3D SYSTEM CORP. IS LOOKING BULLISH*Some indicators are bullish.

*TD Count has been started with green.

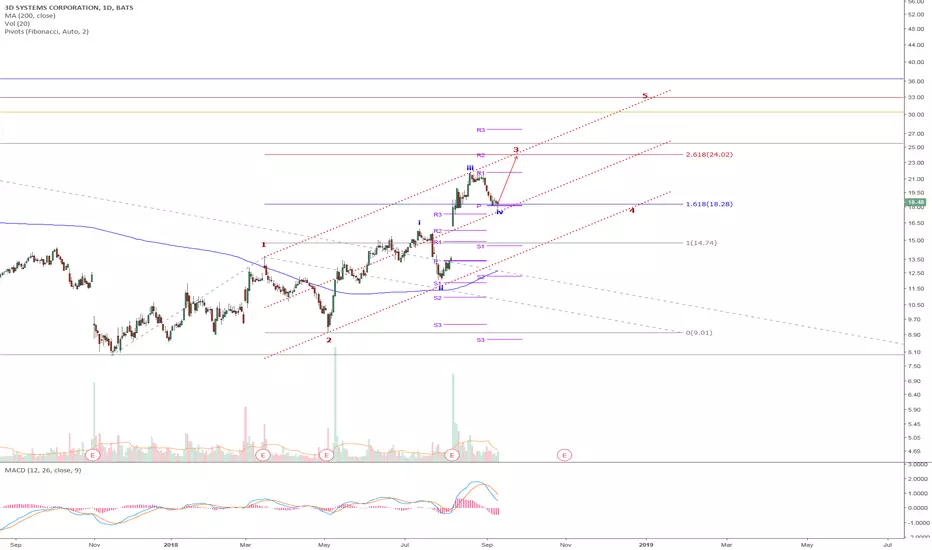

DDD looks like bullish. Non-targeting bullish move, what i expecting for this week.

Trade ideas

ddd1y Target Est 13,86

The 3D printing industry has been quietly rebuilding following the incredible run-up in 2013 that ended with an equally spectacular collapse. Turns out additive manufacturing technology wasn't quite ready for prime time. Judging from continued losses around the industry, there's a ways to go yet. But that didn't stop Wall Street and investors from rewarding 3D Systems (NYSE:DDD) with a 67% stock gain in August.

The industry leader reported second-quarter 2018 adjusted earnings that were better than analysts had expected. Yet while the additive manufacturing powerhouse continues to expand its core offerings and leverage high-margin business opportunities in healthcare, operating income and cash flow were lower in the first half of this year than in 2017. Looking ahead, is there anything that might make 3D Systems stock a buy?

person using 3D printing machine

IMAGE SOURCE: GETTY IMAGES.

By the numbers

Three numbers ruled the company's second-quarter 2018 earnings report. First, adjusted EPS came in at $0.06, which, although worse than the year-ago period, smoked the average analyst expectation for only $0.01. Second, 3D printer revenue jumped 41% year over year, which was a surprising result.

Third, healthcare applications comprised 34.7% of total revenue, up from 30.4% this time last year. Healthcare revenue tallied $113.8 million in the first six months of 2018, representing one-third of all revenue and powering the overall growth of the top line.

Metric

First Half 2018

First Half 2017

Year-Over-Year Change

Revenue

$342.4 million

$315.9 million

8.3%

Gross profit

$164.0 million

$160.8 million

2%

Operating income

($25.2 million)

($15.9 million)

N/A

Net income

($29.6 million)

($17.9 million)

N/A

Operating cash flow

$9.2 million

$18.6 million

(51%)

As the table above demonstrates, revenue growth since the first half of 2017 has not been met with improved profitability. Even worse, 3D Systems reported a deteriorating bottom line and operating cash flow. One big reason: Selling, general, and administrative expense reached 41% of revenue. That's higher than industry peer Stratasys, which delivered 37% on the same metric in the first half of this year. Both are relatively high -- which helps to explain why neither business is profitable.

Simply put, 3D Systems needs to do a better job reining in expenses as it scales the business. Can new product launches lead to a brighter future?

Looking ahead

In August, 3D Systems launched two new printers that could prove critical to its future. The first, the NextDent 5100, is aimed at providing dental offices with fast and high-quality runs of trays, models, surgical guides, dentures, crowns, and bridges. The company claims the $10,000 printer, tied to its 2017 acquisition of a dental materials company called Vertex, is four times faster than the competition.

The idea is to allow dental offices to improve their workflows by forgoing the postal system without sacrificing quality, courtesy of coupling the portable NextDent 5100 printer with the company's software tools and making the system compatible with industry-standard oral scanning and dental software solutions. It's too early for investors to know how it'll fare, but it could grow into an important avenue for recurring material sales.

