Short SPX-Short SPY with sideways movement into rates

-expect jump for rates conference

-post rates tapers down into end of Sept

SPCUSD trade ideas

SP500 4H🔹 Overall Outlook and Potential Price Movements

In the charts above, we have outlined the overall outlook and possible price movement paths.

As shown, each analysis highlights a key support or resistance zone near the current market price. The market’s reaction to these zones — whether a breakout or rejection — will likely determine the next direction of the price toward the specified levels.

⚠️ Important Note:

The purpose of these trading perspectives is to identify key upcoming price levels and assess potential market reactions. The provided analyses are not trading signals in any way.

✅ Recommendation for Use:

To make effective use of these analyses, it is advised to manually draw the marked zones on your chart. Then, on the 15-minute time frame, monitor the candlestick behavior and look for valid entry triggers before making any trading decisions.

Famous Forex Traders and Their Journeys1. George Soros: The Man Who Broke the Bank of England

George Soros, born in 1930 in Budapest, Hungary, is arguably the most famous forex trader of all time. His journey from a refugee escaping Nazi-occupied Hungary to a billionaire financier is a story of resilience, intelligence, and audacious trading. Soros studied at the London School of Economics under the tutelage of philosopher Karl Popper, whose concept of “reflexivity” would later underpin much of Soros’ trading strategy.

Soros’ approach to forex trading was revolutionary. He believed markets are not always rational, and that human behavior could create trends and anomalies that could be exploited. This philosophy reached its pinnacle on September 16, 1992, known as Black Wednesday, when Soros famously “broke the Bank of England.” Anticipating that the British pound was overvalued and that the UK government would not be able to maintain its currency within the European Exchange Rate Mechanism, Soros shorted $10 billion worth of pounds. When the pound crashed, he reportedly made over $1 billion in profit in a single day.

Soros’ journey teaches traders the power of conviction and risk management. His success was not a product of luck; it was the result of meticulous analysis, understanding macroeconomic fundamentals, and having the courage to act decisively against prevailing market sentiment.

2. Stanley Druckenmiller: The Strategist Behind Soros

Stanley Druckenmiller, often described as one of the greatest traders of the 20th century, was Soros’ right-hand man during the Black Wednesday trade. Born in Pittsburgh in 1953, Druckenmiller’ journey into finance began with studying English and economics before diving into the world of investments.

Druckenmiller’ trading style emphasizes trend-following combined with macroeconomic insights. He often stresses that understanding the “big picture” — interest rates, fiscal policies, and global economic cycles — is key to successful trading. During his tenure at Quantum Fund, he achieved phenomenal returns, often averaging 30% annual returns over decades, a feat almost unheard of in any financial market.

What distinguishes Druckenmiller is his disciplined risk management. He believed in cutting losses quickly and letting winners run — a principle that resonates deeply with forex traders. His journey demonstrates that even within the high-risk world of forex, strategic planning and emotional discipline are essential.

3. Bill Lipschutz: The Currency King

Bill Lipschutz, born in 1956 in New York, is a name synonymous with currency trading. Unlike Soros or Druckenmiller, Lipschutz’ entry into trading was accidental. While studying at Cornell University, he inherited a modest sum and began trading stocks. However, after a significant loss early in his career, he realized that understanding the market psychology was as important as understanding the numbers.

Lipschutz transitioned to forex trading in the 1980s at Salomon Brothers, where he earned the nickname “The Sultan of Currencies.” His approach revolved around market sentiment and positioning, rather than purely technical or fundamental analysis. He emphasized that traders must understand not just the currency, but the forces driving central banks, governments, and large institutional players.

One of his key insights was the importance of risk perception versus actual risk. By controlling his exposure and understanding when markets overreacted, Lipschutz was able to generate consistent profits, making him one of the most respected forex traders globally. His journey illustrates that resilience after setbacks and continuous learning are vital for long-term success.

4. Andrew Krieger: The Aggressive Risk Taker

Andrew Krieger, born in 1956 in New Zealand, gained fame in the late 1980s for his aggressive and highly leveraged forex trades. Krieger worked at Bankers Trust, where he became notorious for his bold positions, particularly his massive short on the New Zealand dollar, known as the “Kiwi.”

In 1987, Krieger identified that the New Zealand dollar was overvalued relative to the U.S. dollar. Exploiting leverage far beyond the bank’s capital, he took positions worth hundreds of millions of dollars, which led to enormous profits when the currency depreciated. His ability to analyze macro trends and exploit market inefficiencies allowed him to achieve results that many considered impossible.

Krieger’s story is both inspirational and cautionary. While it demonstrates the potential of forex trading to generate huge profits, it also underscores the immense risks of leverage. Modern traders can learn from his audacity but must balance it with strict risk controls.

5. Paul Tudor Jones: The Master of Macro

Paul Tudor Jones, born in 1954 in Memphis, Tennessee, is renowned for his macro trading expertise, including currency markets. His career began after graduating from the University of Virginia, when he launched his own trading firm, Tudor Investment Corporation, in 1980.

