Trade ideas

the PopLooks like a reversal here. A break below the lows and I'm incorrect. Everything is popping. Watch Oil for a break up above the 18ma soon.

S&P 500 falls below 6K - key levels to watchAs highlighted the possibility yesterday, the S&P 500 has now fallen to a fresh multi-week low. The old low at 6631 is now the most important level to watch in terms of upside resistance. Above that 6638, yesterday's low, will come into focus ahead of 6650/5 area.

On the downside, the mid-October lows of 6533 and 6500 are the next areas of interest for the bears. Will we get there? Perhaps if NVidia earnings disappoint tomorrow night.

By Fawad Razqzada, market analyst with FOREX.com

#SPX Intraday Institutional Update. 18 November 2025**S&P 500 – Intraday Institutional Update | 18 November 2025**

The index continues to hover in an extremely uncomfortable elevation zone (~6,870–6,920) after failing multiple times to sustain above the psychologically significant 6,900 round. On the 4-hour timeframe, price action is manifesting as a sequence of indecisive, high-wick candles with diminishing real-body progression — a classic hallmark of structural instability at extreme deviation levels.

Key observations from a risk-desk perspective:

- The S&P 500 remains ~480–510 points detached above the 9-period monthly moving average, a magnitude of extension that historically compresses aggressively once bidirectional order flow reasserts itself.

- 4H momentum profiles (RSI, StochRSI, MACD histogram) are flattening to negatively sloping while price refuses to commit directionally — a textbook precursor to sharp liquidity-driven resolution.

- Equal-high retests over the past 72 hours coupled with expanding H4 range ATR but contracting realized volatility underscore fading conviction among fast-money participants.

- Micro-composite breadth (NYSE advance-decline line, % of stocks above 50-day MA) continues to deteriorate beneath the surface, widening the divergence with price.

From a professional standpoint, the current configuration is one of the more precarious “equilibrium-at-extremes” setups we have monitored in the post-2022 regime. The balance of probabilities now leans toward a violent mean-reversion episode rather than an orderly consolidation. Positioning should reflect heightened caution: elevated gamma exposure, concentrated long positioning in systematic vehicles, and still-rich implied volatility term structure all point to asymmetric downside risk in the very near term.

A decisive 4H close below 6,835 would likely trigger stop clusters toward 6,650–6,680 initially, with risk of acceleration toward the 6,400–6,500 zone if monthly support layers fail to attract defensive capital.

Institutional risk committees are strongly encouraged to re-evaluate gross and net exposure, widen hedging coverage, and prepare contingency capital for volatility expansion.

**Tags**

#SP500 #ES_F #Equities #USMarkets #RiskManagement #MarketStructure

#TechnicalAnalysis #Momentum #Breadth #Volatility #GammaExposure

#InstitutionalInvesting #PortfolioConstruction #Hedging #MacroTrading

#SystematicStrategies #VolatilityTargeting #CTAs #RiskParity

#GlobalMacro #AssetAllocation #QuantFinance #TradingDesk

#GoldmanSachs #JPMorgan #MorganStanley #BankofAmerica #Citi

#UBS #DeutscheBank #Barclays #HSBC #BNPP #SocGen #RBC

#Citadel #Millennium #Point72 #TwoSigma #DEShaw #AQR

#Bridgewater #BlackRock #Vanguard #StateStreet #PIMCO #FidelityInvestments

Possible drop and popIf we breakdown at open be careful of a rally to recover 6650 support. Oil is at it's 18ma, needs to get over it to be bullish. Gold maybe rally to 4100 area before further downside. BTC could go a bit lower but again I think it will bounce sooner rather than later.

S&P500 remain under pressure, support at 6580Equities remain under pressure, with the S&P 500 down 0.92% yesterday, marking:

3rd straight decline (first since September)

Worst 3-day stretch since April (-2.61%)

Futures down another ~0.5% this morning

The index has now broken below its 50-day moving average for the first time in 139 sessions—its longest stretch above the level since 2007—adding to technical downside pressure.

Drivers of the Selloff

AI trade concerns continue to weigh:

Nvidia -1.88%, Philadelphia Semi Index -1.55%

JPMorgan’s Daniel Pinto warned of AI-rich valuations posing broader market risk.

