Market cycle topI have reason to believe this cycle will continue until we tag ATH or the next fib 1.618 target which exceed the previous ATH. We now hit the 100% fib target so this could be one of the better buy the dip opportunities that we'll see for a long time.

SP500 trade ideas

S&P 500 Daily Chart Analysis For Week of Sep 19, 2025Technical Analysis and Outlook:

In the trading session of the previous week, the S&P 500 Index demonstrated a significant upward price movement following a severe drawdown on Tuesday. The index successfully reached the Outer Index Rally level of 6620 and is currently progressing towards the established target of the Inner Index Rally at 6704, with the potential for further upward momentum to extend to the Outer Index Rally level of 6768.

It is essential to acknowledge that upon achieving the target of the Inner Index Rally at 6704, the expected price action is likely to initiate a substantial pullback, which is projected to aim for the target Mean Support level of 6585 and may extend to the Mean Support at 6485. Nonetheless, this primary segment of intermediary In Force Retracement pullback is likely to facilitate a considerable rebound, allowing for a subsequent retest of the Outer Index Rally level of 6704.

S&P reaching 6666...what could ever go wrong?There's a healthy does of bullishness as tech companies buy from their neighbors with CAPEX (100% depreciation) and short term rate cuts. The stock market is at the most expensive level, ever, blowing out PE and CAPE ratios. While I hope the economy does better, a pull back is healthy. Many of the leading indicators show bright red, and some are choosing to ignore. I guess time will tell! Best of luck and keep an eye on VIX (UVIX). There's a Volmageddon 2.0 in the making.....

SP500 needs oxygenLike climbing Everest without oxygen. The SP500 hasn't had a break since April. Maybe it needs a break, maybe it's a dangerous buying zone, the risk-reward ratio is too high. Sometimes doing nothing is the best trade. So let's wait. Stay tuned.

SPX for Friday 19th SeptemberPrice movement has got really messy now.That is without the spikes.Direction is unclear

SPX updated for Friday 19th Se[temberI have despiked the chart to expose the trend.There are downward spikes making it difficult to read

S&P 500 | Bullish ContinuationS&P500 is in bullish continuation pattern while printing HHs and HLs with no divergence on any timrframe,which indicates that there is a continuation pattern.

S&P/Nasdaq bearish caseBearish case for equities today:

This count has short-term pain for long-term gain.

Looking for initial pump, then dump over the next few days, target buy below 6144 for S&P and 22226 for Nasdaq.

If correct, VIX (UVIX) should pop.

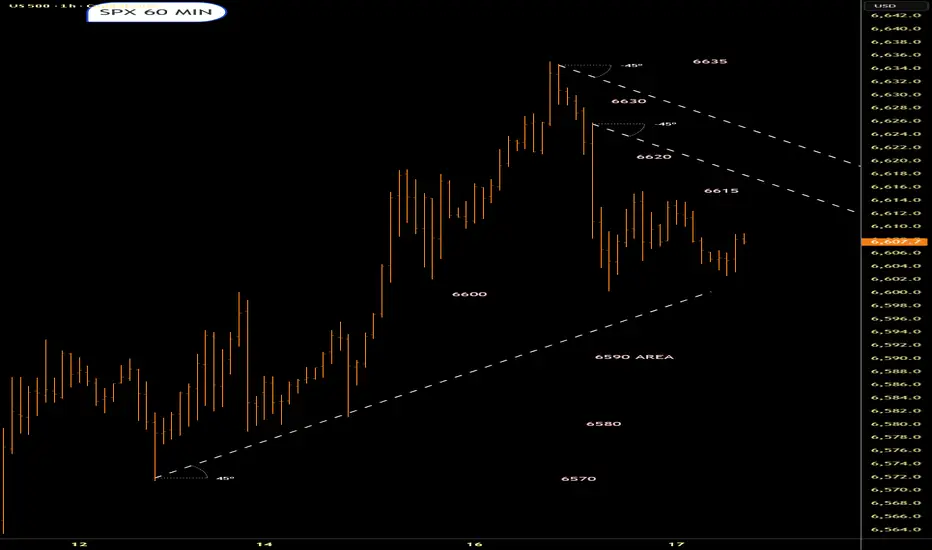

SPX,.Areas of possible interestFOMC day.So could be a tad wild.Possible areas pf interest marked.It might not stay in the pattern.Possible fakes below 6600

Global Commodity Supercycles1. What Is a Commodity Supercycle?

