band", color=color.green, display = isBB ? display.all : display.none, editable = isBB)

bbLowerBand = plot(smoothingMA - smoothingStDev, title = "Lower Bollinger Band", color=color.green, display = isBB ? display.all : display.none, editable = isBB)

fill(bbUpperBand, bbLowerBand, color= isBB ? color.new(color.green, 90) : na, title="Bollinger Bands Background Fill", display = isBB ? display.all : display.none, editable = isBB)

Multi-Sigma Bands [fmb]Multi-Sigma Bands plots standard deviation (sigma) bands around a selectable basis (SMA, EMA, RMA, or Linear Regression). It’s designed to help you spot when price is behaving “normally” versus when it’s stretching into statistically extended territory.

What it shows

- Basis: the central reference line (your chosen basis type)

- ±1σ zone: the common range where price spends much of its time

- ±2σ zone: extended range where moves often become more emotional or trend-driven

- ±3σ zone: extreme range where price is statistically stretched (risk increases)

How to read it

- Inside ±1σ

- Often normal behaviour and mean-reverting price action around the basis.

- Between ±1σ and ±2σ

- A meaningful extension. In trends, price can “walk” these areas for longer than expected.

- Between ±2σ and ±3σ

- Rare extension. Can signal exhaustion, blow-off behaviour, or capitulation depending on direction and context.

How traders typically use it

- Trend context

- In strong uptrends, price may ride the upper bands (+1σ to +2σ) repeatedly.

- In strong downtrends, the lower bands (-1σ to -2σ) can act the same way.

- Bands show statistical stretch, not automatic reversal signals.

- Extension and risk framing

- The farther price is from the basis, the more “stretched” it is.

- That usually means chasing becomes riskier and entries require tighter confirmation.

- Range behaviour

- Ranges often oscillate around the basis, with frequent returns toward the middle zone.

Settings

- Source: what price series to use (Close by default)

- Length: lookback used for both basis and standard deviation

- Basis: SMA, EMA, RMA, or LinReg

- Stdev smoothing: optional smoothing on standard deviation for cleaner bands

- σ multipliers: customise σ1, σ2, σ3 (defaults: 1, 2, 3)

- Force Monthly Data (optional): calculate bands using a higher-timeframe source to reduce noise and focus on macro structure

Disclaimer

This indicator is for informational and educational purposes only and is not financial advice. Always use risk management and confirm with market structure and trend context.

Luminous Volume Flow [Pineify]Luminous Volume Flow

The Luminous Volume Flow is a specialized volume-based momentum oscillator designed to uncover the underlying buying and selling pressure within the market. Unlike traditional volume indicators that simply aggregate volume based on the close relative to the open, LVF analyzes intrabar dynamics—specifically the relationship between the close price and the high/low wicks—to estimate the dominance of buyers or sellers.

By smoothing this raw volume delta and applying a signal line, the LVF provides a clear visual representation of volume flow, helping traders identify trend strength, potential reversals, and momentum shifts with high-definition "luminous" visuals.

Key Features

Intrabar Pressure Analysis : Calculates buying and selling pressure based on wick dynamics and price polarity to provide a more granular view of market sentiment.

Multi-Type Smoothing : Offers selectable Moving Average types (SMA, EMA, RMA) for the main Flow Line to adapt to different market volatilities.

Luminous Visuals : Utilizes dynamic color gradients that brighten as momentum expands and darken as it contracts, offering immediate visual feedback on trend intensity.

Sentiment Cloud : Fills the area between the Flow and Signal lines to clearly visualize the prevailing bullish or bearish sentiment.

High-Contrast Signals : Optional high-contrast signal markers for clear crossover identification.

How It Works

The LVF operates on a multi-stage calculation process:

Pressure Calculation : The script compares the lower wick (Close - Low) against the upper wick (High - Close).

If the lower wick is longer, it suggests buying pressure (rejection of lower prices), and volume is assigned to Buy Pressure .

If the upper wick is longer, it suggests selling pressure (rejection of higher prices), and volume is assigned to Sell Pressure .

If equal, the Close > Open polarity is used as a tie-breaker.

Raw Delta : The difference between Buy and Sell Pressure is calculated to determine the net volume flow for the bar.

Flow Line : The Raw Delta is smoothed using a user-selected Moving Average (SMA, EMA, or RMA) over the Flow Length period. This creates the main oscillator line.

Signal Line : An EMA of the Flow Line is calculated to generate the Signal Line, similar to the MACD mechanic.

Histogram : The difference between the Flow Line and Signal Line determines the Histogram, which drives the "Luminous" color gradient logic.

Trading Ideas and Insights

Trend Confirmation : When the Flow Line is above the Signal Line and the Cloud is green, the bullish trend is supported by volume. Conversely, a red cloud indicates bearish volume dominance.

Momentum Crossovers : The triangle shapes indicate crossovers between the Flow and Signal lines. A triangle up (Green) suggests a potential bullish entry or invalidation of a short bias. A triangle down (Red) suggests a bearish turn.