Broad selling across the S&P:

407 decliners, most in 5 weeks

Equal-weight S&P -1.31%, Russell 2000 -1.96%, both at lowest since August

Credit risk sentiment deteriorated:

US HY +5bps, IG +1bps wider

Amazon priced $15bn in new bonds, adding to supply pressure

Mega-cap Tech

Mag-7 only slightly lower (-0.08%), saved by:

Alphabet +3.11% on Berkshire stake news

Apple sentiment mixed:

Design group loss, but strong China iPhone 17 sales (+37%) provided support

Crypto Risk Pressure

Bitcoin -3.3%, touching its lowest since April

Down ~4% YTD 2025

Down nearly 30% from highs 6 weeks ago

Modest rebound this morning helping stabilize risk tone

Macro Tone

Mass layoffs surged in October (Cleveland Fed) → signs of labour softening

Focus shifts to Thursday’s delayed September jobs report for confirmation

Trading Takeaway

Tone remains fragile, but S&P futures and Bitcoin stabilizing suggest some cooling of the global selloff.

Break of the 50-day MA is a key technical negative; next support levels likely in focus.

AI sector weakness + broader macro softening remain dominant headwinds today.

Key Support and Resistance Levels

Resistance Level 1: 6707

Resistance Level 2: 6757

Resistance Level 3: 6785

Support Level 1: 6580

Support Level 2: 6554

Support Level 3: 6530

This communication is for informational purposes only and should not be viewed as any form of recommendation as to a particular course of action or as investment advice. It is not intended as an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Opinions, estimates and assumptions expressed herein are made as of the date of this communication and are subject to change without notice. This communication has been prepared based upon information, including market prices, data and other information, believed to be reliable; however, Trade Nation does not warrant its completeness or accuracy. All market prices and market data contained in or attached to this communication are indicative and subject to change without notice.

S&P500 close to confirming the new Bear Cycle.The S&P500 index (SPX) broke below its 1D MA50 again yesterday (even closed the day below) and is showing clear signs of weakness at least for the short-term.

This can't be ignored as it may be transferred to the long-term time-frames where the market has been forming a Bearish Divergence on its 1W RSI since October 27. RSI Lower Highs against the market's Higher Highs.

This is similar to the November 15 2021 1W RSI Bearish Divergence, which led to one last quick rally and 1.5 month later the Bull Cycle topped and the 2022 inflation crisis Bear Cycle started.

The signal was given by a weekly closing below the 1D MA100 (red trend-line), which has been the market's natural Support in the past 5 months and also during every major Bullish Leg of the Bull Cycle.

As a result, if the index closes a 1W candle below its 1D MA100, we will call the start of a new Bear Cycle, potentially aiming for the 1W MA200 (orange trend-line), which is where the 2022 Bear Cycle bottomed after a -27.62% correction. Our Target Zone for the next long-term buying will be 5300 - 5000, assuming the top is already in. If not, the -27.62% decline will be re-adjusted to the new top.

---

** Please LIKE 👍, FOLLOW ✅, SHARE 🙌 and COMMENT ✍ if you enjoy this idea! Also share your ideas and charts in the comments section below! This is best way to keep it relevant, support us, keep the content here free and allow the idea to reach as many people as possible. **

---

💸💸💸💸💸💸

👇 👇 👇 👇 👇 👇

Trading Hours Showdown: Stocks, FX, Crypto and When to SleepSome markets close, some don’t, and some don’t care that you need rest.

If financial markets were people, they’d each have wildly different sleeping habits. Stocks tuck themselves in usually at 4 p.m. (that is, where they originate from), FX stays up all night but insists it’s “fine,” and crypto is that friend who messages you at 3 a.m. with a life-changing idea (and a 12% move for fun).

Understanding when each market is awake, liquid, and volatile is one of the most underrated skills a trader can have. It’s not just about timing entries; it’s about managing risk while you’re away from your devices.

Let’s break down the global sleep schedule and why your portfolio should care.

🌅 Stocks: The 9-to-5ers of the Financial World

US stocks like routine. They open at 9:30 a.m. ET, close at 4 p.m., and observe weekends and holidays like well-behaved citizens.