A commodity supercycle refers to a prolonged period (typically 20–40 years) during which commodity prices rise significantly above long-term averages, driven by sustained demand growth, supply constraints, and structural economic shifts. Unlike typical business cycles of 5–10 years, supercycles are much longer and tied to transformational changes in the global economy.

Key features include:

Long Duration: Lasts for decades, not years.

Broad-Based Price Increases: Not limited to one commodity, but a basket (energy, metals, agriculture).

Demand Shock Driven: Triggered by industrial revolutions, urbanization waves, or technological breakthroughs.

Slow Supply Response: Mines, oil fields, and farms take years to scale up, prolonging shortages.

Eventual Bust: Once supply catches up or demand slows, prices collapse, starting a long down-cycle.

2. Historical Commodity Supercycles

Economists often identify four major supercycles since the 19th century.

a) The Industrial Revolution Supercycle (Late 1800s – Early 1900s)

Drivers: Industrialization in the U.S. and Europe, railroad expansion, urban growth.

Key Commodities: Coal, steel, iron, copper.

Impact: Prices soared as cities and factories expanded. Demand for energy and metals fueled new empires. Eventually, productivity gains and resource discoveries (new coal fields, iron ore mines) balanced the market.

b) The Post-War Reconstruction Supercycle (1940s–1960s)

Drivers: World War II destruction, followed by reconstruction in Europe and Japan.

Key Commodities: Steel, oil, cement, agricultural products.

Impact: The Marshall Plan, industrial rebuilding, and mass consumption pushed commodity demand sky-high. OPEC began forming as oil became the lifeblood of economies. The cycle peaked in the 1960s before slowing in the 1970s.

c) The Oil Shock and Emerging Markets Supercycle (1970s–1990s)

Drivers: Oil embargo (1973), Iran Revolution (1979), rapid urbanization in parts of Asia.

Key Commodities: Crude oil, gold, agricultural goods.

Impact: Oil prices quadrupled in the 1970s, fueling inflation and recessions. Gold became a safe haven. By the 1980s, new oil production in the North Sea and Alaska helped break the cycle.

d) The China-Driven Supercycle (2000s–2014)

Drivers: China’s rapid industrialization and urbanization, joining the WTO (2001).

Key Commodities: Iron ore, copper, coal, crude oil, soybeans.

Impact: China’s demand for steel, infrastructure, and energy triggered the largest commodity boom in modern history. Copper and iron ore prices quadrupled. Oil hit $147/barrel in 2008. The cycle began unwinding after 2014 as China shifted toward services and renewable energy, and global supply caught up.

3. The Anatomy of a Supercycle

Each supercycle follows a predictable pattern:

Stage 1: Triggering Event

A major economic or geopolitical transformation sparks sustained demand. Examples: Industrial revolution, post-war reconstruction, or China’s rise.

Stage 2: Demand Surge

Factories, cities, and infrastructure consume massive amounts of raw materials. Demand far outpaces supply.

Stage 3: Price Boom

Commodity prices skyrocket. Exporting nations enjoy “commodity windfalls.” Importers face inflation and trade deficits.

Stage 4: Supply Response

High prices incentivize new investments—new oil rigs, mines, farmland. But supply takes years to come online.

Stage 5: Oversupply & Demand Slowdown

Eventually, supply outpaces demand (especially if growth slows). Prices collapse, ushering in a prolonged downcycle.

4. Economic and Social Impacts of Supercycles

Supercycles are double-edged swords.

Positive Impacts:

Export Windfalls: Resource-rich countries (e.g., Brazil, Australia, Middle East) see growth, jobs, and government revenues.

Industrial Expansion: Importing nations can grow rapidly by using commodities for infrastructure.

Innovation Incentives: High prices drive efficiency, substitution, and technology (e.g., shale oil, renewable energy).

Negative Impacts:

Dutch Disease: Commodity booms can overvalue currencies, hurting manufacturing exports.

Volatility: Dependence on commodity cycles creates fiscal instability (e.g., Venezuela, Nigeria).

Inequality: Resource wealth often benefits elites, not the wider population.

