NVDA Cooked!?If you find this information inspiring/helpful, please consider a boost and follow! Any questions or comments, please leave a comment!

NVDA Price Action Update: Key Levels To Watch

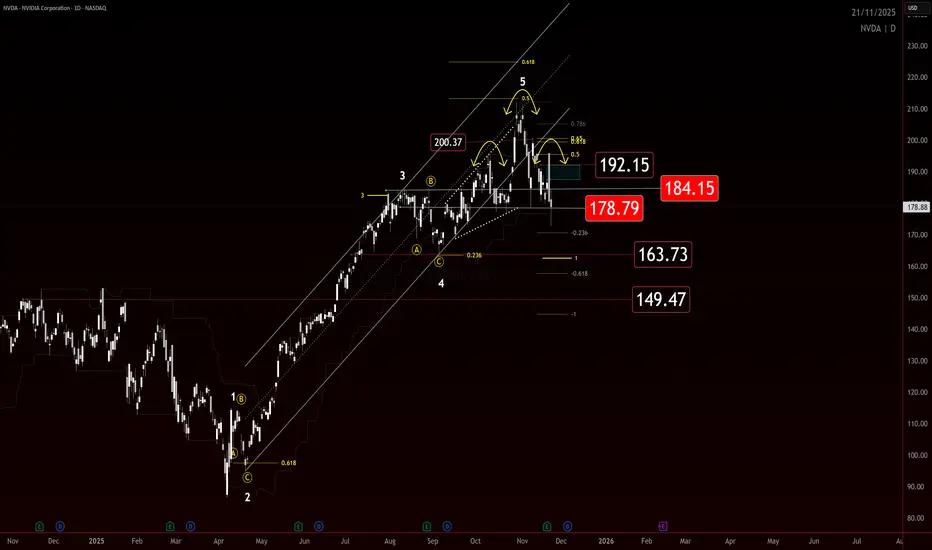

NVDA is cooked if it cannot reclaim the key levels overhead. Price is currently testing 178 and this area is critical for determining whether buyers still have any momentum left.

To flip this structure back upward, NVDA needs an impulse through 178 and then 184. Anything that retraces in a choppy or corrective manner within the impulsive range from 195 is suspect and suggests continuation lower.

If buyers fail to generate an impulsive move from here, the downside levels below come back into play. Seller control increases with every failed retest and every weak bounce.

This is a simple structure play. Impulsive strength is required to shift control. Corrective behavior keeps the door open for further decline.

Trade safe and trade clarity.

Trade ideas

Stocks Worth Your AttentionI wanted to share a list of high growth, high margin stocks that are worth looking into. This is where I pull a lot of my core positions from.

HIMS is noteworthy as it's also one of the most heavily shorted stocks at the moment and THE best performer on my ranking.

These stocks are essentially cash cows dominating their space. Please do look into each one carefully. This list is algo generated and not combed through by me yet. So make sure the stock's earnings and trend are to your liking.

Enjoy and good luck!

NVDA CORRECTION - MONTHLYThe last 2 corrections based on Monthly chart were roughly 55% and 65%.

Weekly and Monthly charts on indices look like they are trending down. Weekly VIX is in an uptrend. Weekly DXY is in an uptrend.

Overall, it feels like the safest bet is cash or maybe bonds. I don’t love the bond charts, so cash?? Even Buffet has a big cash position…

** This post is my opinion on investment positions, not trading. I use daily or intraday for trading TA.

NVIDIA (NVDA): Where Are We in the Cycle?Ticker: NVDA

Category: Market Structure / Elliott Wave Analysis

Author’s note: Educational analysis — not financial advice.

🧠 Market Context

NVIDIA has been one of the strongest growth stories in the last market cycle. However, after such a powerful move, many traders are now asking: Where are we in the broader structure — and what could come next?

From a structural perspective, NVDA appears to have completed its third Elliott Wave, with the fourth wave currently in progress. This phase often reflects a period of consolidation, where the market digests previous gains before potentially starting the fifth wave.

📊 Elliott Wave Structure

Through the lens of Elliott Wave theory:

Wave 3 — likely completed after the parabolic advance that marked NVIDIA’s latest all-time highs.