There’s also pre-market and after-hours trading, but liquidity dries up real fast and moves tend to be exaggerated.

Why it matters:

Limited hours = overnight gap risk

Most volume typically happens in the first and last 30 minutes

Big news after hours can cause violent opens the next day

Stops can’t protect you when price jumps over your level

Every trader eventually experiences the heartbreak of a perfect setup ruined by an overnight earnings surprise. Consider it a rite of passage.

🌍 Forex: The Market with No Bedtime

FX ( forex or foreign exchange) trades 24 hours a day, five days a week, rotating through global sessions:

Asia (Tokyo)

Europe (London)

US (New York)

That’s a 120-hour work week with no break. Think of it like a global relay race where someone is always awake and analyzing inflation differentials.

Why traders love it:

Continuous liquidity = fewer gaps

Beautiful macro-driven trends

Volatility waves follow session overlaps (London–NY especially)

But…

FX weekends could be silent killers. You’re unprotected from Friday close to Sunday open. That’s plenty of time for geopolitical headlines, surprise events, central bank drama, or a country deciding to unpeg its currency.

🔥 Crypto: The Market That Never Sleeps or Blinks

The cryptocurrency market trades 24/7/365. No days off, no weekends, no holidays, no rest. Just pure, unfiltered price action around the clock.

This sounds great until you realize you can never fully unplug. Bitcoin BITSTAMP:BTCUSD does not respect your circadian rhythm.

Why it’s unique:

No “overnight gaps” because it never closes

But liquidity gaps may appear during low-volume hours

Late-night moves can be extreme due to thin order books

Leverage unwinds can trigger liquidation cascades at 3 a.m.

Global retail participation exaggerates emotional spikes

Crypto doesn’t gap like stocks, but it drifts, snaps, and rips through levels and can make your stomach churn.

🧭 Liquidity: The Real Story Behind the Sleep Schedule

Across markets, the one concept that ties them all together is liquidity. That is, how deep the order book is and how efficiently your trades can execute.

Stocks

Thick liquidity during US hours

Thin, jumpy after-hours

Prone to large news-driven gaps

Forex

Deep liquidity almost 24 hours a day

Most volume during London–NY overlap

Macro news instantly reflected in price

Crypto

Liquidity pockets vary wildly

Exchanges differ in depth

Weekends and Asia-over-US crossovers can trigger whipsaws

😴 The Question of Sleep (And How Traders Manage It)

Traders eventually learn a few things about trading various asset classes.

If you:

Hate surprises → Avoid overnight stock positions

Love macro trends → FX is your playground

Enjoy volatility → Crypto keeps things interesting

Value sleep → Choose an asset class that aligns with your time zone and day trade it

Choosing a market to trade isn’t just about your strategy, but also about your lifestyle.

Volatility doesn’t just depend on the asset. It depends on when you’re watching.

Off to you : How do you deal with trading different assets in different time zones? Are you a niche player or a broader market maven? Share your comments below!

