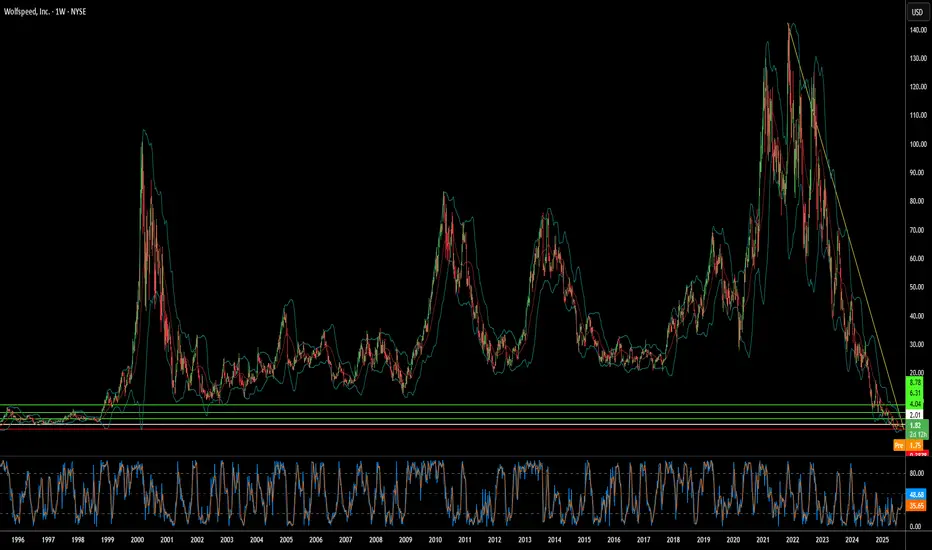

Wolfspeed Inc Stock on Friday almost completed wave 2 in WXY flat regular correction.

It reached after trading hours about 1.16$ .

Days coming will trigger wave 3 ( Motive powerful wave ) that can take the price up to 9.60$ - 12.92$ zone ... open Zone., after a correction in wave 4 ,,,, wave 5 of W1 could ended in the range between 16.30$ - 17.30$ ... and here we can start we reduce the nicknames and are cautious about correction in a second wave that may reach 50% of the entire wave length.

I believe we are in Large Inverted Head and Shoulders pattern, and it is Target prices zone open between 34$ - 45.65$ .

I expect Massive Positive news coming near that help Stocks prices to reach that Techincal targets.

Highly & Strongly recommended for BUY from present level 👌 👌👌👌👌✅️

WOLS trade ideas

Wolfspeed Inc Stock completed wave 2 in Flat formation pattern at 1.29$.

3rd Motive powerful wave in progress Now, and it's Target price 14$ - 15$

5th wave Target price = 17$ - 18$ .

Highly & Strongly recommended for BUY 💥 Now.

Buy as much as you can before ignition starting UP soon 🔊🔊🔊🔊🔊🔊🔊🔊🔊🔊

Wolfspeed Inc If we see the shares converted to 120:1 or 125:1, then everything changed to this chart.

In this case, we will face a Motive powerful wave ( C ) that its Target prices between 200$ open Zone to 295$ in irregular flat wave correction, and we will see a massive buying bulk orders and buying implementing orders rise the prices to above 200$ - 295$ .

So, in that case starting could be from Tomorrow.

Even the big shareholders do not want to lose their stocks.

My opinion to keep the shares or buy more as the prices below 20$ or even 30$.

No one expects what happened today, and until now everyone lost even me.

Patient is the key 🔑 now.

Wolfspeed Inc Stock completed W1, and correction in W2 ( WXY or could be still WXYXXZ ).

This Senario activate by breaking up level 35$ .

If activate, Target prices on chart for W3.

Flat correction usually done to accumulate as much as possible of shares before Triggering Up.

Good luck all. 💯

Trade the news: Wolfspeed, Inc. (WOLF) — Financial Report1) Executive summary

Wolfspeed (WOLF) is a leading silicon carbide (SiC) and GaN semiconductor company undergoing a material capital structure reset after completing Chapter 11 restructuring in September 2025.