Jones’ fame skyrocketed when he correctly predicted and profited from the 1987 stock market crash. While primarily an equity trader, Jones’ strategies often involve currencies, particularly in the context of macroeconomic shifts. His trading philosophy blends technical analysis, historical patterns, and market psychology, emphasizing flexibility and adaptability.

He is a strong advocate of risk management, famously stating, “The most important rule of trading is to play great defense, not great offense.” This principle applies directly to forex, where volatility can be extreme, and losses can compound quickly. Jones’ journey highlights the need to combine strategy with discipline to thrive in global markets.

6. Richard Dennis and the Turtle Traders

Richard Dennis, born in 1949 in Chicago, was a commodities and forex trader famous for the “Turtle Traders” experiment. Dennis believed that trading could be taught systematically and sought to prove this by training novices in his rules-based approach.

The Turtle Traders, under Dennis’ guidance, followed strict mechanical systems to trade currencies and commodities. The results were extraordinary: many of his students went on to become successful traders, demonstrating that disciplined, rules-based trading could outperform intuition alone.

Dennis’ legacy emphasizes that forex success is not only about intelligence but about discipline, rules, and psychological resilience. His journey underscores the importance of methodology and consistency in trading.

7. Kathy Lien: The Modern Forex Strategist

Kathy Lien, born in 1978 in New York, represents a modern generation of forex traders. With a PhD in international economics, Lien has leveraged her academic background to become a leading currency strategist and author.

Lien’ career spans trading at major banks such as JP Morgan and FXCM, where she honed her skills in both fundamental and technical analysis. She is renowned for translating complex market data into actionable trading strategies, particularly for retail traders.

Her philosophy focuses on risk-adjusted trading, macroeconomic insights, and disciplined execution. Lien also emphasizes the importance of continual learning and adapting to market changes — crucial in today’s fast-evolving forex landscape. Her journey inspires traders, especially women, to pursue excellence in a male-dominated field.

8. Lessons from Famous Forex Traders

Examining the journeys of these iconic traders reveals common threads that aspiring forex traders can emulate:

Risk Management is Paramount: Every successful trader prioritizes controlling losses over chasing profits.

Market Psychology Matters: Understanding human behavior in markets is as critical as analyzing charts or economic indicators.

Adaptability and Flexibility: Markets change, and strategies must evolve.

Discipline Over Intuition: Mechanical systems, rules, and structured approaches often outperform gut feelings.

Continuous Learning: Even legendary traders constantly refine their methods and knowledge.

Boldness Balanced with Strategy: High conviction trades yield high rewards, but reckless risk-taking can be catastrophic.

9. Conclusion

The journeys of famous forex traders illustrate that success in the currency markets is a blend of intellect, discipline, risk management, and psychological resilience. From Soros’ historic pound short to Lien’s modern strategies, each trader exemplifies unique paths and philosophies. Their stories serve as both inspiration and practical guidance for anyone seeking to navigate the complexities of the forex market.

Forex trading is not merely a pursuit of wealth; it is a test of strategy, patience, and mental fortitude. By studying the journeys of these iconic figures, traders can learn that success is rarely accidental — it is crafted through rigorous analysis, unwavering discipline, and a willingness to learn from every win and loss.

Currency as a Tool of Power1. Historical Roots: Currency as Sovereignty

Currency has always carried political symbolism. Ancient kingdoms used coins not only as units of trade but also as markers of authority. The image of a ruler on a coin reinforced legitimacy and sovereignty. The Roman denarius, stamped with the Emperor’s profile, became a sign of imperial unity across vast territories.

The Chinese dynasties pioneered paper currency as early as the Tang and Song periods. This innovation extended state power by standardizing economic exchange across provinces. Similarly, medieval Europe saw kingdoms fight wars not just with armies but also by debasement of coinage—reducing precious metal content to finance conflicts while eroding rivals’ trust.

Thus, from the beginning, currency was about more than economics—it was about political stability and dominance. Control over minting and distribution meant control over trade routes, taxation, and governance.

2. Currency and Empire: Financial Foundations of Power

Empires rose and fell on their ability to control currency. During the Age of Exploration, Spain and Portugal amassed silver and gold from the New World, fueling European dominance. Yet, overreliance on bullion caused inflation (the so-called “Price Revolution”) and weakened Spanish hegemony.

By contrast, the British Empire leveraged financial sophistication. London’s banking system, supported by the pound sterling, became the backbone of international trade in the 19th century. The empire’s naval dominance was matched by financial dominance: colonies used sterling, and global contracts were denominated in British currency.

This marked the evolution of a reserve currency system, where the strength of a currency allowed an empire to project influence far beyond its borders.

3. The U.S. Dollar: Modern Currency Hegemony

After World War II, the Bretton Woods Agreement (1944) established the U.S. dollar as the anchor of the global financial system. Currencies were pegged to the dollar, which itself was backed by gold at $35/ounce. Even after the U.S. abandoned the gold standard in 1971, the dollar retained its dominance due to trust in American financial markets, political stability, and military power.