Environmental Stress: Mining, drilling, and farming expansion often degrade ecosystems.

5. Current Debate: Are We Entering a New Supercycle?

Since 2020, analysts have speculated about a new global commodity supercycle.

Drivers Supporting a New Cycle:

Energy Transition: Shift to renewables and electric vehicles massively increases demand for copper, lithium, cobalt, and rare earths.

Infrastructure Spending: U.S., EU, and China launching trillions in green infrastructure projects.

Geopolitical Shocks: Russia-Ukraine war disrupted oil, gas, and wheat markets.

Supply Constraints: Years of underinvestment in mining and oil exploration after 2014 downturn.

Population Growth: Rising consumption in India, Africa, and Southeast Asia.

Drivers Against:

Technological Substitution: Recycling, efficiency, and alternatives (e.g., hydrogen, battery innovation) could cap demand.

Climate Policies: Push for decarbonization reduces long-term oil and coal demand.

Economic Uncertainty: Global recession risks, debt crises, and deglobalization trends.

Likely Scenario:

Instead of a broad-based boom like the 2000s, we may see a “green supercycle”—metals (copper, lithium, nickel) rising sharply while fossil fuels face structural decline.

6. The Role of Investors in Commodity Supercycles

Supercycles are not just macroeconomic phenomena—they also attract investors and speculators.

How Investors Play Them:

Futures Contracts: Traders bet on rising/falling commodity prices.

Equities: Buying mining, energy, and agriculture companies.

ETFs & Index Funds: Exposure to commodity baskets.

Hedging: Airlines hedge oil, food companies hedge wheat, etc.

Risks:

Mis-timing cycles leads to heavy losses.

High volatility compared to stocks and bonds.

Political risk in resource-rich countries.

Lessons from History

No Cycle Lasts Forever: Every boom is followed by a bust.

Supply Always Catches Up: High prices incentivize investment, eventually cooling prices.

Policy and Technology Matter: Wars, sanctions, renewables, and discoveries reshape cycles.

Diversification Is Key: Countries and investors relying only on commodities face huge risks.

Conclusion

Global commodity supercycles are among the most powerful forces shaping economies, markets, and geopolitics. From fueling industrial revolutions to triggering financial crises, commodities underpin human progress and conflict alike.

Today, the world may be on the cusp of a new, “green” commodity supercycle driven by decarbonization, electrification, and geopolitical rivalry. Metals like copper, lithium, and nickel may play the role that oil and steel did in past cycles. Yet, history teaches us caution—supercycles generate immense opportunities but also volatility, inequality, and environmental costs.

For policymakers, the challenge is to manage windfalls responsibly. For investors, it is to ride the wave without being crushed by it. And for societies, it is to ensure that the benefits of supercycles support long-term sustainable development rather than short-lived booms and painful busts.

SPX Elliott Count. (W3 of 3). S&P 500: Elliott Wave.

Targets:

8,293 then 7,204 finally 9,823.

SPX is currently in sub-wave 5 in W3 of W3. From this point we should see an aggressive push to 8,293 following a pullback then continuation.

SPX into the open / Tuesday 16th SeptemberTrend is up.Coming off the boil a tad.Lets see who has control.?

SPX & NDX : Stay heavy on positionsSPX & NDX : Stay heavy on positions (2x leverage)

- Market slowly shifting from sidelines to risk-on.

** This analysis is based solely on the quantification of crowd psychology.

It does not incorporate price action, trading volume, or macroeconomic indicators.

The Global Shadow Banking System1. Understanding Shadow Banking

1.1 Definition

Shadow banking refers to the system of credit intermediation that occurs outside the scope of traditional banking regulation. Coined by economist Paul McCulley in 2007, the term highlights how non-bank entities perform bank-like functions such as maturity transformation (borrowing short-term and lending long-term), liquidity transformation, and leverage creation—yet without the same safeguards, such as deposit insurance or central bank backstops.

1.2 Key Characteristics

Non-bank entities: Shadow banking is carried out by hedge funds, money market funds, private equity firms, securitization vehicles, and other institutions.

Credit intermediation: It channels savings into investments, much like traditional banks.

Regulatory arbitrage: It often arises where financial activity moves into less regulated areas to avoid capital and liquidity requirements.

Opacity: Complex instruments and off-balance sheet entities make it difficult to track risks.