Expansion vs. Contraction : Pay attention to the brightness of the histogram columns. Bright colors indicate expanding momentum (a strong move), while darker, fading colors suggest the move is losing steam, potentially preceding a consolidation or reversal.

How multiple components work together

This script combines the logic of Volume Delta analysis with Signal Line Crossover mechanics (popularized by MACD). By applying trend-following smoothing to raw volume data, we transform erratic volume spikes into a coherent flow. The "Luminous" visual layer is added to make the data interpretation intuitive—removing the need to mentally calculate the rate of change based on histogram height alone.

Unique Aspects

Adaptive Gradient Coloring : The histogram doesn't just show positive/negative values; it visually communicates the *acceleration* of the move via color intensity based on standard deviation.

Wick-Based Volume Attribution : Instead of a binary close-to-open comparison, LVF respects the price action within the candle (the wicks), acknowledging that a long lower wick on a red candle can actually represent significant buying interest.

How to Use

Add the indicator to your chart.

Adjust the Flow Length to match your trading timeframe (lower for scalping, higher for swing trading).

Select your preferred Smoothing Type (EMA is default and recommended for responsiveness).

Use the "Sentiment Cloud" filter: Look for long signals only when the cloud is green, and short signals when the cloud is red.

Monitor the Luminous Histogram for signs of exhaustion (colors fading) to manage exits.

Customization

Flow Length : Period for the main smoothing (Default: 14).

Signal Length : Period for the signal line (Default: 9).

Smoothing Type : Choose between SMA, EMA, or RMA.

Colors : Fully customizable colors for Bullish/Bearish phases and signals.

Chart Bars : Option to color the main chart candles based on the Flow direction.

Conclusion

The Luminous Volume Flow is a robust tool for traders who want to go beyond price action and understand the volume dynamics driving the market. By visualizing the flow of buying and selling pressure with advanced smoothing and reactive visuals, it provides a clearer picture of market sentiment than standard volume bars.

Institutional Alpha Vector | D_QUANT Institutional Alpha Vector | D_QUANT

Overview

The Institutional Alpha Vector (IAV) is an original trend-following framework that replaces single-indicator bias with a Weighted Composite Score . Instead of relying on a simple moving average, this script aggregates four distinct quantitative dimensions—Price, Momentum, Volatility, and Volume—into a normalized value called the "Alpha Vector."

The goal of this tool is to identify "Institutional Consensus"—periods where multiple mathematical models align in the same direction, reducing the likelihood of false breakouts in choppy markets.

How It Works: The Quantitative Engines

The script calculates four independent signals. For each module, a state is stored (1 for Bullish, -1 for Bearish, 0 for Neutral).

1. Price Filter (Hull Moving Average):

The script uses an HMA (a weighted moving average that reduces lag by using the square root of the period). A signal is triggered when the price crosses over/under this "Spine."

2. Volatility Regime (RMA + ATR):

This module uses a Moving Average (RMA) combined with an Average True Range (ATR) offset. It acts as a volatility filter that price must move beyond 1 ATR from the mean to register a trend, ensuring the market isn't just "drifting."

3. Momentum Physics (ADX/DMI):

Based on J. Welles Wilder’s Directional Movement Index. It checks if the is above (or vice versa) but only if the ADX (Average Directional Index) is above a user-defined threshold (default: 10), confirming the presence of a strong trend.

4. Institutional Flow (Chaikin Money Flow):

This confirms price action with volume. It calculates the accumulation/distribution of money flow over a specific period. A signal is only valid if the CMF is positive (Bullish) or negative (Bearish).

The Alpha Vector Calculation

This is the core "originality" of the script. The indicator takes the active modules and calculates a Composite Score :

This results in a value between -1.0 and +1.0 .

* High Confidence Long: When the score exceeds +0.1 (adjustable).

* High Confidence Short: When the score drops below -0.1 (adjustable).

* Neutral Zone: When the score is near 0, the script colors the bars grey, signaling a lack of institutional consensus.

Visual Intelligence: The "Electric Conduit"

The script visualizes market energy through a custom rendering engine:

* The Spine: A central line representing the HMA trend.

* The Conduit (Fill): A dynamic gradient that expands or contracts based on the ATR (Average True Range) . This allows traders to see "volatility expansion" (wide ribbon) vs "compression" (tight ribbon) at a glance.

* Bar Coloring : Automatically aligns the chart candles with the Alpha Vector state to remove cognitive load.

How to Use

1. Define your Strategy: In the settings, you can toggle specific modules. If you are trading a low-volume asset, you might disable the **CMF** module.

2. Identify the Consensus: Look for the ribbon to change from Grey (Neutral) to Cyan/Gold.

3. Monitor the HUD: A small dashboard in the bottom right displays the live Alpha Vector score. A score of 1.0 means all four engines are in 100% bullish agreement.

Disclaimer: Trading involves significant risk. This tool is for educational and analytical purposes and does not constitute financial advice.

SuperRSI: Enhanced MomentumTitle: SuperRSI: Enhanced Momentum

Description:

Overview The SuperRSI is not your standard Relative Strength Index. While traditional RSI calculates momentum based solely on close prices, this "Titan Edition" incorporates price structure breakouts. It analyzes whether the price is breaking new highs or lows within the lookback period to calculate momentum. This makes the SuperRSI significantly more responsive to volatility and genuine market action than the classic formula.