The dollar became not just a currency but a global standard:

Trade Dominance: Most international commodities—oil, gas, metals—are priced in dollars (“petrodollar” system).

Financial Institutions: IMF and World Bank largely operate on dollar reserves.

Investment Flows: Global investors see U.S. Treasury bonds as the safest assets.

This dominance gave the U.S. extraordinary power: it could print currency to fund deficits, influence global liquidity, and impose sanctions by restricting dollar-based transactions.

4. Currency as Economic Weapon: Sanctions and Restrictions

Currency can be directly weaponized. In modern geopolitics, restricting access to currency flows is as potent as military intervention.

SWIFT System Control: The U.S. and EU can cut off nations from the international payment network, crippling trade.

Iran Example: When sanctions limited Iran’s access to the dollar system, its economy shrank drastically despite having vast oil reserves.

Russia (2022): Western nations froze Russia’s foreign exchange reserves and limited its ability to transact in dollars/euros, undermining financial stability.

Currency control enables “bloodless warfare”—crippling economies without direct conflict. It demonstrates how financial architecture is as much a battlefield as physical territory.

5. Currency and Global Trade Imbalances

A strong or weak currency shapes trade flows, giving nations leverage:

China’s Strategy: By managing the yuan’s exchange rate, China boosts exports while building vast dollar reserves.

U.S. Deficit Power: The U.S. can sustain trade deficits because its currency is the world’s reserve, allowing it to pay for imports with paper rather than real goods.

Currency Wars: Countries engage in competitive devaluations to make exports cheaper, leading to tensions and instability.

Thus, exchange rates are not just technical matters but instruments of industrial strategy and geopolitical rivalry.

6. Reserve Currencies and Trust as Power

For a currency to wield global power, it must be trusted. Trust depends on:

Economic Stability: Strong GDP, low inflation, predictable policies.

Financial Markets: Deep, liquid markets that allow global investors to park capital.

Military Backing: The ability to enforce international order.

The euro, launched in 1999, was designed to rival the dollar, but its influence remains limited due to political fragmentation. The Japanese yen and British pound play regional roles but lack global dominance.

China’s yuan (renminbi) is increasingly used in trade, especially with developing nations, but strict capital controls limit its reach. Still, initiatives like the Belt and Road and the creation of the Asian Infrastructure Investment Bank (AIIB) suggest Beijing’s intent to expand yuan influence.

7. Currency as Cultural and Psychological Power

Currency also carries symbolic weight. People worldwide recognize the U.S. dollar as a store of value, often hoarding it in unstable economies (e.g., Argentina, Zimbabwe). In such cases, the dollar acts as an alternative government, providing psychological stability when local systems fail.

Tourists, businesses, and migrants all rely on dominant currencies, reinforcing their prestige and soft power. A strong, trusted currency enhances national identity and global appeal.

8. Digital Currencies: The New Frontier of Power

The 21st century has introduced a new battlefield: digital and decentralized currencies.

Cryptocurrencies like Bitcoin challenge state monopoly over money. They are borderless, resistant to censorship, and appealing in nations with weak currencies. However, volatility limits their mainstream role.

Central Bank Digital Currencies (CBDCs) represent the state’s countermeasure. China’s digital yuan is the most advanced, aiming to bypass the dollar system and enhance domestic surveillance.

U.S. and EU are exploring CBDCs cautiously, aware that digital currency could reshape financial flows, privacy, and power distribution.

If widely adopted, digital currencies could redefine currency as a tool of power, shifting influence from states to either tech platforms or transnational coalitions.

9. Currency and the Future Multipolar World

The 20th century was marked by unipolar dominance of the U.S. dollar. The 21st may become more multipolar, with multiple reserve currencies coexisting: dollar, euro, yuan, and possibly digital currencies.

Key trends shaping the future:

De-dollarization: Countries like Russia, China, and Middle Eastern powers are reducing reliance on the dollar.

Commodity-Backed Trade: Proposals for oil or gold-backed trade currencies.

Regional Blocs: African and Latin American nations considering shared currencies to reduce dependency.

Technological Shifts: Blockchain, digital wallets, and cross-border payment systems eroding U.S. control.

In this scenario, currency will continue to be a battlefield for influence, independence, and survival.

10. Ethical and Social Dimensions of Currency Power

Currency dominance is not neutral—it comes with consequences:

Dependency: Developing nations tied to foreign currencies lose policy autonomy.

Inequality: Global south often pays the price of financial crises originating in the global north.

Exploitation: Control over currency systems allows powerful nations to extract value from weaker economies.

Thus, the debate around currency power is also a debate about justice, sovereignty, and fairness in global finance.

Conclusion: The Eternal Struggle for Monetary Power

Currency is more than money—it is a weapon, a shield, and a stage for power struggles. From the Roman denarius to the British pound, from the U.S. dollar to the digital yuan, nations have used currency to expand influence, enforce dominance, and reshape the world order.

In the future, battles over currency will not only determine economic prosperity but also geopolitical survival. Whoever controls the dominant currency controls the rules of global trade, investment, and even war.