1.3 Distinction from Traditional Banking

Unlike regulated banks:

Shadow banks cannot access central bank liquidity in times of crisis.

They lack deposit insurance, increasing systemic vulnerability.

They rely heavily on short-term wholesale funding such as repurchase agreements (repos).

2. Historical Evolution of Shadow Banking

2.1 Early Developments

Shadow banking’s roots can be traced to the 1970s and 1980s, when deregulation in advanced economies allowed financial innovation to flourish. Rising global capital flows created demand for new instruments outside traditional bank lending.

2.2 Rise of Securitization

The 1980s–2000s saw the explosion of securitization, where loans (e.g., mortgages) were bundled into securities and sold to investors. Special Purpose Vehicles (SPVs) and conduits became central actors in shadow banking, financing long-term assets with short-term borrowing.

2.3 Pre-Crisis Boom (2000–2007)

The shadow system expanded rapidly before the 2008 financial crisis. Investment banks, money market funds, and structured investment vehicles financed trillions in mortgage-backed securities (MBS) and collateralized debt obligations (CDOs). This system appeared efficient but was highly fragile.

2.4 The 2008 Financial Crisis

When U.S. subprime mortgage markets collapsed, shadow banks faced a sudden liquidity freeze. Lacking deposit insurance and central bank support, institutions like Lehman Brothers collapsed, triggering global contagion. The crisis revealed the systemic importance—and dangers—of shadow banking.

2.5 Post-Crisis Reconfiguration

After 2008, regulators tightened banking rules, pushing even more activities into the shadow system. Simultaneously, reforms such as tighter money market fund rules sought to contain systemic risks. Despite these efforts, shadow banking has continued to grow, especially in China and emerging markets.

3. Structure of the Shadow Banking System

The shadow banking universe is diverse, consisting of multiple actors and instruments.

3.1 Key Entities

Money Market Funds (MMFs) – Provide short-term financing by investing in highly liquid securities.

Hedge Funds & Private Equity – Use leverage to provide credit, often in riskier markets.

Structured Investment Vehicles (SIVs) – Finance long-term securities through short-term borrowing.

Finance Companies – Offer consumer and business loans without deposit funding.

Broker-Dealers – Rely on repo markets to fund securities inventories.

Securitization Conduits & SPVs – Issue asset-backed securities (ABS).

3.2 Instruments and Mechanisms

Repos (Repurchase Agreements) – Short-term loans secured by collateral.

Commercial Paper – Unsecured short-term debt issued by corporations or conduits.

Mortgage-Backed Securities (MBS) – Bundled mortgage loans sold to investors.

Collateralized Debt Obligations (CDOs) – Structured products pooling various debt instruments.

Derivatives – Instruments like credit default swaps (CDS) that transfer credit risk.

3.3 Interconnectedness

The system is deeply interconnected with traditional banks. Many shadow entities rely on bank credit lines, while banks invest in shadow assets. This interdependence amplifies systemic risk.

4. Global Dimensions of Shadow Banking

4.1 United States

The U.S. remains the epicenter, with trillions in assets managed by MMFs, hedge funds, and securitization vehicles. Its role in the 2008 crisis highlighted its global impact.

4.2 Europe

European banks historically relied on securitization and repo markets, making shadow banking integral to cross-border finance. Luxembourg and Ireland are major hubs due to favorable regulations.

4.3 China

China’s shadow banking system emerged in the 2000s as a response to tight bank lending quotas. Wealth management products (WMPs), trust companies, and informal lending channels fueled rapid credit growth. While supporting growth, they also raised concerns of hidden debt risks.

4.4 Emerging Markets

In Latin America, Africa, and Southeast Asia, shadow banking fills credit gaps left by underdeveloped banking sectors. However, limited oversight raises systemic vulnerabilities.

5. Benefits of Shadow Banking

Despite its risks, shadow banking provides several advantages:

Credit Diversification – Expands funding beyond banks.

Market Liquidity – Enhances efficiency in capital markets.

Financial Innovation – Encourages new instruments and risk-sharing mechanisms.

Access to Credit – Supports SMEs and consumers underserved by traditional banks.

Global Capital Mobility – Facilitates international investment flows.

6. Risks and Challenges

6.1 Systemic Risk

Shadow banking increases interconnectedness, making financial crises more contagious.