Wave 4 — a corrective phase, potentially forming a sideways or slightly downward structure.

Wave 5 (ahead?) — may still occur, possibly extending above the upper boundary of the current price channel.

However, once the fifth wave completes, markets typically enter a longer consolidation or corrective phase — often retracing 50–60% of the total move from the highs.

⚙️ Volatility and Price Range

Currently, NVDA is trading within a broad channel, roughly between $100 and $400+.

Volatility remains elevated — which suggests that the sideways phase could persist for several months, or even longer.

Such behavior is common in late-cycle stages when large market participants distribute part of their holdings while retail interest remains high.

📈 Key Takeaways

The main impulsive move seems to have already played out.

The market may enter a range-bound or sideways phase, with local rallies still possible.

Correction risks are gradually increasing, especially if the fifth wave develops and fails to sustain new highs.

In short, this might not be the best time to chase — but rather to observe how price behaves within the current channel.

💬 Final Thoughts

This analysis is purely educational and reflects one possible scenario based on market structure.

No one can predict the exact timing or depth of the next move — the market always decides.

👉 What do you think?

Are we already in the correction phase, or is there still one more leg up left for NVDA?

Share your view in the comments below 👇

NVDA ALERT: Critical Drop AheadNvidia remains in a broader uptrend, but the chart shows a clear trendline breakout followed by the beginning of a pullback.

Using Fibonacci, a correction typically starts after a red candle forms following a sequence of green candles. In most cases, the pullback continues toward the 0.5 retracement level. In this setup, the 0.5 level aligns with a major key support, increasing its importance.

On the weekly timeframe, the 50 EMA is also converging at the same zone, which often acts like a magnet for price. This creates multiple confirmations pointing toward a potential move downward.

The weekly chart has printed a bearish engulfing , followed by three consecutive red candles, adding another strong confirmation for a continued correction.

Both MACD and RSI are sloping downward, supporting the bearish momentum.

If price reaches the expected zone, monitoring the reaction will be critical. A deeper decline into the global trendline is possible only if the key level is broken, though this scenario appears less likely.

Overall, NVDA shows several aligned signals indicating a move toward the correction zone before any potential recovery.

NVDA TARGETSupport and 200 ma down at 155. Where it goes from there is a ?? — that 😈 top seems hard to get above.

Hi, i'm trying to revisit the Nvidia Journey here i'm trying to do some historical analysis , trying to find some important historical patterns which impacted the Nvidia price movement then and still valid or might impact the future price movement

I' hv a strong believe that price move within the constraint of the historical patterns and form new one for the future

full analysis will take few days, today , i'm starting with simple tl/angles formed by the first 2 monthly candles , in next 3 graphics u will find the impact of these 2 angles

Global Economy Shifts1. Multipolarity and the Rebalancing of Global Power

For decades, the global economy operated under a largely unipolar structure led by the United States and its Western allies. Today, this dominance is fading as new economic blocs rise. Emerging markets—most notably China, India, Southeast Asia, the Middle East, and Africa—are becoming engines of global growth.

Rise of Asia

Asia now contributes more than half of global economic growth. China remains the world’s second-largest economy despite slowing growth, while India is emerging as the fastest-growing major economy, driven by demographics, domestic consumption, and digital infrastructure.

Shift Toward Regional Blocs

Increasing geopolitical tensions between the U.S. and China have accelerated the formation of economic blocs:

BRICS+ expansion has brought new resource-rich members.

Regional trade agreements such as RCEP and CPTPP are reshaping Asia-Pacific integration.

The European Union, despite internal challenges, is investing in strategic autonomy, green energy, and advanced manufacturing.

This move toward multipolarity is redefining investment flows, supply chains, and diplomatic alignments.

2. Technological Transformation and the Digital Economy

Technology is the most powerful force reshaping global economic structures. The accelerating adoption of AI, automation, robotics, and digital platforms is altering productivity, labor markets, and competitive advantages.

Artificial Intelligence as a Growth Catalyst

AI is transforming sectors such as finance, healthcare, logistics, and manufacturing. Countries that invest heavily in AI—like the U.S., China, and South Korea—are gaining competitive edges.