The story of currency as a tool of power is not over. It is evolving—toward a world where trust, technology, and multipolar rivalry will decide whose money rules the global stage.

Pullback long - H4Trend is bullish -> looking for long setup

We had a pullback to the EMA support

Trendline has been broken

Entry: breakout candle

Stop: low of the breakout candle

S&P 500 Wave Analysis – 26 September 2025

- &P 500 index reversed from support level 6600.00

- Likely to rise to resistance level 6700.00

S&P 500 index recently reversed up from the key support level 6600.00 (which also reversed the index in the middle of September) coinciding with the 20-day moving average and the 38.2% Fibonacci correction of the upward impulse from last month.

The upward reversal from the support level 6600.00 continues the active short-term impulse wave 3 of the intermediate impulse wave (5) from the start of August.

Given the strong daily uptrend, S&P 500 index can be expected to rise further to the next resistance level 6700.00 (which reversed the price earlier this month).

Post PCE thoughts.PCE data in line with expectations, personal income and spending slightly up, all in all, when I saw the data, I felt it would potentially be good for the S&P and also the USD. But both the S&P and the USD are nonplussed.

The GBP has positive momentum, but it's not something I can hang my hat on while the rest of the currencies are behaving incoherently. All in all, i'd like to place a risk on trade, but I don't have conviction in the direction of the currencies over the next few hours.

Which means I'll close the book on a week of only trade, which stopped out. Mildly disappointing but I look forward to the new week.

Weekly Review and currency overview to follow. Wishing you a lovely weekend.

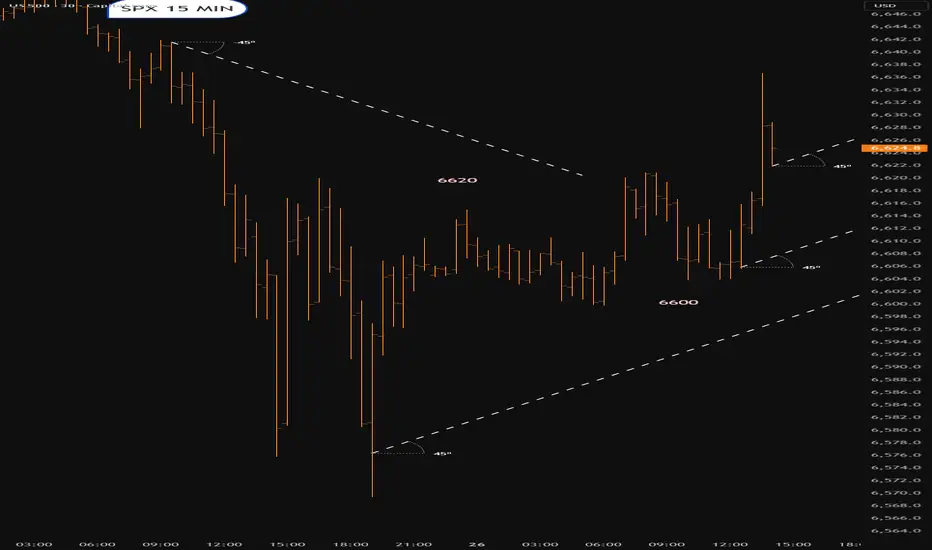

SPX .Bullish pattern/short termNeed to watch for failed signals/upside and maybe we even get a failed pattern and a dump.Lets see

SPX Supported by Trendline and Rate Cut ExpectationsThe S&P 500 has been climbing steadily, with the ascending trendline from April acting as a reliable backbone for the move. Despite short-term volatility, buyers continue to defend higher lows. Coupled with expectations of interest rate cuts, the trend structure remains intact unless key supports give way.

🔍 Technical Analysis

Current price: 6,584

The green trendline (since April) is guiding the advance.

Price is consolidating near highs, supported by demand zones underneath.

🛡️ Support Zones & Stop-Loss (White Lines):

🟢 6,537 – 1H Support (Medium Risk)

First line of defense for short-term traders.

Stop-loss: Below 6,513

🟡 6,018 – Daily Support (Swing Trade Setup)

Stronger base for medium-term positioning.

Stop-loss: Below 5,919

🧭 Outlook

Bullish Case: Hold above 6,537 + April trendline intact → continuation toward new highs above 6,600–6,700.

Bearish Case: Break below 6,537 could trigger a correction into 6,018. Losing that zone would weaken the April trendline structure.

Bias: Bullish while April trendline holds.

🌍 Fundamental Insight

Rate cut expectations continue to provide a macro tailwind for equities. With inflation moderating and yields easing, investors remain willing to support risk assets. A sudden shift in data or Fed tone, however, could test the resilience of the April trendline.

✅ Conclusion

The S&P 500 remains in a strong bullish structure, anchored by the April trendline. Unless supports at 6,537 or 6,018 are lost, the path of least resistance remains higher.

If you found this useful, please don’t forget to like and follow for more structure-based insights.

⚠️ Disclaimer

This analysis is for educational purposes only and does not constitute financial, investment, or trading advice.