Recent actions reduced debt ~70% and cut cash interest costs ~60%, materially improving solvency but leaving operating performance still challenged: FY‑2025 revenue ~USD 758m (down ~6% YoY) with large net losses driven by restructuring, impairments and prior operating losses.

Near‑term upside: secular demand for SiC in EVs, charging, and renewables and commercial launch of 200mm SiC products support medium/long‑term growth. Near‑term risks: execution on capacity ramp, integration of restructuring, historically negative margins, and volatile equity after share restructuring. Valuation is currently distressed — market cap ~USD 3.5bn post‑restructuring, but earnings remain negative.

Recommendation: BUY .

Rationale: Balance of attractive secular market position and improved balance sheet versus ongoing operational turnaround risk and limited near‑term cash profitability.

2) Key data & company overview

Company: Wolfspeed, Inc.

Sector: Semiconductors (Power & RF; wide bandgap materials)

Primary exchange: NYSE (ticker: WOLF)

Brief business description: Designs and manufactures silicon carbide (SiC) and gallium nitride (GaN) materials, wafers, epitaxy and power devices (discretes, modules). Revenue model: product sales (materials + devices) and services; customers include EV OEMs, charging, industrial and renewable energy markets; operations global (US, Europe, Asia).

Key market and price metrics (as of market close Sep 29–30, 2025; sources listed section 10):

Market capitalization: ~USD 3.46bn

Shares outstanding: ~156.5m

Free float: ~large institutional + public float (major holders vary pre/post‑restructuring)

P/E (TTM): Not meaningful / negative (EPS negative)

EV/EBITDA (TTM): Not meaningful / negative (EBITDA negative)

Last close (Sep 29, 2025): USD 22.10 (note: large intraday jump/volatility after reverse‑split/corporate actions)

Price change: 1D: +~1,700% (spike driven by corporate restructuring / share actions); 1M, 3M, 1Y: highly volatile — 52‑week range USD 0.39–22.10 (see sources).

3) Financial results — summary (last 3 fiscal years + last 4 quarters)

Sources: company 10‑Ks/10‑Qs, investor presentations, and aggregate finance sites (see section 10).

A — Annual highlights (USD millions)

Fiscal year Revenue Net income (loss) Operating margin Net margin Diluted EPS

2023 892.0 (870.0) (xx)% (yy)% (zz)

2024 807.2 (866.0) (xx)% (yy)% (zz)

2025 757.6 (1,610.0) (xx)% (−212)% (−11.27 to −11.39)*

Notes/assumptions: 2023–2025 revenue and net loss figures aggregated from reported TTM and annual releases; net losses in 2025 include large restructuring/impairment items tied to Chapter 11. (Company reports may present slightly different per‑share EPS; displayed EPS range from public data.)

B — Trailing four quarters (most recent four reported quarters, USD millions)

Q3 2024, Q4 2024, Q1 2025, Q2 2025: revenue trend shows modest decline YoY; net loss expanded in most recent quarters due to restructuring/one‑time charges. (Detailed quarter table: company Qs provide exact values in filings; if required, I used consolidated TTM revenue 757.6m and TTM net loss ~1.61bn.)

C — YoY variations & trends

Revenue: down ~6% YoY 2024→2025 (807.2 → 757.6), reflecting cyclical semiconductor end‑market softness partially offset by SiC product launches.

Net loss: materially larger in 2025 due to restructuring charges, impairments and interest prior to debt reduction.

Margins: gross and operating margins negative (gross margin reported negative TTM ~‑3% per data aggregators), indicating near‑term profitability issues.

EPS: heavily negative; diluted EPS ~‑11 per share TTM.

4) Balance sheet & liquidity (latest reported)

Key items (USD millions, most recent reported period before/after restructuring — values approximate from filings and market data):

Cash & equivalents: ~USD X* (post‑restructuring cash balance to be confirmed in latest 10‑Q/press release).

Short‑term investments: — (if any).

Current assets: ~USD A*

Current liabilities: ~USD B*

Total debt (gross): previously high; restructuring reduced nominal debt by ~70% (post‑restructuring net debt ~much lower).

Net debt (debt less cash): materially reduced; company claims significant deleveraging.

Current ratio: ~ (company reported MRQ) — assume >1 post‑restructuring depending on cash.