Digital Infrastructure Expansion

Digital connectivity has become the backbone of national competitiveness. Innovations such as:

5G and upcoming 6G networks

Cloud computing

Quantum technologies

Blockchain and digital payments

are enabling new business models. Digital public infrastructure (DPI), led by India’s UPI, Aadhaar, and ONDC, is becoming a blueprint for emerging markets.

Techno-Economic Fragmentation

However, technology is also driving global fragmentation:

Competing semiconductor supply chains

Restrictions on data flows

Tech-related sanctions

Global technology standards may split into competing spheres, creating challenges for multinational corporations.

3. Geopolitical Conflicts and De-Risking of Supply Chains

Conflicts such as the Russia–Ukraine war, Middle East instability, and U.S.–China tensions have triggered a significant rethinking of global supply chains.

From Globalization to “De-Risking”

Countries are not fully de-globalizing, but they are diversifying away from single-source dependencies. This has led to:

Nearshoring (e.g., U.S. companies shifting production to Mexico)

Friendshoring (production moving among geopolitical allies)

China+1 strategy (India, Vietnam, Indonesia as beneficiaries)

Resilience Over Efficiency

Companies are prioritizing:

Multi-location manufacturing

Strategic stockpiling

Strengthening logistics networks

Supply chains are becoming more regional and networked, reducing vulnerability to shocks.

4. Green Transition and the Economics of Climate Change

Climate change is reshaping policymaking and investment decisions. Governments and corporations are transitioning toward low-carbon economies, driving structural changes across energy, transportation, manufacturing, and agriculture.

Shift Toward Clean Energy

Renewables—solar, wind, hydro, hydrogen—are experiencing massive investment. Nations like China lead in solar manufacturing, Europe in wind technology, and the Middle East in green hydrogen.

Electric Vehicle (EV) Transformation

EV adoption is accelerating globally, forcing:

Auto companies to redesign supply chains

Battery manufacturers to secure critical mineral sources

Governments to provide subsidies and carbon regulations

Climate-Resilient Infrastructure

Rising temperatures and extreme weather events require substantial investment in resilient infrastructure, influencing fiscal priorities worldwide.

5. Demographic Changes and Labor Market Evolution

Demographics play a critical role in shaping economic potential.

Aging Economies

Developed nations—Japan, South Korea, much of Europe, and even China—face aging populations, shrinking workforces, and rising healthcare burdens. This leads to:

Lower long-term growth

Higher fiscal pressure

Increased need for automation and immigration

Youthful Economies

In contrast, India, Africa, and parts of Southeast Asia have young populations and rapidly urbanizing societies. These countries will be key drivers of global labor supply and consumer demand in coming decades.

Future of Work

Automation and AI will redefine jobs across sectors. While high-skilled workers benefit from rising productivity, low-skilled jobs face displacement. Upskilling, remote work, and gig economy platforms are altering labor structures.

6. Shifts in Global Trade, Currency, and Finance

Global trade patterns are being reshaped by:

Tariffs and trade barriers

Sanctions

New trade agreements

Carbon border taxes

Changing Currency Dynamics

While the U.S. dollar remains dominant, alternative currency arrangements are gaining traction:

BRICS countries exploring settlement in local currencies

Digital currencies and central bank digital currencies (CBDCs)

Bilateral trade agreements bypassing the dollar

Although the dollar’s dominance will not end soon, its relative share is gradually declining.

Capital Flow Reconfiguration

Investments are moving into:

Resilient supply chains

Green energy

Technology hubs

Emerging markets

Sovereign wealth funds, especially from the Middle East, are playing a major role in global capital allocation.

7. Consumer Behavior and Market Transformations

Consumers are shifting their preferences due to technological access, environmental awareness, and rising incomes.

Key trends include:

Increased digital consumption

Demand for sustainable products

Rapid growth of e-commerce and online services

Preference for personalized and subscription-based models

Emerging market middle classes—especially in India, Indonesia, and Africa—are becoming major contributors to global consumption growth.