SPX into the open.Friday 26th SeptemberRecoiling after an oversold sell off.Looks like it might test that downtrend.lets see what happens

SPX frothy watersWe are currently operating firmly within the 4–5 range of several market cycles — a pattern that appears to be repeating consistently. Under such conditions, a prudent strategy is to remain mostly inactive, engaging only in limited, low-risk trades. Favor small positions, selling into strength and buying into weakness — in essence, "sell high, buy low."

Attempting to chase uptrends or buy into rallies while selling during minor corrections is likely to result in premature stop-outs, effectively eroding the gains accumulated thus far. The risk of giving back profits is elevated in this phase of the cycle.

A more significant pullback or structural correction is not expected until sometime after the first quarter of next year. Until then, restraint and precision are paramount.

Gold’s Decade Shines Less Brightly for Stocks: The New Rational

Gold’s Decade Shines Less Brightly for Stocks: The New Rationale for the King Metal

For over a decade, the narrative surrounding gold was one of stark contrast to the equity markets. As stock indices, powered by tech innovation and ultra-low interest rates, embarked on a historic bull run, gold was often relegated to the sidelines—a relic for the fearful, an underperforming asset in a world chasing yield. The 2010s were, without question, the decade of the stock market. Gold’s shine, by comparison, seemed dull.

But a perceptible shift is underway. The latest rally in gold, which has seen it scale unprecedented nominal heights, is not the frantic, fear-driven surge of past crises. Instead, it appears to be driven by a more sober, strategic, and perhaps more durable force: the rational calculations of central banks and a fundamental rewiring of the global financial architecture. This new rationale suggests that gold’s resurgence may not spell immediate doom for stocks, as traditional wisdom would hold, but rather reflects a new, more complex macroeconomic reality where the two can coexist, albeit with gold casting a long, less brilliant shadow over the equity landscape.

The Ghost of Gold Rallies Past: A Tale of Fear and Froth

To understand the significance of the current rally, one must first revisit the drivers of previous gold booms. Historically, gold’s major upward moves were tightly correlated with periods of acute stress and negative real interest rates.

The post-2008 financial crisis surge, which took gold from around $800 an ounce in 2008 to over $1,900 in 2011, was a classic "fear trade." The world was confronting a systemic banking collapse, unprecedented monetary experimentation in the form of Quantitative Easing (QE), and rampant fears of runaway inflation and currency debasement. Gold was the safe haven, the hedge against a collapsing system. Similarly, the spike in mid-2020, at the onset of the COVID-19 pandemic, was a panic-driven flight to safety as global economies screeched to a halt.

These rallies shared common characteristics: they were often sharp, volatile, and ultimately prone to significant retracements. When the immediate crisis abated—when inflation failed to materialize post-2008, or when fiscal and monetary stimulus ignited a V-shaped stock market recovery in 2020—the rationale for holding a non-yielding asset weakened. Money flowed back into risk assets like stocks. Gold’s role was binary: it was the asset for when things were falling apart. In a functioning, risk-on market, it had little place.

This created the perception of an inverse relationship. A strong gold price was a signal of market distress, and thus, bad for stocks. But this decade is different.

The New Architects: Central Banks and Strategic Repatriation

The most profound change in the gold market has been the transformation of its largest and most influential buyers: central banks. For years, the narrative was that developed Western central banks, holders of the world’s primary reserve currencies, were gradually diversifying away from gold. The modern financial system, built on the U.S. dollar, Treasury bonds, and other interest-bearing instruments, was deemed superior.

That assumption has been decisively overturned. Since around 2010, but accelerating dramatically in recent years, central banks—particularly those in emerging economies—have become net purchasers of gold on a massive and sustained scale. The World Gold Council reports that central banks have been adding to their reserves for over a decade, with annual purchases hitting multi-decade records.

This buying is not driven by panic. It is a calculated, long-term strategic move rooted in three key rationales:

1. De-dollarization and Geopolitical Hedging: The weaponization of the U.S. dollar through sanctions, particularly against Russia following its invasion of Ukraine, served as a wake-up call for nations not squarely in the U.S. geopolitical orbit. Holding vast reserves in U.S. Treasury bonds suddenly carried a new risk: they could be frozen or seized. Gold, by contrast, is a sovereign asset. It can be held within a nation’s own vaults, is nobody’s liability, and is beyond the reach of any other country’s financial system. For China, Russia, India, Turkey, and many nations in the Global South, accumulating gold is a strategic imperative to reduce dependency on the dollar and insulate their economies from geopolitical friction.

2. Diversification Against Fiscal Profligacy: Even for allies of the U.S., the sheer scale of U.S. government debt is a growing concern. With debt-to-GDP ratios at record levels in many developed nations and little political will to address them, the long-term value of fiat currencies is being questioned. Central banks are increasingly viewing gold as a perennial hedge against the fiscal and monetary policies of their allies—a form of insurance against the potential devaluation of the very government bonds that form the backbone of their reserves.