The second printer launched last month was the Figure 4 Standalone, which specializes in low-volume production applications where speed is valuable. That's not to suggest it sacrifices on accuracy, however, as the $21,900 machine boasts six sigma (an engineering standard for reproducibility and quality) repeatability. The target market is mainly R&D and design departments that want to save time in the design, build, test cycle and utilize rapid prototyping.

While the new product launches are encouraging, investors have seen these trickle out time and time again over the years with little impact on profitability. That suggests that it's best to wait and receive confirmation of real-world market traction before getting too excited.

This is a risky 3D-printing stock

Thanks to a huge leap in stock price in August, shares of 3D Systems stack up surprisingly well against the total return (stock performance plus dividends) of the S&P 500 in the last three years. Unfortunately for investors that are all too familiar with volatility, there's not much reason to expect the gains to hold if the business cannot demonstrate sustainable and profitable growth. While the company is increasing its presence in high-margin healthcare markets, that simply hasn't translated into an expanding bottom line. Until that occurs, I think 3D Systems stock is one for investors to avoid.

Patient Long on 3D SystemsAs prices shoot up today, going to wait for a pullback into a demand zone to take a long. Weekly trend is clearly up and so is daily trend.

Prices currently being in a supply zone, going to wait a bit.

DDD: Tricky play....beaten down but recently been talked about.Earning is near (8/7) and can go up to 14.50-15.00. Trading in this range for sometime.

$DDD always was a dog buy few days now ,if you noted as I have, it was a shift into uptrend , usually have a good trading experience in tech , including $DDD

Some option calls may be worth to check out quickly , Cheers and happy profitable trading !

Short Term Long...SoonThese are my ideas on the TA of DDD based on trend lines, volume and RSI/Stoch indicators.

DDD: A long period of consolidation appears over.A 5-wave down followed by a long period of consolidation appears over

Toward the 9Wait with patience to valuate a buy opportunity. Bear signal might be arrived. When will it arrive at 9? I will never know.

Technical Trade to $13.50 w/ Dual Fib Levels AligningThe 3D printing sector was upgraded this year and set to grow because of reduced costs with machines, materials and increased investments in R&D and manufacturing capabilities. I've personally bought a Crealtiy CR-10S to support a small, side business I have. 3D Systems Corp. has been hit hard and dropped to levels that were near a bottom. Through all the volatility in 2018 and its EC, it's held up, slowly sustained across a level and gradually moved upwards. Technical trading for the short term puts it near $13.50 with momentum and without going outside of its consistent range. As of this writing, levels are slightly under trend lines where accumulation is usually not a bad idea. Once it breaks out in its first fib pattern, the second, overlayed fib pattern shows some potential higher PT levels that could be reached if conditions are primed. Volume is never crazy, so I'd recommend setting about a month's time for a trade.

DDD: Buy the breakout and the crossoverBackdrop

Since the positive pre-announcement of last week, the stock has popped and broken its up-channel resistance at $12.

All the while, the SMA 50 has crossed the SMA100 to the upside, providing a "golden-cross" positive cross-over setup.

The stock has since given back some 8% - Been waiting for it to consolidate towards the resistance-turned-support.

Trade setup

Today, it looked compelling to buy the shares, which were further consolidating in a weak market.

Purchased DDD at $12.15, just above the support.

Expect the target to be reached in 4 months.

Risk analysis

Target $16

Stop $10

R/R 2x

DDD needs some affirmations*DDD looks to retest $9.80 before pursuing $11.42 and $12.28*

Good looking stock with momentum and volume. RSI is right in the middle, plenty of room to retest several price points.

Friday's bear volume was nominal, indicating that the confidence level is still good. If the bears came in and drove this price down further than $9.80, the next stopping point is $9.30, along Trending Support.

I think a good buy could be $9.80 with confirmation candles + volume, a dip buy at $9.30 with momentum.

*Let's see what happens!*

*Disclaimer- I am not a financial advisor. These are merely my opinions. Do your own research and formulate your own opinions regarding any moves you make. Seek professional assistance.

DDD needs some affirmation*DDD looks to retest $9.80 before pursuing $11.42 and $12.28*

Good looking stock with momentum and volume. RSI is right in the middle, plenty of room to retest several price points.

Friday's bear volume was nominal, indicating that the confidence level is still good. If the bears came in and drove this price down further than $9.80, the next stopping point is $9.30, along Trending Support.

I think a good buy could be $9.80 with confirmation candles + volume, a dip buy at $9.30 with momentum.

*Let's see what happens!*

*Disclaimer- I am not a financial advisor. These are merely my opinions. Do your own research and formulate your own opinions regarding any moves you make. Seek professional assistance.

Symmetrical Triangle ON WATCHSymmetrical triangles are neutral. Breakout w/ close 3% from line should result in ≈ 18% move from trendline.

If price doesn't breakout before apex regard formation as invalid.