Conclusion: A Transformative Decade Ahead

The global economy is transitioning through a period of deep structural change. Multipolarity, technological acceleration, shifting demographics, climate imperatives, and geopolitical tensions are transforming how nations trade, innovate, and grow.

The next decade will be defined by adaptability. Countries and companies that invest in technology, diversify supply chains, embrace sustainability, and harness human capital will emerge as winners. As economic power diffuses and the global order evolves, agility and resilience will shape the new world economy.

NVDA PUT Trade — QuantSignals Katy High-Conviction ShortNVDA | QuantSignals Katy 1M Prediction (2025-11-21)

Current Price: $178.81

Predicted Close: $173.03 (-3.23%)

30-min Target: $177.19 (-0.91%)

Trend: Bearish

Confidence: 75%

Volatility: 49.6%

Trade Signal

Direction: PUT

Entry: $178.81

Target: $174.18

Stop Loss: $181.49

Expected Move: -3.23%

Summary: 1 trade signal generated from 1 successful analysis.

NVDA Head and Shoulders- Dec Rate Cuts has changed setupNvidia’s setup has shifted. With the Fed signaling a likely rate cut on December 10th, the market will start baking that optimism into asset prices ahead of time. When monetary conditions ease, high-valuation tech often gets an extra tailwind, which means the expected head-and-shoulders pattern on NVDA may fail to play out cleanly. The chart might still roll over, but the macro backdrop now works against a decisive breakdown. Short positions here demand caution.

Original post

Nvidia’s bear case rests on one core idea: the stock price assumes a flawless, world-eating AI future, and markets almost never deliver on “perfection narratives.” NVDA trades at extreme valuation multiples for a hardware-driven, highly cyclical business. Those multiples only hold if AI infrastructure spending keeps compounding at its current breathtaking pace for years. But that demand is dangerously concentrated in a handful of hyperscalers who are spending now and rationalizing later. Michael Burry’s recent argument sharpens this point: he claims true end-demand for AI horsepower is vastly overstated, and that much of the current GPU frenzy is a self-reinforcing loop of capital, hype, and accounting gimmicks rather than broad, organic need. If boards pause to question real ROI, or if the circular funding loop breaks Nvidia’s revenue curve can flatten quickly, dragging the valuation down with it.

Competition, long dismissed by NVIDIA bulls, is another structural headwind. AMD is now shipping accelerators that hyperscalers are actually integrating, and every major cloud provider is building in-house silicon to reduce dependence on NVDA’s margins. Even if Nvidia maintains leadership, it doesn’t need to lose the crown to lose the multiple, slight shifts in workload allocation or a handful of missed design wins are enough to pressure margins. And Burry’s critique deepens this point: he argues Nvidia’s reported profitability is flattered by depreciation assumptions and massive stock-based compensation that buybacks have failed to offset, meaning the “true” economic profit is less bulletproof than headlines suggest. Add to that the fact that U.S. export controls have effectively erased the China data-center market, once 20–25% of revenues and expectations of a seamless global TAM look increasingly unrealistic.

Technically, NVDA is doing exactly what a euphoric, overowned stock does when gravity starts tugging: momentum is fading, the price is slipping under short-term moving averages, and reactions to spectacular earnings have been strangely sluggish. That’s often the early signature of distribution rather than accumulation. And this lines up directly with Burry’s broader thesis: when a narrative becomes crowded and reflexive, the slightest wobble triggers violent air pockets. NVDA has become the ultimate proxy for the AI boom, the most crowded long in the market, meaning it’s the first thing funds sell when risk appetite cools, and the last thing buyers chase during corrections.

Put simply, Nvidia is a phenomenal company priced as if nothing can ever go wrong, while Burry is arguing that much of what looks “perfect” is not what it seems. The bear case isn’t that Nvidia collapses. It’s that the AI boom normalizes, competition accelerates, accounting realities catch up, margins slip toward something earthbound, and investors recalibrate how much they’re willing to pay. In that world, NVDA doesn’t need bad news to fall. It only needs the news to arrive slightly less euphoric than the fantasies currently baked into the price.