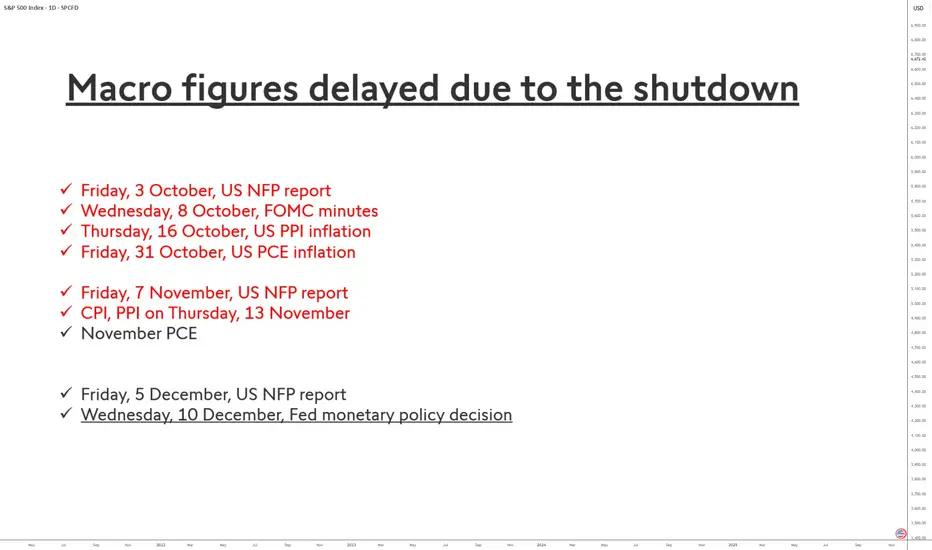

Imminent End of the U.S. Statistical Blackout!The prolonged shutdown of the U.S. federal government has had an exceptional impact on the release of some of the country’s most important economic statistics. Indicators such as the employment report (NFP), PCE inflation, or the CPI are the backbone of the Federal Reserve’s monetary policy and heavily influence financial market volatility. Their delay therefore creates a true statistical “black hole.”

Why are these indicators delayed?

Two federal agencies have been affected:

• the Bureau of Labor Statistics (BLS), responsible for NFP and CPI;

• the Bureau of Economic Analysis (BEA), which publishes PCE inflation as well as household income and spending data.

During the shutdown, these agencies had to suspend the collection, processing, and validation of data. Unlike a simple administrative pause, this disrupts complex statistical pipelines built on surveys of businesses and households. Some data cannot be “caught up” immediately because they depend on strict deadlines, which explains why certain series may be incomplete, revised late, or even canceled.

The case of Non-Farm Payrolls (NFP)

The October NFP report — normally released in early November — was entirely blocked. Signals from the BLS suggest that this report may be partially or totally compromised, especially the household survey, which is more difficult to reconstruct.

By contrast, the September report, which was also delayed, now has a confirmed publication date: Thursday, November 20, 2025.

For the October report, there is still no official date. The most likely estimates point to a possible release in late November or early December, provided the data quality is deemed acceptable.

The case of PCE inflation

The October PCE inflation figure — scheduled for October 31 — was also halted. The BEA announced it would revise its entire calendar but has not yet provided firm replacement dates.

Economists currently expect a publication around November 26, 2025, potentially in a partially “imputed” form (with statistical estimates filling missing data).

Market consequences

The absence of these key data forces investors and the Fed to navigate blindly. Volatility could remain elevated until the full or partial release of these indicators, which should gradually return to a normal schedule starting in December.

DISCLAIMER:

This content is intended for individuals who are familiar with financial markets and instruments and is for information purposes only. The presented idea (including market commentary, market data and observations) is not a work product of any research department of Swissquote or its affiliates. This material is intended to highlight market action and does not constitute investment, legal or tax advice. If you are a retail investor or lack experience in trading complex financial products, it is advisable to seek professional advice from licensed advisor before making any financial decisions.

This content is not intended to manipulate the market or encourage any specific financial behavior.

Swissquote makes no representation or warranty as to the quality, completeness, accuracy, comprehensiveness or non-infringement of such content. The views expressed are those of the consultant and are provided for educational purposes only. Any information provided relating to a product or market should not be construed as recommending an investment strategy or transaction. Past performance is not a guarantee of future results.

Swissquote and its employees and representatives shall in no event be held liable for any damages or losses arising directly or indirectly from decisions made on the basis of this content.

The use of any third-party brands or trademarks is for information only and does not imply endorsement by Swissquote, or that the trademark owner has authorised Swissquote to promote its products or services.

Swissquote is the marketing brand for the activities of Swissquote Bank Ltd (Switzerland) regulated by FINMA, Swissquote Capital Markets Limited regulated by CySEC (Cyprus), Swissquote Bank Europe SA (Luxembourg) regulated by the CSSF, Swissquote Ltd (UK) regulated by the FCA, Swissquote Financial Services (Malta) Ltd regulated by the Malta Financial Services Authority, Swissquote MEA Ltd. (UAE) regulated by the Dubai Financial Services Authority, Swissquote Pte Ltd (Singapore) regulated by the Monetary Authority of Singapore, Swissquote Asia Limited (Hong Kong) licensed by the Hong Kong Securities and Futures Commission (SFC) and Swissquote South Africa (Pty) Ltd supervised by the FSCA.