3. A Return to a Multi-Polar Financial World: The post-Bretton Woods era has been dominated by the U.S. dollar. There are increasing signs that the world is shifting towards a multi-polar system, with the euro, Chinese yuan, and possibly other currencies playing larger roles. In such a transitional period, gold’s historical role as a neutral, trusted store of value becomes immensely attractive. It is the one asset that is not tied to the economic fortunes or policies of a single nation.

This central bank demand provides a powerful, structural floor under the gold price. It is consistent, price-insensitive buying (they are not chasing momentum but executing a strategy) that is largely divorced from the short-term sentiment swings of the stock market. This is the "more rational calculation" that makes the current rally fundamentally different and potentially longer-lasting.

The Interest Rate Conundrum: Gold’s Old Nemesis Loses Its Bite

For years, the primary argument against gold was simple: it offers no yield. In a world of rising interest rates, where investors can earn a attractive, risk-free return on cash or government bonds, the opportunity cost of holding gold becomes prohibitive. The theory held that the Federal Reserve’s aggressive hiking cycle from 2022 onward would crush the gold price.

It didn’t. Gold not only weathered the storm but continued its ascent. This paradox reveals another layer of the new rationale.

While nominal rates rose, real interest rates (nominal rates minus inflation) have been more ambiguous. Periods of high inflation meant that even with higher rates, the real return on cash and bonds was often negative or minimal. In such an environment, gold, as a traditional inflation hedge, retains its appeal.

More importantly, the market’s focus has shifted from the level of rates to their trajectory. There is a growing belief that the era of structurally higher interest rates is unsustainable, given the colossal levels of global debt. Servicing this debt becomes exponentially more difficult as rates rise. Therefore, many market participants are betting that the current rate cycle represents a peak, and that central banks will be forced to cut rates sooner rather than later, regardless of the inflation fight. Gold performs well in a environment of falling rates, and this anticipation is being priced in now.

Furthermore, high rates have begun to expose fragilities in the system, from regional banking crises in the U.S. to debt distress in emerging markets. In this sense, high rates haven't killed gold’s appeal; they have reinforced its role as a hedge against the consequences of high rates—namely, financial instability.

A Less Bright Shine for Stocks: Coexistence in a New Reality

So, what does this new, rationally-driven gold bull market mean for stocks? The relationship is no longer a simple inverse correlation. It is more nuanced, suggesting a future of coexistence rather than direct competition, but one where gold’s strength signals underlying headwinds that will dim the stellar returns equities enjoyed in the previous decade.

1. The End of the "Free Money" Era: The 2010s were built on a foundation of zero interest rates and quantitative easing. This environment was nirvana for growth stocks, particularly in the tech sector, as future earnings were discounted at very low rates, justifying sky-high valuations. The new macroeconomic order—one of higher structural inflation, larger government debt, and geopolitical fragmentation—is inherently less favorable to such valuation models. Gold’s strength is a symptom of this new order. It doesn’t mean stocks will collapse, but it does suggest that the era of effortless, broad-based double-digit annual returns is likely over. Returns will be harder won, more selective, and more volatile.

2. A Hedge Within a Portfolio, Not a Replacement: Investors are now likely to view gold not as a binary alternative to stocks, but as a critical component of a diversified portfolio. In a world of heightened geopolitical risk and uncertain monetary policy, holding a portion in gold provides stability. This means fund flows are not a simple zero-sum game between the SPDR Gold Trust (GLD) and the SPDR S&P 500 ETF (SPY). Institutions and individuals may increase allocations to both, using gold to mitigate the specific risks that now loom over the equity landscape.

3. Sectoral Winners and Losers: A strong gold price is a direct positive for gold mining stocks, a sector that has been largely neglected for years. This could lead to a resurgence in this niche part of the market. Conversely, the factors driving gold—higher inflation and rates—are headwinds for long-duration assets like high-flying tech stocks. The outperformance may shift towards value-oriented sectors, commodities, and industries with strong pricing power and tangible assets. The stock market’s shine may dim overall, but it will create bright spots in new areas.

4. The Signal of Sustained Uncertainty: Ultimately, a gold market driven by central bank de-dollarization and fiscal concerns is a barometer of persistent, low-grade global uncertainty. This is not the acute panic of 2008, but a chronic condition of fragmentation and distrust. Such an environment is not conducive to the explosive, confidence-driven growth that stock markets thrive on. It favors caution, resilience, and tangible value over speculative growth. Gold’s steady ascent is the clearest signal of this psychological shift.

Conclusion: A Duller but More Enduring Glow

The gold rally of the 2020s is not a siren call of an imminent market crash. It is the quiet, determined accumulation of a strategic asset by the world’s most powerful financial institutions. It is a vote of no confidence in the unfettered dominance of the current financial order and a bet on a more fragmented, uncertain future.

For stock market investors, this does not necessarily portend a bear market. Instead, it heralds a more challenging environment where the tailwinds of globalization and cheap money have reversed. The dazzling shine of the stock market’s previous decade is likely to be replaced by a duller, more realistic glow. Returns will be more modest, risks more pronounced, and the need for prudent diversification more critical than ever.