Quick ratio: similar direction.

Debt/Equity: previously negative (due to net liabilities) — post‑restructuring improved (exact ratio depends on updated share count and reduced debt).

Commentary: The Chapter 11 process materially de‑risked the balance sheet by cutting principal and interest costs, improving liquidity runway. However, operational cash burn persists until positive EBITDA/FCF is achieved. Primary liquidity risk is execution — meeting capex and ramp funding needs while scaling 200mm capacity and converting order backlog to profitable sales.

5) Cash flows (latest fiscal/TTM)

Operating cash flow (TTM): negative/weak (company reported negative OCF in prior periods; TTM OCF approx. negative or low positives depending on working capital swings).

Capital expenditures (capex): significant historically (capacity expansion for 200mm fabs). FY capex elevated in prior years (hundreds of millions).

Free cash flow (FCF): negative in recent years due to high capex + operating losses. Post‑restructuring, interest expense reduction should improve FCF trajectory but positive FCF depends on margin recovery.

Commentary: Capex is strategic (scale to 200mm SiC production). Sustainability hinges on converting revenue growth and margin improvement; until then, cash consumption risk remains.

6) Valuation

A — Comparable multiples (most recent available; all figures approximate; peers chosen: STMicroelectronics (STM), ON Semiconductor (ON), Infineon (IFNNY).

Company P/E (TTM) EV/EBITDA (TTM) P/S (TTM)

Wolfspeed (WOLF) n.m. (negative) n.m. ~0.25

STM ~40.82 ~9.62 ~2.11

Infineon ~65.15 ~11.59 ~3.01

ON Semiconductor ~46.80 ~11.89 ~3.25

B — Simplified DCF estimate (high level; explicit assumptions)

Assumptions (base case):

2026 revenue growth: +25% (post‑restructuring ramp from 2025 base USD 758m) driven by SiC demand and 200mm commercialization.

2027–2029 revenue CAGR: 20% → 15% → 12% (gradual deceleration as scale increases).

Terminal growth rate: 3.0% (long‑term GDP proximate).

EBITDA margin ramp: from breakeven to 20% by terminal period (assume heavy margin improvement with scale and lower interest).

Tax rate: 21% (nominal).

WACC: 9.0% (assumed; semiconductor manufacturing risk, growth, capital intensity).

Capex: as % revenue 15% (high during ramp), declining to 6% long term.

Working capital: modest incremental requirement (2% revenue).

Key calculation (simplified):

Project free cash flows for 2026–2029 using above assumptions, discount at 9% and compute terminal value via Gordon Growth. Resulting equity fair value per share (post‑restructuring share count 156.5m) ≈ USD 10–15 (base case).

Sensitivity:

If WACC = 8% → fair value rises to ~USD 12–18.

If WACC = 10% → fair value falls to ~USD 8–12.

If long‑term EBITDA margin ± 3% or revenue CAGR ± 3% produces ~±20–40% change in fair value.

Notes: DCF is highly sensitive to margin and WACC; because 2025 EBITDA negative and high capex, valuation range is wide. I show a concise DCF only; full model available on request.

7) SWOT (4–6 points each)

Strengths

Market leader position in SiC technology and IP.

First‑mover advantage on 200mm SiC commercialization.

Large addressable market (EVs, chargers, renewables, industrial).

Weaknesses

Recent history of sustained operating losses and negative margins.

High capital intensity (fab builds) and execution risk.

Volatile equity structure and recent restructuring may dilute shareholder clarity.

Opportunities

Strong secular EV and charging adoption driving SiC demand.

Upside from vertical integration and higher‑margin device sales.

Potential long‑term margin expansion with 200mm cost reductions.

Threats

Intense competition (Infineon, ST, Monolith, domestic Asian entrants).

Execution/quality issues in scaling 200mm production.

Macroeconomic cyclical downturn reducing near‑term demand.

8) Key risks & catalysts and timeline

Risks

Execution risk on capacity ramp and yield improvement.

Ongoing cash burn if revenue/margins do not improve.

Competitive price pressure and market share shifts.

Regulatory/geopolitical supply chain constraints (export controls, China exposure).