6.2 Maturity and Liquidity Mismatch

Borrowing short-term while investing in long-term assets creates vulnerability to runs.

6.3 Leverage

High leverage amplifies both profits and losses, making collapses more severe.

6.4 Opacity and Complexity

Structured products like CDOs obscure underlying risks.

6.5 Regulatory Arbitrage

Activities shift to less regulated domains, making oversight difficult.

6.6 Spillover to Traditional Banking

Banks are exposed through investments, credit lines, and funding dependencies.

Conclusion

The global shadow banking system is a double-edged sword. On one hand, it enhances financial diversity, supports credit creation, and fuels innovation. On the other, it introduces opacity, leverage, and systemic fragility that can destabilize economies. The 2008 crisis demonstrated how vulnerabilities in the shadow system can trigger global turmoil.

Going forward, regulators must adopt balanced approaches: tightening oversight without stifling beneficial innovation. International coordination is critical, given the cross-border nature of shadow banking. As financial technology evolves, the boundaries between traditional banks, shadow entities, and digital platforms will blur even further.

Ultimately, shadow banking is not merely a “shadow” but an integral part of modern finance—one that demands vigilance, transparency, and adaptive regulation to ensure it serves as a force for stability and growth rather than crisis and contagion.

A Tolled BellThe first bell has rung. A bridge is being paved across the $6000 range.

IF it blows up, it likely won't happen until the bridge is constructed and sentiment improves. Expect a few heartfelt endeavors to shoot above $6,660. Base case is long term crab market.

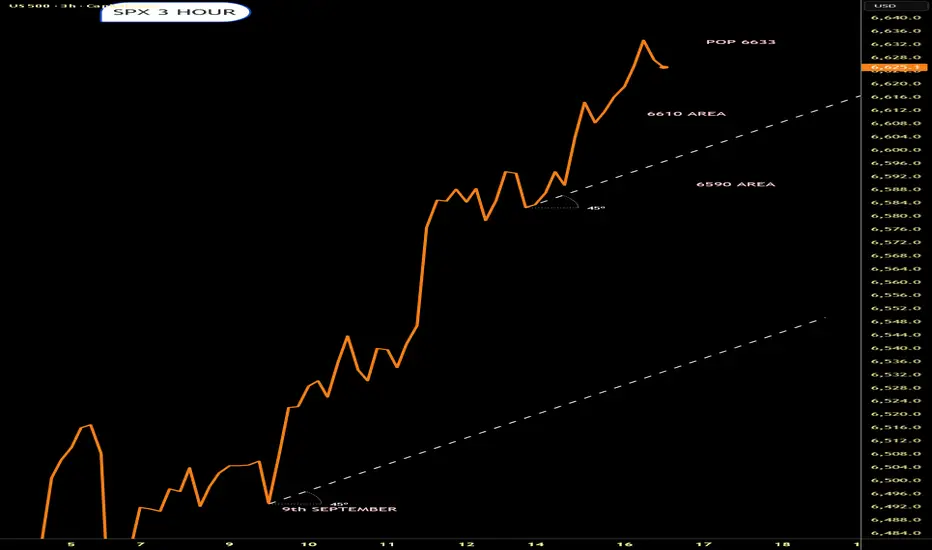

it's always the market of stockpickersS&P 500 (SPX): The uptrend continues, with the SPX reaching a new high and nearing a secondary target of 6,625. However, there are significant risks, including historically poor performance during the last ten trading days of September, which coincides with an expected Fed rate cut on September 17. Other risks include narrowing market breadth, NVIDIA's stock trading in a narrow range, and a "Dow Theory" divergence where the industrial average's breakout is unconfirmed by the transportation average.

S&P500 | H1 Head and shoulders | GTradingMethodHello Traders.

🧐 Market Overview:

I am still holding a short on the rising wedge visible on the 4-hour chart. While the S&P 500 has broken out to the upside of the wedge, there’s still a real chance this could be a fake out.

The RSI is showing overbought conditions across the 1H, 2H, and 4H timeframes, which makes it difficult for price to push higher without cooling off first. From a probability standpoint, I see the short as more favorable here than chasing longs.

With hindsight I should have waited for a reversal pattern to open shorts when trying to trade the risking wedge on the 4 hour chart.