In this new era, gold and stocks will learn to coexist. The king of metals is no longer just a refuge for the fearful; it has become a strategic holding for the rational. Its decade may not shine with the same speculative brilliance as the stock market’s last bull run, but its light may well prove to be more enduring, illuminating a path through a landscape of greater complexity and risk. The lesson for investors is clear: the old rules are changing, and in this new game, gold holds a very strong hand.

SPX .A fake above 6660A fake nove above 6660.Now back in support for a rethink.Lets see if suppport holds.?

Major Global Soft Commodity Markets1. Understanding Soft Commodities

1.1 Definition and Classification

Soft commodities are raw materials that are cultivated, harvested, and traded for various purposes, including food, feed, fuel, and fiber. Unlike hard commodities such as metals and energy resources, softs are perishable and subject to seasonal cycles. They are typically traded on futures markets, allowing producers to hedge against price fluctuations and investors to speculate on price movements.

1.2 Key Characteristics

Perishability: Most soft commodities have a limited shelf life, requiring efficient storage and transportation systems.

Seasonality: Production cycles are influenced by planting and harvesting seasons, affecting supply and prices.

Geographic Concentration: Certain regions dominate the production of specific soft commodities, making them vulnerable to local disruptions.

Price Volatility: Prices can be highly volatile due to factors like weather events, pests, and geopolitical tensions.

2. Major Soft Commodities and Their Markets

2.1 Coffee

Coffee is one of the world's most traded commodities, with Brazil, Vietnam, and Colombia being the top producers. The market is influenced by factors such as climate conditions, currency fluctuations, and global demand trends. Futures contracts for coffee are traded on exchanges like ICE Futures U.S., providing a benchmark for global prices.

2.2 Cocoa

Cocoa is primarily produced in West Africa, with Ivory Coast and Ghana leading global production. The market has experienced significant price fluctuations due to supply deficits, often caused by adverse weather conditions and political instability in producing countries. The New York Cocoa Exchange, now part of ICE Futures U.S., plays a crucial role in setting global cocoa prices.

2.3 Sugar

Sugar is a staple in the global food industry, with Brazil, India, and China being major producers. The market is influenced by factors such as government policies, biofuel mandates, and global consumption patterns. Futures contracts for sugar are traded on exchanges like ICE Futures U.S., providing transparency and liquidity to the market.

2.4 Cotton

Cotton is essential for the textile industry, with China, India, and the United States being the largest producers. The market is affected by factors like weather conditions, labor costs, and global demand for textiles. Futures contracts for cotton are traded on exchanges such as ICE Futures U.S., offering a platform for price discovery and risk management.

2.5 Corn and Soybeans

Corn and soybeans are vital for food, feed, and biofuel industries. The United States is a leading producer of both crops, with significant exports to countries like China and Mexico. Futures contracts for these commodities are traded on exchanges like the CME Group, providing mechanisms for hedging and speculation.

2.6 Wheat

Wheat is a staple food for billions worldwide, with major producers including Russia, the United States, and China. The market is influenced by factors such as weather conditions, global demand, and trade policies. Futures contracts for wheat are traded on exchanges like the CME Group, offering a platform for price discovery and risk management.

3. Trading and Investment in Soft Commodities

3.1 Futures Markets

Futures markets are central to the trading of soft commodities, allowing producers to hedge against price fluctuations and investors to speculate on price movements. Exchanges like ICE Futures U.S. and the CME Group provide platforms for trading futures contracts, offering transparency and liquidity to the market.

3.2 Exchange-Traded Funds (ETFs)

ETFs provide investors with exposure to soft commodities without the need to directly trade futures contracts. For example, the Teucrium Corn Fund (CORN) and the Teucrium Soybean Fund (SOYB) offer investors a way to invest in these commodities through the stock market.

3.3 Physical Trading

Physical trading involves the buying and selling of actual commodities, often through long-term contracts between producers and consumers. Companies like ECOM Agroindustrial play a significant role in the physical trading of commodities such as coffee, cocoa, and cotton.

4. Factors Influencing Soft Commodity Markets

4.1 Weather and Climate Conditions

Adverse weather events like droughts, floods, and hurricanes can significantly impact the production of soft commodities, leading to supply shortages and price volatility.

4.2 Geopolitical Events

Political instability, trade disputes, and sanctions can disrupt supply chains and affect the prices of soft commodities.

4.3 Economic Policies

Government policies, such as subsidies, tariffs, and biofuel mandates, can influence the production and consumption of soft commodities, impacting their market dynamics.

4.4 Global Demand Trends

Changes in consumer preferences, population growth, and dietary habits can affect the demand for soft commodities, influencing their prices.

5. Challenges and Risks in Soft Commodity Markets

5.1 Price Volatility

Soft commodity markets are characterized by high price volatility due to factors like weather conditions, geopolitical events, and market speculation.

5.2 Supply Chain Disruptions

Natural disasters, transportation issues, and political instability can disrupt supply chains, leading to shortages and price increases.

5.3 Regulatory Uncertainty

Changes in government policies, such as trade restrictions and environmental regulations, can create uncertainty in the market.