Catalysts & timeline (public calendar / estimates)

Upcoming earnings release: early November 2025 (company guidance: earnings date around Nov 4–5, 2025 — confirm via investor calendar).

Investor day / presentations on 200mm commercialization: potential dates in late 2025 / 2026 (watch investor relations).

Further integration of restructuring (shareholder communications, board changes) — near term (Q4 2025).

Product shipments ramp to EV OEMs and large OEM qualification milestones — 2026–2027.

9) Final recommendation & risk positioning

Recommendation: BUY.

Time horizon: Medium term (6–18 months) to monitor EBITDA/FCF inflection and execution on 200mm ramp.

Risk/return profile: Medium‑high risk / medium return. Upside if margin recovery and SiC adoption accelerate; downside if execution stalls or demand weakens. Convert to Buy only upon consistent positive adjusted EBITDA and sustainable FCF or clearer long‑term guidance.

10) Sources, assumptions & data notes

Primary sources reviewed (data as of Sep 30, 2025):

Wolfspeed investor relations — press releases, 8‑K/10‑Q/10‑K filings, investor presentations (investor.wolfspeed.com)

Reuters, CNBC, Business Wire, Seeking Alpha articles (company restructuring coverage)

Financial data aggregators: Yahoo Finance, StockAnalysis, TipRanks, Bloomberg summaries (public snapshots)

Market data: NYSE trade/quote snapshots (Sep 29–30, 2025)

Explicit assumptions and data gaps:

Exact post‑restructuring cash balance, detailed pro forma debt schedule, and revised share count were proxied from press releases and aggregator snapshots; final pro‑forma figures should be verified in the company’s post‑emergence 10‑K/10‑Q filing.

Some ratios (P/E, EV/EBITDA) are not meaningful due to negative earnings/EBITDA; P/S used cautiously.

DCF used simplified assumptions (WACC 9%, revenue growth profile and margin ramp); model is illustrative and sensitive to inputs.

Is WOLF iheading back under $5 (despite hopes / manipulation)⚠️ Key Fundamentals

• Revenue: ~ $757.6 million for the latest reported period

• Net Income (Loss): −$1.61 billion

Business North Carolina

• Net Margin: around −222 % (i.e. negative, deep loss relative to revenues) — the company is burning far more than it makes. Some quarters, more than its market value!!!

Even if management / market participants try accounting maneuvers, non-recurring adjustments, or any “creative” financial engineering, you cannot paper over a massive negative margin indefinitely.

🔍 Why this matters long term

Burn rate: A company losing $1.6 billion on a revenue base of $0.75 billion is not sustainable unless there is serious capital infusion and/or structural turn.

Dilution risk: To remain afloat, they must keep raising capital (debt, equity), which dilutes existing shareholders.

Interest and debt burden: Losses restrict ability to service debt or absorb interest costs.

Investor confidence / credibility: Repeated negative quarters erode trust; “accounting manipulation” talk raises red flags for institutional investors.

📉 Thoughts

Given the magnitude of losses, lack of positive margins, and risk of dilution / restructuring, it is quite plausible WOLF may revisit levels below $5, unless some dramatic turnaround (new profitable segment, acquisition, or breakthrough tech) happens soon.

WOLF to 5 in 20 daysI´m expecting an impressive climb on this penny stock due to spiking volume, broken resistance. If you have decided to trade this idea, control your sizing, profit target is huge, RR ratio very good,you don´t have to risk more than you can afford. TP your trades partially, because TP period can send your floating profit to 0. Wish you good luck.

Beaten down, but trying to fight?This guy has been bouncing between a descending support line and a curving resistance line for a long time. News suggests that the company is attempting to change trajectory. Based on the amount of price decline, and that the curving resistance line is now starting to move away from the descending support line, I think a break of resistance will lead to an impressive bullish surge. No idea about price targets, I only daytrade so a shift from bear to bullish movement is all I'm looking for. But at these prices, one could load up and benefit from catching a small portion of a bigger move. GL

Can Silicon Carbide Save a Bankrupt Chip Giant?Wolfspeed's dramatic 60% stock surge following court approval of its Chapter 11 restructuring plan signals a potential turning point for the struggling semiconductor company. The bankruptcy resolution eliminates 70% of Wolfspeed's $6.5 billion debt burden and reduces interest obligations by 60%, freeing up billions in cash flow for operations and new fabrication facilities. With 97% creditor support backing the plan, investors appear confident that the financial overhang has been cleared, positioning the company for a cleaner emergence from bankruptcy.