Key Features

Titan Calculation Logic: Uses High/Low breakouts to capture true momentum, making it faster and more sensitive than standard RSI.

Dynamic Trend Coloring: The RSI line automatically changes color to give you an instant visual bias:

Green: RSI is above the Signal Line (Bullish Momentum).

Red: RSI is below the Signal Line (Bearish Momentum).

Signal Line Filtering: Includes a built-in "Slow Signal" (EMA based) to help filter out market noise and identify sustainable trends.

Visual Gradients: Clear background fills for Overbought (OB) and Oversold (OS) zones to highlight extreme conditions.

How to Use

Trend Identification: Simply look at the line color. If it’s Green, momentum is bullish. If it’s Red, momentum is bearish.

Entry & Exit Signals: Watch for the crossover between the RSI line and the Signal Line. A cross above is a buy signal; a cross below is a sell signal.

Overbought/Oversold:

Above 80: Extreme bullish momentum (potential reversal or strong trend continuation).

Below 20: Extreme bearish momentum.

Settings

Fully customizable lengths for RSI and Signal lines.

Adjustable Smoothing methods (RMA, SMA, EMA).

Customizable Overbought/Oversold levels (Default: 80/20)

العنوان: SuperRSI: Enhanced Momentum

الوصف:

نظرة عامة مؤشر SuperRSI ليس مجرد مؤشر قوة نسبية تقليدي. بينما يعتمد الـ RSI العادي على أسعار الإغلاق فقط، تعتمد هذه النسخة المطور (Titan Edition) على اختراقات الهيكل السعري. يقوم المؤشر بحساب الزخم بناءً على ما إذا كان السعر يكسر قمماً جديدة أو قيعانًا جديدة خلال الفترة المحددة. هذا يجعله أكثر استجابة للتقلبات وحركة السوق الحقيقية مقارنة بالمعادلة الكلاسيكية.

أهم المميزات

معادلة Titan للزخم: تستخدم اختراقات القمم والقيعان (High/Low) لالتقاط الزخم الحقيقي، مما يجعله أسرع وأدق من RSI العادي.

تلوين ديناميكي للاتجاه: يتغير لون خط المؤشر تلقائياً ليعطيك رؤية فورية للاتجاه:

اللون الأخضر: الـ RSI يتداول فوق خط الإشارة (زخم صاعد).

اللون الأحمر: الـ RSI يتداول تحت خط الإشارة (زخم هابط).

فلترة الإشارات: يحتوي على "خط إشارة" مدمج (Slow Signal) لتنقية ضجيج السوق (Noise) وتحديد الاتجاهات المستدامة.

تدرجات لونية: خلفيات واضحة لمناطق التشبع الشرائي (Overbought) والتشبع البيعي (Oversold).

طريقة الاستخدام

تحديد الاتجاه: انظر ببساطة إلى لون الخط. إذا كان أخضر فالزخم شرائي، وإذا كان أحمر فالزخم بيعي.

إشارات الدخول والخروج: راقب التقاطع بين خط الـ RSI وخط الإشارة. التقاطع لأعلى يعتبر إشارة شراء، والتقاطع لأسفل يعتبر إشارة بيع.

مناطق التشبع:

فوق 80: تشبع شرائي (احتمالية انعكاس أو استمرار قوي للترند).

تحت 20: تشبع بيعي.

الإعدادات

إمكانية تعديل المدة الزمنية (Length) للـ RSI وخطوط الإشارة.

خيارات متعددة لنوع المتوسط المستخدم (RMA, SMA, EMA).

مستويات تشبع قابلة للتعديل (الافتراضي: 80/20).

FxInside// This Pine Script® code is subject to the terms of the Mozilla Public License 2.0 at mozilla.org

// © yyy_trade

//@version=6

indicator("FxInside", overlay = true, max_lines_count = 500)

lineColor = input.color(color.new(color.blue, 12), "FxLineColor")

type vaild_struct

float high

float low

int time

type fx

string dir

chart.point point

var array valid_arr = array.new()

var fx lastFx = na

var float motherHigh = na

var float motherLow = na

isInsideBar = high <= high and low >= low

if isInsideBar and na(motherHigh)

motherHigh := high

motherLow := low

isExtendedInsideBar = not na(motherHigh) and high <= motherHigh and low >= motherLow

body_color = input.color(color.new(color.orange, 0), "实体颜色")

wick_color = input.color(color.new(color.orange, 0), "影线颜色")

border_color = input.color(color.new(color.orange, 0), "边框颜色")

plotcandle(open, high, low, close, color=isExtendedInsideBar ? body_color : na, wickcolor=isExtendedInsideBar ? wick_color : na, bordercolor =isExtendedInsideBar ? border_color : na ,editable=false)

if not na(motherHigh) and (high > motherHigh or low < motherLow)

motherHigh := na

motherLow := na

// 以下为分型折线逻辑,如不需要可删除