6. Outlook for Soft Commodity Markets

6.1 Emerging Markets

Countries in Asia and Africa are becoming increasingly important players in the production and consumption of soft commodities, influencing global market trends.

6.2 Technological Advancements

Innovations in agricultural technology, such as precision farming and biotechnology, have the potential to improve yields and reduce the environmental impact of soft commodity production.

6.3 Sustainability Initiatives

There is a growing emphasis on sustainable practices in the production and trade of soft commodities, driven by consumer demand and regulatory pressures.

7. Conclusion

Soft commodities are integral to the global economy, influencing food security, industrial production, and trade dynamics. Their markets are complex and influenced by a myriad of factors, including weather conditions, geopolitical events, and economic policies. Understanding these markets is crucial for producers, traders, and investors alike to navigate the challenges and opportunities they present.

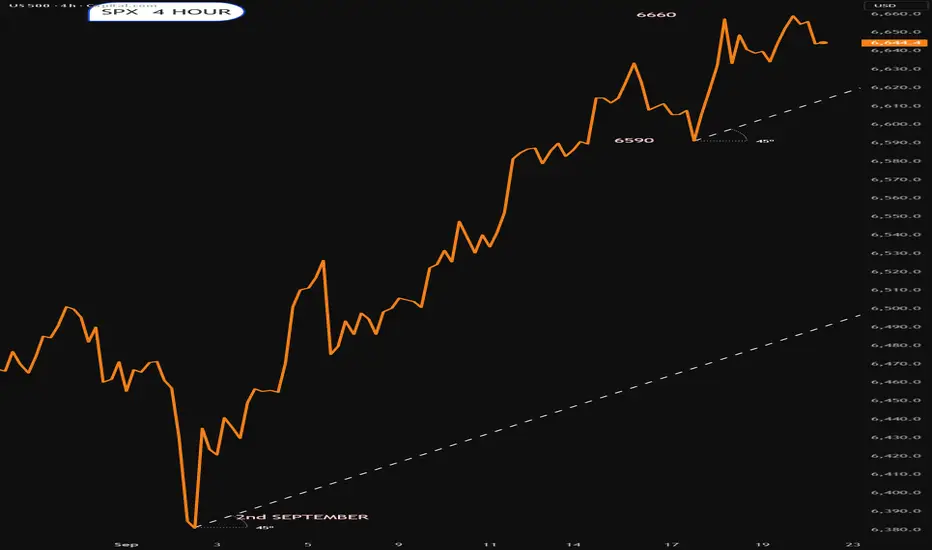

SPX Wave 4 nearZooming out to the longer-term view, it appears we are approaching a Wave 4 of a higher degree. After the completion of this corrective phase, I expect a final Wave 5 of the primary degree to unfold, likely carrying into the first quarter of next year, ( next year 1st 1/4 SPX 7,200-ish)

The next bubble? It is amazing to see the power of the U.S market.

The Economy and Wall Streets splitted paths a long time ago...

Inflation?

Wars?

Euro Zone Crisis?

Call it market manipulation or a rigid game... betting against the market should be only a short term strategy.

Close in on last segmentWell 6666 is the sign of the devil..Can it take that out .?

lets see what happens

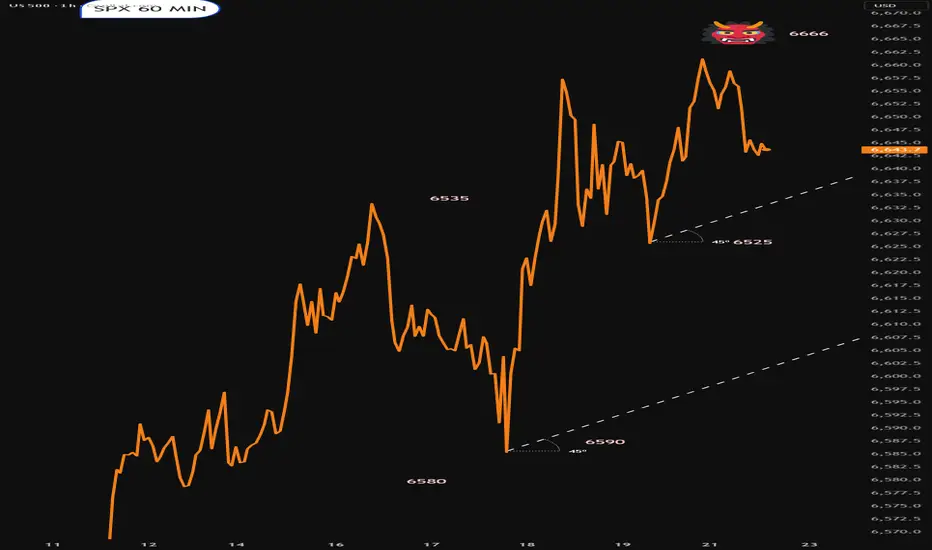

SPX despikedGot rid of some of the spikes to expose the trend.The range now seems to be 6590-6660 areas

SPX into the open/Monday 22nd SeptemberTrend markedDare ya sell it.? Really needs to pull back.that might not happen