Products and services of Swissquote are only intended for those permitted to receive them under local law.

All investments carry a degree of risk. The risk of loss in trading or holding financial instruments can be substantial. The value of financial instruments, including but not limited to stocks, bonds, cryptocurrencies, and other assets, can fluctuate both upwards and downwards. There is a significant risk of financial loss when buying, selling, holding, staking, or investing in these instruments. SQBE makes no recommendations regarding any specific investment, transaction, or the use of any particular investment strategy.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. The vast majority of retail client accounts suffer capital losses when trading in CFDs. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Digital Assets are unregulated in most countries and consumer protection rules may not apply. As highly volatile speculative investments, Digital Assets are not suitable for investors without a high-risk tolerance. Make sure you understand each Digital Asset before you trade.

Cryptocurrencies are not considered legal tender in some jurisdictions and are subject to regulatory uncertainties.

The use of Internet-based systems can involve high risks, including, but not limited to, fraud, cyber-attacks, network and communication failures, as well as identity theft and phishing attacks related to crypto-assets.

Artificial Intelligence & Tech Stocks Rally1. The Rise of AI as an Economic Catalyst

AI has shifted from being a futuristic concept to a real-world productivity enhancer. It now influences every major industry: financial services, healthcare, manufacturing, retail, cybersecurity, logistics, and more. Technologies such as deep learning, natural language processing, and autonomous systems have prompted companies worldwide to accelerate their digital transformation.

The introduction of large language models (LLMs), AI chips, robotics, and automation has created a new economic cycle driven by data, computing power, and algorithmic intelligence. As a result, companies directly involved in AI development—along with those supplying the hardware and cloud platforms—have become market favorites.

Investors increasingly view AI as the next “industrial revolution” capable of reshaping global productivity, profitability, and innovation. This belief has driven massive capital inflows into tech stocks, especially those perceived as leaders in AI research and commercialization.

2. Key Drivers Behind the AI-Fueled Tech Rally

A. Explosive Growth of Generative AI

The launch of advanced generative AI systems dramatically accelerated interest in AI stocks. Major companies quickly integrated generative AI into search engines, productivity tools, customer support, and software development workflows. This rapid adoption strengthened the revenue outlook for tech giants and reinforced investor confidence.

B. Demand for High-Performance Computing & AI Chips

Semiconductor companies, particularly those producing AI GPUs and specialized accelerators, have emerged as the backbone of the AI revolution. The massive need for computational power has pushed chip manufacturers to record valuations. Cloud service providers and hyperscale data centers are investing billions to upgrade their infrastructure to handle AI workloads.

C. Cloud Expansion & Software AI Integration

Tech firms integrating AI into their existing cloud and software offerings have seen rising subscription revenue and improved customer retention. The “AI upgrade cycle”—where businesses adopt AI features as part of cloud services—has enhanced long-term earnings visibility for cloud companies.

D. Automation & Productivity Gains

AI-driven automation is helping businesses improve productivity while reducing costs. Companies that demonstrate measurable efficiency gains from AI adoption are rewarded by investors, who view this as margin-expansion potential. As firms show better earnings due to AI-enabled efficiencies, market optimism increases.

E. Global Government Support

Governments worldwide are prioritizing AI policy, infrastructure, and innovation funding. This includes national AI strategies, incentives for semiconductor manufacturing, and investment in digital public infrastructure. These initiatives create favorable environments for AI-driven business growth, further strengthening investor sentiment.

3. Major Sectors Benefiting from the AI Rally

1. Semiconductor & Chip Manufacturing

AI requires enormous computing power, leading to unprecedented demand for GPUs, neural processing units (NPUs), and specialized chips. Semiconductor companies have seen massive revenue growth due to AI training and inference workloads.

2. Cloud Computing Platforms

AWS, Microsoft Azure, Google Cloud, and others are increasingly viewed as the “AI backbone” because they host AI models and provide infrastructure. Cloud giants benefit from scalable subscription revenue and enterprise AI spending.