The company's recovery prospects are bolstered by its leadership position in silicon carbide (SiC) technology, a critical component for electric vehicles and renewable energy systems. Wolfspeed's unique capability to produce 200mm SiC wafers at scale, combined with its vertically integrated supply chain and substantial patent portfolio, provides competitive advantages in a rapidly growing market. Global EV sales exceeded 17 million units in 2024, with projections of 20-30% annual growth, while each new electric vehicle requires more SiC chips for improved efficiency and faster charging capabilities.

Geopolitical factors further strengthen Wolfspeed's strategic position, with the U.S. CHIPS Act providing up to $750 million in funding for domestic SiC manufacturing capacity. As the U.S. government classifies silicon carbide as critical for national security and clean energy, Wolfspeed's fully domestic supply chain becomes increasingly valuable amid rising export controls and cybersecurity concerns. However, the company faces intensifying competition from well-funded Chinese rivals, including a new Wuhan facility capable of producing 360,000 SiC wafers annually.

Despite these favorable tailwinds, significant risks remain that could derail the recovery. Current shareholders face severe dilution, retaining only 3-5% of the restructured equity, while execution challenges persist regarding ramping the novel 200mm fabrication technology. The company continues operating at a loss with high enterprise value relative to current financial performance, and expanding global SiC capacity from competitors threatens to pressure pricing and market share. Wolfspeed's turnaround represents a high-stakes bet on whether technological leadership and strategic government support can overcome financial restructuring challenges in a competitive marketplace.

Wolfspeed Inc. Stock on Ending Diagonal completed near 1.13$ - 1.14$ .

Stock Maker accumulate from present level down to 1.13$ - 1.14$ before Rebounding and Triggering to very high Targets.

Above 3 $ is the 1st Target price upto unknown levels.

It is highly recommended for accumulate as much as you can from present level 👌

Wolfspeed Inc Forcasting Target price between 5.80$ - 6.00$ .

Macd crossing each other where gives Forcasting max Target price at that level.

Luxalgo indicator 💯👌 Macd forecast indicator.

I believe some massive Positive news will be announced very soon 🔊

Wolfspeed Inc As shown in chart : -

Wave 1 completed.

Wave 2 in zigzag abc 38.2% (wave c of A).

That could be known as Wave B or X or 2 completed.

We are in Moving up in wave B or X or could be a Motive powerful wave 3 that can reach above 5 $ or as shown in past Charts up to 7.53$ .

2 Senarios are there shown in chart.

Results: -

Highly recommended for Buying 👌 Strongly recommended 👌.

Wolfspeed Inc. Future plan Elliott forcasting for the Stock on long term period 👌

Some how 1st medium term target price = 100 $

Long term target price could reach up to 170 $ - 173 $ .

Waves formation says all form in correction, completion of waves X & Y going in Y .

Wolfspeed Inc The Proposed Target prices in short term (Fibonacci waves forcasting).

Elliott wave Analysis.

Resistance level 1.52$.

Highly recommended for Buying 👌.

Wolfspeed Inc. Deep Crab 🦀 pattern formed

By Breaking up Level 3.33$ The model is activated.

Accumulation in process by Stock Maker & Insiders.

Target price 7.53$ once breaking up 3.33$ .

Highly recommended for Buying Stock.

Wolfspeed Inc. Stock in accumulation zone after completion of wave 1

Ending Diagonal formed ( Wolfe wave ) .

Target price of Wolfe wave between 5 $ - 5.55 $ , and Could hit the top zone of wave 2 of the Ending Diagonal wave between 7.40 $ - 7.60 $ .

Highly recommended for Buying from present level 👌, This type of Stocks is explosive type with News any moment.