#NVDA #Bearish #HeadandShoulders #MichaelBurry

NVDA Head and Shoulders- Neckline BrokenNvidia’s bear case rests on one core idea: the stock price assumes a flawless, world-eating AI future, and markets almost never deliver on “perfection narratives.” NVDA trades at extreme valuation multiples for a hardware-driven, highly cyclical business. Those multiples only hold if AI infrastructure spending keeps compounding at its current breathtaking pace for years. But that demand is dangerously concentrated in a handful of hyperscalers who are spending now and rationalizing later. Michael Burry’s recent argument sharpens this point: he claims true end-demand for AI horsepower is vastly overstated, and that much of the current GPU frenzy is a self-reinforcing loop of capital, hype, and accounting gimmicks rather than broad, organic need. If boards pause to question real ROI — or if the circular funding loop breaks — Nvidia’s revenue curve can flatten quickly, dragging the valuation down with it.

Competition, long dismissed by NVIDIA bulls, is another structural headwind. AMD is now shipping accelerators that hyperscalers are actually integrating, and every major cloud provider is building in-house silicon to reduce dependence on NVDA’s margins. Even if Nvidia maintains leadership, it doesn’t need to lose the crown to lose the multiple — slight shifts in workload allocation or a handful of missed design wins are enough to pressure margins. And Burry’s critique deepens this point: he argues Nvidia’s reported profitability is flattered by depreciation assumptions and massive stock-based compensation that buybacks have failed to offset — meaning the “true” economic profit is less bulletproof than headlines suggest. Add to that the fact that U.S. export controls have effectively erased the China data-center market — once 20–25% of revenues — and expectations of a seamless global TAM look increasingly unrealistic.

Technically, NVDA is doing exactly what a euphoric, overowned stock does when gravity starts tugging: momentum is fading, the price is slipping under short-term moving averages, and reactions to spectacular earnings have been strangely sluggish. That’s often the early signature of distribution rather than accumulation. And this lines up directly with Burry’s broader thesis: when a narrative becomes crowded and reflexive, the slightest wobble triggers violent air pockets. NVDA has become the ultimate proxy for the AI boom, the most crowded long in the market — meaning it’s the first thing funds sell when risk appetite cools, and the last thing buyers chase during corrections.

Put simply, Nvidia is a phenomenal company priced as if nothing can ever go wrong — while Burry is arguing that much of what looks “perfect” is not what it seems. The bear case isn’t that Nvidia collapses. It’s that the AI boom normalizes, competition accelerates, accounting realities catch up, margins slip toward something earthbound, and investors recalibrate how much they’re willing to pay. In that world, NVDA doesn’t need bad news to fall. It only needs the news to arrive slightly less euphoric than the fantasies currently baked into the price.

#NVDA #Bearish #HeadandShoulders #MichaelBurry

Concerns on market specifically NVDA - Not financial adviceSome thoughts and concerns watching the market as an amateur investor looking at historical shifts and trends. This is not a prediction and not to be considered financial advice in any manner shape or form. It is simply a personal opinion based on my impression of the market. Please discuss any choice you make in the market regarding trades with a financial advisor or planner as this opinion is just an uneducated perspective to be taken with a grain of salt from someone who does not work in the financial industry. There are several factors I have taken into account regarding the economy, job losses, looming Debt Wall, real estate market concerns, tariff pain points for US, recession chatter, dollar weakness, US debt and my personal gut check.

Disclosure - I do not currently hold NVDA but I have a standing buy order for my personal account for NVDA at $50. I do not know the market well enough to short.

Bear case $NVDAIf we’re sitting in a 1999-style setup — which the chart strongly suggests — then the next move shouldn’t surprise anyone:

NASDAQ:NVDA

DECODED ANALYSIS OF NVIDIANVIDIA is currently in its second last quarterly pattern. After correcting its uptrend form, to restore this pattern the price must either move above $213.99 or hold the support levels at $158.96, $156.29, with major support at $151.05.

Broken pattern support, $106.90

Quarterly skip support, $27.51

Multiple skip supports, lowest at $0.0385

Above current resistance levels are $213.99, $229.61, $250.86, $269.46

Resistance noted for 2030 at $618.83

This message is for educational purposes only.

Always DYOR.