3. Software as a Service (SaaS)

SaaS companies integrating AI into CRM, automation, analytics, and productivity tools are experiencing an upgrade cycle. New AI features allow them to charge premium subscription fees, boosting profitability.

4. Cybersecurity

AI-powered cybersecurity systems detect threats faster and manage huge volumes of data. With rising cybercrime, demand for AI-based security tools continues to expand.

5. Robotics & Automation

AI is powering industrial robotics, warehouse automation, and autonomous machinery. The increased demand for efficiency in logistics and manufacturing fuels revenue growth for automation firms.

6. Consumer Technology

AI is enhancing smartphones, smart home systems, wearables, and personal digital assistants. Tech companies adding AI capabilities have seen surging demand for next-generation devices.

4. Why Investors Are Bullish on AI's Long-Term Outlook

A. Multi-Trillion Dollar Market Potential

AI’s total addressable market (TAM) is expected to surpass trillions of dollars over the next decade. Analysts predict long-term growth across nearly every industry, making AI one of the largest commercial opportunities in history.

B. Continuous Innovation & Rapid Deployment

AI models and systems improve continuously. Every new innovation—smarter models, faster chips, more efficient algorithms—creates new commercial opportunities. This rapid pace of change fuels sustained investor enthusiasm.

C. Enterprise Adoption at Massive Scale

Companies across sectors are integrating AI into operations, decision-making, and customer experience. Enterprise adoption is one of the biggest drivers of long-term revenue growth for AI suppliers and service providers.

D. Network Effects & Data Advantages

Companies with massive data pools, extensive user bases, and strong computational capacity benefit from network effects. This creates “winner-take-most” dynamics favoring tech giants—which attract substantial investor capital.

5. Risks & Challenges to the AI Tech Rally

While the AI-driven rally is strong, it is not without risks:

1. Overvaluation Concerns

Some tech stocks have reached extremely high valuations. If earnings growth fails to match expectations, corrections may occur.

2. Supply Chain Constraints

AI hardware requires complex semiconductor supply chains. Shortages in advanced chips could impact production and revenue.

3. Regulatory & Ethical Uncertainty

Governments are increasing oversight over AI data use, privacy, and safety. Regulatory risks can affect growth prospects.

4. High Capital Expenditure

AI infrastructure—data centers, chips, cloud systems—is extremely expensive. Some companies may face profitability pressures due to high capex.

5. Competitive Intensity

AI markets are highly competitive. New entrants, rapid innovations, or pricing pressures could disrupt market leaders.

6. Future Outlook of AI & Tech Stocks

The long-term outlook for AI and tech remains highly positive. Over the next decade, AI is expected to shape global economic growth, productivity, and technological innovation. Key trends include:

Expansion of generative AI across enterprise workflows

Surge in demand for AI chips, data centers, and cloud computing

Growing adoption in healthcare, finance, logistics, education, and retail

AI-powered robotics reshaping manufacturing

Increased global investment in digital and computational infrastructure

Despite market volatility or occasional corrections, AI’s economic impact is expected to grow significantly, making AI and tech stocks central to modern global portfolios.

SPX Possibly Breaking SupportPreviously support held on this Higher Low, but it is now creating a bear trend by showing us a Lower High, and now breaking support to possibly create a Lower Low. Wait for a retest on the support which will act as resistance, or on the trendline for a low risk short entry. Feel free to drop your thoughts/opinions!

Megaphone Broadening Top Likely on SPXOver the last few months, the market has been increasingly difficult to trade as it searches for direction. Stop losses were triggered for longs on Oct 10, and shorts were equally liquidated on the run up beginning Oct 27th. What has formed is a broadening top, confirmed by two points of touch on each side of the pattern.

Broadening patterns can go in both directions, but supporting information suggests this is the end of the bull market:

On the weekly chart, there is a MACD cross.

There is a clearly defined 5 wave structure from the October 2022 bottom. It is a textbook example of Elliot Wave Theory.

Multiple analysts have shown that stock valuations are near historical extremes. It is highly likely that the market is in an AI bubble.

How am I trading this? I have sold all long positions. I am swinging puts that I will close out at the bottom of the megaphone. Once a breakout occurs, a pullback is highly likely to follow, even going so far as to return inside the pattern (60% of the time). If a pullback does occur, I'll load up on long dated puts to profit off a potential bear market.