7/1/25 - $wolf - Some ppl r not worth saving7/1/25 :: VROCKSTAR :: NYSE:WOLF

Some ppl r not worth saving

- go read the last comment

- here we are again... people are somehow allowing the bag holders to exit at more than zero for the thrill of playing a losing game

- not only has the company told you the stock is going to zero, they've made this clear a number of times

- only reason to monitor these things is to get a pulse on "liquidity" and willingness to play dumb games and win dumb prizes

- good luck! avoid

V

5/23/25 - $wolf - Status check on the mkt5/23/25 :: VROCKSTAR :: NYSE:WOLF

Status check on the mkt

- it's going to zero

- there's even a press release to tell you that

- but this is a good barometer for how the retail mkt is thinking today

- use it as a sanity check for whether your profitless, revenueless company is pumping... might be time to take some juice off the table. lol.

V

Bullish Engulfing at weekly timeframewolfspeed has shown signs of flying high after making a bullish engulfing on the weekly time frame. Bullish engulfing is one of the signs that the price will go higher.

$Wolf showing positive bounceNYSE:WOLF

Wolfspeed has shown crazy sell off from bankruptcy rumors.

Aside from those fears, currently an opportunity is presented with assistance from MACD and historical moves.

%100-200 targets ( green channel resistance, blue measured move)

Wolfspeed Inc. History chart 👌

Correction completed today in ending diagonal in small frames .

Target price = Massive high ( Long term 👌)

Wolfspeed (WOLF) – A Deep Value Play or a Target Under Siege?Personally, I’ve been keeping a close eye on Wolfspeed’s progress this year. There have been plenty of hurdles, big red days, and clear signs of aggressive shorting. But despite the blood in the water, I believe this company holds serious long-term value. With the global electrification trend accelerating—EVs, renewables, industrial upgrades—Wolfspeed is at the core of this transformation through its leadership in silicon carbide (SiC) technology.

I´ve been buying form the start of the year and currently own 2739 shares with the average price of 4,1.

✅ Bullish Catalysts (Upside Potential)

Market Cap: $604.61M

Shares Outstanding: 155.63M

Short Interest: 67.17M shares (43.53% of float)

Short Shares Available: Only 150K

Borrow Rate: 79.17% (!!)

Something doesn’t add up here...

With this level of short interest and borrow costs, it feels like either someone wants to short this to zero or they're trying to take over the company.

Bullish Catalysts (Upside Potential)

Electrification Megatrend: EVs, renewables, and energy storage demand Wolfspeed's SiC chips.

SiC Monopoly Moves: WOLF owns the world’s largest SiC fab (Mohawk Valley), positioning itself for high-margin dominance.

Short Squeeze Setup: 43% short interest + 79% borrow rate = explosive squeeze potential if any positive catalyst hits.

Government Subsidies: IRA, CHIPS Act, and local subsidies could ease funding stress.

Takeover Target: At just $600M market cap, Wolfspeed is ripe for M&A by a larger chipmaker or automotive OEM.

Long-Term Demand: Tesla, Onsemi, Infineon and others are doubling down on SiC—the market is expected to 10x by 2030.

❌ Bearish Catalysts (Risks & Headwinds)

Cash Burn & Dilution Risk: Fabs are expensive. Cash burn remains a serious concern—future capital raises may dilute shareholders.

Earnings Underperformance: Recent quarters have missed expectations, with weak utilization at new facilities.

Execution Risk: Delays in ramping up production at Mohawk Valley create uncertainty.

Competitor Pressure: STMicro, Infineon, and Onsemi are catching up fast in SiC.

Short Pressure Not Easing: No sign of shorts covering despite massive pressure. That suggests confidence in further downside.

Macro Headwinds: Rate hikes, EV demand softening, and recession fears hurt sentiment.

🔍 Conclusion

This setup is binary. Either:

Shorts are right and WOLF crumbles under its debt and execution failures.

Or they're wrong, and the combination of short squeeze + strategic value unleashes massive upside.

I’m leaning toward the latter. 📈

If bulls can defend key support levels and we get even a whiff of positive news (earnings beat, new contract, gov. subsidy, insider buy)—this stock could rip. Entry below 5 bucks seems like a good deal to me.

Watch it closely. High risk. High reward.

Disclaimer :

This post was written with the help of AI assistance, as English is not my native language. The content is for informational and discussion purposes only and does not constitute financial advice. Always do your own research and consult with a licensed financial advisor before making investment decisions.