Berish ViewAfter 1 way rally in this stock and after Q3 Good No. We think it's now going to Consolidate face or seen some corrections.

Berish H&S Pattern seen so below yday low .

The confirmation done and stock min 5 to 10% down side seen.

SL is yday high closing.

Disclaimer:- it's my Personal view.

NVDA - The Truth About Nvidia's ReversalAfter an impulse wave always comes a correction. Here you see the wave A going down and the wave B going up. The unexpected reversal everyone is talking about is the start of wave C to the downside.

The insane wave B has run its course and hit the ceiling. There's no more room to go. That's why there was a reversal. It has nothing to do with external forces or circumstances. It's the nature of the Elliott Wave.

All the optimism for Nvidia has been factored into wave B. You can easily tell by how long and extended the wave is. High optimism always accelerates the price, which results in longer impulse waves. In other words, all the juice has been squeezed and there's no more juice to squeeze. Nothing lasts forever. It's time for wave C to make an appearance.

NVDA down MVP SYSTEM

MOMENTUM:

RSI Broke down from widening wedge

VOLUME:

to downside

PRICE ACTION:

big red engulfing at the lower border of the widening wedge

I don’t hold positions in NVDA. I use it as a barometer for the market.

Nvidia Bearish Engulfing Candle at 100 DMAIf this breaks through the 100DMA and has a sustained drop, expect it to go to the next support level of $150 to $152.

How dip can this get ?,bulls needs to defend 181-180 rangeNASDAQ:NVDA bears pushed market lower from a high of 196 ;looking at the chart we see price breaking-through our channel and price trading below our 50 day moving Average ,bulls have to defend 181-180 range a break will signal more selling pressure with remediate support at 177 and 164

Nvidia Erases Post-Earnings RallyShortly after publishing its earnings, shares of tech giant Nvidia jumped more than 5% at the start of the session; however, a new bearish sentiment quickly took hold of the market, and the stock fell over 7% in the final trading hours, wiping out the gains seen after the results. The company reported strong figures, with revenue of $57 billion, above the expected $54 billion, and projected fourth-quarter sales near $65 billion.

Despite the positive numbers, selling pressure began weighing on the price, mainly because the optimism was likely already priced in, prompting short-term profit-taking. In addition, growing concerns about emerging competition have fueled ongoing weakness in the stock. If market confidence fails to recover soon, selling pressure could intensify in the coming sessions.

Uptrend Losing Momentum

Since November 11, indecisive price action has led to a break of the long-standing upward trendline that had been guiding the stock’s movement. This uncertainty has created a short-term sideways range, with a ceiling at $196 and a floor at $179 per share. As long as these levels hold, a neutral and sideways phase is likely to dominate, indicating lack of clear direction in the short term.

RSI

The RSI remains slightly below the neutral 50 level, suggesting that selling momentum slightly outweighs buying pressure, though not strongly enough to establish a consistent short-term trend. As long as the RSI stays near 50, neutrality in price movement is likely to persist.

TRIX

The TRIX indicator shows a downward slope, moving closer to the zero line, indicating a balance in the strength of the exponential moving averages. This reinforces the indecision in the stock’s short-term behavior.

Key Levels to Watch:

$196 – Main Resistance: Corresponds to the most recent upward retracement zone. A break above this level could revive the bullish bias and reactivate the long-term uptrend.

$188 – Nearby Barrier: Area aligned with the 50-period simple moving average. Price moves near this level could support the formation of a more defined sideways range.

$179 – Key Support: Represents the lowest area from the past two months and serves as the most critical bearish barrier. A drop below this level could trigger a stronger selling bias and mark the start of a short-term downtrend.

Written by Julian Pineda, CFA, CMT – Market Analyst

NVDA | Post-Earnings Exhaustion Near Recent Highs – What’s Next?NVIDIA delivered another exceptional quarter, with revenue surging and demand for AI infrastructure remaining firm. Yet the market’s reaction was notably muted, signalling that expectations may already be stretched in the short term.

Technical Lens:

The share price gapped higher after earnings but struggled to break above its recent peak. It slipped back toward the pre-announcement zone, which suggests fatigue after months of strong momentum. The anchored VWAP from the last significant swing remains an important reference point below current prices, acting as fair-value support throughout the year.