SPX: Correction?SPX:

.

Correction?

Distribution forming pattern on Daily Timeframe- Head and Shoulder.

Wait for confirmation, upon breaking key important key level.

Wait and see!

.

US STOCKS- WALL STREET DREAM- LET'S THE MARKET SPEAK!

$SPX:Bearish technical indicators are accumulating:SPX: Bearish technical indicators are accumulating:

1) A sell signal on the MACD.

2) The RSI14 is at 42.

3) There has been a break below the 10, 20, and 50-period simple moving averages.

4) There is an inability to break above the horizontal resistance at 6765.

It is evident that the bullish momentum that followed the extremely bearish candlestick on October 10th has stalled, resulting in sideways trading with a slight downward trend. However, there is no immediate cause for concern since an underlying pressure is currently halting the decline.

At this point, we could expect a bullish flag pattern to emerge, which will be confirmed by the market's reaction to NVDA's results next Wednesday. The lower limit of the anticipated flag aligns with a 1x1 extension for wave (C). If the situation worsens and the flag is broken, it may transform into a zig-zag pattern, with extension targets for wave (C) indicated on the chart. Consider viewing this as an opportunity to enter a long position.

S&P anticipation for the 2025 ending It requires no many words to tell the trues.

I Think it might be double zigzag reaching at least 5800, in zone where 4th wave ending

SPX500 Breakdown Warning: Major Supports— Bigger Crash Ahead?The S&P 500 index ( SP:SPX ) has become increasingly significant recently, and it has a notable impact on cryptocurrency markets, especially Bitcoin ( BINANCE:BTCUSDT ). Therefore, analyzing the S&P 500 not only benefits its own market but also enhances our understanding of related markets.

Fundamental Analysis:

Volume confirms distribution, while the ongoing U.S. government shutdown delays critical data (CPI, PPI), fueling uncertainty and risk-off sentiment. Fed’s hawkish pause on rate cuts and tech sector rotation (TSLA -6%( NASDAQ:TSLA ), NVDA -3.5%( NASDAQ:NVDA )) reinforce bearish momentum. Also, YTD performance now -3.2% in November — on pace for the worst monthly drop since 2008 (-7.5%

Technical Analysis:

From a technical perspective, the S&P 500 index is breaking the Support zone($6,773_$6,710) and moving near the Support lines and 50_SMA(Daily) . Given recent data, there’s a possibility that these supports may break.

Additionally, according to Elliott Wave Theory , we can expect more corrective waves ahead.

I expect the SPX500 index to decline to $6,633 after the support cluster is broken in the first step.

First Target: $6,633

Second Target: $6,583

Stop Los(SL): $6,815

Please respect each other's ideas and express them politely if you agree or disagree.

S&P 500 Index Analyze (SPX500USD), 4-hour time frame.

Be sure to follow the updated ideas.

Do not forget to put a Stop loss for your positions (For every position you want to open).

Please follow your strategy and updates; this is just my Idea, and I will gladly see your ideas in this post.

Please do not forget the ✅' like '✅ button 🙏😊 & Share it with your friends; thanks, and Trade safe.

String rejection from support. pull back S&p500 LongStrong rejection from support. A good pullback expected in FRED:SP500

US500 - BEARISHEvening all!

Keeping it simple and short, the dollar is undervalued, and everything (indexes, crypto, precious metals) all melting up at the same time - im anticipating an end to 2025 that see's the dollar rise, and the melt up, melt down!

For US 500 - Target/draw on liquidity is the Weekly STL overall.

$SPX 1H – Bear Flag (Nov 17) $SP:SPX #SPX SP:SPX

After the dump off the late-October supply zone, SPX has formed a rising parallel channel that looks like a classic bear flag on the 1H. The pole is the leg from ~6,82x into the mid-6,64x flush; the flag is now a cleaner channel anchored off the post-spike higher lows and multiple swing highs.