If the head and shoulders pattern on the 1H chart fails, then a possible double top on the 2H chart may form. I’ll post an update if that scenario plays out and I have time.

NB! I do not have confirmation to enter the head and shoulders short yet. It is only on my radar for now.

📊 Trade Plan:

Risk/Reward: 3.8

Entry: 6 589.7

Stop Loss: 6 599

Take Profit 1 (50%): 6 560.2

Take Profit 2 (50%): 6 544.2

💡 GTradingMethod Tip:

A favorable setup doesn’t guarantee success, but managing risk and aligning with probability is how I stay consistent over the long term.

🙏 Thanks for checking out my post!

Make sure to follow me to catch the next idea and please share your thoughts — I’d like to hear them.

📌 Please note: This is not financial advice. This content is to track my trading journey and for educational purposes only.

US500 In strong bullish momentumFundamentals

The US500 remains supported by resilient earnings and the prospect of Federal Reserve easing, yet it faces notable vulnerabilities. While softer jobs growth and weakening leading indicators strengthen the case for upcoming rate cuts, a short term tailwind for equities, they also highlight the economy’s underlying fragility.

At the same time, elevated valuations and heavy market concentration in a handful of mega-cap leaders leave the index exposed to sharper corrections should sentiment shift.

For traders, monitoring sector rotation, earnings revisions, and macroeconomic signals will be critical to navigating opportunities while managing downside risks.

Technicals

US500 price action reveals a strong bullish trend, supported by momentum indicators and consistent uptrends, though signs of overbought conditions suggest a potential for short term pullbacks.

Key Support and Resistance Levels

Immediate Support: 6,545 is a key technical support zone; below this, 6,505 is a significant psychological and trend support zone.

Immediate Resistance: 6,630 is the nearest overhead ceiling, followed by 6,690.

Analysis by Terence Hove, Senior Financial Markets Strategist at Exness

SPX Supported by Trendline and Rate Cut ExpectationsThe S&P 500 has been climbing steadily, with the ascending trendline from April acting as a reliable backbone for the move. Despite short-term volatility, buyers continue to defend higher lows. Coupled with expectations of interest rate cuts, the trend structure remains intact unless key supports give way.

🔍 Technical Analysis

Current price: 6,584

The green trendline (since April) is guiding the advance.

Price is consolidating near highs, supported by demand zones underneath.

🛡️ Support Zones & Stop-Loss (White Lines):

🟢 6,537 – 1H Support (Medium Risk)

First line of defense for short-term traders.

Stop-loss: Below 6,513

🟡 6,018 – Daily Support (Swing Trade Setup)

Stronger base for medium-term positioning.

Stop-loss: Below 5,919

🧭 Outlook

Bullish Case: Hold above 6,537 + April trendline intact → continuation toward new highs above 6,600–6,700.

Bearish Case: Break below 6,537 could trigger a correction into 6,018. Losing that zone would weaken the April trendline structure.

Bias: Bullish while April trendline holds.

🌍 Fundamental Insight

Rate cut expectations continue to provide a macro tailwind for equities. With inflation moderating and yields easing, investors remain willing to support risk assets. A sudden shift in data or Fed tone, however, could test the resilience of the April trendline.

✅ Conclusion

The S&P 500 remains in a strong bullish structure, anchored by the April trendline. Unless supports at 6,537 or 6,018 are lost, the path of least resistance remains higher.

If you found this useful, please don’t forget to like and follow for more structure-based insights.

⚠️ Disclaimer

This analysis is for educational purposes only and does not constitute financial, investment, or trading advice.

Puts might work todayRising wedge broke bearish Timber below I would just watch and see if we roll over today and spy goes for 654-652 zone for a bounce or lower

S&P500 Historical Price Highs vs. Inflation-Adjusted Highs Nominal Price Definition (most used in history books & Wall Street research)

Inflation-Adjusted Definition (shown in your chart)

If you bought the 1929 top, you weren’t truly back to even (after inflation) until 1958.

Same with the 1968 top — real break-even wasn’t until the early ’90s.

Same with the 2000 top — real break-even was ~2016.

This method shows how devastating secular bears are if you happen to buy at the peak and hold. It makes the secular bears look even longer, because inflation erodes your gains even when the index regains its nominal high.