Scenarios:

• If the anchored VWAP continues to draw price lower, the shares may drift into that support zone before sentiment resets and buyers return.

• If the post-earnings gap is reclaimed and price pushes through prior highs, it would indicate that momentum is re-energising sooner than expected.

Catalysts:

Upcoming macro data, broader equity market sentiment, and any fresh commentary on AI demand or supply constraints may influence whether NVIDIA consolidates or attempts another move toward new highs.

Takeaway:

The fundamentals remain strong, but the technical picture hints at a near-term pause. The anchored VWAP zone sits as the key decision point for the next phase of the trend.

NVDA | Long | R/S Flip at 172 + 0.5 Fib | Nov 20, 2025NVDA | Long | R/S Flip at 172 + 0.5 Fib + VWAP Support in Rising Channel | Nov 20, 2025

🔹 Thesis Summary

NVIDIA remains the S&P 500’s largest single weight and the AI-infrastructure bellwether. After a fast shakeout to channel support, the chart sets up a defined-risk long as risk sentiment sits at Extreme Fear—a backdrop that historically favors mean reversion and leadership rebounds.

🔹 Trade Setup

Bias: Long

Entry Zone: 172–182 (R/S flip and ~0.5 retrace inside the ascending channel)

Stop Loss: 152–156 (below VWAP/structure and prior base)

Take-Profits:

TP1: 188–192 (channel mid / prior supply)

TP2: 205–208 (upper-mid channel)

TP3: 214–220 (channel top / measured move)

Max Target: 230–246 (channel extension if trend resumes)

R:R (from ~175): ~1.5–3.0 depending on exit path and scaling.

🔹 Narrative & Context

Structure: Daily up-channel intact; recent spike down tagged the lower rail and immediately reclaimed the R/S band near 172. That zone aligns with ~0.5 Fib of the prior impulse and anchored VWAP support—classic “shakeout-and-go” anatomy.

Flow: Pullbacks within strong secular trends often pivot when broader risk metrics hit extremes. Current readings show Extreme Fear across equities and crypto (dashboard needles in single-digits/low-teens), consistent with forced-de-risking rather than trend change.

Leadership: Info Tech is 34% of the S&P 500 by weight. NVDA itself sits at ~8.06% of the index’s top-25 weight table—structurally important for passive flows. Re-risking tends to bid the heaviest weights first, providing tailwinds if indices stabilize.

Correlations to watch: NQ strength, breadth stabilization in SOX, and dollar drift lower typically amplify NVDA recovery legs.

🔹 Valuation & Context (Pro Metrics, Framed Simply)

Forward P/E: ~35–45x vs Semi/Tech peers typically ~20–25x → Market pays a premium per $1 of next-12-mo earnings → Premium reflects dominant AI compute share and visibility; multiple compression risk is why we anchor to defined stop.

P/FCF: High-teens to 20s vs peers in low-teens → Investors pay up for cash conversion → Acceptable so long as AI DC demand/ASP mix persists.

Quality (ROE/ROIC): Very high (well above typical large-cap tech) → Capital turns + software stack (CUDA) lift returns → Supports buying pullbacks, not chasing verticals.

Growth: EPS growth well above sector on AI data-center ramps → Outlier growth justifies trend-following bias.

Risk (Debt/Equity): Low/Conservative → Balance sheet flexibility if cycle wobbles.

🔹 Contrarian Angle (Your Edge)

Consensus fixates on “too expensive” optics and headline sentiment. The technical reaction at 172–182 with fear gauges at extremes argues for a positioning reset, not a trend break. With channel structure intact and flows concentrated in megacap AI, we see a credible path toward 214–220 first, then 230–246 on continuation.

🔹 Risks

Positioning/Multiple Risk: Any guide-down or supply hiccup can compress the premium multiple.

Sector Rotation: A sharp unwind in AI/semis or factor shift to defensives.

Macro Shock: Dollar spike/real-yield jump or regulatory headlines impacting export mix.

🔹 Macro Considerations

Sentiment: Equity & crypto Fear & Greed dials show Extreme Fear (single-digit/low-teens) — fuel for relief rallies when flows turn.