Check 1h charts from Nov 13 and Nov 14

Price is currently riding the lower rail of the flag near 6,70x. A decisive 1H close below the channel and 6,70x would confirm a breakdown, opening room toward the 6,65x–6,64x demand zone and a potential measured-move extension. If instead we bounce and reclaim the upper rail (~6,77x–6,78x) and hold above it, the bear-flag idea weakens and this turns into a deeper mean-reversion squeeze rather than immediate continuation. #SPX

SPX 500: Stocks look heavy US stocks are testing their session lows with major indices looking heavy amid the unwinding of carry trades...

Concerns about Japan’s growing debt are intensifying. The government seems to be trying to have it both ways—implementing a massive fiscal stimulus package worth 17 trillion yen while opposing monetary policy normalization by the Bank of Japan. This conflicting stance has led to a sharp decline in the yen and bond prices, pushing Japanese yields higher. Markets now worry that the government is mishandling the economy, demanding higher returns to compensate for what they perceive as rising risk in holding Japanese debt.

So why does this matter for US stocks? The turbulence in Japanese markets may be triggering a carry trade unwind, similar to what happened in the summer of 2024. In a carry trade, investors borrow funds from countries with very low interest rates—like Japan—and invest them in higher-yielding assets such as stocks, gold, or cryptocurrencies denominated in stronger currencies like the U.S. dollar. As Japanese yields climb, the cost of maintaining these trades rises. With yields now becoming uncomfortably high, traders are being forced to reduce leveraged positions across markets, including US stocks.

By Fawad Razaqzada, market analyst with FOREX.com

SPX QuantSignals: Bullish Bias SPX QuantSignals Katy 1M Prediction 2025-11-17

Symbol: SPX

Price: 6706.78

Model: Katy AI 1M Prediction

Trend: Bullish

Confidence: 64.6%

🔮 Vision Summary

SPX maintains a bullish short-term structure, with the model projecting a move toward 6753.08 (+0.69%).

Momentum remains positive as long as price holds above 6700, with 30-minute targets signaling continued upward drift toward 6730.49.

Volatility remains moderate (27.3%), supporting steady trend continuation rather than sharp mean-reversion.

📈 Key Levels

Entry Zone: 6706.78

Upside Target: 6743.82 – 6753.08

Support / Invalidation: 6606.18

🧭 Vision Bias

Bullish — Model indicates upward continuation with controlled volatility and stable trend strength.

Break below 6700 weakens the signal; break below 6606 invalidates the forecast.

SPX weekly overview🔺 Chart Summary – Symmetrical Triangle + Key Levels

chart clearly shows a large symmetrical triangle forming on the SPX 1-hour timeframe:

1. Triangle Structure

Upper trendline (descending): Connecting the lower highs from the recent peak.

Lower trendline (ascending): Connecting higher lows from the last big dip.

Price is currently squeezing toward the apex, meaning volatility may contract before a bigger breakout move.

Resistance Levels

6750–6760 zone: Immediate resistance; price is struggling here.

6830–6860 zone: Major resistance cluster from previous swing highs.

Above that: Trendline resistance will be the next barrier.

Support Levels

6700–6710 zone: Very important short-term support.

6640–6650 zone: Stronger support; matches previous reaction lows.

6580–6600: Deeper support and bottom of the triangle approach.

4. Market Implication

Bullish: Break above the descending trendline + close above 6760 opens path toward 6830–6860.

Bearish: Break below the ascending trendline + close under 6640 opens path toward 6580 and further.

5. Overall View

The index is coiling inside a tightening triangle, meaning a major move is likely soon. Right now, SPX is in neutral-to-slightly-bearish territory until it reclaims the 6750–6760 zone.

SPX500 | Key Levels Ahead of Nvidia EarningsSPX500 | Overview

U.S. stock futures edge higher as investors await Nvidia’s earnings report and delayed government data, which could provide clues about the economy and the Federal Reserve’s next policy steps.

Technically:

The SPX500 remains in a neutral-to-bearish zone, with direction depending on the upcoming 4H candle close.

A close below 6755 would confirm a bearish continuation toward 6706 and 6670.

However, a 4H close above 6769 would shift momentum to a bullish trend, targeting 6813 and 6838.

Pivot Line: 6754

Support: 6706 · 6670 · 6637

Resistance: 6770 · 6813 · 6838