Index Mechanics: Tech at 34% of S&P weight; NVDA among top index constituents (~8.06% of top-25 weight list). Stabilization in SPX/NQ mechanically supports NVDA.

Flow Triggers: SOX breadth thrust, NQ reclaim of prior breakdown area, and any cooling in rates/FX volatility would accelerate the upside path.

🔹 Bottom Line

NVDA’s premium is real, but so are its cash generation and AI demand drivers. The 172–182 buy-zone offers a clean, conviction long with 152–156 as invalidation. Manage in tranches toward 188 / 205 / 214–220, leaving a runner for 230–246 if momentum and macro confirm.

🔹 Forward Path

If this gains traction (10+ likes), I’ll post: (1) a weekly/time-frame add-on with updated channel math, (2) live notes on any break/retest of 205 and 214–220, and (3) Q&A on risk management.

Like & Follow for structured ideas, not signals. I post high-conviction setups here before broader narratives play out.

⚠️ Disclaimer: This is not financial advice. Do your own research. Levels derived from the attached chart; sentiment and index weights from the referenced images. Charts/visuals may include AI enhancements.

🔹 Footnote

Forward P/E: Price divided by expected earnings over the next 12 months. Lower = cheaper relative to profits.

P/FCF (Price-to-Free-Cash-Flow): Price vs. the cash left after investments. A measure of efficiency.

FCF Yield: Free cash flow per share ÷ price per share. Higher = more cash returned for each dollar invested.

ROE (Return on Equity): Net income ÷ shareholder equity. Shows management efficiency with investor capital.

ROIC (Return on Invested Capital): Net income ÷ all invested capital (equity + debt). A purer profitability gauge.

Debt/Equity: Debt divided by equity. <1 usually means balance sheet is conservative.

R:R (Risk-to-Reward): Ratio of expected upside vs. downside. 3:1 = you risk $1 to make $3.

NVDA LongBroader Market Structure

NVDA has been in a short-term bullish corrective structure after forming a BOS at $179.91, which marked the end of the prior bearish leg. Since that break, price has been forming higher lows and higher highs on the intraday structure. However, the most recent swing into the $194–$195 supply produced a sharp rejection, showing that the bullish structure is still counter-trend relative to the larger bearish swing from the $202–$205 highs. No new CHoCH has printed yet, but the aggressive selloff from $195 signals a potential short-term shift in control back toward sellers unless demand holds.

Supply & Demand Zones

The upper supply zone at $194–$195 remains strong; price dropped sharply from this level with long-bodied bearish candles, showing active institutional selling and low willingness from buyers to absorb orders. The deeper supply above, between $199–$202, is an even stronger zone because it originated the major downside impulse that broke structure.

On the buy side, the demand at $185–$183 previously showed clear strength—buyers stepped in aggressively and pushed price upward with momentum—which tells us the zone still carries validity. The lower demand between $181–$178 is even more important, as it’s the origin of the BOS at $179.91 and represents the last confirmed defensive line for bulls.

Price Action Within the Marked Region

Price is currently falling from the $195 rejection and heading toward the $185–$183 demand you marked. Candles show increasing wick size on the way down, suggesting early signs of selling exhaustion but not yet a reversal. As price enters this demand, we should see either absorption or continuation. If buyers defend the zone as they did previously, a corrective bounce toward $192–$194 is likely. If demand fails, price will unwind quickly into the deeper $181–$178 liquidity pocket.

Expectation, Bias & Invalidation

Trade bias: short-term bullish, expecting price to dip into demand and bounce into the lower supply.

Expected direction: a pullback into $185–$183, followed by a rally into $192–$194.

Invalidation: a clean close below $183, which would signal sellers have regained full control and shift the outlook to bearish continuation toward $181–$178.

Momentum & Candle Behavior

Momentum currently favors sellers, given the fast drop from supply, but the decline is becoming more controlled—suggesting momentum is fading as price approaches demand. No confirming reversal candles have appeared yet; we will need to see a long-wick rejection, engulfing candle, or clear absorption footprint at demand to confirm the bounce scenario.